Selling Air Time is Getting Easier for Broadcast Radio

Is broadcast radio losing its power? It doesn’t appear to be, and the medium may be of interest to investors that prefer to shy away from short-lived investment trends and instead look to more easily understood opportunities. According to the industry publication Ad Age, the industry is nearing an intersection where “18- to 49-year-olds are spending more time listening to radio than watching linear TV.” At least one large company has reworked its advertising budget to save money with the expectation of reaching more people. Is this a trend hat will grow?

Re-investing in Radio

Soap opera’s got their start nearly 100 years ago as Proctor and Gamble, manufacturer of soap and candles, created the addictive entertainment to position its product ads in front of the typical soap decision maker of the time. As TV became a fixture in households in the 1950s, P&G adapted and brought the shows and the advertising to television. Last year P&G increased its spending on traditional broadcast radio by 43%. Despite all the new advertising options available, and the ability to refine targeting, P&G has a method to their madness, and it’s worth understanding.

Why the Reversal?

Last year, in the face of rising costs, the marketing giant came under margin pressure. In an attempt to minimize price hikes and maintain old margins, they cut ad spending by 10%, with a new budget of $2.2 billion.

The CEO Jon Moeller had told P&G brand marketers to focus on how many people they reach and how often, rather than how targeted or how much they spend. Chief Brand Officer Marc Pritchard became focused on the effectiveness of radio, connected TV, and streaming free ad-supported TV (FAST).

Belt Tightening

Just as inflation has caused many households to be more frugal, perhaps use less expensive brands, and eat more at home, companies like P&G are finding they are taking a similar approach. And if it helps keep prices down, they can more easily retain customers and attract new ones.

Here is some data on the extreme cost of reaching a broadcast TV audience. In the business, CPM (cost per mile) is a paid ad method where there is a certain rate for every 1000 impressions an ad receives. The CPM to reach TV audiences is as high as $35 to $65. For comparison, YouTube video CPMs range from $20 to $25, and linear TV is in the $10 to $15 range.

But radio can be bought in the $5-$6 CPM range. The targeting may not be as precise as broadcast TV or other media, but the amount spent for every 1000 impressions is a fraction of the alternatives.

Other large advertisers are stepping up their radio efforts as well. Pharmaceutical companies Pfizer, and Johnson & Johnson have started to spend more. According ad intelligence provider Vivvix. Pfizer became a top-five radio advertiser last year. They did this by more than doubling spending.

If you haven’t been following media companies, there is some acclimating to terminology, seasons, and how they profit. Two key places for information is the media report that Noble Capital Markets published late January of this year. The report which is available at this link was prepared by top analysts and discusses the recent state of radio, TV, digital media, and publishing.

A video produced just weeks before the published report by members of the same team can be helpful in providing you with insight as to one media company’s strengths over another. The video, featuring Michael Kupinski, Director of Research at Noble Capital Markets, is a half-hour full of insights. At this link.

Do you wish to hear directly from management of broadcast media companies impacted by new trends?

There are two companies that will be conducting three roadshows in Florida over the next two weeks. If you can attend, you’ll have the opportunity to hear directly from management what the future expectations are, and you’ll have the opportunity to ask questions of your own. The company names, locations and dates are available at this link,along with other scheduled roadshows.

Take Away

The most talked about stocks on the chat boards aren’t the only actionable opportunities astute investors can select from. As with all investing, growing your knowledge base can help one expand their watch-list.

P&G’s ad spend adjustment comes at a time when standard AM/FM radio has caught to and is neck and neck with linear TV (for people 18-49 in the U.S.). Radio audiences may not be growing, but they are not declining as broadcast TV audiences have – they are fairly consistent, and ad costs are a great value at a time when companies are dealing with their own increasing costs. This is getting the attention of large advertisers, and it perhaps should get the attention of investors.

Much of the Noise this Week Could Be from Outside of US Markets?

The U.S. does not get a great deal of economic data to react to this week. But that usually means the focus shifts, and market participants grasp onto signs they may otherwise ignore. There are many inflation reports during the week. They are from outside of the U.S. economy until Friday morning. Global inflation, not just trading partners could impact other nations. This is because if one region raises its benchmark interest rate, others either follow or risk weakening its own native currency.

March German inflation will come late in the week, starting with Germany’s CPI on Thursday. This will be followed by France’s CPI on Friday, then the full Eurozone later Friday. February PCE data from the U.S. will also be posted on Friday. Australia will be posting its February CPI on Wednesday. Most reports are expected to show declines, with the reservation that much of the reduced increases are derived from lower fuel costs. This would suggest that economic forces raising prices are still largely at work.

Monday 3/27

• No pertinent Economic numbers are to be released

Tuesday 3/28

• 10:00 AM ET, Consumer Confidence, after two months of market surprising declines, the consumer confidence index is not expected to perk up in March, the consensus is instead a further decline in confidence to a consensus 101.0 versus February’s 102.9.

• 10:00 AM ET, Michael Barr, the Vice Chair for Supervision at the Federal Reserve will give Testimony before the Michael Barr, the Vice Chair for Supervision at the Federal Reserve will give Testimony before the U.S. Senate Committee on Banking, Housing, and Urban Affairs. Watch here.

• 1:00 PM ET, Money Supply, since some banks have experienced difficulties with lower deposits, is becoming closely watch report once more. The prior month, money supply read 30.9 billion. The measure has two main components, M1 and M2. M1 is included in M2. M1, the more narrowly defined measure, consists of the most liquid forms of money, namely currency and checkable deposits. The non-M1 components of M2 are primarily household holdings of savings deposits, small time deposits, and retail money market mutual funds.

Wednesday 3/29

• 10:00 AM ET, Michael Barr will testify before the U.S. House Financial Services CommitteeThe Energy Information Administration (EIA) Petroleum Status Report, provides weekly information on petroleum inventories in the U.S., whether produced here or abroad. The level of inventories helps determine prices for petroleum products.

• 10:00 AM ET, Pending Home Sales during February are expected to rise 1.0 percent on top of January’s 8.1 percent elevation.

Thursday 3/30

• 8:30 AM ET, GDP’s third estimate for 4Q 2022 is expected to remain at 2.7 percent growth in the quarter’s second estimate. Personal consumption expenditures, at 1.4 percent growth in the second estimate, is also expected to remain unchanged.

• 4:30 PM ET, The Fed’s Balance Sheet has received more attention since the beginning of quantitative tightening (Q.T.). The last report should an increase as a result of the new Bank Term Funding Program (BTFP).

Friday 3/31

• 8:30 AM ET, Personal Income and Outlays is expected to have risen 0.3 percent in February with consumption expenditures expected to have increased 0.2 percent. In January there was a rise of 0.6 percent for income and 1.8 percent surge for consumption. Inflation readings for February are expected at monthly increases of 0.4 percent both overall and for the core (versus 0.6 percent increases for both in January) for annual rates of 5.1 and 4.7 percent (versus January’s respective rates of 5.4 and 4.7 percent).

• 10:00 AM ET, Consumer Sentiment in late March is expected to be unchanged from the mid-month flash of 63.4.

What Else

We congratulate all the NCAA basketball teams that made the final four teams competing in the NCAA championships. This includes the Florida Atlantic University basketball team that has made the final four for the first time. While we wish all teams well, the large investor conference sponsored by Channelchek, NobleCon19, will be held at the elaborate College of Business Executive Education at FAU. So this adds to all of our interest at Channelchek. These final March Madness games start on Saturday, April 1st, and while we officially don’t have a consensus read on the final outcome, we hope for excellent play from all. Learn more about the NobleCon19 conference on the FAU campus by clicking here.

PHOENIX, March 24, 2023 (GLOBE NEWSWIRE) — QuoteMedia, Inc. (OTCQB: QMCI), a leading provider of market data and financial applications, today announced that it has achieved SOC 2 Type II accreditation.

The SOC 2 Type II accreditation is a rigorous certification that requires companies to demonstrate their ability to securely manage customer data and protect against unauthorized access. The accreditation is awarded to companies that have implemented a comprehensive set of controls and processes to ensure the confidentiality, integrity, and availability of their services.

“We are thrilled to have achieved SOC 2 Type II accreditation, which is a testament to our commitment to providing the highest levels of security and reliability to our customers,” said Dave Shworan, CEO of QuoteMedia Ltd. “As a leading provider of financial market data and solutions, we understand the critical importance of safeguarding our customers’ data, and we take this responsibility very seriously.”

To achieve SOC 2 Type II accreditation, QuoteMedia underwent a demanding audit by an independent third-party auditor. The audit assessed the company’s controls and processes related to security, availability, processing integrity, confidentiality, and privacy. QuoteMedia’s implementation of robust controls and processes is evidence of its dedication to maintaining a secure and reliable environment for customer data.

About QuoteMedia

QuoteMedia is a leading software developer and cloud-based syndicator of financial market information and streaming financial data solutions to media, corporations, online brokerages, and financial services companies. The Company licenses interactive stock research tools such as streaming real-time quotes, market research, news, charting, option chains, filings, corporate financials, insider reports, market indices, portfolio management systems, and data feeds. QuoteMedia provides industry leading market data solutions and financial services for companies such as the Nasdaq Stock Exchange, TMX Group (TSX Stock Exchange), Canadian Securities Exchange (CSE), London Stock Exchange Group, FIS, U.S. Bank, Bank of Montreal (BMO), Broadridge Financial Systems, JPMorgan Chase, Scotiabank, CI Financial, Canaccord Genuity Corp., Hilltop Securities, Avantax, Stockhouse, Zacks Investment Research, General Electric, Boeing, Bombardier, Telus International, Business Wire, PR Newswire, The Goldman Sachs Group, Regal Securities, ChoiceTrade, Cetera Financial Group, Dynamic Trend, Inc., Credential Qtrade Securities, CNW Group, iA Private Wealth, Ally Invest, Inc., Suncor, Leede Jones Gable, Firstrade Securities, Charles Schwab, First Financial, Equisolve, Stock-Trak, Mergent, Cision and others. Quotestream®, QMod™ and Quotestream Connect™ are trademarks of QuoteMedia. For more information, please visit www.quotemedia.com.

One Stop Systems, Inc. (OSS) designs and manufactures innovative AI Transportable edge computing modules and systems, including ruggedized servers, compute accelerators, expansion systems, flash storage arrays, and Ion Accelerator™ SAN, NAS, and data recording software for AI workflows. These products are used for AI data set capture, training, and large-scale inference in the defense, oil and gas, mining, autonomous vehicles, and rugged entertainment applications. OSS utilizes the power of PCI Express, the latest GPU accelerators and NVMe storage to build award-winning systems, including many industry firsts, for industrial OEMs and government customers. The company enables AI on the Fly® by bringing AI datacenter performance to ‘the edge,’ especially on mobile platforms, and by addressing the entire AI workflow, from high-speed data acquisition to deep learning, training, and inference. OSS products are available directly or through global distributors. For more information, go to www.onestopsystems.com.

Joe Gomes, Managing Director – Generalist Analyst, Noble Capital Markets, Inc.

Joshua Zoepfel, Research Associate, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

4Q22 Results. Revenue of $18.2 million, up 2.7% y-o-y, but about $1 million below expectations as the Disguise business was weaker than expected. We had forecast $19 million. Driven by one-time items, OSS reported a GAAP net loss of $3.3 million, or a loss of $0.16/sh in the quarter, compared to a loss of $386,243, or a loss of $0.02/sh per share last year. We had forecast net income of $0.4 million, or $0.02 per share.

Military Opportunities Expanding. OSS is now engaged with eight of the top 10 largest military prime contractors in the U.S., with multiple prime contractor bids to the DOD using OSS products. OSS has won two new military programs already in 2023, with eight more in the pipeline.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

Michael Kupinski, Director of Research, Noble Capital Markets, Inc.

Patrick McCann, Research Associate, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

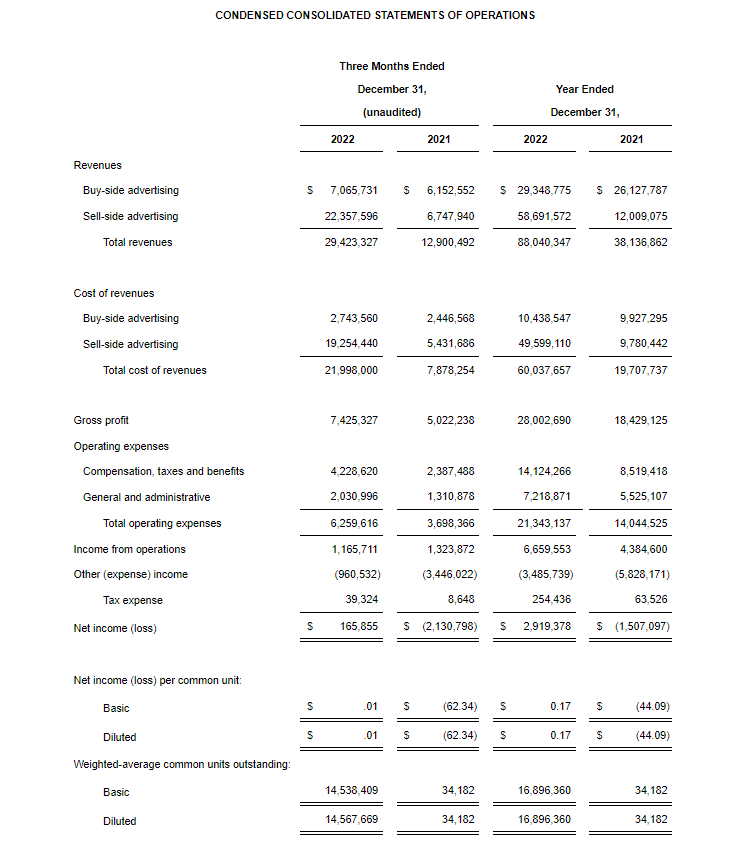

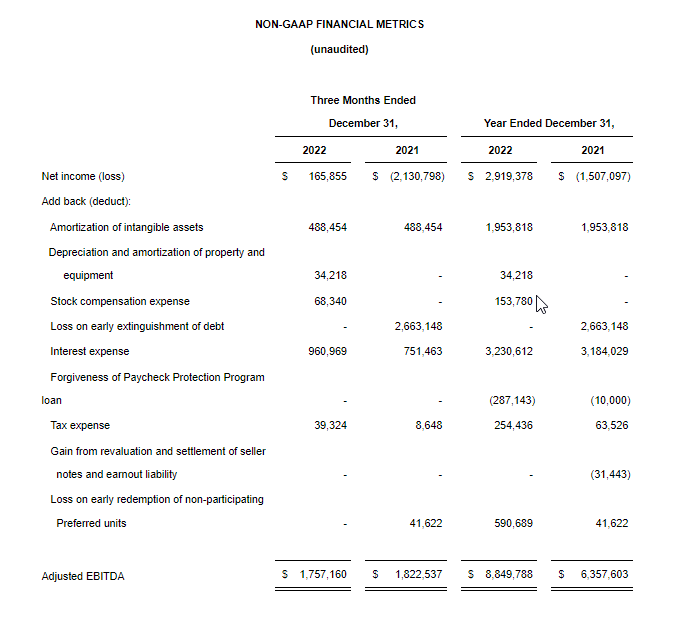

Strong Q4 results. The company reported strong Q4 revenue of $29.4 million, in line with our estimate of $29.3 million. The quarter was driven by robust Sell-side advertising revenues of $22.4million, an increase of 231% from the prior year period. Q4 Adj. EBITDA of $1.8 million was flat year over year and missed our estimate of $2.7 million, largely due to elevated compensation costs.

2023 outlook. The company is shifting its focus to pursue larger, but more price sensitive clients. As such, we expect higher investment and compensation costs to support larger accounts. The company plans to invest to offer new products, like data analytics to support higher future margins. We believe adj. EBITDA will be flat over the prior year, given increased investment and lower margin clients.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

Defense Metals Corp. is a mineral exploration and development company focused on the acquisition, exploration and development of mineral deposits containing metals and elements commonly used in the electric power market, defense industry, national security sector and in the production of green energy technologies, such as, rare earths magnets used in wind turbines and in permanent magnet motors for electric vehicles. Defense Metals owns 100% of the Wicheeda Rare Earth Element Property located near Prince George, British Columbia, Canada. Defense Metals Corp. trades in Canada under the symbol “DEFN” on the TSX Venture Exchange, in the United States, under “DFMTF” on the OTCQB and in Germany on the Frankfurt Exchange under “35D”.

Mark Reichman, Senior Research Analyst, Natural Resources, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

Prelude to an updated mineral resource estimate. Defense Metals recently updated its 3-D geological model of the Wicheeda Rare Earth Element (REE) deposit. The update incorporated results from drilling completed during 2021 and 2022 that is not reflected in the January 2022 preliminary economic assessment (PEA), and will be used to update the mineral resource estimate and incorporated into a preliminary feasibility study (PFS) expected to be completed during the first quarter of 2024.

A lot of new information. Results for 47 holes representing 10,876 meters of drilling has now been included in the updated geological model. The drilling programs were designed to: 1) increase mineral resource confidence from inferred to indicated and measured categories, 2) define the northern endpoint of the Wicheeda carbonate complex, and 3) to provide detailed geotechnical and hydrogeological drilling data for advanced pit slope and mine design. By way of comparison, current resources outlined in the January 2022 preliminary economic assessment were based on a total of 27 diamond drill holes representing 4,249 meters of drilling.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

Image: Congressional Hearings with Byte Dance (TikTok) CEO, C-SPAN (YouTube)

Should the US Ban TikTok? Can It? A Cybersecurity Expert Explains the Risks the App Poses

TikTok CEO Shou Zi Chew testified before the House Energy and Commerce Committee on March 23, 2023, amid a chorus of calls from members of Congress for the federal government to ban the Chinese-owned video social media app and reports that the Biden administration is pushing for the company’s sale.

The federal government, along with many state and foreign governments and some companies, has banned TikTok on work-provided phones. This type of ban can be effective for protecting data related to government work.

But a full ban of the app is another matter, which raises a number of questions: What data privacy risk does TikTok pose? What could the Chinese government do with data collected by the app? Is its content recommendation algorithm dangerous? And is it even possible to ban an app?

This article was republished with permission from The Conversation, a news site dedicated to sharing ideas from academic experts. It represents the research-based findings and thoughts of, Doug Jacobson, Professor of Electrical and Computer Engineering, Iowa State University.

Vacuuming Up Data

As a cybersecurity researcher, I’ve noted that every few years a new mobile app that becomes popular raises issues of security, privacy and data access.

Apps collect data for several reasons. Sometimes the data is used to improve the app for users. However, most apps collect data that the companies use in part to fund their operations. This revenue typically comes from targeting users with ads based on the data they collect. The questions this use of data raises are: Does the app need all this data? What does it do with the data? And how does it protect the data from others?

So what makes TikTok different from the likes of Pokemon-GO, Facebook or even your phone itself? TikTok’s privacy policy, which few people read, is a good place to start. Overall, the company is not particularly transparent about its practices. The document is too long to list here all the data it collects, which should be a warning.

There are a few items of interest in TikTok’s privacy policy besides the information you give them when you create an account – name, age, username, password, language, email, phone number, social media account information and profile image – that are concerning. This information includes location data, data from your clipboard, contact information, website tracking, plus all data you post and messages you send through the app. The company claims that current versions of the app do not collect GPS information from U.S. users. There has been speculation that TikTok is collecting other information, but that is hard to prove.

If most apps collect data, why is the U.S. government worried about TikTok? First, they worry about the Chinese government accessing data from its 150 million users in the U.S. There is also a concern about the algorithms used by TikTok to show content.

Data in the Chinese Government’s Hands

If the data does end up in the hands of the Chinese government, the question is how could it use the data to its benefit. The government could share it with other companies in China to help them profit, which is no different than U.S. companies sharing marketing data. The Chinese government is known for playing the long game, and data is power, so if it is collecting data, it could take years to learn how it benefits China.

One potential threat is the Chinese government using the data to spy on people, particularly people who have access to valuable information. The Justice Department is investigating TikTok’s parent company, ByteDance, for using the app to monitor U.S. journalists. The Chinese government has an extensive history of hacking U.S. government agencies and corporations, and much of that hacking has been facilitated by social engineering – the practice of using data about people to trick them into revealing more information.

The second issue that the U.S. government has raised is algorithm bias or algorithm manipulation. TikTok and most social media apps have algorithms designed to learn a user’s interests and then try to adjust the content so the user will continue to use the app. TikTok has not shared its algorithm, so it’s not clear how the app chooses a user’s content.

The algorithm could be biased in a way that influences a population to believe certain things. There are numerous allegations that TiKTok’s algorithm is biased and can reinforce negative thoughts among younger users, and be used to affect public opinion. It could be that the algorithm’s manipulative behavior is unintentional, but there is concern that the Chinese government has been using or could use the algorithm to influence people.

If the federal government comes to the conclusion that TikTok should be banned, is it even possible to ban it for all of its 150 million existing users? Any such ban would likely start with blocking the distribution of the app through Apple’s and Google’s app stores. This might keep many users off the platform, but there are other ways to download and install apps for people who are determined to use them.

A more drastic method would be to force Apple and Google to change their phones to prevent TikTok from running. While I’m not a lawyer, I think this effort would fail due to legal challenges, which include First Amendment concerns. The bottom line is that an absolute ban will be tough to enforce.

There are also questions about how effective a ban would be even if it were possible. By some estimates, the Chinese government has already collected personal information on at least 80% of the U.S. population via various means. So a ban might limit the damage going forward to some degree, but the Chinese government has already collected a significant amount of data. The Chinese government also has access – along with anyone else with money – to the large market for personal data, which fuels calls for stronger data privacy rules.

Are You at Risk?

So as an average user, should you worry? Again, it is unclear what data ByteDance is collecting and if it can harm an individual. I believe the most significant risks are to people in power, whether it is political power or within a company. Their data and information could be used to gain access to other data or potentially compromise the organizations they are associated with.

The aspect of TikTok I find most concerning is the algorithm that decides what videos users see and how it can affect vulnerable groups, particularly young people. Independent of a ban, families should have conversions about TikTok and other social media platforms and how they can be detrimental to mental health. These conversations should focus on how to determine if the app is leading you down an unhealthy path.

The Details of the Hindenberg Research Report Include Serious Allegations

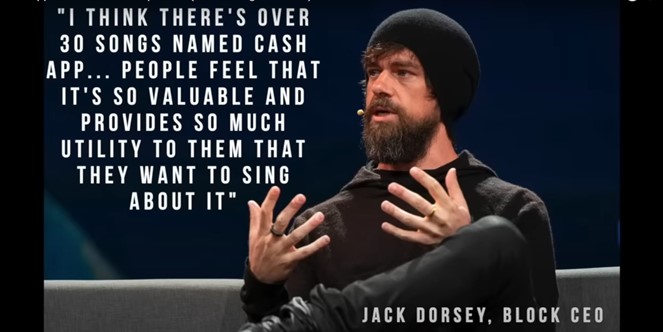

A legal face-off may be brewing as Block (SQ), the other company co-founded by Jack Dorsey, calls on the SEC for what Block calls an “inaccurate report.” The report Block (formerly Square) is referring to was released by Hindenberg Research on March 23. The research contends that Dorsey’s fintech company showed, “willingness to facilitate fraud against consumers and the government, avoid regulation, dress up predatory loans and fees as revolutionary technology, and mislead investors with inflated metrics.”

What is each side claiming, and what is the responsibility in releasing a report that may take Hindenberg into a fight with a company with a $44 billion market cap?

Who’s Involved?

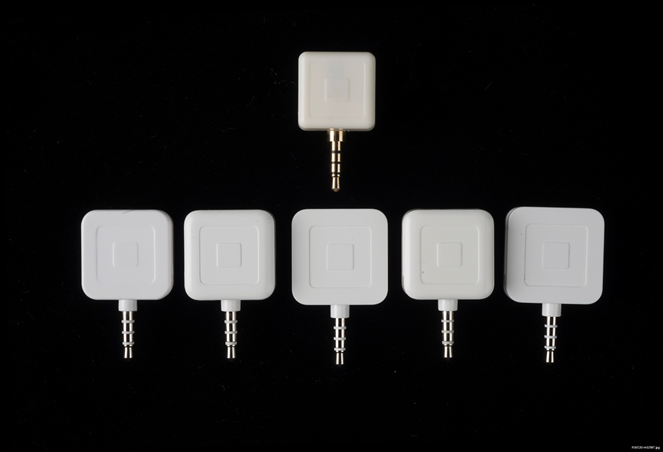

Block is a financial technology company specializing in mobile payments founded in 2009 by Jack Dorsey and Jim McKelvey. The company’s flagship product is a small, square-shaped credit card reader that plugs into a smartphone or tablet and allows businesses to accept credit and debit card payments. Block has added other financial products and services, including point-of-sale software, payroll processing, and business loans.

Hindenburg Research provides investors with investigative research and analysis for the purpose of helping them identify potential risks or fraudulent practices in publicly traded companies. They are described as a short-selling, research-based firm. The Research is often considered within the context of its short-position investment strategy.

Image: Block’s flagship product – Nat’l Museum of American History Smithsonian Institution (Flickr)

What is Hindenberg’s Claim?

The research firm with a reputation of looking below the surface for trouble at firms, says Block is not what it claims to be. According to the Hindenberg report, the Dorsey-founded firm claims to have developed a frictionless and magical financial technology. The mission of this technology, the report quotes Block as saying is to empower the “unbanked” and the “underbanked.”

Hindenberg says that over two years of investigation that involved dozens of interviews with former employees that Block has systematically taken advantage of the demographics it claims to be helping. This refers to the stated mission of helping the underbanked. Instead, the research firm says this stands in conflict with, “the company’s willingness to facilitate fraud against consumers and the government, avoid regulation, and dress up predatory loans and fees as revolutionary technology, and mislead investors with inflated metrics.”

The two years of investigation also indicated that Block severely overstated its user counts and has understated its customer acquisition costs. This information, the report says, is based on former employees’ estimation that 40%-75% of accounts they reviewed were fake, involved in fraud, or were additional accounts tied to a single individual.

They claim a key metric that investors use to value the company are unclear. That is, how many individuals are on the Cash App. The report accuses the company reporting of misleading “transacting active” metrics filled with fake and duplicate accounts. Hindenberg says, “Block can and should clarify to investors an estimate on how many unique people actually use Cash App.”

Hindenberg said the app is used for illegal activity and points to all the rap songs written about engaging in illegal activity, activity made possible with the help of the app. The research company even made a compilation video to demonstrate this point (link to video under “Sources” below).

A line in one of the songs is, “I paid them hitters through Cash App.” Heritage contests that Block paid to promote the video for the song called “Cash App” which described paying contract killers through the app. The song’s artist was later arrested for attempted murder.

According to the Hindenberg report, Block’s Cash App was also cited “by far” as the top app used in reported U.S. sex trafficking, according to a leading non-profit organization. Multiple Department of Justice complaints outline how Cash App has been used to facilitate sex trafficking, including sex trafficking of minors.

Beyond alleged facilitation of payment for crimes, the platform, former employees contend, is overrun with scam accounts and fake users. Examples of obvious distortions of user numbers is that “Jack Dorsey” has multiple fake accounts, including some that appear aimed at scamming Cash App users. “Elon Musk” and “Donald Trump” who have dozens of accounts in their names. Hindenberg contends they tested this flaw, “we ordered a Cash Card under our obviously fake Donald Trump account, checking to see if Cash App’s compliance would take issue—the card promptly arrived in the mail,” they gave as an example.

Block’s Response

Not to be dissed, management at Block called out the threatening press release. “We intend to work with the SEC and explore legal action against Hindenburg Research for the factually inaccurate and misleading report they shared about our Cash App business today.”

The Dorsey founded firm suggested that the research firm wrote the report for dubious reasons and that it may be part of an orchestrated reverse pump and dump, “Hindenburg is known for these types of attacks, which are designed solely to allow short sellers to profit from a declined stock price. We have reviewed the full report in the context of our own data and believe it’s designed to deceive and confuse investors.”

The company than comforted stakeholders saying, “we are a highly regulated public company with regular disclosures, and are confident in our products, reporting, compliance programs, and controls. We will not be distracted by typical short seller tactics.”

There’s Smoke, is There Fire?

Are the initial disparaging claims against Block’s business accurate? Is there merit to what Block says of Hindenberg Research? As Block may be seeking a legal remedy, it is unlikely that either party will be very vocal from here.

For investors, it’s logical that both parties cannot be right at the same time. One of the parties is overstating truth. If Block is indeed working with the SEC, this truth should eventually surface.

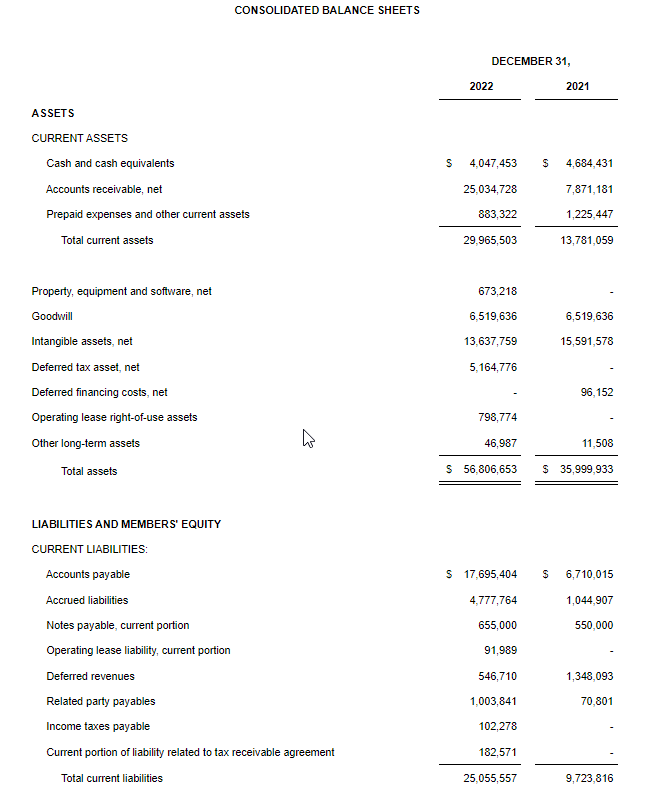

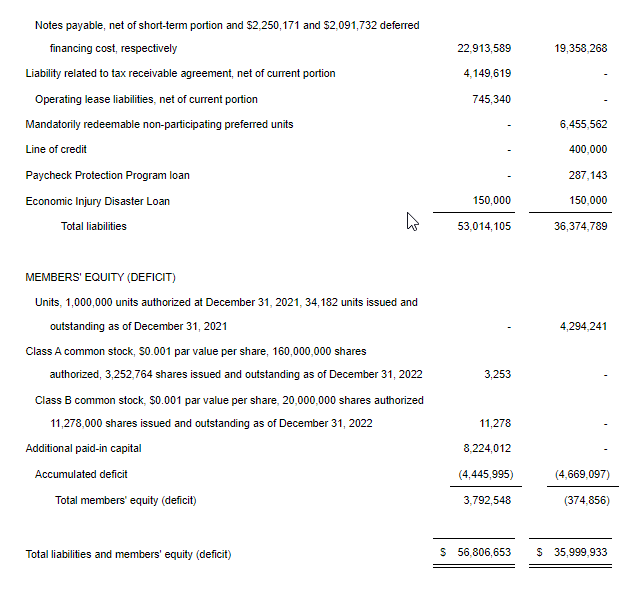

Full-Year 2022 Revenue Up 131% Year-Over-Year to $88.0 Million

Fourth Quarter 2022 Revenue Up 128% to $29.4 Million

HOUSTON, March 23, 2023 /PRNewswire/ — Direct Digital Holdings, Inc. (Nasdaq: DRCT) (“Direct Digital Holdings” or the “Company”), a leading advertising and marketing technology platform operating through its companies Colossus Media, LLC (“Colossus SSP”), Huddled Masses LLC (“Huddled Masses”) and Orange142, LLC (“Orange142”), today announced financial results for the fourth quarter and fiscal year ended December 31, 2022.

Mark Walker, Chairman and Chief Executive Officer, commented, “We are pleased to report that 2022, our first year as a public company, saw robust financial performance, significant operational expansion and continued gains in market share for Direct Digital Holdings. Both our quarterly and full-year results capitalized on brands and businesses moving dollars away from less efficient traditional advertising outlets towards digital media. We are expecting strong double-digit percentage revenue growth in FY 2023 across both our sell- and buy-side business segments as we further drive customer adoption of our digital advertising solutions.”

Keith Smith, President, added, “Our fourth quarter and full-year 2022 performance, particularly during a difficult macroeconomic environment, is a testament to our market-leading approach working with middle market and multicultural audiences. Looking ahead, we are excited to continue scaling across these fast-growing and underrepresented communities from a position of financial strength, which we expect will give us a significant competitive advantage for sustainable, long-term growth.”

Fourth Quarter 2022 Financial Highlights:

Revenue was $29.4 million in the fourth quarter of 2022, an increase of $16.5 million, or 128% over the $12.9 million in the same period of 2021.

Sell-side advertising segment revenue grew to $22.3 million and contributed $15.6 million of the increase, or 231% growth over the $6.7 million of sell-side revenue in the same period of 2021.

Buy-side advertising segment revenue grew to $7.1 million and contributed $0.9 million of the increase, or 15% growth over the $6.2 million of buy-side revenue in the same period of 2021.

Operating income was $1.2 million for the fourth quarter of 2022 compared to $1.3 million in the same period of 2021.

Net income was $0.2 million in the fourth quarter of 2022, compared to a net loss of $2.1 million in the same period of 2021.

Adjusted EBITDA(1) was $1.8 million in the fourth quarter 2022, compared to $1.8 million in the same period of 2021.

Fiscal Year 2022 Financial Highlights:

Revenue in fiscal year 2022 was $88.0 million, an increase of $49.9 million, or 131%, over the $38.1 million in fiscal year 2021.

Sell-side advertising segment ended the year at $58.7 million in revenue and contributed $46.7 million of the increase, or 389% growth over the $12.0 million of sell-side revenue in fiscal year 2021.

Buy-side advertising segment ended the year at $29.3 million in revenue and contributed $3.2 million of the increase, or 12% growth over the $26.1 million of buy-side revenue in fiscal year 2021.

Operating income increased $2.3 million, or 52%, to $6.7 million for 2022 compared to operating income of $4.4 million for 2021.

Operating income for the buy-side and sell-side advertising segments combined totaled $14.0 million, an increase of $7.1 million, or 102%, compared to $6.9 million for 2021.

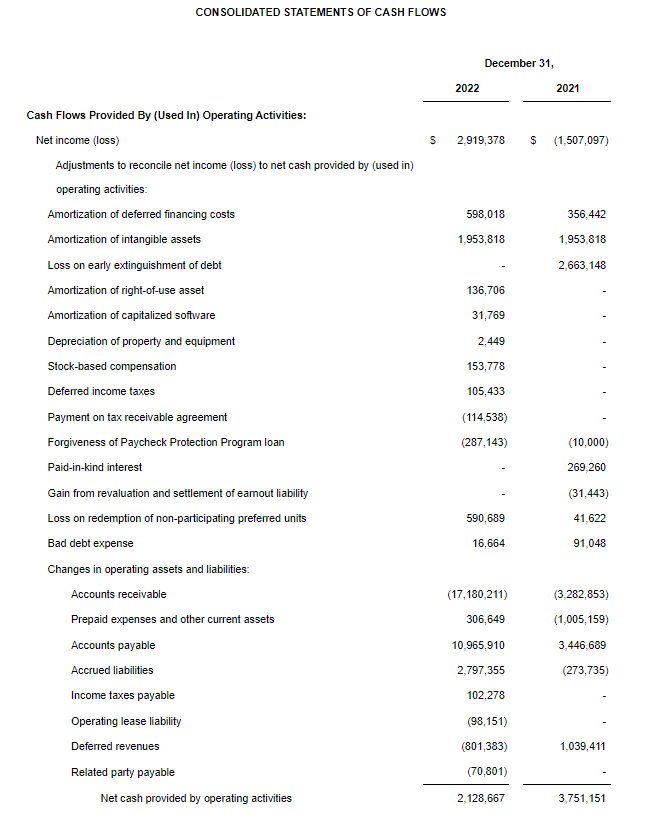

Net income for 2022 was $2.9 million, compared to a net loss of $1.5 million in 2021.

Adjusted EBITDA(1) for 2022 was $8.8 million, compared to $6.4 million for 2021.

Cash and accounts receivable balances as of December 31, 2022 were $29.1 million compared to $12.6 million as of December 31, 2021.

As previously disclosed, on January 9, 2023, the Company entered into a Loan and Security Agreement with Silicon Valley Bank which provides for a revolving credit facility (the “Credit Facility”). As the Company had not yet drawn any amounts under the Credit Facility, the Company issued a notice of termination of the Loan and Security Agreement and is in the process of terminating the Credit Facility. The Company has received a consent to terminate the Credit Facility and a waiver of the terms relating to the Credit Facility under its Term Loan and Security Agreement, dated as of December 3, 2021, with Lafayette Square Loan Servicing, LLC.

Based on our expectations of cash flows from operations and the available cash held, we believe that we will have sufficient cash resources to finance our operations and service any debt obligations until at least the end of fiscal year 2023.

Business Highlights

For the fourth quarter ended December 31, 2022, Direct Digital Holdings processed approximately 132 billion monthly impressions through its sell-side advertising segment, an increase of 81% over the same period of 2021, with over 833 billion bid requests for the quarter.

In addition, the Company’s sell-side advertising platforms received over 17 billion bid responses in the fourth quarter of 2022, an increase of over 25% over the same period in 2021, through 170,000 buyers for the quarter, which equates to a 109% increase over the same period in 2021.

The Company’s buy-side advertising segment served approximately 218 customers in the fourth quarter of 2022, an increase of 7% compared to the same period of 2021.

Financial Outlook

Assuming the U.S. economy does not experience any major economic conditions that deteriorate or otherwise significantly reduce advertiser demand, we estimate the following:

For fiscal year 2023, we expect revenue to be in the range of $118 million to $122 million, or 36% year-over-year growth at the mid-point.

“As we enter into our second year as a public company, we remain disciplined in our strategic organic growth initiatives, continue to focus on increasing EBITDA and aim to provide maximum value for our shareholders,” commented Susan Echard, Chief Financial Officer.

Conference Call and Webcast Details

Direct Digital will host a conference call on Thursday, March 23, 2023 at 5:00 p.m. Eastern Time to discuss the Company’s fourth quarter and full-year financial results. The live webcast and replay can be accessed at https://ir.directdigitalholdings.com/. Please access the website at least fifteen minutes prior to the call to register, download and install any necessary audio software. For those who cannot access the webcast, a replay will be available at https://ir.directdigitalholdings.com/ for a period of twelve months.

Footnote

(1) “Adjusted EBITDA” is a non-GAAP financial measure. The section titled “Non-GAAP Financial Measures” below describes our usage of non-GAAP financial measures and provides reconciliations between historical GAAP and non-GAAP information contained in this press release.

Forward Looking Statements

This press release may contain forward-looking statements within the meaning of federal securities laws, including the Private Securities Litigation Reform Act of 1995, Section 27A of the Securities Act of 1933, as amended, and Section 21E of the Securities Exchange Act of 1934, as amended, and which are subject to certain risks, trends and uncertainties.

As used below, “we,” “us,” and “our” refer to the Company. We use words such as “could,” “would,” “may,” “might,” “will,” “expect,” “likely,” “believe,” “continue,” “anticipate,” “estimate,” “intend,” “plan,” “project” and other similar expressions to identify forward-looking statements, but not all forward-looking statements include these words. All statements contained in this press release that do not relate to matters of historical fact should be considered forward-looking statements.

All of our forward-looking statements involve estimates and uncertainties that could cause actual results to differ materially from those expressed in or implied by the forward-looking statements. Our forward-looking statements are based on assumptions that we have made in light of our industry experience and our perceptions of historical trends, current conditions, expected future developments and other factors we believe are appropriate under the circumstances. Although we believe that these forward-looking statements are based on reasonable assumptions, many factors could affect our actual operating and financial performance and cause our performance to differ materially from the performance expressed in or implied by the forward-looking statements, including, but not limited to: our dependence on the overall demand for advertising, which could be influenced by economic downturns; any slow-down or unanticipated development in the market for programmatic advertising campaigns; the effects of health epidemics; operational and performance issues with our platform, whether real or perceived, including a failure to respond to technological changes or to upgrade our technology systems; any significant inadvertent disclosure or breach of confidential and/or personal information we hold, or of the security of our or our customers’, suppliers’ or other partners’ computer systems; any unavailability or non-performance of the non-proprietary technology, software, products and services that we use; unfavorable publicity and negative public perception about our industry, particularly concerns regarding data privacy and security relating to our industry’s technology and practices, and any perceived failure to comply with laws and industry self-regulation; restrictions on the use of third-party “cookies,” mobile device IDs or other tracking technologies, which could diminish our platform’s effectiveness; any inability to compete in our intensely competitive market; any significant fluctuations caused by our high customer concentration; our limited operating history, which could result in our past results not being indicative of future operating performance; any violation of legal and regulatory requirements or any misconduct by our employees, subcontractors, agents or business partners; any strain on our resources, diversion of our management’s attention or impact on our ability to attract and retain qualified board members as a result of being a public company; our dependence, as a holding company, of receiving distributions from Direct Digital Holdings, LLC to pay our taxes, expenses and dividends; and other factors and assumptions discussed in the “Risk Factors,” “Management’s Discussion and Analysis of Financial Conditions and Results of Operations” and other sections of our filings with the Securities and Exchange Commission that we make from time to time. Should one or more of these risks or uncertainties materialize or should any of these assumptions prove to be incorrect, our actual operating and financial performance may vary in material respects from the performance projected in these forward-looking statements. Further, any forward-looking statement speaks only as of the date on which it is made, and except as required by law, we undertake no obligation to update any forward-looking statement contained in this Current Report on Form 8-K to reflect events or circumstances after the date on which it is made or to reflect the occurrence of anticipated or unanticipated events or circumstances, and we claim the protection of the safe harbor for forward-looking statements contained in the Private Securities Litigation Reform Act of 1995.

About Direct Digital Holdings

Direct Digital Holdings (Nasdaq: DRCT), owner of operating companies Colossus SSP, Huddled Masses, and Orange 142, brings state-of-the-art sell- and buy-side advertising platforms together under one umbrella company. Direct Digital Holdings’ sell-side platform, Colossus SSP, offers advertisers of all sizes extensive reach within general market and multicultural media properties. The company’s subsidiaries Huddled Masses and Orange142 deliver significant ROI for middle market advertisers by providing data-optimized programmatic solutions at scale for businesses in sectors that range from energy to healthcare to travel to financial services. Direct Digital Holdings’ sell- and buy-side solutions manage approximately 90,000 clients monthly, generating over 100 billion impressions per month across display, CTV, in-app and other media channels. Direct Digital Holdings is the ninth black-owned company to go public in the U.S and was named a top minority-owned business by The Houston Business Journal.

NON-GAAP FINANCIAL MEASURES

In addition to our results determined in accordance with U.S. generally accepted accounting principles (“GAAP”), including, in particular operating income, net cash provided by operating activities, and net income, we believe that earnings before interest, taxes, depreciation and amortization (“EBITDA”), as adjusted for stock compensation expense, forgiveness of Paycheck Protection Program loans, gain from revaluation and settlement of seller notes and earnout liability, loss on early extinguishment of debt, and loss on early redemption of non-participating preferred units (“Adjusted EBITDA”), a non-GAAP financial measure, is useful in evaluating our operating performance. The most directly comparable GAAP measure to Adjusted EBITDA is net income (loss).

In addition to operating income and net income, we use Adjusted EBITDA as a measure of operational efficiency. We believe that this non-GAAP financial measure is useful to investors for period-to-period comparisons of our business and in understanding and evaluating our operating results for the following reasons:

Adjusted EBITDA is widely used by investors and securities analysts to measure a company’s operating performance without regard to items such as depreciation and amortization, interest expense, provision for income taxes, and certain one-time items such as acquisition transaction costs and gains from settlements or loan forgiveness that can vary substantially from company to company depending upon their financing, capital structures and the method by which assets were acquired;

Our management uses Adjusted EBITDA in conjunction with GAAP financial measures for planning purposes, including the preparation of our annual operating budget, as a measure of operating performance and the effectiveness of our business strategies and in communications with our board of directors concerning our financial performance; and

Adjusted EBITDA provides consistency and comparability with our past financial performance, facilitates period-to-period comparisons of operations, and also facilitates comparisons with other peer companies, many of which use similar non-GAAP financial measures to supplement their GAAP results.

Our use of this non-GAAP financial measure has limitations as an analytical tool, and you should not consider it in isolation or as a substitute for analysis of our financial results as reported under GAAP. The following table presents a reconciliation of Adjusted EBITDA to net income (loss) for each of the periods presented:

Collaboration builds off clinical data demonstrating rigosertib’s activity against PLK1 and may inform a precision medicine approach towards rigosertib’s evaluation in new indications

Collaboration will leverage ENLIGHT, a pan-cancer response predictor scalable to all cancer types and all targeted and immune checkpoint blockade (ICB) oncology drugs

NEWTOWN, Pa. & TEL AVIV, Israel, March 23, 2023 (GLOBE NEWSWIRE) — Onconova Therapeutics, Inc. (NASDAQ: ONTX), (“Onconova”), a clinical-stage biopharmaceutical company focused on discovering and developing novel products for patients with cancer, and Pangea Biomed, a company combining machine learning and deep RNA analysis to expand access to precision oncology, today announced a research collaboration between the companies. The collaboration will leverage Pangea Biomed’s proprietary algorithmic platform, ENLIGHT, with the goal of identifying biomarkers of response to Onconova’s proprietary investigational product candidate rigosertib.

Rigosertib has a multi-faceted mechanism of action targeting proteins containing the RAS binding domain, allowing it to modulate the PI3K and PLK1 pathways, as well as the tumor immune microenvironment. Clinical data have suggested the anti-cancer activity of rigosertib plus checkpoint inhibition in KRAS-mutated non-small cell lung cancer, and of rigosertib monotherapy in advanced squamous cell carcinoma complicating recessive dystrophic epidermolysis bullosa, an ultra-rare condition driven by PLK1 overexpression.

“Rigosertib’s ability to potently inhibit PLK1 and modulate the tumor immune microenvironment confers broad potential to treat a range of solid cancers,” said Steven M. Fruchtman, M.D., President and Chief Executive Officer of Onconova. “By leveraging Pangea’s AI platform to identify predictive biomarkers of response to rigosertib, we aim to inform a precision medicine approach to selecting additional PLK1-dependent tumors and other indications for its potential evaluation. We believe this approach will increase the probability of success for rigosertib’s future development programs.”

“Precision medicine is the future of oncology, but gaps in the industry’s current biomarker approaches overly narrow patient populations for promising drugs,” said Pangea Biomed Chief Executive Officer Tuvik Beker, Ph.D. “ENLIGHT goes beyond standard biomarkers to expand patient populations for targeted therapies, in addition to surfacing new biomarkers for existing drugs. We’re hopeful our platform can help Onconova accelerate rigosertib’s successful development in a variety of difficult-to-treat cancers.”

Pangea Biomed’s ENLIGHT platform is a pan-cancer response predictor that evaluates in vitro, preclinical, and clinical datasets to build genetic interaction maps that infer functional relationships between gene pairs to reveal tumor vulnerabilities to specified therapies. Onconova and Pangea Biomed will chart genetic interactions related to PLK1 to identify a biomarker of response to rigosertib based on its inhibitory activity against this protein. The ENLIGHT platform will then be applied to generate additional genetic interaction maps around other pathways targeted by rigosertib. Per a collaboration agreement between the companies, Onconova retains all rights to rigosertib and will own intellectual property that may result from the research collaboration.

About Onconova Therapeutics, Inc.

Onconova Therapeutics is a clinical-stage biopharmaceutical company focused on discovering and developing novel products for patients with cancer. The Company has proprietary targeted anti-cancer agents designed to disrupt specific cellular pathways that are important for cancer cell proliferation.

Onconova’s novel, proprietary multi-kinase inhibitor narazaciclib (formerly ON 123300) is being evaluated in two separate and complementary Phase 1 dose escalation and expansion studies. These trials are currently underway in the United States and China. Based on preclinical and clinical studies of CDK 4/6 inhibitors, Onconova is also planning a combination trial of narazaciclib with estrogen blockade in advanced endometrial cancer, as well as its clinical study in additional indications.

Onconova’s product candidate rigosertib is being studied in multiple investigator-sponsored studies, including a dose-escalation and expansion Phase 1/2a study of oral rigosertib in combination with nivolumab in patients with KRAS+ non-small cell lung cancer, and a Phase 2 program evaluating rigosertib monotherapy in advanced squamous cell carcinoma complicating recessive dystrophic epidermolysis bullosa (RDEB-associated SCC).

Founded in 2018, Pangea Biomed developed ENLIGHT – the world’s most advanced multi-cancer, multi-therapy response predictor. By combining machine learning and deep RNA analysis, the company is mapping tumor molecular signatures to dynamically and adaptively personalize cancer care for a healthier world. Pangea aims to bring effective precision oncology to cancer patients, improve oncology drug development and empower oncologists to treat patients with success. Pangea is backed by NFX, and its technology has been published in leading journals, including Cell, Med, Science Advances, Cancer Cell, Journal for ImmunoTherapy of Cancer and Nature Communications.

Forward Looking Statements

Some of the statements in this release are forward-looking statements within the meaning of Section 27A of the Securities Act of 1933, as amended, Section 21E of the Securities Exchange Act of 1934, as amended, and the Private Securities Litigation Reform Act of 1995, and involve risks and uncertainties. These statements relate to Onconova’s expectations regarding its clinical development and trials, its product candidates, its business and financial position. Onconova has attempted to identify forward-looking statements by terminology including “believes,” “estimates,” “anticipates,” “expects,” “plans,” “intends,” “may,” “could,” “might,” “will,” “should,” “preliminary,” “encouraging,” “approximately” or other words that convey uncertainty of future events or outcomes. Although Onconova believes that the expectations reflected in such forward-looking statements are reasonable as of the date made, expectations may prove to have been materially different from the results expressed or implied by such forward-looking statements. These statements are only predictions and involve known and unknown risks, uncertainties, and other factors, including the success and timing of Onconova’s clinical trials, investigator-initiated trials and regulatory agency and institutional review board approvals of protocols, Onconova’s collaborations, market conditions and those discussed under the heading “Risk Factors” in Onconova’s most recent Annual Report on Form 10-K and quarterly reports on Form 10-Q. Any forward-looking statements contained in this release speak only as of its date. Onconova undertakes no obligation to update any forward-looking statements contained in this release to reflect events or circumstances occurring after its date or to reflect the occurrence of unanticipated events.

Onconova Company Contact: Mark Guerin Onconova Therapeutics, Inc. 267-759-3680 ir@onconova.us https://www.onconova.com/contact/

Onconova Investor Contact: Bruce Mackle LifeSci Advisors, LLC 646-889-1200 bmackle@lifesciadvisors.com

CHATHAM, N.J., March 23, 2023 (GLOBE NEWSWIRE) — Tonix Pharmaceuticals Holding Corp. (Nasdaq: TNXP), a clinical-stage biopharmaceutical company, today announced that Seth Lederman, M.D., Chief Executive Officer of Tonix Pharmaceuticals, will deliver an oral presentation and the Company will present a poster at the 5th International Congress on Controversies in Fibromyalgia being held March 30-31, 2023 at the Austria Trend Hotel Savoyen Vienna, Vienna, Austria.

Copies of the Company’s presentation and poster will be available under the Scientific Presentations tab of the Tonix website at www.tonixpharma.com following the conference. In addition to the presentation, the Company’s submitted abstract will be published in an online supplement to the journal Clinical and Experimental Rheumatology in a special issue on Fibromyalgia. Additional meeting information can be found on the International Congress on Controversies in Fibromyalgia website here.

Oral Presentation Details

Topic:

Efficacy and Safety of TNX-102 SL (Sublingual Cyclobenzaprine) for the Treatment of Fibromyalgia: Results from the Randomized, Placebo Controlled RELIEF Trial

Location:

Austria Trend Hotel Savoyen Vienna, Vienna, Austria

Date:

Thursday March 30, 2023

Time:

5:10 p.m. CEST

Poster Presentation Details

Title:

Efficacy and Safety of TNX-102 SL (Sublingual Cyclobenzaprine) for the Treatment of Fibromyalgia: Results from the Randomized, Placebo Controlled RELIEF Trial

Location:

Austria Trend Hotel Savoyen Vienna, Vienna, Austria

Date/Time:

On display through duration of conference March 30-31, 2023

Tonix Pharmaceuticals Holding Corp.*

Tonix is a clinical-stage biopharmaceutical company focused on discovering, licensing, acquiring and developing therapeutics to treat and prevent human disease and alleviate suffering. Tonix’s portfolio is composed of central nervous system (CNS), rare disease, immunology and infectious disease product candidates. Tonix’s CNS portfolio includes both small molecules and biologics to treat pain, neurologic, psychiatric and addiction conditions. Tonix’s lead CNS candidate, TNX-102 SL (cyclobenzaprine HCl sublingual tablet), is in mid-Phase 3 development for the management of fibromyalgia with interim data expected in the second quarter of 2023. TNX-102 SL is also being developed to treat Long COVID, a chronic post-acute COVID-19 condition, for which a Phase 2 study was initiated in the third quarter of 2022. TNX-1900 (intranasal potentiated oxytocin), a small molecule in development for chronic migraine, is currently enrolling with interim data expected in the fourth quarter of 2023. TNX-601 ER (tianeptine hemioxalate extended-release tablets), a once-daily formulation of tianeptine being developed as a treatment for major depressive disorder (MDD), is also currently enrolling with interim data expected in the fourth quarter of 2023. TNX-1300 (cocaine esterase) is a biologic designed to treat cocaine intoxication and has been granted Breakthrough Therapy designation by the FDA. A Phase 2 study of TNX-1300 is expected to be initiated in the second quarter of 2023. Tonix’s rare disease portfolio includes TNX-2900 (intranasal potentiated oxytocin) for the treatment of Prader-Willi syndrome. TNX-2900 has been granted Orphan Drug designation by the FDA. Tonix’s immunology portfolio includes biologics to address organ transplant rejection, autoimmunity and cancer, including TNX-1500, which is a humanized monoclonal antibody targeting CD40-ligand (CD40L or CD154) being developed for the prevention of allograft and xenograft rejection and for the treatment of autoimmune diseases. A Phase 1 study of TNX-1500 is expected to be initiated in the second quarter of 2023. Tonix’s infectious disease pipeline includes TNX-801, a vaccine in development to prevent smallpox and mpox, for which a Phase 1 study is expected to be initiated in the second half of 2023. TNX-801 also serves as the live virus vaccine platform or recombinant pox vaccine platform for other infectious diseases. The infectious disease portfolio also includes TNX-3900, a class of broad-spectrum small molecule oral antivirals.

*All of Tonix’s product candidates are investigational new drugs or biologics and have not been approved for any indication.

This press release and further information about Tonix can be found at www.tonixpharma.com.

Forward Looking Statements

Certain statements in this press release are forward-looking within the meaning of the Private Securities Litigation Reform Act of 1995. These statements may be identified by the use of forward-looking words such as “anticipate,” “believe,” “forecast,” “estimate,” “expect,” and “intend,” among others. These forward-looking statements are based on Tonix’s current expectations and actual results could differ materially. There are a number of factors that could cause actual events to differ materially from those indicated by such forward-looking statements. These factors include, but are not limited to, risks related to the failure to obtain FDA clearances or approvals and noncompliance with FDA regulations; delays and uncertainties caused by the global COVID-19 pandemic; risks related to the timing and progress of clinical development of our product candidates; our need for additional financing; uncertainties of patent protection and litigation; uncertainties of government or third party payor reimbursement; limited research and development efforts and dependence upon third parties; and substantial competition. As with any pharmaceutical under development, there are significant risks in the development, regulatory approval and commercialization of new products. Tonix does not undertake an obligation to update or revise any forward-looking statement. Investors should read the risk factors set forth in the Annual Report on Form 10-K for the year ended December 31, 2022, as filed with the Securities and Exchange Commission (the “SEC”) on March 13, 2023, and periodic reports filed with the SEC on or after the date thereof. All of Tonix’s forward-looking statements are expressly qualified by all such risk factors and other cautionary statements. The information set forth herein speaks only as of the date thereof.

Travelzoo® provides its 30 million members with exclusive offers and one-of-a-kind experiences personally reviewed by our deal experts around the globe. We have our finger on the pulse of outstanding travel, entertainment, and lifestyle experiences. We work in partnership with more than 5,000 top travel suppliers—our long-standing relationships give Travelzoo members access to irresistible deals.

Michael Kupinski, Director of Research, Noble Capital Markets, Inc.

Patrick McCann, Research Associate, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

Strong Q4 results. The company reported strong Q4 operating results, with revenue up 31.6% to $18.6 million and Adj. EBITDA up an impressive 328% to $4.7 million. Notably, the company’s North America segment grew revenue by 53% and reported margins of 29%. The company benefited from favorable travel trends and lower operating expenses, particularly marketing expenses.

Favorable trends. The company has positive revenue and margin momentum moving into 2023. Management highlighted the opportunity for further margin growth given potential advertising price increases in Q2. The company appears to be benefiting from pent up travel demand from its travel enthusiast base.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

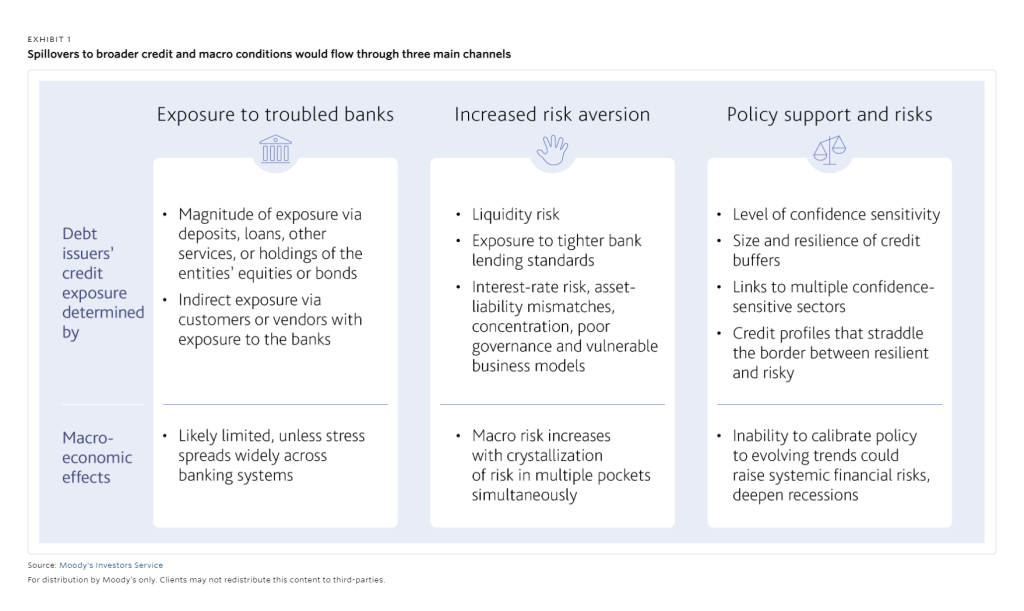

Fragile Investor Confidence Could Create Greater Repercussions, Says Moody’s

Bankdemic?

Moody’s Investors Service is cautiously optimistic bank problems will not spill over into the broader economy. However, in a new report, this top-three rating agency said they believe the financial regulators have acted in a way to prevent ripple effects from stressed banks, but they admit there is a good deal of uncertainty in both investor confidence and the economy as a whole. Moody’s wrote that “there is a risk that policymakers will be unable to curtail the current turmoil without longer-lasting and potentially severe repercussions within and beyond the banking sector.”

The reason for the rating services concern is, “even before bank stress became evident, we had expected global credit conditions to continue to weaken in 2023 as a result of significantly higher interest rates and lower growth, including recessions in some countries.” Moody’s said that the longer financial conditions remain tight, the greater the chance that industries outside of banking will experience problems.

Moody’s outlined three channels by which bank problems could become contagious to other sectors.

The first and most possible channel would be the problems encountered by entities with direct and indirect exposure to troubled banks. These can come in different forms. Financial and nonfinancial entities in the private and public sectors could have direct exposure to banks via deposits, loans, other transactional facilities, or direct holdings of weakened banks’ stocks or bonds. Unrelated, they may rely on a troubled bank for services essential to their business.

As it relates to this first channel, the rating agency wrote, “Monitoring and evaluating the direct and indirect links at the entity level will be a key focus of our credit analysis over the coming weeks and months.” Moody’s mentioned Credit Suisse by name in their note, saying the consequences of the UBS takeover are still unfolding, “Given the size and systemic importance of Credit Suisse, there likely will be varied consequences of its takeover for a range of financial actors with direct exposure to the bank.” The rating agency also believes the rapid completion of the deal appears to have avoided widespread contagion across the banking sector.”

The second channel Moody’s indicates could be most potent. It is that broader problems within the banking sector would cause banks to have stricter lending practices. Moody’s says that if this occurred, it would impact customers that are “liquidity-constrained.” The domino impact would then be that investors and lenders may become more cautious, “with particular regard to entities that are exposed to risks similar to those of the troubled banks.”

From this scenario, there is a potential for shocks from interest rate risk, asset-liability mismatches, a large imbalance of assets or liabilities, poor governance, weak profits, and higher leverage.

The third risk is seen as policy risk. For policymakers whose main focus is taming inflation, the bank problems pose additional challenges to steering the economy to a soft landing. Policy actions and expectations will continue to serve to shape market sentiment. Moody’s baseline case forecasts that it expects policy responses to be rapid if risks emerge. This could help keep entity-level issues from becoming systemic problems. Moody’s note recognizes that policy and implementation are challenging, and there are risks of policy missteps, limitations, or unintended consequences.

“One key policy challenge is how policymakers will address both inflation and financial stability risks,” Moody’s explained that inflation is still high and labor market strength continues. “the failure to rein in inflation now could lead to de-anchoring of inflation expectations and increased nominal bond yields, forcing even more tightening later to restore monetary policy credibility.”

Moody’s wrote that the actions taken by the central banks, and financial regulators show that they recognize the importance of agility and coordination to address arising problems while not acting in a way to add more stress and create a systemic crisis.

Take Away

The recent downfall of a few banks demonstrates how pulling liquidity out of an overly stimulated economy can cause withdrawal pains. Whether the new, tighter credit conditions will tip the economy into a deeper economic downturn as the spillover effect spreads to other sectors remains to be seen. If it occurs, Moody’s expects it would come from the interplay between preexisting credit risks, policy actions, and market sentiment. But, its role as a rating agency is to highlight possible risks. This is not a forecast, there forecast is that regulators and policymakers will have eventually succeeded to contain any ripple effects.

{kind=link}