Research News and Market Data on UUUU

Webcast on March 10, 2023

Preparing multiple uranium mines for production, completing profitable sales & developing rare earth refining capacity to power up to 1 million EVs per year by late-2023 or early-2024, while strengthening the balance sheet and avoiding debt.

LAKEWOOD, Colo., March 8, 2023 /CNW/ – Energy Fuels Inc. (NYSE American: UUUU) (TSX: EFR) (“Energy Fuels” or the “Company”) today reported its financial results for the year ended December 31, 2022. The Company’s Annual Report on Form 10-K has been filed with the U.S. Securities and Exchange Commission (“SEC“) and may be viewed on the Electronic Document Gathering and Retrieval System (“EDGAR“) at www.sec.gov/edgar.shtml, on the System for Electronic Document Analysis and Retrieval (“SEDAR“) at www.sedar.com, and on the Company’s website at www.energyfuels.com. Unless noted otherwise, all dollar amounts are in U.S. dollars.

Financial Highlights:

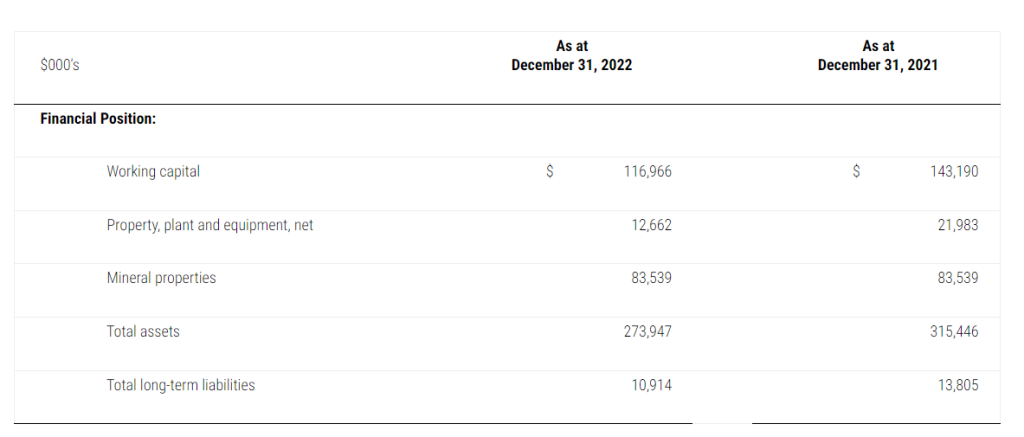

- At December 31, 2022, the Company had a robust balance sheet with $116.97 million of working capital, including $62.80 million of cash and cash equivalents, $12.19 million of marketable securities, $38.16 million of inventory, and no debt. At current commodity prices, the Company’s product inventory has a value of $62.48 million;

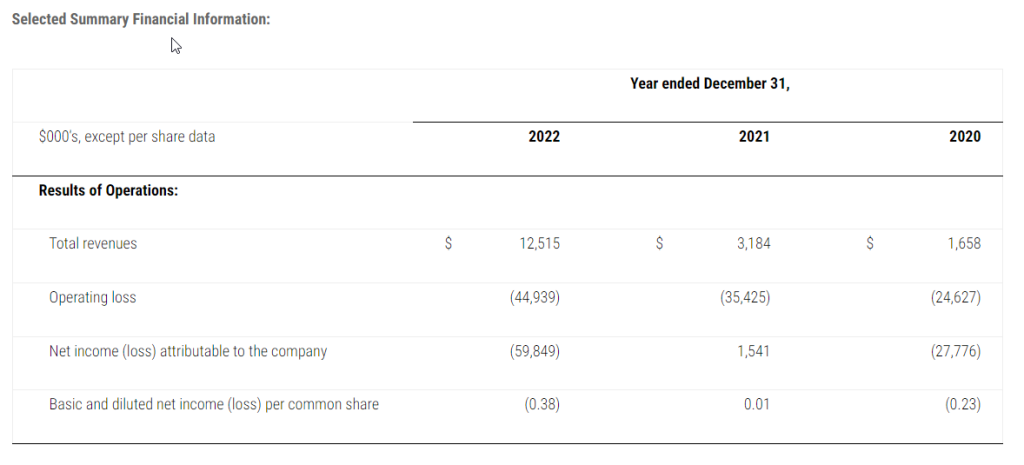

- During the year ended December 31, 2022, the Company incurred a net loss of $59.85 million or $0.38 per share, due in large part to: i) a non-cash mark-to-market loss on investments accounted for at fair value of $16.90 million; ii) increased expenses associated with preparing four(4) of our uranium mines for production; iii) development expenses associated with developing commercial rare earth element (“REE“) separation capabilities in addition to our existing mixed REE carbonate (“RE Carbonate“) commercial production capabilities; (iv) expenses associated with advancing our medical isotope initiatives;(v) increased selling, general and administrative expenses arising from costs associated with acquiring the South Bahia monazite sand project in Brazil (the “Bahia Project“) and costs associated with the sale of the Company’s Alta Mesa in situ recovery (“ISR“) project in Texas; and (vi) increased other selling, general and administrative expenses associated with significant additions to personnel, enhanced business processes, and other general and administrative expenses required to support all these increased levels of activity.

- The Company held 1,027,000 pounds of finished uranium (“U3O8“) inventory at year end, along with approximately 985,000 pounds of finished vanadium (“V2O5“) inventory. At March 8, 2023, following sale and purchase transactions discussed below, the Company held 847,000 pounds of U3O8 and approximately 945,000 pounds of V2O5 inventory.

Uranium Highlights:

- During 2022, the Company produced 162,000 pounds of U3O8 at its White Mesa Mill in Utah (the “Mill“) and remains the largest producer of uranium in the U.S.

- During 2022, the Company was awarded four (4) new uranium supply contracts, with deliveries beginning in 2023, of which three (3) are long-term contracts with U.S. nuclear utilities and one (1) is with the U.S. government to supply the newly established strategic U.S. Uranium Reserve (“U.S. Uranium Reserve“).

- In January 2023, the Company completed the sale of 300,000 pounds of U.S.-origin U3O8 to the U.S. Uranium Reserve realizing total gross proceeds of $18.47 million, or $61.57 per pound of U3O8, resulting in an expected margin of approximately $35.85 per pound of uranium.

- During Q4-2022 and Q1-2023, the Company purchased a total of 301,052 pounds. of U.S.-origin U3O8 on the spot market for a weighted-average price of $50.08 per pound.

- During 2022, the Company made significant progress in preparing four (4) of its conventional uranium and uranium/vanadium mines to be ready to resume uranium ore production, including significant workforce expansion and performing needed rehabilitation of surface and underground infrastructure.

- On February 15, 2023, the Company announced it had completed its previously announced sale of its Alta Mesa ISR Project to enCore Energy Corp. (“enCore“) for total consideration of $120 million, comprised of $60 million in cash and $60 million in a secured convertible note bearing interest at a rate of eight percent (8%) per annum, convertible into common shares of enCore at a price of $2.9103 per share. This sale of a lower priority project provides Energy Fuels with significant additional cash and working capital, enabling the Company to ramp-up its US industry-leading uranium and REE production, while avoiding dilution to shareholders.

Rare Earth Element Highlights:

- During 2022, the Company produced approximately 205 metric tons (“MT“) of high-purity, partially separated RE Carbonate from monazite, containing approximately 95 MT of total rare earth oxides (“TREO“), which is the most advanced REE material being produced commercially in the U.S. today. In Q4-2022, the Company received approximately 600 MT of monazite, which is expected to be processed into 375 to 485 MT of RE Carbonate, containing 175 to 225 MT or TREO, during 2023.

- In early 2023, the Company began modifying and enhancing its existing solvent extraction (“SX“) circuits at the Mill to be able to produce separated REE oxides (“Phase 1“). “Phase 1” is expected to be completed and fully commissioned by late 2023 or early 2024 and have the capacity to produce roughly 800 to 1,000 MT of recoverable separated neodymium-praseodymium (“NdPr“) oxide per year, subject to securing sufficient monazite feed, or enough to provide the permanent magnets to power up to 1 million electric vehicles (“EVs“) per year, which is expected to position the Company as one of the world’s leading producers of NdPr outside of China. “Phase 1” capital costs are expected to total approximately $25 million. The Company is also proceeding with engineering on further enhancements to expand NdPr production capability (“Phase 2“) by 2026 and to produce separated dysprosium (“Dy“), terbium (“Tb“) and potentially other REE materials in the future (“Phase 3“) from monazite and potentially other REE process streams by 2027.

- On February 13, 2023, the Company announced it had completed its previously announced acquisition of a large heavy mineral project in Brazil (the “Bahia Project“), which has the potential to supply the Company’s growing REE business with significant quantities of REE-bearing natural monazite sand for decades. The Bahia Project also contains significant quantities of high-value titanium (ilmenite and rutile) and zirconium (zircon) minerals.

- The Company is currently in active discussions with several additional suppliers of natural monazite around the world to significantly increase the supply of feed for our growing REE initiative.

Vanadium Highlights:

- During 2022, the Company sold approximately 642,000 pounds of existing V2O5 inventory (as ferrovanadium, “FeV“), for an average weighted net price of $13.67 per pound of V2O5.

Medical Isotope Highlights:

- The Company continued advancing its program to evaluate the potential to recover radioisotopes from its process streams for use in emerging targeted alpha therapy (“TAT“) cancer therapeutics.

Mark S. Chalmers, Energy Fuels’ President and CEO, stated:

“2022 was an extraordinary year for Energy Fuels as we expanded our US industry-leading uranium business and established a new, sustainable US rare earth supply chain that is already commercially producing the most advanced rare earth material in the US today. We believe we have clearly emerged as one of the leading U.S. critical mineral companies, producing many of the raw materials needed for the clean energy transition.

“In 2022, positive uranium market fundamentals were magnified by concerns over security of supply, potentially creating new market dynamics for nuclear fuel. Nations around the world are embracing nuclear, as it provides clean, carbon-free electricity on a 24/7 basis, making it indispensable in the fight against climate change. Existing uranium mines globally are depleting, and underinvestment in new mines globally over the past several years could cause supply shortfalls in the coming years. These market fundamentals alone are the best I’ve seen in decades. Then, just over a year ago, Russia invaded Ukraine. Regrettably, the world has allowed Russian state-owned entities to exert disproportionate influence over global uranium and nuclear fuel supply chains over the past several years. Our company has been a leader warning about the inherent risks of such dependence since at least 2017. Most governments and utilities are taking concrete action to stop funding Russia’s war effort in Ukraine through uranium and nuclear fuel purchases. Energy Fuels continues to stand ready to supply and increase the availability of secure, US-produced uranium.

“We have been very active in the uranium space over the past year. In 2022, we began readying several of our conventional uranium and uranium/vanadium mines for production. We have hired about 30 people, and we are making the investments required to put one or more of these facilities into production as soon as later this year. We were also the only U.S. company to produce material quantities of uranium in 2022, having produced 162,000 pounds during Q4-2022, far more than any other company in the U.S. We are proud to have had the opportunity to sell 300,000 pounds of U.S.-produced uranium to the newly established strategic U.S. Uranium Reserve, which is a small but important step in re-establishing the U.S. nuclear fuel capabilities that will allow us to reduce our reliance on Russian uranium imports. We also have another 260,000 pounds of uranium deliveries to a U.S. utility later this year. Our strong uranium inventory position, which currently sits at 847,000 pounds along with another approximately 351,000 pounds contained in ore on the pad at the Mill, together with planned production, will allow us to meet contract deliveries over the life of those contracts, while also providing the flexibility to sell into the spot market and sign new long-term contracts under favorable market conditions.

“2022 was also an incredible year for our rare earth business. No other company is making progress like Energy Fuels in the rare earth space. We continued to produce and optimize our production of partially separated mixed RE Carbonate, though we produced less than expected due to a delay in deliveries that pushed late-2022 production into early-2023. We announced that we are beginning development of a rare earth separation circuit at the Mill that is expected to be commissioned in late-2023 or early-2024. Once operational, this circuit will have the capacity to produce up to 1,000 MT of refined NdPr oxide per year, or enough for up to one million EVs per year. We are also securing the monazite required to feed our rare earth infrastructure, including our recent acquisition of the Bahia Project — a large rare earth, titanium and zirconium project in Brazil — with additional third-party purchases of monazite from Chemours and others expected to be in the pipeline. Today, Energy Fuels’ mixed RE Carbonate is already the most advanced rare earth material commercially produced in the U.S. If we continue to be successful, no other U.S. company will be producing commercial quantities of refined NdPr products ready for offtake as quickly as Energy Fuels.

“We opportunistically sold some of our vanadium inventory in 2022, and we are looking to potentially sell more with V2O5 prices gaining strength recently. Further, our medical isotope initiative is continuing to progress well, and we hope to have more announcements on this very soon.

“Finally, we continue to manage our cash, assets, and working capital to achieve all these heightened initiatives. We take pride in maintaining a strong balance sheet and maintaining the flexibility to do big things. At the end of 2022, we had about $117 million of working capital, with inventories considerably worth more if you apply today’s market prices for uranium and vanadium. In January 2023, we completed the sale of 300,000 pounds of U3O8 to the U.S. Department of Energy for $18.5M. In February 2023, we closed on the sale of our Alta Mesa property in Texas, adding another $120 million to our treasury. Of this, $60 million is in cash and $60 million is in a convertible note bearing interest at eight percent per annum, or about $4.8 million per year.

“We accomplished a great deal over the past year, but this is just the beginning. We have market, geopolitical, and societal tailwinds behind all the commodities we produce, and we fully intend to continue building our critical mineral processes and capabilities. We look forward to providing more updates on future milestones as we achieve them in the weeks and months to come.”

Webcast at 11:00 am ET on March 10, 2023:

Energy Fuels will be hosting a video webcast on March 10, 2023 at 11:00 1m ET (9:00 am MT) to discuss its FY-2022 financial results, the outlook for 2023, and its uranium, rare earths, vanadium, and medical isotopes initiatives. To join the webcast and access the presentation and viewer-controlled webcast slides, please click on the link below:

By clicking this link and registering your name and phone number, the system will call you and place you directly into the call without talking to an operator. If you wish to call in on your own, please dial in to 1-888-664-6392 (toll free in the U.S. and Canada).

A link to a recorded version of the proceedings will be available on the Company’s website shortly after the webcast by calling 1-888-390-0541 (toll free in the U.S. and Canada) and by entering the code 145847#. The recording will be available until March 24, 2023.

Financial Discussion:

At December 31, 2022, the Company had $116.97 million of working capital, including $74.27 million of cash and cash equivalents and marketable securities and $38.16 million of inventory, including approximately 1,027,000 pounds of uranium and 985,000 pounds of high-purity vanadium, both in the form of finished, immediately marketable product. The current spot price of U3O8, according to TradeTech, is $50.50 per pound, and the current mid-point spot price of V2O5, according to Fastmarkets, is $10.78 per pound. Based on those spot prices, the Company’s uranium and vanadium inventories have a current market value of $51.86 million and $10.62 million, respectively, totaling $62.48 million

For the year ended December 31, 2022, we recognized a net loss of $59.85 million or $0.38 per share compared to net income of $1.54 million or $0.01 per share for the year ended December 31, 2021. The change between periods was primarily due to (i) a gain of $35.73 million recognized on the sale of a portfolio of the Company’s non-core conventional uranium projects to Consolidated Uranium Inc. (“CUR“) in 2021 primarily in exchange for shares in CUR; (ii) a non-cash mark-to-market loss on investments accounted for at fair value of $16.90 million in 2022 due primarily to a decrease in the market price of our CUR shares over 2022 (iii) increased expenses in 2022 associated with preparing four (4) of our uranium mines for production or operational readiness amounting to $2.4 million; (iv) development expenses in 2022 associated with developing commercial REE separation capabilities in addition to our existing mixed RE Carbonate commercial production capabilities; (v) expenses in 2022 associated with advancing our medical isotope initiatives; (vi) increased transaction expenses in 2022 arising from costs associated with acquiring the Bahia Project and costs associated with the sale of the Company’s Alta Mesa project in Texas; and (vii) increased other selling, general and administrative expenses in 2022 of $10.2 million associated with significant additions to executive and management/supervisory personnel (including non-cash share-based compensation of $2.5 million), enhanced business processes, and other general and administrative expenses required to support all these increased levels of activity, partially offset by increased revenues in 2022.

Sale to the U.S. Uranium Reserve:

On December 16, 2022, the Company announced it had been awarded a contract to sell 300,000 pounds of U3O8 for $18.5 million ($61.57 per pound of U3O8) to the U.S. government for the establishment of the U.S. Uranium Reserve, resulting in an expected margin of approximately $35.85 per pound of uranium. The Uranium Reserve is intended to be a backup source of supply for domestic nuclear power plants in the event of a significant market disruption. The Company completed the transfer and received the proceeds in January 2023.

Update on Rare Earth Initiatives and the Bahia Project:

Earlier this year, the Company began “Phase 1” REE separation, which includes modifications and enhancements to the existing SX circuits at the Mill. “Phase 1” is expected to have the capacity to process approximately 8,000 to 10,000 MT of monazite per year, producing roughly 4,000 to 5,000 MT TREO, containing roughly 800 to 1,000 MT of recoverable separated NdPr oxide per year. Because Energy Fuels is utilizing existing infrastructure at the Mill, “Phase 1” capital is expected to total only about $25 million. “Phase 1” is expected to be operational later this year or early 2024, subject to receipt of sufficient monazite supply and successful development and commissioning. If these milestones are achieved, Energy Fuels believes it will be the ‘first to market’ among U.S. companies with commercial quantities of separated NdPr available to EV, renewable energy, and other companies for offtake. Later, the Company expects to complete further enhancements to the Mill to expand NdPr production capability (“Phase 2“) by 2026 and to produce separated Dy, Tb and potentially other REE materials in the future (“Phase 3“) from monazite and potentially other REE-bearing process streams by 2027.

On February 13, 2023, the Company announced it had completed the previously announced acquisition of the Bahia Project located between the towns of Prado and Caravelas in the State of Bahia, Brazil totaling 15,089.71 hectares (approximately 37,300 acres or 58.3 square miles). The Bahia Project is a well-known heavy mineral sand (“HMS“) deposit that has the potential to supply 3,000 – 10,000 MT of natural monazite per year for decades to the Mill for processing into high-purity RE Carbonate, separated REE oxides and other REE products and materials. The Bahia Project is also expected to produce large quantities of high-quality titanium (ilmenite and rutile) and zirconium (zircon) minerals that are also in high demand. REE production is highly complementary to Energy Fuels’ existing US-leading uranium business, as monazite and other major REE-bearing minerals naturally contain uranium that will be recovered and other impurities that will be removed at the Mill before further processing into advanced high-purity REE materials. 3,000 – 10,000 MT of monazite contains roughly 1,500 – 5,000 MT of TREO, including 300 – 1,000 MT of NdPr and significant commercial quantities of Dy and Tb.

Prior to the closing on the Bahia Project, the Company commenced a sonic drilling program to further define and quantify the HMS resource, particularly at depth. The limited sonic drilling completed by Energy Fuels over the past few months appears to be confirming that the mineral-bearing sands continue at depth. The Company finished phase 1 of sonic drilling at the Bahia Project on February 14, 2023 totaling 2,266 meters. The Company plans to announce phase 1 drilling results this year and start phase 2 drilling in Q3-2023. Once data from both drill programs are available, the Company plans to engage industry leaders to calculate an initial mineral resource estimate for use in an S-K 1300 (U.S.) compliant Initial Assessment and an NI 43-101 (Canada) compliant Technical Report.

Prior owners of the Bahia Project performed extensive exploration work on the property, including the drilling of over 3,300 hand augur drill holes and a gamma survey of the region. Data from the drilling was used to publish highly detailed exploration and “reserve” reports prepared between 2016 and 2022 that were submitted to the National Mineral Agency of Brazil (“ANM“) in order to move the areas forward toward mining. Based on these seventeen historical reports dated between October 20, 2016 and April 29, 2022, the Bahia Project is estimated to contain 204 million MT of HMS, containing 7.18 million MT of heavy minerals at an average grade of 3.52%, including monazite concentrations in the HMS concentrate between 0.66% and 13.1%. It should be noted that these numbers are historical in nature and a Qualified Person under S-K 1300 or NI-43-101 has not done sufficient work to classify the estimates as a current estimate of Mineral Resources, Mineral Reserves, or exploration results. The Company is not treating these estimates as a current estimate of Mineral Resources, Mineral Reserves or exploration results. Further drilling and data collection might not prove out these numbers.

Sale of Alta Mesa Property to enCore Energy:

On February 15, 2023, the Company announced it had completed the sale (the “Closing“) of three (3) wholly owned subsidiaries that together hold the Alta Mesa ISR Project (“Alta Mesa“) to enCore Energy Corp. (“enCore“) for total consideration of $120 million (the “Transaction“). The consideration is comprised of:

- $60 million cash at or prior to Closing; and

- $60 million in a secured convertible note (the “Note“), payable two (2) years from the Closing, bearing annual interest of eight percent (8%). The Note will be convertible at Energy Fuels’ election into enCore common shares at a conversion price of $2.9103 per share, being a 20% premium to the 10-day volume-weighted average price of enCore shares ending the day before the Closing. enCore was recently listed on the NYSE American and also trades on the TSX Venture Exchange.

The Note is guaranteed by enCore and is fully secured by Alta Mesa. Unless a block trade or similar distribution is executed by Energy Fuels to sell enCore shares received upon conversion of the Note, Energy Fuels will be limited to converting the Note into a maximum of $10 million principal amount per thirty (30) day period.

In addition, enCore replaced the existing reclamation bonds for the Alta Mesa project shortly after the Closing, which will result in Energy Fuels receiving an additional $3.6 million cash as a return of collateral from those bonds. The Transaction is also expected to reduce the Company’s holding costs related to Alta Mesa by approximately $2 million per year.

The Transaction provides Energy Fuels with significant additional cash and working capital, enabling the Company to ramp-up its US industry-leading uranium and REE production, while avoiding dilution to shareholders. In addition, the Note provides Energy Fuels with significant exposure to uranium market upside through potential conversion into enCore common shares.

Operations Update and Outlook for 2023:

Overview

The Company continues to believe that uranium supply and demand fundamentals point to higher sustained uranium prices in the future. The Company believes that nuclear energy, fueled by uranium, is experiencing a global resurgence with an increased focus by governments, policymakers, and citizens on decarbonization, electrification, and security of energy supply. In addition, Russia’s invasion of Ukraine and the entry into the uranium market by financial entities purchasing uranium on the spot market to hold for the long-term has the potential to result in higher sustained spot and term prices and, perhaps, induce utilities to enter into more long-term contracts with non-Russian producers like Energy Fuels to foster security of supply, avoid transportation issues, and ensure more certain pricing.

In 2022, we entered into three long-term uranium contracts with major U.S. utilities for which the Company is beginning to perform the necessary work to recommence production at one or more of its mines, starting as soon as 2023. Until such time when the Company has ramped back up to commercial uranium production, it can rely on its significant uranium inventories to fulfill its new contract requirements, including its recent purchases of U.S. origin uranium on the spot market.

The Company is seeking additional sources of natural monazite to supply feedstock to its emerging REE projects. The Company is also evaluating the potential to recover radioisotopes for use in the development of TAT medical isotopes for the treatment of cancer and continues its support of U.S. governmental activities to assist the U.S. uranium mining industry, including expanding the new U.S. Uranium Reserve Program, supporting efforts to restore domestic nuclear fuel capabilities, and advocating for the responsible sourcing of uranium and nuclear fuel.

We continually evaluate the optimal mix of production, inventory and purchases in order to retain the flexibility to deliver long-term value.

Mill Activities

During the year ended December 31, 2022, the Company recovered and packaged approximately 162,000 pounds of its final uranium product, U3O8, at the Mill, which was added to the Company’s finished product inventory. The Mill recovered an additional small quantity of uranium, which was retained in-circuit and was not packaged in 2022. During 2022, the Mill also focused on its mixed RE Carbonate production and produced approximately 205 MT of high-purity, partially separated mixed RE Carbonate during 2022, while working to secure additional monazite ore feedstock to increase production. The Mill did not recover any vanadium in 2022.

During 2023, the Company does not plan to recover uranium at the Mill, other than from its monazite processing which will likely remain in circuit and not be packaged in 2023. During early 2023, the Company expects to process approximately 600 MT of monazite delivered late in 2022 from Chemours and recover approximately 175 to 225 MT of TREO at the Mill in the form of approximately 375 to 485 MT of RE Carbonate. The Company expects to receive an additional 400 – 700 MT of monazite from Chemours later in 2023, which the Company expects to process for the recovery of uranium and production of separated NdPr and a heavy REE (Sm+) Re Carbonate upon commissioning of the Mill’s Phase 1 REE Separation circuit in late 2023 or early 2024. The Company is also in active discussion with several parties globally to acquire additional quantities of natural monazite, which if secured and delivered to the Mill, could result in significant additional quantities of uranium and separated NdPr and heavy REE (Sm+) Re Carbonate production in 2024 and beyond.

No vanadium production is currently planned during 2023, though the Company continually monitors its inventory and vanadium markets to guide future potential vanadium production.

Conventional Mine Activities

During the year ended December 31, 2022, the Company performed rehabilitation and development work on its La Sal, Beaver, Whirlwind and Pinyon Plain projects for future potential production, including engineering, procurement, construction management, increased development activities, significant workforce expansion and needed rehabilitation of surface and underground infrastructure, while its other conventional mining properties remain on standby. The Company expects to continue its rehabilitation and development work, as it prepares these mines for future production. Although, the timing of the Company’s plans to extract and process mineralized materials from these projects will be based on current contract requirements, inventory levels, sustained improvements in general market conditions, procurement of suitable sales contracts and/or the expansion of the U.S. Uranium Reserve Program, the Company is making the investments required to put one or more of these facilities into production as soon as later in 2023.

The Company is selectively advancing certain permits at its other major conventional uranium projects, such as the Roca Honda, Sheep Mountain, and Bullfrog Projects. All these projects serve as important pipeline assets for the Company’s future conventional production capabilities, as market conditions may warrant.

ISR Mine Activities

The Company expects to produce insignificant quantities of U3O8 in the year ending December 31, 2023 from Nichols Ranch. Until such time when (i) market conditions improve sufficiently, (ii) suitable term sales contracts can be procured, and/or (iii) the U.S. Uranium Reserve Program is expanded, the Company expects to maintain the Nichols Ranch Project on standby and defer development of further wellfields and header houses. The Company currently holds 34 fully permitted, undeveloped wellfields at Nichols Ranch, including four additional wellfields at the Nichols Ranch wellfields, 22 wellfields at the adjacent Jane Dough wellfields, and eight wellfields at the Hank Project, which is fully permitted to be constructed as a satellite facility to the Nichols Ranch Plant.

Inventory

As of December 31, 2022, the Company had approximately 1,027,000 pounds of finished uranium inventories located at North American conversion facilities. Additionally, the Company had approximately 351,000 pounds of additional U3O8 contained in stockpiled Alternate Feed Materials and other ore inventory at the Mill that can be recovered relatively quickly in the future, as general market conditions may warrant. During Q1-2023, the Company completed the purchase 120,000 additional pounds of uranium and the sale of 300,000 pounds of uranium to the U.S. Uranium Reserve, resulting in the Company holding approximately 847,000 pounds of U3O8 in inventory as of March 8, 2023. The Company expects to deliver 260,000 pounds of U3O8 under its existing uranium term contracts in 2023, resulting in expected uranium inventories to total approximately 587,000 pounds of U3O8 at year-end 2023, subject to currently unplanned uranium spot sales and purchases.

The Company currently has approximately 945,000 pounds of V2O5 in inventory, and there remains an estimated 1.0 to 3.0 million pounds of additional solubilized recoverable V2O5 remaining in tailings solutions awaiting future recovery, as market conditions may warrant.

Sales Update and Outlook for 2023

Uranium Sales

While the Company did not sell uranium during the year ended December 31, 2022, the Company entered into four (4) uranium sale and purchase agreements in 2022, three (3) with major U.S. nuclear utilities and one (1) with the U.S. Uranium Reserve. Under these contracts, the Company expects to sell 560,000 pounds of U3O8 during 2023 with an expected weighted-average sales price of $58 – $60 per pound, subject to then-prevailing market prices at the time of delivery.

The three (3) utility contracts require deliveries of uranium between 2023 and 2030, with base quantities totaling 3.0 million pounds of uranium over the period, and up to 4.1 million pounds of uranium if all remaining options are exercised. Having observed a marked uptick in interest from nuclear utilities seeking long-term uranium supply, the Company remains actively engaged in pursuing additional selective long-term uranium sales contracts. During 2023, the Company expects to sell 260,000 pounds of its U3O8 inventory into these contracts at an expected sales price of approximately $54 – $58 per pound, subject to inflation and spot prices in effect at the time of delivery. In addition, in January 2023, the Company completed the sale of 300,000 pounds of its inventories located at ConverDyn to the U.S. Uranium Reserve, receiving total proceeds of $18.47 million ($61.57 per pound).

To provide the Company with additional flexibility to fulfill its contract obligations and gain direct exposure to potential future uranium price increases, the Company has recently purchased a total of 301,052 lbs. of U.S. origin uranium on the spot market for a weighted-average gross price of approximately $50.08 per pound.

Vanadium Sales

As a result of strengthening vanadium markets, during the year ended December 31, 2022, the Company sold approximately 642,000 pounds of the Company’s existing inventory of V2O5 (as FeV) at a net weighted average price of $13.67 per pound of V2O5. The Company expects to sell its remaining finished vanadium product when justified into the metallurgical industry, as well as other markets that demand a higher purity product, including the aerospace, chemical, and potentially the vanadium battery industries. The Company expects to sell to a diverse group of customers in order to maximize revenues and profits. The vanadium produced in the 2018/19 Pond Return campaign was a high-purity vanadium product of 99.6%-99.7% V2O5. The Company believes there may be opportunities to sell certain quantities of this high-purity material at a premium to reported spot prices.

The Company intends to continue to selectively sell itsV2O5 inventory on the spot market as markets warrant but will otherwise continue to maintain its vanadium in inventory.

Rare Earth Sales

The Company commenced its commercial production of a mixed RE Carbonate in March 2021 and has shipped all its RE Carbonate produced to-date to Neo Performance Material’s (“Neo’s“) REE separation plant, Silmet, located in Estonia where it is currently being fed into their separation process. All RE Carbonate produced at the Mill in 2022 was sold to Neo for separation at Silmet. Until such time as the Company commissions its own separation circuits at the Mill, which is expected to be in late 2023 or early 2024, all or a portion of RE Carbonate production is expected to be sold to Neo for separation at Silmet and/or, potentially, to other REE separation facilities outside of the U.S. To the extent not sold, the Company expects to stockpile mixed RE Carbonate at the Mill for future separation and other downstream REE processing at the Mill or elsewhere. During the year ended December 31, 2022, the Company sold approximately 89,000 kilograms of RE Carbonate at an average price of $23.88 per kilogram of RE Carbonate.

While the Company continues to make progress on its mixed RE Carbonate production and additional funds are spent on process enhancements, improving recoveries, product quality and other optimization, profits from this initiative are expected to be minimal until such time when monazite throughput rates are increased and optimized. However, even at the current throughput rates, the Company is recovering most of its direct costs of this growing initiative, with the other costs associated with ramping up production and process enhancements at the Mill being expensed as underutilized capacity production costs applicable to RE Carbonate and development expenditures. Throughout this process, the Company is gaining important knowledge, experience and technical information, all of which are valuable for current and future mixed RE Carbonate production and planned future production of separated REE oxides and other advanced REE materials at the Mill or elsewhere.

ABOUT ENERGY FUELS

Energy Fuels is a leading US-based critical minerals company. The Company mines uranium and produces natural uranium concentrates that are sold to major nuclear utilities for the production of carbon-free nuclear energy. Energy Fuels recently began production of advanced rare earth element (“REE“) materials, including mixed REE carbonate, and plans to produce commercial quantities of separated REE oxides in the future. Energy Fuels also produces vanadium from certain of its projects, as market conditions warrant, and is evaluating the recovery of radionuclides needed for emerging cancer treatments. Its corporate offices are in Lakewood, Colorado, near Denver, and substantially all its assets and employees are in the United States. Energy Fuels holds two of America’s key uranium production centers: the White Mesa Mill in Utah and the Nichols Ranch in-situ recovery (“ISR“) Project in Wyoming. The White Mesa Mill is the only conventional uranium mill operating in the US today, has a licensed capacity of over 8 million pounds of U3O8 per year, has the ability to produce vanadium when market conditions warrant, as well as REE products, from various uranium-bearing ores. The Nichols Ranch ISR Project is on standby and has a licensed capacity of 2 million pounds of U3O8 per year. The Company recently acquired the Bahia Project in Brazil, which is believed to have significant quantities of titanium (ilmenite and rutile), zirconium (zircon) and REE (monazite) minerals. In addition to the above production facilities, Energy Fuels also has one of the largest NI 43-101 compliant uranium resource portfolios in the US and several uranium and uranium/vanadium mining projects on standby and in various stages of permitting and development. The primary trading market for Energy Fuels’ common shares is the NYSE American under the trading symbol “UUUU,” and the Company’s common shares are also listed on the Toronto Stock Exchange under the trading symbol “EFR.” Energy Fuels’ website is www.energyfuels.com.

Daniel Kapostasy, P.G., Director of Technical Services for Energy Fuels, is a Qualified Person as defined by Canadian National Instrument 43-101 and has reviewed and approved the technical disclosure contained in this news release, including sampling, analytical, and test data underlying such disclosure.

The data collected and provided in this disclosure related to the Bahia Project is derived entirely from the exploration reports for each of the seventeen ANM Process Areas. Dan Kapostasy, Director of Technical Services and a Qualified Person for the Company has reviewed these reports in detail and discussed the methods used with the project geologist in charge of field and laboratory activities for the previous owners. This person is also currently an employee of Energy Fuels Brazil, Ltda. Heavy mineral concentrations were derived for every meter drilled using heavy liquid separations, a standard method of heavy mineral determination.

To determine the concentration of the various heavy minerals in a sample, the heavy fraction was separated from the silica sand by using heavy liquid separation. The heavy fraction was then mounted in epoxy or dispersed on slide glass and viewed under a microscope. A geologist can then identify the various minerals and determine the concentration of each mineral through a process called point counting, whereby the geologist identifies each sand grain individually, tallies the number of each mineral and then divides by the total.

Verification of the heavy mineral concentration was started by the Company in September 2022, when it hired a contract driller to collect samples using a sonic rig. While no laboratory analyses have been received to date, visual estimation of the heavy mineral quantity indicates that the historical values seen at the various Process Areas are valid.

Cautionary Note Regarding Forward-Looking Statements: This news release contains certain “Forward Looking Information” and “Forward Looking Statements” within the meaning of applicable United States and Canadian securities legislation, which may include, but are not limited to, statements with respect to: production and sales forecasts; costs of production; any expectation that the Company will be awarded any future sales under the U.S. Uranium Reserve; scalability, and the Company’s ability and readiness to re-start, expand or deploy any of its existing projects or capacity to respond to any improvements in uranium market conditions or in response to the Uranium Reserve; any expectation as to future uranium, vanadium, RE Carbonate, REE oxide, or REE market fundamentals or sales; any expectation as to recommencement of production at any of the Company’s uranium mines or the timing thereof; any expectation regarding any remaining dissolved vanadium in the Mill’s tailings facility solutions or the ability of the Company to recover any such vanadium at acceptable costs or at all; any expectation as to timelines for the permitting and development of projects; any expectation as to longer term fundamentals in the market and price projections; any expectation as to the implications of the current Russian invasion of Ukraine on uranium, vanadium or other commodity markets; any expectation that the Company will maintain its position as a leading U.S.-based critical minerals company; any expectation with respect to timelines to production; any expectation that the sale of the Alta Mesa project and the use of the proceeds from that sale will not result in any dilution to shareholders; any expectation that the Mill will be successful in producing RE Carbonate on a full-scale commercial basis; any expectation that Energy Fuels will be successful in developing U.S. separation, or other value-added U.S. REE production capabilities at the Mill, or otherwise, including the timing of any such initiatives and the expected production capacity or capital and operating costs associated with any such production capabilities; any expectation with respect to the future demand for REEs; any expectation with respect to the quantities of monazite to be acquired by Energy Fuels, the quantities of RE Carbonate or REE oxides to be produced by the Mill or the quantities of contained TREO in the Mill’s RE Carbonate; any expectation that the Company may sell its separated NdPr oxide to major electric vehicle manufacturers in the U.S. and Europe; any expectation that the Bahia Project has the potential to feed the Mill with REE and uranium-bearing monazite sand for decades or at all; any expectation that the Company will complete comprehensive sonic drilling and geophysical mapping at the Bahia Project or complete an Initial Assessment under SK-1300 (U.S.) and a Technical Report Technical Report under NI 43-101 (Canada) during Q4-2023 or Q1-2024, or otherwise; any expectation that the Company’s evaluation of thorium and radium recovery at the Mill will be successful; any expectation that the potential recovery of medical isotopes from any thorium or radium recovered at the Mill will be feasible; any expectation that any thorium, radium or other isotopes can be recovered at the Mill and sold on a commercial basis; any expectation as to the quantities to be delivered under existing uranium sales contracts; any expectation that the Company will be successful in completing any additional contracts for the sale of uranium to U.S. utilities on commercially reasonable terms or at all; and any expectation that the Company will generate net income in future periods. Generally, these forward-looking statements can be identified by the use of forward-looking terminology such as “plans,” “expects,” “does not expect,” “is expected,” “is likely,” “budgets,” “scheduled,” “estimates,” “forecasts,” “intends,” “anticipates,” “does not anticipate,” or “believes,” or variations of such words and phrases, or state that certain actions, events or results “may,” “could,” “would,” “might” or “will be taken,” “occur,” “be achieved” or “have the potential to.” All statements, other than statements of historical fact, herein are considered to be forward-looking statements. Forward-looking statements involve known and unknown risks, uncertainties and other factors which may cause the actual results, performance or achievements of the Company to be materially different from any future results, performance or achievements express or implied by the forward-looking statements. Factors that could cause actual results to differ materially from those anticipated in these forward-looking statements include risks associated with: commodity prices and price fluctuations; engineering, construction, processing and mining difficulties, upsets and delays; permitting and licensing requirements and delays; changes to regulatory requirements; legal challenges; the availability of sources of Alternate Feed Materials and other feed sources for the Mill; competition from other producers; public opinion; government and political actions; available supplies of monazite; the ability of the Mill to produce RE Carbonate, REE oxides or other REE products to meet commercial specifications on a commercial scale at acceptable costs or at all; market factors, including future demand for REEs; the ability of the Mill to be able to separate radium or other radioisotopes at reasonable costs or at all; market prices and demand for medical isotopes; and the other factors described under the caption “Risk Factors” in the Company’s most recently filed Annual Report on Form 10-K, which is available for review on EDGAR at www.sec.gov/edgar.shtml, on SEDAR at www.sedar.com, and on the Company’s website at www.energyfuels.com. Forward-looking statements contained herein are made as of the date of this news release, and the Company disclaims, other than as required by law, any obligation to update any forward-looking statements whether as a result of new information, results, future events, circumstances, or if management’s estimates or opinions should change, or otherwise. There can be no assurance that forward-looking statements will prove to be accurate, as actual results and future events could differ materially from those anticipated in such statements. Accordingly, the reader is cautioned not to place undue reliance on forward-looking statements. The Company assumes no obligation to update the information in this communication, except as otherwise required by law.

SOURCE Energy Fuels Inc.

For further information: Investor Inquiries: Energy Fuels Inc., Curtis Moore, VP – Marketing and Corporate Development, (303) 974-2140 or Toll free: (888) 864-2125, investorinfo@energyfuels.com , www.energyfuels.com