BOCA RATON, Fla.–(BUSINESS WIRE)–Jul. 26, 2023– The ODP Corporation (“ODP,” or the “Company”) (NASDAQ:ODP), a leading provider of business services, products and digital workplace technology solutions to businesses and consumers will announce second quarter 2023 financial results before the market open on Wednesday, August 9th, 2023. The ODP Corporation will webcast a call with financial analysts and investors that day at 9:00 am Eastern Time which will be accessible to the media and the general public.

To listen to the conference call via webcast, please visit The ODP Corporation’s Investor relations website at investor.theodpcorp.com. A replay of the webcast will be available approximately two hours following the event. A copy of the earnings press release, supplemental financial disclosures and presentation will also be available on the website.

About The ODP Corporation

The ODP Corporation (NASDAQ:ODP) is a leading provider of products and services through an integrated business-to-business (B2B) distribution platform and omnichannel presence, which includes world-class supply chain and distribution operations, dedicated sales professionals, a B2B digital procurement solution, online presence and a network of Office Depot and OfficeMax retail stores. Through its operating companies Office Depot, LLC; ODP Business Solutions, LLC; Veyer, LLC; and Varis, Inc., The ODP Corporation empowers every business, professional, and consumer to achieve more every day. For more information, visit theodpcorp.com.

ODP and ODP Business Solutions are trademarks of ODP Business Solutions, LLC. Office Depot is a trademark of The Office Club, LLC. OfficeMax is a trademark of OMX, Inc. Veyer is a trademark of Veyer, LLC. Varis is a trademark of Varis Inc. Grand&Toy is a trademark of Grand & Toy, LLC in Canada. Any other product or company names mentioned herein are the trademarks of their respective owners.

Worldcoin Crypto Project Launched by OpenAI’s Sam Altman

In a revolutionary move, OpenAI CEO Sam Altman began rolling out Worldcoin on July 24. The cryptocurrency project aims to reinvent the way the world identifies living, breathing humans compared to AI bots. The core offering of Worldcoin is its innovative World ID, often described as a “digital passport” that serves as proof of a person’s human identity. But that is just the beginning of the project goals.

To obtain a World ID, users must undergo an in-person iris scan using Worldcoin’s revolutionary ‘orb.’ This silver ball, about the size of a bowling ball, ensures the legitimacy of the individual’s identity, subsequently creating the unique World ID.

The brains behind this revolutionary project are the San Francisco and Berlin-based organization, Tools for Humanity. During its beta phase, the project amassed an impressive 2 million users, and with the official launch on Monday, Worldcoin is rapidly expanding its ‘orbing’ operations to 35 cities across 20 countries.

In select countries, early adopters will be rewarded with Worldcoin’s own cryptocurrency token, WLD. This incentive has already driven WLD’s price to soar after the announcement. On Binance, the world’s largest, WLD reached a peak price of $5.29 and continued to trade at $2.49 (from an initial starting price of $0.15) as of 11:00 AM ET. Notably, the trading volume on Binance has reached a staggering $25.1 million.

The Role of Blockchain

Blockchains play a crucial role in this project, as they securely store World IDs while preserving user privacy and preventing any single entity from controlling or shutting down the system, according to co-founder Alex Blania.

One key application of World IDs is its ability to distinguish between real individuals and AI bots in the age of generative AI chatbots like ChatGPT, which are adept at mimicking human language. By leveraging World IDs, online platforms can effectively combat the infiltration of AI bots into human interactions.

Economic Implications of AI

Altman emphasized the economic implications of AI, stating that people will be profoundly impacted by AI’s capabilities. “People will be supercharged by AI, which will have massive economic implications,” he said.

One interesting example of what Altman believes AI can eventually provide is universal basic income (UBI), a social benefits program aimed at providing financial support to every individual. According to Altman, as AI gradually takes over many human tasks, UBI can play a vital role in mitigating income inequality. Since World IDs are exclusive to genuine human beings, they can act as a safeguard against fraud in UBI distributions.

Though Altman acknowledged that a world with widespread UBI is likely in the distant future and the logistics of such a system are still unclear, he believes that Worldcoin paves the way for experiments and solutions to tackle this societal challenge.

The launch of Worldcoin marks a significant step in the convergence of cryptocurrency and AI technologies, with potential far-reaching effects on how we identify ourselves and interact in the digital age. As the project gains momentum, financial market professionals should closely monitor the developments surrounding Worldcoin and its impact on the future of money.

Image: The author attending a stylish financial industry event in Boca Raton, FL

The Emerging Financial Centers and the Brain Drain from Other Cities are Changing Where Deals Get Done

They used to call it “god’s waiting room,” now they call it home.

If you haven’t guessed, I’m talking about Florida, and more specifically, the big-name financial firms that have either moved their headquarters to “Wall Street South” or have built a much larger presence in West Palm Beach, Miami, Fort Lauderdale, or the Tampa area. I made the move myself some years back after more than 20 years managing large funds for some of the most prestigious firms in NYC – now, some of those very firms are discovering what I have learned, that the weather, costs, and culture make both living and working a lot easier.

Each investment company that chooses South Florida as a region to grow its firm, brings even more sophisticated investors and dealmakers to those already in the state —face-to-face networking is now high caliber and done with ease. Everyone in the industry is benefitting from the closer proximity to each other and being able to meet and make introductions in an environment that, in my opinion, is much more conducive to making acquaintances, building trust, and even having some fun.

Florida is a Disruptor

My old firm, Goldman Sachs, just built out 35,000 feet of office space in the Miami, Brickell area. This is on top of their ongoing presence in Miami and West Palm Beach. They aren’t alone, the absence of a state income tax, coupled with a government that is business-friendly helped prompt hedge fund billionaires and native New Yorkers Paul Singer and Carl Icahn to relocate their firms to Florida.

Other prestigious firms have done the same; Blackstone opened an office in Downtown Miami in 2021. Citadel, relocated its headquarters from Chicago to Miami in 2021. D1 Capital Partners, a hedge fund, announced plans to relocate to South Florida in 2022. Merrill Lynch expanded its presence within Florida a bit sooner, 2020. Hedge fund, Tiger Global Management, announced plans to relocate to South Florida in 2022. In November of 2022, fund manager Ark Invest founded by Cathie Wood moved its headquarters out of NYC to St. Petersburg, FL. And the list goes on, and is growing.

In addition to lower costs of business, the areas these companies are moving to offer an educated base and a financially astute talent pool from which to hire.

And the financially savvy populous is getting deeper as professionals looking to relocate out of colder, high tax states, are moving down and becoming part of the already strong ecosystem. The ever-increasing depth of players include experienced attorneys, accountants, bankers, consultants, insurers, IT experts, and others with which to conduct world-class business dealings.

The other ingredients are here as well. Asset managers require convenient public and private executive airports. Local officials must also be conversant enough in their industry to regulate it intelligently, S. Florida checks both of those boxes too. It takes more than one large asset management firm to generate a demand for services sufficient to build the critical mass necessary to sustain an ecosystem. Florida has passed the tipping point and has already been labeled “Wall Street South.”

Florida Infrastructure

The ecosystem also includes facilities for tradeshows, networking events, and conferences. As an example, this coming December 3-5, Noble Capital Markets, a boutique investment bank located in Boca Raton, FL, will hold its massive, 19th annual investment conference, NobleCon19, at the 52,000 square foot, state-of-the art facility just opened on the Florida Atlantic University campus (FAU), in Boca Raton.

Noble’s 19th Annual Small-cap Investor Conference has been the “must-go” event in the area for 19 years. In 2023 the Noble can now expand this annual event into a facility that boasts the latest technology and conference facilities. This means investors and presenters at NobleCon19 will have an ideal setting to discover new opportunities and more room to welcome and network with the areas new financial executive neighbors, along with other attendees from across the globe.

From Good to Great

There are three defining factors that have helped the S. Florida region grow from an area with many small and mid-size financial firms to a strong and expanding financial center.

In no particular order, these include:

Greater reliance on virtual teams now makes physical proximity to key players less important . Even as many firms reel staff back into the office, companies are far more comfortable reaching team members virtually.

More associated professionals are moving to the emerging centers. When major investors and financial services giants such as Goldman Sachs, Blackstone, Citadel,Ark Invest, and Icahn Enterprises set up shop in a location, expertise follows. This is almost a requirement in sectors such as private equity, where deals are paved by personal relationships, social networks and professional networks.

The major cities in Florida already have existing professional and educational infrastructures. Of course, if the firms leadership is from out of town, it will naturally have a bias in favor of the schools they attended or are familiar with. But it is becoming easier to lose that bias when they learn that, for instance, in Palm County, Florida Atlantic University College of Business’ Executive Education just earned a prestigious global endorsement in the 2023 Financial Times rankings for open enrollment professional education programs – FAU ranked No. 2 in the United States.

Home Life

As one might imagine, with thousands of highly paid professionals looking for homes and “their new favorite restaurants” that real estate values are increasing and entire neighborhoods are becoming wealthier at every level. This growth feeds on itself and the improvements draw more top talent that then call South Florida the place they live and work.

Take Away

South Florida lost its reputation as a large retirement home where Grandma lives, and is now seen as an emerging financial powerhouse where big and small financial firms want to be to do business, grow their network, and live a better life.

With modern infrastructure, lower costs, top professionals, entertainment, and state of the art conference facilities, the trend is likely to continue.

Strategic restructuring follows comprehensive review of company’s growth and efficiency objectives as part of ongoing transformation

Aggressive action builds on strategic progress to monetize non-core assets, reinvest capital in organic and inorganic growth initiatives, and shift to higher-margin, higher-growth business mix

Actions expected to result in meaningful, sustainable EBITDA margin expansion beginning immediately, and substantial improvement in the second half of 2023 and beyond

TROY, Mich., July 20, 2023 /PRNewswire/ — Kelly (Nasdaq: KELYA, KELYB), a leading global specialty talent solutions provider, today announced strategic restructuring actions that will further optimize the company’s operating model to enhance organizational efficiency and effectiveness. These actions are part of the comprehensive transformation initiative the company announced in May to drive EBITDA margin improvement and accelerate long-term profitable growth.

The strategic restructuring actions realign business-critical resources to Kelly’s business units, streamline corporate resources, reduce redundant organizational layers, and optimize work processes. These structural changes simplify the company’s operations and unlock additional resources to invest in growth. As a result of these actions, the company has implemented a workforce reduction plan and notified affected employees in accordance with applicable employment laws and regulations. Employees whose roles were included in the workforce reduction are eligible for applicable severance, benefits, and outplacement services.

“Today marks a difficult but necessary step forward on Kelly’s journey to accelerate profitable growth,” said Peter Quigley, president and chief executive officer. “These actions follow an exhaustive review of the company’s business and functional operations to determine how we can work more efficiently to improve profitability over the long term. I am confident the structural improvements we have made to Kelly’s operating model position the company to pursue new avenues of growth that will enable it to deliver greater value for customers, talent, and shareholders.”

As a result of the strategic restructuring actions, Kelly expects to see meaningful expansion of its EBITDA margin beginning immediately with substantial improvement in the second half of 2023 and beyond. The company expects to incur a restructuring charge from these actions in the range of $7.5-$8.5 million in the third quarter of 2023. Mr. Quigley and Olivier Thirot, executive vice president and chief financial officer, will provide additional details about the strategic restructuring as it relates to the company’s ongoing transformation, including expectations for EBITDA margin improvement, during its upcoming second-quarter earnings conference call on August 10, 2023.

About Kelly®

Kelly Services, Inc. (Nasdaq: KELYA, KELYB) helps companies recruit and manage skilled workers and helps job seekers find great work. Since inventing the staffing industry in 1946, we have become experts in the many industries and local and global markets we serve. With a network of suppliers and partners around the world, we connect more than 450,000 people with work every year. Our suite of outsourcing and consulting services ensures companies have the people they need, when and where they are needed most. Headquartered in Troy, Michigan, we empower businesses and individuals to access limitless opportunities in industries such as science, engineering, technology, education, manufacturing, retail, finance, and energy. Revenue in 2022 was $5.0 billion. Learn more at kellyservices.com.

Forward-Looking Statements

This release contains statements that are forward looking in nature and, accordingly, are subject to risks and uncertainties. These statements are made under the “safe harbor” provisions of the U.S. Private Securities Litigation Reform Act of 1995. Statements that are not historical facts, including statements about Kelly’s financial expectations, are forward-looking statements. Factors that could cause actual results to differ materially from those contained in this release include, but are not limited to, (i) changing market and economic conditions, (ii) disruption in the labor market and weakened demand for human capital resulting from technological advances, loss of large corporate customers and government contractor requirements, (iii) the impact of laws and regulations (including federal, state and international tax laws), (iv) unexpected changes in claim trends on workers’ compensation, unemployment, disability and medical benefit plans, (v) litigation and other legal liabilities (including tax liabilities) in excess of our estimates, (vi) our ability to achieve our business’s anticipated growth strategies, (vi) our future business development, results of operations and financial condition, (vii) damage to our brands, (viii) dependency on third parties for the execution of critical functions, (ix) conducting business in foreign countries, including foreign currency fluctuations, (x) availability of temporary workers with appropriate skills required by customers, (xi) cyberattacks or other breaches of network or information technology security, and (xii) other risks, uncertainties and factors discussed in this release and in the Company’s filings with the Securities and Exchange Commission. In some cases, forward-looking statements can be identified by words or phrases such as “may,” “will,” “expect,” “anticipate,” “target,” “aim,” “estimate,” “intend,” “plan,” “believe,” “potential,” “continue,” “is/are likely to” or other similar expressions. All information provided in this press release is as of the date of this press release and we undertake no duty to update any forward-looking statement to conform the statement to actual results or changes in the Company’s expectations.

BRENTWOOD, Tenn., July 19, 2023 (GLOBE NEWSWIRE) — CoreCivic, Inc. (NYSE: CXW) (the Company) announced today that it will release its 2023 second quarter financial results after the market closes on Monday, August 7, 2023. A live broadcast of CoreCivic’s conference call will begin at 10:00 a.m. central time (11:00 a.m. eastern time) on Tuesday, August 8, 2023.

To participate via telephone and join the call live, please register in advance here https://register.vevent.com/register/BI245ce05fd4c64a6ead7845124358177d. Upon registration, telephone participants will receive a confirmation email detailing how to join the conference call, including the dial-in number and a unique passcode.

Participants may access the audio-only webcast of the conference call from the Company’s website at www.corecivic.com under the “Events & Presentations” section of the “Investors” page. A replay of the webcast will be available for seven days.

About CoreCivic

CoreCivic is a diversified, government-solutions company with the scale and experience needed to solve tough government challenges in flexible, cost-effective ways. We provide a broad range of solutions to government partners that serve the public good through high-quality corrections and detention management, a network of residential and non-residential alternatives to incarceration to help address America’s recidivism crisis, and government real estate solutions. We are the nation’s largest owner of partnership correctional, detention and residential reentry facilities, and believe we are the largest private owner of real estate used by government agencies in the United States. We have been a flexible and dependable partner for government for 40 years. Our employees are driven by a deep sense of service, high standards of professionalism and a responsibility to help government better the public good. Learn more at www.corecivic.com.

BRENTWOOD, Tenn., June 14, 2023 (GLOBE NEWSWIRE) — CoreCivic, Inc. (NYSE: CXW) (CoreCivic or the Company) announced today it has entered into a lease agreement with the Oklahoma Department of Corrections (ODOC) for the company-owned, 1,670-bed Davis Correctional Facility (DCF), which the Company currently operates under a management contract with ODOC that is currently scheduled to expire on June 30, 2023. CoreCivic expects to enter into a 90-day contract extension for the current management contract, after which time operations will transfer from CoreCivic to ODOC in accordance with the new lease agreement. The new lease agreement includes a base term commencing October 1, 2023, with a scheduled expiration date of June 30, 2029, and unlimited two-year renewal options.

Terms of the 90-day contract extension are expected to remain consistent with the existing management contract at the DCF. Annual rental revenue generated from the ODOC at the DCF under the new lease agreement will be $7.5 million during the base term and will be reported in the CoreCivic Properties business segment upon lease commencement.

About CoreCivic

CoreCivic is a diversified, government-solutions company with the scale and experience needed to solve tough government challenges in flexible, cost-effective ways. CoreCivic provides a broad range of solutions to government partners that serve the public good through high-quality corrections and detention management, a network of residential and non-residential alternatives to incarceration to help address America’s recidivism crisis, and government real estate solutions. CoreCivic is the nation’s largest owner of partnership correctional, detention and residential reentry facilities, and one of the largest prison operators in the United States. CoreCivic has been a flexible and dependable partner for government for 40 years. CoreCivic’s employees are driven by a deep sense of service, high standards of professionalism and a responsibility to help government better the public good. Learn more at www.corecivic.com.

Forward-Looking Statements

This press release contains statements as to CoreCivic’s beliefs and expectations of the outcome of future events that are “forward-looking” statements within the meaning of Section 21E of the Securities Exchange Act of 1934, as amended, and the Private Securities Litigation Reform Act of 1995, as amended. These forward-looking statements are subject to risks and uncertainties that could cause actual results to differ materially from the statements made. These include, but are not limited to, the risks and uncertainties associated with executing a contract extension of the current management contract under substantially the same terms as the existing management contract, the successful transition of operations from CoreCivic to ODOC, and the financial impact of the new lease agreement.

CoreCivic takes no responsibility for updating the information contained in this press release following the date hereof to reflect events or circumstances occurring after the date hereof or the occurrence of unanticipated events or for any changes or modifications made to this press release or the information contained herein by any third-parties, including, but not limited to, any wire or internet services.

TROY, Mich., June 7, 2023 /PRNewswire/ — Kelly (Nasdaq: KELYA, KELYB), a leading specialty talent solutions provider, today announced it will participate in the Sidoti Virtual Investor Conference on Wednesday, June 14, 2023.

Olivier Thirot, executive vice president and chief financial officer, and James Polehna, chief investor relations officer and corporate secretary, will participate in virtual one-on-one meetings. A copy of Kelly’s investor presentation is also available at kellyservices.com.

About Kelly®

Kelly Services, Inc. (Nasdaq: KELYA, KELYB) helps companies recruit and manage skilled workers and helps job seekers find great work. Since inventing the staffing industry in 1946, we have become experts in the many industries and local and global markets we serve. With a network of suppliers and partners around the world, we connect more than 450,000 people with work every year. Our suite of outsourcing and consulting services ensures companies have the people they need, when and where they are needed most. Headquartered in Troy, Michigan, we empower businesses and individuals to access limitless opportunities in industries such as science, engineering, technology, education, manufacturing, retail, finance, and energy. Revenue in 2022 was $5.0 billion. Learn more at kellyservices.com.

This Week Will Feature Few Economic Releases and a Focus on Next Weeks FOMC

The week ahead is quiet on the economic release front. And there won’t be any market moving Fed president addresses to keep the market on its toes; the Fed members are in a blackout period leading up to next week’s June 13-14 FOMC meeting.

The markets can also stop talking about whether the US will default on debt as the short end of the fixed-income market will have to adjust to a sudden but short-lived increase in US Treasury bills.

Monday 6/5

10:00 AM ET, Factory Orders are expected to have risen 0.8 percent in April versus March’s 0.9 percent rise. Durable Goods Orders for April, which have already been released and are one of two major components of this report, rose 1.1 percent on the month. Factory Orders are a leading indicator, it represents the dollar level of new orders for both durable and nondurable goods.

10:00 AM ET, The Institute for Supply Management Services (ISM Services) is expected to be relatively steady at 52 for May after a 51.9 print in April.

Tuesday 6/6

Nothing Scheduled

Wednesday 6/7

8:30 PM ET, International Trade in Goods and Services is expected to show a deficit of $75.4 billion for April for total goods and services trade which would compare with a $64.2 billion deficit in March. Advance data on the goods side of April’s report showed a very large $12.1 billion deepening in the deficit.

10:30 AM ET, The Energy Information Administration (EIA) will be providing its scheduled weekly information on petroleum inventories, whether produced in the US or abroad. The level of inventories helps determine prices for petroleum products.

3:00 PM ET, Consumer Credit is expected to have increased by $21.0 billion in April versus an increase of $26.5 billion in March. This report has surprised on the high side the last three months.

Thursday 6/8

8:30 AM ET, Jobless claims for the week ending June 3 are expected to have increased to 240,000 versus 232,000 in the prior week. This has been a very closely watched report as it is expected it has indicated the Fed has room to tighten further if other data remain too strong.

10:00 AM ET, Wholesale Inventories will be released as a second estimate before the final. The second estimate for April is expected to be a 0.2 percent decline, unchanged from the first estimate. Wholesale trade measures the dollar value of sales made and inventories held by merchant wholesalers. It is a component of business sales and inventories Corporate Profits are pulled from the national income and product accounts (NIPA) and are presented in different forms.

4:30 PM ET, The Federal Reserve’s Balance Sheet has attracted additional attention as it is a good indicator of whether it is following its quantitative tightening plan, and whether there has been a significant change in banks looking to the Fed, which may mean trouble in the sector. For the week ending June 7, the Federal Reserve is expected to hold assets worth $8.386 trillion. This would be a week-on-week decline of $50.4 billion. All non-cash assets can be viewed as money that at one time was injected into the economy as stimulation.

Friday 6/9

10:00 AM ET, The Quarterly Services Survey focuses on information and technology-related service industries. These include information; professional, scientific and technical services; administrative & support services; and waste management and remediation services. Services revenue is expected to have increased by 2.9%.

What Else

The key factors that the Fed will consider when making their decision next week at the FOMC meeting are the pace and trend of economic growth, the level of inflation, the strength of the labor market, and the risk of recession.

Additionally, the FOMC will have to determine if the moves to date will have a more substantial impact over time. Currently, inflation is not coming down, jobs are abundant relative to job seekers, and the risk of a recession over the next two quarters seems low. For these reasons, some believe the Fed will remain hawkish yet pause for this meeting. However, next week during the first day of the two-day meeting CPI (consumer inflation) will be released. It would be premature to forecast a Fed decision until the contents of that report are known.

Reliable Data, Not Emotions, are Pointing to a Growing U.S. Economy

In roughly one month, we will be halfway through 2023. While many point to the Fed’s pace of tightening and the downward sloping yield curve, as a reason to run around like Chicken Little warning of a coming recession, a fresh read of the economic tea leaves tells a different story. Just today, May 23, the PMI Output Index (PMI) rose to its highest reading in over a year. Home sales figures were also reported to show that new homes in May sold at the highest rate in over a year. These are both reliable leading indicators that point to growth in both services and manufacturing.

U.S. Composite PMI Output Index

Business activity in the U.S. increased to a 13-month high in May due in large part to strong growth in the services sector. This is a reliable indication that economic expansion has growing momentum. Despite the negative talk of those that are concerned that the Fed has lifted interest rates closer to historical norms and that the yield curve is still inverted, in part due to Covid era Fed yield-curve-control, the numbers suggest less caution might be warranted.

S&P Global said on Tuesday (May 23) its flash U.S. Composite PMI Output Index, which tracks the manufacturing and services sectors, rose to a reading of 54.5 this month. It indicates the highest level since April 2022 and is up from a reading of 53.4 in April. A reading above 50 indicates growth, this is the fourth consecutive month it has been above 50. The consensus among economists was only 52.6.

Home Sales

One sector that is directly impacted by interest rates is real estate. However, new home sales rose in April, this is a clear sign that prospective buyers are making deals with builders.

New homes in April were sold at a seasonally-adjusted annual rate of 683,000, Its the highest rate since March 2022. The April data represents a 4.1% gain from March’s revised rate of 656,000,. The report was from the Census and Department of Housing and Urban Development and was reported Tuesday May 23. Economists had expected new home sales to decline to 670,000 from a March rate of 683,000. It was the largest month-over-month increase since December 2022.

Leading Indicators

PMI is forward-looking as it surveys purchasing managers’ expectations and intentions for the coming months. By capturing their sentiment on future orders, production plans, and hiring intentions, PMI offers insights into economic trends that have yet to be reflected in other after-the-fact indicators.

Home sales are considered a leading indicator because they can serve as a measure of other needs and broader economic trends. Home sales have a significant impact on related sectors, such as construction, home improvement, finance, and consumer spending. Changes in home sales can influence economic activity and indicate shifts in consumer confidence, employment levels, and overall economic health.

While many economic reports offer rear-view mirror data, these reports are true indicators of business behavior as it plans for future expectations, and consumer behavior as it is confident that it will have the resources available to purchase and outfit a new home.

The upbeat reports prompted the Atlanta Federal Reserve to raise its second-quarter gross domestic product estimate to a 2.9% annualized rate from a 2.6% pace. The economy grew at a 1.1% rate in the first quarter.

Take Away

Many economists are negative about the economic outlook later this year. Market participants have been positioning themselves with the notion that there may be a late year recession. Is the notion misguided? Recent data suggests there may be buying opportunities for those willing to go against the tide of pundits preaching recession.

No one has a crystal ball. In good markets and bad, there is no replacement for good research before you put on a position, and then for as long as the position remains in your portfolio.

Channelchek is a great resource for information to follow the companies not likely being reported in traditional outlets. Turn to this online free resource as you evaluate small and microcap stocks.

TROY, Mich., May 19, 2023 /PRNewswire/ — Kelly (Nasdaq: KELYA, KELYB), a leading specialty talent solutions provider, today announced that at its 2023 Annual Shareholders Meeting held on May 17, 2023, Kelly shareholders elected nine individuals to serve one-year terms on its board of directors.

The newly elected directors are Gerald S. Adolph, retired senior partner, strategy and M&A, Booz & Co.; George S. Corona, retired president and chief executive officer, Kelly; Robert S. Cubbin, retired president and chief executive officer, Meadowbrook Insurance Group, Inc.; Amala Duggirala, executive vice president and chief information officer, United Services Automobile Association (USAA); InaMarie Felix Johnson, former chief people and diversity officer, Zendesk, Inc.; Terrence B. Larkin, retired executive vice president, business development, general counsel and corporate secretary, Lear Corporation; Leslie A. Murphy, CPA, president and chief executive officer, Murphy Consulting, Inc.; Donald R. Parfet, managing director, Apjohn Group, LLC; and Peter W. Quigley, president and chief executive officer, Kelly.

Following the election of the board of directors, the board appointed Mr. Larkin to the position of chairman of the board, effective immediately. An attorney with 28 years of experience in business law, Mr. Larkin has served as an independent director on Kelly’s board since 2010 and brings a valuable combination of complex problem-solving skills, legal and governance expertise, and global experience. He succeeds Mr. Parfet, who has elected to step down as chairman of the board, a position in which he has served since 2018. Mr. Parfet will continue his service on Kelly’s board as an independent director.

“On behalf of the entire board of directors, I would like to thank Don for his distinguished leadership during the last five years. Kelly has benefited immensely from his guidance and insights as the Company has executed its specialty strategy and transformed its portfolio,” said Mr. Larkin. “I am grateful for the opportunity to serve as Kelly’s next chairman, and I look forward to continuing to work with Don and the rest of the board to carry out our responsibility to Kelly’s shareholders as the Company embarks on the next phase of its growth journey.”

About Kelly®

Kelly Services, Inc. (Nasdaq: KELYA, KELYB) helps companies recruit and manage skilled workers and helps job seekers find great work. Since inventing the staffing industry in 1946, we have become experts in the many industries and local and global markets we serve. With a network of suppliers and partners around the world, we connect more than 450,000 people with work every year. Our suite of outsourcing and consulting services ensures companies have the people they need, when and where they are needed most. Headquartered in Troy, Michigan, we empower businesses and individuals to access limitless opportunities in industries such as science, engineering, technology, education, manufacturing, retail, finance, and energy. Revenue in 2022 was $5.0 billion. Learn more at kellyservices.com.

Q1 revenue down 2.2%; down 1.4% in constant currency; organic revenue nearly flat (down 0.5% in constant currency)

Q1 gross profit down 1.7%; down 0.8% in constant currency; delivered continued improvement in GP rate, 20.0%, up 10 bps year-over-year

Q1 operating earnings of $10.7 million, including a $5.7 million restructuring charge, or $16.4 million on an adjusted basis

Initiated a comprehensive business transformation program to significantly improve EBITDA margin

TROY, Mich., May 11, 2023 /PRNewswire/ — Kelly (Nasdaq: KELYA, KELYB), a leading specialty talent solutions provider, today announced results for the first quarter of 2023.

Peter Quigley, president and chief executive officer, announced revenue for the first quarter of 2023 totaled $1.3 billion, a 2.2% decrease, or 1.4% decrease in constant currency, compared to the corresponding quarter of 2022, with organic, constant currency revenue down 0.5%. Year-over-year revenue trends were impacted by foreign currency headwinds and the impact of the sale of Russian operations in July 2022. Year-over-year results in the quarter also reflect the impact of the 2022 acquisitions of RocketPower, a recruitment process outsourcing firm, and Pediatric Therapeutic Services, a specialty firm providing in-school therapy services.

“Taking into account well recognized macroeconomic headwinds, we delivered solid results as our specialty solutions proved more resilient than others. Our Education segment and our more profitable outcome-based solutions in both P&I and SET continued to deliver solid growth, while, as expected, our staffing businesses faced decreased demand in this environment,” said Quigley.

Kelly reported operating earnings in the first quarter of 2023 of $10.7 million, compared to earnings of $23.4 million reported in the first quarter of 2022. Earnings in the first quarter of 2023 included a $5.7 million restructuring charge. The restructuring charge reflects cost management actions in response to the current demand levels and to reposition the Professional & Industrial staffing business to better capitalize on opportunities in local markets. Excluding the restructuring charge, adjusted earnings from operations were $16.4 million. Earnings in the first quarter of 2022 included a $0.9 million gain on sale of assets and adjusted earnings were $22.5 million. Adjusted earnings declined year-over-year primarily as a result of lower revenues.

Earnings per share in the first quarter of 2023 were $0.29 compared to a loss per share of $1.23 in the first quarter of 2022. Included in the earnings per share in the first quarter of 2023 is an $0.11 per share restructuring charge, net of tax. Included in the first quarter of 2022 is a $1.69 loss per share, net of tax, on the sale of Kelly’s investment in Persol Holdings common shares and related transactions, partially offset by a $0.02 per share gain on sale of real property, net of tax. On an adjusted basis, earnings per share were $0.40 in the first quarter of 2023, a decline of 9% from $0.44 per share in the corresponding quarter of 2022.

As Kelly approaches the three-year anniversary of its operating model, Quigley went on to introduce a new phase in the company’s journey toward profitable growth. “We have made progress on our growth journey. Now, with an eye to the future, we are taking a bold approach to accelerate profitable growth. I’ve established a Transformation Management Office reporting directly to me and engaged an expert consulting firm to support our aggressive ambitions to create structural improvements in our business designed to convert our revenue and gross margin gains to significantly improve our EBITDA.” Quigley noted that regular progress updates will be provided starting in August.

Kelly also reported that on May 9, its board of directors declared a dividend of $0.075 per share. The dividend is payable on June 6, 2023, to shareholders of record as of the close of business on May 22, 2023.

In conjunction with its first-quarter earnings release, Kelly has published a financial presentation on the Investor Relations page of its public website and will host a conference call at 9 a.m. ET on May 11 to review the results and answer questions. The call may be accessed in one of the following ways:

Via the Telephone (877) 692-8955 (toll free) or (234) 720-6979 (caller paid) Enter access code 5728672 After the prompt, please enter ”#”

A recording of the conference call will be available after 2:30 p.m. ET on May 11, 2023, at (866) 207-1041 (toll-free) and (402) 970-0847 (caller-paid). The access code is 4789007#. The recording will also be available at kellyservices.com during this period.

This release contains statements that are forward looking in nature and, accordingly, are subject to risks and uncertainties. These factors include, but are not limited to, changing market and economic conditions, the impact of the novel coronavirus (COVID-19) outbreak, competitive market pressures including pricing and technology introductions and disruptions, disruption in the labor market and weakened demand for human capital resulting from technological advances, competition law risks, the impact of changes in laws and regulations (including federal, state and international tax laws), unexpected changes in claim trends on workers’ compensation, unemployment, disability and medical benefit plans, or the risk of additional tax liabilities in excess of our estimates, our ability to achieve our business strategy, our ability to successfully develop new service offerings, material changes in demand from or loss of large corporate customers as well as changes in their buying practices, risks particular to doing business with government or government contractors, the risk of damage to our brands, our exposure to risks associated with services outside traditional staffing, including business process outsourcing, services of licensed professionals and services connecting talent to independent work, our increasing dependency on third parties for the execution of critical functions, our ability to effectively implement and manage our information technology strategy, the risks associated with past and future acquisitions, including risk of related impairment of goodwill and intangible assets, exposure to risks associated with certain equity investments, including with strategic partners, risks associated with conducting business in foreign countries, including foreign currency fluctuations, risks associated with violations of anti-corruption, trade protection and other laws and regulations, availability of qualified full-time employees, availability of temporary workers with appropriate skills required by customers, liabilities for employment-related claims and losses, including class action lawsuits and collective actions, our ability to sustain critical business applications through our key data centers, risks arising from failure to preserve the privacy of information entrusted to us or to meet our obligations under global privacy laws, the risk of cyberattacks or other breaches of network or information technology security, our ability to realize value from our tax credit and net operating loss carryforwards, our ability to maintain specified financial covenants in our bank facilities to continue to access credit markets, and other risks, uncertainties and factors discussed in this release and in the Company’s filings with the Securities and Exchange Commission. Actual results may differ materially from any forward-looking statements contained herein, and we undertake no duty to update any forward-looking statement to conform the statement to actual results or changes in the Company’s expectations.

About Kelly®

Kelly Services, Inc. (Nasdaq: KELYA, KELYB) helps companies recruit and manage skilled workers and helps job seekers find great work. Since inventing the staffing industry in 1946, we have become experts in the many industries and local and global markets we serve. With a network of suppliers and partners around the world, we connect more than 450,000 people with work every year. Our suite of outsourcing and consulting services ensures companies have the people they need, when and where they are needed most. Headquartered in Troy, Michigan, we empower businesses and individuals to access limitless opportunities in industries such as science, engineering, technology, education, manufacturing, retail, finance, and energy. Revenue in 2022 was $5.0 billion. Learn more at kellyservices.com.

Inflation in Argentina so far in 2023 is running at 126.4%. Meanwhile, its GDP has declined by 3.1%. This certainly meets the definition of hyperinflation. Can this situation occur in the U.S. economy? Hyperinflation is when prices of goods and services in the economy run up rapidly; at the same time, it causes the value of the nation’s currency to fall rapidly. It’s a devastating phenomenon that has serious consequences for businesses, investors, and households. Below we explore the causes of hyperinflation, its effects on the economy, and some ways to protect investable assets against it.

Causes of Hyperinflation

Hyperinflation can be caused by a variety of factors, but one ingredient that is most common is excessive money printing by the country’s central bank. When a central bank allows excessive cash in circulation, especially if it is during a period of low or negative growth, natural economic forces that occur when there is an abundance of currency chasing the same or fewer goods, serves to drive up prices and down currency values. This inflation can quickly spiral out of control, leading to hyperinflation. Other causes could include shortages of goods or services driving prices up as demand outstrips available supply.

Effects on the Economy

Excessive inflation is not good for anyone that holds the impacted currency. Businesses can command higher prices, but they will also be paying higher prices to run their business and receiving payment with notes with far less purchasing power. This is because hyperinflation increases costs for labor and raw materials, weighing down profit margins. Less obvious, but certainly adding to the hardship, is that businesses may have trouble securing financing and loans during hyperinflation; this can limit their ability to function or grow.

For households and individuals, hyperinflation also rapidly decreases purchasing power, as prices for goods and services jump up. This lowers living standards in the country as people are forced to pay more for the same goods and services. Additionally, hyperinflation can lead to a loss of confidence in the currency. Behavior including the belief that items should be purchased now because they will be more expensive tomorrow leads to hoarding and other actions that create shortages and drives up prices even further.

How Some Prepare for Hyperinflation

Hyperinflation is rare, yet, once the wheels start turning, such as they did in Venezuela in 2016, or Germany in 1923, it is important for businesses and individuals to take steps to prepare for the possibility. Here are ways that people have prepared for excessive inflation in their native currency.

Diversify Your Investments: While some believe it is always prudent to stay widely diversified, it may offer even more protection when the economy goes through the turmoil of excessive inflation. Preparing in this way means spreading your investments across a variety of asset classes, such as stocks, bonds, real estate, and commodities. This will help by avoiding any one particular asset class that gets hit hard. Keep in mind, stocks are often a good hedge against moderate inflation, and precious metals have historically been looked to for protection in times of extreme inflation. Earnings of companies that export are not expected to suffer as much as importers.

Hold Some Assets Denominated in Other Currencies: This can include established digital currencies, foreign stocks, bonds, that are not denominated in your own home currency. By holding assets denominated in other currencies, you can protect yourself from its devaluation versus others.

Invest in Hard Assets: Hard assets, such as gold and silver, land, and even tools can be a good way to protect yourself or your business from hyperinflation. These assets have intrinsic value and can retain their value even if the currency they are denominated in loses value. Remember that if inflation remains, it is likely to cost more in the coming months for the same piece of office equipment that helps your business run more efficiently.

Cryptocurrencies: Keeping within the guidelines of diversification, more established tokens such as bitcoin and ether are considered by some to help protect from hyperinflation. A word of caution, cryptocurrencies have little history against currency devaluation and inflation. The theory however is these digital currencies are decentralized and not subject to the same inflationary pressures as fiat currencies.

Take Away

In 2018 inflation in Venezuela exceeded 1,000,000%, proving, when the recipe for higher prices is in place, the unimaginable can happen.

While there is no consumer or investor that can proactively impact a rising price freight train, if hyperinflation is expected, there are steps one can take to reduce the negative impacts. These financial steps can be as simple as buying things today that you expect to need later, and more substantially diversifying your portfolio toward hard assets, companies that export to countries not experiencing inflation, and even bonds with either short maturities or an inflation factor as part of the return.

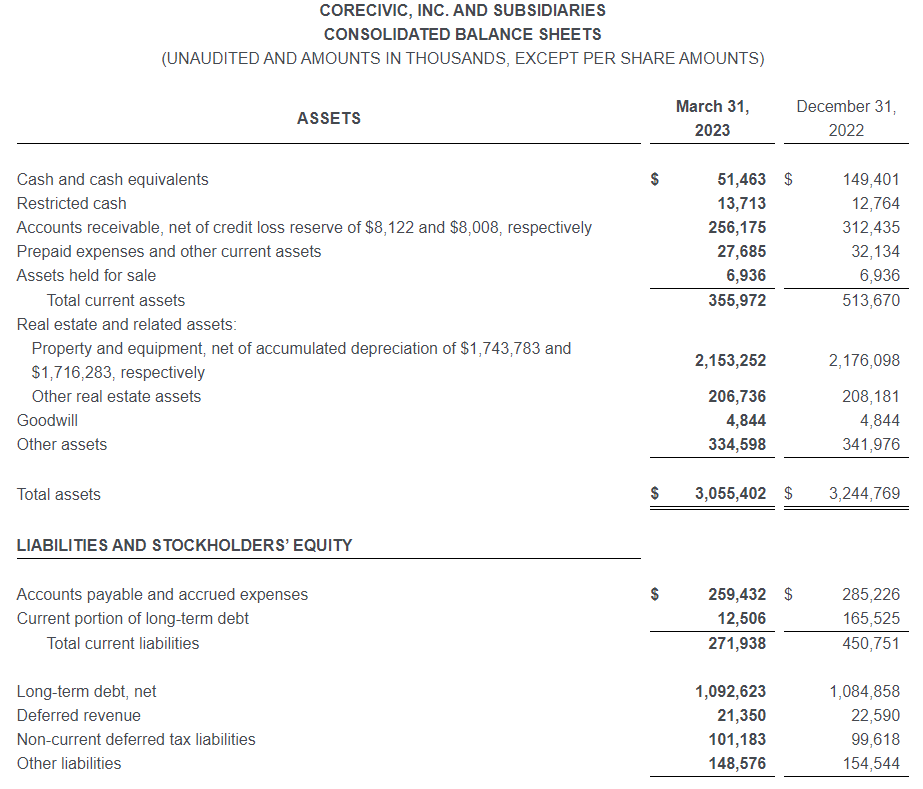

BRENTWOOD, Tenn., May 03, 2023 (GLOBE NEWSWIRE) — CoreCivic, Inc. (NYSE: CXW) (the Company) announced today its financial results for the first quarter of 2023.

Damon T. Hininger, CoreCivic’s President and Chief Executive Officer, said, “We are pleased to report first quarter results that were in line with our expectations, while we continue to operate through a challenging labor market and execute on our long-term capital allocation strategy. During the first quarter, we generated $73.7 million of EBITDA that, along with existing liquidity, enabled us to repay in full the $153.8 million outstanding balance of our 4.625% Senior Notes that were scheduled to mature on May 1, 2023. We also continued to execute on our share repurchase program during the quarter by repurchasing 2.5 million shares, representing an additional 2% of our outstanding shares, at a total cost of $24.9 million.

Hininger continued, “We’re also proud to have recently released our fifth Environmental, Social and Governance (ESG) Report. The ESG report details the ways we delivered reentry and vocational programming designed to prepare those in our care for long-lasting success upon reentry to their communities during 2022, a mission that our organization has been carrying out for more than 40 years. I hope you have an opportunity to review our latest ESG report to learn more about CoreCivic and the important services we provide. We are proud of our history and our accomplishments that truly help individuals in our care change their lives for the better primarily through the strength and volume of our evidence-based programs.”

Financial Highlights – First Quarter 2023

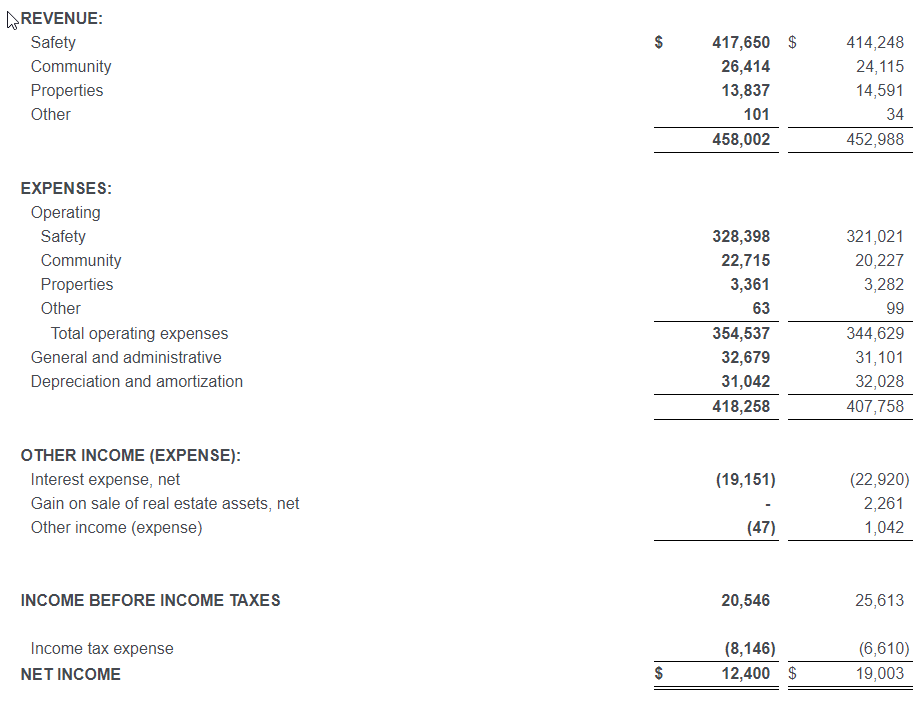

Total revenue of $458.0 million

CoreCivic Safety revenue of $417.7 million

CoreCivic Community revenue of $26.4 million

CoreCivic Properties revenue of $13.8 million

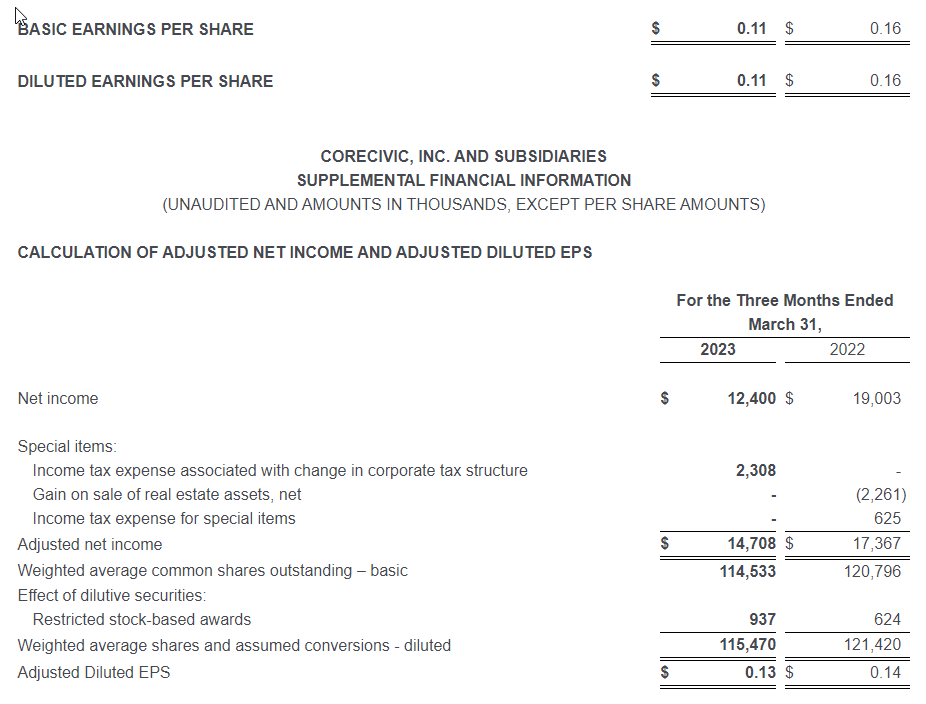

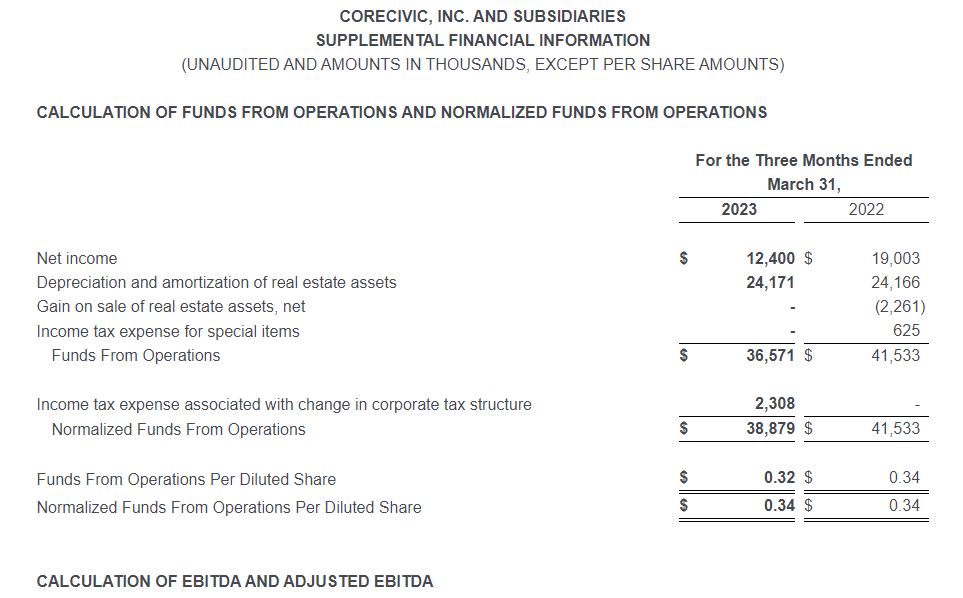

Net Income of $12.4 million

Diluted earnings per share of $0.11

Adjusted Diluted EPS of $0.13

Normalized Funds From Operations per diluted share of $0.34

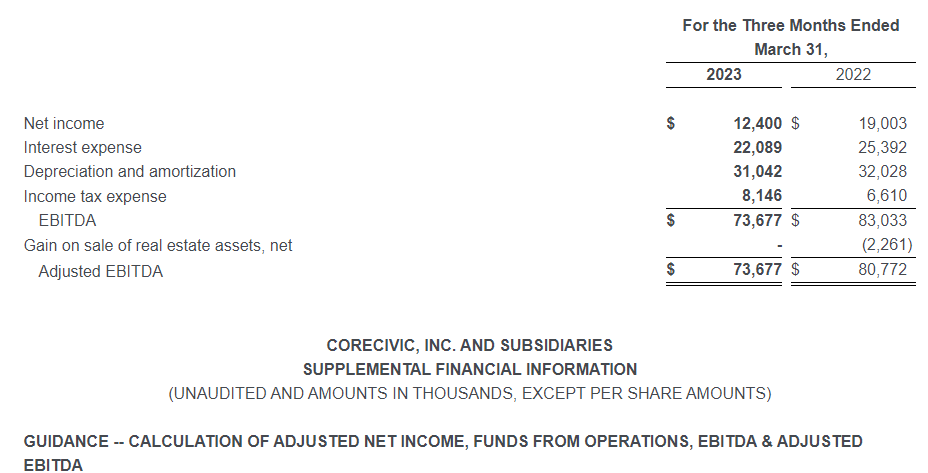

EBITDA of $73.7 million

First Quarter 2023 Financial Results Compared With First Quarter 2022

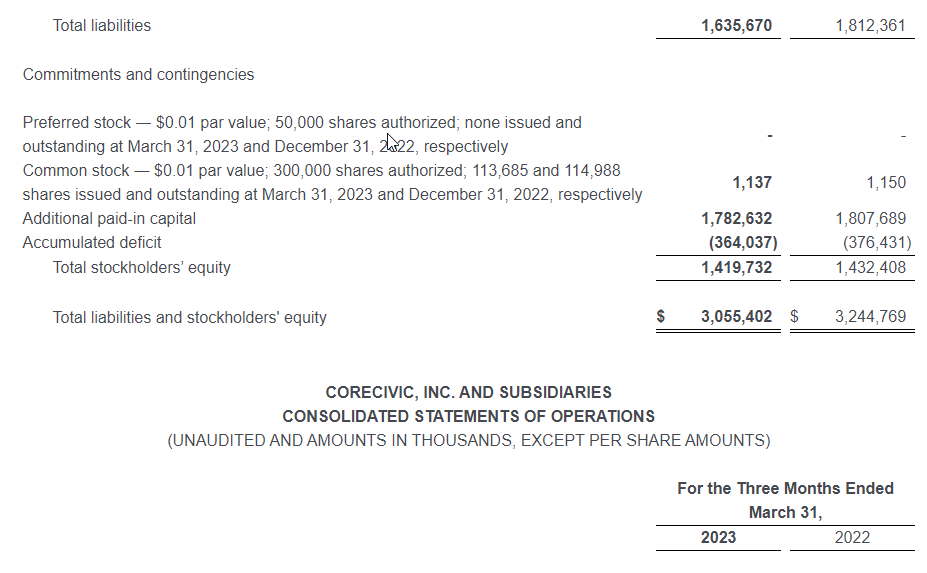

Net income in the first quarter of 2023 totaled $12.4 million, or $0.11 per diluted share, compared with net income in the first quarter of 2022 of $19.0 million, or $0.16 per diluted share. Adjusted for special items, adjusted net income in the first quarter of 2023 was $14.7 million, or $0.13 per diluted share (Adjusted Diluted EPS), compared with adjusted net income in the first quarter of 2022 of $17.4 million, or $0.14 per diluted share. Special items for each period are presented in detail in the calculation of Adjusted Diluted EPS in the Supplemental Financial Information following the financial statements presented herein.

The $0.01 per share decline in Adjusted Diluted EPS occurred despite transitioning to the previously announced contract with the state of Arizona at our 3,060-bed La Palma Correctional Center in Arizona, the expiration of our contract with the Federal Bureau of Prisons (BOP) at the McRae Correctional Facility on November 30, 2022, and ongoing labor market pressures, including above average wage inflation. We substantially completed the transition of inmate populations at the La Palma facility by the end of 2022, but we continued to incur elevated operating expenses during the first quarter of 2023 due to ongoing efforts to attract and retain local staff at the facility. Despite the expiration of the contract with the BOP at the McRae facility, a facility we sold to the state of Georgia in 2022, our renewal rate on owned and controlled facilities remains high at 94% over the previous five years. We believe our renewal rate on existing contracts remains high due to a variety of reasons including the aged and constrained supply of available beds within the U.S. correctional system, our ownership of the majority of the beds we operate, the value our government partners place in the wide range of recidivism-reducing programs we offer to those in our care, and the cost effectiveness of the services we provide.

Earnings before interest, taxes, depreciation and amortization (EBITDA) was $73.7 million in the first quarter of 2023, compared with $83.0 million in the first quarter of 2022. Adjusted EBITDA was $73.7 million in the first quarter of 2023, compared with $80.8 million in the first quarter of 2022. Adjusted EBITDA of $80.8 million in the prior year quarter excludes a net gain on sale of real estate assets. Adjusted EBITDA decreased from the prior year quarter primarily due to the previously mentioned transition of offender populations at our La Palma Correctional Center, which resulted in a reduction in EBITDA of $7.4 million, and the expiration of our BOP contract at the McRae Correctional Facility in November 2022, which resulted in a reduction in EBITDA of $2.3 million from the first quarter of 2022 to the first quarter of 2023. Due to an improving labor market, we achieved higher staffing levels in the first quarter of 2023 than in the prior year quarter; however, we incurred higher wage rates than in the prior year quarter in order to attract and retain facility staff in the challenging labor market. We also incurred higher travel expenses in order to augment staffing levels at multiple facilities. We believe these investments in staffing are positioning us to manage the increased number of residents we anticipate at our facilities once the remaining occupancy restrictions attributable to COVID-19 are removed, most notably Title 42, a policy that denies entry at the United States border to asylum-seekers and anyone crossing the border without proper documentation or authority in an effort to contain the spread of COVID-19. Title 42 is currently scheduled to end in May 2023. Despite the difficult labor market, we have been able to reduce certain labor-related expenses, such as registry nursing and temporary incentives, which moderated during the first quarter of 2023 compared with the first quarter of 2022.

Funds From Operations (FFO) was $36.6 million, or $0.32 per diluted share, in the first quarter of 2023, compared to $41.5 million, or $0.34 per diluted share, in the first quarter of 2022. Normalized FFO, which excludes special items, was $38.9 million, or $0.34 per diluted share, in the first quarter of 2023, compared with $41.5 million, or $0.34 per diluted share, in the first quarter of 2022. Normalized FFO was impacted by the same factors that affected Adjusted EBITDA.

Adjusted Net Income, EBITDA, Adjusted EBITDA, FFO, and Normalized FFO, and, where appropriate, their corresponding per share amounts, are measures calculated and presented on the basis of methodologies other than in accordance with generally accepted accounting principles (GAAP). Please refer to the Supplemental Financial Information and the note following the financial statements herein for further discussion and reconciliations of these measures to net income, the most directly comparable GAAP measure.

Asset Dispositions and Assets Held for Sale

During the third quarter of 2022, we began marketing for sale our Roth Hall Residential Reentry Center and the Walker Hall Residential Reentry Center, both of which are located in Philadelphia, Pennsylvania and reported in our CoreCivic Properties segment. The properties were classified as held for sale as of March 31, 2023 and December 31, 2022. A purchase and sale agreement for these two Philadelphia properties was executed in March 2023 and the properties were sold on May 2, 2023, generating net sales proceeds of $5.8 million, which approximated the carrying value of the properties. We are also marketing for sale a residential reentry center in Denver, Colorado with a carrying value of $1.2 million and reported in our CoreCivic Community segment, which was also classified as held for sale as of March 31, 2023.

Share Repurchases

On May 12, 2022, our Board of Directors approved a share repurchase program authorizing the Company to repurchase up to $150.0 million of our common stock. On August 2, 2022, our Board of Directors authorized an increase in our share repurchase program of up to an additional $75.0 million in shares of our common stock, or a total of up to $225.0 million. During the first quarter of 2023, we repurchased 2.5 million shares of our common stock at an aggregate purchase price of $24.9 million, excluding fees, commissions and other costs related to the repurchases. Since the share repurchase program was authorized, through March 31, 2023, we have repurchased a total of 9.1 million shares at an aggregate price of $99.4 million under this share repurchase program.

As of March 31, 2023, we had $125.6 million remaining under the share repurchase program authorized by the Board of Directors. Additional repurchases of common stock will be made in accordance with applicable securities laws and may be made at management’s discretion within parameters set by the Board of Directors from time to time in the open market, through privately negotiated transactions, or otherwise. The share repurchase program has no time limit and does not obligate us to purchase any particular amount of our common stock. The authorization for the share repurchase program may be terminated, suspended, increased or decreased by our Board of Directors in its discretion at any time.

Debt Repayments

On December 22, 2022, we delivered an irrevocable notice to the trustee of the holders of the 4.625% Senior Notes that we elected to redeem in full the 4.625% Senior Notes that remained outstanding on February 1, 2023. The 4.625% Senior Notes were redeemed on February 1, 2023 at a redemption price equal to 100% of the principal amount of the outstanding 4.625% Senior Notes, which amounted to $153.8 million, plus accrued and unpaid interest to, but not including, the redemption date. We used a combination of cash on hand and available capacity under our Revolving Credit Facility to fund the redemption. During the first quarter of 2023, we reduced our total debt balance by $146.2 million, or by $48.2 million net of the change in cash. Following the redemption of the 4.625% Senior Notes, we have no debt maturities until 2026.

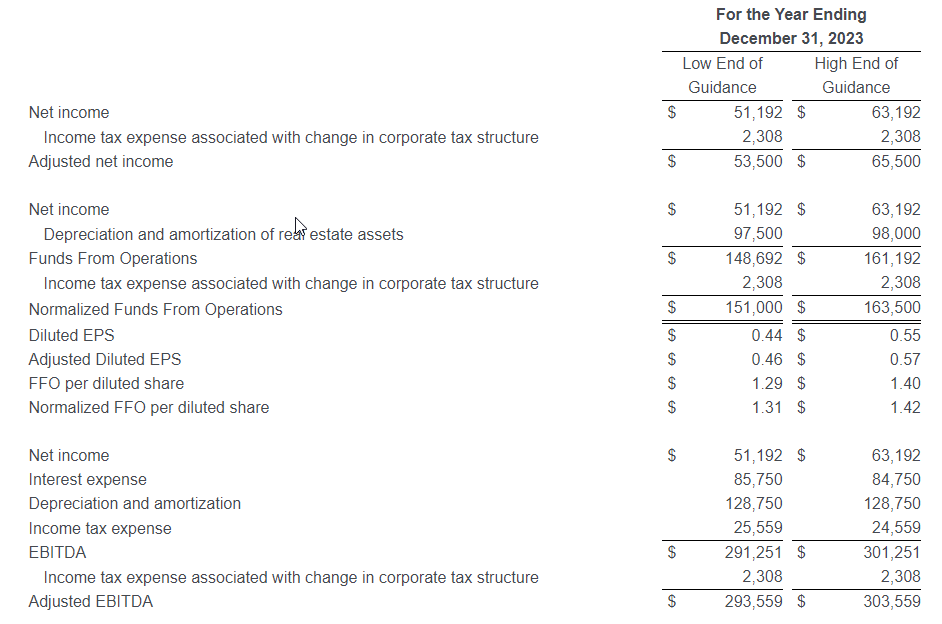

2023 Financial Guidance

Based on current business conditions, we are providing the following update to our financial guidance for the full year 2023:

Guidance Full Year 2023

Prior Guidance Full Year 2023

Net income

$51.2 million to $63.2 million

$58.0 million to $75.0 million

Adjusted net income

$53.5 million to $65.5 million

$58.0 million to $75.0 million

Diluted EPS

$0.44 to $0.55

$0.50 to $0.65

Adjusted Diluted EPS

$0.46 to $0.57

$0.50 to $0.65

FFO per diluted share

$1.29 to $1.40

$1.35 to $1.50

Normalized FFO per diluted share

$1.31 to $1.42

$1.35 to $1.50

EBITDA

$291.3 million to $301.3 million

$298.5 million to $313.5 million

Adjusted EBITDA

$293.6 million to $303.6 million

$298.5 million to $313.5 million

Financial guidance has been updated to reflect a favorable $0.01 per share variance to our internal forecast for the first quarter of 2023, offset by $0.04 per share to reflect the non-renewal of our lease with the state of Oklahoma at our North Fork Correctional Facility expiring June 30, 2023, which we previously disclosed on April 24, 2023. In addition, we continue to negotiate in good faith with the state of Oklahoma for the renewal of our contract to manage our Davis Correctional Facility, which also expires June 30, 2023, and operated at a loss during 2022 and the first quarter of 2023. However, we have not yet been able to reach acceptable terms. Our updated guidance was further reduced by $0.03 per share to reflect the potential transition of inmate populations out of the Davis Correctional Facility during the second quarter of 2023 and idle operations during the second half of the year, which we did not contemplate in our previous forecast. If we are able to reach acceptable terms on a new agreement, the $0.03 per share reduction will be avoided, as we would exceed our forecast by approximately $0.02 per share during the second quarter by avoiding the transition, and we would further exceed our guidance during the second half of 2023, the magnitude of which would depend on the terms of a new agreement.

During 2023, we expect to invest $64.0 million to $67.0 million in capital expenditures, consisting of $36.0 million to $37.0 million in maintenance capital expenditures on real estate assets, $25.0 million to $26.0 million for maintenance capital expenditures on other assets and information technology, and $3.0 million to $4.0 million for other capital investments. These capital expenditure amounts are unchanged from our previous guidance.

Supplemental Financial Information and Investor Presentations

We have made available on our website supplemental financial information and other data for the first quarter of 2023. Interested parties may access this information through our website at http://ir.corecivic.com/ under “Financial Information” of the Investors section. We do not undertake any obligation and disclaim any duties to update any of the information disclosed in this report.

Management may meet with investors from time to time during the second quarter of 2023. Written materials used in the investor presentations will also be available on our website beginning on or about May 19, 2023. Interested parties may access this information through our website at http://ir.corecivic.com/ under “Events & Presentations” of the Investors section.

Conference Call, Webcast and Replay Information

We will host a webcast conference call at 10:00 a.m. central time (11:00 a.m. eastern time) on Thursday, May 4, 2023, which will be accessible through the Company’s website at www.corecivic.com under the “Events & Presentations” section of the “Investors” page.

To participate via telephone and join the call live, please register in advance here https://register.vevent.com/register/BI6394fffe952b47d497a2735e53d08f32. Upon registration, telephone participants will receive a confirmation email detailing how to join the conference call, including the dial-in number and a unique passcode.

About CoreCivic

CoreCivic is a diversified, government-solutions company with the scale and experience needed to solve tough government challenges in flexible, cost-effective ways. We provide a broad range of solutions to government partners that serve the public good through high-quality corrections and detention management, a network of residential and non-residential alternatives to incarceration to help address America’s recidivism crisis, and government real estate solutions. We are the nation’s largest owner of partnership correctional, detention and residential reentry facilities, and one of the largest prison operators in the United States. We have been a flexible and dependable partner for government for 40 years. Our employees are driven by a deep sense of service, high standards of professionalism and a responsibility to help government better the public good. Learn more at www.corecivic.com.

Forward-Looking Statements

This press release contains statements as to our beliefs and expectations of the outcome of future events that are “forward-looking” statements within the meaning of Section 21E of the Securities Exchange Act of 1934, as amended, and the Private Securities Litigation Reform Act of 1995, as amended. These forward-looking statements are subject to risks and uncertainties that could cause actual results to differ materially from the statements made. These include, but are not limited to, the risks and uncertainties associated with: (i) changes in government policy, legislation and regulations that affect utilization of the private sector for corrections, detention, and residential reentry services, in general, or our business, in particular, including, but not limited to, the continued utilization of our correctional and detention facilities by the federal government, including as a consequence of the United States Department of Justice, or DOJ, not renewing contracts as a result of President Biden’s Executive Order on Reforming Our Incarceration System to Eliminate the Use of Privately Operated Criminal Detention Facilities, or the Private Prison EO, impacting utilization primarily by the BOP and the United States Marshals Service, and the impact of any changes to immigration reform and sentencing laws (we do not, under longstanding policy, lobby for or against policies or legislation that would determine the basis for, or duration of, an individual’s incarceration or detention); (ii) our ability to obtain and maintain correctional, detention, and residential reentry facility management contracts because of reasons including, but not limited to, sufficient governmental appropriations, contract compliance, negative publicity and effects of inmate disturbances; (iii) changes in the privatization of the corrections and detention industry, the acceptance of our services, the timing of the opening of new facilities and the commencement of new management contracts (including the extent and pace at which new contracts are utilized), as well as our ability to utilize available beds; (iv) general economic and market conditions, including, but not limited to, the impact governmental budgets can have on our contract renewals and renegotiations, per diem rates, and occupancy; (v) fluctuations in our operating results because of, among other things, changes in occupancy levels; competition; contract renegotiations or terminations; inflation and other increases in costs of operations, including a continuing rise in labor costs; fluctuations in interest rates and risks of operations; (vi) the duration of the federal government’s denial of entry at the United States southern border to asylum-seekers and anyone crossing the southern border without proper documentation or authority in an effort to contain the spread of COVID-19, a policy known as Title 42 (Title 42 is expected to end May 11, 2023, when President Biden has decided to lift the public health emergency for COVID-19, although its termination may be subject to ongoing litigation, the outcome of which is unclear. Most recently, on December 27, 2022, the Supreme Court granted a stay on the cessation of Title 42, while it considers an appeal by a group of states to continue the expulsions.); (vii) our ability to successfully identify and consummate future development and acquisition opportunities and realize projected returns resulting therefrom; (viii) our ability to have met and maintained qualification for taxation as a real estate investment trust, or REIT, for the years we elected REIT status; and (ix) the availability of debt and equity financing on terms that are favorable to us, or at all. Other factors that could cause operating and financial results to differ are described in the filings we make from time to time with the Securities and Exchange Commission.

We take no responsibility for updating the information contained in this press release following the date hereof to reflect events or circumstances occurring after the date hereof or the occurrence of unanticipated events or for any changes or modifications made to this press release or the information contained herein by any third-parties, including, but not limited to, any wire or internet services.

NOTE TO SUPPLEMENTAL FINANCIAL INFORMATION

Adjusted Net Income, EBITDA, Adjusted EBITDA, FFO, and Normalized FFO, and, where appropriate, their corresponding per share metrics are non-GAAP financial measures. The Company believes that these measures are important operating measures that supplement discussion and analysis of the Company’s results of operations and are used to review and assess operating performance of the Company and its properties and their management teams. The Company believes that it is useful to provide investors, lenders and security analysts disclosures of its results of operations on the same basis that is used by management.

FFO, in particular, is a widely accepted non-GAAP supplemental measure of performance of real estate companies, grounded in the standards for FFO established by the National Association of Real Estate Investment Trusts (NAREIT). NAREIT defines FFO as net income computed in accordance with GAAP, excluding gains (or losses) from sales of property and extraordinary items, plus depreciation and amortization of real estate and impairment of depreciable real estate and after adjustments for unconsolidated partnerships and joint ventures calculated to reflect funds from operations on the same basis. As a company with extensive real estate holdings, we believe FFO and FFO per share are important supplemental measures of our operating performance and believe they are frequently used by securities analysts, investors and other interested parties in the evaluation of REITs and other real estate operating companies, many of which present FFO and FFO per share when reporting results. EBITDA, Adjusted EBITDA, and FFO are useful as supplemental measures of performance of the Company’s properties because such measures do not take into account depreciation and amortization, or with respect to EBITDA, the impact of the Company’s tax provision and financing strategies. Because the historical cost accounting convention used for real estate assets requires depreciation (except on land), this accounting presentation assumes that the value of real estate assets diminishes at a level rate over time. Because of the unique structure, design and use of the Company’s properties, management believes that assessing performance of the Company’s properties without the impact of depreciation or amortization is useful. The Company may make adjustments to FFO from time to time for certain other income and expenses that it considers non-recurring, infrequent or unusual, even though such items may require cash settlement, because such items do not reflect a necessary or ordinary component of the ongoing operations of the Company. Normalized FFO excludes the effects of such items. The Company calculates Adjusted Net Income by adding to GAAP Net Income expenses associated with the Company’s debt repayments and refinancing transactions, and certain impairments and other charges that the Company believes are unusual or non-recurring to provide an alternative measure of comparing operating performance for the periods presented.

Other companies may calculate Adjusted Net Income, EBITDA, Adjusted EBITDA, FFO, and Normalized FFO differently than the Company does, or adjust for other items, and therefore comparability may be limited. Adjusted Net Income, EBITDA, Adjusted EBITDA, FFO, and Normalized FFO and, where appropriate, their corresponding per share measures are not measures of performance under GAAP, and should not be considered as an alternative to cash flows from operating activities, a measure of liquidity or an alternative to net income as indicators of the Company’s operating performance or any other measure of performance derived in accordance with GAAP. This data should be read in conjunction with the Company’s consolidated financial statements and related notes included in its filings with the Securities and Exchange Commission.