Joe Gomes, Managing Director, Equity Research Analyst, Generalist , Noble Capital Markets, Inc.

Joshua Zoepfel, Research Associate, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

A Response. On Friday, Lifeway’s Board responded to the recent letter released by Kanen Wealth Management (KWM). As one would expect, the Board disagrees with the points laid out by KWM. From a governance standpoint, the Board noted its belief the executive team is successfully executing the Lifeway 2.0 strategy, has aligned interests with shareholders given insiders’ 18% ownership stake, and has consistently engaged with shareholders.

Operating Highlights. The Board goes on to point out a number of operating highlights, including: (i) 14 consecutive quarters of strong year-over-year net sales growth, (ii) growth into the 9th largest U.S. yogurt manufacturer, (iii) a growing customer base, (iv) positioned to capitalize on macro trends as customer demand for kefir grows, and (v) total shareholder return of 44% over the last year and 191% over the past three years, among other points.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

Townsquare is a community-focused digital media and digital marketing solutions company with market leading local radio stations, principally focused outside the top 50 markets in the U.S. Our assets include a subscription digital marketing services business, Townsquare Interactive, providing website design, creation and hosting, search engine optimization, social media and online reputation management as well as other digital monthly services for approximately 26,800 SMBs; a robust digital advertising division, Townsquare IGNITE, a powerful combination of a) an owned and operated portfolio of more than 330 local news and entertainment websites and mobile apps along with a network of leading national music and entertainment brands, collecting valuable first party data, and b) a proprietary digital programmatic advertising technology stack with an in-house demand and data management platform; and a portfolio of 321 local terrestrial radio stations in 67 U.S. markets strategically situated outside the Top 50 markets in the United States. Our portfolio includes local media brands such as WYRK.com, WJON.com, and NJ101.5.com and premier national music brands such as XXLmag.com, TasteofCountry.com, UltimateClassicRock.com and Loudwire.com.

Michael Kupinski, Director of Research, Equity Research Analyst, Digital, Media & Technology , Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

Repurchase at a discount. The company announced that it repurchased and retired 1.5 million shares from Madison Square Garden Company (MSG) at $9.70 per share, an 8.5% discount on the recent market price. The share repurchase accounts for nearly half of MSG’s previous ownership, and approximately 8.5% of total TSQ shares outstanding. The move follows an earlier move to initiate a hefty quarterly dividend. Separately, the TSQ shares will join the Russell 3000 and Small-Cap Russell 2000 Indices.

Ample liquidity, accretive to per share estimates. We estimate that the company had $67 million in cash prior to the repurchase and retains a substantial cash position following the transaction. The move is accretive to cash flow and earnings per share estimates, which are being adjusted to reflect the fewer shares outstanding.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

Are Higher Interest Rates Going to Be Devastatingly Expensive to the US Treasury?

The Federal Open Market Committee (FOMC) has raised the overnight Fed Funds target rate from near zero to around 5% in less than a year and a half. That multiple from its starting point is huge and, as designed, driven up other rates, both savings and lending. Given the pace that rates have gone up, the cost of refinancing or rolling existing debt for the federal and municipal governments, businesses, and households, has obviously experienced a large cost increase. When treasury debt matures, the US government decides whether to “roll over” their debt by issuing new securities at the current rate—or find other resources to repay borrowers. When rolling, far more is required to be borrowed just to stay even and cover interest rate costs. Below we use numbers from Federal Reserve branch to determine how much more it will cost.

The Federal Reserve Bank of St Louis (FRED), compiled data on the increased cost of US borrowing as a direct result of the Federal Reserve’s tighter monetary policy. The sheer magnitude of the amount borrowed, and the impact of interest rates make clear the US either will be increasing its borrowings, just to stay even with rollovers, or will need to cut back by spending. Cutting back spending removes economic stumulus. Below are the FRED numbers on how interest costs are expected to change.

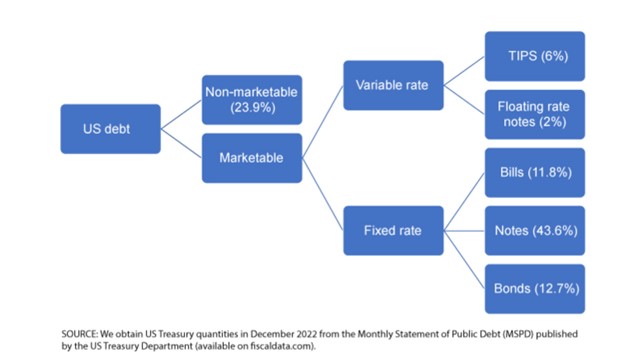

US Government Debt Breakdown

The total public debt, according to the US Treasury Department, is just over $31.4 trillion

Of the $31.4 trillion, about $7.5 trillion or 23.9% is nonmarketable debt—mainly consisting of the social security trust fund, military retirement funds, and the civil service retirement fund.

That leaves $23.9 trillion in marketable debt. $2.5 trillion is in variable-rate debt and increases when rates rise. The variable category is made up of Treasury inflation-indexed notes (TIPS) and floating-rate notes (FRNs). TIPS make up 6% of the overall US debt, have original maturities of 5, 10, or 30 years. FRNs make up only 2% of US debt, have maturity of 2 years, and interest payments are based on a fixed spread and a variable index rate calculated weekly.

Then there are $21.4 trillion in fixed-rate marketable securities. This final category contains bills, notes, and bonds, which make up 11.8%, 43.6%, and 12.7% of the US debt, respectively. The only differences in these instruments is that bills are discounted to yield the rate, while notes and bonds have semiannual interest rate payments. “notes” is the term used from 2-10 year maturities, bonds are from 10-20 years

Focusing only on the 68.1% fixed-rate of marketable U.S. debt, consisting of bills, notes, and bonds and for ease, using end of the year December 2022 to use specific securities and their roll dates, this is what the St. Louis Federal Reserve laid out.

The debt maturing each year has been broken down into different colors below by maturity. For example, the orange portion of the 2023 column represents two-year US Treasury debt maturing in the year 2023.

Notice about 30% of existing debt is maturing in 2023. And nearly 62% of existing US debt is coming due in the nine years after 2023. Finally, 18% of existing Treasury debt is very long dated and will not come due for at least 10 years. So 82% will reset at current rates within the next nine years.

Maturity Dispersion

Aside from quantity and maturity, the calculations aren’t complete without factoring in the yield of the current debt. Remember, the current interest rate levels are not the first time visiting 4% or higher.

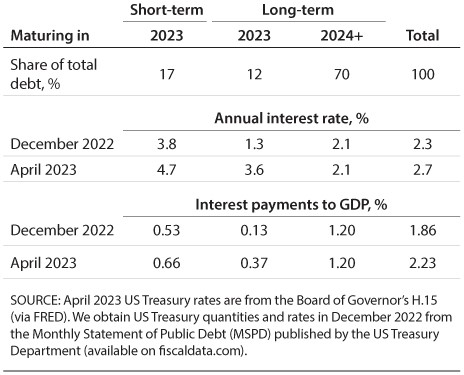

FRED used data on quantities and prices from December 2022 and compared it with the interest expense the US government would pay on the same quantity of debt using the new, higher interest rates in April 2023. Here, FRED assumed that the US government will keep the same debt schedule as in 2022. In other words, for any debt maturing during 2023, the government will issue another security with the same quantity and maturity—but at the new interest rate. They define short-term debt as any security with maturity less than or equal to one year and long-term debt as any security with maturity greater than one year.

Maturing Interest Rate, New Interest Rate

Short-term debt maturing in 2023 makes up about 17% of the outstanding. However, because this debt is short term, most of it had already been rolled over at higher interest rates in 2022. The December 2022 average rate on the short-term debt was already 3.8% and therefore increased only 0.9%—to 4.7%—in April. The long-term debt maturing in 2023 is almost 12% of debt, and the average rate increases from 1.3% to 3.6%, which is fairly large. Long-term debt maturing after 2024 will have the same interest rate, since the federal government is not rolling it over in 2023. Long-term debt makes up just over 70% of the existing debt.

To get some idea of the magnitude of $98 billion, the St. Louis Fed provided two examples: First, the Federal Reserve pays the Treasury Department revenue or remittances, which basically contain all remaining Fed revenue after operating expense. Fed remittances were $105 billion in 2021 and were negative $54 billion in 2022, in part due to the increases in interest rates. In 2021, this was an example of an inflow, or payment, to the government. Second, an example of an outflow, or expense incurred by the government, the US Department of Transportation spent $114 billion in 2022.

Bringing in the variable rate debt that we excluded earlier, the Congressional Budget Office (CBO) has forecasted for interest expense payments over GDP in the next 10 years. The CBO’s projections include variable-rate marketable securities—TIPS and FRNs—so they of course will of course be added to the fixed rate securities.

Take Away

What the US government spends, is generally stimulative. Money spent on interest would also seem to work its way into the system and be stimulative, but in the face of inflation, more goods or services is not necessarily attainable with the larger payments.

The US government had $21.4 trillion in outstanding US Treasury debt as of December 2022. Given large increases to interest rates over the past year, FRED estimated that it will cost the US government an additional $98 billion to pay interest on their debt in 2023.

The estimate is close to that made by the CBO as well. While the number seems large, relative to flows in and out of the US Treasury it is in line and not by comparison large.

The report from the Federal Reserve Branch concluded if long-term rates remain high, servicing the debt will become a larger and larger portion of the overall government expense.

The Importance Of Securities Research and Analysis May Inspire A Reversal in Regulations

The US Securities and Exchange Commission has avoided confrontation for a few years with European Union securities laws by extending exceptions to US brokers in the states that are subject to the EU’s MIFID II rules. The rules require that brokers charge clients separately for their analysis on stocks or bonds, and not provide it as an accommodation. In the US, charging for “advice” would cause brokers to have to register with FINRA as Investment Advisors – this opens up a new set of difficulties. The stand-off has been headed for a showdown for a while, and this coming July 3rd is when the SEC exception that exempts brokers expires.

Will Showdown be Averted?

The SEC exceptions to US brokers that have EU clients have been in place for five years, occasionally being extended – but the last extension expiring in a few weeks, may not get pushed out. SEC Chair Gary Gensler has been emphatic that he does not intend to extend any longer. The EU’s Markets in Financial Instruments directive threw a monkey wrench into a long-held custom of sell-side research by banning the common practice of accommodating clients by not directly charging for bond or equity analysis. Instead, in effect, “bundling” the service with research costs covered by trading commissions.

During the time that the EU has had MiFID II in place, an explicit price tag for research to investors has resulted in reduced company stock coverage. The new and growing concern is that the rules are hurting Europe’s financial markets — especially its small-caps. This is an important driver for the EU to consider a different tack.

Until now, without the SEC exemption from domestic rules, brokers in the huge US economy would have had to figure out how to take payment for research from their clients bound by MiFID. Or, alternatively, their clients would do without this important investment tool. The timeline is tight, but the problem for US brokers may be averted if the EU lawmakers act.

Will Europe Change Course?

With the SEC’s no-action letter expiring, the timing couldn’t be better. Investment firms following the rules of both regulators would cause a situation where US firms stop providing as much investment research to buy-side investors. Equity research is not only important to investors evaluating companies, but it is important to the companies themselves that need to be understood in order to attract capital and have enough active trading in their company to maintain suitable liquidity. This is especially true of small-cap and microcap stocks.

According to Reuters, the “states will seek a near total U-turn on the rules behind so-called unbundling.” MiFID II reforms, in place since 2018, may be adjusted to not conflict with the US model that separates brokers and investment advisors, requiring different licensing and different responsibilities of each.

The proposals suggest that an investment firm would only have to inform clients whether they are paying for research along with trading jointly, and record the charges attributable to each. This is different from unbundling, where from the client’s perspective, the research is a separate product, and decided on and paid for as an add-on to any other business.

Investors Could Win

While it was unclear how the showdown might come to an end, the new proposal, a dramatic turnaround from the EU on its current regulations, could finally resolve the regulator’s game of chicken and, at the same time, create an environment where investors benefit from more available information.

The original EU rule was intended to separate what lawmakers thought could be conflicts of interest when the selling broker also provides research while at the same time may have other banking and business relationships with the company it is providing research on.

The EU’s answer was to separate the two. But over time, according to Reuters, “evidence suggests research provision across the region has suffered as a result.” It lead to less research being distributed, which is viewed as negative to investors and the investor process.

What’s the Next Step?

The EU States’ plan talks with the European Parliament. The final shape of any regulatory changes will be decided in the negotiations, and the exact timetable for a conclusion is not yet clear.

Take Away

The prospect of a flip-flop on the MiFID rules comes at a key moment for the brokerage and securities research industries. In the US, a waiver allowing brokers to charge European clients separately for trading and for research is about to expire. At expiration, they’d have to adapt to the regulatory mismatch or drop the clients.

The drama is set against a very tight timeline.

As an interesting note, Channelchek is a platform that houses quality equity research and data on small and microcap companies. The information is at no cost to investors and is in no way tied to securities transactions. If you haven’t signed up to view this research, do this now.

This Week We’ll See if the Small-Cap Rally Continues, and Which Individual Stocks Move from the Russell Reconstitution

The FOMC interest rate pause at 5.00-5.25% last week created investor uncertainty as there was little forward guidance as the policymakers insist they remain data dependent. Chair Jerome Powell was emphatic in his comments to the press on Wednesday that getting inflation down to the 2 percent average inflation target is the FOMC’s unanimous goal – although there may be differences on the speed or level at which rates need to be adjusted.

Powell will have the spotlight again this week as he gives two testimony’s, the first on Wednesday before the House Financial Services Panel, and then on Thursday before the Senate Banking Committee.

While the mood of markets is still apprehensive, this did not stop the S&P 500 from rallying and reaching the highest weekly close since April 2022.

Monday 6/19

• US Markets closed in celebration of the Juneteenth holiday.

Tuesday 6/20

• 8:30 PM ET, May Housing starts are expected to hold steady after experiencing a bounce in April. Exonomists expect May’s starts to have been 1.433 million, they were 1.416 million in April.

Wednesday 6/21

• 10:00 AM ET, Federal Reserve Chairman Powell will appear before House Financial Services Panel.

• 10:00 AM – 4:00 PM ET, While Fed Chair Powell will be getting the attention as he reads prepared remarks and answers question, the day will be filled with other FOMC members speaking and sharing their view and outlook for the first time since the June FOMC meeting concluded. This includes Lisa Cook at 10:00 AM ET, Philip Jefferson also at 10:00 AM ET, Austan Goolsbee at 12:25 PM ET, and Loretta Mester at 4:00 PM ET.

Thursday 6/22

• 8:30 AM ET, Jobless Claims for the June 17 week, is expected to remain near the previous weeks level. The consensus is 261,000 versus 262,000 last week.

• 10:00 AM ET, Existing Home sales for May are expected to slip slightly to a 4.25 million rate. The National Association of Realtors described sales as “bouncing back and forth” but remaining “above recent cyclical lows.”

• 10:00 AM ET, Federal Reserve Chairman Powell will again be the focus as he appears before the Senate Banking Panel.

• 10:00 AM ET, The Index of Leading Indicators was down by 0.6 percent in April, for May it is expected to post a 14th straight decline, the consensus is down 0.7 percent. This index has been in sharp decline and has long been a trendline toward slow or no economic growth. signaling a pending recession.

• 4:30 PM ET, Factors Affecting Reserve Balances, otherwise known as The Fed’s Balance Sheet or the H.4.1 report is a weekly report of a consolidated balance sheet for all 12 Reserve Banks that lists factors supplying reserves into the banking system and factors absorbing reserves from the system. The report is officially named Factors Affecting Reserve Balances, otherwise known as the “H.4.1” report.

Friday 6/23

• 9:45 AM ET, The Purchasing Managers Index (PMI) is not expected to show significant change in June compared to May; manufacturing underperformed at 48.5 and services even though services were strong at 53.5.

What Else

On Friday the Russell Indexes will have new components beginning the moment the market closes. The following Monday morning the indexes will reflect these changes, and index funds that are designed to match the performance of the funds will hopefully have gotten their trades off in time. Expect some interesting moves of a few stocks on Friday as a result.

Small-cap stocks have joined the stock market rally in June and, according to an article in Morningstar, “trouncing the larger indexes.”

Noble Capital Markets has been hosting road shows of interesting small-cap companies in various cities and towns throughout the US. This week features a very busy week with company’s speaking to potential investors in St. Louis and Florida. Also there will be two virtual events, so that no one is excluded by geography. Become informed here.

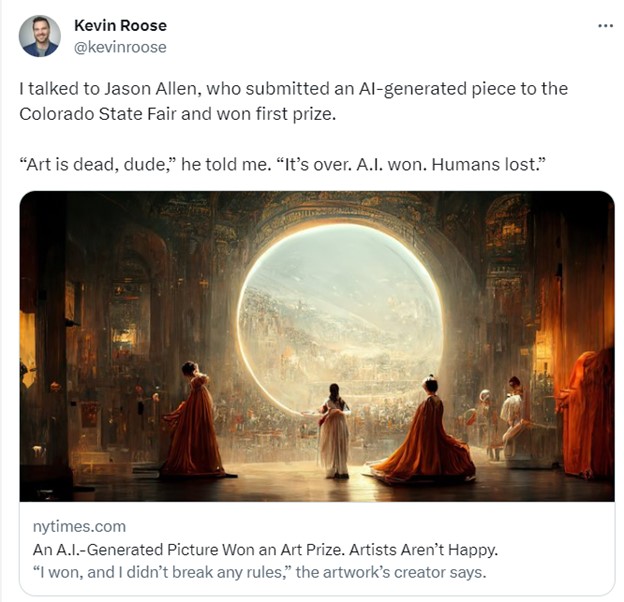

Will Copyright Law Favor Artificial Intelligence End Users?

In 2022, an AI-generated work of art won the Colorado State Fair’s art competition. The artist, Jason Allen, had used Midjourney – a generative AI system trained on art scraped from the internet – to create the piece. The process was far from fully automated: Allen went through some 900 iterations over 80 hours to create and refine his submission.

Yet his use of AI to win the art competition triggered a heated backlash online, with one Twitter user claiming, “We’re watching the death of artistry unfold right before our eyes.”

As generative AI art tools like Midjourney and Stable Diffusion have been thrust into the limelight, so too have questions about ownership and authorship.

These tools’ generative ability is the result of training them with scores of prior artworks, from which the AI learns how to create artistic outputs.

Should the artists whose art was scraped to train the models be compensated? Who owns the images that AI systems produce? Is the process of fine-tuning prompts for generative AI a form of authentic creative expression?

This article was republished with permission from The Conversation, a news site dedicated to sharing ideas from academic experts. It represents the research-based findings and thoughts of, Robert Mahari, JD-PhD Student, Massachusetts Institute of Technology (MIT), Jessica Fjeld, Lecturer on Law, Harvard Law School, and Ziv Epstein, PhD Student in Media Arts and Sciences, Massachusetts Institute of Technology (MIT).

On one hand, technophiles rave over work like Allen’s. But on the other, many working artists consider the use of their art to train AI to be exploitative.

We’re part of a team of 14 experts across disciplines that just published a paper on generative AI in Science magazine. In it, we explore how advances in AI will affect creative work, aesthetics and the media. One of the key questions that emerged has to do with U.S. copyright laws, and whether they can adequately deal with the unique challenges of generative AI.

Copyright laws were created to promote the arts and creative thinking. But the rise of generative AI has complicated existing notions of authorship.

Photography Serves as a Helpful Lens

Generative AI might seem unprecedented, but history can act as a guide.

Take the emergence of photography in the 1800s. Before its invention, artists could only try to portray the world through drawing, painting or sculpture. Suddenly, reality could be captured in a flash using a camera and chemicals.

As with generative AI, many argued that photography lacked artistic merit. In 1884, the U.S. Supreme Court weighed in on the issue and found that cameras served as tools that an artist could use to give an idea visible form; the “masterminds” behind the cameras, the court ruled, should own the photographs they create.

From then on, photography evolved into its own art form and even sparked new abstract artistic movements.

AI Can’t Own Outputs

Unlike inanimate cameras, AI possesses capabilities – like the ability to convert basic instructions into impressive artistic works – that make it prone to anthropomorphization. Even the term “artificial intelligence” encourages people to think that these systems have humanlike intent or even self-awareness.

This led some people to wonder whether AI systems can be “owners.” But the U.S. Copyright Office has stated unequivocally that only humans can hold copyrights.

So who can claim ownership of images produced by AI? Is it the artists whose images were used to train the systems? The users who type in prompts to create images? Or the people who build the AI systems?

Infringement or Fair Use?

While artists draw obliquely from past works that have educated and inspired them in order to create, generative AI relies on training data to produce outputs.

This training data consists of prior artworks, many of which are protected by copyright law and which have been collected without artists’ knowledge or consent. Using art in this way might violate copyright law even before the AI generates a new work.

Still from ‘All watched over by machines of loving grace’ by Memo Akten, 2021. Created using custom AI software. Memo Akten, CC BY-SA

For Jason Allen to create his award-winning art, Midjourney was trained on 100 million prior works.

Was that a form of infringement? Or was it a new form of “fair use,” a legal doctrine that permits the unlicensed use of protected works if they’re sufficiently transformed into something new?

While AI systems do not contain literal copies of the training data, they do sometimes manage to recreate works from the training data, complicating this legal analysis.

Will contemporary copyright law favor end users and companies over the artists whose content is in the training data?

To mitigate this concern, some scholars propose new regulations to protect and compensate artists whose work is used for training. These proposals include a right for artists to opt out of their data’s being used for generative AI or a way to automatically compensate artists when their work is used to train an AI.

Muddled Ownership

Training data, however, is only part of the process. Frequently, artists who use generative AI tools go through many rounds of revision to refine their prompts, which suggests a degree of originality.

Answering the question of who should own the outputs requires looking into the contributions of all those involved in the generative AI supply chain.

The legal analysis is easier when an output is different from works in the training data. In this case, whoever prompted the AI to produce the output appears to be the default owner.

However, copyright law requires meaningful creative input – a standard satisfied by clicking the shutter button on a camera. It remains unclear how courts will decide what this means for the use of generative AI. Is composing and refining a prompt enough?

Matters are more complicated when outputs resemble works in the training data. If the resemblance is based only on general style or content, it is unlikely to violate copyright, because style is not copyrightable.

The illustrator Hollie Mengert encountered this issue firsthand when her unique style was mimicked by generative AI engines in a way that did not capture what, in her eyes, made her work unique. Meanwhile, the singer Grimes embraced the tech, “open-sourcing” her voice and encouraging fans to create songs in her style using generative AI.

If an output contains major elements from a work in the training data, it might infringe on that work’s copyright. Recently, the Supreme Court ruled that Andy Warhol’s drawing of a photograph was not permitted by fair use. That means that using AI to just change the style of a work – say, from a photo to an illustration – is not enough to claim ownership over the modified output.

While copyright law tends to favor an all-or-nothing approach, scholars at Harvard Law School have proposed new models of joint ownership that allow artists to gain some rights in outputs that resemble their works.

In many ways, generative AI is yet another creative tool that allows a new group of people access to image-making, just like cameras, paintbrushes or Adobe Photoshop. But a key difference is this new set of tools relies explicitly on training data, and therefore creative contributions cannot easily be traced back to a single artist.

The ways in which existing laws are interpreted or reformed – and whether generative AI is appropriately treated as the tool it is – will have real consequences for the future of creative expression.

DALLAS, June 16, 2023 (GLOBE NEWSWIRE) — Permex Petroleum Corporation (CSE: OIL) (OTCQB: OILCF) (FSE: 75P0) (“Permex” or the “Company“), is pleased to announce the extension of its early warrant exercise program (the “Program”), as initially announced by the Company in its news release dated May 18, 2023 (the “Initial News Release”).

The Program was announced with the intention to encourage the exercise of up to 1,015,869 unlisted common share purchase warrants of the Company (the “Eligible Warrants”). Pursuant to the Program, the Company amended the exercise price of the outstanding Eligible Warrants to USD$2.86 per Eligible Warrant, from May 18, 2023, at 9:00 a.m. (Vancouver time) until June 16, 2023 at 5:00 p.m. (Vancouver time). The Company now wishes to extend the Program until June 30, 2023 at 5:00 p.m. (the “Extended Exercise Deadline”).

As part of the Program, the Company will also offer, to each holder of Eligible Warrants (the “Warrant Holders”) who exercises any Eligible Warrants until the Extended Exercise Deadline, the issuance of one additional common share purchase warrant for each such exercised Eligible Warrant (each, an “Incentive Warrant”). Each Incentive Warrant entitles the Warrant Holder to purchase one common share of the Company (each, a “Share”) for a period of 5 years from the date of issuance, at a price of USD$4.50 per Share. The Company may also issue pre-funded common share purchase warrants (each, a “Pre-Funded Warrant”) in lieu of Shares, upon the exercise of Eligible Warrants, to certain Warrant Holders. Each Pre-Funded Warrant will allow the holder thereof to acquire one Share at a nominal exercise price of USD$0.01 and will not expire.

The Eligible Warrants which remain unexercised following the completion of the Extended Early Deadline will continue to be exercisable, on the terms existing immediately prior to the implementation of the Program, and no further Incentive Warrants will be granted on the exercise of the Eligible Warrants following the Extended Exercise Deadline.

For additional information on the Program, please refer to the Initial News Release.

The Incentive Warrants, and any securities issuable on the exercise thereof, will be subject to a four-month hold period from the date of issuance pursuant to applicable Canadian securities laws, in addition to such other restrictions as may apply under applicable securities laws of jurisdictions outside of Canada. None of the securities issued in connection with the Program will be registered upon issuance under the United States Securities Act of 1933, as amended (the “1933 Act“), and none of them may be offered or sold in the United States absent registration or an applicable exemption from the registration requirements of the 1933 Act. The Company has agreed to file a registration statement with the U.S. Securities and Exchange Commission to register the Shares within 30 days of the end of the Extended Exercise Deadline. This news release shall not constitute an offer to sell or a solicitation of an offer to buy nor shall there be any sale of the securities in any state where such offer, solicitation, or sale would be unlawful.

Or for investor relations, please contact: Renmark Financial Communications Inc. Steve Hosein: shosein@renmarkfinancial.com Tel.: (416) 644-2020 or (212)-812-7680 www.renmarkfinancial.com

Forward Looking Statements

This release includes certain statements and information that may constitute forward-looking information within the meaning of applicable Canadian and United States securities laws. Forward-looking statements relate to future events or future performance and reflect the expectations or beliefs of management of the Company regarding future events. Generally, forward-looking statements and information can be identified by the use of forward-looking terminology such as “intends” or “anticipates”, or variations of such words and phrases or statements that certain actions, events or results “may”, “could”, “should”, “would” or “occur”. This information and these statements, referred to herein as “forward‐looking statements”, are not historical facts, are made as of the date of this news release and include without limitation, statements regarding discussions of future plans, estimates and forecasts and statements as to management’s expectations and intentions with respect to, among other things: the anticipated timing and completion of the Program.

These forward‐looking statements involve numerous risks and uncertainties and actual results might differ materially from results suggested in any forward-looking statements. These risks and uncertainties include, among other things: delays in obtaining or failures to obtain required regulatory approvals for the Program from the CSE; market uncertainty; and the inability of the Company to raise proceeds pursuant to the Program.

In making the forward-looking statements in this news release, the Company has applied several material assumptions, including without limitation, that: the Company will obtain the required CSE approval for the Program; and the Company will be able to raise proceeds under the Program.

Although management of the Company has attempted to identify important factors that could cause actual results to differ materially from those contained in forward-looking statements or forward-looking information, there may be other factors that cause results not to be as anticipated, estimated or intended. There can be no assurance that such statements will prove to be accurate, as actual results and future events could differ materially from those anticipated in such statements. Accordingly, readers should not place undue reliance on forward-looking statements and forward-looking information. Readers are cautioned that reliance on such information may not be appropriate for other purposes. The Company does not undertake to update any forward-looking statement, forward-looking information or financial out-look that are incorporated by reference herein, except in accordance with applicable securities laws. We seek safe harbor.

DALLAS, June 16, 2023 (GLOBE NEWSWIRE) — Permex Petroleum Corporation (CSE: OIL) (OTCQB: OILCF) (FSE:75P0) (“Permex” or the “Company”) announces that it has retained Renmark Financial Communications USA Inc. (“Renmark”), an arm’s length party to the Company, to provide investor relations services (the “Services”) to the Company.

Renmark was engaged to heighten market and investor awareness for the Company and broaden the Company’s reach within the investment community. In implementing its investor relations program, Renmark employs a number of different communication methods, including live phone calls and emails. To reach new potential investors, for an additional set-up fee, Renmark will organize virtual non-deal roadshows for senior management in zones across the USA, Canada, and Europe. Additionally, Renmark will ensure the timely disclosure of Company information to existing and potential shareholders and electronically send documents and factsheets to prospective shareholders.

Renmark has been engaged by the Company for an initial 7-month period (the “InitialTerm”) which commenced on May 1, 2023; the term will automatically continue after the Initial Term on a monthly basis, unless terminated in accordance with the investor relations agreement (the “Agreement”) among the parties.

As consideration for the Services, the Company will pay Renmark a monthly fee of USD$9,000, (the “MonthlyService Fee”) during the Initial Term. The Monthly Service Fee becomes payable on the first day of each month during the Initial Term. Renmark is also entitled to reimbursement for all expenses reasonably incurred, subject to the terms of the Agreement.

The Company and Renmark act at arm’s length, and Renmark has no present interest, directly or indirectly, in the Company or its securities, or any right or present intent to acquire such an interest.

About Permex Petroluem Corporation

Permex Petroleum is a uniquely positioned junior oil & gas company with assets and operations across the Permian Basin of West Texas and the Delaware Sub-Basin of New Mexico. The Company focuses on combining its low-cost development of Held by Production assets for sustainable growth with its current and future Blue-Sky projects for scale growth. The Company, through its wholly owned subsidiary, Permex Petroleum US Corporation, is a licensed operator in both states, and owns and operates on private, state and federal land. For more information, please visit www.permexpetroleum.com.

About Renmark Financial Communications USA Inc.

Renmark Financial Communications is a full-service investor relations firm representing small, medium, and large cap public companies trading on all major North American exchanges. Renmark facilitates connections between their clients and key stakeholders in order to assist their clients in efficiently achieving their milestones. Renmark has offices in Toronto, Montreal, New York, and Atlanta.

Or for Investor Relations, please contact: Renmark Financial Communications Inc. 121 King Street West Suite 1140 Toronto ON M5H 3T9

Steve Hosein: shosein@renmarkfinancial.com Tel.: (416) 644-2020 or (212)-812-7680 www.renmarkfinancial.com

Forward-Looking Statements

This news release contains forward-looking statements relating to Renmark heightening the market and investor awareness of the Company and broadening the Company’s reach within the investment community, fees payable to Renmark, and other statements that are not historical facts. Forward-looking statements are often identified by terms such as “will”, “may”, “should”, “anticipate”, “expects” and similar expressions. All statements other than statements of historical fact, included in this release are forward-looking statements that involve risks and uncertainties. There can be no assurance that such statements will prove to be accurate and actual results and future events could differ materially from those anticipated in such statements. Important factors that could cause actual results to differ materially from the Company’s expectations include those relating to the ability of Renmark to heighten the market and investor awareness of the Company and broaden the Company’s reach within the investment community, and other risks detailed from time to time in the filings made by the Company with securities regulations.

The reader is cautioned that assumptions used in the preparation of any forward-looking informationmay provetobeincorrect.Eventsorcircumstancesmaycauseactualresultstodiffermateriallyfromthose predictedasaresultofnumerousknownandunknownrisks,uncertainties,andotherfactors,manyof which are beyond the control of the Company. The reader is cautioned not to place undue reliance onany forward-looking information. Such information, although considered reasonable by management atthe time of preparation, may prove to be incorrect and actual results may differ materially fromthose anticipated.Forward-lookingstatementscontainedinthisnewsreleaseareexpresslyqualifiedbythis cautionarystatement.Theforward-lookingstatementscontainedinthisnewsreleasearemadeasofthe dateofthisnewsreleaseandtheCompanywillupdateorrevisepubliclyanyoftheincludedforward- looking statements as expressly required by applicablelaw.

CALGARY, AB, June 15, 2023 /CNW/ – Alvopetro Energy Ltd. (TSXV: ALV) (OTCQX: ALVOF) announces that our Board of Directors has declared a quarterly dividend of US$0.14 per common share, payable in cash on July 14, 2023, to shareholders of record at the close of business on June 30, 2023. This dividend is designated as an “eligible dividend” for Canadian income tax purposes.

Dividend payments to non-residents of Canada will be subject to withholding taxes at the Canadian statutory rate of 25%. Shareholders may be entitled to a reduced withholding tax rate under a tax treaty between their country of residence and Canada. For further information, see Alvopetro’s website at https://alvopetro.com/Dividends-Non-resident-Shareholders.

Alvopetro Energy Ltd.’svision is to become a leading independent upstream and midstream operator in Brazil. Our strategy is to unlock the on-shore natural gas potential in the state of Bahia in Brazil, building off the development of our Caburé natural gas field and our strategic midstream infrastructure.

Neither the TSX Venture Exchange nor its Regulation Services Provider (as that term is defined in the policies of the TSX Venture Exchange) accepts responsibility for the adequacy or accuracy of this news release.

All amounts contained in this new release are in United States dollars, unless otherwise stated and all tabular amounts are in thousands of United States dollars, except as otherwise noted.

Forward-Looking Statements and Cautionary Language.This news release contains “forward-looking information” within the meaning of applicable securities laws. The use of any of the words “will”, “expect”, “intend” and other similar words or expressions are intended to identify forward-looking information. Forward–looking statements involve significant risks and uncertainties, should not be read as guarantees of future performance or results, and will not necessarily be accurate indications of whether or not such results will be achieved. A number of factors could cause actual results to vary significantly from the expectations discussed in the forward-looking statements. These forward-looking statements reflect current assumptions and expectations regarding future events. Accordingly, when relying on forward-looking statements to make decisions, Alvopetro cautions readers not to place undue reliance on these statements, as forward-looking statements involve significant risks and uncertainties. More particularly and without limitation, this news release contains forward-looking information concerning the Company’s plans for dividends in the future, the timing and amount of such dividends and the expected tax treatment thereof. The forward–looking statements are based on certain key expectations and assumptions made by Alvopetro, including but not limited to equipment availability, the timing of regulatory licenses and approvals, the success of future drilling, completion, testing, recompletion and development activities, the outlook for commodity markets and ability to access capital markets, the impact of the COVID-19 pandemic and other significant worldwide events, the performance of producing wells and reservoirs, well development and operating performance, foreign exchange rates, general economic and business conditions, weather and access to drilling locations, the availability and cost of labour and services, environmental regulation, including regulation relating to hydraulic fracturing and stimulation, the ability to monetize hydrocarbons discovered, expectations regarding Alvopetro’s working interest in properties and the outcome of any redeterminations, the regulatory and legal environment and other risks associated with oil and gas operations. The reader is cautioned that assumptions used in the preparation of such information, although considered reasonable at the time of preparation, may prove to be incorrect. Actual results achieved during the forecast period will vary from the information provided herein as a result of numerous known and unknown risks and uncertainties and other factors. In addition, the declaration, timing, amount and payment of future dividends remain at the discretion of the Board of Directors. Although Alvopetro believes that the expectations and assumptions on which such forward-looking information is based are reasonable, undue reliance should not be placed on the forward-looking information because Alvopetro can give no assurance that it will prove to be correct. Readers are cautioned that the foregoing list of factors is not exhaustive. Additional information on factors that could affect the operations or financial results of Alvopetro are included in our annual information form which may be accessed on Alvopetro’s SEDAR profile at www.sedar.com. The forward-looking information contained in this news release is made as of the date hereof and Alvopetro undertakes no obligation to update publicly or revise any forward-looking information, whether as a result of new information, future events or otherwise, unless so required by applicable securities laws.

PDS Biotech is a clinical-stage immunotherapy company developing a growing pipeline of molecularly targeted cancer and infectious disease immunotherapies based on the Company’s proprietary Versamune® and Infectimune™ T-cell activating technology platforms. Our Versamune®-based products have demonstrated the potential to overcome the limitations of current immunotherapy by inducing in vivo, large quantities of high-quality, highly potent polyfunctional tumor specific CD4+ helper and CD8+ killer T-cells. PDS Biotech has developed multiple therapies, based on combinations of Versamune® and disease-specific antigens, designed to train the immune system to better recognize diseased cells and effectively attack and destroy them. The Company’s pipeline products address various cancers including HPV16-associated cancers (anal, cervical, head and neck, penile, vaginal, vulvar) and breast, colon, lung, prostate and ovarian cancers.

Robert LeBoyer, Senior Vice President, Equity Research Analyst, Biotechnology, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

The Phase 2 VERSATILE-002 Trial Remains Misunderstood. We have received inquiries from investors about the data in the recent ASCO presentation by PDS Biotech. We believe there is some misunderstanding of the trial design, outcome data, and the trial’s definition of efficacy. In view of the fundamental progress and stock price decline, we believe this is a buying opportunity.

Trial Data Has Led To Misinterpretation. The Phase 2 VERSATILE-002 trial has a primary endpoint of best overall response rate (ORR). To be considered a responder, patients need to have tumor shrinkage of at least 30% in two MRI scans. Patients with one positive scan are considered unconfirmed responses until they have a second confirming scan at least 9 weeks later. Both confirmed and unconfirmed responses were reported at the recent ASCO conference.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

Mark Reichman, Managing Director, Equity Research Analyst, Natural Resources, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

All resolutions passed. Aurania Resources hosted an Annual and Special Meeting on June 14th during which shareholders approved all resolutions, including the election of directors, the appointment of Aurania’s external auditor, the incentive stock option plan for the upcoming year, and amendments to the company’s restricted stock unit plan. The formal part of the meeting was followed by an update from Aurania’s Chairman, President and CEO, Dr. Keith Barron. We anticipate the company may elaborate on Dr. Barron’s comments during the meeting shortly.

Interim funding. Dr. Barron recently extended the company an unsecured loan of C$2,000,000 bearing an interest rate of 2% per annum. The loan will help fund the company’s corporate expenses and working capital needs, along with exploration expenses in Ecuador. The company will likely need to raise additional capital to fund its exploration and drilling plans for the remainder of the year.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

Investors Already Wary of Big Tech’s Dizzying Heights May Deviate Away From Swelling Large Cap Weightings

What’s different about this year’s Russell Index Reconstitution?

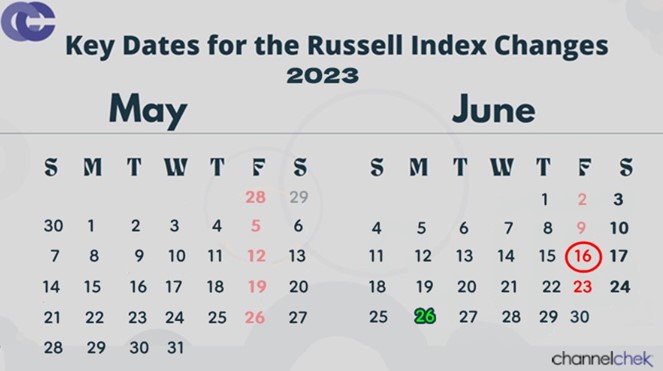

When the market closes on Friday, June 23rd , the overall FTSE Russell 3000 index and the other indexes that it impacts, including the Russell 1000 Large-cap and Russell 2000 Small-cap index, will be rebalanced to reflect current market-cap size. When the bell rings on Monday June 26th, the indexes will have different members and adjusted weighting of those constituents. Some market watchers and analysts expect this year to be a “headache” for active portfolio managers. Here’s why.

The new FTSE Russell makeup is already known. There is only a small chance a change in that might occur between now and Friday, it is largely assured that the reconstitution will increase the concentration of the top ten biggest companies in the large-cap Russell 1000 Index to a historical high of 29%. Active managers that are already underweighted mega-caps and big tech represented in the large-cap indexes will have to decide if they are going to increase holdings or be even more underweighted in comparison to an index that investors are likely to compare them to.

Additionally, while active fund managers are freer to weight their portfolios (within the boundaries of the fund’s prospectus), investors tend to compare the returns of index funds to the performance of managed funds when investing. This would increase the size of the bet in terms of fund percentage for managed funds, some already underweighted in tech. They’ll have a decision to make.

Further confusing things on the large-cap side is that the wisdom of diversification is being tested. If ten of the largest company’s make up 29% of an index, one that financial advisors and mom-and-pop investors are comparing them to, then roughly mimicking its concentrations would reduce diversification. Investing in a fund with a more even balance of stocks had once been the primary driver of mutual funds’ growth in popularity.

The rebalancing will heap a higher weighting to mega-cap names, including those referred to as FAANG stocks. This group of companies have already had tremendous gains this year, a pace that history would indicate is not sustainable.

Just look at the numbers, as we near the mid-year mark in 2023.

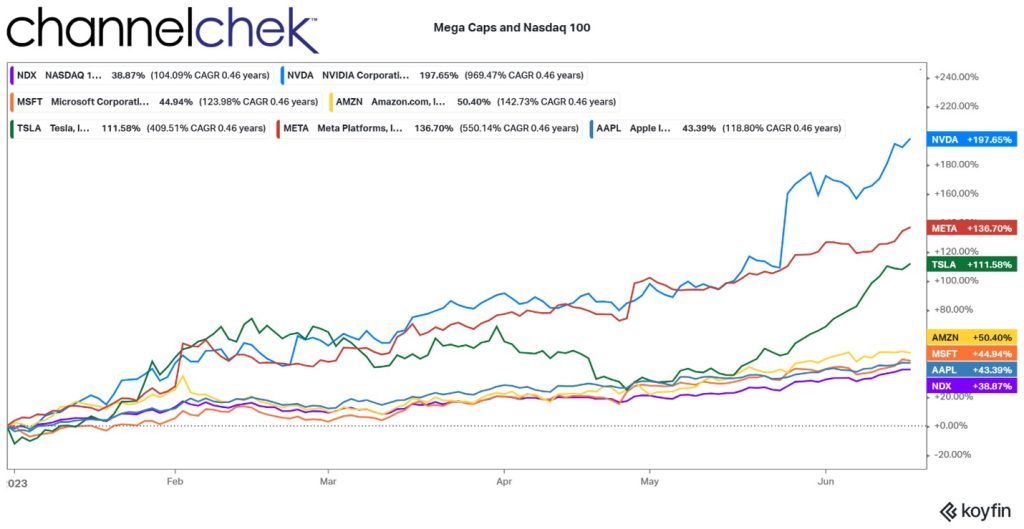

To date the top 100 stocks in the Nasdaq, heavily weighted with mega-caps and large-cap tech, has increased 38.87%. Using historical returns, most would forecast that these topstocks have much more downside for the next six months than upside. Yet, to stay on the same playing field with index funds, managed money would have to bet against stock market history.

The largest of stocks, as demonstrated below, are pulling a lot of weight. Nvidia (NVDA) is up nearly 200%, Meta (META) returned 137%, Tesla (TSLA) is also up over 100%. A fund manager with flexibility could be torn; on the one hand, afraid to bet against such momentum, on the other, historical probabilities suggest they should.

There’s recent evidence that portfolio managers are looking for value away from the mega-cap stocks that have had the kind of run that in some cases made them twice as expensive. The Russell Small-cap Index, which is part of the June rebalancing is made up of the lowest 2,000 companies in terms of market cap of the broader Russell 3000. June has been a great month for the index so far. The index month-to-date is up 7.75% compared to the Nasdaq 100’s 6.56%. This beats June’s returns for Microsoft (MSFT), Apple (AAPL), and Amazon, among others. The performance, which includes an increase of 3.6% and a 2.8% jump on June 6th indicates investors are rotating away from large-cap stocks that have become historically expensive and into smaller companies that are cheap by historical standards.

The reconstitution also provides investors in the weeks and hours leading up to the rebalance to speculate on how the rebalance will impact individual stocks. Since the preliminary list of changes was announced last month, companies expected to be added to the Russell 1000 Index have gained 4.9%, while the those that moved to a smaller-cap index have grown 11.3%, according to data compiled by Wells Fargo (6/14/23).

Take Away

The Russell Reconstitution elevates the percentage weighting of mega-cap tech stocks that usually trade in rough tandem. Mutual fund managers, and other managed money will have to rethink their weighting of a sector that has already skyrocketed on speculation of future growth.

There has already been signs of a slowdown of interest in mega-tech, compared to a significant increase in attention to small-caps that are cheap by most measures. If the rotation continues, money managers that adhere to tried and true wisdom related to diversification, and metrics like P/E ratios, may wind up the year outperforming the indexed funds they tend to be compared to.

June Quad-Witching is the Friday Before a Three-Day Weekend

Double, triple, and quadruple witching hours are often characterized by increased stock market activity as traders manage expiring positions in the last hours of trading. Friday, June 16th is a quadruple witching which may demonstrate increased activity as it leads into a weekend where markets are closed on Monday.

The term “quadruple witching hour” is used to describe the simultaneous expiration of stock options, stock index futures, and stock index options and single stock futures contracts on the same day. This happens only four times a year on the third Friday just before a quarter end. The same expiration date of all three types of stock derivatives can cause unusual swings as expiring derivative positions can cause increased trading volume and unusual price action in the underlying assets as traders close, roll, or offset expiring derivative positions, particularly in the final hour of trading.

Options Expirations and Futures Contracts

Stock index options, and stock options, are financial instruments that grant the holder the contractual right, but not the obligation, to buy (call option), or sell (put option) a specific quantity of an underlying security or value of an underlying index at a predetermined price (strike price) within a specified period. The final day of the period is known as the option’s expiration date.

Stock index options are options based on the broad market indexes, such as the S&P 500 or the NASDAQ-100. These options give investors exposure to the overall market’s performance rather than individual stocks.

Stock options work similarly, but are based not on index values, but on stock price.

Stock index futures and single stock index futures are contracts that obligate (not optional) traders to buy or sell an index at a specific price or a single stocks at a specific price on a future date.

Expiration Fridays often witness heightened trading activity, as investors attempt to rebalance portfolios and positions. This can cause increased volume and produce significant price fluctuations in the underlying, impacting both individual stocks and the overall market.

Arbitrage Opportunities

Though much of the trading in closing, opening, and offsetting futures and options contracts during witching days is related to the squaring of positions, this increased, and at times, frantic activity can create price inefficiencies, this may provide short-term arbitrage opportunities for those skilled and quick enough.

The arbatrageurs would generate even more volume into the close on quadruple witching days as traders attempt to profit on small price imbalances with large trades that may execute a buy and sell in seconds.

Additional Reasons To Care About Triple Witching

As four types of derivatives, with related underlying indexes and securities expire, traders, especially before a long weekend, will often seek to close out all of their open positions well in advance of the close. This can lead to increased trading volume and intraday swings. Traders with large short positions are particularly exposed to price movements that could be more difficult to manage leading up to expiration. Arbitrageurs try to take advantage of abnormal price action, this actually serves to keep prices more in synch.

The higher trading volumes can be one-sided and potentially result in wider bid-ask spreads and greater slippage. Investors mindful of the potential one-sided liquidity challenges may decide to wait for the smoke to clear the following week, or see if they can benefit by feeding into demand if they can.

Traders who are skilled at interpreting trends, and have great execution, may find quick opportunities to make money during these multiple expiration dates.

Take Away

Quadruple expiration dates, which happen four times a year, can have significant implications for traders and investors. It is best to, at a minimum, know the dates to understand unusual price moves. Understanding the intricacies of option expiration, and multiple witching hours helps investors navigate markets. Advanced traders may even find ways to capitalize on the moves intraday.

June 2023 is unusual in that the quadruple witching hour comes before a three-day weekend; this could push more volatility to earlier periods during the afternoon.