LAKE ZURICH, Ill.–(BUSINESS WIRE)– ACCO Brands Corporation (NYSE: ACCO) today announced that its board of directors has declared a quarterly cash dividend of $0.075 per share. The dividend will be paid on June 9, 2023, to stockholders of record as of the close of business on May 19, 2023.

“This is the Company’s 22nd quarterly cash dividend since it began paying dividends in 2018. The Company’s dividend has become an important part of our capital allocation strategy and we remain committed to supporting our quarterly dividend with our robust free cash flow. At the current stock price, on an annualized basis, our shareholders are receiving an almost 7% yield on their investment,” said Boris Elisman, Chairman and Chief Executive Officer of ACCO Brands.

About ACCO Brands Corporation

ACCO Brands, the Home of Great Brands Built by Great People, designs, manufactures and markets consumer and end-user products that help people work, learn, play and thrive. Our widely recognized brands include AT-A-GLANCE®, Five Star®, Kensington®, Leitz®, Mead®, PowerA®, Swingline®, Tilibra® and many others. More information about ACCO Brands Corporation (NYSE: ACCO) can be found at www.accobrands.com.

Joe Gomes, Managing Director, Equity Research Analyst, Generalist , Noble Capital Markets, Inc.

Joshua Zoepfel, Research Associate, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

Placing Her Stamp. Vera Bradley CEO Jackie Ardrey announced additional corporate organizational changes as well as targeting $12 million of incremental cost reductions, the majority of which should fall to the bottom line. We view the announcement as Ms. Ardrey putting her stamp on the Company from a management perspective, while right-sizing the expense structure of the Company.

New CFO. Michael Schwindle will join Vera Bradley as CFO on May 8th. Mr. Schwindle has previously worked with CEO Ardrey. Mr. Schwindle is a 30-year retail industry veteran, including 15 years as a CFO in such firms as accessory and jewelry retailer Claire’s, Fleet Farm, Payless ShoeSource, Harry & David, and Musician’s Friend. Mr. Schwindle began his career at Deloitte & Touche LLP.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

– Newly appointed CFO Michael Schwindle brings well-rounded fiscal, operational, and strategic leadership to support Project Restoration –

– Company targeting $12 million in incremental cost reductions in addition to $27 million previously identified –

FORT WAYNE, Ind., April 25, 2023 (GLOBE NEWSWIRE) — Vera Bradley, Inc. (Nasdaq: VRA) (the “Company”) today announced the Company is making additional corporate organizational changes and targeting $12 million in incremental cost reductions for the fiscal year ending February 3, 2024, including the elimination of approximately 25 corporate positions as part of an overall plan to further right-size the expense structure of the enterprise.

Jackie Ardrey, Chief Executive Officer of the Company, noted, “We are committed to returning Vera Bradley and Pura Vida to profitable growth and generating strong cash flow as a Company, which I believe will deliver value to our shareholders over the long term. Earlier this year, we launched Project Restoration, focusing on four key pillars of the business for each brand – Consumer, Brand, Product, and Channel – to drive this long-term profitable growth.”

“The work on Project Restoration started this quarter,” Ardrey continued, “and it is supported by improved financial discipline and cost control. These efforts together will make us a stronger, healthier Company on the top and bottom line.”

“I am pleased to announce that Michael Schwindle will join the Company as Chief Financial Officer on May 8. His track record of driving profitable growth, along with his passion for retail and operational excellence, will be instrumental as the Company executes Project Restoration and in the years beyond,” Ardrey said.

Schwindle is a retail industry veteran with over 30 years of experience, including more than 15 years in Chief Financial Officer roles, delivering strong results through profit improvement and by providing innovative solutions. Since early 2020, he has served as CFO for accessory and jewelry retailer Claire’s. Previously, he held CFO roles at specialty retailers Fleet Farm, Payless ShoeSource, Harry & David, and Musician’s Friend, as well as other key financial roles at Home Depot and Limited Brands. Schwindle began his career at Deloitte & Touche LLP.

John Enwright, the Company’s Chief Financial Officer, will be stepping down as a result of the reorganization. Enwright will work closely with Schwindle through early June to ensure a smooth transition. Ardrey noted, “On behalf of the Board and our entire team, I want to thank John for his many contributions during his nine years of service and for his commitment to our Company, brands, culture, and Associates. We wish him all the best in the future.”

The Company is making several organizational changes in the Marketing, Ecommerce, Product Design, and Product Development areas that will eliminate approximately 25 corporate positions. The Company will also reduce other non-payroll costs throughout the organization, including but not limited to: non-working marketing expenses, third-party contracts and professional services, logistics, operational costs, and travel.

Ardrey noted, “This flattened and streamlined organizational structure will help us improve execution; make faster decisions; and provide support for the Consumer, Brand, Product, and Channel pillars of Project Restoration. These most recent organizational changes and non-payroll expense reductions are expected to produce annualized savings of approximately $12 million, on top of the $27 million of cost reductions previously identified and largely realized in fiscal 2023. All of these initiatives should position Vera Bradley, Inc. to be a stronger, more nimble organization.”

“We are committed to delivering improved value to our shareholders,” Ardrey continued. “These efforts will allow us to reset our expense base and simplify the organization, so we can focus fully on Project Restoration and on delivering both healthy top- and bottom-line growth in the future.”

About Vera Bradley, Inc.

Vera Bradley, Inc. operates two unique lifestyle brands – Vera Bradley and Pura Vida. Vera Bradley and Pura Vida are complementary businesses, both with devoted, emotionally-connected, and multi-generational female customer bases; alignment as casual, comfortable, affordable, and fun brands; positioning as “gifting” and socially-connected brands; strong, entrepreneurial cultures; a keen focus on community, charity, and social consciousness; multi-channel distribution strategies; and talented leadership teams aligned and committed to the long-term success of their brands.

Vera Bradley, based in Fort Wayne, Indiana, is a leading designer of women’s handbags, luggage and other travel items, fashion and home accessories, and unique gifts. Founded in 1982 by friends Barbara Bradley Baekgaard and Patricia R. Miller, the brand is known for its innovative designs, iconic patterns, and brilliant colors that inspire and connect women unlike any other brand in the global marketplace. In July 2019, Vera Bradley, Inc. acquired a 75% interest in Creative Genius, Inc., which also operates under the name Pura Vida Bracelets (“Pura Vida”). Pura Vida, based in La Jolla, California, is a digitally native, highly-engaging lifestyle brand founded in 2010 by friends Paul Goodman and Griffin Thall. Pura Vida has a differentiated and expanding offering of bracelets, jewelry, and other lifestyle accessories.

Vera Bradley Safe Harbor Statement

Certain statements in this release are “forward-looking statements” made pursuant to the safe-harbor provisions of the Private Securities Litigation Reform Act of 1995. Such forward-looking statements reflect the Company’s current expectations or beliefs concerning future events and are subject to various risks and uncertainties that may cause actual results to differ materially from those that we expected, including: possible adverse changes in general economic conditions and their impact on consumer confidence and spending; possible inability to predict and respond in a timely manner to changes in consumer demand; possible loss of key management or design associates or inability to attract and retain the talent required for our business; possible inability to maintain and enhance our brands; possible inability to successfully implement the Company’s long-term strategic plans; possible inability to successfully open new stores, close targeted stores, and/or operate current stores as planned; incremental tariffs or adverse changes in the cost of raw materials and labor used to manufacture our products; possible adverse effects resulting from a significant disruption in our distribution facilities; or business disruption caused by pandemics. Risks, uncertainties, and assumptions also include the possibility that Pura Vida acquisition benefits may not materialize as expected and that Pura Vida’s business may not perform as expected. More information on potential factors that could affect the Company’s financial results is included from time to time in the “Risk Factors” and “Management’s Discussion and Analysis of Financial Condition and Results of Operations” sections of the Company’s public reports filed with the SEC, including the Company’s Form 10-K for the fiscal year ended January 28, 2023. We undertake no obligation to publicly update or revise any forward-looking statement.

CONTACTS: Investors: Julia Bentley, VP of Investor Relations and Communications jbentley@verabradley.com (260) 207-5116

LAKE ZURICH, Ill.–(BUSINESS WIRE)– ACCO Brands Corporation (NYSE: ACCO) today announced that it will release its first quarter 2023 earnings after the market close on May 4, 2023. The Company will host a conference call and webcast to discuss the results on May 5 at 8:30 a.m. EST. The webcast can be accessed through the Investor Relations section of www.accobrands.com and will be available for replay.

About ACCO Brands Corporation

ACCO Brands, the Home of Great Brands Built by Great People, designs, manufactures and markets consumer and end-user products that help people work, learn, play and thrive. Our widely recognized brands include AT-A-GLANCE®, Five Star®, Kensington®, Leitz®, Mead®, PowerA®, Swingline®, Tilibra® and many others. More information about ACCO Brands Corporation (NYSE: ACCO) can be found at www.accobrands.com.

Christopher McGinnis Investor Relations (847) 796-4320

JERICHO, N.Y.–(BUSINESS WIRE)– 1-800-FLOWERS.COM, Inc. (NASDAQ: FLWS) (the “Company”),a leading provider of gifts designed to help inspire customers to give more, connect more, and build more and better relationships, today announced that the Company will release financial results for its fiscal 2023 third quarter on Thursday, May 11, 2023. The press release will be issued prior to market opening and will be followed by a conference call with members of senior management at 8:00 a.m. (ET).

The conference call will be available via live webcast from the Investors section of the Company’s website at 1800flowersinc.com. A recording of the call will be posted on the website within two hours of the call’s completion. A telephonic replay of the call can be accessed beginning at 2:00 p.m. (ET) on May 11, 2023, through May 18, 2023, at: (US) 1-877-344-7529; (Canada) 855-669-9658; (International) 1-412-317-0088; enter conference ID: #4785326.

Special Note Regarding Forward-Looking Statements:

Some of the statements contained in the Company’s scheduled Thursday, May 11, 2023, press release and conference call regarding its results for its fiscal 2023 third quarter, other than statements of historical fact, may be forward-looking within the meaning of the Private Securities Litigation Reform Act of 1995. These statements involve risks and uncertainties that could cause actual results to differ materially from those expressed or implied in the applicable statements. For a more detailed description of these and other risk factors, please refer to the Company’s SEC filings including its Annual Reports and Forms 10K and 10Q available at the Investor Relations section of the Company’s website at 1800flowersinc.com. The Company expressly disclaims any intent or obligation to update any of the forward-looking statements made in the scheduled conference call and any recordings thereof, or in any of its SEC filings, except as may be otherwise stated by the Company.

About 1-800-FLOWERS.COM, Inc.

1-800-FLOWERS.COM, Inc. is a leading provider of gifts designed to help inspire customers to give more, connect more, and build more and better relationships. The Company’s e-commerce business platform features an all-star family of brands, including: 1-800-Flowers.com®, 1-800-Baskets.com®, Cheryl’s Cookies®, Harry & David®, PersonalizationMall.com®, Shari’s Berries®, FruitBouquets.com®, Things Remembered®, Moose Munch®, The Popcorn Factory®, Wolferman’s Bakery®, Vital Choice®, Stock Yards® and Simply Chocolate®. Through the Celebrations Passport® loyalty program, which provides members with free standard shipping and no service charge across our portfolio of brands, 1-800-FLOWERS.COM, Inc. strives to deepen relationships with customers. The Company also operates BloomNet®, an international floral and gift industry service provider offering a broad-range of products and services designed to help members grow their businesses profitably; Napco℠, a resource for floral gifts and seasonal décor; DesignPac Gifts, LLC, a manufacturer of gift baskets and towers; and Alice’s Table®, a lifestyle business offering fully digital livestreaming and on demand floral, culinary and other experiences to guests across the country. 1-800-FLOWERS.COM, Inc. was recognized among the top 5 on the National Retail Federation’s 2021 Hot 25 Retailers list, which ranks the nation’s fastest-growing retail companies, and was named to the Fortune 1000 list in 2022. Shares in 1-800-FLOWERS.COM, Inc. are traded on the NASDAQ Global Select Market, ticker symbol: FLWS. For more information, visit 1800flowersinc.com or follow @1800FLOWERSInc on Twitter.

Classic Burger Chain Broadens International Presence with Newest BengaluruLocation

LOS ANGELES, April 18, 2023 (GLOBE NEWSWIRE) — FAT (Fresh. Authentic. Tasty.) Brands Inc., parent company of Johnny Rockets and 16 other restaurant concepts, announces a new location in India at the Kempegowda International Airport in partnership with HMSHost. Located in Bengaluru, the capital city of Karnataka, the new Johnny Rockets serves the classic fare that put the brand on the map over 35 years ago, including juicy, made-to-order burgers and hand-spun shakes.

“Expanding Johnny Rockets’ presence in non-traditional venues continues to be a key growth objective for the brand,” said Jake Berchtold, COO of FAT Brands’ Fast Casual Division. “Strategically, we are pleased to spearhead this type of expansion in a country like India, where we see significant opportunity to build our footprint.”

“We are seeing exciting times in the air travel industry as the demand remains strong in both the domestic and international travel spaces,” said Jagvir Singh Rana, Managing Director, India and Middle East, HMSHost. “With increased travel and the opening of T2 at Bengaluru International Airport, guest expectations are sure to increase. By partnering with Johnny Rockets, we aim to not only give our guests varied food choices but also an experience they will cherish forever.”

The first Johnny Rockets restaurant opened June 6, 1986, on Melrose Avenue in Los Angeles. Since that time, the chain’s timeless all-American brand has connected with customers across the U.S. and in 25 other countries around the globe.

The Johnny Rockets team’s passion for delivering fresh, classic American fare is only equaled by their commitment to providing a superb guest experience. The new location’s menu includes cooked-to-order burgers, indulgent, hand-spun real ice cream shakes, crispy fries, halal chicken options and more.

The new Bengaluru Johnny Rockets is located at Kempegowda International Airport, Terminal 2, Devanhalli, Bengaluru, and is open from 2 a.m. to 12 a.m. daily.

FAT Brands (NASDAQ: FAT) is a leading global franchising company that strategically acquires, markets and develops fast casual, quick-service, casual and polished casual dining restaurant concepts around the world. The Company currently owns 17 restaurant brands: Round Table Pizza, Fatburger, Marble Slab Creamery, Johnny Rockets, Fazoli’s, Twin Peaks, Great American Cookies, Hot Dog on a Stick, Buffalo’s Cafe & Express, Hurricane Grill & Wings, Pretzelmaker, Elevation Burger, Native Grill & Wings, Yalla Mediterranean and Ponderosa and Bonanza Steakhouses, and franchises and owns over 2,300 units worldwide. For more information on FAT Brands, please visit www.fatbrands.com.

About Johnny Rockets Founded in 1986 on Melrose Avenue in Los Angeles, Johnny Rockets is a world-renowned international franchise that offers high-quality, innovative menu items including Certified Angus Beef® cooked-to-order hamburgers, veggie burgers, chicken sandwiches, crispy fries, and rich, delicious hand-spun shakes and malts. With over 325 locations in over 25 countries around the globe, this dynamic lifestyle brand offers friendly service and upbeat music contributing to the chain’s signature atmosphere of relaxed, casual fun.

Joe Gomes, Managing Director – Generalist Analyst, Noble Capital Markets, Inc.

Joshua Zoepfel, Research Associate, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

FY22 Results. Lifeway reported record full year revenue of $141.6 million for 2022, up 18.9% y-o-y. Higher volumes of drinkable kefir, increased pricing, and a full year of Glen Oaks drove the increased top line. Gross margin of 18.9% was constrained due to increased raw material costs. Lifeway reported full year net income of $0.9 million, or EPS of $0.06, down from $3.3 million, or EPS of $0.21, for 2021.

4Q22. The fourth quarter was the 13th straight quarter of y-o-y net sales growth. Revenues came in at $35.8 million, up 15.7% y-o-y, but modestly below our $39 million projection. Lifeway generated $716,000 of net income, or EPS of $0.05, in the quarter, compared to a loss of $93,000, or a loss of $0.01/sh, in 4Q21. We were at net income of $1.1 million, or $0.07/sh.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

FAT Brands (NASDAQ: FAT) is a leading global franchising company that strategically acquires, markets, and develops fast casual, quick-service, casual dining, and polished casual dining concepts around the world. The Company currently owns 17 restaurant brands: Round Table Pizza, Fatburger, Marble Slab Creamery, Johnny Rockets, Fazoli’s, Twin Peaks, Great American Cookies, Hot Dog on a Stick, Buffalo’s Cafe & Express, Hurricane Grill & Wings, Pretzelmaker, Elevation Burger, Native Grill & Wings, Yalla Mediterranean and Ponderosa and Bonanza Steakhouses, and franchises and owns over 2,300 units worldwide. For more information on FAT Brands, please visit www.fatbrands.com.

Joe Gomes, Managing Director – Generalist Analyst, Noble Capital Markets, Inc.

Joshua Zoepfel, Research Associate, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

Board Changes. Yesterday, FAT Brands announced a nearly wholesale change to its Board. We believe the changes were made in an effort to help separate the Company from the ongoing derivative lawsuits and the government investigation, as well as give the still to be appointed new CEO a “clean slate” to execute the business plan. In addition, FAT Brands elected “controlled company” status for purposes of the government governance rules. While always a controlled company, FAT Brands had previously elected to follow the “majority of independent directors” rule. The move to “controlled company” status could save the Company about $1 million per year.

The New Board. Of the former directors, only Andrew Wiederhorn and Lynne Collier remain. Additions to the Board include five insiders, including Mr. Wiederhorn’s three sons, all of whom hold leadership positions at FAT Brands, and three independent directors — Mark Elenowitz, Kenneth Kepp, and Tyler Child.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

Bassett Furniture Industries, Incorporated manufactures, markets, and retails home furnishings in the United States. The company operates in three segments: Wholesale, Retail, and Logistical Services. It is involved in the design, manufacture, sourcing, sale, and distribution of furniture products to a network of company-owned and licensee-owned Bassett Home Furnishings (BHF) retail stores, as well as independent furniture retailers; and wood and upholstery operations. As of September 16, 2017, the company operated a network of 91 company-and licensee-owned stores. It also provides shipping, delivery, and warehousing services to customers in the furniture industry. In addition, the company owns and leases retail store properties. It also distributes its products through other multi-line furniture stores, Bassett galleries or design centers, specialty stores, and mass merchants. Bassett Furniture Industries was founded in 1902 and is based in Bassett, Virginia.

Joe Gomes, Managing Director – Generalist Analyst, Noble Capital Markets, Inc.

Joshua Zoepfel, Research Associate, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

1Q23 Results. Bassett missed on both our top and bottom line projections as the hangover from 2022 continued. The Company reported revenue of $107.7 million, short of our $111 million estimate, and down 8.6% y-o-y. Wholesale revenue declined 16%, while Retail revenue rose 1.3%. Operating income was $2.7 million, down from $6.5 million in 1Q22. Bassett reported net income of $1.4 million, or $0.16 per share, compared to net income from continuing operations of $4.3 million, or $0.44 per share, in the prior year. We had forecast EPS of $0.30.

Operating Environment. The post-COVID operating environment remains challenging. While backlog levels have returned to more normalized levels, the Company continues to work through higher cost inventory as well as a shift in consumer dollars away from furniture. Wholesale orders fell 18% y-o-y in 1Q23, while retail written orders were off 16% y-o-y.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

New 501(c)(3) Organization FormedtoFurtherUnite Communities in Which Restaurant Franchising Company Operates

LOS ANGELES, March 22, 2023 (GLOBE NEWSWIRE) — FAT (Fresh. Authentic. Tasty.) Brands Inc., a leading global franchising company that owns restaurant brands including Johnny Rockets, Fatburger, Round Table Pizza, Twin Peaks, Fazoli’s and 12 other concepts, is pleased to announce the official launch of its newly formed 501(c)(3) charitable organization, FAT Brands Foundation. Created to amplify the existing charitable efforts of its 17-brand portfolio, the foundation will partner with local non-profit organizations in areas in which FAT Brands has a presence to provide essential programs to help families and communities thrive.

“Giving back has always been a part of the FAT Brands DNA,” said Jessica Wiederhorn, President of FAT Brands Foundation and Head of Non-Traditional Sales and Partnerships at FAT Brands. “With our company continuing to grow in size, we wanted to take our charitable efforts to the next level by launching a new arm that more broadly supports our employees and customers’ beloved communities. We are excited to be officially live and to have the opportunity to become more engrained with local non-profits that are committed to making a positive impact in the markets where we operate. Our mission is wide-ranging so we can meaningfully serve each community on a local, specific level.”

The foundation was seeded with a $250,000 donation from FAT Brands upon its inception and will continue to receive support from its parent company to further the directive of the organization in the years to come. For non-profits interested in applying for a grant or for those interested in donating to the foundation, please visit www.fatbrands.com/foundation.

About FAT (Fresh. Authentic. Tasty.) Brands FAT Brands (NASDAQ: FAT) is a leading global franchising company that strategically acquires, markets, and develops fast casual, quick-service, casual dining, and polished casual dining concepts around the world. The Company currently owns 17 restaurant brands: Round Table Pizza, Fatburger, Marble Slab Creamery, Johnny Rockets, Fazoli’s, Twin Peaks, Great American Cookies, Hot Dog on a Stick, Buffalo’s Cafe & Express, Hurricane Grill & Wings, Pretzelmaker, Elevation Burger, Native Grill & Wings, Yalla Mediterranean and Ponderosa and Bonanza Steakhouses, and franchises and owns over 2,300 units worldwide.

AboutFAT Brands Foundation Founded in 2022, the FAT Brands Foundation was created to uplift and unite the communities in which FAT Brands operates. While the company’s 17-brand portfolio is deeply rooted in charitable initiatives both locally and nationally, FAT Brands, as an organization, is seeking to magnify those efforts further. The 501(c)(3) organization is aimed at partnering with local non-profit organizations to provide essential programs to help families and communities thrive.

For more than 45 years, 1-800-Flowers.com has offered truly original floral arrangements, plants and unique gifts to celebrate birthdays, anniversaries, everyday occasions, and seasonal holidays, and to deliver comfort during times of grief. Backed by a caring team obsessed with service, 1-800-Flowers.com provides customers thoughtful ways to express themselves and connect with the most important people in their lives. 1-800-Flowers.com is part of the 1-800-FLOWERS.COM, Inc. family of brands. Shares in 1-800-FLOWERS.COM, Inc. are traded on the NASDAQ Global Select Market, ticker symbol: FLWS.

Michael Kupinski, Director of Research, Noble Capital Markets, Inc.

Jacob Mutchler, Research Associate, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

Highlights from recent NDR. This report highlights investor meetings hosted in Southern Florida last week by Chris McCann, CEO; Tom Hartnett, President; Bill Shea, CFO; and Andy Milevoj, Sr. VP Investor Relations.

On the hunt for acquisitions. The company has made successful acquisitions during uncertain economic times, such as the acquisition of Harry & David in 2014, a year of sluggish economic growth. Management indicated that acquisitions is the best use of cash at this time, which may position the company for enhanced revenue and cash flow growth. Notably, the company indicated that it has always acquired for cash.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

Joe Gomes, Managing Director – Generalist Analyst, Noble Capital Markets, Inc.

Joshua Zoepfel, Research Associate, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

4QFY23 Results. Net revenue of $147.1 million came in above guidance of $136-$141 million, and our $138 million estimate. Expanded promotional activity negatively impacted adjusted gross margin, which declined 240bp y-o-y. GAAP EPS loss was $0.91, while adjusted EPS was $0.16, compared to EPS of $0.15 and $0.17, respectively, in 4QFY22, and our $0.15 estimate.

Improving Sales Trends. In the fourth quarter, sales trends at both Vera Bradley and Pura Vida improved over prior quarters, with Vera Bradley total sales down just 1% and Pura Vida sales down less than 5% on a year-over-year basis. Targeted customer retention efforts led to increased Vera Bradley e-commerce revenues, while Full-Line and Factory store revenues continued to be negatively affected by traffic levels. At Pura Vida, e-commerce trends improved over previous quarters due to strategic promotions.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

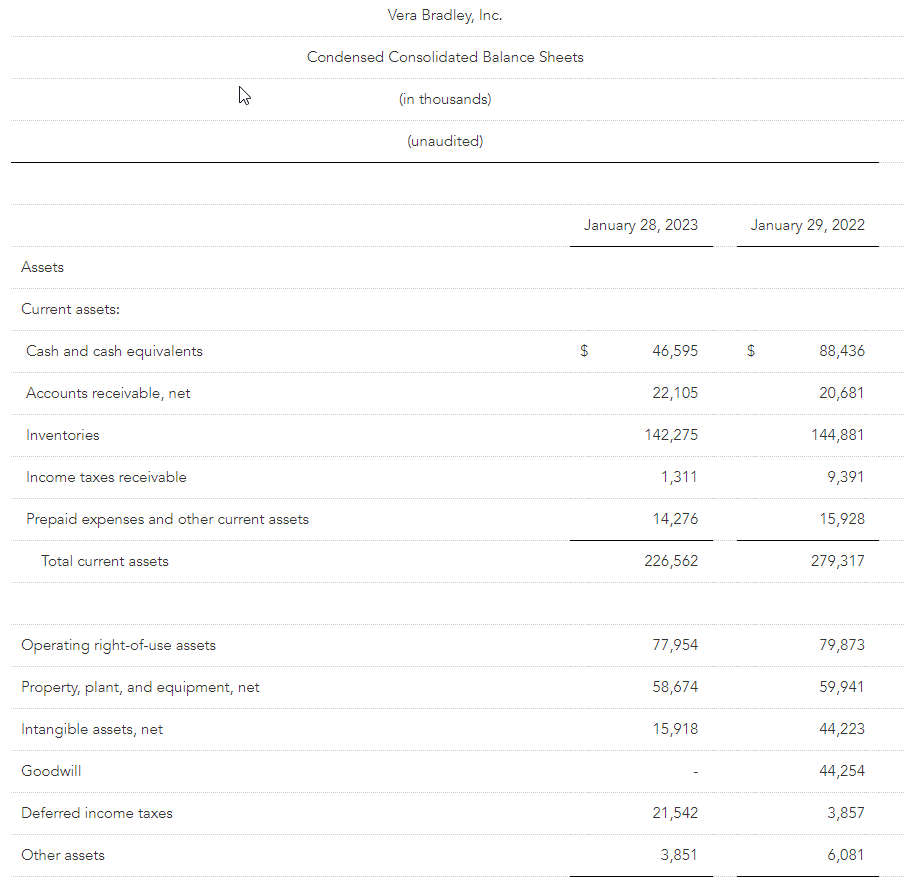

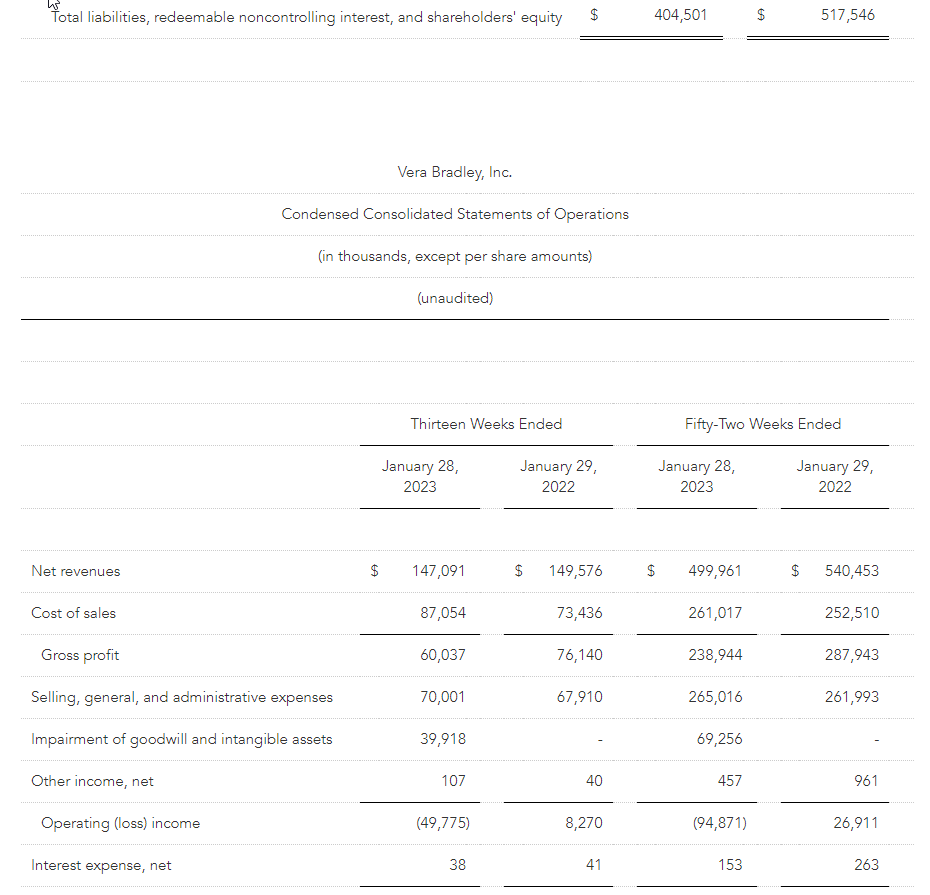

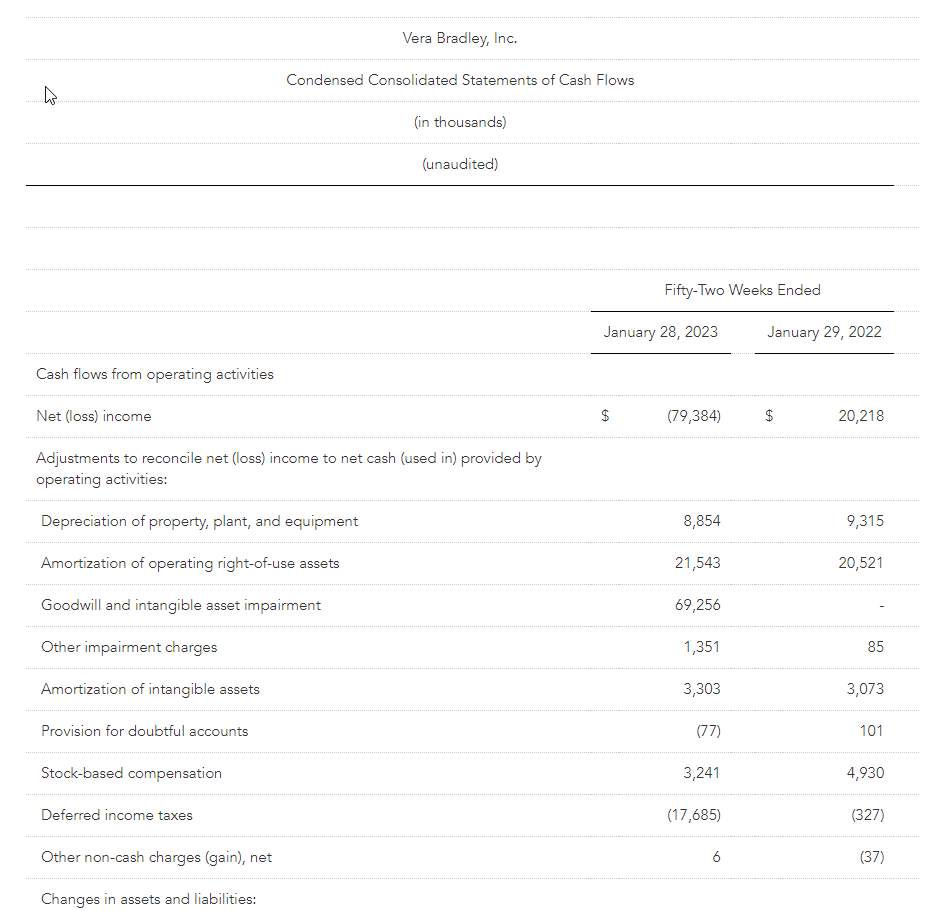

Net revenues totaled $500.0 million for the fiscal year

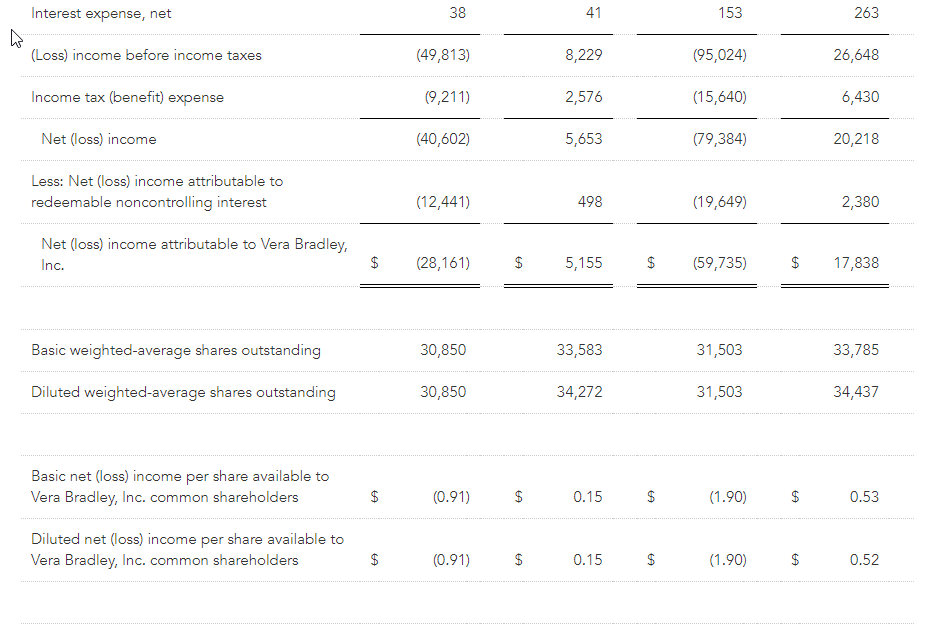

Net loss totaled ($59.7) million, or ($1.90) per diluted share, for fiscal year; excluding certain items, non-GAAP net income totaled $7.6 million, or $0.24 per diluted share

Balance sheet remains strong, with cash and cash equivalents of $46.6 million and no debt

Management provides guidance for fiscal year ending February 3, 2024

FORT WAYNE, Ind., March 08, 2023 (GLOBE NEWSWIRE) — Vera Bradley, Inc. (Nasdaq: VRA) (or the “Company”) today announced its financial results for the fourth quarter and fiscal year ended January 28, 2023 (“Fiscal 2023”).

In this release, Vera Bradley, Inc. or “the Company” refers to the entire enterprise and includes both the Vera Bradley and Pura Vida brands. “Vera Bradley” on a stand-alone basis refers only to the Vera Bradley brand.

Fourth Quarter and Fiscal Year Comments

Jackie Ardrey, Chief Executive Officer of the Company, noted, “We focused on driving revenues in the fourth quarter through targeted, strategic promotions on seasonal, giftable, and key items. As a result, total Company fourth quarter revenues outperformed our guidance, although gross margins remained under pressure. Diligent expense control enabled us to deliver fourth quarter non-GAAP diluted EPS of $0.16, which was nearly flat with last year.

“In the fourth quarter, sales trends at both Vera Bradley and Pura Vida improved over prior quarters, with Vera Bradley total sales down just 1% and Pura Vida sales down less than 5% on a year-over-year basis. For the fourth consecutive quarter, the Vera Bradley Indirect Channel experienced year-over-year revenue growth. Targeted customer retention efforts led to increased Vera Bradley e-commerce revenues, while Full-Line and Factory store revenues continued to be negatively affected by traffic levels, although trends improved throughout the quarter.”

Ardrey continued, “At Pura Vida, e-commerce trends improved over previous quarters due to strategic promotions; however, overall challenges continued to persist in our social and digital media effectiveness coupled with rising digital media costs. And, we experienced a year-over-year sales decline in our wholesale channel. On the plus side, Pura Vida Full-Line retail stores continued to perform ahead of our expectations, and they drove improved e-commerce traffic and revenues in their markets.

“We also took the opportunity in the fourth quarter to reset and appropriately position the Pura Vida business for the future, by recording goodwill and tradename impairments and necessary inventory write-offs.

“We ended the fiscal year with consolidated revenues of $500 million. During the year, we began to see stabilization in our supply chain, diligently controlled our expenses, and carefully managed our cash. During the fourth quarter, we meaningfully reduced our year-end inventory levels from the third quarter.”

Ardrey added, “Although Fiscal 2023 had its challenges, we took actions and laid the groundwork to position the Company for the future.

“On a corporate basis:

In mid-2022, we collaboratively identified $25 million in annualized cost-reduction initiatives and efficiency processes. The expense savings were derived across various areas of the Company, including payroll reductions, retail store efficiencies, marketing expenses, information technology contracts and projects, professional services, and logistics and operational costs. Many of the savings were realized in Fiscal 2023.

In January 2023, we further streamlined our corporate structure by eliminating the positions of Vera Bradley Brand President, Chief Creative Officer, and Chief Revenue Officer, and by adding the position of Chief Marketing Officer, designed to drive additional annual cost savings of approximately $2 million, add more focus on marketing and merchandising, and position the Company to deliver steady top- and bottom-line growth. These decisions were made in order to right-size our leadership team and cost structure for the size of our business, to address the continuing challenging macro environment, and to best position us to achieve our long-term strategic plans.

Subsequent to the end of Fiscal 2023, in January 2023, we acquired the remaining 25% interest in Pura Vida from founders Griffin Thall and Paul Goodman for $10 million.

We continued to make investments in customer data science, business analytics, and pricing optimization, allowing us to collect and analyze data and make fact-based decisions to more efficiently run our business.

“At the Vera Bradley brand:

We expanded our robust product innovation pipeline, including launching our Featherweight Collection; continued another year of iconic product collaborations, including with Disney, Harry Potter, and Crocs; and expanded our cozy, sleep, and outerwear collections.

We continued to strengthen and rationalize our store base. We opened five new Factory stores and closed 19 underperforming Full-Line stores and one Factory store, ending the fiscal year with 51 Full-Line and 79 Factory locations. We also continued to expand options for customers to shop, like enhancing our presence in third-party marketplaces and adding boutiques in select high-traffic airports.

“At the Pura Vida brand:

We entered into several high-profile product collaborations, with brands such as Hello Kitty, Disney, and Harry Potter, and expanded our product offerings by launching our demi-fine collection and expanding our assortment of engravable jewelry, all designed to bring new customers to our brand.

We focused on building a more diverse, innovative, effective, and performance-based marketing program to drive Pura Vida e-commerce sales. We began the process of implementing a comprehensive customer data platform to build a single, coherent, complete view of each Pura Vida customer so that we can better target and personalize marketing and become less reliant on third-party marketing. This project is scheduled for completion this spring. We continued to engage our micro influencers, significantly expanded our TikTok presence, launched impactful ads on connected TV, optimized SMS, and aggressively explored other methods to effectively reach our customers.

We opened three new Pura Vida Full-Line stores during the year, bringing our Full-Line store count to four, which collectively are exceeding our expectations. These four stores are playing a role in driving new customer acquisition as we continue to diversify our marketing platforms, and they demonstrate the power a retail presence can have in driving digital sales, omni-channel loyalty, and spending.”

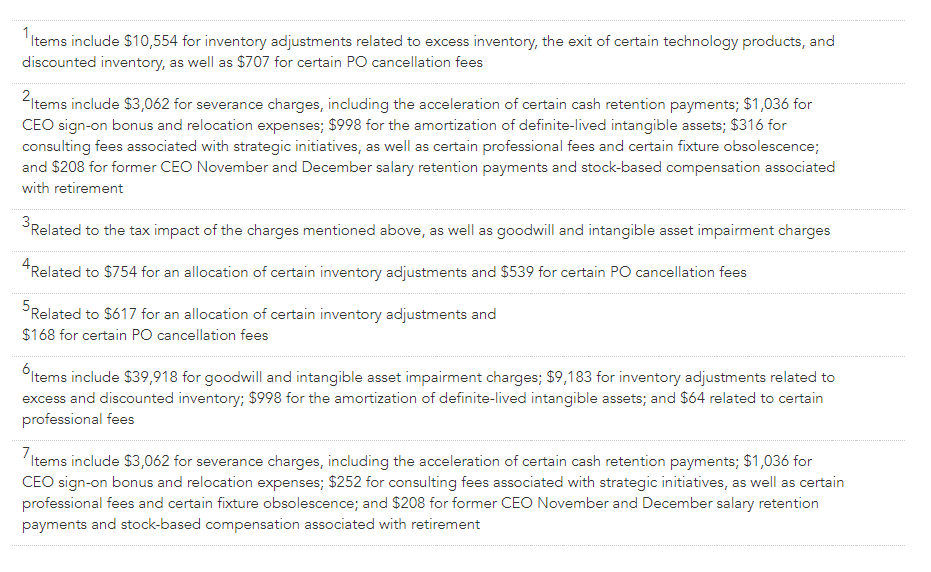

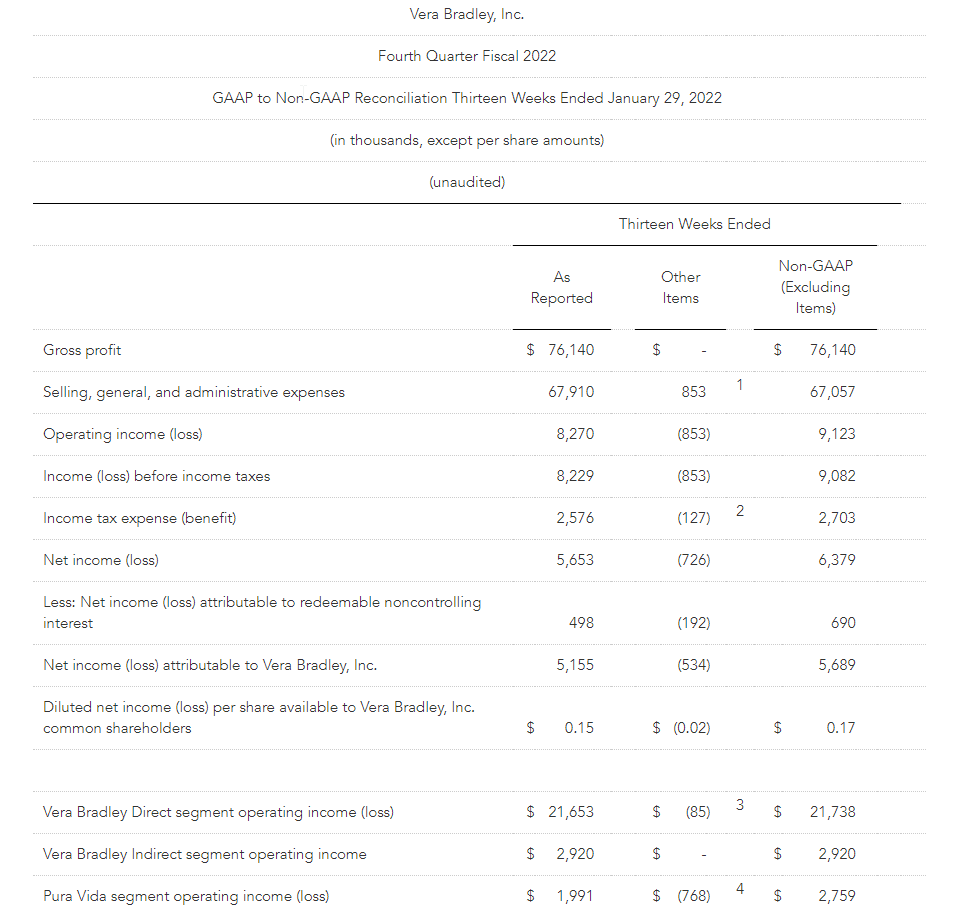

Summary of Financial Performance for the Fourth Quarter

Consolidated net revenues totaled $147.1 million for the current year fourth quarter compared to $149.6 million in the prior year fourth quarter.

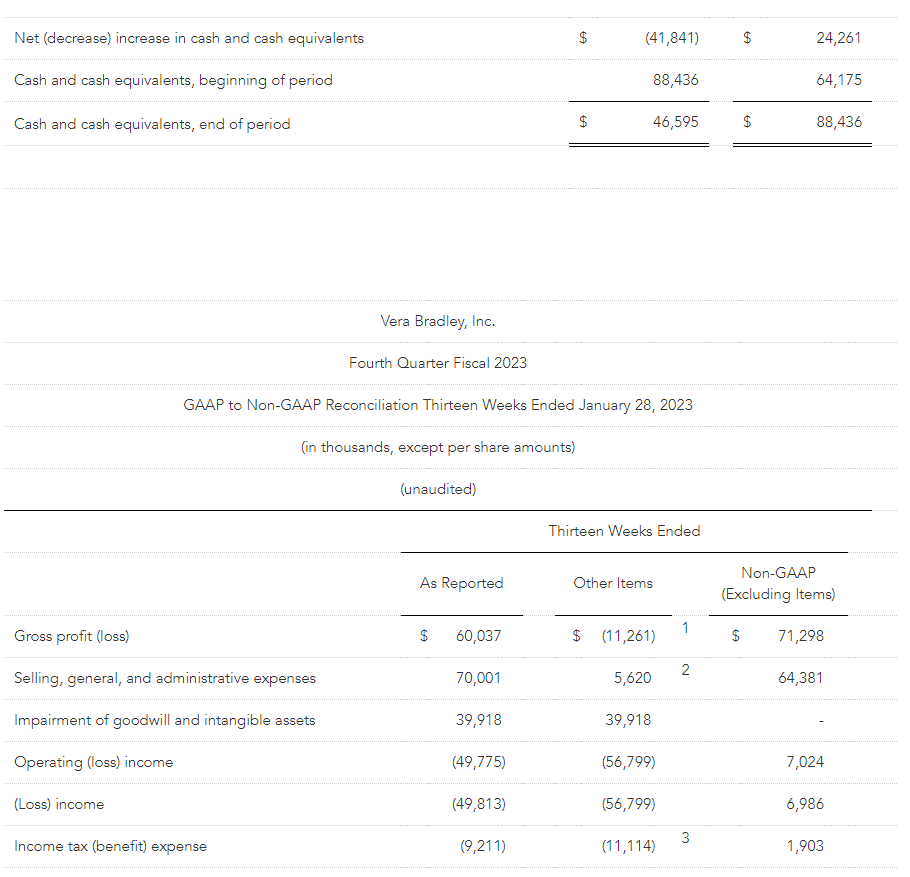

For the current year fourth quarter, Vera Bradley, Inc.’s consolidated net loss totaled ($28.2) million, or ($0.91) per diluted share. These results included $33.1 million of net after tax charges, comprised of $22.4 million of goodwill and intangible asset impairment charges; $6.7 million of net inventory and purchase order-related adjustments; $2.4 million of severance, retention, and stock-based retirement compensation charges; $0.8 million related to new CEO sign-on bonus and relocation expenses; $0.5 million for the amortization of definite-lived intangible assets; and $0.3 million of consulting and professional fees primarily associated with strategic initiatives. On a non-GAAP basis, Vera Bradley, Inc.’s consolidated fourth quarter net income totaled $5.0 million, or $0.16 per diluted share.

For the prior year fourth quarter, Vera Bradley, Inc. consolidated net income totaled $5.2 million, or $0.15 per diluted share. These results included $0.5 million of net after tax charges primarily related to intangible asset amortization. On a non-GAAP basis, excluding these charges, Vera Bradley, Inc.’s prior year consolidated fourth quarter net income totaled $5.7 million, or $0.17 per diluted share.

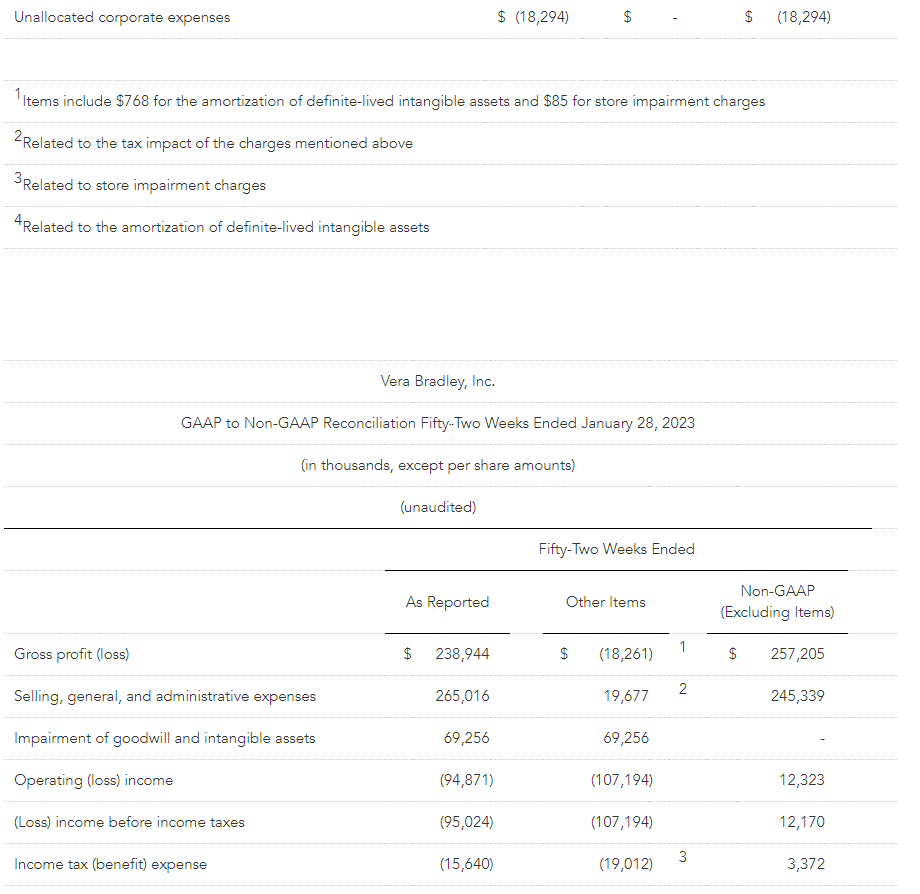

Summary of Financial Performance for the Fiscal Year

Consolidated net revenues totaled $500.0 million for Fiscal 2023 compared to $540.5 million for Fiscal 2022.

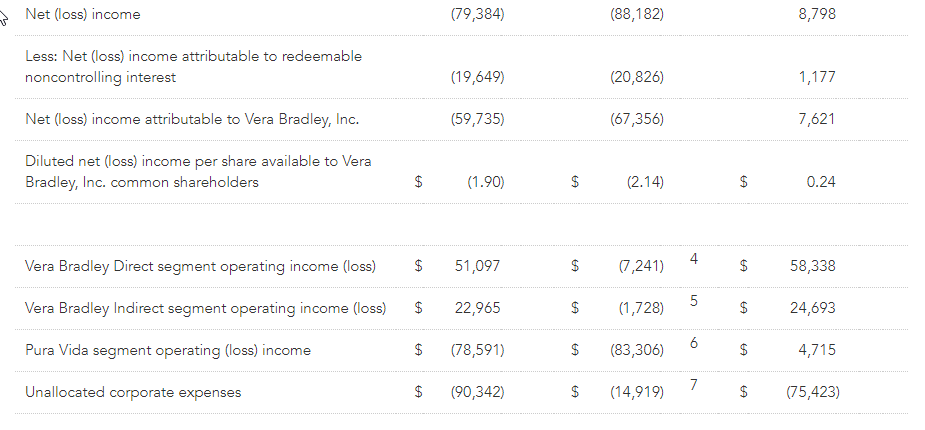

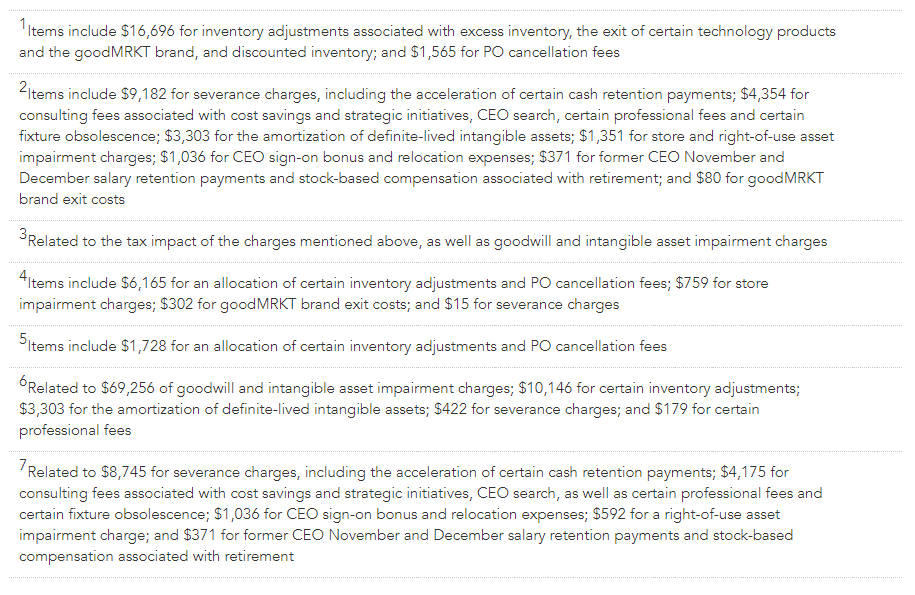

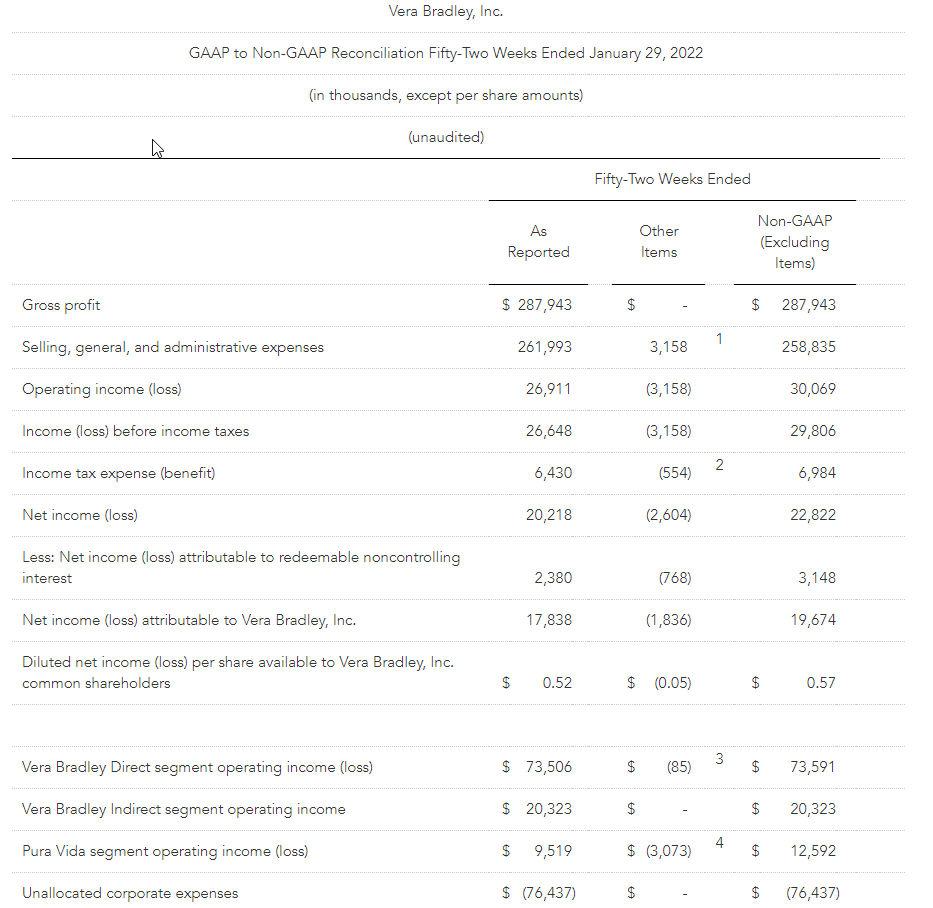

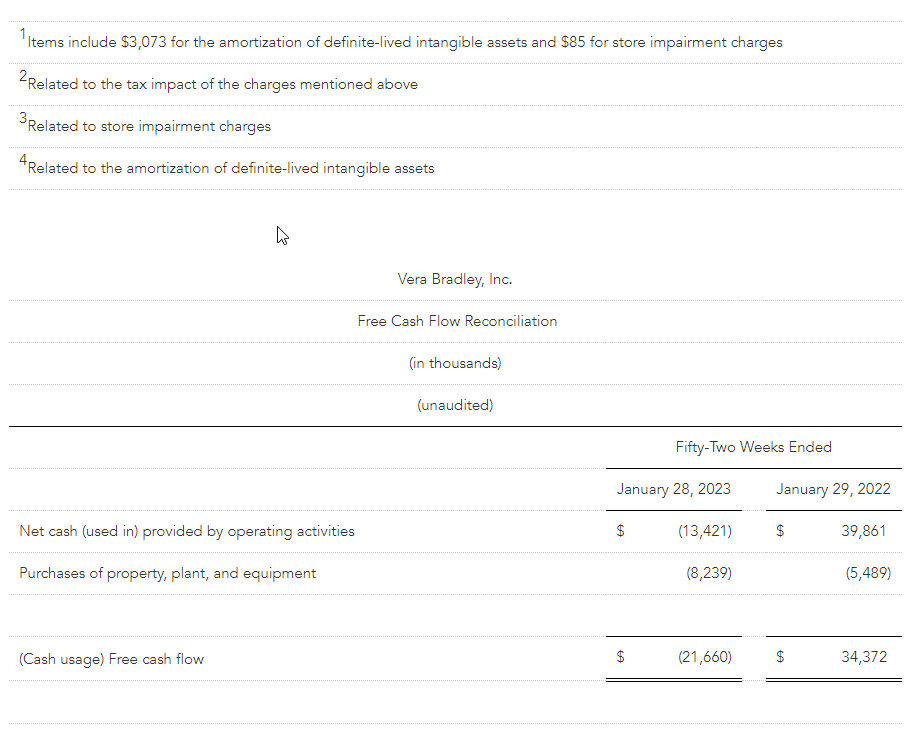

For the current fiscal year, Vera Bradley, Inc.’s consolidated net loss totaled ($59.7) million, or ($1.90) per diluted share. These results included $67.4 million of net after tax charges, comprised of $40.6 million of goodwill and intangible asset impairment charges; $12.2 million of net inventory and purchase order-related adjustments; $7.4 million of severance, retention, and stock-based retirement compensation charges; $3.3 million of consulting and professional fees primarily associated with cost savings initiatives, the CEO search, and strategic initiatives; $1.8 million for the amortization of definite-lived intangible assets; $1.0 million of store and right-of-use asset impairment charges; $0.8 million related to the new CEO sign-on bonus and relocation expenses; and $0.3 million of goodMRKT exit costs. On a non-GAAP basis, Vera Bradley, Inc.’s consolidated net income totaled $7.6 million, or $0.24 per diluted share.

For the prior fiscal year, Vera Bradley, Inc.’s consolidated net income totaled $17.8 million, or $0.52 per diluted share. These results included $1.8 million of net after tax charges primarily related to intangible asset amortization. On a non-GAAP basis, excluding these charges, Vera Bradley, Inc.’s prior year consolidated net income totaled $19.7 million, or $0.57 per diluted share.

Looking Ahead

Ardrey noted, “We are committed to returning Vera Bradley and Pura Vida to profitable growth and generating strong cash flow as a Company, which I believe will deliver value to our shareholders over the long term. Since joining the Company in November, I am more convinced than ever that both brands have enormous potential, and I am very excited about the future of Vera Bradley, Inc. We have a portfolio of two iconic, lifestyle brands; multi-generational customers with remarkable loyalty and devotion; impressive brand recognition; a solid balance sheet; and an extraordinary culture. We have some heavy lifting to do in fiscal 2024, but I am confident that we will emerge a stronger Company.”

Ardrey continued, “At both brands, we are embarking on Project Restoration and will focus on four key pillars – Consumer, Brand, Product, and Channel – to drive this long-term profitable growth.

“At Vera Bradley:

Consumer: We will focus on restoring brand relevancy, targeting casual and feminine 35 to 54 year old women who value both fashion and function.

Brand: We will strategically market our distinctive and unique position as a feminine, fashionable brand that connects with consumers on a deep, emotional level.

Product: We will refocus on core categories and items we are “best at,” by innovating and expanding within our core products. We will elevate our colorful feminine heritage, keeping it distinctive but more trend relevant through updated print and design. We also will innovate into strategic adjacent lifestyle item introductions that make sense for our customers.

Channel: We will accelerate our digital-first focus and online presence, build a balanced footprint that more clearly differentiates Full-Line from Factory stores, and target and/or strengthen relationships with strategically-aligned wholesale partners.

“At Pura Vida:

Consumer: We will sharpen our focus on the care-free 18 to 24 collegiate girl, who both those younger and older aspire to be.

Brand: We will recenter our brand ethos on “living life to the fullest,” with marketing authentically sharing real moments, places, and faces.

Product: We will focus on delivering unique, fun, playful designs that are affordable and accessible with a dominant emphasis on bracelets and jewelry, as well as other strategic, adjacent categories.

Channel: We will have a strong focus on restoring e-commerce growth; strategic growth of wholesale by pursuing larger, more strategic partnerships and expanding larger existing accounts; and refining our existing store model.”

“To support growth and development of our two brands, on a corporate basis, we will continue to make strategic investments in the right talent to help drive the transformation and diligently manage our supply chain, gross margin, SG&A expenses, and cash flow,” Ardrey concluded.

Non-GAAP Numbers

The current year non-GAAP fourth quarter income statement numbers referenced below exclude the previously outlined charges for goodwill and intangible asset impairment; net inventory and purchase order-related adjustments; severance, retention, and stock-based retirement compensation; new CEO sign-on bonus and relocation; amortization of definite-lived intangible assets; and consulting and professional fees primarily associated with strategic initiatives. The current year non-GAAP fiscal year income statement numbers also exclude the previously outlined charges for cost savings initiatives and the CEO search, store and right-of-use asset impairment charges, and goodMRKT exit costs. The prior year non-GAAP fourth quarter and fiscal year income statement numbers referenced below exclude the previously outlined intangible asset amortization and store impairment charges.

Fourth Quarter Details

Current year fourth quarter Vera Bradley Direct segment revenues totaled $99.5 million, a 4.6% decrease from $104.4 million in the prior year fourth quarter. Comparable sales decreased 4.5% from the prior year. The Company permanently closed 19 Full-Line stores and one Factory store and opened five Factory stores in the last twelve months.

Vera Bradley Indirect segment revenues totaled $16.7 million, a 28.5% increase over $13.0 million in the prior year fourth quarter. The increase was broad-based with both specialty and key accounts posting year-over-year sales gains.

Pura Vida segment revenues totaled $30.9 million, a 4.2% decrease from $32.2 million in the prior year fourth quarter. The decline was primarily related to lower wholesale sales, partially offset by new store openings.

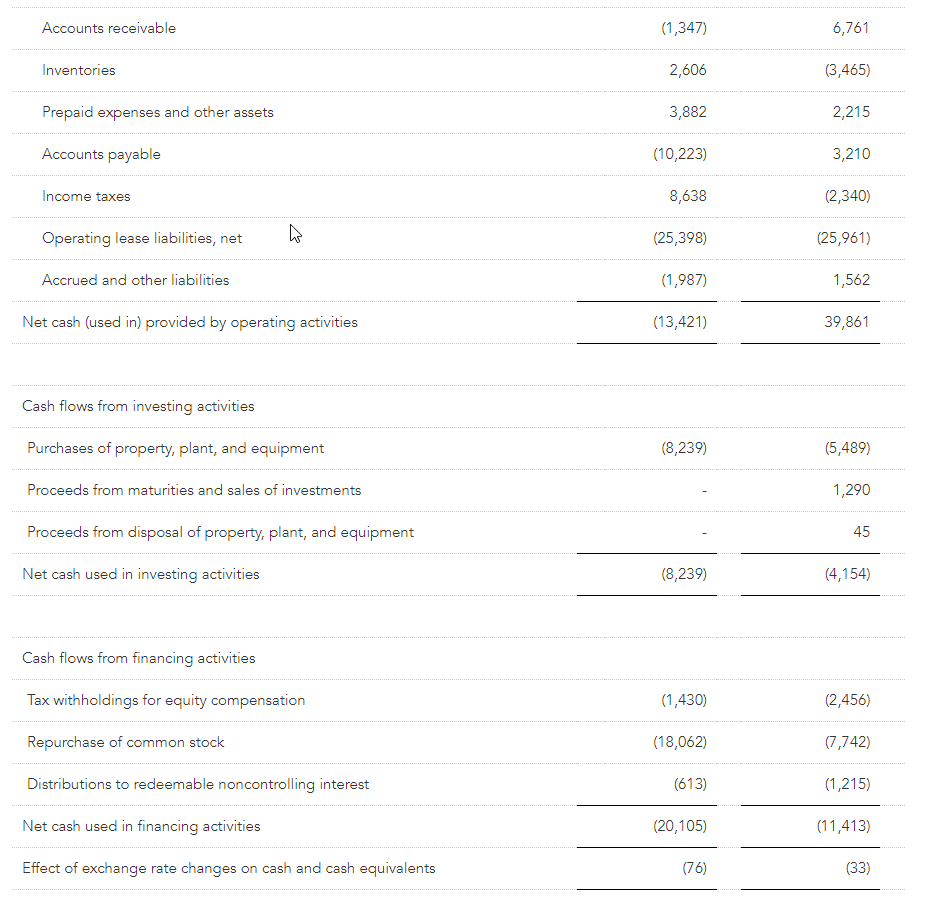

Fourth quarter consolidated gross profit totaled $60.0 million, or 40.8% of net revenues, compared to $76.1 million, or 50.9% of net revenues, in the prior year fourth quarter. On a non-GAAP basis, current year consolidated gross profit totaled $71.3 million, or 48.5% of net revenues. The current year gross profit rate primarily was negatively affected by higher inbound and outbound freight expense and increased promotional activity, partially offset by price increases.

Consolidated SG&A expense totaled $70.0 million, or 47.6% of net revenues, compared to $67.9 million, or 45.4% of net revenues, in the prior year fourth quarter. On a non-GAAP basis, consolidated SG&A expense totaled $64.4 million, or 43.8% of net revenues, compared to $67.1 million, or 44.8% of net revenues, in the prior year fourth quarter. Vera Bradley’s SG&A current year expenses were lower than the prior year primarily due to cost reduction initiatives and a reduction in variable-related expenses due to the lower sales volume.

The Company’s fourth quarter consolidated operating loss totaled ($49.8) million, or (33.8%) of net revenues, compared to operating income of $8.3 million, or 5.5% of net revenues, in the prior year fourth quarter. On a non-GAAP basis, fourth quarter consolidated operating income totaled $7.0 million, or 4.8% of net revenues, compared to $9.1 million, or 6.1% of net revenues, in the prior year.

By segment:

Vera Bradley Direct fourth quarter operating income was $18.5 million, or 18.6% of Direct net revenues, compared to $21.7 million, or 20.7% of Direct net revenues, in the prior year. On a non-GAAP basis, current year Direct fourth quarter operating income was $19.8 million, or 19.9% of Direct net revenues, compared to $21.7 million, or 20.8% of Direct net revenues, in the prior year.

Vera Bradley Indirect fourth quarter operating income was $4.6 million, or 27.3% of Indirect net revenues, compared to $2.9 million, or 22.5% of Indirect net revenues, in the prior year. On a non-GAAP basis, current year Indirect fourth quarter operating income was $5.3 million, or 32.0% of Indirect net revenues.

Pura Vida’s current year fourth quarter operating loss was ($49.8) million, or (161.2%) of Pura Vida net revenues, compared to operating income of $2.0 million, or 6.2% of Pura Vida net revenues, in the prior year. On a non-GAAP basis, Pura Vida’s current year fourth quarter operating income was $0.4 million, or 1.3% of Pura Vida net revenues, compared to $2.8 million, or 8.6% of Pura Vida net revenues, in the prior year.

Details for the Fiscal Year

Vera Bradley Direct segment revenues for the current fiscal year totaled $328.2 million, 7.5% decrease from $354.9 million in the prior year. Comparable sales declined 9.5% for the fiscal year.

Vera Bradley Indirect segment revenues for the fiscal year totaled $73.3 million, an 11.1% increase over $66.0 million in the prior year, primarily reflecting an increase in certain key account orders.

Current year Pura Vida segment revenues totaled $98.4 million, a 17.7% decrease from $119.6 million in the prior year. Pura Vida’s e-commerce revenues continue to be negatively impacted by the shift in social and digital media effectiveness and rising digital media costs, and a decline in sales to wholesale accounts.

Consolidated gross profit for the current fiscal year totaled $238.9 million, or 47.8% of net revenues, compared to $287.9 million, or 53.3% of net revenues, last year. On a non-GAAP basis, gross profit for the current fiscal year totaled $257.2 million, or 51.4% of net revenues. The current year gross profit rate primarily was negatively affected by higher inbound and outbound freight expense and increased promotional activity, partially offset by price increases.

For the fiscal year, consolidated SG&A expense totaled $265.0 million, or 53.0% of net revenues, compared to $262.0 million, or 48.5% of net revenues, in the prior year. On a non-GAAP basis, SG&A expense totaled $245.3 million, or 49.1% of net revenues, in the current year, compared to $258.8 million, or 47.9% of net revenues, in the prior year. Vera Bradley’s SG&A current year expenses were lower than the prior year primarily due to cost reduction initiatives and a reduction in variable-related expenses due to the lower sales volume.

For the fiscal year, the Company’s consolidated operating loss totaled ($94.9) million, or (19.0%) of net revenues, compared to operating income of $26.9 million, or 5.0% of net revenues, in the prior year. On a non-GAAP basis, the Company’s consolidated operating income was $12.3 million, or 2.5% of net revenues, compared to $30.1 million, or 5.6% of net revenues, in the prior year.

By segment:

Vera Bradley Direct operating income was $51.1 million, or 15.6% of Direct net revenues, compared to $73.5 million, or 20.7% of Direct net revenues, in the prior year. On a non-GAAP basis, Direct operating income was $58.3 million, or 17.8% of Direct net revenues, for the current year, compared to $73.6 million, or 20.7% of Direct net revenues, in the prior year.

Vera Bradley Indirect operating income was $23.0 million, or 31.3% of Indirect net revenues, compared to $20.3 million, or 30.8% of Indirect net revenues, in the prior year. On a non-GAAP basis, current year Indirect operating income totaled $24.7 million, or 33.7% of Indirect net revenues.

Pura Vida’s operating loss was ($78.6) million, or (79.9%) of Pura Vida net revenues, compared to operating income of $9.5 million, or 8.0% of Pura Vida net revenues, in the prior year. On a non-GAAP basis, Pura Vida’s operating income was $4.7 million, or 4.8% of Pura Vida net revenues, compared to $12.6 million, or 10.5% of Pura Vida net revenues, in the prior year.

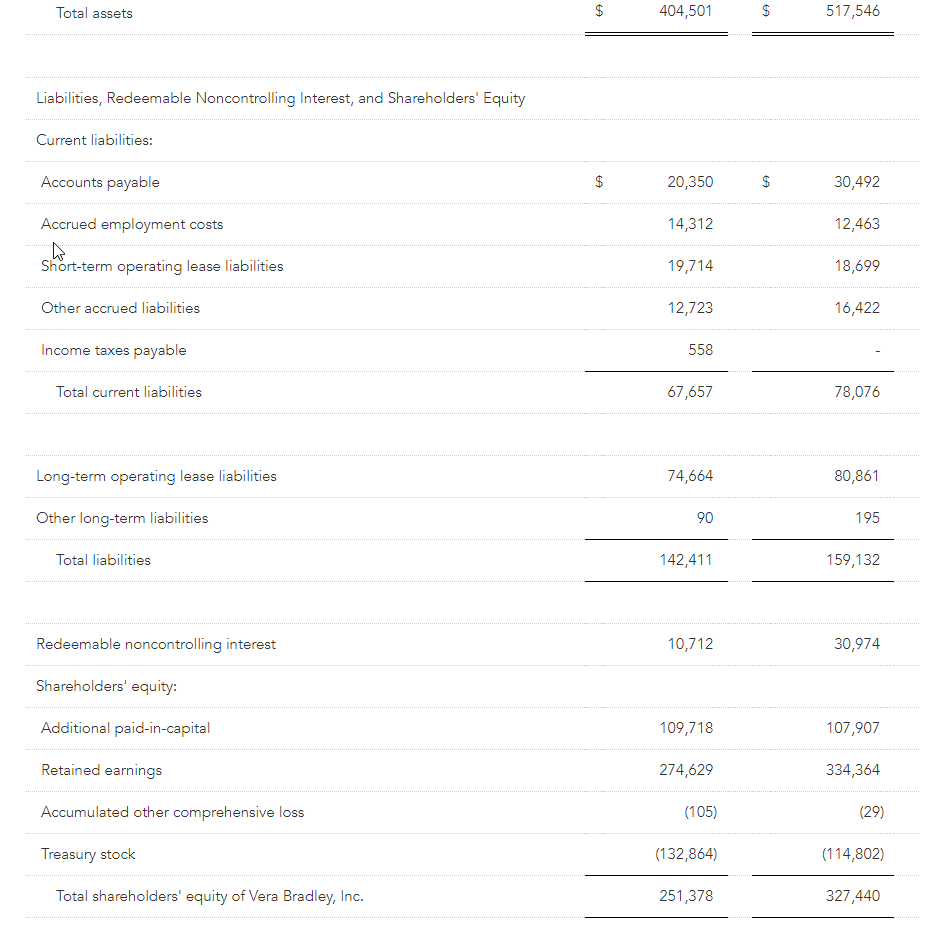

Balance Sheet

Net capital spending for the fiscal year totaled $8.2 million compared to $5.5 million in the prior year.

Cash and cash equivalents as of January 28, 2023 totaled $46.6 million compared to $88.4 million at the prior fiscal year end. The Company had no borrowings on its $75 million ABL credit facility at fiscal year end.

Total fiscal year-end inventory was $142.3 million, compared to $144.9 million at last fiscal year end. Total current year inventory was lower than the prior year primarily due to inventory adjustments associated with excess and discounted inventory, partially offset by incremental logistics costs burdening overall inventory.

During the fourth quarter, the Company repurchased approximately $0.8 million of its common stock (approximately 187,000 shares at an average price of $4.20), bringing the Company’s Fiscal 2023 purchases to $18.1 million (approximately 2.8 million shares at an average price of $6.40). The Company’s $50.0 million share repurchase authorization expires in December 2024. Since Fiscal 2015, the Company has repurchased $132.9 million, or approximately 12.1 million shares, of its common stock.

Forward Outlook

Management is providing estimates for the fiscal year ending February 3, 2024 (“Fiscal 2024”) based on current macroeconomic trends and expectations. Ardrey noted, “We anticipate the Fiscal 2024 macroeconomic environment to continue to be unpredictable and that this year will be a rebuilding year for both of our brands. We expect to take advantage of gross margin improvement opportunities and manage our expense structure diligently.”

The Company is not providing detailed guidance for the first fiscal quarter of 2024 but expects revenues and diluted loss per share to be approximately in line with the prior year. Ardrey stated, “In the first quarter, we will work to stabilize the business. We hope to see momentum build as the year progresses.”

Excluding net revenues, all forward-looking guidance numbers referenced below are non-GAAP. The prior year income statement numbers exclude the previously disclosed charges for goodwill and intangible asset impairment; net inventory and purchase order-related adjustments; severance, retention, and stock-based retirement compensation; consulting and professional fees primarily associated with cost savings initiatives, the CEO search, and strategic initiatives; amortization of definite-lived intangible assets; store and right-of-use asset impairment charges; new CEO sign-on bonus and relocation; and goodMRKT exit costs. Current year guidance excludes any similar charges.

For Fiscal 2024, the Company’s expectations are as follows:

Consolidated net revenues of $490 to $510 million. Net revenues totaled $500.0 million in Fiscal 2023. Both Vera Bradley and Pura Vida revenues are expected to be approximately flat on a year-over-year basis.

A consolidated gross profit percentage of 52.6% to 53.6% compared to 51.4% in Fiscal 2023. The expected year-over-year increase is primarily related to reduced inbound freight expense, partially offset by deleveraged overhead costs related to reduced inventory purchases.

Consolidated SG&A expense of $241 to $251 million compared to $245.3 million in Fiscal 2023. Year-over-year changes in SG&A expense primarily are being driven by restoring short-term and long-term incentive compensation to normal levels, offset by Company-wide cost reduction initiatives.

Consolidated operating income of $17.3 to $21.7 million compared to $12.3 million in Fiscal 2023.

Free cash flow of between $25 and $30 million compared to a cash usage of $21.7 million in Fiscal 2023.

Consolidated diluted EPS of $0.40 to $0.50 based on diluted weighted-average shares outstanding of 31.0 million and an effective tax rate of approximately 28%. Diluted EPS totaled $0.24 last year.

Net capital spending of approximately $5 million compared to $8.2 million in the prior year, reflecting investments associated with new Vera Bradley Factory stores and technology and logistics enhancements.

Disclosure Regarding Non-GAAP Measures

The Company’s management does not, nor does it suggest that investors should, consider the supplemental non-GAAP financial measures in isolation from, or as a substitute for, financial information prepared in accordance with accounting principles generally accepted in the United States (“GAAP”). Further, the non-GAAP measures utilized by the Company may be unique to the Company, as they may be different from non-GAAP measures used by other companies.

The Company believes that the non-GAAP measures presented in this earnings release, including (cash usage) free cash flow; cost of sales; gross profit; selling, general, and administrative expenses; impairment of goodwill and intangible assets; operating (loss) income; net (loss) income; net (loss) income attributable and available to Vera Bradley, Inc.; and diluted net (loss) income per share available to Vera Bradley, Inc. common shareholders, along with the associated percentages of net revenues, are helpful to investors because they allow for a more direct comparison of the Company’s year-over-year performance and are consistent with management’s evaluation of business performance. A reconciliation of the non-GAAP measures to the most directly comparable GAAP measures can be found in the Company’s supplemental schedules included in this earnings release.

Call Information

A conference call to discuss results for the fourth quarter and fiscal year is scheduled for today, Wednesday, March 8, 2023, at 9:30 a.m. Eastern Time. A broadcast of the call will be available via Vera Bradley’s Investor Relations section of its website, www.verabradley.com. Alternatively, interested parties may dial into the call at (888) 204-4368, and enter the access code 3761893. A replay will be available shortly after the conclusion of the call and remain available through March 22, 2023. To access the recording, listeners should dial (844) 512-2921, and enter the access code 3761893.

About Vera Bradley, Inc.

Vera Bradley, Inc. operates two unique lifestyle brands – Vera Bradley and Pura Vida. Vera Bradley and Pura Vida are complementary businesses, both with devoted, emotionally-connected, and multi-generational female customer bases; alignment as casual, comfortable, affordable, and fun brands; positioning as “gifting” and socially-connected brands; strong, entrepreneurial cultures; a keen focus on community, charity, and social consciousness; multi-channel distribution strategies; and talented leadership teams aligned and committed to the long-term success of their brands.

Vera Bradley, based in Fort Wayne, Indiana, is a leading designer of women’s handbags, luggage and other travel items, fashion and home accessories, and unique gifts. Founded in 1982 by friends Barbara Bradley Baekgaard and Patricia R. Miller, the brand is known for its innovative designs, iconic patterns, and brilliant colors that inspire and connect women unlike any other brand in the global marketplace.

In July 2019, Vera Bradley, Inc. acquired a 75% interest in Creative Genius, Inc., which also operates under the name Pura Vida Bracelets (“Pura Vida”). Pura Vida, based in La Jolla, California, is a digitally native, highly-engaging lifestyle brand founded in 2010 by friends Paul Goodman and Griffin Thall. Pura Vida has a differentiated and expanding offering of bracelets, jewelry, and other lifestyle accessories. The Company acquired the remaining 25% of Pura Vida in January 2023, subsequent to the end of Fiscal 2023.

The Company has three reportable segments: Vera Bradley Direct (“VB Direct”), Vera Bradley Indirect (“VB Indirect”), and Pura Vida. The VB Direct business consists of sales of Vera Bradley products through Vera Bradley Full-Line and Factory stores in the United States, www.verabradley.com, www.verabradley.ca, Vera Bradley’s online outlet site, and the Vera Bradley annual outlet sale in Fort Wayne, Indiana. The VB Indirect business consists of sales of Vera Bradley products to approximately 1,700 specialty retail locations throughout the United States, as well as select department stores, national accounts, third party e-commerce sites, and third-party inventory liquidators, and royalties recognized through licensing agreements related to the Vera Bradley brand. The Pura Vida segment consists of sales of Pura Vida products through the Pura Vida websites, www.puravidabracelets.com, www.puravidabracelets.eu, and www.puravidabracelets.ca; through the distribution of its products to wholesale retailers and department stores; and through its Pura Vida retail stores.

Website Information

We routinely post important information for investors on our website www.verabradley.com in the “Investor Relations” section. We intend to use this webpage as a means of disclosing material, non-public information and for complying with our disclosure obligations under Regulation FD. Accordingly, investors should monitor the Investor Relations section of our website, in addition to following our press releases, SEC filings, public conference calls, presentations and webcasts. The information contained on, or that may be accessed through, our webpage is not incorporated by reference into, and is not a part of, this document.

Investors and other interested parties may also access the Company’s most recent Corporate Responsibility and Sustainability Report outlining its ESG (Environmental, Social, and Governance) initiatives at https://verabradley.com/pages/corporate-responsibility.

Vera Bradley Safe Harbor Statement

Certain statements in this release are “forward-looking statements” made pursuant to the safe-harbor provisions of the Private Securities Litigation Reform Act of 1995. Such forward-looking statements reflect the Company’s current expectations or beliefs concerning future events and are subject to various risks and uncertainties that may cause actual results to differ materially from those that we expected, including: possible adverse changes in general economic conditions and their impact on consumer confidence and spending; possible inability to predict and respond in a timely manner to changes in consumer demand; possible loss of key management or design associates or inability to attract and retain the talent required for our business; possible inability to maintain and enhance our brands; possible inability to successfully implement the Company’s long-term strategic plans; possible inability to successfully open new stores, close targeted stores, and/or operate current stores as planned; incremental tariffs or adverse changes in the cost of raw materials and labor used to manufacture our products; possible adverse effects resulting from a significant disruption in our distribution facilities; or business disruption caused by pandemics. Risks, uncertainties, and assumptions also include the possibility that Pura Vida acquisition benefits may not materialize as expected and that Pura Vida’s business may not perform as expected. More information on potential factors that could affect the Company’s financial results is included from time to time in the “Risk Factors” and “Management’s Discussion and Analysis of Financial Condition and Results of Operations” sections of the Company’s public reports filed with the SEC, including the Company’s Form 10-K for the fiscal year ended January 29, 2022. We undertake no obligation to publicly update or revise any forward-looking statement. Financial schedules are attached to this release.

CONTACTS: Investors: Julia Bentley, VP of Investor Relations and Communications jbentley@verabradley.com (260) 207-5116