Apple has once again proven its staying power in the global tech landscape, briefly touching a $4 trillion market capitalization before pulling back slightly. The milestone underscores renewed investor optimism as strong early sales of the new iPhone 17 lineup signal that Apple’s growth engine remains alive and well.

According to data from Counterpoint Research, the iPhone 17 series outperformed its predecessor, the iPhone 16, during its first 10 days of release in both the U.S. and China—two of Apple’s most important markets. Year over year, iPhone sales surged 14%, with the base iPhone 17 and high-end iPhone 17 Pro drawing the most attention from consumers. The newly introduced iPhone Air also saw solid momentum, slightly outselling the discontinued iPhone Plus.

Apple’s stock climbed on the back of these strong figures, propelling its valuation into the $4 trillion club alongside fellow tech giants Nvidia and Microsoft. While Apple has flirted with this threshold before, the combination of resilient hardware demand and ongoing investor confidence helped push it back into record territory.

Still, not all analysts are convinced the sales surge will hold steady. Recent tracking from Jefferies suggests iPhone demand may be cooling slightly week over week, with delivery lead times shortening across major markets. In the U.S. and Europe, the once-long waits for iPhone 17 Pro and Pro Max models have largely disappeared, hinting that initial supply bottlenecks have eased.

Even so, Apple’s iPhone remains its crown jewel. The device generated $201.2 billion in revenue in 2024, more than half of the company’s total $391 billion. Its Services segment—covering everything from Apple TV+ to iCloud—added another $96.2 billion, showcasing the company’s ability to diversify beyond hardware.

Unlike Nvidia and Microsoft, whose valuations have surged on the strength of artificial intelligence development, Apple has taken a more measured approach. The company has yet to unveil its long-awaited AI-powered version of Siri, even as competitors like Google and Samsung continue to push forward with AI-enhanced products such as Gemini and Galaxy AI.

Despite that, Apple’s ecosystem remains unmatched. With over one billion active iPhones worldwide, along with a growing base of Apple Watch, AirPods, and service subscribers, the company benefits from an unparalleled level of customer loyalty. Each product launch not only drives revenue but reinforces a network of users deeply embedded in Apple’s ecosystem.

For investors, the story is clear: Apple may not be leading the AI revolution—yet—but its scale, cash flow, and brand strength continue to make it one of the most dependable growth stories in global markets. The $4 trillion mark is less about a temporary milestone and more about a company that continues to define what long-term market dominance looks like.

MIAMI, Oct. 09, 2025 (GLOBE NEWSWIRE) — SKYX Platforms Corp. (NASDAQ: SKYX) (d/b/a SKYX Technologies) (the “Company” or “SKYX”), a highly disruptive platform technology company with over 100 pending and issued patents globally and over 60 lighting and home décor websites, with a mission to make homes and buildings become safe and smart as the new standard, today provided the following corporate updated on its progress.

Market Acceptance, Progress and Recent Events:

After reporting 15.7 million in cash and cash equivalents as of June 30, 2025, SKYX has raised an additional $3.25 million in September from an existing lead investor.

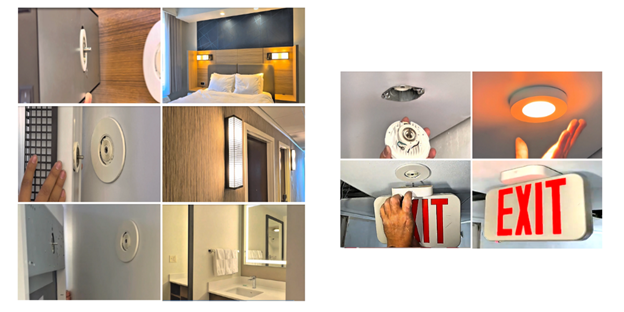

SKYX has successfully demonstrated its technology during a Marriott Hotel renovation, incorporating its advanced and smart plug & play technologies, including ceiling lighting, recessed lights, downlights, wall lights, EXIT, and EMERGENCY lights, plug-in LED backlight mirrors among others. For Marriott video demo CLICK HERE.

SKYX will supply more than 10,000 of its advanced smart plug-and-play technologies to a 278-apartment project in Austin, Texas, being developed by Landmark Companies — a prominent developer with 27 years of experience and a track record of building tens of thousands of modern homes and buildings across Texas, Florida, Colorado, and other locations. For information about Landmark Companies projects Click Here.

SKYX is expected to deploy over 500,000 units of its advanced Plug & Play smart home technologies to Miami’s $3 billion mixed-use Urban Smart Home City project, located in the heart of the city. The Plug & Play smart home technologies will include SKYX’s AI-powered ecosystem, its all-in-one smart home platform technology, as well as ceiling lighting, recessed lights, downlights, wall lights, EXIT, and EMERGENCY lights, plug-in LED backlight mirrors among others. SKYX’s full suite of smart platform products will be utilized throughout the entire project.

The groundbreaking Smart Home Mixed-Use Major Urban Development Will Redefine Miami’s Urban Landscape

The architecture and design of the Miami Smart Home City is led by world-renowned architectural firm Arquitectonica. The $3 billion development is led by SG Holdings, a distinguished joint venture comprised of Swerdlow Group, SJM Partners, and Alben Duffie—each renowned for transformative urban projects.

SKYX has financial backing from U.S. and global manufacturers to support its massive product deployment.

SKYX’s Safety Code Standardization Team has gained the support of a prominent new leader who is actively engaging with key government safety organizations — marking a significant step forward in the Company’s efforts to establish mandatory safety standardization for its advanced safe ceiling technologies.

SKYX is progressing toward a winter launch of its turbo heater & ceiling fan to support its path to cash-flow positivity in 2025. The ceiling fan and space heater category represents a multi-billion-dollar market with tens of millions of units sold annually in the U.S.

Management is expecting to secure additional significant business opportunities.

Company expects its products to be in 50,000 U.S. and Canadian units-home Management expects to achieve its goal of being cash flow positive by the end of 2025.

SKYX revenues increased for 6 comparable quarters from Q1 2024 through Q2 2025 with $19M in Q1/24, 21.4M in Q2/24, $22.2M in Q3/24, $23.7M in Q4/24, $20.1M in Q1/25, and $23.1M in Q2/25

Net cash used in operating activities for the Second quarter ending June 30, 2025, decreased sequentially by 54% to $2.0 million compared to $4.3 million in the First quarter of 2025.

The gross profit for the Second quarter ending June 30, 2025, increased sequentially by 23% to $7.0 million, compared to the First quarter ending March 31, 2025.

The gross margin for the Second quarter ending June 30, 2025, increased sequentially by 7% to 30.3%, compared to the First quarter ending March 31, 2025.

Management expects to achieve its goal of being cash flow positive by the end of 2025.

SKYX revenues increased for 6 comparable quarters from Q1 2024 through Q2 2025 with $19M in Q1/24, $21.4M in Q2/24, $22.2M in Q3/24, $23.7M in Q4/24, $20.1M in Q1/25, and $23.1M in Q2/25

Net cash used in operating activities for the Second quarter ending June 30, 2025, decreased sequentially by 54% to $2.0 million compared to $4.3 million in the First quarter of 2025.

The gross profit for the Second quarter ending June 30, 2025, increased sequentially by 23% to $7.0 million, compared to the First quarter ending March 31, 2025.

The gross margin for the Second quarter ending June 30, 2025, increased sequentially by 7% to 30.3%, compared to the First quarter ending March 31, 2025.

Over the past year, SKYX has secured a total of $15 million in investments from strategic investors, led by global Marriott Hotel chain owner. The round also included significant participation from company insiders — including SKYX President Steve Schmidt, CEO Lenny Sokolow and former CEO John Campi — underscoring their continued confidence in SKYX’s strategic vision and growth trajectory.

As common with companies such as ours when sales are converted into cash rapidly, often referred to as the “Dell Working Capital Model”, the Company leverages its trades payable to finance its operations, to enhance its cash position and to lower its cost of capital.

The Company announced a U.S. strategic manufacturing partnership with Profab Electronics, a premier electronics contract manufacturer based in Pompano Beach, Florida. This collaboration marks a significant step forward in SKYX’s commitment to building a resilient, efficient, and localized supply chain for its innovative product lines. This is in addition to manufacturing collaborations in Vietnam, Taiwan, China and Cambodia.

The Company strongly believes its products have the potential to save insurance companies billions of dollars annually by reducing the risks of fires, ladder falls, electrocutions, and other related incidents. Management expects that once the full range and variations of its safe plug-and-play products are completed, they will begin to be recommended by insurance companies.

SKYX’s technologies provide opportunities for recurring revenues through interchangeability, upgrades, monitoring, and subscriptions. Company is focused on the “Razor & Blades” model and its product range includes its advanced ceiling electrical outlet (Razor) and its advance and smart home plug & play products (Blades) including its advance and smart home plug & play platform products, lighting, recessed lights, down lights, EXIT signs, emergency lights, ceiling fans, chandeliers/pendants, holiday/kids/themes lights, indoor/outdoor wall lights among other. Company’s plug & play technology enables an installation of lighting, fans, and smart home products in high-rise buildings and hotels within days rather than months.

Company’s total addressable market (TAM) in the U.S. is roughly $500 billion with over 4.2 billion ceiling applications in the U.S. alone. Expected revenue streams from retail and professional segments include product sales, royalties, licensing, subscription, monitoring, and sale of global country rights.

Company continues to utilize its e-commerce platform of over 60 websites for lighting and home décor to educate and enhance its market penetration to both retail and professional segments.

Company is collaborating with Home Depot and Wayfair for Its Advanced and Smart Plug & Play products for both retail and professional segments. SKYX’s product offering will include a variety of its advanced and Smart Plug & Play products including Retrofit Kits, Smart Light Fixtures, Smart Ceiling Fans, Ceiling Outlet Receptacles, Recessed Lights and more.

SKYX collaborates with U.S. and world leading lighting companies including Kichler Quoizel, European leading company, EGLO, and worlding lighting manufacturer Ruee.

Collaborated with Cavco Homes, a leading U.S. prefabricated home manufacturer, for integrating our advanced and smart plug & play technologies into Cavco’s high-end premium homes shown at the builder show. Cavco is a public company that has sold nearly one million homes and continues to deliver close to 20,000 annually.

Three luxury developments by Forte Developments, including an 80-story high-rise in Miami’s Brickell District and projects in Clearwater Beach and Jupiter, Florida, will feature SKYX’s technology. More than 12,000 smart plug & play products, including ceiling outlets, lighting, fans, and emergency fixtures, will be supplied across 400+ units. A 1,000-unit mixed-use development by Jeremiah Baron Companies will incorporate smart plug & play technologies, with 140 units receiving initial product supply. This product rollout will include ceiling outlets, lighting, fans, and emergency fixtures, with deliveries continuing throughout construction.

A strategic partnership with JIT Electrical Supply, a leading builder supplier, will expand SKYX’s footprint in electrical, lighting, and ceiling fan markets. JIT, which has supplied over 100,000 U.S. homes, will distribute SKYX’s lighting solutions, ceiling fans, recessed lights, emergency lights, exit signs, and indoor/outdoor wall lights beginning early 2025.

Huey Long, former Amazon E-Commerce Director and executive at Walmart and Ashley Furniture, has joined as head of SKYX’s e-commerce platform. He will collaborate with the existing team to expand market penetration across 60 lighting and home décor websites and other key e-commerce channels in the U.S. and Canada.

Safety Standardization Mandatory Code / Insurance Specification and Recommendation

SKYX’s Safety Code Standardization Team is receiving support from a new significant prominent leader with its government safety agency’s process for a safety mandatory standardization of its electrical ceiling outlet/receptacle technology.

SKYX’s code team, led by industry veterans Mark Earley, former head of the National Electrical Code (NEC), and Eric Jacobson, former President and CEO of the American Lighting Association (ALA). Company’s safety Code Standardization team believes it will achieve assistance from additional safety organizations with its code mandatory safety standardization efforts based on the product’s significant safety aspects. Mr. Earley and Mr. Jacobson were instrumental in numerous code and safety changes in both the electrical and lighting industries. Both strongly believe that, considering the Company’s standardization progress including its product specification approval voting for by ANSI / NEMA (American National Standardization Institute / National Electrical Manufacturers Association) and being voted into 10 segments in the NEC Code Book, it has met the necessary safety conditions for becoming a ceiling safety standardization requirement for homes and buildings.

With respect to insurance companies, the Company strongly believes its products can save insurance companies many billions of dollars annually by reducing fires, ladder falls, and electrocutions among other things. Management expects that once it completes an entire range and variations of its safe advanced plug & play products it will start being recommended by insurance companies.

As electricity is a standard in every home and building, our mission is to make homes and buildings become safe-advanced and smart as the new standard. SKYX has a series of highly disruptive advanced-safe-smart platform technologies, with over 100 U.S. and global patents and patent pending applications. Additionally, the Company owns over 60 lighting and home decor websites for both retail and commercial segments. Our technologies place an emphasis on high quality and ease of use, while significantly enhancing both safety and lifestyle in homes and buildings. We believe that our products are a necessity in every room in both homes and other buildings in the U.S. and globally. For more information, please visit our website at https://skyplug.com/ or follow us on LinkedIn.

Forward-Looking Statements

Certain statements made in this press release are not based on historical facts but are forward-looking statements. These statements can be identified by the use of forward-looking terminology such as “aim,” “anticipate,” “believe,” “can,” “could,” “continue,” “estimate,” “expect,” “evaluate,” “forecast,” “guidance,” “intend,” “likely,” “may,” “might,” “objective,” “ongoing,” “outlook,” “plan,” “potential,” “predict,” “probable,” “project,” “seek,” “should,” “target” “view,” “will,” or “would,” or the negative thereof or other variations thereon or comparable terminology, although not all forward-looking statements contain these words. These statements reflect the Company’s reasonable judgment with respect to future events and are subject to risks, uncertainties and other factors, many of which have outcomes difficult to predict and may be outside our control, that could cause actual results or outcomes to differ materially from those in the forward-looking statements. Such risks and uncertainties include statements relating to the Company’s ability to successfully launch, commercialize, develop additional features and achieve market acceptance of its products and technologies and integrate its products and technologies with third-party platforms or technologies; the Company’s efforts and ability to drive the adoption of its products and technologies as a standard feature, including their use in homes, hotels, offices and cruise ships; the Company’s ability to capture market share; the Company’s estimates of its potential addressable market and demand for its products and technologies; the Company’s ability to raise additional capital to support its operations as needed, which may not be available on acceptable terms or at all; the Company’s ability to continue as a going concern; the Company’s ability to execute on any sales and licensing or other strategic opportunities; the possibility that any of the Company’s products will become National Electrical Code (NEC)-code or otherwise code mandatory in any jurisdiction, or that any of the Company’s current or future products or technologies will be adopted by any state, country, or municipality, within any specific timeframe or at all; risks arising from mergers, acquisitions, joint ventures and other collaborations; the Company’s ability to attract and retain key executives and qualified personnel; guidance provided by management, which may differ from the Company’s actual operating results; the potential impact of unstable market and economic conditions on the Company’s business, financial condition, and stock price; and other risks and uncertainties described in the Company’s filings with the Securities and Exchange Commission, including its periodic reports on Form 10-K and Form 10-Q. There can be no assurance as to any of the foregoing matters. Any forward-looking statement speaks only as of the date of this press release, and the Company undertakes no obligation to update or revise any forward-looking statements, whether as a result of new information, future events or otherwise, except as required by U.S. federal securities laws.

Investor Relations Contact: Jeff Ramson PCG Advisory [email protected]

SKYX is Expected to Supply Over 10,000 Units Including its Advanced Smart Plug & Play Technologies comprising Ceiling Lighting, Ceiling Fans, Recessed Lights, Down Lights, EXIT Signs, Emergency Lights, Indoor and Outdoor Wall Lights Among Other Advanced Smart Products

Landmark Companies are Prominent Developers with 27 Years of Experience Building Tens of Thousands of Units Specializing in Modern Homes and Buildings with Over 3000 Units in Development in Texas, Florida, and Colorado, Among Other Locations

SKYX and Landmark are Expected to Collaborate on Additional Upcoming Landmark Projects

MIAMI, Oct. 01, 2025 (GLOBE NEWSWIRE) — SKYX Platforms Corp. (NASDAQ: SKYX) (d/b/a SKYX Technologies) (the “Company” or “SKYX”), a highly disruptive platform technology company with over 100 pending and issued patents globally and over 60 lighting and home décor websites, with a mission to make homes and buildings become safe and smart as the new standard, today announced that it will supply its advanced smart plug and play technologies to a 278-apartment project in the Austin Manor area in Texas. The 278-apartment project is led by prominent developers Landmark Companies. The project will feature a wide range of amenities, including swimming pools, a state-of-the-art gym, modern meeting conference facilities, and landscaped green spaces, among others.

SKYX is expected to provide over 10,000 units of its advanced and smart plug & play technologies, including ceiling lighting, recessed lights, downlights, wall lights, EXIT, and EMERGENCY lights, plug-in LED backlight mirrors among other SKYX products.

Landmark Companies are prominent developers with 27 Years of experience building tens of thousands of units specializing in modern homes and buildings in Texas, Florida and Colorado, among other locations.

Julia Baytler, CEO of Landmark Companies, said; “We are excited to collaborate with SKYX to bring their innovative technologies into our Austin Manor project. At Landmark, our focus has always been on creating modern, high-quality living spaces that enhance the daily lives of our residents. By integrating SKYX’s advanced plug-and-play solutions, we are raising the standard of safety, convenience, and design for our communities, and we look forward to expanding this collaboration across future developments.”

Rani Kohen, Founder and Executive Chairman, of SKYX Platforms, said; “We are very pleased to be working with prominent developers like Landmark Companies. We look forward to collaborating with them to enhance home values while creating safer, more advanced, and smarter buildings for the future.”

As electricity is a standard in every home and building, our mission is to make homes and buildings become safe-advanced and smart as the new standard. SKYX has a series of highly disruptive advanced-safe-smart platform technologies, with over 100 U.S. and global patents and patent pending applications. Additionally, the Company owns over 60 lighting and home decor websites for both retail and commercial segments. Our technologies place an emphasis on high quality and ease of use, while significantly enhancing both safety and lifestyle in homes and buildings. We believe that our products are a necessity in every room in both homes and other buildings in the U.S. and globally. For more information, please visit our website at https://skyplug.com/ or follow us on LinkedIn.

Forward-Looking Statements Certain statements made in this press release are not based on historical facts but are forward-looking statements. These statements can be identified by the use of forward-looking terminology such as “aim,” “anticipate,” “believe,” “can,” “could,” “continue,” “estimate,” “expect,” “evaluate,” “forecast,” “guidance,” “intend,” “likely,” “may,” “might,” “objective,” “ongoing,” “outlook,” “plan,” “potential,” “predict,” “probable,” “project,” “seek,” “should,” “target” “view,” “will,” or “would,” or the negative thereof or other variations thereon or comparable terminology, although not all forward-looking statements contain these words. These statements reflect the Company’s reasonable judgment with respect to future events and are subject to risks, uncertainties and other factors, many of which have outcomes difficult to predict and may be outside our control, that could cause actual results or outcomes to differ materially from those in the forward-looking statements. Such risks and uncertainties include statements relating to the Company’s ability to successfully launch, commercialize, develop additional features and achieve market acceptance of its products and technologies and integrate its products and technologies with third-party platforms or technologies; the Company’s efforts and ability to drive the adoption of its products and technologies as a standard feature, including their use in homes, hotels, offices and cruise ships; the Company’s ability to capture market share; the Company’s estimates of its potential addressable market and demand for its products and technologies; the Company’s ability to raise additional capital to support its operations as needed, which may not be available on acceptable terms or at all; the Company’s ability to continue as a going concern; the Company’s ability to execute on any sales and licensing or other strategic opportunities; the possibility that any of the Company’s products will become National Electrical Code (NEC)-code or otherwise code mandatory in any jurisdiction, or that any of the Company’s current or future products or technologies will be adopted by any state, country, or municipality, within any specific timeframe or at all; risks arising from mergers, acquisitions, joint ventures and other collaborations; the Company’s ability to attract and retain key executives and qualified personnel; guidance provided by management, which may differ from the Company’s actual operating results; the potential impact of unstable market and economic conditions on the Company’s business, financial condition, and stock price; and other risks and uncertainties described in the Company’s filings with the Securities and Exchange Commission, including its periodic reports on Form 10-K and Form 10-Q. There can be no assurance as to any of the foregoing matters. Any forward-looking statement speaks only as of the date of this press release, and the Company undertakes no obligation to update or revise any forward-looking statements, whether as a result of new information, future events or otherwise, except as required by U.S. federal securities laws.

Investor Relations Contact: Jeff Ramson PCG Advisory [email protected]

Successfully completed AI pilot with Microsoft – now live – boosts fraud detection

FLORHAM PARK, N.J. — Conduent Incorporated (Nasdaq: CNDT), a global technology-driven business solutions and services company, is embedding generative AI (GenAI) and other advanced AI technologies into its suite of solutions for state and federal agencies. These technologies aim to improve the disbursement of critical government benefits, enhance the citizen experience, and fortify fraud prevention across major aid programs like Medicaid and the Supplemental Nutrition Assistance Program (SNAP).

As part of a recently completed GenAI pilot with Microsoft – originally announced in 2024 and now fully deployed – Conduent has significantly increased its fraud detection capacity for its largest open-loop payment card programs. Because these cards can be used at a wide range of merchants, monitoring for fraud is particularly complex. Leveraging AI, a small team of specialists can now surveil tens of thousands of accounts for suspicious activity, including identity theft and account takeover with significant improvement in accuracy. This capability is in the process of being scaled to other payment card programs.

Following the pilot’s success, Conduent is now seeking to apply similar AI methodologies to help detect and prevent fraud in Medicaid and closed-loop EBT cards, including SNAP benefits – helping safeguard usage at approved retailers. A leader in government payment disbursements, Conduent currently supports electronic payments for public programs in 37 states.

“As states adapt to evolving budget constraints and eligibility requirements, AI can empower agencies to reduce fraud and improper payments while improving service delivery,” said Anna Sever, President, Government Solutions at Conduent. “With decades of experience supporting critical government programs, Conduent is deepening its investment in AI to expand these gains across multiple programs.”

Transforming Customer Support with AI

Conduent is also deploying AI to drive improvements in the contact center experience for public benefit recipients. A standout example is the Conduent GenAI-powered capability that equips agents with instant access to accurate, program-specific information – reducing call handling times.

Conduent provides U.S. agencies with solutions for healthcare claims administration, government benefit payments, eligibility and enrollment, and child support. Visit Conduent Government Solutions to learn more.

About Conduent

Conduent delivers digital business solutions and services spanning the commercial, government and transportation spectrum – creating valuable outcomes for its clients and the millions of people who count on them. The Company leverages cloud computing, artificial intelligence, machine learning, automation and advanced analytics to deliver mission-critical solutions. Through a dedicated global team of approximately 56,000 associates, process expertise and advanced technologies, Conduent’s solutions and services digitally transform its clients’ operations to enhance customer experiences, improve performance, increase efficiencies and reduce costs. Conduent adds momentum to its clients’ missions in many ways including disbursing approximately $85 billion in government payments annually, enabling 2.3 billion customer service interactions annually, empowering millions of employees through HR services every year and processing nearly 13 million tolling transactions every day. Learn more at www.conduent.com.

Conduent is a trademark of Conduent Incorporated in the United States and/or other countries. Other names may be trademarks of their respective owners.

SKYX’s Marriott Renovation Demonstration Validated the Significant Safety, Simplicity, Time Savings and Cost Savings Provided by SKYX’s Technologies During a Renovation Process

The Marriott Renovation Demo Incorporated SKYX’s Advanced and Smart Plug & Play Technologies, Including Ceiling lighting, Recessed Lights, Down Lights, Wall Lights, EXIT and Emergency Lights, Plug-In LED Backlight Mirrors, Among Others

SKYX Expects Its Technologies to Be Utilized and Included in Additional Marriot Renovations as well as in Additional Hotel Brands

Major Hotel Chains Commonly Require Its Hotels to Conduct a Full Renovation Every 7 Years

MIAMI, Sept. 03, 2025 (GLOBE NEWSWIRE) — SKYX Platforms Corp. (NASDAQ: SKYX) (d/b/a SKYX Technologies) (the “Company” or “SKYX”), a highly disruptive platform technology company with over 100 pending and issued patents globally and over 60 lighting and home décor websites, with a mission to make homes and buildings become safe and smart as the new standard, today announced that it successfully demonstrated its advanced technologies during a renovation at a Marriott SpringHill Suites Hotel owned by the Shaner Group as SKYX continues to grow its market penetration in U.S. and Canada (renovation video demo link included below).

During the Marriott renovation demonstration, SKYX incorporated its advanced and smart plug & play technologies, including ceiling lighting, recessed lights, downlights, wall lights, EXIT, and EMERGENCY lights, plug-in LED backlight mirrors among others.

SKYX’s Marriott renovation demonstration validated the significant safety aspects, time savings, and cost savings provided by SKYX’s technologies during a hotel renovation process. Major hotel chains commonly require its hotels to conduct a full renovation every 7 years. SKYX expects its technologies to be utilized and included in additional Marriott renovations as well as in other hotel brands.

SKYX Technologies’ demonstration at Marriot

Rani Kohen, Founder and Executive Chairman, of SKYX Platforms, said; “We are happy to report that we have successfully demonstrated our technology’s ability to provide significant hotel safety, time savings and cost savings during hotel renovation and buildouts while advancing and accelerating the renovation of hotels. We hope to continue demonstrating our technologies’ abilities in additional projects and remain focused on further scaling our footprint and unlocking long-term value through future recurring revenue opportunities.”

Lance Shaner, Founder of the Shaner Hotel Group, said; “We clearly recognize SKYX’s significant value of time saving, cost saving, and safety as demonstrated during our Marriott SpringHill Suites hotel renovation. As a significant long-term minded SKYX investor, I strongly believe that SKYX’s game-changing advanced and smart platform technologies will make hotels, buildings, and homes advanced, smart, and safe instantly, while saving cost, time, and lives.”

To view SKYX’s Technology Demo at Springs Hill Marriott CLICK HERE

About SKYX Platforms Corp.

As electricity is a standard in every home and building, our mission is to make homes and buildings become safe-advanced and smart as the new standard. SKYX has a series of highly disruptive advanced-safe-smart platform technologies, with over 100 U.S. and global patents and patent pending applications. Additionally, the Company owns over 60 lighting and home decor websites for both retail and commercial segments. Our technologies place an emphasis on high quality and ease of use, while significantly enhancing both safety and lifestyle in homes and buildings. We believe that our products are a necessity in every room in both homes and other buildings in the U.S. and globally. For more information, please visit our website at https://skyplug.com/ or follow us on LinkedIn.

Forward-Looking Statements Certain statements made in this press release are not based on historical facts but are forward-looking statements. These statements can be identified by the use of forward-looking terminology such as “aim,” “anticipate,” “believe,” “can,” “could,” “continue,” “estimate,” “expect,” “evaluate,” “forecast,” “guidance,” “intend,” “likely,” “may,” “might,” “objective,” “ongoing,” “outlook,” “plan,” “potential,” “predict,” “probable,” “project,” “seek,” “should,” “target” “view,” “will,” or “would,” or the negative thereof or other variations thereon or comparable terminology, although not all forward-looking statements contain these words. These statements reflect the Company’s reasonable judgment with respect to future events and are subject to risks, uncertainties and other factors, many of which have outcomes difficult to predict and may be outside our control, that could cause actual results or outcomes to differ materially from those in the forward-looking statements. Such risks and uncertainties include statements relating to the Company’s ability to successfully launch, commercialize, develop additional features and achieve market acceptance of its products and technologies and integrate its products and technologies with third-party platforms or technologies; the Company’s efforts and ability to drive the adoption of its products and technologies as a standard feature, including their use in homes, hotels, offices and cruise ships; the Company’s ability to capture market share; the Company’s estimates of its potential addressable market and demand for its products and technologies; the Company’s ability to raise additional capital to support its operations as needed, which may not be available on acceptable terms or at all; the Company’s ability to continue as a going concern; the Company’s ability to execute on any sales and licensing or other strategic opportunities; the possibility that any of the Company’s products will become National Electrical Code (NEC)-code or otherwise code mandatory in any jurisdiction, or that any of the Company’s current or future products or technologies will be adopted by any state, country, or municipality, within any specific timeframe or at all; risks arising from mergers, acquisitions, joint ventures and other collaborations; the Company’s ability to attract and retain key executives and qualified personnel; guidance provided by management, which may differ from the Company’s actual operating results; the potential impact of unstable market and economic conditions on the Company’s business, financial condition, and stock price; and other risks and uncertainties described in the Company’s filings with the Securities and Exchange Commission, including its periodic reports on Form 10-K and Form 10-Q. There can be no assurance as to any of the foregoing matters. Any forward-looking statement speaks only as of the date of this press release, and the Company undertakes no obligation to update or revise any forward-looking statements, whether as a result of new information, future events or otherwise, except as required by U.S. federal securities laws.

Investor Relations Contact: Jeff Ramson PCG Advisory [email protected]

FLORHAM PARK, N.J. — Conduent Incorporated (Nasdaq: CNDT), a global technology-driven business solutions and services company, today announced it has successfully completed a refinancing of its existing term loan and revolving credit agreements.

Key Highlights of the Refinancing:

Full Prepayment of the Term Loan

Renewed Revolving Credit Facility

New Performance Letter of Credit Facility

Giles Goodburn, Conduent’s CFO, commented, “Completing this refinancing marks a key milestone in our strategy, further strengthening our financial foundation and positioning Conduent for future growth. This transaction provides the right mix of debt instruments to support our operations and capital allocation strategy.”

Additional details of the refinancing can be found in Conduent’s 8-K which will be filed with the U.S. Securities and Exchange Commission.

About Conduent

Conduent delivers digital business solutions and services spanning the commercial, government and transportation spectrum – creating valuable outcomes for its clients and the millions of people who count on them. The Company leverages cloud computing, artificial intelligence, machine learning, automation and advanced analytics to deliver mission-critical solutions. Through a dedicated global team of approximately 56,000 associates, process expertise and advanced technologies, Conduent’s solutions and services digitally transform its clients’ operations to enhance customer experiences, improve performance, increase efficiencies and reduce costs. Conduent adds momentum to its clients’ missions in many ways including disbursing approximately $85 billion in government payments annually, enabling 2.3 billion customer service interactions annually, empowering millions of employees through HR services every year and processing nearly 13 million tolling transactions every day. Learn more at www.conduent.com.

Conduent is a trademark of Conduent Incorporated in the United States and/or other countries. Other names may be trademarks of their respective owners.

Fourth Quarter of Fiscal Year 2025 – Consolidated Earnings Highlights

Revenue of $345.1 million

Net income of $12.9 million

Adjusted EBITDA* of $2.7 million

Fiscal Year 2026 Guidance Ranges:

Revenue expected in a range of $1.650 billion to $1.750 billion

Adjusted EBITDA* expected in a range of $120 million to $150 million

Fourth Quarter Fiscal Year 2025 – Segment Highlights

Senior

Revenue of $82.5 million

Adjusted EBITDA* of $7.7 million

Approved Medicare Advantage policies of 85,344

Healthcare Services

Revenue of $214.0 million

Adjusted EBITDA* of $11.9 million

108,018 SelectRx members

Life

Revenue of $48.0 million

Adjusted EBITDA* of $6.9 million

OVERLAND PARK, Kan.–(BUSINESS WIRE)– This press release is to correct and replace the previously issued press release to reflect the following:

On the Consolidated Statements of Comprehensive Income (Loss) for the three-month period ending June 30, 2025, the amount reported for the Selling, general and administrative line item is $41,591,000 and for the Technical development line item it is $9,594,000. In the prior version of the press release, these amounts were inadvertently transposed on the Consolidated Statements of Comprehensive Income (Loss). The correction has no impact on the reported Net Income or Adjusted EBITDA for the period presented.

The updated release reads:

SELECTQUOTE, INC. REPORTS FOURTH QUARTER OF FISCAL YEAR 2025 RESULTS

Fourth Quarter of Fiscal Year 2025 – Consolidated Earnings Highlights

Revenue of $345.1 million

Net income of $12.9 million

Adjusted EBITDA* of $2.7 million

Fiscal Year 2026 Guidance Ranges:

Revenue expected in a range of $1.650 billion to $1.750 billion

Adjusted EBITDA* expected in a range of $120 million to $150 million

Fourth Quarter Fiscal Year 2025 – Segment Highlights

Senior

Revenue of $82.5 million

Adjusted EBITDA* of $7.7 million

Approved Medicare Advantage policies of 85,344

Healthcare Services

Revenue of $214.0 million

Adjusted EBITDA* of $11.9 million

108,018 SelectRx members

Life

Revenue of $48.0 million

Adjusted EBITDA* of $6.9 million

SelectQuote, Inc. (NYSE: SLQT) reported consolidated revenue for the fourth quarter of fiscal year 2025 of $345.1 million compared to consolidated revenue for the fourth quarter of fiscal year 2024 of $307.2 million. Consolidated net income for the fourth quarter of fiscal year 2025 was $12.9 million compared to consolidated net loss for the fourth quarter of fiscal year 2024 of $31.0 million. Finally, consolidated Adjusted EBITDA* for the fourth quarter of fiscal year 2025 was $2.7 million compared to consolidated Adjusted EBITDA* for the fourth quarter of fiscal year 2024 of $14.4 million.

Tim Danker, SelectQuote Chief Executive Officer, commented “The strength of our holistic healthcare services model was broadly exhibited in fiscal 2025, and we firmly believe the years ahead will increasingly drive substantial value for each of our stakeholders. Policyholders and patients will continue to benefit from our information advantage through tailored advice and healthcare solutions, which ultimately result in better health outcomes. Our insurance and healthcare service partners benefit from better treatment fit and adherence, which eliminates waste and serves to ease the historical trend of rising healthcare costs for Americans. Additionally, we believe our shareholders will benefit as SelectQuote’s diverse breadth of revenues drive increasing cash flow, which will accelerate and compound with new growth initiatives in the future.”

Mr. Danker continued, “We are proud to have delivered financial results well in excess of our initial expectations for the 3rd consecutive year. Over that period, our Adjusted EBITDA results have outperformed our forecasts by more than 20% each year. Our leadership and workforce have accomplished these results through significant change in Medicare Advantage in each year. We credit the talent and hard work of our people and are exceedingly proud of the track record SelectQuote has built as an agile, innovative and reliable source of value for Americans seeking healthcare that best fits their needs.”

* See “Non-GAAP Financial Measures” below.

Segment Results

We currently have three reportable segments: 1) Senior, 2) Healthcare Services and 3) Life. The performance measures of the segments include total revenue and Adjusted EBITDA.* Costs of commissions and other services revenue, cost of goods sold-pharmacy revenue, marketing and advertising, selling, general, and administrative, and technical development operating expenses that are directly attributable to a segment are reported within the applicable segment. Indirect costs of revenue, marketing and advertising, selling, general, and administrative, and technical development operating expenses are allocated to each segment based on varying metrics such as headcount. Adjusted EBITDA is our segment profit measure to evaluate the operating performance of our business. We define Adjusted EBITDA as income (loss) before income tax expense (benefit) plus: (i) interest expense, net; (ii) depreciation and amortization; (iii) share-based compensation; (iv) goodwill, long-lived asset, and intangible assets impairments; (v) transaction costs; (vi) loss on disposal of property, equipment and software, net; (vii) other non-recurring expenses and income; (viii) changes in fair value of warrant liabilities. Adjusted EBITDA margin is calculated as Adjusted EBITDA divided by revenue.

Senior

Financial Results

The following table provides the financial results for the Senior segment for the periods presented:

Operating Metrics

Submitted Policies

Submitted policies are counted when an individual completes an application with our licensed agent and provides authorization to the agent to submit the application to the insurance carrier partner. The applicant may have additional actions to take before the application will be reviewed by the insurance carrier.

The following table shows the number of submitted policies for the periods presented:

Approved Policies

Approved policies represents the number of submitted policies that were approved by our insurance carrier partners for the identified product during the indicated period. Not all approved policies will go in force.

The following table shows the number of approved policies for the periods presented:

Lifetime Value of Commissions per Approved Policy

Lifetime value of commissions per approved policy represents commissions estimated to be collected over the estimated life of an approved policy based on multiple factors, including but not limited to, contracted commission rates, carrier mix and expected policy persistency with applied constraints. The lifetime value of commissions per approved policy is equal to the sum of the commission revenue due upon the initial sale of a policy, and when applicable, an estimate of future renewal commissions.

The following table shows the lifetime value of commissions per approved policy for the periods presented:

Healthcare Services

Financial Results

The following table provides the financial results for the Healthcare Services segment for the periods presented:

Operating Metrics

Members

The total number of SelectRx members represents the amount of active customers to which an order has been shipped and the prescriptions per day represents the total average prescriptions shipped per business day. These two metrics are the primary drivers of revenue for Healthcare Services.

* See “Non-GAAP Financial Measures” below.

The following table shows the total number of SelectRx members as of the periods presented:

The total number of SelectRx members increased by 31% as of June 30, 2025, compared to June 30, 2024, due to our strategy to grow SelectRx membership.

The following table shows the average prescriptions shipped per day for the periods presented:

Combined Senior and Healthcare Services – Consumer Per Unit Economics

Combined Senior and Healthcare Services consumer per unit economics represents total MA and MS commissions; other product commissions; other revenues, including revenues from Healthcare Services; and operating expenses associated with Senior and Healthcare Services, each shown per number of approved MA and MS policies over a given time period. Management assesses the business on a per-unit basis to help ensure that the revenue opportunity associated with a successful policy sale is attractive relative to the marketing acquisition cost. Because not all acquired leads result in a successful policy sale, all per-policy metrics are based on approved policies, which is the measure that triggers revenue recognition.

The MA and MS commission per MA/MS policy represents the LTV for policies sold in the period. Other commission per MA/MS policy represents the LTV for other products sold in the period, including DVH prescription drug plan, and other products, which management views as additional commission revenue on our agents’ core function of MA/MS policy sales. Pharmacy revenue per MA/MS policy represents revenue from SelectRx, and other revenue per MA/MS policy represents revenue from Population Health, production bonuses, marketing development funds, lead generation revenue, and adjustments from the Company’s reassessment of its cohorts’ transaction prices. Total operating expenses per MA/MS policy represents all of the operating expenses within Senior and Healthcare Services. The revenue to customer acquisition cost (“CAC”) multiple represents total revenue as a multiple of total marketing acquisition cost, which represents the direct costs of acquiring leads. These costs are included in marketing and advertising expense within the total operating expenses per MA/MS policy.

The following table shows combined Senior and Healthcare Services consumer per unit economics for the periods presented. Based on the seasonality of Senior and the fluctuations between quarters, we believe that the most relevant view of per unit economics is on a rolling 12-month basis. All per MA/MS policy metrics below are based on the sum of approved MA/MS policies, as both products have similar commission profiles.

Total revenue per MA/MS policy increased 22% for the twelve months ended June 30, 2025, compared to the twelve months ended June 30, 2024, primarily due to the increase in pharmacy revenue. Total operating expenses per MA/MS policy increased 27% for the twelve months ended June 30, 2025, compared to the twelve months ended June 30, 2024, driven by an increase in cost of goods sold-pharmacy revenue for Healthcare Services due to the growth of the business.

Life

Financial Results

The following table provides the financial results for the Life segment for the periods presented:

Operating Metrics

Life premium represents the total premium value for all policies that were approved by the relevant insurance carrier partner and for which the policy document was sent to the policyholder and payment information was received by the relevant insurance carrier partner during the indicated period. Because our commissions are earned based on a percentage of total premium, total premium volume for a given period is the key driver of revenue for our Life segment.

The following table shows term and final expense premiums for the periods presented:

Earnings Conference Call

SelectQuote, Inc. will host a conference call with the investment community on August 21, 2025, beginning at 8:30 a.m. ET. To register for this conference call, please use this link: https://registrations.events/direct/Q4I547808. After registering, a confirmation will be sent via email, including dial-in details and unique conference call codes for entry. Registration is open through the live call, but to ensure you are connected for the full call we suggest registering at least 10 minutes before the start of the call. The event will also be webcasted live via our investor relations website https://ir.selectquote.com/investor-home/default.aspx.

Non-GAAP Financial Measures

This release includes certain non-GAAP financial measures intended to supplement, not substitute for, comparable GAAP measures. To supplement our financial statements presented in accordance with GAAP and to provide investors with additional information regarding our GAAP financial results, we have presented in this release Adjusted EBITDA, which is a non-GAAP financial measure. This non-GAAP financial measure is not based on any standardized methodology prescribed by GAAP and is not necessarily comparable to any similarly titled measure presented by other companies. We define Adjusted EBITDA as net income (loss) before income tax expense (benefit), plus interest expense, depreciation and amortization, changes in fair value of warrant liabilities, and certain add-backs for non-cash or non-recurring expenses, including restructuring and share-based compensation expenses. The most directly comparable GAAP measure is net income (loss) before income tax expense (benefit). We monitor and have presented in this release Adjusted EBITDA because it is a key measure used by our management and Board of Directors to understand and evaluate our operating performance, establish budgets, and develop operational goals for managing our business. In particular, we believe that excluding the impact of these expenses in calculating Adjusted EBITDA can provide a useful measure for period-to-period comparisons of our core operating performance.

Reconciliations of net income (loss) before income tax expense (benefit) to Adjusted EBITDA are presented below beginning on page 12. The Company is unable to provide a quantitative reconciliation of forward-looking Adjusted EBITDA to its most directly comparable GAAP measure without unreasonable effort because it is not possible to predict certain information included in the calculation of such GAAP measure, including the fair value of outstanding warrants to purchase shares of the Company’s common stock. The unavailable information could have a significant impact on the Company’s GAAP financial results.

Forward Looking Statements

This release contains forward-looking statements. These forward-looking statements reflect our current views with respect to, among other things, future events and our financial performance. These statements are often, but not always, made through the use of words or phrases such as “may,” “should,” “could,” “predict,” “potential,” “believe,” “will likely result,” “expect,” “continue,” “will,” “anticipate,” “seek,” “estimate,” “intend,” “plan,” “projection,” “would” and “outlook,” or the negative version of those words or other comparable words or phrases of a future or forward-looking nature. These forward-looking statements are not historical facts and are based on current expectations, estimates and projections about our industry, management’s beliefs and certain assumptions made by management, many of which, by their nature, are inherently uncertain and beyond our control. Accordingly, we caution you that any such forward-looking statements are not guarantees of future performance and are subject to risks, assumptions and uncertainties that are difficult to predict. Although we believe that the expectations reflected in these forward-looking statements are reasonable as of the date made, actual results may prove to be materially different from the results expressed or implied by the forward-looking statements.

There are or will be important factors that could cause our actual results to differ materially from those indicated in these forward-looking statements, including, but not limited to, the following: our reliance on a limited number of insurance carrier partners and any potential termination of those relationships or failure to develop new relationships; existing and future laws and regulations affecting the health insurance market; changes in health insurance products offered by our insurance carrier partners and the health insurance market generally; insurance carriers offering products and services directly to consumers; changes to commissions paid by insurance carriers and underwriting practices; competition with brokers, exclusively online brokers and carriers who opt to sell policies directly to consumers; competition from government-run health insurance exchanges; developments in the U.S. health insurance system; our dependence on revenue from carriers in our senior segment and downturns in the senior health as well as life, automotive and home insurance industries; our ability to develop new offerings and penetrate new vertical markets; risks from third-party products; failure to enroll individuals during the Medicare annual enrollment period; our ability to attract, integrate and retain qualified personnel; our dependence on lead providers and ability to compete for leads; failure to obtain and/or convert sales leads to actual sales of insurance policies; access to data from consumers and insurance carriers; accuracy of information provided from and to consumers during the insurance shopping process; cost-effective advertisement through internet search engines; ability to contact consumers and market products by telephone; global economic conditions, including inflation and tariffs; disruption to operations as a result of future acquisitions; significant estimates and assumptions in the preparation of our financial statements; impairment of goodwill; existing or potential litigation and other legal proceedings or inquiries, including the Department of Justice action alleging violations of the federal False Claims Act; our existing and future indebtedness; our ability to maintain compliance with our debt covenants; access to additional capital; failure to protect our intellectual property and our brand; fluctuations in our financial results caused by seasonality; accuracy and timeliness of commissions reports from insurance carriers; timing of insurance carriers’ approval and payment practices; factors that impact our estimate of the constrained lifetime value of commissions per policyholder; changes in accounting rules, tax legislation and other legislation; disruptions or failures of our technological infrastructure and platform; failure to maintain relationships with third-party service providers; cybersecurity breaches or other attacks involving our systems or those of our insurance carrier partners or third-party service providers; our ability to protect consumer information and other data; failure to market and sell Medicare plans effectively or in compliance with laws; and other factors related to our pharmacy business, including manufacturing or supply chain disruptions, access to and demand for prescription drugs, contractual reimbursement rates, and regulatory changes or other industry developments that may affect our pharmacy operations. For a further discussion of these and other risk factors that could impact our future results and performance, see the section entitled “Risk Factors” in our Annual Report on Form 10-K for the fiscal year ended June 30, 2025 (the “Annual Report”) and subsequent periodic reports filed by us with the Securities and Exchange Commission. Accordingly, you should not place undue reliance on any such forward-looking statements. Any forward-looking statement speaks only as of the date on which it is made, and, except as otherwise required by law, we do not undertake any obligation to publicly update or review any forward-looking statement, whether as a result of new information, future developments or otherwise..

About SelectQuote:

Founded in 1985, SelectQuote (NYSE: SLQT) pioneered the model of providing unbiased comparisons from multiple, highly-rated insurance companies, allowing consumers to choose the policy and terms that best meet their unique needs. Two foundational pillars underpin SelectQuote’s success: a strong force of highly-trained and skilled agents who provide a consultative needs analysis for every consumer, and proprietary technology that sources and routes high-quality leads. Today, the Company operates an ecosystem offering high touchpoints for consumers across insurance, pharmacy, and virtual care.

With an ecosystem offering engagement points for consumers across insurance, Medicare, pharmacy, and value-based care, the company now has three core business lines: SelectQuote Senior, SelectQuote Healthcare Services, and SelectQuote Life. SelectQuote Senior serves the needs of a demographic that sees around 10,000 people turn 65 each day with a range of Medicare Advantage and Medicare Supplement plans. SelectQuote Healthcare Services is comprised of the SelectRx Pharmacy, a Patient-Centered Pharmacy Home™ (PCPH) accredited pharmacy, SelectPatient Management, a provider of chronic care management services, and Healthcare Select which proactively connects consumers with a wide breadth of healthcare services supporting their needs.

NEW YORK, August 11, 2025 /PRNewswire/ — Bit Digital, Inc. (Nasdaq: BTBT) (“Bit Digital” or the “Company”), in New York, announced today that it will release its Second Quarter 2025 results on Thursday, August 14, 2025, after the stock market closes. Senior management will host a live webcast and conference call to review on August 15, 2025, at 10:00 a.m. ET.

To register for the earnings call, please click here. Additionally, participants can join the conference call by dialing 1-800-289-0462 (passcode: 423774).

The Company will issue a press release regarding Second Quarter 2025 earnings prior to the conference call. The press release will be posted on the Bit Digital website at www.bit-digital.com.

About Bit Digital Bit Digital is a publicly traded digital asset platform focused on Ethereum-native treasury and staking strategies. The Company began accumulating and staking ETH in 2022 and now operates one of the largest institutional Ethereum staking infrastructures globally. Bit Digital’s platform includes advanced validator operations, institutional-grade custody, active protocol governance, and yield optimization. Through strategic partnerships across the Ethereum ecosystem, Bit Digital aims to deliver exposure to secure, scalable, and compliant access to onchain yield. For additional information, please contact [email protected], visit our website at www.bit-digital.com, or follow us on LinkedIn or X.

Investor Notice Investing in our securities involves a high degree of risk. Before making an investment decision, you should carefully consider the risks, uncertainties and forward-looking statements described under “Risk Factors” in Item 1A of our Annual Report on Form 10-K for the year ended December 31, 2024 (Annual Report) and any subsequently filed quarterly reports on Form 10-Q and any Current Reports on Form 8-K. If any material risk was to occur, our business, financial condition or results of operations would likely suffer. In that event, the value of our securities could decline and you could lose part or all of your investment. The risks and uncertainties we describe are not the only ones facing us. Additional risks not presently known to us or that we currently deem immaterial may also impair our business operations. In addition, our past financial performance may not be a reliable indicator of future performance, and historical trends should not be used to anticipate results in the future. See “Safe Harbor Statement” below.

Safe Harbor Statement This press release may contain certain “forward-looking statements” relating to the business of Bit Digital, Inc., and its subsidiary companies. All statements, other than statements of historical fact included herein are “forward-looking statements.” These forward-looking statements are often identified by the use of forward-looking terminology such as “believes,” “expects,” or similar expressions, involving known and unknown risks and uncertainties. Although the Company believes that the expectations reflected in these forward-looking statements are reasonable, they do involve assumptions, risks and uncertainties, and these expectations may prove to be incorrect. Investors should not place undue reliance on these forward-looking statements, which speak only as of the date of this press release. The Company’s actual results could differ materially from those anticipated in these forward-looking statements as a result of a variety of factors, including those discussed in the Company’s periodic reports that are filed with the Securities and Exchange Commission and available on its website at http://www.sec.gov. All forward-looking statements attributable to the Company or persons acting on its behalf are expressly qualified in their entirety by these factors. Other than as required under the securities laws, the Company does not assume a duty to update these forward-looking statements.

ISG (Information Services Group) (Nasdaq: III) is a leading global technology research and advisory firm. A trusted business partner to more than 700 clients, including more than 75 of the world’s top 100 enterprises, ISG is committed to helping corporations, public sector organizations, and service and technology providers achieve operational excellence and faster growth. The firm specializes in digital transformation services, including automation, cloud and data analytics; sourcing advisory; managed governance and risk services; network carrier services; strategy and operations design; change management; market intelligence and technology research and analysis. Founded in 2006, and based in Stamford, Conn., ISG employs more than 1,300 digital-ready professionals operating in more than 20 countries—a global team known for its innovative thinking, market influence, deep industry and technology expertise, and world-class research and analytical capabilities based on the industry’s most comprehensive marketplace data. For additional information, visit www.ISG-One.com

Joe Gomes, CFA, Managing Director, Equity Research Analyst, Generalist , Noble Capital Markets, Inc.

Jacob Mutchler, Research Associate, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

Riding the Waves. ISG is riding two key waves, one is AI adoption, with clients investing aggressively in modernizing their technology operations and infrastructure to support it. The other is cost optimization, as one of the means of funding the AI adoption is through optimization of cloud, infrastructure, and software costs.

AI & Recurring Revenue. AI-related revenue was 2.5x higher than it was a year ago. And in both the second quarter and first half, nearly 20% of total revenue was AI related. Recurring revenues in the second quarter reached $28 million, up 7% sequentially and represented 45% of overall revenue.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

Company to Provide Corporate Updates Including New Developments, Second Quarter 2025 Overview and Financial Results; Conference Call to be Held Tuesday, August 12, 2025, at 4:30 PM Eastern Time

Time of Event changed from 10:00 AM EST to 4:30 PM EST

MIAMI, Aug. 08, 2025 (GLOBE NEWSWIRE) — SKYX Platforms Corp. (NASDAQ: SKYX) (d/b/a “SKYX Technologies”), a highly disruptive advanced and smart home platform technology company for homes and buildings, with more than 100 issued and pending patents globally and a portfolio of over 60 lighting and home décor websites, announces today that it will host a Corporate Update call and present its second quarter 2025 overview and financial results. The conference call will be held on Tuesday, August 12, 2025, at 4:30 p.m. Eastern Time.

SKYX Participating Members will include:

Rani Kohen, Founder and Executive Chairman

Steve Schmidt, SKYX President, (former CEO of Nielsen Data Corporation and former President of Office Depot International)

A playback of the call will be available until September 12, 2025.

Replay Dial-In: 1-844-512-2921 or 1-412-317-6671 Replay Pin Number: 10202040

About SKYX Platforms Corp. As electricity is a standard in every home and building, our mission is to make homes and buildings become safe-advanced and smart as the new standard. SKYX has a series of highly disruptive advanced-safe-smart platform technologies, with over 100 U.S. and global patents and patent pending applications. Additionally, the Company owns over 60 lighting and home decor websites for both retail and commercial segments. Our technologies place an emphasis on high quality and ease of use, while significantly enhancing both safety and lifestyle in homes and buildings. We believe that our products are a necessity in every room in both homes and other buildings in the U.S. and globally. For more information, please visit our website at https://skyplug.com/ or follow us on LinkedIn.

Forward-Looking Statements Certain statements made in this press release are not based on historical facts, but are forward-looking statements. These statements can be identified by the use of forward-looking terminology such as “aim,” “anticipate,” “believe,” “can,” “could,” “continue,” “estimate,” “expect,” “evaluate,” “forecast,” “guidance,” “intend,” “likely,” “may,” “might,” “objective,” “ongoing,” “outlook,” “plan,” “potential,” “predict,” “probable,” “project,” “seek,” “should,” “target” “view,” “will,” or “would,” or the negative thereof or other variations thereon or comparable terminology, although not all forward-looking statements contain these words. These statements reflect the Company’s reasonable judgment with respect to future events and are subject to risks, uncertainties and other factors, many of which have outcomes difficult to predict and may be outside our control, that could cause actual results or outcomes to differ materially from those in the forward-looking statements. Such risks and uncertainties include statements relating to the Company’s ability to successfully launch, commercialize, develop additional features and achieve market acceptance of its products and technologies and integrate its products and technologies with third-party platforms or technologies; the Company’s efforts and ability to drive the adoption of its products and technologies as a standard feature, including their use in homes, hotels, offices and cruise ships; the Company’s ability to capture market share; the Company’s estimates of its potential addressable market and demand for its products and technologies; the Company’s ability to raise additional capital to support its operations as needed, which may not be available on acceptable terms or at all; the Company’s ability to continue as a going concern; the Company’s ability to execute on any sales and licensing or other strategic opportunities; the possibility that any of the Company’s products will become National Electrical Code (NEC)-code or otherwise code mandatory in any jurisdiction, or that any of the Company’s current or future products or technologies will be adopted by any state, country, or municipality, within any specific timeframe or at all; risks arising from mergers, acquisitions, joint ventures and other collaborations; the Company’s ability to attract and retain key executives and qualified personnel; guidance provided by management, which may differ from the Company’s actual operating results; the potential impact of unstable market and economic conditions on the Company’s business, financial condition, and stock price; and other risks and uncertainties described in the Company’s filings with the Securities and Exchange Commission, including its periodic reports on Form 10-K and Form 10-Q. There can be no assurance as to any of the foregoing matters. Any forward-looking statement speaks only as of the date of this press release, and the Company undertakes no obligation to update or revise any forward-looking statements, whether as a result of new information, future events or otherwise, except as required by U.S. federal securities laws.

Investor Relations Contact: Jeff Ramson PCG Advisory [email protected]

Company to Provide Corporate Updates Including New Developments, Second Quarter 2025 Overview and Financial Results; Conference Call to be Held Tuesday, August 12, 2025, at 10:00 A.M. Eastern Time

MIAMI, Aug. 07, 2025 (GLOBE NEWSWIRE) — SKYX Platforms Corp. (NASDAQ: SKYX) (d/b/a “SKYX Technologies”), a highly disruptive advanced and smart home platform technology company for homes and buildings, with more than 100 issued and pending patents globally and a portfolio of over 60 lighting and home décor websites, announces today that it will host a Corporate Update call and present its second quarter 2025 overview and financial results. The conference call will be held on Tuesday, August 12, 2025, at 10:00 a.m. Eastern Time.

SKYX Participating Members will Include:

Rani Kohen, Founder and Executive Chairman

Steve Schmidt, SKYX President, (former CEO of Nielsen Data Corporation and former President of Office Depot International)

A playback of the call will be available until September 12, 2025.

Replay Dial-In: 1-844-512-2921 or 1-412-317-6671 Replay pin number 10202040

About SKYX Platforms Corp. As electricity is a standard in every home and building, our mission is to make homes and buildings become safe-advanced and smart as the new standard. SKYX has a series of highly disruptive advanced-safe-smart platform technologies, with over 100 U.S. and global patents and patent pending applications. Additionally, the Company owns over 60 lighting and home decor websites for both retail and commercial segments. Our technologies place an emphasis on high quality and ease of use, while significantly enhancing both safety and lifestyle in homes and buildings. We believe that our products are a necessity in every room in both homes and other buildings in the U.S. and globally. For more information, please visit our website at https://skyplug.com/ or follow us on LinkedIn.

Forward-Looking Statements Certain statements made in this press release are not based on historical facts, but are forward-looking statements. These statements can be identified by the use of forward-looking terminology such as “aim,” “anticipate,” “believe,” “can,” “could,” “continue,” “estimate,” “expect,” “evaluate,” “forecast,” “guidance,” “intend,” “likely,” “may,” “might,” “objective,” “ongoing,” “outlook,” “plan,” “potential,” “predict,” “probable,” “project,” “seek,” “should,” “target” “view,” “will,” or “would,” or the negative thereof or other variations thereon or comparable terminology, although not all forward-looking statements contain these words. These statements reflect the Company’s reasonable judgment with respect to future events and are subject to risks, uncertainties and other factors, many of which have outcomes difficult to predict and may be outside our control, that could cause actual results or outcomes to differ materially from those in the forward-looking statements. Such risks and uncertainties include statements relating to the Company’s ability to successfully launch, commercialize, develop additional features and achieve market acceptance of its products and technologies and integrate its products and technologies with third-party platforms or technologies; the Company’s efforts and ability to drive the adoption of its products and technologies as a standard feature, including their use in homes, hotels, offices and cruise ships; the Company’s ability to capture market share; the Company’s estimates of its potential addressable market and demand for its products and technologies; the Company’s ability to raise additional capital to support its operations as needed, which may not be available on acceptable terms or at all; the Company’s ability to continue as a going concern; the Company’s ability to execute on any sales and licensing or other strategic opportunities; the possibility that any of the Company’s products will become National Electrical Code (NEC)-code or otherwise code mandatory in any jurisdiction, or that any of the Company’s current or future products or technologies will be adopted by any state, country, or municipality, within any specific timeframe or at all; risks arising from mergers, acquisitions, joint ventures and other collaborations; the Company’s ability to attract and retain key executives and qualified personnel; guidance provided by management, which may differ from the Company’s actual operating results; the potential impact of unstable market and economic conditions on the Company’s business, financial condition, and stock price; and other risks and uncertainties described in the Company’s filings with the Securities and Exchange Commission, including its periodic reports on Form 10-K and Form 10-Q. There can be no assurance as to any of the foregoing matters. Any forward-looking statement speaks only as of the date of this press release, and the Company undertakes no obligation to update or revise any forward-looking statements, whether as a result of new information, future events or otherwise, except as required by U.S. federal securities laws.

Investor Relations Contact: Jeff Ramson PCG Advisory [email protected]

The following news was originally announced in ISG’s second-quarter 2025 results release today:

Acquisition will add to ISG’s client base, geographic footprint and capabilities to serve Italy’s public and private sectors

STAMFORD, Conn. ― Information Services Group (ISG) (Nasdaq: III), a global AI-centered technology research and advisory firm, today announced it has signed a definitive agreement to acquire Martino & Partners, a highly respected strategic advisory firm serving public and private sectors clients in Italy. The transaction is expected to close in early September.

The addition of Milan-based Martino & Partners will expand ISG’s client base, geographic footprint and capabilities in Italy, including AI, in a market with emerging growth potential fueled by European Union-funded technology modernization programs and a focus on AI and cost optimization.

“This acquisition represents a further investment in our European business and expands our addressable market in Italy, where we see an emerging growth opportunity,” said Michael P. Connors, chairman and CEO of ISG. “Martino & Partners brings more than 20 new clients to ISG Italy; expands our public sector reach beyond the central government to serve municipal entities, and gives us a strong presence in northern Italy, where many leading commercial enterprises are located.”

The combined businesses, which will go to market as ISG Italy, will have nearly 40 professionals working out of multiple locations, including Milan and Rome.

“Martino and Partners is the perfect complement to our ISG Italy business,” Connors said. “We have worked together previously on several client engagements, so we are very familiar with the firm, their leadership and their talented professionals. This is a win-win for both firms.”

The acquisition comes at a time of emerging demand for advisory services in Italy, particularly in the public sector, which is seeking strategic advice and support to leverage programs such as the Next Generation EU and Digital Decade initiatives to modernize technology infrastructure and services. Overall interest in AI and cost optimization continues to be high as companies look to use technology to become more efficient and gain competitive advantage in a challenging macro environment.

“Since our founding 10 years ago, Martino & Partners has earned a reputation as one of the leading strategic advisory firms in Italy,” said Andrea Martino, the firm’s co-founder and CEO, who will serve as CEO of ISG Italy. “Our approach is to think big, speak plainly and challenge conventional wisdom. We are excited to be joining forces with ISG, whose global resources and strong domain expertise will make our combined businesses an even more powerful player with stronger growth potential in the Italian marketplace.”

In addition to Martino, ISG Italy’s senior management team will include Claudia De Roma, Martino & Partners co-founder, who will lead the ISG Italy public administration segment.