Joe Gomes, CFA, Managing Director, Equity Research Analyst, Generalist , Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

Approval. On Friday, shareholders of both Steelcase and HNI Corporation voted to approve the merger of the two companies, as originally disclosed on August 4th. Recall, HNI is acquiring Steelcase in a cash and stock transaction, with a total consideration of approximately $2.2 billion to Steelcase common shareholders at the time of announcement. Under the terms of the agreement, Steelcase shareholders will receive $7.20 in cash and 0.2192 shares of HNI common stock for each share of Steelcase they own.

Details. At the special meeting of Steelcase’s shareholders held Friday, approximately 99.60% of the shares voted on the Steelcase Merger Proposal, representing approximately 69.93% of the total outstanding shares of Steelcase common stock as of October 14, 2025, were cast in favor of the Steelcase Merger Proposal.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

Joe Gomes, CFA, Managing Director, Equity Research Analyst, Generalist , Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

2Q26. In what is likely the Company’s final quarterly report as a public company, Steelcase reported better than expected results. Results benefitted from continued strengthening of demand from large corporate customers and International growth driven by India, China, and the United Kingdom. Improved International volume drove a $5 million reduction in y-o-y adjusted operating loss in the International segment. These were Steelcase’s highest quarterly results over the past five years.

Financials. Revenue of $897.1 million rose 4.8% y-o-y and exceeded the $890 million high end of management’s guidance. We were at $875 million. Gross margin of 34.4% was flat y-o-y and exceeded the 33.5% high end of guidance. Adjusted EBITDA totaled $99.6 million, or 11.1% of revenue, up from $89.5 million and 10.5% in 2Q25. Adjusted EPS was $0.45, versus $0.39 last year and above management’s $0.40 high end guide. We were at $0.36.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

Joe Gomes, CFA, Managing Director, Equity Research Analyst, Generalist , Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

To Be Acquired. Steelcase has entered into an agreement to be acquired by HNI Corporation in a cash and stock transaction with total consideration of approximately $2.2 billion to Steelcase common shareholders, or about $18.30/sh, an 80% premium to Friday’s close.

Details. Under the terms of the agreement, Steelcase shareholders will receive $7.20 in cash and 0.2192 shares of HNI common stock for each share of Steelcase. The implied per share purchase price of $18.30 is based on HNI’s closing share price of $50.62 on Friday, August 1, 2025, reflecting a valuation multiple at transaction close for Steelcase of approximately 5.8x TTM adjusted EBITDA, inclusive of run-rate cost synergies of $120 million. Upon closing, HNI shareholders will own approximately 64%, and Steelcase shareholders will own approximately 36% of the combined company. The deal is expected to close by year-end.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

HNI Corporation has announced a definitive agreement to acquire Steelcase Inc. in a cash-and-stock deal valued at approximately $2.2 billion. The strategic acquisition unites two iconic names in workplace furniture and design, combining their strengths in innovation, manufacturing, and dealer networks to form a dominant force in the commercial interiors market.

Under the terms of the deal, Steelcase shareholders will receive $7.20 in cash and 0.2192 shares of HNI common stock for each Steelcase share they own. Based on HNI’s stock price as of August 1, 2025, the total purchase price comes to about $18.30 per share. Once finalized, HNI shareholders will own roughly 64% of the combined entity, while Steelcase shareholders will hold the remaining 36%.

HNI Chairman and CEO Jeffrey Lorenger emphasized the complementary nature of the merger, stating, “This acquisition brings together two respected companies with strong brands and decades of leadership in the industry.” Lorenger will continue to lead the combined company, which will retain HNI’s headquarters in Muscatine, Iowa, and keep Steelcase’s base in Grand Rapids, Michigan.

The new entity will have a pro forma annual revenue of $5.8 billion and adjusted EBITDA of approximately $745 million, with anticipated annual cost synergies of $120 million. Financially, the acquisition positions the company for long-term earnings growth, with projections for accretive non-GAAP EPS by 2027 and a return to pre-acquisition leverage within 18 to 24 months.

The companies’ combined strengths span across corporate, healthcare, education, hospitality, and small-to-midsize business markets. With their complementary product portfolios and broad dealer networks, the merger enhances their ability to serve a wider range of customers with innovative solutions for modern workspaces. Both firms bring decades of product design expertise and a shared commitment to purpose-driven leadership and environmental stewardship.

Steelcase CEO Sara Armbruster called the merger a “bold step” that ushers in a new era for the company, employees, and customers. “Together, we will redefine what’s possible in the world of work, workers, and workplaces,” she said.

The transaction has received strong early support from key stakeholders. Some Steelcase shareholders have already agreed to vote in favor of the deal, and committed financing is in place from JPMorgan Chase and Wells Fargo. The merger is expected to close by the end of 2025, pending shareholder and regulatory approvals.

Advisors for the deal include J.P. Morgan Securities for HNI, and Goldman Sachs and BofA Securities for Steelcase. Legal counsel is being provided by Davis Polk & Wardwell for HNI and Skadden, Arps, Slate, Meagher & Flom for Steelcase.

The deal signals a major consolidation in the commercial furniture sector and positions the combined company to lead the evolution of the workplace at a time when hybrid work, digital transformation, and sustainable design continue to reshape business environments.

Highly Complementary Brand Portfolios, Dealer Networks, and Industry Segments will Enhance Customer Reach

Combined Capabilities to Drive Accretion and Accelerate Strategic Initiatives to Better Serve Customers

HNI and Steelcase to Host Conference Call and Webcast at 8:30 AM ET Today

MUSCATINE, Iowa & GRAND RAPIDS, Mich.–(BUSINESS WIRE)– HNI Corporation (NYSE: HNI) and Steelcase Inc. (NYSE: SCS) today announced that they have entered into a definitive agreement under which HNI will acquire Steelcase in a cash and stock transaction, with a total consideration of approximately $2.2 billion to Steelcase common shareholders.

Under the terms of the agreement, Steelcase shareholders will receive $7.20 in cash and 0.2192 shares of HNI common stock for each share of Steelcase they own. The implied per share purchase price of $18.30 is based on HNI’s closing share price of $50.62 on Friday, August 1, 2025, reflecting a valuation multiple at transaction close1 for Steelcase of approximately 5.8x TTM2 Adjusted EBITDA, inclusive of run-rate cost synergies of $120 million. Upon closing, HNI shareholders will own approximately 64% and Steelcase shareholders will own approximately 36% of the combined company.

“This acquisition brings together two respected companies with complementary strengths and represents an exciting milestone in HNI’s growth journey,” said Jeffrey Lorenger, HNI’s Chairman, President, and Chief Executive Officer. “We have long admired Steelcase for its insight-led approach, which has helped shape our industry for decades. With the Steelcase portfolio of brands and as in-office work trends accelerate, we will be even better positioned to meet the evolving needs of the workplace, enhance dealer and customer relationships, unlock new opportunities for growth, and create compelling value for the combined company’s shareholders.”

“Joining with HNI is a bold step that marks the next era for Steelcase, our customers, dealers, and employees,” said Sara Armbruster, President and Chief Executive Officer of Steelcase. “Together, we will be positioned to redefine what’s possible in the world of work, workers, and workplaces. Like Steelcase, HNI is an organization that leads with purpose, shares similar values, and puts the customer at the center of everything they do. I’m excited to see this combination shape our industry.”

Compelling Strategic Benefits

Combines Complementary Portfolios and Dealer Networks to Enhance Customer Reach: HNI’s and Steelcase’s geographic footprints and dealer networks are highly complementary, which bolsters the combined company’s ability to serve more customers across diverse industry segments, including small and medium business, large corporate, healthcare, education, and hospitality customers. The companies have the industry’s most respected and widely recognized brands, allowing the combined company to better support an expanded customer base and capture growth opportunities from industry tailwinds.

Brings Together World-Class Capabilities: Uniting a strong innovation engine with operational excellence, the combined organization will accelerate delivery of more advanced solutions to customers, while increasing value for shareholders.

Strong Financial Profile: The combined company will have pro forma annual revenue of approximately $5.8 billion, pro forma Adjusted EBITDA of approximately $745 million, and 2.1x net leverage. 3 These metrics are based on each company’s respective last reported 12-month results and are inclusive of annual run-rate synergies. Net leverage is expected to return to pre-acquisition levels within 18-24 months.

Highly Synergistic Combination: With recent experience in M&A execution and a disciplined integration approach, HNI’s proven ability to successfully combine core capabilities and deliver cost synergies will maximize the new organization’s future success. Annual run-rate synergies are expected to total $120 million when fully mature. The company projects the combination will be highly accretive to non-GAAP earnings per share beginning in 2027.

Accelerates Strategic Framework: The acquisition is fully aligned with HNI’s strategic framework focused on driving long-term profitable growth. With an enhanced financial profile, the new company will also be better positioned to accelerate and increase investments in long-term operational enhancements, digital transformation, and customer-centric buying experiences.

HNI and Steelcase share a deep commitment to respecting people, protecting the planet, operating with excellence, and acting with integrity. As a stronger and more diversified organization, the combined company will bring together the strengths of both HNI and Steelcase to create new career growth opportunities for team members, deliver more value for customers, and further support and invest in the communities where they operate.

Following the close of the transaction, the combined company will continue to be led by Jeffrey Lorenger, HNI’s Chairman, President, and Chief Executive Officer. HNI will continue to operate its corporate headquarters in Muscatine, Iowa, and Steelcase will maintain its headquarters in Grand Rapids, Michigan. HNI will maintain the Steelcase brand following the transaction’s close. In addition, post-closing, HNI’s Board of Directors will expand from 10 directors to 12, to include two of Steelcase’s current independent board members.

Approvals, Financing, and Timing to Close

The transaction, which is expected to close by the end of calendar year 2025, is subject to approval by HNI and Steelcase shareholders, the receipt of required regulatory clearances, and the satisfaction of other customary closing conditions.

Certain shareholders of Steelcase have entered into a voting agreement to vote in favor of the transaction at the special meeting of Steelcase shareholders to be held in connection with the transaction.

In support of the transaction, JPMorgan Chase Bank, N.A. and Wells Fargo Bank, N.A. have executed a commitment letter to provide committed financing to HNI, subject to the terms and conditions therein.

Advisors

J.P. Morgan Securities LLC is serving as exclusive financial advisor to HNI, and Davis Polk & Wardwell LLP is serving as legal counsel. Goldman Sachs & Co. LLC and BofA Securities are serving as financial advisors to Steelcase, and Skadden, Arps, Slate, Meagher & Flom LLP is serving as legal counsel.

Conference Call, Webcast and Presentation

HNI and Steelcase will hold a conference call to discuss the transaction today, August 4, 2025 at 8:30 a.m. Eastern Time. To listen, call (855) 761-5600 and use conference ID number 7006893. Access to a live audio webcast and slide presentation will be available on the Events & Presentations page of the Investor Relations section of HNI Corporation’s website or at the following link: https://events.q4inc.com/attendee/369737700 [events.q4inc.com].

About HNI Corporation

HNI Corporation (NYSE: HNI) has been improving where people live, work, and gather for more than 75 years. HNI is a manufacturer of workplace furnishings and residential building products, operating under two segments. The Workplace Furnishings segment is a leading global designer and provider of commercial furnishings, going to market under multiple unique brands. The Residential Building Products segment is the nation’s leading manufacturer and marketer of hearth products, which include a full array of gas, electric, wood, and pellet-burning fireplaces, inserts, stoves, facings, and accessories. More information can be found on the Corporation’s website at www.hnicorp.com.

About Steelcase

Steelcase (NYSE: SCS) is a global design and thought leader in the world of work. Our purpose is to help the world work better. Along with more than 30 creative and technology partner brands, we research, design and manufacture furnishings and solutions for many of the places where work happens — including offices, homes, and learning and health environments. Together with our 11,300 employees, we’re working toward better futures for the wellbeing of people and the planet. Our solutions come to life through our global community of expert Steelcase dealers in approximately 790 locations, store.steelcase.com and other retail partners. For more information, visit Steelcase.com.

Forward-Looking Statements

This communication contains forward-looking statements within the meaning of Section 21E of the Securities Exchange Act of 1934 and Section 27A of the Securities Act of 1933, which involve risks and uncertainties. Any statements about HNI’s, Steelcase’s or the combined company’s plans, objectives, expectations, strategies, beliefs, or future performance or events and any other statements to the extent they are not statements of historical fact are forward-looking statements. Words, phrases or expressions such as “anticipate,” “believe,” “could,” “confident,” “continue,” “estimate,” “expect,” “forecast,” “hope,” “intend,” “likely,” “may,” “might,” “objective,” “plan,” “possible,” “potential,” “predict,” “project”, “target,” “trend” and similar words, phrases or expressions are intended to identify forward looking statements but are not the exclusive means of identifying such statements. Forward-looking statements are based on information available and assumptions made at the time the statements are made. Forward-looking statements involve risks and uncertainties that could cause actual results to differ materially from those expressed in or implied by the forward-looking statements. Forward-looking statements in this communication include, but are not limited to, statements about the benefits of the transaction between HNI and Steelcase (the “Transaction”), including future financial and operating results, the combined company’s plans, objectives, expectations and intentions, and other statements that are not historical facts.

The following Transaction-related factors, among others, could cause actual results to differ materially from those expressed in or implied by forward-looking statements: the occurrence of any event, change, or other circumstance that could give rise to the right of one or both of the parties to terminate the definitive merger agreement between HNI and Steelcase; the outcome of any legal proceedings that may be instituted against HNI or Steelcase; the possibility that the Transaction does not close when expected or at all because required regulatory, shareholder, or other approvals and other conditions to closing are not received or satisfied on a timely basis or at all (and the risk that seeking or obtaining such approvals may result in the imposition of conditions that could adversely affect the combined company or the expected benefits of the Transaction); the risk that the benefits from the Transaction may not be fully realized or may take longer to realize than expected, including as a result of changes in, or problems arising from, general economic and market conditions, interest and exchange rates, monetary policy, trade policy (including tariff levels), laws and regulations and their enforcement, and the degree of competition in the geographic and business areas in which HNI and Steelcase operate; any failure to promptly and effectively integrate the businesses of HNI and Steelcase; the possibility that the Transaction may be more expensive to complete than anticipated, including as a result of unexpected factors or events; reputational risk and potential adverse reactions of HNI’s or Steelcase’s customers, employees or other business partners, including those resulting from the announcement, pendency or completion of the Transaction; the dilution caused by HNI’s issuance of additional shares of its capital stock in connection with the Transaction; and the diversion of management’s attention and time to the Transaction from ongoing business operations and opportunities.

Additional important factors relating to Steelcase that could cause actual results to differ materially from those in forward-looking statements include, but are not limited to, competitive and general economic conditions domestically and internationally; acts of terrorism, war, governmental action, natural disasters, pandemics and other Force Majeure events; cyberattacks; changes in the legal and regulatory environment; changes in raw material, commodity and other input costs; currency fluctuations; changes in customer demand; and the other risks and contingencies detailed in Steelcase’s most recent Annual Report on Form 10-K and its other filings with the U.S. Securities and Exchange Commission (the “SEC”).

Additional important factors relating to HNI that could cause actual results to differ materially from those in forward-looking statements include, but are not limited to, HNI’s ultimate realization of the anticipated benefits of the acquisition of Kimball International; disruptions in the global supply chain; the effects of prolonged periods of inflation and rising interest rates; labor shortages; the levels of office furniture needs and housing starts; overall demand for HNI’s products; general economic and market conditions in the United States and internationally; industry and competitive conditions; the consolidation and concentration of HNI’s customers; HNI’s reliance on its network of independent dealers; change in trade policy, including with respect to tariff levels; changes in raw material, component, or commodity pricing; market acceptance and demand for HNI’s new products; changing legal, regulatory, environmental, and healthcare conditions; the risks associated with international operations; the potential impact of product defects; the various restrictions on HNI’s financing activities; an inability to protect HNI’s intellectual property; cybersecurity threats, including those posed by potential ransomware attacks; impacts of tax legislation; and force majeure events outside HNI’s control, including those that may result from the effects of climate change, a description of which risks and uncertainties and additional risks and uncertainties can be found in HNI’s most recent Annual Report on Form 10-K and its other filings with the SEC.

These factors are not necessarily all of the factors that could cause HNI’s, Steelcase’s or the combined company’s actual results, performance, or achievements to differ materially from those expressed in or implied by any forward-looking statements. Other unknown or unpredictable factors also could harm HNI’s, Steelcase’s or the combined company’s results.

All forward-looking statements attributable to HNI, Steelcase, or the combined company, or persons acting on HNI’s or Steelcase’s behalf, are expressly qualified in their entirety by the cautionary statements set forth above. Forward-looking statements speak only as of the date they are made, and HNI and Steelcase do not undertake or assume any obligation to update publicly any of these statements to reflect actual results, new information or future events, changes in assumptions, or changes in other factors affecting forward-looking statements, except to the extent required by applicable law. If HNI or Steelcase updates one or more forward-looking statements, no inference should be drawn that HNI or Steelcase will make additional updates with respect to those or other forward-looking statements. Further information regarding HNI, Steelcase and factors that could affect the forward-looking statements contained herein can be found in HNI’s Annual Report on Form 10-K, its Quarterly Reports on Form 10-Q, and its other filings with the SEC, and in Steelcase’s Annual Report on Form 10-K, its Quarterly Reports on Form 10-Q, and its other filings with the SEC.

No Offer or Solicitation

This communication is not an offer to sell or the solicitation of an offer to buy any securities, nor shall there be any sale of securities in any jurisdiction in which such offer, solicitation or sale would be unlawful prior to registration or qualification under the securities laws of such jurisdiction. No offer of securities shall be made except by means of a prospectus meeting the requirements of Section 10 of the Securities Act of 1933, as amended.

Important Information and Where to Find It

In connection with the Transaction, HNI will file with the SEC a Registration Statement on Form S-4 to register the shares of HNI common stock to be issued in connection with the Transaction. The Registration Statement will include a joint proxy statement of HNI and Steelcase that also constitutes a prospectus of HNI. The definitive joint proxy statement/prospectus will be sent to the shareholders of each of HNI and Steelcase.

INVESTORS AND SECURITY HOLDERS ARE URGED TO READ THE REGISTRATION STATEMENT ON FORM S-4 AND THE JOINT PROXY STATEMENT/PROSPECTUS WHEN THEY BECOME AVAILABLE, AS WELL AS ANY OTHER RELEVANT DOCUMENTS FILED WITH THE SEC IN CONNECTION WITH THE TRANSACTION OR INCORPORATED BY REFERENCE INTO THE JOINT PROXY STATEMENT/PROSPECTUS, BECAUSE THEY CONTAIN OR WILL CONTAIN IMPORTANT INFORMATION REGARDING HNI, STEELCASE, THE TRANSACTION AND RELATED MATTERS.

Investors and security holders may obtain free copies of these documents and other documents filed with the SEC by HNI or Steelcase through the website maintained by the SEC at http://www.sec.gov or from HNI at its website, www.hnicorp.com, or from Steelcase at its website, www.steelcase.com (information included on or accessible through either of HNI’s or Steelcase’s website is not incorporated by reference into this communication).

Participants in the Solicitation

HNI, Steelcase, their respective directors and certain of their respective executive officers may be deemed to be participants in the solicitation of proxies in connection with the Transaction under the rules of the SEC. Information about the interests of the directors and executive officers of HNI and Steelcase and other persons who may be deemed to be participants in the solicitation of proxies in connection with the Transaction and a description of their direct and indirect interests, by security holdings or otherwise, will be included in the joint proxy statement/prospectus related to the Transaction, which will be filed with the SEC. Information about the directors and executive officers of HNI and their ownership of HNI common stock is set forth in the definitive proxy statement for HNI’s 2025 Annual Meeting of Shareholders, filed with the SEC on March 11, 2025; in Table I (Information about our Executive Officers) at the end of Part I of HNI’s Annual Report on Form 10 K for the fiscal year ended December 28, 2024, filed with the SEC on February 25, 2025; in HNI’s Current Report on Form 8 K filed with the SEC on June 20, 2025; in the Form 3 and Form 4 statements of beneficial ownership and statements of changes in beneficial ownership filed with the SEC by HNI’s directors and executive officers; and in other documents filed by HNI with the SEC. Information about the directors and executive officers of Steelcase and their ownership of Steelcase common stock can be found in Steelcase’s definitive proxy statement in connection with its 2025 Annual Meeting of Shareholders, filed with the SEC on May 28, 2025; under the heading “Supplementary Item. Information About Our Executive Officers” in Steelcase’s Annual Report on Form 10 K for the fiscal year ended February 28, 2025, filed with the SEC on April 18, 2025; in Steelcase’s Amendment No. 1 to Current Report on Form 8-K/A filed with the SEC on July 11, 2025; in the Form 3 and Form 4 statements of beneficial ownership and statements of changes in beneficial ownership filed with the SEC by Steelcase’s directors and executive officers; and in other documents filed by Steelcase with the SEC. Free copies of the documents referenced in this paragraph may be obtained as described above under the heading “Important Information and Where to Find It.”

____________________

1 Assumes transaction close at 12/31/2025 with $21 million of net debt; equity consideration is at time of announcement

2 TTM as of 05/30/2025

3 Includes EBITDA add-backs, which encompass two-year look-forward run-rate synergies, as defined within the credit agreement

HNI Corporation

Investors Vincent P. Berger Executive Vice President and Chief Financial Officer (563) 272-7400

Matthew S. McCall Vice President, Investor Relations and Corporate Development (563) 275-8898

Media Lauren Odell / Felipe Ucrós Gladstone Place Partners hni@gladstoneplace.com (212) 230-5930

Joe Gomes, CFA, Managing Director, Equity Research Analyst, Generalist , Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

1Q26. Steelcase reported solid results for the first quarter of fiscal 2026. Revenue grew 7% y-o-y to $779 million, towards the upper end of guidance. We had forecast $760 million and the consensus was $762 million. Gross margin of 33.9% was up 170 bp y-o-y and above management’s 33% guide. Steelcase reported net income of $13.6 million, or EPS of $0.11, and adjusted EPS of $0.20, compared to $10.9 million, $0.09, and $0.16, respectively, last year. We were at adjusted EPS of $0.14, while consensus was $0.13.

Quarterly Drivers. The Americas business was up 9%, both on a reported and organic basis, driven by a higher beginning backlog compared to the prior year and included strong growth from large corporate, government, and healthcare customers. International was up 1% on a reported basis but down 1% on an organic basis, driven by declines in Germany and France, mostly offset by growth in India, the UK, and China.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

RTO Trends. While overall office occupancy improvement trends have somewhat flattened, Steelcase’s key end market, firms in Class A office space, are improving as more large companies are becoming more aggressive about employees returning to the office. And split working environments can be a benefit to Steelcase as employees need to set up work-from-home offices. Steelcase continues to lead the transformation of the workplace.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

Joe Gomes, CFA, Managing Director, Equity Research Analyst, Generalist , Noble Capital Markets, Inc.

Joshua Zoepfel, Research Associate, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

4Q Results. Revenue of $788 million rose 1.7% y-o-y, exceeded our expectation of $775 million, and was at the high end of guidance. Impacted by the revenue mix, gross margin of 31.9% was below our 33.3% projection. Adjusted EBITDA came in at $40.4 million, below our $52.5 million projection. Net income, aided by $21.8 million of favorable tax items, totaled $27.6 million, or $0.23/sh. Adjusted EPS was $0.26, up from $0.23 last year.

Promising Order Growth. Organic order growth in the fourth quarter was 9%, driven by a 12% increase in Americas orders and 1% International order growth. This was the sixth consecutive quarter of year-over-year order growth in the Americas, reflecting continued gains in market share, in our view. Order growth was seen across most customer segments, with especially strong growth from large corporate and government customers.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

GRAND RAPIDS, Mich., March 06, 2025 (GLOBE NEWSWIRE) — Steelcase Inc. (NYSE: SCS) will webcast a discussion of its fourth quarter and fiscal year 2025 financial results on Thursday, March 27, 2025 at 8:30 a.m. ET. A link to the webcast will be available at http://ir.steelcase.com and a replay of the webcast will be available shortly after the call concludes. The news release detailing the financial results will be issued the previous day, March 26, 2025, after the market closes.

About Steelcase Inc.

Established in 1912, Steelcase is a global design, research and thought leader in the world of work. We help people do their best work by creating places that work better. Along with more than 30 creative and technology partner brands, we design and manufacture innovative furnishings and solutions for the many places where work happens — including learning, health and work from home. Our solutions come to life through our community of expert Steelcase dealers in approximately 770 locations, as well as our online Steelcase store and other retail partners. Founded in Grand Rapids, Michigan, Steelcase is a publicly traded company with fiscal year 2024 revenue of $3.2 billion. With our 11,300 global employees and dealer community, we come together for people and the planet — using our business to help the world work better.

CONTACT:

Investor Contact: Mike O’Meara Investor Relations ir@steelcase.com

Revenue growth of 2% driven by 5% growth in the Americas

Gross margin improvement of100 basis points

Total liquidity strengthened by $152 million

Americas posted order growth of 2% compared to prior year

Outlook for fiscal 2025 adjusted earnings per share exceeds company targets

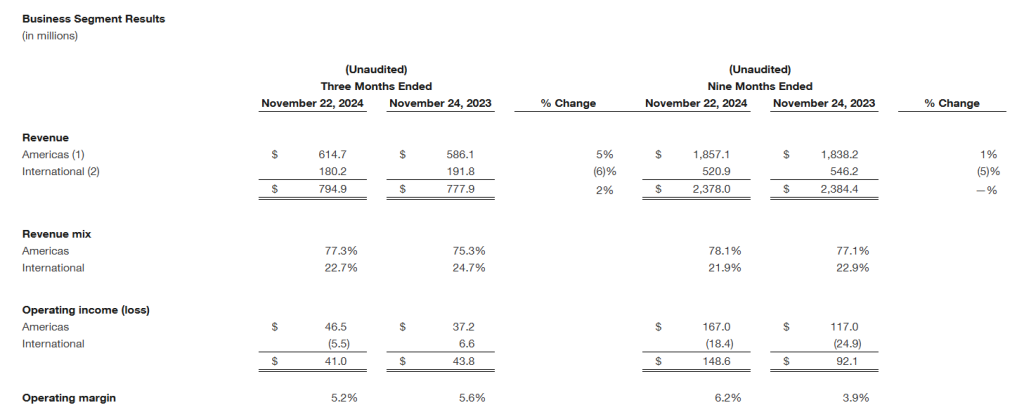

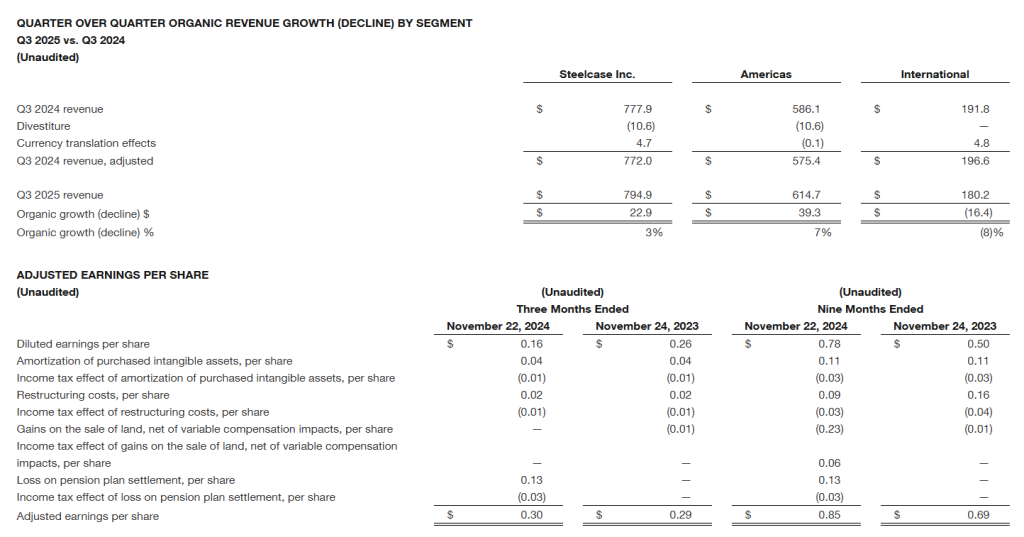

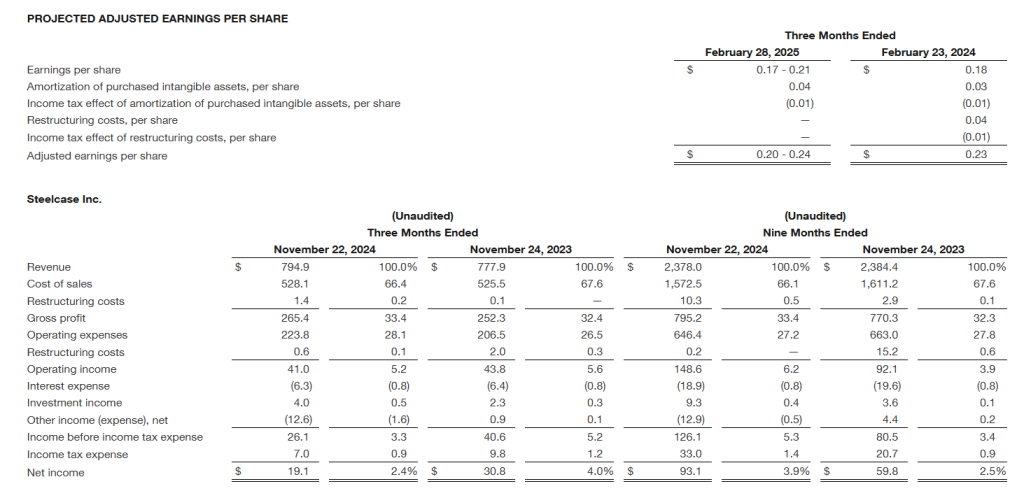

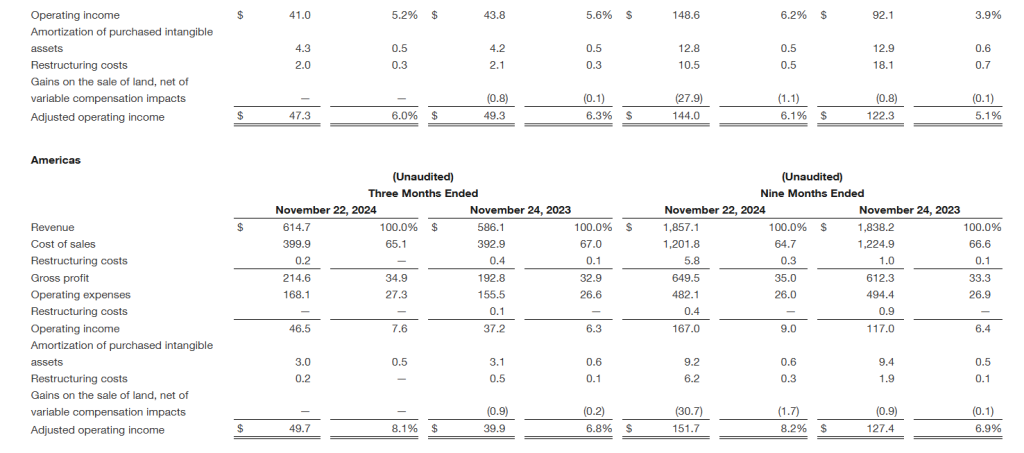

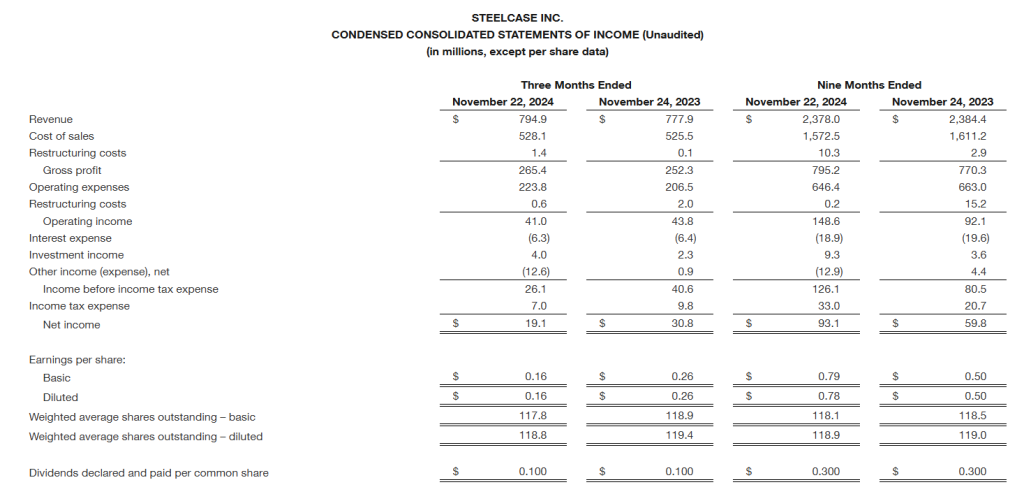

GRAND RAPIDS, Mich., Dec. 18, 2024 (GLOBE NEWSWIRE) — Steelcase Inc. (NYSE: SCS) today reported third quarter revenue of $794.9 million, net income of $19.1 million, or $0.16 per share, and adjusted earnings per share of $0.30. In the prior year, Steelcase reported revenue of $777.9 million and net income of $30.8 million, or $0.26 per share, and had adjusted earnings per share of $0.29.

Revenue and order growth (decline) compared to the prior year were as follows:

Revenue grew 2 percent in the third quarter compared to the prior year, with 5 percent growth in the Americas and a 6 percent decline in International. On an organic basis, revenue grew 3 percent, with 7 percent growth in the Americas and an 8 percent decline in International. The Americas growth benefited from a higher percentage of the beginning backlog shipping during the quarter compared to the prior year and included higher revenue from government, large corporate, healthcare and education customers, while the International decline was driven by most markets in Asia Pacific, except India, and France.

Orders (adjusted for the impact of a divestiture and currency translation effects) declined modestly in the third quarter compared to the prior year, and included 2 percent growth in the Americas and an 8 percent decline in International. The order growth in the Americas was driven by government customers. Orders from large corporate customers strengthened in the last month of the quarter, but modestly declined overall in the third quarter compared to the prior year. The order decline in International was driven by most markets in Asia Pacific and France, net of growth in Germany and some smaller markets in EMEA.

“Our Americas business posted 7% organic revenue growth this quarter driven by growth across many of our customer segments, and we delivered higher than expected adjusted earnings per share,” said Sara Armbruster, president and CEO. “As we continue to focus on serving our customers and supporting their workplace strategies, we posted another quarter of order growth in the Americas, and we are pleased with the improved trends we saw from our large corporate customers near the end of the quarter and into December.”

Operating income (loss) and adjusted operating income (loss) were as follows:

Operating income of $41.0 million in the third quarter represented a decrease of $2.8 million compared to the prior year. The prior year included a $9.5 million benefit from a decrease in the valuation of an acquisition earnout liability and $5.4 million of gains on the sale of fixed assets, including land, in the Americas. The current year included the benefits of higher revenue and gross margin in the Americas compared to the prior year. Adjusted operating income of $47.3 million in the third quarter represented a decrease of $2.0 million compared to the prior year.

“Our International results in the third quarter were below our expectations and were impacted by demand and some customer-driven shipment delays,” said Dave Sylvester, senior vice president and CFO. “We implemented additional restructuring actions and other cost reduction measures during the third quarter, which together are projected to drive approximately $5 million of annualized cost savings by the start of fiscal 2026. Also, we are encouraged by higher project activity levels from some of our global customers in our international markets and recent wins related to large opportunities with national accounts in France, Germany and the Middle East.”

Gross margin of 33.4 percent in the third quarter represented an improvement of 100 basis points compared to the prior year driven by the benefits of revenue growth in the Americas and cost reduction initiatives, including savings from our previously announced restructuring actions.

Operating expenses of $223.8 million in the third quarter represented an increase of $17.3 million compared to the prior year. The prior year included favorable impacts of a $9.5 million decrease in the valuation of an acquisition earnout liability and $5.4 million of gains on the sale of fixed assets, including land. The remaining increase was driven by $6.0 million of higher employee costs, partially offset by a $4.4 million decrease from a divestiture.

Other expense, net of $12.6 million in the third quarter included a $15.2 million non-cash charge related to the annuitization of a pension plan.

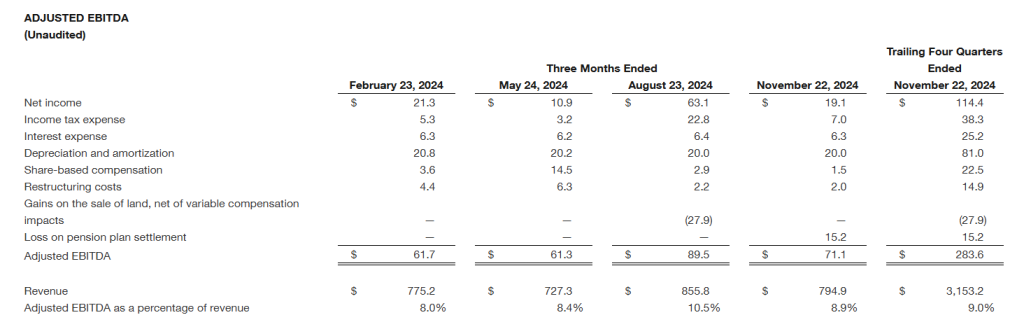

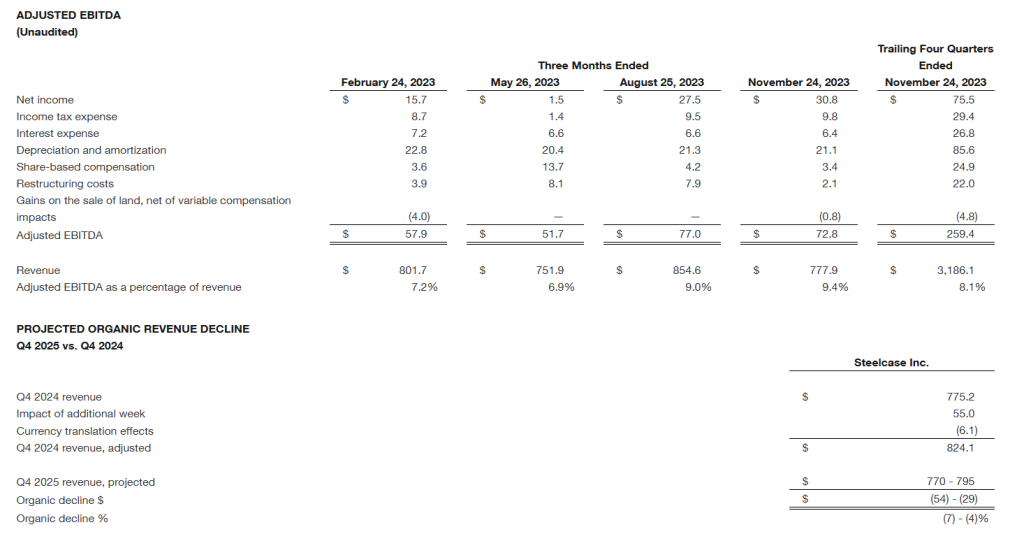

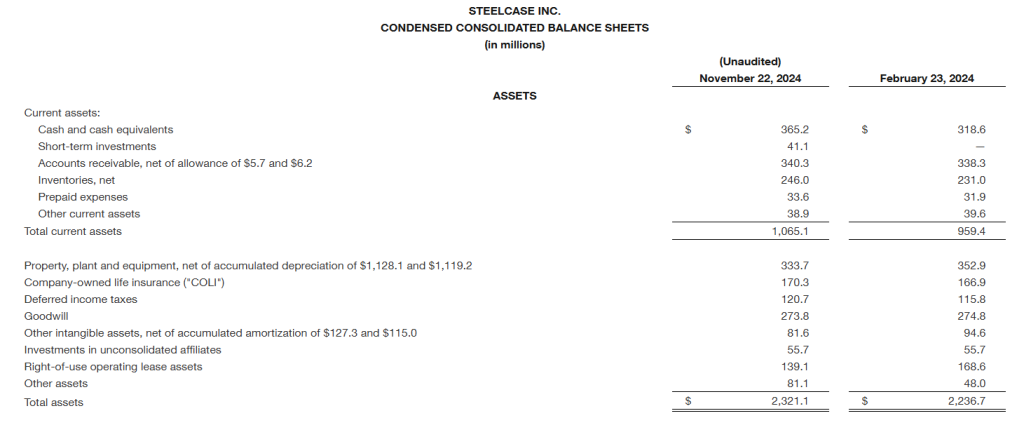

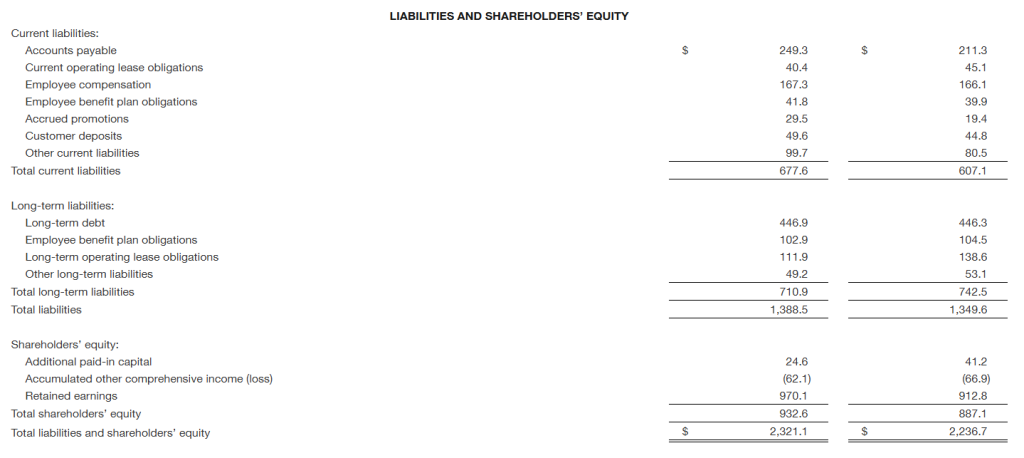

Total liquidity, which is comprised of cash and cash equivalents, short-term investments and the cash surrender value of company-owned life insurance, aggregated to $576.6 million at the end of the third quarter and represented an increase of $152.0 million compared to the prior year. Total debt was $446.9 million. Trailing four quarter adjusted EBITDA of $283.6 million (or 9.0 percent of revenue) represented an increase of 9 percent compared to the prior year.

The Board of Directors has declared a quarterly cash dividend of $0.10 per share, to be paid on or before January 13, 2025, to shareholders of record as of December 30, 2024.

Outlook

At the end of the third quarter, the company’s backlog was approximately $664 million, which was 5 percent lower than the prior year. Orders in the first three weeks of the fourth quarter grew 15 percent compared to the prior year and included a number of large projects scheduled to ship beyond the end of the quarter. The company expects fourth quarter fiscal 2025 revenue, which contains an additional week compared to the prior year, to be in the range of $770 to $795 million. The company reported revenue of $775.2 million in the fourth quarter of fiscal 2024. The projected revenue range translates to a decline of 1 percent to growth of 3 percent compared to the prior year, or a decline of 4 to 7 percent on an organic basis.

The company expects to report earnings per share of between $0.17 to $0.21 for the fourth quarter of fiscal 2025 and adjusted earnings per share of between $0.20 to $0.24. The company reported earnings per share of $0.18 and adjusted earnings per share of $0.23 in the fourth quarter of fiscal 2024.

The fourth quarter estimates include:

gross margin of approximately 33.5 percent,

projected operating expenses of between $230 to $235 million, which includes $4.3 million of amortization of purchased intangible assets,

projected interest expense, net of investment income and other income, net, of approximately $1 million and

a projected effective tax rate of approximately 27 percent.

“As work and work patterns continue to change, we remain focused on developing new solutions and evolving our capabilities to better serve our customers and dealers,” said Sara Armbruster. “Our teams have successfully driven higher levels of profitability all year and we are pleased that our fiscal 2025 adjusted earnings per share are projected to finish above our target.”

Business Segment Footnotes

The Americas segment serves customers in the U.S., Canada, the Caribbean Islands and Latin America with a comprehensive portfolio of furniture, architectural, textile and surface imaging products that are marketed to corporate, government, healthcare, education and retail customers primarily through the Steelcase, AMQ, Coalesse, Designtex, HALCON, Orangebox, Smith System and Viccarbe brands.

The International segment serves customers in EMEA and Asia Pacific with a comprehensive portfolio of furniture and architectural products that are marketed to corporate, government, healthcare, education and retail customers primarily through the Steelcase, Coalesse, Orangebox, Smith System and Viccarbe brands.

Webcast

Steelcase will discuss third quarter results and business outlook on a conference call at 8:30 a.m. Eastern time tomorrow. Listeners may access the conference call at http://ir.steelcase.com.

Non-GAAP Financial Measures

This earnings release contains certain non-GAAP financial measures. A “non-GAAP financial measure” is defined as a numerical measure of a company’s financial performance that excludes or includes amounts so as to be different than the most directly comparable measure calculated and presented in accordance with GAAP in the condensed consolidated statements of income, balance sheets or statements of cash flows of the company. The non-GAAP financial measures used are (1) organic revenue growth (decline), (2) adjusted operating income (loss), (3) adjusted earnings per share and (4) adjusted EBITDA. Pursuant to the requirements of Regulation G, the company has provided a reconciliation of each of the non-GAAP financial measures to the most directly comparable GAAP financial measure in the tables above. These measures are supplemental to, and should be used in conjunction with, the most comparable GAAP measures. Management uses these non-GAAP financial measures to monitor and evaluate financial results and trends.

Organic Revenue Growth (Decline)

The company defines organic revenue growth (decline) as revenue growth (decline) excluding the impact of acquisitions and divestitures and foreign currency translation effects. Organic revenue growth (decline) is calculated by adjusting prior year revenue to include revenues of acquired companies prior to the date of the company’s acquisition, to exclude revenues of divested companies and to use current year average exchange rates in the calculation of foreign-denominated revenue. The company believes organic revenue growth (decline) is a meaningful metric to investors as it provides a more consistent comparison of the company’s revenue to prior periods as well as to industry peers.

Adjusted Operating Income (Loss) and Adjusted Earnings Per Share

The company defines adjusted operating income (loss) as operating income (loss) excluding amortization of purchased intangible assets, restructuring costs (benefits) and gains (losses) on the sale of land, net of variable compensation impacts. The company defines adjusted earnings per share as earnings per share excluding amortization of purchased intangible assets, restructuring costs (benefits), gains (losses) on the sale of land, net of variable compensation impacts, and gains (losses) on pension plan settlements, and the related income tax effects of these items.

Amortization of purchased intangible assets: The company may record intangible assets (such as backlog, dealer relationships, trademarks, know-how and designs and proprietary technology) when it acquires companies. The company allocates the fair value of purchase consideration to net tangible and intangible assets acquired based on their estimated fair values. The fair value estimates for these intangible assets require management to make significant estimates and assumptions, which include the useful lives of intangible assets. The company believes that adjusting for amortization of purchased intangible assets provides a more consistent comparison of its operating performance to prior periods as well as to industry peers.

Restructuring costs (benefits): Restructuring costs (benefits) may be recorded as the company’s business strategies change or in response to changing market trends and economic conditions. The company believes that adjusting for restructuring costs (benefits), which are primarily associated with business exit and workforce reduction costs, provides a more consistent comparison of its operating performance to prior periods as well as to industry peers.

Gains (losses) on the sale of land, net of variable compensation impacts: We may sell land when conditions are favorable. Gains and losses on the sale of land may increase or decrease, respectively, our variable compensation expense. We believe adjusting for these items provides a more consistent comparison of our operating performance to prior periods as well as to industry peers. In Q2 2025, we began adjusting for these items, as we realized a significant gain on the sale of land during the quarter which had a significant impact on our variable compensation expense, and we have adjusted the prior periods presented for consistency and comparability.

Gains (losses) on pension plan settlements: We realize gains or losses previously reported as unrealized in Accumulated other comprehensive income (loss) in Other income (expense), net, in connection with pension plan settlements when all risks related to the benefit obligations to plan participants and plan assets are transferred. We believe adjusting for the gains or losses on pension plan settlements provides a more consistent comparison of our operating performance to prior periods as well as to industry peers.

Adjusted EBITDA

The company defines adjusted EBITDA as earnings before interest, taxes, depreciation and amortization (“EBITDA”) adjusted to exclude share-based compensation, restructuring costs (benefits), gains (losses) on the sale of land, net of variable compensation impacts, and gains (losses) on pension plan settlements. The company believes adjusted EBITDA provides investors with useful information regarding the operating profitability of the company as well as a useful comparison to other companies. EBITDA is a measurement commonly used in capital markets to value companies and is used by the company’s lenders and rating agencies to evaluate its performance. The company adjusts EBITDA for share-based compensation as it represents a significant non-cash item which impacts its earnings. The company also adjusts EBITDA for restructuring costs, gains (losses) on the sale of land, net of variable compensation impacts, and gains (losses) on pension plan settlements to provide a more consistent comparison of its earnings to prior periods as well as to industry peers.

Forward-looking Statements

From time to time, in written and oral statements, the company discusses its expectations regarding future events and its plans and objectives for future operations. These forward-looking statements discuss goals, intentions and expectations as to future trends, plans, events, results of operations or financial condition, or state other information relating to the company, based on current beliefs of management as well as assumptions made by, and information currently available to, the company. Forward-looking statements generally are accompanied by words such as “anticipate,” “believe,” “could,” “estimate,” “expect,” “forecast,” “intend,” “may,” “possible,” “potential,” “predict,” “project,” “target” or other similar words, phrases or expressions. Although the company believes these forward-looking statements are reasonable, they are based upon a number of assumptions concerning future conditions, any or all of which may ultimately prove to be inaccurate. Forward-looking statements involve a number of risks and uncertainties that could cause actual results to differ materially from those in the forward-looking statements and vary from the company’s expectations because of factors such as, but not limited to, competitive and general economic conditions domestically and internationally; acts of terrorism, war, governmental action, natural disasters, pandemics and other Force Majeure events; cyberattacks; changes in the legal and regulatory environment; changes in raw material, commodity and other input costs; currency fluctuations; changes in customer demand; and the other risks and contingencies detailed in the company’s most recent Annual Report on Form 10-K and its other filings with the Securities and Exchange Commission. Steelcase undertakes no obligation to update, amend, or clarify forward-looking statements, whether as a result of new information, future events, or otherwise.

About Steelcase Inc.

Established in 1912, Steelcase is a global design, research and thought leader in the world of work. We help people do their best work by creating places that work better. Along with more than 30 creative and technology partner brands, we design and manufacture furnishings and solutions for the many places where work happens – including learning, health and work from home. Our solutions come to life through our community of expert Steelcase dealers in approximately 770 locations, as well as our online Steelcase store and other retail partners. Founded in Grand Rapids, Michigan, Steelcase is a publicly traded company with fiscal year 2024 revenue of $3.2 billion. With approximately 11,300 global employees and our dealer community, we come together for people and the planet – using our business to help the world work better.

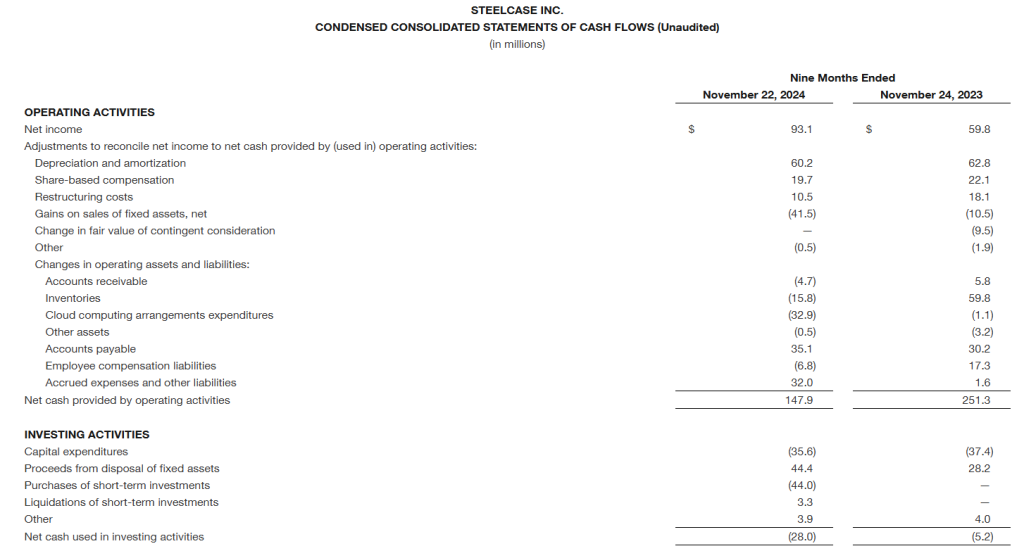

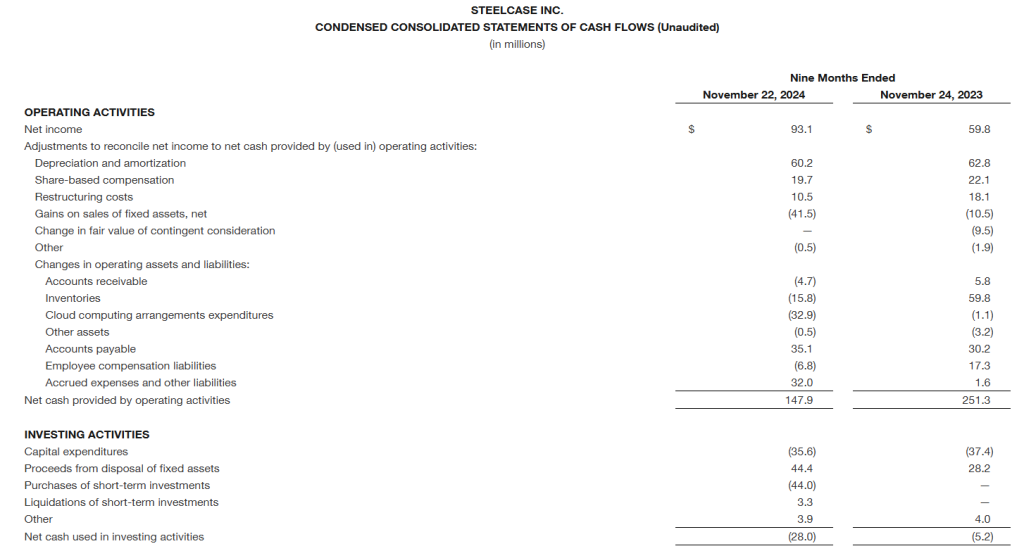

(1) These amounts include restricted cash of $7.3 and $6.8 as of February 23, 2024 and February 24, 2023, respectively.

(2) These amounts include restricted cash of $7.2 and $7.1 as of November 22, 2024 and November 24, 2023, respectively.

Restricted cash primarily represents funds held in escrow for potential future workers’ compensation and product liability claims. The restricted cash balance is included as part ofOther assetson the Condensed Consolidated Balance Sheets.

Joe Gomes, CFA, Managing Director, Equity Research Analyst, Generalist , Noble Capital Markets, Inc.

Joshua Zoepfel, Research Associate, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

3Q25 Results. Revenue was $794.9 million, up 2.1% y-o-y, with higher revenue from government, large corporate, healthcare, and education customers as the drivers. Organic revenue was up 3%, with Americas up 7% and International off 8%. Gross margin came in at 33.4%, up 100 bp y-o-y. GAAP EPS totaled $0.16 versus $0.26, while adjusted EPS was $0.30 versus $0.29.

Green Shoots. Orders in the first three weeks of 4Q25 grew 15% y-o-y. Internationally, Steelcase is seeing higher project activity levels, with recent wins related to large opportunities with national accounts in France, Germany, and the Middle East. Continuation of such trends would bode well for future performance.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

Joe Gomes, CFA, Managing Director, Equity Research Analyst, Generalist , Noble Capital Markets, Inc.

Joshua Zoepfel, Research Associate, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

A New Plan. Yesterday, after the market closed, Steelcase filed an 8-k with the Securities & Exchange Commission reporting the Company has entered into a stock repurchase agreement with an independent third party broker. The agreement was established in accordance with Rule 10b5-1 of the Securities Exchange Act of 1934. We believe share repurchases are a good use of excess cash on the balance sheet at current prices.

Details. The broker is authorized to repurchase up to 1.5 million shares of the Company’s common stock on behalf of the Company during the period from October 11, 2024 through December 20, 2024, subject to certain price, market and volume constraints specified in the agreement. At yesterday’s closing price, acquiring the shares would cost approximately $19 million and the 1.5 million shares represent approximately 1.6% of the outstanding Class A shares. The Company has $79.9 million remaining under its $100 million share repurchase plan authorization.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

Joe Gomes, CFA, Managing Director, Equity Research Analyst, Generalist , Noble Capital Markets, Inc.

Joshua Zoepfel, Research Associate, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

Initiating Research Coverage. We are initiating research coverage of Steelcase Inc. with an Outperform rating and a $16 price target. Already the global leader in the office furniture marketplace, we believe there is a substantial opportunity to capture additional wallet share. The Company’s research driven approach is a competitive differentiator, in our view.

Largest, But Room to Grow. Despite being the market leader, we believe Steelcase can benefit from a rising market share in a growing market. Steelcase’s overall market share is relatively modest, providing opportunity for Steelcase to capture additional market share, while secular trends are driving overall growth in the market, with the worldwide Office Furniture space projected to grow at a 7.1% CAGR through 2032.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.