FLORHAM PARK, N.J., Oct. 31, 2022 (GLOBE NEWSWIRE) — PDS Biotechnology Corporation (Nasdaq: PDSB), a clinical-stage immunotherapy company developing a growing pipeline of targeted immunotherapies for cancer and infectious disease, today announced that the Company will release financial results for the third quarter of 2022 on Monday, November 14, 2022, before the market opens. Following the release, management will host a conference call to review the financial results and provide a business update.

After the live webcast, the event will be archived on PDS Biotech’s website for six months.

About PDS Biotechnology PDS Biotech is a clinical-stage immunotherapy company developing a growing pipeline of targeted cancer and infectious disease immunotherapies based on our proprietary Versamune® and Infectimune™ T cell-activating technology platforms. We believe our targeted Versamune® based candidates have the potential to overcome the limitations of current immunotherapy by inducing large quantities of high-quality, potent polyfunctional tumor specific CD4+ helper and CD8+ killer T cells. To date, our lead Versamune® clinical candidate, PDS0101, has demonstrated the potential to reduce tumors and stabilize disease in combination with approved and investigational therapeutics in patients with a broad range of HPV-positive cancers in multiple Phase 2 clinical trials. Our Infectimune™ based vaccines have also demonstrated the potential to induce not only robust and durable neutralizing antibody responses, but also powerful T cell responses, including long-lasting memory T cell responses in pre-clinical studies to date. To learn more, please visit www.pdsbiotech.com or follow us on Twitter at @PDSBiotech.

Versamune® is a registered trademark and Infectimune™ is a trademark of PDS Biotechnology.

CARLSBAD, Calif.–(BUSINESS WIRE)–Oct. 31, 2022– Lineage Cell Therapeutics, Inc. (NYSE American and TASE: LCTX), a clinical-stage biotechnology company developing allogeneic cell therapies for unmet medical needs, announced today that Jill Howe will join as the Company’s Chief Financial Officer, effective November 14, 2022. Ms. Howe brings more than 20 years of significant strategic, financial, and operational experience to Lineage, with an emphasis on capital strategy, corporate finance, treasury management, global infrastructure, and operational excellence. Ms. Howe has successfully built biotechnology organizations and implemented operational infrastructures alongside the execution of over $1.66 billion of capital raising transactions and will bring extensive strategic experience to the role. Most recently, Ms. Howe was Chief Financial Officer of DTx Pharma, and prior to that, was Vice President of Finance and Treasurer at Gossamer Bio, Inc., serving an integral role in the company’s initial public offering (IPO) and concurrent listing on the Nasdaq Global Select Market, various follow-on and debt deals, and overseeing all aspects of finance and accounting operations globally.

“Jill is a wonderful addition to our executive team as we work to establish Lineage as a leader in cell therapy and cell transplant medicine,” stated Brian M. Culley, Lineage CEO. “She is a successful executive with an extensive track record of execution in capital raising, strategic financial management, global expansion, and support, as well as mergers & acquisitions, and reflects the newest expansion of our team. Our continued growth will allow Lineage to exhibit greater productivity and increase the breadth of what we are able to accomplish in the months and years ahead.”

Ms. Howe most recently served as Chief Financial Officer of DTx Pharma, a biotechnology company creating novel RNA-based therapeutics to treat the genetic drivers of disease. From 2018 to 2021, she served as Vice President of Finance and Treasurer for Gossamer Bio, Inc. (NASDAQ: GOSS), a clinical-stage biopharmaceutical company focused on discovering, acquiring, developing and commercializing therapeutics in the disease areas of immunology, inflammation and oncology, where she managed all aspects of finance operations, accounting, and global IT and real estate efforts, including the building-out of world-class labs and office space. She also served as a Board member of all Irish and Luxembourg subsidiaries of Gossamer Bio. From 2016 through 2017 she served as Controller & Director of Finance at Amplyx Pharmaceuticals, Inc., a company dedicated to the development of therapies for debilitating and life-threatening diseases that affect people with compromised immune systems, which was subsequently acquired by Pfizer, Inc. From 2013 to 2016 she served as Controller & Director of Finance at Receptos, Inc. (NASDAQ: RCPT), which was subsequently acquired by Celgene, Inc. for more than $7 billion. Prior to that, from 2006 to 2013 she worked in various accounting roles, leading up to Director of Finance, at Somaxon Pharmaceuticals, Inc. (NASDAQ: SOMX), which was acquired by Pernix in 2012. Ms. Howe earned her Bachelor of Arts in Accounting from San Diego State University and serves on the Board of Directors of various nonprofit, private and public biotechnology companies. In 2022, Ms. Howe won the 2022 CFO of the Year Award in the small business category from the San Diego Business Journal and was specifically recognized for her leadership in building and managing successful financial teams, laying the groundwork for success, and as a San Diegan, for contributions to the community through her local charity work.

About Lineage Cell Therapeutics, Inc.

Lineage Cell Therapeutics is a clinical-stage biotechnology company developing novel cell therapies for unmet medical needs. Lineage’s programs are based on its robust proprietary cell-based therapy platform and associated in-house development and manufacturing capabilities. With this platform Lineage develops and manufactures specialized, terminally differentiated human cells from its pluripotent and progenitor cell starting materials. These differentiated cells are developed to either replace or support cells that are dysfunctional or absent due to degenerative disease or traumatic injury or administered as a means of helping the body mount an effective immune response to cancer. Lineage’s clinical programs are in markets with billion dollar opportunities and include five allogeneic (“off-the-shelf”) product candidates: (i) OpRegen, a retinal pigment epithelial cell therapy in development for the treatment of geographic atrophy secondary to age-related macular degeneration, is being developed under a worldwide collaboration with Roche and Genentech, a member of the Roche Group; (ii) OPC1, an oligodendrocyte progenitor cell therapy in Phase 1/2a development for the treatment of acute spinal cord injuries; (iii) VAC2, a dendritic cell therapy produced from Lineage’s VAC technology platform for immuno-oncology and infectious disease, currently in Phase 1 clinical development for the treatment of non-small cell lung cancer; (iv) ANP1, an auditory neuronal progenitor cell therapy for the potential treatment of auditory neuropathy; and (v) PNC1, a photoreceptor neural cell therapy for the treatment of vision loss due to photoreceptor dysfunction or damage. For more information, please visit www.lineagecell.com or follow the company on Twitter @LineageCell.

Forward-Looking Statements

Lineage cautions you that all statements, other than statements of historical facts, contained in this press release, are forward-looking statements. Forward-looking statements, in some cases, can be identified by terms such as “believe,” “aim,” “may,” “will,” “estimate,” “continue,” “anticipate,” “design,” “intend,” “expect,” “could,” “can,” “plan,” “potential,” “predict,” “seek,” “should,” “would,” “contemplate,” “project,” “target,” “tend to,” or the negative version of these words and similar expressions. Such statements include, but are not limited to, statements relating to: Ms. Howe’s employment with Lineage and the anticipated or implied benefits thereof to Lineage and Lineage’s continued growth and ability to exhibit greater productivity in the future. Forward-looking statements involve known and unknown risks, uncertainties and other factors that may cause Lineage’s actual results, performance or achievements to be materially different from future results, performance or achievements expressed or implied by the forward-looking statements in this press release, including, but not limited to, the risks and uncertainties inherent in Lineage’s business and other risks discussed in Lineage’s filings with the Securities and Exchange Commission (SEC). Lineage’s forward-looking statements are based upon its current expectations and involve assumptions that may never materialize or may prove to be incorrect. All forward-looking statements are expressly qualified in their entirety by these cautionary statements. Further information regarding these and other risks is included under the heading “Risk Factors” in Lineage’s periodic reports with the SEC, including Lineage’s most recent Annual Report on Form 10-K and Quarterly Report on Form 10-Q filed with the SEC and its other reports, which are available from the SEC’s website. You are cautioned not to place undue reliance on forward-looking statements, which speak only as of the date on which they were made. Lineage undertakes no obligation to update such statements to reflect events that occur or circumstances that exist after the date on which they were made, except as required by law.

CHATHAM, N.J., Oct. 31, 2022 (GLOBE NEWSWIRE) — Tonix Pharmaceuticals Holding Corp. (Nasdaq: TNXP), a clinical-stage biopharmaceutical company, announced today that Jessica Morris, Chief Operating Officer of Tonix Pharmaceuticals, will present at BioFuture on Tuesday, November 8, 2022, at 11:00 a.m. ET, and host investor meetings. The conference is being held at the Lotte New York Palace in New York City.

Investors interested in arranging a meeting with the Company’s management during the conference can register at the BioFuture website at www.biofuture.com. The presentation can be accessed via the conference’s virtual platform by registered conference attendees and will also be available under the Presentations tab of the Tonix website at www.tonixpharma.com.

Tonix Pharmaceuticals Holding Corp.*

Tonix is a clinical-stage biopharmaceutical company focused on discovering, licensing, acquiring and developing therapeutics to treat and prevent human disease and alleviate suffering. Tonix’s portfolio is composed of central nervous system (CNS), rare disease, immunology and infectious disease product candidates. Tonix’s CNS portfolio includes both small molecules and biologics to treat pain, neurologic, psychiatric and addiction conditions. Tonix’s lead CNS candidate, TNX-102 SL (cyclobenzaprine HCl sublingual tablet), is in mid-Phase 3 development for the management of fibromyalgia with a new Phase 3 study launched in the second quarter of 2022 and interim data expected in the second quarter of 2023. TNX-102 SL is also being developed to treat Long COVID, a chronic post-acute COVID-19 condition. Tonix initiated a Phase 2 study in Long COVID in the third quarter of 2022 and expects interim data in the second quarter of 2023. TNX-1300 (cocaine esterase) is a biologic designed to treat cocaine intoxication and has been granted Breakthrough Therapy designation by the FDA. A Phase 2 study of TNX-1300 is expected to be initiated in the first quarter of 2023. TNX-1900 (intranasal potentiated oxytocin), a small molecule in development for chronic migraine, is expected to enter the clinic with a Phase 2 study in the fourth quarter of 2022. TNX-601 ER (tianeptine hemioxalate extended-release tablets) is a once-daily formulation of tianeptine being developed as a potential treatment for major depressive disorder (MDD) with a Phase 2 study expected to be initiated in the first quarter of 2023. Tonix’s rare disease portfolio includes TNX-2900 (intranasal potentiated oxytocin) for the treatment of Prader-Willi syndrome. TNX-2900 has been granted Orphan Drug designation by the FDA. Tonix’s immunology portfolio includes biologics to address organ transplant rejection, autoimmunity and cancer, including TNX-1500, which is a humanized monoclonal antibody targeting CD40-ligand (CD40L or CD154) being developed for the prevention of allograft and xenograft rejection and for the treatment of autoimmune diseases. A Phase 1 study of TNX-1500 is expected to be initiated in the first half of 2023. Tonix’s infectious disease pipeline consists of a vaccine in development to prevent smallpox and monkeypox, next-generation vaccines to prevent COVID-19, and a platform to make fully human monoclonal antibodies to treat COVID-19. TNX-801, Tonix’s vaccine in development to prevent smallpox and monkeypox, also serves as the live virus vaccine platform or recombinant pox vaccine (RPV) platform for other infectious diseases. A Phase 1 study of TNX-801 is expected to be initiated in Kenya in the first half of 2023. Tonix’s lead vaccine candidate for COVID-19 is TNX-1850, a live virus vaccines based on Tonix’s recombinant pox live virus vector vaccine platform.

*All of Tonix’s product candidates are investigational new drugs or biologics and have not been approved for any indication.

This press release and further information about Tonix can be found at www.tonixpharma.com.

Forward Looking Statements

Certain statements in this press release are forward-looking within the meaning of the Private Securities Litigation Reform Act of 1995. These statements may be identified by the use of forward-looking words such as “anticipate,” “believe,” “forecast,” “estimate,” “expect,” and “intend,” among others. These forward-looking statements are based on Tonix’s current expectations and actual results could differ materially. There are a number of factors that could cause actual events to differ materially from those indicated by such forward-looking statements. These factors include, but are not limited to, risks related to the failure to obtain FDA clearances or approvals and noncompliance with FDA regulations; delays and uncertainties caused by the global COVID-19 pandemic; risks related to the timing and progress of clinical development of our product candidates; our need for additional financing; uncertainties of patent protection and litigation; uncertainties of government or third party payor reimbursement; limited research and development efforts and dependence upon third parties; and substantial competition. As with any pharmaceutical under development, there are significant risks in the development, regulatory approval and commercialization of new products. Tonix does not undertake an obligation to update or revise any forward-looking statement. Investors should read the risk factors set forth in the Annual Report on Form 10-K for the year ended December 31, 2021, as filed with the Securities and Exchange Commission (the “SEC”) on March 14, 2022, and periodic reports filed with the SEC on or after the date thereof. All of Tonix’s forward-looking statements are expressly qualified by all such risk factors and other cautionary statements. The information set forth herein speaks only as of the date thereof.

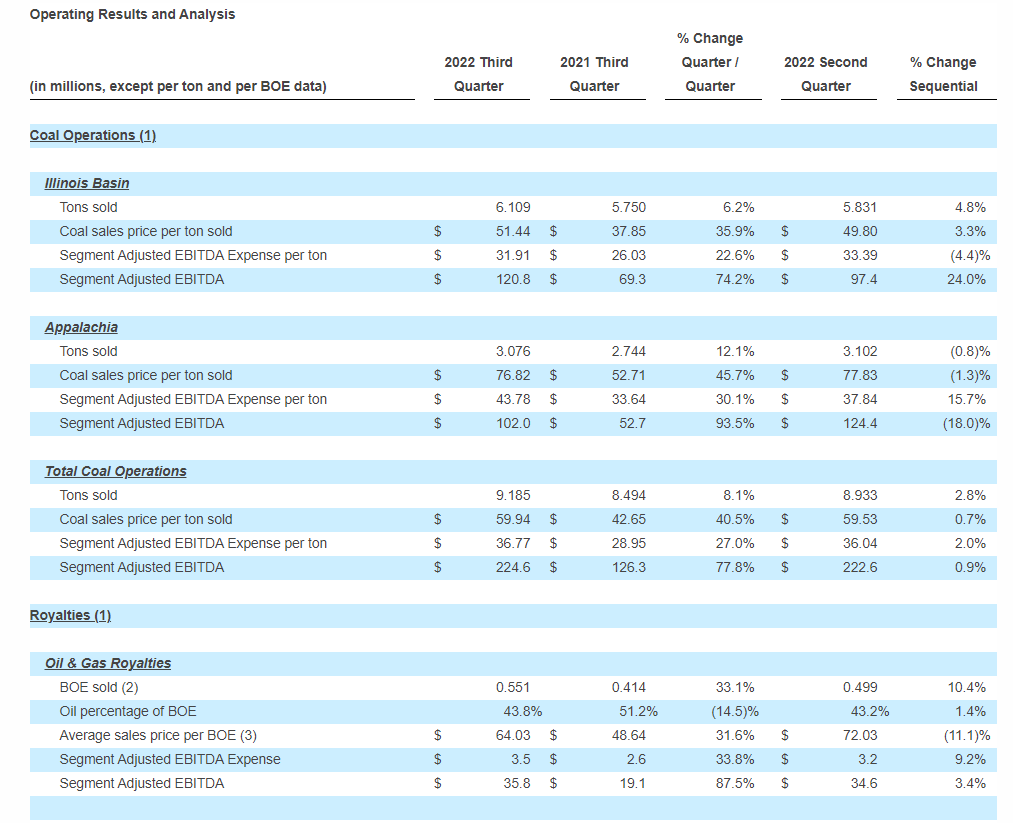

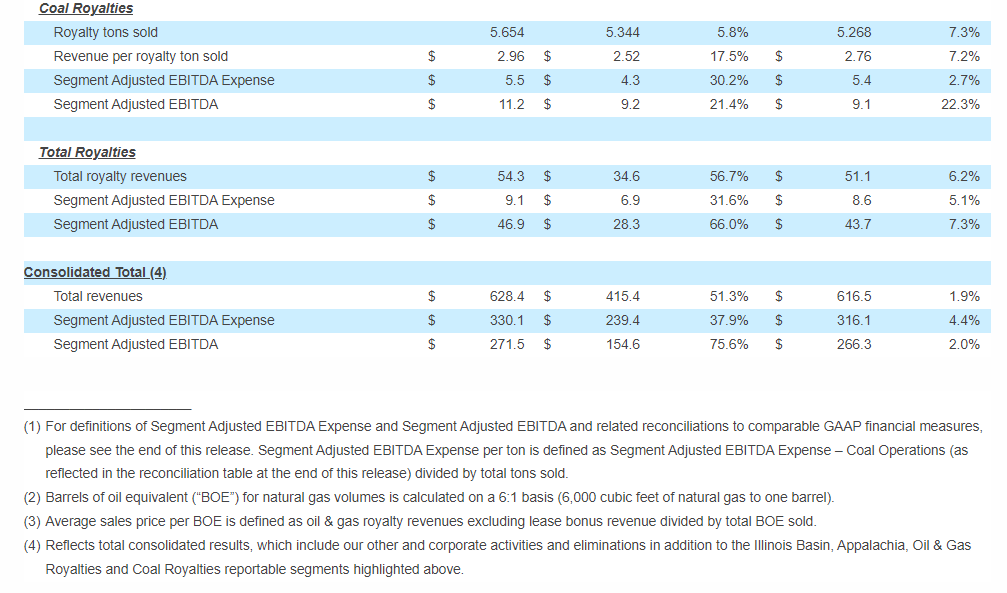

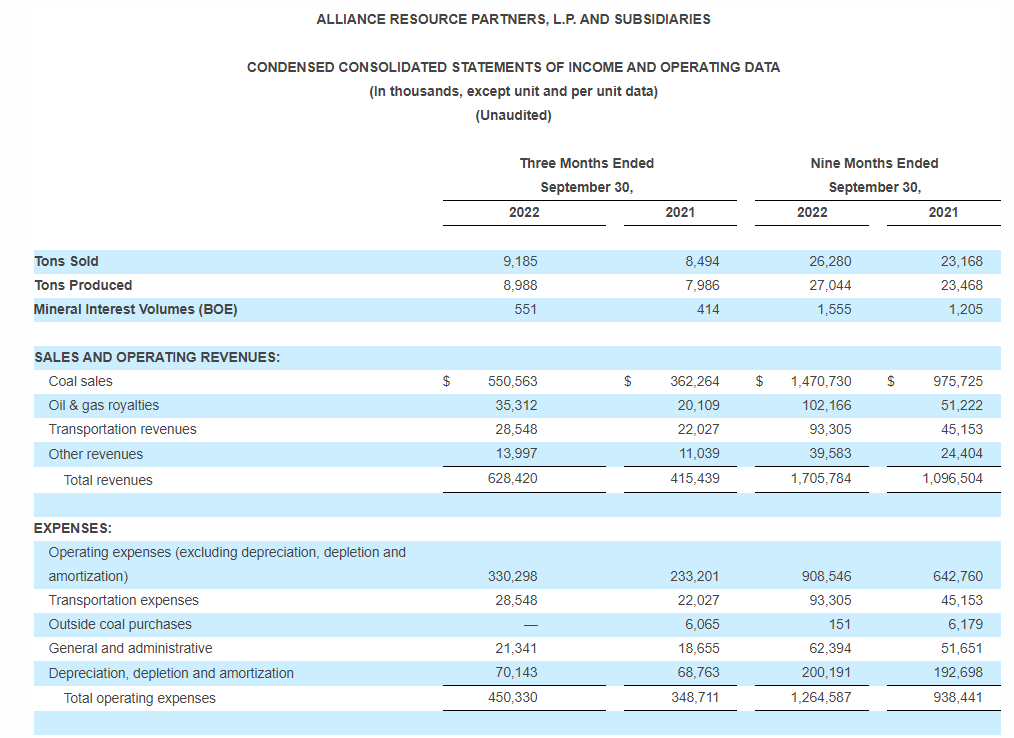

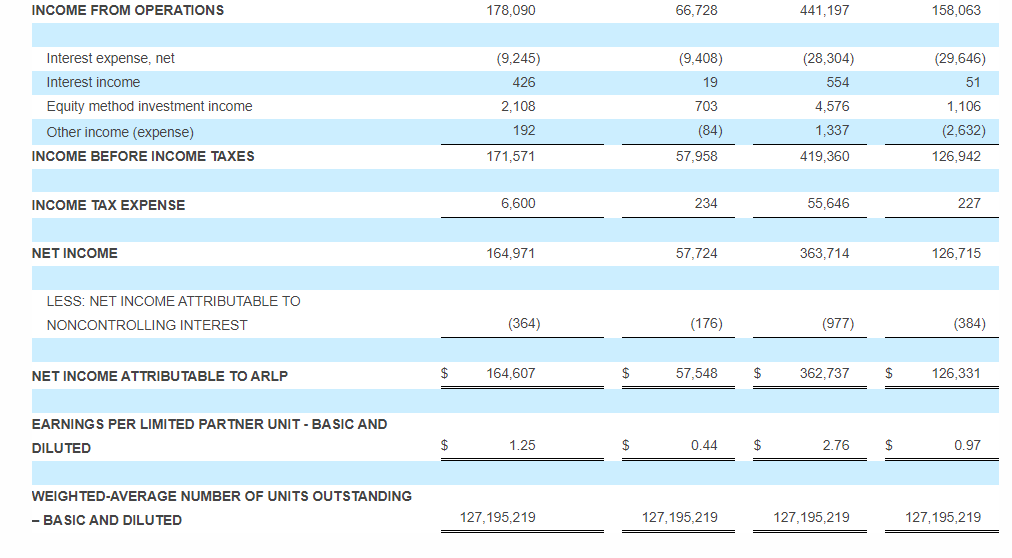

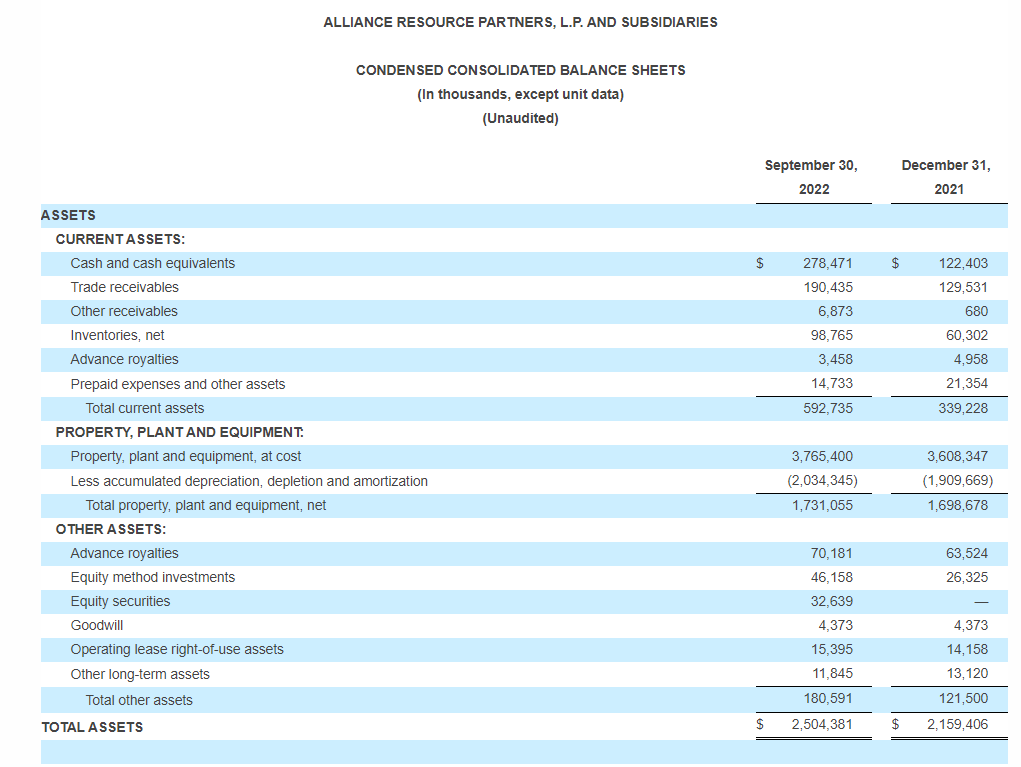

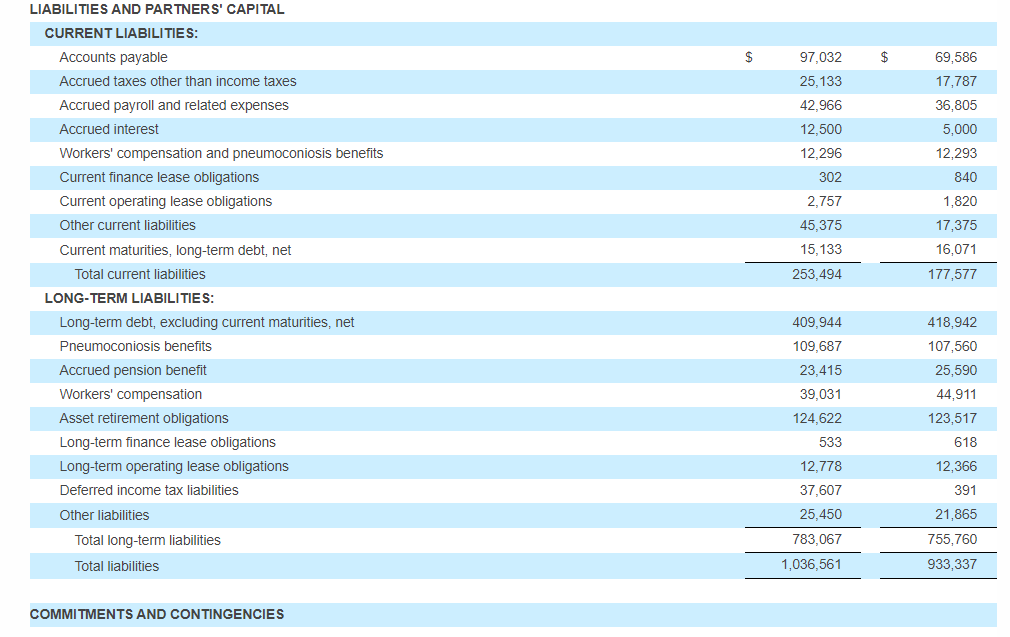

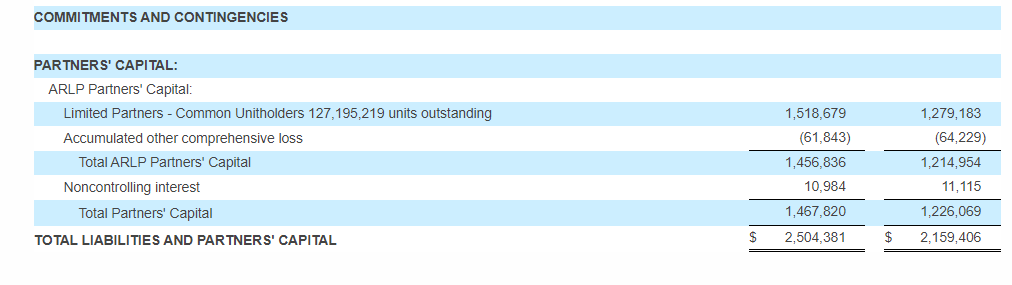

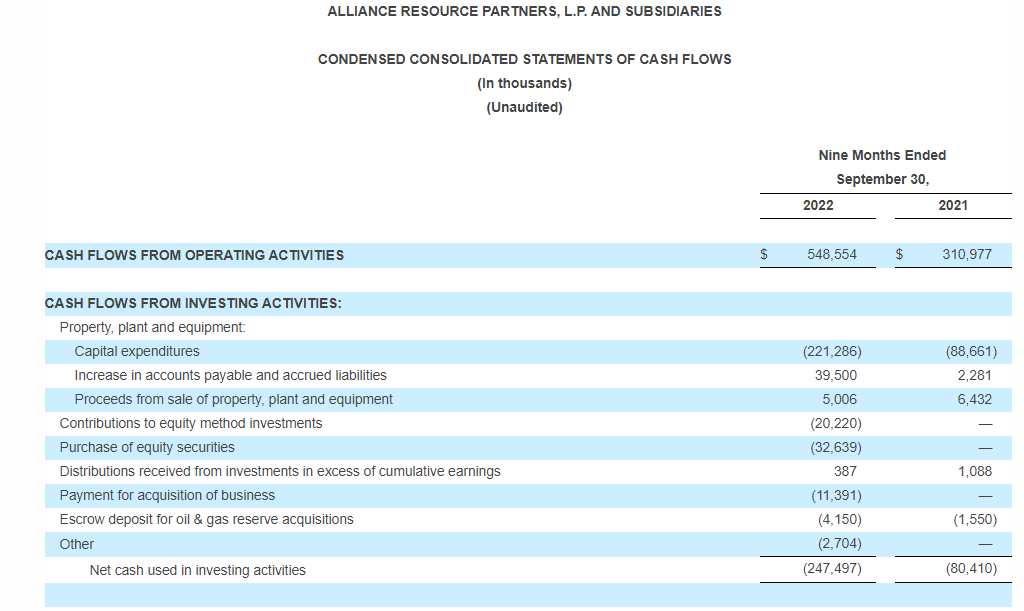

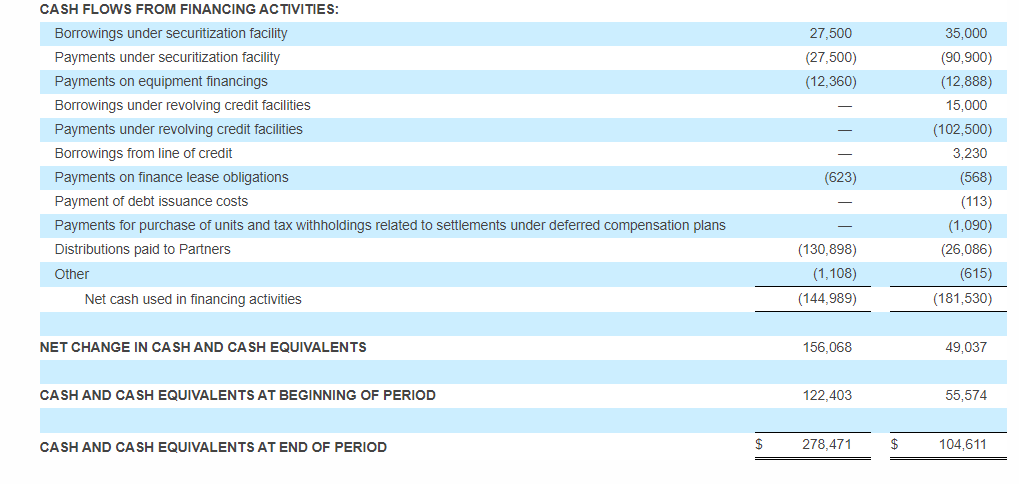

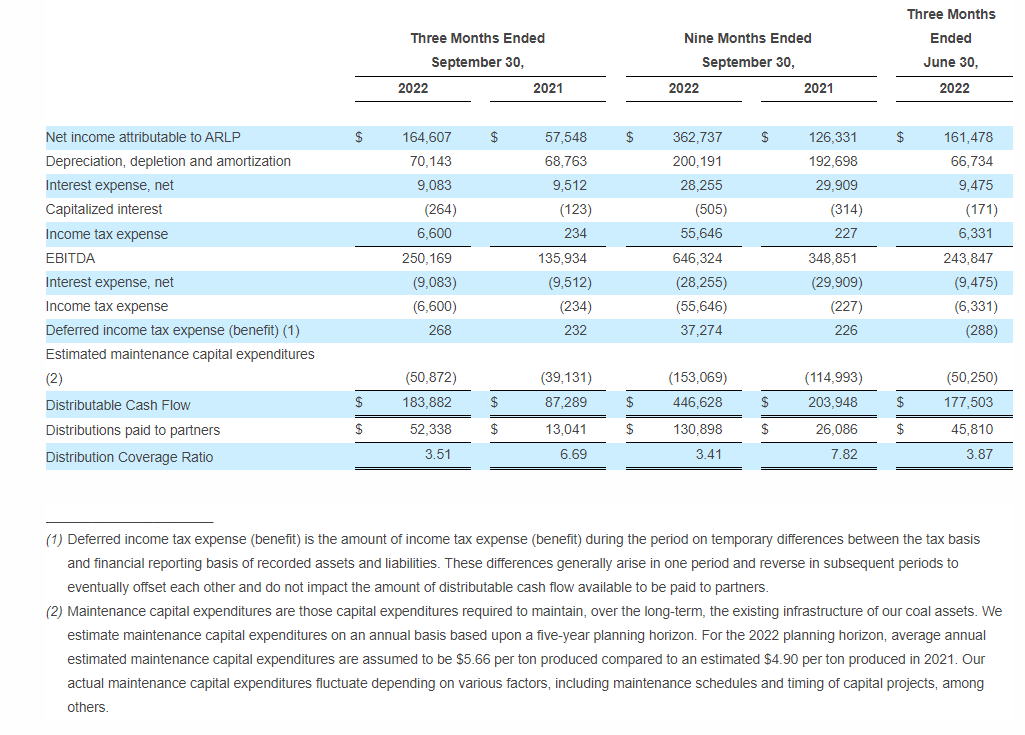

TULSA, Okla.–(BUSINESS WIRE)– Alliance Resource Partners, L.P. (NASDAQ: ARLP) today reported substantial increases to financial and operating results for the quarter ended September 30, 2022 (the “2022 Quarter”) compared to the quarter ended September 30, 2021 (the “2021 Quarter”). Total revenues in the 2022 Quarter increased 51.3% to a record $628.4 million compared to $415.4 million for the 2021 Quarter as a result of significantly higher coal sales revenues, which rose $188.3 million to $550.6 million, and oil & gas royalties revenues, which jumped 75.6% to $35.3 million. Coal sales revenues increased on the strength of record coal sales prices, which rose 40.5% in the 2022 Quarter to $59.94 per ton sold, and increased coal sales volumes, which were 8.1% higher compared to the 2021 Quarter. Oil & gas royalties revenue in the 2022 Quarter benefited from significantly higher volumes and sales price realizations per BOE, which increased 33.1% and 31.6%, respectively, compared to the 2021 Quarter. Total operating expenses increased to $450.3 million in the 2022 Quarter, compared to $348.7 million in the 2021 Quarter, due primarily to increased coal sales volumes and ongoing inflationary cost pressures. Net income for the 2022 Quarter increased 186.0% to $164.6 million, or $1.25 per basic and diluted limited partner unit, compared to $57.5 million, or $0.44 per basic and diluted limited partner unit, for the 2021 Quarter. EBITDA also increased 84.0% in the 2022 Quarter to $250.2 million compared to $135.9 million in the 2021 Quarter. (Unless otherwise noted, all references in the text of this release to “net income” refer to “net income attributable to ARLP.” For a definition of EBITDA and related reconciliation to its comparable GAAP financial measure throughout this release, please see the end of this release.)

Performance in the 2022 Quarter also improved compared to the quarter ended June 30, 2022 (the “Sequential Quarter”) as modest increases to coal sales volumes and pricing pushed both coal sales and total revenues higher by 3.5% and 1.9%, respectively. Increased revenues, partially offset by higher total operating expenses in the 2022 Quarter, led net income and EBITDA higher by 1.9% and 2.6%, respectively, both as compared to the Sequential Quarter.

Total revenues increased 55.6% to $1.71 billion for the nine months ended September 30, 2022 (the “2022 Period”), compared to $1.10 billion for the nine months ended September 30, 2021 (the “2021 Period”), primarily due to substantial increases in prices and volumes from both coal and oil & gas royalties. Higher revenues, partially offset by increased total operating and income tax expenses, led to significantly higher net income, which rose 187.1% to $362.7 million for the 2022 Period, or $2.76 per basic and diluted limited partner unit, compared to $126.3 million, or $0.97 per basic and diluted limited partner unit, for the 2021 Period. EBITDA increased 85.3% in the 2022 Period to $646.3 million compared to $348.9 million in the 2021 Period.

As previously announced on October 28, 2022, the Board of Directors of ARLP’s general partner (the “Board”) increased the cash distribution to unitholders for the 2022 Quarter to $0.50 per unit (an annualized rate of $2.00 per unit), payable on November 14, 2022, to all unitholders of record as of the close of trading on November 7, 2022. The announced distribution represents a 150.0% increase over the cash distribution of $0.20 per unit for the 2021 Quarter and a 25.0% increase over the cash distribution of $0.40 per unit for the Sequential Quarter.

“With energy market fundamentals remaining favorable during the 2022 Quarter, ARLP again delivered strong financial and operating performance, as we posted record quarterly total revenues and income from operations as well as significant increases to net income and EBITDA compared to the 2021 Quarter,” said Joseph W. Craft III, Chairman, President and Chief Executive Officer. “Higher coal sales and production volumes combined with record per ton price realizations drove our total Coal Segment Adjusted EBITDA up 77.8% to $224.6 million as margins per ton sold jumped $9.58 compared to the 2021 Quarter. Strong energy markets also continued to benefit our royalty businesses as increased volumes and commodity price realizations led to increased total royalty revenue and record Segment Adjusted EBITDA during the 2022 Quarter.”

Mr. Craft added, “ARLP was also able to execute new coal sales commitments for delivery of 5.6 million tons through 2025 at prices supporting higher margins in the future. With ARLP sold out for this year and solid contracted coal sales volumes in 2023 and 2024, we have good visibility into our ability to generate cash flow growth over the next several years. Reflecting our strong year-to-date performance and future expectations, ARLP’s Board elected to accelerate our previously planned increases to cash distributions to unitholders by declaring a $0.50 per unit distribution for the 2022 Quarter, as communicated last week.”

ARLP’s coal sales prices per ton increased significantly in both the Illinois Basin and Appalachia compared to the 2021 Quarter as improved price realizations in both the domestic and export markets drove coal sales prices higher by 35.9% and 45.7% in the Illinois Basin and Appalachia, respectively. Compared to the Sequential Quarter, coal sales price realizations improved as well. Increased domestic sales volumes drove coal sales volumes higher by 6.2% and 12.1% in the Illinois Basin and Appalachia, respectively, compared to the 2021 Quarter. Compared to the Sequential Quarter, Illinois Basin coal sales volumes increased 4.8% as a result of higher sales volumes at our Gibson South and Hamilton mines while coal sales volumes in Appalachia remained relatively consistent. ARLP ended the 2022 Quarter with total coal inventory of 1.4 million tons, representing an increase of 0.4 million tons compared to the end of the 2021 Quarter and a decrease of 0.2 million tons compared to the end of the Sequential Quarter.

Segment Adjusted EBITDA Expense per ton increased by 22.6% and 30.1% in the Illinois Basin and Appalachia, respectively, compared to the 2021 Quarter primarily as a result of ongoing inflationary pressures on numerous expense items, most notably labor-related expenses, supply and maintenance costs as well as increased sales-related expenses due to higher price realizations. Longwall moves at our Hamilton and Tunnel Ridge mines during the 2022 Quarter also contributed to higher per ton expenses compared to the 2021 Quarter. Compared to the Sequential Quarter, Segment Adjusted EBITDA Expense per ton in the Illinois Basin decreased 4.4% in the 2022 Quarter due to increased sales volumes, lower roof support expenses, higher recoveries at our Gibson South and Hamilton mines and a $6.5 million non-cash contingent accrual recorded in the Sequential Quarter related to our 2015 purchase of the Hamilton mine. These decreases were partially offset by an extended longwall move at our Hamilton mine during the 2022 Quarter. In Appalachia, Segment Adjusted EBITDA Expense per ton increased 15.7% compared to the Sequential Quarter as a result of adverse mining conditions and preparation plant maintenance improvements at MC Mining, higher labor-related expenses and supply costs as well as a longwall move at our Tunnel Ridge mine in the 2022 Quarter. These increases were partially offset by lower sales-related expenses due to decreased price realizations and increased recoveries at our Mettiki and Tunnel Ridge mines.

Our Oil & Gas Royalties segment had significantly higher volumes and sales price realizations per BOE in the 2022 Quarter which drove Segment Adjusted EBITDA higher by 87.5% to a record $35.8 million compared to $19.1 million for the 2021 Quarter. Compared to the Sequential Quarter, Segment Adjusted EBITDA increased by 3.4% in the 2022 Quarter primarily due to higher oil & gas volumes, which rose by 10.4%, partially offset by lower price realizations, which decreased by 11.1%.

Segment Adjusted EBITDA for our Coal Royalties segment increased to $11.2 million, representing increases of 21.4% and 22.3% compared the 2021 and Sequential Quarters, respectively, as a result of increased royalty tons sold and higher average royalty rates per ton.

Outlook

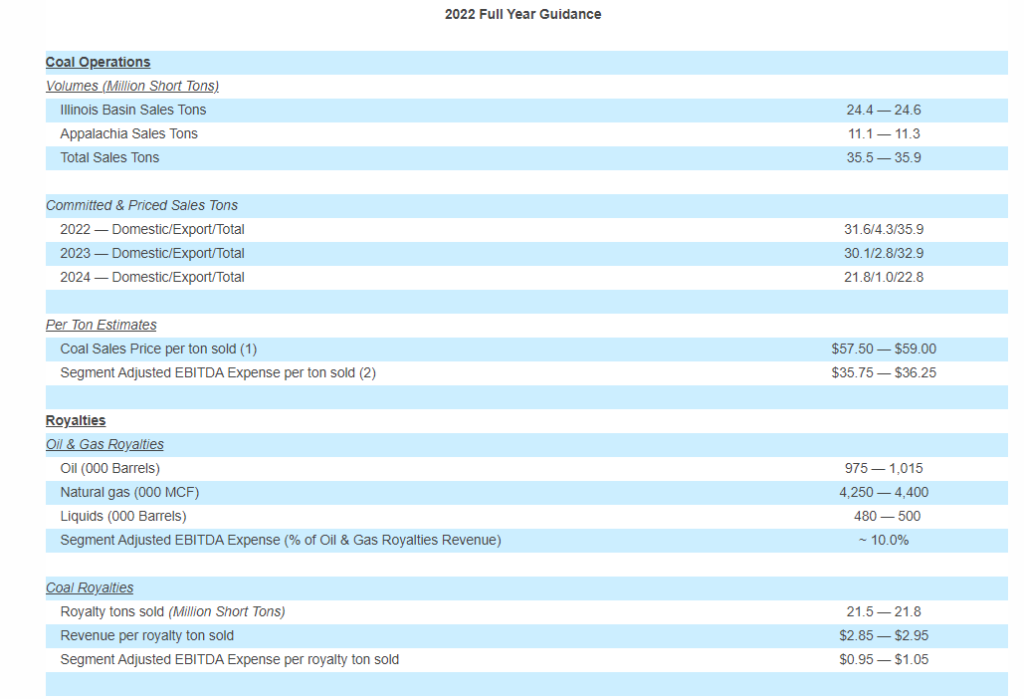

“Assisted by the supply driven energy crisis the world has experienced this year, ARLP is on track to achieve record financial results in 2022,” said Mr. Craft. “Since we have not seen a meaningful supply response, we expect the global energy markets will continue to be favorable for the foreseeable future. Based upon this view and our current contracted coal sales volumes, we expect to add up to two million tons of Illinois basin production next year giving us confidence our Partnership’s 2023 financial results will grow beyond this year’s record performance. In the near term, inflation pressures and continuing transportation challenges are the most significant issues our coal operations and marketing teams are managing. Rail performance has recently improved but low water levels and lock outages have impacted both exports destined for the U.S. Gulf and domestic barge traffic. These potential shipping delays may lead us to defer some of this year’s contracted tons into early next year. We have therefore adjusted our expectations for 2022 coal sales volumes, prices and costs as noted in the updated guidance table below. Our oil & gas royalties segment continues to benefit from increased drilling and completion activity by operators on our acreage and we have adjusted volume expectations accordingly.”

Mr. Craft continued, “Since our last earnings call in July, ARLP continued to invest for future growth. In keeping with our objective of reinvesting cash flows generated by our oil & gas royalty segment, we recently closed two transactions totaling $94.5 million to acquire an additional 4,322 net oil & gas royalty acres in the Permian Basin. There are currently 1,200 producing wells, 101 wells to be completed and 98 permitted locations on the acquired acreage, providing ARLP with line of sight to future oil & gas production growth. To enhance our long-lived, efficient mining operations and to maximize cash flow from our existing coal assets, we recently committed to access a resource area containing approximately 110 million tons adjacent to our River View mine allowing us to produce from a more productive, higher yield coal seam area and capture the opportunity to fully utilize existing infrastructure at this operation. In addition, during the 2022 Quarter, we added 69 million tons of lower cost, lower sulfur coal adjacent to our low-cost Tunnel Ridge longwall mine. We expect both of these investments will payout on cost savings alone and also give us the opportunity to add tons beyond 2024 to meet market demand, if available. Finally, ARLP recently elected to hold its commitment to Francis Energy at its initial $20 million convertible note investment. We remain interested in the EV infrastructure market and continue to evaluate opportunities in the industry to create value potential for ARLP.”

Mr. Craft concluded, “These are exciting times for ARLP. We believe our current core businesses are well positioned to deliver significant cash flows for some time to come, allowing ARLP to provide attractive cash returns to unitholders, effectively manage our balance sheet and invest in new opportunities to create long-term value for all of our stakeholders.”

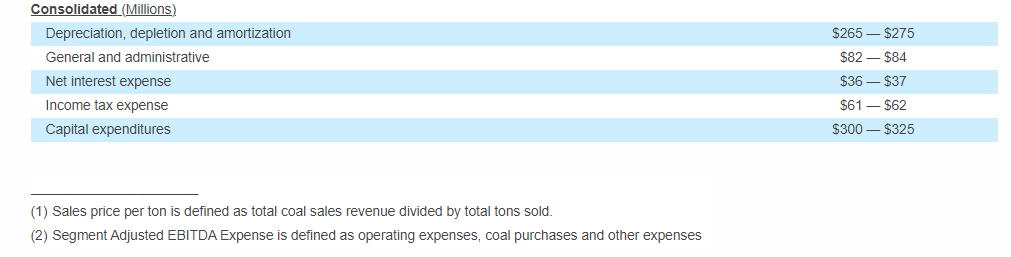

ARLP’s updated full year 2022 guidance is outlined below:

A conference call regarding ARLP’s 2022 Quarter financial results is scheduled for today at 10:00 a.m. Eastern. To participate in the conference call, dial (877) 407-0784 and request to be connected to the Alliance Resource Partners, L.P. earnings conference call. International callers should dial (201) 689-8560 and request to be connected to the same call. Investors may also listen to the call via the “investor relations” section of ARLP’s website at http://www.arlp.com.

An audio replay of the conference call will be available for approximately one week. To access the audio replay, dial U.S. Toll Free (844) 512-2921; International Toll (412) 317-6671 and request to be connected to replay using access code 13733069.

About Alliance Resource Partners, L.P.

ARLP is a diversified energy company that is currently the largest coal producer in the eastern United States. ARLP also generates operating and royalty income from mineral interests it owns in strategic coal and oil & gas producing regions in the United States. In addition, ARLP is positioning itself as an energy provider for the future by leveraging its core technology and operating competencies to make strategic investments in the fast-growing energy and infrastructure transition.

News, unit prices and additional information about ARLP, including filings with the Securities and Exchange Commission (“SEC”), are available at http://www.arlp.com. For more information, contact the investor relations department of ARLP at (918) 295-7674 or via e-mail at investorrelations@arlp.com.

The statements and projections used throughout this release are based on current expectations. These statements and projections are forward-looking, and actual results may differ materially. These projections do not include the potential impact of any mergers, acquisitions or other business combinations that may occur after the date of this release. We have included more information below regarding business risks that could affect our results.

FORWARD-LOOKING STATEMENTS: With the exception of historical matters, any matters discussed in this press release are forward-looking statements that involve risks and uncertainties that could cause actual results to differ materially from projected results. Those forward-looking statements include expectations with respect to our future financial performance, coal and oil & gas consumption and expected future prices, our ability to increase unitholder distributions in future quarters, business plans and potential growth with respect to our energy and infrastructure transition investments, optimizing cash flows, reducing operating and capital expenditures, preserving liquidity and maintaining financial flexibility, among others. These risks to our ability to achieve these outcomes include, but are not limited to, the following: the outcome or escalation of current hostilities in Ukraine, the severity, magnitude, and duration of the COVID-19 pandemic and the emergence of new virus variants, including impacts of the pandemic and of businesses’ and governments’ responses to the pandemic, including actions to mitigate its impact and the development of treatments and vaccines, on our operations and personnel, and on demand for coal, oil, and natural gas, the financial condition of our customers and suppliers, available liquidity and capital sources and broader economic disruptions; changes in macroeconomic and market conditions and market volatility arising from hostilities in Ukraine, including inflation, changes in coal, oil, natural gas, and natural gas liquids prices, and the impact of such changes and volatility on our financial position; decline in the coal industry’s share of electricity generation, including as a result of environmental concerns related to coal mining and combustion and the cost and perceived benefits of other sources of electricity and fuels, such as oil & gas, nuclear energy, and renewable fuels; changes in global economic and geo-political conditions or in industries in which we or our customers operate; changes in coal prices and/or oil & gas prices, demand and availability which could affect our operating results and cash flows; actions of the major oil-producing countries with respect to oil production volumes and prices could have direct and indirect impacts over the near and long term on oil & gas exploration and production operations at the properties in which we hold mineral interests; changes in competition in domestic and international coal markets and our ability to respond to such changes; potential shut-ins of production by operators of the properties in which we hold mineral interests due to low oil, natural gas, and natural gas liquid prices or the lack of downstream demand or storage capacity; risks associated with the expansion of our operations and properties; our ability to identify and complete acquisitions; our ability to identify and invest in new energy and infrastructure transition ventures; the success of our development plans for our wholly owned subsidiary, MatrixDesign Group, LLC, and our investments in emerging infrastructure and technology companies; dependence on significant customer contracts, including renewing existing contracts upon expiration; adjustments made in price, volume, or terms to existing coal supply agreements; the effects of and changes in trade, monetary and fiscal policies and laws, including the interest rate policies of the Federal Reserve Board; the effects of and changes in taxes or tariffs and other trade measures adopted by the United States and foreign governments; legislation, regulations, and court decisions and interpretations thereof, both domestic and foreign, including those relating to the environment and the release of greenhouse gases, mining, miner health and safety, hydraulic fracturing, and health care; deregulation of the electric utility industry or the effects of any adverse change in the coal industry, electric utility industry, or general economic conditions; investors’ and other stakeholders’ increasing attention to environmental, social and governance matters; liquidity constraints, including those resulting from any future unavailability of financing; customer bankruptcies, cancellations or breaches to existing contracts, or other failures to perform; customer delays, failure to take coal under contracts or defaults in making payments; our productivity levels and margins earned on our coal sales; disruptions to oil & gas exploration and production operations at the properties in which we hold mineral interests; changes in equipment, raw material, service or labor costs or availability, including due to inflationary pressures; changes in our ability to recruit, hire and maintain labor, including as a result of the potential impact of government-imposed vaccine mandates; our ability to maintain satisfactory relations with our employees; increases in labor costs including costs of health insurance and taxes resulting from the Affordable Care Act, adverse changes in work rules, or cash payments or projections associated with workers’ compensation claims; increases in transportation costs and risk of transportation delays or interruptions; operational interruptions due to geologic, permitting, labor, weather, supply chain shortages of equipment or mine supplies, or other factors; risks associated with major mine-related accidents, mine fires, mine floods or other interruptions; results of litigation, including claims not yet asserted; foreign currency fluctuations that could adversely affect the competitiveness of our coal abroad; difficulty maintaining our surety bonds for mine reclamation as well as workers’ compensation and black lung benefits; difficulty in making accurate assumptions and projections regarding post-mine reclamation as well as pension, black lung benefits, and other post-retirement benefit liabilities; uncertainties in estimating and replacing our coal mineral reserves and resources; uncertainties in estimating and replacing our oil & gas reserves; uncertainties in the amount of oil & gas production due to the level of drilling and completion activity by the operators of our oil & gas properties; uncertainties in the future of the electric vehicle industry and the market for EV charging stations; the impact of current and potential changes to federal or state tax rules and regulations, including a loss or reduction of benefits from certain tax deductions and credits; difficulty obtaining commercial property insurance, and risks associated with our participation in the commercial insurance property program; evolving cybersecurity risks, such as those involving unauthorized access, denial-of-service attacks, malicious software, data privacy breaches by employees, insiders or others with authorized access, cyber or phishing-attacks, ransomware, malware, social engineering, physical breaches, or other actions; and difficulty in making accurate assumptions and projections regarding future revenues and costs associated with equity investments in companies we do not control.

Additional information concerning these and other factors can be found in ARLP’s public periodic filings with the SEC, including ARLP’s Annual Report on Form 10-K for the year ended December 31, 2021, filed on February 25, 2022 and amended on August 26, 2022, and ARLP’s Quarterly Reports on Form 10-Q for the quarters ended March 31, 2022 and June 30, 2022, filed on May 9, 2022 and August 8, 2022, respectively. Except as required by applicable securities laws, ARLP does not intend to update its forward-looking statements.

Reconciliation of GAAP “net income attributable to ARLP” to non-GAAP “EBITDA” and “Distributable Cash Flow” (in thousands).

EBITDA is defined as net income attributable to ARLP before net interest expense, income taxes and depreciation, depletion and amortization. Distributable cash flow (“DCF”) is defined as EBITDA excluding interest expense (before capitalized interest), interest income, income taxes and estimated maintenance capital expenditures. Distribution coverage ratio (“DCR”) is defined as DCF divided by distributions paid to partners.

Management believes that the presentation of such additional financial measures provides useful information to investors regarding our performance and results of operations because these measures, when used in conjunction with related GAAP financial measures, (i) provide additional information about our core operating performance and ability to generate and distribute cash flow, (ii) provide investors with the financial analytical framework upon which management bases financial, operational, compensation and planning decisions and (iii) present measurements that investors, rating agencies and debt holders have indicated are useful in assessing us and our results of operations.

EBITDA, DCF and DCR should not be considered as alternatives to net income attributable to ARLP, net income, income from operations, cash flows from operating activities or any other measure of financial performance presented in accordance with GAAP. EBITDA and DCF are not intended to represent cash flow and do not represent the measure of cash available for distribution. Our method of computing EBITDA, DCF and DCR may not be the same method used to compute similar measures reported by other companies, or EBITDA, DCF and DCR may be computed differently by us in different contexts (i.e. public reporting versus computation under financing agreements).

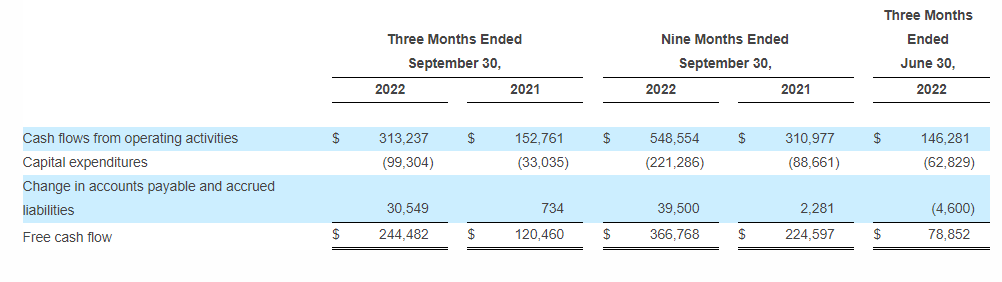

Reconciliation of GAAP “Cash flows from operating activities” to non-GAAP “Free cash flow” (in thousands).

Free cash flow is defined as cash flows from operating activities less capital expenditures and the change in accounts payable and accrued liabilities from purchases of property plant and equipment. Free cash flow should not be considered as an alternative to cash flows from operating activities or any other measure of financial performance presented in accordance with GAAP. Our method of computing free cash flow may not be the same method used by other companies. Free cash flow is a supplemental liquidity measure used by our management to assess our ability to generate excess cash flow from our operations.

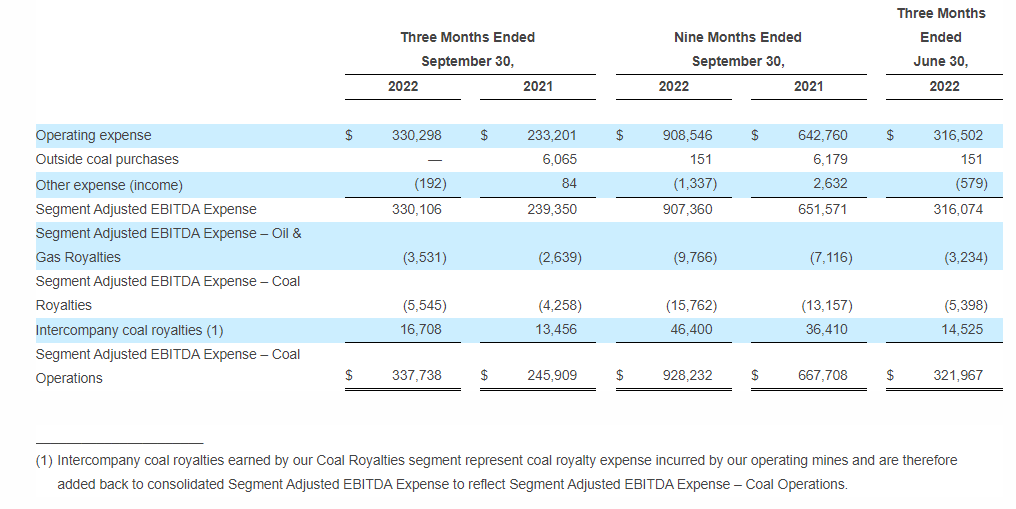

Reconciliation of GAAP “Operating Expenses” to non-GAAP “Segment Adjusted EBITDA Expense” and Reconciliation of non-GAAP ” EBITDA” to “Segment Adjusted EBITDA” (in thousands).

Segment Adjusted EBITDA Expense includes operating expenses, coal purchases and other expense. Transportation expenses are excluded as these expenses are passed through to our customers and, consequently, we do not realize any margin on transportation revenues. Segment Adjusted EBITDA Expense is used as a supplemental financial measure by our management to assess the operating performance of our segments. Segment Adjusted EBITDA Expense is a key component of EBITDA in addition to coal sales, royalty revenues and other revenues. The exclusion of corporate general and administrative expenses from Segment Adjusted EBITDA Expense allows management to focus solely on the evaluation of segment operating performance as it primarily relates to our operating expenses. Segment Adjusted EBITDA Expense – Coal Operations excludes expenses of our Oil & Gas Royalties segment and is adjusted for intercompany interactions with our Coal Royalties segment.

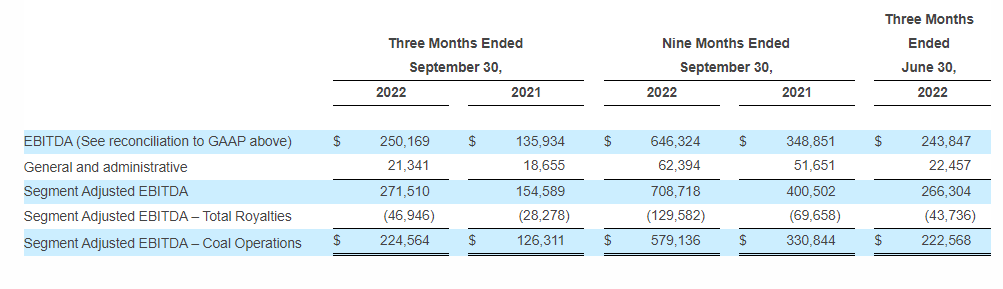

Segment Adjusted EBITDA is defined as net income attributable to ARLP before net interest expense, income taxes, depreciation, depletion and amortization and general and administrative expenses. Segment Adjusted EBITDA – Coal Operations excludes the contribution of our Oil & Gas and Coal Royalties segments to allow management to focus solely on the operating performance of our Illinois Basin and Appalachia segments.

Brian L. Cantrell Alliance Resource Partners, L.P. (918) 295-7673

TORONTO–(BUSINESS WIRE)– Sierra Metals Inc. (TSX: SMT) (BVL:SMT) (NYSE AMERICAN: SMTS) (“Sierra Metals” or “the Company”) confirms that it received an unsolicited, non-binding letter of intent (the “LOI”) following the close of business on October 27, 2022 from Compañia Minera Kolpa S.A. (“Kolpa”), among others.

The LOI outlines indicative terms for a proposed: (a) business combination of Kolpa and Sierra Metals; and (b) concurrent financing by an investment firm (collectively, the “Proposal”).

The LOI was submitted by Kolpa with its shareholders Arias Resource Capital Fund II L.P. and Arias Resource Capital Fund II (Mexico) L.P., among others. The LOI states that Arias Resource Capital Fund II L.P. and Arias Resource Capital Fund II (Mexico) L.P. and other members of the Arias Group (and principals) hold approximately 27% of the common shares of Sierra Metals.

As previously announced, a Special Committee of the independent members of Sierra Metals’ Board of Directors (the “Special Committee”) was formed with a mandate that includes exploring, reviewing and considering financing, restructuring and strategic options in the best interests of Sierra Metals.

The Special Committee is reviewing and considering the Proposal, with the assistance of financial and legal advisors to the Special Committee and to the Company. The Special Committee will consider the benefits of the Proposal to the Company and its stakeholders and all viable alternatives that may be or may become available to the Company. No decisions or recommendations have been made by the Special Committee regarding the transactions that are the subject of the Proposal at this time and the LOI has not been executed by the Company. Shareholders do not need to take any action with respect to the Proposal at this time.

The Company will continue to provide appropriate disclosure of any material developments as they arise.

About Sierra Metals

Sierra Metals is a diversified Canadian mining company with Green Metal exposure including copper production and base metal production with precious metals byproduct credits, focused on the production and development of its Yauricocha Mine in Peru, and Bolivar and Cusi Mines in Mexico. The Company is focused on increasing production volume and growing mineral resources. The Company also has large land packages at all three mines with several prospective regional targets providing longer-term exploration upside and mineral resource growth potential.

For further information regarding Sierra Metals, please visit www.sierrametals.com or contact:

This press release contains forward-looking information within the meaning of Canadian and United States securities legislation, including the course of action, if any, to be pursued in response to the Proposal. Forward-looking information relates to future events or the anticipated performance of Sierra Metals and reflect management’s expectations or beliefs regarding such future events and anticipated performance based on an assumed set of economic conditions and courses of action. In certain cases, statements that contain forward-looking information can be identified by the use of words such as “plans”, “expects”, “is expected”, “budget”, “scheduled”, “estimates”, “forecasts”, “intends”, “anticipates”, “believes” or variations of such words and phrases or statements that certain actions, events or results “may”, “could”, “would”, “might”, or “will be taken”, “occur” or “be achieved” or the negative of these words or comparable terminology. By its very nature forward-looking information involves known and unknown risks, uncertainness and other factors that may cause actual performance of Sierra Metals to be materially different from any anticipated performance expressed or implied by such forward-looking information. The Company has made certain assumptions regarding, among other things, the strategic alternatives that may be available to it. By its very nature forward-looking information involves known and unknown risks, uncertainties and other factors that may cause actual performance of Sierra Metals to be materially different from any anticipated performance expressed or implied by such forward-looking information.

Forward-looking information is subject to a variety of risks and uncertainties, which could cause actual events or results to differ from those reflected in the forward-looking information, including, without limitation, the risks described under the heading “Risk Factors” in the Company’s annual information form dated March 16, 2022 for its fiscal year ended December 31, 2021 and other risks identified in the Company’s filings with Canadian securities regulators and the United States Securities and Exchange Commission, which filings are available at www.sedar.com and www.sec.gov, respectively.

The risk factors referred to above are not an exhaustive list of the factors that may affect any of the Company’s forward-looking information. Forward-looking information includes statements about the future and is inherently uncertain, and the Company’s actual achievements or other future events or conditions may differ materially from those reflected in the forward-looking information due to a variety of risks, uncertainties and other factors. The Company’s statements containing forward-looking information are based on the beliefs, expectations, and opinions of management on the date the statements are made, and the Company does not assume any obligation to update such forward-looking information if circumstances or management’s beliefs, expectations or opinions should change, other than as required by applicable law. For the reasons set forth above, one should not place undue reliance on forward-looking information.

With more than 60 units, RCI Hospitality Holdings, Inc., through its subsidiaries, is the country’s leading company in adult nightclubs and sports bars/restaurants. Clubs in New York City, Chicago, Dallas-Fort Worth, Houston, Miami, Minneapolis, Denver, St. Louis, Charlotte, Pittsburgh, Raleigh, Louisville, and other markets operate under brand names such as Rick’s Cabaret, XTC, Club Onyx, Vivid Cabaret, Jaguars Club, Tootsie’s Cabaret, Scarlett’s Cabaret, Diamond Cabaret, and PT’s Showclub. Sports bars/restaurants operate under the brand name Bombshells Restaurant & Bar.

Joe Gomes, Senior Research Analyst, Noble Capital Markets, Inc.

Joshua Zoepfel, Research Associate, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

Keeps Getting Clubs. RCI Hospitality announced last week the acquisition of Heartbreakers Adult Nightclub for $9 million. The 5-stage, 23,000 square foot Heartbreakers club is located at 3200 Gulf Freeway, Dickinson, TX, and the Company acquired the club using $4.0 million in cash and $5.0 million in a 15-year, 6% real estate seller financing note. The Company did not release any financials for the club but we would expect the price to be within RCI’s 3-5x adjusted EBITDA for the club.

Area Around the Club. Dickinson, Texas had a population of 20,870 in 2020 according to Data USA with a median household income of $70,468. The median household income is a positive for RICK in our view as it is higher than the median income in the United States ($67,521), which we believe provides the Company with higher spending customers as the population has higher disposable income. The location of the club is also a positive due to it being near a freeway, which provides visibility to potential customers. Established in 1986, Heartbreakers is the number one adult entertainment venue in the Galveston, Texas, area.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

Joe Gomes, Senior Research Analyst, Noble Capital Markets, Inc.

Joshua Zoepfel, Research Associate, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

Why ORN? We believe the new management team, with its relevant industry experience, sees the robust end markets and opportunities to build the business, both organically and inorganically. We believe Orion is uniquely positioned to capitalize on the extraordinary market potential, both in the Marine sector and the Concrete business.

Near-term: Picking Low Hanging Fruit. While the new management team sets a course for the business, they are taking advantage of low hanging fruit to improve near-term operational results, such as continued improvement in contracts and reducing overhead burden.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

Cumulus Media (NASDAQ: CMLS) is an audio-first media company delivering premium content to over a quarter billion people every month — wherever and whenever they want it. Cumulus Media engages listeners with high-quality local programming through 406 owned-and-operated radio stations across 86 markets; delivers nationally-syndicated sports, news, talk, and entertainment programming from iconic brands including the NFL, the NCAA, the Masters, CNN, the AP, the Academy of Country Music Awards, and many other world-class partners across more than 9,500 affiliated stations through Westwood One, the largest audio network in America; and inspires listeners through the Cumulus Podcast Network, its rapidly growing network of original podcasts that are smart, entertaining and thought-provoking. Cumulus Media provides advertisers with personal connections, local impact and national reach through broadcast and on-demand digital, mobile, social, and voice-activated platforms, as well as integrated digital marketing services, powerful influencers, full-service audio solutions, industry-leading research and insights, and live event experiences. Cumulus Media is the only audio media company to provide marketers with local and national advertising performance guarantees. For more information visit www.cumulusmedia.com.

Michael Kupinski, Director of Research, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

Favorable Q3 results. The company reported Q3 revenue of $233.5 million, just above our expectation of $230 million. Despite revenue decreasing 2% from the previous quarter Adj. EBITDA grew by 1.6% to $46.6 million beating our forecast of $41.7 million by 11.7%.

Lowers guidance. Q4 revenue is expected to decline low to mid single digits in spite of influx of Political advertising, which too appears softer than expected.Local advertising appears to have softened, which implies that local businesses are now feeling the affect of the economic headwinds. Management lowered Adj. EBITDA guidance from a range of $175 million to $200 million to a range of $160 million to $170 million.

This Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

A Blood Test that Screens for Multiple Cancers at Once Promises to Boost Early Detection

Detecting cancer early before it spreads throughout the body can be lifesaving. This is why doctors recommend regular screening for several common cancer types, using a variety of methods. Colonoscopies, for example, screen for colon cancer, while mammograms screen for breast cancer.

While important, getting all these tests done can be logistically challenging, expensive and sometimes uncomfortable for patients. But what if a single blood test could screen for most common cancer types all at once?

This is the promise of multicancer early detection tests, or MCEDs. This year, President Joe Biden identified developing MCED tests as a priority for the Cancer Moonshot, a US$1.8 billion federal effort to reduce the cancer death rate and improve the quality of life of cancer survivors and those living with cancer.

This article was republished with permission from The Conversation, a news site dedicated to sharing ideas from academic experts. It represents the research-based findings and thoughts of Colin Pritchard, Professor of Laboratory Medicine and Pathology, University of Washington.

As a laboratory medicine physician and researcher who develops molecular tests for cancer, I believe MCED tests are likely to transform cancer screening in the near future, particularly if they receive strong federal support to enable rapid innovation.

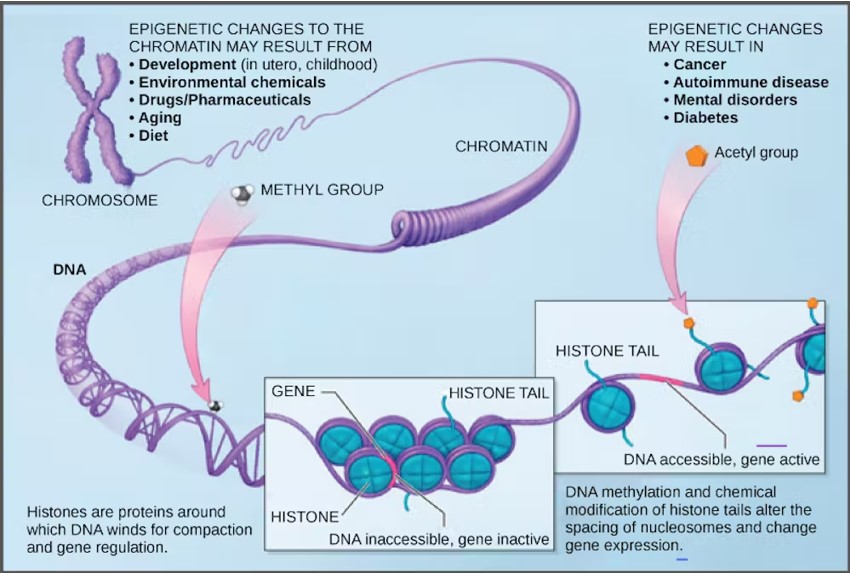

How MCED Tests Work

All cells in the body, including tumor cells, shed DNA into the bloodstream when they die. MCED tests look for the trace amounts of tumor DNA in the bloodstream. This circulating “cell-free” DNA contains information about what type of tissue it came from and whether it is normal or cancerous.

Testing to look for circulating tumor DNA in the blood is not new. These liquid biopsies – a fancy way of saying blood tests – are already widely used for patients with advanced-stage cancer. Doctors use these blood tests to look for mutations in the tumor DNA that help guide treatment. Because patients with late-stage cancer tend to have a large amount of tumor DNA circulating in the blood, it’s relatively easy to detect the presence of these genetic changes.

MCED tests are different from existing liquid biopsies because they are trying to detect early-stage cancer, when there aren’t that many tumor cells yet. Detecting these cancer cells can be challenging early on because noncancer cells also shed DNA into the bloodstream. Since most of the circulating DNA in the bloodstream comes from noncancer cells, detecting the presence of a few molecules of cancer DNA is like finding a needle in a haystack.

Making things even more difficult, blood cells shed abnormal DNA naturally with aging, and these strands can be confused for circulating cancer DNA. This phenomenon, known as clonal hematopoiesis, confounded early attempts at developing MCED tests, with too many false positive results.

Fortunately, newer tests are able to avoid blood cell interference by focusing on a type of “molecular barcode” embedded in the cancer DNA that identifies the tissue it came from. These barcodes are a result of DNA methylation, naturally existing modifications to the surface of DNA that vary for each type of tissue in the body. For example, lung tissue has a different DNA methylation pattern than breast tissue. Furthermore, cancer cells have abnormal DNA methylation patterns that correlate with cancer type. By cataloging different DNA methylation patterns, MCED tests can focus on the sections of DNA that distinguish between cancerous and normal tissue and pinpoint the cancer’s origin site.

DNA contains molecular patterns that indicate where in the body it came from. (CNX OpenStax/Wikimedia Commons)

Testing Options

There are currently several MCED tests in development and in clinical trials. No MCED test is currently FDA-approved or recommended by medical societies.

In 2021, the biotech company GRAIL, LLC launched the first commercially available MCED test in the U.S. Its Galleri test claims to detect over 50 different types of cancers. At least two other U.S.-based companies, Exact Sciences and Freenome, and one Chinese company, Singlera Genomics, have tests in development. Some of these tests use different cancer detection methods in addition to circulating tumor DNA, such as looking for cancer-associated proteins in blood.

MCED tests are not yet typically covered by insurance. GRAIL’s Galleri test is currently priced at $949, and the company offers a payment plan for people who have to pay out of pocket. Legislators have introduced a bill in Congress to provide Medicare coverage for MCED tests that obtain FDA approval. It is unusual for Congress to consider legislation devoted to a single lab test, and this highlights both the scale of the medical market for MCED and concerns about disparities in access without coverage for these expensive tests.

How Should MCED Tests be Used?

Figuring out how MCED tests should be implemented in the clinic will take many years. Researchers and clinicians are just beginning to address questions on who should be tested, at what age, and how past medical and family history should be taken into account. Setting guidelines for how doctors will further evaluate positive MCED results is just as important.

There is also concern that MCED tests may result in overdiagnoses of low-risk, asymptomatic cancers better left undetected. This happened with prostate cancer screening. Previously, guidelines recommended that all men ages 55 to 69 regularly get blood tests to determine their levels of PSA, a protein produced by cancerous and noncancerous prostate tissue. But now the recommendation is more nuanced, with screening suggested on an individual basis that takes into account personal preferences.

Another concern is that further testing to confirm positive MCED results will be costly and a burden to the medical system, particularly if a full-body scan is required. The out-of-pocket cost for an MRI, for example, can run up to thousands of dollars. And patients who get a positive MCED result but are unable to confirm the presence of cancer after extensive imaging and other follow-up tests may develop lifelong anxiety about a potentially missed diagnosis and continue to take expensive tests in fruitless search for a tumor.

Despite these concerns, early clinical studies show promise. A 2020 study of over 10,000 previously undiagnosed women found 26 of 134 women with a positive MCED test were confirmed to have cancer. A 2021 study sponsored by GRAIL found that half of the over 2,800 patients with a known cancer diagnosis had a positive MCED test and only 0.5% of people confirmed to not have cancer had a false positive test. The test performed best for patients with more advanced cancers but did detect about 17% of the patients who had very-early-stage disease.

MCED tests may soon revolutionize the way clinicians approach cancer screening. The question is whether the healthcare system is ready for them.

What Other Than a Large Rate Hike Can Investors Expect this Week?

Another 75 basis point hike is expected on Wednesday after the November 1-2 FOMC meeting. The discussion that is expected to immediately follow is will the Federal Reserve slow or pause its tightening from there. Those answers can’t be certain as even the Fed hasn’t seen the economic numbers unfold that will lead to the next meeting and play a part in the decision.

Since March, the FOMC has raised rates a cumulative 300 basis points. If they move .75 percent this week, the fed funds target range will be 3.75%-4.00%. This range was last experienced after the January 2008 meeting.

In September’s Summary of Economic Projections, the FOMC forecast for the fed funds rate was 1.25 percent above the current level or .50 percent above what most expect we will have by the end of the week. The statement and remarks following the next FOMC meeting by Chairman Powell may suggest that the FOMC is going to slow down the upward movement in rates while they see if previous rate hikes have begun to have a slowing impact on the economic pace.

The second scheduled event with the most potential to impact markets is the October Employment Situation on Thursday.

From there, all attention and talk may be on the elections next week, as they can have a powerful impact on market moves.

Monday 10/31

9:45 am US Chicago Purchasing Managers Report (PMI). The consensus is 47.3. For September, this survey of business conditions in the Chicago area showed a collapse to 45.7. A small improvement is expected from the October Survey

10:30 am Dallas Fed Manufacturing Survey is expected to come in at -18.0. This would be the sixth straight negative reading. This survey tracks manufacturing in Texas; for September, the results were -17.2.

3:00 pm US Farm Prices are expected to have come down during October by -1.8%, showing a year-over-year rate of 20% increase in farm prices. This is an important inflationary gauge as farm prices are a leading indicator of food price changes Consumer Price Index (CPI). There is a direct relationship between inflation and interest rates; markets can be influenced as interest rate expectations rise and fall.

Tuesday 11/1

The Federal Open Market Committee meets eight times a year in order to determine the near-term direction of monetary policy. The November meeting extends through November 2. After the meeting, typically at 2 pm, any change in monetary policy is announced.

10:00 am US Construction Spending is expected to have fallen by -.5%. Construction spending fell 0.7 percent in August, which was the seventh straight lower-than-expected result, showing lower activity in this important economic sector.

10:00 am JOLTS report consensus is 9.875 million. These reported job openings have been falling over several months; the previous month’s (August) openings reported were 10.05 million. The acronym JOLTS stands for Job Openings and Labor Turnover Survey.

Wednesday 11/2

Motor Vehicle Sales (US) are expected to have increased to 14.2 million from 13.5 million in September. The pattern of consumption is a direct influencer on company earnings and stock prices. Strong economic growth translates to healthy corporate profits and higher stock prices.

10:30 am EIA Petroleum Report shows crude inventory changes, as well as gasoline and other petroleum products. The Energy Information Administration provides this report weekly. During periods when inflation and fuel prices are a concern, the data in these reports can play a wider-than-normal role in influencing stock, bond, and of course, commodity price levels.

FOMC Announcement usually comes at 2:00 pm. The expectations had not changed since the last meeting when it became widely expected that the Federal Reserve would raise overnight lending rates at this meeting by 0.75%. A big focus will be on the policy statement following the meeting to sense at what pace removing accommodation will continue in the US.

Thursday 11/3

8:30 am US Jobless Clams are expected to be 222,000 for the week ending October 29. The prior week they had been 217,000. Employment is one of the Feds’ primary concerns as it fights inflation which also tops the list.

10:00 am US Factory orders are expected to have risen in September by 0.3%. The prior month this leading indicator of future economic activity was flat.

10:30 am EIA Natural Gas weekly report will update the current stocks and storage as well as production information from five regions within the US.

Friday 11/4

8:30 am, the Employment Situation report is released. It is expected to show an unemployment rate of 3.6%, or 210,000. The results of this survey have the potential to jar markets late in the week as one of the more important measures of a healthy economy (weak or overheated) is employment levels.

What Else

If the week brings more clarity from the Federal Reserve and likely next moves, investors may begin to focus on retail numbers as the calendar moves toward the shopping season.

Is the Halloween Investment Strategy a Trick or a Treat?

What Is the Halloween Strategy? Is it statistically reliable? What have the results been?

The directive, “Always remember to buy in November,” has a few different names; the Halloween effect, the Halloween indicator, are among the more common. It answers the question, If I sell in May and walk away, when do I come back? This is because the “Halloween Strategy” and the “Sell in May” strategies are related — they are different ways of suggesting the same action. The results should be identical.

What Is It?

The Halloween strategy is over a century old. Buying when October ends is essentially a market-timing strategy based on the thought that the overall stock market performs better between Oct. 31st (Halloween) and May 1st than it performs from May through the end of October. The directive suggests first that market timing yields better results than buy and hold. Secondly, it says the probability of better results compared to buying and holding is increased, over this period. Those who subscribe to this approach recommend not investing at all during the summer months.

Evidence suggests this strategy does perform well over time, but despite many theories, there is no clear or agreed-upon reason. A famous study was done by Sven Bouman (AEGON Asset Mgmt.) and Ben Jacobsen (Erasmus University Rotterdam) and published in the American Economic Review December 2002. The study documents the existence of a strong seasonal effect in stock returns based on the Halloween indicator. They found the “inherited wisdom” to be true globally and useful in 36 of the 37 developed and emerging markets they studied. They reported the Sell in May effect tends to be particularly strong in European countries and is robust over time. Their sample evidence shows that in the UK the effect has been noticeable since 1694. They also reported, “While we have examined a number of possible explanations, none of these appears to explain the puzzle convincingly.”

Is it Reliable?

I didn’t go back as far as 1694 the way Sven and Ben did. And I didn’t collect data from emerging and developed markets around the globe. More pertinent to Channelchek readers is whether this strategy used on the U.S. markets has been worthwhile.

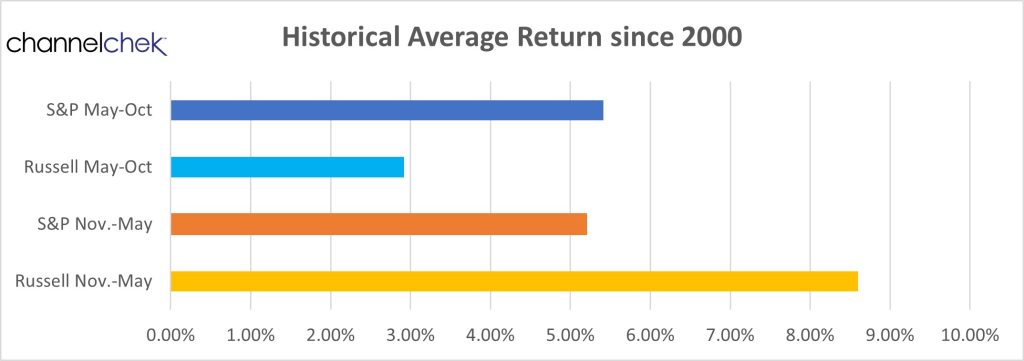

Data Source: Koyfin

The above chart is a compilation of average results for two six-month periods, May through October and November through April. It also looks at two different indexes, the largest stocks in the S&P 500 (blue shades) index and small-cap stocks of the Russell 2000 (orange shades).

What was discovered is that during the period, investors in either of these indexes would have had positive earnings during either “season.” So it supports “buy and hold” wisdom or, at least, staying invested. During the Halloween through May period, the smallcap Russell returned 8.60%, while during the other six months, performance was a weaker 2.92%. The S&P 500 maintained consistent averages in the low 5% area for either period.

What Have the Results Been?

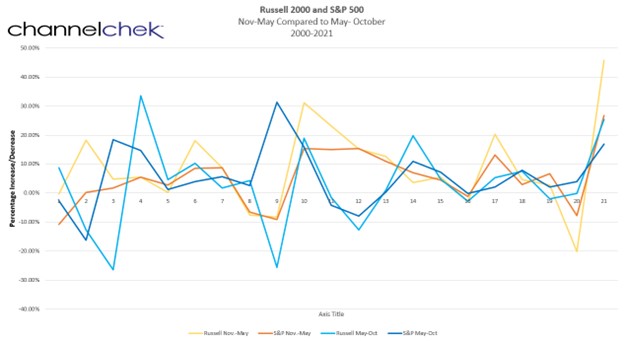

Since the turn of the century, investors would have fared better if they bought stocks represented in the small-cap average after Halloween, then moved to S&P 500 stocks in May. Below are the results of the 21 periods. The highest returns of either index occurred during the latest Halloween to May cycle. It was the small-cap index that measured a 45.76% gain. The index also measured the second-highest gain during the Sell in May 2004 measurement period. The Sell in May small-cap index also can claim the two lowest performance numbers.

Data Source: Koyfin

Take-Away

The Halloween strategy says that investors should be fully invested in stocks from November through April, and out of stocks from May through October. Variations of this strategy and its accompanying axioms have been around for over a century. Looking at the last 21 years, a deviation that would have paid off would have been moving to small-caps after Halloween.

Both “seasons,” for both measured indexes had positive average earnings. So the notion of staying fully invested is supported using recent data.

TULSA, Okla.–(BUSINESS WIRE)– Alliance Resource Partners, L.P. (NASDAQ: ARLP) today announced that the Board of Directors of ARLP’s general partner approved an increased cash distribution to its unitholders for the quarter ended September 30, 2022 (the “2022 Quarter”).

ARLP unitholders will receive a cash distribution for the 2022 Quarter of $0.50 per unit (an annualized rate of $2.00 per unit), payable on November 14, 2022 to all unitholders of record as of the close of trading on November 7, 2022. The announced distribution represents a 150.0% increase over the cash distribution of $0.20 per unit for the quarter ended September 30, 2021 and a 25.0% increase over the cash distribution of $0.40 per unit for the quarter ended June 30, 2022.

As previously announced, ARLP will report financial results for the 2022 Quarter before the market opens on Monday, October 31, 2022 and Alliance management will discuss these results during a conference call beginning at 10:00 a.m. Eastern that same day.

To participate in the conference call, dial (877) 407-0784 and request to be connected to the Alliance Resource Partners, L.P. earnings conference call. International callers should dial (201) 689-8560 and request to be connected to the same call. Investors may also listen to the call via the “investor relations” section of ARLP’s website at http://www.arlp.com.

An audio replay of the conference call will be available for approximately one week. To access the audio replay, dial U.S. Toll Free (844) 512-2921; International Toll (412) 317-6671 and request to be connected to replay using access code 13733069.

This announcement is intended to be a qualified notice under Treasury Regulation Section 1.1446-4(b), with 100% of the partnership’s distributions to foreign investors attributable to gross income, gain or loss that is effectively connected with a United States trade or business. Accordingly, ARLP’s distributions to foreign investors are subject to federal income tax withholding at the highest applicable tax rate.

About Alliance Resource Partners, L.P.

ARLP is a diversified energy company that is currently the largest coal producer in the eastern United States. ARLP also generates operating and royalty income from mineral interests it owns in strategic coal and oil & gas producing regions in the United States. In addition, ARLP is positioning itself as an energy provider for the future by leveraging its core technology and operating competencies to make strategic investments in the fast-growing energy and infrastructure transition.

News, unit prices and additional information about ARLP, including filings with the Securities and Exchange Commission (“SEC”), are available at http://www.arlp.com. For more information, contact the investor relations department of ARLP at (918) 295-7674 or via e-mail at investorrelations@arlp.com.

Brian L. Cantrell Alliance Resource Partners, L.P. (918) 295-7673

MELVILLE, N.Y.–(BUSINESS WIRE)–Oct. 27, 2022– October 27, 2022– Comtech (NASDAQ: CMTL) announced today that during its first quarter of fiscal 2023, the Company was awarded over $50.0 million of incremental funding on an existing contract to provide next generation troposcatter systems in support of the U.S. military. For over 50 years, Comtech has been a world leader in the design and supply of modernized troposcatter technologies. Our Troposcatter Family of Systems are just one way that Comtech helps to ensure that our customers can count on secure, uninterrupted connectivity where (and when) it matters most.

About Comtech

Comtech Telecommunications Corp. is a leading global provider of next-generation 911 emergency systems and secure wireless communications technologies to commercial and government customers around the world. Headquartered in Melville, New York and with a passion for customer success, Comtech designs, produces and markets advanced and secure wireless solutions. For more information, please visit www.comtech.com or see our Signals blog at https://www.comtech.com/comtech-signals/.

Forward-Looking Statements

Certain information in this press release contains statements that are forward-looking in nature and involve certain significant risks and uncertainties. Actual results could differ materially from such forward-looking information. The Company’s Securities and Exchange Commission filings identify many such risks and uncertainties. Any forward-looking information in this press release is qualified in its entirety by the risks and uncertainties described in such Securities and Exchange Commission filings.