ISG (Information Services Group) (Nasdaq: III) is a leading global technology research and advisory firm. A trusted business partner to more than 700 clients, including more than 75 of the world’s top 100 enterprises, ISG is committed to helping corporations, public sector organizations, and service and technology providers achieve operational excellence and faster growth. The firm specializes in digital transformation services, including automation, cloud and data analytics; sourcing advisory; managed governance and risk services; network carrier services; strategy and operations design; change management; market intelligence and technology research and analysis. Founded in 2006, and based in Stamford, Conn., ISG employs more than 1,300 digital-ready professionals operating in more than 20 countries—a global team known for its innovative thinking, market influence, deep industry and technology expertise, and world-class research and analytical capabilities based on the industry’s most comprehensive marketplace data. For additional information, visit www.ISG-One.com

Joe Gomes, Managing Director, Equity Research Analyst, Generalist , Noble Capital Markets, Inc.

Joshua Zoepfel, Research Associate, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

August. Information Services Group announced yesterday that the Company’s Executive Vice President and CFO Bert Alfonso will be retiring in August to devote more time to family matters. Michael A. Sherrick will be succeeding him effective August 7th. Mr. Sherrick will report to chairman and CEO Michael Connors and join the ISG Executive Board.

Michael Sherrick’s Background. Mr. Sherrick provides ISG with over 25 years of financial and operating experience, as his most recent position was from Cognizant Software & Platform Engineering as senior vice president and chief operating officer. Cognizant Technology Solutions Corporation is a global provider of information technology, consulting and business process services, similar to ISG.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

Sherrick brings significant tech industry, operational and financial expertise to role

STAMFORD, Conn.–(BUSINESS WIRE)– Information Services Group (ISG) (Nasdaq: III), a leading global technology research and advisory firm, today announced that Humberto “Bert” Alfonso, executive vice president and chief financial officer, will retire in August to devote more time to family matters and that Michael A. Sherrick has been named to succeed him, effective August 7.

“I want to express my deepest gratitude to Bert for his valued service to ISG,” said Michael P. Connors, chairman and CEO. “I have known Bert for many years and will miss his wise counsel and contributions to the firm. Everyone here at ISG extends our best wishes to Bert and his family.”

Sherrick joins ISG from Cognizant Technology Solutions Corporation, a $19 billion global provider of information technology, consulting and business process services. He currently serves as senior vice president and chief operating officer of Cognizant Software & Platform Engineering.

At ISG, Sherrick will have global responsibility for finance, investor relations, legal, and mergers and acquisitions. He will report to Connors and join the internal ISG Executive Board.

“I am delighted Michael is joining ISG,” said Connors. “With his unique combination of technology industry knowledge, experience in operations, strategy and finance, and background in investment banking and financial services, Michael will quickly become a key contributor in advancing our ISG NEXT operating model and helping us drive growth and value in the years ahead.”

Sherrick brings more than 25 years of financial and operating experience to ISG. He joined Cognizant in 2016 where he was appointed to a series of roles, including COO of Cognizant Digital Systems and Technology and COO of Cognizant Americas, before assuming his current position.

Prior to joining Cognizant, in 2013 Sherrick co-founded Scoria Capital Partners, where, as a portfolio manager, he managed the firm’s investments in the technology, business services and consumer sectors. Earlier in his career, he held positions with S.A.C. Capital, Morgan Stanley and PwC, among others. Sherrick holds a B.A. degree in economics from Bucknell University and is both a licensed certified public accountant (CPA) and a chartered financial analyst (CFA).

About ISG

ISG (Information Services Group) (Nasdaq: III) is a leading global technology research and advisory firm. A trusted business partner to more than 900 clients, including more than 75 of the world’s top 100 enterprises, ISG is committed to helping corporations, public sector organizations, and service and technology providers achieve operational excellence and faster growth. The firm specializes in digital transformation services, including automation, cloud and data analytics; sourcing advisory; managed governance and risk services; network carrier services; strategy and operations design; change management; market intelligence and technology research and analysis. Founded in 2006, and based in Stamford, Conn., ISG employs more than 1,600 digital-ready professionals operating in more than 20 countries—a global team known for its innovative thinking, market influence, deep industry and technology expertise, and world-class research and analytical capabilities based on the industry’s most comprehensive marketplace data. For more information, visit www.isg-one.com.

With BlackRock filing for a Bitcoin-related ETF this month, and then Citadel, Charles Schwab, and Fidelity backing a cryptocurrency exchange, there is again talk of Bitcoin (BTC) more than retracing its previous all-time high. BlackRock’s proposed product is designed, as are other crypto ETFs, to trade like a stock. This helps satisfy those that want ease of trading, exposure of their qualified retirement money, and all investments on one statement. A consolidated statement is also a benefit of Citadel, Schwab, and Fidelity’s exchange plans.

This adds fuel to the momentum Bitcoin has relative to other assets.

Another reason for increased expectations for Bitcoin’s performance is, next year Bitcoin’s is scheduled to halve, sometimes called its “halving event.” This halving happens every four years as Bitcoin rewards to miners are cut in half (miner’s payout will be reduced to 3.125 BTC). The event is viewed as positive for Bitcoin’s price. This is because halving helps in reducing supply. Historically, halving has brought higher Bitcoin values.

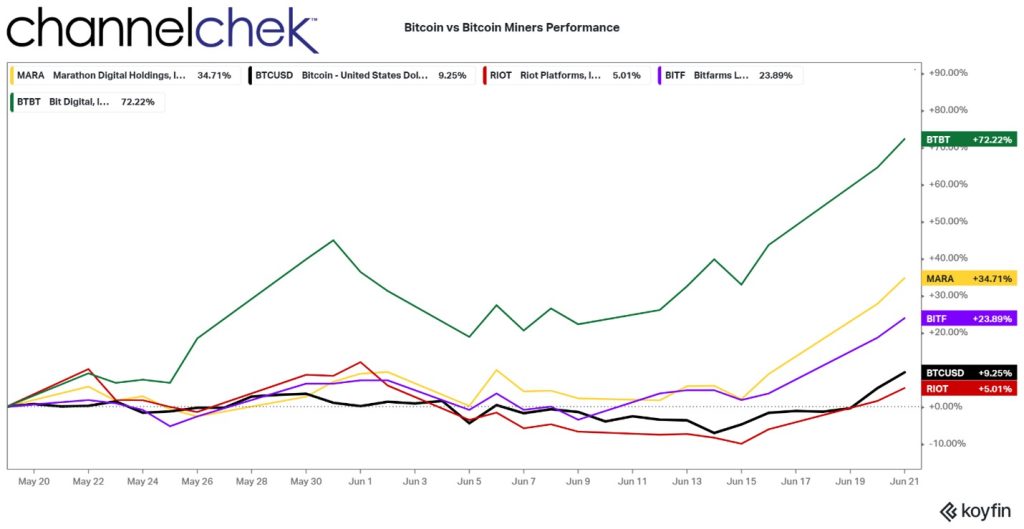

Exposure to Bitcoin price movements are, for some investors, already in their traditional brokerage accounts, and when desired, has found its way into IRA’s and other tax-advantaged retirement accounts. This is accomplished using the strong correlation between Bitcoin mining stocks, and the trend and momentum of Bitcoins measured against US Dollar value (BTCUSD) .

Over the past month as Bitcoin rose more than double that of the S&P 500 as a percentage, many Bitcoin mining stocks crushed the crypto’s performance. Both Bitcoin and Bitcoin miners historically move in the same direction, but the magnitude varies.

Currently, many mining stocks are experiencing a much greater magnitude.

To demonstrate how mining stocks provide stock portfolios the overall direction of Bitcoin, but differ in terms of degree, the chart above plots four Bitcoin mining companies against the BTCUSD. The overall direction is visually correlated to $Dollar/Bitcoin percentage moves. However, there are huge variations in that performance. The top performer represented above is Bit Digital, Inc. (BTBT). The New York-headquartered, large-scale mining business, with operations across the U.S. and Canada also acts as a validator of Ethereum. This is common stock and avoids the contortions and management fees of gaining exposure through an ETF, and of course, can be obtained through an investors traditional stockbroker. While Bit Digital rose 72.22% during the last 30 days, Bitcoin rose near 10%.

The weakest Bitcoin mining company pictured here is Riot. Riot has deployed one of the mining industry’s largest fleets of self-mining hardware. While the period represented above is only the past 30 days, Bitcoin strength is still represented in this laggard.

Take Away

The new possibility that BlackRock gets approval for a Bitcoin ETF and that a consortium of brokerage firms create a crypto exchange, is expected to lead to a growth in demand for cryptocurrency. Investors may be able to capture directional performance of Bitcoin using the stocks of Bitcoin miners, and have these assets listed on their current brokerage holding reports, and even house them in qualified tax-advantaged accounts.

The launch of a Bitcoin ETF could certainly help increase exposure to the token and drive up demand because it makes it easier for consumers to purchase, and crypto exchanges have also come under regulatory scrutiny as of late. If an investor is looking to accomplish this, they may wish to evaluate whether they can meet their needs using Bitcoin mining stocks.

Featured product launches top the agenda for the industry’s leading conference for technology and business providers, September 11-13, in Dallas

STAMFORD, Conn.–(BUSINESS WIRE)– Information Services Group (ISG) (Nasdaq: III), a leading global technology research and advisory firm, said today it will unveil a groundbreaking SaaS-based sourcing platform and a new research and advisory service for enterprise-scale AI at its 2023 ISG Sourcing Industry Conference (SIC), the industry’s premier annual event for service and technology providers, this September.

The next-gen sourcing platform, currently under development, will digitize all elements of ISG’s market-leading sourcing transactions business to better serve clients, improve transaction speed and efficiency and allow ISG to expand into other market segments. The SaaS solution will draw on ISG’s unmatched data assets, intellectual property and proprietary tools – supported by AI to provide real-time insights and predictive analytics and streamline the entire transaction process to accelerate time to agreement.

“Speed and current market data are especially critical to our clients in today’s environment where many more sourcing transactions of varying sizes and complexity are required to power the modern digital enterprise. Agility and market-pricing insights are key competitive advantages,” said Todd Lavieri, vice chairman of ISG and president of ISG Americas and Asia Pacific. “Our next-gen sourcing platform will meet these needs and strengthen our position as the industry’s sourcing advisor of choice, helping our clients drive even better business results.”

During the 17th annual SIC, September 11–13 in Frisco, Tex., near Dallas, ISG will also unveil a new research and advisory service dedicated to helping clients understand the business implications of adopting AI at scale, develop the right technical infrastructure for such implementations, and evaluate, source and prepare their organizations to adopt enterprise-scale AI solutions.

“ISG has always been a leader in refining and redefining the IT sourcing advisory market,” Lavieri said. “The AI claims, benefits and capabilities being discussed across the market need independent, third-party evaluations.”

Lavieri noted companies seeking to implement enterprise AI at scale will face a unique set of challenges, especially amid the public debate and controversy triggered by AI models like ChatGPT.

“With our industry-leading IT provider research and insights, ISG is uniquely positioned to guide our clients through this complex process, ensuring they can adopt AI at scale – technically, securely and ethically – to maximize ROI and business value,” he said.

ISG will soon publish a new report, “The State of Enterprise AI 2023,” based on its extensive research into the market for enterprise AI and its evaluations of the pure-play AI solutions providers that are meeting the early demand for such capabilities. The study will point to what Fortune 500 leaders have accomplished in their first steps toward enterprise-grade AI, and the assets and methodologies cutting-edge providers are using to help clients achieve their objectives.

The two new ISG capabilities will be showcased in front of an audience of hundreds of sourcing industry leaders who will gather at the SIC in September, at the Westin Dallas Stonebriar Golf Resort & Spa. Dozens of ISG advisors will deliver keynote presentations and host panel discussions, breakout sessions and one-on-one meetings, sharing insights from real-world client engagements and the industry’s most comprehensive marketplace data.

Additional information and registration for the 2023 SIC are available on the event website.

About ISG

ISG (Information Services Group) (Nasdaq: III) is a leading global technology research and advisory firm. A trusted business partner to more than 900 clients, including more than 75 of the world’s top 100 enterprises, ISG is committed to helping corporations, public sector organizations, and service and technology providers achieve operational excellence and faster growth. The firm specializes in digital transformation services, including automation, cloud and data analytics; sourcing advisory; managed governance and risk services; network carrier services; strategy and operations design; change management; market intelligence and technology research and analysis. Founded in 2006, and based in Stamford, Conn., ISG employs more than 1,600 digital-ready professionals operating in more than 20 countries—a global team known for its innovative thinking, market influence, deep industry and technology expertise, and world-class research and analytical capabilities based on the industry’s most comprehensive marketplace data. For more information, visit www.isg-one.com.

Blackboxstocks, Inc. is a financial technology and social media hybrid platform offering real-time proprietary analytics and news for stock and options traders of all levels. Our web-based software employs “predictive technology” enhanced by artificial intelligence to find volatility and unusual market activity that may result in the rapid change in the price of a stock or option. Blackbox continuously scans the NASDAQ, New York Stock Exchange, CBOE, and all other options markets, analyzing over 10,000 stocks and up to 1,500,000 options contracts multiple times per second. We provide our users with a fully interactive social media platform that is integrated into our dashboard, enabling our users to exchange information and ideas quickly and efficiently through a common network. We recently introduced a live audio/video feature that allows our members to broadcast on their own channels to share trade strategies and market insight within the Blackbox community. Blackbox is a SaaS company with a growing base of users that spans 42 countries; current subscription fees are $99.97 per month or $959.00 annually. For more information, go to: www.blackboxstocks.com .

Joe Gomes, Managing Director, Equity Research Analyst, Generalist , Noble Capital Markets, Inc.

Joshua Zoepfel, Research Associate, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

Another Step. Blackboxstocks and Evtec Group announced the execution of a Securities Exchange Agreement (SEA) on June 9th. The SEA provides for a mutual investment between the two companies as an initial step towards completing the planned merger between Blackboxstocks and Evtec Group Limited, Evtec Aluminium Limited, and Evtec Automotive Limited (collectively “Evtec”).

Details. Under the terms of the SEA, Blackboxstocks will issue 2.4 million shares of a newly created Series B Convertible Preferred Stock in exchange for 4,086 newly issued preferred shares of Evtec Group Limited. The Series B Preferred Stock is non-voting and will be convertible into common stock on a one-for-one basis only after receiving stockholder approval. The preferred shares issued by Evtec Group are non-voting and convertible into common shares on a one-for-one basis immediately prior to, or at the time of, the merger between the companies.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

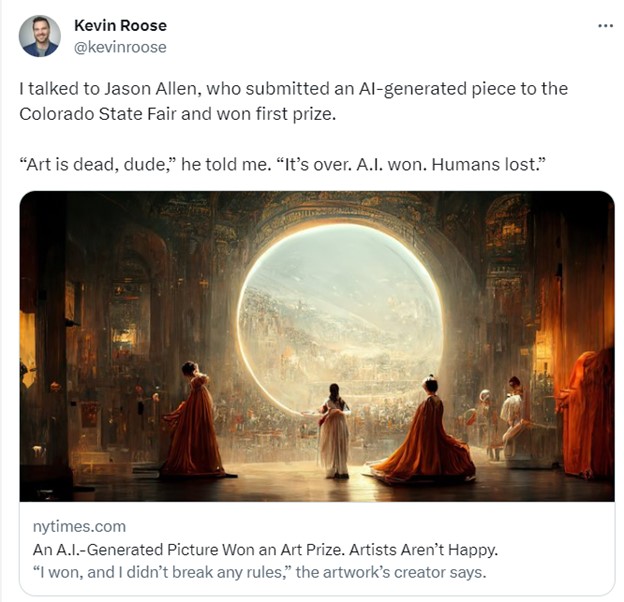

Will Copyright Law Favor Artificial Intelligence End Users?

In 2022, an AI-generated work of art won the Colorado State Fair’s art competition. The artist, Jason Allen, had used Midjourney – a generative AI system trained on art scraped from the internet – to create the piece. The process was far from fully automated: Allen went through some 900 iterations over 80 hours to create and refine his submission.

Yet his use of AI to win the art competition triggered a heated backlash online, with one Twitter user claiming, “We’re watching the death of artistry unfold right before our eyes.”

As generative AI art tools like Midjourney and Stable Diffusion have been thrust into the limelight, so too have questions about ownership and authorship.

These tools’ generative ability is the result of training them with scores of prior artworks, from which the AI learns how to create artistic outputs.

Should the artists whose art was scraped to train the models be compensated? Who owns the images that AI systems produce? Is the process of fine-tuning prompts for generative AI a form of authentic creative expression?

This article was republished with permission from The Conversation, a news site dedicated to sharing ideas from academic experts. It represents the research-based findings and thoughts of, Robert Mahari, JD-PhD Student, Massachusetts Institute of Technology (MIT), Jessica Fjeld, Lecturer on Law, Harvard Law School, and Ziv Epstein, PhD Student in Media Arts and Sciences, Massachusetts Institute of Technology (MIT).

On one hand, technophiles rave over work like Allen’s. But on the other, many working artists consider the use of their art to train AI to be exploitative.

We’re part of a team of 14 experts across disciplines that just published a paper on generative AI in Science magazine. In it, we explore how advances in AI will affect creative work, aesthetics and the media. One of the key questions that emerged has to do with U.S. copyright laws, and whether they can adequately deal with the unique challenges of generative AI.

Copyright laws were created to promote the arts and creative thinking. But the rise of generative AI has complicated existing notions of authorship.

Photography Serves as a Helpful Lens

Generative AI might seem unprecedented, but history can act as a guide.

Take the emergence of photography in the 1800s. Before its invention, artists could only try to portray the world through drawing, painting or sculpture. Suddenly, reality could be captured in a flash using a camera and chemicals.

As with generative AI, many argued that photography lacked artistic merit. In 1884, the U.S. Supreme Court weighed in on the issue and found that cameras served as tools that an artist could use to give an idea visible form; the “masterminds” behind the cameras, the court ruled, should own the photographs they create.

From then on, photography evolved into its own art form and even sparked new abstract artistic movements.

AI Can’t Own Outputs

Unlike inanimate cameras, AI possesses capabilities – like the ability to convert basic instructions into impressive artistic works – that make it prone to anthropomorphization. Even the term “artificial intelligence” encourages people to think that these systems have humanlike intent or even self-awareness.

This led some people to wonder whether AI systems can be “owners.” But the U.S. Copyright Office has stated unequivocally that only humans can hold copyrights.

So who can claim ownership of images produced by AI? Is it the artists whose images were used to train the systems? The users who type in prompts to create images? Or the people who build the AI systems?

Infringement or Fair Use?

While artists draw obliquely from past works that have educated and inspired them in order to create, generative AI relies on training data to produce outputs.

This training data consists of prior artworks, many of which are protected by copyright law and which have been collected without artists’ knowledge or consent. Using art in this way might violate copyright law even before the AI generates a new work.

Still from ‘All watched over by machines of loving grace’ by Memo Akten, 2021. Created using custom AI software. Memo Akten, CC BY-SA

For Jason Allen to create his award-winning art, Midjourney was trained on 100 million prior works.

Was that a form of infringement? Or was it a new form of “fair use,” a legal doctrine that permits the unlicensed use of protected works if they’re sufficiently transformed into something new?

While AI systems do not contain literal copies of the training data, they do sometimes manage to recreate works from the training data, complicating this legal analysis.

Will contemporary copyright law favor end users and companies over the artists whose content is in the training data?

To mitigate this concern, some scholars propose new regulations to protect and compensate artists whose work is used for training. These proposals include a right for artists to opt out of their data’s being used for generative AI or a way to automatically compensate artists when their work is used to train an AI.

Muddled Ownership

Training data, however, is only part of the process. Frequently, artists who use generative AI tools go through many rounds of revision to refine their prompts, which suggests a degree of originality.

Answering the question of who should own the outputs requires looking into the contributions of all those involved in the generative AI supply chain.

The legal analysis is easier when an output is different from works in the training data. In this case, whoever prompted the AI to produce the output appears to be the default owner.

However, copyright law requires meaningful creative input – a standard satisfied by clicking the shutter button on a camera. It remains unclear how courts will decide what this means for the use of generative AI. Is composing and refining a prompt enough?

Matters are more complicated when outputs resemble works in the training data. If the resemblance is based only on general style or content, it is unlikely to violate copyright, because style is not copyrightable.

The illustrator Hollie Mengert encountered this issue firsthand when her unique style was mimicked by generative AI engines in a way that did not capture what, in her eyes, made her work unique. Meanwhile, the singer Grimes embraced the tech, “open-sourcing” her voice and encouraging fans to create songs in her style using generative AI.

If an output contains major elements from a work in the training data, it might infringe on that work’s copyright. Recently, the Supreme Court ruled that Andy Warhol’s drawing of a photograph was not permitted by fair use. That means that using AI to just change the style of a work – say, from a photo to an illustration – is not enough to claim ownership over the modified output.

While copyright law tends to favor an all-or-nothing approach, scholars at Harvard Law School have proposed new models of joint ownership that allow artists to gain some rights in outputs that resemble their works.

In many ways, generative AI is yet another creative tool that allows a new group of people access to image-making, just like cameras, paintbrushes or Adobe Photoshop. But a key difference is this new set of tools relies explicitly on training data, and therefore creative contributions cannot easily be traced back to a single artist.

The ways in which existing laws are interpreted or reformed – and whether generative AI is appropriately treated as the tool it is – will have real consequences for the future of creative expression.

Comtech Telecommunications Corp. engages in the design, development, production, and marketing of products, systems, and services for advanced communications solutions in the United States and internationally. It operates in three segments: Telecommunications Transmission, Mobile Data Communications, and RF Microwave Amplifiers. The Telecommunications Transmission segment provides satellite earth station equipment and systems, over-the-horizon microwave systems, and forward error correction technology, which are used in various commercial and government applications, including backhaul of wireless and cellular traffic, broadcasting (including HDTV), IP-based communications traffic, long distance telephony, and secure defense applications. The Mobile Data Communications segment provides mobile satellite transceivers, and computers and satellite earth station network gateways and associated installation, training, and maintenance services; supplies and operates satellite packet data networks, including arranging and providing satellite capacity; and offers microsatellites and related components. The RF Microwave Amplifiers segment designs, develops, manufactures, and markets satellite earth station traveling wave tube amplifiers (TWTA) and broadband amplifiers. Its amplifiers are used in broadcast and broadband satellite communication; defense applications, such as telecommunications systems and electronic warfare systems; and commercial applications comprising oncology treatment systems, as well as to amplify signals carrying voice, video, or data for air-to-satellite-to-ground communications. The company serves satellite systems integrators, wireless and other communication service providers, broadcasters, defense contractors, military, governments, and oil companies. Comtech markets its products through independent representatives and value-added resellers. The company was founded in 1967 and is headquartered in Melville, New York.

Joe Gomes, Managing Director, Equity Research Analyst, Generalist , Noble Capital Markets, Inc.

Joshua Zoepfel, Research Associate, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

Delivering on the Transformation. Led by CEO Ken Peterman, Comtech is delivering on its transformation. 3Q23 was the sixth consecutive quarter of top line revenue growth, with improving adjusted EBITDA margins. The Company is seeing noticeable improvement in its growth and profit improvement initiatives, in our view.

3Q23 Results. Revenue of $136.3 million was up 1.9% sequentially, within guidance. Y-o-Y revenue was up 11.6%. We were at $136 million. Adjusted EBITDA totaled $12.5 million, versus $11.2 million in 3Q22. We were at $12.2 million. Comtech reported a net loss of $9.2 million, or a loss of $0.33 per share, compared to a net loss of $1.7 million, or $0.06 per share last year. Adjusted EPS was $0.11 versus $0.25. We had forecast a net loss of $4 million, or a loss of $0.14 per share and adjusted EPS of $0.12.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

Enabling Better Drug Discovery Outcomes with Machine Learning

Can the long road to bring new medical treatments or therapies to market be shortened by introducing artificial intelligence? AI applied to the early stage of the discovery process, which often involves new insight into a disease or treatment mechanism, may soon provide researchers many more potential candidates or designs to evaluate. AI can also help in the sorting and evaluation of these candidates to improve the success rates of those that make it into the lab for further study.

Benefits AI Brings to Biotech Research

The cost of bringing a single drug to market in terms of time and money is substantial. Estimates are in the $2.8 billion range, and the average timeline for drug development exceeds a decade. On top of this, there is a low level of certainty of taking a promising molecule all the way to market. The success rate of translating preclinical research findings into effective clinical treatments is low; failure rates are estimated to be around 90%.

The refinement of digital sorting and calculating with advanced computational technologies, such as artificial intelligence (AI) and machine learning (ML), have the potential to revolutionize pharmaceutical research and development (R&D). Despite it still being a young technology, AI-enabled applications and algorithms are already making an impact in drug discovery and development processes.

One of the significant benefits of ML in drug development is its ability to recognize patterns and unveil insights that might be missed by conventional data analysis or take substantially less time to recognize. AI, and ML technologies can help a biotech company do precursory evaluation, accelerate the design and testing of molecules, streamline the testing processes, and provide a faster understanding along the way if the molecule will perform as expected. With improved clinical success and reduced costs throughout the development pipeline, AI may be shot in the arm the industry needs.

Adoption of AI in Biotechnology

While any full-scale adoption of AI in the pharmaceutical industry is still evolving and finding its place, implementation and investment are growing. Top global pharmaceutical companies have increased their R&D investment in AI by nearly 25% over the past three years – this indicates a recognition of the perceived benefits.

The interest and investment in AI drug discovery is fueled by several factors. As touched on earlier, a more efficient and cost-effective drug development process would be of great benefit. AI can significantly reduce both time and cost. And the sooner more effective treatments are available, the better. Chronic diseases, such as cancer, autoimmune problems, neurological disorders, and cardiovascular diseases, creates an ongoing demand for improved drugs and therapies. AI’s ability to analyze vast amounts of data, identify patterns, and then learn from the information at an accelerated rate can allow researchers to shorten timelines to final conclusions.

Even more exciting is the growing availability of large datasets thanks to the rise of big data. With an increase in the volume, variety and velocity of data, and the AI-assisted ability to make sense of it, outcomes are expected to be improved. These datasets, obtained from various sources like electronic medical records and genomic databases, allow successful AI applications in drug discovery. Technological advancements, especially in ML algorithms, have been contributing to the growth of AI in medicine. And they are growing more sophisticated, allowing for accurate pattern identification in complex biological systems. Collaborations between academia, industry, and government agencies have further accelerated growth sharing knowledge and resources.

Trends in AI and ML Biotechnology

While considered a young technological field, AI-enabled drug discovery is being shaped by a number of new trends and technologies. Modern AI algorithms are now capable of analyzing intricate biological systems and foretelling the effects of medications on human cells and tissues. By detecting probable adverse effects early on in the development phase, the predictive ability helps prevent failures in the later stages.

By generating candidates that fit certain requirements, generative models can accelerate the design of completely new medications. But other technology is also now available to assist. By offering scalable processing resources, cloud computing dramatically cuts down on both time and expense. By simulating the interaction of hundreds of chemicals with disease targets, virtual drug screening enables the fast screening of drugs.

A higher understanding of disease biology and the discovery of new therapeutic targets is being made possible by integrative techniques that incorporate many data sources not available a short while ago.

Constraints on AI-Assisted Biotech Research

While AI can speed up certain aspects of drug discovery, it cannot replace most traditional lab testing. Hands-on experimentation and data collection on living organisms are expected to always be necessary, many of these processes during the clinical trial stages cannot be sped up.

Regulatory bodies, like the FDA, are also cautious about embracing AI fully, raising concerns about transparency and accountability in decision-making processes.

.

Take Away

The near future of artificial intelligence and machine learning assuming a larger role in enabling drug discovery and more efficient R&D looks bright. The technology offers real promise for more efficient and cost-effective drug development processes – this would address the need for new therapies for chronic diseases.

The time-consuming process of testing on real subjects is not expected to be replaced or overly streamlined by technology, but finding subjects and evaluating results can also benefit from the new technology.

Regulation on Artificial Intelligence Innovation is Dumb, Says IBM CEO

Is IBM’s CEO flip-flopping on the impact of artificial Intelligence on jobs? What are his thoughts on AI regulation? In an interview with Bloomberg last month, IBM’s CEO Arvind Krishna said his company would slow or suspend hiring because he expects about 30% of nearly 26,000 positions could be replaced by AI over a five-year period at his company, that was calculated as 7,800 supplanted by AI. In a new interview this month with Barron’s, Krishna addresses the expected impact on jobs and makes light of the idea that humanity is at great risk from AI technology.

Spoiler Alert, AI is Good

AI will actually create, not destroy jobs – and it is not going to destroy the world. This is the view of IBM’s CEO Krishna, discussing artificial Intelligence in a feature with Barron’s published in the most recent Tech Trader column.

Addressing AI job loss, which he has been quoted as expecting, at least for IBM, the blue-chip CEO says he’s somewhat irritated about a recent flurry of news stories that quoted him as saying that IBM could replace 7,800 workers with AI software. Krishna says his comments were taken out of context. He tried to set the record straight explaining, that he actually said was that over the next five years, 30% to 50% of repetitive white-collar jobs could be replaced by AI. He also added the bottom end of the range was most likely. The number used in the reporting came from his response to a follow-up question with the Bloomberg reporter. Krishna was asked how many IBM employees meet the description, he estimated 10%. The math, based on IBM’s workforce, was used to come up with 7,800 employees.

The IBM CEO says the calculation left out another key piece of information.

“I also said that AI is going to create more jobs than it takes away,” Krishna said, “the same way that the agricultural revolution and the services revolution created way more jobs than those that got taken away.” He says we will need new “prompt engineers” to lever AI tools, and more fact-checking to address the accelerated creation of misinformation that he thinks will inevitably accompany the creation of AI tools.

Are Their AI Risks?

On humanity’s risks from AI and potential regulation, the IBM CEO explained, the assertion by some that AI represents an existential threat to humanity—that there’s a risk that AI gets smarter than humans, and then somehow wipes us off the face of the Earth, is bunk – or highly unlikely.

“I’m not there fundamentally,” he said. “It seems like a pretty big stretch. These things are great at memorization and pattern matching. They don’t yet have a knowledge representation. They don’t have any symbolic manipulation. They do math by memory, not by understanding math. There are a lot of things that are yet to be done,” said Krishna.

It was noted in the interview that some people are using nightmare scenarios to make a case for strict regulation of artificial Intelligence and machine learning. While he agrees all should be careful about how and where they use AI, he doesn’t think aggressive regulation is called for. He even believes that any US regulation would cause cheaters within the States or competitive countries, without the imposition of US regulation, to move forward as they see appropriate.

“We don’t want to have regulation on innovation. That’s dumb actually,” said Krishna. “All you are going to do is give an advantage to those who choose to ignore the regulation and those who work outside the US boundaries.”

An AI Quantum Leap?

Quantum computing is a rapidly-emerging technology that harnesses the laws of quantum mechanics to solve problems too complex for classical computers. IBM is a leader in this field. As it relates to the potential combination of AI and quantum computing Krishna thinks we are close to the day when quantum computing will mesh with AI, and open new areas of computing power.

Krishna suggested that to explore benefits of this, one might want to consider the future of the chemical and pharmaceutical industry. “Maybe we go through reading all the literature—that’s AI—and we find some gaps in knowledge,” he says. “Today you fill in those gaps by doing a wet lab experiment which might take three to six months or more. In three to five years, a quantum computer will be able to simulate those experiments and fill in the gaps in a few minutes,” he said.

A key power of quantum computing is its ability to work on vast amounts of data at the same time. Looking further out, perhaps a decade, Krishna expects that quantum computers will be able to create AI models. “Current models with hundreds of billions of parameters can take two to three months to train on a very large cluster of GPUs. With a quantum computer, you’ll be able to train the same model overnight,” he said. His expectation is, “You’ll be able to solve problems that are far beyond what the biggest supercomputers in the world can do now.”

Take Away

As part of his position as CEO of IBM, Arvind Krishna has a window seat to much of the cutting-edge changes in computing technology, including artificial Intelligence. He suggests he was not fully quoted in the article that Bloomberg did covering AI and that the technology is expected to create jobs. It may, however alter available occupations while creating new needs.

He is not in the camp that massive regulation is needed to keep the innovative technology at bay; Krishna believes creative development is best when there is a level playing field.

How Can Congress Regulate AI? Erect Guardrails, Ensure Accountability and Address Monopolistic Power

OpenAI CEO Sam Altman urged lawmakers to consider regulating AI during his Senate testimony on May 16, 2023. That recommendation raises the question of what comes next for Congress. The solutions Altman proposed – creating an AI regulatory agency and requiring licensing for companies – are interesting. But what the other experts on the same panel suggested is at least as important: requiring transparency on training data and establishing clear frameworks for AI-related risks.

Another point left unsaid was that, given the economics of building large-scale AI models, the industry may be witnessing the emergence of a new type of tech monopoly.

This article was republished with permission from The Conversation, a news site dedicated to sharing ideas from academic experts. It represents the research-based findings and thoughts of Anjana Susarla, Professor of Information Systems, Michigan State University.

As a researcher who studies social media and artificial intelligence, I believe that Altman’s suggestions have highlighted important issues but don’t provide answers in and of themselves. Regulation would be helpful, but in what form? Licensing also makes sense, but for whom? And any effort to regulate the AI industry will need to account for the companies’ economic power and political sway.

An Agency to Regulate AI?

Lawmakers and policymakers across the world have already begun to address some of the issues raised in Altman’s testimony. The European Union’s AI Act is based on a risk model that assigns AI applications to three categories of risk: unacceptable, high risk, and low or minimal risk. This categorization recognizes that tools for social scoring by governments and automated tools for hiring pose different risks than those from the use of AI in spam filters, for example.

The U.S. National Institute of Standards and Technology likewise has an AI risk management framework that was created with extensive input from multiple stakeholders, including the U.S. Chamber of Commerce and the Federation of American Scientists, as well as other business and professional associations, technology companies and think tanks.

Federal agencies such as the Equal Employment Opportunity Commission and the Federal Trade Commission have already issued guidelines on some of the risks inherent in AI. The Consumer Product Safety Commission and other agencies have a role to play as well.

Rather than create a new agency that runs the risk of becoming compromised by the technology industry it’s meant to regulate, Congress can support private and public adoption of the NIST risk management framework and pass bills such as the Algorithmic Accountability Act. That would have the effect of imposing accountability, much as the Sarbanes-Oxley Act and other regulations transformed reporting requirements for companies. Congress can also adopt comprehensive laws around data privacy.

Regulating AI should involve collaboration among academia, industry, policy experts and international agencies. Experts have likened this approach to international organizations such as the European Organization for Nuclear Research, known as CERN, and the Intergovernmental Panel on Climate Change. The internet has been managed by nongovernmental bodies involving nonprofits, civil society, industry and policymakers, such as the Internet Corporation for Assigned Names and Numbers and the World Telecommunication Standardization Assembly. Those examples provide models for industry and policymakers today.

Licensing Auditors, Not Companies

Though OpenAI’s Altman suggested that companies could be licensed to release artificial intelligence technologies to the public, he clarified that he was referring to artificial general intelligence, meaning potential future AI systems with humanlike intelligence that could pose a threat to humanity. That would be akin to companies being licensed to handle other potentially dangerous technologies, like nuclear power. But licensing could have a role to play well before such a futuristic scenario comes to pass.

Algorithmic auditing would require credentialing, standards of practice and extensive training. Requiring accountability is not just a matter of licensing individuals but also requires companywide standards and practices.

Experts on AI fairness contend that issues of bias and fairness in AI cannot be addressed by technical methods alone but require more comprehensive risk mitigation practices such as adopting institutional review boards for AI. Institutional review boards in the medical field help uphold individual rights, for example.

Academic bodies and professional societies have likewise adopted standards for responsible use of AI, whether it is authorship standards for AI-generated text or standards for patient-mediated data sharing in medicine.

Strengthening existing statutes on consumer safety, privacy and protection while introducing norms of algorithmic accountability would help demystify complex AI systems. It’s also important to recognize that greater data accountability and transparency may impose new restrictions on organizations.

Scholars of data privacy and AI ethics have called for “technological due process” and frameworks to recognize harms of predictive processes. The widespread use of AI-enabled decision-making in such fields as employment, insurance and health care calls for licensing and audit requirements to ensure procedural fairness and privacy safeguards.

Requiring such accountability provisions, though, demands a robust debate among AI developers, policymakers and those who are affected by broad deployment of AI. In the absence of strong algorithmic accountability practices, the danger is narrow audits that promote the appearance of compliance.

AI Monopolies?

What was also missing in Altman’s testimony is the extent of investment required to train large-scale AI models, whether it is GPT-4, which is one of the foundations of ChatGPT, or text-to-image generator Stable Diffusion. Only a handful of companies, such as Google, Meta, Amazon and Microsoft, are responsible for developing the world’s largest language models.

Given the lack of transparency in the training data used by these companies, AI ethics experts Timnit Gebru, Emily Bender and others have warned that large-scale adoption of such technologies without corresponding oversight risks amplifying machine bias at a societal scale.

It is also important to acknowledge that the training data for tools such as ChatGPT includes the intellectual labor of a host of people such as Wikipedia contributors, bloggers and authors of digitized books. The economic benefits from these tools, however, accrue only to the technology corporations.

Proving technology firms’ monopoly power can be difficult, as the Department of Justice’s antitrust case against Microsoft demonstrated. I believe that the most feasible regulatory options for Congress to address potential algorithmic harms from AI may be to strengthen disclosure requirements for AI firms and users of AI alike, to urge comprehensive adoption of AI risk assessment frameworks, and to require processes that safeguard individual data rights and privacy.

Looking Back at the Markets in May and Forward to June

Conviction in the overall stock market was weak in May, while enthusiasm for specific sectors was strong. June investors may regain some clarity as markets may be relieved from the debt ceiling dark cloud that kept investors overly cautious. But a renewed fear that the Fed is losing ground to inflation may become the focal point until the coming FOMC meeting. In the meantime, any increase in the debt limit signed into law kicks the can down the road, ongoing increases in borrowing and spending may not haunt the overall market in June, but the path of escalating debt is unsustainable for a healthy U.S. economy.

The next scheduled FOMC meeting is June 13-14. We will have another look at consumer inflation numbers before the June 14 Fed monetary policy decision date CPI (June 13).

While the Fed is wrestling with stubborn inflation, it is keeping an eye on the strong labor markets, which provides leeway and perhaps even a strong reason fo it to continue riding the economic break pedal by being increasingly less accommodative. Although low unemployment is desirable, tight labor markets are helping to drive prices up. The Fed aims to find a better balance.

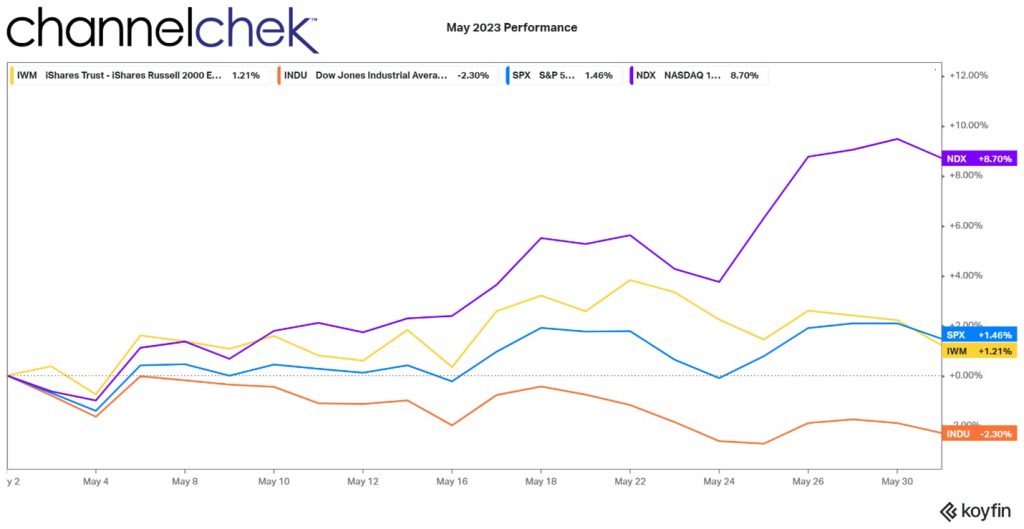

Three broad stock market indices (S&P 500, Nasdaq 100, and Russell 2000) are positive on the month of May. The Dow Industrials spent the entire month in negative territory. The Nasdaq 100 was the big winner (+8.7%) on the back of tech stocks as many have been inspired by the earnings performance and stock price performance of Nvidia (NVDA). The S&P 500 (+1.46%) and Russell 2000 (+1.21%) had a good showing putting the Russell 2000 back in positive territory for 2023. The Dow Industrials is negative (-2.30%), leaving this NYSE index down (-.72%) on the year.

During June, inflation showed signs that it was not decelerating but instead could be building strength. While the Fed raised rates by .25% and continued on pace with quantitative tightening, the impact has been seen as a sharp decrease in money supply (M2), but the central banks’ intended effect has not been realized.

Monetary policy is seen as having a lagging effect; that is to say, when the Fed pushes rates up today, it may take a year to work its way into the system to cause slowing and less demand to reduce price increases. Whether the Fed has done enough can only be seen in the rearview mirror months from now.

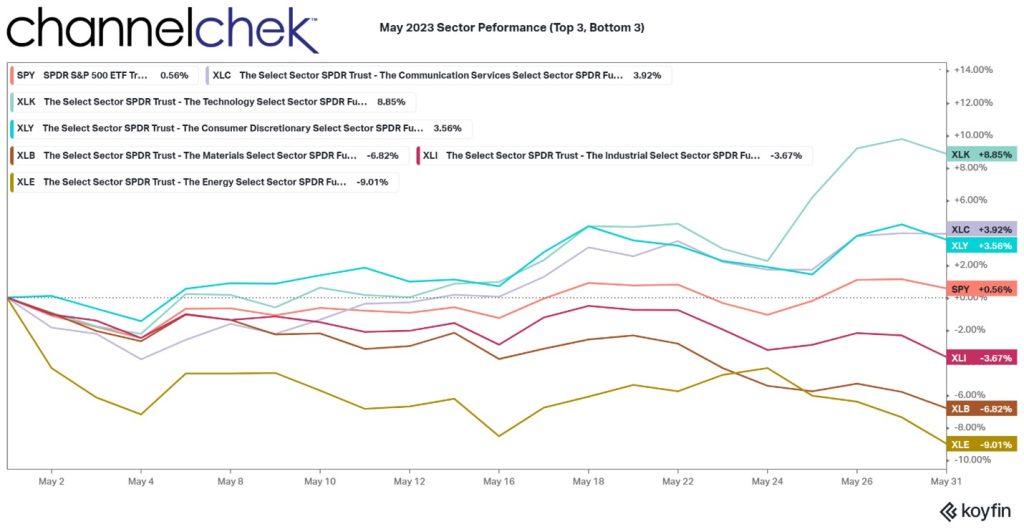

Of the 11 S&P market sectors (SPDRs), three were in positive territory as May came to a close. Technology, ticker XLK (+8.85%), was the only sector that showed an increase the previous month as well (.08%). That is followed by Communications Services, ticker XLC (3.92%), and Consumer Discretionary, ticker XLY, (+3.56%).

The S&P 500, which is comprised of the 11 market sectors, was barely positive during the month of May (+56%).

Of the three worst performers are Industrials, ticker XLI (-3.67%), it faired the best as the industrial sector has been relatively flat on the year. The Materials, ticker XLB, (-6.87%) took a larger hit as commodities prices dropped during the month; this sector was positive on the year going into May. Energy, ticker XLE, (-11.73%) has been volatile during 2023. It is just off its low (-12%) that it reached in mid-March.

Looking Forward

The job market is strong, and inflation, at best, isn’t declining; this makes it more comfortable for the Fed to raise rates. Another way to look at it is it creates a need for them to continue to hammer away to reverse the inflationary trend – and the economic latitude in which to do it.

While the energy sector was the worst performer among S&P 500 sectors, there are factors suggesting the trend could hold until OPEC and Russia begin to work in synch again. Oil prices are near their lowest levels all year, reflecting a drop in global demand, on the output side, since October, OPEC+ was supposed to be reducing production by 3.5 million barrels a day. There are signs that a key country in the alliance isn’t adhering to the announced production cuts. Whether this causes additional “cheating”, or causes the cartel to force members to fall in line remains to be seen.

Technology stocks, particularly those that could possibly benefit from the artificial intelligence revolution, are likely to be among the focus for a while. The sudden broad awareness of what the technology can do has sent investors scrambling for exposure. Whether the potential (AI) is unleashed quickly or the promise of AI now takes a slower road remains to be seen.

The Russell Reconstitution will be complete as of the first Monday in June. The index will have its new components and the portfolio managers of indexed funds ought to own the stocks that were added to the indexes in their funds and sell out of those that are no longer in the funds index. This creates a lot of activity around June 24. When the market opens on June 27, the index with its new makeup will be set.

Take-Away

The market was full of uncertainty in May. Yet three of the four major market indexes were higher. The signing into law of an increased debt ceiling will make one of the most worrisome objections to being involved disappear. This may unleash buyers that were sidelined.

Technology, caused by high expectations of AI was the focus during May; often, hype causes investors to shoot first and aim later. There will be winners and losers in this technology segment, as with any investment; remove yourself from the hype, carefully evaluate the opportunity, and read the professional research, positive and negative, of those you trust.

By the end of the month we will have two quarters of 2023 behind us, and there are no signs of a recession and little on the horizon to cause U.S. growth to falter quickly enough for there to be a recession this year. It is unlikely the Fed will ease in 2023. It is, however, likely a pause will eventually happen. There are reasons to believe that the pause won’t happen in June.

The axiom, sell in May and walk away is in question. Three of the four major indexes were up in May, so the jury is still out as to whether selling made sense for 2023.

Investors Have Far Fewer Reservations Against Investing in Leisure

Memorial Day Weekend in the U.S. marks the beginning of the travel season. After a few years on hiatus, as a result of Covid-19 restrictions, travel in 2023 is expected to surpass pre-pandemic numbers. While many investors are focused on the debt ceiling, less accommodative monetary policy, and looking for an entry point to invest in AI technology, post-pandemic travel plans are increasing – and the returns of some companies reflect this. One segment of the travel sector has benefitted and provided double-digit YTD stock returns. Below we discuss this segment and the potential for the future.

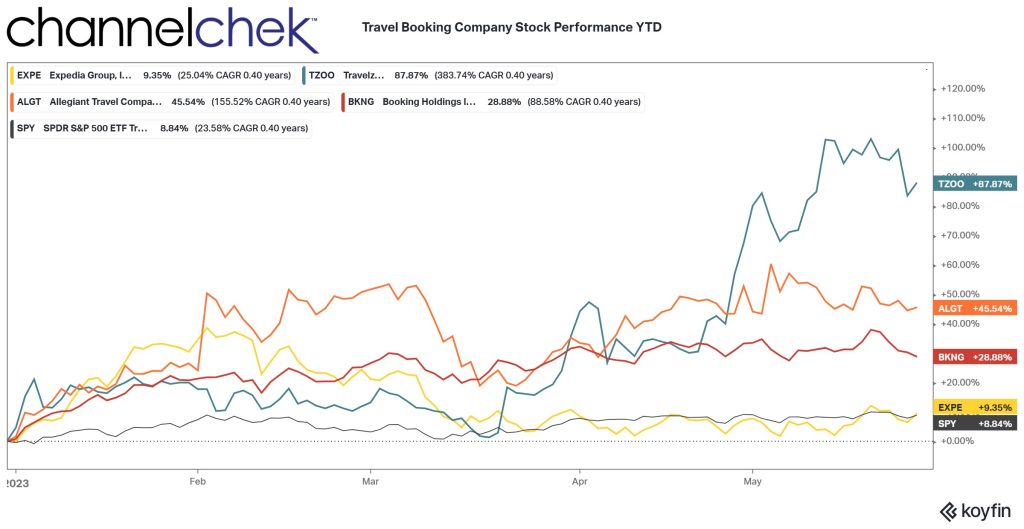

Travel Booking Stocks

When was the last time you went to an airline website to book a flight with them, or even a hotel for that matter? Most of us now find ourselves on a booking website when we’re planning a vacation. On these platforms, we can compare prices more easily, and if we’d like, add on extras like a car rental. Some even have proprietary package deals.

Technological advancements have created even greater efficiencies among booking and vacation travel package companies. Other positives for growth are pent-up demand, diversified revenue streams, and valuations still considered attractive. These all provide a backdrop and potential for the medium and long-term growth of the travel booking industry.

The chart above is a year-to-date sampling of examples of stocks in this leisure segment that have outperformed the overall market (S&P 500). Below, from weakest performer to strongest, are details of each company’s unique business, market cap, and other interesting investor information:

Expedia (EXPE) is a global travel company that provides a wide range of travel services, including flights, hotels, car rentals, and vacation packages.

This is a large cap stock with a current market cap of $14.33 billion, at $96.85 per share.

The company is headquartered in Seattle, Washington.

Booking Holdings (BKNG) is a travel company that owns a number of popular travel brands, including Booking.com, Priceline.com, and Kayak.com.

This is a large-cap stock with a current market cap of $97.61 billion, at $45.41 per share.

The company is headquartered in Norwalk, CT.

Allegiant Travel (ALGT) is a leisure travel company that provides travel services and other products to under-served cities in the U.S. This includes flights between vacation destinations. As of February 1, 2023, Allegiant operated a fleet of 122 Airbus A320 series aircraft.

This is a small cap stock with a current market cap of $1.85 billion, at a price of $99.96 per share.

The company is headquartered in Las Vegas, Nevada.

Travelzoo (TZOO) has a unique business model as it operates as an Internet media company that provides travel, entertainment, and deals from travel and leisure businesses worldwide. Publication products include the Travelzoo Top 20 email newsletter, Travelzoo emails, Travelzoo Network, Travelzoo mobile applications, Jack’s Flight Club website, Jack’s Flight Club mobile applications, and Jack’s Flight Club newsletters.

The year-to-date performance of TZOO is 10x that of the S&P 500.

In a research report dated April 28, 2023, Michael Kupinski, the senior research analyst for media and entertainment, had this to say about Travelzoo, “We believe that there is a disconnect with investors and the improved fundamentals at the company. Near current levels, the TZOO shares appear compelling, trading at 5.3 times Enterprise Value to our 2024 cash flow estimate or below the low end of the company’s 10-year and 15-year average trading ranges.” See the report here.

Current market cap is $133.05 million, at $8.69 per share.

The company is headquartered in New York, NY.

Image: “This Memorial Day weekend could be the busiest at airports since 2005” – AAA Newsroom

Take Away

Travel booking companies are well-positioned to benefit from the recovery of the overall leisure industry. Small cap travel booking companies are often more nimble and innovative than larger companies; this could give them an advantage in the travel booking market.

People are spending more money on travel. Companies like those mentioned above welcome the opening of China, allowing citizens to travel and return. In addition to the overall post-pandemic volume of business, travelers are spending more money on trips than they did before the restrictions.

Sound Ventures is More Evidence of How Much Capital AI is Attracting

Around investment circles, it is not unusual to debate what Cathie Wood is touting as disruptive and “the next big thing.” Another hedge fund manager that gets that kind of attention is Michael Burry, whose Tweets are followed by an army of “Burryologists” working to decode his words or advice. But the watercooler talk never before included Ashton Kutcher – at least not until now. The actor, originally made famous by his portrayal of a less-than-intelligent character on the TV sitcom, That 70’s Show, is a partner in a successful hedge fund he co-founded.

The firm, Sound Ventures, made news this month with an announcement that it had closed a $240 million artificial intelligence (AI) fund. The stated purpose of the fund is to invest in early-stage AI companies that have the potential to make a significant impact on life. Part of Kutcher’s interest in AI is what he believes the technology’s has potential to solve some of the world’s biggest problems. His list includes poverty, disease, and climate change. Kutcher and his business partner, Guy Oseary, say they are committed to investing in AI companies that are working to make a positive impact on the world.

Since 2015, Sound Ventures has invested in a number of successful companies that, include tech disruptors Airbnb, Spotify, and Uber. As far as AI, Kutcher says he is most interested in AI companies that have the potential to revolutionize various industries, the focus being companies that are at the forefront of this technology.

The venture Capital (VC) firm announced in early May that it closed the Sound Ventures AI Fund. The fund was oversubscribed by nearly $240 million. It is noteworthy that C3.AI, the heart of ChatGPT, has a market cap of just 10 to 12 times this amount. So while this may not sound like a huge sum, it is significant relative to the size of the companys the fund may invest in.

The fund seeks to invest in AI businesses at the foundation model layer. Currently, the fund’s portfolio of companies includes OpenAI, Anthropic and StabilityAI. Kutcher, Oseary and Effie Epstein lead Sound Ventures as general partners.

Sound Ventures has already been investing in AI for the past decade, “and we believe that this moment in history will dictate the trajectory of this technology,” Epstein said. “Our team is well positioned to continue investing in and supporting exceptional founders that are thoughtfully shaping the future through artificial intelligence.”

Take Away

Famous investors and famous people have the ability to draw attention to their investment activities. Actor Ashton Kutcher, his neighbor Guy Oseary, who is a talent manager, and Effie Epstein, who was formerly head of investor relations at iHeartMedia, are able to draw a good deal of attention to their investment work.

The activity of Sound Ventures also demonstrates the ability to raise capital for anything that is tied to artificial intelligence.