The U.S. national debt surpassed $33 trillion for the first time ever this week, hitting $33.04 trillion according to the Treasury Department. This staggering sum exceeds the size of the entire U.S. economy and equals about $100,000 per citizen.

For investors, the ballooning national debt raises concerns about future tax hikes, inflation, and government spending cuts that could impact markets. While the debt level itself may seem abstract, its trajectory has real implications for portfolios.

Over 50% of the current national debt has accumulated since 2019. Massive pandemic stimulus programs, tax cuts, and a steep drop in tax revenues all blew up the deficit during Covid-19. Interest costs on the debt are also piling up.

Some level of deficit spending was needed to combat the economic crisis. But years of expanding deficits have brought total debt to the highest level since World War II as a share of GDP.

With debt now exceeding the size of the economy, there is greater risk of reduced economic output from crowd-out effects. High debt levels historically hamper GDP growth.

Economists worry that high debt will drive up borrowing costs for consumers and businesses as the government competes for limited capital. The Congressional Budget Office projects interest costs will soon become the largest government expenditure as rates rise.

Higher interest rates will consume more tax revenue just to pay interest, leaving less funding available for programs and services. Taxes may have to be raised to cover these costs.

Rising interest costs will also put more pressure on the Federal Reserve to keep rates low and monetize the debt through quantitative easing. This could further feed inflation.

If interest costs spiral, government debt could eventually reach unsustainable levels and require restructuring. But well before that, the debt overhang will influence policy and markets.

As debt concerns mount, investors may rotate to inflation hedges like gold and real estate. The likelihood of higher corporate and individual taxes could hit equity valuations and consumer spending.

But government spending cuts to social programs and defense would also ripple through the economy. Leaner budgets would provide fiscal headwinds reducing growth.

With debt limiting stimulus options, creative monetary policy would be needed in the next recession. More radical measures by the Fed could introduce volatility.

While the debt trajectory is troubling, a crisis is not imminent. Still, prudent investors should account for fiscal risks in their portfolio positioning and outlook. The ballooning national debt will shape policy and markets for years to come.

The Federal Reserve is stuck between a rock and a hard place as it aims to curb high inflation without inflicting too much damage on economic growth. This precarious balancing act has major implications for both average citizens struggling with rising prices and investors concerned about asset values.

For regular households, the current bout of high inflation straining budgets is public enemy number one. Prices are rising at 8.3% annually, squeezing wages that can’t keep pace. Everything from groceries to rent to healthcare is becoming less affordable. Meanwhile, rapid Fed rate hikes intended to tame inflation could go too far and tip the economy into recession, slowing the job market and risking higher unemployment.

However, new economic research suggests the Fed also needs to be cognizant of rate hikes’ impact on the supply side of the economy. Supply chain bottlenecks and constrained production have been key drivers of this inflationary episode. Aggressive Fed action that suddenly squelches demand could backfire by inhibiting business investment, innovation, and productivity growth necessary to expand supply capacity.

For example, sharply higher interest rates make financing more expensive, deterring business investment in new factories, equipment, and technologies. Tighter financial conditions also restrict lending to startups and venture capital for emerging technologies. All of this could restrict supply, keeping prices stubbornly high even in a weak economy.

This means the Fed has to walk a tightrope, moderating demand enough to curb inflation but not so much that supply takes a hit. The goal is to lower costs without forcing harsh rationing of demand through high unemployment. A delicate balance is required.

For investors, rapidly rising interest rates have already damaged asset prices, bringing an end to the long-running stock market boom. Higher rates make safe assets like bonds more appealing versus risky bets like stocks. And expectations for Fed hikes ahead impact share prices and other securities.

But stock markets could stabilize if the Fed manages to engineering the elusive “soft landing” – bringing down inflation while avoiding recession. The key is whether moderating demand while supporting supply expansion provides stable growth. However, uncertainty remains high on whether the Fed’s policies will thread this narrow needle.

Overall, the Fed’s inflation fight has immense stakes for Americans’ economic security and investors’ asset values. Walking the tightrope between high inflation and very slow growth won’t be easy. Aggressive action risks supply problems and recession, but moving too slowly could allow inflation to become entrenched. It’s a delicate dance with high stakes riding on success.

The Consumer Price Index (CPI) increased 0.6% in August on a seasonally adjusted basis, quickening from the 0.2% rise seen in July, according to the Bureau of Labor Statistics’ latest report. Over the past 12 months through August, headline CPI inflation stands at 3.7% before seasonal adjustment, up from 3.2% for the 12-month period ending in July.

The August monthly gain was primarily driven by a spike of 10.6% in the gasoline index. Gasoline was coming off a tamer 0.2% increase in July. Food prices also contributed to inflationary pressures, with the food at home index edging up 0.2% again last month. The food away from home index rose 0.3%.

Meanwhile, the energy index excluding gasoline picked up as well. Natural gas costs ticked up 0.1%, electricity prices rose 0.2%, and fuel oil prices surged 9.1%.

The core CPI, which removes volatile food and energy categories, rose 0.3% in August after a 0.2% gain in July. The shelter index has been a main driver of core inflation. It covers rental costs and owners’ equivalent rent, both of which have rapidly increased due to imbalances between housing supply and demand.

On an annual basis, the energy index has fallen 3.6%, as gasoline, natural gas and fuel oil costs are down over the past 12 months. However, the food and core indexes are up 4.3% and 4.3% year-over-year, respectively.

Within the core CPI, the main drivers have been shelter costs, up 7.3% over the last 12 months, along with auto insurance (+19.1%), recreation services (+3.5%), personal care (+5.8%) and new vehicles (+2.9%). Medical care services inflation has also accelerated to 6.6% over the past year.

Geographically, inflation varies significantly by region. The Northeast has seen 4.2% CPI inflation over the past year, the Midwest 3.9%, the South 3.7%, and the West just 2.9%. By city size, larger metropolitan areas over 1.5 million people have experienced 3.8% inflation, compared to 3.6% for mid-sized cities and 3.7% in smaller cities.

August’s monthly data shows inflation quickened after signs of cooling in July. While gasoline futures retreated in September, shelter inflation remains stubbornly high with no meaningful relief expected until mortgage rates decline substantially.

With core inflation running well above the Fed’s 2% target, further interest rate hikes are anticipated to combat still-high inflation. But the path to a soft economic landing appears increasingly narrow amid recession risks.

The next CPI update will be released in mid-October, shedding light on whether persistent pricing pressures are continuing to squeeze household budgets. For now, the August report shows inflation picking up steam after the prior month’s encouraging data.

Yet the larger concern remains the entrenched inflation in essentials like food, rent and medical care. Shelter inflation in particular has shown little sign of abating, as rental rates and housing prices remain disconnected from incomes.

Mortgage rates have soared above 6% in 2023 after starting the year around 3%. The sharp rise in financing costs continues to shut many homebuyers out of the market. Until mortgage rates meaningfully decline, shelter inflation is likely to persist.

And that will be challenging as long as the Fed keeps interest rates elevated. Monetary policy has lagged in responding to inflation, putting central bankers in catch-up mode. Further rate hikes are expected in the coming months absent a significant cooling in pricing pressures.

But the risks of the Fed overtightening and spurring a recession continue to intensify. The path to a soft landing for the economy is looking increasingly precarious.

For consumers, it means further inflationary pain is likely in store before a sustained moderation emerges. Budgets will remain pressured by pricier essentials, leaving less room for discretionary purchases.

While the monthly data will remain volatile, the overall trend points to stubborn inflation persisting through year-end. The Fed will be closely watching to see if their actions to date have slowed price gains enough. If not, consumers should prepare for more rate hikes and resulting economic uncertainty into 2024.

New applications for U.S. unemployment benefits fell unexpectedly last week to the lowest level since mid-February, signaling the job market remains tight even as broader economic headwinds build.

Initial jobless claims declined by 13,000 to 216,000 in the week ended September 2, the Labor Department reported Thursday. That was below economist forecasts for a rise to 234,000 and marked the fourth straight week of declines.

Continuing claims, which track ongoing unemployment, also dropped to 1.679 million for the week ended August 26. That was the lowest point since mid-July.

The downward trend in both initial and continuing claims points to ongoing resilience in the labor market amid strong employer demand for workers.

There are some emerging signs of softness, however. The unemployment rate ticked higher to 3.8% in August as labor force participation increased. Job growth also moderated in the latest month, though remains healthy.

Worker productivity rebounded at a 3.5% annualized pace in the second quarter, the fastest rise since 2020. Moderating labor cost growth could also help the Federal Reserve combat high inflation.

While jobless claims remain near historic lows, economists will keep a close eye on any notable changes that could indicate potential layoffs, although the Federal Reserve has recently taken a more measured approach to rate hikes aimed at moderating economic demand.

Currently, the most recent data confirms a remarkably robust job market, despite concerns about inflation and slowing growth. This resilience provides hope that any potential economic downturn in the future might be less severe than previously anticipated.

China and Japan are actively defending their currencies against the rising US dollar, sparking inflation concerns. Both the yen and yuan have depreciated significantly due to market expectations of prolonged higher interest rates by the US Federal Reserve.

In response, China’s central bank is providing robust guidance through its daily yuan reference rate to prevent excessive weakening. Japan has issued a stern warning against rapid yen depreciation, signaling readiness for intervention.

Despite these efforts, doubts linger about their effectiveness, especially if the Federal Reserve maintains a hawkish stance or China’s economic recovery remains sluggish. The strong US dollar also affects European currencies, with the euro and pound hitting their lowest levels since June, raising concerns of quicker rate cuts by eurozone and UK central banks to counter rising borrowing costs. Investors globally watch closely as central banks and the Federal Reserve navigate these currency dynamics, with potential implications for inflation and future monetary policies.

The U.S. jobs report for August is out, with 187,000 jobs added to the economy in August. This is slightly higher than the 170,000 economists had expected. On the other side, unemployment is up slightly, at 3.8%. This is 0.3% higher than economists had predicted. Wages increased slightly, up 0.2% month-over-month, and remain up more than 4% over last year.

About the U.S. Jobs Report

The U.S. jobs report, specifically the nonfarm payroll report, is a critical economic indicator that holds immense significance for both financial markets and policymakers. This report, typically released on the first Friday of each month by the U.S. Bureau of Labor Statistics, provides crucial insights into the health of the labor market in the United States.

The report serves as a barometer of economic health. It offers valuable data on the number of jobs created or lost in the previous month, the unemployment rate, and wage growth. This information helps economists and investors gauge the overall economic performance and can influence their outlook on future economic conditions. If job creation exceeds expectations, it can signal a robust economy, potentially leading to higher consumer spending and business investments.

This report also has a significant impact on financial markets. Stock, bond, and currency markets can experience substantial volatility on the day of the report’s release. Positive job growth can boost investor confidence and lead to stock market gains, while weaker-than-expected data can trigger market sell-offs. Additionally, the Federal Reserve closely monitors the jobs report when making decisions about interest rates and monetary policy, making it a key factor in shaping the direction of these markets in the medium to long term.

In summary, the U.S. jobs report is a vital economic indicator that provides insights into the labor market’s health and has a profound impact on financial markets, influencing investor sentiment, asset prices, and even central bank decisions. It is closely watched by economists, investors, and policymakers alike for its role in shaping economic outlooks and investment strategies.

Image: President Jimmy Carter and Chinese Vice Premier Deng Xiaoping meet outside of the Oval Office on Jan. 30, 1979

The US and China May Be Ending an Agreement on Science and Technology Cooperation − A Policy Expert Explains What This Means for Research

A decades-old science and technology cooperative agreement between the United States and China expires this week. On the surface, an expiring diplomatic agreement may not seem significant. But unless it’s renewed, the quiet end to a cooperative era may have consequences for scientific research and technological innovation.

The possible lapse comes after U.S. Rep. Mike Gallagher, R-Wis., led a congressional group warning the U.S. State Department in July 2023 to beware of cooperation with China. This group recommended to let the agreement expire without renewal, claiming China has gained a military advantage through its scientific and technological ties with the U.S.

The State Department has dragged its feet on renewing the agreement, only requesting an extension at the last moment to “amend and strengthen” the agreement.

The U.S. is an active international research collaborator, and since 2011 China has been its top scientific partner, displacing the United Kingdom, which had been the U.S.‘s most frequent collaborator for decades. China’s domestic research and development spending is closing in on parity with that of the United States. Its scholastic output is growing in both number and quality. According to recent studies, China’s science is becoming increasingly creative, breaking new ground.

This article was republished with permission from The Conversation, a news site dedicated to sharing ideas from academic experts. It represents the research-based findings and thoughts of,Caroline Wagner, Professor of Public Affairs, The Ohio State University.

As a policy analyst and public affairs professor, I research international collaboration in science and technology and its implications for public policy. Relations between countries are often enhanced by negotiating and signing agreements, and this agreement is no different. The U.S.’s science and technology agreement with China successfully built joint research projects and shared research centers between the two nations.

U.S. scientists can typically work with foreign counterparts without a political agreement. Most aren’t even aware of diplomatic agreements, which are signed long after researchers have worked together. But this is not the case with China, where the 1979 agreement became a prerequisite for and the initiator of cooperation.

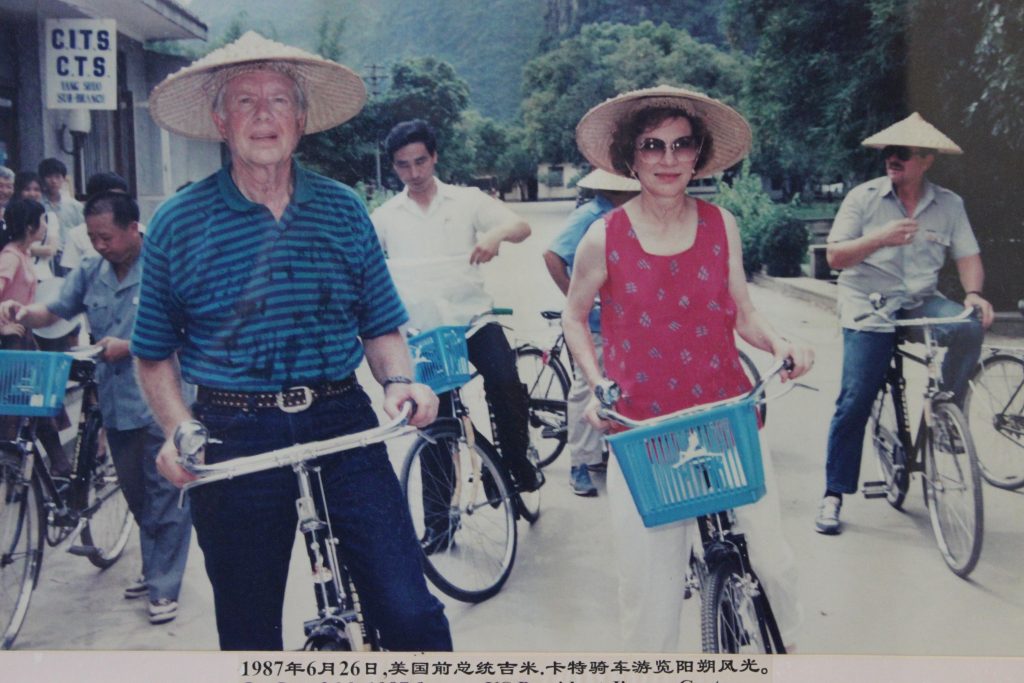

In 1987 former President Jimmy Carter visited Yangshuo, his wife Rosalyn and he insisted that went around Yangshuo countryside by bicycle.

A 40-Year Diplomatic Investment

The U.S.-China science and technology agreement was part of a historic opening of relations between the two countries, following decades of antagonism and estrangement. U.S. President Richard Nixon set in motion the process of normalizing relations with China in the early 1970s. President Jimmy Carter continued to seek an improved relationship with China.

China had announced reforms, modernizations and a global opening after an intense period of isolation from the time of the Cultural Revolution from the late 1950s until the early 1970s. Among its “four modernizations” was science and technology, in addition to agriculture, defense and industry.

While China is historically known for inventing gunpowder, paper and the compass, China was not a scientific power in the 1970s. American and Chinese diplomats viewed science as a low-conflict activity, comparable to cultural exchange. They figured starting with a nonthreatening scientific agreement could pave the way for later discussions on more politically sensitive issues.

On July 28, 1979, Carter and Chinese Premier Deng Xiaoping signed an “umbrella agreement” that contained a general statement of intent to cooperate in science and technology, with specifics to be worked out later.

In the years that followed, China’s economy flourished, as did its scientific output. As China’s economy expanded, so did its investment in domestic research and development. This all boosted China’s ability to collaborate in science – aiding their own economy.

Early collaboration under the 1979 umbrella agreement was mostly symbolic and based upon information exchange, but substantive collaborations grew over time.

A major early achievement came when the two countries published research showing mothers could ingest folic acid to prevent birth defects like spina bifida in developing embryos. Other successful partnerships developed renewable energy, rapid diagnostic tests for the SARS virus and a solar-driven method for producing hydrogen fuel.

Joint projects then began to emerge independent of government agreements or aid. Researchers linked up around common interests – this is how nation-to-nation scientific collaboration thrives.

Many of these projects were initiated by Chinese Americans or Chinese nationals working in the United States who cooperated with researchers back home. In the earliest days of the COVID-19 pandemic, these strong ties led to rapid, increased Chinese-U.S. cooperation in response to the crisis.

Time of Conflict

Throughout the 2000s and 2010s, scientific collaboration between the two countries increased dramatically – joint research projects expanded, visiting students in science and engineering skyrocketed in number and collaborative publications received more recognition.

As China’s economy and technological success grew, however, U.S. government agencies and Congress began to scrutinize the agreement and its output. Chinese know-how began to build military strength and, with China’s military and political influence growing, they worried about intellectual property theft, trade secret violations and national security vulnerabilities coming from connections with the U.S.

Recent U.S. legislation, such as the CHIPS and Science Act, is a direct response to China’s stunning expansion. Through the CHIPS and Science Act, the U.S. will boost its semiconductor industry, seen as the platform for building future industries, while seeking to limit China’s access to advances in AI and electronics.

A Victim of Success?

Some politicians believe this bilateral science and technology agreement, negotiated in the 1970s as the least contentious form of cooperation – and one renewed many times – may now threaten the United States’ dominance in science and technology. As political and military tensions grow, both countries are wary of renewal of the agreement, even as China has signed similar agreements with over 100 nations.

The United States is stuck in a world that no longer exists – one where it dominates science and technology. China now leads the world in research publications recognized as high quality work, and it produces many more engineers than the U.S. By all measures, China’s research spending is soaring.

Even if the recent extension results in a renegotiated agreement, the U.S. has signaled to China a reluctance to cooperate. Since 2018, joint publications have dropped in number. Chinese researchers are less willing to come to the U.S. Meanwhile, Chinese researchers who are in the U.S. are increasingly likely to return home taking valuable knowledge with them.

The U.S. risks being cut off from top know-how as China forges ahead. Perhaps looking at science as a globally shared resource could help both parties craft a truly “win-win” agreement.

Heading Into the Unofficial End of Summer, Powell Gave the Market a Lot to Think About

The last “unofficial” week of summer will likely be characterized by light trading, which could amplify volatility. This week follows what is viewed by many as a more hawkish tone than expected by Fed Chair Powell on Friday. The next FOMC meeting is not until September 19–20; that is a long time to obsess over every economic number, and there are many key numbers that will be released this week. Investors will be watching the labor report, alongside the PCE price index, personal income and spending data, JOLTS job openings, ISM Manufacturing PMI, and the second estimate of Q2 GDP growth.

Monday 8/28

• 10:30 AM ET, the Dallas Fed Manufacturing Index is expected to post a 16th straight negative number, at a steep minus 21.0 in August versus minus 20.0 in July. The survey asks manufacturers whether output, employment, orders, prices and other indicators increased, decreased or remained unchanged over the previous month. Responses are aggregated into an index where positive values generally indicate growth while negative values generally indicate contraction.

Tuesday 8/29

• 10:00 AM ET, Consumer Confidence is expected to dip slightly in August, at a consensus 116.5 versus July’s 117.0. This report has exceeded not only the consensus in the last three reports but the full consensus range as well.

• 10:00 AM ET, The JOLTS report consensus for July is 9.559 million near its June’s 9.582 million level. Economist consensus have been fairy accurate for this well monitored indicator. The JOLTS report tracks monthly change in job openings and offers rates on hiring and quits.

Wednesday 8/30

• 8:30 AM ET, GDP (the second estimate of second-quarter) is expected to show no change from 2.4 percent growth in the quarter’s first estimate. Personal Consumption Expenditures (PCE), at 1.6 percent growth in the first estimate, is expected to come in at 1.7 percent in the second estimate.

• 10:00 AM ET, Pending Home Sales are expected to fall by 0.4% after rising .3% in June. The National Association of Realtors developed the Pending Home Sales report as a leading indicator of housing activity. Specifically, it is a leading indicator of existing home sales, not new home sales. A pending sale is one in which a contract was signed, but not yet closed. It usually takes four to six weeks to close a contracted sale. Home transactions are a harbinger for economic activity.

• 10:00 AM ET, The State Street Investor Confidence Index measures confidence by looking at actual levels of risk in investment portfolios. This is not an attitude survey. The State Street Investor Confidence Index measures confidence directly by assessing the changes in investor holdings of equities. The prior number (July) was 96.2%.

• 10:30 PM ET, EIA The Energy Information Administration (EIA) provides the Petroleum Status Report weekly with information on petroleum inventories in the US, whether produced in the US or abroad. The level of inventories helps determine prices for petroleum products.

Thursday 8/30

• 7:30 AM ET, The Challenger Job-Cut Report for August will be reported and compared to last months 23,697 job cuts.

• 8:30 AM ET, Jobless claims for the week ended 8/26 are expected to come in at 238,000. The prior week the figure was 230,000.

• 8:30 AM ET, Personal Income is expected to have risen 0.3 percent in July with Consumption Expenditures expected to increase a solid 0.6 percent. These stats will be compared with June’s 0.3 percent increase for income and 0.5 percent increase for consumption.

• 9:45 AM ET, The Chicago PMI is expected to have risen in August to 44.6 versus 42.8 in July which was the eleventh straight month of sub-50 contraction.

• 3:00 PM ET, Farm Prices for July are expected to have risen month over month by 0.4%, however year-on-year declined by 5.3%. Farm prices are a leading indicator of food price changes in the producer and consumer price indices. There is not a one-to-one correlation, but general trends move in tandem. Inflation is a general increase in the prices of goods and services.

• 4:30 PM ET, The Fed’s Balance Sheet totaled $8.139 trillion last week. Further declines in line with the Feds quantitative tightening (QT) is expected.

Friday 9/1

• 8:30 AM ET, the Employment Situation report is expected to show a moderating but still strong 170,000 increase for nonfarm payroll growth in August versus 187,000 in July which was a bit lower than expected. Average hourly earnings in August are expected to rise 0.3 percent on the month for a year-over-year rate of 4.4 percent; these would compare with 0.4 and 4.4 percent in the prior two reports. August’s unemployment rate is expected to hold unchanged at 3.5 percent.

• 10:00 AM ET, The ISM manufacturing index has been in contraction the last nine months. August’s consensus is 46.8 versus July’s 46.4.

• 10:00 AM ET, Construction Spending for July is expected to have risen 0.5% to match June’s 0.5% increase that had benefited from a second strong month for residential spending.

What Else

There is no early close scheduled for the US markets on Friday before the three day Labor Day weekend.

Have you attended an in-person roadshow organized by Noble Capital Markets. Noble has been reaching out to retail and institutional investors and holding these events designed for investors to meet management teams. Investors have been able to discover more about their companies, often enough to make an informed decision. The forum has been getting rave reviews from investors and company management teams. Use this link to see if a roadshow is scheduled near you.

The Fed Is Losing Tens of Billions: How Are Individual Federal Reserve Banks Doing?

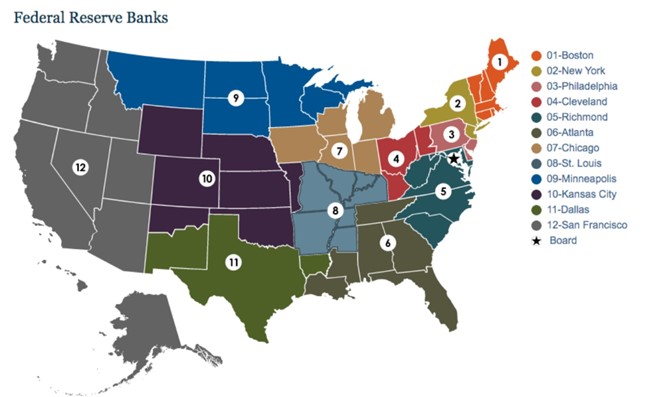

The Federal Reserve System as of the end of July 2023 has accumulated operating losses of $83 billion and, with proper, generally accepted accounting principles applied, its consolidated retained earnings are negative $76 billion, and its total capital negative $40 billion. But the System is made up of 12 individual Federal Reserve Banks (FRBs). Each is a separate corporation with its own shareholders, board of directors, management and financial statements. The commercial banks that are the shareholders of the Fed actually own shares in the particular FRB of which they are a member, and receive dividends from that FRB. As the System in total puts up shockingly bad numbers, the financial situations of the individual FRBs are seldom, if ever, mentioned. In this article we explore how the individual FRBs are doing.

All 12 FRBs have net accumulated operating losses, but the individual FRB losses range from huge in New York and really big in Richmond and Chicago to almost breakeven in Atlanta. Seven FRBs have accumulated losses of more than $1 billion. The accumulated losses of each FRB as of July 26, 2023 are shown in Table 1.

Table 1: Accumulated Operating Losses of Individual Federal Reserve Banks

New York ($55.5 billion)

Richmond ($11.2 billion )

Chicago ( $6.6 billion )

San Francisco ( $2.6 billion )

Cleveland ( $2.5 billion )

Boston ( $1.6 billion )

Dallas ( $1.4 billion )

Philadelphia ($688 million)

Kansas City ($295 million )

Minneapolis ($151 million )

St. Louis ($109 million )

Atlanta ($ 13 million )

The FRBs are of very different sizes. The FRB of New York, for example, has total assets of about half of the entire Federal Reserve System. In other words, it is as big as the other 11 FRBs put together, by far first among equals. The smallest FRB, Minneapolis, has assets of less than 2% of New York. To adjust for the differences in size, Table 2 shows the accumulated losses as a percent of the total capital of each FRB, answering the question, “What percent of its capital has each FRB lost through July 2023?” There is wide variation among the FRBs. It can be seen that New York is also first, the booby prize, in this measure, while Chicago is a notable second, both having already lost more than three times their capital. Two additional FRBs have lost more than 100% of their capital, four others more than half their capital so far, and two nearly half. Two remain relatively untouched.

Table 2: Accumulated Losses as a Percent of Total Capital of Individual FRBs

New York 373%

Chicago 327%

Dallas 159%

Richmond 133%

Boston 87%

Kansas City 64%

Cleveland 56%

Minneapolis 56%

San Francisco 48%

Philadelphia 46%

St. Louis 11%

Atlanta 1%

Thanks to statutory formulas written by a Congress unable to imagine that the Federal Reserve could ever lose money, let alone lose massive amounts of money, the FRBs maintained only small amounts of retained earnings, only about 16% of their total capital. From the percentages in Table 2 compared to 16%, it may be readily observed that the losses have consumed far more than the retained earnings in all but two FRBs. The GAAP accounting principle to be applied is that operating losses are a subtraction from retained earnings. Unbelievably, the Federal Reserve claims that its losses are instead an intangible asset. But keeping books of the Federal Reserve properly, 10 of the FRBs now have negative retained earnings, so nothing left to pay out in dividends.

On orthodox principles, then, 10 of the 12 FRBs would not be paying dividends to their shareholders. But they continue to do so. Should they?

Much more striking than negative retained earnings is negative total capital. As stated above, properly accounted for, the Federal Reserve in the aggregate has negative capital of $40 billion as of July 2023. This capital deficit is growing at the rate of about $ 2 billion a week, or over $100 billion a year. The Fed urgently wants you to believe that its negative capital does not matter. Whether it does or what negative capital means to the credibility of a central bank can be debated, but the big negative number is there. It is unevenly divided among the individual FRBs, however.

With proper accounting, as is also apparent from Table 2, four of the FRBs already have negative total capital. Their negative capital in dollars shown in Table 3.

Table 3: Federal Reserve Banks with Negative Capital as of July 2023

New York ($40.7 billion)

Chicago ($ 4.6 billion )

Richmond ($ 2.8 billion )

Dallas ($514 million )

In these cases, we may even more pointedly ask: With negative capital, why are these banks paying dividends?

In six other FRBs, their already shrunken capital keeps on being depleted by continuing losses. At the current rate, they will have negative capital within a year, and in 2024 will face the same fundamental question.

What explains the notable differences among the various FRBs in the extent of their losses and the damage to their capital? The answer is the large difference in the advantage the various FRBs enjoy by issuing paper currency or dollar bills, formally called “Federal Reserve Notes.” Every dollar bill is issued by and is a liability of a particular FRB, and the FRBs differ widely in the proportion of their balance sheets funded by paper currency.

The zero-interest cost funding provided by Federal Reserve Notes reduces the need for interest-bearing funding. All FRBs are invested in billions of long-term fixed-rate bonds and mortgage securities yielding approximately 2%, while they all pay over 5% for their deposits and borrowed funds—a surefire formula for losing money. But they pay 5% on smaller amounts if they have more zero-cost paper money funding their bank. In general, more paper currency financing reduces an FRB’s operating loss, and a smaller proportion of Federal Reserve Notes in its balance sheet increases its loss. The wide range of Federal Reserve Notes as a percent of various FRBs’ total liabilities, a key factor in Atlanta’s small accumulated losses and New York’s huge ones, is shown in Table 4.

Table 4: Federal Reserve Notes Outstanding as a Percent of Total Liabilities

Atlanta 64%

St. Louis 60%

Minneapolis 58%

Dallas 51%

Kansas City 50%

Boston 45%

Philadelphia 44%

San Francisco 39%

Cleveland 38%

Chicago 26%

Richmond 23%

New York 17%

The Federal Reserve System was originally conceived not as a unitary central bank, but as 12 regional reserve banks. It has evolved a long way toward being a unitary organization since then, but there are still 12 different banks, with different balance sheets, different shareholders, different losses, and different depletion or exhaustion of their capital. Should it make a difference to a member bank shareholder which particular FRB it owns stock in? The authors of the Federal Reserve Act thought so.

About the Author

Alex J. Pollock is a Senior Fellow at the Mises Institute, and is the co-author of Surprised Again! — The Covid Crisis and the New Market Bubble (2022). Previously he served as the Principal Deputy Director of the Office of Financial Research in the U.S. Treasury Department (2019-2021), Distinguished Senior Fellow at the R Street Institute (2015-2019 and 2021), Resident Fellow at the American Enterprise Institute (2004-2015), and President and CEO, Federal Home Loan Bank of Chicago (1991-2004). He is the author of Finance and Philosophy—Why We’re Always Surprised (2018).

Federal Reserve Chairman’s Speech at Jackson Hole Symposium Sparks Speculation on Subject and Market Impact

There’s an economic concept that is expected to be included in Fed Chair Powell’s next speech that may soon become the new buzzword. It may be worth a minute now to be sure there is a thorough understanding. Especially if his address at the Jackson Hole Symposium begins to drive markets one way or the other. Other news outlets say Powell’s address may be a pivotal moment that could potentially reshape the stock market landscape. Last year they said the same thing, but instead his address was a yawner, ultra-safe, with no new information for the markets to use.

Scheduled for 10:05 ET Friday morning, Powell’s address, it is said, may center around the concept of the neutral rate of interest, a theoretical but influential notion that holds the potential to send ripples through financial markets.

The neutral rate of interest, also referred to as r* or r-star, represents the level of real short-term interest rates anticipated to prevail when the U.S. economy is at its peak strength and inflation remains stable. Analysts estimate this real neutral rate to be around 0.5%, calculated by deducting the Federal Reserve’s 2% inflation target from policymakers’ latest predictions for the long-term trajectory of the fed funds rate. Speculation suggests that the neutral rate might be on the rise, given the current economic performance.

Amidst an environment where the U.S. economy appears to be gathering momentum, even following a series of interest rate hikes that brought rates to a 22-year high of 5.25%-5.5%, the stakes are high for determining the correct theoretical level for the neutral rate. The economy achieved a robust growth rate of 2% in the first quarter, followed by 2.4% in the second quarter. The Atlanta Fed’s GDPNow model projects an astonishing 5.8% growth rate for real gross domestic product in the third quarter, a figure met with skepticism but indicative of the economy’s notable resilience.

Investors will be hanging on the Fed chair’s every utterance, clarity from Powell’s address to better comprehend the Fed’s perspective on this crucial neutral rate. What a higher neutral rate could mean is policymakers could find themselves compelled to implement additional hikes to fed-funds. This scenario would result in longer periods of higher borrowing costs and a delay in the timing of the first rate reduction.

Traders and investors have already adjusted their expectations to anticipate the Federal Reserve maintaining elevated interest rates for a longer period.

This year has seen significant gains in the stock market, with the Dow Jones Industrial Average (DJIA) rising by 4%, the S&P 500 (SPX) surging by 15.5%, and the Nasdaq Composite (COMP) leading the pack with a remarkable 31.1% increase. Investors and traders are cautiously optimistic about a scenario where the U.S. economy navigates a soft landing, with inflation trending downward.

In the days leading up to Powell’s speech at the Kansas City Fed’s Jackson Hole symposium, the Treasury market has already incorporated expectations of stronger-than-anticipated U.S. economic growth. Yields for 10-year and 30-year Treasury bonds reached multiyear highs, though they retraced slightly in the days following. However, market participants anticipate potential fluctuations in response to Powell’s remarks, which could trigger further yield adjustments.

The recent upswing in yields, leading to the highest closing levels since 2007 and 2011 for the 10-year and 30-year rates, respectively, has been given as the reason for the decline in U.S. stock values during August. The S&P 500 experienced a decline of over 3% during the month.

Take Away

Understanding r* or r-star in advance may prevent some scurrying at 10:10 AM ET tomorrow. While Market participants eagerly await Powell’s speech, hoping for insights that will shed light on the Federal Reserve’s outlook regarding the neutral rate and its potential impact on monetary policy and the stock market, last year his words were short, and seemed to be designed to convey nothing new.

What to Expect Out of This Year’s Jackson Hole Symposium

Since 1978, the Federal Reserve Bank of Kansas City has sponsored an annual event to discuss an important economic issue facing the U.S. and world economies. From 1982, the symposium has been hosted at the Jackson Lake Lodge at Grand Teton National Park, in Wyoming. The event brings together economists, financial market participants, academics, U.S. government representatives, and news media to discuss long-term policy issues of mutual concern. The 2023 Economic Policy Symposium. “Structural Shifts in the Global Economy,” will be held Aug. 24-26.

Those attending are selected based on each year’s topic with consideration for regional diversity, background, and industry. In a typical year, about 120 people attend.

The event features a collegiate feel with thoughtful discussion among the participants. The caliber and status of participants and the important topics being discussed draw substantial interest from the financial community in the symposium. Despite the interest in the annual event, The Jackson Hole event works best as a smaller open discussion, attendance at the event is limited.

Similarly, although the Federal Reserve District Bank receives numerous requests from media outlets worldwide, press attendance is also limited to a group that is selected to provide important transparency to the symposium, but not overwhelm or influence the proceedings. All symposium participants, including members of the press, pay a fee to attend. The fees are then used to recover event expenses.

Source: Federal Reserve, Kansas City, MO

What’s discussed?

The Kansas City Fed chooses the topic each year and asks experts to write papers on related subtopics. To date, more than 150 authors have presented papers on topics such as inflation, labor markets and international trade. All papers are available online.

Papers provided to the Bank in advance and presented at the annual economic policy symposium will be posted online at the time they are presented at the event. Other papers, such as conference comments, are posted as they become available. Additionally, transcripts of the proceedings are posted on the website as they become available, a process that generally takes a few months. Finally, the papers and transcripts are compiled into proceedings books which are both posted on the website and published in a volume that is available online or in print, free of charge.

Source: Federal Reserve, Kansas City, MO

Worldwide Representation

The goal of the Economic Policy Symposium when it began was to provide a vehicle for promoting public discussion and exchanging ideas. Throughout the event’s history in Jackson Hole, attendees from 70 countries have gathered to share their diverse perspectives and experiences.

Source: Federal Reserve, Kansas City, MO

This year’s theme will explore several significant, and potentially long-lasting, developments affecting the global economy. While the immediate disruption of the pandemic is fading, there likely will be long-lasting aftereffects for how economies are structured, both domestically and globally, as trade networks shift, and global financial flows react. Similarly, the policy response to the pandemic and its aftermath could have persistent effects as economies adjust to rapid shifts in the stance of monetary policy and a substantial increase in sovereign debt. The papers will share how these developments are likely to affect the context for growth and monetary policy in the coming decade.

The full agenda will be available at the start of the event on Thursday, Aug. 24 at 8 p.m. ET/6 p.m. MT. Federal Reserve Chair Jerome Powell’s remarks will be streamed on the Kansas City Fed’s YouTube channel, on Friday, Aug. 25 at 10:05 a.m. ET/8:05 a.m. MT. Papers and other materials will be posted on the Kansas City Fed’s website as they are presented during the event.

What Else

The markets seem to be expecting hawkish comments from the US Central Bank President on Friday at Jackson Hole. This is being priced in, as investors expect the Fed Chair may say something that spooks the bond market which naturally impacts stocks. There has been a lot of talk about how central banks globally should treat target inflation, all ears will be on that subject.

Image: External Affairs Ministers at BRICS foreign ministers meeting, MEA Photogallery (Flickr)

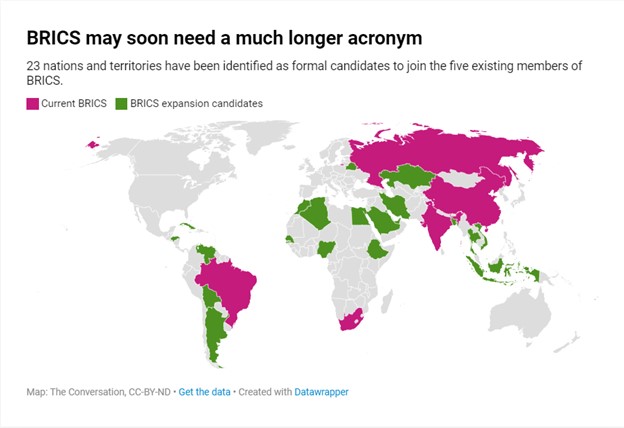

An Expansion of BRICS Countries Would Increase its Negotiating Strength

When leaders of the BRICS group of large emerging economies – Brazil, Russia, India, China and South Africa – meet in Johannesburg for two days beginning on Aug. 22, 2023, foreign policymakers in Washington will no doubt be listening carefully.

The BRICS group has been challenging some key tenets of U.S. global leadership in recent years. On the diplomatic front, it has undermined the White House’s strategy on Ukraine by countering the Western use of sanctions on Russia. Economically, it has sought to chip away at U.S. dominance by weakening the dollar’s role as the world’s default currency.

And now the group is looking at expanding, with 23 formal candidates. Such a move – especially if BRICS accepts Iran, Cuba or Venezuela – would likely strengthen the group’s anti-U.S. positioning.

This article was republished with permission from The Conversation, a news site dedicated to sharing ideas from academic experts. It represents the research-based findings and thoughts of, Mihaela Papa, Senior Fellow, The Fletcher School, Tufts University, Frank O’Donnell, Adjunct Lecturer in the International Studies Program, Boston College, Zhen Han, Assistant Professor of Global Studies, Sacred Heart University.

So what can Washington expect next, and how can it respond?

Our research team at Tufts University has been working on a multiyear Rising Power Alliances project that has analyzed the evolution of BRICS and the group’s relationship with the U.S. What we have found is that the common portrayal of BRICS as a China-dominated group primarily pursuing anti-U.S. agendas is misplaced.

Rather, the BRICS countries connect around common development interests and a quest for a multipolar world order in which no single power dominates. Yet BRICS consolidation has turned the group into a potent negotiation force that now challenges Washington’s geopolitical and economic goals. Ignoring BRICS as a major policy force – something the U.S. has been prone to do in the past – is no longer an option.

Reining in the America bashing

At the dawn of BRIC cooperation in 2008 – before South Africa joined in 2010, adding an “S” – members were mindful that the group’s existence could lead to tensions with policymakers who viewed the U.S. as the world’s “indispensable nation.”

As Brazil’s former Foreign Minister Celso Amorim observed at the time, “We should promote a more democratic world order by ensuring the fullest participation of developing countries in decision-making bodies.” He saw BRIC countries “as a bridge between industrialized and developing countries for sustainable development and a more balanced international economic policy.”

While such realignments would certainly dilute U.S. power, BRIC explicitly refrained from anti-U.S. rhetoric.

After the 2009 BRIC summit, the Chinese foreign ministry clarified that BRIC cooperation should not be “directed against a third party.” Indian Foreign Secretary Shivshankar Menon had already confirmed that there would be no America bashing at BRIC and directly rejected China’s and Russia’s efforts to weaken the dollar’s dominance.

Rather, the new entity complemented existing efforts toward multipolarity – including China-Russia cooperation and the India, Brazil, South Africa trilateral dialogue. Not only was BRIC envisioned as a forum for ideas rather than ideologies, but it also planned to stay open and transparent.

BRICS alignment and tensions with the US

Today, BRICS is a formidable group – it accounts for 41% of the world’s population, 31.5% of global gross domestic product and 16% of global trade. As such, it has a lot of bargaining power if the countries act together – which they increasingly do. During the Ukraine war, Moscow’s BRICS partners have ensured Russia’s economic and diplomatic survival in the face of Western attempts to isolate Moscow. Brazil, India, China and South Africa engaged with Russia in 166 BRICS events in 2022. And some members became crucial export markets for Russia.

The group’s political development – through which it has continually added new areas of cooperation and extra “bodies” – is impressive, considering the vast differences among its members.

We designed a BRICS convergence index to measure how BRICS states converged around 47 specific policies between 2009 and 2021, ranging from economics and security to sustainable development. We found deepening convergence and cooperation across these issues and particularly around industrial development and finance.

But BRICS convergence does not necessarily lead to greater tension with the United States. Our data finds limited divergence between the joint policies of BRICS and that of the U.S. on a wide range of issues. Our research also counters the argument that BRICS is China-driven. Indeed, China has been unable to advance some key policy proposals. For example, since the 2011 BRICS summit, China has sought to establish a BRICS free trade agreement but could not get support from other states. And despite various trade coordination mechanisms in BRICS, the overall trade among BRICS remains low – only 6% of the countries’ combined trade.

However, tensions between the United States and BRICS exist, especially when BRICS turns “bloc-like” and when U.S. global interests are at stake. The turning point for this was 2015, when BRICS achieved major institutional growth under Russia’s presidency. This coincided with Moscow enhancing its pivot to China and BRICS following Western sanctions over Russia’s annexation of Crimea in 2014. Russia was eager to develop alternatives to Western-led institutional and market mechanisms it could no longer benefit from.

That said, important champions of BRICS convergence are also close strategic partners to the U.S. For example, India has played a major role in strengthening the security dimension of BRICS cooperation, championing a counter-terrorism agenda that has drawn U.S. opposition due to its vague definition of terrorist actors.

Further constraints on U.S. power may emerge from BRICS transitioning to using local currencies over the dollar and encouraging BRICS candidate countries to do the same. Meanwhile, China and Russia’s efforts to engage BRICS on outer space governance is another trend for policymakers in Washington to watch.

Toward a US BRICS Policy?

So where does a more robust – and potentially larger – BRICS leave the U.S.?

To date, U.S. policy has largely ignored BRICS as an entity. The U.S. foreign and defense policymaking apparatus is regionally oriented. In the past 20 years, it has pivoted from the Middle East to Asia and most recently to the Indo-Pacific region.

When it comes to the BRICS nations, Washington has focused on developing bilateral relations with Brazil, India and South Africa, while managing tensions with China and isolating Russia. The challenge for the Biden administration is understanding how, as a group, BRICS’ operations and institutions affect U.S. global interests.

Meanwhile, BRICS expansion raises new questions. When asked about U.S. partners such as Algeria and Egypt wanting to join BRICS, the Biden administration explained that it does not ask partners to choose between the United States and other countries.

But the international demand for joining BRICS calls for a deeper reflection on how Washington pursues foreign policy.

Designing a BRICS-focused foreign policy is an opportunity for the United States to innovate around addressing development needs. Rather than dividing countries into friendly democracies and others, a BRICS-focused policy can see the Biden administration lead on universal development issues and build development-focused, close relationships that encourage a better alignment between countries of the Global South and the United States.

It could also allow the Biden administration to deepen cooperation with India, Brazil, South Africa and some of the new BRICS candidates. Areas of focus could include issues where the BRICS countries have struggled to coordinate their policy, such as AI development and governance, energy security and global restrictions on chemical and biological weapons.

Developing a BRICS policy could help re-imagine U.S. foreign policy and ensure that the United States is well positioned in a multipolar world.

Bitcoin and Ethereum had a bad day. After gaining a lot of upward momentum from late June after Blackrock, Fidelity, and Invesco filed to create bitcoin-related exchange traded funds (ETFs), the volatile assets have shown cryptocurrency investors that the bumpy ride is not yet over. What’s causing it this time? Fortunately, it is not fraud or wrongdoing creating the turbulence. Instead, three factors external to the business of trading, mining, or exchanging digital assets are at work.

Background

On Thursday, August 17, and accelerating on August 18, the largest cryptocurrencies dropped precipitously. Bitcoin even broke down and fell below the psychologically important $26,000 US dollar price level before bouncing. While some are pointing to CME options expiration on the third Friday of each month, most are pointing to a Wall Street Journal article, and blaming Elon Musk, as the reason the asset class was nudged off a small cliff. There are other less highlighted, but important, catalysts that added to the flash-crash; these, along with the WSJ story, will be explained below.

Smells like Musk

What could SpaceX, the company owned and run by Elon Musk, possibly have to do with a crypto selloff? On Thursday, the crypto market had a downward spike around 5 PM ET. It was just after the Wall Street Journal revealed a change in the accounting valuation of SpaceX’s crypto assets. Reportedly, SpaceX marked down the value of its bitcoin assets by a substantial $373 million over the past two years. Additionally, the company has executed on crypto asset divestitures as well. When the reduction took place is uncertain, but cryptocurrency holdings have been reduced both in terms of the amount of coins and the value each coin is held for on the books.

Elon Musk’s reputation is that of a forward thinker, and one that embraces, if not leads, technology. He has significant influence over cryptocurrency valuations, often instigating pronounced market fluctuations brought about by Musk’s influential posts on his social media company, X. The reduction coincides with a similar crypto reduction on the books of publicly held, Musk-led, Tesla (TSLA). The electric car manufacturer had previously disclosed in its annual earnings report that it had liquidated 75% of its bitcoin reserves.

While it should not be surprising that two companies stepped away from speculation on something unrelated to their business or lowered support for the still young blockchain technology, it gave a reason for a reaction to this and other festering dynamics.

Wary of Gary

The Chairman of the Securities and Exchange Commission (SEC), Gary Gensler, is viewed as a “Whack-a Mole” to crypto stakeholders that prefer more autonomy than regulation. Every time the SEC gets knocked down as a potential regulator, it resurfaces, and crypto businesses have to deal with the agency again.

Last month, Judge Analisa Torres made a pivotal decision in a case involving payment company Ripple Labs and the Commission. Her verdict declared that a substantial portion of sales of the token XRP did not fall under the category of securities transactions. The SEC claimed it was a security. This judgement was hailed as a triumph for the crypto sector and catalyzed an impressive 20% uptick in the exchange Coinbase’s stock in a single day.

On the same Thursday as the WSJ article, the SEC showed its face again with a strong response to the earlier ruling. Judge Torres allowed the SEC’s request for an “interlocutory” appeal on her ruling. This process will involve the SEC presenting its motion, followed by Ripple’s counterarguments. This is slated to continue until mid-September. Afterward, the Judge will determine whether the agency can effectively challenge her token classification ruling in an appellate court.

The still young asset class, its exchange methods, valuation, and usage techniques, once they are more clearly defined, will serve to add stability and reduce risk and shocks in crypto and the surrounding businesses. The longer the legal system and regulatory entities take, including Congress, the longer it will take for cryptocurrencies to find the more settled mainstream place in the markets they desire.

Rate Spate

The eighteen-month-long spate of rate hikes in the U.S. and across the globe is providing an alternative investment choice instead of what are viewed as riskier assets. Coincidentally, again on Thursday, August 17, the ten-year US Treasury Note hit a yield higher than the markets have experienced in 12 years. At 4.31%, investors can lock in a known annual return for ten years that exceeds the current and projected inflation rate.

Take Away

The volatility in the crypto asset class has been dramatic – not for the weak-stomached investor. On the same day in August, three unrelated events together helped cause the asset class to spike down. These include an article in a top business news publication indicating that one of the world’s most recognized cryptocurrency advocates has reduced bitcoin’s exposure to his companies. The SEC being granted a rematch in a landmark case that it had recently lost, where the earlier outcome gave no provision for the SEC to treat cryptocurrencies like a security. And rounding out the triad of events on crypto’s throttleback Thursday, yields are up across the curve to levels not seen in a dozen years. Investor’s seeking a place to reduce risk can now provide themselves with interest payments in excess of inflation.

But despite the ups and downs, bitcoin is up 56.7% year-to-date, 11.1% over the past 12 months, 110.5% over three years, 300% over five years, and astronomical amounts over longer periods. Related companies like bitcoin miners, crypto exchanges, and blockchain companies have also experienced growth similar to that found in few other industries over the past decade.