Key Points: – The Consumer Price Index (CPI) rose 2.8% year-over-year in February, with food, medical care, and auto costs still climbing. – A dozen large Grade A eggs now average $5.90, up 59% from a year ago. – Inflation remains above the Fed’s 2% target, likely delaying any interest rate cuts.

American consumers continue to feel the sting of stubborn inflation as essential goods and services remain costly despite an overall slowdown in price growth. The latest Consumer Price Index (CPI) report showed a 2.8% year-over-year increase in February, a slight cooling from previous months but still well above the Federal Reserve’s 2% target.

One of the most notable price hikes continues to be in food costs, particularly for eggs. A dozen large Grade A eggs averaged $5.90 in February, a staggering 59% increase from a year ago. Other breakfast staples like coffee and bacon have also risen, adding to household grocery bills. While some categories, such as fruits and vegetables, saw modest declines, overall grocery prices remain elevated. Eating out is also becoming more expensive, with restaurant prices climbing 3.7% over the past year.

Medical expenses are another growing burden for consumers, with hospital costs up 3.6% year-over-year and nursing home care rising by 4.1%. Home healthcare costs surged 5.6%, reflecting the increasing demand for in-home medical services. Meanwhile, health insurance premiums climbed 3.9%, further squeezing household budgets already stretched thin by higher living costs.

The rising costs extend beyond healthcare and food, impacting transportation as well. Used car prices, which had been easing in previous months, surged again by 2.2% in January and another 0.9% in February. Auto insurance, a major expense for many households, has increased nearly 11% over the past year. Insurers continue to raise premiums as they struggle with underwriting losses, which have persisted for three consecutive years. However, there was some relief at the gas pump, with gasoline prices dipping slightly to a national average of $3.08 per gallon as of mid-March, down from $3.39 a year ago.

With inflation still running above target, the Federal Reserve faces a difficult decision in the coming months. The central bank has signaled that it will likely keep interest rates steady at its next policy meeting, as economic uncertainty surrounding tariffs and supply chain disruptions remains a concern. The Fed’s cautious stance reflects the balancing act it must perform—ensuring inflation continues to cool while avoiding any moves that could trigger a broader economic slowdown.

For consumers, the persistence of high prices across essential categories underscores the challenges of managing household budgets in this inflationary environment. While some areas, such as gasoline and certain food items, have seen modest relief, overall costs remain elevated. Policymakers will continue monitoring inflation trends closely, but for now, Americans should brace for continued financial strain as they navigate these price increases.

Saga Communications, Inc. is a broadcast company whose business is primarily devoted to acquiring, developing and operating radio stations. Saga currently owns or operates broadcast properties in 27 markets, including 79 FM and 33 AM radio stations. Saga’s strategy is to operate top billing radio stations in mid sized markets, defined as markets ranked (by market revenues) from 20 to 200. Saga’s radio stations employ a myriad of programming formats, including Active Rock, Adult Album Alternative, Adult Contemporary, Country, Classic Country, Classic Hits, Classic Rock, Contemporary Hits Radio, News/Talk, Oldies and Urban Contemporary. In operating its stations, Saga concentrates on the development of strong decentralized local management, which is responsible for the day-to-day operations of the stations in their market area and is compensated based on their financial performance as well as other performance factors that are deemed to effect the long-term ability of the stations to achieve financial objectives. Saga began operations in 1986 and became a publicly traded company in December 1992. The stock trades on NASDAQ under the ticker symbol “SGA”.

Michael Kupinski, Director of Research, Equity Research Analyst, Digital, Media & Technology , Noble Capital Markets, Inc.

Jacob Mutchler, Research Associate, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

An in-line quarter. The company reported Q4 revenue of $28.8 million and adj. EBITDA of $3.1 million, both of which declined over the prior year period, but were modestly better than our estimates of $27.7 million and $2.3 million, respectively. Notably, the company is focused on its blended digital growth strategy and reducing costs and improving profitability. We believe the company’s strategic actions are a step in the right direction for returning toward revenue and adj. EBITDA growth.

Cost-effective digital growth strategy. A key focus of the company is reducing costs that have no impact on revenue and continuing to emphasize the roll out of its blended digital advertising strategy. Notably, the blended strategy combines radio and digital advertising to provide a consistent message to customers on both mediums and to drive radio listeners to digital platforms. We view the company’s emphasis on the unique strategy favorably.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

The E.W. Scripps Company (NASDAQ: SSP) is a diversified media company focused on creating a better-informed world. As one of the nation’s largest local TV broadcasters, Scripps serves communities with quality, objective local journalism and operates a portfolio of 61 stations in 41 markets. The Scripps Networks reach nearly every American through the national news outlets Court TV and Newsy and popular entertainment brands ION, Bounce, Defy TV, Grit, ION Mystery, Laff and TrueReal. Scripps is the nation’s largest holder of broadcast spectrum. Scripps runs an award-winning investigative reporting newsroom in Washington, D.C., and is the longtime steward of the Scripps National Spelling Bee. Founded in 1878, Scripps has held for decades to the motto, “Give light and the people will find their own way.”

Michael Kupinski, Director of Research, Equity Research Analyst, Digital, Media & Technology , Noble Capital Markets, Inc.

Jacob Mutchler, Research Associate, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

Q4 results exceed expectations. Revenues increased a strong 18.3% to $728.4 million, beating our $716.1 million estimate. The results benefited from better core advertising ($147.4 million vs our $143.0 million est.) and higher Political revenue ($174.4 million vs our $172.0 million est.). Adj. EBITDA was $229.6 million, better than our $226.1 million estimate. Figure #1 Q4 Results highlight our estimates versus reported results.

Sluggish start. Management provided lackluster Q1 revenue guidance, expecting Local Media revenue to be down high single- digits with Scripps Networks revenue to be down mid single-digits. The sluggish Q1 reflects the absence of Political revenue, but likely weak core spot and National spot advertising. Notably, management guided interest expense to be $175 million to $185 million, less than our estimate of roughly $200 million.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

Joe Gomes, CFA, Managing Director, Equity Research Analyst, Generalist , Noble Capital Markets, Inc.

Joshua Zoepfel, Research Associate, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

4Q Results. CVG reported 4Q24 revenue of $163.3 million, down 15.7% y-o-y due to ongoing weakness in the Construction and Ag markets, as well as a drop in Class 8 truck builds. Adjusted EBITDA was $0.9 million, down from $8.3 million. CVG reported an adjusted loss from continuing operations of $5.1 million, or a loss of $0.15/sh, compared to adjusted net income of $2.1 million, or EPS of $0.06, in 4Q23.

Strategic Initiatives. The Company implemented a number of strategic initiatives during 2024, including portfolio rationalization and the elimination of some 1,300 positions. These should result in some $15 million of gross savings in 2025, which should help improve margins.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

Key Points: – BMS is acquiring 2seventy bio for $5.00 per share, an 88% premium to its last closing price. – The deal strengthens BMS’s cell and gene therapy portfolio, particularly in multiple myeloma treatment. – The acquisition comes amid increased M&A activity in biotech, signaling confidence in the sector’s long-term potential.

Bristol Myers Squibb (BMY) has announced a definitive agreement to acquire 2seventy bio (TSVT) in an all-cash deal valued at approximately $286 million. This acquisition further strengthens BMS’s foothold in the oncology space, particularly through its access to Abecma, an FDA-approved CAR T-cell therapy for multiple myeloma. The deal is expected to close in the second quarter of 2025, pending regulatory approvals and shareholder consent.

BMS’s acquisition of 2seventy bio aligns with its broader strategy to expand its presence in the high-growth cell and gene therapy market. 2seventy bio has focused exclusively on Abecma, a treatment developed in collaboration with BMS, to extend and improve the lives of patients with relapsed or refractory multiple myeloma. With this acquisition, BMS will take full control of Abecma’s commercialization and development, streamlining operations and potentially accelerating future advancements.

Chip Baird, CEO of 2seventy bio, emphasized the significance of the transaction, stating: “This acquisition ensures Abecma continues to reach patients in need while maximizing value for our stakeholders.” BMS, with its expansive resources and global reach, is well-positioned to drive further innovation in the cell therapy space.

The biotech sector has seen a resurgence in M&A activity, with pharmaceutical giants seeking to bolster their pipelines amid ongoing scientific advancements and a challenging regulatory landscape. The acquisition of 2seventy bio comes at a time when investors are looking for signs of stability in biotech, and deals like this reinforce confidence in the sector’s long-term growth potential.

The broader biotechnology sector, as measured by the iShares Biotechnology ETF (IBB), has posted gains year-to-date, reflecting renewed investor interest in the space. As larger pharmaceutical companies look to capitalize on cutting-edge therapies, small and mid-cap biotech firms with promising assets are becoming increasingly attractive acquisition targets. The deal values 2seventy bio at a significant premium, rewarding shareholders with an 88% increase from its prior trading price. However, it also raises questions about the long-term independence of innovative biotech firms. While consolidation can lead to greater efficiency and resource allocation, it may also reduce competition and limit the number of standalone biotech companies driving early-stage innovation.

For BMS, the acquisition is a strategic move to reinforce its oncology pipeline amid growing competition in the CAR T-cell therapy space. With this deal, BMS is betting on continued demand for personalized cell-based therapies and positioning itself to lead in this evolving field. Biotech acquisitions are often driven by the need for pharmaceutical companies to secure new revenue streams as patents on existing drugs expire. By acquiring 2seventy bio, BMS gains a competitive advantage in the high-value oncology segment, ensuring its ability to remain a dominant force in the industry.

Bristol Myers Squibb’s acquisition of 2seventy bio represents a significant development in the biotech sector. As M&A activity accelerates, the deal underscores the importance of targeted therapies in oncology and highlights the ongoing push by pharmaceutical giants to secure cutting-edge treatments. For investors, this acquisition may serve as a signal that biotech remains a strong sector, with potential for both innovation and consolidation in the years ahead.

Key Points: – The Russell 2000 is down 2.8% for the day but remains up 9.55% year-to-date, while the NASDAQ-100 is down 4.3% for the day and 10% for the year. – The Volatility Index (VIX) is at elevated levels, signaling increased investor uncertainty. – While growth stocks face sell-offs, value stocks have shown relative resilience

The current market environment is one defined by stark contrasts. On one hand, major indices are faltering, led by a steep sell-off in technology stocks. The NASDAQ-100, once the pillar of market growth, is now in free fall, weighed down by declining FAANG stocks. Investors who previously viewed these stocks as untouchable are now reassessing their portfolios amid shifting economic conditions and concerns over stretched valuations.

At the same time, small-cap value stocks—often overlooked in favor of high-flying growth names—are quietly proving their resilience. While the iShares Morningstar Small-Cap Value ETF (ISCV) is down 3.7% year-to-date, this decline is minor compared to the broader indices. Historically, small-cap value stocks have shown their ability to outperform in recovery phases following market downturns, and many investors are beginning to recognize their potential.

What’s Driving the Shift Toward Value?

For years, growth stocks dominated, fueled by ultra-low interest rates and a market environment that rewarded future earnings potential over present fundamentals. That equation is shifting. With inflation concerns persisting and central banks maintaining a cautious approach to monetary policy, investors are prioritizing stability, profitability, and tangible value over speculative bets.

Warren Buffett’s move to trim his exposure to large-cap tech stocks speaks volumes about the changing investment landscape. Buffett, long known for his disciplined approach to investing, has historically favored companies with strong balance sheets, consistent earnings, and reasonable valuations. The fact that he is reducing positions in FAANG stocks suggests that even legendary investors see potential trouble ahead for high-growth names.

The Case for Small-Cap Value Stocks

Why should investors pay attention to small-cap value stocks right now? One key reason is valuation. While growth stocks have commanded high price-to-earnings (P/E) multiples, small-cap value stocks remain attractively priced, often trading at a discount relative to their historical averages. Additionally, many of these companies are less dependent on global economic conditions and trade policies, making them more insulated from external shocks.

Another factor is performance in post-recession recoveries. Historically, small-cap stocks tend to outperform large-cap stocks after periods of economic turmoil. When investor sentiment shifts and risk appetite returns, small-cap value stocks often experience significant upside, benefiting from their relatively lower valuations and higher growth potential.

Conclusion

The current market turbulence is forcing investors to rethink their strategies. While growth stocks, particularly in the tech sector, face continued headwinds, small-cap value stocks offer a compelling alternative for those seeking stability and potential upside. History suggests that in times of market uncertainty, companies with strong fundamentals and reasonable valuations often emerge as winners. While risks remain, the shift toward value is already underway—and small caps may be poised to shine in the months ahead.

By The Comtech Editorial Team – Mar 11, 2025 | 2 min read

CHANDLER, Ariz. – March, 11 2025– Comtech Telecommunications Corp. (NASDAQ: CMTL) (“Comtech” or the “Company”), a global communications technology leader, today announced that it plans to release its second quarter fiscal 2025 results after the market closes on Wednesday, March 12, 2025.

Following the release of the second quarter fiscal 2025 financial results, Comtech’s leadership team invites shareholders, potential shareholders, and other interested parties to join a conference call at 5:00 p.m. ET on Wednesday, March 12, to discuss the Company’s results, operations, and business trends.

A real-time webcast of the call will be available to the public at the investor relations section of the Comtech web site at www.comtech.com. Alternatively, investors can access the conference call by dialing (800) 274-8461 (primary) or (203) 518-9814 (alternate) and using the conference ID “Comtech.” A replay of the call will be available until Wednesday, March 19, by dialing (800) 938-2241 or (402) 220-1121.

About Comtech

Comtech Telecommunications Corp. is a leading provider of satellite and space communications technologies; terrestrial and wireless network solutions; Next Generation 911 (NG911) and emergency services; and cloud native capabilities to commercial and government customers around the world. Through its culture of innovation and employee empowerment, Comtech leverages its global presence and decades of technology leadership and experience to create some of the world’s most innovative solutions for mission-critical communications. For more information, please visit www.comtech.com.

Forward-Looking Statements

Certain information in this press release contains statements that are forward-looking in nature and involve certain significant risks and uncertainties. Actual results and performance could differ materially from such forward-looking information. The Company’s Securities and Exchange Commission filings identify many such risks and uncertainties. Any forward-looking information in this press release is qualified in its entirety by the risks and uncertainties described in such Securities and Exchange Commission filings.

Partnership to elevate guest experience through supply of premium terry cloth towels and bedding

BOCA RATON, Fla.–(BUSINESS WIRE)–Mar. 11, 2025– ODP Business Solutions, a leading supplier of workplace solutions and services and a division of The ODP Corporation (NASDAQ: ODP), today announced a new distribution partnership with luxury linens and terry cloth towels brand Sobel Westex, signaling continued growth in the hospitality sector. This collaboration positions ODP Business Solutions as a key supplier for in-room needs, reinforcing its commitment to delivering premium products and services across diverse sectors.

“This partnership exemplifies our commitment to driving growth in the hospitality sector while demonstrating our ability to deliver trusted brands and products across diverse industries, extending beyond office supplies,” said David Centrella, executive vice president of The ODP Corporation and president of ODP Business Solutions. “By integrating Sobel Westex’s renowned luxury bedding and terry cloth towels into our portfolio, we’re not just meeting but exceeding the expectations of our clients.”

Sobel Westex is a leading global hospitality and retail textile company known for its commitment to quality, innovation and sustainability. Through ODP Business Solutions’ expansive customer roster and logistic infrastructure, Sobel Westex will now provide their comprehensive range of hospitality products that extend far beyond the traditional, offering premium pillows, plush terry towels, high-quality linens, blankets, pool towels and spa-like robes, all designed to create a luxurious and inviting atmosphere.

“When we look at this new partnership with ODP Business Solutions, we know it will be a transformative venture for both of our companies and can change the hospitality industry as we know it. Their exceptional distribution expertise and extensive customer network make it an easy decision to trust them with our product portfolio,” said Walter Pelaez, chief executive officer at Sobel Westex.

Sobel Westex’s offerings are all crafted from high-quality materials like premium cotton, ensuring temperature regulation and superior comfort, durability and luxury across their entire product line. Their commitment to excellence is reflected in products that are meticulously crafted to provide unparalleled comfort and sophistication, catering to travelers who expect the finest hospitality experiences.

“Introducing Sobel Westex’s luxury products to our hospitality distribution services allows us to offer our customers the opportunity to create truly memorable guest experiences,” said Nisha Brown, vice president of marketing & product management at ODP Business Solutions. “From crisp, high-quality sheets to plush, indulgent bedding, superior linens provide weary travelers with the comfort they crave, transforming a night’s rest into a truly rejuvenating experience. This partnership aligns perfectly with our commitment to delivering trusted brands and extraordinary products across all industries we serve.”

This partnership announcement follows ODP Business Solutions’ recent milestone agreement with a leading hospitality management company, becoming a key supplier and distribution partner. ODP Business Solutions will continue delivering high-quality solutions in traditional product categories, including furniture, professional cleaning and breakroom, while expanding into new categories to better serve the needs of its hospitality customers and customers across other verticals.

ODP Business Solutions is a trusted partner with more than 30 years of experience working with businesses to adapt to the ever-changing world of work. From technology transformation, sustainability, innovative workspace design, cleaning and breakroom, and everything in between, ODP Business Solutions has the integrated products and services businesses need. Powered by a collaborative team of experienced business consultants, world-class logistics and trusted brand names, ODP Business Solutions advances how the working world gets work done. For more information on ODP Business Solutions, visit www.odpbusiness.com.

ODP Business Solutions is a division of The ODP Corporation (NASDAQ: ODP). ODP and ODP Business Solutions are trademarks of ODP Business Solutions, LLC. Any other product or company names mentioned herein are the trademarks of their respective owners.

About Sobel Westex:

Sobel Westex is the leading manufacturer to the hospitality and home fashion industry globally. Sobel Westex has successfully integrated design, manufacturing and distribution around the world. The company provides their clients with the highest quality experiences for bed linens, terry, robes, blankets, pillows and beyond. Sobel Westex’s wealth of products is equaled only by their depth of experience and service, which is why they measure their partnerships not in years, but in decades. For more information on Sobel Westex or to contact a representative, visit www.sobelathome.com.

About The ODP Corporation

The ODP Corporation (NASDAQ:ODP) is a leading provider of products and services through an integrated business-to-business (B2B) distribution platform and omnichannel presence, which includes world-class supply chain and distribution operations, dedicated sales professionals, online presence and a network of Office Depot and OfficeMax retail stores. Through its operating companies Office Depot, LLC; ODP Business Solutions, LLC; and Veyer, LLC, The ODP Corporation empowers every business, professional, and consumer to achieve more every day. For more information, visit theodpcorp.com.

This communication may contain forward-looking statements within the meaning of the Private Securities Litigation Reform Act of 1995. These statements or disclosures may discuss goals, intentions and expectations as to future trends, plans, events, results of operations, cash flow or financial condition, or state other information relating to, among other things, The ODP Corporation (“the Company”), based on current beliefs and assumptions made by, and information currently available to, management. Forward-looking statements generally will be accompanied by words such as “anticipate,” “believe,” “plan,” “could,” “estimate,” “expect,” “forecast,” “guidance,” “expectations”, “outlook,” “intend,” “may,” “possible,” “potential,” “predict,” “project,” “propose” “aim” or other similar words, phrases or expressions, or other variations of such words. These forward-looking statements are subject to various risks and uncertainties, many of which are outside of the Company’s control. There can be no assurances that the Company will realize these expectations or that these beliefs will prove correct, and therefore investors and stakeholders should not place undue reliance on such statements.

Investors and shareholders should carefully consider the foregoing factors and the other risks and uncertainties described in the Company’s Annual Reports on Form 10-K, Quarterly Reports on Form 10-Q, and Current Reports on Form 8-K filed with the U.S. Securities and Exchange Commission. The Company does not assume any obligation to update or revise any forward-looking statements.

RESTON, Va., March 11, 2025 /PRNewswire/ — V2X, Inc. (NYSE: VVX) was awarded a new $100 million contract to support the U.S. Navy’s Aegis Ashore facilities in Poland. These facilities are a crucial component of NATO’s missile defense system, designed to detect, track, and intercept ballistic missiles in flight. As a key element in transatlantic security, this site strengthens NATO’s defense against the increasing threat of ballistic missiles.

“This contract underscores our commitment to high-consequence missions,” said Jeremy C. Wensinger, President and Chief Executive Officer of V2X. For the past four years, V2X has provided support services at the U.S. Navy’s Aegis Ashore sister site in Romania. “This award marks a significant step in strengthening NATO’s defense and protecting European populations against global threats,” Wensinger added.

The contract is firm-fixed-price with a one-year base period, seven one-year options, and an additional six-month extension.

About V2X

V2X builds innovative solutions that integrate physical and digital environments by aligning people, actions, and technology. V2X is embedded in all elements of a critical mission’s lifecycle to enhance readiness, optimize resource management, and boost security. The company provides innovation spanning national security, defense, civilian, and international markets. With a global team of approximately 16,000 professionals, V2X enables mission success by injecting AI and machine learning capabilities to meet today’s toughest challenges across all operational domains.

Media Contact Angelica Spanos Deoudes Senior Director, Marketing and Communications Angelica.Deoudes@goV2X.com 571-338-5195

Investor Contact Mike Smith, CFA Vice President, Treasury, Corporate Development and Investor Relations IR@goV2X.com

SAN DIEGO, March 11, 2025 (GLOBE NEWSWIRE) — Kratos Defense & Security Solutions, Inc. (Nasdaq: KTOS), a technology company in the defense, national security, and global markets, today announced the award of the Short/Medium Range Sub-Orbital Vehicle (SSOV) II contract as a partner to Corvid Technologies, LLC. The contract, awarded by the Naval Surface Warfare Center, Port Hueneme, White Sands Detachment, will encompass the design, manufacture, and delivery of short- and medium-range suborbital vehicles, including provision of ground test hardware, special test equipment, materials, engineering, and launch support services. The contract includes options which, if exercised, bring the potential subcontract value to greater than $50 million.

Josh Peterson, Senior Vice President at Kratos Defense & Rocket Support Services, said, “This subcontract award as a partner to Corvid Technologies underscores our team’s ability to deliver advanced, cost-effective solutions that meet the critical launch service needs of our customers. The suborbital vehicle configurations provided under this contract significantly enhance the nation’s ability to rapidly and affordably demonstrate emerging technologies. We are proud to continue supporting the Naval Surface Warfare Center, Port Hueneme, White Sands Detachment, in this very vital mission.”

Work under the subcontract will be performed for U.S. and international customers, including Australia and the United Kingdom, in support of missile defense target missions and defense launch services. Launch vehicles under the contract will include Kratos’ Oriole Rocket Motor, Thrust Vector Control and other hardware and Systems to assist in performing complex mission trajectories.

About Kratos Defense & Security Solutions Kratos Defense & Security Solutions, Inc. (Nasdaq: KTOS) is a technology, products, system and software company addressing the defense, national security, and commercial markets. Kratos makes true internally funded research, development, capital, and other investments to rapidly develop, produce, and field solutions that address our customers’ mission critical needs and requirements. At Kratos, affordability is a technology, and we seek to utilize proven, leading-edge approaches and technology, not unproven bleeding-edge approaches or technology, with Kratos’ approach designed to reduce cost, schedule, and risk, enabling us to be first to market with cost-effective solutions. We believe that Kratos is known as an innovative disruptive change agent in the industry, a company that is an expert in designing products and systems up front for successful rapid, large quantity, low-cost future manufacturing which is a value add competitive differentiator for our large traditional prime system integrator partners and also to our government and commercial customers. Kratos intends to pursue program and contract opportunities as the prime or lead contractor when we believe that our probability of win (PWin) is high and any investment required by Kratos is within our capital resource comfort level. We intend to partner and team with a large, traditional system integrator when our assessment of PWin is greater or required investment is beyond Kratos’ comfort level. Kratos’ primary business areas include virtualized ground systems for satellites and space vehicles including software for command and control; telemetry, tracking, and control; jet-powered unmanned aerial drone systems; advanced vehicles and rocket systems; propulsion systems for drones, missiles, loitering munitions, supersonic systems, space craft, and launch systems; C5ISR and microwave electronic products for missile, radar, missile defense, space, satellite, counter UAS, directed energy, communication, and other systems; and virtual and augmented reality training systems for the warfighter. For more information, visit www.KratosDefense.com.

Notice Regarding Forward-Looking Statements Certain statements in this press release may constitute “forward-looking statements” within the meaning of the Private Securities Litigation Reform Act of 1995. These forward-looking statements are made on the basis of the current beliefs, expectations, and assumptions of the management of Kratos and are subject to significant risks and uncertainty. Investors are cautioned not to place undue reliance on any such forward-looking statements. All such forward-looking statements speak only as of the date they are made, and Kratos undertakes no obligation to update or revise these statements, whether as a result of new information, future events, or otherwise. Although Kratos believes that the expectations reflected in these forward-looking statements are reasonable, these statements involve many risks and uncertainties that may cause actual results to differ materially from what may be expressed or implied in these forward-looking statements. For a further discussion of risks and uncertainties that could cause actual results to differ from those expressed in these forward-looking statements, as well as risks relating to the business of Kratos in general, see the risk disclosures in the Annual Report on Form 10-K of Kratos for the year ended December 29, 2024, and in subsequent reports on Forms 10-Q and 8-K and other filings made with the SEC by Kratos.

Accelerating operational momentum through strategic portfolio actions

Provides outlook and guidance for full year 2025

NEW ALBANY, Ohio, March 10, 2025 (GLOBE NEWSWIRE) — CVG (NASDAQ: CVGI), a diversified industrial products and services company, today announced financial results for its fourth quarter and full year ended December 31, 2024.

As a result of completing our strategic portfolio actions, the following are reported as discontinued operations: (1) the Industrial Automation segment, and (2) the financial information from the Cab Structures facility that was previously reported in Vehicle Solutions and Aftermarket and Accessories. CVG has three reportable segments for 2024: Vehicle Solutions, Electrical Systems and Aftermarket & Accessories. The results and comparisons presented below reflect continuing operations unless otherwise noted.

Fourth Quarter 2024 Highlights(Compared with prior-year period, where comparisons are noted)

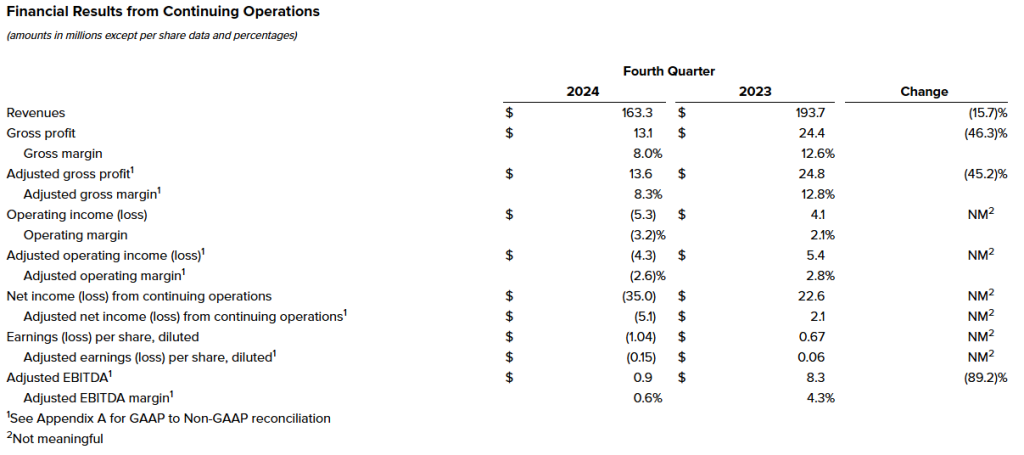

Revenue of $163.3 million, down 15.7% due primarily to a global softening in Construction and Agriculture customer demand and drop-in Class 8 Heavy Truck builds.

Operating loss of $5.3 million, and adjusted operating loss of $4.3 million, down compared to operating income of $4.1 million and adjusted operating income of $5.4 million. The decrease in operating income was driven primarily by lower sales volumes and operational inefficiencies.

Net loss from continuing operations of $35.0 million, or $(1.04) per diluted share, compared to net income of $22.6 million, or $0.67 per diluted share. Net loss included a non-cash tax valuation allowance of $28.8 million. Adjusted net loss from continuing operations of $5.1 million, or $(0.15) per diluted share, compared to adjusted net income of $2.1 million, or $0.06 per diluted share.

Adjusted EBITDA of $0.9 million, down 89.2%, with an adjusted EBITDA margin of 0.6%, down from 4.3%.

The sale of CVG’s Industrial Automation business closed on October 30, 2024, allowing CVG to focus on its core segments.

Full Year 2024 Highlights(Compared with prior-year period, where comparisons are noted)

Revenue of $723.4 million, down 13.4%, driven by a global softening in customer demand and the wind-down of certain programs in our Vehicle Solutions segment.

New business wins in excess of $97 million when fully ramped; these wins were concentrated in our Electrical Systems segment, predominantly outside of Construction and Agriculture end markets.

Operating loss of $0.8 million, down $40.6 million, and adjusted operating income of $6.5 million, down $35.2 million. The decrease in operating income was due to lower sales volumes and operational inefficiencies.

Continued shifting production capacity to new, lower-cost facilities in Morocco and Mexico, in an effort to improve operating leverage.

James Ray, President and Chief Executive Officer, said, “2024 was a year of meaningful change for CVG. Over the course of the year, we undertook immediate and decisive actions, including the divestitures of non-strategic assets and businesses, and improvement initiatives that we believe position us for future accretive growth. Even in the face of continued external market headwinds, we believe the improvement initiatives executed in 2024 will unlock significant operational efficiencies that we have already started to benefit from in 2025. Additionally, we were pleased to open our new Morocco facility and we continue to ramp up our facility in Aldama, Mexico.”

Mr. Ray continued, “Moving forward, our team is focused on accelerating the operational momentum we’ve built, driving margin accretive growth through a product-focused, operationally efficient enterprise strategy. With a stronger foundation, and as our key end markets stabilize, we expect that we will continue to strengthen the company’s position in the market and deliver value for our stakeholders.”

Andy Cheung, Chief Financial Officer, added, “CVG delivered results consistent with our adjusted full-year guidance ranges, which reflect the Company’s past portfolio and restructuring actions. We anticipate that the benefits from these strategic efforts will become more apparent in 2025 despite notable end market softening and the slower than expected ramp of new business wins. We believe that these organizational improvements, combined with working capital and inventory reductions driving increased cash generation this year, will greatly improve our ability to continue paying down debt. We have implemented a more focused business strategy and continue to streamline our enterprise cost structure. We expect to see EBITDA growth and margin expansion in 2025 which are reflected in our full year 2025 guidance ranges.”

Consolidated Results from Continuing Operations

Fourth Quarter 2024 Results

Fourth quarter 2024 revenues were $163.3 million compared to $193.7 million in the prior year period, a decline of 15.7%. The decrease in revenues is due primarily to lower sales as a result of a softening in customer demand in our Vehicle Solutions and Electrical Systems segments.

Operating loss for the fourth quarter 2024 was $5.3 million compared to operating income of $4.1 million in the prior year period. Excluding special costs, the fourth quarter of 2024 adjusted operating loss was $4.3 million, down from adjusted operating income of $5.4 million in 2023. The decline in adjusted operating income was driven primarily by the impact of lower sales volumes, unfavorable mix, and operational inefficiencies.

Interest expense was $2.2 million and $2.3 million for the fourth quarter ended December 31, 2024 and 2023, respectively.

Net loss from continuing operations was $35.0 million, or $(1.04) per diluted share, for the fourth quarter 2024 compared to net income of $22.6 million, or $0.67 per diluted share, in the prior year period.

At December 31, 2024, the Company had $50.5 million outstanding borrowings on its revolving credit facility, $26.6 million of cash and $84.4 million availability from revolving credit facilities, resulting in total liquidity of $111.0 million.

Fourth Quarter 2024 Segment Results (Compared with prior-year period, where comparisons are noted)

Vehicle Solutions Segment

Revenues were $91.4 million compared to $107.1 million for the prior year period, a decrease of 14.7% primarily due to lower sales volume as a result of decreased customer demand and the wind-down of certain programs.

Operating income for the fourth quarter 2024 was $1.7 million compared to $3.6 million in the prior year period, a decrease of 52.5%, primarily due to lower customer demand, operational remediation investments, and increased freight costs. The fourth quarter of 2024 adjusted operating income was $2.8 million compared to $4.0 million in the prior year period, a decrease of 30.5%.

Electrical Systems Segment

Revenues were $40.3 million compared to $56.2 million in the prior year period, a decrease of 28.3%, primarily resulting from a global softening in the Construction & Agriculture end-markets.

Operating loss was $1.7 million compared to operating income of $6.7 million, a decrease of 125.2% primarily attributable to lower sales volumes and unfavorable foreign exchange.

Aftermarket and Accessories Segment

Revenues were $31.6 million compared to $30.4 million in the prior year period, an increase of 4.0%, primarily resulting from slightly higher customer demand driving increased volumes.

Operating income was $3.2 million compared to $3.3 million in the prior year period, a decrease of 4.6%. The decrease in operating income was increased manufacturing costs. The fourth quarter of 2024 adjusted operating income was $3.1 million compared to $3.3 million in the prior year period.

Outlook

CVG is providing the following outlook for the full year 2025:

Metric

2025 Outlook ($ millions)

Net Sales

$670 – $710

Adjusted EBITDA

$25 – $30

This outlook reflects, among others, current industry forecasts for North American Class 8 truck builds. According to ACT Research, 2025 North American Class 8 truck production levels are expected to be at 316,000 units. The 2024 actual Class 8 truck builds according to the ACT Research was 332,382 units.

Construction and Agriculture end markets are projected to decline approximately 5-10% in 2025. However, we expect contribution from new business wins outside of Construction and Agriculture end markets in Electrical Systems to soften this decline.

Effective January 1, 2025, the Company announced a new organizational structure designed to enhance alignment with its customers and end markets. Under this new structure, CVG will reorganize its vertical business units into the following three operating divisions and reporting segments: Global Electrical Systems, Global Seating, Trim Systems and Components. As part of this realignment, the Company’s Aftermarket & Accessories business unit will be absorbed in these three segments. Its seating and electrical portfolio will transition to Global Seating and Global Electrical Systems, respectively. Its wiper systems will become part of the newly formed Trim Systems and Components business unit in addition to the trim and components businesses from the prior Vehicle Solutions segment. CVG expects this structure to enhance clarity and focus, with each business unit positioned to deliver on its specific strategic and operational objectives.

GAAP to Non-GAAP Reconciliation

A reconciliation of GAAP to non-GAAP financial measures referenced in this release is included as Appendix A to this release.

Conference Call

A conference call to discuss this press release is scheduled for Tuesday, March 11, 2025, at 8:30 a.m. ET. Management intends to reference the Q4 2024 Earnings Call Presentation posted on our website during the conference call. To participate, dial (800) 549-8228 using conference code 45919. International participants dial (289) 819-1520 using conference code 45919.

This call is being webcast and can be accessed through the “Investors” section of CVG’s website at www.cvgrp.com, where it will be archived for one year.

A telephonic replay of the conference call will be available for a period of two weeks following the call. To access the replay, dial (888) 660-6264 using access code 45919 and international callers can dial (289) 819-1325 using access code 45919.

Company Contact

Andy Cheung Chief Financial Officer CVG IR@cvgrp.com

Commercial Vehicle Group, Inc. and its subsidiaries, is a global provider of systems, assemblies and components to the global commercial vehicle market and the electric vehicle markets. We deliver real solutions to complex design, engineering and manufacturing problems while creating positive change for our customers, industries, and communities we serve. Information about the Company and its products is available on the internet at www.cvgrp.com.

Forward-Looking Statements

This press release contains forward-looking statements within the meaning of Section 21E of the Securities Exchange Act of 1934, as amended, and Section 27A of the Securities Act of 1933, as amended. For this purpose, any statements contained herein that are not statements of historical fact, including without limitation, certain statements herein regarding industry outlook, the Company’s expectations for future periods with respect to its plans to improve financial results, the future of the Company’s end markets changes in the Class 8 and Class 5-7 North America truck build rates, performance of the global construction and agricultural equipment business, the Company’s prospects in the wire harness and electric vehicle markets, the Company’s initiatives to address customer needs, organic growth, the Company’s strategic plans and plans to focus on certain segments, competition faced by the Company, volatility in and disruption to the global economic environment, including global supply chain constraints, inflation and labor shortages, tariffs and counter-measures, financial covenant compliance, anticipated effects of acquisitions or divestitures, production of new products, plans for capital expenditures and our results of operations or financial position and liquidity, may be deemed to be forward-looking statements. Without limiting the foregoing, the words “believe”, “anticipate”, “plan”, “expect”, “intend”, “will”, “should”, “could”, “would”, “project”, “continue”, “likely”, and similar expressions, as they relate to us, are intended to identify forward-looking statements. The important factors discussed in “Item 1A – Risk Factors” in the Company’s Annual Report on Form 10-K, among others, could cause actual results to differ materially from those indicated by forward-looking statements made herein and presented elsewhere by management from time to time. Such forward-looking statements represent management’s current expectations and are inherently uncertain. Investors are warned that actual results may differ from management’s expectations. Additionally, various economic and competitive factors could cause actual results to differ materially from those discussed in such forward-looking statements, including, but not limited to, factors which are outside our control.

Any forward-looking statement that we make in this press release speaks only as of the date of such statement, and we undertake no obligation to update any forward-looking statement or to publicly announce the results of any revision to any of those statements to reflect future events or developments. Comparisons of results for current and any prior periods are not intended to express any future trends or indications of future performance, unless specifically expressed as such, and should only be viewed as historical data.

Robert LeBoyer, Senior Vice President, Equity Research Analyst, Biotechnology, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

Recent Price Weakness Forces Move To The OTC Bulletin Board. As the recent decline in the overall markets was affecting companies in many sectors, the closing price of Zomedica stock fell below $0.10 per share on March 3. This crossed a threshold set by the New York American exchange, forcing the delisting of ZOM shares. Zomedica shares began trading on the OTCQB Venture Market under the symbol ZOMDF. There were no other events or crisis that caused the delisting.

During 2024, Zomedica Has Met All Of The Product Goals We Expected. Over the past year, Zomedica has introduced several new assays for use with its TRUFORMA diagnostics platform. These assays are sold to veterinary practices for use with TRUFORMA diagnostic instruments, allowing the veterinarian to run tests without sending samples to an outside lab. This allows the diagnosis in a few minutes and allows the practice to capture the profit from the tests. The TRUFORMA assays, reported as diagnostic consumables, have been one of the sources of sales growth over the past year.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

Robert LeBoyer, Senior Vice President, Equity Research Analyst, Biotechnology, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

We Are Initiating Coverage Of Gyre Therapeutics With An Outperform Rating. Gyre Therapeutics is a pharmaceutical company developing drugs for inflammatory diseases that lead to fibrosis. It currently markets Etuary (pirfenidone) in China for idiopathic pulmonary fibrosis. The lead drug in the pipeline is Hydronidone, a new molecule derived from pirfenidone, that is in a Phase 3 clinical trial in China. The data announcement is expected to report Phase 3 clinical trial results in March 2025.

Hydronidone Was Developed To Improve Efficacy and Side Effects. Hydronidone is a structural analogue of pirfenidone that was developed to improve efficacy with a more tolerable side effect profile. It is in Phase 3 trial in China for fibrosis of the liver after hepatitis B (HBV) infections. Hydronidone targets steps in the Transforming Growth Factor (TGF)-ß1 pathway as well as the downstream genes and liver cells it activates to produce fibrotic tissue. Data from the Phase 3 in China will be used to design a Phase 2a trial in the US, expected to begin in late FY2025.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.