Why the Future Value of the Lottery’s Grand Prize is Significantly Higher than Last Year

There is a link between the current $1.9 billion Powerball prize money and Federal Reserve Chair Jerome Powell – and it is inflating the prize money.

A new billionaire was not minted over the weekend, at least not because of winning the enormous Powerball jackpot prize. So the weekend prize money, plus a small fortune more, is up for grabs at 10:59 PM Monday, November 7. The headline prize money, in this case, $1.9 billion, is the future value of the cash award, which, according to Powerball.com, is $929.1 million. The larger, almost two billion amount, would not have been nearly as large last year. Its sum is much bigger because the Fed has been jacking up interest rates.

To drill down a bit more, the prize calculation uses the 30-year U.S. Treasury bond interest rate to determine the annuity paid to the winner based on the cash lump sum award. The present value of that number, even if on par with a cash award a year ago, would pay a substantially larger annuity. And it is the annuity that is the advertised prize, which draws more and more players as it grows. The more players, the higher the present value or cash prize.

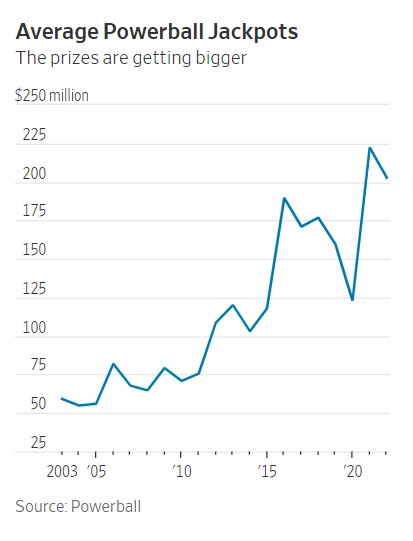

A year ago (November 8, 2021), the 30-year US Treasury bond had a yield of 1.90%. This was used to calculate the headline prize amount. Today, the same term Treasury is yielding 4.27%. This yield impact is roughly reflected in the average prizes over the years.

The Numbers Boiled Down Further

Of all ticket sales, 34% of Powerball ticket sales fund the grand prize. Another 16% fund the lower-tier prizes. (The remaining 50% goes to various state programs, operating costs, and retailer commissions.) If a winner chooses the lump sum payout, they receive the 34%. If instead, the winner chooses the jackpot in annual payments over 30 years, the prize money is invested in a portfolio of bonds.

The last time a winner chose an annuity was in 2014.

Economists who have researched lotteries have learned that once jackpots near the $500 million mark, non-regular lottery players are more likely to take a chance. The $500 million or more mark is where the media begins to make “lottery fever” a news event worth reporting on. The added publicity then feeds more money into the pot.

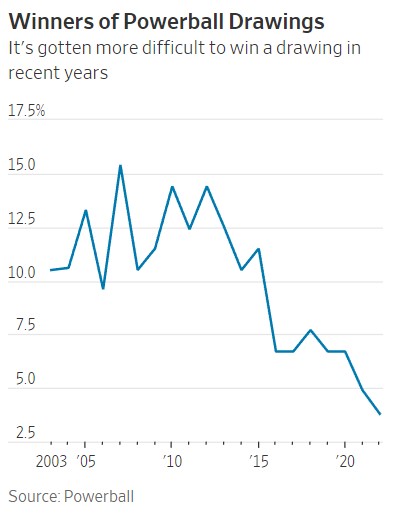

The prize pools are also growing because the games of chance have become statistically more difficult to take the top prize. In 2015, Powerball increased the cost of the ticket and altered the game to make it easier for players to win smaller prizes while reducing the odds of winning the headline prize.

Only 3.8% of drawings so far this year had had a winner, down from roughly 11% in 2014, the last full year before the change went into effect.

This is why the five times in the U.S. where $1 billion has been surpassed have all been recent. They include the biggest one, a $1.58 billion prize from Powerball in 2016, followed by a $1.53 billion Mega Millions jackpot in 2018 and this week’s $1.5 billion Powerball prize.

Lottery tickets also tend to become more popular during economic downturns and when people become more money conscious.

Even though the odds of winning Powerball are 1 in 292.2 million, players will take a shot and buy a ticket to have the fantasy. If the prize money continues to reach over $500 million on a regular basis, it may work against the program as those who don’t normally play won’t feel it is a special event.

These Are the New Federal Tax Brackets and Standard Deductions For 2023

Now for the inflation good news. Thankfully, as it relates to federal income taxes, the IRS makes annual adjustments to certain tax provisions. Simply put, the higher the inflation, the more tax credit benefit, which includes tax credits and taxable wages adjusted downward. So, in addition to receiving much higher COLA increases on Social Security payments and earning an interest rate in excess of 9% on U.S. Savings Bonds, those making an income in 2023 are likely to see more take-home pay.

The IRS Numbers Are In

The IRS announced the 2023 inflation adjustments to the standard deduction and other tax provisions for the 2023 tax year. The adjustments affect 60 provisions in the tax code, and leave a few key provisions unchanged.

Highlights of Changes in Revenue Procedure 2021-38

The tax year 2023 adjustments described below generally apply to tax returns filed in 2024. A higher level of details about these annual adjustments can be found in IRS Revenue Procedure 2022-38PDF.

The standard deduction for married couples filing jointly for tax year 2023 rises to $27,700 up $1,800 from the prior year. For single taxpayers and married individuals filing separately, the standard deduction rises to $13,850 for 2023, up $900, and for heads of households, the standard deduction will be $20,800 for tax year 2023, up $1,400 from the amount for tax year 2022.

Marginal Rates: For tax year 2023, the top tax rate remains 37% for individual single taxpayers with incomes greater than $578,125 ($693,750 for married couples filing jointly).

The other rates are:

35% for incomes over $231,250 ($462,500 for married couples filing jointly);

32% for incomes over $182,100 ($364,200 for married couples filing jointly);

24% for incomes over $95,375 ($190,750 for married couples filing jointly);

22% for incomes over $44,725 ($89,450 for married couples filing jointly);

12% for incomes over $11,000 ($22,000 for married couples filing jointly).

The lowest rate is 10% for incomes of single individuals with incomes of $11,000 or less ($22,000 for married couples filing jointly).

The Alternative Minimum Tax exemption amount for tax year 2023 is $81,300 and begins to phase out at $578,150 ($126,500 for married couples filing jointly for whom the exemption begins to phase out at $1,156,300). The 2022 exemption amount was $75,900 and began to phase out at $539,900 ($118,100 for married couples filing jointly for whom the exemption began to phase out at $1,079,800).

The tax year 2023 maximum Earned Income Tax Credit amount is $7,430 for qualifying taxpayers who have three or more qualifying children, up from $6,935 for tax year 2022. The revenue procedure contains a table providing maximum EITC amount for other categories, income thresholds and phase-outs.

For 2023, the monthly limitation for the qualified transportation fringe benefit and the monthly limitation for qualified parking increases to $300, up $20 from the limit for 2022.

For the taxable years beginning in 2023, the dollar limitation for employee salary reductions for contributions to health flexible spending arrangements increases to $3,050. For cafeteria plans that permit the carryover of unused amounts, the maximum carryover amount is $610, an increase of $40 from taxable years beginning in 2022.

For tax year 2023, participants who have self-only coverage in a Medical Savings Account, the plan must have an annual deductible that is not less than $2,650, up $200 from tax year 2022; but not more than $3,950, an increase of $250 from tax year 2022. For self-only coverage, the maximum out-of-pocket expense amount is $5,300, up $350 from 2022. For tax year 2023, for family coverage, the annual deductible is not less than $5,300, up from $4,950 for 2022; however, the deductible cannot be more than $7,900, up $500 from the limit for tax year 2022. For family coverage, the out-of-pocket expense limit is $9,650 for tax year 2023, an increase of $600 from tax year 2022.

For tax year 2023, the foreign earned income exclusion is $120,000 up from $112,000 for tax year 2022.

Estates of decedents who die during 2023 have a basic exclusion amount of $12,920,000, up from a total of $12,060,000 for estates of decedents who died in 2022.

The annual exclusion for gifts increases to $17,000 for calendar year 2023, up from $16,000 for calendar year 2021.

The maximum credit allowed for adoptions for tax year 2023 is the amount of qualified adoption expenses up to $15,950, up from $14,890 for 2022.

Brand New for 2023

The Inflation Reduction Act extended some energy-related tax breaks and indexed for inflation the energy-efficient commercial buildings deduction beginning with the tax year 2023. For 2023, the applicable dollar value used to determine the maximum allowance of the deduction is $0.54 increased by $0.02 for each percentage point by which the total annual energy and power costs for the building are certified to be reduced by a percentage greater than 25 percent (but not above $1.07). The applicable dollar value used to determine the increased deduction amount for certain property is $2.68 increased (but not above $5.36) by $0.11 for each percentage point by which the total annual energy and power costs for the building are certified to be reduced by a percentage greater than 25 percent.

Items Unaffected by Inflation Indexing

By statute, these items that were indexed for inflation in the past are currently not adjusted.

The personal exemption for tax year 2023 remains at 0, as it was for 2022, this elimination of the personal exemption was a provision in the Tax Cuts and Jobs Act.

For 2023, as in 2022, 2021, 2020, 2019 and 2018, there is no limitation on itemized deductions, as that limitation was eliminated by the Tax Cuts and Jobs Act.

The modified adjusted gross income amount used by joint filers to determine the reduction in the Lifetime Learning Credit provided in § 25A(d)(2) is not adjusted for inflation for taxable years beginning after December 31, 2020. The Lifetime Learning Credit is phased out for taxpayers with modified adjusted gross income in excess of $80,000 ($160,000 for joint returns).

What Else is Impacted

The maximum contribution amount for a 401(k) or similar workplace retirement plan is governed by yet another formula that uses September inflation data. It is estimated that the contribution limit will increase to $22,500 in 2023 from $20,500 this year and the catch-contribution amount for those age 50 or more will rise from $6,500 to at least $7,500.

The child tax credit under current law is $2,000 per child is not adjusted for inflation. But the additional child tax credit, which is refundable and available even to taxpayers that have no tax liability, is adjusted for inflation. It is expected to increase from $1,500 to $1,600 in 2023.

For those that look forward to capping out payments to Social Security, there is bad news. This has also increased. According to the 2022 Social Security Trustees Report, the wage base tax rate is projected to increase 5.5% from $147,000 to $155,100 in 2023.

Costs are rising, but so are deductions. It’s improbable that the reduced taxes will offset skyrocketing inflation, but at least there is one financial category that is helped by the increases.