A significant valuation disconnect has been building in U.S. equity markets for nearly three years — and the Q1 2026 earnings season made it harder to ignore.

Small and microcap companies are delivering some of the strongest earnings growth numbers in years, yet their valuation multiples remain near historic lows relative to large caps. For investors willing to look beyond the mega-cap trade, the message is clear:

Small caps may be entering one of the more attractive valuation reset windows in a generation.

Where Valuations Stand Right Now

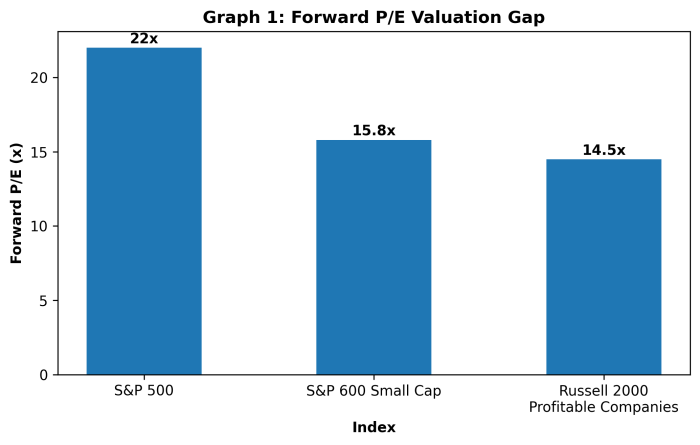

The S&P 500 currently trades at approximately 22x forward earnings, above both its five-year and ten-year averages. By comparison, profitable Russell 2000 companies trade closer to 14–15x, while the S&P 600 small cap index trades around 15.8x.

That places the large-cap valuation premium at roughly 30% to 42% over small caps — one of the widest spreads seen in the past two decades.

The valuation disconnect is even more pronounced when looking at EV/EBIT, a metric many institutional investors prefer for cross-cap comparisons. According to Royce Investment Partners, the Russell 2000’s EV/EBIT relative to large caps is near its lowest level in more than 25 years.

What the Earnings Data Shows

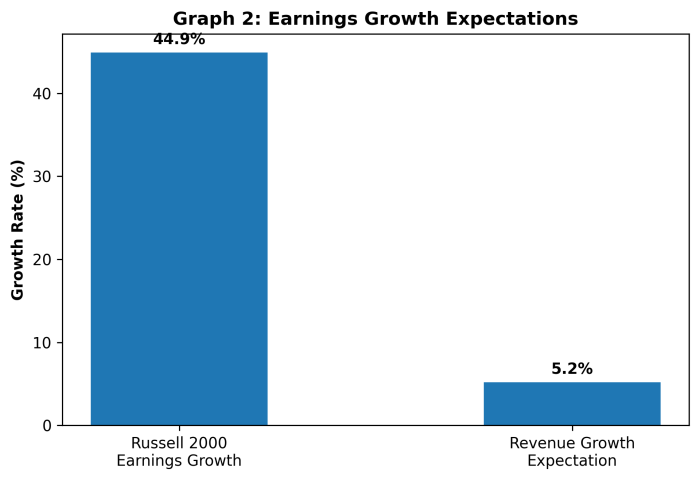

The valuation gap would be easier to justify if small caps were underperforming fundamentally. But that is not what the data shows.

Heading into Q1 2026, the Russell 2000 carried consensus earnings growth expectations of approximately 44.9% year over year, with revenue growth projected at 5.2%. That combination suggests improving operating leverage as smaller companies recover from a prolonged period of pressure caused by higher rates, inflation, and tighter capital conditions.

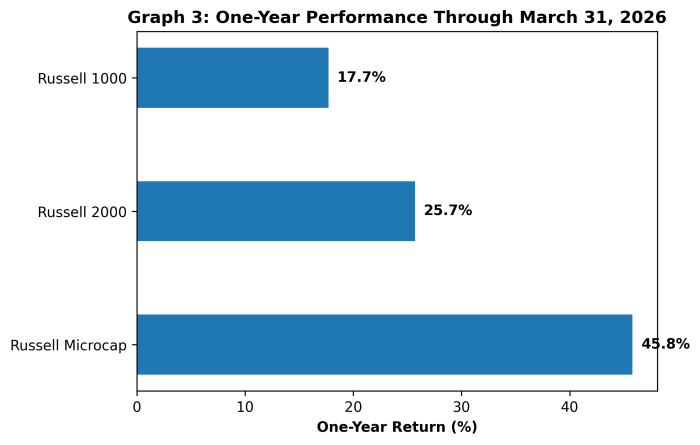

Performance has already started to reflect the shift.

The Historical Context

For much of the past 25 years, small caps traded at a valuation premium to large caps because of their higher growth potential. That relationship inverted during the higher-rate cycle, as smaller companies faced greater pressure from financing costs, inflation, and reduced investor risk appetite.

That inversion pushed the valuation spread to levels not seen since the dot-com era.

Historically, when valuation gaps between small and large caps have reached this kind of extreme, small caps have often gone on to deliver above-average returns over the following three to five years.

One additional data point reinforces the opportunity: the Russell 2000’s weight within the Russell 3000 currently sits at approximately 4.6%, well below its historical average of 7.6%. In other words, small caps remain structurally underrepresented in the broader market.

Time to Revisit Small Caps

- Strong earnings growth.

- Historically discounted valuations.

- Improving fundamentals.

- Low investor allocation.

That combination may create one of the more compelling small and microcap opportunities investors have seen in years.

Against this backdrop, Noble Capital Markets will host its upcoming Virtual Small Cap Conference on June 3–4, giving investors an opportunity to hear directly from emerging growth companies across multiple sectors.

For investors looking to identify opportunities before broader market recognition returns to the asset class, this may be an important time to listen, compare, and look deeper into the small-cap universe.

The valuation gap is real. The earnings recovery is underway. The time to revisit small caps may be now.