Michael Kupinski, Director of Research, Equity Research Analyst, Digital, Media & Technology , Noble Capital Markets, Inc.

Jacob Mutchler, Research Associate, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

Highlights from a fireside chat. This report highlights a fireside chat with Adolfo Villagomez, CEO, who discussed the company’s four pillar initiative to transform the company into a more efficient, growth focused company.

Improving the company’s cost structure. Management has implemented a comprehensive review of the organization’s operations with the goal of reducing redundancies and improving productivity. The company is targeting approximately $50 million in run-rate cost savings across fiscal years 2026 and 2027, achieved through initiatives such as workforce streamlining, supply chain optimization, procurement improvements, and the reduction of organizational layers.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

Walmart has officially joined the $1 trillion market-cap club, a milestone once reserved almost exclusively for Big Tech giants. Shares of the world’s largest retailer surged to record highs this week, pushing its valuation past the trillion-dollar mark for the first time in its 60-plus-year history. The move underscores a profound shift in how investors view Walmart—not merely as a defensive, low-margin retailer, but as a technology-enabled consumer platform built for the modern economy.

At the core of Walmart’s rise is its ability to thrive across economic cycles. While inflation and tighter budgets have driven value-conscious consumers toward lower prices, Walmart has simultaneously attracted higher-income shoppers through faster delivery, broader online assortments, and improved digital experiences. That rare ability to gain market share both up and down the income ladder has become one of its most powerful competitive advantages.

The transformation did not happen overnight. After lagging peers in e-commerce during the early 2000s, Walmart spent years rebuilding its digital foundation. Today, its online marketplace spans everything from groceries and household staples to luxury resale items and collectibles. More importantly, Walmart has built a fast-growing ecosystem around its core retail business, including advertising, membership programs, fulfillment services, and data-driven logistics—higher-margin segments that investors increasingly reward with premium valuations.

Technology is now central to Walmart’s strategy. The company has been aggressively deploying artificial intelligence across its operations to improve scheduling, inventory management, pricing, and supply-chain efficiency. Recent partnerships with Alphabet and OpenAI signal an ambition to embed Walmart directly into emerging AI-driven shopping workflows, allowing consumers to browse and purchase products through conversational platforms like ChatGPT and Google’s Gemini. These initiatives have helped reframe Walmart as a serious tech contender rather than a legacy retailer playing catch-up.

Investor confidence has followed. Walmart’s stock is up double digits this year, outperforming the broader market and earning a spot in the Nasdaq 100 Index—an unusual distinction for a consumer staples company. Analysts point to consistent execution, disciplined cost control, and management’s willingness to reinvest savings into price leadership as key drivers of continued momentum.

Still, the trillion-dollar valuation raises questions about how much upside remains. Walmart now trades at more than 40 times forward earnings, near all-time highs, leaving less room for error. Competition is intensifying as Amazon doubles down on speed and logistics, Aldi expands its U.S. footprint, and Target works to revive growth through design-focused merchandising. Execution missteps or slowing consumer demand could test investor patience.

Yet Walmart’s recent decision to raise full-year sales and profit guidance has helped quiet some concerns. Management continues to signal a conservative outlook, a strategy that has historically set the stage for earnings beats. With fourth-quarter results approaching, the market will be watching closely for confirmation that Walmart can sustain growth while justifying its premium multiple.

Ultimately, Walmart’s ascent into the trillion-dollar club reflects a broader reality: scale, data, logistics, and technology now matter as much in retail as they do in software. By combining everyday value with digital innovation, Walmart has rewritten its investment narrative—and in the process, secured its place among the most valuable companies on the planet.

Holiday Period Total Net Sales Increased 5.3% vs. Last Year Led by 9.7% Growth in Direct-to-Consumer Segment

NEW YORK–(BUSINESS WIRE)– Vince Holding Corp., (Nasdaq: VNCE) (“VNCE” or the “Company”), a global retail platform, today announced sales for the nine-week holiday period ended January 3, 2026.

Holiday Sales Highlights (Unaudited Results for Nine-Week Period Ended January 3, 2026)

Total company net sales increased 5.3% compared to the prior year period

Direct-to-Consumer segment sales increased 9.7% compared to the prior year period

Wholesale segment sales decreased 2.7% compared to the prior year period

Brendan Hoffman, Chief Executive Officer of VNCE commented, “Our direct-to-consumer segment continues to deliver exceptional results, building on the strong momentum from our strategic investments in customer experience enhancements and e-commerce capabilities. Within wholesale, we have continued to see strong performance at the register with key partners helping to offset disruption in receipt flow with Saks Global given current dynamics. This overall performance, combined with our disciplined approach to balancing strategic pricing changes, promotional activity, and cost management, demonstrates the strength of our business model. As we look ahead, we will continue to execute and deliver on our strategic priorities that we believe will position us well for long-term profitable growth.”

Based on holiday sales performance, total company net sales have trended in line with prior guidance and Adjusted EBITDA as a % of Net Sales and Adjusted Operating Income as a % of Net Sales have trended in line with the higher end of prior guidance ranges for the fourth quarter and full year fiscal 2025.

The Company continues to monitor developments with its wholesale partner, Saks Global, and guidance does not reflect any outcome of its reported status. Saks Global represented less than 7% of total company net sales as of Fiscal 2024.

The holiday sales results reported in this press release are unaudited and preliminary. These amounts are based on currently available information and are subject to change following the completion of any customary financial closing procedures for the fiscal quarter ending January 31, 2026.

ICR Conference As previously announced, the Company will be presenting at the 28th Annual ICR Conference today, Monday, January 12, 2026, at 8:30 AM Eastern Time. The audio portion of the presentation will be webcast live on the investor relations section of the Company’s website, http://investors.vince.com/.

ABOUT VINCE HOLDING CORP.

Vince Holding Corp. is a global retail platform that operates the Vince brand women’s and men’s ready to wear business. Vince, established in 2002, is a leading global luxury apparel and accessories brand best known for creating elevated yet understated pieces for every day effortless style. Vince Holding Corp. operates 46 full-price retail stores, 14 outlet stores, and its e-commerce site, as well as through premium wholesale channels globally. Please visit www.vince.com for more information.

Forward-Looking Statements: This document, and any statements incorporated by reference herein contain forward-looking statements under the Private Securities Litigation Reform Act of 1995. Forward-looking statements include statements regarding, among other things, our current expectations about possible or assumed future results of operations of the Company and are indicated by words or phrases such as “may,” “will,” “should,” “believe,” “expect,” “seek,” “anticipate,” “intend,” “estimate,” “plan,” “target,” “project,” “forecast,” “envision” and other similar phrases. Although we believe the assumptions and expectations reflected in these forward-looking statements are reasonable, these assumptions and expectations may not prove to be correct and we may not achieve the results or benefits anticipated. These forward-looking statements are not guarantees of actual results, and our actual results may differ materially from those suggested in the forward-looking statements. These forward-looking statements involve a number of risks and uncertainties, some of which are beyond our control, including, without limitation: changes to and unpredictability in the trade policies and tariffs imposed by the U.S. and the governments of other nations; our ability to maintain our larger wholesale partners; our ability to maintain adequate cash flow from operations or availability under our revolving credit facility to meet our liquidity needs; general economic conditions; restrictions on our operations under our credit facilities; our ability to improve our profitability; our ability to accurately forecast customer demand for our products; our ability to maintain the license agreement with ABG Vince, a subsidiary of Authentic Brands Group; ABG Vince’s expansion of the Vince brand into other categories and territories; ABG Vince’s approval rights and other actions; our ability to realize the benefits of our strategic initiatives; the execution of our customer strategy; our ability to make lease payments when due; our ability to open retail stores under favorable lease terms and operate and maintain new and existing retail stores successfully; our operating experience and brand recognition in international markets; our ability to remediate the identified material weakness in our internal control over financial reporting; our ability to comply with domestic and international laws, regulations and orders; increased scrutiny regarding our approach to sustainability matters and environmental, social and governance practices; competition in the apparel and fashion industry; the transition associated with the appointment of new chief executive officer and new chief financial officer; our ability to attract and retain key personnel; seasonal and quarterly variations in our revenue and income; the protection and enforcement of intellectual property rights relating to the Vince brand; our ability to successfully conclude remaining matters following the wind down of the Rebecca Taylor business; the extent of our foreign sourcing; our reliance on independent manufacturers; our ability to ensure the proper operation of the distribution facilities by third-party logistics providers; fluctuations in the price, availability and quality of raw materials; the ethical business and compliance practices of our independent manufacturers; our ability to mitigate system or data security issues, such as cyber or malware attacks, as well as other major system failures; our ability to adopt, optimize and improve our information technology systems, processes and functions; our ability to comply with privacy-related obligations; our status as a “controlled company”; our status as a “smaller reporting company”; and other factors as set forth from time to time in our Securities and Exchange Commission filings, including those described under “Item 1A—Risk Factors” in our Annual Report on Form 10-K and Quarterly Reports on Form 10-Q. We intend these forward-looking statements to speak only as of the time of this release and do not undertake to update or revise them as more information becomes available, except as required by law.

Michael Kupinski, Director of Research, Equity Research Analyst, Digital, Media & Technology , Noble Capital Markets, Inc.

Jacob Mutchler, Research Associate, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

Execution inflection driven by digital and DTC momentum. 2025 marked a clear improvement in operating execution, led by stronger e-commerce performance, enhanced digital capabilities, and early traction from the dropship initiative, which collectively supported revenue growth and improved operating leverage.

Pricing power and profitability improved despite cost headwinds. The company demonstrated brand resilience through higher average selling prices, stable unit volumes, improved full-price sell-through, and disciplined cost management, allowing it to offset tariff and freight pressures and deliver meaningful adjusted EBITDA upside.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

Michael Kupinski, Director of Research, Equity Research Analyst, Digital, Media & Technology , Noble Capital Markets, Inc.

Jacob Mutchler, Research Associate, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

Solid Q3 Results. The company reported Q3 revenue of $85.1 million, beating our estimate of $80.0 million by 6.4%. Adj. EBITDA of $6.5 million, strongly outperformed our estimate of $1.7 million by 289%. The strong operating results were driven by growth in the wholesale and direct-to-consumer channels, its e-commerce platform, and by effective tariff mitigation strategies.

Digital momentum. Notably, the company’s e-commerce platform experienced triple-digit traffic growth late in the quarter, creating a strong backdrop for the launch of its dropship initiative. While the initiative currently offers only footwear, the company highlighted encouraging early results and plans to expand product offerings, leveraging its partnership with Authentic Brands. In our view, the dropship strategy provides the company with a capital-efficient way to broaden product offerings while gathering customer insight.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

Michael Kupinski, Director of Research, Equity Research Analyst, Digital, Media & Technology , Noble Capital Markets, Inc.

Jacob Mutchler, Research Associate, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

Q3 Results. The company reported Q3 revenue of $1.1 million and an adj. EBITDA loss of $0.7 million, both of which were modestly lower than our estimates of $1.6 million and a loss of $0.2 million, respectively, as illustrated in Figure #1 Q3 Results. Notably, sales for C. Wonder and Christie Brinkley’s TWRHLL were disrupted by tariff-related vendor issues and HSN’s studio transition during Q3, which have since been resolved.

Strategic partnerships. The company’s new influencer brands, with Jenny Martinez, Gemma Stafford, Cesar Millan, and Coco Rocha, are expected to launch in Q1 2026. Notably, these celebrity partnerships drove the increase in the company’s social media following from 5 million at the start of the year to its current following of 46 million. In our view, the company is well positioned to reach its goal of 100 million social media followers in 2026.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

For more than 45 years, 1-800-Flowers.com has offered truly original floral arrangements, plants and unique gifts to celebrate birthdays, anniversaries, everyday occasions, and seasonal holidays, and to deliver comfort during times of grief. Backed by a caring team obsessed with service, 1-800-Flowers.com provides customers thoughtful ways to express themselves and connect with the most important people in their lives. 1-800-Flowers.com is part of the 1-800-FLOWERS.COM, Inc. family of brands. Shares in 1-800-FLOWERS.COM, Inc. are traded on the NASDAQ Global Select Market, ticker symbol: FLWS.

Michael Kupinski, Director of Research, Equity Research Analyst, Digital, Media & Technology , Noble Capital Markets, Inc.

Jacob Mutchler, Research Associate, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

Q1 Results. The company reported Q1 revenue of $215.2 million, and an adj. EBITDA loss of $32.9 million, both of which were largely in line with our estimates of $217.9 million and a loss of $33.0 million, respectively. Revenue decreased 11.1% over the prior year period, in part, driven by the company’s strategic decision to focus on positive marketing contribution.

Focused on profitability. In an effort to mitigate the impact of tariffs and soft demand, there is a focus on reducing costs and maintaining stable profitability. As such, operating expenses were $127.3 million in the quarter, down $12 million y-o-y. When excluding non-recurring charges and deferred compensation effects, operating expenses were $124.9 million. The operational expense reductions were driven by a 15.8% reduction in marketing spend, reduced labor costs, and early progress from the company’s efficiency initiatives.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

Michael Kupinski, Director of Research, Equity Research Analyst, Digital, Media & Technology , Noble Capital Markets, Inc.

Jacob Mutchler, Research Associate, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

Exits its Mizrahi interest. The company transferred its remaining 17.5% interest in Isaac Mizrahi to IM Topco, effectively exiting its interest in the brand. The exit of the Mizrahi relationship with Xcel caps a storied and successful run with the company since 2011. Under Xcel, Mizrahi expanded its categories and collections on QVC and into such retailers as Bloomingdale’s and Nordstrom.

Financial upside. Xcel has a participation right should IM Topco sell the company above $46.0 million, coincidentally, the price that Xcel sold its 60% interest. Xcel would receive 15% of the net consideration in excess of the $46 million. In addition, we believe that the company will benefit from the absent of costs related to the brand, particularly employee costs.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

Michael Kupinski, Director of Research, Equity Research Analyst, Digital, Media & Technology , Noble Capital Markets, Inc.

Jacob Mutchler, Research Associate, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

Solid Q2 Results. The company reported Q2 revenue of $73.2 million, modestly beating our estimate of $72.0 million, and adj. EBITDA of $6.7 million, which strongly outperformed our estimate of $0.85 million by 685%. The strong adj. EBITDA was largely driven by management’s ability to execute on its tariff mitigation strategies, resulting in an improved gross profit margin.

Mitigating tariff impacts. Importantly, the company’s gross profit margin increased 300 basis points over the prior year period. The improvement was driven by lower product costing and higher pricing, contributing a 340 basis point improvement, as well as less discounting, which resulted in a 210 basis point improvement. However, the positive margin contributions were softened by tariff and freight impacts of 170 basis points and 100 basis points, respectively.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

Net Sales of $73.2 Million Net Income of $12.1 Million; Adjusted Net Income of $4.9 Million Adjusted EBITDA of $6.7 Million, an increase of $4.0 Million vs. Q2 FY2024

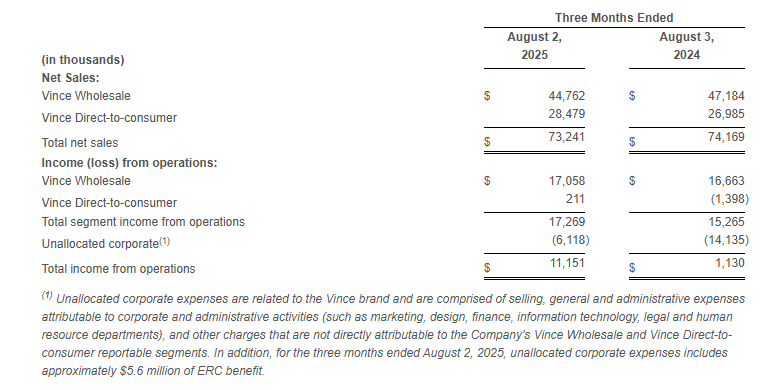

NEW YORK–(BUSINESS WIRE)– Vince Holding Corp. (NYSE: VNCE) (“VNCE” or the “Company”), a global contemporary retailer, today reported its financial results for the second quarter ended August 2, 2025.

Brendan Hoffman, Chief Executive Officer of VNCE said, “We are very proud of our second quarter performance which reflects disciplined execution and strong customer reception to our product offerings especially as we elongated our full-price selling season. As we remain mindful of the dynamic macro environment, our ability to navigate today’s challenges while preserving product quality and customer loyalty remains our utmost priority. Given the strength of our underlying trends, we are pleased to be in a position to begin to reinvest in the business as we remain focused on the growth opportunities ahead for the Vince brand as well as the Vince Holding Corp. platform.”

In this press release, the Company is presenting its financial results in conformity with U.S. generally accepted accounting principles (“GAAP”) as well as on an “adjusted” basis. Adjusted results presented in this press release are non-GAAP financial measures. See “Non-GAAP Financial Measures” below for more information about the Company’s use of non-GAAP financial measures and Exhibit 3 and Exhibit 4 to this press release for a reconciliation of GAAP measures to such non-GAAP measures.

For the second quarter ended August 2, 2025:

Total Company net sales decreased 1.3% to $73.2 million compared to $74.2 million in the second quarter of fiscal 2024. The year-over-year decrease was driven by a 5.1% decline in the wholesale segment partially offset by a 5.5% increase in direct-to-consumer segment. The decline in the wholesale segment was primarily due to the shift in timing of fall shipments compared to the prior year as a result of the earlier uncertainty with respect to tariff policies and impact.

Gross profit was $36.9 million, or 50.4% of net sales, compared to gross profit of $35.1 million, or 47.4% of net sales, in the second quarter of fiscal 2024. The increase in gross margin rate was primarily driven by approximately 340 basis points due to the favorable impact of lower product costing and higher pricing, and approximately 210 basis points due to the favorable impact of lower discounting, partially offset by approximately 170 basis points due to higher tariffs, and approximately 100 basis points due to increased freight costs.

Selling, general, and administrative expenses were $25.8 million, or 35.2% of sales, compared to $34.0 million, or 45.8% of sales, in the second quarter of fiscal 2024. The decrease in SG&A dollars was primarily driven by the receipt of payroll tax credit payments from the U.S. Department of the Treasury under the Employee Retention Credit program (the “ERC benefit”). The ERC benefit was approximately $7.2 million, of which $5.6 million related to the original payroll tax credit claims and was recorded in SG&A as an offset to compensation expenses, with the remaining $1.6 million of interest payments recorded as Other income.

Income from operations was $11.2 million compared to income from operations of $1.1 million in the same period last year. Excluding the payments from the ERC benefit, Adjusted income from operations* was $5.5 million for the second quarter of fiscal 2025.

Income tax expense was $0.1 million, which represents a discrete tax expense relating to interest received in connection with the ERC benefit. The Company has year-to-date ordinary pre-tax losses and is anticipating annual ordinary pre-tax income for the fiscal year. The Company has determined that it is more likely than not that the tax benefit of the year-to-date ordinary pre-tax loss will not be realized in the current or future years and as such, tax provisions for the interim periods should not be recognized until the Company has year-to-date ordinary pre-tax income. The tax provision in the second quarter of fiscal 2025 compares to an income tax benefit of $0.8 million in the same period last year.

Net income was $12.1 million or $0.93 per diluted share compared to net income of $0.6 million or $0.05 per diluted share in the same period last year. Excluding the payments from the ERC benefit and its discrete tax effect, the Adjusted net income* was $4.9 million or $0.38 per diluted share in the second quarter of fiscal 2025.

Adjusted EBITDA* was $6.7 million compared to $2.7 million in the same period last year.

The Company ended the quarter with 58 company-operated Vince stores, a net decrease of 3 stores since the second quarter of fiscal 2024.

Second Quarter Review

Net sales decreased 1.3% to $73.2 million as compared to the second quarter of fiscal 2024.

Wholesale segment sales decreased 5.1% to $44.8 million compared to the second quarter of fiscal 2024.

Direct-to-consumer segment sales increased 5.5% to $28.5 million compared to the second quarter of fiscal 2024.

Income from operations excluding unallocated corporate expenses was $17.3 million compared to income from operations of $15.3 million in the same period last year.

Net Sales and Operating Results by Segment:

Balance Sheet

At the end of the second quarter of fiscal 2025, total borrowings under the Company’s debt agreements totaled $31.1 million and the Company had $42.6 million of excess availability under its revolving credit facility.

Net inventory at the end of the second quarter of fiscal 2025 was $76.7 million compared to $66.3 million at the end of the second quarter of fiscal 2024. The year-over-year increase in inventory was driven by approximately $5.2 million higher inventory carrying value due to tariffs as well as our strategic decision to ship goods earlier in advance of the expiration of reciprocal tariff extensions.

During the quarter ended August 2, 2025, the Company did not issue shares of common stock under the ATM program. The Company continues to have shares available under the program to exercise with proceeds to be used as sources, along with cash from operations, to fund future growth.

Outlook

For the third quarter of fiscal 2025 the Company expects the following:

• Net sales to be approximately flat to up 3% compared to the prior year period.

• Adjusted operating income as a percentage of net sales to be approximately 1% to 4%.

• Adjusted EBITDA as a percentage of net sales to be approximately 2% to 5%.

The above guidance assumes $4 million to $5 million in expected incremental tariff costs, of which the Company expects to mitigate approximately 50% through changes to country of origin, vendor negotiations as well as select and strategic price increases.

Given the uncertainty related to the potential impact and duration of current tariff policy, the Company is not providing guidance for the full year fiscal 2025.

Strategic Partnership with Authentic Brands Group

On May 25, 2023, the Company announced that it completed the previously announced transaction (the “Authentic Transaction”) with Authentic Brands Group (“Authentic”).

In connection with the Authentic Transaction, VNCE entered into an exclusive, long-term license agreement (the “License Agreement”) with Authentic for usage of the contributed intellectual property for VNCE’s existing business in a manner consistent with the Company’s current wholesale, retail and e-commerce operations. The License Agreement contains an initial ten-year term and eight ten-year renewal options allowing VNCE to renew the agreement.

*Non-GAAP Financial Measures

In addition to reporting financial results in accordance with GAAP, the Company has provided, with respect to the financial results relating to the three and six months ended August 2, 2025 and August 3, 2024, adjusted EBITDA, which is a non-GAAP measure. Adjusted EBITDA is calculated as earnings before interest, taxes, depreciation and amortization, share-based compensation, capitalized cloud computing amortization, ERC benefit, and gain on sale of Rebecca Taylor, Inc. and its wholly owned subsidiary (“Gain on Sale of Subsidiary”). For the three and six months ended August 2, 2025 and August 3, 2024, respectively, the Company has provided adjusted income (loss) from operations, adjusted income (loss) before income taxes and equity in net income (loss) of equity method investment, adjusted income (loss) before equity in net income (loss) of equity method investment, adjusted net income (loss), and adjusted earnings (loss) per share, which are non-GAAP measures, in order to eliminate the effect of the ERC benefit, Discrete Tax Effect Associated with ERC benefit, and Gain on Sale of Subsidiary.

The Company believes that the presentation of these non-GAAP measures facilitates an understanding of the Company’s continuing operations without the impact associated with the aforementioned items. While these types of events can and do recur periodically, they are excluded from the indicated financial information due to their impact on the comparability of earnings across periods. Non-GAAP financial measures should not be considered in isolation from, or as a substitute for, financial information prepared in accordance with GAAP. A reconciliation of GAAP to non-GAAP results has been provided in Exhibit 3 and Exhibit 4 to this press release.

Conference Call

A conference call to discuss the first quarter results will be held today, September 10, 2025, at 4:30 p.m. ET, hosted by Vince Holding Corp. Chief Executive Officer, Brendan Hoffman, and Chief Financial Officer, Yuji Okumura. During the conference call, the Company may make comments concerning business and financial developments, trends and other business or financial matters. The Company’s comments, as well as other matters discussed during the conference call, may contain or constitute information that has not been previously disclosed.

Those who wish to participate in the call may do so by dialing (833) 470-1428, conference ID 030527. Any interested party will also have the opportunity to access the call via the Internet at http://investors.vince.com/. To listen to the live call, please go to the website at least 15 minutes early to register and download any necessary audio software. For those who cannot listen to the live broadcast, a recording will be available for 12 months after the date of the event. Recordings may be accessed at http://investors.vince.com.

ABOUT VINCE HOLDING CORP.

Vince Holding Corp. is a global retail company that operates the Vince brand women’s and men’s ready to wear business. Vince, established in 2002, is a leading global luxury apparel and accessories brand best known for creating elevated yet understated pieces for every day effortless style. Vince Holding Corp. operates 45 full-price retail stores, 14 outlet stores, and its e-commerce site, as well as through premium wholesale channels globally. Please visit www.vince.com for more information.

Forward-Looking Statements: This document, and any statements incorporated by reference herein contain forward-looking statements under the Private Securities Litigation Reform Act of 1995. Forward-looking statements include the statements under “Outlook” above as well as statements regarding, among other things, our current expectations about possible or assumed future results of operations of the Company and are indicated by words or phrases such as “may,” “will,” “should,” “believe,” “expect,” “seek,” “anticipate,” “intend,” “estimate,” “plan,” “target,” “project,” “forecast,” “envision” and other similar phrases. Although we believe the assumptions and expectations reflected in these forward-looking statements are reasonable, these assumptions and expectations may not prove to be correct and we may not achieve the results or benefits anticipated. These forward-looking statements are not guarantees of actual results, and our actual results may differ materially from those suggested in the forward-looking statements. These forward-looking statements involve a number of risks and uncertainties, some of which are beyond our control, including, without limitation: changes to and unpredictability in the trade policies and tariffs imposed by the U.S. and the governments of other nations; our ability to maintain adequate cash flow from operations or availability under our revolving credit facility to meet our liquidity needs; general economic conditions; restrictions on our operations under our credit facilities; our ability to improve our profitability; our ability to maintain our larger wholesale partners; our ability to accurately forecast customer demand for our products; our ability to maintain the license agreement with ABG Vince, a subsidiary of Authentic Brands Group; ABG Vince’s expansion of the Vince brand into other categories and territories; ABG Vince’s approval rights and other actions; our ability to realize the benefits of our strategic initiatives; the execution of our customer strategy; our ability to make lease payments when due; our ability to open retail stores under favorable lease terms and operate and maintain new and existing retail stores successfully; our operating experience and brand recognition in international markets; our ability to remediate the identified material weakness in our internal control over financial reporting; our ability to comply with domestic and international laws, regulations and orders; increased scrutiny regarding our approach to sustainability matters and environmental, social and governance practices; competition in the apparel and fashion industry; the transition associated with the appointment of new chief executive officer and new chief financial officer; our ability to attract and retain key personnel; seasonal and quarterly variations in our revenue and income; the protection and enforcement of intellectual property rights relating to the Vince brand; our ability to successfully conclude remaining matters following the wind down of the Rebecca Taylor business; the extent of our foreign sourcing; our reliance on independent manufacturers; our ability to ensure the proper operation of the distribution facilities by third-party logistics providers; fluctuations in the price, availability and quality of raw materials; the ethical business and compliance practices of our independent manufacturers; our ability to mitigate system or data security issues, such as cyber or malware attacks, as well as other major system failures; our ability to adopt, optimize and improve our information technology systems, processes and functions; our ability to comply with privacy-related obligations; our ability to regain compliance with the New York Stock Exchange (the “NYSE”) Listed Company Manual and maintain a listing of our common stock on the NYSE; our status as a “controlled company”; our status as a “smaller reporting company”; and other factors as set forth from time to time in our Securities and Exchange Commission filings, including those described under “Item 1A—Risk Factors” in our Annual Report on Form 10-K and Quarterly Reports on Form 10-Q. We intend these forward-looking statements to speak only as of the time of this release and do not undertake to update or revise them as more information becomes available, except as required by law.

Michael Kupinski, Director of Research, Equity Research Analyst, Digital, Media & Technology , Noble Capital Markets, Inc.

Jacob Mutchler, Research Associate, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

Solid Q2 Results. The company reported Q2 revenue of $73.2 million, modestly beating our estimate of $72.0 million, and adj. EBITDA of $6.7 million, which strongly outperformed our estimate of $0.85 million by 685%, as illustrated in Figure #1 Q2 Results. The strong adj. EBITDA was largely driven by management’s ability to execute on its tariff mitigation strategies, resulting in an improved gross profit margin.

Mitigating tariff impacts. Importantly, the company’s gross profit margin increased 300 basis points over the prior year period. The improvement was driven by lower product costing and higher pricing, contributing a 340 basis point improvement, as well as less discounting, which resulted in a 210 basis point improvement. However, the positive margin contributions were softened by tariff and freight impacts of 170 basis points and 100 basis points, respectively.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

Michael Kupinski, Director of Research, Equity Research Analyst, Digital, Media & Technology , Noble Capital Markets, Inc.

Jacob Mutchler, Research Associate, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

Q2 Results. The company reported Q2 revenue of $1.3 million and an adj. EBITDA loss of $0.3 million, as illustrated in Figure #1 Q2 results. Importantly, while revenue was 22.3% lower than our estimate of $1.7 million, the adj. EBITDA loss of $0.3 million was largely in line with our expectations of a loss of $0.35 million. Furthermore, the on target adj. EBITDA figure was driven by the company’s strategic cost reduction and business transformation efforts, as well as the Lori Goldstein divestiture.

Favorable outlook. While the company is approaching the back half of the year with caution, largely driven by potential tariff impacts, we believe it stands to benefit from a number of favorable developments. Notably, the company is launching its Longaberger brand in Q3 on QVC and announced an accelerated timeline for its new influencer brands. Additionally, the company stands to benefit from its Halston brand as royalties kick in.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

500 5th Avenue 20th Floor New York, NY 10110 United States Sector(s): Consumer Cyclical Industry: Apparel Manufacturing Full Time Employees: 599 Key Executives Name Title Pay Exercised Year Born Mr. Jonathan CEO & Director 825.62k N/A 1958 Ms. Marie Fogel Senior VP and Chief Merchandising & Manufacturing Officer 633.19k N/A 1961 Mr. John Chief Financial Officer

Michael Kupinski, Director of Research, Equity Research Analyst, Digital, Media & Technology , Noble Capital Markets, Inc.

Jacob Mutchler, Research Associate, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

Solid Q1 results. the company reported Q1 revenue of $57.9 million and an adj. EBITDA loss of $3.0 million, both of which were better than our estimates of $56.0 million and a loss of $5.5 million, respectively. Notably, while revenue and adj. EBITDA are both modestly lower than the prior year period; we view the Q1 results favorably, given the company’s ability to manage the uncertain tariff outlook.

Tariff mitigation. The company highlighted that it has been taking steps to reduce its exposure to China, currently roughly 60% of its cost of goods sold. Notably, the company is sourcing from other countries and expects that China will be roughly 25% of its cost of goods by the end of 2025. The company has leadership located in the sourcing countries to ensure product quality.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.