Schwazze (OTCQX:SHWZ, NEO:SHWZ) is building a premier vertically integrated regional cannabis company with assets in Colorado and New Mexico and will continue to take its operating system to other states where it can develop a differentiated regional leadership position. Schwazze is the parent company of a portfolio of leading cannabis businesses and brands spanning seed to sale. The Company is committed to unlocking the full potential of the cannabis plant to improve the human condition. Schwazze is anchored by a high-performance culture that combines customer-centric thinking and data science to test, measure, and drive decisions and outcomes. The Company’s leadership team has deep expertise in retailing, wholesaling, and building consumer brands at Fortune 500 companies as well as in the cannabis sector. Schwazze is passionate about making a difference in our communities, promoting diversity and inclusion, and doing our part to incorporate climate-conscious best practices.

Joe Gomes, Managing Director, Equity Research Analyst, Generalist , Noble Capital Markets, Inc.

Joshua Zoepfel, Research Associate, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

2Q Results. Schwazze reported revenue of $42.4 million, down from last year’s $44.3 million. We had estimated revenue of $44 million. Schwazze reported a net loss, before preferred dividends, of $6.6 million, compared to net income of $33.8 million last year, which was impacted by unrealized derivative gains. After preferred dividends, net loss was $8.96 million, or a loss of $0.15/sh, versus net income of $32.1 million, or $0.24/sh, last year. Adjusted EBITDA was $13.8 million, or a margin of 32.6%, compared to $15 million, or 33.9%, last year. We had projected a $3.4 million net loss, or $0.06/sh.

Playbook Protecting Margins. By implementing its “go deep” retail strategy in its Colorado and New Mexico markets, Schwazze has been able to capture market share while cost optimization and operating efficiencies are enabling the Company to protect margins, as seen in 2Q23 gross margin of 57.9% up from 56.8% in 2Q22.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

With more than 60 units, RCI Hospitality Holdings, Inc., through its subsidiaries, is the country’s leading company in adult nightclubs and sports bars/restaurants. Clubs in New York City, Chicago, Dallas-Fort Worth, Houston, Miami, Minneapolis, Denver, St. Louis, Charlotte, Pittsburgh, Raleigh, Louisville, and other markets operate under brand names such as Rick’s Cabaret, XTC, Club Onyx, Vivid Cabaret, Jaguars Club, Tootsie’s Cabaret, Scarlett’s Cabaret, Diamond Cabaret, and PT’s Showclub. Sports bars/restaurants operate under the brand name Bombshells Restaurant & Bar.

Joe Gomes, Managing Director, Equity Research Analyst, Generalist , Noble Capital Markets, Inc.

Joshua Zoepfel, Research Associate, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

Third Quarter Results. RCI reported revenue of $77.1 million, up 9% y-o-y and in-line with our $77.8 million estimate. Net income was $9.1 million, or EPS of $0.96 compared to $13.9 million, or $1.48, last year with 3Q23 results impacted by higher expenses and one-time costs. Adjusted EPS was $1.30 versus $1.60. Adjusted EBITDA was at $22.7 million versus $24.6 million last year. We estimated net income of $12.9 million, EPS of $1.34, and adjusted EBITDA of $24.9 million.

Tough Comps and a Tough Environment. We would note 3Q22 had one of the highest levels of operating leverage in the last five years, as the business benefitted from the COVID emergence, directly impacting y-o-y comparisons. A continued uncertain economic environment also impacted results to a degree.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

Kelly (Nasdaq: KELYA, KELYB) connects talented people to companies in need of their skills in areas including Science, Engineering, Education, Office, Contact Center, Light Industrial, and more. We’re always thinking about what’s next in the evolving world of work, and we help people ditch the script on old ways of thinking and embrace the value of all workstyles in the workplace. We directly employ nearly 350,000 people around the world and connect thousands more with work through our global network of talent suppliers and partners in our outsourcing and consulting practice. Revenue in 2021 was $4.9 billion. Visit kellyservices.com and let us help with what’s next for you.

Joe Gomes, Managing Director, Equity Research Analyst, Generalist , Noble Capital Markets, Inc.

Joshua Zoepfel, Research Associate, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

2Q Results. Kelly reported revenues of $1.22 billion, a 3.9% decrease, or down 4.5% in constant currency, from the prior year. Organic revenue was down 2.2% in constant currency. We estimated revenue at $1.24 billion. GP rate was down 90 basis points to 19.8% primarily due to lower permanent placements fees. Net income was $7.5 million, or EPS of $0.20, compared to $2.2 million, or EPS of $0.06 last year. Adjusted EPS was $0.36 versus $0.45. We were at $0.44.

Transformation Plan. Kelly is moving quickly, already seeing benefits from its cost optimization and efficiencies programs. Next up will be a focus on growth, both organic, especially capturing a higher wallet share from existing clients, as well as a renewed inorganic focus.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

Comstock (NYSE: LODE) innovates technologies that contribute to global decarbonization and circularity by efficiently converting under-utilized natural resources into renewable fuels and electrification products that contribute to balancing global uses and emissions of carbon. The Company intends to achieve exponential growth and extraordinary financial, natural, and social gains by building, owning, and operating a fleet of advanced carbon neutral extraction and refining facilities, by selling an array of complimentary process solutions and related services, and by licensing selected technologies to qualified strategic partners. To learn more, please visit www.comstock.inc.

Mark Reichman, Managing Director, Equity Research Analyst, Natural Resources, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

Innovative feedstocks for renewable fuel producers. Comstock Fuels demonstrated the production of lignocellulosic bio-intermediates suitable for use in existing renewable fuel refineries at pilot scale and the capability for ongoing operations. A baseline lifecycle carbon analysis (LCA) model has also been developed with a third-party to validate industry-leading carbon intensity scores for fuel produced through its pathways. Management is engaged with multiple potential customers and partners for early adopter commercial agreements and expects one or more agreements to be completed this year.

Advancing toward commercialization. Comstock Metals has leased an operating facility in Silver Springs, Nevada and submitted all permits for operating its proprietary metal processing and recycling system. Comstock anticipates full deployment of its entire production system by the end of 2023 with operations commencing upon receipt of the permits. Comstock Metals has engaged suppliers to secure photovoltaic feedstocks and expects initial supply-revenue agreements in advance of production.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

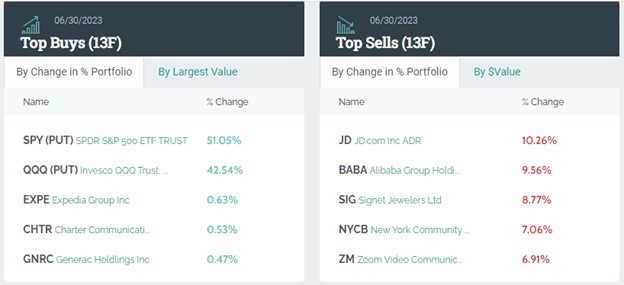

Michael Burry Has a Huge Bet According to His Just Filed SEC 13-F Report

It looks like Michael Burry has changed his mind, again. At the beginning of 2023, Burry, the founder of Scion Asset Management, was not positive at all on the stock market. The market then moved up in an epic rally. By late March, he announced in a tweet, “I was wrong to say sell.” Over the coming months stocks that had been beaten down the prior year, moved up significantly.

In his quarterly SEC 13-F filing today, the hedge fund manager that was portrayed in the movie “The Big Short” reported that he is more than just short the S&P 500 and Nasdaq 100. Burry held a huge leveraged short position as of June 30th. The position represents 84% of Scion’s assets under management (AUM), and is in the form of an all-or-nothing marketable options trade.

Burry recognized losses during the second quarter. The long positions he had put on earlier were underwater when he sold. The only conclusion is that he must have switched again from bullish to bearish – at least on these specific stocks. He then, with a broad brush, shorted large-cap stocks using stock options on ETFs. As of quarter-end 51.05% of his portfolio held puts on SPY and 42.54% held puts on QQQ.

Burry manages $1.7 billion. The puts used to short the S&P 500 ETF (SPY) and Nasdaq 100 (QQQ) is a broad brush that shows a great deal of confidence that large-cap stocks are headed lower before the options expire. It is a huge bet, while a short using puts has less downside than a straight short that, if unmanaged, can move against the owner an infinite amount, options have a window when they can be sold or exercised. If the position doesn’t work out, losses can be 100%.

Take Away

A lot can be learned from celebrity investors and fund managers. The lesson that investors may glean from Michael Burry’s first six months of 2023 is that you don’t sit in a bad position. Or, changing your mind is okay. The new positions indicate a high degree of confidence that large-cap stocks will fall apart over the coming months. It is just two positions, but they speak volumes in terms of his market call.

The SEC May be Poised to Become more Accommodating to Cryptocurrency

In what is being reported as a developing story that can significantly impact securities and crypto regulation, rumors are circulating that SEC Chair Gary Gensler may be on the way out as head of the agency. The reports are pointing to Hester Pierce as the most likely person to replace him. How would this impact public markets and the future state of cryptocurrency regulation? We discuss these questions and thoughts below.

Background

Whale (@whalechart) is a crypto news provider with an account on the microblogging platform X. It is widely respected, with 363,000 followers. Whale announced this morning (August 14), “SEC Commissioner Hester Peirce is being considered to replace Gary Gensler as the head of the regulatory agency.” This small post (or tweet) has triggered waves of speculation about the upcoming course of securities regulation for both registered products and cryptocurrencies like Bitcoin.

Ms. Peirce is known for her strong support of innovation and outside-the-box thinking. She has been a commissioner of the SEC since 2018, appointed by President Trump. Pierce is a former academic and lawyer who has specialized in securities law and financial regulation. She is known for her views on the regulation of cryptocurrencies and other emerging technologies.

What the SEC May Look Like Under Hester Pierce

Peirce, who has a reputation as being pro-innovation, has been a bold advocate for embracing disruptive technologies like cryptocurrencies and blockchain. If the rumors are accurate and she does find her way to the position of top securities cop, it could signal a shift towards a more accommodating regulatory stance, with a leader whose thoughts on fintech and digital assets are known.

If the days are indeed numbered for the SEC’s current head Gary Gensler, the traditional and digital asset markets would mainly view this as a positive. President Biden’s appointee, Gary Gensler, has been a catalyst behind the intensified scrutiny and rule-making within the overall cryptocurrency realm. His time in the position has led the SEC’s tightening its grip on digital asset exchanges and clamping down on many Initial Coin Offerings (ICOs).

Gensler has been acting to protect consumers, but many critics argue that the SEC under his lead, has been led to too much interference in free markets. With Peirce potentially in the drivers seat, the probability of the regulator embracing crypto assets in a less restrictive way increases dramatically.

Those impacted the most by a changed SEC head have weighed in already with diverse ideologies and opinions. Advocates assert that her penchant for innovation could sow the seeds for heightened financial growth. They contend that a friendlier regulatory outlook might be the medicine needed to embolden new ideas and investors to explore new opportunities – this, they say, could give the economy a lift.

Those opposed to a Hester Peirce nomination warn against a looser regulatory environment that could leave investors exposed to heightened risks. Their call is for the SEC to remain a vigilant guardian of investor interests, standing as a wall against potential deceit or market manipulation.

As the news regarding Peirce’s probable elevation continues to spread on social media and in articles like this, the pressing question many market participants are trying to discern is, will the SEC take a gentler road to new tech innovations or will it hold overly tight to its role concerning investor safety? If the change happens, there could be a celebratory bump in the value of crypto assets and others.

The Trading Week Ahead Could See Investors Continuing to Adjust to the Flattening Yield Curve

Bill Ackman says he’s short the U.S. Treasury long bond. Michael Burry, who tends to see things before others, had been short a derivative of Treasuries two summers ago, was he involved in interest rates this most recent quarter-end? We will get a glimpse into what these two, plus Warren Buffett and a host of others, as time runs out on their 13-F filing as of the close of business on Monday.

Last week many investors went from betting on a soft-landing a few weeks ago to now thinking interest rates along the curve are too low. The impetus for the shift was the CPI and PPI reports last week had provided nothing for the Fed to stop or slow down tightening. This concerns stock market investors. Higher rates, at a minimum, are beginning to provide an attractive alternative to a stock market that has already run up above average. This is because investors can now be choosier as their cash is far more productive, even after inflation, than it has been in years. Individual companies that have great prospects, rather index ETFs where you hold the good with the bad, would seem more prudent in the current scenario.

Monday 8/14

• 13-F Day is the SEC deadline for funds that manage more than $100 million in assets, that they must divulge positions held as of the end of the previous quarter. For example, Michael Burry’s Scion Asset Management hedge fund, Warren Buffett’s Berkshire Capital Holdings, and all U.S. asset managers of size have 45 days from quarter-end to file. A very large percentage choose to file on the 45th day, August 14th is 45 days from June 30th. Investors pour through the 13_f filings of top investors looking for insights.

Tuesday 8/15

• 8:30 AM ET, The consensus for Retail Sales for July is up 0.4% after an unexpectedly poor showing in June of a gain of 0.2%. Retail sales measure the total receipts at stores that sell merchandise and related services to final consumers. Sales are by retail and food services stores.

• 8:30 AM ET, Import and Export Prices are expected to show that import prices increased 0.2% in July after falling 0.2% in June. Export prices are expected to have increased 0.1% after dropping 0.9% in June. The underlying value of this report is the measure of global inflationary trends. Import price indexes are compiled for the prices of goods that are bought in the United States but produced abroad and export price indexes are compiled for the prices of goods sold abroad but produced within the U.S.

• 4:00 AM ET, Treasury International Capital is the tracking of who holds U.S. securities, or put another way, where in the world are U.S. Stocks, U.S. Treasuries, Agencies, and Corporate Bonds. TIC has recently been watched by a wider group as it is a measure of foreign demand for our assets. The prior number (May) showed net long-term transactions abroad of U.S. securities at $25.8 billion.

Wednesday 8/16

• 7:00 AM ET, The Mortgage Bankers Association (MBA) compiles data which indicates demand for mortgages. Data from the previous week indicate a drop in their Purchasing index of 2.7%, and a decline in its Refinance index of 4.0%.

• 8:30 AM ET, Housing Starts month over month for July are expected to have increased to 1.464 million from 1.44 million in June.

• 9:15 AM ET, Industrial Production had fallen 0.5 percent for two straight months; forecasters expect a rebound of 0.3 percent in July. After falling 0.3 and 0.2 percent, manufacturing output is seen as unchanged. Capacity utilization is expected to rise to 79.1 from 78.9 percent, still below what is considered inflationary.

• 10:30 PM ET, The Energy Information Administration (EIA) provides weekly information on petroleum inventories in the U.S., whether produced here or abroad. The inventory level impacts prices for petroleum products.

• 2:00 PM ET, FOMC minutes are from the meeting three weeks ago, where the Fed adjusted the overnight target upward. This report has recently been market-moving as it details the issues of debate and consensus among policymakers.

Thursday 8/17

• 8:30 AM ET, Initial Jobless Claims are expected to have fallen the week ended August 12th to 240,000 following a 21,000 jump to 248,000 last week, in the absence of inflation data, the market places adds emphasis on unexpected results in the labor market.

• 10:00 AM ET, E-Commerce Retail Sales for the second quarter are scheduled for release. During the first quarter, online retail transactions had increased by 3%.

• 4:30 AM ET, the weekly report on the Fed’s Balance Sheet is now awaited each week as it provides statistics on whether the Fed is fulfilling its quantitative tightening promise on schedule. It also could provide an early tip-off if there is a problem within the banking system. The report from the week prior showed $8.208 trillion in assets, and bank reserve credit declining $18,685 billion.

Friday 8/18

• 10:00 AM ET, The Quarterly Services Survey is not usually a large focus, but it is the only economic number printing on what may very well be a lightly traded late summer Friday. The report includes industry information; professional, scientific, and technical services; administrative & support services; and waste management (NAICS 51, 54, and 56). Last quarter, these industries experienced 2.9% growth, or 9.7% year-on-year.

What Else

A press release dated Friday, August 11th, stated that Greg Steube, a Representative from Florida’s 17th district had filed “Articles of Impeachment Against Joseph Robinette Biden, Jr., President of the United States, For High Crimes and Misdemeanors.” What this could mean for markets, if the past is an indicator, is very little. There could be days where traders are largely distracted by news stories that may come from this, but the soundness of the U.S. or the global economy is not likely to be hanging in the balance on any outcome from the proceedings.

Topline Results from Four CNS Clinical Trials Expected in the Third and Fourth Quarters of 2023

Fibromyalgia Topline Results Expected in the Fourth Quarter of 2023 for Phase 3 Potentially NDA-Enabling Study of the Centrally-Acting Non-Opioid Analgesic TNX-102 SL

Completed Strategic Acquisition of Two Marketed Acute Migraine Products: Zembrace® SymTouch® (sumatriptan injection) and Tosymra® (sumatriptan nasal spray)

CHATHAM, N.J., Aug. 10, 2023 (GLOBE NEWSWIRE) — Tonix Pharmaceuticals Holding Corp. (Nasdaq: TNXP) (Tonix or the Company), a biopharmaceutical company, today announced financial results for the second quarter ended June 30, 2023, and provided an overview of recent operational highlights.

“We have recently completed enrollment in four clinical trials for central nervous system (CNS) indications, representing our continuing progress towards bringing forth new treatments for serious CNS conditions that affect large patient populations,” said Seth Lederman, M.D., Chief Executive Officer of Tonix. “We look forward to data readouts before year-end 2023 for fibromyalgia, fibromyalgia-type Long COVID, chronic migraine, and depression. The topline results from the Phase 3 fibromyalgia trial are of particular importance because we believe the RESILIENT trial, if successful, will be the final efficacy trial required for submitting a New Drug Application (NDA) for approval by the U.S. Food and Drug Administration (FDA).”

On June 30, 2023, Tonix completed the acquisition of two marketed products from Upsher-Smith Laboratories, LLC (Upsher-Smith): Zembrace® SymTouch® (sumatriptan injection) 3 mg and Tosymra® (sumatriptan nasal spray) 10 mg. Zembrace SymTouch and Tosymra are both non-oral proprietary products indicated for the treatment of acute migraine with or without aura in adults. Zembrace SymTouch is the only branded sumatriptan autoinjector professionally promoted in the United States and is designed for ease of use and favorable tolerability with a low 3 mg dose. Tosymra is a novel intranasal sumatriptan product formulated with a permeation enhancer that provides rapid and efficient absorption of sumatriptan. Collectively, these products generated gross factory sales of approximately $30 million for the twelve months ended March 31, 2023. Zembrace SymTouch and Tosymra each may provide onset of migraine pain relief in as few as 10 minutes for some patients and currently have patent protection to 2036 and 2031, respectively.

Seth Lederman continued, “The acquisition of these two marketed products is transformative for Tonix as we believe that we are on track to become a fully integrated pharmaceutical company and to expand our expertise in CNS disorders by interacting with health care providers and payers. The build out of our commercial capabilities is timely, given the potential 2025 launch of TNX-102 SL (cyclobenzaprine HCl sublingual tablets) for fibromyalgia, if results from the RESILIENT trial are positive. The two marketed acute migraine products also align strongly with our clinical product candidate TNX-1900 (intranasal potentiated oxytocin), in development as a preventive medication in chronic migraineurs.”

“We plan to submit an IND to study TNX-2900 (intranasal potentiated oxytocin) in Prader-Willi syndrome, for which Orphan Drug Designation has already been granted by the FDA,” said Gregory Sullivan, M.D., Chief Medical Officer of Tonix Pharmaceuticals. “Academic collaborators have initiated enrollment in three Phase 2 investigator-initiated trials studying TNX-1900 (intranasal potentiated oxytocin). The trials in adolescent obesity and binge eating disorder at Massachusetts General Hospital (MGH) have the potential to expand the use of TNX-1900 to the treatment of disorders of appetite, eating behaviors and weight. The trial in social anxiety at University of Washington has the potential to expand the use of TNX-1900 to the treatment of disorders of social functioning.”

Dr. Lederman continued, “During the second quarter of 2023, we also announced the prioritization of our clinical stage CNS programs and de-prioritization of our COVID-19 vaccine and related therapeutic programs, as well as certain other preclinical programs in order to reallocate cash and resources. We also streamlined several CNS studies by eliminating interim analyses and reducing enrollment targets to ensure data readouts this year. We incurred a one-time cash outlay related to our acquisition of Zembrace SymTouch and Tosymra in the second quarter.”

Recent Highlights—Marketed Products

On June 30, 2023, Tonix completed the acquisition of two currently marketed products from Upsher-Smith Laboratories, LLC (Upsher-Smith): Zembrace SymTouch (sumatriptan injection) 3 mg and Tosymra (sumatriptan nasal spray) 10 mg. Zembrace SymTouch and Tosymra are both indicated for the treatment of acute migraine with or without aura in adults.

Recent Highlights—Key Product Candidates*

Upcoming Data Readouts in Central Nervous System (CNS) Pipeline During 2023

Fibromyalgia (4Q): Phase 3 Potentially NDA-Enabling Study of TNX-102 SL

Fibromyalgia-Type Long COVID (3Q): Phase 2 Proof-of-Concept Study of TNX-102 SL

Chronic Migraine (4Q): Phase 2 Proof-of-Concept Study of TNX-1900

Depression (4Q): Phase 2 Proof-of-Concept Study of TNX-601 ER

Central Nervous System (CNS) Pipeline

TNX-102 SL (cyclobenzaprine HCl sublingual tablets): once-daily at bedtime small molecule for the management of fibromyalgia (FM) – centrally-acting, non-opioid analgesic.

In August 2023, the Company announced that it completed enrollment of its potentially confirmatory Phase 3 RESILIENT trial of TNX-102 SL (cyclobenzaprine HCl sublingual tablets) 5.6 mg in fibromyalgia. A total of 457 participants were randomized in the trial, which, if successful, may serve as the final, well-controlled efficacy trial required for submission of an NDA for approval by the FDA. RESILIENT is a registration-quality, double-blind, placebo-controlled study.

Topline results from the RESILIENT trial are expected in the fourth quarter of 2023

TNX-102 SL for the treatment of Fibromyalgia-Type Long COVID, also known as Post-Acute Sequelae of COVID-19 (PASC)

In August 2023, the Company announced it completed the clinical phase of the PREVAIL study, a Phase 2 proof-of-concept study of TNX-102 SL for fibromyalgia-type Long COVID, as the last patient completed their final study visit. PREVAIL is a registration-quality, double-blind, placebo-controlled study.

Topline results from the PREVAIL Phase 2 trial are expected in the third quarter of 2023.

TNX-1900 (intranasal potentiated oxytocin): small peptide for migraine, craniofacial pain, social anxiety disorder, insulin resistance and related disorders, and adolescent obesity and binge eating disorder

Tonix has developed a formulation of intranasal oxytocin that contains magnesium (Mg2+) which is believed to potentiate the effects of oxytocin and may address the “inverted U” dose response of oxytocin. The company believes that if Mg2+ reduces the high dose inhibition of oxytocin alone, then the new formulation may improve consistency in clinical trials.

Enrollment has been completed in the proof-of-concept Phase 2 PREVENTION study of TNX-1900 for the prevention of migraine headache in chronic migraineurs with a total of 88 patients enrolled. PREVENTION is a registration-quality, double-blind, placebo-controlled study.

Topline results from the PREVENTION Phase 3 trial are expected in the fourth quarter of 2023.

In July 2023, Tonix announced that the first participant was enrolled in the investigator-initiated Phase 2 STROBE Study of TNX-1900 for the treatment of binge-eating disorder at the Massachusetts General Hospital (MGH) under the direction of Principal Investigator Elizabeth Lawson. Tonix is supporting the STROBE study through a clinical trial agreement with MGH.

In July 2023, Tonix announced that the first participant was enrolled in a Phase 2 investigator-initiated, proof-of-concept study of TNX-1900 for enhancing social safety learning in social anxiety disorder (SAD) under the direction of Principal Investigator Angela Fang. Tonix entered into an agreement with the University of Washington to examine the potential role of TNX-1900 in enhancing vicarious extinction learning in SAD, compared to healthy controls.

In July 2023, Tonix announced that the first participant was enrolled in the Phase 2 POWER study of TNX-1900 for the treatment of pediatric obesity with MGH under the direction of Principal Investigator Elizabeth Lawson. MGH is the sponsor of the National Institutes of Health-funded trial, being conducted under an investigator-initiated IND.

In May 2023, Tonix entered into a research collaboration agreement with the principal investigator of the study, Dr. Antoinette Maassen van den Brink, Professor of Neurovascular Pharmacology, Erasmus University Medical Center, to evaluate the effect of TNX-1900 on capsaicin- or electrical stimulation-induced forehead dermal blood flow in health female volunteers.

TNX-601 ER (tianeptine hemioxalate extended-release tablets): a once-daily orally administered small molecule for the treatment of major depressive disorder (MDD), posttraumatic stress disorder (PTSD), neurocognitive dysfunction associated with corticosteroid use, and potentially Alzheimer’s disease

Enrollment has been completed in the proof-of-concept Phase 2 UPLIFT study for the treatment of MDD, with 116 patients enrolled. UPLIFT is a registration-quality, double-blind, placebo-controlled study.

Topline results for the UPLIFT Phase 2 trial are expected in the fourth quarter of 2023.

Scientists at Tonix’s Research and Development Center (RDC) in Frederick, Md. established the molecular mechanism of action of tianeptine, the active ingredient of TNX-601 ER. The research supports a direct role for restoring neuroplasticity and neurogenesis, and upsets previously held beliefs about the significance of neurotransmitters in treating depression. It also provides clarity on why tianeptine does not cause sexual dysfunction, weight gain or several other treatment-limiting toxicities associated with traditional antidepressants.

TNX-4300 (estianeptine): small molecule oral therapeutic for MDD, bipolar disorder, Alzheimer’s disease and Parkinson’s disease

In July 2023, the Company announced that it would focus resources on the development of single isomer TNX-4300 as a first-in-class oral therapy for mood disorders, Alzheimer’s disease and other psychiatric and neurodegenerative conditions with memory deficits. The decision follows the Company’s announcement in May 2023 of the isolation and characterization of the (S)-isomer of tianeptine, which activates PPAR-β/δ, restores neuroplasticity in neuronal tissue culture and is free of µ-opioid receptor activity.

Tonix expects to initiate a potentially pivotal Phase 2 clinical study of TNX-1300 for the treatment of cocaine intoxication in the third quarter of 2023. In 2022, Tonix was awarded a Cooperative Agreement grant from the National Institute on Drug Abuse (NIDA), part of the National Institutes of Health (NIH), to support development of TNX-1300.

TNX-1300 has been granted Breakthrough Therapy designation by the FDA.

Rare Disease Pipeline

TNX-2900 (intranasal potentiated oxytocin): small peptide for the treatment of Prader-Willi syndrome (PWS)

TNX-2900 has been granted Orphan Drug designation from the FDA for the treatment of PWS and the preparation of the IND is in process.

TNX-2900 is in development to treat PWS and the planned clinical study will study its effects on hyperphagia, or pathological over-eating, in children and young adult patients with PWS.

Immunology Pipeline

TNX-1500 (anti-CD40L monoclonal antibody): third generation anti-CD40L monoclonal antibody for prophylaxis of organ transplant rejection and treatment of autoimmune disorders.

In May 2023, the IND for prevention of organ rejection in patients receiving a kidney transplant was cleared by FDA. A first-in-human Phase 1 study is expected to start in the third quarter of 2023. The first indication for TNX-1500 will be prophylaxis of organ rejection in adult patients receiving a kidney transplant, but multiple additional indications are possible, including autoimmune diseases. Two peer reviewed publications described the work at the Massachusetts General Hospital on allogeneic transplants in animals.1,2

*All of Tonix’s product candidates are investigational new drugs or biologics and none have been approved for any indication.

1Lassiter, G., et al. (2023). TNX-1500, a crystallizable fragment–modified anti-CD154 antibody, prolongs non-human primate renal allograft survival. American Journal of Transplantation. https://doi.org/10.1016/j.ajt.2023.03.022

2Miura, S., et al. (2023). TNX-1500, a crystallizable fragment–modified anti-CD154 antibody, prolongs non-human primate cardiac allograft survival. American Journal of Transplantation. https://doi.org/10.1016/j.ajt.2023.03.025

Recent Highlights—Financial

As of June 30, 2023, Tonix had approximately $25.6 million of cash and cash equivalents, compared to $120.2 million as of December 31, 2022. Subsequent to the end of the second quarter of 2023, Tonix raised $7.0 million in gross proceeds through a public offering of its common stock. Cash used in operations was approximately $56.3 million for the six months ended June 30, 2023, compared to $52.2 million for the same period in 2022. Cash used by investing activities for the six months ended June 30, 2023 was approximately $27.8 million, primarily driven by the purchase of certain assets from Upsher-Smith Laboratories, LLC.

The acquisition cost of Zembrace SymTouch and Tosymra was $15 million, consisting of $12 million up front and an additional deferred payment of $3.0 million. We also purchased inventory for $10.0 million and expect to pay an additional $1.3 million related to an inventory adjustment.

On April 8, 2020, the Company entered into a sales agreement with AGP of up to $320.0 million in at-the-market offerings sales. During the quarter ended June 30, 2023, the Company sold approximately 0.4 million shares of common stock under the sales agreement, for net proceeds of approximately $1.0 million.

On August 1, 2023, the Company sold in a public offering securities consisting of 2,530,000 shares of common stock, pre-funded warrants to purchase up to 4,470,000 shares of common stock, and accompanying common warrants to purchase 7,000,000 shares of common stock, at $1.00 per unit of common stock and common warrant, and $0.99 per pre-funded warrant and common warrant. The Company received net proceeds of approximately $6.2 million, after deducting underwriting discount and other offering expenses.

Second Quarter 2023 Financial Results

R&D expenses for the second quarter 2023 were approximately $22.0 million, compared to $16.6 million for the same period in 2022. As expected, R&D expenses have increased during 2023 due to progressing clinical development programs forward and investing in our preclinical development pipeline.

G&A expenses for the second quarter 2023 were $7.0 million, compared to $6.8 million for the same period in 2022.

Net loss available to common stockholders was $28.4 million, or $2.68 per share, basic and diluted, for the second quarter 2023, compared to net loss available to common stockholders of $27.4 million, or $7.64 per share, basic and diluted, for the same period in 2022. The basic and diluted weighted average common shares outstanding for the second quarter 2023 was 10,587,096 compared to 3,584,699 shares for the same period in 2022.

Tonix Pharmaceuticals Holding Corp.*

Tonix is a biopharmaceutical company focused on commercializing, developing, discovering and licensing therapeutics to treat and prevent human disease and alleviate suffering. Tonix markets Zembrace® SymTouch® (sumatriptan injection) 3 mg and Tosymra® (sumatriptan nasal spray) 10 mg. Zembrace SymTouch and Tosymra are each indicated for the treatment of acute migraine with or without aura in adults. Tonix’s development portfolio is composed of central nervous system (CNS), rare disease, immunology and infectious disease product candidates. Tonix’s CNS development portfolio includes both small molecules and biologics to treat pain, neurologic, psychiatric and addiction conditions. Tonix’s lead CNS candidate, TNX-102 SL (cyclobenzaprine HCl sublingual tablet), is in mid-Phase 3 development for the management of fibromyalgia, having completed enrollment in a potentially registration-enabling study, and with topline data expected in the fourth quarter of 2023. TNX-102 SL is also being developed to treat Long COVID, a chronic post-acute COVID-19 condition. Enrollment in a Phase 2 study has been completed, and topline results are expected in the third quarter of 2023. TNX-601 ER (tianeptine hemioxalate extended-release tablets), is a once-daily formulation being developed as a treatment for major depressive disorder (MDD). Enrollment is now complete in the UPLIFT trial of TNX-601 ER in MDD and topline results are expected in the fourth quarter of 2023. TNX-4300 (estianeptine) is a small molecule oral therapeutic in preclinical development to treat MDD, Alzheimer’s disease and Parkinson’s disease. TNX-1900 (intranasal potentiated oxytocin), is in development for chronic migraine, and the PREVENTION study has completed enrollment with topline data expected in the fourth quarter of 2023. TNX-1300 (cocaine esterase) is a biologic designed to treat cocaine intoxication and has been granted Breakthrough Therapy designation by the FDA. A Phase 2 study of TNX-1300 is expected to be initiated in the third quarter of 2023. Tonix’s rare disease development portfolio includes TNX-2900 (intranasal potentiated oxytocin) for the treatment of Prader-Willi syndrome. TNX-2900 has been granted Orphan Drug designation by the FDA. Tonix’s immunology development portfolio includes biologics to address organ transplant rejection, autoimmunity and cancer, including TNX-1500, which is a humanized monoclonal antibody targeting CD40-ligand (CD40L or CD154) being developed for the prevention of allograft rejection and for the treatment of autoimmune diseases. A Phase 1 study of TNX-1500 is expected to be initiated in the third quarter of 2023. Tonix’s infectious disease pipeline includes TNX-801, a vaccine in development to prevent smallpox and mpox. TNX-801 also serves as the live virus vaccine platform or recombinant pox vaccine platform for other infectious diseases. The infectious disease development portfolio also includes TNX-3900 and TNX-4000, classes of broad-spectrum small molecule antivirals.

*Tonix’s product development candidates are investigational new drugs or biologics and have not been approved for any indication.

Tonix Medicines has contracted to acquire the Zembrace SymTouch and Tosymra registered trademarks. Intravail is a registered trademark of Aegis Therapeutics, LLC, a wholly owned subsidiary of Neurelis, Inc.

This press release and further information about Tonix can be found at www.tonixpharma.com.

Forward Looking Statements

Certain statements in this press release are forward-looking within the meaning of the Private Securities Litigation Reform Act of 1995. These statements may be identified by the use of forward-looking words such as “anticipate,” “believe,” “forecast,” “estimate,” “expect,” and “intend,” among others. These forward-looking statements are based on Tonix’s current expectations and actual results could differ materially. There are a number of factors that could cause actual events to differ materially from those indicated by such forward-looking statements. These factors include, but are not limited to, risks related to the failure to obtain FDA clearances or approvals and noncompliance with FDA regulations; risks related to the failure to successfully market any of our products; risks related to the timing and progress of clinical development of our product candidates; our need for additional financing; uncertainties of patent protection and litigation; uncertainties of government or third party payor reimbursement; limited research and development efforts and dependence upon third parties; and substantial competition. As with any pharmaceutical under development, there are significant risks in the development, regulatory approval and commercialization of new products. Tonix does not undertake an obligation to update or revise any forward-looking statement. Investors should read the risk factors set forth in the Annual Report on Form 10-K for the year ended December 31, 2022, as filed with the Securities and Exchange Commission (the “SEC”) on March 13, 2023, and periodic reports filed with the SEC on or after the date thereof. All of Tonix’s forward-looking statements are expressly qualified by all such risk factors and other cautionary statements. The information set forth herein speaks only as of the date thereof.

TONIX PHARMACEUTICALS HOLDING CORP. CONDENSED CONSOLIDATED STATEMENTS OF OPERATIONS (In Thousands, Except Share and Per Share Amounts) (unaudited)

Three Months Ended June 30,

Six Months Ended June 30,

2023

2022

2023

2022

COSTS AND EXPENSES:

Research and development

$

21,976

$

16,579

$

48,487

$

35,001

General and administrative

7,026

6,757

14,417

14,771

29,002

23,336

62,904

49,772

Operating loss

(29,002

)

(23,336

)

(62,904

)

(49,772

)

Interest and other income, net

646

196

1,543

215

Net loss

(28,356

)

(23,140

)

(61,361

)

(49,557

)

Preferred stock deemed dividend

—

4,255

—

4,255

Net loss available to common stockholders

$

(28,356

)

$

(27,395

)

$

(61,361

)

$

(53,812

)

Net loss per common share, basic and diluted

$

(2.68

)

$

(7.64

)

$

(5.88

)

$

(17.28

)

Weighted average common shares outstanding, basic and diluted

10,587,096

3,584,699

10,428,678

3,113,965

See the accompanying notes to the condensed consolidated financial statements

1The condensed consolidated balance sheet for the year ended December 31, 2022 has been derived from the audited financial statements but do not include all of the information and footnotes required by accounting principles generally accepted in the United States for complete financial statements.

Zembrace® SymTouch® (sumatriptan Injection): IMPORTANT SAFETY INFORMATION

Zembrace SymTouch (Zembrace) can cause serious side effects, including heart attack and other heart problems, which may lead to death. Stop use and get emergency help if you have any signs of a heart attack:

discomfort in the center of your chest that lasts for more than a few minutes or goes away and comes back

severe tightness, pain, pressure, or heaviness in your chest, throat, neck, or jaw

pain or discomfort in your arms, back, neck, jaw or stomach

shortness of breath with or without chest discomfort

breaking out in a cold sweat

nausea or vomiting

feeling lightheaded

Zembrace is not for people with risk factors for heart disease (high blood pressure or cholesterol, smoking, overweight, diabetes, family history of heart disease) unless a heart exam shows no problem.

Do not use Zembrace if you have:

history of heart problems

narrowing of blood vessels to your legs, arms, stomach, or kidney (peripheral vascular disease)

uncontrolled high blood pressure

hemiplegic or basilar migraines. If you are not sure if you have these, ask your provider.

had a stroke, transient ischemic attacks (TIAs), or problems with blood circulation

severe liver problems

taken any of the following medicines in the last 24 hours: almotriptan, eletriptan, frovatriptan, naratriptan, rizatriptan, ergotamines, dihydroergotamine.

are taking certain antidepressants, known as monoamine oxidase (MAO)-A inhibitors or it has been 2 weeks or less since you stopped taking a MAO-A inhibitor. Ask your provider for a list of these medicines if you are not sure.

an allergy to sumatriptan or any of the components of Zembrace

Tell your provider about all of your medical conditions and medicines you take, including vitamins and supplements.

Zembrace can cause dizziness, weakness, or drowsiness. If so, do not drive a car, use machinery, or do anything where you need to be alert.

Zembrace may cause serious side effects including:

changes in color or sensation in your fingers and toes

sudden or severe stomach pain, stomach pain after meals, weight loss, nausea or vomiting, constipation or diarrhea, bloody diarrhea, fever

cramping and pain in your legs or hips; feeling of heaviness or tightness in your leg muscles; burning or aching pain in your feet or toes while resting; numbness, tingling, or weakness in your legs; cold feeling or color changes in one or both legs or feet

increased blood pressure including a sudden severe increase even if you have no history of high blood pressure

medication overuse headaches from using migraine medicine for 10 or more days each month. If your headaches get worse, call your provider.

serotonin syndrome, a rare but serious problem that can happen in people using Zembrace, especially when used with anti-depressant medicines called SSRIs or SNRIs. Call your provider right away if you have: mental changes such as seeing things that are not there (hallucinations), agitation, or coma; fast heartbeat; changes in blood pressure; high body temperature; tight muscles; or trouble walking.

hives (itchy bumps); swelling of your tongue, mouth, or throat

seizures even in people who have never had seizures before

The most common side effects of Zembrace include: pain and redness at injection site; tingling or numbness in your fingers or toes; dizziness; warm, hot, burning feeling to your face (flushing); discomfort or stiffness in your neck; feeling weak, drowsy, or tired.

Tell your provider if you have any side effect that bothers you or does not go away. These are not all the possible side effects of Zembrace. For more information, ask your provider.

This is the most important information to know about Zembrace but is not comprehensive. For more information, talk to your provider and read the Patient Information and Instructions for Use. You can also visit www.upsher-smith.com or call 1-888-650-3789.

You are encouraged to report adverse effects of prescription drugs to the FDA. Visit www.fda.gov/medwatch, or call 1-800-FDA-1088.

INDICATION AND USAGE

Zembrace is a prescription medicine used to treat acute migraine headaches with or without aura in adults who have been diagnosed with migraine.

Zembrace is not used to prevent migraines. It is not known if it is safe and effective in children under 18 years of age.

Tosymra can cause serious side effects, including heart attack and other heart problems, which may lead to death. Stop Tosymra and get emergency medical help if you have any signs of heart attack:

discomfort in the center of your chest that lasts for more than a few minutes or goes away and comes back

severe tightness, pain, pressure, or heaviness in your chest, throat, neck, or jaw

pain or discomfort in your arms, back, neck, jaw, or stomach

shortness of breath with or without chest discomfort

breaking out in a cold sweat

nausea or vomiting

feeling lightheaded

Tosymra is not for people with risk factors for heart disease (high blood pressure or cholesterol, smoking, overweight, diabetes, family history of heart disease) unless a heart exam is done and shows no problem.

Do not use Tosymra if you have:

history of heart problems

narrowing of blood vessels to your legs, arms, stomach, or kidney (peripheral vascular disease)

uncontrolled high blood pressure

severe liver problems

hemiplegic or basilar migraines. If you are not sure if you have these, ask your healthcare provider.

had a stroke, transient ischemic attacks (TIAs), or problems with blood circulation

taken any of the following medicines in the last 24 hours: almotriptan, eletriptan, frovatriptan, naratriptan, rizatriptan, ergotamines, or dihydroergotamine. Ask your provider if you are not sure if your medicine is listed above.

are taking certain antidepressants, known as monoamine oxidase (MAO)-A inhibitors or it has been 2 weeks or less since you stopped taking a MAO-A inhibitor. Ask your provider for a list of these medicines if you are not sure.

an allergy to sumatriptan or any ingredient in Tosymra

Tell your provider about all of your medical conditions and medicines you take, including vitamins and supplements.

Tosymra can cause dizziness, weakness, or drowsiness. If so, do not drive a car, use machinery, or do anything where you need to be alert.

Tosymra may cause serious side effects including:

changes in color or sensation in your fingers and toes

sudden or severe stomach pain, stomach pain after meals, weight loss, nausea or vomiting, constipation or diarrhea, bloody diarrhea, fever

cramping and pain in your legs or hips, feeling of heaviness or tightness in your leg muscles, burning or aching pain in your feet or toes while resting, numbness, tingling, or weakness in your legs, cold feeling or color changes in one or both legs or feet

increased blood pressure including a sudden severe increase even if you have no history of high blood pressure

medication overuse headaches from using migraine medicine for 10 or more days each month. If your headaches get worse, call your provider.

serotonin syndrome, a rare but serious problem that can happen in people using Tosymra, especially when used with anti-depressant medicines called SSRIs or SNRIs. Call your provider right away if you have: mental changes such as seeing things that are not there (hallucinations), agitation, or coma; fast heartbeat; changes in blood pressure; high body temperature; tight muscles; or trouble walking.

hives (itchy bumps); swelling of your tongue, mouth, or throat

seizures even in people who have never had seizures before

The most common side effects of Tosymra include: tingling, dizziness, feeling warm or hot, burning feeling, feeling of heaviness, feeling of pressure, flushing, feeling of tightness, numbness, application site (nasal) reactions, abnormal taste, and throat irritation.

Tell your provider if you have any side effect that bothers you or does not go away. These are not all the possible side effects of Tosymra. For more information, ask your provider.

This is the most important information to know about Tosymra but is not comprehensive. For more information, talk to your provider and read the Patient Information and Instructions for Use. You can also visit www.upsher-smith.com or call 1-888-650-3789.

You are encouraged to report negative side effects of prescription drugs to the FDA. Visit www.fda.gov/medwatch, or call 1-800-FDA-1088.

INDICATION AND USAGE Tosymra is a prescription medicine used to treat acute migraine headaches with or without aura in adults.

Tosymra is not used to treat other types of headaches such as hemiplegic or basilar migraines or cluster headaches.

Tosymra is not used to prevent migraines. It is not known if Tosymra is safe and effective in children under 18 years of age.

Anticipate topline results from the Phase 1 monotherapy and Phase 1/2 combination study with letrozole in Q4 2023

Plans are underway for a registrational trial with rigosertib in patients with RDEB-associated squamous cell carcinoma based on a constructive Type B FDA meeting held in June

Company to host conference call and webcast at 4:30 p.m. ET on Thursday, August 10, 2023

NEWTOWN, Pa., Aug. 10, 2023 (GLOBE NEWSWIRE) — Onconova Therapeutics, Inc. (NASDAQ: ONTX), (“Onconova” or “the Company”), a clinical-stage biopharmaceutical company focused on discovering and developing novel products for patients with cancer, today reported second quarter 2023 financial results and provided an update on recent pipeline progress. Management plans to host a conference call and live webcast at 4:30 p.m. ET today to discuss these results.

“We are very encouraged about the recent progress that the Onconova team has made for our two lead programs, narazaciclib, a differentiated multikinase CDK4/6 inhibitor targeting proteins involved in resistance pathways, and rigosertib, a cell signaling inhibitor, over the last few months, while effectively managing our financial resources. In addition, we are pleased that Victor Moyo, M.D., a highly experienced and successful clinical researcher and drug developer, has agreed to join the Company as Consulting Chief Medical Officer. We look forward to sharing several important updates in the coming months,” said Steve Fruchtman, M.D., President and Chief Executive Officer.

Dr. Fruchtman continued, “For narazaciclib, our efforts have been dedicated to completing a Phase 1 program and defining a recommended Phase 2 dose to support evaluation of narazaciclib in a randomized trial. Onconova believes this CDK4/6 compound has the potential to provide differentiated efficacy based on targeting proteins that have been implicated in resistance mechanisms and the potential for an improved safety profile. We are pleased to see target engagement based on an assay measuring proliferation. We expect to report the results from our Phase 1 monotherapy and Phase 1/2 combination study with letrozole in Q4 2023. The readout will include safety, pharmacokinetics and the definition of a recommended Phase 2 dose.”

Dr. Fruchtman concluded, “For rigosertib, we continue to believe this rigosertib’s unique action on cell signaling pathways, including K-RAS and PLK-1, combined with an acceptable safety profile, could position it as an attractive anti-cancer agent. In June, we had a constructive Type B meeting with the FDA for the use of rigosertib monotherapy in the lead, ultra-rare indication of RDEB-associated squamous cell carcinoma. Based on that meeting and the impressive clinical responses in previously refractory patients we have seen and presented at major medical meetings, we plan to design a registrational trial and will look to provide an update on next steps in H1 2024. In the meantime, we continue to support two investigator sponsored studies for rigosertib, underway in melanoma and KRAS mutated non-small cell lung cancer which includes any KRAS mutation that may be present.”

Second Quarter Financial Results Cash and cash equivalents as of June 30, 2023, were $29.7 million, compared to $38.8 million as of December 31, 2022. The Company believes that its cash and cash equivalents will be sufficient to fund ongoing clinical trials and business into the second quarter of 2024.

Research and development expenses were $2.5 million for the second quarter of 2023, compared with $2.0 million for the second quarter of 2022.

General and administrative expenses were $2.2 million for the second quarter of 2023, compared with $2.1 million for the second quarter of 2022.

Net loss for the second quarter of 2023 was $4.3 million, or $0.20 per share on 21.0 million weighted shares outstanding, compared with a net loss of $4.0 million, or $0.19 per share for the second quarter of 2022 on 20.9 million weighted shares outstanding.

Conference Call and Webcast Information Interested parties who wish to participate in the conference call may do so by dialing:

(800) 715-9871 for domestic and

(646) 307-1963 for international callers and

Using conference ID 9506701

Those interested in listening to the conference call via the internet may do so by visiting the investors and media page on the Company’s website at www.onconova.com and clicking on the webcast link. In addition to the live webcast, a replay will be available on the Onconova website for 90 days following the call.

About Onconova Therapeutics, Inc. Onconova Therapeutics is a clinical-stage biopharmaceutical company focused on discovering and developing novel products for patients with cancer. The Company’s product candidates include proprietary targeted anti-cancer agents designed to disrupt specific cellular pathways that are important for cancer cell proliferation.

Onconova’s novel, proprietary multi-kinase inhibitor narazaciclib (formerly ON 123300) is being evaluated in a Phase 1/2 combination trial with the estrogen blocker, letrozole, in advanced low grade endometrial cancer (NCT05705505). Based on preclinical and clinical studies of CDK 4/6 inhibitors, Onconova is also evaluating opportunities for combination studies with narazaciclib and letrozole in additional indications.

Onconova’s product candidate rigosertib is being studied in multiple investigator-sponsored studies. These studies include a dose-escalation and expansion Phase 1/2a study of oral rigosertib in combination with nivolumab in patients with KRAS+ non-small cell lung cancer (NCT04263090), a Phase 2 program evaluating oral or IV rigosertib monotherapy in advanced squamous cell carcinoma complicating recessive dystrophic epidermolysis bullosa (RDEB-associated SCC (NCT03786237, NCT04177498), and a Phase 2 trial evaluating rigosertib in combination with pembrolizumab in patients with metastatic melanoma (NCT05764395).

Forward Looking Statements Some of the statements in this release are forward-looking statements within the meaning of Section 27A of the Securities Act of 1933, as amended, Section 21E of the Securities Exchange Act of 1934, as amended, and the Private Securities Litigation Reform Act of 1995, and involve risks and uncertainties. These statements relate to Onconova’s expectations regarding its clinical development and trials, its product candidates and its business and financial position. Onconova has attempted to identify forward-looking statements by terminology including “believes,” “estimates,” “anticipates,” “expects,” “plans,” “intends,” “may,” “could,” “might,” “will,” “should,” “preliminary,” “encouraging,” “approximately” or other words that convey uncertainty of future events or outcomes. Although Onconova believes that the expectations reflected in such forward-looking statements are reasonable as of the date made, expectations may prove to have been materially different from the results expressed or implied by such forward-looking statements. These statements are only predictions and involve known and unknown risks, uncertainties, and other factors, including the success and timing of Onconova’s clinical trials, investigator-sponsored trials, regulatory agency and institutional review board approvals of protocols, Onconova’s collaborations, market conditions and those discussed under the heading “Risk Factors” in Onconova’s most recent Annual Report on Form 10-K and quarterly reports on Form 10-Q. Any forward-looking statements contained in this release speak only as of its date. Onconova undertakes no obligation to update any forward-looking statements contained in this release to reflect events or circumstances occurring after its date or to reflect the occurrence of unanticipated events.

CHELMSFORD, MA / ACCESSWIRE / August 10, 2023 / Harte Hanks, Inc. (NASDAQ:HHS), a leading global customer experience company focused on bringing companies closer to customers for 100 years, today announced financial results for the second quarter and six-month period ended June 30, 2023.

Kirk Davis, Chief Executive Officer, commented: “My favorable impressions of Harte Hanks were confirmed in my first month as CEO; Harte Hanks has great people and significant capabilities that are desired by global brands. The pandemic had a positive, multi-year impact on our business, which we’re now beyond. In addition, many of our customers have curtailed budgets for 2023 due to concerns about the economy. This necessitates our near-term focus on further aligning our cost structure, and in addition, shifting some of our current spend to bolster sales productivity.”

“The second quarter results represent a baseline for our expectations in the near term and present a solid foundation on which to build,” added Mr. Davis. “We’re focused on bolstering our sales pipeline, retooling our marketing programs, improving sales effectiveness, and leveraging a new partnership we’ve struck with a highly reputable business development company. Our acquisition of InsideOut in December of 2022 expands our end-to-end offering and specifically our lead generation capabilities. We expect to build on the consistent profitability that has been achieved and position Harte Hanks to generate more sustainable, profitable growth. We’re excited to deliver on these objectives. Additionally, the company executed on its stock repurchase plan by repurchasing almost 315,000 shares.”

Second Quarter Financial Highlights

Total revenues for Q2 2023 were $47.8 million, up 1.4% sequentially and down 1.6% year over year compared to $48.6 million in Q2 2022. Included in 2023 was $2.3 million from InsideOut acquired in fourth quarter of 2022.

Operating income was $1.7 million compared to $4.0 million in the prior-year quarter.

Net income of $0.6 million compared to net income of $4.5 million in the prior year.

Diluted EPS was $0.08 compared to $0.52 for the prior year’s second quarter.

EBITDA was $2.7 million compared to $4.6 million in the same period in the prior year.[1] Adjusted EBITDA, which excludes stock-based compensation and severance, was $4.4 million compared to $5.2 million.

Segment Highlights

Customer Care, $17.2 million in revenue, 36% of total – Segment revenue increased $1.8 million or 11.9% versus prior year and EBITDA totaled $3.0 million for the quarter, up 18.3% year-over-year. New business wins that are expected to positively impact results during the second quarter include:

A multi-national pharmaceutical company has engaged Harte Hanks to develop the strategy for their long-term Customer Service Experience. The scope includes the analysis and validation of their Customer Service vision, benchmarking, gap analysis and a blueprint with an implementation roadmap to inform their 2024 plans to optimize their Customer Care strategy and delivery.

One of the largest consultancy firms in the world has selected Harte Hanks to support a state government’s rollout of Medicaid renewal support for its constituents. This program helps Medicaid users renew for services, as well as provides education on how to engage and leverage the online systems to improve use of these benefits.

Fulfillment & Logistics Services, $19.6 million in revenue, 41% of total – Segment revenue decreased slightly versus the prior year quarter and EBITDA for Q2 2023 totaled $1.9 million, down $1.2 million or 39%. Revenue mix drove the reduced EBITDA margins as growth in lower-margin logistics revenue was offset by reduced volumes in our financial services vertical that yielded higher margins. New business wins during the second quarter include:

Harte Hanks Fulfillment won New Logo business with a major international manufacturer, providing fulfillment support for a new program of Direct-to-Customer hearing aid sales. As a major player in the industry, the manufacturer is well-positioned for growth as the hearing aid market pivots from prescription-only into “Over the Counter” space.

A leading branding company selected Harte Hanks Fulfillment to manage the production, kitting, and distribution of 150k+ curated Food & Beverage product gift boxes for a Fortune 50 retail partner. After producing several million kits on this partner’s behalf over the past year, this represents the first instance where the relationship has fully leveraged our FDA approved, climate-controlled facility for food grade items.

Marketing Services, $10.9 million in revenue, 23% of total – Segment revenue declined $2.5 million (19%) compared to the prior year quarterand EBITDA for the quarter totaled $1.3 million vs. $1.8 million. Pressure on both revenue and EBITDA was driven by a reduction in legacy direct mail campaigns and lighter project volumes. New business wins during second quarter include:

A major insurance carrier supporting government employees has selected Harte Hanks to help facilitate their email transition to a new CRM. While this organization is an existing customer for our Customer Care and Fulfillment segments, this is the first engagement for this client with our Marketing Services team.

One of the largest online travel agencies has expanded its services with Harte Hanks to support an ‘Always On’ nurture program for their global business customers.

Consolidated Second Quarter 2023 Results

Second quarter revenues were $47.8 million, down 1.6% from $48.6 million in the second quarter of 2022. The Company’s Customer Care segment grew, largely offsetting declines in Fulfillment & Logistics Services and Marketing Services.

Second quarter operating income was $1.7 million, compared to operating income of $4.0 million in the second quarter of 2022. The decrease resulted from a less favorable revenue mix and lower consolidated revenue.

Net income for the quarter was $0.6 million, or $0.08 per diluted share, compared to net income of $4.5 million, or $0.52 per diluted share, in the second quarter last year. Results this quarter included $1.2 million of pension expense, as well as $503,000 in stock-based compensation and $1.2 million in severance, largely related to the CEO transition. The severance and other costs related to the CEO transition created a non-recurring, $0.12 per share impact, without tax impact, in the second quarter of 2023.

Consolidated Year-to-Date 2023 Results

Year-to-date revenues were $94.9 million, down 2.8% from $97.6 million in the same period of 2022. Year-to-date operating income was $2.7 million, compared to operating income of $7.9 million. Net loss for the first six months was $(0.2) million, or $(0.03) per diluted share, compared to net income of $7.8 million, or $0.91 per diluted share, in the first six months of last year.

Balance Sheet and Liquidity

Harte Hanks ended the quarter with $13.4 million in cash and cash equivalents and $24 million of capacity on its credit line. The Company has no outstanding debt as of June 30, 2023. The Company’s financial position continues to be strong, and it is well-positioned to execute on its long-term growth strategies in 2023 and beyond.

During the quarter, Harte Hanks repurchased approximately 315,000 shares at an average price of $5.97 per share for a total of $1.9 million.

Conference Call Information

The Company will host a conference call and live webcast to discuss these results on Thursday, August 10, 2023 at 4:30 p.m. EST. Interested parties may access the webcast at https://investors.hartehanks.com/events or may access the conference call by dialing (877) 545-0320 in the United States or (973) 528-0002 from outside the U.S. and using access code 183563.

A replay of the call can also be accessed via phone through August 24, 2023 by dialing (877) 481-4010 from the U.S., or (919) 882-2331 from outside the U.S. The conference call replay passcode is 48804.

About Harte Hanks:

Harte Hanks (NASDAQ:HHS) is a leading global customer experience company whose mission is to partner with clients to provide them with CX strategy, data-driven analytics and actionable insights combined with seamless program execution to better understand, attract and engage their customers.

Using its unparalleled resources and award-winning talent in the areas of Customer Care, Fulfillment and Logistics, and Marketing Services, Harte Hanks has a proven track record of driving results for some of the world’s premier brands, including Bank of America, GlaxoSmithKline, Unilever, Pfizer, HBOMax, Volvo, Ford, FedEx, Midea, Sony and IBM among others. Headquartered in Chelmsford, Massachusetts, Harte Hanks has over 2,500 employees in offices across the Americas, Europe, and Asia Pacific.

As used herein, “Harte Hanks” or “the Company” refers to Harte Hanks, Inc. and/or its applicable operating subsidiaries, as the context may require. Harte Hanks’ logo and name are trademarks of Harte Hanks.

Our press release and related earnings conference call contain “forward-looking statements” within the meaning of U.S. federal securities laws. All such statements are qualified by this cautionary note, provided pursuant to the safe harbor provisions of Section 27A of the Securities Act of 1933 and Section 21E of the Securities Exchange Act of 1934. Statements other than historical facts are forward-looking and may be identified by words such as “may,” “will,” “expects,” “believes,” “anticipates,” “plans,” “estimates,” “seeks,” “could,” “intends,” or words of similar meaning. These forward-looking statements are based on current information, expectations and estimates and involve risks, uncertainties, assumptions and other factors that are difficult to predict and that could cause actual results to vary materially from what is expressed in or indicated by the forward-looking statements. In that event, our business, financial condition, results of operations or liquidity could be materially adversely affected and investors in our securities could lose part or all of their investments. These risks, uncertainties, assumptions and other factors include: (a) local, national and international economic and business conditions, including (i) the outbreak of diseases, such as the COVID-19 coronavirus, which has curtailed travel to and from certain countries and geographic regions, created supply chain disruption and shortages, disrupted business operations and reduced consumer spending, (ii) market conditions that may adversely impact marketing expenditures, (iii) the impact of the Russia/Ukraine conflict on the global economy and our business, including impacts from related sanctions and export controls and (iv) the impact of economic environments and competitive pressures on the financial condition, marketing expenditures and activities of our clients and prospects; (b) the demand for our products and services by clients and prospective clients, including (i) the willingness of existing clients to maintain or increase their spending on products and services that are or remain profitable for us, and (ii) our ability to predict changes in client needs and preferences; (c) economic and other business factors that impact the industry verticals we serve, including competition and consolidation of current and prospective clients, vendors and partners in these verticals; (d) our ability to manage and timely adjust our facilities, capacity, workforce and cost structure to effectively serve our clients; (e) our ability to improve our processes and to provide new products and services in a timely and cost-effective manner though development, license, partnership or acquisition; (f) our ability to protect our facilities against security breaches and other interruptions and to protect sensitive personal information of our clients and their customers; (g) our ability to respond to increasing concern, regulation and legal action over consumer privacy issues, including changing requirements for collection, processing and use of information; (h) the impact of privacy and other regulations, including restrictions on unsolicited marketing communications and other consumer protection laws; (i) fluctuations in fuel prices, paper prices, postal rates and postal delivery schedules; (j) the number of shares, if any, that we may repurchase in connection with our repurchase program; (k) unanticipated developments regarding litigation or other contingent liabilities; (l) our ability to complete anticipated divestitures and reorganizations, including cost-saving initiatives; (m) our ability to realize the expected tax refunds; and (n) other factors discussed from time to time in our filings with the Securities and Exchange Commission, including under “Item 1A. Risk Factors” in our Annual Report on Form 10-K for the year ended December 31, 2022 which was filed on March 31, 2023. The forward-looking statements in this press release and our related earnings conference call are made only as of the date hereof, and we undertake no obligation to update publicly any forward-looking statement, even if new information becomes available or other events occur in the future.

Supplemental Non-GAAP Financial Measures:

The Company reports its financial results in accordance with generally accepted accounting principles (“GAAP”). However, the Company may use certain non-GAAP measures of financial performance in order to provide investors with a better understanding of operating results and underlying trends to assess the Company’s performance and liquidity in this press release and our related earnings conference call. We have presented herein a reconciliation of these measures to the most directly comparable GAAP financial measure.

The Company presents the non-GAAP financial measure “Adjusted Operating Income (Loss)” as a measure useful to both management and investors in their analysis of the Company’s financial results because it facilitates a period-to-period comparison of Operating Revenue and Operating Income (Loss) by excluding restructuring expense, impairment expense and stock-based compensation. The most directly comparable measure for this non-GAAP financial measure is Operating Income (Loss).

The Company presents the non-GAAP financial measure “EBITDA” and “Adjusted EBITDA” as a supplemental measure of operating performance in order to provide an improved understanding of underlying performance trends. The Company defines “Adjusted EBITDA” as earnings before interest expense net, income tax expense (benefit), depreciation expense, stock compensation expense and severance expenses. The most directly comparable measure for each of EBITDA and Adjusted EBITDA is Net Income (Loss). We believe each of EBITDA and Adjusted EBITDA are important performance metrics because they facilitates the analysis of our results, exclusive of certain non-cash items, non-recurring or special charges and items we believe do not directly correlate to our business operations; however, we urge investors to review the reconciliation of each of EBITDA and Adjusted EBITDA to the comparable GAAP Net Income (Loss), which is included in this press release, and not to rely on any single financial measure to evaluate the Company’s financial performance.

The use of non-GAAP measures do not serve as a substitute and should not be construed as a substitute for GAAP performance but should provide supplemental information concerning our performance that our investors and we find useful. The Company evaluates its operating performance based on several measures, including this non-GAAP financial measures. The Company believes that the presentation of this non-GAAP financial measures in this press release and earnings conference call presentations are useful supplemental financial measures of operating performance for investors because they facilitate investors’ ability to evaluate the operational strength of the Company’s business. However, there are limitations to the use of this non-GAAP measures, including that they may not be calculated the same by other companies in our industry limiting their use as a tool to compare results. Any supplemental non-GAAP financial measures referred to herein are not calculated in accordance with GAAP and they should not be considered in isolation or as substitutes for the most comparable GAAP financial measures.

EBITDA is the Company’s measure of segment profitability.

1 EBITDA is a non-GAAP financial measure. See “Supplemental Non-GAAP Financial Measures” below. EBITDA is also the Company’s measure of segment profitability.

Investor Relations Contact:

Rob Fink or Tom Baumann 646.809.4048 / 646.349.6641 FNK IR HHS@fnkir.com

Harte Hanks, Inc.

Consolidated Statements of Operations (Unaudited)

Three Months Ended June 30,

Six Months Ended June 30,

In thousands, except per share data

2023

2022

2023

2022

Revenues………………………………………………………………………………..

$

47,762

$

48,553

$

94,882

$

97,615

Operating expenses

Labor…………………………………………………………………………………..

26,666

25,109

51,131

51,027

Production and distribution……………………………………………………….

13,328

13,507

27,780

26,225

Advertising, selling, general and administrative………………………………

5,065

5,340

11,149

11,273

Depreciation and amortization expense………………………………………..

Second Quarter 2023 Revenue Up 67% Year-Over-Year to $35.4 Million

Company Raises Full-Year 2023 Revenue Guidance