In the realm of economic indicators, few metrics capture the pulse of consumer sentiment and economic vitality quite like new home sales. The recent surge in new home sales in the United States, hitting a six-month high in March, is a beacon of hope amidst a backdrop of economic uncertainties. This uptick not only signifies resilience in the housing sector but also holds implications for small-cap investors and the broader macroeconomic landscape.

The Commerce Department’s latest report delivered a bullish narrative, showcasing an impressive 8.8% increase in new home sales, with a seasonally adjusted annual rate soaring to 693,000 units. This surge, attributed partly to the persistent shortage of previously owned homes on the market, underscores the robust demand for housing despite challenges such as escalating mortgage rates.

For small-cap investors, this uptick in new home sales is more than just a statistical blip—it’s a promising indicator of consumer confidence and economic buoyancy. Strong housing demand typically translates into a flurry of economic activity, benefiting small-cap companies operating in sectors ranging from home construction and building materials to home improvement and real estate services.

However, amid the celebratory numbers lies a cautionary tale. The accompanying rise in the median house price, coupled with the upward trajectory of mortgage rates, paints a nuanced picture. While higher home prices can fuel revenues for homebuilders and related industries, concerns about affordability may cast a shadow on overall housing market growth, impacting small caps tethered to this sector.

Zooming out to the macroeconomic panorama, the implications of these housing market dynamics are far-reaching. A robust housing sector is not just about building and selling homes; it’s a linchpin of economic stability, contributing significantly to GDP growth, job creation, and wealth accumulation.

Economists and savvy investors are keeping a keen eye on how these developments unfold in the coming months. The recent uptick in mortgage rates, coupled with a slight dip in mortgage applications, hints at potential headwinds for new home sales. This cautious sentiment underscores the delicate dance between market exuberance and economic prudence.

Regional nuances in new home sales add depth to the narrative. While all four U.S. regions experienced increases in new home sales, sentiments among single-family homebuilders remain cautious. Buyers, in turn, are treading carefully, weighing the impact of rising interest rates on their purchasing power.

For small-cap aficionados navigating this dynamic terrain, a balanced approach is the name of the game. While opportunities may abound in sectors riding the housing market wave, strategic risk management and diversified portfolios are non-negotiables in today’s evolving economic landscape.

In summary, the resurgence in new home sales injects a dose of optimism into the market narrative. However, prudence tempered with opportunism will be the guiding ethos for investors eyeing the small-cap space amid shifting economic tides.

Mortgage rates have climbed over the past year, hovering around 7% for a 30-year fixed rate mortgage. This is significantly higher than the 3% rates seen during the pandemic in 2021. Rates are being pushed higher by several key factors.

Inflation has been the main driver of increased borrowing costs. The consumer price index rose 7.5% in January 2024 compared to a year earlier. While this was down slightly from December, inflation remains stubbornly high. The Federal Reserve has been aggressively raising interest rates to combat inflation. This has directly led to higher mortgage rates.

As the Fed Funds rate has climbed from near zero to around 5%, mortgage rates have followed. Additional Fed rate hikes are expected this year as well, keeping upward pressure on mortgage rates. Though inflation eased slightly in January, it remains well above the Fed’s 2% target. The central bank has signaled they will maintain restrictive monetary policy until inflation is under control. This means mortgage rates are expected to remain elevated in the near term.

Another factor pushing rates higher is the winding down of the Fed’s bond buying program, known as quantitative easing. For the past two years, the Fed purchased Treasury bonds and mortgage-backed securities on a monthly basis. This helped keep rates low by increasing demand. With these purchases stopped, upward pressure builds on rates.

The yield on the 10-year Treasury note also influences mortgage rates. As this yield has climbed from 1.5% to around 4% over the past year, mortgage rates have moved higher as well. Investors demand greater returns on long-term bonds as inflation eats away at fixed income. This in turn pushes mortgage rates higher.

With mortgage rates elevated, the housing market is feeling the effects. Home sales have slowed significantly as higher rates reduce buyer affordability. Prices are also starting to moderate after rapid gains the past two years. Housing inventory is rising while buyer demand falls. This should bring more balance to the housing market after it overheated during the pandemic.

For potential homebuyers, elevated rates make purchasing more expensive. Compared to 3% rates last year, the monthly mortgage payment on a median priced home is around 60% higher at current 7% rates. This prices out many buyers, especially first-time homebuyers. Households looking to move up in home size also face much higher financing costs.

Those able to buy may shift to adjustable rate mortgages (ARMs) to get lower initial rates. But ARMs carry risk as rates can rise substantially after the fixed period. Lower priced homes and smaller mortgages are in greater demand. Refinancing has also dropped off sharply as existing homeowners already locked in historically low rates.

There is hope that mortgage rates could decline later this year if inflation continues easing. However, most experts expect rates to remain above 6% at least through 2024 until inflation is clearly curtailed. This will require the Fed to maintain their aggressive stance. For those able to buy at current rates, refinancing in the future is likely if rates fall. But higher rates look to be the reality for 2024.

The US housing market continues to show signs of a significant downturn, with existing home sales in September dropping to the slowest pace since October 2010. This marks a 15.4% decline compared to September 2022, according to new data from the National Association of Realtors (NAR).

The sharp drop in home sales highlights how rising mortgage rates and declining affordability are severely impacting the housing market. The average 30-year fixed mortgage rate now sits around 8%, more than double what it was just a year ago. This rapid surge in borrowing costs has priced many buyers out of the market, especially first-time homebuyers.

Only 27% of September home sales went to first-time buyers, well below the historical norm of 40%. Many simply cannot afford today’s high home prices and mortgage payments. As a result, sales activity has fallen dramatically. The current sales pace of 3.96 million units annualized is down markedly from over 6 million just two years ago, when rates were around 3%.

At the same time, inventory remains extremely tight. There were just 1.13 million existing homes available for sale at the end of September, an over 8% decline from last year. This persistent shortage of homes for sale continues to put upward pressure on prices. The median sales price in September hit $394,300, up 2.8% from a year ago.

While higher prices are squeezing buyers, they are not denting demand enough to significantly expand inventory. Many current homeowners are reluctant to sell and give up their ultra-low mortgage rates. This dynamic is keeping the market undersupplied, even as sales cool.

Not all buyers are impacted equally by higher rates. Sales have held up better on the upper end of the market, while declining sharply for mid-priced and affordable homes. This divergence reflects that high-end buyers often have more financial flexibility, including the ability to purchase in cash.

All-cash sales represented 29% of transactions in September, up notably from 22% a year earlier. Wealthier buyers with financial assets can better absorb higher borrowing costs. In contrast, first-time buyers and middle-income Americans are being squeezed the most by rate hikes.

Looking ahead, the housing slowdown is likely to persist and potentially worsen. Mortgage applications are now at their lowest level since 1995, signaling very weak demand ahead. And while inflation has eased slightly, the Federal Reserve is still expected to continue raising interest rates further to combat it.

Higher rates mean reduced affordability and housing activity, especially if home prices remain elevated due to limited inventory. This perfect storm in the housing market points to significant headwinds for the broader economy going forward.

The housing sector has historically been a key driver of economic growth in the US. But with sales and construction activity slowing substantially, it may act as a drag on GDP growth in coming quarters. Combined with declining affordability, fewer homes being purchased also means less spending on furniture, renovations, and other housing-related items.

Some analysts believe the Fed’s aggressive rate hikes will ultimately tip the economy into a recession. The depth of the housing market downturn so far this year does not bode well from a macroeconomic perspective. It signals households are pulling back materially on major purchases, which could contribute to a broader economic contraction.

While no significant recovery is expected in the near-term, lower demand could eventually help rebalance the market. As sales moderate, competitive bidding may ease, taking some pressure off prices. And if economic conditions worsen substantially, the Fed may again reverse course on interest rates. But for now, the housing sector appears poised for more weakness ahead. Homebuyers and investors should brace for ongoing volatility and uncertainty.

Consumer inflation accelerated more than expected in September due largely to intensifying shelter costs, putting further pressure on household budgets and keeping the Federal Reserve on high alert.

The consumer price index (CPI) increased 0.4% last month after rising 0.1% in August, the Labor Department reported Thursday. On an annual basis, prices were up 3.7% through September.

Both the monthly and yearly inflation rates exceeded economist forecasts of 0.3% and 3.6% respectively.

The higher than anticipated inflation extends the squeeze on consumers in the form of elevated prices for essentials like food, housing, and transportation. It also keeps the Fed under the microscope as officials debate further interest rate hikes to cool demand and restrain prices.

The main driver behind the inflation uptick in September was shelter costs. The shelter index, which includes rent and owners’ equivalent rent, jumped 0.6% for the month. Shelter costs also posted the largest yearly gain at 7.2%.

On a monthly basis, shelter accounted for over half of the total increase in CPI. Surging rents and housing costs reflect pandemic trends like strong demand amid limited supply.

“Just because the rate of inflation is stable for now doesn’t mean its weight isn’t increasing every month on family budgets,” noted Robert Frick, corporate economist at Navy Federal Credit Union. “That shelter and food costs rose particularly is especially painful.”

Energy and Food Costs Also Climb

While shelter led the inflation surge, other categories saw notable increases as well in September. Energy costs rose 1.5% led by gasoline, fuel oil, and natural gas. Food prices gained 0.2% for the third consecutive month, with a 6% jump in food away from home.

On an annual basis, energy costs were down 0.5% but food was up 3.7% year-over-year through September.

Used vehicle prices declined 2.5% in September but new vehicle costs rose 0.3%. Overall, transportation services inflation eased to 0.9% annually in September from 9.5% in August.

Wage Growth Lags Inflation

Rising consumer costs continue to outpace income growth, squeezing household budgets. Average hourly earnings rose just 0.2% in September, not enough to keep pace with the 0.4% inflation rate.

That caused real average hourly earnings to fall 0.2% last month. On a yearly basis, real wages were up only 0.5% through September—a fraction of the 3.7% inflation rate over that period.

American consumers have relied more heavily on savings and credit to maintain spending amid high inflation. But rising borrowing costs could limit their ability to sustain that trend.

Fed Still Focused on Inflation Fight

The hotter-than-expected CPI print keeps the Fed anchored on inflation worries. Though annual inflation has eased from over 9% in June, the 3.7% rate remains well above the Fed’s 2% target.

Officials raised interest rates by 75 basis points in both September and November, pushing the federal funds rate to a range of 3-3.25%. Markets expect another 50-75 basis point hike in December.

Treasury yields surged following the CPI report, reflecting ongoing inflation concerns. Persistently high shelter and food inflation could spur the Fed to stick to its aggressive rate hike path into 2023.

Taming inflation remains the Fed’s number one priority, even at the risk of slowing economic growth. The latest CPI data shows they still have work to do on that front.

All eyes will now turn to the October and November inflation reports heading into the pivotal December policy meeting. Further hotter-than-expected readings could force the Fed’s hand on more supersized rate hikes aimed at cooling demand and prices across the economy.

Mortgage rates crossed the 7% threshold this past week, as the 30-year fixed rate hit 7.31% according to Freddie Mac data. This marks the highest level for mortgage rates since late 2000.

The implications extend far beyond the housing market alone. The sharp rise in rates stands to impact the stock market, economic growth, and investor sentiment through various channels.

For stock investors, higher mortgage rates pose risks of slower economic growth and falling profits for rate-sensitive sectors. Housing is a major component of GDP, so a pullback in home sales and construction activity would diminish economic output.

Slower home sales also mean less revenue for homebuilders, real estate brokers, mortgage lenders, and home furnishing retailers. With housing accounting for 15-18% of economic activity, associated industries make up a sizable chunk of the stock market.

A housing slowdown would likely hit sectors such as homebuilders, building materials, home improvement retailers, and home furnishing companies the hardest. Financial stocks could also face challenges as mortgage origination and refinancing drop off.

Broader economic weakness resulting from reduced consumer spending power would likely spillover to impact earnings across a wide swath of companies and market sectors. Investors may rotate to more defensive stocks if growth concerns escalate.

Higher rates also signal tightening financial conditions, which historically leads to increased stock market volatility and investor unease. Between inflation cutting into incomes and higher debt servicing costs, consumers have less discretionary income to sustain spending.

Reduced consumer spending has a knock-on effect of slowing economic growth. If rate hikes intended to fight inflation go too far, it raises the specter of an economic contraction or recession down the line.

For bond investors, rising rates eat into prices of existing fixed income securities. Bonds become less attractive compared to newly issued debt paying higher yields. Investors may need to explore options like floating rate bonds and shorter duration to mitigate rate impacts.

Rate-sensitive assets that did well in recent years as rates fell may come under pressure. Real estate, utilities, long-duration bonds, and growth stocks with high valuations are more negatively affected by rising rate environments.

Meanwhile, cash becomes comparatively more attractive as yields on savings accounts and money market funds tick higher. Investors may turn to cash while awaiting clarity on inflation and rates.

The Fed has emphasized its commitment to bringing inflation down even as growth takes a hit. That points to further rate hikes ahead, meaning mortgage rates likely have room to climb higher still.

Whether the Fed can orchestrate a soft landing remains to be seen. But until rate hikes moderate, investors should brace for market volatility and economic uncertainty.

Rising mortgage rates provide yet another reason for investors to ensure their portfolios are properly diversified. Maintaining some allocation to defensive stocks and income plays can help smooth out risk during periods of higher volatility.

While outlooks call for slower growth, staying invested with a long-term perspective is typically better than market timing. Patience and prudent risk management will be virtues for investors in navigating markets in the year ahead.

A perfect storm is brewing in the US housing market. Mortgage rates have surged above 7% just as millennials, the largest generation, reach peak homebuying age. This collision of rising interest rates and unmet demand is causing substantial disruption, as seen in the sharp decline in home sales, cautious builders and a looming affordability crisis that threatens the broader economy.

Mortgage rates have taken off as the Federal Reserve aggressively raises interest rates to fight inflation. The average 30-year fixed rate recently hit 7.18%, according to Freddie Mac, the highest level since 2001. This has severely hampered housing affordability and demand. Fannie Mae, the mortgage finance giant, forecasts total home sales will drop to 4.8 million this year, the slowest pace since 2011 when the housing market was still recovering from the Great Recession.

Fannie Mae expects sales to struggle through 2024 as rates remain elevated. It predicts the US economy will enter a recession in early 2024, further dragging down the housing market. Home prices are also likely to drop as high rates impede sales. This could hurt consumer confidence and discretionary spending, considering the critical role housing plays in household wealth.

Higher rates have pumped up monthly mortgage payments and made homes less affordable. Take a $500,000 home purchased with a 20% down payment. At a 2.86% mortgage rate two years ago, the monthly payment would have been $1,656. With rates now at 7.18%, that same home has a monthly cost of $3,077, according to calculations by Axios. That 87% payment surge makes purchasing unattainable for many buyers.

These affordability challenges are hitting just as millennials reach peak homebuying age. The largest cohorts of this generation were born in the late 1980s and early 1990s, making them between 32 and 34 years old today. That’s when marriage, childbearing and demand for living space typically accelerate.

However, homebuilders have been reluctant to significantly ramp up construction with rates so high. Housing starts experienced a significant decline of 11.3% in August, according to Census Bureau data, driven by a decline in apartment buildings. Single-family starts dipped 4.3% to an annual pace of 941,000, 16% below the average from mid-2020 to mid-2022. Homebuilder sentiment has also plunged, according to the National Association of Home Builders.

This pullback in new construction comes even as there is strong interest from millennials and other buyers. Though mortgage rates moderated the overheated housing market earlier this year, national home prices remain just below their all-time highs, up 13.5% from two years ago, according to the S&P Case-Shiller index.

Some analysts say the only solution is to significantly boost supply. But that seems unlikely with builders cautious and financing costs high. The housing crisis has no quick fix and will continue to be an anchor on the broader economy. Millennials coming of age and mortgage rates spiraling upwards have sparked a perfect storm, broken the housing market, and darkened the country’s economic outlook.

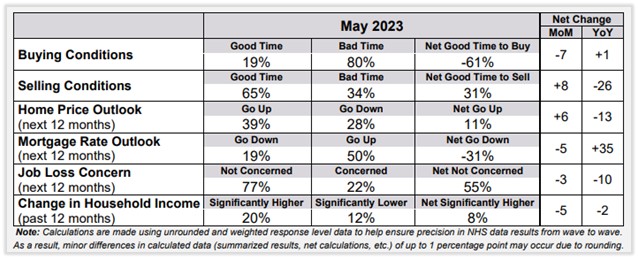

The underlying dynamics of the housing market are not what one might expect. Especially with home prices still near its peak after mortgage rates more than doubled over the past year and a half. One of the unique nuances of today’s housing market is what some are calling the “golden handcuffs” that may apply to anyone who has a home with a mortgage of 3.5% or lower. These owners are slow to sell; this is keeping a supply of homes off the market. The lack of homes for sale is keeping prices up despite the higher cost of borrowing. As witnessed in a monthly survey conducted by Fannie Mae, the attitudes of adults in the U.S., as it relates to buying, or selling, are fairly extreme, with many of the survey responses hit all-time highs and lows in terms of expectations.

Fannie Mae’s National Housing Survey

The National Housing Survey (NHS) is a monthly temperature check of attitudes among the general population related to home-owning, renting, household finances, and confidence in the economy. Each respondent is asked more than 100 questions; this makes the survey far more detailed than other measures of housing attitudes or expectations. Six of the questions are used to derive the Home Purchasing Sentiment Index (HPSI).

The overall economy typically benefits from housing turnover, as new buyers decorate and make a house, or condo, a home.

Below is the noteworthy response data from the six questions Fannie Mae uses for its index.

Home Purchase Sentiment Index (HPSI)

Fannie Mae’s Home Purchase Sentiment Index (HPSI) decreased in May by 1.2 points to 65.6. The HPSI is down 2.6 points compared to the same time last year.

Below are the May statistics on some of the most relevant questions.

Good/Bad Time to Buy:

The percentage of respondents who say it is a good time to buy a home decreased from 23% to 19%, while the percentage who say it is a bad time to buy increased from 77% to 80%. As a result, the net share of those who say it is a good time to buy decreased by 7 percentage points month over month.

Good/Bad Time to Sell:

The percentage of respondents who say it is a good time to sell a home increased from 62% to 65%, while the percentage who say it’s a bad time to sell decreased from 38% to 34%. As a result, the net share of those who say it is a good time to sell increased 8 percentage points month over month.

The percentage of respondents who say home prices will go up in the next 12 months increased from 37% to 39%, while the percentage who say home prices will go down decreased from 32% to 28%. The share who think home prices will stay the same increased from 31% to 33%. As a result, the net share of those who say home prices will go up increased 6 percentage points month over month.

Mortgage Rate Expectations:

The percentage of respondents who say mortgage rates will go down in the next 12 months decreased from 22% to 19%, while the percentage who expect mortgage rates to go up increased from 47% to 50%. The share who think mortgage rates will stay the same remained unchanged at 31%. As a result, the net share of those who say mortgage rates will go down over the next 12 months decreased five percentage points month over month.

Job Loss Concern:

The percentage of respondents who say they are not concerned about losing their job in the next 12 months decreased from 79% to 77%, while the percentage who say they are concerned increased from 21% to 22%. As a result, the net share of those who say they are not concerned about losing their job decreased three percentage points month over month.

Household Income:

The percentage of respondents who say their household income is significantly higher than it was 12 months ago decreased from 24% to 20%, while the percentage who say their household income is significantly lower increased from 11% to 12%. The percentage who say their household income is about the same increased from 64% to 67%. As a result, the net share of those who say their household income is significantly higher than it was 12 months ago decreased five percentage points month over month.

Spring is typically a time when people look to buy homes. With summer less than two weeks away, many who might have purchased a new home opted to wait, or could not find what they were looking for. “As we near the end of the spring homebuying season, the latest HPSI results indicate that affordability hurdles, including high home prices and mortgage rates, remain top of mind for consumers, most of whom continue to tell us that it’s a bad time to buy a home but a good time to sell one,” said Mark Palim, Fannie Mae Vice President and Deputy Chief Economist.

“Consumers also indicated that they don’t expect these affordability constraints to improve in the near future, with significant majorities thinking that both home prices and mortgage rates will either increase or remain the same over the next year. Notably, the same factors impacting affordability may also be affecting the perceived ease of getting a mortgage. This was particularly true among renters: 81% believe it would be difficult to get a mortgage today, matching a survey high,” according to Palim.

Take Away

Consumers don’t expect housing affordability to improve anytime soon. At the same time, and for related reasons, rents have increased. As with most markets, one would expect if the buyers step back, prices might come down in response. An odd dynamic at play now, though, is that many people that are in a home, are staying put because moving might mean saying goodbye to a mortgage rate near 3% and then having to secure one that is nearly five percentage points higher.

Housing Is Getting Less Affordable. Governments Are Making It Worse

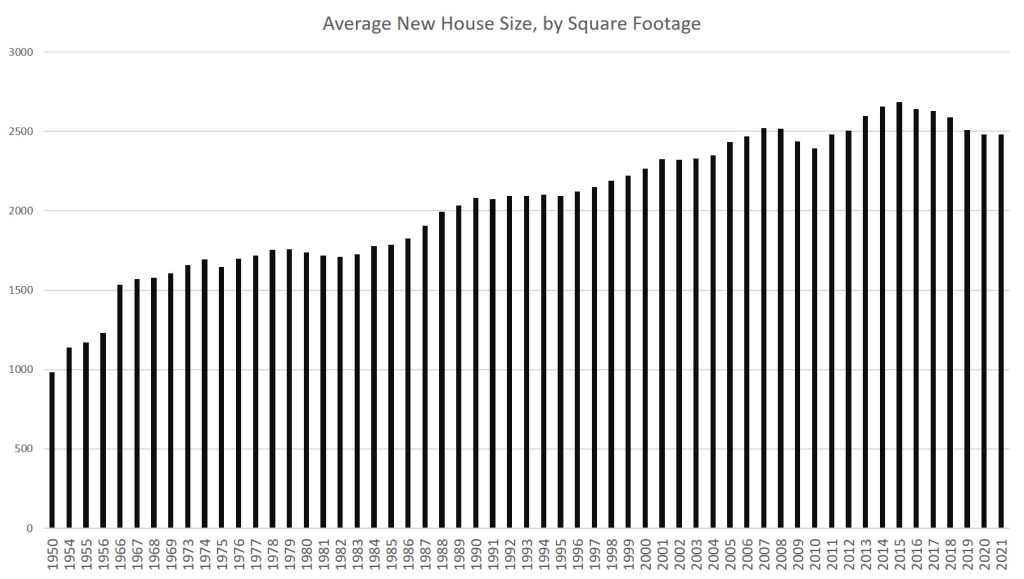

The average square footage in new single-family houses has been declining since 2015. House sizes tend to fall just during recessionary periods. It happened from 2008 to 2009, from 2001 to 2002, and from 1990 to 1991.

But even with strong economic-growth numbers well into 2019, it looks like demand for houses of historically large size may have finally peaked even before the 2020 recession and our current economic malaise. (Square footage in new multifamily construction has also increased.)

According to Census Bureau data, the average size of new houses in 2021 was 2,480 square feet. That’s down 7 percent from the 2015 peak of 2,687.

2015’s average, by the way, was an all-time high and represented decades of near-relentless growth in house sizes in the United States since the Second World War. Indeed, in the 48 years from 1973 to 2015, the average size of new houses increased by 62 percent from 1,660 to 2,687 square feet. At the same time, the quality of housing also increased substantially in everything from insulation, to roofing materials, to windows, and to the size and availability of garages.

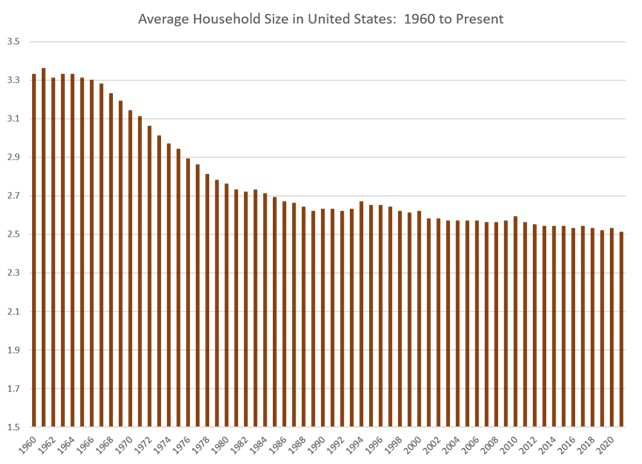

Meanwhile, the size of American households during this period decreased 16 percent from 3.01 to 2.51 people.

Yet, even with that 7 percent decline in house size since 2015, the average new home in America as of 2021 was still well over 50 percent larger than they were in the 1960s. Home size isn’t exactly falling off a cliff. US homes, on a square-foot-per-person basis, remain quite large by historical standards. Since 1973, square footage per person in new houses has nearly doubled, rising from 503 square feet per person in 1973 to 988 square feet person in 2021. By this measure, new house size actually increased from 2020 to 2021.

This continued drive upward in new home size can be attributed in part to the persistence of easy money over the past decade. Even as homes continued to stay big—and thus stay comparatively expensive—it was not difficult to find buyers for them. Continually falling mortgage rates to historical lows below even 3 percent in many cases meant buyers could simply borrow more money to buy big houses.

But we may have finally hit the wall on home size. In recent months we’re finally starting to see evidence of falling home sales and falling home prices. It’s only now, with mortgage rates surging, inflation soaring, and real wages falling—and thus home price affordability falling—that there are now good reasons for builders to think “wow, maybe we need to build some smaller, less costly homes.” There are many reasons to think that they won’t, and that for-purchase homes will simply become less affordable. But it’s not the fault of the builders.

This wouldn’t be a problem in a mostly-free market in which builders could easily adjust their products to meet the market where it’s at. In a flexible and generally free market, builders would flock to build homes at a price level at which a large segment of the population could afford to buy those houses. But that’s not the sort of economy we live in. Rather, real estate and housing development are highly regulated industries at both the federal level and at the local level. Thanks to this, it is becoming more and more difficult for builders to build smaller houses at a time when millions of potential first-time home buyers would gladly snatch them up.

How Government Policy Led to a Codification of Larger, More Expensive Houses

In recent decades, local governments have continued to ratchet up mandates as to how many units can be built per acre, and what size those new houses can be. As The Washington Post reported in 2019, various government regulations and fees, such as “impact fees,” which are the same regardless of the size of the unit, “incentivize developers to build big.” The Post continues, “if zoning allows no more than two units per acre, the incentive will be to build the biggest, most expensive units possible.”

Moreover, community groups opposed to anything that sounds like “density” or “upzoning” will use the power of local governments to crush developer attempts to build more affordable housing. However, as The Post notes, at least one developer has found “where his firm has been able to encourage cities to allow smaller buildings the demand has been strong. For those building small, demand doesn’t seem to be an issue.”

Similarly, in an article last month at The New York Times, Emily Badger notes the central role of government regulations in keeping houses big and ultimately increasingly unaffordable. She writes how in recent decades,

“Land grew more expensive. But communities didn’t respond by allowing housing on smaller pieces of it. They broadly did the opposite, ratcheting up rules that ensured builders couldn’t construct smaller, more affordable homes. They required pricier materials and minimum home sizes. They wanted architectural flourishes, not flat facades. …”

It is true that in many places empty land has increased in price, but in areas where the regulatory burden is relatively low—such as Houston—builders have nonetheless responded with more building of housing such as townhouses.

In many places, however, regulations continue to push up the prices of homes.

Badger notes that in Portland, Oregon, for example, “Permits add $40,000-$50,000. Removing a fir tree 36 inches in diameter costs another $16,000 in fees.” A lack of small “starter homes” is not due to an unwillingness on the part of builders. Governments have simply made smaller home unprofitable.

“You’ve basically regulated me out of anything remotely on the affordable side,” said Justin Wood, the owner of Fish Construction NW.

In Savannah, Ga., Jerry Konter began building three-bed, two-bath, 1,350-square-foot homes in 1977 for $36,500. But he moved upmarket as costs and design mandates pushed him there.

“It’s not that I don’t want to build entry-level homes,” said Mr. Konter, the chairman of the National Association of Home Builders. “It’s that I can’t produce one that I can make a profit on and sell to that potential purchaser.”

Those familiar with how local governments zone land and set building standards will not be surprised by this. Local governments, pressured by local homeowners, will intervene to keep lot sizes large, and to pass ordinances that keep out housing that might be seen by voters as “too dense” or “too cheap-looking.”

Yet, as much as existing homeowners and city planners would love to see nothing but upper middle-class housing with three-car garages along every street, the fact is that not everyone can afford this sort of housing. But that doesn’t mean people in the middle can only afford a shack in a shanty town either — so long as governments will allow more basic housing to be built.

But there are few signs of many local governments relenting on their exclusionary housing policies, and the result has been an ossified housing policy designed to reinforce existing housing, while denying new types of housing that is perhaps more suitable to smaller households and a more stagnant economic environment.

Eventually, though, something has to give. Either governments persist indefinitely with restrictions on “undesirable” housing — which means housing costs skyrocket — or local governments finally start to allow builders to build housing more appropriate to the needs of the middle class.

If current trends continue, we may finally see real pressure to get local governments to allow more building of more affordable single-family homes, or duplexes, or townhouses. If interest rates continue to march upward, this need will become only more urgent. Moreover, as homebuilding materials continue to become more expensive thanks to 40-year highs in inflation—thanks to the Federal Reserve—there will be even more need to find ways to cut regulatory costs in other areas.

For now, the results have been spotty. But where developers are allowed to actually build for a middle-class clientele, it looks like there’s plenty of demand.

About the Author

Ryan McMaken (@ryanmcmaken) is a senior editor at the Mises Institute. Ryan has a bachelor’s degree in economics and a master’s degree in public policy and international relations from the University of Colorado. He is the author of Breaking Away: The Case for Secession, Radical Decentralization, and Smaller Polities (forthcoming) and Commie Cowboys: The Bourgeoisie and the Nation-State in the Western Genre. He was a housing economist for the State of Colorado.