Meme Stocks are Putting Up a Strong Offense – Is this a Positive Sign for the Broader Market?

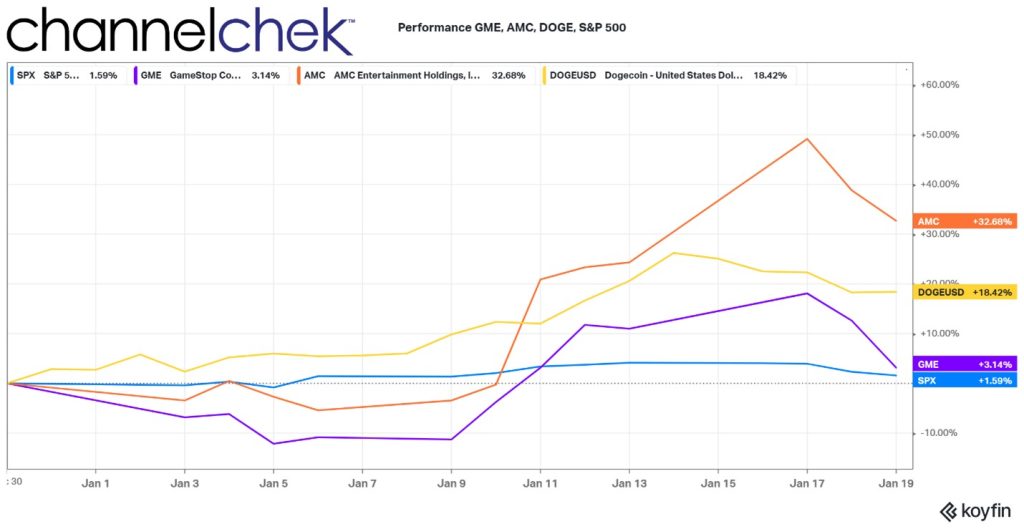

During the first three weeks of 2023, meme stocks and crypto tokens, often viewed in the same category, have scored early. Have meme stock investors now come off the sidelines after the poor performance last year? In 2022 they completely failed to repeat their historic 2021 wins. So the current rally is a great sign.

Successful meme trading occurs when there is a mass movement by retail accounts. So far in 2023, like flipping a New Year’s switch, retail is again causing a commotion. And by looking at the trending hashtags and cashtags on Reddit and Twitter, fans are also making an increased volume of noise.

Looking at the 2023 performance chart above, the S&P 500 ($SPY) opened the year more positively than the prior year ended. While one obviously can not extrapolate out the current 1.59% return for the year, annualizing it helps bring the short period being measured into perspective. The overall market is running at a 30.50% pace this year. Wow.

The performance of GameStop ($GME), which was one of the original and among the most recognized meme stocks, is outperforming the overall market by double. While it is well off its high reached earlier this week, the above 3% return is running well ahead of the overall stock market.

The cryptocurrency in the group, the often maligned Dogecoin (DOGE.X), which is legendary as it started as a parody token, has been tracking Bitcoins (BTC.X) rise closely. DOGE is up over 18% on the year, averaging an increase near 1% per day.

AMC Entertainment ($AMC), which is off its high of almost 50% a few days ago, now has returned over 32% to those holding the stock. To put this in perspective, it has an annualized return in 2023, so far, of 628%. This likely has gotten ahead of itself, time will tell, but it is the clear MVP among the meme stocks to date.

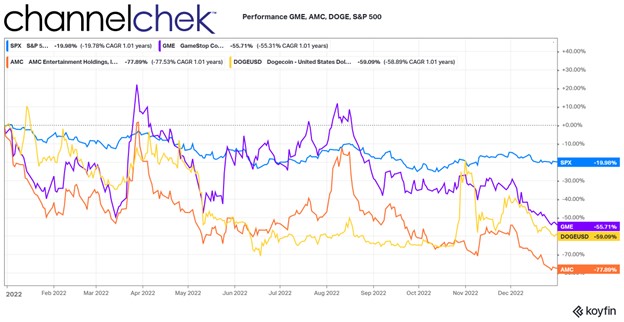

Last year the overall market, despite being down near 20%,, trounced the meme stocks that have thus far put in a stellar showing in 2023.

Is Meme Rally a Reason for Optimism?

Retail dollars coming in off the sidelines and mounting enough of a drive to force values up so quickly indicates a mood change that may play out elsewhere in the financial markets. The average trade size of retail is so small that it indicates a large wave of willingness, if not outright optimism, that putting money in play will lead to gains. Similar forces are causing money to move into mutual funds and ETFs, which serves to put upward pressure on the overall market.

Wall Street’s so-called “fear gauge,” the Volatility Index ($VIX) dropped on average 1% a day since the start of the year. This is a spectacular trend. It now stands near its long-term average of 21; a reading above 30 is considered bearish. The $VIX was last near these levels in April of last year. The overall market stood 15% higher back then compared to today.

The Volatility Index has applications across digital assets as well. On a scale of 1-100, where 100 is overly greedy, The Crypto Fear and Greed Index stands near neutral at 52. This is also the most optimistic reading since April. It may be considered even more positive since the digital asset market is still digesting the “unprecedented” bankruptcy of crypto exchange FTX.

Meme mania has never been about macro; more about crowd behavior, commitment, and momentum. But there are fundamentals that are viewed by stock investors of all varieties that likely have fed into the burst of interest. First, economic data suggests that inflation is trending lower. This deceleration lessens the need for the Federal Reserve to put the brakes on the economy. The enthusiasm is just more pronounced among this style of retail traders that are loud and proud. They serve as cheerleaders to captivate the imagination of more traditional investors.

Take Away

The overall financial markets opened with a sigh of relief in 2023. Meme stocks and crypto opened the year with extreme optimism. The optimism isn’t without cause; a number of factors point to a much better environment than the dismal returns of last year.

Will this contagion, led by many small accounts, inspire further the larger individual and institutional investors to commit investments in the broader markets, there are many signs that suggest the year is starting that way, fear of missing out will build with each day that the markets move in a positive direction.

The so-called Beige Book is receiving much more attention from market participants than it has in years as they seek insight into the near- and long-term economic direction. The report is published eight times yearly and released about two weeks before the FOMC scheduled meetings. It contains anecdotal trends and moods from each of the 12 Federal Reserve districts. The information is collected and summarized and is relied on as part of the discussion topics at the Fed policy meetings.

The report released on January 18th was collected on or before January 9th. While each Federal Reserve district may have different economic experiences, for example, manufacturing regions may have a very different perspective than agricultural areas or districts where service jobs are more prevalent.

30,000 Foot View

The first Beige Book of 2023 shows the US economy is holding steady. However, there are only small amounts of growth experienced in some regions, while others expect small pockets of expansion. This overall summary would be difficult to use as an argument for the Fed to alter course from its stated intention of additional tightening, including Fed Funds rate hikes. The next meeting will be held on January 31st and February 1st.

“On balance, contacts across districts said they expected future price growth to moderate further in the year ahead,” the survey said.

The report doesn’t contain many surprises and confirms current expectations that residential real estate activity is sluggish, the labor market is strong, and that inflation is running at a slower pace of growth.

There is very little in January’s Beige Book that would alter analysts’ expectations of what the next monetary policy adjustment might be. Those that are expecting a 0.50% increase are not likely to shift their thinking from the summaries, and those expecting a 0.25% hike are similarly not inclined to shift their thinking. Most analysts fall into one of these two categories.

A Sign the Markets Wanted

In a recent interview, Cleveland Fed President Loretta Mester said the slowdown in inflation shows the Fed’s work raising rates is having the desired effect; she also suggested that further increases are still needed. “We’re beginning to see the kind of actions that we need to see,” Mester stated; these are “good signs that things are moving in the right direction. That’s important input into how we’re thinking about where policy needs to go.” This is heartening for those hoping for fewer rate hikes as Mester is considered one of the US central bank’s more hawkish members.

Take Away

The markets got a mixed bag with no clear change of direction from the summary of Federal reserve districts, otherwise known as the Beige Book. This could mean there will be few surprises at the close of the FOMC meeting on February 1st.

At least one Fed hawk is softening her rhetoric going into the meeting. If the trend continues, the prospect of fewer rate hikes should be viewed as positive for stocks and positive for bonds.

Deep sea sponges and other creatures live on and among valuable manganese nodules like this one that could be mined from the seafloor. (GEOMAR)

Deep Seabed Mining Plans Pit Renewable Energy Demand Against Ocean Life in a Largely Unexplored Frontier

As companies race to expand renewable energy and the batteries to store it, finding sufficient amounts of rare earth metals to build the technology is no easy feat. That’s leading mining companies to take a closer look at a largely unexplored frontier – the deep ocean seabed.

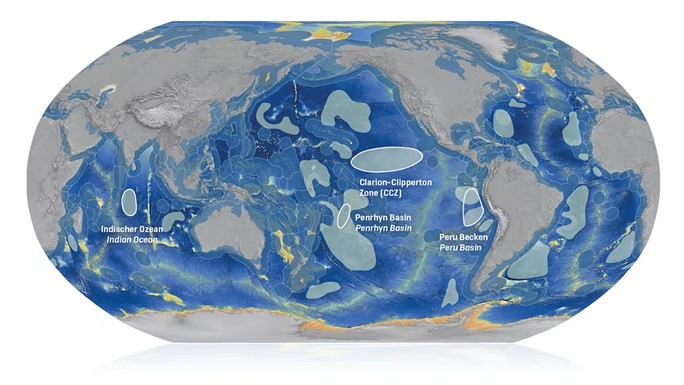

A wealth of these metals can be found in manganese nodules that look like cobblestones scattered across wide areas of deep ocean seabed. But the fragile ecosystems deep in the oceans are little understood, and the mining codes to sustainably mine these areas are in their infancy.

A fierce debate is now playing out as a Canadian company makes plans to launch the first commercial deep sea mining operation in the Pacific Ocean.

The Metals Company completed an exploratory project in the Pacific Ocean in fall 2022. Under a treaty governing the deep sea floor, the international agency overseeing these areas could be forced to approve provisional mining there as soon as spring 2023, but several countries and companies are urging a delay until more research can be done. France and New Zealand have called for a ban on deep sea mining.

As scholars who have long focused on the economic, political and legal challenges posed by deep seabed mining, we have each studied and written on this economic frontier with concern for the regulatory and ecological challenges it poses.

Manganese nodules on the seafloor in the Clarion-Clipperton Zone, between Hawaii and Mexico, . (GEOMAR)

What’s Down There, and Why Should We Care?

A curious journey began in the summer of 1974. Sailing from Long Beach, California, a revolutionary ship funded by eccentric billionaire Howard Hughes set course for the Pacific to open a new frontier — deep seabed mining.

Widespread media coverage of the expedition helped to focus the attention of businesses and policymakers on the promise of deep seabed mining, which is notable given that the expedition was actually an elaborate cover for a CIA operation.

The real target was a Soviet ballistic missile submarine that had sunk in 1968 with all hands and what was believed to be a treasure trove of Soviet state secrets and tech onboard.

The expedition, called Project Azorian by the CIA, recovered at least part of the submarine – and it also brought up several manganese nodules from the seafloor.

Manganese nodules are roughly the size of potatoes and can be found across vast areas of seafloor in parts of the Pacific and Indian oceans and deep abyssal plains in the Atlantic. They are valuable because they are exceptionally rich in 37 metals, including nickel, cobalt and copper, which are essential for most large batteries and several renewable energy technologies.

Manganese nodules form as metals accumulate around a shell or part of another nodule. (GEOMAR)

These nodules form over millennia as metals nucleate around shells or broken nodules. The Clarion-Clipperton Zone, between Mexico and Hawaii in the Pacific Ocean, where the mining test took place, has been estimated to have over 21 billion metric tons of nodules that could provide twice as much nickel and three times more cobalt than all the reserves on land.

Mining in the Clarion-Clipperton Zone could be some 10 times richer than comparable mineral deposits on land. All told, estimates place the value of this new industry at some US$30 billion annually by 2030. It could be instrumental in feeding the surging global demand for cobalt that lies at the heart of lithium-ion batteries.

Yet, as several scientists have noted, we still know more about the surface of the moon than what lies at the bottom of the deep seabed.

Deep Seabed Ecology

Less than 10% of the deep seabed has been mapped thoroughly enough to understand even the basic features of the structure and contents of the ocean floor, let alone the life and ecosystems therein.

Even the most thoroughly studied region, the Clarion-Clipperton Zone, is still best characterized by the persistent novelty of what is found there.

Brightly colored sea cucumbers and many other unusual deep sea creatures live among the nodules in the Clarion-Clipperton Zone (GEOMAR)

Brightly colored sea cucumbers and many other unusual deep sea creatures live among the nodules in the Clarion-Clipperton Zone. (GEOMAR)

Between 70% and 90% of living things collected in the Clarion-Clipperton Zone have never been seen before, leaving scientists to speculate about what percentage of all living species in the region has never been seen or collected. Exploratory expeditions regularly return with images or samples of creatures that would richly animate science fiction stories, like a 6-foot-long bioluminescent shark.

Also unknown is the impact that deep sea mining would have on these creatures.

An experiment in 2021 in water about 3 miles (5 kilometers) deep off Mexico found that seabed mining equipment created sediment plumes of up to about 6.5 feet (2 meters) high. But the project authors stressed that they didn’t study the ecological impact. A similar earlier experiment was conducted off Peru in 1989. When scientists returned to that site in 2015, they found some species still hadn’t fully recovered.

Environmentalists have questioned whether seafloor creatures could be smothered by sediment plumes and whether the sediment in the water column could effect island communities that rely on healthy oceanic ecosystems. The Metals Company has argued that its impact is less than terrestrial mining.

Given humanity’s lack of knowledge of the ocean, it is not currently possible to set environmental baselines for oceanic health that could be used to weigh the economic benefits against the environmental harms of seabed mining.

Scarcity and the Economic Case for Mining

The economic case for deep seabed mining reflects both possibility and uncertainty.

On the positive side, it could displace some highly destructive terrestrial mining and augment the global supply of minerals used in clean energy sources such as wind turbines, photovoltaic cells and electric vehicles.

Terrestrial mining imposes significant environmental damage and costs to human health of both the miners themselves and the surrounding communities. Additionally, mines are sometimes located in politically unstable regions. The Democratic Republic of Congo produces 60% of the global supply of cobalt, for example, and China owns or finances 80% of industrial mines in that country. China also accounts for 60% of the global supply of rare earth element production and much of its processing. Having one nation able to exert such control over a critical resource has raised concerns.

Deep seabed mining comes with significant uncertainties, however, particularly given the technology’s relatively early state.

First are the risks associated with commercializing a new technology. Until deep sea mining technology is demonstrated, discoveries cannot be listed as “reserves” in firms’ asset valuations. Without that value defined, it can be difficult to line up the significant financing needed to build mining infrastructure, which lessens the first-mover advantage and incentivizes firms to wait for someone else to take the lead.

Commodity prices are also difficult to predict. Technology innovation can reduce or even eliminate the projected demand for a mineral. New mineral deposits on land can also boost supply: Sweden announced in January 2023 that it had just discovered the largest deposit of rare earth oxides in Europe.

In all, embarking on deep seabed mining involves sinking significant costs into new technology for uncertain returns, while posing risks to a natural environment that is likely to rise in value.

Who Gets to Decide the Future of Seafloor Mining?

The United Nations Convention on the Law of the Sea, which came into force in the early 1990s, provides the basic rules for ocean resources.

It allows countries to control economic activities, including any mining, within 200 miles of their coastlines, accounting for approximately 35% of the ocean. Beyond national waters, countries around the world established the International Seabed Authority, or ISA, based in Jamaica, to regulate deep seabed mining.

Critically, the ISA framework calls for some of the profits derived from commercial mining to be shared with the international community. In this way, even countries that did not have the resources to mine the deep seabed could share in its benefits. This part of the ISA’s mandate was controversial, and it was one reason that the United States did not join the Convention on the Law of the Sea.

Where large numbers of manganese nodules are found. The areas with the greatest concentrations are circled. (GEOMAR)

Where large numbers of manganese nodules are found. The areas with the greatest concentrations are circled. (GEOMAR)

With little public attention, the ISA worked slowly for several decades to develop regulations for exploration of undersea minerals, and those rules still aren’t completed. More than a dozen companies and countries have received exploration contracts, including The Metals Company’s work under the sponsorship of the island nation of Nauru.

ISA’s work has started to draw criticism as companies have sought to initiate commercial mining. A recent New York Times investigation of internal ISA documents suggested the agency’s leadership has downplayed environmental concerns and shared confidential information with some of the companies that would be involved in seabed mining. The ISA hasn’t finalized environmental rules for mining.

Much of the coverage of deep seabed mining has been framed to highlight the climate benefits. But this overlooks the dangers this activity could pose for the Earth’s largest pristine ecology – the deep sea. We believe it would be wise to better understand this existing, fragile ecosystem better before rushing to mine it.

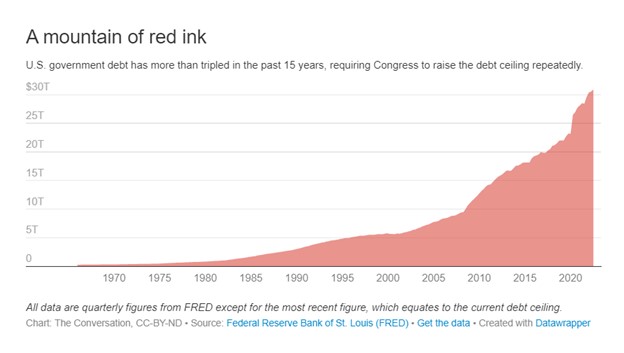

Why America Has a Debt Ceiling: Five Questions Answered

The Treasury Department on Jan. 13, 2023, said it expects the U.S. to hit the current debt limit of $31.38 trillion on Jan. 19. After that, the government would take “extraordinary measures” – which could extend the deadline until May or June – to avoid default. A default, even a risk of default would drive bond prices (interest rates) much higher than they currently are.

Is the debt ceiling still a good idea?

Economist Steve Pressman is a professor at The New School in Manhattan, below he explains the debt ceiling is and why we have it – and then shares his opinion on its usefulness.

What is the Debt Ceiling?

Like the rest of us, governments must borrow when they spend more money than they receive. They do so by issuing bonds, which are IOUs that promise to repay the money in the future and make regular interest payments. Government debt is the total sum of all this borrowed money.

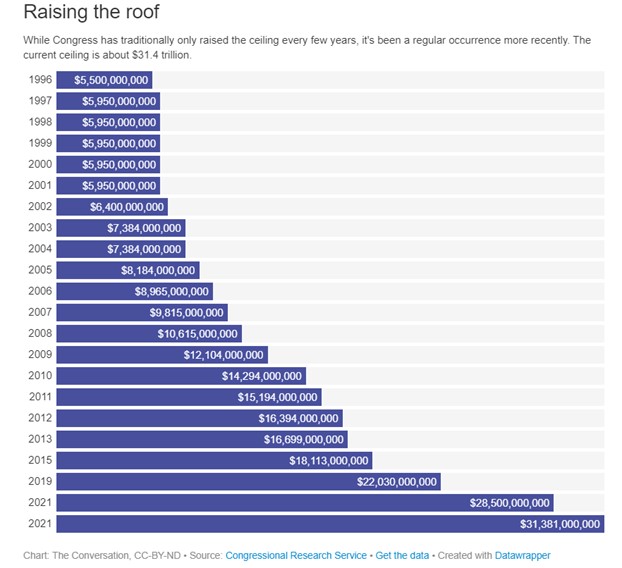

The debt ceiling, which Congress established a century ago, is the maximum amount the government can borrow. It’s a limit on the national debt.

What’s the National Debt?

On Jan. 10, 2023, U.S. government debt was $30.92 trillion, about 22% more than the value of all goods and services that will be produced in the U.S. economy this year.

Around one-quarter of this money the government actually owes itself. The Social Security Administration has accumulated a surplus and invests the extra money, currently $2.8 trillion, in government bonds. And the Federal Reserve holds $5.5 trillion in U.S. Treasurys.

The rest is public debt. As of October 2022, foreign countries, companies and individuals owned $7.2 trillion of U.S. government debt. Japan and China are the largest holders, with around $1 trillion each. The rest is owed to U.S. citizens and businesses, as well as state and local governments.

Before 1917, Congress would authorize the government to borrow a fixed sum of money for a specified term. When loans were repaid, the government could not borrow again without asking Congress for approval.

The Second Liberty Bond Act of 1917, which created the debt ceiling, changed this. It allowed a continual rollover of debt without congressional approval.

Congress enacted this measure to let then-President Woodrow Wilson spend the money he deemed necessary to fight World War I without waiting for often-absent lawmakers to act. Congress, however, did not want to write the president a blank check, so it limited borrowing to $11.5 billion and required legislation for any increase.

The debt ceiling has been increased dozens of times since then and suspended on several occasions. The last change occurred in December 2021, when it was raised to $31.38 trillion.

Currently, the U.S. Treasury has under $400 billion cash on hand, and the U.S. government expects to borrow around $100 billion each month this year.

When the U.S. nears its debt limit, the Treasury secretary – currently Janet Yellen – can use “extraordinary measures” to conserve cash, which she indicated would begin on Jan. 19. One such measure is temporarily not funding retirement programs for government employees. The expectation will be that once the ceiling is raised, the government would make up the difference. But this will buy only a small amount of time.

If the debt ceiling isn’t raised before the Treasury Department exhausts its options, decisions will have to be made about who gets paid with daily tax revenues. Further borrowing will not be possible. Government employees or contractors may not be paid in full. Loans to small businesses or college students may stop.

When the government can’t pay all its bills, it is technically in default. Policymakers, economists and Wall Street are concerned about a calamitous financial and economic crisis. Many fear that a government default would have dire economic consequences – soaring interest rates, financial markets in panic and maybe an economic depression.

Under normal circumstances, once markets start panicking, Congress and the president usually act. This is what happened in 2013 when Republicans sought to use the debt ceiling to defund the Affordable Care Act.

But we no longer live in normal political times. The major political parties are more polarized than ever, and the concessions McCarthy gave Republicans may make it impossible to get a deal on the debt ceiling.

Is There a Better Way?

One possible solution is a legal loophole allowing the U.S. Treasury to mint platinum coins of any denomination. If the U.S. Treasury were to mint a $1 trillion coin and deposit it into its bank account at the Federal Reserve, the money could be used to pay for government programs or repay government bondholders. This could even be justified by appealing to Section 4 of the 14th Amendment to the U.S. Constitution: “The validity of the public debt of the United States … shall not be questioned.”

Few countries even have a debt ceiling. Other governments operate effectively without it. America could too. A debt ceiling is dysfunctional and periodically puts the U.S. economy in jeopardy because of political grandstanding.

The best solution would be to scrap the debt ceiling altogether. Congress already approved the spending and the tax laws that require more debt. Why should it also have to approve the additional borrowing?

It should be remembered that the original debt ceiling was put in place because Congress couldn’t meet quickly and approve needed spending to fight a war. In 1917 cross-country travel was by rail, requiring days to get to Washington. This made some sense then. Today, when Congress can vote online from home, this is no longer the case.

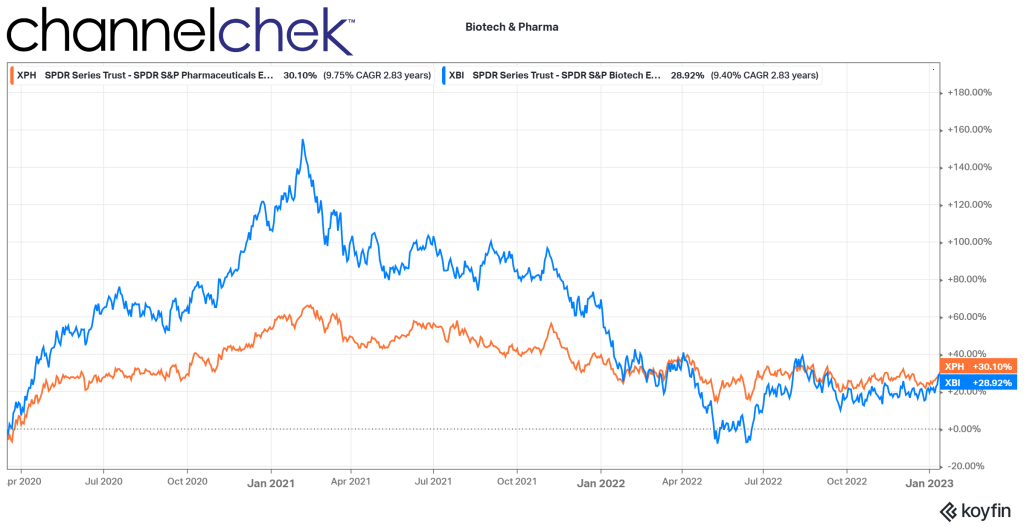

More Singles and Doubles for Investors in Biotech Expected (Few Home Runs)

Biotech has been highlighted by us a few times in recent weeks because of the potential the current financial dynamics could have for companies and investors. This past weekend, fresh out of the JP Morgan Health conference, a number of major publications have echoed a similar sentiment. A weekend piece in Barron’s in particular, caught my attention — its overall conclusion is the same as our readers have seen on Channelchek, but the path taken to get to the conclusion is somewhat different.

Health Landscape

From March 2020 until February 2021, biotech stocks were on a tear. The increase of 155%, as measured by the XBI, can be attributed to the intense focus on healthcare during the period. Higher demand for anything healthcare-related drove share prices among the companies in this sector. This went a long way to provide capital to companies whose very nature are high costs and low revenue. The strength of the sector brought up the deserving, along with others that benefitted from biotech’s overall momentum.

The peak was nearly two years ago. Just as interest in biotech strengthened less than deserving companies, the weakness that followed has brought down many companies that would likely be valued much higher if not for the “throw the baby out with the bathwater” effect, especially with so many sector index fund investors.

This weakness must have been a painful transition for management of companies that are enthusiastic about the prospects of their research and development but now find they may be in survival mode and now spend more time pitching their story and plans while hoping for an overall rise in interest in the sector.

Biotech Mood 2023

The challenge for smaller biotech and medical device companies, which ordinarily spend many years developing products, while benefiting from few or none on the market, is that current valuations have made it a steeper uphill battle to raise new funds for their work and if they do, they may over dilute current shares.

There is a change in the mood of life sciences companies. the Barron’s article, titled, Tanking Biotech Stocks Will Mean a Big Year for Deals. Who Could Benefit? wrote, “With reality setting in, it’s a buyer’s market for companies looking for acquisitions and partnerships, according to the pharmaceutical and medical technology execs who gathered at the J.P. Morgan healthcare investor conference.” JP Morgan describes this annual event as the largest and most informative healthcare investment symposium in the industry. It connects global industry leaders, emerging fast-growth companies, innovative technology creators and members of the investment community.

The conference had been on hiatus for a couple of years in response to pandemic concerns. Certainly there was a lot of new and interesting information to be absorbed and understood.

An overall impression coming from this 41st health symposium is that management of the cash-starved small firms are in a situation where they either have to make a deal with a partner or acquirer or perish. The realization has set in that terms or prices they may have once been able to command are not today’s reality.

Geoff Martha , CEO of Medtronic (MDT), a medical device manufacturer, is quoted as telling Barron’s “We’re getting lots of calls from companies that literally we talked to six months ago.” He explained, back we’d offer, “we’ll buy you for X amount,” and the response would be, “No way, we’re worth [two times that].” The Medtronic CEO said they are now calling back trying to restart the conversations.

Speaking about the terms now expected, the chief financial officer of Gilead Sciences (GILD) is quoted as saying, “It’s changed completely in terms of both the deal structures they’ll contemplate, the valuations that they’re thinking about,”

Large pharmaceutical companies such as Gilead have the means to provide a non-dilutive source of funds; they are coming off a number of very profitable years and are looking for more rewarding uses of their cash. This doesn’t mean they are willing to cut large acquisition checks; the current trend seems to be more partnering deals – collaborations that keep the best ideas moving forward.

The risk-reward analysis by the large pharmaceutical companies is versus low-return financial assets on the balance sheet. “We can make a lot of investments because it’s not high cost,” says Anat Ashkenazi, CFO of Eli Lilly (LLY). “And we know some of these will fail, some will succeed. That’s how we operate.”

This has ushered in a health industry where large companies with cash to spend are capable of placing many well analyzed bets on future devices and drugs from small companies that now must make a deal or risk perishing.

Take Away

When a small biotech company gets an infusion of cash from collaborating with a big pharmaceutical company, its stock typically reacts very positively. This is not the same level of reaction as an outright purchase, but worthwhile just the same. There is an atmosphere where these partnerships and collaborations are likely to occur with more frequency. This could add to the number of small biotech stock potential winners early in 2023.

Discover Inner Details from the Health Symposium

Investors eager to discover more about the companies at the JPM conference, what was said, where the industry is going, and actionable investor possibilities, can immerse themselves in this info deeper next week.

Here’s how.

Noble Capital Markets’ equity analysts and investment bankers attended the meetings, lunches, cocktail events, and interviewed company management. Next week they will share their collective takeaways. It is perhaps better than having endured the unusually bad weather yourself in San Francisco, get more information here!

Can the S&P Hold Above 4,000? Will Fed Presidents Change Market Expectations?

The S&P 500 closed on the cusp of 4,000 last week; while this is still nearly 800 points from an all-time-high if it should break through and hold, it could have positive psychological value for equity markets.

Two reports this week that have the potential to drive direction are both released on Wednesday. They are the December numbers on retail sales and the Fed’s Beige Book. Earnings season is also in full swing beginning this week. The reporting results of companies such as Netflix on Thursday may have an impact and set the stage for specific sectors and markets.

The Beige Book will provide a sense of economic conditions across the 12 Federal Reserve Districts, measuring the period between late November and early January. The tone of the last three releases points toward the US economy sitting on the brink of recession. There will be information on how interest rates are impacting housing markets and the strength of the labor market in different districts. The evidence in the report could mean the difference between a 0.25% increase or a 0.50% increase after the FOMC meeting held on January 31 through February 1.

Monday 1/16

US Markets and Government Offices closed (MLK Jr. Day).

Tuesday 1/17

8:30 AM ET, The Empire State Manufacturing Index disappointed in December with a reading of minus 11.2. The estimate for January is less negative minus 7.5. It tallies, each first of the month, the same pool of roughly 200 manufacturing executives (usually the CEO or the president) responses to a questionnaire on an assortment of indicators from the previous month.

3:00 PM ET, John Williams, the President of the Federal Reserve Bank of New York will be speaking. The New York Fed President is a particularly influential voting member of the FOMC. There is the possibility of insight into how that member may have changed their leaning on policy, which could impact markets.

Wednesday 1/18

8:30 AM ET, PPI- Final Demand Numbers will be released for December; they are expected to have fallen 0.1 percent on the month for a year-over-year increase of 6.8%. This would compare with a 7.4% year-over-year level in November.

8:30 AM ET, Retail Sales are expected to fall 0.9% in December on top of November’s weaker-than-expected 0.6% decline. Ex-vehicle sales slipped 0.2% in November, with this measure expected to fall 0.5% in December. When excluding both vehicles and gasoline, sales are expected to read 0.1% higher.

9:00 AM ET, the President of the Atlanta Fed, Raphael Bostic, will be speaking. Any time a voting member of the FOMC is speaking publicly, there is the potential for insight into how that member may have adjusted their leaning on policy. Atlanta Fed events are often broadcast live on this YouTube channel.

9:15 AM ET, Industrial Production has been contracting, and further the contraction is expected to continue with a consensus loss estimate of 0.1% for December. Manufacturing output is expected to fall 0.2%.

9:30 AM ET, the Chief Executive Officer of the St. Louis Fed, James Bullard, will be speaking.

10:00 AM ET, Business inventories in November are expected to rise 0.4% following a 0.3% build in October.

2:00 PM ET, Beige Book Release.

Thursday 1/19

8:30 AM ET, December’s annualized rates are expected at 1.358 million for starts and 1.380 million for permits which would compare with 1.427 and 1.342 million in November.

8:30 AM ET, Jobless claims for the January 14 week are expected to rise slightly to 215,000 versus 205,000 and 206,000 in the two prior weeks.

8:30 AM ET, The Philadelphia Fed manufacturing index is expected to come in at minus 10.0 in January. This report has been contracting for six of the last seven reports.

9:00 AM ET, Federal Reserve Bank of Boston Fed President Susan Collins is scheduled to speak.

The debt ceiling may be reached as per US Treasury Secretary Janet Yellen.

Friday 1/20

• 10:00 AM ET, Existing home sales in December are expected to have declined further to a 3.955 million annualized rate versus November’s lower-than-expected 4.090 million.

1:00 PM ET, Better World Acquisition (BWAC) will be interviewed in a C-Suite style interview. A video will be made available here on Channelchek.

What Else

The Federal Reserve members can impact longer-term interest rates by impacting expectations they set through their speeches. Some say their voices have been drowned out by analysts and media reporting. For this reason, Fed rhetoric may become elevated as we approach the next FOMC meeting that begins late month.

Earnings season begins to ramp up just as a major index at psychologically important levels. This could be what sets the tone for the stock market and various sectors for the first quarter.

In the future, the energy needed to run the powerful computers on board a global fleet of autonomous vehicles could generate as many greenhouse gas emissions as all the data centers in the world today.

That is one key finding of a new study from MIT researchers that explored the potential energy consumption and related carbon emissions if autonomous vehicles are widely adopted.

The data centers that house the physical computing infrastructure used for running applications are widely known for their large carbon footprint: They currently account for about 0.3 percent of global greenhouse gas emissions, or about as much carbon as the country of Argentina produces annually, according to the International Energy Agency. Realizing that less attention has been paid to the potential footprint of autonomous vehicles, MIT researchers built a statistical model to study the problem. They determined that 1 billion autonomous vehicles, each driving for one hour per day with a computer consuming 840 watts, would consume enough energy to generate about the same amount of emissions as data centers currently do.

The researchers also found that in over 90 percent of modeled scenarios, to keep autonomous vehicle emissions from zooming past current data center emissions, each vehicle must use less than 1.2 kilowatts of power for computing, which would require more efficient hardware. In one scenario — where 95 percent of the global fleet of vehicles is autonomous in 2050, computational workloads double every three years, and the world continues to decarbonize at the current rate — they found that hardware efficiency would need to double faster than every 1.1 years to keep emissions under those levels.

“If we just keep the business-as-usual trends in decarbonization and the current rate of hardware efficiency improvements, it doesn’t seem like it is going to be enough to constrain the emissions from computing onboard autonomous vehicles. This has the potential to become an enormous problem. But if we get ahead of it, we could design more efficient autonomous vehicles that have a smaller carbon footprint from the start,” says first author Soumya Sudhakar, a graduate student in aeronautics and astronautics.

Sudhakar wrote the paper with her co-advisors Vivienne Sze, associate professor in the Department of Electrical Engineering and Computer Science (EECS) and a member of the Research Laboratory of Electronics (RLE); and Sertac Karaman, associate professor of aeronautics and astronautics and director of the Laboratory for Information and Decision Systems (LIDS). The research appears today in the January-February issue of IEEE Micro.

Modeling Emissions

The researchers built a framework to explore the operational emissions from computers on board a global fleet of electric vehicles that are fully autonomous, meaning they don’t require a backup human driver.

The model is a function of the number of vehicles in the global fleet, the power of each computer on each vehicle, the hours driven by each vehicle, and the carbon intensity of the electricity powering each computer.

“On its own, that looks like a deceptively simple equation. But each of those variables contains a lot of uncertainty because we are considering an emerging application that is not here yet,” Sudhakar says.

For instance, some research suggests that the amount of time driven in autonomous vehicles might increase because people can multitask while driving, and the young and the elderly could drive more. But other research suggests that time spent driving might decrease because algorithms could find optimal routes that get people to their destinations faster.

In addition to considering these uncertainties, the researchers also needed to model advanced computing hardware and software that didn’t exist yet.

To accomplish that, they modeled the workload of a popular algorithm for autonomous vehicles, known as a multitask deep neural network, because it can perform many tasks at once. They explored how much energy this deep neural network would consume if it were processing many high-resolution inputs from many cameras with high frame rates simultaneously.

When they used the probabilistic model to explore different scenarios, Sudhakar was surprised by how quickly the algorithms’ workload added up.

For example, if an autonomous vehicle has 10 deep neural networks processing images from 10 cameras, and that vehicle drives for one hour a day, it will make 21.6 million inferences each day. One billion vehicles would make 21.6 quadrillion inferences. To put that into perspective, all of Facebook’s data centers worldwide make a few trillion inferences each day (1 quadrillion is 1,000 trillion).

“After seeing the results, this makes a lot of sense, but it is not something that is on a lot of people’s radar. These vehicles could actually be using a ton of computer power. They have a 360-degree view of the world, so while we have two eyes, they may have 20 eyes, looking all over the place and trying to understand all the things that are happening at the same time,” Karaman says.

Autonomous vehicles would be used for moving goods, as well as people, so there could be a massive amount of computing power distributed along global supply chains, he says. And their model only considers computing — it doesn’t take into account the energy consumed by vehicle sensors or the emissions generated during manufacturing.

Keeping Emissions in Check

To keep emissions from spiraling out of control, the researchers found that each autonomous vehicle needs to consume less than 1.2 kilowatts of energy for computing. For that to be possible, computing hardware must become more efficient at a significantly faster pace, doubling in efficiency about every 1.1 years.

One way to boost that efficiency could be to use more specialized hardware, which is designed to run specific driving algorithms. Because researchers know the navigation and perception tasks required for autonomous driving, it could be easier to design specialized hardware for those tasks, Sudhakar says. But vehicles tend to have 10- or 20-year lifespans, so one challenge in developing specialized hardware would be to “future-proof” it so it can run new algorithms.

In the future, researchers could also make the algorithms more efficient, so they would need less computing power. However, this is also challenging because trading off some accuracy for more efficiency could hamper vehicle safety.

Now that they have demonstrated this framework, the researchers want to continue exploring hardware efficiency and algorithm improvements. In addition, they say their model can be enhanced by characterizing embodied carbon from autonomous vehicles — the carbon emissions generated when a car is manufactured — and emissions from a vehicle’s sensors.

While there are still many scenarios to explore, the researchers hope that this work sheds light on a potential problem people may not have considered.

“We are hoping that people will think of emissions and carbon efficiency as important metrics to consider in their designs. The energy consumption of an autonomous vehicle is really critical, not just for extending the battery life, but also for sustainability,” says Sze.

Cathie Wood Reveals 2022’s Most Disruptive and Innovative Technologies

ARK Invest’s Cathie Wood penned a lookback-themed article about the innovations and disruptive companies of 2022. The purpose seemed to be to remind followers that although during the year, investors may have become disheartened with innovation, ‘look at the amazing opportunities that occurred.’ The innovations and companies highlighted were somewhat overlooked; following the path we are accustomed to from many breakthroughs, they fly under the radar. Then, suddenly they’re widely adopted. Below are many of her picks for innovation and companies she may now wish her funds held large positions in.

The Future of Internet

Suddenly everyone is talking about ChatGPT. According to Wood, artificial intelligence (AI), specifically, ChatGPT is advancing at a pace that is surprising even by standards set by earlier versions. This version of GPT-3, optimized for conversation, signed up one million users in just five days. By comparison, this onboarding of users is incredibly fast benchmarked against the original GPT-3, which took 24 months to reach the same level.

In 2022, TV advertising in the US underwent significant changes. Traditional, non-addressable, non-interactive TV ad spending dropped by 2% to $70 billion, according to Wood. Connected TV (CTV) ad spending on the same terms increased by 14% to ~$21 billion. Pure-play CTV operator Roku’s advertising platform revenue increased 15% year-over-year in the third quarter, the latest report available, while traditional TV scatter markets plummeted 38% year-over-year in the US. Roku maintained its position in the CTV market as the leading smart TV vendor in the US, accounting for 32% of the market.

Digital Wallets are replacing both credit cards and cash. In the category of offline commerce. They overtook cash as the top transaction method in 2020 and accounted for 50% of global online commerce volume in 2021. As an example of the growth, Square’s payment volume soared 193%, six times faster than the 30% increase in total retail spending 2019-2022 (relative to pre-COVID levels).

While overall e-commerce spending increased by 99% over the last three years, social commerce merchandise volume grew even faster. Shopify’s gross merchandise volume grew by 312%, almost four times faster than overall e-commerce and taking a significant share from other retail.

Underlying public blockchains continue to process transactions despite what may be going on surrounding the connected industries. Wood says it highlights that “their transparent, decentralized, and auditable ledgers could be a solution to the fraud and mismanagement associated with centralized, opaque institutions.” She explains, “After the FTX collapse, the share of trading volume on decentralized exchanges, which allow for trading without a central intermediary, rose 37% from 8.35% to 11.44%.

Genomic Revolution

Base editing and multiplexing have the potential to provide more effective CAR-T treatments for patients with otherwise incurable cancers. Cathie Wood provided an example from 2022 about a young girl in the UK with leukemia that went from hopeless in May to Canver-free in November.

In 2022 Dutch scientists at the Hubrecht Institute, UMC Utrecht, and the Oncode Institute used another form of gene editing called prime editing to correct the mutation that causes cystic fibrosis in human stem cells. Another example of how it is being adopted comes from Korean researchers at Yonsei University that used prime editing successfully to treat liver and eye diseases in adult mice.

CRISPR gene editing in Cathie’s words, “has delivered functional cures for beta-thalassemia and sickle cell disease.” She gives examples: CRISPR Therapeutics and Vertex Pharmaceuticals which together have treated more than 75 patients, resulting in some well-publicized “functional cures”. They are expecting FDA approval for Exa-Cel, the treatment for sickle cell and beta thalassemia, in early 2023.

In the category the Ark Invest founder referred to as other cell and gene therapies, she says in 2022, regulators approved several landmark cell and gene therapies. The examples she used to highlight this are Hemgenix for the treatment of Haemophilia B, Zyntelgo for beta thalassemia, Skysona for cerebral adrenoleukodystrophy, Yescarta and Breyanzi for Non-Hodgkin lymphoma, Tecartus for mantle cell lymphoma, and Carvykti and Abecma for multiple myeloma.

Liquid biopsies, blood tests via molecular diagnostic testing are enabling the early detection of colorectal cancer which, if discovered at or before stage 1, have a five-year survival rate greater than 90%. Late-stage or metastatic cancers account for more than 55% of deaths over a five-year period, but only 17% of new diagnoses.

Autonomous Technology & Robotics

During 2022 electric vehicle maker Tesla sales increased by 49% even as automobile sales declined by 8%. Tesla’s share of total auto sales in the US has increased to 3.8% from 1.4% in three years.

During 2022, GM expanded its autonomous driving taxi service to most of San Francisco in the first large-scale rollout in a major US city. Then it launched in both Phoenix and Austin late in the year. The automaker with a stodgy reputation, managed to compress the time to commercialization from nine years in San Francisco to just 90 days in Austin. Tesla, for its part, expanded access to its FSD (full self-driving) beta software to all owners in North America who had requested access.

By January 4, 2023, both Amazon and Walmart had begun deliveries using drones in select US cities. Autonomous logistics technology is no longer futuristic and is likely to continue being adopted and expanded.

Across the top 50 medical device companies, 90% rely on 3D printing for prototyping, testing, and even in some cases printing medical devices.

In 2022, SpaceX nearly doubled the number of rockets it launched to 61. It reused the same rocket in as few as 21 days, a dramatic improvement over the 356 days required for its first rocket reuse. Private Space Exploration is a reality. 61 rockets is an average of more than one per week.

Take Away

Hedge fund manager Cathie Wood took the new year as an opportunity to communicate examples of game-changing innovation that the equity market largely ignored in 2022. She finds these as confidence building that the premise of many of her managed funds is with merit. More importantly, in the face of market headwinds and media criticism, she wants these examples to help boost investor confidence “that ARK’s strategies are on the right side of change.” She tells readers, “innovation solves problems and has historically gained share during turbulent times.”

Unbalanced Hype in the Markets Surrounding the “Unknowable” Could be Costly

“It’s not knowable” if there will be a recession in 2023, said Fed Chair Jerome Powell recently. A month earlier, after the last change in monetary policy, he said it is easier to go too far and bring the economy back than to do too little and then have to then tame stronger inflationary pressures. The most recent CPI number shows a trend that policymakers want to see, but it likely is not a number the Fed will pivot off of. After all, for the Consumer Price Index (CPI) to rise by 6.5% YoY means that cost increases experienced by consumers are running more than three times higher than the Fed’s stated target. Of course, the rate increases have not had time to work their way into the system; they haven’t even fully worked their way into the interest rate markets.

An Alternative Way to Look at Tightening

Relatively speaking, a hypothetical decline in your investment account by 2% last month may be an improvement in performance if it had been down 3% the month before. But if your need to meet your goals is a positive 8%, then you still have a lot of work to do in order to consider yourself successful. The same for the Fed policymakers. US dollar buying power is losing ground, just not as quickly as it was. And since the inflation rate is also subject to what savers and investors call ‘the miracle of compounding’ and the jobs market is strong, the Fed has motivation and room to keep pulling money from the system and raising interest rates – the sooner, the better based on Powell’s statements.

And it may be that they are willingly driving the economy into reverse to stop service costs from rising as quickly, and bring inflationary wage increases lower. Workers, after all, have not reacted to the possibility of a recession. They still feel at ease leaving their employers at a very high pace, and the layoff rate is still near a record low. To demonstrate, the economy added 223,000 in payroll employment in December (well above the 200,000 forecast — and the unemployment rate came down to 3.5%, below the 3.7% forecast. This may not seem high compared to the gains just after the pandemic opening, but it is quite steamy.

Take Away

The financial news has been full of ‘pivot’ headlines for months. When it comes to the “unknowable,” it is important to remind oneself, as an investor, that very few things are a done deal until they happen. The big picture is the bond market has not priced itself in a way that fully reflects the Fed tightening of short-term rates. This represents difficulty for the Fed, and the Fed is looking for slower economic growth.

Throughout 2022, the big question while consumers faced increasing prices was whether the Federal Reserve would push the economy into decline. Their intent, after years of excessive stimulus, is to slow economic growth to bring inflation down. The Fed hiked interest rates seven times during 2022, its aggressive tactics caused some to worry about job losses and a recession. With an inflation rate that Powell thinks is more than three times too high, investors must consider that the Fed has different goals than investors but the same as consumers. We are all consumers, we’re not all investors.

As a final note, what the year brings is unknowable. There are always stocks going up, going down, and tracking sideways. A 2% inflation rate is easier to beat in terms of performance as an equity market investor than a 4% or 6% level. What the Fed will do, they likely don’t know for sure themselves; our job, that of investors, is to not get caught up in hype. And the markets and the media are breeding grounds for hype.

The Data Supporting Small-Caps Should Attract Money from Former Mega-Cap-Only Investors

When I see an investment statistic that reads, “in the past, this has happened 100% of the time,” I not only take note for my own portfolio consideration, I share it with my more risk-averse investment friends. It’s now mid-January, and like many investors, I have read dozens of 2023 forecasts and projections. I value the ones where the forecaster likely has skin in the game (i.e.: not many economists), and I am more highly interested in those that support forecasts with stats (ie: most economists). I came across a stat of ‘100% of the time’ from a trusted source that has skin in the game – this is certainly share-worthy.

Source

Each month Royce Investment Partners publishes an interview-style update between founder Chuck Royce and Co-CIO Frank Gannon. It’s always full of statistics and probability analysis. It never fails to be interesting and very often worthwhile. Investment decisions based on hard data from the past are less speculative, this doesn’t always make the investment a win, but it lowers the need for guessing. And if the stats are based on a large enough sample period, confidence to act overrides underlying opinion or emotions. The most recent publication from Royce Associates, LLC offers very compelling data.

The update includes a look at the stock market trends of late last year and why they’re confident small-cap stocks can achieve a positive return that could outpace larger-cap sectors. Especially for those companies whose underlying data meet criteria that they also explain.

Rear Looking View

The two were able to put the challenges for many investors last year in context by first talking about how infrequently bonds and stocks have gone down in the same year. This left 60/40 investors without anything to be happy about. Then they switched to small cap versus large cap, which they say was the third worst year for both the small-cap Russell 2000 Index, which fell 20.4%, and the Russell 1000 Index, which declined 19.1%. The third worst since each index’s inception at the end of 1978. According to the Royce update, “only two years had lower returns—and it was the same two years for both indexes—2008 during the Financial Crisis and 2002 through the worst year of the Internet Bubble.”

Forward-Looking View

As indicated above, Royce Associates believes small-cap is well positioned for positive returns and long-term comparative performance. The argument is hinged mainly on valuation but also on past behavior.

Valuation, they explain, even after last year’s sell-off, “remained near its lowest rate in 20 years compared to large-cap’s, based on our preferred valuation metric of the median last 12 months’ enterprise value to earnings before taxes (LTM EV/EBIT).” Royce recognized that accompanying the worldwide equity sell-off, many small-cap stocks were taken lower unrelated to financial fundamentals and/or operational expertise. “We have often been struck by the contrast between the more confident—albeit cautious—outlooks from the many management teams we’ve met with and the fatalistic headlines we see almost every day,” they explain.

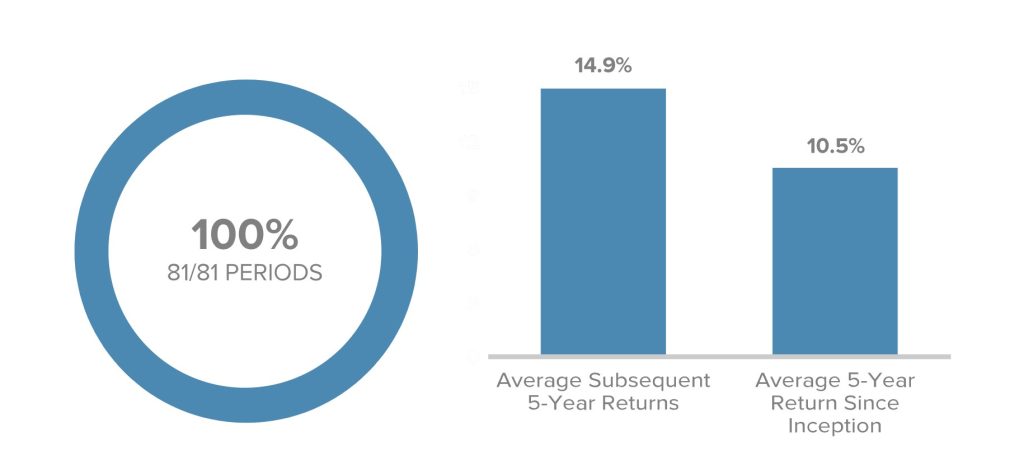

A High Probability of Positive Small-Cap Performance Ahead? Average Subsequent Five-Year Annualized Performance for the Russell 2000 in Trailing Five-Year Return Ranges of less than 5% from 12/31/83 through 12/31/22:

Source: Royce Investment Partners (Past performance is no guarantee of future results).

Frank Gannon says, “small-cap’s historical performance patterns show that below-average longer-term return periods have been followed by those with above-average longer-term returns—and the subsequent periods have enjoyed positive returns most of the time.” Drilling down to the numbers of the market’s current state, he says, “Subsequent annualized three-year returns from three-year entry points of less than 5% have been positive 99% of the time—that is, in 75 out of 76 three-year annualized periods—averaging 16.1% since the Russell 2000s 12/31/78 inception.”

Stretching the investment period out to five years had even higher probabilities and positive outcomes. “The Russell 2000 also had positive annualized five-year returns 100% of the time—that is, in all 81 five-year periods—and averaged an impressive 14.9% following five-year periods with annualized returns of 5% or less. We think this is especially relevant now because the respective three- and five-year annualized returns for the Russell 2000 as of 12/31/22 were 3.1% and 4.1%.”

On the subject of inflation, the Royce review was also positive. “Small-cap has beaten inflation in every decade going back to the 1930s—and is the only equity class to have done so.” Details of how this and other numbers are derived can be found in the article (available here).

Take-Away

While Royce Investment Partners, a fund company that holds small-cap stocks as its specialty, is not affiliated with Channelchek, or Noble Capital Markets, the monthly and quarterly newsletter/blog is always looked forward to. New readers should be ready for numbers and details backing up their stated positions. This is something not always found in public forecasts by other investment officers or portfolio managers. It’s more longwinded than some, but this is good because sound bites are not very helpful when one investor is trying to understand the thoughts of another.

To find data on ‘less-followed’ stocks, sign- up here for Channelchek and get immediate, no-cost access to information on over 6,000 small and microcap companies.

Triggering Cancer Cells to Become Normal Cells – How Stem Cell Therapies Can Provide New Ways to Stop Tumors from Spreading or Growing Back

How cells become cancerous is a process researchers are still trying to fully understand. Generally, normal cells grow and multiply through controlled cell division, where old and damaged cells are replaced after they die by new cells. Sometimes this process stops working, leading cells to start growing uncontrollably and develop into a tumor.

Traditionally, cancer treatments like chemotherapy, immunotherapy, radiation and surgery focus on killing cancer cells. Another type of treatment using stem cells called differentiation therapy, however, focuses on persuading cancer cells to become normal cells.

Two economists discussed that and more in a recent wide-ranging and exclusive interview for The Conversation. Brian Blank is a finance professor at Mississippi State University who specializes in the study of corporations and how they respond to economic downturns, Huanhuan Joyce Chen, Assistant Professor of Molecular Engineering, University of Chicago Pritzker School of Molecular Engineering and Abhimanyu Thakur,Postdoctoral Scholar in Molecular Engineering, University of Chicago Pritzker School of Molecular Engineering.

We are researchers who study how stem cells, or immature cells that can develop into different types of cells, behave in states of health and disease. We believe that stem cells can provide potential treatments for cancer of all types in many different ways.

How Do Stem Cells Contribute to Cancer?

Stem cells are unspecialized cells, meaning they can eventually become any one of the various types of cells that make up different parts of the body. They can replenish cells in the skin, bone, blood and other organs during development and regenerate and repair tissues when they’re damaged.

There are different types of stem cells. Embryonic stem cells are the first cells that initially form after a sperm fertilizes an egg and can give rise to all other cell types in the human body. Adult stem cells are more mature, meaning they can replace damaged cells only in one type of organ and have a limited ability to multiply. Researchers can reprogram adult stem cells, or differentiated cells, in the lab to act like embryonic stem cells.

Because stem cells can survive longer than regular cells, they have a much higher probability of accumulating genetic mutations that can result in loss of control over their growth and ability to regenerate. This is why many tumors harbor a small subpopulation of cells that function like stem cells. These so-called cancer stem cells are thought to be responsible at least in part for cancer initiation, progression, metastasis, recurrence and treatment resistance.

What is Differentiation Therapy?

Accumulating evidence is also showing that cancer stem cells can differentiate into multiple cell types, including noncancerous cells. Researchers are taking advantage of this fact through a type of treatment called differentiation therapy.

The concept of differentiation therapy originated from scientists observing that hormones and cytokines, which are proteins that play a key role in cell communication, can stimulate stem cells to mature and lose their ability to regenerate. It followed that forcing cancer stem cells to differentiate into more mature cells could subsequently stop them from multiplying uncontrollably, making them become normal cells.

Differentiation therapy has been successful in treating acute promyelocytic leukemia, an aggressive blood cancer. In this case, retinoic acid and arsenic are used to block a protein that stops myeloid cells, a type of blood cell derived from the bone marrow, from fully maturing. By allowing these cells to fully mature, they lose their cancerous qualities.

Furthermore, because differentiation therapy doesn’t focus on killing cancer cells and doesn’t surround healthy cells in the body with harmful chemicals, it can be less toxic than traditional treatments.

Using Stem Cells to Treat Cancer

There are many other potential ways to use stem cells to treat cancer. For example, cancer stem cells can be directly targeted to stop their growth, or turned into “Trojan horses” that attack other tumor cells.

Quiescent cancer stem cells, which don’t divide but are still alive, are another potential drug target. These cells typically play a big role in treatment resistance for various cancer types because they are able to regenerate and avoid death even better than regular cancer stem cells. Their quiescent quality can persist for decades and lead to a cancer relapse. They are also challenging to distinguish from regular cancer stem cells, making them difficult to study.

Researchers can also genetically engineer stem cells to express a protein that binds to a desired target in a cancer cell, increasing the efficacy of treatments by releasing drugs right at the tumor. For example, mesenchymal stem cells derived from bone marrow naturally migrate toward and stick to tumors, and can be used to deliver cancer drugs directly to cancer cells.

Stem cells can also be used to make organoid models, or miniature versions of organs, to screen potential cancer drugs and study the underlying mechanisms that lead to cancer.

Challenges in Stem Cell Therapy

Although, stem cells hold numerous advantages in their use in cancer therapy, they also face various challenges. For example, many current stem cell therapies that aren’t used in combination with other drugs are unable to completely eliminate tumors. There are also concerns about stem cell therapies potentially promoting tumor growth.

Despite these challenges, we believe that stem cell technologies have the potential to open new avenues for cancer therapy. Integrating genetic engineering with stem cells can overcome the major drawbacks of chemotherapeutics, such as toxicity to healthy cells. With further research, cancer stem cell therapies may one day become part of the standard of care for many types of cancer.

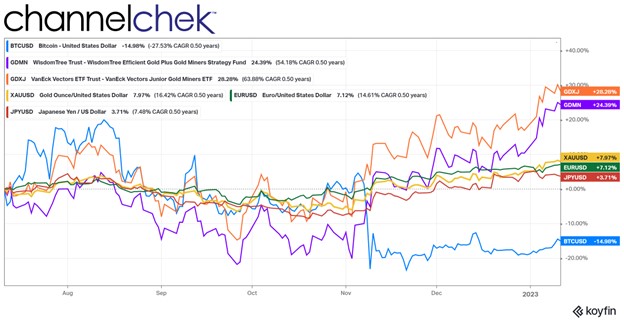

Gold is rising amid a weakening dollar and languishing cryptocurrencies as weaknesses in these asset classes are causing institutions and small investors alike to back off. What’s going on with gold and all the different methods for investors to gain exposure (bullion, ETF trusts, mining stocks)? And can it be believed? While several dynamics could indicate a perfect storm for exposure to gold prices, there have been a number of “head-fakes” over the past few years that have disappointed investors. Let’s look at what has been driving the recent upward march in the metal, which is still considered a store of value.

What’s Going On?

Gold futures touched an eight-month high on Wednesday, January 11 (Six-month chart below). The US dollar (shown here vs Yen and Euro) has been losing its strength in response to central bank hawkishness overseas coupled with a sizable decline in US bond yields.

The ramp up of China’s economy after a long period of Covid-related restrictions is pushing precious and industrial metal prices higher as demand is expected to escalate. Copper is also benefiting as futures contracts for this highly conductive metal reached its highest level since June.

The concerns over the global economy in 2023 also have some wealth managers allocating a larger portion to gold and silver for “investment insurance”. Gold historically has a low correlation to stock prices. Investors who were relying on a 60/40 (stocks & bonds) allocation to hedge each other against one asset class tumbling found they could have benefited from further diversification

Outlook (Bullion/Miners)

In a survey conducted before Christmas, BullionVault users forecast a gold price of $2,012.60 for the end of 2023, with nearly 38% of the 1,829 full responses pointing to the need to spread risk and diversify portfolios as the top reason for investing in bullion.

In his quarterly report on metals and mining, the Noble Capital Markets senior equity analyst, Mark Reichaman shared an outlook that sounded positive but cautious on precious metals miners. “We think precious metals prices around current levels are sufficient for mining companies to be profitable and attract new investment. Our outlook is for range-bound pricing around current levels with a modest upward bias in the first half of 2023, said Reichamn who focuses on materials and mining.

Take Away

A dollar trending upward attracts assets from across the globe. The long trend seems to have broken which has left higher demand for gold and gold mining investments. Also feeding into the demand is China reopening manufacturing that had been shuttered.

The crypto crash and current uncertainty have had the affect of causing investors in these alternative assets to move to other investments.

There has been a move by investors looking for alternative allocations to more traditional stock and bond holdings, including registered investment advisors (RIA). The 60/40 portfolio took a huge hit last year, an allocation to less correlated gold and gold stocks may be deemed prudent by those not looking to repeat.

Fed Chair Jerome Powell made three strong points during the panel on “Central Bank Independence and the Mandate—Evolving Views,” which just took place in Stockholm. These points include the role of elected representatives and unelected agency officials, the transparency of a central bank’s intents and actions while remaining independent of political agendas, and not becoming sidetracked from the established mandates.

Continued Independence and Transparency

Powell reminded the international audience, which included central bankers, that the purpose of monetary policy independence is the benefits allowed the policymakers. This independence can insulate policy decisions from short-term political considerations. “Price stability is the bedrock of a healthy economy and provides the public with immeasurable benefits over time. But restoring price stability when inflation is high can require measures that are not popular in the short term as we raise interest rates to slow the economy,” said Powell. The head of the US central bank then explained the absence of politics over central bank decisions provides for less conflicted decision-making in light of short-lived political considerations.

While speaking from a US point of view, Powell said that in a “well-functioning democracy, important public policy decisions should be made, in almost all cases, by the elected branches of government.” He explained that agencies trusted to act independently, such as the Federal Reserve, should have a narrow and explicitly defined mission that protects the agency from fleeting political considerations.

Within this kind of independence in a representative democracy, including transparency that allows for oversight, the Fed and other agencies find legitimacy. Powell said about of the current makeup of the Fed, “We are tightly focused on achieving our statutory mandate and on providing useful and appropriate transparency.”

Focus on Mandates

Climate change is not part of the US central bank’s statutory goals and authority. On the subject of climate, Powell added, “we resist the temptation to broaden our scope to address other important social issues of the day. Taking on new goals, however worthy, without a clear statutory mandate would undermine the case for our independence.”

In the area of bank regulation, Powell told the audience that independence helps ensure that the public can be confident that the overseer’s supervisory decisions are not influenced by political considerations. In response to his own hypothetical question about whether it is wise to incorporate into bank supervision the perceived risks associated with climate change, consistent with existing mandates, Powell sounded strongly opposed. “Addressing climate change seems likely to require policies that would have significant distributional and other effects on companies, industries, regions, and nations. Decisions about policies to directly address climate change should be made by the elected branches of government and thus reflect the public’s will as expressed through elections.”

He did, however, share his view that any climate-related financial risks that pose material risks to the banking system are the Fed’s responsibility and under their supervision. “But without explicit congressional legislation, it would be inappropriate for us to use our monetary policy or supervisory tools to promote a greener economy or to achieve other climate-based goals. We are not, and will not be, a “climate policymaker.”

Take Away

On January 10th, the head of the US central bank participated in an international symposium to mark the end of Stefan Ingves’ time as governor of Sweden’s central bank. Senior central bank officials and prominent academics participate in four panels that address central bank independence from various angles – climate, payments, mandates, and global policy coordination. Fed Chair Powell stood determined and resolute that the Fed’s mandate is narrow, well-defined, and should not be clouded with short-term political goals.

There has been pressure on the Fed to adopt additional mandates that include social reforms and climate concerns. His talk before a world audience may be the first time Jerome Powell has publicly addressed this pressure. The US House of Representatives has just shifted its balance to a more conservative power base; this may have had an empowering impact on Powell’s open remarks.