Oil markets wrapped up their third consecutive week of gains on Friday as investors watched closely for U.S. President Donald Trump’s next move regarding the Israel-Iran conflict. West Texas Intermediate (WTI) crude settled just below $75 per barrel, while Brent crude, the global benchmark, hovered around $76, both on track to post roughly 3% gains for the week.

The latest rally in oil prices was largely driven by geopolitical tensions ignited by renewed hostilities between Israel and Iran. While the conflict hasn’t disrupted oil flows yet, the mere prospect of a wider regional escalation has kept traders on edge.

Early Friday trading saw a slight dip in prices as Trump signaled a potential preference for diplomacy over immediate military intervention. “We’ll give diplomacy a chance,” he told reporters on Thursday, suggesting that a final decision on U.S. involvement is still pending. This hint of restraint helped cool the market’s reaction temporarily but did little to derail the broader upward trend in crude prices.

Despite rising oil prices, analysts from major financial institutions remain cautious about the long-term impact of the conflict on global energy markets. Citi’s commodities research team believes the risk of significant supply disruption remains limited.

“Disrupting oil supply isn’t in the interest of either Iran or the U.S.,” said Spiro Dounis, Citi’s senior energy analyst. He noted that even if Iran’s 1.1 million barrels per day of oil exports were completely halted, Brent prices would likely rise only modestly to the $75–78 range — not far above current levels.

Goldman Sachs offered a more dramatic short-term outlook, estimating that in the event of an actual disruption, oil prices could temporarily surge to $90 per barrel. However, the bank expects prices to normalize over the next year, potentially falling back to the $60 range in 2026 as supply recovers.

Importantly, current oil flows remain uninterrupted. Shipments through the Strait of Hormuz — one of the world’s most crucial maritime oil chokepoints — continue unimpeded, and Iranian exports have not declined, easing some of the market’s worst fears.

A key factor cushioning the market is spare production capacity among OPEC+ members. The alliance, which includes major oil producers like Saudi Arabia and Russia, has been gradually increasing output in recent months, providing a potential buffer against sudden supply shocks.

“Above-average global spare capacity — equivalent to 4–5% of global demand — is the main cushion against Iran-specific disruptions,” said Goldman’s Daan Struyven. He pointed to the bloc’s strategic unwinding of production cuts as a stabilizing force in the current market environment.

With uncertainty still looming over the geopolitical situation in the Middle East, oil prices are likely to remain volatile in the near term. Much will depend on whether Trump follows through with military action or continues to push for a diplomatic resolution. For now, investors will be watching closely, knowing that even the perception of risk can be enough to sway global oil markets.

Robert LeBoyer, Senior Vice President, Equity Research Analyst, Biotechnology, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

Preparing For AVERSA Fentanyl Clinical Testing. Nutriband and its partner Kindeva announced that it has completed commercial manufacturing processes and scale-up for AVERSA Fentanyl, its abuse-deterrent fentanyl patch. This allows the company begin manufacturing clinical supplies and filing the IND (Investigational New Drug application) for the Phase 1 clinical study within the timeframe we anticipated. Only a single Phase 1 study is needed to file the application for marketing approval.

Manufacturing Completion Is A Significant Milestone. This scale-up is a significant step that demonstrates the ability to apply Kindeva’s transdermal patch technology for commercial scale production of AVERSA Fentanyl patches. We expect the IND filing to be completed shortly, with clinical testing to follow as expected.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

MAIA is a targeted therapy, immuno-oncology company focused on the development and commercialization of potential first-in-class drugs with novel mechanisms of action that are intended to meaningfully improve and extend the lives of people with cancer. Our lead program is THIO, a potential first-in-class cancer telomere targeting agent in clinical development for the treatment of NSCLC patients with telomerase-positive cancer cells. For more information, please visit www.maiabiotech.com.

Robert LeBoyer, Senior Vice President, Equity Research Analyst, Biotechnology, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

MAIA Makes Its Third Supply Agreement. MAIA announced that it has entered a supply agreement with Genentech/Roche to test THIO (ateganosine) in combination with Tecentriq (atezolizumab, Roche’s PD-L1 checkpoint inhibitor) for the treatment of several hard-to-treat cancers. MAIA now has supply agreements to test THIO in combination with checkpoint inhibitors from three global pharmaceutical companies, which we see as an indicator of interest for future partnerships.

PD-1 or PD-1L? That Is The Question. Checkpoint inhibitors block the interaction of the surface proteins PD-1 (programmed death receptor-1) with PD-1L (the programed death receptor-1 ligand). When the PD-1 receptor binds to the PD-1L ligand, it inhibits the immune response. Checkpoint inhibitors are monoclonal antibody drugs against PD-1 or PD-L1 that block this interaction, allowing cancer cells to be recognized by a patient’s immune system and killed.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

Euroseas Ltd. was formed on May 5, 2005 under the laws of the Republic of the Marshall Islands to consolidate the ship owning interests of the Pittas family of Athens, Greece, which has been in the shipping business over the past 140 years. Euroseas trades on the NASDAQ Capital Market under the ticker ESEA. Euroseas operates in the container shipping market. Euroseas’ operations are managed by Eurobulk Ltd., an ISO 9001:2008 and ISO 14001:2004 certified affiliated ship management company, which is responsible for the day-to-day commercial and technical management and operations of the vessels. Euroseas employs its vessels on spot and period charters and through pool arrangements.

Mark Reichman, Managing Director, Equity Research Analyst, Natural Resources, Noble Capital Markets, Inc.

Hans Baldau, Associate Analyst, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

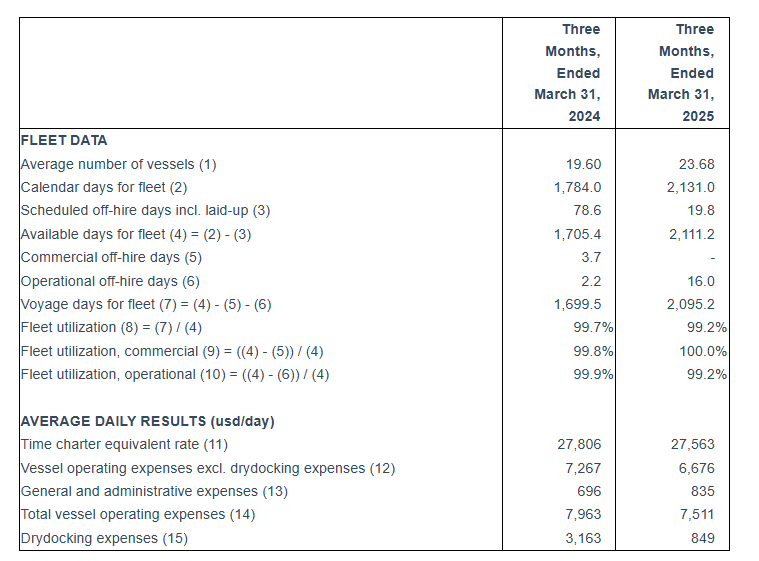

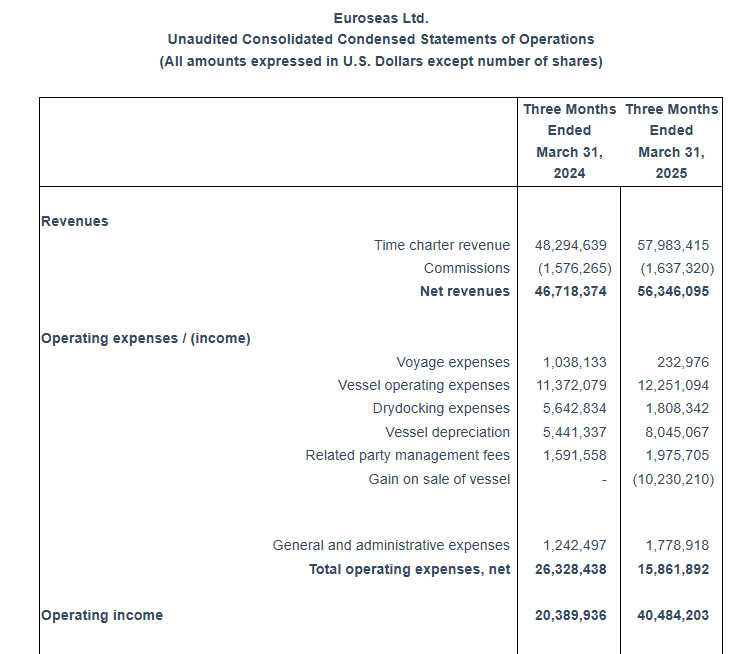

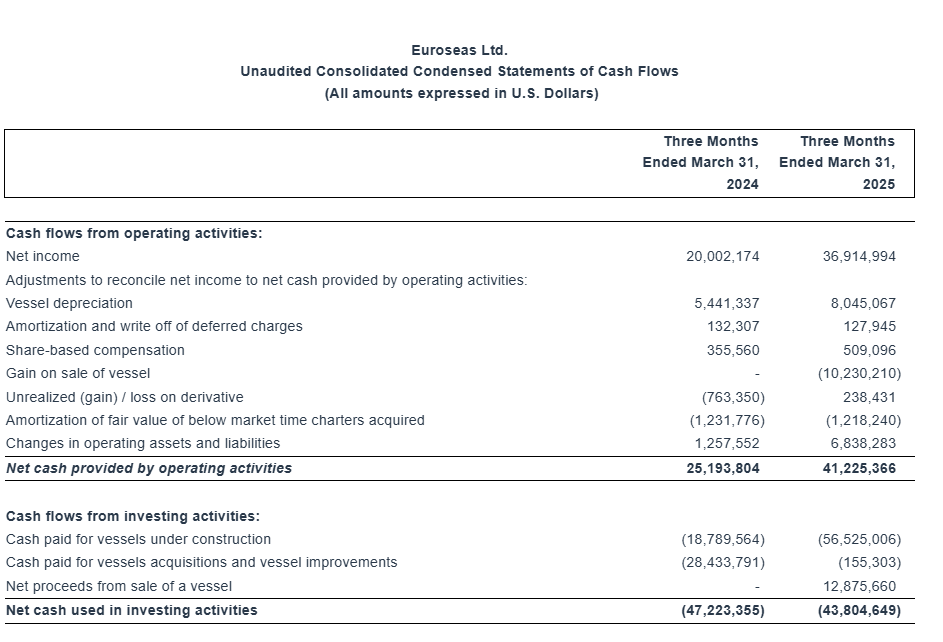

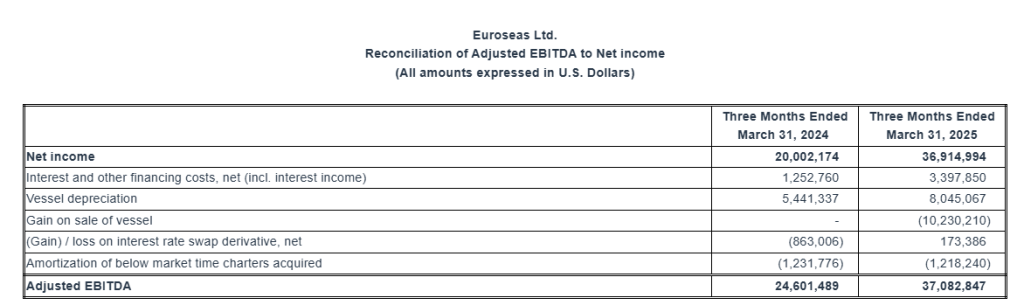

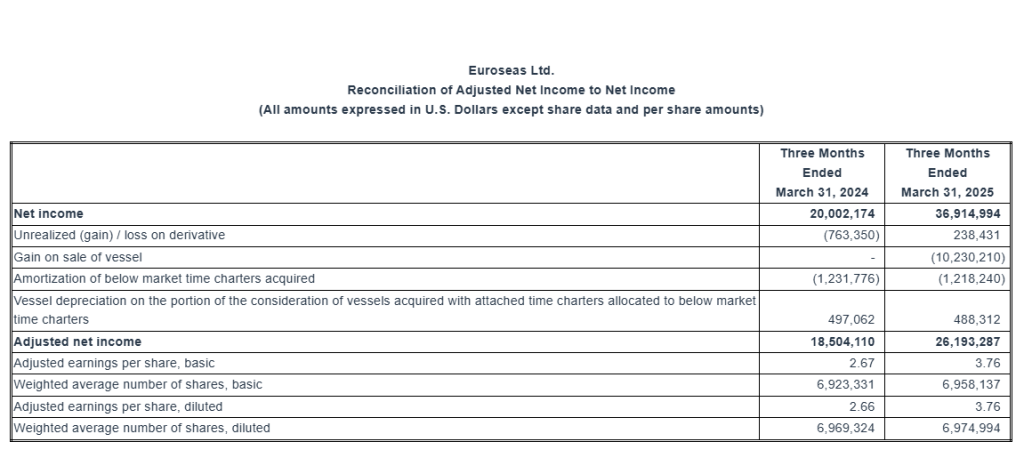

First quarter 2025 financial results. Euroseas Ltd. reported adjusted EBITDA and earnings per share (EPS) of $37.1 million and $3.76, respectively, compared to $24.6 million and $2.66 during the prior year period. Revenue increased due to a higher average number of vessels compared to the same period last year, while operating expenses declined. We had projected adjusted EBITDA and EPS of $34.7 million and $3.35, respectively. Relative to our estimates, revenues were higher, based on an average daily time charter equivalent rate of $27,806, versus our estimate of $26,221, while operating expenses were lower. Vessel operating expenses totaled $12.3 million compared to our estimate of $13.3 million.

Market outlook. The containership sector may face some challenges, including the potential for transit to resume through the Suez Canal, weaker economic conditions due to fluid trade policies, and a high industry order book, which could increase the supply of vessels. However, the company’s strong charter coverage through 2026 could insulate it from the potential for lower rates. Moreover, the feeder and intermediate segments of the market have relatively low order books, and demand for vessels remains strong.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

Semiconductor stocks stumbled Friday after reports surfaced that the U.S. government is considering revoking waivers that currently allow major global chipmakers to use American technology in their Chinese operations.

According to The Wall Street Journal, Commerce Department official Jeffrey Kessler informed executives from Samsung Electronics, SK Hynix, and Taiwan Semiconductor Manufacturing Company (TSMC) earlier this week that the Biden administration is reviewing whether to terminate these exemptions. The waivers had enabled companies to export U.S. chipmaking tools and software to facilities in China, despite existing export controls.

The news triggered a wave of selling across the semiconductor sector. The VanEck Semiconductor ETF (SMH) dropped around 1%, while individual stocks including Nvidia, Qualcomm, and Marvell Technology fell roughly 1%. TSMC shares declined more than 2% as investors reacted to the potential disruption to its China-based operations.

The Commerce Department’s move signals a possible escalation in the ongoing tech tensions between Washington and Beijing. Although the two nations recently agreed on the framework of a second trade deal during meetings in London, the Biden administration has continued to tighten restrictions on advanced chip technology exports, citing national security concerns.

“These waivers were a key lifeline for chipmakers operating in China,” said Adam Kinley, an analyst at EastWest Securities. “If revoked, companies like TSMC and Samsung could face operational hurdles, reallocation costs, and potentially a sharp drop in revenue tied to China-based production.”

The semiconductor industry has already been navigating growing restrictions. In 2022 and 2023, the U.S. introduced sweeping controls limiting China’s access to advanced AI chips and tools required for high-end semiconductor fabrication. The latest efforts to close loopholes reflect Washington’s concern that Beijing could exploit foreign chip factories operating inside China to circumvent those controls.

The impact of these export curbs is already being felt. Nvidia, a leading AI chipmaker, disclosed last month that U.S. government restrictions on its China-bound H20 chips contributed to an estimated $8 billion hit in sales. CEO Jensen Huang described the China market—once worth $50 billion to U.S. chip companies—as “effectively closed.”

The potential rollback of waivers could further strain U.S.-China trade relations, particularly as China has denounced these restrictions as discriminatory. While the current policy discussions are ongoing and no final decision has been made, the possibility of more sweeping limits has introduced fresh volatility into the sector.

Investors and chipmakers alike will be watching closely for any formal announcements in the coming weeks. A reversal of the waivers would force affected companies to reevaluate supply chains, consider shifting manufacturing operations out of China, and potentially delay production schedules.

In the near term, analysts expect heightened market sensitivity to any government signals or diplomatic developments related to U.S.-China tech policy. As Washington balances national security priorities with global economic interests, the semiconductor industry finds itself once again at the center of geopolitical risk.

In a historic move for the crypto industry, the U.S. Senate has passed the GENIUS Act—short for Guiding and Establishing National Innovation for US Stablecoins—laying the foundation for the first federal framework governing stablecoins. Though the bill still awaits approval from the House of Representatives and President Trump’s signature, its Senate passage marks a seismic shift in crypto policy that could reshape the digital asset landscape.

Stablecoins, digital tokens typically pegged to the U.S. dollar, are widely used for trading, payments, and preserving value in volatile markets. The GENIUS Act aims to bring oversight and legitimacy to this rapidly growing segment by requiring issuers to maintain full reserves in cash or U.S. Treasury assets, undergo routine audits, and publicly disclose their reserve compositions monthly.

The legislation has already catalyzed a dramatic response. According to CoinDesk, the total market capitalization of stablecoins surged to a record $251.7 billion, reflecting a 22% year-to-date increase. Industry leaders, including Circle (CRCL)—the largest U.S. stablecoin issuer—have hailed the bill as a breakthrough. Circle’s stock has soared 400% since going public in early June, signaling investor confidence in the sector’s regulated future.

“This bill gives us the right foundation,” said Dante Disparte, Circle’s Chief Strategy Officer. “Whether you’re a bank, a fintech, or a non-bank issuer, you now have a common regulatory floor.”

One of the most consequential elements of the GENIUS Act is its two-tiered regulatory approach: large issuers with over $10 billion in assets will fall under federal oversight, led by the Federal Reserve and Office of the Comptroller of the Currency (OCC), while smaller issuers will be supervised by state regulators. Additionally, the act prohibits stablecoins from paying interest, a provision meant to draw a clear line between digital currencies and traditional savings products.

The bill also restricts members of Congress and their families from profiting off stablecoin ventures—though notably excludes President Trump and his family, sparking some partisan criticism. Trump’s growing involvement in the sector, including the launch of USD1 stablecoin by his crypto firm World Liberty Financial, has raised eyebrows and energized Republican support.

Big banks and corporations are now eyeing stablecoin issuance. Bank of America has confirmed it is exploring options, and Amazon and Walmart are reportedly assessing opportunities, though both companies remain cautious. The potential for new entrants to bypass traditional payment rails like Visa and Mastercard could be disruptive—and lucrative.

Despite concerns over investor runs and tech monopolies, the GENIUS Act includes strict consumer protection clauses, criminal penalties for noncompliance, and Treasury approval for tech firms wishing to issue stablecoins. Treasury Secretary Scott Bessent projects the U.S. stablecoin market could exceed $2 trillion by 2028 if the bill becomes law.

As the House prepares to review the bill—possibly attaching it to broader crypto legislation—investors are bracing for what could be the most significant wave of adoption and innovation in crypto history. If passed in full, the GENIUS Act could signal not just regulation—but a rebranding of stablecoins from speculative tools to mainstream financial instruments.

Nutriband and Kindeva have completed commercial manufacturing process scale-up for its lead product Aversa™ Fentanyl, an abuse-deterrent fentanyl patch

Nutriband is partnering with Kindeva to develop Aversa™ Fentanyl which combines Nutriband’s Aversa™ abuse-deterrent technology with Kindeva’s FDA-approved fentanyl patch

ORLANDO, Fla., June 18, 2025 (GLOBE NEWSWIRE) — Nutriband Inc. (NASDAQ:NTRB)(NASDAQ:NTRBW), a company engaged in the development of prescription transdermal pharmaceutical products, today announced that it has completed commercial manufacturing process scale-up for its lead product, Aversa™ Fentanyl, with Kindeva, a leading global contract development and manufacturing organization (CDMO) focused on drug-device combination products.

Nutriband is partnering with Kindeva to develop Aversa™ Fentanyl which combines Nutriband’s Aversa™ abuse-deterrent technology with Kindeva’s FDA-approved fentanyl patch. Aversa Fentanyl is manufactured at Kindeva’s state-of-the-art transdermal manufacturing facility located in the United States. The next step is to manufacture clinical supplies and file an Investigational New Drug (IND) application with the FDA to initiate a human abuse liability clinical study.

“We are excited to achieve this commercial development milestone with our partner, Kindeva. Completing the commercial manufacturing scale-up is an important step towards development of a commercially viable product and eventual NDA filing. This achievement demonstrates the compatibility of the Aversa™ abuse deterrent platform technology with established transdermal patch manufacturing processes. Aversa Fentanyl has the potential to be the first abuse deterrent pain patch on the market,” said Gareth Sheridan, CEO, Nutriband.

Nutriband’s AVERSA™ abuse-deterrent technology can be utilized to incorporate aversive agents into transdermal patches to prevent the abuse, diversion, misuse, and accidental exposure of drugs with abuse potential including opioids and stimulants. The AVERSA™ abuse-deterrent technology has the potential to improve the safety profile of transdermal drugs susceptible to abuse, such as fentanyl, while making sure that these drugs remain accessible to those patients who really need them.

AVERSA Fentanyl has the potential to be the world’s first abuse-deterrent opioid patch designed to deter the abuse and misuse and reduce the risk of accidental exposure of transdermal fentanyl patches. AVERSA Fentanyl has the potential to reach peak annual US sales of $80 million to $200 million.1 While initially concentrating on the US market, the unmet medical need for adequate pain management is a global problem, and our goal is to make AVERSA a global solution strategically targeting all major medical markets in the world.

The AVERSA™ abuse deterrent technology is protected by a broad international intellectual property portfolio with patents issued in 46 countries including the United States, Europe, Japan, Korea, Russia, China, Canada, Mexico, and Australia.

1 Health Advances Aversa Fentanyl market analysis report 2022

About AVERSA™ Abuse-Deterrent Transdermal Technology

Nutriband’s AVERSA™ abuse-deterrent transdermal technology incorporates aversive agents into transdermal patches to prevent the abuse, diversion, misuse, and accidental exposure of drugs with abuse potential. The AVERSA™ abuse-deterrent technology has the potential to improve the safety profile of transdermal drugs susceptible to abuse, such as fentanyl, while making sure that these drugs remain accessible to those patients who really need them. The technology is covered by a broad intellectual property portfolio with patents granted in the United States, Europe, Japan, Korea, Russia, China, Canada, Mexico, and Australia.

About Nutriband Inc.

We are primarily engaged in the development of a portfolio of transdermal pharmaceutical products. Our lead product under development is an abuse-deterrent fentanyl patch incorporating our AVERSA™ abuse-deterrent technology. AVERSA™ technology can be incorporated into any transdermal patch to prevent the abuse, misuse, diversion, and accidental exposure of drugs with abuse potential.

The Company’s website is www.nutriband.com. Any material contained in or derived from the Company’s websites or any other website is not part of this press release.

About Kindeva

At Kindeva, we manufacture more tomorrows for patients worldwide. With best-in-class facilities and comprehensive CDMO services, we offer more than manufacturing—we deliver strategic value. Our global network of 10 manufacturing and R&D sites offer exceptional integrated knowledge and capabilities, including Annex 1-compliant state-of-the-art aseptic fill finish capacity and next-generation sustainable inhalation propellant technology. By combining expertise in injectable, pulmonary, nasal and dermal drug delivery, we help meet the demands of today and deliver the possibilities of tomorrow. Find out more at https://www.kindevadd.com.

Forward-Looking Statements

Certain statements contained in this press release, including, without limitation, statements containing the words ‘’believes,” “anticipates,” “expects” and words of similar import, constitute “forward-looking statements” within the meaning of the Private Securities Litigation Reform Act of 1995. Such forward-looking statements involve both known and unknown risks and uncertainties. The Company’s actual results may differ materially from those anticipated in its forward-looking statements as a result of a number of factors, including those including the Company’s ability to develop its proposed abuse-deterrent fentanyl transdermal system and other proposed products, its ability to obtain patent protection for its abuse technology, its ability to obtain the necessary financing to develop products and conduct the necessary clinical testing, its ability to obtain Federal Food and Drug Administration approval to market any product it may develop in the United States and to obtain any other regulatory approval necessary to market any product in other countries, including countries in Europe, its ability to market any product it may develop, its ability to create, sustain, manage or forecast its growth; its ability to attract and retain key personnel; changes in the Company’s business strategy or development plans; competition; business disruptions; adverse publicity and international, national and local general economic and market conditions and risks generally associated with an undercapitalized developing company, as well as the risks contained under “Risk Factors” and “Management’s Discussion and Analysis of Financial Condition and Results of Operations” in the Company’s Form S-1, Forms 10-K’s and Forms 10-Q’s, and the Company’s other filings with the Securities and Exchange Commission. Except as required by applicable law, we undertake no obligation to revise or update any forward-looking statements to reflect any event or circumstance that may arise after the date hereof.

ATHENS, Greece, June 18, 2025 (GLOBE NEWSWIRE) — Euroseas Ltd. (NASDAQ: ESEA, the “Company” or “Euroseas”), an owner and operator of container carrier vessels and provider of seaborne transportation for containerized cargoes, announced today its results for the three-month period ended March 31, 2025 and declared a common stock dividend.

First Quarter 2025 Financial Highlights:

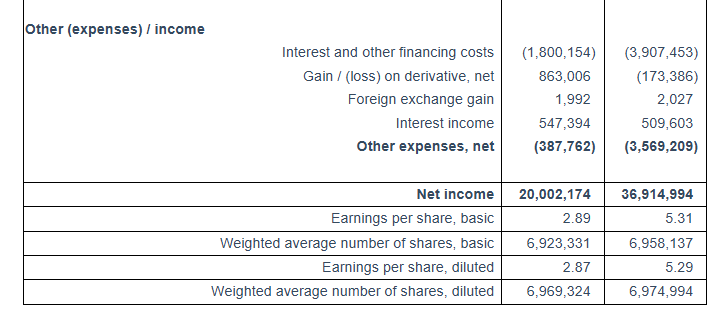

Total net revenues of $56.3 million. Net income of $36.9 million or $5.31 and $5.29 earnings per share basic and diluted, respectively. Adjusted net income1 for the period was $26.2 million or $3.76 per share basic and diluted.

Adjusted EBITDA1 was $37.1 million.

An average of 23.71 vessels were owned and operated during the first quarter of 2025 earning an average time charter equivalent rate of $27,563 per day.

Declared a quarterly dividend of $0.65 per share for the first quarter of 2025 payable on or about July 16, 2025 to shareholders of record on July 9, 2025, as part of the Company’s common stock dividend plan.

On March 17, 2025 the Company completed the spin-off of three of its subsidiaries containing its two older vessels, M/V Aegean Express and M/V Joanna, along with the proceeds from the earlier sale of the vessel M/V Diamantis P, into Euroholdings Ltd. (NASDAQ: EHLD). Beginning on March 18, 2025, Euroholdings Ltd. operates as an independent company.

On May 29, 2025, the Company announced that it has signed an agreement to sell M/V Marcos V, a 6,350 teu intermediate containership built in 2005, to an unaffiliated third party, for $50 million. The vessel is scheduled to be delivered to its buyer in October 2025. The Company is expected to recognize a gain on the sale in excess of $8.50 million, or $1.20 per share.

As of June 18, 2025 we had repurchased 463,074 of our common stock in the open market for a total of about $10.5 million, since the initiation of our share repurchase plan of up to $20 million announced in May 2022.

________________________ 1 Adjusted EBITDA, Adjusted net income and Adjusted earnings per share are not recognized measurements under US GAAP (GAAP) and should not be used in isolation or as a substitute for Euroseas financial results presented in accordance with GAAP. Refer to a subsequent section of the Press Release for the definitions and reconciliation of these measurements to the most directly comparable financial measures calculated and presented in accordance with GAAP.

Aristides Pittas, Chairman and CEO of Euroseas commented: “During the first quarter of 2025, the containership markets showed further strength, with both smaller and larger feeder segments seeing notable rate increases. This positive momentum has continued into the second quarter, with particularly strong gains in the smaller feeder segment. Market strength is also reflected in the secondhand S&P market, where demand for existing tonnage remains firm despite the continued delivery of newbuilds. Reflecting this dynamic, we successfully finalized the sale of one of our intermediate vessels, the M/V Marcos V, to an unaffiliated third party. The market strength is further reflected in our chartering activity resulting in almost 100% charter coverage for 2025 and in excess of 65% for 2026.

“Looking ahead, the containership sector may face notable challenges, primarily due to the high overall orderbook and the possibility that liner companies may resume transits through the Suez Canal. However, elevated geopolitical uncertainty driven by ongoing and escalating tensions between Iran and Israel compounded by uncertainty surrounding the U.S. Administration’s proposed tariffs add another layer of complexity. Specifically, on the supply-side while the orderbook remains high and represents the key challenge for the sector, it is heavily concentrated on larger vessel sizes. In contrast, the feeder and intermediate segments, where our fleet is concentrated, have historically low orderbooks; in addition, due to the higher proportion of older tonnage in these size segments, they are likely to experience a reduction in fleet supply over the coming years. This evolving fleet profile supports the view that, despite the potential risk of cascading from larger vessels, the fundamentals for feeder and intermediate containerships remain favorable.

“On the fleet growth front, we continue to consider ways of further modernizing our fleet. We will be soon retrofitting one more of our secondhand vessels with energy-saving devices. We have further improved our fleet profile by having transferred our two oldest ships to Euroholdings, a spin-off from our company, to pursue a separate independent market and investment strategy. Given our solid liquidity position, our Board has decided to maintain our high yielding quarterly dividend of $0.65 per share. We are also continuing our share buyback program, as our shares are trading at a substantial discount to our net asset value, despite the visibility of our revenues and earnings. As always, we remain committed to identifying attractive investment opportunities that enhance shareholder value and drive sustainable returns.”

Tasos Aslidis, Chief Financial Officer of Euroseas commented: “Our revenues for the first quarter of 2025 are increased by approximately 20% compared to the same period of 2024. This was mainly the result of the increased average number of vessels owned and operated in the first quarter of 2025, compared to the corresponding period of 2024. The Company operated an average of 23.68 vessels, versus 19.60 vessels during the same period last year. Net revenues amounted to $56.3 million for the first quarter of 2025 compared to $46.7 million for the first quarter of 2024.

“Total daily vessel operating expenses, including management fees, general and administrative expenses, but excluding drydocking costs, were $6,676 during the first quarter of 2025 compared $7,276 to the same quarter of last year. This was the result of the lower operating costs of the nine newbuilding vessels delivered during last year and in the first quarter of 2025. In the first quarter of 2024 the Company operated only five of these newbuilding vessels, while the rest were delivered gradually until January 2025.

“Adjusted EBITDA1 during the first quarter of 2025 was $37.1 million compared to $24.6 million achieved in the first quarter of last year.

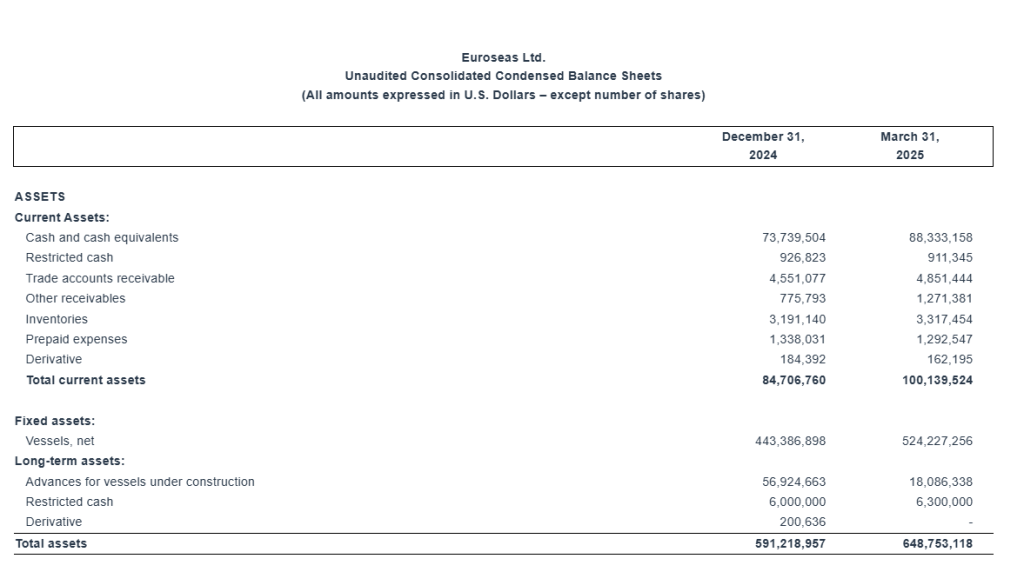

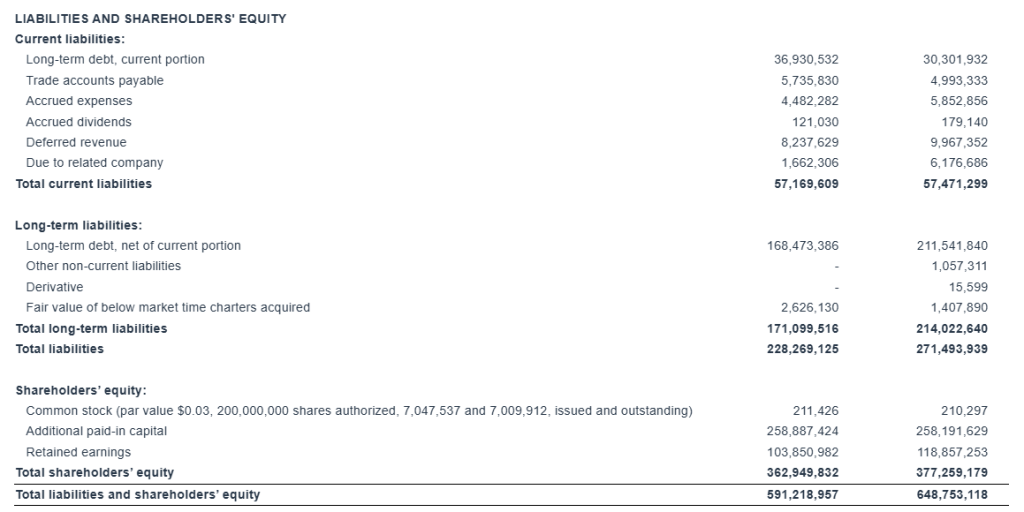

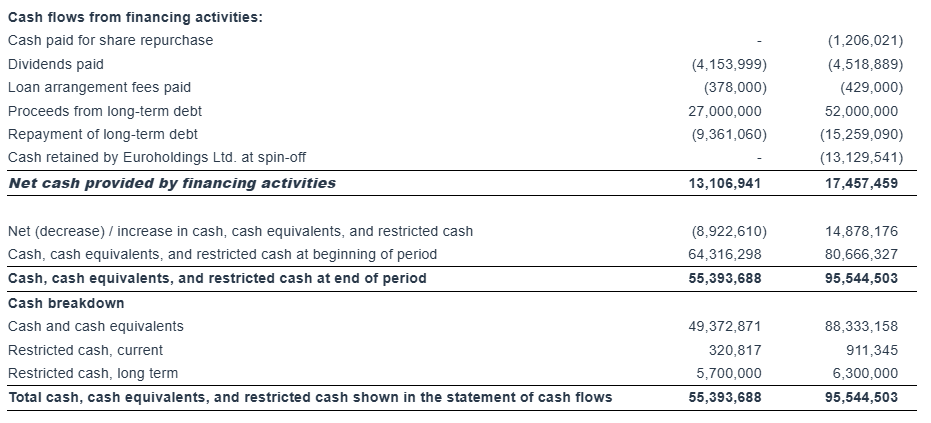

“As of March 31, 2025, our outstanding bank debt (before deducting the unamortized loan fees) was $244.0 million, versus restricted and unrestricted cash of approximately $95.5 million. As of the same date, our scheduled debt repayments over the next 12 months amounted to about $30.7 million (excluding the unamortized loan fees).”

First Quarter 2025 Results: For the first quarter of 2025, the Company reported total net revenues of $56.3 million representing an 20.6% increase over total net revenues of $46.7 million during the first quarter of 2024. On average, 23.68 vessels were owned and operated during the first quarter of 2025 earning an average time charter equivalent rate of $27,563 per day compared to 19.60 vessels in the same period of 2024 earning on average $27,806 per day. The Company reported a net income for the period of $36.9 million, as compared to a net income of $20.0 million for the first quarter of 2024.

Voyage expenses for the first quarter of 2025 amounted to $0.2 million as compared to voyage expenses of $1.0 million for the same period of 2024. The increased amount of 2024 is mainly attributable to bunkers consumption by three of our vessels (M/V “Synergy Antwerp”, M/V “Synergy Oakland” and M/V “Marcos”) during their drydock period.

Vessel operating expenses for the first quarter of 2025 amounted to $12.3 million as compared to $11.4 million for the same period of 2024. The increased amount is due to the higher number of vessels owned and operated in the first quarter of 2025 compared to the corresponding period of 2024.

Depreciation expense for the first quarter of 2025 amounted to $8.0 million compared to $5.4 million for the same period of 2024 due to the increased number of vessels in the Company’s fleet.

Related party management fees for the first quarter of 2025 increased to $2.0 million from $1.6 million for the same period of 2024 as a result of the higher number of vessels in our fleet and the adjustment for inflation in the daily vessel management fee, effective from January 1, 2025, increasing it from 810 Euros to 840 Euros.

In the first quarter of 2025 two of our vessels completed extensive repairs afloat for a total cost of $1.8 million. In the first quarter of 2024 three of our vessels completed their special survey with drydock for a total cost of $5.6 million.

General and administrative expenses slightly increased to $1.8 million in the first quarter of 2025, as compared to $1.2 million in the first quarter of 2024 due to increased professional fees and increased cost for our stock incentive plan.

Interest and other financing costs for the first quarter of 2025 amounted to $3.9 million. Capitalized interest charged on the cost of our newbuilding program was $0.1 million for the first quarter of 2025. For the same period of 2024 interest and other financing costs amounted $1.8 million and the capitalized interest charged on the cost of our newbuilding program was $1.4 million. This increase is due to the increased amount of debt in the current period compared to the same period of 2024. For the three months ended March 31, 2025 the Company recognized a $0.17 million loss on its interest rate swap contract, comprising a $0.07 million realized gain and a $0.24 million unrealized loss. For the three months ended March 31, 2024 the Company recognized a $0.86 million gain on its interest rate swap contracts, comprising a $0.10 million realized gain and a $0.76 million unrealized gain.

Adjusted EBITDA1 for the first quarter of 2025 was $37.1 million, compared to $24.6 million achieved for the first quarter of 2024, primarily higher revenues due to the higher number of vessels owned and operated.

Basic and diluted earnings per share for the first quarter of 2025 was $5.31 and $5.29, respectively, calculated on 6,958,137 basic and 6,974,994 diluted weighted average number of shares outstanding compared to basic and diluted earnings per share of $2.89 and $2.87, respectively for the first quarter of 2024, calculated on 6,923,331 basic and 6,969,324 diluted weighted average number of shares outstanding.

The adjusted earnings per share for the quarter ended March 31, 2025 would have been $3.76 per share basic and diluted, respectively, compared to adjusted earnings of $2.67 and $2.66 per share basic and diluted, respectively, for the first quarter of 2024. Usually, security analysts include Adjusted Net Income in their determination of published estimates of earnings per share.

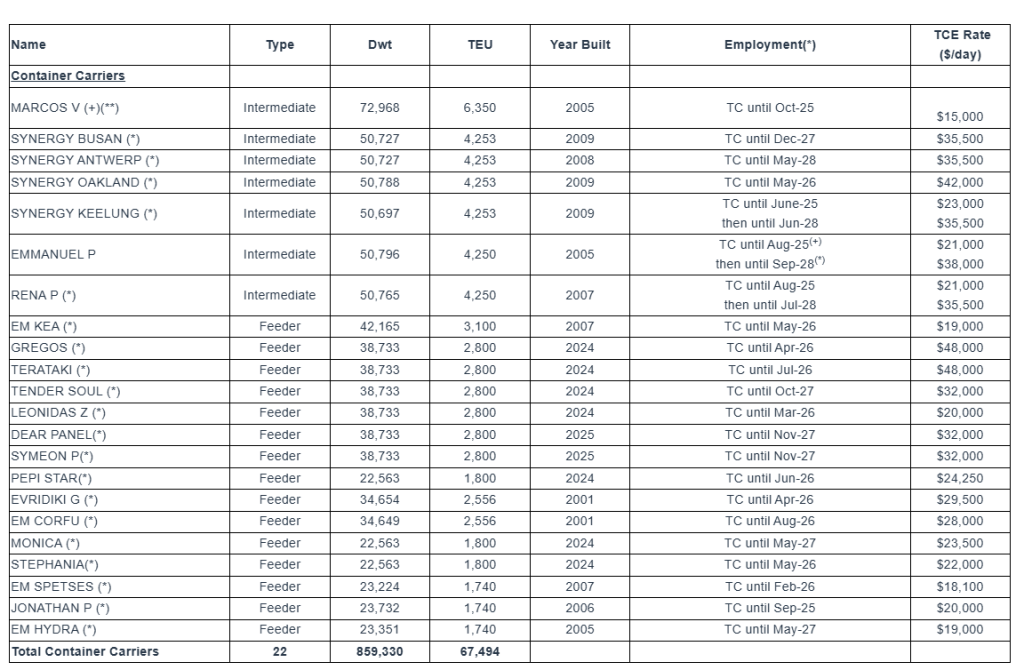

Fleet Profile: The Euroseas Ltd. fleet profile as of June 18, 2025 is as follows:

Summary Fleet Data:

(1) Average number of vessels is the number of vessels that constituted the Company’s fleet for the relevant period, as measured by the sum of the number of calendar days each vessel was a part of the Company’s fleet during the period divided by the number of calendar days in that period.

(2) Calendar days. We define calendar days as the total number of days in a period during which each vessel in our fleet was in our possession including off-hire days associated with major repairs, drydockings or special or intermediate surveys or days of vessels in lay-up. Calendar days are an indicator of the size of our fleet over a period and affect both the amount of revenues and the amount of expenses that we record during that period.

(3) The scheduled off-hire days including vessels laid-up, vessels committed for sale or vessels that suffered unrepaired damages, are days associated with scheduled repairs, drydockings or special or intermediate surveys or days of vessels in lay-up, or vessels that were committed for sale or suffered unrepaired damages.

(4) Available days. We define available days as the Calendar days in a period net of scheduled off-hire days as defined above. We use available days to measure the number of days in a period during which vessels were available to generate revenues.

(5) Commercial off-hire days. We define commercial off-hire days as days a vessel is idle without employment.

(6) Operational off-hire days. We define operational off-hire days as days associated with unscheduled repairs or other off-hire time related to the operation of the vessels.

(7) Voyage days. We define voyage days as the total number of days in a period during which each vessel in our fleet was in our possession net of commercial and operational off-hire days. We use voyage days to measure the number of days in a period during which vessels actually generate revenues or are sailing for repositioning purposes.

(8) Fleet utilization. We calculate fleet utilization by dividing the number of our voyage days during a period by the number of our available days during that period. We use fleet utilization to measure a company’s efficiency in finding suitable employment for its vessels and minimizing the amount of days that its vessels are off-hire for reasons such as unscheduled repairs or days waiting to find employment.

(9) Fleet utilization, commercial. We calculate commercial fleet utilization by dividing our available days net of commercial off-hire days during a period by our available days during that period.

(10) Fleet utilization, operational. We calculate operational fleet utilization by dividing our available days net of operational off-hire days during a period by our available days during that period.

(11) Time charter equivalent rate, or TCE, is a measure of the average daily net revenue performance of our vessels. Our method of calculating TCE is determined by dividing time charter revenue and voyage charter revenue, if any, net of voyage expenses by voyage days for the relevant time period. Voyage expenses primarily consist of port, canal and fuel costs that are unique to a particular voyage, which would otherwise be paid by the charterer under a time charter contract, or are related to repositioning the vessel for the next charter. TCE, which is a non-GAAP measure, provides additional meaningful information in conjunction with voyage revenues, the most directly comparable GAAP measure, because it assists our management in making decisions regarding the deployment and use of our vessels and because we believe that it provides useful information to investors regarding our financial performance. TCE is a standard shipping industry performance measure used primarily to compare period-to-period changes in a shipping company’s performance despite changes in the mix of charter types (i.e., spot voyage charters, time charters and bareboat charters) under which the vessels may be employed between the periods. Our definition of TCE may not be comparable to that used by other companies in the shipping industry.

(12) We calculate daily vessel operating expenses, which includes crew costs, provisions, deck and engine stores, lubricating oil, insurance, maintenance and repairs and related party management fees by dividing vessel operating expenses and related party management fees by fleet calendar days for the relevant time period. Drydocking expenses are reported separately.

(13) Daily general and administrative expenses are calculated by us by dividing general and administrative expenses by fleet calendar days for the relevant time period.

(14) Total vessel operating expenses, or TVOE, is a measure of our total expenses associated with operating our vessels. TVOE is the sum of vessel operating expenses, related party management fees and general and administrative expenses; drydocking expenses are not included. Daily TVOE is calculated by dividing TVOE by fleet calendar days for the relevant time period.

(15) Daily drydocking expenses is calculated by us by dividing drydocking expenses by the fleet calendar days for the relevant period, Drydocking expenses include expenses during drydockings that would have been capitalized and amortized under the deferral method. Drydocking expenses could vary substantially from period to period depending on how many vessels underwent drydocking during the period. The Company expenses drydocking expenses as incurred.

Conference Call and Webcast: Today, Wednesday, June 18, 2025 at 09:30 a.m. Eastern Time, the Company’s management will host a conference call and webcast to discuss the results.

Conference Call details: Participants should dial into the call 10 minutes before the scheduled time using the following numbers: 877 405 1226 (US Toll-Free Dial In) or +1 201 689 7823 (US and Standard International Dial In). Please quote “Euroseas” to the operator and/or conference ID 13754421. Click here for additional participant International Toll -Free access numbers.

Alternatively, participants can register for the call using the call me option for a faster connection to join the conference call. You can enter your phone number and let the system call you right away. Click here for the call me option.

Audio Webcast – Slides Presentation: There will be a live and then archived webcast of the conference call and accompanying slides, available on the Company’s website. To listen to the archived audio file, visit our website http://www.euroseas.gr and click on Company Presentations under our Investor Relations page. Participants to the live webcast should register on the website approximately 10 minutes prior to the start of the webcast.

The slide presentation for the first quarter ended March 31, 2025, will also be available in PDF format minutes prior to the conference call and webcast, accessible on the company’s website (www.euroseas.gr) on the webcast page. Participants to the webcast can download the PDF presentation.

Adjusted EBITDA Reconciliation:

Euroseas Ltd. considers Adjusted EBITDA to represent net income before interest and other financing costs, income taxes, depreciation, (gain) / loss on interest rate swap derivative, net, gain on sale of vessel, and amortization of fair value of below market time charters acquired. Adjusted EBITDA does not represent and should not be considered as an alternative to net income, as determined by United States generally accepted accounting principles, or GAAP. Adjusted EBITDA is included herein because it is a basis upon which the Company assesses its financial performance and liquidity position and because the Company believes that this non-GAAP financial measure assists our management and investors by increasing the comparability of our performance from period to period by excluding the potentially disparate effects between periods of financial costs, loss / (gain) on interest rate swaps, gain on sale of vessel, depreciation, and amortization of below market time charters acquired. The Company’s definition of Adjusted EBITDA may not be the same as that used by other companies in the shipping or other industries.

Adjusted net income and Adjusted earnings per share Reconciliation: Euroseas Ltd. considers Adjusted net income to represent net income before unrealized (gain) / loss on derivative, gain on sale of vessel, amortization of below market time charters acquired and vessel depreciation on the portion of the consideration of vessels acquired with attached time charters allocated to below market time charters. Adjusted net income and Adjusted earnings per share are included herein because we believe they assist our management and investors by increasing the comparability of the Company’s fundamental performance from period to period by excluding the potentially disparate effects between periods of the aforementioned items, which may significantly affect results of operations between periods.

Adjusted net income and Adjusted earnings per share do not represent and should not be considered as an alternative to net income or earnings per share, as determined by GAAP. The Company’s definition of Adjusted net income and Adjusted earnings per share may not be the same as that used by other companies in the shipping or other industries. Adjusted net income and Adjusted earnings per share are not adjusted for all non-cash income and expense items that are reflected in our statement of cash flows.

About Euroseas Ltd. Euroseas Ltd. was formed on May 5, 2005 under the laws of the Republic of the Marshall Islands to consolidate the ship owning interests of the Pittas family of Athens, Greece, which has been in the shipping business over the past 140 years. Euroseas trades on the NASDAQ Capital Market under the ticker ESEA.

Euroseas operates in the container shipping market. Euroseas’ operations are managed by Eurobulk Ltd., an ISO 9001:2008 and ISO 14001:2004 certified affiliated ship management company, which is responsible for the day-to-day commercial and technical management and operations of the vessels. Euroseas employs its vessels on spot and period charters and through pool arrangements.

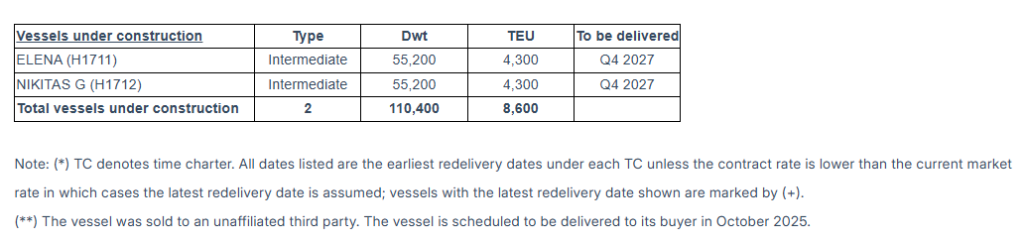

The Company has a fleet of 22 vessels, including 15 Feeder containerships and 7 Intermediate containerships. Euroseas 22 containerships have a cargo capacity of 67,494 teu. After the delivery of two intermediate containership newbuildings in the fourth quarter of 2027, Euroseas’ fleet will consist of 24 vessels with a total carrying capacity of 76,094 teu.

Forward Looking Statement This press release contains forward-looking statements (as defined in Section 27A of the Securities Act of 1933, as amended, and Section 21E of the Securities Exchange Act of 1934, as amended) concerning future events and the Company’s growth strategy and measures to implement such strategy; including expected vessel acquisitions and entering into further time charters. Words such as “expects,” “intends,” “plans,” “believes,” “anticipates,” “hopes,” “estimates,” and variations of such words and similar expressions are intended to identify forward-looking statements. Although the Company believes that the expectations reflected in such forward-looking statements are reasonable, no assurance can be given that such expectations will prove to have been correct. These statements involve known and unknown risks and are based upon a number of assumptions and estimates that are inherently subject to significant uncertainties and contingencies, many of which are beyond the control of the Company. Actual results may differ materially from those expressed or implied by such forward-looking statements. Factors that could cause actual results to differ materially include, but are not limited to changes in the demand for containerships, competitive factors in the market in which the Company operates; risks associated with operations outside the United States; and other factors listed from time to time in the Company’s filings with the Securities and Exchange Commission. The Company expressly disclaims any obligations or undertaking to release publicly any updates or revisions to any forward-looking statements contained herein to reflect any change in the Company’s expectations with respect thereto or any change in events, conditions or circumstances on which any statement is based.

Agreement to support future studies investigating the combination of ateganosine and atezolizumab for safe and effective cancer treatments

CHICAGO–(BUSINESS WIRE)– MAIA Biotechnology, Inc. (NYSE American: MAIA), a clinical-stage biopharmaceutical company focused on developing targeted immunotherapies for cancer, today announced its entry into a clinical master supply agreement with Roche for future studies investigating the combination of MAIA’s telomere-targeting agent ateganosine (THIO), sequenced with Roche’s checkpoint inhibitor (CPI), atezolizumab (Tecentriq®), for the treatment of multiple hard-to-treat cancers.

“In preclinical studies, ateganosine was found to be highly synergistic and effective in combination with Roche’s anti-PD-L1 agent atezolizumab,” said MAIA Chairman and CEO Vlad Vitoc, M.D. “We are pleased to partner with world-renowned Roche and we look forward to further strengthening our mission to find safe and effective cancer treatments.”

About Ateganosine

Ateganosine (THIO, 6-thio-dG or 6-thio-2’-deoxyguanosine) is a first-in-class investigational telomere-targeting agent currently in clinical development to evaluate its activity in non-small cell lung cancer (NSCLC). Telomeres, along with the enzyme telomerase, play a fundamental role in the survival of cancer cells and their resistance to current therapies. The modified nucleotide 6-thio-2’-deoxyguanosine induces telomerase-dependent telomeric DNA modification, DNA damage responses, and selective cancer cell death. Ateganosine-damaged telomeric fragments accumulate in cytosolic micronuclei and activate both innate (cGAS/STING) and adaptive (T-cell) immune responses. The sequential treatment with ateganosine followed by PD-(L)1 inhibitors resulted in profound and persistent tumor regression in advanced, in vivo cancer models by induction of cancer type–specific immune memory. Ateganosine is presently developed as a second or later line of treatment for NSCLC for patients that have progressed beyond the standard-of-care regimen of existing checkpoint inhibitors.

About MAIA Biotechnology, Inc.

MAIA is a targeted therapy, immuno-oncology company focused on the development and commercialization of potential first-in-class drugs with novel mechanisms of action that are intended to meaningfully improve and extend the lives of people with cancer. Our lead program is ateganosine (THIO), a potential first-in-class cancer telomere targeting agent in clinical development for the treatment of NSCLC patients with telomerase-positive cancer cells. For more information, please visit www.maiabiotech.com.

Tecentriq® (atezolizumab) is a registered trademark of Genentech, a member of the Roche Group.

Forward-Looking Statements

MAIA cautions that all statements, other than statements of historical facts contained in this press release, are forward-looking statements. Forward-looking statements are subject to known and unknown risks, uncertainties, and other factors that may cause our or our industry’s actual results, levels or activity, performance or achievements to be materially different from those anticipated by such statements. The use of words such as “may,” “might,” “will,” “should,” “could,” “expect,” “plan,” “anticipate,” “believe,” “estimate,” “project,” “intend,” “future,” “potential,” or “continue,” and other similar expressions are intended to identify forward-looking statements. However, the absence of these words does not mean that statements are not forward-looking. For example, all statements we make regarding (i) the initiation, timing, cost, progress and results of our preclinical and clinical studies and our research and development programs, (ii) our ability to advance product candidates into, and successfully complete, clinical studies, (iii) the timing or likelihood of regulatory filings and approvals, (iv) our ability to develop, manufacture and commercialize our product candidates and to improve the manufacturing process, (v) the rate and degree of market acceptance of our product candidates, (vi) the size and growth potential of the markets for our product candidates and our ability to serve those markets, and (vii) our expectations regarding our ability to obtain and maintain intellectual property protection for our product candidates, are forward looking. All forward-looking statements are based on current estimates, assumptions and expectations by our management that, although we believe to be reasonable, are inherently uncertain. Any forward-looking statement expressing an expectation or belief as to future events is expressed in good faith and believed to be reasonable at the time such forward-looking statement is made. However, these statements are not guarantees of future events and are subject to risks and uncertainties and other factors beyond our control that may cause actual results to differ materially from those expressed in any forward-looking statement. Any forward-looking statement speaks only as of the date on which it was made. We undertake no obligation to publicly update or revise any forward-looking statement, whether as a result of new information, future events or otherwise, except as required by law. In this release, unless the context requires otherwise, “MAIA,” “Company,” “we,” “our,” and “us” refers to MAIA Biotechnology, Inc. and its subsidiaries.

500 5th Avenue 20th Floor New York, NY 10110 United States Sector(s): Consumer Cyclical Industry: Apparel Manufacturing Full Time Employees: 599 Key Executives Name Title Pay Exercised Year Born Mr. Jonathan CEO & Director 825.62k N/A 1958 Ms. Marie Fogel Senior VP and Chief Merchandising & Manufacturing Officer 633.19k N/A 1961 Mr. John Chief Financial Officer

Michael Kupinski, Director of Research, Equity Research Analyst, Digital, Media & Technology , Noble Capital Markets, Inc.

Jacob Mutchler, Research Associate, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

Solid Q1 results. the company reported Q1 revenue of $57.9 million and an adj. EBITDA loss of $3.0 million, both of which were better than our estimates of $56.0 million and a loss of $5.5 million, respectively. Notably, while revenue and adj. EBITDA are both modestly lower than the prior year period; we view the Q1 results favorably, given the company’s ability to manage the uncertain tariff outlook.

Tariff mitigation. The company highlighted that it has been taking steps to reduce its exposure to China, currently roughly 60% of its cost of goods sold. Notably, the company is sourcing from other countries and expects that China will be roughly 25% of its cost of goods by the end of 2025. The company has leadership located in the sourcing countries to ensure product quality.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

Patrick McCann, CFA, Research Analyst, Noble Capital Markets, Inc.

Michael Kupinski, Director of Research, Equity Research Analyst, Digital, Media & Technology , Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

Highlights from Noble’s Emerging Growth Virtual Conference. Vijay Kotte, CEO, presented at Noble’s Virtual Equity conference June 4 & 5th. Mr. Kotte highlighted the company’s proprietary technology, consumer-centric Medicare policy platform, and gave an update on recent developments. A rebroadcast is available here.

Purpose-built technology. Mr. Kotte emphasized the company’s use of proprietary machine learning tools alongside licensed agents to tailor recommendations to each consumer’s needs. With Medicare beneficiaries typically choosing from 40–50 plans, this technology plays a key role in efficiently identifying the most suitable options.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

The Federal Reserve held interest rates steady on Wednesday for the fourth consecutive meeting, keeping its benchmark rate in the range of 4.25% to 4.5% and reaffirming its forecast for two interest rate cuts before the end of 2025. The decision, which was supported unanimously by the Federal Open Market Committee, underscores the central bank’s cautious approach as it navigates a complex economic environment shaped by persistent inflation, slower growth expectations, and growing political pressure from the Trump administration.

Despite recent signs that inflation has eased modestly, the Fed raised its inflation outlook for the year. Officials now expect core PCE inflation, the central bank’s preferred metric, to end 2025 at 3.1%, up from a previous estimate of 2.8%. That adjustment reflects concerns that tariffs and other policy shifts under President Trump’s administration may continue to elevate prices and complicate the Fed’s path to achieving its 2% inflation target. At the same time, economic growth projections were lowered, with the Fed now anticipating annual GDP growth of 1.4%, down from 1.7%. The unemployment rate is also expected to climb slightly, from 4.4% to 4.5%, signaling a potential slowdown in the labor market as higher borrowing costs weigh on hiring and business investment.

The Fed’s statement noted that “uncertainty about the economic outlook has diminished, but remains elevated,” marking a shift in tone from earlier warnings that uncertainty was rising. While this change suggests that some risks may be stabilizing, policymakers remain sharply divided over the appropriate course of action. Eight officials project two rate cuts this year, while seven expect no cuts at all. Two members see a single cut, and two others anticipate as many as three. This internal split reflects the complexity of balancing inflation management with support for economic growth, particularly in a volatile political climate.

President Trump, who has been increasingly vocal in his criticism of Fed Chair Jerome Powell, once again expressed dissatisfaction with the central bank’s approach. Hours before the rate announcement, Trump took aim at Powell in front of reporters, joking that he might appoint himself to the Fed, claiming, “Maybe I should go to the Fed; I’d do a much better job.” He continued his push for lower rates by declaring that inflation is no longer a concern, stating, “We have no inflation, we have only success.” This political pressure has not gone unnoticed, but Powell and other Fed officials appear focused on maintaining their independence and credibility by anchoring decisions in economic data rather than political narratives.

Markets responded calmly to the announcement, with the S&P 500 rising 0.18% and the Dow Jones Industrial Average gaining 0.21%. Investors largely interpreted the Fed’s decision as a sign that rate cuts remain on the table, just not at the pace the White House may want. For now, the Fed continues to walk a careful line, seeking to bring inflation down without derailing a fragile recovery. With just months left in the year and political tensions rising, all eyes will remain on Powell and the FOMC as they weigh their next move.

ATLANTA, June 17, 2025 (GLOBE NEWSWIRE) — DLH Holdings Corp. (NASDAQ: DLHC) (“DLH” or the “Company”), a leading provider of science research and development, systems engineering and integration, and digital transformation and cybersecurity solutions announced today that three DLH solutions developed in collaboration with military health leadership have been named 2025 FORUM Innovation Award winners.

Each year, the FORUM Innovation Awards recognize top IT programs nominated and selected by their peers for pushing the technology envelope, showcasing breakthrough innovation, and rewarding the leadership and teamwork that improve and advance each agency’s mission.

“DLH and our partners in the military health community operate at the leading-edge of scientific discovery and technological innovation,” said Zach Parker, DLH President and CEO. “Each of these award-winning projects demonstrate the life-saving impact that the work of our data scientists, engineers, and health experts has on Warfighter readiness.”

The 2025 FORUM Innovation Award winners are:

Telerobotic Operator Network (TRON) – DHA MRDC TATRC

TRON is a groundbreaking initiative which allows surgeons to operate on patients located far away by combining virtual reality, digital twin, AI, and robotics. With this technology, doctors and medics can remotely provide vital care on wounded Warfighters operating in hazardous conditions that would ordinarily make treatment nearly impossible.

AutoDoc – DHA MRDC TATRC

Collecting accurate, actionable data is central to developing life-saving automated casualty care solutions, but data collection at the point of care typically requires caregivers to stop providing treatment for the sake of documentation. Automating Documentation (“AutoDoc”) delivers a suite of sensors that passively collect accurate and reliable data on patients and medics in challenging operational environments and high stress situations – allowing medics to focus on the vital care they are providing.

Joint Patient Safety Reporting (JPSR) – DHA PEO Medical Systems, DADIO/J-6

Accurate, comprehensive event reporting is crucial for patient safety, but Warfighter health data is often partitioned between the Defense Health Agency (“DHA”) and Department of Veterans Affairs (“VA”). JPSR securely integrates patient health data into a single system for quantitative and comparative data analysis, including customizable analytical tools, reports, and dashboards which allow for at-a-glance monitoring, measuring, and analysis. This unified system gives caregivers the full visibility they need.

“For over twenty years, DLH has joined forces with military partners to drive research and development, including integrating AI/ML technologies, autonomous medical systems, and interoperable telemedicine platforms,” said Mary Dowdall, President, Advanced Mission Solutions. “These awards demonstrate the value of our enduring collaboration and demonstrate our company’s ability to execute at the nexus of science and technology.”

About DLH

DLH (NASDAQ: DLHC), a Russell 2000 company, enhances technology, public health, and cyber security readiness missions through science, technology, cyber, and engineering solutions and services. Our experts solve some of the most complex and critical missions faced by customers today, leveraging digital transformation, artificial intelligence, advanced analytics, cloud-based applications, telehealth systems, and more. With over 2,400 employees dedicated to the idea that “Your Mission is Our Passion,” DLH brings a unique combination of technology, innovation, and world-class expertise to improve lives across the globe. For more information, visit www.DLHcorp.com.

INVESTOR RELATIONS Contact: Chris Witty Phone: 646-438-9385 Email: cwitty@darrowir.com