Salem Media Group is America’s leading multimedia company specializing in Christian and conservative content, with media properties comprising radio, digital media and book and newsletter publishing. Each day Salem serves a loyal and dedicated audience of listeners and readers numbering in the millions nationally. With its unique programming focus, Salem provides compelling content, fresh commentary and relevant information from some of the most respected figures across the Christian and conservative media landscape.

Michael Kupinski, Director of Research, Noble Capital Markets, Inc.

Patrick McCann, Research Associate, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

Updates Q3 guidance. Management lowered Q3 revenue guidance from a range of 6% to 8% growth to a range of flat to a positive 2%. The company indicated that the lower revenue outlook was due to a shift in revenue related to the Dinesh D’Souza book slipping into Q4 and softer expectations in its SalemNow segment.

SalemNow likely disappointing. We believe that the softer revenue expectations in SalemNow is likely related to a poor performance for Uncle Tom II. We like the company’s expansion into content, which can be very lucrative, but the success of the content is hard to predict.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

Gregory Aurand, Senior Research Analyst, Healthcare Services & Medical Devices, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

What’s in a name? The rebranding identifies the Company’s CHITOSAN based regenerative medicine technology while expanding the scope of the technology beyone orthopedics. While the near term pipeline is focused on the repair of orthopedic soft tissue (rotator cuff and meniscus) as initial markets with great need, the Company’s proprietary platform has much broader potential regenerative applications, including in cardiovascular, dermatology, wound healing, oncology and neurology.

Tickers will change. The corporate rebranding was approved at the last Annual General and Special Meeting of Shareholders held July 21, 2022, following the passing of a special resolution authorizing a name change. Effective on or around September 12th, shares will begin trading on the CSE as CHGX. Subject to change, it is expected that the OTCQB ticker will also be updated to CHGX.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

Defense Metals Corp. is a mineral exploration and development company focused on the acquisition, exploration and development of mineral deposits containing metals and elements commonly used in the electric power market, defense industry, national security sector and in the production of green energy technologies, such as, rare earths magnets used in wind turbines and in permanent magnet motors for electric vehicles. Defense Metals owns 100% of the Wicheeda Rare Earth Element Property located near Prince George, British Columbia, Canada. Defense Metals Corp. trades in Canada under the symbol “DEFN” on the TSX Venture Exchange, in the United States, under “DFMTF” on the OTCQB and in Germany on the Frankfurt Exchange under “35D”.

Mark Reichman, Senior Research Analyst, Natural Resources, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

First Nations agreement. Defense Metals entered into a Mineral Exploration Agreement with the McLeod Lake Indian Band that addresses the interests of both parties with respect to mineral exploration activities at the company’s Wicheeda Rare Earth Element project. The agreement provides a framework for communication and cooperation going forward which we think promotes cooperative collaboration and further de-risks the project.

Fostering a collaborative and mutually beneficial relationship. In addition to providing the McLeod Lake Indian Band with input into how exploration activities proceed, the agreement provides economic opportunities for the First Nations community and establishes a path for potential future commercial involvement.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

Bassett Furniture Industries, Incorporated manufactures, markets, and retails home furnishings in the United States. The company operates in three segments: Wholesale, Retail, and Logistical Services. It is involved in the design, manufacture, sourcing, sale, and distribution of furniture products to a network of company-owned and licensee-owned Bassett Home Furnishings (BHF) retail stores, as well as independent furniture retailers; and wood and upholstery operations. As of September 16, 2017, the company operated a network of 91 company-and licensee-owned stores. It also provides shipping, delivery, and warehousing services to customers in the furniture industry. In addition, the company owns and leases retail store properties. It also distributes its products through other multi-line furniture stores, Bassett galleries or design centers, specialty stores, and mass merchants. Bassett Furniture Industries was founded in 1902 and is based in Bassett, Virginia.

Joe Gomes, Senior Research Analyst, Noble Capital Markets, Inc.

Joshua Zoepfel, Research Associate, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

Purchase of Noa Home. Basset purchased Noa Home, Inc., a a mid-priced e-commerce furniture retailer headquartered in Montreal, Canada. We believe the purchase provides multiple benefits to Bassett, including a greater online presence, including for Bassett products, as well as allowing the Company to attract more digitally native consumers.

Transaction Details. The purchase price included cash payments of CAD$2.0 million paid to the co-founders of Noa and approximately CAD$5.7 million for the repayment of existing debt. The Noa co-founders also will have the opportunity to receive additional annual cash payments of CAD$1.33 million per year for the following three fiscal years based on established increases in net revenues and achieving certain internal EBITDA goals.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

NEW YORK, NY / ACCESSWIRE / September 7, 2022 / Engine Gaming and Media, Inc. (“Engine” or the “Company”) (NASDAQ:GAME) (TSX-V:GAME), a data-driven, gaming, media and influencer marketing platform company, today announced that management will present during Benzinga’s All Access investor event taking place Friday, September 9, 2022.

Tom Rogers, Executive Chairman of Engine, and Lou Schwartz, Chief Executive Officer of Engine, are scheduled to host a presentation and Q&A session during the event as follows.

A live video webcast will be available using the link above – an archived replay will be made available after the live event on the Benzinga YouTube Channel. For more information on Benzinga All Access, please contact your Benzinga representative.

About Engine Gaming and Media, Inc.

Engine Gaming and Media, Inc. (NASDAQ:GAME) (TSX-V:GAME) provides unparalleled live streaming data and social analytics, influencer relationship management and monetization, and programmatic advertising to support the world’s largest video gaming companies, brand marketers, ecommerce companies, media publishers and agencies to drive new streams of revenue. The company’s subsidiaries include Stream Hatchet, the global leader in gaming video distribution analytics; Sideqik, a social influencer marketing discovery, analytics, and activation platform; and Frankly Media, a digital publishing platform used to create, distribute, and monetize content across all digital channels. Engine generates revenue through a combination of software-as-a-service subscription fees, managed services, and programmatic advertising. For more information, please visit www.enginegaming.com.

Investor Relations Contact:

Shannon Devine MZ North America Main: 203-741-8811 GAME@mzgroup.us

NEW YORK, NY / ACCESSWIRE / September 7, 2022 / Engine Gaming and Media, Inc. (“Engine” or the “Company”) (NASDAQ:GAME) (TSX-V:GAME), a data-driven, gaming, media and influencer marketing platform company, today announced management’s participation in the H.C. Wainwright 24th Annual Global Investment Conference being held September 12-14 virtually and at the Lotte New York Palace Hotel in New York City.

The Company’s Executive Chairman, Tom Rogers, and Chief Executive Officer, Lou Schwartz, will be available for in person one-on-one meetings with investors. To schedule a meeting with Engine’s management, please contact your conference representative or you may also email your request to GAME@mzgroup.us. The Company will also be giving a presentation on Tuesday September 13 at 12:00 p.m. eastern time at the conference. The presentation will be broadcasted live and can be streamed by clicking here.

About Engine Gaming and Media, Inc.

Engine Gaming and Media, Inc. (NASDAQ:GAME) (TSX-V:GAME) provides unparalleled live streaming data and social analytics, influencer relationship management and monetization, and programmatic advertising to support the world’s largest video gaming companies, brand marketers, ecommerce companies, media publishers and agencies to drive new streams of revenue. The company’s subsidiaries include Stream Hatchet, the global leader in gaming video distribution analytics; Sideqik, a social influencer marketing discovery, analytics, and activation platform; and Frankly Media, a digital publishing platform used to create, distribute, and monetize content across all digital channels. Engine generates revenue through a combination of software-as-a-service subscription fees, managed services, and programmatic advertising. For more information, please visit www.enginegaming.com.

Investor Relations Contact:

Shannon Devine MZ North America Main: 203-741-8811 GAME@mzgroup.us

Noble Capital Markets, a full-service SEC / FINRA registered broker-dealer, dedicated exclusively to serving underfollowed small/microcap companies through investment banking, wealth management, trading & execution, and equity research activities (and the provider of equity research on Channelchek), is pleased to announce the return of in-person meetings with executives from companies listed on Channelchek. Qualified Investors, at all levels, as well as registered representatives, are welcome to attend these breakfasts and lunches at no cost, and with no obligation to invest. LIMITED SEATING AVAILABILITY.

To request attendance, click the registration link(s) below. A Noble representative will contact you to request qualification information, and to provide you full location and attendance details (based upon availability). NOTE: All attendees must be preregistered and qualified; no admittance of unregistered guests at the door. Limited opportunity to attend future meetings for no-shows. For general MEET the MANAGEMENT inquiries, please contact Dustin Cronk, Head of Institutional Relationships at Noble Capital Markets at dcronk@noblecapitalmarkets.com

VANCOUVER, BC, Sept. 7, 2022 /CNW/ – Defense Metals Corp. (“Defense Metals” or the “Company“) ( TSXV: DEFN) (OTCQB: DFMTF) (FSE: 35D) is very pleased to announce it has entered into a Mineral Exploration Agreement (the “Agreement“) with the McLeod Lake Indian Band regarding its Wicheeda Rare Earth Element (“REE”) exploration project located 80 kilometres northeast of Prince George, Canada.

The Agreement addresses the immediate interests of the parties with respect to mineral exploration activities related to the project, and puts into place a framework for communication and cooperation going forward. In addition to providing McLeod Lake Indian Band with meaningful input into how these activities are to proceed, the Agreement provides current economic opportunities for the community and establishes a roadmap for potential future commercial involvement as the exploration activities advance.

“We are delighted to have the McLeod Lake Indian Band engaged with Defense Metals and the opportunities presented by the Wicheeda exploration project,” said Craig Taylor, CEO of Defense. “We look forward to building a long-term and mutually beneficial relationship with the McLeod Lake Indian Band through the implementation of this initial agreement.”

“McLeod Lake Indian Band has always been open to working with companies that respect our rights, laws and interests in the protection of our lands, and that provide meaningful economic and commercial opportunities for our community,” said Chief Harley Chingee. “We are therefore pleased to have completed this initial agreement with Defense Metals, and look forward to its successful implementation.”

About McLeod Lake Indian Band

McLeod Lake Indian Band is part of the Tse’khene group of Aboriginal peoples. The main community of McLeod Lake Indian Band is located near the unincorporated village of McLeod Lake, approximately 150 kilometers north of Prince George.

About Defense Metals Corp.

Defense Metals Corp. is a mineral exploration and development company focused on the acquisition, exploration and development of mineral deposits containing metals and elements commonly used in the electric power market, defense industry, national security sector and in the production of green energy technologies, such as, rare earths magnets used in wind turbines and in permanent magnet motors for electric vehicles. Defense Metals owns 100% of the Wicheeda Rare Earth Element property located near Prince George, British Columbia, Canada. Defense Metals Corp. trades in Canada on the TSX Venture Exchange under the symbol “DEFN”, in the United States, under “DFMTF” on the OTCQB and in Germany on the Frankfurt Exchange under “35D”.

Neither the TSX Venture Exchange nor its Regulation Services Provider (as that term is defined in the policies of the TSX Venture Exchange) accepts responsibility for the adequacy or accuracy of this news release.

Cautionary Statement Regarding “Forward-Looking” Information

This news release contains “forward-looking information or statements” within the meaning of applicable securities laws, which may include, without limitation, statements relating to advancing the Wicheeda REE Project, the Company’s plans for its Wicheeda REE Project, the expected outcomes and benefits of the Agreement with the MLIB, the technical, financial and business prospects of the Company, its project and other matters. All statements in this news release, other than statements of historical facts, that address events or developments that the Company expects to occur, are forward-looking statements. Although the Company believes the expectations expressed in such forward-looking statements are based on reasonable assumptions, such statements are not guarantees of future performance and actual results may differ materially from those in the forward-looking statements. Such statements and information are based on numerous assumptions regarding present and future business strategies and the environment in which the Company will operate in the future, including the price of rare earth elements, the anticipated costs and expenditures, the ability to achieve its goals, that general business and economic conditions will not change in a material adverse manner, that financing will be available if and when needed and on reasonable terms. Such forward-looking information reflects the Company’s views with respect to future events and is subject to risks, uncertainties and assumptions, including the risks and uncertainties relating to the interpretation of exploration results, risks related to the inherent uncertainty of exploration and cost estimates, the potential for unexpected costs and expenses and those other risks filed under the Company’s profile on SEDAR at www.sedar.com. While such estimates and assumptions are considered reasonable by the management of the Company, they are inherently subject to significant business, economic, competitive and regulatory uncertainties and risks. Factors that could cause actual results to differ materially from those in forward looking statements include, but are not limited to, continued availability of capital and financing and general economic, market or business conditions, adverse weather and climate conditions, failure to maintain or obtain all necessary government permits, approvals and authorizations, failure to maintain community acceptance (including First Nations), risks relating to unanticipated operational difficulties (including failure of equipment or processes to operate in accordance with specifications or expectations, cost escalation, unavailability of personnel, materials and equipment, government action or delays in the receipt of government approvals, industrial disturbances or other job action, and unanticipated events related to health, safety and environmental matters), risks relating to inaccurate geological and engineering assumptions, decrease in the price of rare earth elements, the impact of Covid-19 or other viruses and diseases on the Company’s ability to operate, an inability to predict and counteract the effects of COVID-19 on the business of the Company, including but not limited to, the effects of COVID-19 on the price of commodities, capital market conditions, restriction on labour and international travel and supply chains, loss of key employees, consultants, or directors, increase in costs, delayed drilling results, litigation, and failure of counterparties to perform their contractual obligations. The Company does not undertake to update forward-looking statements or forward-looking information, except as required by law.

Publication of this Scientific Paper on the Safety of Oxidized Beta Carotene is a milestone on the path to broader regulatory clearance to market and sell OxC-beta™ Products in the U.S. and supports wide-spread adoption of the technology around the world

Ottawa, ON /Business Wire/ September 7, 2022 /– Avivagen Inc. (TSXV:VIV, OTCQB:VIVXF) (“Avivagen”), a life sciences corporation focused on developing and commercializing products for livestock, companion animal and human applications that safely enhances feed intake and supports immune function, thereby supporting general health and performance, is pleased to announce that its scientific paper entitled “Safety and uptake of fully Oxidized Beta Carotene” (the active ingredient in the company’s OxC-beta™ product line) has been published in the Journal of Food and Chemical Toxicology. A link to the article is provided below.

“With any innovative product, adoption and uptake require a robust understanding of the benefits and safety of that product and necessitate significant scrutiny. Avivagen has been working tirelessly to showcase the multiple, compelling use cases of OxC-beta and concurrent proven safety. This new peer reviewed publication, one of now ten such publications on OxC-beta, represents the cumulative work on the attractive safety profile of our product. This pioneering work by Dr. Graham Burton, co-founder of Avivagen, and his team lays important groundwork to seek further regulatory approvals for OxC-beta in the U.S. and around the world, for multiple use cases and with strong, proven scientific underpinnings expected by our end market customers.”, said Kym Anthony, Avivagen CEO. “We look forward to sharing these results with existing and new customers and providing this to regulatory bodies around the world as we look to further expand our access to large markets.”

About OxC-beta™ Technology β-carotene has been primarily recognized for the health benefits it provides when it is transformed into vitamin A by biochemical reaction with oxygen in the body. Avivagen discovered that spontaneous oxidation of β-carotene produces a mixture of oxidation compounds other than vitamin A that also provide important health benefits. The mixture of β-carotene oxidation compounds, OxC-beta, a product developed by Avivagen, contains neither β-carotene or vitamin A, indicating its health benefits stem uniquely from the oxidation compounds themselves. Incorporation of OxC-beta into products for livestock, companion animal and humans show a range of practical benefits. A peer reviewed paper just published in the prestigious Food and Chemical Toxicology journal (https://doi.org/10.1016/j.fct.2022.113387) has reported that OxC-beta has a very high margin of safety and the discovery that the natural counterpart of OxC-beta is present at significant levels in mouse tissues and blood. A standard toxicology study conducted in rats established a No Observed Adverse Effect Level that is several thousand-fold higher than the level of supplementation with OxC-beta used in livestock, companion animals and humans. These findings are highly significant in establishing the safety of OxC-beta with respect to regulatory approvals of the product in various major jurisdictions.

About Avivagen Avivagen is a life sciences corporation focused on developing and commercializing products for livestock, companion animal and human applications that, by safely supporting immune function, promote general health and performance. It is a public corporation traded on the TSX Venture Exchange under the symbol VIV and is headquartered in Ottawa, Canada, based in partnership facilities of the National Research Council of Canada. For more information, visit www.avivagen.com. The contents of the website are expressly not incorporated by reference in this press release.

About OxC-beta™ Livestock Avivagen’s OxC-beta™ technology is derived from Avivagen discoveries about β-carotene and other carotenoids, compounds that give certain fruits and vegetables their bright colours. Through support of immune function the technology provides a non-antibiotic means of promoting health and growth. OxC-beta™ Livestock is a proprietary product shown to be an effective and economic alternative to the antibiotics commonly added to livestock feeds. The product is currently available for sale in the United States, Philippines, Mexico, Taiwan, New Zealand, Thailand, Brazil, Australia, Vietnam and Malaysia.

Avivagen’s OxC-beta™ Livestock product is safe, effective and could fulfill the global mandate to remove all in-feed antibiotics as growth promoters. Numerous international livestock trials with poultry and swine using OxC-beta™ Livestock have proven that the product performs as well as, and, sometimes, in some aspects, better than in-feed antibiotics.

Forward Looking Statements This news release includes certain forward-looking statements that are based upon the current expectations of management. Forward-looking statements involve risks and uncertainties associated with the business of Avivagen Inc. and the environment in which the business operates. Any statements contained herein that are not statements of historical facts may be deemed to be forward-looking, including those identified by the expressions “aim”, “anticipate”, “appear”, “believe”, “consider”, “could”, “estimate”, “expect”, “if”, “intend”, “goal”, “hope”, “likely”, “may”, “plan”, “possibly”, “potentially”, “pursue”, “seem”, “should”, “whether”, “will”, “would” and similar expressions.

Statements set out in this news release relating to the potential positive impacts expected to arise from the publication of the above referenced article, the possibility for further regulatory approvals and expanded use cases for Avivagen’s products, the future growth and prospects for Avivagen and the possibility for OxC-beta™ Livestock to replace antibiotics in livestock feeds as growth promoters are forward-looking statements. These forward-looking statements are subject to a number of risks and uncertainties that could cause actual results or events to differ materially from current expectations. For instance, Avivagen’s products may not gain market acceptance or regulatory approval in new jurisdictions or for new applications and may not be widely accepted as a replacement for antibiotics as growth promoters in livestock feeds due to many factors, many of which are outside of Avivagen’s control. Readers are referred to the risk factors associated with the business of Avivagen set out in Avivagen’s most recent management’s discussion and analysis of financial condition available at www.SEDAR.com. Except as required by law, Avivagen assumes no obligation to update the forward-looking statements, or to update the reasons why actual results could differ from those reflected in the forward-looking statements.

Neither TSX Venture Exchange nor its Regulation Services Provider (as that term is defined in the policies of the TSX Venture Exchange) accepts responsibility for the adequacy or accuracy of this release.

For more information: Avivagen Inc. Drew Basek Director of Investor Relations 100 Sussex Drive, Ottawa, Ontario, Canada K1A 0R6 Phone: 416-540-0733 E-mail: d.basek@avivagen.com

IRVING, Texas–(BUSINESS WIRE)– Salem Media Group, Inc. (NASDAQ: SALM) today announced revisions to its third quarter 2022 revenue. Taking into account the postponement of the forthcoming book, 2000 Mules by Dinesh D’Souza, until the fourth quarter, lower than expected revenue on SalemNOW and the impact on advertising revenue due to the weakening economic environment, the company now expects third quarter 2022 total revenue to be between flat and an increase of 2% over third quarter 2021 total revenue of $66.0 million.

ABOUT SALEM MEDIA GROUP:

Salem Media Group is America’s leading multimedia company specializing in Christian and conservative content, with media properties comprising radio, digital media and book and newsletter publishing. Each day Salem serves a loyal and dedicated audience of listeners and readers numbering in the millions nationally. With its unique programming focus, Salem provides compelling content, fresh commentary and relevant information from some of the most respected figures across the Christian and conservative media landscape. Learn more about Salem Media Group, Inc. at www.salemmedia.com, Facebook and Twitter.

Why So Much Money from Overseas is Flowing to Soft U.S. Markets

In 2016, Mohamed El-Erian, chief economic advisor at Allianz, and President of Queens’ College, Cambridge published a book called The Only Game in Town. It was written during a period approximately halfway between the last big stock market sell-off and the 2022 bear market. In it he suggests the only reason investment dollars from overseas are flocking to U.S. markets is because we are “the cleanest dirty shirt.” In other words, the U.S. economy and financial system may not be great, but it is far more appealing than the alternatives.

Labor Day 2022 is now behind us, the S&P 500 is down 16% YTD, the economy receded during the first half of the year and its growth is probably still stunted. The U.S. Treasury index indicates that bonds are down 11% YTD, so why are international money flows moving to U.S. markets? Do investors from overseas think this is a buying opportunity, are we the “cleanest dirty shirt,” or is there something else?

There are probably a number of correct answers, which, when taken together, provides the reason. Investors need to be aware of the dynamics as flows into and out of the U.S. impact all of the country’s markets, including real estate and currency.

“The U.S. looks the least challenged in a very challenging world,” Christopher Smart, chief global strategist at Barings and head of the Barings Investment Institute told the Wall Street Journal. “Everybody is slowing down, but the U.S., because of the continuing strength of the jobs market, still seems to be slowing more slowly,” he added.

And the data shows just how much money is reaching our markets. Assets have been withdrawn from international stock funds for 20 consecutive weeks, according to Refinitiv Lipper data. Money flows have been in to U.S. equity-focused stock and mutual funds for four of the past six weeks.

The U.S., relative to large economies outside of the states is better; employment is strong, there are expectations that a long protracted recession isn’t likely, and consumer spending hasn’t faded, while price increases (inflation) have been tapered.

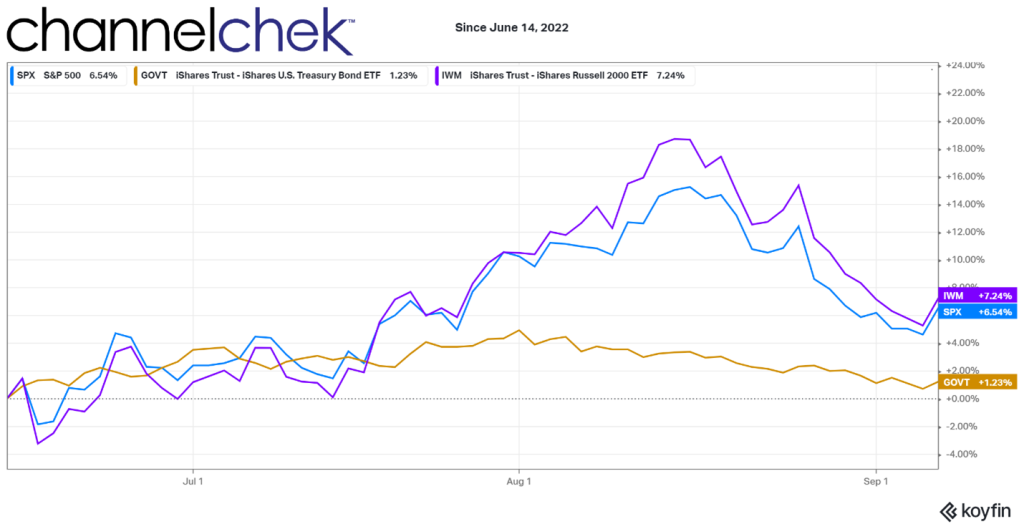

Recent performance of U.S. markets has been impressive. Since the low point of the year (June 14), the small-cap Russell 2000 index is up 7.2%, the S&P 500 is up 6.5% and even U.S. Treasuries are positive despite the Fed’s stated intention of higher rates.

The S&P 500 has outpaced major stock indexes in Europe and Asia since hitting its low for the year in mid-June, meanwhile the pan-continental Stoxx Europe 600 has added only 2.9%, Japan’s Nikkei 225 has advanced 4.5%. Germany’s DAX and the Shanghai Composite have slid 1.3% over the same period.

And there is one other self-fulfilling incentive for U.S. dollar-denominated assets; the dollar has surged to a 20-year high relative to a standard basket of global currencies. To date it is 25.2% stronger than the yen, it increased 12.2% higher versus the euro, and gained 15% above the British pound. Even with the U.S. major indices down, investor conversion back to non-U.S. native currency is a big win compared to what they would have lost. And for U.S. investors that were in international markets, they are better off having repatriated their dollars, even if they are down on the year.

The longer the dollar’s strength continues, the more the strength will feed on itself.

What investors should pay particular attention to now is anything that may trigger a turnaround, and money going back into international markets. This does not seem imminent, but it helps to know what is making “other shirts dirtier.”

Among Europe’s challenges are war-related supply shortages which have led to skyrocketing gas and electricity prices. Recently added to the list, Russia’s Gazprom PJSC said Friday (Sept. 2), that it would suspend the Nord Stream natural-gas pipeline to Germany. Winter is coming and the continent is on the path to a worsening energy problem, one that would add to upward inflation pressures for them.

China the world’s second-largest economy, has been severely weakened by the impact of its response to Covid-19. Other factors weighing on its economy are a real-estate downturn, heightened regulation of technology companies, and unusually bad weather. Weakness in China creates problems for economies around the globe since much of the world’s commodities and manufacturing come from the country.

A turnaround in these factors, such as a friendly resolution to the war, increased productivity from China, or lower inflation across Europe and the tide may turn causing more investment to gravitate away from the U.S., creating less demand for assets here. To date, there is no sign that any of these possibilities are imminent, and the longer the U.S. is the only game in town, the more money will be kept in U.S. dollar assets and the more upward pressure there will be on these assets.

What We Can Learn About SPAC Investments from Trump Media/DWAC

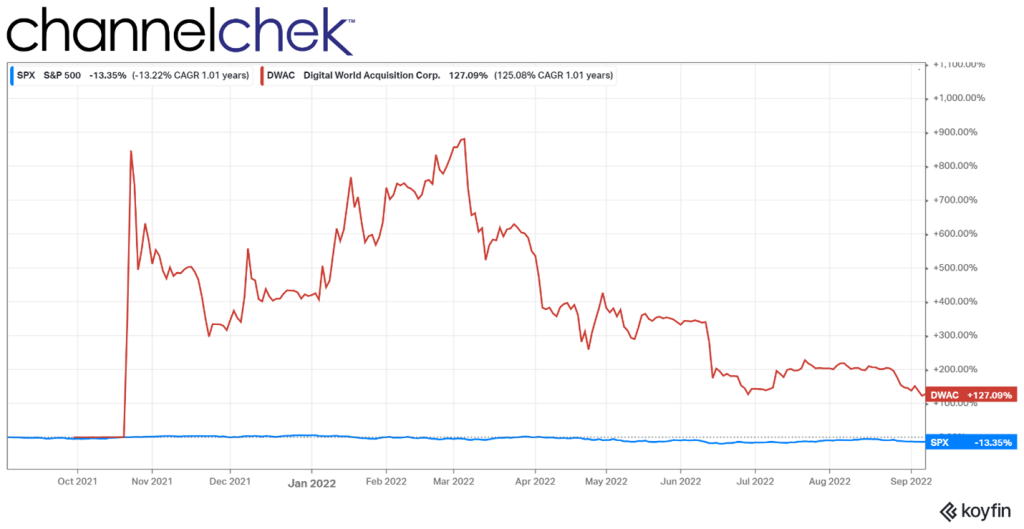

Digital World Acquisition Corp. (DWAC), the special purpose acquisition corporation (SPAC) that agreed to merge with Trump Media (TMTG), and take it public a year ago, needs 65% shareholder approval to extend its acquisition deadline by a year. The uncertainty over whether the SPAC would get the necessary votes to merge with the social media startup caused profit taking in the SPAC which still trades at more than double its IPO price.

Reuters reported late Monday (September 5), there has not been enough votes to reach a 65% threshold of “in favor” shareholder support to extend the merger completion date by one-year. A shareholder meeting Tuesday was adjourned and will resume on Thursday (September 8) where they will take up voting again.

In a federal filing Tuesday, DWAC said that if shareholders do not approve the extension, its sponsor, ARC Global Investments, would contribute about $2.9 million to extend the deadline until Dec. 8, 2022. The purpose of the deadline is to make time for all parties to address government investigations into the deal and make other necessary disclosures. If the three-month extension doesn’t prove to be enough time, another three-month extension is possible. This won’t be necessary if the shareholder vote garners a 65% approval of the extension.

After any SPAC exhausts extension options, it is faced with a final deadline. Should it not make the deadline, it must liquidate and return cash to shareholders. Such deadlines and extensions are commonplace in the world of SPACs. Scrambling for the parties to meet deadlines is not uncommon in SPAC merger deals. What is interesting in the DWAC TMTG acquisition is there are original IPO investors that at the time did not know who Digital World would unearth as a target candidate. They paid the $10 IPO price and, within a month, saw their share price jump up more than 800%. Even today these investors are up 124%, and if the SPAC liquidated tomorrow (near $10 per share) they will have outperformed the S&P 500 by double digits.

No matter the results, the SPAC IPO investors could consider themselves as having done better investing in the SPAC than most alternatives. But there are presumably also shareholders that bought shortly after the merger announcement that if liquidated and all the money held in escrow is returned, could lose several times their investment depending on what price they chased it to.

Shareholder voting is seldom in person and instead takes place by phone, online or via mail. Shareholders are urged to vote as reaching a 65% base of shareholders is difficult enough, reaching a 65% threshold of shareholders voting one way or another is even more difficult. Digital World Chief Executive Patrick Orlando said last week the SPAC was having trouble getting enough individuals to vote through their brokers.

The SPAC is held by a high percentage of retail accounts, this may explain the lack of voting. Failure to approve the extension will almost certainly cost current holders of DWAC money. If the deal falls through, shareholders will get roughly $10 a share, about half of the current share price.

Should the merger succeed, Digital World Acquisition would provide about $290 to the former president’s company. This could go a long way in building the brand and user base. Additionally, it is said that the two sides have investor commitments for roughly $1 billion private investment in public equity (PIPE), that would close alongside the merger.

TMTG raised about $20 million in convertible bonds last year and an additional $15 million in the first quarter of 2022. If the SPAC deal falls through there are options to keep the fledgling media company alive as a private company. On TMTG’s Truth Social on Friday, the former president responded to worries about the SPAC merger by saying, “In any event, I don’t need financing. ‘I’m really rich!’ Private company anyone?”

The Story of War and Peace in the Currency Markets

There is a story of war and peace in the contemporary currency markets. It has a main plot and many subplots. As yet, the story is without end. That may come sooner than many now expect.

The narrator today has a more challenging job than the teller of the story about neutral, Entente, and Central Power currencies during World War I. (See Brown, Brendan “Monetary Chaos in Europe” chapter 2 [Routledge, 2011].)

Today’s Russia war (whether the military conflict in Ukraine or the EU/US-Russia economic war) is not so all-pervasive in global economic and monetary affairs, though it is doubtless prominent. The monetary setting of the story today is much more nuanced than in World War I when the prevailing expectation was that peace would mark the start of a journey where key currencies eventually returned to their prewar gold parities.

In the 1914–18 conflict, any sudden news of a possible end to the conflict—as with the peace notes of President Woodrow Wilson in December 1916—would cause a sharp fall of the neutral currencies (Swiss franc, Dutch guilder, Spanish peseta), a big rise in the German mark and Austrian-Hungarian crown, and lesser rises in sterling and the French franc. Today, in principle, a sudden emergence of peace diplomacy would most plausibly send the euro and British pound higher on the one hand and the Canadian dollar, US dollar, and Swiss franc lower on the other hand.

Mutual exhaustion and military stalemate are a combination from which surprise diplomatic moves to end war can emerge. These circumstances apply today.

Ukraine is falling into an economic abyss—much of its infrastructure reportedly destroyed and its government is resorting to the money printing press to pay its soldiers (see Kenneth Rogoff et al., “Macroeconomic Policies for Wartime Ukraine,” Center for Economic and Policy Research, August 12, 2022). General economic aid from Western donors (as against military aid) is running far short of promises. All these pictures of Russian munitions stores on fire may or may not have excited some potential donors, but they have not heralded any breakthrough.

The human toll—both amongst military personnel and civilians—fans Moscow propaganda that the US and UK are willing to conduct their proxy war against Russia down to the life of the last Ukrainian soldier.

Meanwhile there are these presumably leaked stories in the Washington Post about how President Volodymyr Zelensky betrayed the Ukrainian people by not sharing with them in late 2021 and early 2022 the US intelligence alerts about a looming Russian invasion. According to the stories, many Ukrainians resent that they were not warned by their government and do not accept its shocking excuses (for example, to prevent a flight of capital out of the country).

Is all this preparing ground for a possible power shift in Kiev that might favor an early diplomatic solution even in time for President Joe Biden to claim credit ahead of the midterms? Western Europe will be spared some pain this winter if the initial ceasefire agreement includes a provision that Moscow desist from turning off the gas pipelines.

The purpose here is not to predict the war’s outcome but to describe a peace scenario that is within the mainstream and to map out how the rising likelihood of its realization would influence currency markets.

The main channel of influence on currencies would be the course of the EU/US-Russia economic war. A ceasefire would excite expectations of big relief to the natural gas shortage in Western Europe.

Prices there for natural gas would plunge. In turn, that would lift consumer and business spirits, now depressed by feared astronomic gas bills and even gas rationing this winter. Massive programs to relieve fuel poverty, financed by monetary inflation, would stop in their tracks. The European Central Bank (ECB) could move resolutely to tighten monetary conditions as the depression fears faded.

We could well imagine that the peace scenario would mean the European economies in 2023 would rebound from a winter downturn. That would coincide with the US economy sinking into recession as the “Powell disinflation” works its way through—including continued bubble bursting in the tech space and residential construction sector plus a possible private equity bust.

A big rise of the euro under the peace scenario, though likely, is not a slam-dunk proposition. Russia might delay turning the gas pipelines back on until there is an assurance about its central bank’s frozen deposits in Western Europe. There has been chatter from the top of the Organisation for Economic Co-operation and Development (OECD) down that a reparations commission would sequester these.

More broadly, it could be that most European households are not cutting back their spending to the extent assumed in the consensus economic forecasts. Many individuals may have never believed that the high natural gas prices would persist beyond this winter. Then they faced, in effect, a transitory rather than permanent tax rise. Economic theory suggests that such transitory taxes, paid in this case to North American natural gas producers, have much less impact than permanent ones on spending.

There are still the deep ailments of the euro. How can the ECB ever normalize monetary conditions when so much of the monetary base is backed by loans and credits to weak sovereigns and banks (see Brendan Brown, “ECB’s Long Journey into Currency Collapse Just Got a Lot Shorter,” Mises Wire, July 23, 2022)?

In principle, the US dollar, and even more so the Canadian dollar, would lose from peace as they have gained from war. Both have obtained fuel from the boom in their issuing country’s energy sector. In neither country has there been aggregate real income loss due to the economic war—in fact, there has been a gain in the case of Canada. A further positive for the US dollar has been the boom in the US armaments sector—and this should continue beyond a ceasefire.

Peace will not deflect Europe from seeking to diversify its energy supplies away from Russia and to North American gas and to renewables. But we can imagine that in the long-run, Germany could have a comparative advantage in the renewable space; and North America could lose potential sales outside Europe to Russian gas at discounted prices. Russia is widely expected to prioritize a vamped-up construction program for LNG (liquid natural gas) terminals. These will enable the export of its natural gas to world markets.

Bottom line: peace is likely to be a negative for the US dollar. But transcending this influence is the huge issue of how and when US monetary inflation regains virulence.

About the Author:

Brendan Brown is a founding partner of Macro Hedge Advisors (www.macrohedgeadvisors.com) and senior fellow at Hudson Institute. He is an international monetary and financial economist, consultant, and author, his roles have included Head of Economic Research at Mitsubishi UFJ Financial Group and is also a Senior Fellow of the Mises Institute. Brendan authored Europe’s Century of Crises under Dollar Hegemony: A Dialogue on the Global Tyranny of Unsound Money with Philippe Simonnot.

The article was republished with permission from The Mises Institute. The original version can be found here.