InPlay Oil is a junior oil and gas exploration and production company with operations in Alberta focused on light oil production. The company operates long-lived, low-decline properties with drilling development and enhanced oil recovery potential as well as undeveloped lands with exploration possibilities. The common shares of InPlay trade on the Toronto Stock Exchange under the symbol IPO and the OTCQX Exchange under the symbol IPOOF.

Mark Reichman, Managing Director, Equity Research Analyst, Natural Resources, Noble Capital Markets, Inc.

Hans Baldau, Associate Analyst, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

Third-quarter 2025 results. InPlay reported third-quarter results, with production averaging 18,970 barrels of oil equivalent per day (boe/d), up 7% from Q2 and 131% higher than Q3 2024. This was above our forecast of 18,695 boe/d, due to continued outperformance of wells drilled in the first quarter of 2025 and low decline base production. Revenue totaled C$79.3 million, below our forecast of C$86.8 million due to lower natural gas pricing. Adjusted funds flow (AFF) came in at C$26.8 million, or C$0.96 per share, modestly below our C$28.0 million, or $1.00 per share estimate, mainly due to the variance in revenue.

Market outlook. We think 2026 will offer a more favorable environment for InPlay. It will mark the first full year of results post-Pembina acquisition, unlocking the benefits of greater scale, infrastructure control, and an expanded drilling inventory. While near-term pricing remains soft, we expect stronger demand, slower supply growth, and potential for tighter oil and gas markets to support improved realizations and higher netbacks through 2026. With enhanced gas processing capacity and capital flexibility, InPlay remains well-positioned to capitalize on an improving macro backdrop.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

Michael Kupinski, Director of Research, Equity Research Analyst, Digital, Media & Technology , Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

Overachieves fiscal first quarter. Total revenues increased a solid 10.9% to $253.9 million, better than our $244.0 million estimate, bolstered by a 59% increase in movie sales. In addition, adj. EBITDA of $12.2 million, up roughly 260% y-o-y, was better than our $9.5 million estimate, reflecting a 330 basis point improvement in margins. Figure #1 Q3 Results highlights our estimates and the recent results.

Strong movie sales likely to continue. Movie sales revenues increased 59% to $84.0 million, well above our $74.9 million estimate, a reflection of a recent licensing agreement with Paramount Pictures, and, to a smaller extent, strong Steelbook sales. The Paramount Pictures licensing revenue lift is likely to bolster total company revenues for the next few quarters.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

Day One Biopharmaceuticals announced a definitive agreement to acquire Mersana Therapeutics (Nasdaq: MRSN), marking a strategic move to strengthen its position in oncology drug development. The deal, valued at up to $285 million, combines Day One’s commercial expertise with Mersana’s innovative antibody-drug conjugate (ADC) technology, expanding the company’s pipeline in targeted cancer therapies.

Under the terms of the agreement, Day One will acquire Mersana through a tender offer followed by a merger, offering $25 per share in cash upfront and up to $30.25 per share in additional contingent value rights (CVRs). The CVRs are tied to the achievement of specific clinical, regulatory, and commercial milestones, particularly related to Emi-Le (emiltatug ledadotin), Mersana’s B7-H4-directed ADC candidate. The total equity value at closing is estimated at $129 million, with the full deal potentially reaching $285 million if all milestones are met.

The acquisition highlights Day One’s intent to broaden its oncology focus beyond its current lead programs. Known for its commitment to developing therapies for pediatric and underserved cancer populations, Day One plans to leverage Mersana’s ADC platforms—Dolasynthen and Immunosynthen—to accelerate the development of next-generation cancer treatments.

For Mersana, the deal represents both validation and a strategic exit amid a challenging biotech funding environment. The company has been recognized for its innovative ADC technology, which delivers cytotoxic and immune-modulating agents directly to cancer cells, minimizing harm to healthy tissue. Its lead candidate, Emi-Le, is currently being explored for the treatment of triple-negative breast cancer and adenoid cystic carcinoma, both areas with high unmet clinical needs.

Upon completion of the acquisition, Mersana will become a wholly owned subsidiary of Day One, and its common stock will be delisted from public exchanges. The transaction is expected to close by the end of January 2026, subject to customary regulatory approvals and the tender of a majority of Mersana’s outstanding shares.

The merger agreement was unanimously approved by Mersana’s board of directors, which has recommended that shareholders tender their shares once the offer is formally launched. Key shareholders, including affiliates of Bain Capital Life Sciences, representing approximately 8.5% of outstanding shares, have already agreed to support the transaction.

Financially, TD Cowen is serving as Mersana’s advisor, while WilmerHale is acting as legal counsel. Fenwick & West LLP is representing Day One in the deal.

This acquisition aligns with broader industry trends in oncology, where partnerships and mergers are accelerating innovation in targeted therapies. ADCs have become one of the most promising drug classes in oncology, combining precision targeting with potent efficacy. The addition of Mersana’s technology could give Day One a competitive edge in developing more effective, tumor-specific treatments.

With closing anticipated early next year, the merger positions Day One Biopharmaceuticals as a growing force in precision oncology, combining innovative science with a mission-driven focus on expanding treatment options for patients of all ages battling cancer.

Anthropic, one of the fastest-growing artificial intelligence firms in the world, has announced an ambitious $50 billion plan to expand its U.S. infrastructure footprint through a series of advanced data centers starting in Texas and New York. The project, developed in partnership with AI cloud platform Fluidstack, positions the company as a major force in the domestic AI buildout race.

The initiative will fund the creation of custom-designed facilities built specifically to handle Anthropic’s rapidly scaling AI models and enterprise workloads. The company said the first sites will go live in 2026 and are expected to generate 800 permanent jobs and more than 2,000 construction roles across both states.

By building its own network of high-performance data centers, Anthropic aims to ensure greater control over compute availability, energy efficiency, and long-term scalability — key components in the race to dominate AI infrastructure. The decision also aligns with growing policy pressure from Washington to keep cutting-edge AI capacity within U.S. borders, protecting national interests and technological sovereignty.

This investment underscores Anthropic’s aggressive growth trajectory and signals that the company is willing to match, if not challenge, industry leader OpenAI’s spending spree. OpenAI has already committed more than $1.4 trillion in long-term infrastructure investments through partnerships with Nvidia, Oracle, Broadcom, Microsoft, and Google.

Anthropic’s partnership with Fluidstack — known for supplying GPU clusters to major AI players like Meta, Midjourney, and Mistral — reflects a strategic effort to move fast. Fluidstack’s expertise in scaling GPU infrastructure at record speed and efficiency gives Anthropic a distinct operational advantage as competition for compute power intensifies.

The company’s enterprise business has surged dramatically over the past year, serving more than 300,000 organizations. The number of enterprise accounts generating over $100,000 annually has nearly increased sevenfold, with projections showing Anthropic could reach profitability by 2028. By comparison, OpenAI is still expected to report multi-billion-dollar operating losses through that same period.

Beyond Texas and New York, Anthropic’s infrastructure expansion already includes a massive $11 billion data center campus in Indiana, developed with Amazon. The facility is operational, providing Anthropic with one of the largest AI-focused compute environments in the U.S. The company has also expanded its long-term compute partnership with Google, with additional commitments valued in the tens of billions.

Industry observers say Anthropic’s move could reshape the competitive landscape of AI infrastructure, helping to diversify the market beyond the dominance of hyperscale cloud providers. However, the scale of AI-related construction and energy use is prompting questions about sustainability and grid capacity — particularly as multiple firms rush to deploy gigawatt-scale facilities across the country.

With a $50 billion budget and an expanding nationwide footprint, Anthropic is betting big on the idea that the next wave of AI breakthroughs will depend not just on smarter algorithms, but on physical infrastructure capable of powering them at scale.

SAN DIEGO, Nov. 12, 2025 (GLOBE NEWSWIRE) — Kratos Defense & Security Solutions, Inc. (Nasdaq: KTOS), a technology company in the defense, national security, and global markets, today announced that its Indiana Payload Integration Facility (IPIF) for Hypersonic Systems located in Crane, Indiana, is on schedule to be fully mission capable by the end of 2026. The state-of-the-art facility is now under roof, and work is progressing rapidly to finalize equipment-bearing foundations and erect interior structures.

Kratos’ IPIF, which is estimated to cost more than $50 million once complete, is designed and purpose-built for rapid, affordable preparation of experimental payloads to significantly boost the tempo of flight testing for next-generation hypersonic systems and technologies and to accelerate the development of new and advanced weapons systems.

The state-of-the-art, 68,000-square-foot complex will feature advanced manufacturing and test capabilities along with enhanced workflows to boost the tempo of critical hypersonic vehicle and payload activities for programs such as the Multi-Service Advanced Capabilities Hypersonic Testbed (MACH-TB) program. The project demonstrates Kratos’ steadfast commitment to advancing hypersonic system development and expanding crucial industrial base infrastructure needed to accelerate Mach 5+ flight testing. The facility is expected to create over 100 high-tech jobs when complete, with an estimated average annual wage of $80,000+.

Josh Peterson, Senior Vice President and Product Manager for Kratos Launch Vehicles, said: “We’re pleased with the tremendous progress made so far, and extremely excited to get to work processing experiments and payloads for MACH-TB. This building’s design, which was heavily influenced by engineers and technicians with countless years of test vehicle experience, promises to accelerate throughput and provide a needed boost to the pace of hypersonic testing.”

Mike Johns, Senior Vice President of Kratos SRE, said: “This is an important addition to the hypersonics test infrastructure located near NSWC Crane and will be a national asset for the hypersonics test and experimentation community across the country. The entire community in Southern Indiana has been very helpful and supportive getting this project off the ground, and it is one of many new projects Kratos is bringing to the area.”

Dave Carter, President of Kratos Defense & Rocket Support Services, said: “Kratos is proud to be leading the MACH-TB industry team and building the facilities needed to augment our nation’s capabilities to advance hypersonic testing. The IPIF will provide needed infrastructure to accelerate the advancement of critical hypersonic technologies.”

Kratos remains at the forefront of hypersonic and advanced technology development and testing, providing affordable, high-performance solutions to meet the needs of the U.S. military and allied nations. Kratos is the only company delivering both propulsion and flyer systems, which includes Kratos’ low cost Erinyes Hypersonic Flyer, Dark Fury, Zeus and Oriole Solid Rocket Motors, along with other Kratos systems and technologies. Kratos provides unmatched innovation, disruptive capabilities, mission responsiveness and affordability to our customers across our portfolio of systems.

For more information on Kratos and its hypersonic programs, visit www.kratosdefense.com.

About Kratos Defense & Security Solutions Kratos Defense & Security Solutions, Inc. (NASDAQ: KTOS) is a technology, products, system and software company addressing the defense, national security, and commercial markets. Kratos makes true internally funded research, development, capital and other investments, to rapidly develop, produce and field solutions that address our customers’ mission critical needs and requirements. At Kratos, affordability is a technology, and we seek to utilize proven, leading edge approaches and technology, not unproven bleeding edge approaches or technology, with Kratos’ approach designed to reduce cost, schedule and risk, enabling us to be first to market with cost effective solutions. We believe that Kratos is known as an innovative disruptive change agent in the industry, a company that is an expert in designing products and systems up front for successful rapid, large quantity, low-cost future manufacturing which is a value add competitive differentiator for our large traditional prime system integrator partners and also to our government and commercial customers. Kratos intends to pursue program and contract opportunities as the prime or lead contractor when we believe that our probability of win (PWin) is high and any investment required by Kratos is within our capital resource comfort level. We intend to partner and team with a large, traditional system integrator when our assessment of PWin is greater or required investment is beyond Kratos’ comfort level. Kratos’ primary business areas include virtualized ground systems for satellites and space vehicles including software for command & control (C2) and telemetry, tracking and control (TT&C), jet powered unmanned aerial drone systems, advanced vehicles and rocket systems, propulsion systems for drones, missiles, loitering munitions, supersonic systems, space craft and launch systems, C5ISR and microwave electronic products for missile, radar, missile defense, space, satellite, counter UAS, directed energy, communication and other systems, and virtual & augmented reality training systems for the warfighter. For more information, visit www.KratosDefense.com.

Notice Regarding Forward-Looking Statements Certain statements in this press release may constitute “forward-looking statements” within the meaning of the Private Securities Litigation Reform Act of 1995. These forward-looking statements are made on the basis of the current beliefs, expectations and assumptions of the management of Kratos and are subject to significant risks and uncertainty. Investors are cautioned not to place undue reliance on any such forward-looking statements. All such forward-looking statements speak only as of the date they are made, and Kratos undertakes no obligation to update or revise these statements, whether as a result of new information, future events or otherwise. Although Kratos believes that the expectations reflected in these forward-looking statements are reasonable, these statements involve many risks and uncertainties that may cause actual results to differ materially from what may be expressed or implied in these forward-looking statements. For a further discussion of risks and uncertainties that could cause actual results to differ from those expressed in these forward-looking statements, as well as risks relating to the business of Kratos in general, see the risk disclosures in the Annual Report on Form 10-K of Kratos for the year ended December 29, 2024, and in subsequent reports on Forms 10-Q and 8-K and other filings made with the SEC by Kratos.

Launch in Key Global Crypto Market Signals Company’s Growing International Momentum

ATLANTA, Nov. 12, 2025 (GLOBE NEWSWIRE) — Bitcoin Depot (NASDAQ: BTM), a U.S.-based Bitcoin ATM (“BTM”) operator and leading fintech company, today announced its entrance into the Asian market with its expansion into Hong Kong. This move highlights Bitcoin Depot’s accelerating global momentum and strategic focus on expanding into markets where cash-to-crypto access is in high demand.

Hong Kong has rapidly emerged as one of the most watched crypto markets in the world, serving as a key financial hub with growing institutional and retail interest in digital assets. With this launch, Bitcoin Depot will become one of the top five operators in the region.

“Hong Kong is quickly becoming a global center for crypto, with the right mix of regulation, demand, and momentum,” said Scott Buchanan, President & COO of Bitcoin Depot. “What we do best is make Bitcoin easy and accessible in the real world, directly addressing the demand we see in the Hong Kong market. Expanding here is a clear step forward as we continue our mission of bringing Bitcoin to the Masses.®”

This expansion into Hong Kong builds on Bitcoin Depot’s strong operational momentum and growth throughout 2025. It follows the recent retail partnership with GPM Investments, the asset acquisition of National Bitcoin ATM, and the successful rollout of enhancements to its compliance program in October.

Since becoming the first U.S. Bitcoin ATM operator to go public in July 2023, the company has steadily expanded its footprint across North America and Australia, highlighting its ability to scale while maintaining profitability.

Bitcoin Depot’s products and services provide an intuitive, fast, and convenient way to convert cash into Bitcoin. This allows users to access the broader digital financial system, including payments, transfers, remittances, online purchases, and investments.

About Bitcoin Depot Bitcoin Depot Inc. (Nasdaq: BTM) was founded in 2016 with the mission to connect those who prefer to use cash to the broader, digital financial system. Bitcoin Depot provides its users with simple, efficient and intuitive means of converting cash into Bitcoin, which users can deploy in the payments, spending and investing space. Users can convert cash to bitcoin at Bitcoin Depot kiosks in 47 states and at thousands of name-brand retail locations in 31 states through its BDCheckout product. The Company has the largest market share in North America with over 9,000 kiosk locations as of August 2025. Learn more at www.bitcoindepot.com.

Cautionary Note Regarding Forward-Looking Statements This press release and any oral statements made in connection herewith include “forward-looking statements” within the meaning of Section 27A of the Securities Act of 1933, as amended, and Section 21E of the Exchange Act. Forward-looking statements are any statements other than statements of historical fact, and include, but are not limited to, statements regarding the expectations of plans, business strategies, objectives and growth and anticipated financial and operational performance, including our growth strategy and ability to increase deployment of our products and services, the anticipated effects of the Agreement. These forward-looking statements are based on management’s current beliefs, based on currently available information, as to the outcome and timing of future events. Forward-looking statements are often identified by words such as “anticipate,” “appears,” “approximately,” “believe,” “continue,” “could,” “designed,” “effect,” “estimate,” “evaluate,” “expect,” “forecast,” “goal,” “initiative,” “intend,” “may,” “objective,” “outlook,” “plan,” “potential,” “priorities,” “project,” “pursue,” “seek,” “should,” “target,” “when,” “will,” “would,” or the negative of any of those words or similar expressions that predict or indicate future events or trends or that are not statements of historical matters, although not all forward-looking statements contain such identifying words. In making these statements, we rely upon assumptions and analysis based on our experience and perception of historical trends, current conditions, and expected future developments, as well as other factors we consider appropriate under the circumstances. We believe these judgments are reasonable, but these statements are not guarantees of any future events or financial results. These forward-looking statements are provided for illustrative purposes only and are not intended to serve as, and must not be relied on by any investor as, a guarantee, an assurance, a prediction or a definitive statement of fact or probability. Actual events and circumstances are difficult or impossible to predict and will differ from assumptions. Many actual events and circumstances are beyond our control.

These forward-looking statements are subject to a number of risks and uncertainties, including changes in domestic and foreign business, market, financial, political and legal conditions; failure to realize the anticipated benefits of the business combination; future global, regional or local economic and market conditions; the development, effects and enforcement of laws and regulations; our ability to manage future growth; our ability to develop new products and services, bring them to market in a timely manner and make enhancements to our platform; the effects of competition on our future business; our ability to issue equity or equity-linked securities; the outcome of any potential litigation, government and regulatory proceedings, investigations and inquiries; and those factors described or referenced in filings with the Securities and Exchange Commission. If any of these risks materialize or our assumptions prove incorrect, actual results could differ materially from the results implied by these forward-looking statements. There may be additional risks that we do not presently know or that we currently believe are immaterial that could also cause actual results to differ from those contained in the forward-looking statements. In addition, forward-looking statements reflect our expectations, plans or forecasts of future events and views as of the date of this press release. We anticipate that subsequent events and developments will cause our assessments to change.

We caution readers not to place undue reliance on forward-looking statements. Forward-looking statements speak only as of the date they are made, and we undertake no obligation to update publicly or otherwise revise any forward-looking statements, whether as a result of new information, future events, or other factors that affect the subject of these statements, except where we are expressly required to do so by law. All written and oral forward-looking statements attributable to us are expressly qualified in their entirety by this cautionary statement.

IRVINE, Calif., Nov. 12, 2025 (GLOBE NEWSWIRE) — Eledon Pharmaceuticals, Inc. (“Eledon”) (NASDAQ: ELDN), today announced the pricing of its underwritten public offering of (i) 15,152,485 shares of its common stock at a public offering price of $1.65 per share and (ii) in lieu of common stock to certain investors, pre-funded warrants to purchase up to an aggregate of 15,151,515 shares of common stock at a public offering price of $1.649 per pre-funded warrant. The pre-funded warrants will be immediately exercisable and will have an exercise price of $0.001 per share. The gross proceeds from the offering, before deducting underwriting discounts and commissions and offering expenses, are expected to be approximately $50 million. In addition, Eledon has granted to the underwriters a 30-day option to purchase up to 4,545,600 additional shares of common stock at the public offering price, less underwriting discounts and commissions. All of the shares of common stock and pre-funded warrants in the offering are to be sold by Eledon. The offering is expected to close on or about November 13, 2025, subject to the satisfaction of customary closing conditions.

Leerink Partners, Cantor and LifeSci Capital are acting as joint book-running managers for the offering.

Eledon currently intends to use the net proceeds from the offering to support the continued clinical development of its product candidates and advance its pipeline programs as well as for general corporate purposes.

The offering is being made pursuant to a registration statement on Form S-3 (File No. 333-282260), previously filed with the Securities and Exchange Commission (the “SEC”) on September 20, 2024 and declared effective on October 2, 2024. The offering is being made only by means of a prospectus and prospectus supplement that form a part of the registration statement. A preliminary prospectus supplement and accompanying prospectus relating to the offering was filed with the SEC on November 12, 2025 and a final prospectus supplement relating to the offering will be filed with the SEC and available on the SEC’s website at www.sec.gov. Copies of the final prospectus supplement and the accompanying prospectus, once available, may also be obtained by contacting Leerink Partners LLC, Attention: Syndicate Department, 53 State Street, 40th Floor, Boston, Massachusetts 02109, by telephone at (800) 808-7525, ext. 6105, or by email at syndicate@leerink.com, or Cantor Fitzgerald & Co., Attention: Capital Markets, 110 East 59th Street, 6th Floor, New York, NY 10022, or by email at prospectus@cantor.com. The final terms of the proposed offering will be disclosed in a final prospectus supplement to be filed with the SEC.

This press release shall not constitute an offer to sell or the solicitation of an offer to buy, nor shall there be any sale of, these securities in any state or jurisdiction in which such offer, solicitation or sale would be unlawful prior to the registration or qualification under the securities laws of any such state or jurisdiction.

About Eledon Pharmaceuticals and tegoprubart

Eledon Pharmaceuticals, Inc. is a clinical stage biotechnology company that is developing immune-modulating therapies for the management and treatment of life-threatening conditions. Eledon’s lead investigational product is tegoprubart, an anti-CD40L antibody with high affinity for the CD40 Ligand, a well-validated biological target that has broad therapeutic potential. The central role of CD40L signaling in both adaptive and innate immune cell activation and function positions it as an attractive target for non-lymphocyte depleting, immunomodulatory therapeutic intervention. Eledon is building upon a deep historical knowledge of anti-CD40 Ligand biology to conduct preclinical and clinical studies in kidney allograft transplantation, xenotransplantation, and amyotrophic lateral sclerosis (ALS). Eledon is headquartered in Irvine, California.

Forward-Looking Statements

This press release contains “forward-looking statements” within the meaning of the Private Securities Litigation Reform Act of 1995 that involve substantial risks and uncertainties, including statements regarding Eledon’s expectations on the timing and completion of the offering and the anticipated use of proceeds therefrom. No assurance can be given that the offering will be completed on the terms described. Forward-looking statements are inherently uncertain and are subject to numerous risks and uncertainties, including market conditions, failure of customary closing conditions and the risk factors and other matters set forth in the preliminary prospectus supplement and final prospectus supplement that will be filed with the SEC and other risks and uncertainties that could cause Eledon’s actual results to differ materially from the forward-looking statements contained herein are discussed in the company’s quarterly 10-Qs, annual 10-K, and other filings with the SEC, which can be found at www.sec.gov. Any forward-looking statements contained in this press release speak only as of the date hereof and not of any future date, and the company expressly disclaims any intent to update any forward-looking statements, whether as a result of new information, future events or otherwise.

In a move signaling renewed interest in the digital radio sector, Canadian media and technology company Stingray Group has acquired internet radio service TuneIn for $175 million. The deal includes $150 million in cash at closing and up to $25 million in deferred payment, financed through Stingray’s renewed credit facility.

The acquisition marks a major shift in the online streaming landscape. Once valued near $500 million, TuneIn was a pioneer in internet radio streaming, known for bringing traditional radio stations, talk shows, sports broadcasts, and music to a global digital audience. Unlike subscription-heavy services such as Spotify or Apple Music, TuneIn built its business around live radio content accessible across devices, including smart speakers, connected cars, and mobile apps.

Founded in 2002, TuneIn grew to over 75 million monthly active listeners across more than 100 countries and over 200 connected platforms. However, the company faced increasing pressure as consumer listening habits evolved toward on-demand music and podcasts. Despite efforts to diversify into ad-free subscriptions and audiobooks, TuneIn’s growth slowed amid intense competition and changing user expectations.

For Stingray, the deal represents an opportunity to expand beyond its traditional media and music services. Based in Montreal, Stingray operates television music channels, radio stations, and ad-supported streaming platforms. Acquiring TuneIn gives the company instant global reach, access to a vast listener base, and valuable relationships with automakers and device manufacturers. TuneIn’s integration in over 50 car infotainment systems could position Stingray as a stronger player in the in-car audio experience, a fast-growing battleground for streaming companies.

The acquisition values TuneIn at approximately 1.6 times its projected 2025 sales of $110 million and about six times its adjusted EBITDA of $30 million. For a company that once attracted big-name investors and partnerships, the sale price highlights how crowded and capital-intensive the streaming audio market has become.

Still, Stingray appears to be betting on a rebound in digital radio and live content consumption. As advertisers look for alternatives to traditional broadcast and major streaming services, TuneIn’s platform offers diverse ad inventory and a global audience. The acquisition could also help Stingray cross-promote its other media properties, while using TuneIn’s distribution network to scale faster internationally.

The deal is expected to close by year-end, pending customary approvals. Post-acquisition, the TuneIn brand will remain active, while Stingray forecasts that combined revenue will exceed $400 million annually.

For small-cap investors, the move underscores how mid-sized media companies can leverage acquisitions to compete in a market dominated by giants. By acquiring undervalued digital assets like TuneIn, firms such as Stingray can tap into niche but loyal audiences, diversify revenue streams, and strengthen their foothold in the evolving audio ecosystem.

If successful, this acquisition could set the stage for renewed investor confidence in small and mid-cap media technology plays — especially those with the scale and strategy to bridge traditional and digital listening experiences.

Patrick McCann, CFA, Research Analyst, Noble Capital Markets, Inc.

Michael Kupinski, Director of Research, Equity Research Analyst, Digital, Media & Technology , Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

Q3 hits headwind. Conduent reported Q3 revenue of $767 million and adj. EBITDA of $40 million, modestly below our estimates of $794 million and $44 million. While sales in the Commercial segment lagged, Transportation delivered strong revenue growth (+15% Y/Y) and Government margins expanded to 25.6%. Totally company adj. EBITDA margins improved 110 bps year-over-year, underscoring steady operational progress.

Pipeline growing. Overall new business activity was solid with the qualified ACV pipeline rising 9% Y/Y to $3.4 billion, led by Government and Transportation momentum. While the Commercial segment struggled to close sales, we believe a streamlined go-to-market model and early software-licensing traction should support 2026 revenue stabilization.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

Michael Kupinski, Director of Research, Equity Research Analyst, Digital, Media & Technology , Noble Capital Markets, Inc.

Jacob Mutchler, Research Associate, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

Solid Q3 Results. The company reported Q3 revenue of $59.9 million and adj. EBITDA of $9.5 million, both of which surpassed our estimates of $54.0 million and $2.6 million, respectively. Additionally, the strong results surpassed the high end of company issued guidance, of $51.0 million to $58.0 million in revenue and $2.0 million to $6.0 million in adj. EBITDA. Furthermore, the company hit an important milestone, recording net income for the first time since 2021.

Improved operating structure. Over the past several years, the company has significantly lowered its break-even point from $900 million in 2022 to $180 million in 2025, largely through SG&A optimization and the elimination of Multi Layer sales costs. The new model offers enhanced operating leverage, enabling profitability at lower revenue levels and providing a favorable outlook ahead of several new product releases.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

Joe Gomes, CFA, Managing Director, Equity Research Analyst, Generalist , Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

Overview. CVG’s operating environment remains challenged with lower demand in the key Construction, Agriculture, and Class 8 truck end markets. Nonetheless, in 3Q25, the Company saw continued sequential expansion in adjusted gross margin in the quarter. The Company is making progress with customers in regards to mitigating tariff impacts.

3Q25 Results. Revenues of $152.5 million were down 11.2%, primarily due to softening in North American demand. We were at $158 million. Adjusted EBITDA was $4.6 million, up 7.0%, with an adjusted EBITDA margin of 3.0%, up from 2.5% a year ago. CVG reported a net loss from continuing operations of $6.8 million, or $(0.20)/sh and adjusted net loss of $4.6 million, or $(0.14)/sh, compared to net loss from continuing operations of $0.9 million, or $(0.03)/sh, and adjusted net loss of $0.4 million, or $(0.01)/sh.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

CHICAGO, Nov. 11, 2025 (GLOBE NEWSWIRE) — GoHealth, Inc. (GoHealth) (NASDAQ: GOCO), a leading health insurance marketplace and Medicare-focused digital health company, announced that the company will release its third quarter 2025 financial results on the morning of November 13, 2025.

Chief Executive Officer, Vijay Kotte, and Chief Financial Officer, Brendan Shanahan, will host a conference call and live audio webcast on the day of the release at 8:00 a.m. (ET) to discuss the results.

A live audio webcast of the conference call will be available via GoHealth’s Investor Relations website, https://investors.gohealth.com/. A replay of the call will be available via webcast for on-demand listening shortly after the completion of the call.

About GoHealth, Inc.

GoHealth is a leading health insurance marketplace and Medicare-focused digital health company whose purpose is to compassionately ensure consumers’ peace of mind when making healthcare decisions so they can focus on living life. For many of these consumers, enrolling in a health insurance plan is confusing and difficult, and seemingly small differences between health plans may lead to significant out-of-pocket costs or lack of access to critical providers and medicines. GoHealth’s proprietary technology platform leverages modern machine-learning algorithms, powered by over two decades of insurance purchasing behavior, to reimagine the process of matching a health plan to a consumer’s specific needs. Its unbiased, technology-driven marketplace coupled with highly skilled licensed agents has facilitated the enrollment of millions of consumers in Medicare plans since GoHealth’s inception. For more information, visit https://www.gohealth.com.

Third quarter sales of $152 million, EPS of $(0.20), Adjusted EBITDA of $4.6 million Returns to growth in Global Electrical Solutions segment Updates full year 2025 guidance

NEW ALBANY, Ohio, Nov. 10, 2025 (GLOBE NEWSWIRE) — CVG (NASDAQ: CVGI), a diversified industrial products and services company, today announced financial results for its third quarter ended September 30, 2025.

Third Quarter 2025 Highlights(Results from Continuing Operations; compared with prior year, where comparisons are noted)

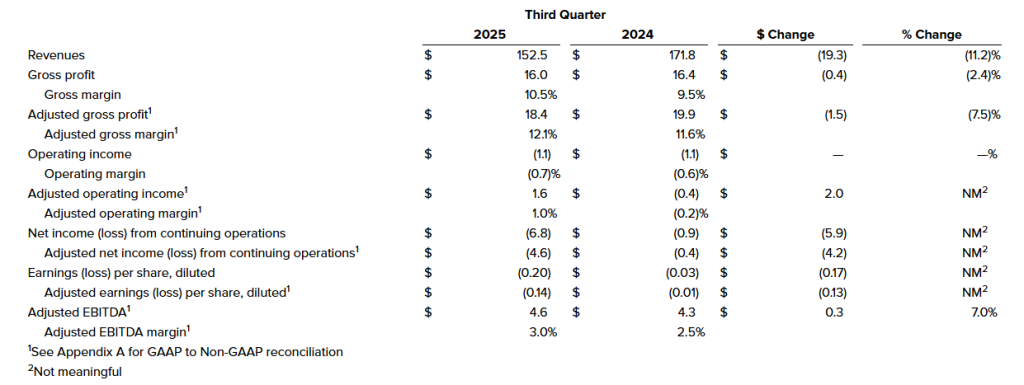

Revenues of $152.5 million, down 11.2%, primarily due to softening in North American demand.

Operating loss of $1.1 million, flat compared to operating loss of $1.1 million. Adjusted operating income of $1.6 million, compared to adjusted operating loss of $0.4 million. The increase in adjusted operating income was primarily attributable to improved gross margin performance and lower SG&A expenses.

Net loss from continuing operations of $6.8 million, or $(0.20) per diluted share and adjusted net loss of $4.6 million, or $(0.14) per diluted share, compared to net loss from continuing operations of $0.9 million, or $(0.03) per diluted share and adjusted net loss of $0.4 million, or $(0.01) per diluted share.

Adjusted EBITDA of $4.6 million, up 7.0%, with an adjusted EBITDA margin of 3.0%, up from 2.5%.

James Ray, President and Chief Executive Officer, said, “In the face of ongoing lower demand in our key Construction, Agriculture, and Class 8 truck end markets, we were pleased with the resilience seen in our third quarter results. We continued to benefit from our operational efficiency improvement and right sizing our manufacturing footprint and enterprise structural cost, evidenced by the continued sequential expansion in our adjusted gross margin in the quarter, despite the lower demand environment. Furthermore, as part of our efforts to preserve margins and position CVG for an eventual end market recovery, we remain focused on reducing SG&A expenses, and we have made demonstrable progress with customers as it relates to mitigating tariff impacts. I want to sincerely thank every member of the CVG team for their commitment, resilience, and focus on execution.”

Mr. Ray continued, “We are encouraged by the continued improvement in Global Electrical Systems segment performance, which returned to year-over-year revenue growth in third quarter, driven by new business wins outside of the Construction and Agriculture end markets, which continue to see lower demand. This segment also saw continued margin expansion year-over-year. In addition, our Global Seating segment expanded margins, as we see the benefits of our operational efficiency improvements, even in a softer demand environment. Our North American-focused Trim Systems and Components segment continues to see weakness as Class 8 production declines year-over year. However, we are taking proactive actions to improve profitability in the face of lower production levels. As an organization, we remain laser-focused on the levers we can control to improve financial performance, drive operational efficiency, and while continuing to launch previously won new customer programs across all segments to best position CVG for the future.”

Andy Cheung, Chief Financial Officer, added, “We are encouraged by our margin performance in the quarter, particularly against a difficult demand backdrop. We continue to optimize our operations to account for individual end market outlooks, particularly in the North American Class 8 truck market. While softer orders led to an inventory increase in the third quarter, we expect to reduce working capital in the fourth quarter. We remain focused on cash generation, with an expectation to drive at least $30 million in free cash flow for the full fiscal year. Continued free cash generation and debt paydown remain our near-term focus areas as we look to drive further cost reductions and improve overall operational efficiency.”

Third Quarter Financial Results from Continuing Operations (amounts in millions except per share data and percentages)

Consolidated Results from Continuing Operations

Third Quarter 2025 Results

Third quarter 2025 revenues were $152.5 million, compared to $171.8 million in the prior year period, a decrease of 11.2%. The overall decrease in revenues was due to lower sales as a result of a softening in customer demand, primarily in the Global Seating and Trim Systems & Components segments.

Operating loss in the third quarter 2025 was flat compared to the prior year period at $1.1 million. Third quarter 2025 adjusted operating income was $1.6 million, compared to loss of $0.4 million in the prior year period. The increase in adjusted operating income was primarily attributable to improved gross margin performance and lower SG&A expenses.

Interest associated with debt and other expenses was $4.1 million and $2.4 million for the third quarter 2025 and 2024, respectively, due to higher interest rates.

Net loss from continuing operations was $6.8 million, or $(0.20) per diluted share, for the third quarter 2025 compared to net loss of $0.9 million, or $(0.03) per diluted share, in the prior year period. Third quarter 2025 adjusted net loss from continuing operations was $4.6 million, or $(0.14) per diluted share, compared to adjusted net loss of $0.4 million, or $(0.01) per diluted share.

On September 30, 2025, the Company had $20.2 million of outstanding borrowings on its U.S. revolving credit facility and $4.2 million outstanding borrowings on its China credit facility, $31.3 million of cash and $96.5 million of availability from the credit facilities (subject to customary borrowing base and other conditions), resulting in total liquidity of $127.8 million.

Third Quarter 2025 Segment Results

Global Seating Segment

Revenues were $68.7 million compared to $76.6 million for the prior year period, a decrease of 10.4%, due to lower sales volume as a result of decreased customer demand.

Operating income was $1.4 million, compared to loss of $1.5 million in the prior year period, an increase of $2.9 million, driven by improved gross margin performance and lower SG&A expenses. Third quarter 2025 adjusted operating income was $2.9 million compared to loss of $0.8 million in the prior year period.

Global Electrical Systems Segment

Revenues were $49.5 million compared to $46.7 million in the prior year period, an increase of 5.9%, primarily as a result of ramping new business wins.

Operating income was $0.8 million compared to loss of $1.5 million in the prior year period, an increase of $2.3 million. The increase in operating income was primarily attributable to higher sales volumes. Third quarter 2025 adjusted operating income was $1.4 million compared to loss of $0.2 million in the prior year period.

Trim Systems and Components Segment

Revenues were $34.3 million compared to $48.4 million in the prior year period, a decrease of 29.2%, primarily due to lower sales volume.

Operating loss was $0.9 million compared to an operating income of $5.4 million in the prior year period. The decrease in operating income was primarily attributable to lower demand and a gain on a facility sale in the prior period. Third quarter 2025 adjusted operating loss was $0.3 million compared to income of $4.1 million in the prior year period.

Outlook

CVG updated the Company’s outlook for the full year 2025, based on current market conditions:

This outlook reflects, among others, current industry forecasts for North America Class 8 truck builds. According to ACT Research, 2025 North American Class 8 truck production levels are expected to be at 239,000 units, down 28% versus the 2024 actual Class 8 truck builds of 332,372 units and down 5% from the time of our second quarter 2025 earnings release, when ACT Research was forecasting 252,000 units for 2025 North American Class 8 truck production.

Construction and Agriculture end markets are projected to decline approximately 5-15% in 2025. However, we expect the contribution from new business wins outside of Construction and Agriculture end markets in Electrical Systems to soften this decline.

GAAP to Non-GAAP Reconciliation

A reconciliation of GAAP to non-GAAP financial measures referenced in this release is included as Appendix A to this release.

Conference Call

A conference call to discuss this press release is scheduled for Tuesday, November 11, 2025, at 8:30 a.m. ET. Management intends to reference the Q3 2025 Earnings Call Presentation during the conference call. To participate, dial (800) 549-8228 using conference code 19689. International participants dial (289) 819-1520 using conference code 19689.

This call is being webcast and can be accessed through the “Investors” section of CVG’s website at ir.cvgrp.com, where it will be archived for one year.

A telephonic replay of the conference call will be available for a period of two weeks following the call. To access the replay, dial (888) 660-6264 using access code 19689#.

Company Contact Andy Cheung Chief Financial Officer CVG IR@cvgrp.com

Investor Relations Contact Ross Collins or Nathan Skown Alpha IR Group CVGI@alpha-ir.com

About CVG

CVG is a global provider of systems, assemblies and components to the global commercial vehicle market and the electric vehicle market. We deliver real solutions to complex design, engineering and manufacturing problems while creating positive change for our customers, industries and communities we serve. Information about the Company and its products is available on the internet at www.cvgrp.com.

Forward-Looking Statements

This press release contains forward-looking statements that are subject to risks and uncertainties. These statements often include words such as “believe”, “anticipate”, “plan”, “expect”, “intend”, “will”, “should”, “could”, “would”, “project”, “continue”, “likely”, and similar expressions. In particular, this press release may contain forward-looking statements about the Company’s expectations for future periods with respect to its plans to improve financial results, the future of the Company’s end markets, changes in the Class 8 and Class 5-7 North America truck build rates, performance of the global construction and agricultural equipment business, the Company’s prospects in the wire harness and electric vehicle markets, the Company’s initiatives to address customer needs, organic growth, the Company’s strategic plans and plans to focus on certain segments, competition faced by the Company, volatility in and disruption to the global economic environment including global supply chain constraints, inflation and labor shortages, tariffs and counter-measures, financial covenant compliance, anticipated effects of acquisitions, production of new products, plans for capital expenditures, and the Company’s financial position or other financial information. These statements are based on certain assumptions that the Company has made in light of its experience as well as its perspective on historical trends, current conditions, expected future developments and other factors it believes are appropriate under the circumstances. Actual results may differ materially from the anticipated results because of certain risks and uncertainties, including those included in the Company’s filings with the SEC. There can be no assurance that statements made in this press release relating to future events will be achieved. The Company undertakes no obligation to update or revise forward-looking statements to reflect changed assumptions, the occurrence of unanticipated events or changes to future operating results over time. All subsequent written and oral forward-looking statements attributable to the Company or persons acting on behalf of the Company are expressly qualified in their entirety by such cautionary statements.

Other Information

Throughout this document, certain numbers in the tables or elsewhere may not sum due to rounding. Rounding may have also impacted the presentation of certain year-on-year percentage changes.