LOS ANGELES, Jan. 26, 2026 (GLOBE NEWSWIRE) — FAT (Fresh. Authentic. Tasty.) Brands Inc. (NASDAQ: FAT) (the “Company”), today announced it has commenced voluntary chapter 11 proceedings in the U.S. Bankruptcy Court for the Southern District of Texas. FAT Brands plans to use the filings to deleverage the balance sheet, maximize value for its stakeholders, and support continued growth of its brands.

FAT Brands’ portfolio of 18 restaurant concepts encompasses more than 2,200 locations worldwide. Iconic brands such as Fatburger, Johnny Rockets, Round Table Pizza, among others, are expected to remain operating as usual during the chapter 11 process, and will continue to provide their signature dining experiences. Trading of FAT Brands’ securities on NASDAQ is expected to continue with a “Q” suffix during this period.

“Our dynamic portfolio of brands has demonstrated tremendous resilience in a challenging restaurant operating environment over the last few years. We are well positioned for long-term profitability and growth. The chapter 11 process will provide us with the opportunity to strengthen our capital structure to support our concepts and ensure they remain at the forefront of their sectors,” said Andy Wiederhorn, CEO of FAT Brands. “We plan to use this process to connect with key stakeholders around a value-maximizing plan and will act prudently to remain steadfast in upholding and protecting stakeholder interests. Our focus in this process remains providing quality service to our customers and supporting our franchise partners and the over 45,000 corporate and franchise employees.”

Bankruptcy Court filings and other information about the claims process and proceedings can be found at a separate website maintained by the Company’s proposed claims and noticing agent, Omni Agent Solutions, Inc., at https://omniagentsolutions.com/FatBrands-TwinHospitality.

Latham & Watkins LLP is serving as legal counsel to the Company. GLC Advisors & Co., LLC is serving as investment banker, Huron Consulting Services LLC is serving as financial advisor, and Omni Agent Solutions, Inc. is serving as claims, noticing and solicitation agent.

About FAT (Fresh. Authentic. Tasty.) Brands FAT Brands (NASDAQ: FAT) is a leading global franchising company that strategically acquires, markets, and develops fast casual, quick-service, casual dining, and polished casual dining concepts around the world. The Company currently owns 18 restaurant brands: Round Table Pizza, Fatburger, Marble Slab Creamery, Johnny Rockets, Fazoli’s, Twin Peaks, Great American Cookies, Smokey Bones, Hot Dog on a Stick, Buffalo’s Cafe & Express, Hurricane Grill & Wings, Pretzelmaker, Elevation Burger, Native Grill & Wings, Yalla Mediterranean and Ponderosa and Bonanza Steakhouses, and franchises and owns over 2,200 units worldwide. For more information on FAT Brands, please visit fatbrands.com.

Forward Looking Statements This Current Report on Form 8-K contains statements that constitute forward-looking statements within the meaning of the Private Securities Litigation Reform Act of 1995 and other securities laws. These forward-looking statements are based upon our present intent, beliefs or expectations, but forward-looking statements are not guaranteed to occur and may not occur. Actual results may differ materially from those contained in or implied by our forward-looking statements as a result of various factors These forward-looking statements include, among others, statements about: the Company’s ability to obtain Bankruptcy Court approval with respect to motions in the Chapter 11 proceedings, including the “first day” relief being requested; the Company’s ability to successfully consummate a restructuring; the expected effects of the Chapter 11 proceedings, on the Company’s business and the interests of various stakeholders; the Company’s ability to continue operating in the ordinary course; the terms, effectiveness, and consummation of a chapter 11 plan; the anticipated capital structure upon emergence from bankruptcy; the expected treatment of claims; the potential cancellation of the Company’s equity; the registration status of any new securities to be issued pursuant to a chapter 11 plan, and the timing of any of the foregoing. Forward-looking statements are based on the Company’s current expectations, assumptions and estimates and are subject to risk, uncertainties, and other important factors that are difficult to predict and that could cause actual results to differ materially and adversely from those expressed or implied. These risks include, among others, those related to: the Company’s ability to confirm and consummate a chapter 11 plan of reorganization; the duration and outcome of the Chapter 11 proceedings; the risk of the Company suffering from a long and protracted restructuring; the impact of the Chapter 11 proceedings on the Company’s operations, reputation and relationships with tenants, lenders, and vendors; the Company having insufficient liquidity; the availability of financing during the pendency of, or after completion of, the Chapter 11 proceedings; the effectiveness of overall restructuring activities pursuant to the Chapter 11 proceedings and any additional strategies that the Company may employ to address its liquidity and capital resources and achieve its stated goals; the potential cancellation of the Company’s equity; and the Company’s historical financial information not being indicative of its future performance as a result of the Chapter 11 proceedings.

The information contained in the Company’s filings with the Securities and Exchange Commission (“SEC”), including under the caption “Risk Factors” in the Company’s Annual Report on Form 10-K for the year ended December 29, 2024 and subsequent filings with the SEC, or incorporated herein or therein, identifies other important factors that could cause differences from our forward-looking statements. The Company’s filings with the SEC are available on the SEC’s website at www.sec.gov.

You should not place undue reliance upon the Company’s forward-looking statements.

Except as required by law, we do not intend to update or change any forward-looking statements as a result of new information, future events or otherwise.

ST. PETERSBURG, Fla., Jan. 26, 2026 (GLOBE NEWSWIRE) — Superior Group of Companies, Inc. (NASDAQ: SGC), a leading global manufacturer and distributor of uniforms, branded products, and call center services, today announced the launch of a comprehensive shareholder rewards program in partnership with Stockperks, the innovative marketplace that connects retail investors with the companies they own.

Through the Stockperks platform, Superior Group of Companies shareholders can access exclusive perks and rewards based on their shareholding levels. Initial perks include gift cards and discounts on Superior Cloth & Stitch healthcare apparel and customized S’well water bottles.

“At SGC, we’re committed to building lasting relationships with all our stakeholders, including our retail investor community,” said Michael Benstock, Chairman and CEO of Superior Group of Companies. “This partnership with Stockperks allows us to extend the same appreciation we show our customers to our shareholders, offering them tangible benefits that reflect our diverse portfolio of quality brands, products and services. We believe this program will strengthen our connection with retail investors and demonstrate our commitment to delivering value beyond financial returns.”

Agnies Watson, CEO and Co-Founder of Stockperks, expressed enthusiasm for the partnership, stating, “Superior Group of Companies has built an impressive portfolio serving a broad range of industries and well-known consumer brands. We are thrilled to welcome them to the Stockperks community. By leveraging our platform, SGC will be able to deepen its engagement with retail investors year-round, providing them with exclusive perks that showcase their exceptional brands. This collaboration exemplifies our commitment to revolutionizing the way companies connect with their shareholders and create a community of loyal and informed individual investors.”

To learn more about Superior Group of Companies and claim shareholder perks, please visit the Stockperks app or www.superiorgroupofcompanies.com.

About Superior Group of Companies, Inc. (SGC): Established in 1920, Superior Group of Companies is comprised of three attractive business segments each serving large, fragmented and growing addressable markets. Across Healthcare Apparel, Branded Products and Contact Centers, each segment enables businesses to create extraordinary brand engagement experiences for their customers and employees. SGC’s commitment to service, quality, advanced technology, and omnichannel commerce provides unparalleled competitive advantages. We are committed to enhancing shareholder value by continuing to pursue a combination of organic growth and strategic acquisitions. For more information, visit www.superiorgroupofcompanies.com.

MIAMI, Jan. 23, 2026 (GLOBE NEWSWIRE) — SKYX Platforms Corp. (NASDAQ: SKYX) (d/b/a SKYX Technologies) (the “Company” or “SKYX”), a highly disruptive smart home platform technology company with over 100 pending and issued patents globally and 60 lighting and home décor websites, with a mission to make homes and buildings become safe and smart as the new standard, today announced that it has entered into a securities purchase agreement with one fundamental institutional investor to raise $25 million of gross proceeds via a registered direct offering.

Under the terms of the securities purchase agreement, the Company will issue, for an aggregate purchase price of $25 million, a total of 10 million shares of common stock, at a purchase price of $2.50 per share with no warrants. The closing of the offering is subject to customary closing conditions and is expected to close on or about January 26, 2026. The Company intends to use the net proceeds from the offering for working capital and general corporate purposes.

Roth Capital Partners is acting as the exclusive placement agent for the offering.

A shelf registration statement on Form S-3 (File No. 333-271698) relating to the securities being offered was originally filed with the U.S. Securities and Exchange Commission (the “SEC”) on May 5, 2023 and declared effective on May 12, 2023. The offering is being made only by means of a prospectus supplement and accompanying prospectus that form a part of the shelf registration statement. The final prospectus supplement and accompanying prospectus relating to the offering will be filed with the SEC and will be available on the SEC’s website at www.sec.gov. Electronic copies of the final prospectus supplement and accompanying prospectus relating to the offering, when available, may be obtained on the SEC’s website at www.sec.gov or by contacting Roth Capital Partners, LLC, 888 San Clemente Drive, Newport Beach, CA 92660 or by email at rothecm@roth.com.

This press release shall not constitute an offer to sell or a solicitation of an offer to buy these securities, nor shall there be any sale of these securities in any state or jurisdiction in which such offer, solicitation or sale would be unlawful, prior to registration or qualification under the securities laws of any such state or jurisdiction.

About SKYX Platforms Corp.

SKYX Platforms Corp. (NASDAQ: SKYX) is a technology platform company focused on making homes and buildings safe, advanced, and smart as the new standard. As electricity is present in every home and building, SKYX is developing disruptive plug & play technologies designed to modernize traditional electrical infrastructure while improving safety, functionality, and ease of use.

The Company holds over 100 issued and pending U.S. and global patents and owns 60 lighting and home décor websites serving both retail and professional markets. SKYX’s platform emphasizes high-quality design, simplicity, and enhanced safety, with applications intended for every room in residential, commercial, hospitality, and institutional buildings worldwide.

SKYX’s technologies support recurring revenue opportunities through product interchangeability, upgrades, AI-enabled services, monitoring, and subscriptions. The Company follows a “razor-and-blades” model, anchored by its advanced ceiling electrical outlet platform and an expanding portfolio of plug & play smart home products, including lighting, recessed and down lights, emergency and exit signage, ceiling fans, chandeliers, indoor and outdoor fixtures, and themed lighting solutions. Its plug & play technology enables rapid installation in high-rise buildings and hotels, reducing deployment timelines from months to days.

SKYX estimates its U.S. total addressable market at approximately $500 billion, with more than 4.2 billion ceiling applications in the U.S. alone. Revenue streams are expected to include product sales, licensing, royalties, subscriptions, monitoring services, and the sale of global country rights.

Forward-Looking Statements Certain statements made in this press release are not based on historical facts but are forward-looking statements. These statements can be identified by the use of forward-looking terminology such as “aim,” “anticipate,” “believe,” “can,” “could,” “continue,” “estimate,” “expect,” “evaluate,” “forecast,” “guidance,” “intend,” “likely,” “may,” “might,” “objective,” “ongoing,” “outlook,” “plan,” “potential,” “predict,” “probable,” “project,” “seek,” “should,” “target,” “view,” “will,” or “would,” or the negative thereof or other variations thereon or comparable terminology, although not all forward-looking statements contain these words. These statements reflect the Company’s reasonable judgment with respect to future events and are subject to risks, uncertainties and other factors, many of which have outcomes difficult to predict and may be outside our control, that could cause actual results or outcomes to differ materially from those in the forward-looking statements. Such risks and uncertainties include statements relating to completion, size and timing of the offering, the Company’s intended use of proceeds from the offering, the Company’s ability to successfully launch, commercialize, develop additional features and achieve market acceptance of its products and technologies and integrate its products and technologies with third-party platforms or technologies; the Company’s efforts and ability to drive the adoption of its products and technologies as a standard feature, including their use in homes, hotels, offices and cruise ships; the Company’s ability to capture market share; the Company’s estimates of its potential addressable market and demand for its products and technologies; the Company’s ability to raise additional capital to support its operations as needed, which may not be available on acceptable terms or at all; the Company’s ability to continue as a going concern; the Company’s ability to execute on any sales and licensing or other strategic opportunities; the possibility that any of the Company’s products will become National Electrical Code (NEC)-code or otherwise code mandatory in any jurisdiction, or that any of the Company’s current or future products or technologies will be adopted by any state, country, or municipality, within any specific timeframe or at all; risks arising from mergers, acquisitions, joint ventures and other collaborations; the Company’s ability to attract and retain key executives and qualified personnel; guidance provided by management, which may differ from the Company’s actual operating results; the potential impact of unstable market and economic conditions on the Company’s business, financial condition, and stock price; and other risks and uncertainties described in the Company’s filings with the Securities and Exchange Commission, including its periodic reports on Form 10-K and Form 10-Q. There can be no assurance as to any of the foregoing matters. Any forward-looking statement speaks only as of the date of this press release, and the Company undertakes no obligation to update or revise any forward-looking statements, whether as a result of new information, future events or otherwise, except as required by U.S. federal securities laws.

Holiday Period Total Net Sales Increased 5.3% vs. Last Year Led by 9.7% Growth in Direct-to-Consumer Segment

NEW YORK–(BUSINESS WIRE)– Vince Holding Corp., (Nasdaq: VNCE) (“VNCE” or the “Company”), a global retail platform, today announced sales for the nine-week holiday period ended January 3, 2026.

Holiday Sales Highlights (Unaudited Results for Nine-Week Period Ended January 3, 2026)

Total company net sales increased 5.3% compared to the prior year period

Direct-to-Consumer segment sales increased 9.7% compared to the prior year period

Wholesale segment sales decreased 2.7% compared to the prior year period

Brendan Hoffman, Chief Executive Officer of VNCE commented, “Our direct-to-consumer segment continues to deliver exceptional results, building on the strong momentum from our strategic investments in customer experience enhancements and e-commerce capabilities. Within wholesale, we have continued to see strong performance at the register with key partners helping to offset disruption in receipt flow with Saks Global given current dynamics. This overall performance, combined with our disciplined approach to balancing strategic pricing changes, promotional activity, and cost management, demonstrates the strength of our business model. As we look ahead, we will continue to execute and deliver on our strategic priorities that we believe will position us well for long-term profitable growth.”

Based on holiday sales performance, total company net sales have trended in line with prior guidance and Adjusted EBITDA as a % of Net Sales and Adjusted Operating Income as a % of Net Sales have trended in line with the higher end of prior guidance ranges for the fourth quarter and full year fiscal 2025.

The Company continues to monitor developments with its wholesale partner, Saks Global, and guidance does not reflect any outcome of its reported status. Saks Global represented less than 7% of total company net sales as of Fiscal 2024.

The holiday sales results reported in this press release are unaudited and preliminary. These amounts are based on currently available information and are subject to change following the completion of any customary financial closing procedures for the fiscal quarter ending January 31, 2026.

ICR Conference As previously announced, the Company will be presenting at the 28th Annual ICR Conference today, Monday, January 12, 2026, at 8:30 AM Eastern Time. The audio portion of the presentation will be webcast live on the investor relations section of the Company’s website, http://investors.vince.com/.

ABOUT VINCE HOLDING CORP.

Vince Holding Corp. is a global retail platform that operates the Vince brand women’s and men’s ready to wear business. Vince, established in 2002, is a leading global luxury apparel and accessories brand best known for creating elevated yet understated pieces for every day effortless style. Vince Holding Corp. operates 46 full-price retail stores, 14 outlet stores, and its e-commerce site, as well as through premium wholesale channels globally. Please visit www.vince.com for more information.

Forward-Looking Statements: This document, and any statements incorporated by reference herein contain forward-looking statements under the Private Securities Litigation Reform Act of 1995. Forward-looking statements include statements regarding, among other things, our current expectations about possible or assumed future results of operations of the Company and are indicated by words or phrases such as “may,” “will,” “should,” “believe,” “expect,” “seek,” “anticipate,” “intend,” “estimate,” “plan,” “target,” “project,” “forecast,” “envision” and other similar phrases. Although we believe the assumptions and expectations reflected in these forward-looking statements are reasonable, these assumptions and expectations may not prove to be correct and we may not achieve the results or benefits anticipated. These forward-looking statements are not guarantees of actual results, and our actual results may differ materially from those suggested in the forward-looking statements. These forward-looking statements involve a number of risks and uncertainties, some of which are beyond our control, including, without limitation: changes to and unpredictability in the trade policies and tariffs imposed by the U.S. and the governments of other nations; our ability to maintain our larger wholesale partners; our ability to maintain adequate cash flow from operations or availability under our revolving credit facility to meet our liquidity needs; general economic conditions; restrictions on our operations under our credit facilities; our ability to improve our profitability; our ability to accurately forecast customer demand for our products; our ability to maintain the license agreement with ABG Vince, a subsidiary of Authentic Brands Group; ABG Vince’s expansion of the Vince brand into other categories and territories; ABG Vince’s approval rights and other actions; our ability to realize the benefits of our strategic initiatives; the execution of our customer strategy; our ability to make lease payments when due; our ability to open retail stores under favorable lease terms and operate and maintain new and existing retail stores successfully; our operating experience and brand recognition in international markets; our ability to remediate the identified material weakness in our internal control over financial reporting; our ability to comply with domestic and international laws, regulations and orders; increased scrutiny regarding our approach to sustainability matters and environmental, social and governance practices; competition in the apparel and fashion industry; the transition associated with the appointment of new chief executive officer and new chief financial officer; our ability to attract and retain key personnel; seasonal and quarterly variations in our revenue and income; the protection and enforcement of intellectual property rights relating to the Vince brand; our ability to successfully conclude remaining matters following the wind down of the Rebecca Taylor business; the extent of our foreign sourcing; our reliance on independent manufacturers; our ability to ensure the proper operation of the distribution facilities by third-party logistics providers; fluctuations in the price, availability and quality of raw materials; the ethical business and compliance practices of our independent manufacturers; our ability to mitigate system or data security issues, such as cyber or malware attacks, as well as other major system failures; our ability to adopt, optimize and improve our information technology systems, processes and functions; our ability to comply with privacy-related obligations; our status as a “controlled company”; our status as a “smaller reporting company”; and other factors as set forth from time to time in our Securities and Exchange Commission filings, including those described under “Item 1A—Risk Factors” in our Annual Report on Form 10-K and Quarterly Reports on Form 10-Q. We intend these forward-looking statements to speak only as of the time of this release and do not undertake to update or revise them as more information becomes available, except as required by law.

Participating in the 28th Annual ICR Conference and Hosting a Fireside Chat at 10:30 AM ET Tomorrow

DENVER–(BUSINESS WIRE)– The ONE Group Hospitality, Inc. (“The ONE Group” or the “Company”) (Nasdaq: STKS) today reported preliminary sales results for the fourth quarter and full year ended December 28, 2025, and announced its participation at the 28th Annual ICR Conference.

Preliminary Sales Results for the Fourth Quarter and Full Year 2025

Our expectations with respect to our sales results for the fourth quarter and full year 2025 discussed below are based upon management estimates for the respective periods. Our expectations are subject to the completion of our financial closing procedures and any adjustments that may result from the completion of the review of our consolidated financial statements for the fourth quarter and full year 2025. Following the completion of our financial closing process and the review of our consolidated financial statements, we may report sales results for the fourth quarter and full year 2025 that could differ from our expectations, and the differences could be material.

The expectations set forth below have been prepared by, and are the responsibility of, our management. Deloitte & Touche, LLP, our independent registered public accounting firm, has not audited, reviewed, compiled or performed any procedures with respect to the preliminary estimates. Accordingly, Deloitte & Touche, LLP, does not express an opinion or any other form of assurance with respect thereto.

Preliminary total GAAP revenues for the full year 2025 are expected to be approximately $805 million, a 20% increase from the prior year’s $673 million. This growth was primarily driven by the acquisition of Benihana in May 2024. Comparable sales* are expected to decrease by approximately 3.7%.

Preliminary total GAAP revenues for the fourth quarter of 2025 are expected to be approximately $207 million, a 6.8% decrease from $222 million in the same quarter of 2024. This decline was primarily driven by RA Sushi and Kona Grill closures as part of the portfolio optimization and the change in the Company’s fiscal year. The Grill closures are expected to reduce total GAAP revenues by approximately 2.4%, representing 35% of the expected total GAAP revenue decline.

Effective January 1, 2025, the Company adopted a new fiscal calendar structure using four 13-week quarters, with a 53rd week added when necessary. The 2025 fiscal year ran from January 1, 2025, to December 28, 2025.

This fiscal calendar change created timing differences that impacted quarterly comparisons: the fourth quarter of 2025 had 91 days versus 92 days in the fourth quarter of 2024. Additionally, the New Year’s Eve holiday shifted from fiscal 2025 to fiscal 2026. The exclusion of New Year’s Eve in the current year impacted total GAAP revenues by approximately 2.5%, representing 37% of the expected total GAAP revenue decline. Fourth quarter comparable sales are expected to decrease by approximately 1.8%.

Preliminary sales highlights for the fourth quarter of 2025 compared to the same quarter in 2024 are as follows:

STK is expected to report positive comparable sales for the quarter of approximately 0.3%, representing the first quarter of positive comparable sales for the brand since 2023;

Benihana is expected to report flat comparable sales for the quarter;

Sequential improvement in consolidated comparable sales* of approximately 4 points from the third quarter driven by all brands during the quarter; and

First conversion of a RA Sushi to an STK in Scottsdale, Arizona is off to a strong start. In addition, in January 2026, the Company temporarily closed five Grills as part of the process to convert to future Benihana and STK restaurants.

“We were pleased to see sequential improvement in our comparable sales at all brands, with STK expected to end the quarter positive and Benihana essentially flat. We are seeing this momentum continue into the new year. We attribute this success to a robust holiday season and the strength of our operations initiatives. Headwinds continue to be strong, which we expect to result in lower-than-anticipated sales during the fourth quarter,” said Emanuel “Manny” Hilario, President and Chief Executive Officer of The ONE Group. “With challenges still impacting the industry, we attribute our traction to execution-driven initiatives within our direct control, including our targeted investments in reservation technology, streamlined operational flow, and comprehensive training initiatives. These efforts enabled us to capture even greater demand during our busiest periods by optimizing Benihana table efficiency while delivering exceptional and unforgettable experiences to our guests.”

“Looking to the new year, our number one priority is to conserve cash with the intent of optimizing our balance sheet. From a development perspective, we are focused on the RA Sushi and Kona Grill conversions to STK and Benihana restaurants and pursuing other asset-light opportunities to drive shareholder value. The recent signing of our Benihana development agreement is a game-changer, demonstrating the strong demand for our iconic brand. Additionally, our successful STK and Benihana openings and conversions, renewal of existing franchise agreements, and expanding presence in professional sports and entertainment stadiums further validate our disciplined approach to capital-efficient growth. We believe our future is bright, and we are well-equipped to capture the significant opportunities ahead of us.”

*Comparable sales, a non-GAAP financial measure, represent total U.S. food and beverage sales at owned and managed units opened for at least a full 24-months. This measure includes total revenue from our owned and managed locations. The Company monitors sales growth at its established restaurant base in addition to growth that results from restaurant acquisitions and new restaurant openings.

2025 Restaurant Development

The following restaurants were opened in 2025:

Franchised Benihana Express restaurant in Miami, Florida (June)

Licensed Benihana concession at UBS Arena in Elmont, New York (December)

Owned Benihana restaurant in San Mateo, California (March)

Owned STK restaurant in Topanga, California (April)

Owned STK restaurant in Los Angeles, California (May – relocation of our existing STK Westwood restaurant)

Owned STK restaurant in Scottsdale, Arizona (October – conversion of a former RA Sushi restaurant)

Owned STK restaurant in Oak Brook, Illinois (December)

Significant Asset-Light Expansion Planned for the Greater San Francisco Bay Area and Professional Sports and Entertainment Stadiums

In December 2025, The ONE Group announced that it entered into its largest asset-light development agreement in the Company’s history, securing development rights for a total of ten restaurants, either Benihana or Benihana Express locations, throughout the Greater San Francisco Bay Area with an experienced operator. This significantly accelerates its West Coast expansion while maintaining the Company’s focus on capital-efficient growth.

The ONE Group also strengthened its presence in high-traffic, professional sports and entertainment stadiums, demonstrating its ability to adapt its premium dining concepts to diverse formats. These partnerships are expected to generate high-margin royalty streams and create millions of fan impressions annually.

The Company renewed a three-year concession agreement at the Mortgage Matchup Center in Phoenix, Arizona, home of the Phoenix Suns (NBA) and Phoenix Mercury (WNBA). The venue currently has a Benihana concession, and the new agreement also provides for STK-branded products to be offered.

The Company also secured a new three-year Benihana concession at UBS Arena in Elmont, New York, home of the New York Islanders (NHL), expanding its reach in the New York metropolitan area. The UBS Arena concession complements the existing Benihana concession at Yankee Stadium.

Capital-Efficient Growth Strategy Planned for 2026

The ONE Group will prioritize capital-efficient growth in 2026, with a goal to significantly reduce discretionary capital expenditures.

New restaurant Company-owned development will be focused on locations requiring $1.5 million or less to open. The Company will also work through its existing pipeline of approximately twelve leases rather than sign new lease agreements, which we believe will strengthen its balance sheet while enhancing financial flexibility.

The ONE Group has identified up to nine additional Kona Grill and RA Sushi locations for conversion to either Benihana or STK formats through the end of 2026. These conversions are expected to require approximately $1 million in capital investment per restaurant and are anticipated to be accretive to EBITDA.

Conference Participation

Emanuel “Manny” Hilario, President and Chief Executive Officer, and Nicole Thaung, Chief Financial Officer, will host a fireside chat at the 28th Annual ICR Conference at 10:30 am Eastern Time on January 13, 2026, and meet with institutional investors in-person on January 12-13, 2026.

The webcast of the fireside chat can be accessed from the Investor Relations tab of the Company’s website at www.togrp.com under “News / Events.”

About The ONE Group

The ONE Group Hospitality, Inc. (Nasdaq: STKS) is an international restaurant company that develops and operates upscale and polished casual, high-energy restaurants and lounges and provides hospitality management services for hotels, casinos and other high-end venues both in the U.S. and internationally. The ONE Group’s focus is to be the global leader in Vibe Dining, and its primary restaurant brands and operations are:

STK, a modern twist on the American steakhouse concept with restaurants in major metropolitan cities in the U.S., Europe, and the Middle East, featuring premium steaks, seafood, and specialty cocktails in an energetic upscale atmosphere.

Benihana, an interactive dining destination with highly skilled chefs preparing food right in front of guests and served in an energetic atmosphere alongside fresh sushi and innovative cocktails. The Company franchises Benihanas in the U.S., Caribbean, Central America, and South America.

Benihana Express, a small footprint casual concept showcasing the best of Benihana but without teppanyaki tables or bar.

Kona Grill, a polished casual, bar-centric grill concept with restaurants in the U.S., featuring American favorites, award-winning sushi, and specialty cocktails in an upscale casual atmosphere.

RA Sushi, a Japanese cuisine concept that offers a fun-filled, bar-forward, upbeat, and vibrant dining atmosphere with restaurants in the U.S. anchored by creative sushi, inventive drinks, and outstanding service.

Salt Water Social is your gateway to the seven seas, featuring an array of signature and unique fresh seafood items, complemented by the highest quality beef dishes and elegant, delicious cocktails.

Samurai, an interactive dining experience located in sunny Miami, FL, provides a distinctive dining experience where skilled personal chefs masterfully perform the ancient art of teppanyaki right before your eyes.

ONE Hospitality, The ONE Group’s food and beverage hospitality services business develops, manages, and operates premier restaurants and turnkey food and beverage services within high-end hotels and casinos currently operating venues in the U.S. and Europe.

Additional information about The ONE Group can be found at www.togrp.com.

Cautionary Statement on Forward-Looking Statements

This press release includes “forward-looking statements” within the meaning of the “safe harbor” provisions of the United States Private Securities Litigation Reform Act of 1995, including with respect to 2025 results, restaurant openings, and performance trends. Forward-looking statements may be identified by the use of words such as “target,” “intend,” “anticipate,” “believe,” “expect,” “estimate,” “plan,” “outlook,” and “project” and other similar expressions that predict or indicate future events or trends or that are not statements of historical matters. A number of factors could cause actual results or outcomes to differ materially from those indicated by such forward-looking statements, including but not limited to: (1) factors beyond our control that affect the number and timing of new restaurant openings, including weather conditions and factors under the control of landlords, contractors and regulatory and/or licensing authorities; (2) changes in applicable laws or regulations; (3) the possibility that The ONE Group may be adversely affected by other economic, business, and/or competitive factors, including economic downturns; (4) the impact of actual and potential changes in immigration policies, including potential labor shortages; (5) the potential impact of the imposition of tariffs, including increases in food prices and inflation and any resulting negative impacts on the macro-economic environment; and (6) other risks and uncertainties indicated from time to time in our filings with the Securities and Exchange Commission, including our Annual Report on Form 10-K filed for the year ended December 31, 2024 and Quarterly Reports on Form 10-Q.

Investors are referred to the most recent reports filed with the Securities and Exchange Commission by The ONE Group. Investors are cautioned not to place undue reliance upon any forward-looking statements, which speak only as of the date made, and we undertake no obligation to update or revise the forward-looking statements, whether as a result of new information, future events or otherwise.

Non-GAAP Measures

The following table presents the elements of the quarterly and annual Comparable Sales measure for 2025:

2025 vs. 2024

Q1Actual

Q2Actual

Q3Actual

Q4Preliminary

Full YearPreliminary

US STK Total Restaurants

(3.6)%

(6.0)%

(5.8)%

0.3%

(3.7)%

Benihana Owned Restaurants

0.7%

0.4%

(4.0)%

(0.4)%

(0.8)%

Grill Concepts Owned Restaurants

(13.7)%

(14.6)%

(11.8)%

(9.4)%

(12.5)%

Combined Comparable Sales

(3.2)%

(4.1)%

(5.9)%

(1.8)%

(3.7)%

Benihana comprises approximately 58% of revenue, STK comprises 25% of revenue and Grill Concepts comprise approximately 17% of revenue.

JERICHO, N.Y.–(BUSINESS WIRE)– 1-800-FLOWERS.COM, Inc. (NASDAQ: FLWS) (the “Company”),a leading provider of thoughtful expressions designed to help inspire customers to give more, connect more, and build more and better relationships, today announced that the Company will release financial results for its fiscal 2026 second quarter on Thursday, January 29, 2026. The press release will be issued before the market opens and will be followed by a conference call with members of senior management at 8:00 a.m. (ET).

The conference call will be available via live webcast from the Investors section of the Company’s website at www.1800flowersinc.com/investors. A replay of the webcast will be available shortly after the live event has concluded. A telephonic replay of the call can be accessed beginning at 2:00 p.m. (ET) on January 29, 2026, through February 5, 2026, by dialing (855) 669-9658 or (412) 317-0088 for international callers; the passcode is 4751964.

Special Note Regarding Forward-Looking Statements:

Some of the statements contained in the Company’s press release and conference call regarding its fiscal 2026 second quarter results, other than statements of historical fact, may be forward-looking within the meaning of the Private Securities Litigation Reform Act of 1995. These statements involve risks and uncertainties that could cause actual results to differ materially from those expressed or implied in the applicable statements. For a more detailed description of these and other risk factors, please refer to the Company’s SEC filings including its Annual Reports and Forms 10K and 10Q available at the Investor Relations section of the Company’s website at 1800flowersinc.com. The Company expressly disclaims any intent or obligation to update any of the forward-looking statements made in the scheduled conference call and any recordings thereof, or in any of its SEC filings, except as may be otherwise stated by the Company.

About 1-800-FLOWERS.COM, Inc.

1-800-FLOWERS.COM, Inc. is a leading provider of thoughtful expressions designed to help inspire customers to share more, connect more, and build more and better relationships. The Company’s e-commerce business platform features an all-star family of brands, including: 1-800-Flowers.com®, 1-800-Baskets.com®, CardIsle®, Cheryl’s Cookies®, Harry & David®, PersonalizationMall.com®, Shari’s Berries®, FruitBouquets.com®, Things Remembered®, Moose Munch®, The Popcorn Factory®, Wolferman’s Bakery®, Vital Choice®, Simply Chocolate® and Scharffen Berger®. Through the Celebrations Passport® loyalty program, which provides members with free standard shipping and no service charge on eligible products across our portfolio of brands, 1-800-FLOWERS.COM, Inc. strives to deepen relationships with customers. The Company also operates BloomNet®, an international floral and gift industry service provider offering a broad-range of products and services designed to help members grow their businesses profitably; Napco℠, a resource for floral gifts and seasonal décor; and DesignPac Gifts, LLC, a manufacturer of gift baskets and towers. 1-800-FLOWERS.COM, Inc. was recognized among America’s Most Trustworthy Companies by Newsweek for 2024. 1-800-FLOWERS.COM, Inc. was also recognized as one of America’s Most Admired Workplaces for 2025 by Newsweek and was named to the Fortune 1000 list in 2022. Shares in 1-800-FLOWERS.COM, Inc. are traded on the NASDAQ Global Select Market, ticker symbol: FLWS. For more information, visit 1800flowersinc.com.

Andy Wiederhorn Appointed Chief Executive Officer; Roger Gondek to Assume Twin Peaks President Role

DALLAS, Dec. 29, 2025 (GLOBE NEWSWIRE) — Twin Hospitality Group Inc. (Nasdaq: TWNP), the parent company of Twin Peaks Restaurant, today announced the appointment of Andy Wiederhorn as Chief Executive Officer, effective immediately, following the termination of Chief Executive Officer Kim Boerema. Additionally, Roger Gondek, currently Chief Operating Officer of Twin Peaks Restaurant, will also assume the role of President of Twin Peaks Restaurant while continuing in his COO responsibilities.

Wiederhorn, who was integral in spinning out Twin Peaks and Smokey Bones into Twin Hospitality Group Inc., has served as Chairman of the Board since August 2025. In this role, he has worked closely with the leadership team to position the company for sustained growth and operational excellence. Gondek has served as Chief Operating Officer of Twin Peaks since 2017 and brings approximately 15 years of experience with the brand, including previous operations leadership roles with Twin Peaks’ largest franchisee.

“I’m pleased to take on the Chief Executive Officer role and continue to collaborate with Roger in his expanded capacity as President,” said Andy Wiederhorn, Chairman and Chief Executive Officer of Twin Hospitality Group. “We remain focused on driving key business initiatives forward, including streamlining operations and enhancing the guest experience. This leadership restructuring optimizes our resources while minimizing overhead, providing additional value as we work to restructure our debt and strengthen the company for long-term success.”

Twin Hospitality Group Inc. Twin Hospitality Group Inc. is a restaurant company that strategically develops and operates specialty casual dining restaurant concepts with a goal to redefine the casual dining category with its experiential driven brands. For more information, visit https://ir.twinpeaksrestaurant.com/.

About Twin Peaks Founded in 2005 in the Dallas suburb of Lewisville, Twin Peaks has 114 locations in the U.S. and Mexico. Twin Peaks is the ultimate sports lodge featuring made-from-scratch food and the coldest beer in the business, surrounded by scenic views and wall-to-wall TVs. At every Twin Peaks, guests are immediately welcomed by a friendly Twin Peaks Girl and served up a menu made for MVPs. From its smashed and seared-to-order burgers to its in-house smoked brisket and wings, guests can expect menu items that satisfy every appetite. To learn more about franchise opportunities, visit twinpeaksfranchise.com. For more information, visit twinpeaksrestaurant.com.

Forward-Looking Statements This press release contains forward-looking statements within the meaning of the Private Securities Litigation Reform Act of 1995, including statements relating to the company’s future operating performance. Forward-looking statements reflect the expectations of management concerning the future and are subject to significant business, economic and competitive risks, uncertainties, and contingencies. These factors are difficult to predict and beyond our control and could cause our actual results to differ materially from those expressed or implied in such forward-looking statements. We refer you to the documents that are filed from time to time by Twin Hospitality Group Inc. with the Securities and Exchange Commission, such as its reports on Form 10-K, Form 10-Q and Form 8-K, for a discussion of these and other factors. We undertake no obligation to update any forward-looking statement to reflect events or circumstances occurring after the date of this press release.

EPOS offers premium commercial and enterprise audio solutions

Transaction enhances and broadens our Kensington computer accessories portfolio into the large global enterprise headset category

Provides key third-party certifications across major unified communications platforms

Attractive purchase price with ultimate synergy savings of approximately $15 million

LAKE ZURICH, Ill.–(BUSINESS WIRE)– ACCO Brands Corporation (NYSE: ACCO) a global leader in branded office and learning products and technology accessories, today announced it has entered into a definitive agreement to acquire EPOS from Demant A/S, a leading Danish hearing healthcare company.

Based in Copenhagen, Denmark, EPOS provides a comprehensive range of premium enterprise wired and wireless headsets, and other audio solutions, that build on over a century of research in psychoacoustics. The EPOS product line is designed to reduce listening fatigue, improve voice clarity and support cognitive performance. The combination of technological innovation and audio excellence has allowed EPOS to earn certification by all major unified communication platforms, making it one of a select group of industry participants with this distinction. Built on the former joint venture between Demant A/S and Sennheiser, EPOS has a long history of delivering premium, feature rich audio solutions, supported by excellent innovation, design and customer experience.

“We are excited to welcome EPOS to the ACCO Brands portfolio. This transaction aligns with our strategy to invest in markets with better growth profiles,” said Tom Tedford, ACCO Brands President and CEO. “EPOS complements and expands our global computer accessories portfolio into the attractive premium enterprise headset category, which is estimated to be $1.7 billion. The addition of EPOS will allow ACCO Brands to deliver a more complete line of workspace technology accessory solutions to our enterprise customers,” said Mr. Tedford.

“I am delighted that ACCO Brands, the owner of Kensington, recognizes the value and the distinctiveness of EPOS and has decided to become our new owner. I see strong synergies and exciting opportunities across both EPOS and Kensington to drive our combined business forward,” stated Jeppe Dalberg-Larsen, President of EPOS.

EPOS generates approximately $80 million in annual revenue. The combination of EPOS and Kensington is expected to drive operational efficiencies, improve sales productivity, and unlock significant synergies. These synergies are expected to be realized over the next two years, with ultimate cost synergies expected to be within the range of $10 to $15 million. As we implement these synergies, we expect 2026 profit to be modestly positive. Restructuring charges are expected to be approximately $7 million.

The transaction is valued at $11.7 million, including up to $3.5 million in deferred payments, funded by ACCO Brands’ existing cash resources. The deal is expected to close in January 2026, subject to customary closing conditions.

About ACCO Brands Corporation

ACCO Brands is the leader in branded consumer products that enable productivity, confidence and enjoyment while working, when learning and while playing. Our widely recognized brands, include AT-A-GLANCE®, Five Star®, Kensington®, Leitz®, Mead®, PowerA®, Swingline®, Tilibra® and many others. More information about ACCO Brands Corporation (NYSE: ACCO) can be found at www.accobrands.com

About Demant A/S

Demant is a world-leading hearing healthcare group built on a heritage of care, health and innovation since 1904. The Group offers innovative technologies, solutions and expertise to help people hear better. In every aspect, from hearing care and hearing aids to diagnostic equipment and services, Demant is active and engaged. Headquartered in Denmark, the Group employs more than 22,000 people globally and is present with solutions in 130 countries creating life-changing differences through hearing health. William Demant Foundation holds the majority of shares in Demant A/S, which is listed on Nasdaq Copenhagen and among the 25 most traded stocks. www.demant.com

Forward-Looking Statements

Statements contained herein, other than statements of historical fact, particularly those anticipating future financial performance, business prospects, growth, strategies, business operations and similar matters, results of operations, liquidity and financial condition, and those relating to synergies, cost reductions, anticipated pre-tax savings, restructuring costs and the satisfaction of closing conditions for the subject transaction are “forward-looking statements” within the meaning of the Private Securities Litigation Reform Act of 1995. These statements are based on the beliefs and assumptions of management based on information available to us at the time such statements are made. These statements, which are generally identifiable by the use of the words “will,” “believe,” “expect,” “intend,” “anticipate,” “estimate,” “forecast,” “future”, “project,” “plan,” and similar expressions, are subject to certain risks and uncertainties, are made as of the date hereof, and we undertake no duty or obligation to update them. Forward-looking statements are subject to the occurrence of events outside the Company’s control and actual results, and the timing of events may differ materially from those suggested or implied by such forward-looking statements due to numerous factors that involve substantial known and unknown risks and uncertainties. Investors and others are cautioned not to place undue reliance on forward-looking statements when deciding whether to buy, sell or hold the Company’s securities.

Our outlook is based on certain assumptions which we believe to be reasonable under the circumstances. These include, without limitation, assumptions regarding consumer demand, tariffs, global geopolitical and economic uncertainties, and fluctuations in foreign currency exchange rates; and the other factors described below.

Among the factors that could cause our actual results to differ materially from our forward-looking statements are: the occurrence of any event, change or other circumstances that could give rise to the right of ACCO Brands or Demant to terminate the transaction, the possibility that the transaction is not completed or, if completed, that the anticipated benefits of the transaction are not realized when expected or at all, including as a result of the impact of, or problems arising from, the integration of EPOS, operating costs and business disruption following the transaction, the integration of EPOS’ products and our ability to realize synergies in the integration, as well as changes in trade policy and regulations, including changes in trade agreements and the imposition of tariffs, and the resulting consequences; global political and economic uncertainties; a limited number of large customers account for a significant percentage of our sales; sales of our products are affected by general economic and business conditions globally and in the countries in which we operate; risks associated with foreign currency exchange rate fluctuations; challenges related to the highly competitive business environment in which we operate; our ability to develop and market innovative products that meet consumer demands and to expand into new and adjacent product categories; our ability to successfully expand our business in emerging markets and the exposure to greater financial, operational, regulatory, compliance and other risks in such markets; the continued decline in the use of certain of our products; risks associated with seasonality, the sufficiency of investment returns on pension assets, risks related to actuarial assumptions, changes in government regulations and changes in the unfunded liabilities of a multi-employer pension plan; any impairment of our intangible assets; our ability to secure, protect and maintain our intellectual property rights, and our ability to license rights from major gaming console makers and video game publishers to support our gaming accessories business; our ability to grow profitably through acquisitions, and successfully integrate them; our ability to successfully execute our multi-year restructuring and cost savings program and realize the anticipated benefits; continued disruptions in the global supply chain; risks associated with inflation and other changes in the cost or availability of raw materials, transportation, labor, and other necessary supplies and services and the cost of finished goods; risks associated with outsourcing production of certain of our products, information technology systems and other administrative functions; the failure, inadequacy or interruption of our information technology systems or their supporting infrastructure; risks associated with a cybersecurity incident or information security breach, including that related to a disclosure of personally identifiable information; risks associated with our indebtedness, including limitations imposed by restrictive covenants, our debt service obligations, and our ability to comply with financial ratios and tests; a change in or discontinuance of our stock repurchase program or the payment of dividends; product liability claims, recalls or regulatory actions; the impact of litigation or other legal proceedings; the impact of additional tax liabilities stemming from our global operations and changes in tax laws, regulations and tax rates; our failure to comply with applicable laws, rules and regulations and self-regulatory requirements, the costs of compliance and the impact of changes in such laws; our ability to attract and retain qualified personnel; the volatility of our stock price; risks associated with circumstances outside our control, including those caused by telecommunication failures, labor strikes, power and/or water shortages, public health crises, such as the occurrence of contagious diseases, severe weather events, war, terrorism and other geopolitical incidents; and other risks and uncertainties described in “Part I, Item 1A. Risk Factors” in our Annual Report on Form 10-K for the year ended December 31, 2024, and in other reports we file with the Securities and Exchange Commission.

For further information:

Christopher McGinnis Investor Relations (847) 796-4320

NEW YORK, Dec. 17, 2025 (GLOBE NEWSWIRE) — Xcel Brands, Inc. (NASDAQ: XELB) (“Xcel” or the “Company”), announces today that it has entered into a securities purchase agreement for a private investment in public equity (“PIPE”) financing that is expected to result in gross proceeds to the Company of approximately $2.05 million, before deducting placement agent fees and offering expenses.

The Company intends to use the net proceeds from the offering for general corporate purposes and working capital.

Pursuant to the terms of the securities purchase agreement, the Company is selling an aggregate of 1,670,055 shares of common stock (or pre-funded warrants in lieu thereof) and common stock purchase warrants to purchase up to 835,023 shares of common stock at a purchase price of $1.2275 per share (or pre-funded warrants in lieu thereof) and one-half common stock purchase warrant, subject to certain beneficial ownership limitations set by each holder. The warrants issued in the offering are exercisable at an exercise price of $3.00 per share, subject to adjustment as provided therein, and will expire five years from the date of issuance.

Wellington Shields & Co. LLC acted as the sole placement agent for the PIPE financing.

The unregistered shares of common stock, pre-funded warrants and warrants sold in the PIPE financing described above were offered under Section 4(a)(2) of the Securities Act of 1933, as amended (the “Act”) and Regulation D promulgated thereunder and, along with the shares of common stock underlying the pre-funded warrants and warrants, have not been registered under the Act or applicable state securities laws. Accordingly, the shares of common stock, the pre-funded warrants, the warrants and the shares of common stock underlying the pre-funded warrants and warrants may not be offered or sold in the United States absent registration with the Securities and Exchange Commission (“SEC”) or an applicable exemption from such registration requirements. The securities were offered only to accredited investors. Pursuant to the terms of the securities purchase agreement with the investors, the Company has agreed to file one or more registration statements with the SEC covering the resale of the unregistered shares of common stock and the shares issuable upon exercise of the unregistered pre-funded warrants and warrants.

This press release shall not constitute an offer to sell or the solicitation of an offer to buy these securities, nor shall there be any sale of these securities in any state or jurisdiction in which such offer, solicitation or sale would be unlawful prior to registration or qualification under the securities laws of any such state or jurisdiction.

About Xcel Brands

Xcel Brands, Inc. (NASDAQ: XELB) is a media and consumer products company engaged in the design, licensing, marketing, live streaming, and social commerce sales of branded apparel, footwear, accessories, fine jewelry, home goods and other consumer products, and the acquisition of dynamic consumer lifestyle brands. Xcel was founded in 2011 with a vision to reimagine shopping, entertainment, and social media as social commerce. Xcel owns the Halston, Judith Ripka, and C. Wonder brands, as well as the co-branded collaboration brands TowerHill by Christie Brinkley, Trust. Respect. Love by Cesar Millan, and GemmaMade by Gemma Stafford, and also holds noncontrolling interests or long-term license agreements in Orme Live, and Mesa Mia Live by Jenny Martinez. Xcel also owns and manages the Longaberger brand through its controlling interest in Longaberger Licensing, LLC. Xcel is pioneering a modern consumer products sales strategy which includes the promotion and sale of products under its brands through interactive television, digital live-stream shopping, social commerce, brick-and-mortar retailers, and e-commerce channels to be everywhere its customers shop. The company’s previously owned and current brands have generated in excess of $5 billion in retail sales via livestreaming in interactive television and digital channels alone, and over 20,000 hours of content production time in live-stream and social commerce. The brand portfolio reaches in excess of 46 million social media followers with broadcast reach into 200 million households. Headquartered in New York City, Xcel Brands is led by an executive team with significant live streaming, production, merchandising, design, marketing, retailing, and licensing experience, and a proven track record of success in elevating branded consumer products companies. For more information, visit www.xcelbrands.com.

NEW YORK–(BUSINESS WIRE)– Vince Holding Corp. (Nasdaq: VNCE) (“VNCE” or the “Company”), a global contemporary retailer, today reported its financial results for the third quarter ended November 1, 2025.

Brendan Hoffman, Chief Executive Officer of VNCE said, “We are extremely proud of our third quarter performance, delivering healthy sales growth across all channels while exceeding expectations for both top and bottom line results. Our direct-to-consumer segment is showing broad-based strength benefiting from enhancements we have made to the customer experience. This includes the store renovations from earlier this year, as well as an e-commerce site refresh, increased marketing support, and the launch of drop-ship capabilities expanding the breadth and depth of our assortment online in the third quarter. This momentum has continued into the fourth quarter with a record holiday sales weekend in direct-to-consumer. As we look ahead, I’m more confident than ever in our trajectory as we successfully balance disciplined execution with strategic reinvestment to position the Vince Holding Corp. platform for sustained long-term profitable growth.”

In this press release, the Company is presenting its financial results in conformity with U.S. generally accepted accounting principles (“GAAP”) as well as on an “adjusted” basis. Adjusted results presented in this press release are non-GAAP financial measures. See “Non-GAAP Financial Measures” below for more information about the Company’s use of non-GAAP financial measures and Exhibit 3 and Exhibit 4 to this press release for a reconciliation of GAAP measures to such non-GAAP measures.

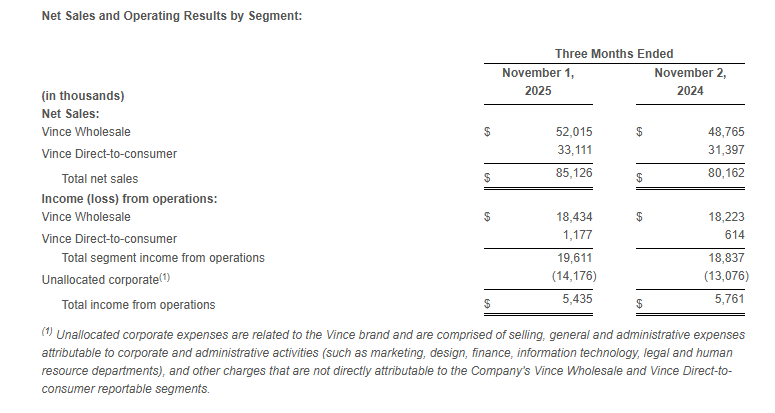

For the third quarter ended November 1, 2025:

Total Company net sales increased 6.2% to $85.1 million compared to $80.2 million in the third quarter of fiscal 2024. The year-over-year increase was driven by a 6.7% increase in the wholesale segment and a 5.5% increase in direct-to-consumer segment.

Gross profit was $41.9 million, or 49.2% of net sales, compared to gross profit of $40.1 million, or 50.0% of net sales, in the third quarter of fiscal 2024. The decrease in gross margin rate was primarily driven by approximately 260 basis points due to the unfavorable impact of higher tariffs and approximately 100 basis points due to increased freight costs, partially offset by a 140 basis points increase due to the favorable impact of lower product costing and higher pricing, and approximately 110 basis points due to the favorable impact of lower discounting.

Selling, general, and administrative expenses were $36.5 million, or 42.8% of sales, compared to $34.3 million, or 42.8% of sales, in the third quarter of fiscal 2024. The increase in SG&A dollars was primarily driven by compensation and benefits and marketing and advertising costs.

Income from operations was $5.4 million compared to income from operations of $5.8 million in the same period last year.

Income tax expense was $2.0 million compared to an income tax expense of $0 in the same period last year. The increase is due to the impact of applying the Company’s estimated annual effective tax rate to the year-to-date ordinary pre-tax income. In the prior comparative period, the Company had year-to-date ordinary pre-tax losses for the interim period and as such, the Company did not record any tax expense.

Net income was $2.7 million or $0.21 per diluted share compared to net income of $4.3 million or $0.34 per diluted share in the same period last year.

Adjusted EBITDA* was $6.5 million compared to $7.4 million in the same period last year.

The Company ended the quarter with 60 company-operated Vince stores, a net decrease of 1 store since the third quarter of fiscal 2024.

Third Quarter Review

Net sales increased 6.2% to $85.1 million as compared to the third quarter of fiscal 2024.

Wholesale segment sales increased 6.7% to $52.0 million compared to the third quarter of fiscal 2024.

Direct-to-consumer segment sales increased 5.5% to $33.1 million compared to the third quarter of fiscal 2024.

Income from operations excluding unallocated corporate expenses was $19.6 million compared to income from operations of $18.8 million in the same period last year.

Balance Sheet

At the end of the third quarter of fiscal 2025, total borrowings under the Company’s debt agreements totaled $36.1 million and the Company had $47.3 million of excess availability under its revolving credit facility.

Net inventory at the end of the third quarter of fiscal 2025 was $75.9 million compared to $63.8 million at the end of the third quarter of fiscal 2024. The year-over-year increase in inventory includes approximately $4.2 million of higher inventory carrying value due to tariffs.

During the quarter ended November 1, 2025, the Company issued and sold 370,878 shares of common stock under the Virtu At-the-Market Offering for aggregate net proceeds of $1,291 at an average price of $3.55 per share. The Company continues to have shares available under the program to exercise with proceeds to be used as sources, along with cash from operations, to fund future growth.

Outlook

For the fourth quarter of fiscal 2025 the Company expects the following:

Net sales to increase approximately 3% to 7% compared to the prior year period.

Adjusted operating income as a percentage of net sales to be approximately 0% to 2%.

Adjusted EBITDA as a percentage of net sales to be approximately 2% to 4%.

For fiscal 2025 the Company expects the following:

Net sales to increase approximately 2% to 3% compared to the prior year.

Adjusted operating income as a percentage of net sales to be approximately 2% to 3%.

Adjusted EBITDA as a percentage of net sales to be approximately 4% to 5%.

The above guidance for the fourth quarter of fiscal 2025 assumes $4 million to $5 million in expected incremental tariff costs, of which the Company expects to continue to partially offset through its mitigation strategies.

Strategic Partnership with Authentic Brands Group

On May 25, 2023, the Company announced that it completed the previously announced transaction (the “Authentic Transaction”) with Authentic Brands Group (“Authentic”).

In connection with the Authentic Transaction, VNCE entered into an exclusive, long-term license agreement (the “License Agreement”) with Authentic for usage of the contributed intellectual property for VNCE’s existing business in a manner consistent with the Company’s current wholesale, retail and e-commerce operations. The License Agreement contains an initial ten-year term and eight ten-year renewal options allowing VNCE to renew the agreement.

*Non-GAAP Financial Measures

In addition to reporting financial results in accordance with GAAP, the Company has provided, with respect to the financial results relating to the three and nine months ended November 1, 2025 and November 2, 2024, adjusted EBITDA, which is a non-GAAP measure. Adjusted EBITDA is calculated as earnings before interest, taxes, depreciation and amortization, share-based compensation, capitalized cloud computing amortization, ERC benefit, and gain on sale of Rebecca Taylor, Inc. and its wholly owned subsidiary (“Gain on Sale of Subsidiary”). For the three and nine months ended November 1, 2025 and November 2, 2024, respectively, the Company has provided adjusted income from operations, adjusted income (loss) before income taxes and equity in net income of equity method investment, adjusted income before equity in net income of equity method investment, adjusted net income, and adjusted earnings per share, which are non-GAAP measures, in order to eliminate the effect of the ERC benefit, Discrete Tax Effect Associated with ERC benefit, and Gain on Sale of Subsidiary.

The Company believes that the presentation of these non-GAAP measures facilitates an understanding of the Company’s continuing operations without the impact associated with the aforementioned items. While these types of events can and do recur periodically, they are excluded from the indicated financial information due to their impact on the comparability of earnings across periods. Non-GAAP financial measures should not be considered in isolation from, or as a substitute for, financial information prepared in accordance with GAAP. A reconciliation of GAAP to non-GAAP results has been provided in Exhibit 3 and Exhibit 4 to this press release.

Conference Call

A conference call to discuss the third quarter results will be held today, December 9, 2025, at 8:30 a.m. ET, hosted by Vince Holding Corp. Chief Executive Officer, Brendan Hoffman, and Chief Financial Officer, Yuji Okumura. During the conference call, the Company may make comments concerning business and financial developments, trends and other business or financial matters. The Company’s comments, as well as other matters discussed during the conference call, may contain or constitute information that has not been previously disclosed.

Those who wish to participate in the call may do so by dialing (833) 470-1428, conference ID 579552. Any interested party will also have the opportunity to access the call via the Internet at http://investors.vince.com/. To listen to the live call, please go to the website at least 15 minutes early to register and download any necessary audio software. For those who cannot listen to the live broadcast, a recording will be available for 12 months after the date of the event. Recordings may be accessed at http://investors.vince.com.

ABOUT VINCE HOLDING CORP.

Vince Holding Corp. is a global retail company that operates the Vince brand women’s and men’s ready to wear business. Vince, established in 2002, is a leading global luxury apparel and accessories brand best known for creating elevated yet understated pieces for every day effortless style. Vince Holding Corp. operates 46 full-price retail stores, 14 outlet stores, and its e-commerce site, as well as through premium wholesale channels globally. Please visit www.vince.com for more information.

Forward-Looking Statements: This document, and any statements incorporated by reference herein contain forward-looking statements under the Private Securities Litigation Reform Act of 1995. Forward-looking statements include the statements under “Outlook” above as well as statements regarding, among other things, our current expectations about possible or assumed future results of operations of the Company and are indicated by words or phrases such as “may,” “will,” “should,” “believe,” “expect,” “seek,” “anticipate,” “intend,” “estimate,” “plan,” “target,” “project,” “forecast,” “envision” and other similar phrases. Although we believe the assumptions and expectations reflected in these forward-looking statements are reasonable, these assumptions and expectations may not prove to be correct and we may not achieve the results or benefits anticipated. These forward-looking statements are not guarantees of actual results, and our actual results may differ materially from those suggested in the forward-looking statements. These forward-looking statements involve a number of risks and uncertainties, some of which are beyond our control, including, without limitation: changes to and unpredictability in the trade policies and tariffs imposed by the U.S. and the governments of other nations; our ability to maintain adequate cash flow from operations or availability under our revolving credit facility to meet our liquidity needs; general economic conditions; restrictions on our operations under our credit facilities; our ability to improve our profitability; our ability to maintain our larger wholesale partners; our ability to accurately forecast customer demand for our products; our ability to maintain the license agreement with ABG Vince, a subsidiary of Authentic Brands Group; ABG Vince’s expansion of the Vince brand into other categories and territories; ABG Vince’s approval rights and other actions; our ability to realize the benefits of our strategic initiatives; the execution of our customer strategy; our ability to make lease payments when due; our ability to open retail stores under favorable lease terms and operate and maintain new and existing retail stores successfully; our operating experience and brand recognition in international markets; our ability to remediate the identified material weakness in our internal control over financial reporting; our ability to comply with domestic and international laws, regulations and orders; increased scrutiny regarding our approach to sustainability matters and environmental, social and governance practices; competition in the apparel and fashion industry; the transition associated with the appointment of new chief executive officer and new chief financial officer; our ability to attract and retain key personnel; seasonal and quarterly variations in our revenue and income; the protection and enforcement of intellectual property rights relating to the Vince brand; our ability to successfully conclude remaining matters following the wind down of the Rebecca Taylor business; the extent of our foreign sourcing; our reliance on independent manufacturers; our ability to ensure the proper operation of the distribution facilities by third-party logistics providers; fluctuations in the price, availability and quality of raw materials; the ethical business and compliance practices of our independent manufacturers; our ability to mitigate system or data security issues, such as cyber or malware attacks, as well as other major system failures; our ability to adopt, optimize and improve our information technology systems, processes and functions; our ability to comply with privacy-related obligations; our status as a “controlled company”; our status as a “smaller reporting company”; and other factors as set forth from time to time in our Securities and Exchange Commission filings, including those described under “Item 1A—Risk Factors” in our Annual Report on Form 10-K and Quarterly Reports on Form 10-Q. We intend these forward-looking statements to speak only as of the time of this release and do not undertake to update or revise them as more information becomes available, except as required by law.

Seasoned Technology Executive to Drive AI, Digital Commerce, and Cybersecurity Innovation

JERICHO, N.Y., Dec. 8, 2025 /PRNewswire/ — Today, 1-800-FLOWERS.COM, Inc. (NASDAQ: FLWS), a leading provider of thoughtful expressions designed to help inspire customers to express and connect, announced the appointment of Alexander Zelikovsky as Chief Information Officer. Zelikovsky’s appointment accelerates the company’s ongoing transformation strategy under CEO Adolfo Villagomez.

As Chief Information Officer, Zelikovsky will lead an enterprise-wide technology strategy to accelerate the company’s digital transformation. His responsibilities include IT applications and platforms, data architecture, data management, cybersecurity, and business intelligence. Zelikovsky will also support the organization’s AI and business optimization efforts by ensuring the technology, data, and platforms are in place to help these initiatives succeed — strengthening the company’s ability to deliver exceptional customer-centric experiences and drive omnichannel growth. He will report directly to 1-800-FLOWERS.COM, Inc. CEO Adolfo Villagomez.

“Alex is a visionary technology leader with proven expertise leading digital transformation initiatives at scale,” said Adolfo Villagomez, CEO of 1-800-FLOWERS.COM, Inc. “His ability to position technology to fuel business growth, enhance operational efficiency, and deliver personalized customer experiences is all critical to driving our transformation strategy forward. His experience in enterprise modernization, AI, and cybersecurity will be instrumental in accelerating growth and innovation across our portfolio. We are thrilled to have Alex join the organization.”

Zelikovsky brings more than 25 years of technology leadership experience, transforming traditional businesses into digital enterprises at global scale. Most recently, he served as Executive Vice President and Global CIO at Pitney Bowes. Prior to that, he held divisional CIO and Head of Digital Technology roles at Kimberly-Clark for both the EMEA and Latin America regions, where he executed comprehensive IT transformation strategies that drove significant business turnarounds and operating profit growth.

“I’m excited to join 1-800-FLOWERS.COM at such a pivotal time in the company’s transformation,” said Zelikovsky. “Adolfo’s vision for building a consumer-centric organization resonates deeply with my approach to technology leadership. The company has built an exceptional portfolio of brands and understands the importance of delivering meaningful and personalized customer experiences. I look forward to partnering with the leadership team to harness technology, data, and innovation to deepen customer relationships, drive operational excellence, and accelerate growth across the business.”

Before joining Kimberly-Clark, Zelikovsky drove the development and execution of Bed Bath & Beyond’s omnichannel technology strategy and was instrumental in building out their multibillion-dollar digital commerce business. His journey into digital technology began at Amazon.com, where he was part of the team that pioneered Amazon’s global distribution network. He has also held senior technology and operations roles at Procter & Gamble and Sephora/LVMH.

Zelikovsky holds an MBA from the University of Chicago’s Booth School of Business and a bachelor’s degree from Brooklyn College, City University of New York. He is the author of “Achieving Stretch Goals Efficiently” and has served as an adjunct professor at Purdue University’s Krannert School of Management, where he developed and taught a graduate course in e-Commerce Strategy and Operations.

About 1-800-FLOWERS.COM, Inc. 1-800-FLOWERS.COM, Inc. is the premier destination for meaningful gifting, helping people express and connect through thoughtful giving. As an omnichannel retailer, the company’s portfolio includes more than 18 premium brands, such as 1-800-Flowers.com®, Harry & David®, PersonalizationMall.com®, and Things Remembered®. 1-800-FLOWERS.COM, Inc. also supports local community businesses nationwide through BloomNet®, its network of local florists and merchants, that enables same-day delivery. The company also operates Napco®, a leading resource for floral gifts and seasonal décor, and DesignPac Gifts, LLC, a manufacturer of gift baskets and towers