Gregory Aurand, Senior Research Analyst, Healthcare Services & Medical Devices, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

FQ3 2023 reported for the period ending October 31, 2022. As expected, no revenues were reported by the Company yesterday. Overall, expenses were higher than expectations, with lower than expected G&A and R&D expenses reported. Fair value adjustments in embedded derivatives, higher share based compensation and financing costs accounted for the difference in reported loss per share of $0.04 vs. our expected $0.03 loss per share. Our full fiscal year 2023 loss per share moves to $0.11 from prior $0.10.

ORTHO-R Phase I trial for rotator cuff completed. The initial portion was completed in early November. There were no safety issues reported, opening up Phase II enrollment at all 10 clinical sites. Phase II enrollment is now expected to be completed by end of calendar second quarter 2023, although this is a slight slippage from our earlier expectations. Patient assessment and scoring will occur after 12-month follow-up.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

The Year 2022 Brought Many Twists and Turns to Share with Readers – the Editor Picks His Favs

All markets are interconnected. In fact, markets are impacted by weather, war, worry, Washington, wages, waste, and that’s just the W’s. So each day, as Channelchek prepares to deliver research, articles, and pertinent video content to subscriber’s inboxes, we plow through a mountain of information and hope to share what is either not being addressed or covered, or present front page news from the point of view of seasoned investors, not rookie news writers.

Below are five articles that were published throughout the year on Channelchek. Although I have favorites not included here, and these are not the most read, I believe the below told a slightly different story than the mainstream narrative. As a content provider to this popular investment research platform, my job is not to call the market, it is to provide thoughts and knowledge to help you make decisions on small and microcap stocks and the overall universe of investment opportunities. Still, the content team is proud when, for example, the entire newswire exploded with the word “pivot” that we then reminded our readers there was nothing indicating a pivot was imminent or even being discussed among FOMC members. As most Channelchek content providers are investors, analysts, and market watchers, we were also proud to serve our readership by being among the first to dig through the $AMC $APE dividend and define the true effects to stakeholders.

I think you’ll find these five articles are still compelling, and if you have not registered for no-cost insights to your inbox each day, here’s your chance to start the New Year from a slightly different investment angle.

“So, ladies and gentlemen, gentlemen and ladies, TODAY WE POUNCE.” This is how the AMC Chairman began his letter to shareholders on August 4. The company announced a unique dividend to be awarded to listed shareholders later in the month. The impact of the dividend is still being felt and discussed among market participants.

In this article explaining the Fed not pivoting but instead doubling down on describing a strong hawkish bias does not necessarily mean bad news for investors in stocks. It’s a follow-up article to Don’t Fear the Rate Hike, which was widely read and shared on social media. There is information in the above Fed pivot article that I am certain will be as pertinent in 2023 as it was in 2022.

#3 What Investors Haven’t Yet Noticed About the Value in Some Biotechs

If you’re shopping for a wallet and one comes complete with $100 worth of cash inside and is priced at $60, would you think there is value to this purchase? A situation similar to this has evolved in many biotech stocks. The article was written in late May, and although it has only played out for a few companies in the sector, conditions still exist for a feeding frenzy in biotech stocks. Information within the article could also apply to other sectors that have lost popularity post Covid19.

The only real contact hedge fund manager Michael Burry has with the outside world is Twitter posts (which, since Musk’s arrival, Burry now promises not to delete), his quarterly SEC filing of holdings, and every four or five years he will allow an interview with Bloomberg via Bloomberg Msg. Investment content providers are all over every tweet and quick to tell the world what it means. There are even YouTube channels that exist only to guess at what Burry’s portfolio at Scion may hold and what Burry (maybe) thinks. They do this because many readers swarm to learn more about what he is preparing for.

Some of the most widely read and long-lived content on Channelchek are articles about this guru. Still we promise to only present his tweets, filings, and thoughts when the information seems useful.

Written in late April, this article hit a need that stayed important to readers throughout 2022. While the exact numbers are no longer current, the knowledge of how one market impacts another is always worth tucking away in the back of your brain so that, as an investor or trader, you can be early on building a position rather than later when the trade may have already hit the news and lost the bulk of its move. While there are always moving pieces, especially when it comes to currency strength, this article, most often discovered through Google searches, is super short but contains useful information.

Happy New Year

Thank you for letting us be a part of 2022. In the coming year, we have plans to continue everything we are now doing and add on some features that we believe will provide users with relevant information not found in too many other places.

If you have not yet signed up, now is a great time to make sure you don’t miss anything. Click Here.

I don’t think I’m a very good businessman. I act too much with the heart. – Pelé

If you treat the holdings in your trading account with any attachment, your ability to sell at the right time will be hindered, and your profit potential will suffer. Ideally, an active trading account accumulates when the selling volume reaches a peak, prices are cheap, and lightens up when prices are sufficiently above the purchase price. Or when there appears to be better used for the account’s capital — including moving to cash equivalents.

The Pelé quote above reminds me of many active traders; they enjoy the rush of playing and know they can only claim a victory when on the field and in play. These traders often stay on the field too long and accumulate losing positions. The markets are not a game where the odds of winning or losing are equal on any given day. Trading the markets is better thought of as a business that, at times should increase inventory and at times scale down.

Think of Your Trading Account as a Business

I struggled this week as I had two positions in the red that, for tax reasons, I should let go of to offset gains and the taxes that go along with those gains. These positions are not acting poorly, but they are negative, and they both are taking longer than I had hoped to pay off. Each easily allows me to immediately purchase a similar position without upsetting the IRS. But I have hesitated to sell all week.

If trading is a business, one does what is believed to net the most profit – always. I’m usually pretty good at this, but these two small positions would represent my first losses of the year in my trading account (hurray for me). I was fortunate enough to spot the market’s relentless one-direction trend in 2022, this allowed me to ride the downward waves. The trend seems to be continuing, so exiting these two holdings and getting back into something with similar attributes makes solid business management sense. But it isn’t that easy, I’m a competitive person. The “sportsman” side of me did not want to take any losses after dozens of wins. Today, the last day of the year, I woke and told myself the intelligent thing is doing what should net more money – not what will net bragging rights over win percentage.

There are many other reasons people don’t sell when the probabilities indicate they should. One is not pre-determining if the trade is behaving as expected; another is falling in love with a stock and not wanting to part with it. Another is knowing you were once up and not wanting to permanently lock in something that is now red. Another may be “addiction to the game,” this burns money; a good trader should be comfortable sitting with a large cash position for weeks or months if that is what makes the most business sense.

All of these feelings that impact behavior are part of being human. There are plenty of other outlets to act on feelings outside of the markets, but investing requires you to act as though you are running a business. Don’t fall in love with your positions, and if they aren’t treating you well, get rid of them.

Image Credit: Mike W. (Flickr)

Car Lot Owner Mentality

This may not work for everyone, but I think of my trading account (not retirement savings) as a used car lot. I am the manager and every one of the cars represents something I want to sell. If you look at your account in this way, stocks are just inventory. If times are good and prices are rising on my inventory, I want to slow down the pace of my selling. When times ahead look as though people may not want the kind of inventory on my lot, I can’t sell fast enough, even if at a loss. The cash then raised serves as dry powder that stands ready to be invested in cars/inventory/stocks believed to be more in demand. Inventory that will provide more of a profit.

By thinking of my account as a car lot, I avoid 95% of the mental, “acting with the heart” trading missteps that I see others get trapped by. I still have a 5% problem that includes wanting a perfect score.

Investors buying and selling on an exchange have a huge advantage over managers of a car lot. For most exchange traded securities, finding someone to close out your position with does not require someone walking in off the street that just happens to want what is on your lot. Investors of securities have sell buttons that alert the investment community that you are unloading. Even thinly traded securities will have someone take the other side of the trade at the right price. There are no other businesses in the world where unwanted inventory is this easy to unload. Traders are like car lot owners with this unique advantage.

Don’t Coddle the HODL Model

While buy and hold may be a good long-term portfolio strategy for retirement money or other long-term assets, holding without reason other than the investment community encourages you to “HODL” forever and not to throw in the towel can get you in trouble. The HODL community encourages investors of certain assets to Hold On for Dear Life; this isn’t trading; it’s a recipe for an ulcer.

When does it make sense to close out a position? In general, there are some marketplace related reasons to unwind a position. These are reasons that are related to the company, changes in the markets, or better opportunity elsewhere. Or non-market-related outside reasons. Perhaps one wishes to use some of the profit to put in a pool, or they wish to stem possible losses while waiting for better clarity. Outsiders encouraging an entire community to hold a position to help push up its price only works until greed kicks in and those sworn to HODL realize the stock is up for unnatural reasons and they should be among the first out.

Kneejerk market reactions to news or events can cause a wave of selling or buying that then settles down and reverses somewhat. This may provide an opportunity to unwind positions into the feeding frenzy and re-enter it when the market settles in at a more level-headed price.

Broaden Investment Base

If you are a used car lot owner during a recession, you may opt to only half-fill your lot and make sure the cars in inventory are affordable to the community you serve. If the economy fires up and money is then widely available, you may want to maximize your inventory and make sure they are cars that will net the most profit. It is important to know a lot about different classes of cars. This is how you run that business, minivans and crossovers some years, even if you like British sports cars.

For trading, after the pandemic plunge in early 2020, the markets had solid trends. First up with many sectors outpacing the others. Then it trended down, with many sectors outpacing the others. Understanding the sectors and companies within the sectors allows better decisions. If you have spent all your time wondering whether you should get into Apple or Tesla at the exclusion of others, while oil companies or utilities were what had a clear trend, or in Nasdaq 100 stocks because the media always talks about them, when small-caps were making their move, you may wish to broaden your focus.

Take-Away

Internal trouble exiting positions impacts more self-directed investors than will ever admit to it on social media (or actual in-the-flesh interaction). If thought of as inventory and a tool for maximizing return, the trouble is put in a place most can handle, as a “business owner,” you are buying what you feel you can sell. That is the only reason to buy. If you don’t know if you can sell it higher tomorrow, but there is something that you believe you can, then perhaps it is time to evaluate dumping, even at a loss, to pick up something else.

Cash can often be that something else. Earning 4% annually on a short t-bill isn’t sexy, but having that liquid holding when opportunity presents itself, allows you to pounce. There is nothing worse than seeing something very clearly as a winning trade and not having the capital to load up on it.

PDS Biotech is a clinical-stage immunotherapy company developing a growing pipeline of molecularly targeted cancer and infectious disease immunotherapies based on the Company’s proprietary Versamune® and Infectimune™ T-cell activating technology platforms. Our Versamune®-based products have demonstrated the potential to overcome the limitations of current immunotherapy by inducing in vivo, large quantities of high-quality, highly potent polyfunctional tumor specific CD4+ helper and CD8+ killer T-cells. PDS Biotech has developed multiple therapies, based on combinations of Versamune® and disease-specific antigens, designed to train the immune system to better recognize diseased cells and effectively attack and destroy them. The Company’s pipeline products address various cancers including HPV16-associated cancers (anal, cervical, head and neck, penile, vaginal, vulvar) and breast, colon, lung, prostate and ovarian cancers.

Robert LeBoyer, Vice President, Research Analyst, Life Sciences , Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

New Data From The Phase 2 Triple Therapy Trial Shows Better Response And Survival Data. PDS Bio announced new data from its Phase 2 trial testing PDS0101 in combination with two immunomodulating drugs. Patients with HPV16-positive cancer received the “Triple Therapy” consisting of PDS0101, an IL-12 fusion protein, and a bivalent checkpoint inhibitor. One of two arms in the trial reached its median objective survival (OS) of 21 months, an improvement over the last interim update and the historical survival of 3 to 4 months.

New Overall Survival Data Shows Improvement Over Last Interim Update. Patients enrolled in the trial had HPV16-positive cancer with progressive disease after standard therapies. Patients who received previous checkpoint inhibitor therapy but no longer responded (checkpoint inhibitor refractory) reached a medial Overall Survival (OS) of 21 months. This compares to the last interim update of 16 months OS with 66% remaining alive. Expected survival for patients at this stage is 3 to 4 months. In the group that was naïve to checkpoint inhibitors, 75% remained alive at a median follow-up of 27 months, so the median OS has not been reached. Expected survival for similar patients is 7 to 11 months.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

Inflation, Unemployment, the Housing Crisis, and a Possible Recession: Two Economists Forecast What’s Ahead in 2023

With the current U.S. inflation rate at 7.1%, interest rates rising and housing costs up, many Americans are wondering if a recession is looming.

Two economists discussed that and more in a recent wide-ranging and exclusive interview for The Conversation. Brian Blank is a finance professor at Mississippi State University who specializes in the study of corporations and how they respond to economic downturns. Rodney Ramcharan is an economist at the University of Southern California who previously held posts with the Federal Reserve and the International Monetary Fund.

Both were interviewed by Bryan Keogh, deputy managing editor and senior editor of economy and business for The Conversation.

Are we headed for a recession in 2023?

Brian Blank: The consensus view among most forecasters is that there is a recession coming at some point, maybe in the middle of next year. I’m a little bit more optimistic than that consensus.

People have been calling for a recession for months now, and this seems to be the most anticipated recession on record. I think that it could still be a ways off. Consumer balance sheets are still relatively strong, stronger than we’ve seen them for most periods.

I think that the labor market is going to remain hotter than people have expected. Right now, over the last eight months, the labor market has added more jobs than anticipated, which is one of the strongest streaks on record. And I think that until consumer balance sheets weaken considerably, we can expect consumer spending, which is the largest part of the economy, to continue to grow quickly.

[But this] doesn’t mean that a recession is not coming. There’s always a recession somewhere down the road.

Rodney Ramcharan: Indeed, yes, there’s a likelihood that the economy is going to contract in the next nine months. The president of the New York Fed expects the unemployment rate to go up from 3.5% currently to somewhere between 4% to 5% in the next year. And I think that will be consistent with a recession.

In terms of how much worse it can be beyond that, it’s going to depend on a number of things. It could depend on whether the Fed is going to accept a higher inflation rate over the medium term or whether it’s really committed to getting the inflation rate down to the 2% rate. So I think that’s the trade-off.

Will unemployment go up?

Blank: [Unemployment] hasn’t risen much, and maybe it’ll pick up to somewhere close to 4%. Many are expecting something like four and a half percent. And I think that’s certainly possible. And I think that we can see small upticks in the coming months.

But I don’t think it’s going to rise as quickly as some people are expecting, in part because what we’ve seen so far is a lack of labor force participation. Until more people enter the labor market, I think there are going to be plenty of jobs to go around.

What is your outlook on interest rates?

Ramcharan: As people find it more and more difficult to find jobs, or to get jobs as they begin to lose jobs, I think that’s going to dampen spending. And we’re seeing that now as the cost of borrowing has gone up sharply, and the Fed is expecting that.

The expectation is the federal funds rate will go up to 5% by next year. If you tack on another couple of points, because of the risk involved, then the cost to borrow to buy a home could potentially get up to 8% for some people. And that could be very expensive.

And the flip side of this for businesses is there’s potentially going to be a slowdown in cash flow. If consumers are not spending, then the revenues that businesses depend on to make investments might not be there.

The additional piece in this puzzle is what the banks will then do. I think banks are going to begin to curtail the extension of credit. So not only will interest rates go up for the typical consumer and the typical business, it’s also likely that they are more likely to experience denial of credit, and so that should together begin to slow spending quite a bit.

After massive increases in housing prices, what caused them to suddenly drop?

Ramcharan: As the Fed lowered interest rates, there was a massive shift among the population for various reasons. They decided that housing was the right investment or the right thing. And so when 50 million people all collectively decide to buy homes, the supply of homes is reasonably constrained in the short run. And so that led to this massive increase in house prices and in rents.

In the last three months, the housing market has cooled sharply. We’re now seeing house prices beginning to fall. I would imagine, going forward, the housing market cooling is going to be a major driver behind the slowdown in the inflation rate and in real estate investment trusts. So that’s positive.

Our recent election just changed the composition of Congress. How will that affect the economy?

Blank: Certainly, when we have a divided Congress, we’re less likely to see decisions made that involve passing legislation that might support the economy. And I think it’s likely the Republican House is going to become a little bit more conservative with spending.

And so if we do start to see a downturn, I think you’re less likely to see legislation that might help support an economy that could be in need of it. That is going to make the job of the Federal Reserve more important.

How certain are these predictions?

Ramcharan: I just want to be careful here and let your viewers know that we’re making these statements based on theory, because the inflation that we’re experiencing now comes about from a pandemic, and there really is no evidence, there’s no data available, that people can look to to say, “What happens to an economy after a pandemic?” That data does not exist.

So we’re trying to piece together the data we do have with the theories we do have, but there’s a huge band of uncertainty about what’s going to happen.

Bitcoin’s Largest Corporate Owner Sold But Remains a net Buyer

“Bitcoin is the exit strategy,” says Michael Saylor, the Executive Chairman overseeing Microstrategy (MSTR), a company he founded. The comment was to a question in a Twitter Space interview with Eric Weiss of Bitcoin Roundtable. During this insightful interview, it becomes clear that the enterprise analytics company stands behind its commitment to the cryptocurrency and is investing in the ecosystem in other ways. Saylor also addressed his recent sale of 704 bitcoin, explaining it created tax benefits that serve stockholders.

The Company is a Bitcoin Maximalist

Bitcoin owners are “Either traders, technocrats, or maximalists.” Explained Saylor in the podcast-style interview.

Accordingly, Saylor says, traders don’t have any opinion on it long-term other than it’s an asset that moves enough to trade. Holding times may be minutes or months.

Technocrats view bitcoin as a digital monetary network like Google or Facebook. It’s a big tech network to them, so if they are bullish on big tech, they will hold bitcoin. And they may try to time their investments based on economic trends.

Maximalists view bitcoin as an instrument of economic empowerment that is just good for the human race. If you’re a maximalist, you don’t try to time it, and you have a much longer time horizon. While the technocrats are looking out 3-5 years, and they think that’s long, maximalists are looking out 10-100 years. Part of that is believing this is good for the human race.

“We’re maximalists, we think bitcoin is more than a digital monetary network; we think it is the digital monetary network. It’s good for the human race, and anything we can do in order to encourage adoption of bitcoin, and help with the adoption, is going to be good for the world.” Saylor while discussing Microstrategy.

Saylor’s company is the largest owner of bitcoin, costing Microstrategy a little more than $4 billion, the crypto assets are now valued just above $2 billion. Saylor says how we acquire bitcoin is less market-driven, as this is permanent capital that flows into the bitcoin ecosystem. Permanent capital that becomes part of the Microstrategy enterprise. Capital that is ongoing and may be held as a base forever.

In Response to December Selling

Michael Saylor recently took some criticism for selling 704 bitcoin after previously repeating he won’t sell bitcoin. He put the confusion to rest by explaining the benefit to stockholders of tax loss harvesting. With crypto the selling is treated as property so you can take the capital loss, “so we have some capital gains we pay taxes on, and then we have some capital, losses in bitcoin, so by selling the bitcoin, and taking the capital loss, we’re able to use that to offset some capital gains.” He added, it’s very tax efficient for the corporation.” Which is good for shareholders.

Lightning Network

Lightning allows “lightning-fast” blockchain payments without worrying about block confirmation times. Payment speed measured in milliseconds to seconds.Security is enforced by blockchain smart-contracts without creating an on-blockchain transaction for individual payments.

Microstrategy has said they will be offering bitcoin Lightning solutions in the first quarter of 2023. This tech investment in the growth of Microstrategy is another way Saylor and company support the bitcoin ecosystem.“If bitcoin is the underlying base layer, I think that Lightning is money over IP.” He said it’s an open permissionless protocol to let eight million people move money and monetary assets at the speed of light.

“We want to make it possible for any enterprise to spin up Lighting infrastructure in an afternoon” and onboard thousands of employees or customers, Saylor explained. “We want to plug it into enterprise technology and make it a marketing strategy for any forward-thinking CMO.”

Areas that MicroStrategy is exploring for Lightning services include online content monetization, enterprise marketing, web paywalls, and internal corporate controls. Every chief marketing officer should be able give away satoshis –– Bitcoin’s smaller denomination unit –– as incentive for customers

Take Away

Bitcoin still has its perma-bulls. Michael Saylor of Microstrategy is solidly in that category. He is not necessarily bullish on other crypto or digital currencies, bitcoin is the digital currency in his mind, and he intends for the ongoing holding of bitcoin and growth of the company in other ways that support its adoption.

Median OS of 21 months in 29 checkpoint inhibitor (CPI) refractory HPV16-positive cancer patients in National Cancer Institute-led Phase 2 clinical trial of PDS0101 triple combination

FLORHAM PARK, N.J., Dec. 28, 2022 (GLOBE NEWSWIRE) — PDS Biotechnology Corporation (Nasdaq: PDSB), a clinical-stage immunotherapy company developing a growing pipeline of targeted immunotherapies for cancer and infectious disease, today announced expanded interim data in a Phase 2 clinical trial investigating the PDS0101-based triple combination therapy in advanced human papillomavirus (HPV)-positive cancers. The triple combination of PDS0101 with the tumor-targeting IL-12 fusion protein M9241 (formerly known as NHS-IL12), and bintrafusp alfa, a bifunctional fusion protein targeting two independent immunosuppressive pathways (PD-L1 and TGF-β), is being studied in CPI-naïve and CPI-refractory patients with advanced HPV-positive anal, cervical, head and neck, vaginal, and vulvar cancers.

The triple combination Phase 2 trial (NCT04287868) is being conducted at the Center for Cancer Research (CCR) at the National Cancer Institute (NCI), one of the Institutes of the National Institutes of Health.

All patients in the study had failed prior treatment with chemotherapy and 90% had failed radiation treatment. The interim efficacy data (n=50) involves 37 HPV16-positive evaluable patients, including 29 patients who have, in addition, failed treatment with CPIs (CPI refractory). Highlights of the expanded interim data are as follows and are consistent with the results presented at American Society of Clinical Oncology (ASCO) Annual Meeting 2022 and prior interim data announced in October:

Median OS is 21 months in 29 checkpoint inhibitor refractory patients who received the triple combination. The reported historical median OS in patients with CPI refractory disease is 3-4 months.

In CPI naïve subjects, 75% remain alive at a median follow-up of 27 months. As a result, median OS has not yet been reached. Historically median OS for similar patients with platinum experienced CPI naïve disease is 7-11 months.

Objective response rate (ORR) in CPI refractory patients who received the optimal dose of the triple combination is 63% (5/8). In current approaches ORR is reported to be less than 10%.

ORR in CPI naïve patients with the triple combination is 88%. In current approaches ORR is reported to be less than 25% with FDA-approved CPIs in HPV-associated cancers.

Safety data have not changed since October’s update. 48% (24/50) of patients experienced Grade 3 (moderate) treatment-related adverse events (AEs), and 4% (2/50) of patients experienced Grade 4 (severe) AEs, compared with approximately 70% of patients receiving the combination of CPIs and chemotherapy reporting Grade 3 and higher treatment-related AEs.

“The expanded data continue to demonstrate the durability and tolerability of the PDS0101-based triple combination therapy in advanced HPV-positive cancers, an extremely challenging population of refractory and previously untreatable HPV-positive patients,” stated Dr. Frank Bedu-Addo, President and Chief Executive Officer of PDS Biotech. “We are pleased to see the continued consistency in the data with each update and we look forward to meeting with the FDA to discuss the registrational pathway.”

Both M9241 and bintrafusp alfa are owned by Merck KGaA, Darmstadt, Germany, and its affiliates.

About PDS Biotechnology

PDS Biotech is a clinical-stage immunotherapy company developing a growing pipeline of targeted cancer and infectious disease immunotherapies based on our proprietary Versamune® and Infectimune™ T cell-activating technology platforms. We believe our targeted Versamune® based candidates have the potential to overcome the limitations of current immunotherapy by inducing large quantities of high-quality, potent polyfunctional tumor specific CD4+ helper and CD8+ killer T cells. To date, our lead Versamune® clinical candidate, PDS0101, has demonstrated the potential to reduce tumors and stabilize disease in combination with approved and investigational therapeutics in patients with a broad range of HPV-positive cancers in multiple Phase 2 clinical trials. Our Infectimune™ based vaccines have also demonstrated the potential to induce not only robust and durable neutralizing antibody responses, but also powerful T cell responses, including long-lasting memory T cell responses in pre-clinical studies to date. To learn more, please visit www.pdsbiotech.com or follow us on Twitter at @PDSBiotech.

About PDS0101

PDS Biotech’s lead candidate, PDS0101, combines the utility of the Versamune® platform with targeted antigens in HPV-positive cancers. In partnership with Merck & Co., PDS Biotech is evaluating a combination of PDS0101 and KEYTRUDA® in a Phase 2 study in first-line treatment of recurrent or metastatic head and neck cancer, and also in second line treatment of recurrent or metastatic head and neck cancer in patients who have failed prior checkpoint inhibitor therapy. A Phase 2 clinical study is also being conducted in both second- and third-line treatment of multiple advanced HPV-positive cancers in partnership with the National Cancer Institute (NCI). A third phase 2 clinical trial in first line treatment of locally advanced cervical cancer is being performed with The University of Texas, MD Anderson Cancer Center.

KEYTRUDA® is a registered trademark of Merck Sharp and Dohme LLC, a subsidiary of Merck & Co., Inc., Rahway, NJ, USA.

Forward Looking Statements

This communication contains forward-looking statements (including within the meaning of Section 21E of the United States Securities Exchange Act of 1934, as amended, and Section 27A of the United States Securities Act of 1933, as amended) concerning PDS Biotechnology Corporation (the “Company”) and other matters. These statements may discuss goals, intentions and expectations as to future plans, trends, events, results of operations or financial condition, or otherwise, based on current beliefs of the Company’s management, as well as assumptions made by, and information currently available to, management. Forward-looking statements generally include statements that are predictive in nature and depend upon or refer to future events or conditions, and include words such as “may,” “will,” “should,” “would,” “expect,” “anticipate,” “plan,” “likely,” “believe,” “estimate,” “project,” “intend,” “forecast,” “guidance”, “outlook” and other similar expressions among others. Forward-looking statements are based on current beliefs and assumptions that are subject to risks and uncertainties and are not guarantees of future performance. Actual results could differ materially from those contained in any forward-looking statement as a result of various factors, including, without limitation: the Company’s ability to protect its intellectual property rights; the Company’s anticipated capital requirements, including the Company’s anticipated cash runway and the Company’s current expectations regarding its plans for future equity financings; the Company’s dependence on additional financing to fund its operations and complete the development and commercialization of its product candidates, and the risks that raising such additional capital may restrict the Company’s operations or require the Company to relinquish rights to the Company’s technologies or product candidates; the Company’s limited operating history in the Company’s current line of business, which makes it difficult to evaluate the Company’s prospects, the Company’s business plan or the likelihood of the Company’s successful implementation of such business plan; the timing for the Company or its partners to initiate the planned clinical trials for PDS0101, PDS0203 and other Versamune® and Infectimune™ based product candidates; the future success of such trials; the successful implementation of the Company’s research and development programs and collaborations, including any collaboration studies concerning PDS0101, PDS0203 and other Versamune® and Infectimune™ based product candidates and the Company’s interpretation of the results and findings of such programs and collaborations and whether such results are sufficient to support the future success of the Company’s product candidates; the success, timing and cost of the Company’s ongoing clinical trials and anticipated clinical trials for the Company’s current product candidates, including statements regarding the timing of initiation, pace of enrollment and completion of the trials (including the Company’s ability to fully fund its disclosed clinical trials, which assumes no material changes to our currently projected expenses), futility analyses, presentations at conferences and data reported in an abstract, and receipt of interim or preliminary results (including, without limitation, any preclinical results or data), which are not necessarily indicative of the final results of the Company’s ongoing clinical trials; any Company statements about its understanding of product candidates mechanisms of action and interpretation of preclinical and early clinical results from its clinical development programs and any collaboration studies; and other factors, including legislative, regulatory, political and economic developments not within the Company’s control, including unforeseen circumstances or other disruptions to normal business operations arising from or related to COVID-19. The foregoing review of important factors that could cause actual events to differ from expectations should not be construed as exhaustive and should be read in conjunction with statements that are included herein and elsewhere, including the risk factors included in the Company’s annual and periodic reports filed with the SEC. The forward-looking statements are made only as of the date of this press release and, except as required by applicable law, the Company undertakes no obligation to revise or update any forward-looking statement, or to make any other forward-looking statements, whether as a result of new information, future events or otherwise.

Versamune® is a registered trademark and Infectimune™ is a trademark of PDS Biotechnology.

Mark Reichman, Senior Research Analyst, Natural Resources, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

A top pick for 2023. During our recent Wall Street Wish List virtual conference, we highlighted our top picks for 2023. Maple Gold Mines Ltd. earned its place based on several competitive advantages, including a large 400 square kilometer land package in a prime location within the highly ranked mining jurisdiction of Quebec, a growing gold resource with significant expansion potential, an experienced management team and industry-leading joint venture partner, and a strong balance sheet.

World class potential. We believe Maple Gold represents an emerging world class gold project in Quebec’s renowned Abitibi Gold Belt. The company is well capitalized and is focused on establishing a new gold district through resource expansion and new discoveries. Both the Douay and Joutel projects have multiple styles of mineralization, including deep controlling structures, which are favorable for exploration and discovery of mineralized systems. Mines in the Abitibi are known for vertical continuity with higher grades at depth. Consequently, there is significant potential to increase the average resource grade with higher grade discoveries at depth.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

Great Lakes Dredge & Dock Corporation is the largest provider of dredging services in the United States. In addition, Great Lakes is fully engaged in expanding its core business into the rapidly developing offshore wind energy industry. The Company has a long history of performing significant international projects. The Company employs experienced civil, ocean and mechanical engineering staff in its estimating, production and project management functions. In its over 131-year history, the Company has never failed to complete a marine project. Great Lakes owns and operates the largest and most diverse fleet in the U.S. dredging industry, comprised of approximately 200 specialized vessels. Great Lakes has a disciplined training program for engineers that ensures experienced-based performance as they advance through Company operations. The Company’s Incident-and Injury-Free® (IIF®) safety management program is integrated into all aspects of the Company’s culture. The Company’s commitment to the IIF® culture promotes a work environment where employee safety is paramount.

Joe Gomes, Senior Research Analyst, Noble Capital Markets, Inc.

Joshua Zoepfel, Research Associate, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

Lowered Expectations. Last week, Great Lakes provided an update for 4Q22, with revenue and gross margins expected to be below previous forecasts. Recall, management had previously expected revenue of $175-$185 million and gross profit margin (gpm) in the “high single digits” for 4Q22. We had estimated revenue of $175 million and a gpm of 6.9%.

Impacts. The quarter is being impacted by a number of items, including the early retirement of the Terrapin Island, unexpected drydocking scope increases for the Ellis Island and Padre Island, weather delays on several projects in the northeast, and some project production issues.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

ARLP is a diversified natural resource company that generates operating and royalty income from coal produced by its mining complexes and royalty income from mineral interests it owns in strategic oil & gas producing regions in the United States, primarily the Permian, Anadarko and Williston basins. ARLP currently produces coal from seven mining complexes its subsidiaries operate in Illinois, Indiana, Kentucky, Maryland and West Virginia. ARLP also operates a coal loading terminal on the Ohio River at Mount Vernon, Indiana. ARLP markets its coal production to major domestic and international utilities and industrial users and is currently the second largest coal producer in the eastern United States. In addition, ARLP is positioning itself as an energy provider for the future by leveraging its core technology and operating competencies to make strategic investments in the fast growing energy and infrastructure transition.

Mark Reichman, Senior Research Analyst, Natural Resources, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

A top pick for 2023. During our recent Wall Street Wish List virtual conference, we highlighted our top picks for 2023. Alliance Resource Partners earned its place based on a superb management team, favorable fundamental outlook, and positive cash flow growth outlook. While fossil fuels are out of favor in some quarters, they power our economy. In our view, the geopolitical weaponizing of global energy supplies, along with the recent cold snap across the U.S. underscore the importance of reliable and affordable domestic supplies of coal, oil, and natural gas. Demand for fossils fuels will likely increase, with renewable energy increasing its share of the market share over time.

Earnings visibility is very strong. During the third quarter, Alliance executed new coal sales commitments for delivery of 5.6 million tons through 2025 at prices supporting higher margins. Based on contracted coal sales volumes in 2023 and 2024, the outlook for cash flow growth appears favorable. Alliance recently added a fifth continuous mining unit at its Gibson South mine and is adding another unit at the Hamilton mine. Within the oil and gas royalty segment, volumes are expected to benefit from two recent acquisitions that added 1,200 producing wells, 101 wells to be completed and 98 permitted locations on the acquired acreage.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

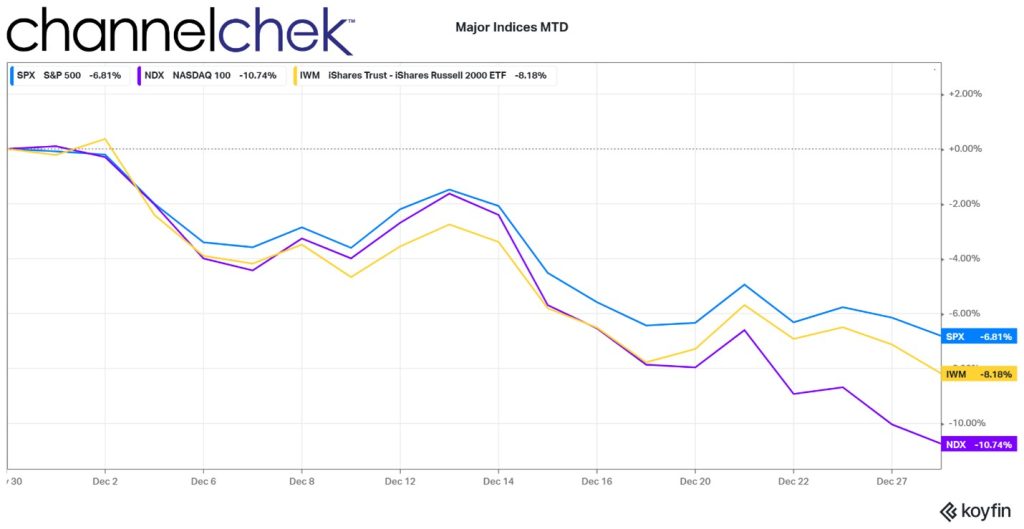

Offsetting portfolio capital gains by taking losses is permitted by the IRS. Within the tax guidelines, this generally occurs during the last month of the year as individuals and financial advisors strive to minimize money owed to the IRS. The stocks sold, naturally, are underperformers. This activity has a tendency to set the stage for a late December rally or a January rebound. This is especially true of the sectors or asset classes that were most sold. This is because portfolio managers often wish to keep a similar allocation, which translates to them then waiting 30 days or more before buying something that may be viewed as substantially similar.

With the major indexes like the S&P 500, Nasdaq 100, and Small Cap S&P 600 all down double digits this year, there are stocks that are doing far worse than index averages – just as there are stocks doing far better. Of course, if you own an ETF, you have to treat it like it is one stock and cannot offset a good underlying individual company sold with an underperforming company. In this way, holders of individual company shares can benefit more because they will have more options. And may even find it easier to qualify for the additional $3,000 tax benefit the IRS allows.

What happens after the 30-day period? Some investors try to get in, or back in, early with the notion that the most beaten-down stocks from 30 days earlier, could quickly bounce back hard for a time. This would all begin to occur following what could be perceived as the tax loss selling dip, (aged 30 days). The so-called Santa Rally is somewhat attributed to this, but that rally has not occurred during December 2022. The chart above shows a very weak December. So the buying may be postponed until early next year.

Without substantial buying this December, the first month or two of 2023 may bring buying as investors replace holdings for allocation purposes, plus any additional purchases used to bring the beaten-down sectors’ portfolio weightings up to whatever fits the investors’ strategy.

DoubleLine founder Jeffrey Gundlach told CNBC on Wednesday that risk assets will likely rally in January once retail investors finish tax-loss selling. Strategists at Evercore wrote on Nov. 30 that they were “buyers of stocks whose 2022 tax loss selling pressure will soon abate.”

Take Away

The main drivers of market moves next year are likely economic concerns such as inflation, recession, and monetary policy. But the potential for the most beaten down sectors this year, those that underperformed in December, may represent opportunity. The opportunity may not be long-lived, but for those involved in the markets, it is worth understanding why it may be occurring.

As the Bear Market Melts Down, Where Will the Grass Be Greenest?

Bear Markets and snowmen have one thing in common; they don’t last forever.

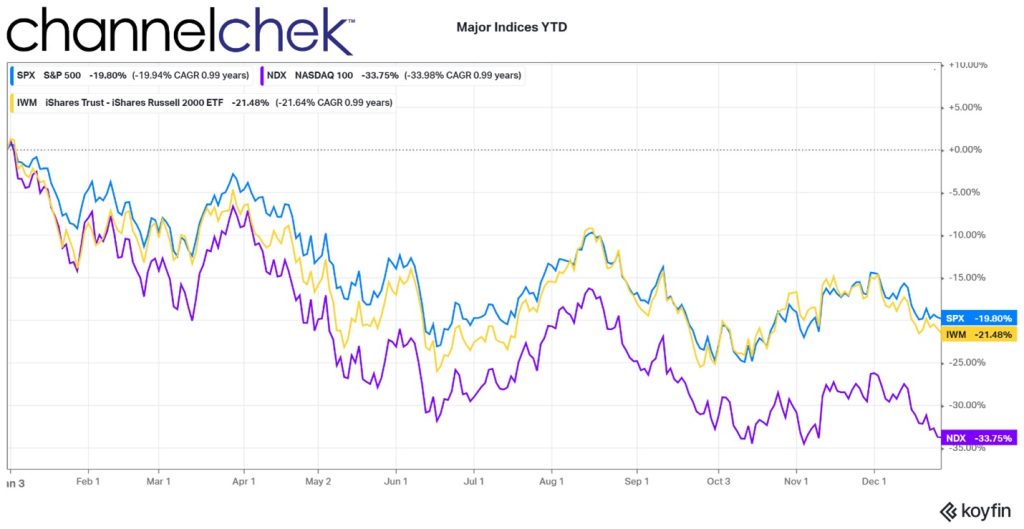

The entry point into an investment can have a huge impact on performance. Exits tend to be more critical when the stock has shown that it is not performing as planned. While this kind of exit may result in a loss, it allows the investor to preserve capital, liquid assets they can deploy if another good entry presents itself. The major stock market indices for 2022 are down 20% and more. Has this sell-off provided for performance-producing entry points in some stocks? Let’s look where we are as the countdown to 2023 has already begun.

About this Bear Market

Bear markets end – they always have. Pinpointing an exact bottom is not possible, so trying to be the first in for that great entry point may include a few false starts and some unhoped-for exits. The current slide in the stock market started around January 1, 2022. This was because some doubted whether inflation was transient at the time; by March, most understood the Fed was concerned that price increases were pervasive.

Fed Chair Powell, along with many Fed Presidents, began speaking hawkishly to not unduly surprise and unsettle markets as the central bank unwound the liquidity used in response to the novel coronavirus. What followed was unprecedented. Overnight lending rates went from an effective 0.08% to an effective 4.33% during the course of the year. This is more than 52 times the base lending rate at the start of the year. With these increases, no wonder the bear market continued.

Where Are We Now?

Expectations of overnight rate hikes in 2023 are for another 0.50%-0.75% increase leaving the target at, or just north of, 5%. This increase in the cost of money is small (.17 times) compared to the massive (52 times) rocking the markets in 2022.

So rate hikes are expected to be much lower as a percentage of current rates next year. And after the last FOMC meeting, markets have seemingly repriced lower with this expectation. If all goes as it is thought it will, the market is already priced for the worst. This is a bullish sign.

Put another way; most believe that with Fed funds beginning 2022 around zero, we’re likely much closer to the end of the Fed Funds tightening than to the beginning.

Inflation (CPI) for December won’t be reported until January 12, 2023. The latest CPI numbers show YoY up 7.1% in November, a slowing from 7.7% in October, which tapered from 8.2% the month before. The November reading of 7.1% taken by itself is a long way away from the Fed’s 2% target. But the trend in the CPI and PCE deflator also suggest the Fed is likely to monitor previous hikes to see if they will have the desired impact.

The Fed Has Been Transparent

The Fed lowered rates in line with what they promised during the pandemic. Then after some transient talk, they raised rates as they expressed they would in 2022. Following the December FOMC meeting, they suggested they were not at the end, but the voting members’ expectations for where they will settle is an average of 5.40%. The forward-looking stock market, if they believe the Fed will again do as promised, should recognize this is a much lower increase. It is perhaps near the time to begin to build on positions. This could be the entry point many investors have been waiting for.

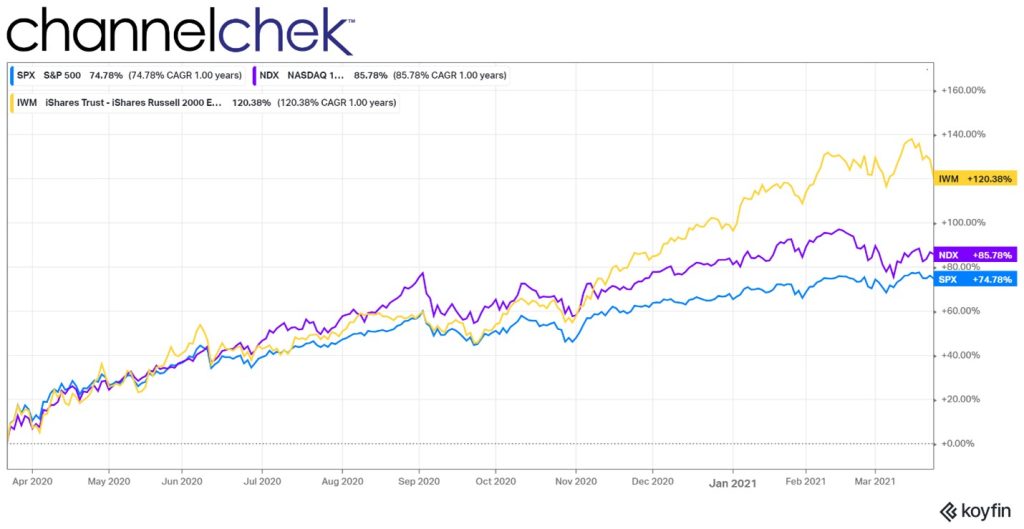

Small Cap Phenomenon

The chart below shows how much small cap stocks outperformed during the 12- months following the pandemic plunge. While small cap outperformance has been experienced during the past century of stocks’ post-sell-off periods, one only has to look back to the pandemic plunge to remember that it was small-caps (depicted below as IWM) that had been beaten down the most and by far outran the other major indices for the next year from the low of 2021.

Could this small cap phenomenon occur again after markets reach the bottom? Data demonstrates that small cap stocks tend to lead following a period of economic dislocation. One reason is US small caps have more of their business within the states and as a bonus, do well with a rising dollar. Current conditions suggest exploring smaller stocks. They have outperformed large caps following nearly every bear market of the last century. And today, the dollar has risen above its six-month high and is trending higher. While past movement comparisons don’t always include all the crosscurrents of the future, a strong argument could be made that a turnaround is near and small caps may again be the leaders by a wide margin.

Some Disclosure

Channelchek, the investment information platform you’re now reding has small cap stocks as its primary focus. The deep platform provides data on over 6000 stocks, with quality research updated regularly on many of them. Channelchek also provides videos and articles that may inspire informed stock selection. Stock selection, rather than just plowing investment dollars into an indexed ETF, may be preferable as indexed ETFs include sectors and stocks that may not be worthy of your portfolio.

Diversification across asset classes, sectors, and market capitalizations is considered prudent for long-term portfolios; individual allocations can be built on depending on where we are in the business and interest rate cycle. This includes an allocation to small cap equities, which perhaps should be expanded if the Fed is near the end of its tightening cycle. It could always be reduced later if the economy is deep into a growth cycle.

Take Away

Although we do not have a crystal ball to know exactly when the best entry point in any company stock is, if a century’s worth of data is any guide, the period following the end of a market downturn has been a good time to increase exposure to the small cap sector.

Register here for daily emails of research and ideas from Channelchek.

What if the U.S. placed a tax on robots? The concept has been publicly discussed by policy analysts, scholars, and Bill Gates (who favors the notion). Because robots can replace jobs, the idea goes, a stiff tax on them would give firms incentive to help retain workers, while also compensating for a dropoff in payroll taxes when robots are used. Thus far, South Korea has reduced incentives for firms to deploy robots; European Union policymakers, on the other hand, considered a robot tax but did not enact it.

Now a study by MIT economists scrutinizes the existing evidence and suggests the optimal policy in this situation would indeed include a tax on robots, but only a modest one. The same applies to taxes on foreign trade that would also reduce U.S. jobs, the research finds.

“Our finding suggests that taxes on either robots or imported goods should be pretty small,” says Arnaud Costinot, an MIT economist, and co-author of a published paper detailing the findings. “Although robots have an effect on income inequality … they still lead to optimal taxes that are modest.”

Specifically, the study finds that a tax on robots should range from 1 percent to 3.7 percent of their value, while trade taxes would be from 0.03 percent to 0.11 percent, given current U.S. income taxes.

“We came into this not knowing what would happen,” says Iván Werning, an MIT economist and the other co-author of the study. “We had all the potential ingredients for this to be a big tax, so that by stopping technology or trade, you would have less inequality, but … for now, we find a tax in the one-digit range, and for trade, even smaller taxes.”

The paper, “Robots, Trade, and Luddism: A Sufficient Statistic Approach to Optimal Technology Regulation,” appears in the advance online form in The Review of Economic Studies. Costinot is a professor of economics and associate head of the MIT Department of Economics; Werning is the department’s Robert M. Solow Professor of Economics.

A Sufficient Statistic: Wages

A key to the study is that the scholars did not start with an a priori idea about whether or not taxes on robots and trade were merited. Rather, they applied a “sufficient statistic” approach, examining empirical evidence on the subject.

For instance, one study by MIT economist Daron Acemoglu and Boston University economist Pascual Restrepo found that in the U.S. from 1990 to 2007, adding one robot per 1,000 workers reduced the employment-to-population ratio by about 0.2 percent; each robot added in manufacturing replaced about 3.3 workers, while the increase in workplace robots lowered wages about 0.4 percent.

In conducting their policy analysis, Costinot and Werning drew upon that empirical study and others. They built a model to evaluate a few different scenarios, and included levers like income taxes as other means of addressing income inequality.

“We do have these other tools, though they’re not perfect, for dealing with inequality,” Werning says. “We think it’s incorrect to discuss this taxes on robots and trade as if they are our only tools for redistribution.”

Still more specifically, the scholars used wage distribution data across all five income quintiles in the U.S. — the top 20 percent, the next 20 percent, and so on — to evaluate the need for robot and trade taxes. Where empirical data indicates technology and trade have changed that wage distribution, the magnitude of that change helped produce the robot and trade tax estimates Costinot and Werning suggest. This has the benefit of simplicity; the overall wage numbers help the economists avoid making a model with too many assumptions about, say, the exact role automation might play in a workplace.

“I think where we are methodologically breaking ground, we’re able to make that connection between wages and taxes without making super-particular assumptions about technology and about the way production works,” Werning says. “It’s all encoded in that distributional effect. We’re asking a lot from that empirical work. But we’re not making assumptions we cannot test about the rest of the economy.”

Costinot adds: “If you are at peace with some high-level assumptions about the way markets operate, we can tell you that the only objects of interest driving the optimal policy on robots or Chinese goods should be these responses of wages across quantiles of the income distribution, which, luckily for us, people have tried to estimate.”

Beyond Robots, an Approach for Climate and More

Apart from its bottom-line tax numbers, the study contains some additional conclusions about technology and income trends. Perhaps counterintuitively, the research concludes that after many more robots are added to the economy, the impact that each additional robot has on wages may actually decline. At a future point, robot taxes could then be reduced even further.

“You could have a situation where we deeply care about redistribution, we have more robots, we have more trade, but taxes are actually going down,” Costinot says. If the economy is relatively saturated with robots, he adds, “That marginal robot you are getting in the economy matters less and less for inequality.”

The study’s approach could also be applied to subjects besides automation and trade. There is increasing empirical work on, for instance, the impact of climate change on income inequality, as well as similar studies about how migration, education, and other things affect wages. Given the increasing empirical data in those fields, the kind of modeling Costinot and Werning perform in this paper could be applied to determine, say, the right level for carbon taxes, if the goal is to sustain a reasonable income distribution.

“There are a lot of other applications,” Werning says. “There is a similar logic to those issues, where this methodology would carry through.” That suggests several other future avenues of research related to the current paper.

In the meantime, for people who have envisioned a steep tax on robots, however, they are “qualitatively right, but quantitatively off,” Werning concludes.