Original CookieCakeFranchiseExpands Florida Footprint

LOS ANGELES, Aug. 29, 2023 (GLOBE NEWSWIRE) — Great American Cookies, the Original Cookie Cake franchise, announces its return to the Orlando market with a new location. Situated in the Orlando International Premium Outlets, the latest store marks another successful Nestlé® Toll House® Café by Chip® conversion by FAT Brands, the parent company of Great American Cookies. The cookie chain has plans to continue its growth in Orlando with new locations set to open later this year.

“We are beyond excited for Great American Cookies to re-enter the Orlando market and offer our signature Cookie Cakes and Cookies to the community once again,” said Allison Lauenstein, President of the QSR Division at FAT Brands Inc. “Our brand has a rich history of creating memorable moments with our freshly baked CookieCakes, and we can’t wait to continue that tradition in Orlando.”

Since 1977, Great American Cookies has baked up a reputation for not only being the creator of the Original Cookie Cake, but also for its famous chocolate chip cookie recipe. Other craveable menu items include Brownies and Double Doozies™, delectable icing sandwiched between two cookies.

The new Great American Cookies Orlando store is located at 4955 International Dr., Unit 1C 02, Orlando, FL. 32819, and is open Monday through Sunday, 11 a.m. to 8 p.m.

About FAT (Fresh. Authentic. Tasty.) Brands FAT Brands (NASDAQ: FAT) is a leading global franchising company that strategically acquires, markets, and develops fast casual, quick-service, casual dining, and polished casual dining concepts around the world. The Company currently owns 17 restaurant brands: Round Table Pizza, Fatburger, Marble Slab Creamery, Johnny Rockets, Fazoli’s, Twin Peaks, Great American Cookies, Hot Dog on a Stick, Buffalo’s Cafe & Express, Hurricane Grill & Wings, Pretzelmaker, Elevation Burger, Native Grill & Wings, Yalla Mediterranean and Ponderosa and Bonanza Steakhouses, and franchises and owns over 2,300 units worldwide. For more information on FAT Brands, please visit www.fatbrands.com.

About Great American Cookies Founded on a family chocolate chip cookie recipe in 1977, Great American Cookies believes that pure, simple delight is part of living a full life. Serving the Original Cookie Cake, fresh baked cookies in a variety of flavors, brownies, and Double Doozies™, we promise to treat you to bites of bliss that prove how sweet life can be. With 400 bakeries across the country and internationally in Bahrain, Guam, Saudi Arabia, and treats available to ship right to your door, the sweet spot is always close to home. For more information, visit www.greatamericancookies.com.

Joe Gomes, Managing Director, Equity Research Analyst, Generalist , Noble Capital Markets, Inc.

Joshua Zoepfel, Research Associate, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

Raising Price Target. With the shares exceeding our $10 price target, we are raising our target to $12. Our new target is 1.1x our 2023 revenue estimate, up from a prior 1.0x, and still well below the specialty foods peer group average of 2.3x. While we were impressed with the second quarter results, rising milk prices and the potential of consumers trading down in a recessionary environment continue to make us take a more conservative approach to valuation.

Shares Up Solidly YTD. On the heels of record quarterly results, LWAY shares appreciated over 60% since August 11th and are now up 77.8% YTD, compared to a 6.2% YTD rise in the Russell 2000. The last time LWAY shares breached the $10 level was back in 2017.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

Office Depot, Inc., together with its subsidiaries, supplies a range of office products and services. It offers merchandise, such as general office supplies, computer supplies, business machines and related supplies, and office furniture through its chain of office supply stores under the Office Depot, Foray, Ativa, Break Escapes, Worklife, and Christopher Lowell brand names. The company also provides graphic design, printing, reproduction, mailing, shipping, and other services through design, print, and ship centers. It has operations throughout North America, Europe, Asia, and Central America. The company also sells its products and services through direct mail catalogs, contract sales force, Internet sites, and retail stores, through a mix of company-owned operations, joint ventures, licensing and franchise agreements, alliances, and other arrangements. As of December 31, 2008, Office Depot operated 1,267 North American retail division office supply stores and 162 international division retail stores, as well as participated under licensing and merchandise arrangements in 98 stores. The company was founded in 1986 and is based in Boca Raton, Florida.

Joe Gomes, Managing Director, Equity Research Analyst, Generalist , Noble Capital Markets, Inc.

Joshua Zoepfel, Research Associate, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

Initiation. We are initiating research coverage of The ODP Corporation with an Outperform rating and a $65 price target. Not your father’s Office Depot, ODP’s four business unit, low cost operating model will highlight each unit’s strength and value, in our view, while an aggressive share repurchase program returns excess capital to shareholders.

Two Established Cash Flowing Businesses. ODP Business Solutions, a leader in the B2B distribution business, and Office Depot, a leading omnichannel retailer of office supplies, form the foundation, with both businesses generating strong cash flows, with Business Solutions set up for long-term growth.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

Joe Gomes, Managing Director, Equity Research Analyst, Generalist , Noble Capital Markets, Inc.

Joshua Zoepfel, Research Associate, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

Increased Demand for Kefir. Lifeway experienced continued momentum in its kefir products, as the Company had its 15th consecutive quarter of topline growth. Higher volumes of the drinkable kefir along with higher prices continued to benefit Lifeway’s sales, while more favorable milk pricing allowed the Company to generate better gross margin, which improved 1,170 basis points over the previous year.

Great 2Q Results. Lifeway reported sales of $39.2 million, above last year’s $33.5 million and our projection of $37.5 million. Gross margin was 28.7% versus 17.0% in the prior year. Net income for Lifeway was $3.16 million, or diluted EPS of $0.21, compared to $0.12 million, or $0.01, last year. We projected net income of $0.97 million, or EPS of $0.06.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

JERICHO, N.Y.–(BUSINESS WIRE)– 1-800-FLOWERS.COM, Inc. (NASDAQ: FLWS) (the “Company”),a leading provider of gifts designed to help inspire customers to give more, connect more, and build more and better relationships, today announced that the Company will release financial results for its fiscal 2023 fourth quarter and full year on Thursday, August 31, 2023. The press release will be issued prior to market opening and will be followed by a conference call with members of senior management at 8:00 a.m. (ET).

The conference call will be available via live webcast from the Investors section of the Company’s website at 1800flowersinc.com. A recording of the call will be posted on the website within two hours of the call’s completion. A telephonic replay of the call can be accessed beginning at 2:00 p.m. (ET) on August 31, 2023, through September 7, 2023, at: (US) 1-877-344-7529; (Canada) 855-669-9658; (International) 1-412-317-0088; enter conference ID: #7782036.

Special Note Regarding Forward-Looking Statements:

Some of the statements contained in the Company’s scheduled Thursday, August 31, 2023, press release and conference call regarding its results for its fiscal 2023 fourth quarter and full year, other than statements of historical fact, may be forward-looking within the meaning of the Private Securities Litigation Reform Act of 1995. These statements involve risks and uncertainties that could cause actual results to differ materially from those expressed or implied in the applicable statements. For a more detailed description of these and other risk factors, please refer to the Company’s SEC filings including its Annual Reports and Forms 10K and 10Q available at the Investor Relations section of the Company’s website at 1800flowersinc.com. The Company expressly disclaims any intent or obligation to update any of the forward-looking statements made in the scheduled conference call and any recordings thereof, or in any of its SEC filings, except as may be otherwise stated by the Company.

About 1-800-FLOWERS.COM, Inc.

1-800-FLOWERS.COM, Inc. is a leading provider of gifts designed to help inspire customers to give more, connect more, and build more and better relationships. The Company’s e-commerce business platform features an all-star family of brands, including: 1-800-Flowers.com®, 1-800-Baskets.com®, Cheryl’s Cookies®, Harry & David®, PersonalizationMall.com®, Shari’s Berries®, FruitBouquets.com®, Things Remembered®, Moose Munch®, The Popcorn Factory®, Wolferman’s Bakery®, Vital Choice®, and Simply Chocolate®. Through the Celebrations Passport® loyalty program, which provides members with free standard shipping and no service charge across our portfolio of brands, 1-800-FLOWERS.COM, Inc. strives to deepen relationships with customers. The Company also operates BloomNet®, an international floral and gift industry service provider offering a broad-range of products and services designed to help members grow their businesses profitably; Napco℠, a resource for floral gifts and seasonal décor; DesignPac Gifts, LLC, a manufacturer of gift baskets and towers; and Alice’s Table®, a lifestyle business offering fully digital livestreaming and on demand floral, culinary and other experiences to guests across the country. 1-800-FLOWERS.COM, Inc. was recognized among the top 5 on the National Retail Federation’s 2021 Hot 25 Retailers list, which ranks the nation’s fastest-growing retail companies, and was named to the Fortune 1000 list in 2022. Shares in 1-800-FLOWERS.COM, Inc. are traded on the NASDAQ Global Select Market, ticker symbol: FLWS. For more information, visit 1800flowersinc.com or follow @1800FLOWERSInc on Twitter.

ACCO Brands Corporation is one of the world’s largest designers, marketers and manufacturers of branded academic, consumer and business products. Our widely recognized brands include AT-A-GLANCE®, Esselte®, Five Star®, GBC®, Kensington®, Leitz®, Mead®, PowerA®, Quartet®, Rapid®, Rexel®, Swingline®, Tilibra®, and many others. Our products are sold in more than 100 countries around the world. More information about ACCO Brands, the Home of Great Brands Built by Great People, can be found at www.accobrands.com.

Joe Gomes, Managing Director, Equity Research Analyst, Generalist , Noble Capital Markets, Inc.

Joshua Zoepfel, Research Associate, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

Margin Focus Remains. Management remains laser focused on restoring margins. In 2Q23, gross margin improved by 450 basis points and adjusted operating margin improved 220 bp year-over-year. The Company upped its full year gross margin goal to 31%-32% from a prior 30.5%. The longer-term goal is for gross margin to return to the 33%+ level.

Debt Reduction to Pay Dividends. Strong cash flow in 1H23 enabled ACCO to reduce its net leverage ratio to 4.3x at the end of the quarter, with management expecting the ratio to be in the 3.3x-3.5x range, below the old 3.5x-3.7x range, by year end. As debt declines, it positively impacts interest expense, providing additional capital to continue reducing debt levels or invest in the business.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

FORT WAYNE, Ind., Aug. 09, 2023 (GLOBE NEWSWIRE) — Vera Bradley, Inc. (Nasdaq: VRA) (the “Company”) today announced that it plans to report results for the second quarter ended July 29, 2023 at 8:00 a.m. Eastern Time on Wednesday, August 30, 2023.

The Company will host a conference call to discuss its financial results at 9:30 a.m. Eastern Time that same day. A live webcast of the conference call will be available on the Investor Relations section of the Company’s website, www.verabradley.com. Alternatively, interested parties may dial into the call at (888) 394-8218, and enter the access code 1990839. A replay will be available shortly after the conclusion of the call and remain available through September 13, 2023. To access the recording, listeners should dial (844) 512-2921, and enter the access code 1990839.

ABOUT VERA BRADLEY, INC.

Vera Bradley, Inc. operates two unique lifestyle brands – Vera Bradley and Pura Vida. Vera Bradley and Pura Vida are complementary businesses, both with devoted, emotionally connected, and multi-generational female customer bases; alignment as causal, comfortable, affordable, and fun brands; positioning as “gifting” and socially-connected brands; strong, entrepreneurial cultures; a keen focus on community, charity, and social consciousness; multi-channel distribution strategies; and talented leadership teams aligned and committed to the long-term success of their brands.

Vera Bradley, based in Fort Wayne, Indiana, is a leading designer of women’s handbags, luggage and other travel items, fashion and home accessories, and unique gifts. Founded in 1982 by friends Barbara Bradley Baekgaard and Patricia R. Miller, the brand is known for its innovative designs, iconic patterns, and brilliant colors that inspire and connect women unlike any other brand in the global marketplace.

In July 2019, Vera Bradley, Inc. acquired a 75% interest in Creative Genius, Inc., which also operates under the name Pura Vida Bracelets (“Pura Vida”). Pura Vida, based in La Jolla, California, is a digitally native, highly engaging lifestyle brand founded in 2010 by friends Paul Goodman and Griffin Thall. Pura Vida has a differentiated and expanding offering of bracelets, jewelry, and other lifestyle accessories. The Company acquired the remaining 25% of Pura Vida in January 2023.

Operational Excellence and Disciplined Capital Allocation Drive Solid Operating Performance and Strong EPS Growth

Second Quarter Revenue of $1.9 Billion with GAAP EPS of $0.87; Adjusted EPS of $0.99

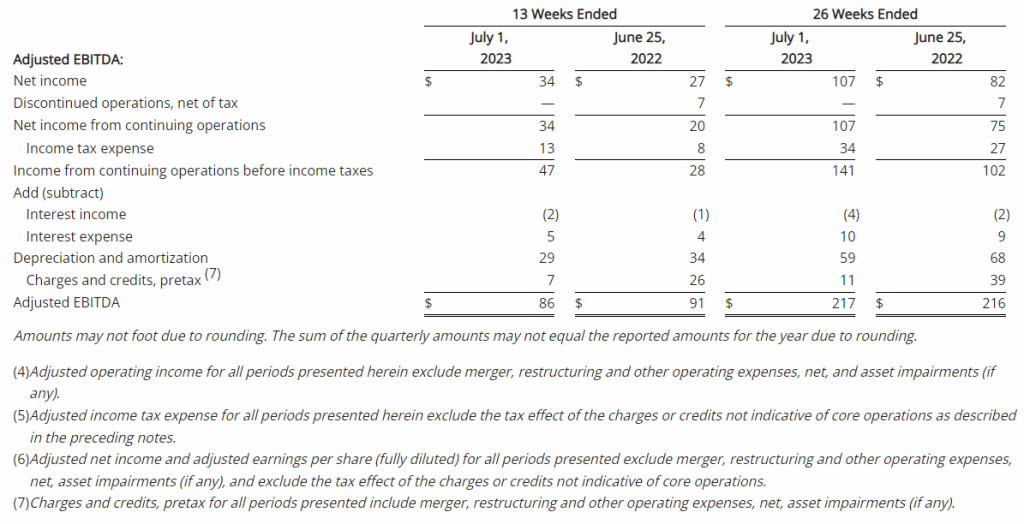

GAAP Operating Income of $46 Million; GAAP Net Income of $34 Million; Adjusted EBITDA of $86 Million

Repurchased $31 Million of Shares in the Second Quarter of 2023

Updates Full-Year 2023 Guidance

BOCA RATON, Fla.–(BUSINESS WIRE)–Aug. 9, 2023– The ODP Corporation (“ODP,” or the “Company”) (NASDAQ:ODP), a leading provider of products, services, and technology solutions to businesses and consumers, today announced results for the second quarter ended July 1, 2023.

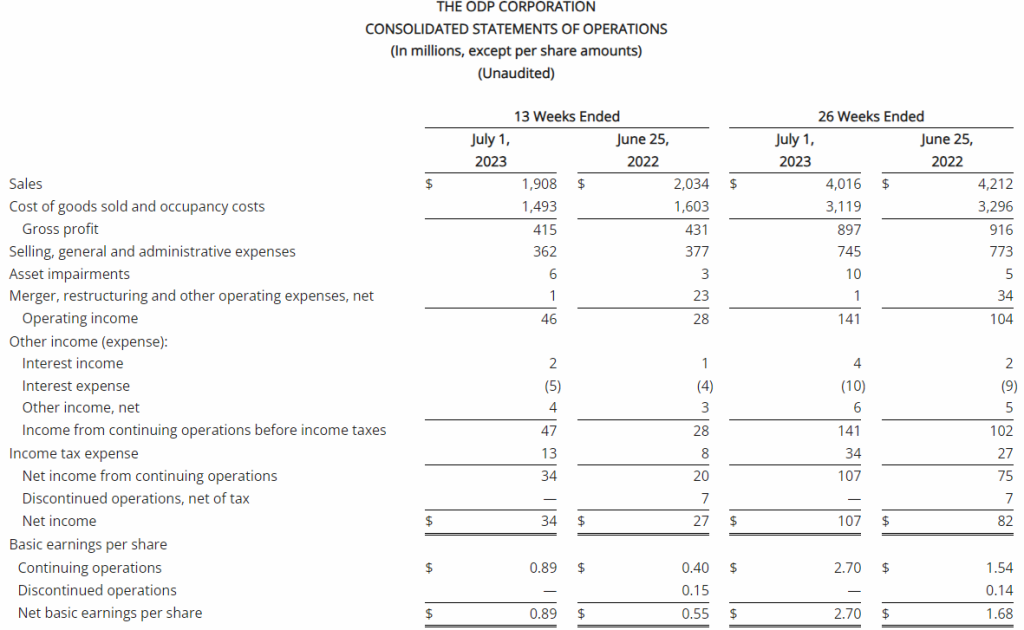

Consolidated (in millions, except per share amounts)

2Q23

2Q22

YTD23

YTD22

Selected GAAP and Non-GAAP measures:

Sales

$1,908

$2,034

$4,016

$4,212

Sales change from prior year period

(6)%

(5)%

Operating income

$46

$28

$141

$104

Adjusted operating income (1)

$53

$54

$152

$143

Net income from continuing operations

$34

$20

$107

$75

Diluted earnings per share from continuing operations

$0.87

$0.39

$2.61

$1.49

Adjusted net income from continuing operations (1)

$39

$39

$114

$104

Adjusted earnings per share from continuing operations (fully diluted)(1)

$0.99

$0.79

$2.80

$2.06

Adjusted EBITDA (1)

$86

$91

$217

$216

Operating Cash Flow from continuing operations

$(8)

$(114)

$149

$(84)

Free Cash Flow(2)

$(31)

$(135)

$97

$(127)

Adjusted Free Cash Flow (3)

$(30)

$(121)

$103

$(106)

Second Quarter 2023 Summary(1)(2)(3)

Total reported sales of $1.9 billion, down 6% versus the prior year, primarily due to lower sales in its Office Depot consumer division, largely driven by 68 fewer retail locations in service compared to the prior year, as well as lower retail and online consumer traffic and transactions

GAAP operating income of $46 million and net income from continuing operations of $34 million, or $0.87 per diluted share, versus $28 million and $20 million, or $0.39 per diluted share, respectively in the prior year

Adjusted operating income of $53 million, compared to $54 million in the second quarter of 2022; adjusted EBITDA of $86 million, compared to $91 million in the second quarter of 2022

Adjusted net income from continuing operations of $39 million, or adjusted diluted earnings per share from continuing operations of $0.99, versus $39 million or $0.79, respectively in the prior year

Operating cash flow from continuing operations of ($8 million) and adjusted free cash flow of ($30 million), versus $(114 million) and $(121 million), respectively in the prior year

Repurchased 724 thousand shares for $31 million in the second quarter of 2023

$1.1 billion of total available liquidity including $335 million in cash and cash equivalents at quarter end

“Our continued focus on operational excellence and disciplined capital allocation drove solid operating results and a strong increase in earnings per share,” said Gerry Smith, chief executive officer of The ODP Corporation. “ODP Business Solutions led the way, expanding its margin profile and driving an impressive year-over-year increase in operating income. Veyer added new third-party business, remaining on-track to more than double external EBITDA in 2023, and Varis continues to onboard customers and incorporate feedback and new features onto its platform. While the weaker macroeconomic environment and somewhat sluggish consumer activity created top-line headwinds in our consumer business during the quarter, Office Depot continued to provide a superior customer experience and we are encouraged by our expanded assortment, which positions us well for the upcoming back-to-school selling season.”

“Combining our solid operating performance with our continued disciplined capital allocation, which included repurchasing about $31 million of our shares in the quarter, we drove an impressive 25% year-over-year increase in adjusted earnings per share in the second quarter,” Smith continued.

“Our low-cost business model, multiple routes to market, and strong balance sheet have us well positioned to continue navigating the ongoing challenging macroeconomic conditions. Moving ahead, we will continue to drive operational excellence across our four business units and prioritize capital allocation, remaining squarely focused on driving value for our shareholders,” Smith concluded.

Consolidated Results

Reported (GAAP) Results

Total reported sales for the second quarter of 2023 were $1.9 billion, a decrease of 6% compared with the same period last year. This was driven primarily by lower sales in its consumer division, Office Depot, primarily due to 68 fewer stores in service compared to last year related to planned store closures, as well as lower retail and online consumer traffic. Sales at ODP Business Solutions Division were flat year over year, as increases in sales for paper and certain adjacency categories, and flexible pricing strategies, were largely offset by lower sales in product categories including ink, toner, office supplies and personal protective equipment. Additionally, Veyer provided strong logistics support for the ODP Business Solutions and Office Depot Divisions, and began to capture additional demand for its supply chain and procurement solutions among other third-party customers.

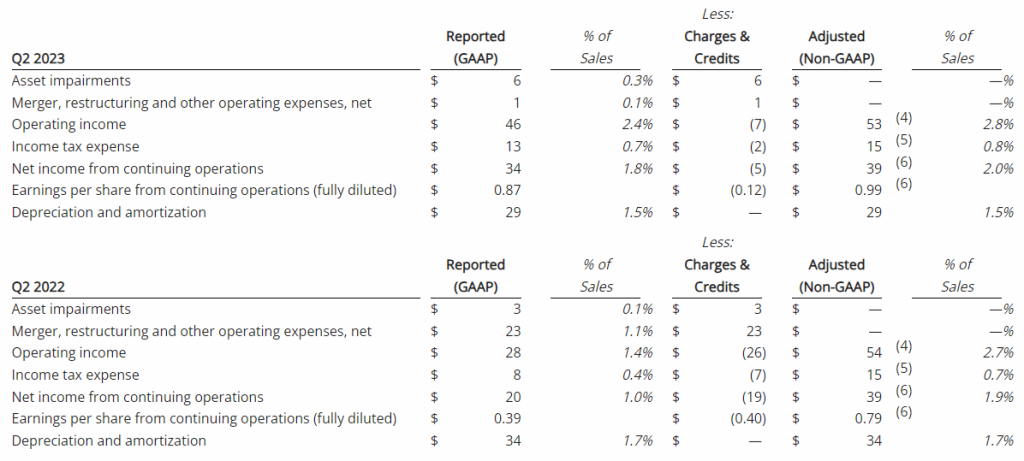

The Company reported operating income of $46 million in the second quarter of 2023, up 64% compared to operating income of $28 million in the prior year period. Operating results in the second quarter of 2023 included $7 million of charges. These charges consisted primarily of $6 million associated with non-cash asset impairments largely related to the operating lease right-of-use (ROU) assets associated with the Company’s retail store locations. Net income from continuing operations was $34 million, or $0.87 per diluted share in the second quarter of 2023, up from $20 million, or $0.39 per diluted share in the second quarter of 2022.

Adjusted (non-GAAP) Results(1)

Adjusted results for the second quarter of 2023 exclude charges and credits totaling $7 million as described above and the associated tax impacts.

Second quarter of 2023 adjusted EBITDA was $86 million compared to $91 million in the prior year period. This included depreciation and amortization of $29 million and $34 million in the second quarters of 2023 and 2022, respectively

Second quarter of 2023 adjusted operating income was $53 million compared to $54 million in the second quarter of 2022

Second quarter of 2023 adjusted net income from continuing operations was $39 million, or $0.99 per diluted share, compared to $39 million, or $0.79 per diluted share, in the second quarter of 2022, an increase of 25% on a per share basis

Division Results

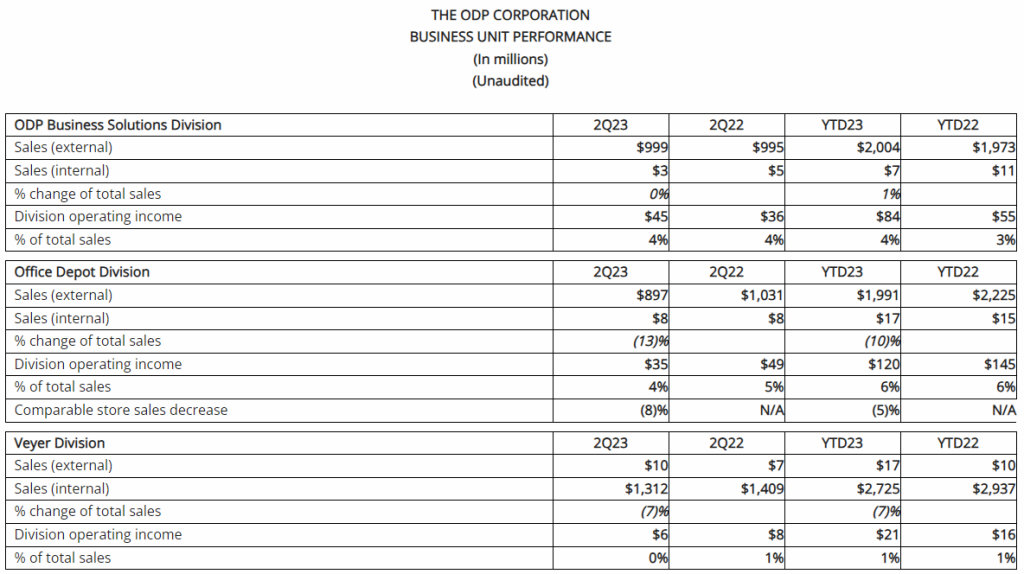

ODP Business Solutions Division

Leading B2B distribution solutions provider serving small, medium and enterprise level companies with an annual trailing-twelve-month revenue in excess of $4 billion

Reported sales were $1.0 billion in the second quarter of 2023, flat compared to the same period last year, as return to the office trends and flexible pricing strategies were offset by higher levels of unemployment and other macroeconomic factors

Drove strong sales in paper and adjacency categories, including furniture, cleaning and breakroom supplies, and copy and print services

Total adjacency category sales, including cleaning and breakroom, furniture, technology, and copy and print, were 44% of total ODP Business Solutions’ sales

Continued strong pipeline and signed renewed business in excess of $100 million in customer agreements

Operating income was $45 million in the second quarter of 2023, up 25% over the same period last year, related primarily to higher gross margins. As a percentage of sales, operating income margin was 4.5%, up 100 basis points compared to the same period last year

Office Depot Division

Leading provider of retail consumer and small business products and services distributed via Office Depot and OfficeMax retail locations and an award-winning eCommerce presence

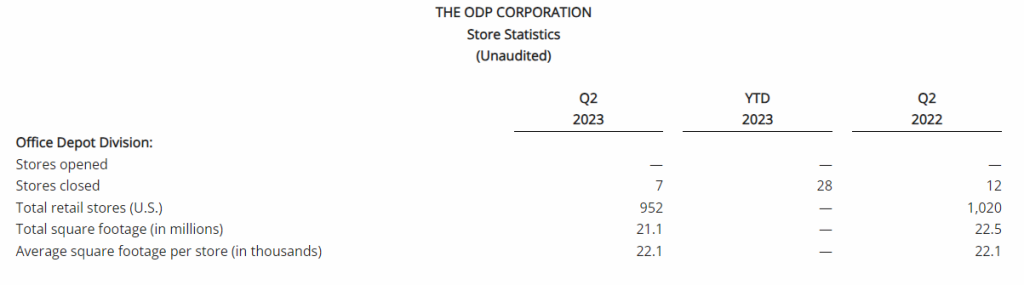

Reported sales were $0.9 billion in the second quarter of 2023, down 13% compared to the prior year period partially due to 68 fewer retail outlets in service associated with planned store closures, as well as lower demand relative to last year in certain product categories and lower online sales. The Company closed 7 retail stores in the quarter and had 952 stores at quarter end. Sales were down approximately 8% on a comparable store basis

Store traffic and demand relative to last year was negatively impacted by the recovery from the pandemic as a greater percentage of customers returned to the office, as well as weaker macroeconomic activity and higher unemployment

Operating income was $35 million in the second quarter of 2023, compared to operating income of $49 million during the same period last year. As a percentage of sales, operating income was 4%, or down approximately 90 basis points compared to the same period last year. This result was primarily driven by the flow through impact from lower sales and impacts related to inflation

Veyer Division

Veyer is a supply chain, distribution, procurement and global sourcing operation, supporting Office Depot and ODP Business Solutions, as well as other third-party customers. Assets and capabilities of Veyer include approximately 9 million square feet of infrastructure; ~100 facilities (distribution centers, cross-docks, and direct import centers); a large private fleet of vehicles; and next-day delivery to 98.5% of US population

In the second quarter of 2023, Veyer provided strong support for its internal customers, ODP Business Solutions and Office Depot, as well as for its third-party customers, generating sales of $1.3 billion

Operating income was $6 million in the second quarter of 2023, down from $8 million in the prior year period related to lower sales in Office Depot

In the quarter relative to last year, sales and EBITDA generated from third party customers was up nearly 62% and over 141%, respectively, resulting in sales of approximately $10 million and EBITDA of $3 million in the quarter

Varis Division

Varis is a tech-enabled B2B indirect procurement marketplace launched in the fourth quarter of 2022, which provides buyers and suppliers a seamless way to transact through the platform’s consumer-like buying experience and advanced spend management tools

Successfully launched the platform in the fourth quarter of 2022; onboarding new customers, incorporating feedback, and adding new features to the platform

Varis generated revenues in the quarter of $2 million, an increase of $1 million compared to the second quarter of 2022

Operating loss was $14 million, compared to an operating loss of $16 million in the second quarter of 2022, primarily driven by lower employee related costs and as the division continued to invest in its business and worked to onboard customers

Share Repurchases

The Company continued to execute under its previously announced $1 billion share repurchase authorization, available through year-end 2025. During the second quarter of 2023, the Company repurchased 724 thousand shares for $31 million. Since the inception of the authorization beginning in November 2022, the Company has repurchased approximately 8.3 million shares for $387 million.

The number of shares to be repurchased in the future and the timing of such transactions will depend on a variety of factors, including market conditions, regulatory requirements, and other corporate considerations. The current authorization could be suspended or discontinued at any time as determined by the Board of Directors.

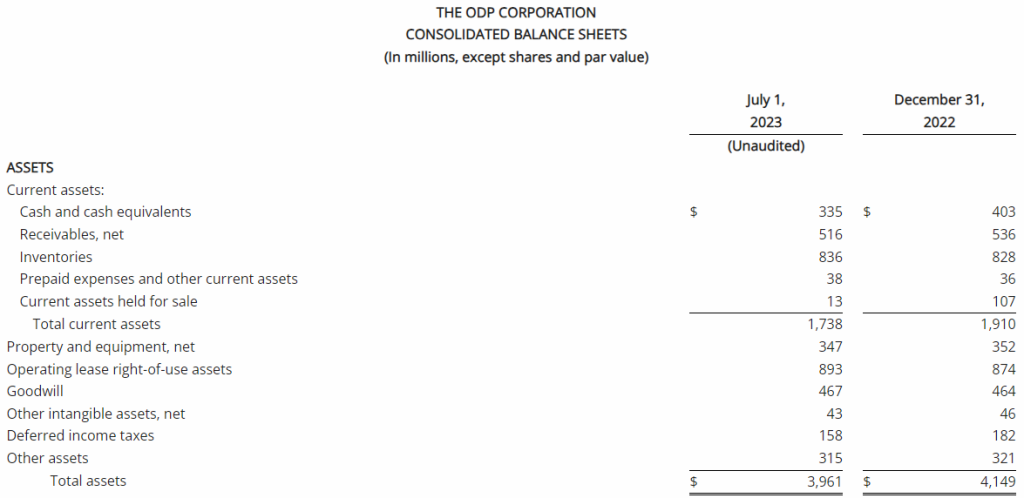

Balance Sheet and Cash Flow

As of July 1, 2023, ODP had total available liquidity of approximately $1.1 billion, consisting of $335 million in cash and cash equivalents and $811 million of available credit under the Third Amended Credit Agreement. Total debt was $181 million.

For the second quarter of 2023, cash used by operating activities of continuing operations was $8 million, which included $1 million in restructuring and other spend, compared to cash used by operating activities of continuing operations of $114 million in the second quarter of the prior year, which included $14 million in restructuring and other spend. The year-over-year improvement in operating cash flow largely related to stronger operating results, prudent inventory management, and timing of certain working capital items.

Capital expenditures in the second quarter of 2023 were $23 million versus $21 million in the prior year period, reflecting continuing growth investments in the Company’s digital transformation, distribution network, and eCommerce capabilities. Adjusted Free Cash outflow(3) was $30 million in the second quarter of 2023, a significant improvement compared to $121 million outflow in the prior year period.

“I would like to thank our entire team for their continued efforts on carefully managing inventory and other working capital items, which resulted in significantly stronger year-over-year cash flow in the quarter,” said Anthony Scaglione, executive vice president and chief financial officer of The ODP Corporation. “As we move into the second half of the year, we will maintain our disciplined approach and focus on managing operating costs, maximizing cash flow in our business, and optimizing our capital allocation plan,” Scaglione added.

Updated 2023 Expectations

“We remain cautiously optimistic about the second half of the year and are excited about the opportunity to continue driving operational excellence and delivering strong value for our shareholders,” said Smith. “While we recognize that the challenging macroeconomic environment is causing somewhat sluggish consumer activity and market disruptions, we’re enthusiastic about our strong position and are focused on driving the assets we control to deliver long-term profitable growth. Through executing along our three horizons strategy, driving our four business unit model, and remaining focused on prudently deploying capital to maximize shareholder value, we’re on a path to unlocking ODP’s potential, creating a compelling value proposition for all of our stakeholders.”

The Company’s full year guidance for 2023 included in this release includes non-GAAP measures, such as adjusted EBITDA, Adjusted Operating Income, Adjusted Earnings per Share and Adjusted Free Cash Flow. These measures exclude charges or credits not indicative of core operations, which may include but not be limited to merger integration expenses, restructuring charges, acquisition-related costs, executive transition costs, asset impairments and other significant items that currently cannot be predicted without unreasonable efforts. The exact amount of these charges or credits are not currently determinable but may be significant. Accordingly, the Company is unable to provide equivalent GAAP measures or reconciliations from GAAP to non-GAAP for these financial measures without unreasonable effort.

The Company is updating its full year guidance for 2023 as follows:

Previous 2023 Guidance

Updated 2023 Guidance

Sales

$8.0 – $8.4 billion

Revised to approximately $8 billion

Adjusted EBITDA

$400 – $430 million

Affirmed

Adjusted Operating Income

$270 – $300 million

Affirmed

Adjusted Earnings per Share(*)

$4.50 – $5.10 per share

Revised to $5.00 – $5.30 per share

Adjusted Free Cash Flow(**)

$200 – $230 million

Affirmed

Capital Expenditures

$100 – $120 million

Affirmed

*Adjusted Earnings per Share (EPS) guidance for 2023 excludes potential discrete (tax) items that may affect quarter to quarter fluctuations and includes expected impact from share repurchases

**Adjusted Free Cash Flow is defined as cash flows from operating activities less capital expenditures excluding cash charges associated with the Company’s Maximize B2B Restructuring and expenses incurred in connection with our previously planned separation of the consumer business and re-alignment

“We delivered solid performance in the first half of the year and remain in a strong capital position with our low-cost business model mindset,” said Scaglione. “While we’re cautious on the state of the consumer and general macroeconomic conditions, our continued focus on operational excellence has us well positioned to continue driving solid results for the balance of the year. Our updated guidance assumes stabilization in overall economic trends in the second half of 2023 and reflects our expectations for revenue trends given first half performance, confirming the low end of our previous full-year revenue guidance range, while reaffirming all other operating metrics and increasing our earnings per share guidance given our strong performance to date, lower than expected interest and tax expense, and continued share buyback activity,” Scaglione added.

The ODP Corporation will webcast a call with financial analysts and investors on August 9, 2023, at 9:00 am Eastern Time, which will be accessible to the media and the general public. To listen to the conference call via webcast, please visit The ODP Corporation’s Investor Relations website at investor.theodpcorp.com. A replay of the webcast will be available approximately two hours following the event.

(1)

As presented throughout this release, adjusted results represent non-GAAP financial measures and exclude charges or credits not indicative of core operations and the tax effect of these items, which may include but not be limited to merger integration, restructuring, acquisition costs, and asset impairments. Reconciliations from GAAP to non-GAAP financial measures can be found in this release as well as on the Company’s Investor Relations website at investor.theodpcorp.com.

(2)

As used in this release, Free Cash Flow is defined as cash flows from operating activities less capital expenditures. Free Cash Flow is a non-GAAP financial measure and reconciliations from GAAP financial measures can be found in this release as well as on the Company’s Investor Relations website at investor.theodpcorp.com.

(3)

As used in this release, Adjusted Free Cash Flow is defined as Free Cash Flow excluding cash charges associated with the Company’s Maximize B2B Restructuring, and expenses incurred in connection with our previously planned separation of the consumer business and re-alignment. Adjusted Free Cash Flow is a non-GAAP financial measure and reconciliations from GAAP financial measures can be found in this release as well as on the Company’s Investor Relations website at investor.theodpcorp.com.

About The ODP Corporation

The ODP Corporation (NASDAQ:ODP) is a leading provider of products, services, and technology solutions through an integrated business-to-business (B2B) distribution platform and omni-channel presence, which includes world-class supply chain and distribution operations, dedicated sales professionals, a B2B digital procurement solution, online presence, and a network of Office Depot and OfficeMax retail stores. Through its operating companies Office Depot, LLC; ODP Business Solutions, LLC; Veyer, LLC; and Varis, Inc, The ODP Corporation empowers every business, professional, and consumer to achieve more every day. For more information, visit theodpcorp.com.

This communication may contain forward-looking statements within the meaning of the Private Securities Litigation Reform Act of 1995. These statements or disclosures may discuss goals, intentions and expectations as to future trends, plans, events, results of operations, cash flow or financial condition, the potential impacts on our business due to the unknown severity and duration of the COVID-19 pandemic, or state other information relating to, among other things, the Company, based on current beliefs and assumptions made by, and information currently available to, management. Forward-looking statements generally will be accompanied by words such as “anticipate,” “believe,” “plan,” “could,” “estimate,” “expect,” “forecast,” “guidance,” “expectations”, “outlook,” “intend,” “may,” “possible,” “potential,” “predict,” “project,” “propose” or other similar words, phrases or expressions, or other variations of such words. These forward-looking statements are subject to various risks and uncertainties, many of which are outside of the Company’s control. There can be no assurances that the Company will realize these expectations or that these beliefs will prove correct, and therefore investors and stakeholders should not place undue reliance on such statements.

Factors that could cause actual results to differ materially from those in the forward-looking statements include, among other things, highly competitive office products market and failure to differentiate the Company from other office supply resellers or respond to decline in general office supplies sales or to shifting consumer demands; competitive pressures on the Company’s sales and pricing; the risk that the Company is unable to transform the business into a service-driven, B2B platform that such a strategy will not result in the benefits anticipated; the risk that the Company will not be able to achieve the expected benefits of its strategic plans, including its strategic shift to maintain all of its businesses under common ownership; the risk that the Company may not be able to realize the anticipated benefits of acquisitions due to unforeseen liabilities, future capital expenditures, expenses, indebtedness and the unanticipated loss of key customers or the inability to achieve expected revenues, synergies, cost savings or financial performance; the risk that the Company is unable to successfully maintain a relevant omni-channel experience for its customers; the risk that the Company is unable to execute the Maximize B2B Restructuring Plan successfully or that such plan will not result in the benefits anticipated; failure to effectively manage the Company’s real estate portfolio; loss of business with government entities, purchasing consortiums, and sole- or limited- source distribution arrangements; failure to attract and retain qualified personnel, including employees in stores, service centers, distribution centers, field and corporate offices and executive management, and the inability to keep supply of skills and resources in balance with customer demand; failure to execute effective advertising efforts and maintain the Company’s reputation and brand at a high level; disruptions in computer systems, including delivery of technology services; breach of information technology systems affecting reputation, business partner and customer relationships and operations and resulting in high costs and lost revenue; unanticipated downturns in business relationships with customers or terms with the suppliers, third-party vendors and business partners; disruption of global sourcing activities, evolving foreign trade policy (including tariffs imposed on certain foreign made goods); exclusive Office Depot branded products are subject to additional product, supply chain and legal risks; product safety and quality concerns of manufacturers’ branded products and services and Office Depot private branded products; covenants in the credit facility; general disruption in the credit markets; incurrence of significant impairment charges; retained responsibility for liabilities of acquired companies; fluctuation in quarterly operating results due to seasonality of the Company’s business; changes in tax laws in jurisdictions where the Company operates; increases in wage and benefit costs and changes in labor regulations; changes in the regulatory environment, legal compliance risks and violations of the U.S. Foreign Corrupt Practices Act and other worldwide anti-bribery laws; volatility in the Company’s common stock price; changes in or the elimination of the payment of cash dividends on Company common stock; macroeconomic conditions such as higher interest rates and future declines in business or consumer spending; increases in fuel and other commodity prices and the cost of material, energy and other production costs, or unexpected costs that cannot be recouped in product pricing; unexpected claims, charges, litigation, dispute resolutions or settlement expenses; catastrophic events, including the impact of weather events on the Company’s business; the discouragement of lawsuits by shareholders against the Company and its directors and officers as a result of the exclusive forum selection of the Court of Chancery, the federal district court for the District of Delaware or other Delaware state courts by the Company as the sole and exclusive forum for such lawsuits; and the impact of the COVID-19 pandemic on the Company’s business. The foregoing list of factors is not exhaustive. Investors and shareholders should carefully consider the foregoing factors and the other risks and uncertainties described in the Company’s Annual Reports on Form 10-K, Quarterly Reports on Form 10-Q, and Current Reports on Form 8-K filed with the U.S. Securities and Exchange Commission. The Company does not assume any obligation to update or revise any forward-looking statements.

THE ODP CORPORATION GAAP to Non-GAAP Reconciliations (Unaudited)

We report our results in accordance with accounting principles generally accepted in the United States (“GAAP”). We also review certain financial measures excluding impacts of transactions that are not related to our core operations (“non-GAAP”). Management believes that the presentation of these non-GAAP financial measures enhances the ability of its investors to analyze trends in its business and provides a means to compare periods that may be affected by various items that might obscure trends or developments in its business. Management uses both GAAP and non-GAAP measures to assist in making business decisions and assessing overall performance. Non-GAAP measures help to evaluate programs and activities that are intended to attract and satisfy customers, separate from expenses and credits directly associated with Merger, restructuring, and certain similar items. Certain non-GAAP measures are also used for short and long-term incentive programs.

Our measurement of these non-GAAP financial measures may be different from similarly titled financial measures used by others and therefore may not be comparable. These non-GAAP financial measures should not be considered superior to the GAAP measures, but only to clarify some information and assist the reader. We have included reconciliations of this information to the most comparable GAAP measures in the tables included within this material.

Free cash flow is a non-GAAP measure, which we define as cash flows from operating activities less capital expenditures. We believe that free cash flow is an important indicator that provides additional perspective on our ability to generate cash to fund our strategy and expand our distribution network. Adjusted free cash flow is also a non-GAAP measure, which we define as free cash flow excluding cash charges associated with the Company’s Maximize B2B Restructuring, and the previously planned separation of the consumer business and re-alignment.

President and Chief Operating Officer Thomas Tedford Appointed Chief Executive Officer Effective October 1, 2023; Boris Elisman to Continue as Executive Chairman Before Retiring in the first half of 2024

LAKE ZURICH, Ill,–(BUSINESS WIRE)– ACCO Brands Corporation (NYSE: ACCO) (the “Company” or “ACCO Brands”), one of the world’s largest suppliers of select categories of branded academic, consumer and business products, today announced its Board of Directors has appointed the Company’s President and Chief Operating Officer, Thomas Tedford, as CEO effective October 1, 2023. Mr. Tedford has also been elected a member of the board effective that date. Mr. Tedford will succeed ACCO Brands current CEO, Boris Elisman, who will continue as Executive Chairman until his retirement in the first half of 2024. He has notified the Board that he will not stand for reelection at the 2024 stockholders’ meeting.

“The appointment of Tom as ACCO Brands next CEO is part of a succession plan that Boris and the Board have been preparing over the past few years,” stated Lead Independent Director, Thomas Kroeger. “We have worked closely with Tom and have full confidence in his commitment to creating value for our shareholders. He brings deep knowledge of our industry, our customers, the overall Company, and its operating segments to his new role. Tom has worked closely with Boris and the Board in developing and executing on the Company’s strategic transformation and will continue to do so, assuring a smooth and seamless transition of leadership and positioning us for profitable growth.”

“On behalf of everyone at ACCO Brands, we would like to thank Boris for his exemplary leadership and dedicated service as CEO. Boris’s innumerable contributions during his 18-year tenure, the last 10 leading the Company as CEO, have successfully expanded the growth opportunities for the Company,” Mr. Kroger concluded.

Mr. Elisman said, “During my tenure at ACCO Brands, the Company and the industry have undergone significant changes and I am proud of our teams’ accomplishments during this period. Having worked closely with Tom for many years, I know the company is in great hands to continue to progress and accelerate profitable growth. It has been my privilege to lead this great company, and I look forward to continuing to serve as Executive Chairman to ensure a smooth transition.”

Mr. Tedford commented, “It is an honor to have the opportunity to lead ACCO Brands and our talented team of dedicated employees as we build upon the current momentum in our business. Boris has been a great mentor and a tremendous leader. I have worked with him for more than a decade and appreciate his leadership and bold actions to transform ACCO Brands. I look forward to continuing to work closely with Boris to complete this leadership transition.”

“I am grateful for the support of our Board of Directors and am excited to work with them and our executive leadership team. I believe there are immense opportunities to enhance our leadership position in key categories, grow through share gains and new innovative product solutions, optimize our supply chain, and improve our margin profile as we remain focused on delivering shareholder value and customer satisfaction. Near-term we are committed to prioritizing our free cash flow towards supporting our dividend and debt reduction,” added Mr. Tedford.

Thomas Tedford Bio

Mr. Tedford joined ACCO Brands in 2010 and was named President and Chief Operating Officer in 2021. From 2011 to 2021, Mr. Tedford served first as Executive Vice President and President of ACCO Brands Americas ultimately becoming Executive Vice President and President, ACCO Brands, North America. During his tenure, he successfully led the operational, cultural and leadership integrations of key strategic acquisitions, the introduction of new products and the development of new markets. Prior to joining ACCO Brands, Mr. Tedford had 15 years of progressive sales, sales leadership, marketing, operational and executive management experience, operating in highly competitive and demanding industries. Mr. Tedford has expertise addressing complex challenges, optimizing performance, developing growth strategies, innovating product solutions, and building high-performing teams.

About ACCO Brands Corporation

ACCO Brands, the Home of Great Brands Built by Great People, designs, manufactures and markets consumer and end-user products that help people work, learn, play, and thrive. Our widely recognized brands include AT-A-GLANCE®, Five Star®, Kensington®, Leitz®, Mead®, PowerA®, Swingline®, Tilibra® and many others. More information about ACCO Brands Corporation (NYSE: ACCO) can be found at www.accobrands.com.

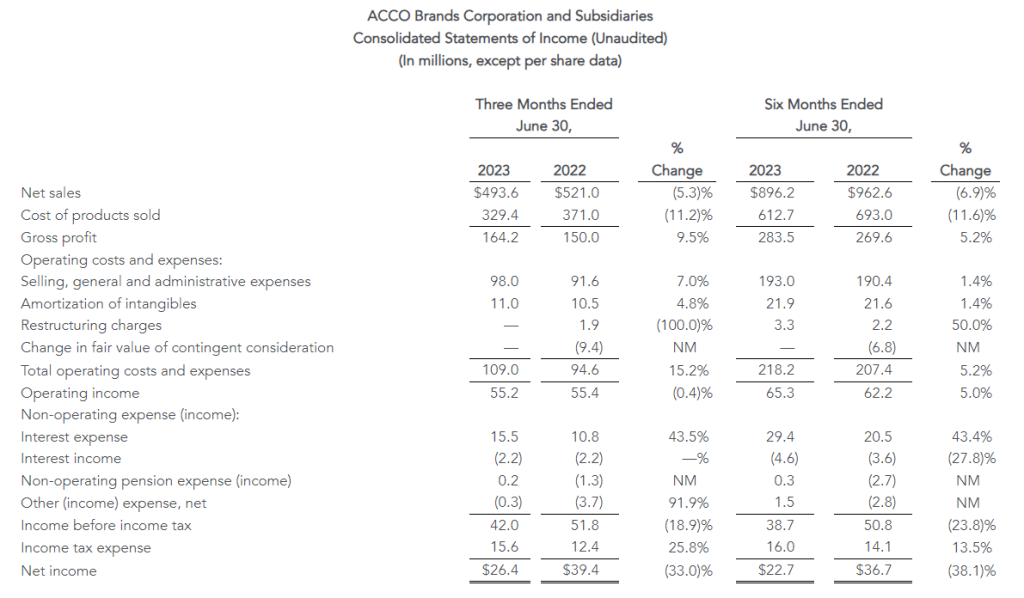

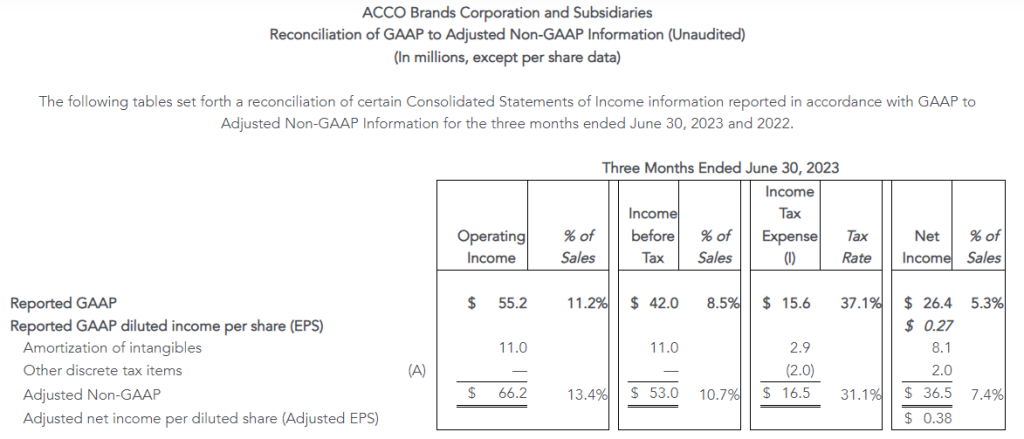

Reported net sales of $494 million, with gross margin expanding 450 basis points

Operating income of $55 million, flat to prior year; adjusted operating income of $66 million grew 14% year over year

EPS of $0.27; adjusted EPS of $0.38, above Company’s outlook

Net operating cash outflow improved $59 million year to date driven by improved working capital management

Maintains full year 2023 adjusted EPS outlook of $1.08 to $1.12

Raises full year 2023 free cash flow outlook to at least $110 million

Lowered end of year consolidated leverage ratio outlook

August 08, 2023 04:00 PM Eastern Daylight Time

LAKE ZURICH, Ill.–(BUSINESS WIRE)–ACCO Brands Corporation (NYSE: ACCO) today announced its second quarter and first six-month results for the period ended June 30, 2023.

“Our top priority entering 2023 was to restore our margin profile, and I’m pleased to report that we have made great progress on that front in the first half. Second quarter and year-to-date gross margin expanded 450 and 360 basis points, respectively, due to greater traction from our pricing, productivity and restructuring initiatives. This has yielded much better than expected adjusted EPS. The higher operating profits experienced through the first six months give us confidence in our full year 2023 outlook for adjusted EPS and free cash flow. While we are pleased with the strong start of the year, we are more cautious on the second half demand environment. With improved working capital management, we are well positioned to end the year with a lower leverage ratio than previously expected. We remain committed to supporting our quarterly dividend and reducing debt with our strong cash flow” said Boris Elisman, Chairman and Chief Executive Officer of ACCO Brands.

“Our results reflect the resilience of our brands and the transformative actions undertaken to expand our product categories, broaden our geographic reach, bring innovative new consumer-centric products to market and streamline our cost structure. We remain confident that our strategy has us positioned to deliver sustainable organic growth as global economies improve,” concluded Mr. Elisman.

Second Quarter Results

Net sales declined 5.3 percent to $493.6 million from $521.0 million in 2022. Adverse foreign exchange reduced sales by $0.8 million, or 0.2 percent. Comparable sales fell 5.1 percent. Both reported and comparable sales declines were due to reduced volume, reflecting a more challenging macroeconomic environment, especially in our EMEA segment, and weaker global sales of computer accessories.

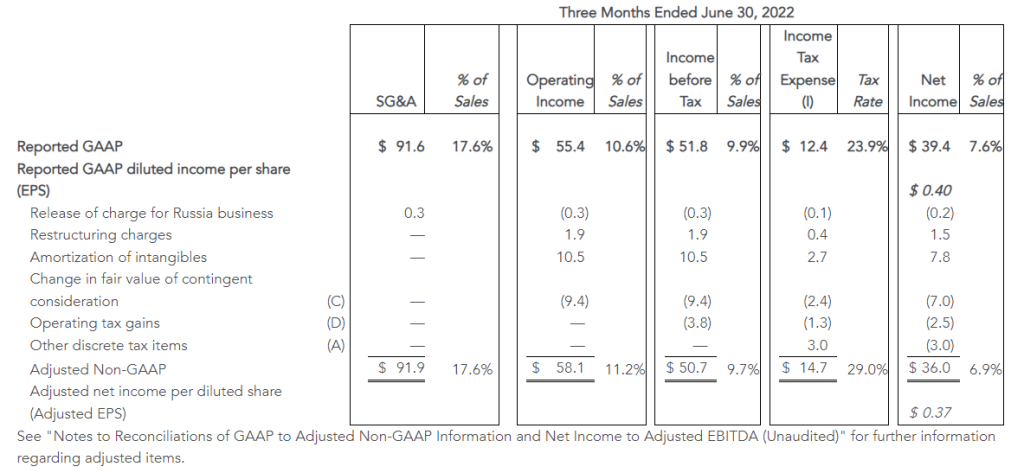

Operating income was $55.2 million versus $55.4 million in 2022. In 2022, operating income benefitted from income related to a change in the value of the PowerA contingent earnout of $9.4 million, partially offset by $1.9 million in restructuring charges. Adjusted operating income increased 14 percent to $66.2 million from $58.1 million in the prior year. This increase reflects improved gross margin from the effect of cumulative global pricing and cost reduction actions, partially offset by negative fixed cost leverage and higher SG&A expense primarily due to an increase in incentive compensation.

The Company reported net income of $26.4 million, or $0.27 per share, compared with prior year net income of $39.4 million, or $0.40 per share. Reported net income in 2023 reflects higher interest, tax and non-operating pension expenses. Reported net income in 2022 benefited from the items noted above in operating income. Adjusted net income was $36.5 million, or $0.38 per share, compared with $36.0 million, or $0.37 per share in 2022. Adjusted net income reflects the increase in adjusted operating income, partially offset by higher interest and non-operating pension expenses.

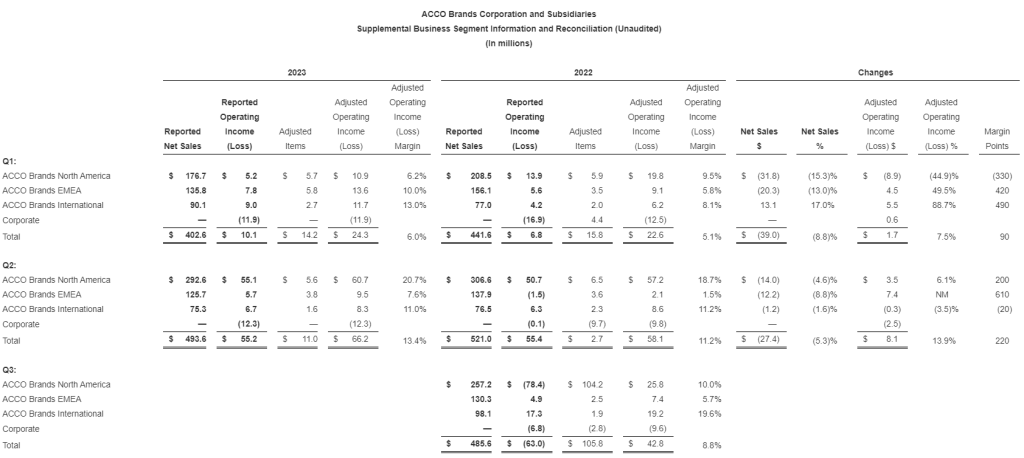

Business Segment Results

ACCO Brands North America – Secondquarter segment net sales of $292.6 million decreased 4.6 percent versus the prior year. Adverse foreign exchange reduced sales by 0.5 percent. Comparable sales of $294.2 million were down 4.1 percent. Both decreases reflect softer demand from business and retail customers due to a weaker macroeconomic environment and lower volumes for computer accessories. These factors more than offset stronger pricing, and volume growth in gaming accessories. Timing for some back-to-school sales was earlier than anticipated.

Second quarter operating income in North America was $55.1 million versus $50.7 million a year earlier, and adjusted operating income was $60.7 million compared to $57.2 million a year ago. Both increases reflect the benefit of pricing and cost actions and favorable mix, which more than offset the impact of lower sales and negative fixed cost leverage.

ACCO Brands EMEA – Secondquarter segment net sales of $125.7 million decreased 8.8 percent versus the prior year. Favorable foreign exchange increased sales by 0.3 percent. Comparable sales of $125.3 million decreased 9.1 percent versus the prior-year period. Both reported and comparable sales declines reflect reduced demand due to a weaker environment in the region and lower volumes for technology accessories. This more than offset the effect of cumulative pricing actions.

Second quarter operating income in EMEA was $5.7 million versus a loss of $1.5 million a year earlier, and adjusted operating income was $9.5 million compared to $2.1 million a year ago. The increases in both reported operating income and adjusted operating income reflect improved gross margins from the cumulative effect of price increases and cost savings actions more than offsetting negative fixed cost leverage.

ACCO Brands International – Secondquarter segment sales of $75.3 million decreased 1.6 percent versus the prior year. Favorable foreign exchange increased sales by 0.7 percent. Comparable sales of $74.8 million decreased 2.3 percent versus the year-ago period. Both sales decreases reflect lower volumes due to weaker economies in Asia and Australia, mostly offset by growth in Latin America.

Second quarter operating income in the International segment was $6.7 million versus $6.3 million a year earlier, with the increase due to lower restructuring expense. Adjusted operating income was $8.3 million compared to $8.6 million a year ago.

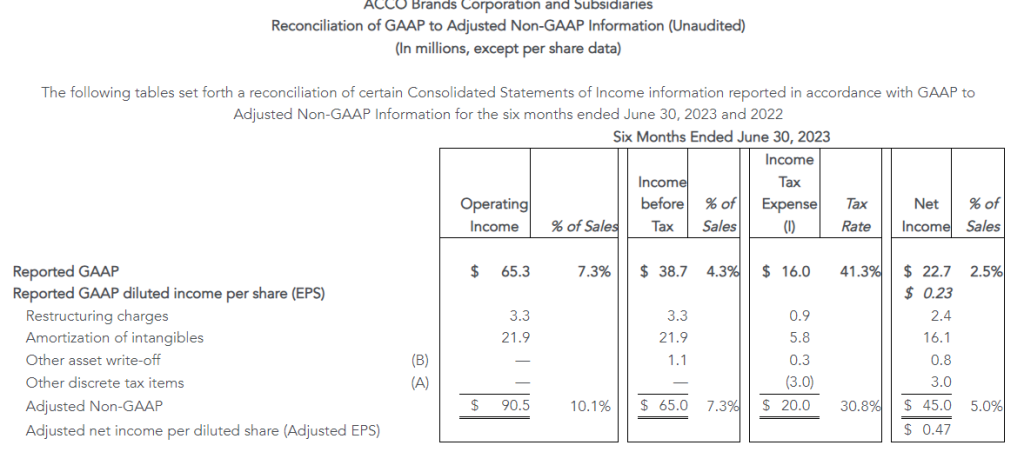

Six Month Results

Net sales decreased 6.9 percent to $896.2 million from $962.6 million in 2022. Adverse foreign exchange reduced sales by $11.4 million, or 1.2 percent. Comparable sales decreased 5.7 percent. Both reported and comparable sales declines reflect lower volume, especially in EMEA and North America due to the challenging macroeconomic environment, lower sales of technology accessories, and the timing of back-to-school shipments and lower channel inventory compared to a year ago. These more than offset the benefit of price increases across all segments, and volume growth in Latin America.

Operating income of $65.3 million compares to operating income of $62.2 million in 2022, which included a benefit of $6.8 million related to a change in the value of the PowerA contingent earnout. Adjusted operating income of $90.5 million increased from $80.7 million last year. Both reported and adjusted operating income increases reflect the benefit of global price increases and cost reduction initiatives, partially offset by higher SG&A expense primarily due to increased incentive compensation.

Net income was $22.7 million, or $0.23 per share, compared with net income of $36.7 million, or $0.37 per share, in 2022. Reported net income in 2023 reflects higher interest, tax and non-operating pension expenses. Reported net income in 2022 benefitted from the items noted above in operating income. Adjusted net income was $45.0 million, compared with $46.4 million in 2022, and adjusted earnings per share were $0.47 for both year periods. Adjusted net income reflects the increase in adjusted operating income offset by higher interest and non-operating pension expenses.

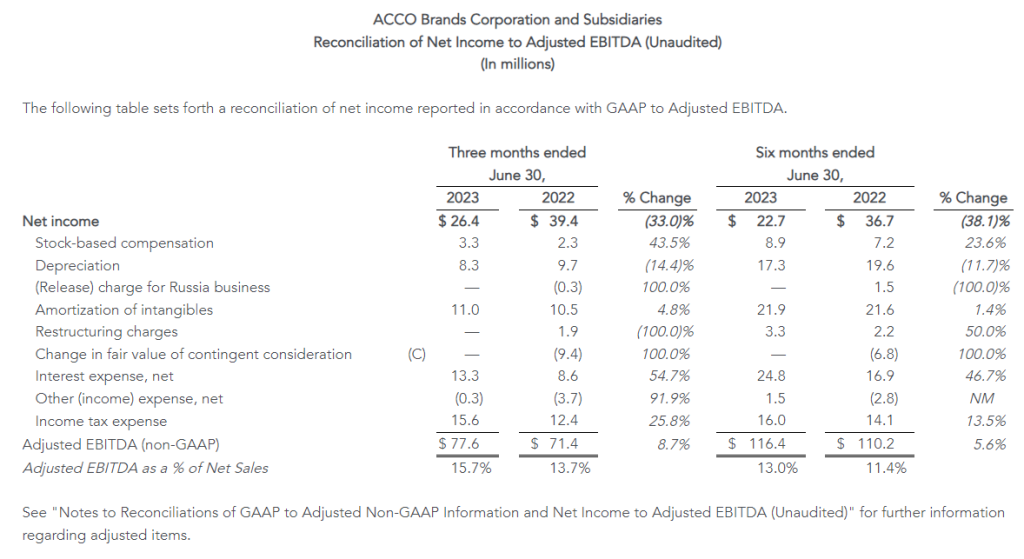

Capital Allocation and Dividend

Year to date, the Company improved its operating cash outflow by $58.6 million to $39.3 million versus $97.9 million in the prior year, driven primarily by improved working capital management. Adjusted free cash flow improved by $50.1 million and was an outflow of $45.4 million versus an outflow of $95.5 million a year earlier. Adjusted free cash flow in 2022 excludes the contingent earnout payment.

On August 1, 2023, ACCO Brands announced that its board of directors declared a regular quarterly cash dividend of $0.075 per share. The dividend will be paid on September 12, 2023, to stockholders of record at the close of business on August 22, 2023.

Full Year 2023 and Third Quarter Outlook

The Company is updating its full year 2023 outlook and providing a 3Q outlook. For the full year, reported sales are expected to be down 1 percent to 3 percent, including a 1.5 percent positive impact from foreign exchange. The Company is also maintaining its full year adjusted EPS outlook to be in the range of $1.08 to $1.12. Mid-teen growth in adjusted operating income is expected to be partially offset by higher interest and non-cash non-operating pension expenses. The Company is raising its 2023 free cash flow outlook to at least $110 million and expects to end the year with a consolidated leverage ratio of 3.3x to 3.5x, lower than previously expected.

In the third quarter, reported sales are expected to be flat to down 3 percent, which includes approximately a 4 percent positive impact from foreign exchange. Adjusted EPS is expected to be in the range of $0.21 to $0.24, which compares to $0.25 of adjusted EPS in the prior-year third quarter.

Webcast

At 8:30 a.m. ET on August 9, 2023, ACCO Brands Corporation will host a conference call to discuss the Company’s second quarter 2023 results. The call will be broadcast live via webcast. The webcast can be accessed through the Investor Relations section of www.accobrands.com. The webcast will be in listen-only mode and will be available for replay following the event.

About ACCO Brands Corporation

ACCO Brands, the Home of Great Brands Built by Great People, designs, manufactures and markets consumer and end-user products that help people work, learn, play and thrive. Our widely recognized brands include AT-A-GLANCE®, Five Star®, Kensington®, Leitz®, Mead®, PowerA®, Swingline®, Tilibra® and many others. More information about ACCO Brands Corporation (NYSE: ACCO) can be found at www.accobrands.com.

Non-GAAP Financial Measures

In addition to financial results reported in accordance with generally accepted accounting principles (GAAP), we have provided certain non-GAAP financial information in this earnings release to aid investors in understanding the Company’s performance. Each non-GAAP financial measure is defined and reconciled to its most directly comparable GAAP financial measure in the “About Non-GAAP Financial Measures” section of this earnings release.

Forward-Looking Statements

Statements contained herein, other than statements of historical fact, particularly those anticipating future financial performance, business prospects, growth, strategies, business operations and similar matters, results of operations, liquidity and financial condition, are “forward-looking statements” within the meaning of the Private Securities Litigation Reform Act of 1995. These statements are based on the beliefs and assumptions of management based on information available to us at the time such statements are made. These statements, which are generally identifiable by the use of the words “will,” “believe,” “expect,” “intend,” “anticipate,” “estimate,” “forecast,” “project,” “plan,” and similar expressions, are subject to certain risks and uncertainties, are made as of the date hereof, and we undertake no duty or obligation to update them. Because actual results may differ materially from those suggested or implied by such forward-looking statements, you should not place undue reliance on them when deciding whether to buy, sell or hold the Company’s securities.

Our outlook is based on certain assumptions, which we believe to be reasonable under the circumstances. These include, without limitation, assumptions regarding the impact of the war in Ukraine; the impact of inflation and global economic uncertainties, fluctuations in foreign currency exchange rates and acquisitions; and the other factors described below.

Among the factors that could cause our actual results to differ materially from our forward-looking statements are: our ability to successfully execute our restructuring plans and realize the benefits of our productivity initiatives; our ability to obtain additional price increases and realize longer-term cost reductions; the ongoing impact of the COVID-19 pandemic; a relatively limited number of large customers account for a significant percentage of our sales; issues that influence customer and consumer discretionary spending during periods of economic uncertainty or weakness; risks associated with foreign currency exchange rate fluctuations; challenges related to the highly competitive business environment in which we operate; our ability to develop and market innovative products that meet consumer demands and to expand into new and adjacent product categories that are experiencing higher growth rates; our ability to successfully expand our business in emerging markets and the exposure to greater financial, operational, regulatory, compliance and other risks in such markets; the continued decline in the use of certain of our products; risks associated with seasonality; the sufficiency of investment returns on pension assets, risks related to actuarial assumptions, changes in government regulations and changes in the unfunded liabilities of a multi-employer pension plan; any impairment of our intangible assets; our ability to secure, protect and maintain our intellectual property rights, and our ability to license rights from major gaming console makers and video game publishers to support our gaming accessories business; continued disruptions in the global supply chain; risks associated with inflation and other changes in the cost or availability of raw materials, transportation, labor, and other necessary supplies and services and the cost of finished goods; risks associated with outsourcing production of certain of our products, information technology systems and other administrative functions; the failure, inadequacy or interruption of our information technology systems or its supporting infrastructure; risks associated with a cybersecurity incident or information security breach, including that related to a disclosure of personally identifiable information; our ability to grow profitably through acquisitions; our ability to successfully integrate acquisitions and achieve the financial and other results anticipated at the time of acquisition, including planned synergies; risks associated with our indebtedness, including limitations imposed by restrictive covenants, our debt service obligations, and our ability to comply with financial ratios and tests; a change in or discontinuance of our stock repurchase program or the payment of dividends; product liability claims, recalls or regulatory actions; the impact of litigation or other legal proceedings; our failure to comply with applicable laws, rules and regulations and self-regulatory requirements, the costs of compliance and the impact of changes in such laws; our ability to attract and retain qualified personnel; the volatility of our stock price; risks associated with circumstances outside our control, including those caused by public health crises, such as the occurrence of contagious diseases, severe weather events, war, terrorism and other geopolitical incidents; and other risks and uncertainties described in “Part I, Item 1A. Risk Factors” in our Annual Report on Form 10-K for the year ended December 31, 2022, and in other reports we file with the Securities and Exchange Commission.

About Non-GAAP Financial Measures

We explain below how we calculate each of our non-GAAP financial measures and a reconciliation of our current period and historical non-GAAP financial measures to the most directly comparable GAAP financial measures follows.

We use our non-GAAP financial measures both to explain our results to stockholders and the investment community and in the internal evaluation and management of our business. We believe our non-GAAP financial measures provide management and investors with a more complete understanding of our underlying operational results and trends, facilitate meaningful period-to-period comparisons and enhance an overall understanding of our past and future financial performance.

Our non-GAAP financial measures exclude certain items that may have a material impact upon our reported financial results such as restructuring charges, transaction and integration expenses associated with material acquisitions, the impact of foreign currency exchange rate fluctuations and acquisitions, unusual tax items, goodwill impairment charges, and other non-recurring items that we consider to be outside of our core operations. These measures should not be considered in isolation or as a substitute for, or superior to, the directly comparable GAAP financial measures and should be read in connection with the Company’s financial statements presented in accordance with GAAP.

Our non-GAAP financial measures include the following:

Comparable Sales : Represents net sales excluding the impact of material acquisitions, if any, with current-period foreign operation sales translated at prior-year currency rates. We believe comparable sales are useful to investors and management because they reflect underlying sales and sales trends without the effect of material acquisitions and fluctuations in foreign exchange rates and facilitate meaningful period-to-period comparisons. We sometimes refer to comparable sales as comparable net sales.

Adjusted Selling, General and Administrative (SG&A) Expenses : Represents selling, general and administrative expenses excluding transaction and integration expenses related to material acquisitions. We believe adjusted SG&A expenses are useful to investors and management because they reflect underlying SG&A expenses without the effect of expenses related to acquiring and integrating acquisitions that we consider to be outside our core operations and facilitate meaningful period-to-period comparisons.

Adjusted Operating Income/Adjusted Income Before Taxes/Adjusted Net Income/Adjusted Net Income Per Diluted Share:Represents operating income, income before taxes, net income, and net income per diluted share excluding restructuring and goodwill impairment charges, the amortization of intangibles, the amortization of the step-up in value of inventory, the change in fair value of contingent consideration, transaction and integration expenses associated with material acquisitions, non-recurring items in interest expense or other income/expense such as expenses associated with debt refinancing, a bond redemption, or a pension curtailment, and other non-recurring items as well as all unusual and discrete income tax adjustments, including income tax related to the foregoing. We believe these adjusted non-GAAP financial measures are useful to investors and management because they reflect our underlying operating performance before items that we consider to be outside our core operations and facilitate meaningful period-to-period comparisons. Senior management’s incentive compensation is derived, in part, using adjusted operating income and adjusted net income per diluted share, which is derived from adjusted net income. We sometimes refer to adjusted net income per diluted share as adjusted earnings per share or adjusted EPS.

Adjusted Income Tax Expense/Rate:Represents income tax expense/rate excluding the tax effect of the items that have been excluded from adjusted income before taxes, unusual income tax items such as the impact of tax audits and changes in laws, significant reserves for cash repatriation, excess tax benefits/losses, and other discrete tax items. We believe our adjusted income tax expense/rate is useful to investors because it reflects our baseline income tax expense/rate before benefits/losses and other discrete items that we consider to be outside our core operations and facilitates meaningful period-to-period comparisons.

Adjusted EBITDA: Represents net income excluding the effects of depreciation, stock-based compensation expense, amortization of intangibles, the change in fair value of contingent consideration, interest expense, net, other (income) expense, net, and income tax expense, the amortization of the step-up in value of inventory, transaction and integration expenses associated with material acquisitions, restructuring and goodwill impairment charges, non-recurring items in interest expense or other income/expense such as expenses associated with debt refinancing, a bond redemption, or a pension curtailment and other non-recurring items. We believe adjusted EBITDA is useful to investors because it reflects our underlying cash profitability and adjusts for certain non-cash charges, and items that we consider to be outside our core operations and facilitates meaningful period-to-period comparisons.

Free Cash Flow/Adjusted Free Cash Flow: Free cash flow represents cash flow from operating activities less cash used for additions to property, plant and equipment. Adjusted free cash flow represents free cash flow, less cash payments made for contingent earnouts, plus cash proceeds from the disposition of assets. We believe free cash flow and adjusted free cash flow are useful to investors because they measure our available cash flow for paying dividends, funding strategic material acquisitions, reducing debt, and repurchasing shares.

Consolidated Leverage Ratio: Represents balance sheet debt, plus debt origination costs and less any cash and cash equivalents divided by adjusted EBITDA. We believe that consolidated leverage ratio is useful to investors since the company has the ability to, and may decide to use, a portion of its cash and cash equivalents to retire debt.

We also provide forward-looking non-GAAP comparable sales, adjusted earnings per share, free cash flow, adjusted free cash flow, adjusted EBITDA, and adjusted tax rate, and historical and forward-looking consolidated leverage ratio. We do not provide a reconciliation of these forward-looking and historical non-GAAP measures to GAAP because the GAAP financial measure is not currently available and management cannot reliably predict all the necessary components of such non-GAAP measures without unreasonable effort or expense due to the inherent difficulty of forecasting and quantifying certain amounts that are necessary for such a reconciliation, including adjustments that could be made for restructuring, integration and acquisition-related expenses, the variability of our tax rate and the impact of foreign currency fluctuation and material acquisitions, and other charges reflected in our historical results. The probable significance of each of these items is high and, based on historical experience, could be material.

Christopher McGinnis Investor Relations (847) 796-4320

FAT Brands (NASDAQ: FAT) is a leading global franchising company that strategically acquires, markets, and develops fast casual, quick-service, casual dining, and polished casual dining concepts around the world. The Company currently owns 17 restaurant brands: Round Table Pizza, Fatburger, Marble Slab Creamery, Johnny Rockets, Fazoli’s, Twin Peaks, Great American Cookies, Hot Dog on a Stick, Buffalo’s Cafe & Express, Hurricane Grill & Wings, Pretzelmaker, Elevation Burger, Native Grill & Wings, Yalla Mediterranean and Ponderosa and Bonanza Steakhouses, and franchises and owns over 2,300 units worldwide. For more information on FAT Brands, please visit www.fatbrands.com.

Joe Gomes, Managing Director, Equity Research Analyst, Generalist , Noble Capital Markets, Inc.

Joshua Zoepfel, Research Associate, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

Factory Utilization. FAT Brands has completed the rollout of cookie offerings at burger portfolio restaurants nationwide, including Fatburger, Johnny Rockets, and Elevation Burger. While consumers will benefit from additional menu choices, the real key is the potential for increased utilization of the manufacturing facility. Recall, this is an asset management will look to monetize and higher utilization will result in increased value for the asset.

Great American Cookie. The cookie concept has opened its 400th location, and operates in 31 states and five countries around the world. In the last two years, the brand has experienced accelerated growth, opening 73 new locations and entering new states such as Alaska, Arizona, Illinois and New Mexico. Just like the cookie roll out to the burger concepts, each additional Great American Cookie location adds to factory utilization.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

ACCO Brands Corporation is one of the world’s largest designers, marketers and manufacturers of branded academic, consumer and business products. Our widely recognized brands include AT-A-GLANCE®, Esselte®, Five Star®, GBC®, Kensington®, Leitz®, Mead®, PowerA®, Quartet®, Rapid®, Rexel®, Swingline®, Tilibra®, and many others. Our products are sold in more than 100 countries around the world. More information about ACCO Brands, the Home of Great Brands Built by Great People, can be found at www.accobrands.com.

Joe Gomes, Managing Director, Equity Research Analyst, Generalist , Noble Capital Markets, Inc.

Joshua Zoepfel, Research Associate, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

Second Quarter Results. ACCO reported net sales of $493.6 million compared to $521.0 million last year. We projected revenue of $490 million. Adverse foreign exchange reduced sales by $0.8 million, or less than 1%. Comparable sales fell 5.1%. ACCO had net income of $26.4 million, or $0.27 per diluted, compared to $39.4 million, or $0.40, last year. Adjusted EPS was $0.38, above the Company’s outlook. We estimated net income of $20 million or diluted EPS of $0.21.

Change in Guidance. ACCO is changing their outlook for the full year 2023, as sales are expected to be down 1-3% from the previous 4-7%, including a 1.5% positive impact from foreign exchange. The Company is maintaining its adjusted EPS outlook ($1.08-$1.12 range), is raising its free cash flow outlook to at least $110 million from a prior $100 million, and is lowering its expected consolidated leverage ratio of 3.3x to 3.5x from 3.5x to 3.7x. All of these are positive developments that stem from the Company’s restructuring process announced earlier this year, in our view.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

Company-Owned Cookie Dough FacilityNow Serving Fatburgerand Johnny Rockets

LOS ANGELES, Aug. 08, 2023 (GLOBE NEWSWIRE) — FAT (Fresh. Authentic. Tasty.) Brands Inc., parent company of Fatburger, Johnny Rockets and 15 other restaurant concepts, today announces the rollout of cookie offerings at burger portfolio restaurants nationwide – Fatburger, Johnny Rockets and Elevation Burger.

The sweet menu rollout is a strategic optimization that leverages FAT Brands’ company-owned manufacturing facility, which produces cookie dough and pretzel mix for sister portfolio brands Great American Cookies and Pretzelmaker. Elevation Burger completed its cookie roll-out earlier in April of this year.

“For both Fatburger and Johnny Rockets, we see these additions as a way to further build and enhance our dessert programs,” said Taylor Fischer, Vice President of Marketing of FAT Brands’ Fast Casual Division. “Playing into synergies is at the core of FAT Brands’ DNA. We are thrilled to be able to tap into our cookie dough facility to provide more delicious offerings for our fans.”

For more information or to find a Fatburger near you, please visit www.Fatburger.com. For more information or to find a Johnny Rockets near you, please visit www.JohnnyRockets.com.

About FAT (Fresh. Authentic. Tasty.) Brands