HOUSTON, Nov. 17, 2022 (GLOBE NEWSWIRE) — Orion Group Holdings, Inc. (NYSE: ORN) (the “Company”), a leading specialty construction company, completed a 15 month rebuild of the recently commissioned Dredge Lavaca. Advancements to the dredge’s ladder, accommodations, and operating systems were made to continue to provide exceptional dredging service to its clients and industry partners in both the public and private sectors along the Gulf Coast. The Lavaca is scheduled to begin work mid-November 2022 on a newly awarded contract for the Port of Corpus Christi and will take part in the continued maintenance of waterways, deepening and widening projects for years to come throughout the Gulf Coast. The design of the dredge, including its modular quarters, walkways, access and egress points, ventilation, handrail & fendering systems have all been engineered specifically with an emphasis on safety. Design improvements to the crew accommodations reduced noise and vibrations during dredging operations and provide a reprieve for the crew during their rest periods. The open-concept lever room allows for the leverman to monitor and control all dredging systems from a specially designed control station with touchscreen displays and floor-to-ceiling windows that provide a 180-degree field of view. Tier III diesel-electric engines and electric winches is another step forward for the Company to continue our commitment to protecting the environment by preventing potential spills and reducing NOx emissions within our operating areas. Orion’s commitment to Safety and “Target Zero” is also instilled into our vetted contractors, and is reflected indirectly in this project, as the project surpassed 65,000 manhours without any lost time incidents or recordable injuries.

Orion Group Holdings, Inc., a leading specialty construction company serving the infrastructure, industrial and building sectors, provides services both on and off the water in the continental United States, Alaska, Canada and the Caribbean Basin through its marine segment and its concrete segment. The Company’s marine segment provides construction and dredging services relating to marine transportation facility construction, marine pipeline construction, marine environmental structures, dredging of waterways, channels and ports, environmental dredging, design, and specialty services. Its concrete segment provides turnkey concrete construction services including pour and finish, dirt work, layout, forming, and rebar across the light commercial, structural and other associated business areas. The Company is headquartered in Houston, Texas with regional offices throughout its operating areas.

Forward-Looking Statements

The matters discussed in this press release may constitute or include projections or other forward-looking statements within the meaning of the Private Securities Litigation Reform Act of 1995, the provisions of which the Company is availing itself. Certain forward-looking statements can be identified by the use of forward-looking terminology, such as ‘believes’, ‘expects’, ‘may’, ‘will’, ‘could’, ‘should’, ‘seeks’, ‘approximately’, ‘intends’, ‘plans’, ‘estimates’, or ‘anticipates’, or the negative thereof or other comparable terminology, or by discussions of strategy, plans, objectives, intentions, estimates, forecasts, outlook, assumptions, or goals. In particular, statements regarding future operations or results, including those set forth in this press release and any other statement, express or implied, concerning future operating results or the future generation of or ability to generate revenues, income, net income, profit, EBITDA, EBITDA margin, or cash flow, including to service debt, and including any estimates, forecasts or assumptions regarding future revenues or revenue growth, are forward-looking statements. Forward looking statements also include estimated project start date, anticipated revenues, and contract options which may or may not be awarded in the future. Forward looking statements involve risks, including those associated with the Company’s fixed price contracts that impacts profits, unforeseen productivity delays that may alter the final profitability of the contract, cancellation of the contract by the customer for unforeseen reasons, delays or decreases in funding by the customer, levels and predictability of government funding or other governmental budgetary constraints and any potential contract options which may or may not be awarded in the future, and are the sole discretion of award by the customer. Past performance is not necessarily an indicator of future results. In light of these and other uncertainties, the inclusion of forward-looking statements in this press release should not be regarded as a representation by the Company that the Company’s plans, estimates, forecasts, goals, intentions, or objectives will be achieved or realized. Readers are cautioned not to place undue reliance on these forward-looking statements, which speak only as of the date hereof. The Company assumes no obligation to update information contained in this press release whether as a result of new developments or otherwise.

Please refer to the Company’s Annual Report on Form 10-K, filed on March 7, 2022, which is available on its website at www.oriongroupholdingsinc.com or at the SEC’s website at www.sec.gov, for additional and more detailed discussion of risk factors that could cause actual results to differ materially from our current expectations, estimates or forecasts.

Vancouver, BC – TheNewswire – November 17, 2022 – Element79 Gold Corp. ( CSE:ELEM) (OTC:ELMGF) (FSE:7YS) (” Element79 Gold “, the ” Company “) today announced it has entered non-binding letters of intent (the ” Centra LOI ” and ” Valdo LOI ” respectively) with Centra Mining Ltd. (” Centra “) and Valdo Minerals Ltd. (” Valdo “), whereby the Company intends to sell a total of five properties from its Battle Mountain Portfolio, which is comprised of fifteen properties located in the famous gold mining district of northeastern Nevada, USA.

The properties being considered for sale include:

The Long Peak Project: 34 unpatented claims in Lander County

The Stargo Project: 337 unpatented claims in Nye County

The Elder Creek Project: 23 unpatented claims in Lander County

The North Mill Creek Project: 6 unpatented claims in Lander County

The Elephant Project: 197 unpatented claims in Lander County

“The potential sale of these claim blocks would allow Element79 Gold to continue unlocking additional value from our vast portfolio of prospective properties while maintaining our established focus on the rapid pace of development at our primary high-grade gold assets,” stated James Tworek, President and CEO of Element79 Gold. “Overall, we believe the Battle Mountain Portfolio contains several additional targets which warrant extensive exploration and prospecting to further validate historic high-grade samples. Selling some of the portfolio has been a corporate strategy point and this is a great opportunity that allows us both unlock value for our shareholders and to focus our energy on our core projects.”

The Long Peak Project

The Long Peak Project (” Long Peak “) is comprised of 34 unpatented claims located near Copper Basin and the Copper Canyon Mine in Lander County, Nevada. Long Peak hosts significant historic prospects, warranting further exploration at Long Peak.

The Stargo Project

The Stargo Project (” Stargo “) is comprised of 337 unpatented claims located south of the Battle Mountain Trend in Nye County, Nevada.The large claim block contains attractive host rocks, tertiary age intrusives, and appropriate aged structural preparation to represent an attractive area for exploration target development.

The North Mill Creek Project

The North Mill Creek Project (” North Mill Creek “) is comprised of 6 unpatented claims located at the margins of the Goat Window in Lander County, Nevada. The Goat Window is an exposure of lower plate rocks beneath the Roberts Mountains Thrust which are the preferred carbonate host of Carlin-type gold deposits. Previous drilling completed at North Mill Creek yielded encouraging results warranting follow-up exploration.

The Elder Creek Project

The Elder Creek Project (” Elder Creek “) is comprised of 23 unpatented claims which cover the historic Elder Creek open-pit mine in Lander County, Nevada. Elder Creek is hosted in upper plate rocks where the mine area is believed to represent leakage from the deeper lower plate of the Roberts Mountains Thrust, suggesting that deeper targets could host significant mineralization within faulted and anticline folded sedimentary beds.

The Elephant Project

The Elephant Project (” Elephant “) is comprised of 197 claims located at the foot of the mine dumps at Nevada Gold Mines’ Phoenix operation. Elephant hosts a covered pediment target with various depths of cover based on the displacement of fault blocks. Limited past drilling has confirmed the presence and mineralization of the Elephant target model.

Terms of The Centra LOI

Under the terms of the Centra LOI, it is anticipated that Centra would purchase all of Element79 Gold’s interests and obligations in relation to Long Peak, and Stargo in exchange for a total consideration of $1,000,000 CAD payable by the issuance of an aggregate of 2,500,000 common shares of Centra at a deemed price of $0.40 CAD per share. The Centra LOI is non-binding and is subject to a 180-day exclusivity period.

Terms of the Valdo LOI

Under the terms of the Valdo LOI, it is anticipated that Valdo would purchase all of Element79 Gold’s interests and obligations in relation to North Mill Creek, Elder Creek, and Elephant in exchange for a total consideration of $1,125,000 CAD payable by the issuance of an aggregate of 3,750,000 common shares of Centra at a deemed price of $0.30 CAD per share. The Valdo LOI is non-binding and is subject to a 180-day exclusivity period.

Qualified Person

The technical information in this release has been reviewed and verified by Neil Pettigrew, M.Sc., P. Geo., Director of Element79 Gold and a “qualified person” as defined by National Instrument 43-101.

About Element79 Gold

Element79 Gold is a mineral exploration company focused on the acquisition, exploration and development of mining properties for gold and associated metals. Element79 Gold has acquired its flagship Maverick Springs Project located in the famous gold mining district of northeastern Nevada, USA, between the Elko and White Pine Counties, where it has recently completed a 43-101-compliant, pit-constrained mineral resource estimate reflecting an Inferred resource of 3.71 million ounces of gold equivalent* “AuEq” at a grade of 0.92 g/t AuEq (0.34 g/t Au and 43.4 g/t Ag)) with an effective date of Oct. 7, 2021 (see news release January 31st, 2022, available on SEDAR). The acquisition of the Maverick Springs Project also included a portfolio of 15 properties along the Battle Mountain trend in Nevada, which the Company is analyzing for further merit of exploration, along with the potential for sale or spin-out. In British Columbia, Element79 Gold has executed a Letter of Intent to acquire a private company which holds the option to 100% interest of the Snowbird High-Grade Gold Project, which consists of 10 mineral claims located in Central British Columbia, approximately 20km west of Fort St. James. In Peru, Element79 Gold holds 100% interest in the past producing Lucero Mine, one of the highest-grade underground mines to be commercially mined in Peru’s history, as well as the past producing Machacala Mine. The Company also has an option to acquire 100% interest in the Dale Property which consists of 90 unpatented mining claims located approximately 100 km southwest of Timmins, Ontario, Canada in the Timmins Mining Division, Dale Township. For more information about the Company, please visit www.element79.gold or www.element79gold.com .

This press contains “forward‐looking information” and “forward-looking statements” under applicable securities laws (collectively, “forward‐looking statements”). These statements relate to future events or the Company’s future performance, business prospects or opportunities that are based on forecasts of future results, estimates of amounts not yet determinable and assumptions of management made in light of management’s experience and perception of historical trends, current conditions and expected future developments. Forward-looking statements include, but are not limited to, statements with respect to: the Company’s plans for its portfolio of mining projects and properties; the Company’s business strategy; future planning processes; exploration activities; the timing and result of exploration activities; capital projects and exploration activities and the possible results thereof; any potential future cash flow and the timing thereof; acquisition opportunities; the impact of acquisitions, if any, on the Company. Assumptions may prove to be incorrect and actual results may differ materially from those anticipated. Consequently, forward-looking statements cannot be guaranteed. As such, investors are cautioned not to place undue reliance upon forward-looking statements as there can be no assurance that the plans, assumptions or expectations upon which they are placed will occur. All statements other than statements of historical fact may be forward‐looking statements. Any statements that express or involve discussions with respect to predictions, expectations, beliefs, plans, projections, objectives or future events or performance (often, but not always, using words or phrases such as “seek”, “anticipate”, “plan”, “continue”, “estimate”, “expect”, “may”, “will”, “project”, “predict”, “forecast”, “potential”, “target”, “intend”, “could”, “might”, “should”, “believe” and similar expressions) are not statements of historical fact and may be “forward‐looking statements”.

Actual results may vary from forward-looking statements. Forward-looking statements are subject to known and unknown risks, uncertainties and other factors that may cause actual results to materially differ from those expressed or implied by such forward-looking statements, including but not limited to: the duration and effects of the coronavirus and COVID-19; risks related to the integration of acquisitions; actual results of exploration activities; conclusions of economic evaluations; changes in project parameters as plans continue to be refined; commodity prices; variations in ore reserves, grade or recovery rates; actual performance of plant, equipment or processes relative to specifications and expectations; accidents; labour relations; relations with local communities; changes in national or local governments; changes in applicable legislation or application thereof; delays in obtaining approvals or financing or in the completion of development or construction activities; exchange rate fluctuations; requirements for additional capital; government regulation; environmental risks; reclamation expenses; outcomes of pending litigation; limitations on insurance coverage as well as those factors discussed in the Company’s other public disclosure documents, available on www.sedar.com . Although the Company has attempted to identify important factors that could cause actual results to differ materially from those contained in forward-looking statements, there may be other factors that cause results not to be as anticipated, estimated or intended. The Company believes that the expectations reflected in these forward‐looking statements are reasonable, but no assurance can be given that these expectations will prove to be correct and such forward‐looking statements included herein should not be unduly relied upon. These statements speak only as of the date hereof. The Company does not intend, and does not assume any obligation, to update these forward-looking statements, except as required by applicable laws.

Source: Element79 Gold

Neither the Canadian Securities Exchange nor the Market Regulator (as that term is defined in the policies of the Canadian Securities Exchange) accepts responsibility for the adequacy or accuracy of this release.

Copyright (c) 2022 TheNewswire – All rights reserved.

BOTHELL, Wash., Nov. 17, 2022 (GLOBE NEWSWIRE) — Cocrystal Pharma, Inc. (Nasdaq: COCP) today announced that CC-42344 demonstrated a favorable safety profile in both the single-ascending dose and the multiple-ascending dose portions of the ongoing Phase 1 study. CC-42344 is a broad-spectrum oral antiviral for the treatment of pandemic and seasonal influenza A with a novel mechanism of action.

“We are encouraged by the clean safety profile observed with all dose levels in both the single-ascending and multiple-ascending dose portions of the Phase 1 study, and we will be assessing the pharmacokinetic data from this trial in the coming weeks,” said Sam Lee, Ph.D., Cocrystal’s President and co-interim CEO. “We remain on track to reach an important milestone of reporting topline Phase 1 study results later this year.

“Influenza is among the most serious global public health threats, particularly with the emergence of pandemic strains and resistance to available drugs,” he added. “Based on a novel mechanism of action and a high barrier to resistance, we believe CC-42344 holds potential to be a best-in-class oral treatment for pandemic and seasonal influenza.”

The randomized, double-controlled, dose-escalating Phase 1 study in Australia was designed to assess the safety, tolerability and pharmacokinetics (PK) of orally administered CC-42344 in healthy adults. In July 2022 Cocrystal reported that PK data from the single-ascending dose portion of the study support once-daily dosing. In October 2022 enrollment in the multiple-ascending dose portion of the trial was completed. The Company plans to present topline study results at the upcoming World Antiviral Congress on December 1, 2022 and to submit an application with the United Kingdom Medicines and Healthcare Products Regulatory Agency to conduct a Phase 2a human challenge study in early 2023. Subject to regulatory agency clearance, the Phase 2a study is expected to be initiated in the second half of 2023.

About CC-42344 CC-42344 is an oral PB2 inhibitor discovered using Cocrystal’s proprietary structure-based drug discovery platform technology. It is specifically designed to be effective against all significant pandemic and seasonal influenza A strains and to have a high barrier to resistance due to the way the virus’ replication machinery is targeted. CC-42344 targets the influenza polymerase, an essential replication enzyme with several highly conserved regions common to multiple influenza strains. In vitro testing showed CC-42344’s excellent antiviral activity against influenza A strains, including pandemic and seasonal strains, as well as against strains resistant to Tamiflu® and Xofluza®, while also demonstrating favorable PK and safety profiles.

About Cocrystal Pharma, Inc. Cocrystal Pharma, Inc. is a clinical-stage biotechnology company discovering and developing novel antiviral therapeutics that target the replication process of influenza viruses, coronaviruses (including SARS-CoV-2), hepatitis C viruses and noroviruses. Cocrystal employs unique structure-based technologies and Nobel Prize-winning expertise to create first- and best-in-class antiviral drugs. For further information about Cocrystal, please visit www.cocrystalpharma.com.

This press release contains forward-looking statements within the meaning of the Private Securities Litigation Reform Act of 1995, including statements regarding our being on track to report topline results of the Phase 1 study later in 2022, the potential of CC-42344 to be a best-in-class candidate for the treatment of seasonal and pandemic influenza, and our expectations and plans to submit an application to the United Kingdom Medicines and Healthcare Products Regulatory Agency to conduct a Phase 2a human challenge study in early 2023 and to initiate the Phase 2a study in the second half of 2023. The words “believe,” “may,” “estimate,” “continue,” “anticipate,” “intend,” “should,” “plan,” “could,” “target,” “potential,” “is likely,” “will,” “expect” and similar expressions, as they relate to us, are intended to identify forward-looking statements. We have based these forward-looking statements largely on our current expectations and projections about future events. Some or all of the events anticipated by these forward-looking statements may not occur. Important factors that could cause actual results to differ from those in the forward-looking statements include, but are not limited to, the risks and uncertainties arising from any future impact of COVID-19 (including long-term or pervasive effects of the virus), inflation, interest rate increases and the war in Ukraine on the U.K. and global economy and on our Company, including supply chain disruptions and our continued ability to proceed with our programs, including our influenza A program, the ability of the contract research organization to recruit patients into clinical trials, the results of future preclinical and clinical studies, and general risks arising from clinical trials. Further information on our risk factors is contained in our filings with the SEC, including our Annual Report on Form 10-K for the year ended December 31, 2021. Any forward-looking statement made by us herein speaks only as of the date on which it is made. Factors or events that could cause our actual results to differ may emerge from time to time, and it is not possible for us to predict all of them. We undertake no obligation to publicly update any forward-looking statement, whether as a result of new information, future developments or otherwise, except as may be required by law.

The health of the US Treasury market impacts almost all other markets. This is because the “risk-free” market (US Treasuries) and its relationship to the US dollar is the foundation from which other markets stand. If it is in trouble, all markets suffer. The “health” measure most associated with securities like treasuries is liquidity or whether money can be raised when needed. Other measures include market spread between the bid and the ask, trading activity levels, and price impact or how a large transaction impacts the price.

A just released report by New York Fed economists Michael Fleming and Claire Nelson discuss the current state of the U.S. Treasury markets from the unique point of view and access to information of the New York Fed.

The report follows:

How Liquid Has the Treasury Market Been in 2022?

Policymakers and market participants are closely watching liquidity conditions in the U.S. Treasury securities market. Such conditions matter because liquidity is crucial to the many important uses of Treasury securities in financial markets. But just how liquid has the market been and how unusual is the liquidity given the higher-than-usual volatility? In this post, we assess the recent evolution of Treasury market liquidity and its relationship with price volatility and find that while the market has been less liquid in 2022, it has not been unusually illiquid after accounting for the high level of volatility.

Why Liquidity Matters

The U.S. Treasury securities market is the largest and most liquid government securities market in the world. Treasury securities are used to finance the U.S. government, to manage interest rate risk, as a risk-free benchmark for pricing other financial instruments, and by the Federal Reserve in implementing monetary policy. Having a liquid market is important for all these purposes and thus of great interest to market participants and policymakers alike.

Measuring Liquidity

Liquidity typically refers to the cost of quickly converting an asset into cash (or vice versa) and is measured in a variety of ways. We consider three commonly used measures, calculated using high-frequency data from the interdealer market: bid-ask spreads, order book depth, and price impact. The measures are for the most recently auctioned

(on-the-run) two-, five-, and ten-year notes (the three most actively traded Treasury securities, as shown in this post) and are calculated for New York trading hours (defined as 7 a.m. to 5 p.m.). Our data source is BrokerTec, which is estimated to account for 80 percent of trading in the electronic interdealer broker market.

The Market Has Been Relatively Illiquid in 2022

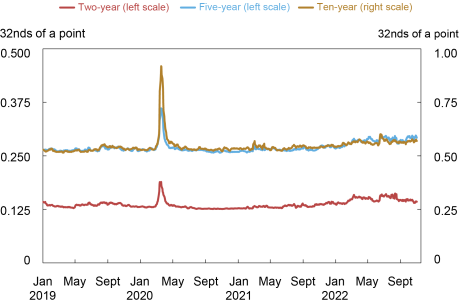

The bid-ask spread—the difference between the lowest ask price and the highest bid price for a security—is one of the most popular liquidity measures. As shown in the chart below, bid-ask spreads have widened out in 2022, but have remained well below the levels observed during the COVID-related disruptions of March 2020 (examined in this post). The widening has been somewhat greater for the two-year note relative to its average and relative to its level in March 2020.

Bid-Ask Spreads Have Widened Modestly

Liberty Street Economics chart plots the five-day moving averages of average daily bid-ask spreads for the two-, five-, and ten-year notes in the interdealer market from January 2, 2019, to October 31, 2022.

Source: Authors’ calculations, based on data from BrokerTec.

Notes: The chart plots five-day moving averages of average daily bid-ask spreads for the on-the-run two-, five-, and ten-year notes in the interdealer market from January 2, 2019, to October 31, 2022. Spreads are measured in 32nds of a point, where a point equals one percent of par.

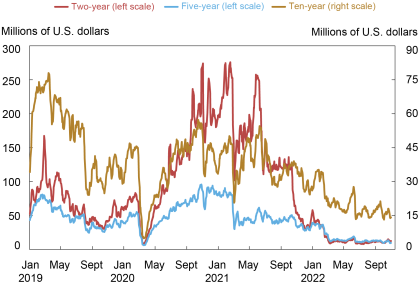

The next chart plots order book depth, measured as the average quantity of securities available for sale or purchase at the best bid and offer prices. Depth levels again point to relatively poor liquidity in 2022, but with the differences across securities more striking. Depth in the two-year note has been at levels commensurate with those of March 2020, whereas depth in the five-year note has remained somewhat higher—and depth in the ten-year note appreciably higher—than the levels of March 2020.

Order Book Depth Lowest since March 2020

Liberty Street Economics chart plots five-day moving averages of average daily depth for the two-, five-, and ten-year notes in the interdealer market from January 2, 2019, to October 31, 2022.

Source: Authors’ calculations, based on data from BrokerTec.

Notes: The chart plots five-day moving averages of average daily depth for the on-the-run two-, five-, and ten-year notes in the interdealer market from January 2, 2019, to October 31, 2022. Data are for order book depth at the inside tier, averaged across the bid and offer sides. Depth is measured in millions of U.S. dollars par.

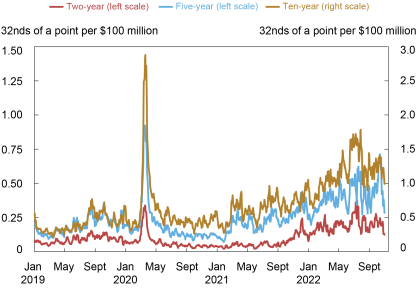

Measures of the price impact of trades also suggest a notable deterioration of liquidity. The next chart plots the estimated price impact per $100 million in net order flow (that is, buyer-initiated trading volume less seller-initiated trading volume). A higher price impact suggests reduced liquidity. Price impact has been high this year, and again more notably so for the two-year note relative to the March 2020 episode. That said, price impact looks to have peaked in late June and July, and to have declined most recently (in October).

Price Impact Highest since March 2020

Liberty Street Economics chart plots the estimated price impact per $100 million in net order flow for the two-, five-, and ten-year notes in the interdealer market from January 2, 2019, to October 31, 2022.Source: Authors’ calculations, based on data from BrokerTec.

Notes: The chart plots five-day moving averages of slope coefficients from daily regressions of one-minute price changes on one-minute net order flow (buyer-initiated trading volume less seller-initiated trading volume) for the on-the-run two-, five-, and ten-year notes in the interdealer market from January 2, 2019, to October 31, 2022. Price impact is measured in 32nds of a point per $100 million, where a point equals one percent of par.

Note that we start our analysis of liquidity in this post in 2019 and not earlier. One reason is to highlight the developments in 2022. Another reason is that the minimum price increment for the two-year note was halved in late 2018, creating a break in the note’s bid-ask spread and depth series. Longer time series of bid-ask spreads, order book depth, and price impact are plotted in this post and this paper. The longer history indicates that the price impact in the two-year note is currently at levels comparable to those seen during the 2007-09 global financial crisis, as well as in March 2020.

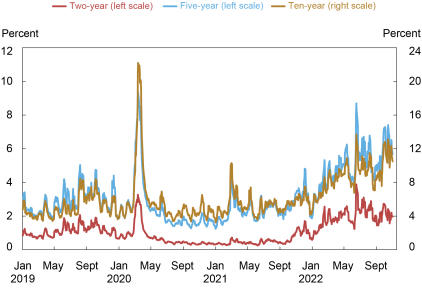

Volatility Has Also Been High

Pandemic-induced supply disruptions, high inflation, policy uncertainty, and geopolitical conflict have led to a sizable increase in uncertainty about the expected path of interest rates, resulting in high price volatility in 2022, as shown in the next chart. As with liquidity, volatility has been especially high lately for the two-year note relative to its history, likely reflecting the importance of near-term monetary policy uncertainty in explaining the current episode. Volatility has caused market makers to widen their bid-ask spreads and post less depth at any given price (to manage the increased risk of taking on positions), and for the price impact of trades to increase, illustrating the well-known negative relationship between volatility and liquidity.

Price Volatility Highest Since March 2020

Liberty Street Economics chart plots five-day moving averages of price volatility for the two-, five-, and ten-year notes in the interdealer market from January 2, 2019, to October 31, 2022.

Source: Authors’ calculations, based on data from BrokerTec.

Notes: The chart plots five-day moving averages of price volatility for the on-the-run two-, five-, and ten-year notes in the interdealer market from January 2, 2019, to October 31, 2022. Price volatility is calculated for each day by summing squared one-minute returns (log changes in midpoint prices) from 7 a.m. to 5 p.m., annualizing by multiplying by 252, and then taking the square root. It is reported in percent.

Liquidity Has Tracked Volatility

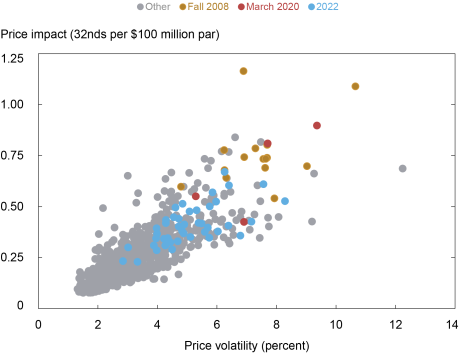

To assess whether liquidity has been unusual given the level of volatility, we provide a scatter plot of price impact against volatility for the five-year note in the chart below. The chart shows that the 2022 observations (in blue) fall in line with the historical relationship. That is, the current level of liquidity is consistent with the current level of volatility, as implied by the historical relationship between these two variables. This is true for the ten-year note as well, whereas for the two-year note the evidence points to somewhat higher-than-expected price impact given the volatility in 2022 (as also occurred in fall 2008 and March 2020).

Liquidity and Volatility in Line with Historical Relationship

Liberty Street Economics chart plots price impact against price volatility by week for the five-year note from January 2, 2005, to October 28, 2022.

Source: Authors’ calculations, based on data from BrokerTec.

Notes: The chart plots price impact against price volatility by week for the on-the-run five-year note from January 2, 2005, to October 28, 2022. The weekly measures for both series are averages of the daily measures plotted in the preceding two charts. Fall 2008 points are for September 21, 2008 – January 3, 2009, March 2020 points are for March 1, 2020 – March 28, 2020, and 2022 points are for January 2, 2022 – October 29, 2022.

The preceding analysis is based on realized price volatility—that is, on how much prices are actually changing. We repeated the analysis with implied (or expected) price volatility, as measured by the ICE BofAML MOVE Index, and found similar results for 2022. That is, liquidity for the five- and ten-year notes is in line with the historical relationship between liquidity and expected volatility, whereas liquidity is somewhat worse for the two-year note.

Note also that while liquidity may not be especially high relative to volatility, one might then ask whether volatility itself is unusually high. Answering this question is beyond our scope here, although we will note that there are good reasons for volatility to be high, as discussed above.

Trading Volume Has Been High

Despite the high volatility and illiquidity, trading volume has held up this year. High trading volume amid high illiquidity is common in the Treasury market, and was also observed during the market disruptions around the near-failure of Long-Term Capital Management (see this paper), during the 2007-09 financial crisis (see this paper), during the October 15, 2014, flash rally (see this post), and during the COVID-19-related disruptions of March 2020 (see this post). Periods of high uncertainty are associated with high volatility and illiquidity but also high trading demand.

Nothing to Be Concerned About?

Not exactly. While Treasury market liquidity has been in line with volatility, there are still reasons to be cautious. The market’s capacity to smoothly handle large flows has been of ongoing concern since March 2020, as discussed in this paper, as Treasury debt outstanding continues to grow. Moreover, lower-than-usual liquidity implies that a liquidity shock will have larger-than-usual effects on prices and perhaps be more likely to precipitate a negative feedback loop between security sales, volatility, and illiquidity. Close monitoring of Treasury market liquidity—and continued efforts to improve the market’s resilience—remain important.

Large-Cap and Small-Cap Stock Return Probabilities

According to Ibbotson Associates’ Stocks, Bonds, Bill and Inflation, small Capitalization stocks outperform Large Capitalization stocks over the long term. (Although there is not a set definition for a Small Cap stock, generally speaking Small Cap stocks are those with a market capitalization below $2 billion today, while Large Cap stocks refer to the S&P 500.) Over the 1926-2018 period, Small Caps produced an average annual return of 11.0% compared to 9.99% for Large Capitalization stocks. (1) But, since 2010, Small Cap stocks have underperformed their Large Cap brethren. From the beginning of 2010 through the end of 2019 the S&P 500 rose 185.2% while the Russell 2000 (a proxy for small cap stocks) was up 145.8%. Over the last decade, the S&P 500 outperformed the Russell 2000 in 6 of the ten years. In 2019, the S&P 500 produced a 28.9% return compared to 23.7% for the Russell 2000. Has the time come for Small Cap stocks to outperform Large Cap stocks?

Positives

Relative Valuation Levels. Valuations for Small Caps are at their most attractive levels since June 2003 relative to Large Caps, according to data from Jefferies Financial Group. Historically, Small Caps have outperformed Large Caps by an average of 6% over the following year when the valuation gaps widens this much. (2)

New Index Highs Are a Historic Positive Sign. This past Thanksgiving, the Russell 2000 hit a new 52-week high after nearly 15 months without breaching it. FactSet and LPL Research data indicate that of the last 11 times the Russell 2000 index hit a new 52-week high, returns for the index were up an average 17% over the next 12 months 10 of those times. (3)

Higher Rate of Earnings Growth. Small Cap stocks produce a higher rate of earnings growth over time than Large Caps. Over the 1987-2017 period, Small Caps average annual recurring earnings growth was 8.15% versus 7.44% for Large Caps. (4)

Positives of Small Caps. As one would expect, most Small Caps are young companies with less international exposure than Large Caps. (5) Small Caps have less research coverage than Large Caps, providing a greater potential of market inefficiencies. (6) Ownership of Small Cap stock is typically concentrated in the hands of founders or management, a group that may be more motivated to increase shareholder value than the highly dispersed ownership of Large Cap shares.

Drawbacks

Higher Returns are due to Higher Risk. According to Alpha Wealth Strategies, Small Caps higher return over time comes with a standard deviation (a measure of risk) of 31.28 compared to just 19.76 for Large Cap stocks. (7) So, yes, an investor is receiving a higher return over time from Small Cap stocks, but the investor is assuming higher risk to achieve those returns.

Greater Volatility. As an example of the greater volatility of Small Caps, the Russell 2000 posted 65 intraday moves of 1% or more in the first 10 months of 2019, double that of the S&P 500. (2)

More Susceptible to Economic Shocks. Given their smaller size, lack of business diversification, and limited access to capital, Small Cap companies have historically been more susceptible to economic shocks. In times of economic uncertainty, many investors flock to Lage Cap stocks that are easier to trade and do not suffer from Small Caps’ business limitations. (8)

Small Caps Risks Relative to Large Caps. Among the greater risks of Small Caps is they tend to be more leveraged than Large Cap stocks with less operational efficiency and pricing power. (3) Small Caps also typically have less liquidity than Large Caps, meaning it may be tougher for investors to either build a position or quickly exit a holding. (6)

The Balanced Case:

While Small Cap stocks make up roughly just 10% of the overall U.S. equity market capitalization, they constitute the vast majority of publicly traded firms. And while Small Cap stocks are more volatile than Large Cap stock, over the last 93 years Small Caps generated positive returns in 68% of the years, compared to 73% of the time for Large Caps. Over the period, Small Caps produced a best one-year return of 142.87% and a 1-year worst return of a negative 58.01%, compared to 53.99% and a negative 43.34% for Large Caps. (7) Given Small Caps superior long-term investment returns compared to Large Caps, Small Caps would appear to be fertile shopping ground for long-term oriented investors.

Motorsport Games to Report Third Quarter 2022 Financial Results

MIAMI, Nov. 15, 2022 (GLOBE NEWSWIRE) — Motorsport Games Inc. (NASDAQ: MSGM) (“Motorsport Games”), a leading racing game developer, publisher and esports ecosystem provider of official motorsport racing series throughout the world will report financial results for the third quarter ended September 30, 2022 on Friday, November 18, 2022, after market close. Management will host a conference call and webcast on the same day at 5:00 p.m. ET to discuss the results.

Participants may access the live webcast on the Company’s investor relations website at https://ir.motorsportgames.com under “Events.” The call may also be accessed by dialing 1 (877) 407-0784 from the U.S., or by dialing 1 (201) 689-8560 internationally.

About Motorsport Games: Motorsport Games, a Motorsport Network company, is a leading racing game developer, publisher and esports ecosystem provider of official motorsport racing series throughout the world. Combining innovative and engaging video games with exciting esports competitions and content for racing fans and gamers, Motorsport Games strives to make the joy of racing accessible to everyone. The Company is the officially licensed video game developer and publisher for iconic motorsport racing series across PC, PlayStation, Xbox, Nintendo Switch and mobile, including NASCAR, INDYCAR, 24 Hours of Le Mans and the British Touring Car Championship (“BTCC”), as well as the industry leading rFactor 2 and KartKraft simulations. rFactor 2 also serves as the official sim racing platform of Formula E, while also powering F1 Arcade through a partnership with Kindred Concepts. Motorsport Games is an award-winning esports partner of choice for 24 Hours of Le Mans, Formula E, BTCC, the FIA World Rallycross Championship and the eNASCAR Heat Pro League, among others. Motorsport Games is building a virtual racing ecosystem where each product drives excitement, every esports event is an adventure and every story inspires.

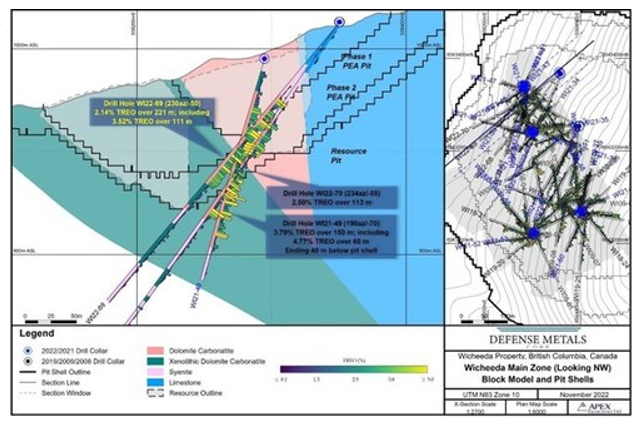

VANCOUVER, BC, Nov. 15, 2022 /PRNewswire/ – Defense Metals Corp. (“Defense Metals” or the “Company“; (TSX-V: DEFN) (OTCQB: DFMTF) (FSE: 35D) is pleased to announce additional partial Rare Earth Element (“REE“) assay results from one additional core hole, totalling 353 metres (m), collared within the northern area of Defense Metals’ 100% owned Wicheeda REE Deposit.

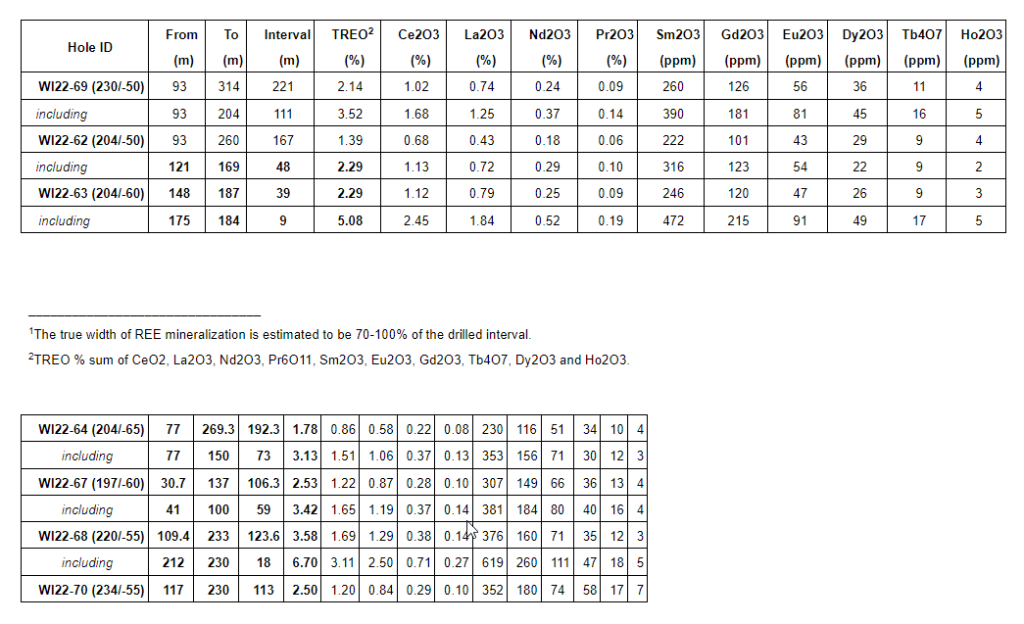

Infill drill hole WI22-69 (-50o dip / 230o azimuth) was drilled southwest within the northern area of the deposit intersected a broad zone of mineralized dolomite carbonatite averaging 2.14% total rare earth oxide (“TREO”) over 221 metres (m)1; including a higher-grade interval averaging 3.52% TREO over 111 m (Figure 1).

With over 5,500 m of drilling in 18 holes now complete as part of the 2022 Wicheeda resource delineation and pit geotechnical program, the Company has released assays for a total of 2,493 m in 7 holes. Assays for the remaining 11 holes totalling 3,017 m are expected in the coming weeks and months.

Luisa Moreno, President, and Director of Defense Metals stated: “With these additional assay results our 2022 drilling continues to yield significant intervals of the high-grade REE dolomite carbonatite (DC) lithology. Recent flotation variability testwork has shown this type of mineralization consistently delivers high grade mineral concentrates greater than 40% TREO, at recoveries in excess of 80% (see Defense Metals news release dated October 17, 2022). All the drill holes released to date have included significant REE mineralized DC intervals. As such Defense Metals is confident the 2022 drilling results will contribute positively to the planned Preliminary Feasibility Study (PFS).”

The 100% owned 4,244 hectare Wicheeda REE Property, located approximately 80 km northeast of the city of Prince George, British Columbia, is readily accessible by all-weather gravel roads and is near infrastructure, including power transmission lines, the CN railway, and major highways.

The Wicheeda REE Project yielded a robust 2021 preliminary economic assessment technical report (PEA) that demonstrated an after-tax net present value (NPV@8%) of $517 million, and 18% IRR3. A unique advantage of the Wicheeda REE Project is the production of a saleable high-grade flotation-concentrate. The PEA contemplates a 1.8 Mtpa (million tonnes per year) mill throughput open pit mining operation with 1.75:1 (waste:mill feed) strip ratio over a 19 year mine (project) life producing and average of 25,423 tonnes REO annually. A Phase 1 initial pit strip ratio of 0.63:1 (waste:mill feed) would yield rapid access to higher grade surface mineralization in year 1 and payback of $440 million initial capital within 5 years.

Methodology and QA/QC

The analytical work reported on herein was performed by ALS Canada Ltd. (ALS) at Langley (sample preparation) and Vancouver (ICP-MS fusion), B.C. ALS is an ISO-IEC 17025:2017 and ISO 9001:2015 accredited geoanalytical laboratory and is independent of the Defense Metals and the QP. Drill core samples were subject to crushing at a minimum of 70% passing 2 mm, followed by pulverizing of a 250-gram split to 85% passing 75 microns. A 0.1-gram sample pulp was then subject to multi-element ICP-MS analysis via lithium-borate fusion to determine individual REE content (ME-MS81h). Defense Metals follows industry standard procedures for the work carried out on the Wicheeda Project, with a quality assurance/quality control (QA/QC) program. Blank, duplicate, and standard samples were inserted into the sample sequence sent to the laboratory for analysis. Defense Metals detected no significant QA/QC issues during review of the data.

Qualified Person

The scientific and technical information contained in this news release as it relates to the Wicheeda REE Project has been reviewed and approved by Kristopher J. Raffle, P.Geo. (BC) Principal and Consultant of APEX Geoscience Ltd. of Edmonton, AB, a director of Defense Metals and a “Qualified Person” as defined in NI 43-101. Mr. Raffle verified the data disclosed which includes a review of the sampling, analytical and test data underlying the information and opinions contained therein.

About Defense Metals Corp.

Defense Metals Corp. is a mineral exploration and development company focused on the acquisition, exploration and development of mineral deposits containing metals and elements commonly used in the electric power markets, defense industry, national security sector and in the production of green energy technologies, such as, rare earths magnets used in wind turbines and in permanent magnet motors for electric vehicles. Defense Metals owns 100% of the Wicheeda Rare Earth Element Deposit located near Prince George, British Columbia, Canada. Defense Metals Corp. trades in Canada under the symbol “DEFN” on the TSX Venture Exchange, in the United States, under “DFMTF” on the OTCQB and in Germany on the Frankfurt Exchange under “35D”.

____________________________

3 Independent Preliminary Economic Assessment for the Wicheeda Rare Earth Element Project, British Columbia, Canada, dated January 6, 2022, with an effective date of November 7, 2021, and prepared by SRK Consulting (Canada) Inc. is filed under Defense Metals Corp.’s Issuer Profile on SEDAR (www.sedar.com).

Neither the TSX Venture Exchange nor its Regulation Services Provider (as that term is defined in the policies of the TSX Venture Exchange) accepts responsibility for the adequacy or accuracy of this news release.

Cautionary Statement Regarding “Forward-Looking” Information

This news release contains “forward–looking information or statements” within the meaning of applicable securities laws, which may include, without limitation, statements relating to advancing the Wicheeda REE Project, drill results including anticipated timeline of such results/assays, the Company’s plan to commence the PFS, the Company’s plans for its Wicheeda REE Project, expanded resource and scale of expanded resource, expected results and outcomes, the technical, financial and business prospects of the Company, its project and other matters. All statements in this news release, other than statements of historical facts, that address events or developments that the Company expects to occur, are forward-looking statements. Although the Company believes the expectations expressed in such forward-looking statements are based on reasonable assumptions, such statements are not guarantees of future performance and actual results may differ materially from those in the forward-looking statements. Such statements and information are based on numerous assumptions regarding present and future business strategies and the environment in which the Company will operate in the future, including the price of rare earth elements, the anticipated costs and expenditures, the ability to achieve its goals, that general business and economic conditions will not change in a material adverse manner, that financing will be available if and when needed and on reasonable terms. Such forward-looking information reflects the Company’s views with respect to future events and is subject to risks, uncertainties and assumptions, including the risks and uncertainties relating to the interpretation of exploration results, risks related to the inherent uncertainty of exploration and cost estimates, the potential for unexpected costs and expenses and those other risks filed under the Company’s profile on SEDAR at www.sedar.com. While such estimates and assumptions are considered reasonable by the management of the Company, they are inherently subject to significant business, economic, competitive and regulatory uncertainties and risks. Factors that could cause actual results to differ materially from those in forward looking statements include, but are not limited to, continued availability of capital and financing and general economic, market or business conditions, adverse weather and climate conditions, failure to maintain or obtain all necessary government permits, approvals and authorizations, failure to maintain community acceptance (including First Nations), risks relating to unanticipated operational difficulties (including failure of equipment or processes to operate in accordance with specifications or expectations, cost escalation, unavailability of personnel, materials and equipment, government action or delays in the receipt of government approvals, industrial disturbances or other job action, and unanticipated events related to health, safety and environmental matters), risks relating to inaccurate geological and engineering assumptions, decrease in the price of rare earth elements, the impact of Covid-19 or other viruses and diseases on the Company’s ability to operate, an inability to predict and counteract the effects of COVID-19 on the business of the Company, including but not limited to, the effects of COVID-19 on the price of commodities, capital market conditions, restriction on labour and international travel and supply chains, loss of key employees, consultants, or directors, increase in costs, delayed drilling results, litigation, and failure of counterparties to perform their contractual obligations. The Company does not undertake to update forward–looking statements or forward–looking information, except as required by law.

Conference Call Tuesday November 15, 2022 at 11:00 AM (EST)

(All $ figures reported in USD)

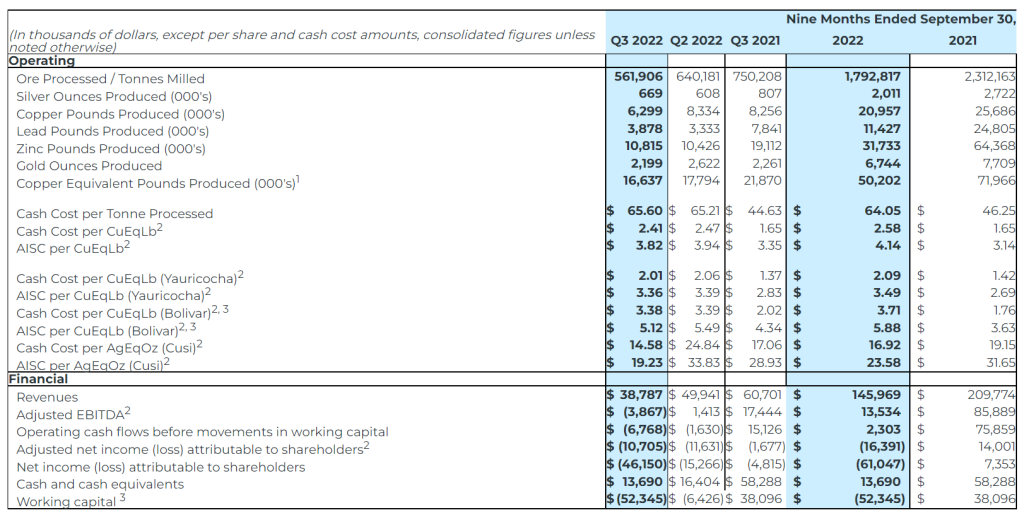

Revenue from metals payable of $38.8 million in Q3 2022, a 36% decrease from $60.7 million in Q3 2021 and a 22% decrease from the previous quarter, due to lower throughput at Yauricocha and slower ramp up at Bolivar as a result of a flooding event and operational restrictions due to limited ventilation in the Bolivar NorthWest zone.

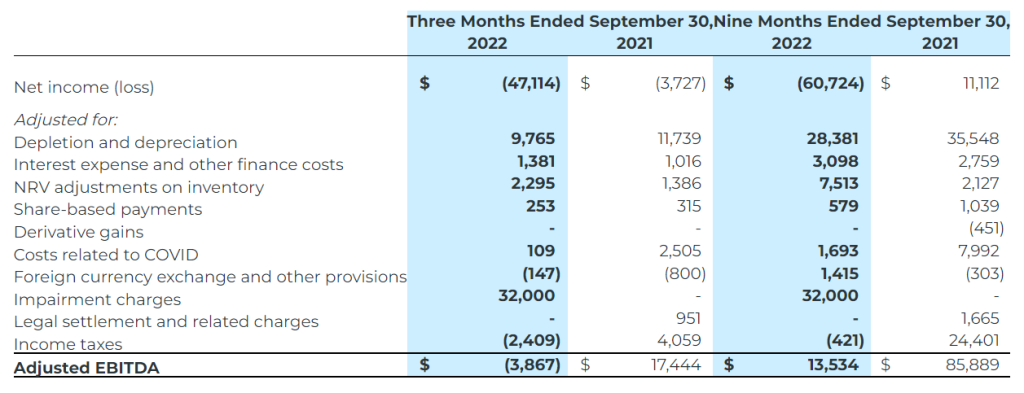

Adjusted EBITDA of $(3.9) million in Q3 2022, compared to $17.4 million in Q3 2021 and $1.4 million in Q2 2022.

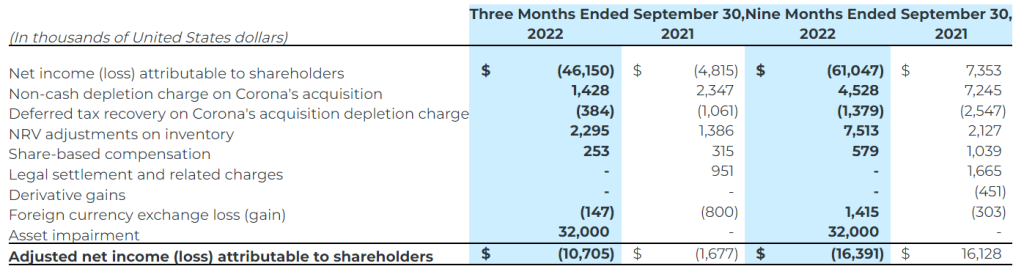

Net loss attributable to shareholders for Q3 2022 of $46.2 million, or $(0.28) per share (basic and diluted), compared to a net loss of $4.8 million, or ($0.03) per share in Q3 2021, and a net loss of $15.3 million or $(0.09) per share in Q2 2022.

Net loss for Q3 2022 and 9M 2022 includes an impairment charge of $25.0 million ($nil for Q3 2021 and 9M 2021) for the Bolivar mine and $7.0 million ($nil for Q3 2021 and 9M 2021) for the Cusi mine.

Adjusted net loss attributable to shareholders(1) of $10.7 million, or $(0.07) per share for Q3 2022, compared to adjusted net loss of $1.7 million or $(0.01) per share for Q3 2021 and an adjusted net loss of $11.6 million, or $0.07 per share for Q2 2022.

$13.7 million of cash and cash equivalents and working capital of $(52.3) million1 as at September 30, 2022.

Net Debt of $73.6 million as at September 30, 2022.

Suspension of production and financial guidance remains in effect.

1 The negative working capital is largely due to the reclassification of the long-term portion of the credit facility as current, resulting from the breach of certain debt covenants as at September 30, 2022. The Company is seeking accommodation from the lending banks in the form of waivers for this non-compliance.

A shareholder conference call will be held Tuesday, November 15, 2022, at 11:00 AM (EST). Click here to register.

TORONTO–(BUSINESS WIRE)– Sierra Metals Inc. (TSX: SMT) (BVL or Bolsa de Valores de Lima: SMT) (NYSE AMERICAN: SMTS) (“Sierra Metals” or “the Company”) today reported revenue of $38.8 million, a 36% decline from Q3 2021 and a 22% decline from Q2 2022, and adjusted EBITDA of $(3.9) million, a 122% decrease from Q3 2021 and a 379% decrease from Q2 2022 on throughput of 561,906 tonnes and metal production of 16.6 million copper equivalent pounds for the three-month period ended September 30, 2022.

Luis Marchese, CEO of Sierra Metals, commented, “the unexpected events during our latest quarter have made for another challenging period at Sierra Metals.

We have all been deeply impacted by the tragic mudslide incident at Yauricocha. As our primary objective remains the safety and well-being of all employees and contractors, a rigorous safety assurance process continues at the mine. Although production is ramping up, full production can only be reached once this process is complete.

In the coming months, we will continue to incorporate ore from the high-grade Fortuna zone and work towards recovery of tonnage at the Yauricocha Mine. In addition, exploration efforts will continue, both inside the mine for near term reach and in brownfield locations in close proximity to operations, in order to generate new exploration targets.”

He continued, “at Bolivar, unexpected flooding during most of the quarter in addition to the operational restrictions due to limited ventilation at the Bolivar NorthWest zone, negatively impacted throughput and grades.

On a consolidated basis, the Company’s revenues and EBITDA decreased 36% and 122%, respectively due to a 24% decrease in copper equivalent production when compared to the same quarter last year, coupled with a reduction in all metals prices, except zinc.”

He concluded, “Recent setbacks at both the Yauricocha and Bolivar Mines have prevented us from achieving full production and our turnaround goals within the initially proposed timeline, leading to suspended 2022 operating guidance. These unexpected challenges have culminated in the liquidity issues facing the Company. The Special Committee of our Board diligently continues its strategic review process. In the meantime, we remain disciplined in our approach to day-to-day operations.”

The following table displays selected financial and operational information for the three months and nine months ended September 30, 2022 compared to the corresponding periods for 2021 and the three months ended June 30, 2022:

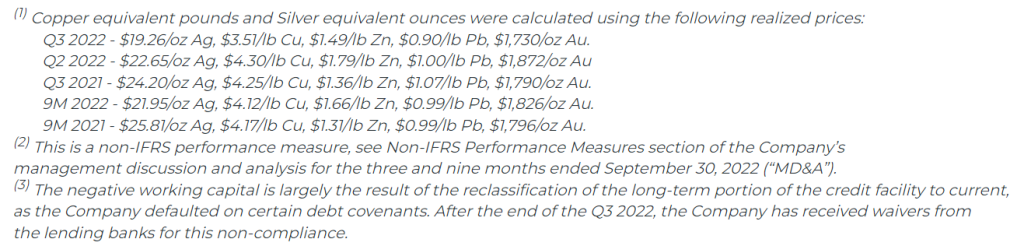

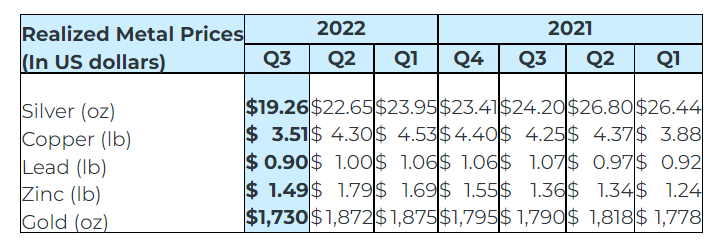

The following table shows the Company’s realized selling prices for the three months ended September 30, 2022, and each of the last six quarters:

Q3 2022 Consolidated Operating Highlights

Copper equivalent production of 16.6 million pounds; a 24% decrease from Q3 2021 and a 7% decrease from Q2 2022.

Consolidated Q3 2022 throughput of 561,906 tonnes was a 25% decrease over the Q3 2021 throughput of 750,208 tonnes. As compared to Q2 2022, consolidated throughput was 12% lower for Q3 2022.

Throughput from the Yauricocha Mine during Q3 2022 was 269,057 tonnes, a 17% decline when compared to Q3 2021 due to the suspension of mining activity and work stoppages during the quarter, which resulted in a 31% decrease in copper equivalent pounds produced. Declining grades due to restricted access to non-permitted areas of the mine also affected production. When compared to the previous quarter, throughput declined by 15%.

At the Bolivar Mine, throughput was 227,669 tonnes during Q3 2022. When compared to Q3 2021, throughput at Bolivar was 38% lower and while grades were higher for silver and gold, they were not enough to offset the lower throughput, resulting in a 16% decrease in copper equivalent pounds produced. Operational ramp up has been slower than expected due to unforeseen flooding in the Bolivar NorthWest zone during the quarter. When compared to Q2 2022, an 11% decrease in throughput, along with lower grades in copper and silver, resulted in a 10% decrease in copper equivalent pound production.

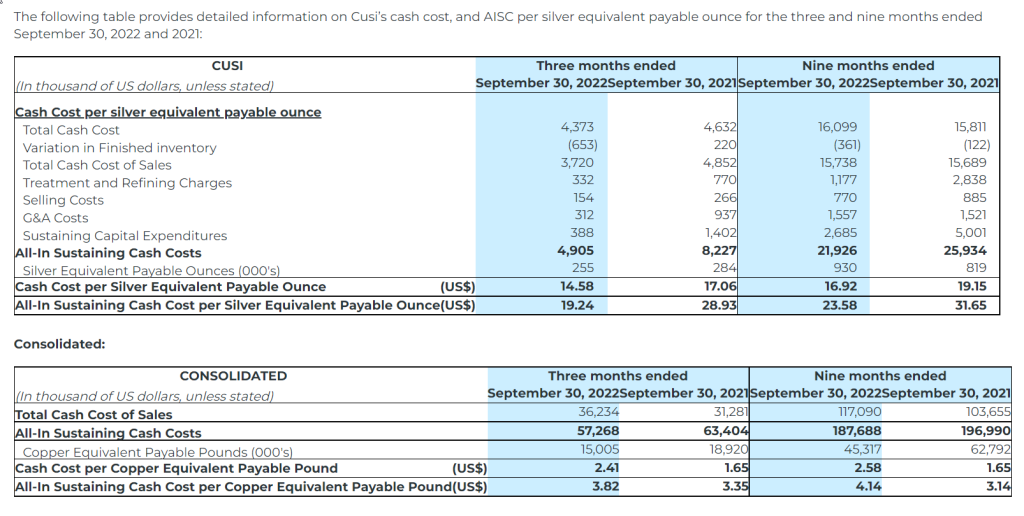

At Cusi, throughput was 65,180 tonnes during Q3 2022. When compared to Q3 2021, a 7% increase in throughput, combined with higher head grades for all metals except lead, resulted in a 22% increase in silver equivalent ounces production. Cusi suffered from an unexpected flooding event that restricted access to the lower areas of the mine during the second quarter. At the beginning of Q3, access to the lower levels of the mine was still limited. While throughput was 2% lower, it was offset by higher grades in all metals, resulting in a 32% increase in silver equivalent ounces produced.

Q3 2022 Consolidated Financial Highlights

Revenues Declined Due to Decrease in Metal Sales and a Drop in Metals Prices

Revenue from metals payable of $38.8 million in Q3 2022 or a decrease of 36% over the revenue of $60.7 million in Q3 2021 due to the decrease in metal sales and the drop in average realized prices for all metals, except zinc, as compared to Q3 2021.

Revenues for Q3 2022 were 22% lower than the revenue of $49.9 million in Q2 2022, as lower production from the Yauricocha and Bolivar Mines impacted metal sales quantities. The average realized prices for Q3 2022 decreased for copper (18%), zinc (17%), lead (10%), silver (15%) and gold (8%) as compared to the same during Q2 2022.

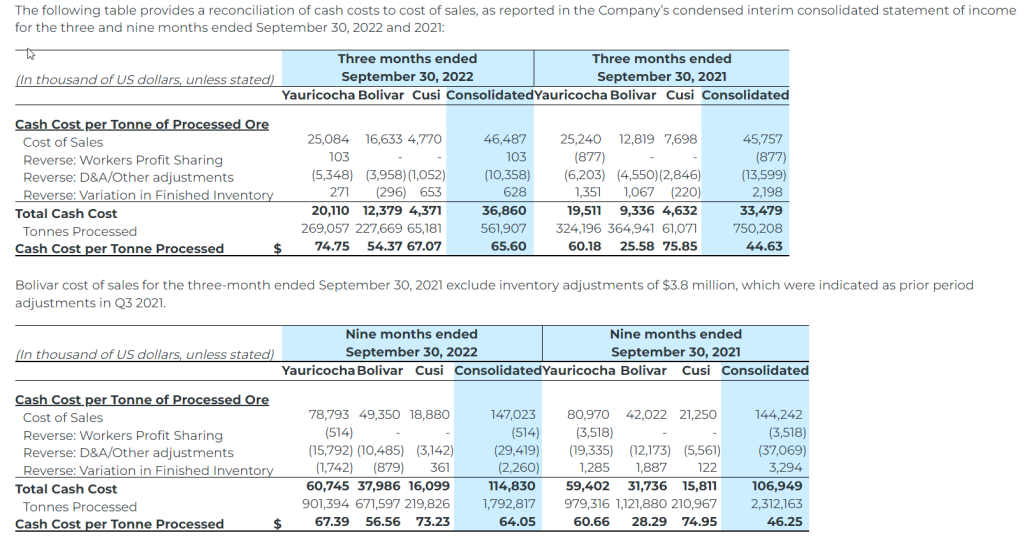

Cost of Operations Increased at Yauricocha and Bolivar Due to Lower Throughput

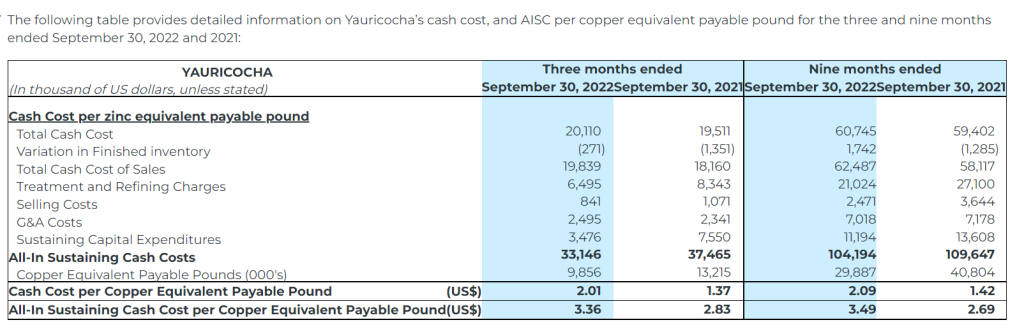

Yauricocha’s cash cost per copper equivalent payable pound was $2.01 (Q3 2021 – $1.37), and AISC (as defined herein) per copper equivalent payable pound of $3.36 (Q3 2021 – $2.83) for Q3 2022. The increase in cash costs and AISC was mainly a result of the 25% decrease in copper equivalent payable pounds as compared to Q3 2021. Despite 14% fewer copper equivalent payable pounds in Q3 2022 as compared to Q2 2022, cash cost and AISC per copper equivalent pound decreased from $2.06 and $3.39 respectively in Q2 2022, due to lower cost of sales and sustaining costs.

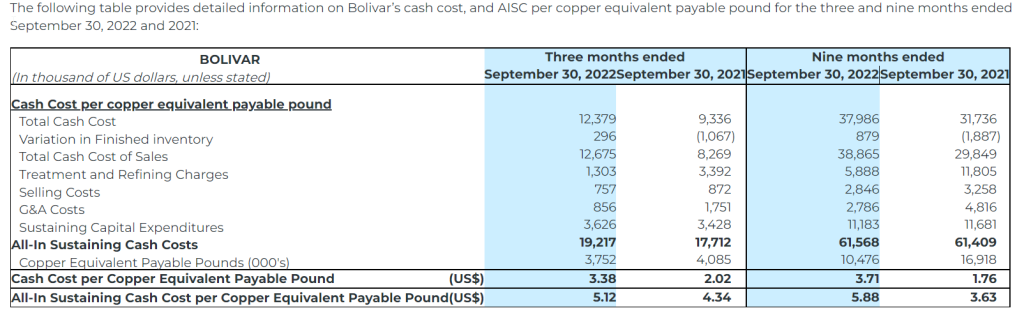

Bolivar’s cash cost per copper equivalent payable pound was $3.38 (Q3 2021 – $2.02), and AISC per copper equivalent payable pound was $5.12 (Q3 2021 – $4.34) for Q3 2022 due to higher operating costs per tonne and an 8% decrease in the copper equivalent payable pounds compared to Q3 2021. Bolivar’s Q3 2022 cash cost and AISC per copper equivalent pound decreased however from $3.39 and $5.49 respectively in Q2 2022.

Cusi’s Q3 2022 cash cost per silver equivalent payable ounce decreased to $14.58 from $17.06 in Q3 2021 as a result of higher grades. AISC per silver equivalent payable ounce decreased to $19.23 (Q3 2021 – $28.93). Unit costs decreased during Q3 2022, despite fewer silver equivalent payable ounces, as a result of lower operating costs per tonne and lower sustaining costs during Q3 2022 as compared to Q3 2021.

EBITDA, Net Income and Cash Flow Generation Impacted by Lower Revenues and Higher Operating Costs

Adjusted EBITDA(1) decreased 122% to $(3.9) million for Q3 2022 compared to $17.4 million in Q3 2021 and a 379% decrease compared to $1.4 million in the previous quarter. The decrease in EBITDA is related to drop in revenues attributable to lower production and higher operating costs during Q3 2022.

Net loss attributable to shareholders for Q3 2022 was $46.2 million or $(0.28) per share (basic and diluted), compared to net loss of $4.8 million or $(0.03) per share (basic and diluted) in Q3 2021 and net loss of $15.3 million or $(0.09) per share (basic and diluted) in Q2 2022.

Adjusted net loss attributable to shareholders(1) of $10.7 million, or $(0.07) per share for Q3 2022, compared to adjusted net loss of $1.7 million or $(0.01) per share for Q3 2021 and adjusted net loss of $11.6 million, or $0.0 per share for Q2 2022.

Operating cash flow before movements in working capital of $(6.8) million for Q3 2022 as compared to $15.1 million of cash generated from operating activities in Q3 2021 and $(1.6) million in Q2 2022. The decrease resulted from lower revenue and higher costs during the quarter.

Cash and cash equivalents of $13.7 million and working capital of $(52.3) million as at September 30, 2022 compared to $34.9 million and $17.3 million, respectively, at the end of 2021. The negative working capital is largely the result of the reclassification of the long-term portion of the credit facility to current, as the Company defaulted on certain debt covenants as of September 30, 2022. The Company is seeking accommodation from the lending banks in the form of waivers for this non-compliance. If the Company is unable to obtain such waivers for the current and any potential future breaches of its debt covenants, it could materially and adversely affect the Company’s future operations, cash flows, earnings, results of operations, financial condition and the economic viability of its projects.

Cash and cash equivalents decreased during the nine-month period ended September 30, 2022 due to $31.2 million used in investing activities offset by $6.1 million of cash generated from operating activities and $3.8 million of cash generated from financing activities.

Financing activities included $25.0 million received from Banco de Credito del Peru (“BCP”) and Banco Santander by the Company’s subsidiary, Sociedad Minera Corona, to finance the repayment of the installments of $18.8 million on the original credit facility received from BCP.

1 This is a non-IFRS performance measure. See the Non-IFRS Performance Measures section of the MD&A.

Project Development

Mine development at Bolivar during Q3 2022 totaled 2,080 meters, which included 1,265 meters of development to prepare stopes for mine production, and 815 meters to development of ramps; and

Mine development at Cusi during Q3 2022 totaled 631 meters.

Exploration Update

Peru:

Approximately 2,532 meters of diamond drilling was completed during Q3 2022 in the Fortuna North, Katty and Violeta zones with the aim to replace and increase the depleted mineral resources. Additionally, approximately 2,000 meters of greenfield exploration drilling was completed in the Tucumachay prospect.

Mexico:

Bolivar

At Bolivar during Q3 2022, 18,318 meters were drilled in the Bolivar West, Bolivar NorthWest, the Cieneguita zones and El Gallo Superior encountering skarn intersections with mineralization. Additionally, infill drilling of 4,479 meters was completed in the Bolivar West, El Gallo Inferior and Bolivar NorthWest zones;

Cusi

During Q3 2022, the Company completed 2,196 meters of infill drilling to support the development of the Santa Rosa de Lima vein and NE Trend.

Covid-19 Update And Outlook

The COVID-19 pandemic has impacted the Company’s operations over the past two years. While there are still concerns regarding the newer variants of the virus, there is reduced pressure on the operations due to relaxed measures as the Company has achieved almost 100% vaccination rate for its employees at all locations. The additional costs related to COVID dropped to $1.7 million during the nine-month period ended September 30, 2022 as compared to $8.0 million spent during the comparative nine-month period of 2021.

Impairment Charge

Lower market capitalization due to the drop in the Company’s share price, declining metal prices, lower production and consequent decrease in profitability were considered as indicators of impairment as on September 30, 2022. The Company performed an impairment analysis for each of its cash generating units (“CGU”) using Life of Mine (“LOM”), which incorporate current operational practices, long term metal prices based on recent analyst consensus and productivity assumptions, based on recent operating experience at the mines.

The Company updated the Bolivar LOM using updated information from the mine performance, required capex, metal prices and discount rate, and concluded that an impairment of $25.0 million was required for the Bolivar CGU.

The Cusi LOM was updated for the latest metal prices and discount rate. Following this analysis, management concluded that an impairment of $7.0 million was needed for the Cusi CGU as on September 30, 2022.

The updated Yauricocha LOM did not indicate any impairment as at September 30, 2022.

Suspended Guidance

In addition to the delays in the anticipated turnaround at the Bolivar mine due to the unexpected flooding in the Bolivar NW zone during the quarter, the Company also experienced production delays at the Yauricocha mine as a result of the mudslide incident and ensuing community blockade in September. Although mining restarted in parts of Yauricocha in October, the Company is following due assurance processes to ensure safe operations in the remaining sections of the mine. In view of these delays, the Company has suspended its production and financial guidance for 2022.

Strategic Review Process

In response to liquidity challenges from an accumulation of operational losses and negative cashflows, primarily from its Mexican operations, the Company announced, on October 18, 2022, the formation of a Special Committee and the initiation of a strategic review process.

The mandate of the Special Committee, comprised of its independent directors, includes exploring, reviewing and considering options to optimize the operations of the Company and possible financing, restructuring and strategic options in the best interests of the Company. Financial and legal advisors with particular expertise in turnaround and restructuring matters have been engaged to advise on this process.

The Company has engaged CIBC Capital Markets as a financial advisor in this process.

Delisting

As previously announced, the Company will voluntarily delist its common shares from the New York Stock Exchange American (“NYSE”) and the Bolsa de Valores de Lima (“BVL”). The final day of trading on the NYSE was today, November 14, 2022 with shares to be suspended from trading before market open on November 15, 2022.

The Company is continuing to pursue its BVL delisting and suspension from trading is anticipated later during the year. An update will be provided once a final trading date of the common shares on the BVL has been confirmed.

The Company’s common shares will continue to be listed and traded in Canadian dollars on the Toronto Stock Exchange.

Conference Call and Webcast

Sierra Metals’ senior management will host a conference call on Tuesday, November 15, 2022, at 11:00 AM (EDT) to discuss the Company’s financial and operating results for the three months ended September 30, 2022.

Via Webcast:

A live audio webcast of the meeting will be available on the Company’s website:

The webcast, along with presentation slides, will be archived for 180 days on www.sierrametals.com.

Via phone:

For those who prefer to listen by phone, dial-in instructions are below. To ensure your participation, please call approximately five minutes prior to the scheduled start time of the call.

Canada dial-in number (Toll Free): 1 833 950 0062 Canada dial-in number (Local): 1 226 828 7575 US dial-in number (Toll Free): 1 844 200 6205 US dial-in number (Local): 1 646 904 5544 All other locations: +1 929 526 1599

Access code: 991150

Press *1 to ask a question, *2 to withdraw your question, or *0 for operator assistance

Non-IFRS Performance Measures

The non-IFRS performance measures presented do not have any standardized meaning prescribed by IFRS and are therefore unlikely to be directly comparable to similar measures presented by other issuers.

Non-IFRS reconciliation of adjusted EBITDA

EBITDA is a non-IFRS measure that represents an indication of the Company’s continuing capacity to generate earnings from operations before taking into account management’s financing decisions and costs of consuming capital assets, which vary according to their vintage, technological currency, and management’s estimate of their useful life. EBITDA comprises revenue less operating expenses before interest expense (income), property, plant and equipment amortization and depletion, and income taxes. Adjusted EBITDA has been included in this document. Under IFRS, entities must reflect in compensation expense the cost of share-based payments. In the Company’s circumstances, share-based payments involve a significant accrual of amounts that will not be settled in cash but are settled by the issuance of shares in exchange for cash. As such, the Company has made an entity specific adjustment to EBITDA for these expenses. The Company has also made an entity-specific adjustment to the foreign currency exchange (gain)/loss. The Company considers cash flow before movements in working capital to be the IFRS performance measure that is most closely comparable to adjusted EBITDA.

The following table provides a reconciliation of adjusted EBITDA to the condensed interim consolidated financial statements for the three and nine months ended September 30, 2022 and 2021:

Non-IFRS reconciliation of adjusted net income

The Company has included the non-IFRS financial performance measure of adjusted net income, defined by management as the net income attributable to shareholders shown in the statement of earnings plus the non-cash depletion charge due to the acquisition of Corona and the corresponding deferred tax recovery and certain non-recurring or non-cash items such as share-based compensation and foreign currency exchange (gains) losses. The Company believes that, in addition to conventional measures prepared in accordance with IFRS, certain investors may want to use this information to evaluate the Company’s performance and ability to generate cash flows. Accordingly, it is intended to provide additional information and should not be considered in isolation or as a substitute for measures of performance in accordance with IFRS.

The following table provides a reconciliation of adjusted net income to the condensed interim consolidated financial statements for the three and nine months ended September 30, 2022 and 2021:

Cash cost per silver equivalent payable ounce and copper equivalent payable pound

The Company uses the non-IFRS measure of cash cost per silver equivalent ounce and copper equivalent payable pound to manage and evaluate operating performance. The Company believes that, in addition to conventional measures prepared in accordance with IFRS, certain investors use this information to evaluate the Company’s performance and ability to generate cash flows. Accordingly, it is intended to provide additional information and should not be considered in isolation or as a substitute for measures of performance prepared in accordance with IFRS.

All-in sustaining cost per silver equivalent payable ounce and copper equivalent payable pound

All‐In Sustaining Cost (“AISC”) is a non‐IFRS measure and was calculated based on guidance provided by the World Gold Council (“WGC”) in June 2013. WGC is not a regulatory industry organization and does not have the authority to develop accounting standards for disclosure requirements. Other mining companies may calculate AISC differently as a result of differences in underlying accounting principles and policies applied, as well as differences in definitions of sustaining versus development capital expenditures.

AISC is a more comprehensive measure than cash cost per ounce/pound for the Company’s consolidated operating performance by providing greater visibility, comparability and representation of the total costs associated with producing silver and copper from its current operations.

The Company defines sustaining capital expenditures as, “costs incurred to sustain and maintain existing assets at current productive capacity and constant planned levels of productive output without resulting in an increase in the life of assets, future earnings, or improvements in recovery or grade. Sustaining capital includes costs required to improve/enhance assets to minimum standards for reliability, environmental or safety requirements. Sustaining capital expenditures excludes all expenditures at the Company’s new projects and certain expenditures at current operations which are deemed expansionary in nature.”

Consolidated AISC includes total production cash costs incurred at the Company’s mining operations, including treatment and refining charges and selling costs, which forms the basis of the Company’s total cash costs. Additionally, the Company includes sustaining capital expenditures and corporate general and administrative expenses. AISC by mine does not include certain corporate and non‐cash items such as general and administrative expense and share-based payments. The Company believes that this measure represents the total sustainable costs of producing silver and copper from current operations and provides the Company and other stakeholders of the Company with additional information of the Company’s operational performance and ability to generate cash flows. As the measure seeks to reflect the full cost of silver and copper production from current operations, new project capital and expansionary capital at current operations are not included. Certain other cash expenditures, including tax payments, dividends and financing costs are also not included.

Additional non-IFRS measures

The Company uses other financial measures, the presentation of which is not meant to be a substitute for other subtotals or totals presented in accordance with IFRS, but rather should be evaluated in conjunction with such IFRS measures. This includes:

Operating cash flows before movements in working capital – excludes the movement from period-to-period in working capital items including trade and other receivables, prepaid expenses, deposits, inventories, trade and other payables and the effects of foreign exchange rates on these items.

This term does not have a standardized meaning prescribed by IFRS, and therefore the Company’s definition is unlikely to be comparable to similar measures presented by other companies. The Company’s management believes that their presentation provides useful information to investors because cash flows generated from operations before changes in working capital excludes the movement in working capital items. This, in management’s view, provides useful information of the Company’s cash flows from operations and is considered to be meaningful in evaluating the Company’s past financial performance or its future prospects. The most comparable IFRS measure is cash flows from operating activities.

Qualified Persons

Américo Zuzunaga, FAusIMM (Mining Engineer) Vice President, Technical is a Qualified Person under National Instrument 43-101 – Standards of Disclosure for Mineral Projects.

About Sierra Metals

Sierra Metals Inc. is a diversified Canadian mining company with Green Metal exposure including increasing copper production and base metal production with precious metals byproduct credits, focused on the production and development of its Yauricocha Mine in Peru, and Bolivar and Cusi Mines in Mexico. The Company is focused on increasing production volume and growing mineral resources. Sierra Metals has recently had several new key discoveries and still has many more exciting brownfield exploration opportunities at all three Mines in Peru and Mexico that are within close proximity to the existing mines. Additionally, the Company also has large land packages at all three mines with several prospective regional targets providing longer-term exploration upside and mineral resource growth potential.

The Company’s Common Shares trade on the Bolsa de Valores de Lima and on the Toronto Stock Exchange under the symbol “SMT” and on the NYSE American Exchange under the symbol “SMTS”.

For further information regarding Sierra Metals, please visit www.sierrametals.com.

This press release contains forward-looking information within the meaning of Canadian and United States securities legislation, including with respect to timing of the conference call, exploration and production plans and the delisting of the Company’s common shares. Forward-looking information relates to future events or the anticipated performance of Sierra and reflect management’s expectations or beliefs regarding such future events and anticipated performance based on an assumed set of economic conditions and courses of action. In certain cases, statements that contain forward-looking information can be identified by the use of words such as “plans”, “expects”, “is expected”, “budget”, “scheduled”, “estimates”, “forecasts”, “intends”, “anticipates”, “believes” or variations of such words and phrases or statements that certain actions, events or results “may”, “could”, “would”, “might”, or “will be taken”, “occur” or “be achieved” or the negative of these words or comparable terminology. By its very nature forward-looking information involves known and unknown risks, uncertainties and other factors that may cause actual performance of Sierra to be materially different from any anticipated performance expressed or implied by such forward-looking information.

Forward-looking information is subject to a variety of risks and uncertainties, which could cause actual events or results to differ from those reflected in the forward-looking information, including, without limitation, the risks described under the heading “Risk Factors” in the Company’s annual information form dated March 16, 2022 for its fiscal year ended December 31, 2021 and other risks identified in the Company’s filings with Canadian securities regulators and the United States Securities and Exchange Commission, which filings are available at www.sedar.com and www.sec.gov, respectively.

The risk factors referred to above are not an exhaustive list of the factors that may affect any of the Company’s forward-looking information. Forward-looking information includes statements about the future and is inherently uncertain, and the Company’s actual achievements or other future events or conditions may differ materially from those reflected in the forward-looking information due to a variety of risks, uncertainties and other factors. The Company’s statements containing forward-looking information are based on the beliefs, expectations, and opinions of management on the date the statements are made, and the Company does not assume any obligation to update such forward-looking information if circumstances or management’s beliefs, expectations or opinions should change, other than as required by applicable law. For the reasons set forth above, one should not place undue reliance on forward-looking information.

Global Restaurant Franchising Company HiresExperienced C-Suite Growth Leader to Drive Expansion Efforts

LOS ANGELES, Nov. 14, 2022 (GLOBE NEWSWIRE) — FAT (Fresh. Authentic. Tasty.) Brands Inc., announces the hiring of its first Chief Growth Officer, Jeremy Theisen. Theisen joins FAT Brands with over 20 years of experience in significantly increasing the revenue stream for high-growth start-ups in the restaurant sector and will be focused on spearheading the growth of the development pipeline across the FAT Brands portfolio. This includes bringing new franchisees into the system and driving multi-unit expansion with existing franchisees.