Motorsport Games, a Motorsport Network company, combines innovative and engaging video games with exciting esports competitions and content for racing fans and gamers around the globe. The Company is the officially licensed video game developer and publisher for iconic motorsport racing series across PC, PlayStation, Xbox, Nintendo Switch and mobile, including NASCAR, INDYCAR, 24 Hours of Le Mans and the British Touring Car Championship (“BTCC”). Motorsport Games is an award-winning esports partner of choice for 24 Hours of Le Mans, Formula E, BTCC, the FIA World Rallycross Championship and the eNASCAR Heat Pro League, among others.

Michael Kupinski, Director of Research, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

Debt for equity swap. The company announced that it entered into an agreement with its majority shareholder, Motorsport Network, to repay $1 million in debt for 338,983 MSGM shares. The move significantly improves the company’s liquidity and reduces its interest expense. Notably, the move adds confidence that Motorsport Network has confidence in Motorsport Games.

Regains compliance with listing rules. Following the move, the company received notice from Nasdaq that Motorsport regained full compliance with the Nasdaq Listing Rules.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

MIAMI, Jan. 30, 2023 (GLOBE NEWSWIRE) — Motorsport Games Inc. (NASDAQ: MSGM) (“Motorsport Games” or the “Company”) today announced that the Company has entered into a debt-for-equity exchange agreement (the “Agreement”) with its majority stockholder, Motorsport Network, LLC (“Motorsport Network”), to repay $1,000,000 in debt (including principal and accrued and not yet paid interest) of the Company under its $12 million line of credit with Motorsport Network.

Under the Agreement, for a period of 60 days from the closing of the transactions contemplated under the Agreement, the Company agreed to file a registration statement with the Securities and Exchange Commission (“SEC”) upon Motorsport Network’s demand in order to register the resale of the shares acquired by Motorsport Network under the Agreement, subject to the terms and conditions of the Agreement. The Agreement also granted certain piggyback registration rights to Motorsport Network.

“This debt exchange benefits our balance sheet, allows us to pay less interest expense and will help Motorsport Games to pursue product development and growth opportunities,” said Dmitry Kozko, CEO and Executive Chairman of Motorsport Games. “This debt exchange also signals the ongoing confidence that our majority shareholder, Motorsport Network, has in Motorsport Games.”

The foregoing summary of the Agreement is incomplete, and further details relating to the Agreement, including additional terms and conditions, and this transaction will be contained in the Current Report on Form 8-K the Company intends to file with the SEC later today.

About Motorsport Games:

Motorsport Games, a Motorsport Network company, is a leading racing game developer, publisher and esports ecosystem provider of official motorsport racing series throughout the world. Combining innovative and engaging video games with exciting esports competitions and content for racing fans and gamers, Motorsport Games strives to make the joy of racing accessible to everyone. The Company is the officially licensed video game developer and publisher for iconic motorsport racing series across PC, PlayStation, Xbox, Nintendo Switch and mobile, including NASCAR, INDYCAR, 24 Hours of Le Mans and the British Touring Car Championship (“BTCC”), as well as the industry leading rFactor 2 and KartKraft simulations. rFactor 2 also serves as the official sim racing platform of Formula E, while also powering F1 Arcade through a partnership with Kindred Concepts. Motorsport Games is an award-winning esports partner of choice for 24 Hours of Le Mans, Formula E, BTCC, the FIA World Rallycross Championship and the eNASCAR Heat Pro League, among others. Motorsport Games is building a virtual racing ecosystem where each product drives excitement, every esports event is an adventure and every story inspires.

Forward Looking Statements:

Certain statements in this press release which are not historical facts are forward-looking statements within the meaning of Section 27A of the Securities Act of 1933, as amended, and Section 21E of the Securities Exchange Act of 1934, as amended, and are provided pursuant to the safe harbor provisions of the Private Securities Litigation Reform Act of 1995. Any statements in this press release that are not statements of historical fact may be deemed forward-looking statements. Words such as “continue,” “will,” “may,” “could,” “should,” “expect,” “expected,” “plans,” “intend,” “anticipate,” “believe,” “estimate,” “predict,” “potential,” and similar expressions are intended to identify such forward-looking statements. All forward-looking statements involve significant risks and uncertainties that could cause actual results to differ materially from those expressed or implied in the forward-looking statements, many of which are generally outside the control of Motorsport Games and are difficult to predict. Examples of such risks and uncertainties include, without limitation, issuance of shares of Class A common stock under the Agreement impacting the value of the Company’s Class A common stock and less than expected benefits, such as the ability to develop product and achieve growth, from any transaction under the Agreement. Additional factors that could cause actual results to differ materially from those expressed or implied in the forward-looking statements can be found in Motorsport Games’ filings with the SEC, including its Annual Report on Form 10-K for the fiscal year ended December 31, 2021, its Quarterly Reports on Form 10-Q filed with the SEC during 2022, as well as in its subsequent filings with the SEC. Motorsport Games anticipates that subsequent events and developments may cause its plans, intentions and expectations to change. Motorsport Games assumes no obligation, and it specifically disclaims any intention or obligation, to update any forward-looking statements, whether as a result of new information, future events or otherwise, except as expressly required by law. Forward-looking statements speak only as of the date they are made and should not be relied upon as representing Motorsport Games’ plans and expectations as of any subsequent date.

Website and Social Media Disclosure:

Investors and others should note that we announce material financial information to our investors using our investor relations website (ir.motorsportgames.com), SEC filings, press releases, public conference calls and webcasts. We use these channels, as well as social media and blogs, to communicate with our investors and the public about our company and our products. It is possible that the information we post on our websites, social media and blogs could be deemed to be material information. Therefore, we encourage investors, the media and others interested in our company to review the information we post on the websites, social media channels and blogs, including the following (which list we will update from time to time on our investor relations website):

MIAMI, Jan. 30, 2023 (GLOBE NEWSWIRE) — Adam Breeden, the pioneer of competitive socialising in the UK and entrepreneurial force behind some of the sector’s most successful concepts, has officially opened his most ambitious and exciting project. F1® Arcade, the world’s first official premium F1 experiential venue, opened on December 12, 2022 in London at One New Change, St Pauls.

The immersive state of the art F1 racing simulation experience comes with 60 motion F1 simulators, powered by the rFactor 2 racing simulation software provided by Motorsport Games, combined with exclusive F1® content, enabling guests to live the thrill of racing, complemented by a best-in-class food and beverage offering created by an executive chef and expert mixologists.

“With a mission of making the thrill of motorsports available to everyone, we graciously appreciate the selection of rFactor 2 to provide the virtual racing experience and real world handling and competition to F1® Arcade and their customers!” said Dmitry Kozko, CEO, at Motorsport Games Inc. (NASDAQ: MSGM) (“Motorsport Games”), a leading racing game developer, publisher and esports ecosystem provider of official motorsport racing series throughout the world.

Dom Duhan, Executive Producer at Studio 397 added, “It was a pleasure for our expert simulation development team at Studio 397 to collaborate on developing the racing elements, and we expect that customers will be blown away by the experience.”

“Since opening F1® Arcade in December, the take up has been absolutely phenomenal. Our ambition was to introduce a truly innovative experience that makes sim racing accessible for all in a fun and premium competitive socialising environment. To deliver on this, we needed a partner that could fully tailor the game experience, which is why we selected rFactor 2 and Motorsport Games to work with us on this project. The reaction from customers in our first month has been fantastic and we look forward to welcoming many more at our first London venue and future venues as we expand,” said Adam Breeden, Founder and Chief Executive of Kindred Concepts.

Future plans for F1® Arcade include a Birmingham, UK site in 2023 with further locations powered by rFactor 2 set to be announced. For all F1® Arcade news, be sure to follow @F1Arcade on social media platforms.

About Motorsport Games: Motorsport Games, a Motorsport Network company, is a leading racing game developer, publisher and esports ecosystem provider of official motorsport racing series throughout the world. Combining innovative and engaging video games with exciting esports competitions and content for racing fans and gamers, Motorsport Games strives to make the joy of racing accessible to everyone. The Company is the officially licensed video game developer and publisher for iconic motorsport racing series across PC, PlayStation, Xbox, Nintendo Switch and mobile, including NASCAR, INDYCAR, 24 Hours of Le Mans and the British Touring Car Championship (“BTCC”), as well as the industry leading rFactor 2 and KartKraft simulations. rFactor 2 also serves as the official sim racing platform of Formula E, while also powering F1 Arcade through a partnership with Kindred Concepts. Motorsport Games is an award-winning esports partner of choice for 24 Hours of Le Mans, Formula E, BTCC, the FIA World Rallycross Championship and the eNASCAR Heat Pro League, among others. Motorsport Games is building a virtual racing ecosystem where each product drives excitement, every esports event is an adventure and every story inspires.

Forward-Looking Statements: Certain statements in this press release which are not historical facts are forward-looking statements within the meaning of Section 27A of the Securities Act of 1933, as amended, and Section 21E of the Securities Exchange Act of 1934, as amended, and are provided pursuant to the safe harbor provisions of the Private Securities Litigation Reform Act of 1995. Any statements in this press release that are not statements of historical fact may be deemed forward-looking statements. Words such as “continue,” “will,” “may,” “could,” “should,” “expect,” “expected,” “plans,” “intend,” “anticipate,” “believe,” “estimate,” “predict,” “potential,” and similar expressions are intended to identify such forward-looking statements. These forward-looking statements include, but are not limited to, statements concerning expectations and benefits of the rFactor 2 simulation platform in powering F1® Arcade, as well as expectations that future F1® Arcade locations will be powered by the rFactor 2 simulation platform. All forward-looking statements involve significant risks and uncertainties that could cause actual results to differ materially from those expressed or implied in the forward-looking statements, many of which are generally outside the control of Motorsport Games and are difficult to predict. Examples of such risks and uncertainties include, but are not limited to: difficulties, delays in or unanticipated events that may impact the timing and expected benefits of the rFactor 2 simulation platform, such as rFactor 2 updates and/or related products and features. Factors other than those referred to above could also cause Motorsport Games’ results to differ materially from expected results. Additional examples of such risks and uncertainties include, but are not limited to: (i) delays and higher than anticipated expenses related to the ongoing and prolonged COVID-19 pandemic, any resurgence of COVID-19 and the Russia invasion of Ukraine; (ii) Motorsport Games’ ability (or inability) to maintain existing, and to secure additional, licenses and other agreements with various racing series; (iii) Motorsport Games’ ability to successfully manage and integrate any joint ventures, acquisitions of businesses, solutions or technologies; (iv) unanticipated operating costs, transaction costs and actual or contingent liabilities; (v) the ability to attract and retain qualified employees and key personnel; (vi) adverse effects of increased competition; (vii) changes in consumer behavior, including as a result of general economic factors, such as increased inflation, higher energy prices and higher interest rates; (viii) Motorsport Games’ inability to protect its intellectual property; and/or (ix) local, industry and general business and economic conditions. Additional factors that could cause actual results to differ materially from those expressed or implied in the forward-looking statements can be found in Motorsport Games’ filings with the Securities and Exchange Commission (the “SEC”), including its Annual Report on Form 10-K for the fiscal year ended December 31, 2021, its Quarterly Reports on Form 10-Q filed with the SEC during 2022, as well as in its subsequent filings with the SEC. Motorsport Games anticipates that subsequent events and developments may cause its plans, intentions and expectations to change. Motorsport Games assumes no obligation, and it specifically disclaims any intention or obligation, to update any forward-looking statements, whether as a result of new information, future events or otherwise, except as expressly required by law. Forward-looking statements speak only as of the date they are made and should not be relied upon as representing Motorsport Games’ plans and expectations as of any subsequent date. Additionally, the business and financial materials and any other statement or disclosure on, or made available through, Motorsport Games’ website or other websites referenced or linked to this press release shall not be incorporated by reference into this press release.

Website and Social Media Disclosure:

Investors and others should note that we announce material financial information to our investors using our investor relations website (ir.motorsportgames.com), SEC filings, press releases, public conference calls and webcasts. We use these channels, as well as social media and blogs, to communicate with our investors and the public about our company and our products. It is possible that the information we post on our websites, social media and blogs could be deemed to be material information. Therefore, we encourage investors, the media and others interested in our company to review the information we post on the websites, social media channels and blogs, including the following (which list we will update from time to time on our investor relations website):

Cumulus Media (NASDAQ: CMLS) is an audio-first media company delivering premium content to over a quarter billion people every month — wherever and whenever they want it. Cumulus Media engages listeners with high-quality local programming through 406 owned-and-operated radio stations across 86 markets; delivers nationally-syndicated sports, news, talk, and entertainment programming from iconic brands including the NFL, the NCAA, the Masters, CNN, the AP, the Academy of Country Music Awards, and many other world-class partners across more than 9,500 affiliated stations through Westwood One, the largest audio network in America; and inspires listeners through the Cumulus Podcast Network, its rapidly growing network of original podcasts that are smart, entertaining and thought-provoking. Cumulus Media provides advertisers with personal connections, local impact and national reach through broadcast and on-demand digital, mobile, social, and voice-activated platforms, as well as integrated digital marketing services, powerful influencers, full-service audio solutions, industry-leading research and insights, and live event experiences. Cumulus Media is the only audio media company to provide marketers with local and national advertising performance guarantees. For more information visit www.cumulusmedia.com.

Michael Kupinski, Director of Research, Noble Capital Markets, Inc.

Jacob Mutchler, Research Associate, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

Tough comps ahead. The conventional investment scenario is to expect a weak first half of 2023 and a stronger second half. However, we believe the absence of high margin political advertising and the dissolution of the WynnBet partnership calls for a more conservative outlook for 2023. In our view, there are troubling near term signs for the company that have led us to take a more sober outlook for 2023.

Economic headwinds and National advertising. Weakness in National advertising continues to be prevalent as macroeconomic headwinds persist. Additionally, we believe Local advertising is starting to show weakness.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

Engine Gaming and Media, Inc. (NASDAQ:GAME) (TSX-V:GAME) provides premium social sports and esports gaming experiences, as well as unparalleled data analytics, marketing, advertising, and intellectual property to support its owned and operated direct-to-consumer properties, while also providing these services to enable its clients and partners. The company’s subsidiaries include Stream Hatchet, the global leader in gaming video distribution analytics; Sideqik, a social influencer marketing discovery, analytics, and activation platform; WinView Games, a social predictive play-along gaming platform for viewers to play while watching live events; and Frankly Media, a digital publishing platform used to create, distribute and monetize content across all digital channels. Engine Media generates revenue through a combination of direct-to-consumer fees, streaming technology and data SaaS-based offerings, and programmatic advertising. For more information, please visit www.enginegaming.com.

Michael Kupinski, Director of Research, Noble Capital Markets, Inc.

Patrick McCann, Research Associate, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

Q1 results. The company reported revenue of $10.3 million, which beat our estimate of $9.8 million by 5%. Revenue was better than expected despite a decrease in advertising revenue due to changes in the algorithms that drive audience traffic. Adj. EBITDA for the quarter was a loss of $2.7 million, in line with our estimate.

Favorable influencer analytics trends. Management noted that there is heightened demand for influencer marketing. Notably. influencer and gaming analytics software as a service (SaaS) revenue grew by 34.6% on a year over year basis, helping to offset a decline in advertising revenues.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

NEW YORK, NY / ACCESSWIRE / January 17, 2023 / Engine Gaming and Media, Inc. (“Engine” or the “Company”) (NASDAQ:GAME)(TSXV:GAME), a data-driven, gaming, media and influencer marketing platform company, today announced results for its fiscal first quarter 2023 ended November 30, 2022. All amounts are stated in U.S. dollars unless otherwise indicated.

Financial Highlights:

The Company announced the successful completion of its strategic process resulting in the signed merger agreement with GameSquare Esports, Inc

For the fiscal first quarter 2023 net loss improved significantly to $5.4 million, compared to $15.2 million in the fiscal fourth quarter 2022, an improvement of 65%

Significant improvement in Adjusted EBITDA of 32% to $(2.7) million in the first fiscal quarter 2023 sequentially compared to an Adjusted EBITDA of $(4.0) million in the fiscal fourth quarter 2022

The Company’s Influencer and Data Technology SaaS revenues increased 35% during the first fiscal quarter of 2023 compared to the first fiscal quarter of 2022

Management Commentary

“We are proud of the continued improvement we have made towards our near-term goal of achieving cash-flow breakeven. This quarter is highlighted by a 65% improvement in net loss of nearly $10 million and a 32% improvement in Adjusted EBITDA on a sequential basis to $(2.7) million, despite the restructuring charges related to discontinued operations said Lou Schwartz, Chief Executive Officer of Engine. “Despite some expected short-term headwinds in the advertising market, driven by Google algorithm changes, we continue to see heightened demand for our influencer and data technology SaaS services by our gaming and brand clients, which grew 35% YoY. We see this as a welcoming trend heading into our merger with GameSquare.”

Tom Rogers, Executive Chairman of the Company, commented on the recently announced merger with GameSquare, adding, “Our strengths speak to the heart of the thesis behind the GameSquare transaction. GameSquare brings content development, a publisher advertising network, and a gaming influencer network, which is complementary to our gaming content analytics technology, our programmatic advertising technology, and our influencer marketing and management technology. When the two companies’ assets are combined, these elements create an end-to-end solution for brands to reach their target audience. Moreover, the combined companies offering provides a highly scaled answer to reach younger demographics at a level sought by brands, which traditional media can no longer perform. In addition, digital advertising continues to be constrained by new privacy protection steps of the major tech players, which has inhibited efficient targeting of certain audiences particularly gaming audiences. Traditional media’s failings and digital advertising limitations create the setting for why the combined company provides a solution to both problems that is both differentiated and scalable.”

Fiscal First Quarter 2023 Financial Results

Total revenue in the fiscal first quarter of 2023 was $10.3 million, compared to revenue of $11.5 million in the fiscal fourth quarter of 2022. Overall Software-as-a-Service (SaaS) revenues were relatively flat due to the declines in legacy content management related SaaS revenues. However, gaming and influencer data and analytics SaaS revenues grew 34.6% YoY. The decrease in advertising revenues was primarily due to changes in Google discovery and algorithms which impacted audience traffic that is expected to gradually improve throughout the fiscal second quarter and fiscal third quarter of 2023.

Expenses in the fiscal first quarter were $15.8 million, an improvement of approximately $6.0 million, when compared to $21.8 million on a sequential basis.

Net Loss in the fiscal first quarter improved 64.7% to $5.4 million, compared to a net loss of $15.2 million in the fiscal fourth quarter of 2022 inclusive of the restructuring charges related to discontinued operations.

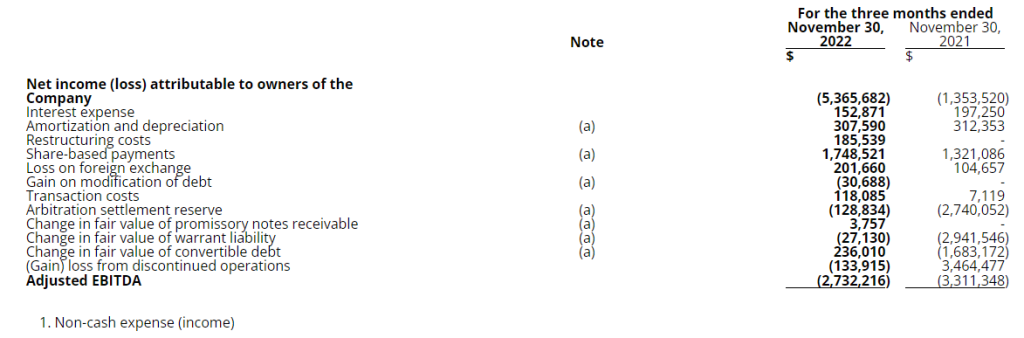

Adjusted EBITDA was $(2.7) million for the fiscal first quarter, an improvement of 32.5% when compared to $(4.0) million in the fiscal fourth quarter of 2022, and when compared to the same year-ago quarter Adjusted EBITDA improved 17.5%.

At November 30, 2022, the Company had cash of $6.9 million.

Recent Operational Highlights:

Successful completion of Strategic Process resulting in signed merger with GameSquare.

Stream Hatchet new and expanded client highlights for the quarter include XSET, Benefit Cosmetics, a16z, Immortal, Tencent and Epic.

Sideqik new and expanded client highlights for the quarter include PDP Gaming, AverMedia, Misfits Gaming and ASUS.

Frankly new and expanded client highlights for the quarter include Citadel Communications, Krol Communications, Beyond TV, Sports News Highlights, Palmetto Network, and BmovieNation.

FY Q1 2023 Earnings Conference Call

Management will host an investor conference call at 8:45 a.m. EDT (5:45 a.m. PDT) today, Tuesday, January 17, 2023, to discuss Engine Gaming and Media, Inc.’s fiscal first quarter 2023 financial results, provide a corporate update, and conclude with a Q&A from participants. To participate, please use the following information:

Please dial in at least 10 minutes before the start of the call to ensure timely participation.

Non-IFRS Measures

The Company reports earnings before interest, taxes, depreciation and amortization (“EBITDA”) and Adjusted EBITDA, which are not financial measures calculated and presented in accordance with International Financial Reporting Standards (“IFRS”) and therefore may not be comparable to similar measures presented by other issuers. EBITDA and Adjusted EBITDA should not be considered in isolation or as a substitute to net income (loss) or any other financial measures of performance or liquidity calculated and presented in accordance with IFRS. The Company defines Adjusted EBITDA as EBITDA, adjusted to exclude certain non-cash charges and other items that we do not believe are reflective of our ongoing operating results. The Company utilizes Adjusted EBITDA internally for purposes of forecasting, determining compensation, and assessing the performance of our business, therefore, we believe this measure provides useful supplemental information that may assist investors in assessing an investment in the Company.

The following unaudited table presents the reconciliation of net loss to Adjusted EBITDA for the three months ended November 30, 2022, and 2021, respectively.

About Engine Gaming and Media, Inc.

Engine Gaming and Media, Inc. (NASDAQ:GAME)(TSXV:GAME) provides unparalleled live streaming data and social analytics, influencer relationship management and monetization, and programmatic advertising to support the world’s largest video gaming companies, brand marketers, ecommerce companies, media publishers and agencies to drive new streams of revenue. The company’s subsidiaries include Stream Hatchet, the global leader in gaming video distribution analytics; Sideqik, a social influencer marketing discovery, analytics, and activation platform; and Frankly Media, a digital publishing platform used to create, distribute, and monetize content across all digital channels. Engine generates revenue through a combination of software-as-a-service subscription fees, managed services, and programmatic advertising. For more information, please visit www.enginegaming.com.

Cautionary Statement on Forward-Looking Information

This news release contains forward-looking statements. Forward-looking statements involve known and unknown risks, uncertainties and other factors which may cause the actual results, performance or achievements of Engine to be materially different from any future results, performance or achievements expressed or implied by the forward-looking statements. Often, but not always, forward-looking statements can be identified by the use of words such as “plans”, “expects” or “does not expect”, “is expected”, “estimates”, “intends”, “anticipates” or “does not anticipate”, or “believes”, or variations of such words and phrases or state that certain actions, events or results “may”, “could”, “would”, “might” or “will” be taken, occur or be achieved. In respect of the forward-looking information contained herein, Engine has provided such statements and information in reliance on certain assumptions that management believed to be reasonable at the time. Forward-looking information involves known and unknown risks, uncertainties and other factors which may cause the actual results, performance or achievements stated herein to be materially different from any future results, performance or achievements expressed or implied by the forward-looking information. Actual results could differ materially from those currently anticipated due to a number of factors and risks. Accordingly, readers should not place undue reliance on forward-looking information contained in this news release.

The forward-looking statements contained in this news release are made as of the date of this release and, accordingly, are subject to change after such date. Engine does not assume any obligation to update or revise any forward-looking statements, whether written or oral, that may be made from time to time by us or on our behalf, except as required by applicable law.

Neither the TSX Venture Exchange nor its Regulation Services Provider (as that term is defined in policies of the TSX Venture Exchange) accepts responsibility for the adequacy or accuracy of this release.

Company Contact:

Lou Schwartz 647-725-7765

Investor Relations Contact:

Shannon Devine Z North America Main: 203-741-8811 GAME@mzgroup.us

With more than 60 units, RCI Hospitality Holdings, Inc., through its subsidiaries, is the country’s leading company in adult nightclubs and sports bars/restaurants. Clubs in New York City, Chicago, Dallas-Fort Worth, Houston, Miami, Minneapolis, Denver, St. Louis, Charlotte, Pittsburgh, Raleigh, Louisville, and other markets operate under brand names such as Rick’s Cabaret, XTC, Club Onyx, Vivid Cabaret, Jaguars Club, Tootsie’s Cabaret, Scarlett’s Cabaret, Diamond Cabaret, and PT’s Showclub. Sports bars/restaurants operate under the brand name Bombshells Restaurant & Bar.

Joe Gomes, Senior Research Analyst, Noble Capital Markets, Inc.

Joshua Zoepfel, Research Associate, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

1Q23 Preliminary Revenues. RCI reported preliminary 1Q23 revenue for the Nightclubs and Bombshells. Total revenues of $69.2 million were up 13.3% year-over-year. Y-o-Y SSS were off 2.7%, but were up 8.6% compared to 1Q20, or prior to any COVID related impacts.

Nightclubs. Revenue of $55.9 million was up 20.7% y-o-y, with SSS up 1.2% y-o-y and up 10.0% from 1Q20. Nightclub sales remained high, reflecting strong contributions from acquisitions, increased VIP spend at many of the northern clubs, and reopened/reformatted clubs, all of which more than offset intermittent softness at some blue collar clubs compared to a year-ago.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

Entravision Communications Corporation is a diversified Spanish-language media company utilizing a combination of television and radio operations to reach Hispanic consumers across the United States, as well as the border markets of Mexico. Entravision owns and/or operates 53 primary television stations and is the largest affiliate group of both the top-ranked Univision television network and Univision’s TeleFutura network, with television stations in 20 of the nation’s top 50 Hispanic markets. The Company also operates one of the nation’s largest groups of primarily Spanish-language radio stations, consisting of 48 owned and operated radio stations.

Michael Kupinski, Director of Research, Noble Capital Markets, Inc.

Patrick McCann, Research Associate, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

Founder & CEO, Walter Ulloa passes. The company announced that founding CEO and Chairman of the Board of Directors, Walter Ulloa, died on December 31, 2022, of a sudden heart attack. The board appointed CFO Chris Young as interim CEO while it begins its search for a new CEO.

Legacy of dynamic leadership. Mr. Ulloa served as chairman and CEO since cofounding the company in 1996. He led the company’s expansion as a Spanish language broadcaster and oversaw its more recent transition to a digital media company with a global presence.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

With more than 60 units, RCI Hospitality Holdings, Inc., through its subsidiaries, is the country’s leading company in adult nightclubs and sports bars/restaurants. Clubs in New York City, Chicago, Dallas-Fort Worth, Houston, Miami, Minneapolis, Denver, St. Louis, Charlotte, Pittsburgh, Raleigh, Louisville, and other markets operate under brand names such as Rick’s Cabaret, XTC, Club Onyx, Vivid Cabaret, Jaguars Club, Tootsie’s Cabaret, Scarlett’s Cabaret, Diamond Cabaret, and PT’s Showclub. Sports bars/restaurants operate under the brand name Bombshells Restaurant & Bar.

Joe Gomes, Senior Research Analyst, Noble Capital Markets, Inc.

Joshua Zoepfel, Research Associate, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

4Q22 Operating Results. RCI recorded revenue of $71.4 million for 4Q22, up 29.9% y-o-y. Adjusted EBITDA in the quarter was $24.2 million, up 37.8% y-o-y and net income rose 361.4% to $10.6 million. EPS was $1.15 and adjusted EPS was $1.45, down 8.2% y-o-y due to a much higher tax rate this year. We had forecast revenue of $68.5 million, adjusted EBITDA of $21 million, and EPS of $1.27.

Segments. Acquisitions drove Nightclubs top line up 40.4% to $56.6 million in the quarter, SSS were up 3.2%. Non-GAAP operating margin was 41.6%, driven by a 53.6% increase in high margin service revenue. Bombshells revenues of $14 million were down slightly from $14.4 million a year ago, SSS were off 13.3%. Operating margin was 18%, ex one time start up costs for the San Antonio location.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

The E.W. Scripps Company (NASDAQ: SSP) is a diversified media company focused on creating a better-informed world. As one of the nation’s largest local TV broadcasters, Scripps serves communities with quality, objective local journalism and operates a portfolio of 61 stations in 41 markets. The Scripps Networks reach nearly every American through the national news outlets Court TV and Newsy and popular entertainment brands ION, Bounce, Defy TV, Grit, ION Mystery, Laff and TrueReal. Scripps is the nation’s largest holder of broadcast spectrum. Scripps runs an award-winning investigative reporting newsroom in Washington, D.C., and is the longtime steward of the Scripps National Spelling Bee. Founded in 1878, Scripps has held for decades to the motto, “Give light and the people will find their own way.”

Michael Kupinski, Director of Research, Noble Capital Markets, Inc.

Jacob Mutchler, Research Associate, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

Launches new sports division. Management believes that sports broadcasting is the most valuable asset in the linear TV market and will be implementing a two prong approach for its national and local strategy. The company believes it can provide a unique value proposition for both a local/regional and a national strategy.

Serves a growing viewership gap. Due to cable cord cutting, the Regional Sports Networks have seen a significant decline in viewership. In many cities, 40% to 50% of the households are not watching cable or satellite. The company’s local strategy will focus on markets where it currently operates two or more stations, furthering its reach in those markets. Management highlighted Phoenix and Detroit as two markets it would be interested in for local sports rights.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

With more than 60 units, RCI Hospitality Holdings, Inc., through its subsidiaries, is the country’s leading company in adult nightclubs and sports bars/restaurants. Clubs in New York City, Chicago, Dallas-Fort Worth, Houston, Miami, Minneapolis, Denver, St. Louis, Charlotte, Pittsburgh, Raleigh, Louisville, and other markets operate under brand names such as Rick’s Cabaret, XTC, Club Onyx, Vivid Cabaret, Jaguars Club, Tootsie’s Cabaret, Scarlett’s Cabaret, Diamond Cabaret, and PT’s Showclub. Sports bars/restaurants operate under the brand name Bombshells Restaurant & Bar.

Joe Gomes, Senior Research Analyst, Noble Capital Markets, Inc.

Joshua Zoepfel, Research Associate, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

Acquisitions. Yesterday, RCI Hospitality announced an agreement to acquire five gentlemen’s clubs, two Baby Dolls, one in Dallas and one in Forth Worth, and three Chicas Locas, one each in Arlington, Dallas, and Houston. The proposed acquisition is the second largest in RCI’s history and one of the largest in the nightclub industry.

Details. RCI is paying $66.5 million for the clubs and associated real estate. The $66.5 million breaks out to $25 million in cash, $25.5 million of 10-year 7% seller notes, and 200,000 restricted shares of stock based on a per share price of $80. The clubs are expected to contribute approximately $11 million of EBITDA in year one, growing to $14-$16 million annually once remodeling and expansion projects are complete.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

Motorsport Games, a Motorsport Network company, combines innovative and engaging video games with exciting esports competitions and content for racing fans and gamers around the globe. The Company is the officially licensed video game developer and publisher for iconic motorsport racing series across PC, PlayStation, Xbox, Nintendo Switch and mobile, including NASCAR, INDYCAR, 24 Hours of Le Mans and the British Touring Car Championship (“BTCC”). Motorsport Games is an award-winning esports partner of choice for 24 Hours of Le Mans, Formula E, BTCC, the FIA World Rallycross Championship and the eNASCAR Heat Pro League, among others.

Michael Kupinski, Director of Research, Noble Capital Markets, Inc.

Patrick McCann, Research Associate, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

Equity purchase agreement. On December 9th 2022, the company entered into an equity purchase agreement with Alumni Capital. The equity purchase agreement alleviates the immediate liquidity concerns and allows the company to continue the development and production of its unique product line well into 2023. Additionally, we believe the agreement has the potential to provide sufficient levels of capital until the company generates positive cash flow in the second half of 2023.

Terms of the agreement. At this time the arrangement stipulates that the company has the right to sell Alumni Capital no more than $2 million in common stock. The company has the option to increase the initial purchase amount to $10 million any time prior to December 31st, 2023. If there is an increase in the initial purchase amount, 2% of the increase will be issued to Alumni Capital as consideration shares, and the company will not receive any proceeds for the issuance of commitment shares. The company will pay the expenses for registration of the shares including legal and accounting.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

Lee Enterprises, Incorporated provides local news, information, and advertising primarily in midsize markets in the United States. It publishes 49 daily newspapers, as well as offers 300 weekly newspapers and specialty publications in 23 states. The company also provides online advertising and services; and online infrastructure and online publishing services for approximately 1,500 daily and weekly newspapers and shoppers. In addition, it offers commercial printing services. The company has a strategic alliance with Yahoo!, Inc. to provide its classified employment advertising customer base the opportunity to post job listings and other employment products on Yahoo!�s HotJobs national platform. Lee Enterprises, Incorporated was founded in 1890 and is based in Davenport, Iowa.

Michael Kupinski, Director of Research, Noble Capital Markets, Inc.

Patrick McCann, Research Associate, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

Solid Q4 results. The company reported strong Q4 revenue of $193.6 million, topping our forecast of $191.2 million. Adj. EBITDA was also favorable at $30.1 million, compared with our estimate of $29.5 million. Figure #1 Q4 Variance illustrates the favorable quarterly performance.

Digital growth accelerates. In spite of an 11% decline in Print revenue, total revenue was flat in the quarter, due to accelerating Digital revenue. Digital revenue grew 33% over the prior year period and accounted for 31% of total company revenue. Digital revenue growth was led by Amplified, the company’s Digital Media Solutions business, which grew 83% over the prior year period.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.