Tokens.com Corp is a publicly traded company that invests in Web3 assets and businesses focused on the Metaverse, NFTs, DeFi, and gaming based digital assets. Tokens.com is the majority owner of Metaverse Group, one of the world’s first virtual real estate companies. Hulk Labs, a wholly-owned Tokens.com subsidiary, focuses on investing in play-to-earn revenue generating gaming tokens and NFTs. Additionally, Tokens.com owns and stakes crypto assets to earn additional tokens. Through its growing digital assets and NFTs, Tokens.com provides public market investors with a simple and secure way to gain exposure to Web3.

Joe Gomes, Senior Research Analyst, Noble Capital Markets, Inc.

Joshua Zoepfel, Research Associate, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

Getting More Cash. Last week, Tokens.com announced the selling of some of the Company’s cryptocurrency inventory in favor of holding cash. This is due to the current volatile environment recently highlighted by the fall of FTX and BlockFi. We believe the selling of cryptocurrency will allow the Company to ride out the volatility of the market and allow the Company to be strategic in future coin purchases.

What Was Sold and Impact. In regards to what was sold from Tokens.com, the Company sold some of the staking rewards generated this year and its smaller non-core holdings of Oasis Rose, ANKR, Mana, and SHIB. The total gross proceeds of the sales is approximately CAD$1.4 million. The Company will now own less Layer 2 assets, although it will continue to focus on holding Layer 1 digital assets including Ethereum and Polkadot.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

Endeavour Silver is a mid-tier precious metals mining company that operates two high-grade, underground, silver-gold mines in Mexico. Endeavour is currently advancing the Terronera mine project towards a development decision, pending financing and final permits and exploring its portfolio of exploration and development projects in Mexico, Chile and the United States to facilitate its goal to become a premier senior silver producer. Our philosophy of corporate social integrity creates value for all stakeholders.

Mark Reichman, Senior Research Analyst, Natural Resources, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

Updated technical report. Endeavour’s Pitarrilla project is an undeveloped silver, lead, and zinc property in Durango State, Mexico and encompasses 4,950 hectares across five concessions with well-developed infrastructure and access to utilities. Endeavor recently published an updated technical report highlighting total open pit and underground indicated mineral resources of 491.6 million ounces of silver, 1.1 million pounds of lead, and 2.6 million pounds of zinc, representing 693.9 million silver equivalent ounces. Total inferred resources include 99.4 million ounces of silver, 281.0 million pounds of lead, and 661 million pounds of zinc, representing 151.2 million silver equivalent ounces.

Next steps. In January, Endeavour will provide more detail regarding 2023 exploration plans at Pitarrilla. We expect it will represent the largest exploration expenditure in 2023, with Terronera shifting to development. At Pitarrilla, Endeavour expects to finish up a 1-kilometer-long tunnel that the previous owners had started which will be used as a drill platform to verify high-grade core.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

Comtech Telecommunications Corp. engages in the design, development, production, and marketing of products, systems, and services for advanced communications solutions in the United States and internationally. It operates in three segments: Telecommunications Transmission, Mobile Data Communications, and RF Microwave Amplifiers. The Telecommunications Transmission segment provides satellite earth station equipment and systems, over-the-horizon microwave systems, and forward error correction technology, which are used in various commercial and government applications, including backhaul of wireless and cellular traffic, broadcasting (including HDTV), IP-based communications traffic, long distance telephony, and secure defense applications. The Mobile Data Communications segment provides mobile satellite transceivers, and computers and satellite earth station network gateways and associated installation, training, and maintenance services; supplies and operates satellite packet data networks, including arranging and providing satellite capacity; and offers microsatellites and related components. The RF Microwave Amplifiers segment designs, develops, manufactures, and markets satellite earth station traveling wave tube amplifiers (TWTA) and broadband amplifiers. Its amplifiers are used in broadcast and broadband satellite communication; defense applications, such as telecommunications systems and electronic warfare systems; and commercial applications comprising oncology treatment systems, as well as to amplify signals carrying voice, video, or data for air-to-satellite-to-ground communications. The company serves satellite systems integrators, wireless and other communication service providers, broadcasters, defense contractors, military, governments, and oil companies. Comtech markets its products through independent representatives and value-added resellers. The company was founded in 1967 and is headquartered in Melville, New York.

Joe Gomes, Senior Research Analyst, Noble Capital Markets, Inc.

Joshua Zoepfel, Research Associate, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

1Q23 Results. Revenue of $131.1 million was up 3.3% sequentially and is the fourth consecutive quarter of growth. Y-o-Y revenue was down 12.2%. We were at $128.3 million. Adjusted EBITDA totaled $10.7 million, nearly double the $5.5 million in 1Q22. We were at $10.2 million. Driven by CEO transition costs, Comtech reported a net loss of $12.8 million, or a loss of $0.46 per share, compared to a net loss of $11.2 million, or $0.43 per share last year. We had forecast a net loss of $3.2 million, or a loss of $0.12 per share.

Making Progress. The transformation of the business into One Comtech is taking root. Key Performance Indicators for the quarter were above expectations. The Senior management team has been restructured and the Company is positioned for growth, in our view.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

“Investors should not care whether the Fed pivots or not if they analyze investment opportunities based on fundamentals and not on monetary laughing gas,” writes economist Daniel Lacalle, PhD. In his latest article, published below. LaCalle takes on the journalists and economists that see market risk differently than himself. This is a thought-provoking read for anyone who has been living on a diet of mostly CNBC, and Yahoo Finance, as exposure to diverse market viewpoints is considered healthy. – Paul Hoffman, Channelchek

Obsessed Investors

In a recent Bloomberg article, a group of economists voiced their fears that the Federal Reserve’s inflation fight may create an unnecessarily deep downturn. However, the Federal Reserve does not create a downturn due to rate hikes; it creates the foundations of a crisis by unnecessarily lowering rates to negative territory and aggressively increasing its balance sheet. It is the malinvestment and excessive risk-taking fuelled by cheap money that lead to a recession.

Those same economists probably saw no risk in negative rates and massive money printing. It is profoundly concerning to see that experts who remained quiet as the world accumulated $17 trillion in negative yielding bonds and central banks’ balance sheets soared to more than $20 trillion now complain that rate hikes may create a debt crisis. The debt crisis, like all market imbalances, was created when central banks led investors to believe that a negative yielding bond was a worthwhile investment because the price would rise and compensate for the loss of yield. A good old bubble.

Multiple expansion has been an easy investment thesis. Earnings downgrades? No problem. Macro weakness? Who cares. Valuations soared simply because the quantity of money was rising faster than nominal GDP (gross domestic product). Printing money made investing in the most aggressive stocks and the riskiest bonds the most lucrative alternative. And that, my friends, is massive asset inflation. The Keynesian crowd repeated that this time would be different and consistently larger quantitative easing programs would not create inflation because it did not happen in the past. And it happened.

Inflation was already evident in assets all over the investment spectrum, but no one seemed to care. It was also evident in non-replicable goods and services. The FAO food price index already reached all-time highs in 2019 without any “supply chain disruption” excuse or blaming it on the Ukraine war. House prices, insurance, healthcare, education… The bubble of cheap money was clear everywhere.

Now many market participants want the Fed to pivot and stop hiking rates. Why? Because many want the easy multiple expansion carry trade back. The fact that investors see a Fed pivot as the main reason to buy tells you what an immensely perverse incentive monetary policy is and how poor the macro and earnings’ outlook are.

Earnings estimates have been falling for 2022 and 2023 all year. The latest S&P 500 earnings’ growth estimates published by Morgan Stanley show a modest 8 and 7 percent rise for this and next year respectively. Not bad? The pace of downgrades has not stopped, and the market is not even adjusting earnings to the downgrade in macroeconomic estimates. When I look at the details of these expectations, I am amazed to see widespread margin growth in 2023 and a backdrop of rising sales and low inflation. Excessively optimistic? I think so.

Few of us seem to realize a Fed pivot is a bad idea, and, in any case, it will not be enough to drive markets to a bull run again because inflationary pressures are stickier than what consensus would want. I find it an exercise in wishful thinking to read so many predictions of a rapid return to 2% inflation, even less, when history shows that once inflation rises above 5% in developed economies, it takes at least a decade to bring it down to 2%, according to Deutsche Bank. Even the OECD expects persistent inflation in 2023 against a backdrop of weakening growth.

Stagflation. That is the risk ahead, and a Fed pivot would do nothing to bring markets higher in that scenario. Stagflation periods have proven to be extremely poor for stocks and bonds, even worse when governments are unwilling to cut deficit spending, because the crowding out of the private sector works against a rapid recovery.

Current inflation expectations suggest the Fed will pivot in the first quarter of 2023. That is an awfully long time in the investment world if you want to bet on a V-shaped market recovery. Even worse, that pivot expectation is based on a surprisingly accelerated reduction in inflation. How can it happen when central banks’ balance sheets have barely moved in local currency, reverse repo liquidity injections reach trillion-dollar levels every month and money supply has barely corrected from the all-time highs of 2022? Many are betting on statistical bodies tweaking the calculation of CPI (consumer price index), and believe me, it will happen, but it will not disguise earnings and margin erosion.

To cut inflation drastically three things need to happen, and only one is not enough. 1) Hike rates. 2) Reduce the balance sheet of central banks meaningfully. 3) Stop deficit spending. This is unlikely to happen anytime soon.

Investors that see the Fed as too hawkish look at money supply growth and how it is falling, but they do not look at broad money accumulation and the insanity of the size of central banks’ balance sheets that have barely moved in local currency. By looking at money supply growth as a variable of tightness in monetary policy they may make the mistake of believing that the tightening cycle is over too soon.

Investors should not care whether the Fed pivots or not if they analyze investment opportunities based on fundamentals and not on monetary laughing gas. Betting on a Fed pivot by adding risk to cyclical and extremely risky assets may be an extremely dangerous position even if the Fed does revert its pace, because it would be ignoring the economic cycle and the earnings reality.

Central banks do not print growth. Governments do not boost productivity. However, both perpetuate inflation and have an incentive to increase debt. Adding these facts to our investment analysis may not guarantee high returns, but it will prevent enormous losses.

Arguments Can be Made for Rates Being Too Low and for Rates Being Too High

The Federal Reserve has raised the Fed Funds rate from an average of 0.08% in January 2022 to its current 4.05%, and a likely adjustment to 4.25% to 4.50% tomorrow. Inflation, as measured by CPI and even the Fed’s favorite, the PCE deflator, has been showing a decreasing rise in prices. So investors within all affected markets are asking, how much more will the Fed raise rates? Ignoring any suggestion that “this time it’s different,” I looked at US interest rates and inflation going back to 1962 and may have found enough consistency and historical norms to help determine what to expect now and why.

Are Increases Nearing an End?

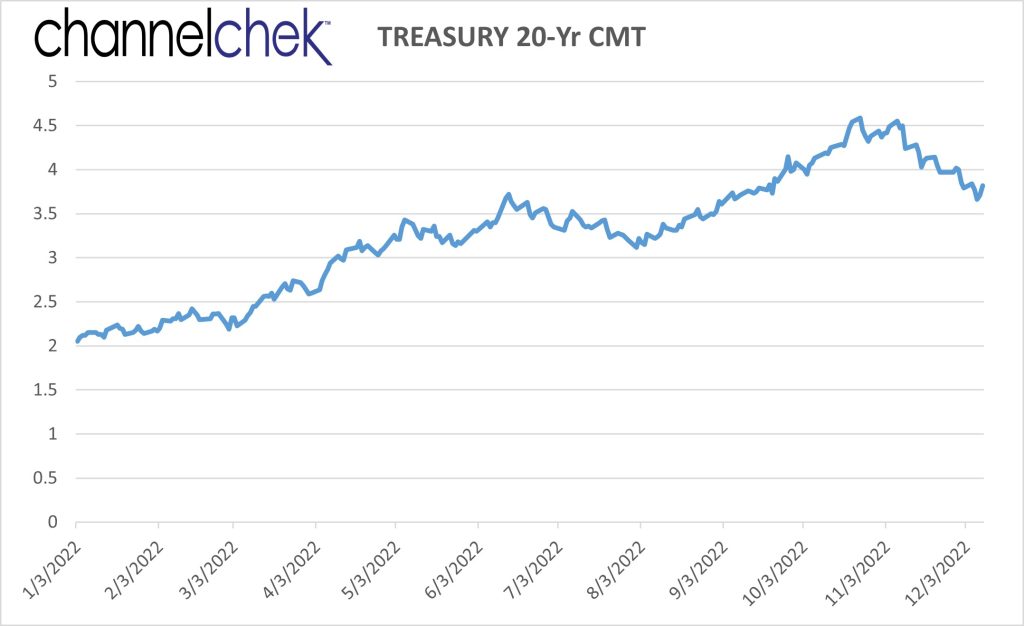

I’ll start with the conclusion. The data suggests that the movement of market rates depends on whether higher current inflation is being caused by temporary or long-lived factors. The 10-year Treasury Note market believes current inflation is mostly temporary. This is shown by its yield, having touched 4.25% in late October, and then falling. The ten-year is now near 3.50%, despite the 0.75% increase in overnight rates implemented on November 2. If the combined wisdom of the Treasury market is reliable, this suggests FOMC rate increases are nearing an end. Perhaps one more smaller hike and then a wait-and-see period. The Fed would then monitor prices while past increases work their way through the economy.

Powell’s Concerns

At his last address on November 30th, Fed Chair Jay Powell indicated he’d rather go too far (with tightening) and then reignite the economy rather than err on the side of not doing enough and having a bigger problem. The markets and the media largely ignored this, but it’s important to know what the Fed Chair believes is prescient and is sharing publicly. Powell also said, “Given our progress in tightening policy, the timing of that moderation is far less significant than the questions of how much further we will need to raise rates to control inflation, and the length of time it will be necessary to hold policy at a restrictive level.” And then he said something very telling, Powell added, “It is likely that restoring price stability will require holding policy at a restrictive level for some time. History cautions strongly against prematurely loosening policy. We will stay the course until the job is done.”

Market Thinks Inflation is Temporary

But, the markets are overjoyed by the last two months of inflation data. Despite what the nations top central banker is saying. Markets may be right, but if they are wrong (bond and stock markets) spotting it early can help stave off losses. If inflation, which is lower than it had been, but not historically low, proves more permanent, for example, if employers continue to have to bid up the price of workers, and demand for goods causes commodity prices to rise, then the Fed will have paused too early. This will lead to a more difficult challenge for the Fed as compared to tightening too much. The data used in this article are from the Federal Reserve Economic Data (FRED) maintained by the Federal Reserve Bank of St. Louis.

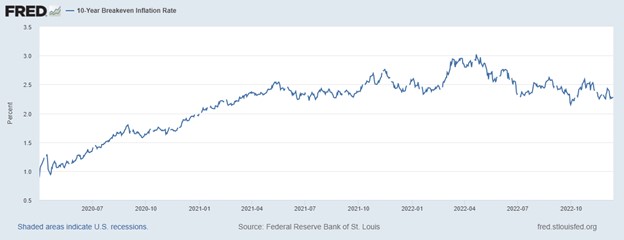

Actual and Expected Inflation

The St. Louis Federal Reserve publishes a market estimate of expected average inflation over the next ten years. It is derived from the 10-year Treasury constant maturity bond and 10-year Treasury inflation-indexed constant maturity bond. It was first published in 2003. Over 2003-2021, 10-year inflation expectation averaged 2.0%, the same as GDP deflator inflation. During the second quarter of 2022, the expected 10-year inflation was 2.7%, or less than 1.0 percentage point above its 2003-2021 average. In contrast, GDP deflator inflation was 7.6%. A significant wedge exists between current and expected inflation.

Source: St. Louis Fed

The breakeven inflation rate represents a measure of expected inflation derived from 10-Year Treasury Constant Maturity Securities (BC_10YEAR) and 10-Year Treasury Inflation-Indexed Constant Maturity Securities (TC_10YEAR). The latest value implies what market participants expect inflation to be in the next 10 years, on average.

Beginning with the end of the last recession on April 1, 2020, the Treasury bond data used in calculating interest rate spreads is obtained directly from the U.S. Treasury Department.

Take Away

The Market’s expectation of 10-year average inflation is dramatically different from current inflation, even at inflation’s new lower pace. This implies the market believes it to be temporary.

If the market’s expectation of inflation is accurate, there is an average difference between Fed Funds and the PCE deflator of 1.6% (since 1962). The last read on PCE was October 2022 at 6%. Reducing this by 1.6 would provide a Fed Funds level of 4.4%. This level is in line with historic averages and likely where we will be after the FOMC meeting wraps up on December 14. This comparatively high rate relative to where we began the year may be considered neutral.

Will the Fed stop at neutral? Are the markets right? Powell said he’d rather err on the side of going beyond what is needed, which suggests the Fed will continue some. As for the markets, being on the side of the markets is how you make money, but getting out before trouble arises is how you keep the money. Markets are not always accurate forecasters and since economic behavior and debt levels tend to adjust slowly, prudent portfolio management suggests it is wise to keep an eye out for today’s interest rates still being too low.

Immunocompromised Individuals, Including Organ Transplant Recipients, are at Increased Risk of Severe COVID-19 and Poor Clinical Outcomes

SARS-CoV-2 has Mutated to Evade the Existing EUA-Approved Therapeutic Monoclonal Antibody Therapies

CHATHAM, N.J., Dec. 12, 2022 (GLOBE NEWSWIRE) — Tonix Pharmaceuticals Holding Corp. (Nasdaq: TNXP), a clinical-stage biopharmaceutical company, today announced that it has obtained an exclusive license from Curia Global, Inc., a leading contract research, development and manufacturing organization, for the development of three humanized murine monoclonal antibodies (mAbs) for the treatment or prophylaxis of SARS-CoV-2 infection. SARS-CoV-2 is the cause of COVID-19.

“We believe that the licensing of these mAbs strengthens our pipeline of next-generation therapeutics to treat COVID-19,” said Seth Lederman, M.D., Chief Executive Officer of Tonix Pharmaceuticals. “Immunocompromised individuals, including organ transplant recipients, are at increased risk of severe COVID-19 and poor clinical outcomes1. Although five monoclonal antibody products, containing seven distinct monoclonal antibodies, have received Emergency Use Authorization (EUA) from the U.S. Food and Drug Administration (FDA) for either treatment or prophylaxis of COVID-19, only a single product, Evusheld®, is still recommended for use as a prophylaxis by the National Institutes of Health COVID-19 Treatment Guidelines Panel or FDA2,3. Moreover, concerns have been raised about the ongoing ability of Evusheld® to prophylax in the face of new variants4. We believe there is a need for second generation mAb treatments and prophylactics for COVID-195. To date, the EUA-approved products have been derived from the blood of COVID-convalescent patients or a humanized mouse6,7. The Company believes that humanized murine monoclonal antibodies discovered by Curia and licensed by Tonix represent a potential new approach to treating SARS-CoV-2 infection. The Company believes that murine monoclonal antibodies have the potential for neutralizing a broader spectrum of SARS-CoV-2 variants and may be harder for SARS-CoV-2 to evade as we face a ‘variant soup’ from both convergent and divergent evolution.”8

Brian Zabel, Ph.D., Senior Director at Curia said, “We are excited to work with Tonix because of their commitment to developing therapeutics to COVID-19. Murine monoclonal antibodies represent a different approach and one that has the potential to generate high affinity antibodies that recognize different epitopes on the SARS-CoV-2 spike protein. Mice have a different repertoire of antibodies and the Curia technology for generating antibodies optimizes the selection of appropriate B cells by the timing of immunization, harvesting approach and screening platform.”

Seth Lederman added, “The potential therapeutic antibodies licensed leverage our expanding internal development and manufacturing capabilities for biologics. These murine monoclonal antibodies and their humanized counterparts build on a base of knowledge from the fully human monoclonal antibody platform, TNX-3600, which we are developing with Columbia University.”

Tonix is a clinical-stage biopharmaceutical company focused on discovering, licensing, acquiring and developing therapeutics to treat and prevent human disease and alleviate suffering. Tonix’s portfolio is composed of central nervous system (CNS), rare disease, immunology and infectious disease product candidates. Tonix’s CNS portfolio includes both small molecules and biologics to treat pain, neurologic, psychiatric and addiction conditions. Tonix’s lead CNS candidate, TNX-102 SL (cyclobenzaprine HCl sublingual tablet), is in mid-Phase 3 development for the management of fibromyalgia with a new Phase 3 study launched in the second quarter of 2022 and interim data expected in the second quarter of 2023. TNX-102 SL is also being developed to treat Long COVID, a chronic post-acute COVID-19 condition. Tonix initiated a Phase 2 study in Long COVID in the third quarter of 2022 and expects interim data in the second quarter of 2023. TNX-1300 (cocaine esterase) is a biologic designed to treat cocaine intoxication and has been granted Breakthrough Therapy designation by the FDA. A Phase 2 study of TNX-1300 is expected to be initiated in the first quarter of 2023. TNX-1900 (intranasal potentiated oxytocin), a small molecule in development for chronic migraine, is expected to enter the clinic with a Phase 2 study in the first quarter of 2023. TNX-601 ER (tianeptine hemioxalate extended-release tablets) is a once-daily formulation of tianeptine being developed as a potential treatment for major depressive disorder (MDD) with a Phase 2 study expected to be initiated in the first quarter of 2023. Tonix’s rare disease portfolio includes TNX-2900 (intranasal potentiated oxytocin) for the treatment of Prader-Willi syndrome. TNX-2900 has been granted Orphan Drug designation by the FDA. Tonix’s immunology portfolio includes biologics to address organ transplant rejection, autoimmunity and cancer, including TNX-1500, which is a humanized monoclonal antibody targeting CD40-ligand (CD40L or CD154) being developed for the prevention of allograft and xenograft rejection and for the treatment of autoimmune diseases. A Phase 1 study of TNX-1500 is expected to be initiated in the first half of 2023. Tonix’s infectious disease pipeline consists of a vaccine in development to prevent smallpox and monkeypox, next-generation vaccines to prevent COVID-19, and a platform to make fully human monoclonal antibodies to treat COVID-19. TNX-801, Tonix’s vaccine in development to prevent smallpox and monkeypox, also serves as the live virus vaccine platform or recombinant pox vaccine (RPV) platform for other infectious diseases. A Phase 1 study of TNX-801 is expected to be initiated in Kenya in the first half of 2023. Tonix’s lead vaccine candidate for COVID-19 is TNX-1850, a live virus vaccines based on Tonix’s recombinant pox live virus vector vaccine platform.

*All of Tonix’s product candidates are investigational new drugs or biologics and have not been approved for any indication.

This press release and further information about Tonix can be found at www.tonixpharma.com.

Forward Looking Statements Certain statements in this press release are forward-looking within the meaning of the Private Securities Litigation Reform Act of 1995. These statements may be identified by the use of forward-looking words such as “anticipate,” “believe,” “forecast,” “estimate,” “expect,” and “intend,” among others. These forward-looking statements are based on Tonix’s current expectations and actual results could differ materially. There are a number of factors that could cause actual events to differ materially from those indicated by such forward-looking statements. These factors include, but are not limited to, risks related to the failure to obtain FDA clearances or approvals and noncompliance with FDA regulations; delays and uncertainties caused by the global COVID-19 pandemic; risks related to the timing and progress of clinical development of our product candidates; our need for additional financing; uncertainties of patent protection and litigation; uncertainties of government or third party payor reimbursement; limited research and development efforts and dependence upon third parties; and substantial competition. As with any pharmaceutical under development, there are significant risks in the development, regulatory approval and commercialization of new products. Tonix does not undertake an obligation to update or revise any forward-looking statement. Investors should read the risk factors set forth in the Annual Report on Form 10-K for the year ended December 31, 2021, as filed with the Securities and Exchange Commission (the “SEC”) on March 14, 2022, and periodic reports filed with the SEC on or after the date thereof. All of Tonix’s forward-looking statements are expressly qualified by all such risk factors and other cautionary statements. The information set forth herein speaks only as of the date thereof.

Motorsport Games, a Motorsport Network company, combines innovative and engaging video games with exciting esports competitions and content for racing fans and gamers around the globe. The Company is the officially licensed video game developer and publisher for iconic motorsport racing series across PC, PlayStation, Xbox, Nintendo Switch and mobile, including NASCAR, INDYCAR, 24 Hours of Le Mans and the British Touring Car Championship (“BTCC”). Motorsport Games is an award-winning esports partner of choice for 24 Hours of Le Mans, Formula E, BTCC, the FIA World Rallycross Championship and the eNASCAR Heat Pro League, among others.

Michael Kupinski, Director of Research, Noble Capital Markets, Inc.

Patrick McCann, Research Associate, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

Equity purchase agreement. On December 9th 2022, the company entered into an equity purchase agreement with Alumni Capital. The equity purchase agreement alleviates the immediate liquidity concerns and allows the company to continue the development and production of its unique product line well into 2023. Additionally, we believe the agreement has the potential to provide sufficient levels of capital until the company generates positive cash flow in the second half of 2023.

Terms of the agreement. At this time the arrangement stipulates that the company has the right to sell Alumni Capital no more than $2 million in common stock. The company has the option to increase the initial purchase amount to $10 million any time prior to December 31st, 2023. If there is an increase in the initial purchase amount, 2% of the increase will be issued to Alumni Capital as consideration shares, and the company will not receive any proceeds for the issuance of commitment shares. The company will pay the expenses for registration of the shares including legal and accounting.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

How Do Floating Wind Turbines Work? Five Companies Just Won the First US Leases for Building them off California’s Coast

Northern California has some of the strongest offshore winds in the U.S., with immense potential to produce clean energy. But it also has a problem. Its continental shelf drops off quickly, making building traditional wind turbines directly on the seafloor costly if not impossible.

Once water gets more than about 200 feet deep – roughly the height of an 18-story building – these “monopile” structures are pretty much out of the question.

A solution has emerged that’s being tested in several locations around the world: wind turbines that float.

In California, where drought has put pressure on the hydropower supply, the state is moving forward on a plan to develop the nation’s first floating offshore wind farms. On Dec. 7, 2022, the federal government auctioned off five lease areas about 20 miles off the California coast to companies with plans to develop floating wind farms. The bids were lower than recent leases off the Atlantic coast, where wind farms can be anchored to the seafloor, but still significant, together exceeding US$757 million.

So, how do floating wind farms work?

Three Main Ways to Float a Turbine

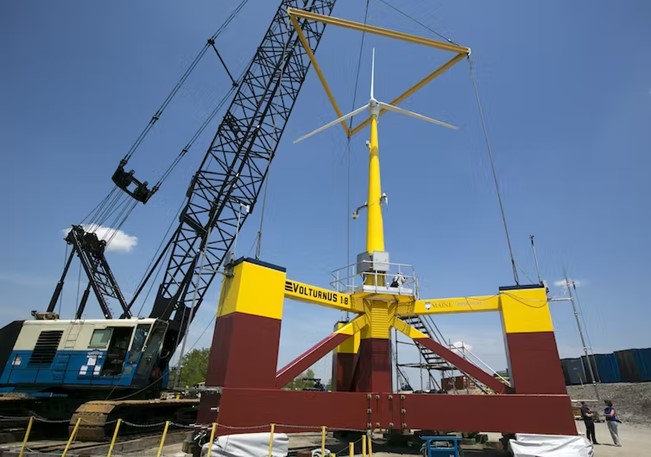

A floating wind turbine works just like other wind turbines – wind pushes on the blades, causing the rotor to turn, which drives a generator that creates electricity. But instead of having its tower embedded directly into the ground or the seafloor, a floating wind turbine sits on a platform with mooring lines, such as chains or ropes, that connect to anchors in the seabed below.

These mooring lines hold the turbine in place against the wind and keep it connected to the cable that sends its electricity back to shore.

Most of the stability is provided by the floating platform itself. The trick is to design the platform so the turbine doesn’t tip too far in strong winds or storms.

Three of the common types of floating wind turbine platform. Josh Bauer/NREL

There are three main types of platforms:

A spar buoy platform is a long hollow cylinder that extends downward from the turbine tower. It floats vertically in deep water, weighted with ballast in the bottom of the cylinder to lower its center of gravity. It’s then anchored in place, but with slack lines that allow it to move with the water to avoid damage. Spar buoys have been used by the oil and gas industry for years for offshore operations.

Semisubmersible platforms have large floating hulls that spread out from the tower, also anchored to prevent drifting. Designers have been experimenting with multiple turbines on some of these hulls.

Tension leg platforms have smaller platforms with taut lines running straight to the floor below. These are lighter but more vulnerable to earthquakes or tsunamis because they rely more on the mooring lines and anchors for stability.

Each platform must support the weight of the turbine and remain stable while the turbine operates. It can do this in part because the hollow platform, often made of large steel or concrete structures, provides buoyancy to support the turbine. Since some can be fully assembled in port and towed out for installation, they might be far cheaper than fixed-bottom structures, which require specialty vessels for installation on site.

The University of Maine has been experimenting with a small floating wind turbine, about one-eighth scale, on a semisubmersible platform with RWE, one of the winning bidders.

Floating platforms can support wind turbines that can produce 10 megawatts or more of power – that’s similar in size to other offshore wind turbines and several times larger than the capacity of a typical onshore wind turbine you might see in a field.

Why Do We Need Floating Turbines?

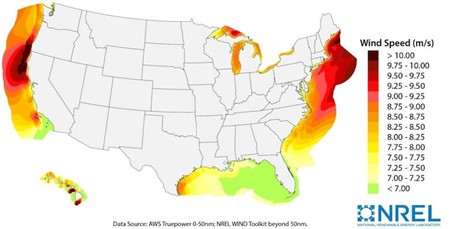

Some of the strongest wind resources are away from shore in locations with hundreds of feet of water below, such as off the U.S. West Coast, the Great Lakes, the Mediterranean Sea and the coast of Japan.

Some of the strongest offshore wind power potential in the U.S. is in areas where the water is too deep for fixed turbines, including off the West Coast. NREL

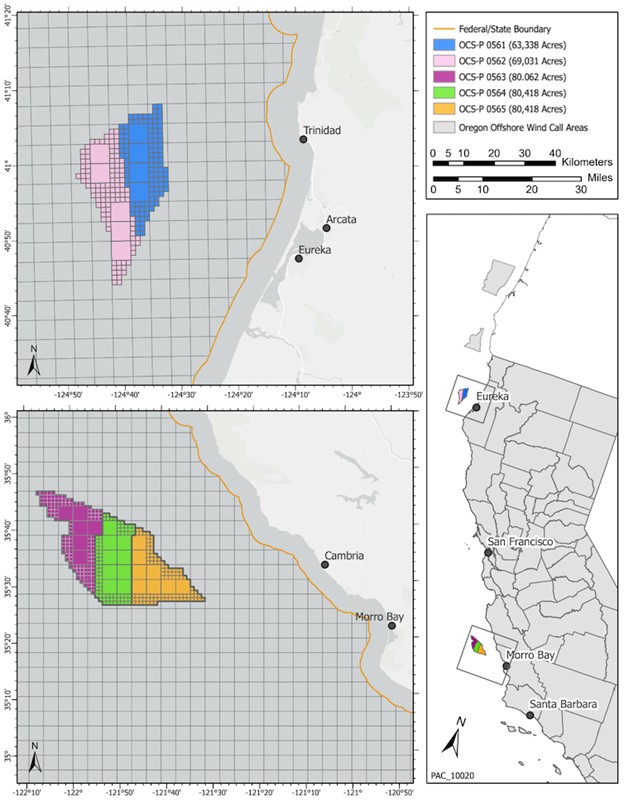

The U.S. lease areas auctioned off in early December cover about 583 square miles in two regions – one off central California’s Morro Bay and the other near the Oregon state line. The water off California gets deep quickly, so any wind farm that is even a few miles from shore will require floating turbines.

Once built, wind farms in those five areas could provide about 4.6 gigawatts of clean electricity, enough to power 1.5 million homes, according to government estimates. The winning companies suggested they could produce even more power.

But getting actual wind turbines on the water will take time. The winners of the lease auction will undergo a Justice Department anti-trust review and then a long planning, permitting and environmental review process that typically takes several years.

The first five federal lease areas for Pacific coast offshore wind energy development. Bureau of Ocean Energy Management

Globally, several full-scale demonstration projects with floating wind turbines are already operating in Europe and Asia. The Hywind Scotland project became the first commercial-scale offshore floating wind farm in 2017, with five 6-megawatt turbines supported by spar buoys designed by the Norwegian energy company Equinor.

Equinor Wind US had one of the winning bids off Central California. Another winning bidder was RWE Offshore Wind Holdings. RWE operates wind farms in Europe and has three floating wind turbine demonstration projects. The other companies involved – Copenhagen Infrastructure Partners, Invenergy and Ocean Winds – have Atlantic Coast leases or existing offshore wind farms.

While floating offshore wind farms are becoming a commercial technology, there are still technical challenges that need to be solved. The platform motion may cause higher forces on the blades and tower, and more complicated and unsteady aerodynamics. Also, as water depths get very deep, the cost of the mooring lines, anchors and electrical cabling may become very high, so cheaper but still reliable technologies will be needed.

But we can expect to see more offshore turbines supported by floating structures in the near future.

This article was republished with permission from The Conversation, a news site dedicated to sharing ideas from academic experts. It represents the research-based findings and thoughts of, Matthew Lackner, Professor of Mechanical Engineering, UMass Amherst.

FOMC Meeting and “Wall Street Wish List” May Impact Your Portfolio Most

Is the Fed really tightening lending rates to cool the economy? Because consumer rates have been headed lower since October. This last FOMC meeting of 2022 may help the markets to understand that something has to give. A 7.7% y-o-y CPI, a 3.75-4.00% Fed Funds target, and a 3.45% 20-year constant maturity treasury can not co-exist for long. Treasury investors either need to earn more to keep up with expected inflation realities, inflation needs to show a more certain downtrend or the Fed needs to go back to lowering Fed Funds levels. Having lived through the last three years of markets, which I can attest from experience, are very different from the previous 30 years, I’m still putting my money on what the Fed Chairman tells us he’s doing. However, markets being what they are will move with the moves of the masses, and that is what’s “right” because that is what makes money.

The December FOMC meeting is front and center this week. We also get a new CPI report pre-meeting. Expect volatility, especially with longer-term treasuries already priced for a great CPI number.

2:00 PM ET, Treasury Statement, forecasters see a $200.0 billion deficit in November that would compare with a $191.3 billion deficit in November a year ago and a deficit in October this year of $87.8 billion. The government’s fiscal year began in October. The size of the budget deficit is important because it impacts the amount of treasury issuance, and then supply and demand take over in terms of interest rates demanded to fill the supply.

Tuesday 12/13

6:00 AM ET, Optimism is expected to remain low. The small business optimism index has been below the historical average of 98 for ten months in a row and deeply so in October at 91.3. November’s consensus is 90.8.

8:30 AM ET, CPI for November is the first information with potential market-altering data to be released this week. It will be the last look at CPI for a month during 2022. CPI is expected to be 0,% for the month or 7.3% y-o-y. Do you remember how the market rallied on the better than the consensus 7.7% last month? Any deviation from the consensus could cause an impact.

Wednesday 12/14

8:30 AM ET, Atlanta Fed Business Inflation Expectations for December. While we have no consensus data, The Atlanta Fed’s Business Inflation Expectations survey came in last month at 3.3% expected. The survey number provides a monthly measure of year-ahead inflation expectations and inflation uncertainty from the perspective of firms. The survey also provides a monthly gauge of firms’ current sales, profit margins, and unit cost changes.

2:00 PM ET, FOMC Announcement, let the trading week unofficially begin as markets shuffle with new information from the 2:00 PM announcement and press conference that follows. After a series of 75 bp moves, the Fed is expected to be less aggressive with a 50 bp increase.

Thursday 12/15

8:30 AM ET, Jobless Claims for the December 10 week are expected to come in at 230,000, or unchanged from the prior week. A large deviation from this number could move markets as employment is a Fed mandate.

9:00 AM ET, Wall Street Wish List. Seasoned Analysts from Noble Capital Market’s veteran team discuss the sectors and companies they cover and perhaps provide actionable ideas as to where they may lean in the year ahead. Information for free online event is here.

Friday 12/16

9:45 AM ET, PMI Composite Flash. At 46.2 in November, the services PMI has been sinking deeper into contraction though expectations for December’s flash is a little slower pace of contraction at 46.5. Manufacturing, at 47.7 in November, is expected little changed at 47.8.

What Else

The weekly focus is on the FOMC decision and press conference. Register for Channelchek emails and receive our synopsis of the FOMC outcome immediately post announcement.

It may turn out that the Wall Street Wish List is the most profitable sharing of ideas that you receive headed into the new year. Don’t miss this by clicking on the banner below to allow you free access.

Fed Wants Inflation to Get Down to 2% – But Why Not Target 3%? Or 0%?

What’s so special about the number 2? Quite a lot, if you’re a central banker – and that number is followed by a percent sign.

That’s been the de facto or official target inflation rate for the Federal Reserve, the European Central Bank and many other similar institutions since at least the 1990s.

But in recent months, inflation in the U.S. and elsewhere has soared, forcing the Fed and its counterparts to jack up interest rates to bring it down to near their target level.

This article was republished with permission from The Conversation, a news site dedicated to sharing ideas from academic experts. It represents the research-based findings and thoughts of, Veronika Dolar, Assistant Professor of Economics, SUNY Old Westbury.

As an economist who has studied the movements of key economic indicators like inflation, I know that low and stable inflation is essential for a well-functioning economy. But why does the target have to be 2%? Why not 3%? Or even zero?

Soaring Inflation

The U.S. inflation rate hit its 2022 peak in July at an annual rate of 9.1%. The last time consumer prices were rising this fast was back in 1981 – over 40 years ago.

Since March 2022, the Fed has been actively trying to decrease inflation. In order to do this, the Fed has been hiking its benchmark borrowing rate – from effectively 0% back in March 2022 to the current range of 3.75% to 4%. And it’s expected to lift interest rates another 0.5 percentage point on Dec. 14 and even more in 2023.

Most economists agree that an inflation rate approaching 8% is too high, but what should it be? If rising prices are so terrible, why not shoot for zero inflation?

Maintaining Stable Prices

One of the Fed’s core mandates, alongside low unemployment, is maintaining stable prices.

Since 1996, Fed policymakers have generally adopted the stance that their target for doing so was an inflation rate of around 2%. In January 2012, then-Chairman Ben Bernanke made this target official, and both of his successors, including current Chair Jerome Powell, have made clear that the Fed sees 2% as the appropriate desired rate of inflation.

Until very recently, though, the problem wasn’t that inflation was too high – it was that it was too low. That prompted Powell in 2020, when inflation was barely more than 1%, to call this a cause for concern and say the Fed would let it rise above 2%.

Many of you may find it counterintuitive that the Fed would want to push up inflation. But inflation that is persistently too low can pose serious risks to the economy.

These risks – namely sparking a deflationary spiral – are why central banks like the Fed would never want to adopt a 0% inflation target.

Perils of Deflation

When the economy shrinks during a recession with a fall in gross domestic product, aggregate demand for all the things it produces falls as well. As a result, prices no longer rise and may even start to fall – a condition called deflation.

Deflation is the exact opposite of inflation – instead of prices rising over time, they are falling. At first, it would seem that falling and lower prices are a good thing – who wouldn’t want to buy the same thing at a lower price and see their purchasing power go up?

But deflation can actually be pretty devastating for the economy. When people feel prices are headed down – not just temporarily, like big sales over the holidays, but for weeks, months or even years – they actually delay purchases in the hopes that they can buy things for less at a later date.

For example, if you are thinking of buying a new car that currently costs US$60,000, during periods of deflation you realize that if you wait another month, you can buy this car for $55,000. As a result, you don’t buy the car today. But after a month, when the car is now for sale for $55,000, the same logic applies. Why buy a car today, when you can wait another month and buy a car for $50,000 next month.

This lower spending leads to less income for producers, which can lead to unemployment. In addition, businesses, too, delay spending since they expect prices to fall further. This negative feedback loop – the deflationary spiral – generates higher unemployment, even lower prices and even less spending.

In short, deflation leads to more deflation. Throughout most of U.S. history, periods of deflation usually go hand in hand with economic downturns.

Everything in Moderation

So it’s pretty clear some inflation is probably necessary to avoid a deflation trap, but how much? Could it be 1%, 3% or even 4%?

Maybe. There isn’t any strong theoretical or empirical evidence for an inflation target of exactly 2%. The figure’s origin is a bit murky, but some reports suggest it simply came from a casual remark made by the New Zealand finance minister back in the late 1980s during a TV interview.

Moreover, there’s concern that creating economic targets for economic indicators like inflation corrupts the usefulness of the metric. Charles Goodhart, an economist who worked for the Bank of England, created an eponymous law that states: “When a measure becomes a target, it ceases to be a good measure.”

Since a core mission of the Fed is price stability, the target is beside the point. The main thing is that the Fed guide the economy toward an inflation rate high enough to allow it room to lower interest rates if it needs to stimulate the economy but low enough that it doesn’t seriously erode consumer purchasing power.

Motorsport Games Enters into Equity Purchase Agreement

MIAMI, Dec. 09, 2022 (GLOBE NEWSWIRE) — Motorsport Games Inc. (NASDAQ: MSGM) (“Motorsport Games” or the “Company”) today announced that the Company has entered into a purchase agreement (the “Agreement”) with an investor for up to $2 million, which amount may increase at the Company’s option to $10 million.

Under the terms and conditions of the Agreement, the Company has the right, but not the obligation, to sell to the investor up to $2 million of its shares of common stock, which amount may increase at the Company’s option to up to $10 million in shares, until December 31, 2023, subject to certain limitations. Any shares of common stock that is sold to the investor will occur at a purchase price that is determined in part by prevailing market prices at the time of each sale. The investor has agreed not to cause or engage in any short selling or hedging of the Company’s common stock. The Company issued common shares to the investor as consideration for the investor’s commitment to purchase the Company’s common stock under the Agreement.

“We are pleased to enter into the purchase agreement and expect to use the proceeds, as available, for product development and other business purposes. This transaction provides us with additional financial flexibility as we continue to execute on our business plan,” said Dmitry Kozko, CEO and Executive Chairman of Motorsport Games.

The foregoing summary of the Agreement is incomplete, and further details relating to the Agreement, including additional terms and conditions, and this transaction will be contained in the Current Report on Form 8-K the Company intends to file with the Securities and Exchange Commission later today.

This press release shall not constitute an offer to sell or the solicitation of an offer to buy these securities, nor will there be any sale of these securities in any jurisdiction in which such offer, solicitation or sale would be unlawful prior to the registration or qualification under the securities laws of any such jurisdiction.

The offering of the securities described in this press release is being made pursuant to the Company’s effective shelf registration statement on Form S-3 (File No. 333-262462) (the “Registration Statement”), and the related base prospectus included in the Registration Statement, as supplemented by a prospectus supplement to be filed with the SEC on or about December 9, 2022. Copies of the prospectus supplement and accompanying prospectus may be obtained when filed with the SEC at the SEC’s website at www.sec.gov.

About Motorsport Games:

Motorsport Games, a Motorsport Network company, is a leading racing game developer, publisher and esports ecosystem provider of official motorsport racing series throughout the world. Combining innovative and engaging video games with exciting esports competitions and content for racing fans and gamers, Motorsport Games strives to make the joy of racing accessible to everyone. The Company is the officially licensed video game developer and publisher for iconic motorsport racing series across PC, PlayStation, Xbox, Nintendo Switch and mobile, including NASCAR, INDYCAR, 24 Hours of Le Mans and the British Touring Car Championship (“BTCC”), as well as the industry leading rFactor 2 and KartKraft simulations. rFactor 2 also serves as the official sim racing platform of Formula E, while also powering F1 Arcade through a partnership with Kindred Concepts. Motorsport Games is an award-winning esports partner of choice for 24 Hours of Le Mans, Formula E, BTCC, the FIA World Rallycross Championship and the eNASCAR Heat Pro League, among others. Motorsport Games is building a virtual racing ecosystem where each product drives excitement, every esports event is an adventure and every story inspires.

FORWARD-LOOKING STATEMENTS

Certain statements in this press release which are not historical facts are forward-looking statements within the meaning of Section 27A of the Securities Act of 1933, as amended, and Section 21E of the Securities Exchange Act of 1934, as amended, and are provided pursuant to the safe harbor provisions of the Private Securities Litigation Reform Act of 1995. Any statements in this press release that are not statements of historical fact may be deemed forward-looking statements. Words such as “continue,” “will,” “may,” “could,” “should,” “expect,” “expected,” “plans,” “intend,” “anticipate,” “believe,” “estimate,” “predict,” “potential,” and similar expressions are intended to identify such forward-looking statements. All forward-looking statements involve significant risks and uncertainties that could cause actual results to differ materially from those expressed or implied in the forward-looking statements, many of which are generally outside the control of Motorsport Games and are difficult to predict. Examples of such risks and uncertainties include, without limitation, sales of shares under the Agreement impacting the price of the Company’s Class A common stock, inability to raise funds under the Agreement due to certain limitations under the Agreement, and less than expected results from the proceeds raised from any transaction under the Agreement. Additional factors that could cause actual results to differ materially from those expressed or implied in the forward-looking statements can be found in Motorsport Games’ filings with the SEC, including its Annual Report on Form 10-K for the fiscal year ended December 31, 2021, its Quarterly Reports on Form 10-Q filed with the SEC during 2022, as well as in its subsequent filings with the SEC. Motorsport Games anticipates that subsequent events and developments may cause its plans, intentions and expectations to change. Motorsport Games assumes no obligation, and it specifically disclaims any intention or obligation, to update any forward-looking statements, whether as a result of new information, future events or otherwise, except as expressly required by law. Forward-looking statements speak only as of the date they are made and should not be relied upon as representing Motorsport Games’ plans and expectations as of any subsequent date.

Website and Social Media Disclosure:

Investors and others should note that we announce material financial information to our investors using our investor relations website (ir.motorsportgames.com), SEC filings, press releases, public conference calls and webcasts. We use these channels, as well as social media and blogs, to communicate with our investors and the public about our company and our products. It is possible that the information we post on our websites, social media and blogs could be deemed to be material information. Therefore, we encourage investors, the media and others interested in our company to review the information we post on the websites, social media channels and blogs, including the following (which list we will update from time to time on our investor relations website):

MELVILLE, N.Y. – December 8, 2022–Comtech (NASDAQ: CMTL), a leading global provider of satellite and space communications and terrestrial and wireless network infrastructures, today announced its first quarter fiscal 2023 financial results and updated its second quarter fiscal 2023 financial targets in a letter to shareholders which is now posted to the Investor Relations section of Comtech’s website.

Investors are invited to access the first quarter fiscal 2023 shareholder letter at its web site at investor.comtech.com. A copy of the letter will also be filed with the Securities and Exchange Commission in a Form 8-K.

Comtech also intends to host a previously scheduled earnings conference call at 5:00PM ET today that is intended to be briefer but provide more time for questions and discussion. Individuals can access the conference call by dialing (800) 225-9448 (domestic) or (203) 518-9708 (international) and using the conference I.D. of “Comtech.” A replay of the conference call will be available for seven days by dialing (800) 839-2434 or (402) 220-7211. A live webcast of the call is also available at investor.comtech.com.

About Comtech

Comtech is a leading global provider of satellite and space communications and terrestrial and wireless network infrastructures to commercial and government customers around the world. Headquartered in Melville, New York and with a passion for customer success, Comtech designs, produces and markets advanced and secure wireless solutions. For more information, please visit www.comtech.com.

Certain information in this press release contains statements that are forward-looking in nature and involve certain significant risks and uncertainties. Actual results could differ materially from such forward-looking information. The Company’s Securities and Exchange Commission filings identify many such risks and uncertainties. Any forward- looking information in this press release is qualified in its entirety by the risks and uncertainties described in such Securities and Exchange Commission filings.

PCMTL

View source version on businesswire.com: https://www.businesswire.com/news/home/20221208005817/en/

Lee Enterprises, Incorporated provides local news, information, and advertising primarily in midsize markets in the United States. It publishes 49 daily newspapers, as well as offers 300 weekly newspapers and specialty publications in 23 states. The company also provides online advertising and services; and online infrastructure and online publishing services for approximately 1,500 daily and weekly newspapers and shoppers. In addition, it offers commercial printing services. The company has a strategic alliance with Yahoo!, Inc. to provide its classified employment advertising customer base the opportunity to post job listings and other employment products on Yahoo!�s HotJobs national platform. Lee Enterprises, Incorporated was founded in 1890 and is based in Davenport, Iowa.

Michael Kupinski, Director of Research, Noble Capital Markets, Inc.

Patrick McCann, Research Associate, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

Solid Q4 results. The company reported strong Q4 revenue of $193.6 million, topping our forecast of $191.2 million. Adj. EBITDA was also favorable at $30.1 million, compared with our estimate of $29.5 million. Figure #1 Q4 Variance illustrates the favorable quarterly performance.

Digital growth accelerates. In spite of an 11% decline in Print revenue, total revenue was flat in the quarter, due to accelerating Digital revenue. Digital revenue grew 33% over the prior year period and accounted for 31% of total company revenue. Digital revenue growth was led by Amplified, the company’s Digital Media Solutions business, which grew 83% over the prior year period.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.