Shareholder Conference Call and Webcast will be held on Wednesday November 16th, 2022

TORONTO–(BUSINESS WIRE)– Sierra Metals Inc. (TSX: SMT) (NYSE American: SMTS) (BVL or Bolsa de Valores de Lima: SMT) (“Sierra Metals” or the “Company”) will release Q3-2022 consolidated financial results on Tuesday November 15th, 2022, after Market Close. Senior Management will also host a webcast and conference call on Wednesday November 16th, 2022, at 11:00 am EST. Details of the Conference Call and Webcast are as follows:

Via Webcast:

A live audio webcast of the meeting will be available on the Company’s website:

The webcast along with presentation slides will be archived for 180 days on www.sierrametals.com.

Via phone:

For those who prefer to listen by phone, dial-in instructions are below. To ensure your participation, please call approximately five minutes prior to the scheduled start time of the call.

Canada dial-in number (Toll Free): 1 833 950 0062 Canada dial-in number (Local): 1 226 828 7575 US dial-in number (Toll Free): 1 844 200 6205 US dial-in number (Local): 1 646 904 5544 All other locations: +1 929 526 1599

Access code: 991150

Press *1 to ask a question, *2 to withdraw your question, or *0 for operator assistance

About Sierra Metals

Sierra Metals Inc. is a diversified Canadian mining company with Green Metal exposure including copper production and base metal production with precious metals byproduct credits, focused on the production and development of its Yauricocha Mine in Peru, and Bolivar and Cusi Mines in Mexico. The Company is focused on increasing production volume and growing mineral resources. The Company has large land packages at all three mines with several prospective regional targets providing longer-term exploration upside and mineral resource growth potential.

The Company’s Common Shares trade on the Bolsa de Valores de Lima and on the Toronto Stock Exchange under the symbol “SMT” and on the NYSE American Exchange under the symbol “SMTS”.

For further information regarding Sierra Metals, please visit www.sierrametals.com or contact:

InPlay Oil is a junior oil and gas exploration and production company with operations in Alberta focused on light oil production. The company operates long-lived, low-decline properties with drilling development and enhanced oil recovery potential as well as undeveloped lands with exploration possibilities. The common shares of InPlay trade on the Toronto Stock Exchange under the symbol IPO and the OTCQX Exchange under the symbol IPOOF.

Michael Heim, CFA, Senior Research Analyst, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

InPlay received Toronto Stock Exchange approval for a Normal Course Issuer Bid. Under the NCIB, InPlay may purchase and cancel up to 10% of public float of the shares of IPO on the TSX subject to a daily limit of 25% of the average daily trading volume. At current prices, the buyback would be approximately C$20 million if maxed out. Management believes the buyback is a prudent step given the energy market volatility and its belief that, at times, its stock is undervalued. We would note that the shares of IPO (and IPOOF on the OTC exchange) have declined 40% off of June peak levels despite very positive recent operational developments (see 9/29/2022 report). NCIB approval follows 9/28/22 comments that Board of Directors had approved a share buyback program.

The company has the cash flow and balance sheet to do a share buyback. At current energy price levels, we expect the company to generate approximately C$150 million in Adjusted Fund Flow, far exceeding recently-raised capital expenditures of C$70-72 million (up from C$18 million in 2020). The company has been paying down debt and expects to reduce its net debt to EBITDA ratio to 0.1-0.2 times by the end of 2022 (implying that the current net debt level of C$52 million will be reduced to C$15-30 million). Net debt, which represented 50% of total capitalization as recently as 2020, now represents less than 10% of capitalization. We believe management has adequate cash flow to continue to grow capital expenditures, pay down debt, and still initiate a share repurchase program.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

Entravision Communications Corporation is a diversified Spanish-language media company utilizing a combination of television and radio operations to reach Hispanic consumers across the United States, as well as the border markets of Mexico. Entravision owns and/or operates 53 primary television stations and is the largest affiliate group of both the top-ranked Univision television network and Univision’s TeleFutura network, with television stations in 20 of the nation’s top 50 Hispanic markets. The Company also operates one of the nation’s largest groups of primarily Spanish-language radio stations, consisting of 48 owned and operated radio stations.

Michael Kupinski, Director of Research, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

Partners with Meta in Ghana. The company announced that it has partnered with Meta (Facebook) to be its ad agency in the country of Ghana. While this is not a large country, with a potential market opportunity of $10 million, it does set the table for future relationships with Meta in other parts of the world.

Accelerated purchase of Cisneros become clear. Entravision recently accelerated the purchase of Cisneros for a total of $44 million of the remaining 49% interest that it did not own. This would free the company to expand its relationship with Meta to other parts of the globe, outside of its current Latin American market. The recent expansion in Ghana is an example of that.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

Gregory Aurand, Senior Research Analyst, Healthcare Services & Medical Devices, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

Pre-clinical in meniscus repair officially begins. ChitogenX announced the second orthopedic indication for ORTHO-R is moving from feasibility studies to formal pre-clinical status, beginning November 2022. Meniscus repair is needed due to acute trauma tears and degenerative tears, but surgical failure rates are currently in the 20%-40% range, offering substantial opportunity for ChitogenX’s platform technology to improve healing outcomes.

Meniscus repair program will test 22 sheep. The sheep will be tested with sutures alone (current standard of care) vs. platelet rich plasma (PRP) alone vs. PRP delivered by ORTHO-R biopolymer. Repair surgeries are scheduled beginning mid-November and should be completed by first of December. Results are expected approximately in 12 months in fall of 2023.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

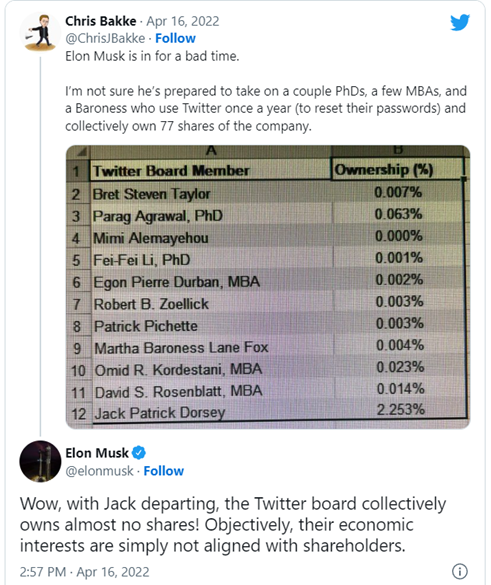

Elon Musk Argues Twitter is Better off Without a Board of Directors – Is He Right?

After a wild ride, it looks like Elon Musk’s bid to buy Twitter will move ahead.

Twitter’s board of directors had sued the Tesla billionaire in July 2022 when Musk tried to terminate the US$44 billion deal. The board has yet to drop its lawsuit to force Musk to complete the buyout, while many parts have been thrown out.

The board has in fact been at the center of this saga since the beginning, when Musk launched his hostile takeover bid while criticizing board members for owning almost no shares of the company they oversee. Twitter founder Jack Dorsey called the board the “dysfunction of the company.”

This article was republished with permission from The Conversation, a news site dedicated to sharing ideas from academic experts. It represents the research-based findings and thoughts of Michael Withers, Associate Professor of Business, Texas A&M University, Steven Boivie, Professor of Management, Texas A&M University.

As experts on corporate governance, we believe this feud raised two important corporate governance questions: What purpose does a board of directors serve? And does it matter if a member owns company stock or not?

‘A Bad Board Will Kill’

“Good boards don’t create good companies, but a bad board will kill a company every time.”

Venture capitalist Fred Destin wrote that in 2018, citing what he called an “old Silicon Valley proverb.” The quote has been making the rounds on Twitter recently in light of Musk’s hostile bid. It even seemed to get a nod from Dorsey himself when he replied to a tweet containing the quote with “big facts.”

This tweet and the general conversation that has emerged have important implications for understanding boards and their role in shepherding a company.

Broadly speaking, a board’s most important roles include hiring, paying and monitoring the chief executive officer.

Academic research suggests that board members at large companies – who typically receive generous compensation packages – may be limited in their ability to perform these tasks effectively. In our work, we found that boards often find it impossible to conduct adequate monitoring and rein in wayward CEOs because there’s just so much information for modern boards to process with their limited time. And the social dynamics involved in the board also make it difficult for directors to speak up and oppose other directors.

In a separate study involving face-to-face interviews with directors, we were consistently told that directors take their board service seriously and operate with their companies’ best interests in mind. But they do so with an eye toward collaborating with the CEO and the rest of the executive team rather than serving as impartial observers, as their “independent” status suggests they should.

While our work didn’t focus on this, if the board and the CEO fundamentally disagree about the direction of company – which was often the case between Dorsey and the Twitter board – it would certainly be problematic and could lead to less than optimal decisions being made.

In other words, a board that isn’t functioning effectively can definitely destroy a company’s value. And some reporting suggests that’s what happened to Twitter, whose shares were trading at less than half their 2021 peak before Musk disclosed he had amassed a 9% ownership stake.

A Raider’s Lament

That brings us to the next question: Does not owning a significant stake in a company you oversee make it more likely that you’ll run it into the ground, as Musk seemed to suggest?

A few days after making his takeover offer on April 14, the billionaire, responding to a tweet showing how few shares Twitter board members own, posted that its directors’ “economic interests are simply not aligned with shareholders.”

Musk’s arguments harked back to takeover bids from the 1980s in which activist investors – or “corporate raiders” – would argue that executives’ interests did not align with those of shareholders. As Gordon Gekko from the film “Wall Street” famously railed against executives of a business he wanted to take over, “Today, management has no stake in the company!”

Musk’s words echo Gekko’s “greed is good” speech, except in regard to independent directors, who comprise the vast majority of corporate boards. By definition, an independent or outside director is one who doesn’t hold an executive role in running the company, such as chief executive officer or chief financial officer.

In reality, Twitter’s board share ownership is very similar to that of other companies.

Independent Twitter directors held a median ownership stake of 0.003% as of May 2022. For comparison, we looked at equity ownership of independent directors of companies listed in the S&P 500 stock index in 2021. We found the median stake was less than 0.01%, and all but a handful of directors held less than 1% of the company’s stock. Median ownership at Musk’s company Tesla is similarly minuscule, at 0.23%.

Whether this makes a difference to a company’s success is hard to assess because research on the topic is rather sparse, in large part because board members have so little equity.

Mixed Research

Academic researchers on effective corporate governance in the 1970s argued that outside directors should avoid owning many shares in the companies they oversee to maintain objectivity. More recently, management scholars have suggested that higher stakes could provide a way to motivate directors to monitor management and make decisions more in line with shareholder interests.

Some researchers have found that boards with larger ownership stakes can improve a company’s operational performance and better align outside directors with the interests of shareholders.

But other work that examined multiple studies shows the impact of director stock ownership is mixed at best, with some studies suggesting higher stakes potentially lead to negative outcomes, such as excessive executive and director compensation.

Since the passage of the Sarbanes–Oxley Act of 2002 after massive accounting scandals at Enron, WorldCom and elsewhere, corporate governance issues such as board oversight have become increasingly important. This led to a number of changes intended to align the interests of managers and those of shareholders, including a focus on board independence and adjusting executive compensation.

Although our research shows boards are limited in their ability to monitor management, they’re still better than nothing.

In his original letter to shareholders announcing his bid, Musk vowed to “unlock” Twitter’s potential as a private company, without a public board. We may finally learn if he’s right.

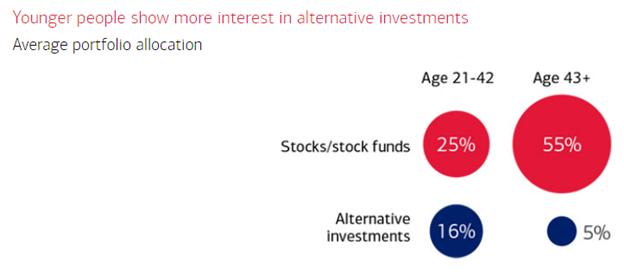

Should Investors Consider Taking Different Steps for Diversification?

Diversification reduces risk; at least, this is what we’re told. It could also limit the upside, but it’s downside that is most concerning to investors. True diversification is a goal embraced by most. Investors used to try to achieve this by buying a broad stock market ETF coupled with a bond ETF. Well, the Fed-induced bond bear market, which is feeding the equity bear market, is a double whammy for these investors. So else is there to pivot to?

Investors’ goals used to be to make sure they achieved above index results, what I am hearing from investors now is they just want to stop losing money. The return benchmark has been changed.

Is Diversification Attainable

Historically, when stock prices have gone down, bonds have appreciated. That’s because rates tended to sink when economic activity faltered and rose when demand for money was higher; this is because the economy was growing. Bond rates today are less driven by economic pace and natural market factors. An active Fed has more control over yields. So this yin and yang relationship between stocks and bonds is much less negatively correlated.

While the U.S. and global economy are in unchartered waters, the scenario where the Fed has promised negative returns on bonds, and while stocks continue to falter from past stimulus being pulled from the economy by the Fed, alternatives may be worth exploring.

Investors, have been told to diversify using registered securities from a young age, at a young age these are often the only options. Securities include registered company stocks and bonds. They are then told the best way to do this is with funds (Mutual funds and ETFs) that contain many securities, thus assuring diversification across that asset class. But, over time, as more have taken to the idea of buying “the market” or selling ”the market” using funds, movements by those getting in or out of the market en-masse impact more and more people. This year trillions have been lost by investors because of this.

Do publicly traded securities still make sense? Chris Hyzy, Chief Investment Officer for Merrill and Bank of America Private Bank says, “We have transitioned into a new investment cycle driven by higher inflation and a pivot by global central banks, among many other factors. This is likely to create higher asset price volatility and new market leaders.” Speaking for B of A he said, “We believe alternative investments can play a role in helping qualified investors pursue today’s opportunities.”

Source: Bank of America (Private Bank)

One “Alternative” that more traditional investors are now looking at is private equity. Private equity involves investment partnerships that buy and manage companies before selling them. Private equity firms operate these investment funds for institutional and other accredited investors. This subset of investment alternatives is often grouped with venture capital and even hedge funds. The Investors are usually required to commit capital for extended periods, the lack of market price swings allows a level of stability not found in the bid/ask tick-by-tick valuations found in the stock or bond markets. This same advantage which allows management to be more focused on managing the company’s long-term viability limits liquidity for investors. This is why access to such investments is limited to institutions and qualifying individuals.

Other Asset Classes

In addition to qualifying as an accredited investor in private equity deals, those interested in alternatives may look to real estate, which also tends to fall with rising interest rates. Precious metals are also an alternative that investors use to diversify. The hedge fund universe provides an assortment of ideas and strategies that the fund managers use that are often de-linked from traditional markets.

Take Away

The Federal Reserve has indicated an unbending resolve to bring inflation. Mathematically this brings bond prices down with higher yields. Higher yields siphon money out of the stock market, which is already at a dimmer point of the business cycle. Alternatives, including private equity, has outperformed public markets and may also help manage portfolio volatility.

Investors that are uncertain if they qualify as an accredited investor may want to Pre-approve. There is no cost, Noble Capital Markets can do this and then provide those that meet the requirements access to its private deals. Knowing the options available and how to use them can provide uncommon and uncorrelated returns to a portfolio.

HOUSTON, Oct. 13, 2022 /PRNewswire/ — Direct Digital Holdings, Inc. (Nasdaq: DRCT) (“Direct Digital Holdings” or the “Company”), a leading advertising and marketing technology platform through its operating companies Colossus Media, LLC, (“Colossus SSP”) Huddled Masses LLC (“Huddled Masses”) and Orange142, LLC (“Orange 142”), today announced that it will report financial results for the third quarter 2022 on November 10, 2022. Management will discuss the results via webcast after market close.

Direct Digital Holdings (Nasdaq: DRCT), owner of operating companies Colossus SSP, Huddled Masses, and Orange 142, brings state-of-the-art sell- and buy-side advertising platforms together under one umbrella company. Direct Digital Holdings’ sell-side platform, Colossus SSP, offers advertisers of all sizes extensive reach within general market and multicultural media properties. The company’s subsidiaries Huddled Masses and Orange142 deliver significant ROI for middle market advertisers by providing data-optimized programmatic solutions at scale for businesses in sectors that range from energy to healthcare to travel to financial services. Direct Digital Holdings’ sell- and buy-side solutions manage approximately 90,000 clients monthly, generating over 100 billion impressions per month across display, CTV, in-app and other media channels. The company has been named a top minority-owned business by The Houston Business Journal.

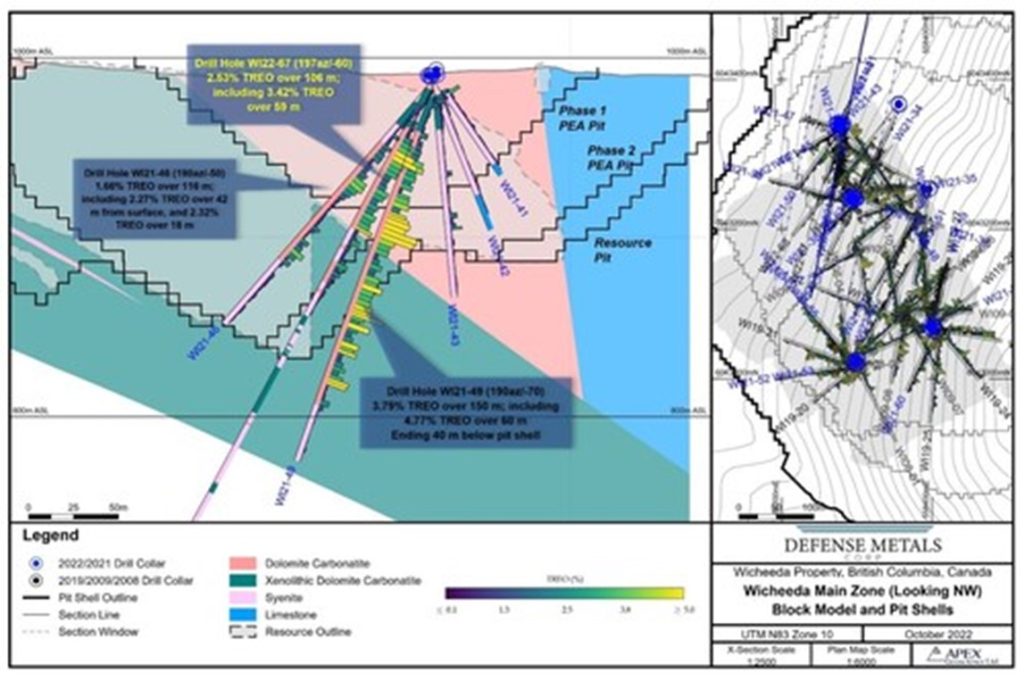

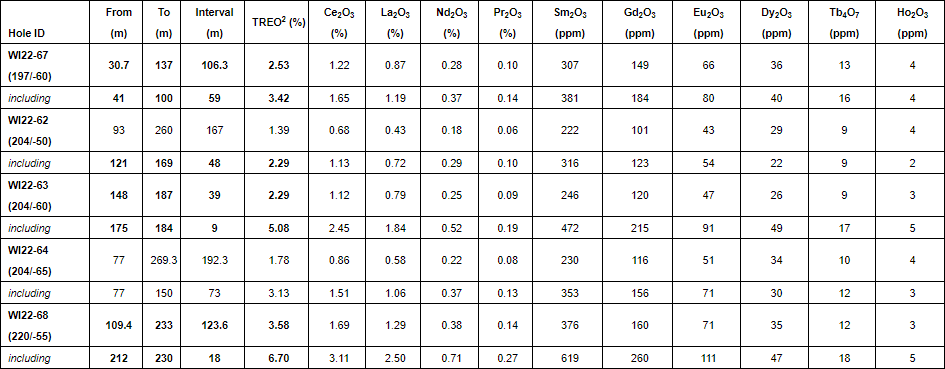

Infill drill hole WI22-67 (-60o dip / 197o azimuth) was drilled southward within the northern area of the deposit and yielded a broad mixed lithology mineralized intercept comprising dolomite carbonatite and syenite averaging 2.53% total rare earth oxide (“TREO”) over 106 metres (m); including a high-grade zone of 3.42% TREO over 59 m1 (Figure 1). The assays reported for WI22-67 are partial from surface to a downhole depth of 155 metres. Assay results for the remaining 165 m to end of hole at 320 m are expected in the coming days.

Craig Taylor, CEO, and Director of Defense Metals stated: “With the release of this additional drill hole, we continue to establish excellent continuity of mineralization in sectional infill drilling. As we advance the Wicheeda Project we know these kinds of results will contribute significantly to our goal of upgraded resource categories necessary to support a future Preliminary Feasibility Study (PFS).”

18th International Rare Earths Conference, Las Vegas, Nevada

Defense Metals and many of its directors, management and advisors will be attending the 18th International Rare Earths Conference on October 17, 2022 to October 19, 2022 in Las Vegas, Nevada. Luisa Moreno, President and Director of the Company will be presenting on the “Wicheeda Deposit: The Next North American REE production“.

About the Wicheeda REE Property

The 100% owned 4,244-hectare Wicheeda REE Property, located approximately 80 km northeast of the city of Prince George, British Columbia, is readily accessible by all-weather gravel roads and is near infrastructure, including power transmission lines, the CN railway, and major highways.

The Wicheeda REE Project yielded a robust 2021 preliminary economic assessment technical report (PEA) that demonstrated an after-tax net present value (NPV@8%) of $517 million, and 18% IRR3. A unique advantage of the Wicheeda REE Project is the production of a saleable high-grade flotation-concentrate. The PEA contemplates a 1.8 Mtpa (million tonnes per year) mill throughput open pit mining operation with 1.75:1 (waste:mill feed) strip ratio over a 19 year mine (project) life producing and average of 25,423 tonnes REO annually. A Phase 1 initial pit strip ratio of 0.63:1 (waste:mill feed) would yield rapid access to higher grade surface mineralization in year 1 and payback of $440 million initial capital within 5 years.

Methodology and QA/QC

The analytical work reported on herein was performed by ALS Canada Ltd. (ALS) at Langley (sample preparation) and Vancouver (ICP-MS fusion), B.C. ALS is an ISO-IEC 17025:2017 and ISO 9001:2015 accredited geoanalytical laboratory and is independent of the Defense Metals and the QP. Drill core samples were subject to crushing at a minimum of 70% passing 2 mm, followed by pulverizing of a 250-gram split to 85% passing 75 microns. A 0.1-gram sample pulp was then subject to multi-element ICP-MS analysis via lithium-borate fusion to determine individual REE content (ME-MS81h). Defense Metals follows industry standard procedures for the work carried out on the Wicheeda Project, with a quality assurance/quality control (QA/QC) program. Blank, duplicate, and standard samples were inserted into the sample sequence sent to the laboratory for analysis. Defense Metals detected no significant QA/QC issues during review of the data.

Qualified Person

The scientific and technical information contained in this news release as it relates to the Wicheeda REE Project has been reviewed and approved by Kristopher J. Raffle, P.Geo. (BC) Principal and Consultant of APEX Geoscience Ltd. of Edmonton, AB, a director of Defense Metals and a “Qualified Person” as defined in NI 43-101. Mr. Raffle verified the data disclosed which includes a review of the sampling, analytical and test data underlying the information and opinions contained therein.

About Defense Metals Corp.

Defense Metals Corp. is a mineral exploration and development company focused on the acquisition, exploration and development of mineral deposits containing metals and elements commonly used in the electric power markets, defense industry, national security sector and in the production of green energy technologies, such as, rare earths magnets used in wind turbines and in permanent magnet motors for electric vehicles. Defense Metals owns 100% of the Wicheeda Rare Earth Element Deposit located near Prince George, British Columbia, Canada. Defense Metals Corp. trades in Canada under the symbol “DEFN” on the TSX Venture Exchange, in the United States, under “DFMTF” on the OTCQB and in Germany on the Frankfurt Exchange under “35D”.

Neither the TSX Venture Exchange nor its Regulation Services Provider (as that term is defined in the policies of the TSX Venture Exchange) accepts responsibility for the adequacy or accuracy of this news release.

Cautionary Statement Regarding “Forward-Looking” Information

This news release contains “forward‐looking information or statements” within the meaning of applicable securities laws, which may include, without limitation, statements relating to advancing the Wicheeda REE Project, drill results including anticipated timeline of such results/assays, upgrading the resource categories, completing the PFS, the Company’s plans for its Wicheeda REE Project, expanded resource and scale of expanded resource, expected results and outcomes, the technical, financial and business prospects of the Company, its project and other matters. All statements in this news release, other than statements of historical facts, that address events or developments that the Company expects to occur, are forward-looking statements. Although the Company believes the expectations expressed in such forward-looking statements are based on reasonable assumptions, such statements are not guarantees of future performance and actual results may differ materially from those in the forward-looking statements. Such statements and information are based on numerous assumptions regarding present and future business strategies and the environment in which the Company will operate in the future, including the price of rare earth elements, the anticipated costs and expenditures, the ability to achieve its goals, that general business and economic conditions will not change in a material adverse manner, that financing will be available if and when needed and on reasonable terms. Such forward-looking information reflects the Company’s views with respect to future events and is subject to risks, uncertainties and assumptions, including the risks and uncertainties relating to the interpretation of exploration results, risks related to the inherent uncertainty of exploration and cost estimates, the potential for unexpected costs and expenses and those other risks filed under the Company’s profile on SEDAR at www.sedar.com. While such estimates and assumptions are considered reasonable by the management of the Company, they are inherently subject to significant business, economic, competitive and regulatory uncertainties and risks. Factors that could cause actual results to differ materially from those in forward looking statements include, but are not limited to, continued availability of capital and financing and general economic, market or business conditions, adverse weather and climate conditions, failure to maintain or obtain all necessary government permits, approvals and authorizations, failure to maintain community acceptance (including First Nations), risks relating to unanticipated operational difficulties (including failure of equipment or processes to operate in accordance with specifications or expectations, cost escalation, unavailability of personnel, materials and equipment, government action or delays in the receipt of government approvals, industrial disturbances or other job action, and unanticipated events related to health, safety and environmental matters), risks relating to inaccurate geological and engineering assumptions, decrease in the price of rare earth elements, the impact of Covid-19 or other viruses and diseases on the Company’s ability to operate, an inability to predict and counteract the effects of COVID-19 on the business of the Company, including but not limited to, the effects of COVID-19 on the price of commodities, capital market conditions, restriction on labour and international travel and supply chains, loss of key employees, consultants, or directors, increase in costs, delayed drilling results, litigation, and failure of counterparties to perform their contractual obligations. The Company does not undertake to update forward‐looking statements or forward‐looking information, except as required by law.

1

The true width of REE mineralization is estimated to be 70-100% of the drilled interval.

2

TREO % sum of CeO2, La2O3, Nd2O3, Pr6O11, Sm2O3, Eu2O3, Gd2O3, Tb4O7, Dy2O3 and Ho2O3.

3

Independent Preliminary Economic Assessment for the Wicheeda Rare Earth Element Project, British Columbia, Canada, dated January 6, 2022, with an effective date of November 7, 2021, and prepared by SRK Consulting (Canada) Inc. is filed under Defense Metals Corp.’s Issuer Profile on SEDAR (www.sedar.com).

JERICHO, N.Y.–(BUSINESS WIRE)– 1-800-FLOWERS.COM, Inc. (NASDAQ: FLWS),a leading provider of gifts designed to help inspire customers to give more, connect more, and build more and better relationships, today announced that the Company will release financial results for its fiscal 2023 first quarter on Thursday, November 3, 2022. The press release will be issued prior to market opening and will be followed by a conference call with members of senior management at 8:00 a.m. (ET).

The conference call will be available via live webcast from the Investors section of the Company’s website at 1800flowersinc.com. A recording of the call will be posted on the website within two hours of the call’s completion. A telephonic replay of the call can be accessed beginning at 2:00 p.m. (ET) on November 3, 2022, through November 10, 2022, at: (US) 1-877-344-7529; (Canada) 855-669-9658; (International) 1-412-317-0088; enter conference ID: #5253715. If you have any questions regarding the above information, please call the Investor Relations office at (516) 237-4617.

Special Note Regarding Forward-Looking Statements: Some of the statements contained in the Company’s scheduled Thursday, November 3, 2022, press release and conference call regarding its results for its fiscal 2023 first quarter, other than statements of historical fact, may be forward-looking within the meaning of the Private Securities Litigation Reform Act of 1995. These statements involve risks and uncertainties that could cause actual results to differ materially from those expressed or implied in the applicable statements. For a more detailed description of these and other risk factors, please refer to the Company’s SEC filings including its Annual Reports and Forms 10K and 10Q available at the Investor Relations section of the Company’s website at 1800flowersinc.com. The Company expressly disclaims any intent or obligation to update any of the forward-looking statements made in the scheduled conference call and any recordings thereof, or in any of its SEC filings, except as may be otherwise stated by the Company.

About 1-800-FLOWERS.COM, Inc. 1-800-FLOWERS.COM, Inc. is a leading provider of gifts designed to help inspire customers to give more, connect more, and build more and better relationships. The Company’s e-commerce business platform features an all-star family of brands, including: 1-800-Flowers.com®, 1-800-Baskets.com®, Cheryl’s Cookies®, Harry & David®, PersonalizationMall.com®, Shari’s Berries®, FruitBouquets.com®, Moose Munch®, The Popcorn Factory®, Wolferman’s Bakery®, Vital Choice®, Stock Yards® and Simply Chocolate®. Through the Celebrations Passport® loyalty program, which provides members with free standard shipping and no service charge across our portfolio of brands, 1-800-FLOWERS.COM, Inc. strives to deepen relationships with customers. The Company also operates BloomNet®, an international floral and gift industry service provider offering a broad-range of products and services designed to help members grow their businesses profitably; Napco℠, a resource for floral gifts and seasonal décor; DesignPac Gifts, LLC, a manufacturer of gift baskets and towers; and Alice’s Table®, a lifestyle business offering fully digital livestreaming and on demand floral, culinary and other experiences to guests across the country. 1-800-FLOWERS.COM, Inc. was recognized among the top 5 on the National Retail Federation’s 2021 Hot 25 Retailers list, which ranks the nation’s fastest-growing retail companies, and was named to the Fortune 1000 list in 2022. Shares in 1-800-FLOWERS.COM, Inc. are traded on the NASDAQ Global Select Market, ticker symbol: FLWS. For more information, visit 1800flowersinc.com or follow @1800FLOWERSInc on Twitter.

CALGARY, Alberta, Oct. 13, 2022 (GLOBE NEWSWIRE) — InPlay Oil Corp. (TSX: IPO) (OTCQX: IPOOF) (“InPlay” or the “Company“) today announced that the Toronto Stock Exchange (“TSX“) has accepted InPlay’s notice of intention to commence a normal course issuer bid (the “NCIB“).

Under the NCIB, InPlay may purchase for cancellation, from time to time, as InPlay considers advisable, up to a maximum of 6,467,875 common shares of InPlay (“Common Shares“), which represents 10% of the Company’s public float of 64,678,759 Common Shares as at October 7, 2022. As of the same date, InPlay had 87,150,301 Common Shares issued and outstanding. Purchases of Common Shares may be made on the open market through the facilities of the TSX and through other alternative Canadian trading platforms at the prevailing market price at the time of such transaction. The actual number of Common Shares that may be purchased for cancellation and the timing of any such purchases will be determined by InPlay, subject to a maximum daily purchase limitation of 112,558 Common Shares which equates to 25% of InPlay’s average daily trading volume of 450,234 Common Shares for the six months ended September 30, 2022. InPlay may make one block purchase per calendar week which exceeds the daily repurchase restrictions. Any Common Shares that are purchased by InPlay under the NCIB will be cancelled.

The NCIB will commence on October 17, 2022 and will terminate on October 16, 2023 or such earlier time as the NCIB is completed or terminated at the option of InPlay.

InPlay believes that implementing the NCIB is a prudent step in this volatile energy market environment, when at times, the prevailing market price does not reflect the underlying value of its Common Shares. The timely repurchase of the Company’s Common Shares for cancellation represents confidence in the long term prospects and sustainability of its business model. This reduction in share count adds per share value to InPlay’s shareholders and adds another tool to management’s disciplined capital allocation strategy.

About InPlay Oil Corp.

InPlay Oil is a junior oil and gas exploration and production company with operations in Alberta focused on light oil production. The Company operates long-lived, low-decline properties with drilling development and enhanced oil recovery potential as well as undeveloped lands with exploration possibilities. The Common Shares on the Toronto Stock Exchange under the symbol IPO and the OTCQX under the symbol IPOOF.

For further information please contact:

Doug Bartole President and Chief Executive Officer InPlay Oil Corp. Telephone: (587) 955-0632

This news release contains certain statements that may constitute forward-looking information within the meaning of applicable securities laws. This information includes, but is not limited to InPlay’s intentions with respect to the NCIB and purchases thereunder and the effects of repurchases under the NCIB. Although InPlay believes that the expectations and assumptions on which the forward-looking statements are based are reasonable, undue reliance should not be placed on the forward-looking statements because InPlay can give no assurance that they will prove to be correct. Since forward-looking statements address future events and conditions by their very nature they involve inherent risks and uncertainties. Actual results could defer materially from those currently anticipated due to a number of factors and risks. Certain of these risks are set out in more detail in InPlay’s Annual Information Form which has been filed on SEDAR and can be accessed at www.sedar.com.

The forward-looking statements contained in this press release are made as of the date hereof and InPlay undertakes no obligation to update publically or revise any forward-looking statements or information, whether as a result of new information, future events or otherwise, unless so required by applicable securities laws.

CAMBRIDGE, Mass.–(BUSINESS WIRE)–Oct. 13, 2022– Axcella Therapeutics (Nasdaq: AXLA), a clinical-stage biotechnology company pioneering a new approach to treat complex diseases using multi-targeted endogenous metabolic modulator (EMM) compositions, today announced that it has entered into a securities purchase agreement with investors in a registered direct offering of 20,847,888 shares of common stock (the “Shares”) at a purchase price of $1.64 per share, resulting in gross proceeds of $34.2 million, including $6.0 million received as the cancellation of indebtedness upon the conversion of unsecured subordinated convertible promissory notes held by Flagship Pioneering.

The offering closed on October 13, 2022. Since this offering was made without an underwriter or a placement agent, Axcella did not pay any underwriting discounts in connection with the transaction. Axcella intends to use the net proceeds from the offering together with existing cash and cash equivalents to advance the Long COVID program, including regulatory engagement and preparation for further clinical development; advance and complete enrollment of its EMMPACT Phase 2b clinical trial in non-alcoholic steatohepatitis (NASH); and for working capital and other general corporate purposes.

The Shares were offered pursuant to a shelf registration statement that was previously filed with the U.S. Securities and Exchange Commission (the “SEC”) and declared effective by the SEC on June 12, 2020. A final prospectus supplement, which contains additional information relating to the offering, has been filed with the SEC and is available on the SEC’s website at www.sec.gov.

This press release shall not constitute an offer to sell or the solicitation of an offer to buy the Shares, nor shall there be any sale of the Shares in any state or other jurisdiction in which such offer, solicitation or sale would be unlawful prior to the registration or qualification under the securities laws of any such state or other jurisdiction.

“We believe investors were attracted by results from our Phase 2a Placebo Controlled Clinical Trial for Long COVID and positive interim data from our Phase 2b study of NASH. In addition to strong support from our largest current investors, this round of financing also included five investors who are new to Axcella as well as certain Directors and members of management of the company,” said Bill Hinshaw, CEO of Axcella.

Simultaneous with the financing, the company is appointing Robert Rosiello and Torben Straight Nissen to its Board of Directors, and Mr. Rosiello also will become Chairman of the Board. Mr. Rosiello is an Executive Partner of Flagship Pioneering, where he focuses on building capability to originate, manage, and grow new Flagship companies, and helps drive Flagship’s strategy, institution building, and growth initiatives. He came to Flagship after a thirty-year career at McKinsey advising CEOs and Boards of leading healthcare, technology and consumer companies. He also has experience managing through periods of change in a public company as CFO, and he has start-up Board experience through his previous service on the board of Flagship company Inari. Mr. Straight Nissen is a Senior Partner at Flagship Pioneering, where he is responsible for company creation in one of Flagship’s newest growth vectors, Preemptive Health and Medicine. He has provided executive and R&D leadership to biotech and pharmaceutical companies for more than twenty years. Prior to joining Flagship, Mr. Straight Nissen headed up Strategic Portfolio Management for Pfizer’s worldwide R&D organization where he oversaw Pfizer’s portfolio spanning discovery to Phase 2b across all major therapeutic areas.

“Axcella’s emerging leadership in therapeutics for Long COVID and NASH make it an exciting time for the company, and I look forward to working with the Axcella management team and Board as we advance the platform and continue to build value in the company,” said Mr. Rosiello.

“Axcella has generated impressive clinical data that demonstrate the potential to harness the power of EMMs to tackle prevalent chronic conditions and I believe the company is now well positioned to provide safe and convenient orally delivered 1st line treatments for diseases with large unmet medical needs, such as NASH and Long COVID,” said Mr. Straight Nissen. “I look forward to working with Bill and his team to bring these important products to patients and their families.”

With Mr. Rosiello and Mr. Straight Nissen joining the Board, David Epstein will step down as Chairman and from the Board. Mr. Epstein has been with the Company for five years and has seen the Company through important milestones with multiple phase 2 programs reporting positive data in large and unserved diseases and now wishes to focus on personal priorities. Mr. Epstein remains highly supportive of the Company and will continue as a consultant to the Company.

Internet Posting of Information

Axcella uses the “Investors and News” section of its website, www.axcellatx.com, as a means of disclosing material nonpublic information, to communicate with investors and the public, and for complying with its disclosure obligations under Regulation FD. Such disclosures include, but may not be limited to, investor presentations and FAQs, Securities and Exchange Commission filings, press releases, and public conference calls and webcasts. The information that we post on our website could be deemed to be material information. As a result, we encourage investors, the media and others interested to review the information that we post there on a regular basis. The contents of our website shall not be deemed incorporated by reference in any filing under the Securities Act of 1933, as amended.

About Axcella Therapeutics (Nasdaq: AXLA)

Axcella is a clinical-stage biotechnology company pioneering a new approach to treat complex diseases using compositions of endogenous metabolic modulators (EMMs). The company’s product candidates are comprised of EMMs and derivatives that are engineered in distinct combinations and ratios to reset multiple biological pathways, improve cellular energetics, and restore homeostasis. Axcella’s pipeline includes lead therapeutic candidates in Phase 2 development for the treatment of Long COVID and NASH. The company’s unique model allows for the evaluation of its EMM compositions through non-IND clinical studies or IND clinical trials. For more information, please visit www.axcellatx.com.

Forward-Looking Statements

This press release contains forward-looking statements within the meaning of the Private Securities Litigation Reform Act of 1995, as amended, including, without limitation, the anticipated closing date of the offering and use of proceeds from the offering, investor motivation to participate in the offering, the expected benefits of Mr. Rosiello’s and Mr. Straight Nissen’s service on the Board of Directors of Axcella and the potential for AXA1125 to serve as a first-line treatment option. The words “may,” “will,” “could,” “would,” “should,” “expect,” “plan,” “anticipate,” “intend,” “believe,” “estimate,” “predict,” “project,” “potential,” “continue,” “target” and similar expressions are intended to identify forward-looking statements, although not all forward-looking statements contain these identifying words. Any forward-looking statements in this press release are based on management’s current expectations and beliefs and are subject to a number of risks, uncertainties and important factors that may cause actual events or results to differ materially from those expressed or implied by any forward-looking statements contained in this press release, including, without limitation, those related to the potential impact of COVID-19 on the company’s ability to conduct and complete its ongoing or planned clinical studies and clinical trials in a timely manner or at all due to patient or principal investigator recruitment or availability challenges, clinical trial site shutdowns or other interruptions and potential limitations on the quality, completeness and interpretability of data the company is able to collect in its clinical trials of AXA1125, other potential impacts on the company’s business and financial results, including with respect to its ability to raise additional capital and operational disruptions or delays, changes in law, regulations, or interpretations and enforcement of regulatory guidance, whether data readouts support the company’s clinical trial plans and timing, clinical trial design and target indications for AXA1125, the clinical development and safety profile of AXA1125 and their therapeutic potential, whether and when, if at all, the company’s product candidates will receive approval from the FDA or other comparable regulatory authorities, potential competition from other biopharma companies in the company’s target indications, and other risks identified in the company’s SEC filings, including Axcella’s Annual Report on Form 10-K, Quarterly Report on Form 10-Q and subsequent filings with the SEC. The company cautions you not to place undue reliance on any forward-looking statements, which speak only as of the date they are made. Axcella disclaims any obligation to publicly update or revise any such statements to reflect any change in expectations or in events, conditions, or circumstances on which any such statements may be based, or that may affect the likelihood that actual results will differ from those set forth in the forward-looking statements. Any forward-looking statements contained in this press release represent the company’s views only as of the date hereof and should not be relied upon as representing its views as of any subsequent date. The company explicitly disclaims any obligation to update any forward-looking statements.

BOTHELL, Wash., Oct. 13, 2022 (GLOBE NEWSWIRE) — Cocrystal Pharma, Inc. (Nasdaq: COCP) announces that President and co-interim CEO Sam Lee, PhD will present data from the Company’s Phase 1 influenza A clinical trial with CC-42344 at the World Antiviral Congress 2022 on Friday, December 1, 2022 at 11:10 a.m. Pacific time. The conference is being held November 28 through December 1 at the Loews Coronado Bay Resort in San Diego.

“We are excited to share data from the first-in-human trial with our novel, broad-spectrum antiviral candidate CC-42344 for the treatment of pandemic and seasonal influenza A, and to discuss our plan to initiate a Phase 2a human challenge influenza A clinical trial,” said Dr. Lee. “It’s an honor to be selected by conference organizers once again for an oral presentation at this prestigious gathering of antiviral experts from around the world.”

The World Antiviral Congress 2022 provides a venue for discussing antiviral vaccines, immunotherapies and antiviral therapies. The World Antiviral Congress 2022 agenda is available here.

About CC-42344 and Influenza

CC-42344 is an oral PB2 inhibitor that blocks an essential step of viral replication and was discovered using Cocrystal’s proprietary structure-based drug discovery platform technology. It is specifically designed to be effective against all significant pandemic and seasonal influenza A strains and to have a high barrier to resistance due to the way the virus’ replication machinery is targeted. CC-42344 targets the influenza polymerase, an essential replication enzyme with several highly essential regions common to multiple influenza strains, including pandemic strains. In vitro testing showed CC-42344’s excellent antiviral activity against influenza A strains, including pandemic and seasonal strains, as well as against strains resistant to Tamiflu® and Xofluza®, while also demonstrating favorable pharmacokinetic and safety profiles.

The global influenza therapeutics market is projected to reach $9.5 billion by 2027 from $6.6 billion in 2020, growing at a 4.8% CAGR between 2021 and 2027, according to a report published by Precision Reports in June 2022.

About Cocrystal Pharma, Inc.

Cocrystal Pharma, Inc. is a clinical-stage biotechnology company discovering and developing novel antiviral therapeutics that target the replication process of influenza viruses, coronaviruses (including SARS-CoV-2), hepatitis C viruses and noroviruses. Cocrystal employs unique structure-based technologies and Nobel Prize-winning expertise to create first- and best-in-class antiviral drugs. For further information about Cocrystal, please visit www.cocrystalpharma.com.

LAKE ZURICH, Ill.–(BUSINESS WIRE)– ACCO Brands Corporation (NYSE: ACCO) announced today an update to the quarter ending September 30, 2022 and its full year 2022 outlook, reflecting a more challenging than anticipated operating environment.

“Our North America segment saw better overall back-to-school sell-through for the season, positive return to office trends and improved brand positioning in the third quarter; however, these improvements were more than offset by retailers’ more cautious approach to inventory replenishment. In Europe, the current energy crisis and persistent inflation has created a more challenging macroeconomic environment, negatively impacting sales and profits in our EMEA segment. These factors offset double-digit sales and profit growth in our International segment,” said Boris Elisman, ACCO Brands Chairman and Chief Executive Officer.

Due to the macroeconomic trends, we are providing a third quarter outlook and lowering our full year 2022 outlook to properly account for reduced channel inventory replenishment, a weaker end-user demand environment, especially in Europe, continued high inflation and adverse foreign exchange impacts. In addition, current market capitalization has triggered a review of our goodwill valuation and we expect to take a yet to be finalized non-cash goodwill impairment charge in the third quarter.

Q3 2022 Outlook

Updated Full Year 2022 Outlook

Previous Full Year 2022 Outlook

Net Sales

$480-$490 million*

$1.940 to $1.980 billion*

$2.015-$2.055 billion

Comparable Sales Growth**

(3%) to (2%)

0.0% to 2.0%

4.0% to 6.0%

Adjusted EPS**

$0.23 to $0.25

$1.05 to $1.10

$1.39 to $1.44

Free Cash Flow**

$90 to $100 million

$135 to $150 million

*Based on spot rates as of 10/10/2022 ** Non-GAAP financial measure

“While there are near-term macroeconomic challenges, the strength of our balance sheet and our ability to generate robust free cash flow will allow ACCO Brands to successfully navigate the current economic uncertainty. We have taken immediate actions to protect profitability and free cash flow by curtailing hiring, reducing inventory, and limiting discretionary spending and capital expenditures. In addition, we are reviewing incremental pricing actions and cost reductions, including facility rationalization projects. We have no debt maturities until 2026 and low annual interest costs. Near-term capital allocation priorities are focused on supporting our dividend and reducing debt. Our strategic transformation plan to be more consumer, brand and technology centric remains intact and we believe it will position us to deliver sustainable organic revenue growth and margin expansion as economies improve,” Elisman concluded.

Third Quarter Results Webcast

The Company will release its third quarter 2022 earnings after the market close on November 7, 2022. The Company will host a conference call and webcast to discuss the results on November 8, 2022 at 8:30 a.m. EST. The webcast can be accessed through the Investor Relations section of www.accobrands.com and will be available for replay.

About ACCO Brands Corporation

ACCO Brands, the Home of Great Brands Built by Great People, designs, manufactures and markets consumer and end-user products that help people work, learn, play and thrive. Our widely recognized brands include AT-A-GLANCE®, Five Star®, Kensington®, Leitz®, Mead®, PowerA®, Swingline®, Tilibra® and many others. More information about ACCO Brands Corporation (NYSE: ACCO) can be found at www.accobrands.com.

Non-GAAP Financial Measures

We have provided certain non-GAAP financial information in this press release to aid investors in understanding the Company’s performance. Each non-GAAP financial measure is defined in the “About Non-GAAP Financial Measures” section of this release.

Forward-Looking Statements

Statements contained in this press release, other than statements of historical fact, particularly those anticipating future financial performance, business prospects, growth, strategies, business operations and similar matters, results of operations, liquidity and financial condition, are “forward-looking statements” within the meaning of the Private Securities Litigation Reform Act of 1995. These statements are based on the beliefs and assumptions of management based on information available to us at the time such statements are made. These statements, which are generally identifiable by the use of the words “will,” “believe,” “expect,” “intend,” “anticipate,” “estimate,” “forecast,” “project,” “plan,” and similar expressions, are subject to certain risks and uncertainties, are made as of the date hereof, and we undertake no duty or obligation to update them. Because actual results may differ materially from those suggested or implied by such forward-looking statements, you should not place undue reliance on them when deciding whether to buy, sell or hold the company’s securities.

Our outlook is based on certain assumptions, which we believe to be reasonable under the circumstances. These include, without limitation, assumptions regarding the impact of the COVID-19 pandemic and the war in Ukraine; changes in the competitive landscape, including ongoing uncertainties in the traditional office products channels; as well as the impact of inflation, fluctuations in foreign currency exchange rates and acquisitions and the other factors described below.

Among the factors that could cause our actual results to differ materially from our forward-looking statements are: our ability to improve profitability and free cash flow in the near-term by curtailing hiring, reducing inventory and limiting discretionary spending and capital expenditures; our ability to obtain additional price increases and realize longer-term cost reductions; the ongoing impact of the COVID-19 pandemic; a relatively limited number of large customers account for a significant percentage of our sales; issues that influence customer and consumer discretionary spending during periods of economic uncertainty or weakness; risks associated with foreign currency exchange rate fluctuations; challenges related to the highly competitive business environment in which we operate; our ability to develop and market innovative products that meet consumer demands and to expand into new and adjacent product categories that are experiencing higher growth rates; our ability to successfully expand our business in emerging markets and the exposure to greater financial, operational, regulatory, compliance and other risks in such markets; the continued decline in the use of certain of our products; risks associated with seasonality; the sufficiency of investment returns on pension assets, risks related to actuarial assumptions, changes in government regulations and changes in the unfunded liabilities of a multi-employer pension plan; any impairment of our intangible assets; our ability to secure, protect and maintain our intellectual property rights, and our ability to license rights from major gaming console makers and video game publishers to support our gaming business; continued disruptions in the global supply chain; risks associated with changes in the cost or availability of raw materials, transportation, labor, and other necessary supplies and services and the cost of finished goods; the continued global shortage of microchips which are needed in our gaming and computer accessories businesses; risks associated with outsourcing production of certain of our products, information technology systems and other administrative functions; the failure, inadequacy or interruption of our information technology systems or its supporting infrastructure; risks associated with a cybersecurity incident or information security breach, including that related to a disclosure of personally identifiable information; our ability to grow profitably through acquisitions; our ability to successfully integrate acquisitions and achieve the financial and other results anticipated at the time of acquisition, including planned synergies; risks associated with our indebtedness, including limitations imposed by restrictive covenants, our debt service obligations, and our ability to comply with financial ratios and tests; a change in or discontinuance of our stock repurchase program or the payment of dividends; product liability claims, recalls or regulatory actions; the impact of litigation or other legal proceedings; our failure to comply with applicable laws, rules and regulations and self-regulatory requirements, the costs of compliance and the impact of changes in such laws; our ability to attract and retain qualified personnel; the volatility of our stock price; risks associated with circumstances outside our control, including those caused by public health crises, such as the occurrence of contagious diseases like COVID-19, severe weather events, war, terrorism and other geopolitical incidents; and other risks and uncertainties described in “Part I, Item 1A. Risk Factors” in our Annual Report on Form 10-K for the year ended December 31, 2021, and in other reports we file with the Securities and Exchange Commission

About Non-GAAP Financial Measures

We use our non-GAAP financial measures both to explain our results to stockholders and the investment community and in the internal evaluation and management of our business. We believe our non-GAAP financial measures provide management and investors with a more complete understanding of our underlying operational results and trends, facilitate meaningful period-to-period comparisons and enhance an overall understanding of our past and future financial performance.

Our non-GAAP financial measures exclude certain items that may have a material impact upon our reported financial results such as restructuring charges, transaction and integration expenses associated with material acquisitions, the impact of foreign currency exchange rate fluctuations and acquisitions, unusual tax items and other non-recurring items that we consider to be outside of our core operations. These measures should not be considered in isolation or as a substitute for, or superior to, the directly comparable GAAP financial measures.

Our non-GAAP financial measures include the following:

Comparable Sales: Represents net sales excluding the impact of material acquisitions with current-period foreign operation sales translated at prior-year currency rates. We believe comparable sales are useful to investors and management because it reflects underlying sales and sales trends without the effect of acquisitions and fluctuations in foreign currency exchange rates and facilitate meaningful period-to-period comparisons. We sometimes refer to comparable sales as comparable net sales.

Adjusted EPS :Represents net income per diluted share excluding restructuring charges, the amortization of intangibles, the amortization of the step-up in value of inventory, the change in fair value of contingent consideration, transaction and integration expenses associated with material acquisitions, non-recurring items in interest expense or other income/expense such as expenses associated with debt refinancing, a bond redemption, or a pension curtailment, and other non-recurring items as well as all unusual and discrete income tax adjustments, including income tax related to the foregoing. We believe adjusted EPS is useful to investors and management because it reflects our underlying operating performance before items that we consider to be outside our core operations and facilitate meaningful period-to-period comparisons. Senior management’s incentive compensation is derived, in part, using adjusted EPS. We sometimes refer to adjusted EPS as adjusted earnings per share or adjusted net income per diluted share.

Free Cash Flow:Represents cash flow from operating activities, excluding cash payments made for contingent earnouts, less cash used for additions to property, plant and equipment, plus cash proceeds from the disposition of assets. We believe free cash flow is useful to investors because it measures our available cash flow for paying dividends, funding strategic material acquisitions, reducing debt, and repurchasing shares.

This press release also provides forward-looking non-GAAP comparable net sales, adjusted earnings per share, and free cash flow. We do not provide a reconciliation of forward-looking comparable net sales, adjusted EPS or free cash flow to GAAP because the GAAP financial measure is not currently available and management cannot reliably predict all of the necessary components of such non-GAAP measures without unreasonable effort or expense due to the inherent difficulty of forecasting and quantifying certain amounts that are necessary for such a reconciliation, including adjustments that could be made for restructuring, integration and acquisition-related expenses, the variability of our tax rate, foreign currency exchange rate fluctuations and material acquisitions, and other items reflected in our historical results. The probable significance of each of these items is high and, based on historical experience, could be material.

Christopher McGinnis Investor Relations (847) 796-4320