SIERRA METALS REPORTS SOLID SECOND QUARTER 2020 PRODUCTION RESULTS INCLUDING STRONG PRODUCTION FROM BOLIVAR, DESPITE THE IMPACT OF THE COVID-19 PANDEMIC

Toronto, ON – July 15, 2020 – Sierra Metals Inc. (TSX: SMT) (BVL: SMT) (NYSE AMERICAN: SMTS) (“Sierra Metals” or “the Company”) is pleased to report second-quarter 2020 production results featuring the strong operational performance at its Bolivar Mine.

Results are from Sierra Metals’ three underground mines in Latin America: The Yauricocha polymetallic mine in Peru, and the Bolivar copper and Cusi silver Mines in Mexico.

Second Quarter 2020 Production Highlights

- Copper production of 9.7 million pounds; in-line with Q2 2019

- Silver production of 0.6 million ounces; a 32% decrease from Q2 2019

- Gold production of 2,762 ounces; a 9% increase from Q2 2019

- Zinc production of 13.7 million pounds; a 17% decrease from Q2 2019

- Lead production of 6.4 million pounds; a 21% decrease from Q2 2019

- Copper equivalent production of 22.7 million pounds; a 10% decrease from Q2 2019

- Production at Yauricocha and Bolivar impacted in April and May due to the government-imposed shutdowns to contain the advancement of COVID-19.

- Cusi remained under care and maintenance throughout the quarter

Quarterly throughput from the Yauricocha and Bolivar Mines was negatively impacted by the shutdowns announced by the Peruvian and the Mexican Governments to contain the advancement of the COVID-19 pandemic. Both the mines, while maintaining essential activities, operated at reduced capacities for the April and May months. These restrictions were relaxed for mining companies in June (as announced in our Press Release dated June 5, 2020), and the Company began to recall its furloughed employees and started ramping up the operations to full capacity. The Cusi mine remained under care and maintenance throughout the quarter, due to its proximity to urban communities.

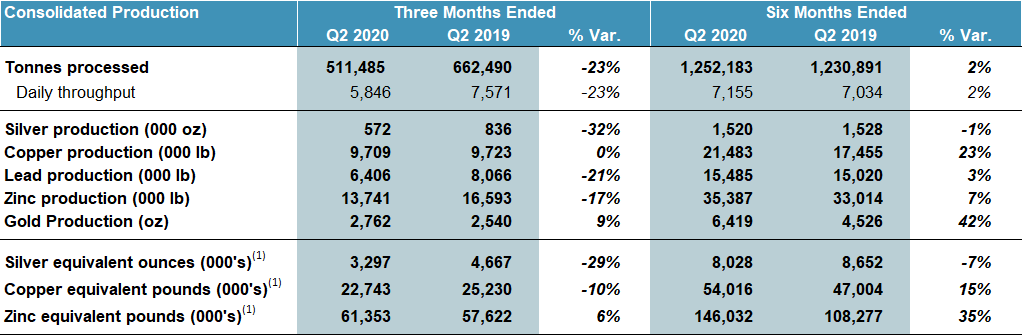

Consolidated production of copper remained in-line at 9.7 million pounds, silver decreased 32% to 0.6 million ounces, lead decreased 21% to 6.4 million pounds, zinc declined 17% to 13.7 million pounds, and gold increased 9% to 2,762 ounces compared to Q2 2019. Consolidated silver production dropped since there was no production at Cusi during the quarter, while gold production increased largely due to higher gold grades from the Bolivar Mine.

The Yauricocha Mine experienced a 20% reduction in throughput during Q2 2020 compared to Q2 2019, due to the afore-mentioned government-imposed state of emergency. The reduction in throughput was partially offset by higher head grades and higher silver and gold recoveries at Yauricocha, which resulted in a 15% decrease in copper equivalent pounds produced during Q2 2020 compared to Q2 2019.

At Bolivar, higher grades and recoveries were partially offset by the 5% decrease in throughput, resulting in a 24% increase in copper equivalent pounds produced during Q2 2020 compared to Q2 2019. A mere 5% decrease in throughput, despite the COVID-19 related shutdown, resulted from the increased plant capacity attributable to the expansion completed at the end of 2019.

Luis Marchese, President, and CEO of Sierra Metals, commented: “The Company had solid production results in the second quarter despite the negative implications of the shutdowns that occurred due to the COVID-19 pandemic. At Yauricocha and Bolivar, the Company was able to maintain essential activities while fully complying with the government protocols during the state of emergency. I want to thank our workers at the mines for their dedication and efforts during these difficult times, which lead the Company to have remarkably high productivity levels. While Cusi remained in care and maintenance due to its proximity to urban centers, we are working through a process that will allow us to safely return workers to the mine and ramp up production. Through the period of downtime, we reviewed our processes at each mine site, targeting improving efficiencies and identifying optimized exploration sequencing to add to our reserves and resources. As we ramp-up towards full capacity, we continue to adhere to strict health protocols protecting our operations, our employees, and the communities in which we operate.”

Consolidated Production Results

(1) Silver equivalent ounces and copper and zinc

equivalent pounds for Q2 2020 were calculated using the following realized

prices: $16.59/oz Ag, $2.40/lb Cu, $0.89/lb Zn, $0.76/lb Pb, $1,722/oz Au.

Silver equivalent ounces and copper and zinc equivalent pounds for Q1 2019 were

calculated using the following realized prices: $14.88/oz Ag, $2.75/lb Cu,

$1.20/lb Zn, $0.85/lb Pb, $1,323/oz Au. Silver equivalent ounces and copper and

zinc equivalent pounds for 6M 2020 were calculated using the following realized

prices: $16.58/oz Ag, $2.46/lb Cu, $0.91/lb Zn, $0.78/lb Pb, $1,654/oz Au.

Silver equivalent ounces and copper and zinc equivalent pounds for 6M 2019 were

calculated using the following realized prices: $15.23/oz Ag, $2.80/lb Cu,

$/1.22lb Zn, $0.90/lb Pb, $1,314/oz Au.

Yauricocha Mine, Peru

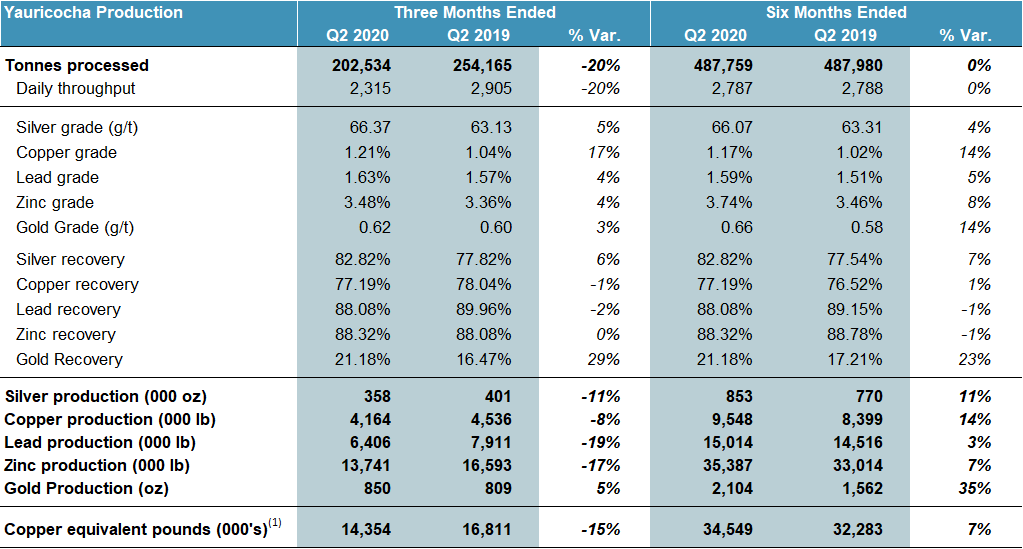

The Yauricocha Mine processed 202,534 tonnes during Q2 2020, which is a 20% decrease from Q2 2019. The decline resulted from the government-imposed state of emergency, which remained in force until June 4, 2020, when the Peruvian government announced the resumption of mining activities as part of phase two of its economic recovery plan. Gradually ramping up its operation, the mine achieved an average throughput of approximately 2,600 tpd in June. The average production for Q2 2020 was 2,315 tpd. The Yauricocha mine has the operational flexibility to recover part of the lost production.

Higher head grades and higher silver and gold recoveries partially offset the impact of lower throughput resulting in a 15% decrease in copper equivalent metal production compared to Q2 2019. Copper and lead recoveries were slightly below the Q2 2019 recoveries, while zinc recoveries were in-line with Q2 2019. Head grades for all metals were higher due to the mining in the cuerpos chicos. Copper grades were particularly higher as a greater proportion of copper sulphides were processed versus polymetallic ore as compared to Q2 2019. Installation of the SK-240 cells and grade analyzers helped achieve higher silver and gold recoveries.

A summary of production from the Yauricocha Mine for Q2 2020 is provided below:

(1) Silver equivalent ounces and copper and zinc

equivalent pounds for Q2 2020 were calculated using the following realized

prices: $16.59/oz Ag, $2.40/lb Cu, $0.89/lb Zn, $0.76/lb Pb, $1,722/oz Au.

Silver equivalent ounces and copper and zinc equivalent pounds for Q1 2019 were

calculated using the following realized prices: $14.88/oz Ag, $2.75/lb Cu,

$1.20/lb Zn, $0.85/lb Pb, $1,323/oz Au. Silver equivalent ounces and copper and

zinc equivalent pounds for 6M 2020 were calculated using the following realized

prices: $16.58/oz Ag, $2.46/lb Cu, $0.91/lb Zn, $0.78/lb Pb, $1,654/oz Au.

Silver equivalent ounces and copper and zinc equivalent pounds for 6M 2019 were

calculated using the following realized prices: $15.23/oz Ag, $2.80/lb Cu, $/1.22lb

Zn, $0.90/lb Pb, $1,314/oz Au.

Bolivar Mine, Mexico

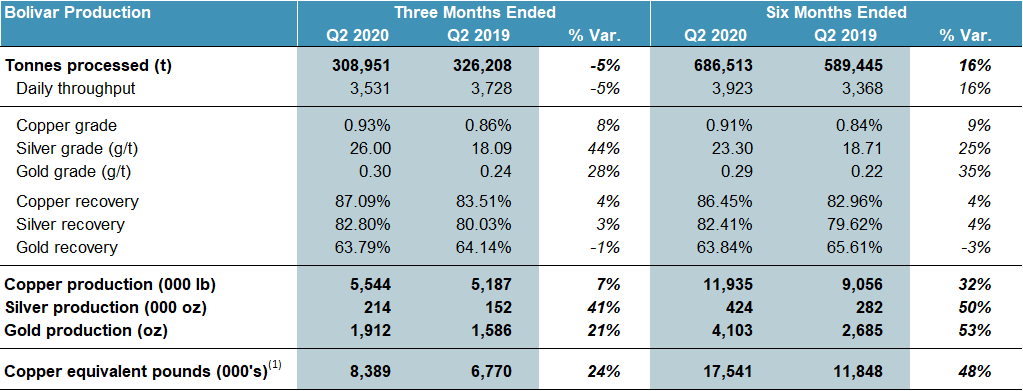

The Bolivar Mine processed 308,951 tonnes in Q2 2020, which is a mere 5% decrease from the Q2 2019 throughput, despite the impact of COVID-19. The average daily throughput realized during the quarter was 3,531 tpd. Head grades for copper, silver, and gold were 8%, 44%, and 28% higher, respectively, as compared to Q2 2019. Higher head grades and higher copper and silver recoveries, partially offset by lower throughput, resulted in a 24% increase in copper equivalent pounds produced during Q2 2020 compared to Q2 2019. In Q2 2020, copper production increased by 7% to 5,544,000 pounds, silver production increased 41% to 214,000 ounces, and gold production increased 21% to 1,912 ounces compared to Q2 2019.

Development and infrastructure improvements, which were on hold during Q2 2020, are planned to resume in the second half of the year in the effort to push throughput at Bolivar to 5,000 tpd by the end of 2020. Copper grades are expected to increase during the second half of the year, as mining is planned in the Mina de Fierro and Bolivar West zones.

A summary of production for the Bolivar Mine for Q2 2020 is provided below:

(1) Silver equivalent ounces and copper and zinc

equivalent pounds for Q2 2020 were calculated using the following realized prices:

$16.59/oz Ag, $2.40/lb Cu, $0.89/lb Zn, $0.76/lb Pb, $1,722/oz Au. Silver

equivalent ounces and copper and zinc equivalent pounds for Q1 2019 were

calculated using the following realized prices: $14.88/oz Ag, $2.75/lb Cu,

$1.20/lb Zn, $0.85/lb Pb, $1,323/oz Au. Silver equivalent ounces and copper and

zinc equivalent pounds for 6M 2020 were calculated using the following realized

prices: $16.58/oz Ag, $2.46/lb Cu, $0.91/lb Zn, $0.78/lb Pb, $1,654/oz Au.

Silver equivalent ounces and copper and zinc equivalent pounds for 6M 2019 were

calculated using the following realized prices: $15.23/oz Ag, $2.80/lb Cu,

$/1.22lb Zn, $0.90/lb Pb, $1,314/oz Au.

Cusi Mine, Mexico

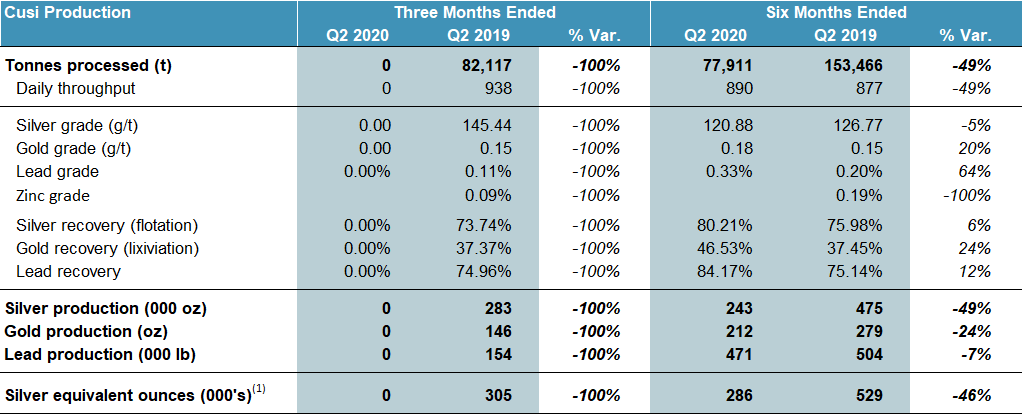

The Cusi Mine remained in care and maintenance throughout the second quarter of 2020, due to the government-mandated shutdown to contain the advancement of COVID-19. As a result, there was no production from Cusi during the quarter. As announced in the press release dated June 18, 2020, this care and maintenance period has allowed the management team to complete an optimized view of the entire mine operation. Changes in the interpretation of the geological system have been made based on updated information from a stockwork tonnage system to a vein model system, which is expected to help better control and improve head grades, dilution and make better use of Cusi’s silver mineral resources.

Mine development is currently on-going at Cusi in a zone that will bypass the previously announced area of subsidence and provide access to higher-grade economic ore to provide feed for the mill. Production is expected to recommence after the mine development work is completed and once a process can be implemented at the mine to mitigate risk to employees at the site through a testing and quarantine methodology similar to the Company’s other operations.

The Company plans to drill an additional 1,000 meters to better understand the mineralization of the new high-grade silver zone in an area called Northeast – Southwest System of Epithermal Veins, as mentioned in the press release dated June 18, 2020.

The management team will continue to ramp throughput up to the targeted 1,200 tpd by the end of the year and will commence studies in the second half of the year for the potential expansion of Cusi.

A summary of production for the Cusi Mine for Q2 2020 is provided below:

(1) Silver equivalent ounces and copper and zinc equivalent pounds for Q2 2020 were calculated using the following realized prices: $16.59/oz Ag, $2.40/lb Cu, $0.89/lb Zn, $0.76/lb Pb, $1,722/oz Au. Silver equivalent ounces and copper and zinc equivalent pounds for Q1 2019 were calculated using the following realized prices: $14.88/oz Ag, $2.75/lb Cu, $1.20/lb Zn, $0.85/lb Pb, $1,323/oz Au. Silver equivalent ounces and copper and zinc equivalent pounds for 6M 2020 were calculated using the following realized prices: $16.58/oz Ag, $2.46/lb Cu, $0.91/lb Zn, $0.78/lb Pb, $1,654/oz Au. Silver equivalent ounces and copper and zinc equivalent pounds for 6M 2019 were calculated using the following realized prices: $15.23/oz Ag, $2.80/lb Cu, $/1.22lb Zn, $0.90/lb Pb, $1,314/oz Au.

Quality Control

All technical data contained in this news release has been reviewed and approved by Americo Zuzunaga, FAusIMM CP (Mining Engineer) and Vice President of Corporate Planning is a Qualified Person and chartered professional qualifying as a Competent Person under the Joint Ore Reserves Committee (JORC) Australasian Code for Reporting of Exploration Results, Mineral Resources, and Ore Reserves.

Augusto Chung, FAusIMM CP (Metallurgist) and Consultant to Sierra Metals, is a Qualified Person and chartered professional qualifying as a Competent Person on metallurgical processes.

About Sierra Metals

Sierra Metals Inc. is a diversified Canadian mining company focused on the production and development of precious and base metals from its polymetallic Yauricocha Mine in Peru, and Bolivar and Cusi Mines in Mexico. The Company is focused on increasing production volume and growing mineral resources. Sierra Metals has recently had several new key discoveries and still has many more exciting brownfield exploration opportunities at all three Mines in Peru and Mexico that are within close proximity to the existing mines. Additionally, the Company also has large land packages at all three mines with several prospective regional targets providing longer-term exploration upside and mineral resource growth potential.

The Company’s Common Shares trade on the Bolsa de Valores de Lima and on the Toronto Stock Exchange under the symbol “SMT” and on the NYSE American Exchange under the symbol “SMTS”.

For further information regarding Sierra Metals, please visit www.sierrametals.com or contact:

|

Mike McAllister

V.P., Investor Relations

Sierra Metals Inc.

+1 (416) 366-7777

Email:

[email protected]

|

|

Luis Marchese

CEO

Sierra Metals Inc.

+1(416) 366-7777

|

Continue to Follow, Like and Watch our progress:

Web: www.sierrametals.com | Twitter: sierrametals | Facebook: SierraMetalsInc | LinkedIn: Sierra Metals Inc |

Instagram: sierrametals

Forward-Looking Statements

This press release contains “forward-looking information” and “forward-looking statements” within the meaning of Canadian and U.S. securities laws (collectively, “forward-looking

information“). Forward-looking information includes, but is not limited to, statements with respect to the date of the 2020 Shareholders’ Meeting and the anticipated filing of the Compensation Disclosure. Any statements that express or involve discussions with respect to predictions, expectations, beliefs, plans, projections, objectives, assumptions or future events or performance (often, but not always, using words or phrases such as “expects”, “anticipates”, “plans”, “projects”, “estimates”, “assumes”, “intends”, “strategy”, “goals”, “objectives”, “potential” or variations thereof, or stating that certain actions, events or results “may”, “could”, “would”, “might” or “will” be taken, occur or be achieved, or the negative of any of these terms and similar expressions) are not statements of historical fact and may be forward-looking information.

Forward-looking information is subject to a variety of risks and uncertainties, which could cause actual events or results to differ from those reflected in the forward-looking information, including, without limitation, the risks described under the heading “Risk Factors” in the Company’s annual information form dated March 30, 2020 for its fiscal year ended December 31, 2019 and other risks identified in the Company’s filings with Canadian securities regulators and the United States Securities and Exchange Commission, which filings are available at www.sedar.com and www.sec.gov, respectively.

The risk factors referred to above are not an exhaustive list of the factors that may affect any of the Company’s forward-looking information. Forward-looking information includes statements about the future and is inherently uncertain, and the Company’s actual achievements or other future events or conditions may differ materially from those reflected in the forward-looking information due to a variety of risks, uncertainties and other factors. The Company’s statements containing forward-looking information are based on the beliefs, expectations and opinions of management on the date the statements are made, and the Company does not assume any obligation to update such forward-looking information if circumstances or management’s beliefs, expectations or opinions should change, other than as required by applicable law. For the reasons set forth above, one should not place undue reliance on forward-looking information.