Element79 Gold is a mineral exploration company focused on the acquisition, exploration and development of mining properties for gold and associated metals. Element79 Gold has acquired its flagship Maverick Springs Project located in the famous gold mining district of northeastern Nevada, USA, between the Elko and White Pine Counties, where it has recently completed a 43-101-compliant, pit-constrained mineral resource estimate reflecting an Inferred resource of 3.71 million ounces of gold equivalent* “AuEq” at a grade of 0.92 g/t AuEq (0.34 g/t Au and 43.4 g/t Ag)) with an effective date of Feb. 4, 2022. The acquisition of the Maverick Springs Project also included a portfolio of 15 properties along the Battle Mountain trend in Nevada, which the Company is analyzing for further merit of exploration, along with the potential for sale or spin-out. In British Columbia, Element79 Gold has executed a Letter of Intent to acquire a private company which holds the option to 100% interest of the Snowbird High-Grade Gold Project, which consists of 10 mineral claims located in Central British Columbia, approximately 20km west of Fort St. James. In Peru, Element79 Gold has signed a letter of intent to acquire the business and assets of Calipuy Resources Inc., which holds 100% interest in the past-producing Lucero Mine, one of the highest-grade underground mines to be commercially mined in Peru’s history, as well as the past-producing Machacala Mine. The Company also has an option to acquire 100% interest in the Dale Property which consists of 90 unpatented mining claims located approximately 100 km southwest of Timmins, Ontario, Canada in the Timmins Mining Division, Dale Township.

Mark Reichman, Senior Research Analyst, Natural Resources, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

Monetizing non-core properties. Element79 Gold executed non-binding letters of intent (LOI) with Centra Mining Ltd. and Valdo Minerals Ltd. to sell five properties from its Battle Mountain development portfolio which is comprised of fifteen properties in northeastern Nevada. The properties being considered for sale include: 1) The Long Peak Project, 2) The Stargo Project, 3) The Elder Creek Project, 4) The North Mill Creek Project, and 5) The Elephant Project.

LOI terms. Centra Mining is expected to purchase Element79 Gold’s interests and obligations associated with Long Peak and Stargo in exchange for C$1,000,000 payable with the issuance of 2.5 million shares of Centra at a deemed price of C$0.40 per share. Valdo is expected to purchase Element79 Gold’s interests and obligations associated with North Mill Creek, Elder Creek, and Elephant in exchange for C$1,125,000 payable with the issuance of 3,750,000 common shares at a deemed price of C$0.30 per share. Both LOI’s are non-binding and subject to a 180-day exclusivity period.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

If Cryptocurrency is not the Safe Haven it was Expected to Be, Will Assets Move Into Gold Investments?

In addition to any information discovered from Michael Burry’s 13F filing earlier this week, he’s been coming out in support of gold. He seems to expect that those that were seeking a “safe harbor investment” in various crypto-related investments are now having a change of mind. Despite his long positions held on September 30 and made public on November 14, he has teased that he could be extremely short the market; presumably, this could include any tradeable asset when you’re an investment analyst of this caliber.

Will Investors Rediscover Gold?

“Long thought that the time for gold would be when crypto scandals merge into contagion,” Burry wrote in a tweet this week.

@michaeljburry

The financial pressures spreading across the crypto industry that have helped destroy the crypto exchange FTX and exposed characters like Sam Bankman-Fried that may have been given too much trust, are causing reduced trust in digital assets.

Supporters and believers in the benefit of crypto had been using bitcoin and other tokens as a means of storage outside of securities. Their expectation has been that crypto is superior as a store of value during periods of inflation, currency depreciation, and economic turmoil.

Crypto prices have not offered much protection against plunging stock, bond, and real estate values. In fact, relative to the strong US dollar, crypto’s value has fallen off a cliff, offering no protection. The overall outstanding crypto worth has gone from $2.2 trillion to around $830 billion. Gold has not been rising during this period, but relative to US dollars, it is down only 3%.

Burry’s likely message is that the escalating cryptocurrency negatives will reduce demand for coins, yet demand for a safe haven asset would not be reduced. This could make gold again one of the only games in town for investors looking to protect against asset erosion.

Is Burry Short?

“You have no idea how short I am,” Burry said in a tweet this week.

@michaeljburry

He does not say he is short at all in this tweet. However, against the backdrop of many previous tweets warning against a market he believes will become more bearish, coupled with a holding report released that has five long holdings, the hedge fund manager of The Big Short fame is likely warning investors not to read too much positive into his fund’s holdings report. That report was released just before the tweet.

The value of long securities held in his roughly $292 million AUM was $41 million. As he demonstrated during the financial crisis, there are non-publicly reported ways to be short, even short beyond your AUM. Fund managers with assets over $100 million only have to disclose US-listed stocks in their 13F filings with the SEC each quarter. Excluded in the reporting are shares sold short, overseas-listed stocks, and other assets such as commodities.

In actuality, Burry’s increased positions in prison stocks and exposure to the company involved in making Artemis’ rocket boosters is more likely a sign that he likes the prospects of some companies while at the same time doesn’t like the broader market outlook.

Positive Tweets

In addition to his positive tweet on gold, Burry has suggested the Federal Reserve’s interest-rate hikes, which have weighed on market prices, could end in the spring. This was reflected in his October 24 tweet “Still think the Fed back off on QT early next year.”

Investing in Gold

Investors that look to gain exposure to gold, will typically buy gold bullion, gold funds, gold futures, and the stocks of gold mining companies. All have unique advantages. Investors looking to research junior miners of gold and other precious metals and natural resources, find Channelchek as an excellent resource to discover and research many different unique, actionable possibilities. Start here.

CHELMSFORD, MA / ACCESSWIRE / November 17, 2022 / Harte Hanks, Inc. (NASDAQ:HHS), a leading global customer experience company, today announced that Brian Linscott, Harte Hanks’ Chief Executive Officer, will be presenting at the Benchmark Company’s 11th Annual Discovery One-on-One Investor Conference to be held Thursday, December 1, 2022 at the New York Athletic Club in New York City.

Harte Hanks is scheduled to participate in one-on-one meetings with institutional analysts and investors throughout the day.

Harte Hanks (Nasdaq: HHS) is a leading global customer experience company whose mission is to partner with clients to provide them with CX strategy, data-driven analytics and actionable insights combined with seamless program execution to better understand, attract, and engage their customers.

Using its unparalleled resources and award-winning talent in the areas of Customer Care, Fulfillment and Logistics, and Marketing Services, Harte Hanks has a proven track record of driving results for some of the world’s premier brands including Bank of America, GlaxoSmithKline, Unilever, Pfizer, HBOMax, Volvo, Ford, FedEx, Midea, Sony and IBM, among others. Headquartered in Chelmsford, Massachusetts, Harte Hanks has over 2,500 employees in offices across the Americas, Europe, and Asia Pacific.

As used herein, “Harte Hanks” or “the Company” refers to Harte Hanks, Inc. and/or its applicable operating subsidiaries, as the context may require. Harte Hanks’ logo and name are trademarks of Harte Hanks.

Investor Relations Contact:

FNK IR Rob Fink or Tom Baumann (646) 809-4048 / (646) 349-6641 HHS@fnkir.com

HOUSTON, Nov. 17, 2022 (GLOBE NEWSWIRE) — Orion Group Holdings, Inc. (NYSE: ORN) (the “Company”), a leading specialty construction company, completed a 15 month rebuild of the recently commissioned Dredge Lavaca. Advancements to the dredge’s ladder, accommodations, and operating systems were made to continue to provide exceptional dredging service to its clients and industry partners in both the public and private sectors along the Gulf Coast. The Lavaca is scheduled to begin work mid-November 2022 on a newly awarded contract for the Port of Corpus Christi and will take part in the continued maintenance of waterways, deepening and widening projects for years to come throughout the Gulf Coast. The design of the dredge, including its modular quarters, walkways, access and egress points, ventilation, handrail & fendering systems have all been engineered specifically with an emphasis on safety. Design improvements to the crew accommodations reduced noise and vibrations during dredging operations and provide a reprieve for the crew during their rest periods. The open-concept lever room allows for the leverman to monitor and control all dredging systems from a specially designed control station with touchscreen displays and floor-to-ceiling windows that provide a 180-degree field of view. Tier III diesel-electric engines and electric winches is another step forward for the Company to continue our commitment to protecting the environment by preventing potential spills and reducing NOx emissions within our operating areas. Orion’s commitment to Safety and “Target Zero” is also instilled into our vetted contractors, and is reflected indirectly in this project, as the project surpassed 65,000 manhours without any lost time incidents or recordable injuries.

Orion Group Holdings, Inc., a leading specialty construction company serving the infrastructure, industrial and building sectors, provides services both on and off the water in the continental United States, Alaska, Canada and the Caribbean Basin through its marine segment and its concrete segment. The Company’s marine segment provides construction and dredging services relating to marine transportation facility construction, marine pipeline construction, marine environmental structures, dredging of waterways, channels and ports, environmental dredging, design, and specialty services. Its concrete segment provides turnkey concrete construction services including pour and finish, dirt work, layout, forming, and rebar across the light commercial, structural and other associated business areas. The Company is headquartered in Houston, Texas with regional offices throughout its operating areas.

Forward-Looking Statements

The matters discussed in this press release may constitute or include projections or other forward-looking statements within the meaning of the Private Securities Litigation Reform Act of 1995, the provisions of which the Company is availing itself. Certain forward-looking statements can be identified by the use of forward-looking terminology, such as ‘believes’, ‘expects’, ‘may’, ‘will’, ‘could’, ‘should’, ‘seeks’, ‘approximately’, ‘intends’, ‘plans’, ‘estimates’, or ‘anticipates’, or the negative thereof or other comparable terminology, or by discussions of strategy, plans, objectives, intentions, estimates, forecasts, outlook, assumptions, or goals. In particular, statements regarding future operations or results, including those set forth in this press release and any other statement, express or implied, concerning future operating results or the future generation of or ability to generate revenues, income, net income, profit, EBITDA, EBITDA margin, or cash flow, including to service debt, and including any estimates, forecasts or assumptions regarding future revenues or revenue growth, are forward-looking statements. Forward looking statements also include estimated project start date, anticipated revenues, and contract options which may or may not be awarded in the future. Forward looking statements involve risks, including those associated with the Company’s fixed price contracts that impacts profits, unforeseen productivity delays that may alter the final profitability of the contract, cancellation of the contract by the customer for unforeseen reasons, delays or decreases in funding by the customer, levels and predictability of government funding or other governmental budgetary constraints and any potential contract options which may or may not be awarded in the future, and are the sole discretion of award by the customer. Past performance is not necessarily an indicator of future results. In light of these and other uncertainties, the inclusion of forward-looking statements in this press release should not be regarded as a representation by the Company that the Company’s plans, estimates, forecasts, goals, intentions, or objectives will be achieved or realized. Readers are cautioned not to place undue reliance on these forward-looking statements, which speak only as of the date hereof. The Company assumes no obligation to update information contained in this press release whether as a result of new developments or otherwise.

Please refer to the Company’s Annual Report on Form 10-K, filed on March 7, 2022, which is available on its website at www.oriongroupholdingsinc.com or at the SEC’s website at www.sec.gov, for additional and more detailed discussion of risk factors that could cause actual results to differ materially from our current expectations, estimates or forecasts.

Vancouver, BC – TheNewswire – November 17, 2022 – Element79 Gold Corp. ( CSE:ELEM) (OTC:ELMGF) (FSE:7YS) (” Element79 Gold “, the ” Company “) today announced it has entered non-binding letters of intent (the ” Centra LOI ” and ” Valdo LOI ” respectively) with Centra Mining Ltd. (” Centra “) and Valdo Minerals Ltd. (” Valdo “), whereby the Company intends to sell a total of five properties from its Battle Mountain Portfolio, which is comprised of fifteen properties located in the famous gold mining district of northeastern Nevada, USA.

The properties being considered for sale include:

The Long Peak Project: 34 unpatented claims in Lander County

The Stargo Project: 337 unpatented claims in Nye County

The Elder Creek Project: 23 unpatented claims in Lander County

The North Mill Creek Project: 6 unpatented claims in Lander County

The Elephant Project: 197 unpatented claims in Lander County

“The potential sale of these claim blocks would allow Element79 Gold to continue unlocking additional value from our vast portfolio of prospective properties while maintaining our established focus on the rapid pace of development at our primary high-grade gold assets,” stated James Tworek, President and CEO of Element79 Gold. “Overall, we believe the Battle Mountain Portfolio contains several additional targets which warrant extensive exploration and prospecting to further validate historic high-grade samples. Selling some of the portfolio has been a corporate strategy point and this is a great opportunity that allows us both unlock value for our shareholders and to focus our energy on our core projects.”

The Long Peak Project

The Long Peak Project (” Long Peak “) is comprised of 34 unpatented claims located near Copper Basin and the Copper Canyon Mine in Lander County, Nevada. Long Peak hosts significant historic prospects, warranting further exploration at Long Peak.

The Stargo Project

The Stargo Project (” Stargo “) is comprised of 337 unpatented claims located south of the Battle Mountain Trend in Nye County, Nevada.The large claim block contains attractive host rocks, tertiary age intrusives, and appropriate aged structural preparation to represent an attractive area for exploration target development.

The North Mill Creek Project

The North Mill Creek Project (” North Mill Creek “) is comprised of 6 unpatented claims located at the margins of the Goat Window in Lander County, Nevada. The Goat Window is an exposure of lower plate rocks beneath the Roberts Mountains Thrust which are the preferred carbonate host of Carlin-type gold deposits. Previous drilling completed at North Mill Creek yielded encouraging results warranting follow-up exploration.

The Elder Creek Project

The Elder Creek Project (” Elder Creek “) is comprised of 23 unpatented claims which cover the historic Elder Creek open-pit mine in Lander County, Nevada. Elder Creek is hosted in upper plate rocks where the mine area is believed to represent leakage from the deeper lower plate of the Roberts Mountains Thrust, suggesting that deeper targets could host significant mineralization within faulted and anticline folded sedimentary beds.

The Elephant Project

The Elephant Project (” Elephant “) is comprised of 197 claims located at the foot of the mine dumps at Nevada Gold Mines’ Phoenix operation. Elephant hosts a covered pediment target with various depths of cover based on the displacement of fault blocks. Limited past drilling has confirmed the presence and mineralization of the Elephant target model.

Terms of The Centra LOI

Under the terms of the Centra LOI, it is anticipated that Centra would purchase all of Element79 Gold’s interests and obligations in relation to Long Peak, and Stargo in exchange for a total consideration of $1,000,000 CAD payable by the issuance of an aggregate of 2,500,000 common shares of Centra at a deemed price of $0.40 CAD per share. The Centra LOI is non-binding and is subject to a 180-day exclusivity period.

Terms of the Valdo LOI

Under the terms of the Valdo LOI, it is anticipated that Valdo would purchase all of Element79 Gold’s interests and obligations in relation to North Mill Creek, Elder Creek, and Elephant in exchange for a total consideration of $1,125,000 CAD payable by the issuance of an aggregate of 3,750,000 common shares of Centra at a deemed price of $0.30 CAD per share. The Valdo LOI is non-binding and is subject to a 180-day exclusivity period.

Qualified Person

The technical information in this release has been reviewed and verified by Neil Pettigrew, M.Sc., P. Geo., Director of Element79 Gold and a “qualified person” as defined by National Instrument 43-101.

About Element79 Gold

Element79 Gold is a mineral exploration company focused on the acquisition, exploration and development of mining properties for gold and associated metals. Element79 Gold has acquired its flagship Maverick Springs Project located in the famous gold mining district of northeastern Nevada, USA, between the Elko and White Pine Counties, where it has recently completed a 43-101-compliant, pit-constrained mineral resource estimate reflecting an Inferred resource of 3.71 million ounces of gold equivalent* “AuEq” at a grade of 0.92 g/t AuEq (0.34 g/t Au and 43.4 g/t Ag)) with an effective date of Oct. 7, 2021 (see news release January 31st, 2022, available on SEDAR). The acquisition of the Maverick Springs Project also included a portfolio of 15 properties along the Battle Mountain trend in Nevada, which the Company is analyzing for further merit of exploration, along with the potential for sale or spin-out. In British Columbia, Element79 Gold has executed a Letter of Intent to acquire a private company which holds the option to 100% interest of the Snowbird High-Grade Gold Project, which consists of 10 mineral claims located in Central British Columbia, approximately 20km west of Fort St. James. In Peru, Element79 Gold holds 100% interest in the past producing Lucero Mine, one of the highest-grade underground mines to be commercially mined in Peru’s history, as well as the past producing Machacala Mine. The Company also has an option to acquire 100% interest in the Dale Property which consists of 90 unpatented mining claims located approximately 100 km southwest of Timmins, Ontario, Canada in the Timmins Mining Division, Dale Township. For more information about the Company, please visit www.element79.gold or www.element79gold.com .

This press contains “forward‐looking information” and “forward-looking statements” under applicable securities laws (collectively, “forward‐looking statements”). These statements relate to future events or the Company’s future performance, business prospects or opportunities that are based on forecasts of future results, estimates of amounts not yet determinable and assumptions of management made in light of management’s experience and perception of historical trends, current conditions and expected future developments. Forward-looking statements include, but are not limited to, statements with respect to: the Company’s plans for its portfolio of mining projects and properties; the Company’s business strategy; future planning processes; exploration activities; the timing and result of exploration activities; capital projects and exploration activities and the possible results thereof; any potential future cash flow and the timing thereof; acquisition opportunities; the impact of acquisitions, if any, on the Company. Assumptions may prove to be incorrect and actual results may differ materially from those anticipated. Consequently, forward-looking statements cannot be guaranteed. As such, investors are cautioned not to place undue reliance upon forward-looking statements as there can be no assurance that the plans, assumptions or expectations upon which they are placed will occur. All statements other than statements of historical fact may be forward‐looking statements. Any statements that express or involve discussions with respect to predictions, expectations, beliefs, plans, projections, objectives or future events or performance (often, but not always, using words or phrases such as “seek”, “anticipate”, “plan”, “continue”, “estimate”, “expect”, “may”, “will”, “project”, “predict”, “forecast”, “potential”, “target”, “intend”, “could”, “might”, “should”, “believe” and similar expressions) are not statements of historical fact and may be “forward‐looking statements”.

Actual results may vary from forward-looking statements. Forward-looking statements are subject to known and unknown risks, uncertainties and other factors that may cause actual results to materially differ from those expressed or implied by such forward-looking statements, including but not limited to: the duration and effects of the coronavirus and COVID-19; risks related to the integration of acquisitions; actual results of exploration activities; conclusions of economic evaluations; changes in project parameters as plans continue to be refined; commodity prices; variations in ore reserves, grade or recovery rates; actual performance of plant, equipment or processes relative to specifications and expectations; accidents; labour relations; relations with local communities; changes in national or local governments; changes in applicable legislation or application thereof; delays in obtaining approvals or financing or in the completion of development or construction activities; exchange rate fluctuations; requirements for additional capital; government regulation; environmental risks; reclamation expenses; outcomes of pending litigation; limitations on insurance coverage as well as those factors discussed in the Company’s other public disclosure documents, available on www.sedar.com . Although the Company has attempted to identify important factors that could cause actual results to differ materially from those contained in forward-looking statements, there may be other factors that cause results not to be as anticipated, estimated or intended. The Company believes that the expectations reflected in these forward‐looking statements are reasonable, but no assurance can be given that these expectations will prove to be correct and such forward‐looking statements included herein should not be unduly relied upon. These statements speak only as of the date hereof. The Company does not intend, and does not assume any obligation, to update these forward-looking statements, except as required by applicable laws.

Source: Element79 Gold

Neither the Canadian Securities Exchange nor the Market Regulator (as that term is defined in the policies of the Canadian Securities Exchange) accepts responsibility for the adequacy or accuracy of this release.

Copyright (c) 2022 TheNewswire – All rights reserved.

BOTHELL, Wash., Nov. 17, 2022 (GLOBE NEWSWIRE) — Cocrystal Pharma, Inc. (Nasdaq: COCP) today announced that CC-42344 demonstrated a favorable safety profile in both the single-ascending dose and the multiple-ascending dose portions of the ongoing Phase 1 study. CC-42344 is a broad-spectrum oral antiviral for the treatment of pandemic and seasonal influenza A with a novel mechanism of action.

“We are encouraged by the clean safety profile observed with all dose levels in both the single-ascending and multiple-ascending dose portions of the Phase 1 study, and we will be assessing the pharmacokinetic data from this trial in the coming weeks,” said Sam Lee, Ph.D., Cocrystal’s President and co-interim CEO. “We remain on track to reach an important milestone of reporting topline Phase 1 study results later this year.

“Influenza is among the most serious global public health threats, particularly with the emergence of pandemic strains and resistance to available drugs,” he added. “Based on a novel mechanism of action and a high barrier to resistance, we believe CC-42344 holds potential to be a best-in-class oral treatment for pandemic and seasonal influenza.”

The randomized, double-controlled, dose-escalating Phase 1 study in Australia was designed to assess the safety, tolerability and pharmacokinetics (PK) of orally administered CC-42344 in healthy adults. In July 2022 Cocrystal reported that PK data from the single-ascending dose portion of the study support once-daily dosing. In October 2022 enrollment in the multiple-ascending dose portion of the trial was completed. The Company plans to present topline study results at the upcoming World Antiviral Congress on December 1, 2022 and to submit an application with the United Kingdom Medicines and Healthcare Products Regulatory Agency to conduct a Phase 2a human challenge study in early 2023. Subject to regulatory agency clearance, the Phase 2a study is expected to be initiated in the second half of 2023.

About CC-42344 CC-42344 is an oral PB2 inhibitor discovered using Cocrystal’s proprietary structure-based drug discovery platform technology. It is specifically designed to be effective against all significant pandemic and seasonal influenza A strains and to have a high barrier to resistance due to the way the virus’ replication machinery is targeted. CC-42344 targets the influenza polymerase, an essential replication enzyme with several highly conserved regions common to multiple influenza strains. In vitro testing showed CC-42344’s excellent antiviral activity against influenza A strains, including pandemic and seasonal strains, as well as against strains resistant to Tamiflu® and Xofluza®, while also demonstrating favorable PK and safety profiles.

About Cocrystal Pharma, Inc. Cocrystal Pharma, Inc. is a clinical-stage biotechnology company discovering and developing novel antiviral therapeutics that target the replication process of influenza viruses, coronaviruses (including SARS-CoV-2), hepatitis C viruses and noroviruses. Cocrystal employs unique structure-based technologies and Nobel Prize-winning expertise to create first- and best-in-class antiviral drugs. For further information about Cocrystal, please visit www.cocrystalpharma.com.

This press release contains forward-looking statements within the meaning of the Private Securities Litigation Reform Act of 1995, including statements regarding our being on track to report topline results of the Phase 1 study later in 2022, the potential of CC-42344 to be a best-in-class candidate for the treatment of seasonal and pandemic influenza, and our expectations and plans to submit an application to the United Kingdom Medicines and Healthcare Products Regulatory Agency to conduct a Phase 2a human challenge study in early 2023 and to initiate the Phase 2a study in the second half of 2023. The words “believe,” “may,” “estimate,” “continue,” “anticipate,” “intend,” “should,” “plan,” “could,” “target,” “potential,” “is likely,” “will,” “expect” and similar expressions, as they relate to us, are intended to identify forward-looking statements. We have based these forward-looking statements largely on our current expectations and projections about future events. Some or all of the events anticipated by these forward-looking statements may not occur. Important factors that could cause actual results to differ from those in the forward-looking statements include, but are not limited to, the risks and uncertainties arising from any future impact of COVID-19 (including long-term or pervasive effects of the virus), inflation, interest rate increases and the war in Ukraine on the U.K. and global economy and on our Company, including supply chain disruptions and our continued ability to proceed with our programs, including our influenza A program, the ability of the contract research organization to recruit patients into clinical trials, the results of future preclinical and clinical studies, and general risks arising from clinical trials. Further information on our risk factors is contained in our filings with the SEC, including our Annual Report on Form 10-K for the year ended December 31, 2021. Any forward-looking statement made by us herein speaks only as of the date on which it is made. Factors or events that could cause our actual results to differ may emerge from time to time, and it is not possible for us to predict all of them. We undertake no obligation to publicly update any forward-looking statement, whether as a result of new information, future developments or otherwise, except as may be required by law.

Mark Reichman, Senior Research Analyst, Natural Resources, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

Initiating with an Outperform rating. We are initiating coverage of LithiumBank Resources Corp. with an Outperform rating and a price target of US$2.75 or C$3.65 per share. LithiumBank is advancing its flagship Boardwalk lithium brine project and is developing several other projects, notably Park Place and Kindersley, in parallel. The company expects to complete a preliminary economic assessment (PEA) for the Boardwalk Project by year-end 2022 to be published in early 2023. Boardwalk could go into production as early as 2026. We have assumed the company is able to upgrade the resource to support 30,400 tonnes of lithium carbonate equivalent production per day over a 20-year life.

Significant indicated and inferred resources. In November 2022, LithiumBank released results from an updated NI 43-101 mineral resource estimate for the Boardwalk project. Resources include 393,000 tonnes of indicated lithium carbonate equivalent resources grading 71.6 milligrams per liter lithium and 5,808,000 tonnes of inferred lithium carbonate equivalent at a grade of 68.0 milligrams per liter lithium. We think management has a credible path to upgrade additional resources to measured and indicated, along with adding resources.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

Codere Online refers, collectively, to Codere Online Luxembourg, S.A. and its subsidiaries. Codere Online launched in 2014 as part of the renowned casino operator Codere Group. Codere Online offers online sports betting and online casino through its state-of-the art website and mobile application. Codere currently operates in its core markets of Spain, Italy, Mexico, Colombia, Panama and the City of Buenos Aires (Argentina). Codere Online’s online business is complemented by Codere Group’s physical presence throughout Latin America, forming the foundation of the leading omnichannel gaming and casino presence in the region.

Michael Kupinski, Director of Research, Noble Capital Markets, Inc.

Patrick McCann, Research Associate, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

Strong Q3 results. Net gaming revenue grew 54% in the quarter to €30.6 million, despite only a 4% increase in active users. Management attributed revenue growth to more spending from existing users. Notably, revenue in Mexico, Spain and Columbia increased 85%, 29% and 100%, respectively.

Revenue outlook on track. Management shifted full year guidance to the higher end of its previous range, now €115 million to €120 million from its previous range of €110 million to €120 million. The shift to the high end of previously issued guidance is progress on the path towards profitability, which management expects to reach in 2024.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

Bowlero Corp. is the worldwide leader in bowling entertainment, media, and events. With more than 300 bowling centers across North America, Bowlero Corp. serves more than 26 million guests each year through a family of brands that includes Bowlero, Bowlmor Lanes, and AMF. In 2019, Bowlero Corp. acquired the Professional Bowlers Association, the major league of bowling, which boasts thousands of members and millions of fans across the globe. For more information on Bowlero Corp., please visit BowleroCorp.com.

Michael Kupinski, Director of Research, Noble Capital Markets, Inc.

Patrick McCann, Research Associate, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

A good start to the fiscal year. Fiscal first quarter revenues exceeded our expectation at $230.3 million versus our estimate of $222.5 million. Notably, the quarter illustrated the return of COVID-impacted business lines. League and Tournament revenue was up 46% and Group Event revenue was up 86%.

Hitting its stride. The company demonstrated favorable revenue trends across all of its business lines with strong growth of Bowling & Shoe (+24.5%), Food & Beverage (+31.2%), and Amusement (+29.9%).

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

The health of the US Treasury market impacts almost all other markets. This is because the “risk-free” market (US Treasuries) and its relationship to the US dollar is the foundation from which other markets stand. If it is in trouble, all markets suffer. The “health” measure most associated with securities like treasuries is liquidity or whether money can be raised when needed. Other measures include market spread between the bid and the ask, trading activity levels, and price impact or how a large transaction impacts the price.

A just released report by New York Fed economists Michael Fleming and Claire Nelson discuss the current state of the U.S. Treasury markets from the unique point of view and access to information of the New York Fed.

The report follows:

How Liquid Has the Treasury Market Been in 2022?

Policymakers and market participants are closely watching liquidity conditions in the U.S. Treasury securities market. Such conditions matter because liquidity is crucial to the many important uses of Treasury securities in financial markets. But just how liquid has the market been and how unusual is the liquidity given the higher-than-usual volatility? In this post, we assess the recent evolution of Treasury market liquidity and its relationship with price volatility and find that while the market has been less liquid in 2022, it has not been unusually illiquid after accounting for the high level of volatility.

Why Liquidity Matters

The U.S. Treasury securities market is the largest and most liquid government securities market in the world. Treasury securities are used to finance the U.S. government, to manage interest rate risk, as a risk-free benchmark for pricing other financial instruments, and by the Federal Reserve in implementing monetary policy. Having a liquid market is important for all these purposes and thus of great interest to market participants and policymakers alike.

Measuring Liquidity

Liquidity typically refers to the cost of quickly converting an asset into cash (or vice versa) and is measured in a variety of ways. We consider three commonly used measures, calculated using high-frequency data from the interdealer market: bid-ask spreads, order book depth, and price impact. The measures are for the most recently auctioned

(on-the-run) two-, five-, and ten-year notes (the three most actively traded Treasury securities, as shown in this post) and are calculated for New York trading hours (defined as 7 a.m. to 5 p.m.). Our data source is BrokerTec, which is estimated to account for 80 percent of trading in the electronic interdealer broker market.

The Market Has Been Relatively Illiquid in 2022

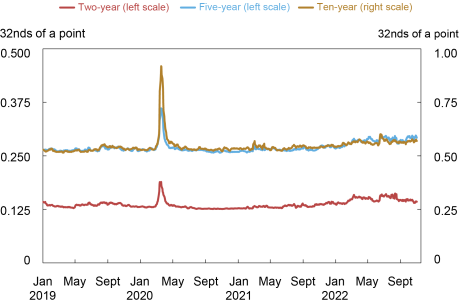

The bid-ask spread—the difference between the lowest ask price and the highest bid price for a security—is one of the most popular liquidity measures. As shown in the chart below, bid-ask spreads have widened out in 2022, but have remained well below the levels observed during the COVID-related disruptions of March 2020 (examined in this post). The widening has been somewhat greater for the two-year note relative to its average and relative to its level in March 2020.

Bid-Ask Spreads Have Widened Modestly

Liberty Street Economics chart plots the five-day moving averages of average daily bid-ask spreads for the two-, five-, and ten-year notes in the interdealer market from January 2, 2019, to October 31, 2022.

Source: Authors’ calculations, based on data from BrokerTec.

Notes: The chart plots five-day moving averages of average daily bid-ask spreads for the on-the-run two-, five-, and ten-year notes in the interdealer market from January 2, 2019, to October 31, 2022. Spreads are measured in 32nds of a point, where a point equals one percent of par.

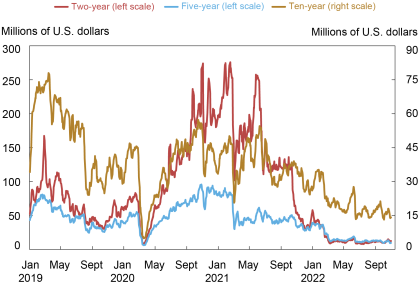

The next chart plots order book depth, measured as the average quantity of securities available for sale or purchase at the best bid and offer prices. Depth levels again point to relatively poor liquidity in 2022, but with the differences across securities more striking. Depth in the two-year note has been at levels commensurate with those of March 2020, whereas depth in the five-year note has remained somewhat higher—and depth in the ten-year note appreciably higher—than the levels of March 2020.

Order Book Depth Lowest since March 2020

Liberty Street Economics chart plots five-day moving averages of average daily depth for the two-, five-, and ten-year notes in the interdealer market from January 2, 2019, to October 31, 2022.

Source: Authors’ calculations, based on data from BrokerTec.

Notes: The chart plots five-day moving averages of average daily depth for the on-the-run two-, five-, and ten-year notes in the interdealer market from January 2, 2019, to October 31, 2022. Data are for order book depth at the inside tier, averaged across the bid and offer sides. Depth is measured in millions of U.S. dollars par.

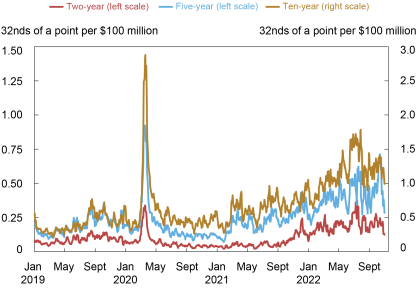

Measures of the price impact of trades also suggest a notable deterioration of liquidity. The next chart plots the estimated price impact per $100 million in net order flow (that is, buyer-initiated trading volume less seller-initiated trading volume). A higher price impact suggests reduced liquidity. Price impact has been high this year, and again more notably so for the two-year note relative to the March 2020 episode. That said, price impact looks to have peaked in late June and July, and to have declined most recently (in October).

Price Impact Highest since March 2020

Liberty Street Economics chart plots the estimated price impact per $100 million in net order flow for the two-, five-, and ten-year notes in the interdealer market from January 2, 2019, to October 31, 2022.Source: Authors’ calculations, based on data from BrokerTec.

Notes: The chart plots five-day moving averages of slope coefficients from daily regressions of one-minute price changes on one-minute net order flow (buyer-initiated trading volume less seller-initiated trading volume) for the on-the-run two-, five-, and ten-year notes in the interdealer market from January 2, 2019, to October 31, 2022. Price impact is measured in 32nds of a point per $100 million, where a point equals one percent of par.

Note that we start our analysis of liquidity in this post in 2019 and not earlier. One reason is to highlight the developments in 2022. Another reason is that the minimum price increment for the two-year note was halved in late 2018, creating a break in the note’s bid-ask spread and depth series. Longer time series of bid-ask spreads, order book depth, and price impact are plotted in this post and this paper. The longer history indicates that the price impact in the two-year note is currently at levels comparable to those seen during the 2007-09 global financial crisis, as well as in March 2020.

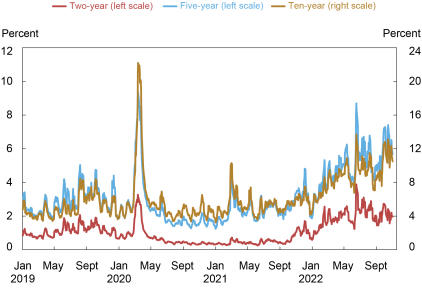

Volatility Has Also Been High

Pandemic-induced supply disruptions, high inflation, policy uncertainty, and geopolitical conflict have led to a sizable increase in uncertainty about the expected path of interest rates, resulting in high price volatility in 2022, as shown in the next chart. As with liquidity, volatility has been especially high lately for the two-year note relative to its history, likely reflecting the importance of near-term monetary policy uncertainty in explaining the current episode. Volatility has caused market makers to widen their bid-ask spreads and post less depth at any given price (to manage the increased risk of taking on positions), and for the price impact of trades to increase, illustrating the well-known negative relationship between volatility and liquidity.

Price Volatility Highest Since March 2020

Liberty Street Economics chart plots five-day moving averages of price volatility for the two-, five-, and ten-year notes in the interdealer market from January 2, 2019, to October 31, 2022.

Source: Authors’ calculations, based on data from BrokerTec.

Notes: The chart plots five-day moving averages of price volatility for the on-the-run two-, five-, and ten-year notes in the interdealer market from January 2, 2019, to October 31, 2022. Price volatility is calculated for each day by summing squared one-minute returns (log changes in midpoint prices) from 7 a.m. to 5 p.m., annualizing by multiplying by 252, and then taking the square root. It is reported in percent.

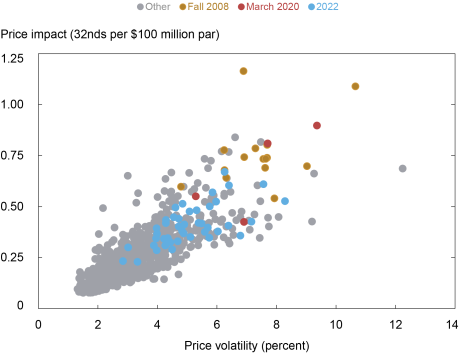

Liquidity Has Tracked Volatility

To assess whether liquidity has been unusual given the level of volatility, we provide a scatter plot of price impact against volatility for the five-year note in the chart below. The chart shows that the 2022 observations (in blue) fall in line with the historical relationship. That is, the current level of liquidity is consistent with the current level of volatility, as implied by the historical relationship between these two variables. This is true for the ten-year note as well, whereas for the two-year note the evidence points to somewhat higher-than-expected price impact given the volatility in 2022 (as also occurred in fall 2008 and March 2020).

Liquidity and Volatility in Line with Historical Relationship

Liberty Street Economics chart plots price impact against price volatility by week for the five-year note from January 2, 2005, to October 28, 2022.

Source: Authors’ calculations, based on data from BrokerTec.

Notes: The chart plots price impact against price volatility by week for the on-the-run five-year note from January 2, 2005, to October 28, 2022. The weekly measures for both series are averages of the daily measures plotted in the preceding two charts. Fall 2008 points are for September 21, 2008 – January 3, 2009, March 2020 points are for March 1, 2020 – March 28, 2020, and 2022 points are for January 2, 2022 – October 29, 2022.

The preceding analysis is based on realized price volatility—that is, on how much prices are actually changing. We repeated the analysis with implied (or expected) price volatility, as measured by the ICE BofAML MOVE Index, and found similar results for 2022. That is, liquidity for the five- and ten-year notes is in line with the historical relationship between liquidity and expected volatility, whereas liquidity is somewhat worse for the two-year note.

Note also that while liquidity may not be especially high relative to volatility, one might then ask whether volatility itself is unusually high. Answering this question is beyond our scope here, although we will note that there are good reasons for volatility to be high, as discussed above.

Trading Volume Has Been High

Despite the high volatility and illiquidity, trading volume has held up this year. High trading volume amid high illiquidity is common in the Treasury market, and was also observed during the market disruptions around the near-failure of Long-Term Capital Management (see this paper), during the 2007-09 financial crisis (see this paper), during the October 15, 2014, flash rally (see this post), and during the COVID-19-related disruptions of March 2020 (see this post). Periods of high uncertainty are associated with high volatility and illiquidity but also high trading demand.

Nothing to Be Concerned About?

Not exactly. While Treasury market liquidity has been in line with volatility, there are still reasons to be cautious. The market’s capacity to smoothly handle large flows has been of ongoing concern since March 2020, as discussed in this paper, as Treasury debt outstanding continues to grow. Moreover, lower-than-usual liquidity implies that a liquidity shock will have larger-than-usual effects on prices and perhaps be more likely to precipitate a negative feedback loop between security sales, volatility, and illiquidity. Close monitoring of Treasury market liquidity—and continued efforts to improve the market’s resilience—remain important.

Joe Gomes, Senior Research Analyst, Noble Capital Markets, Inc.

Joshua Zoepfel, Research Associate, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

3Q22 Results. Lifeway reported record top line for the third quarter with sales up 29.1% y-o-y to $38.1 million. Price and volume in the core kefir product drove the top line results. Kefir unit volumes increased double digits in the quarter. Net income for the quarter totaled $983,000, or $0.06 per share, compared to $480,000, or $0.03 per share last year. We had forecast revenue of $33.5 million and net income of $215,000, or EPS of $0.01.

New Distribution. Management continues to pick up new accounts. Most recently convincing Food Lion to switch to Lifeway branded kefir from an unbranded product, and adding the 975 store Wawa convenience chain in the mid-Atlantic states and the 106 location Plaid Pantry convenience chain serving the Pacific Northwest. These new accounts should help Lifeway to continue to post top line growth.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

Endeavour Silver is a mid-tier precious metals mining company that operates two high-grade, underground, silver-gold mines in Mexico. Endeavour is currently advancing the Terronera mine project towards a development decision, pending financing and final permits and exploring its portfolio of exploration and development projects in Mexico, Chile and the United States to facilitate its goal to become a premier senior silver producer. Our philosophy of corporate social integrity creates value for all stakeholders.

Mark Reichman, Senior Research Analyst, Natural Resources, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

Third quarter 2022 results. Endeavour generated a third quarter adjusted net loss of $3.1 million or ($0.02) per share compared to a net loss of $4.5 million or $(0.03) per share during the prior year period. We had projected net income of $2.0 million or $0.01 per share. Financial results were negatively impacted by the company’s decision to withhold sales for inventory, along with higher direct production costs. At quarter end, Endeavour held 1,527,549 ounces of silver and 3,210 ounces of gold in bullion inventory and 2,770 ounces of silver and 143 ounces of gold in concentrate inventory. For the nine months ended September 30, adjusted EBITDA and EPS amounted to $33.1 million and $(0.01), respectively.

Updating estimates. We expect stronger financial performance during the fourth quarter although we have trimmed our 2022 EPS estimate to $0.06 per share from $0.09 to reflect third quarter financial results. We have lowered our 2023 EBITDA and EPS estimates to $52.5 million and $0.09, respectively, from $0.11 and $53.3 million to reflect modestly lower margin on sales.

This Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

Mark Reichman, Senior Research Analyst, Natural Resources, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

Third quarter 2022 results. Coeur reported a third quarter adjusted net loss of $44.7 million or $(0.16) per share compared to a net loss of $2.9 million or $(0.01) per share during the prior year period. We had forecast a net loss of $3.0 million or $(0.01) per share. Sales were lower and costs applicable to sales were higher than our estimates. Free cash flow was $(115.7) million. For the nine months ended September 30, the company generated adjusted EBITDA in the amount of $103.1 million and free cash flow of $(242.2) million.

Updating estimates. We have lowered our 2022 EBITDA and EPS estimates to $136.3 million and $(0.31), respectively, from $151.8 million and $(0.12). Revisions to our 2022 estimates reflect third quarter results and lower commodity price assumptions in the fourth quarter. Our 2023 estimates remain unchanged.

This Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.