Office Depot, Inc., together with its subsidiaries, supplies a range of office products and services. It offers merchandise, such as general office supplies, computer supplies, business machines and related supplies, and office furniture through its chain of office supply stores under the Office Depot, Foray, Ativa, Break Escapes, Worklife, and Christopher Lowell brand names. The company also provides graphic design, printing, reproduction, mailing, shipping, and other services through design, print, and ship centers. It has operations throughout North America, Europe, Asia, and Central America. The company also sells its products and services through direct mail catalogs, contract sales force, Internet sites, and retail stores, through a mix of company-owned operations, joint ventures, licensing and franchise agreements, alliances, and other arrangements. As of December 31, 2008, Office Depot operated 1,267 North American retail division office supply stores and 162 international division retail stores, as well as participated under licensing and merchandise arrangements in 98 stores. The company was founded in 1986 and is based in Boca Raton, Florida.

Joe Gomes, CFA, Managing Director, Equity Research Analyst, Generalist , Noble Capital Markets, Inc.

Joshua Zoepfel, Research Associate, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

Challenging Conditions. Continuing challenging macroeconomic and business conditions impacted ODP in Q4. ODP Business Solutions faced economic factors that caused enterprise spending constraints in the quarter, while Office Depot had more cautious consumer spending (along with 47 fewer stores). However, fiscal year figures were in-line with management guidance, and management is executing on initiatives to improve traction on both fronts.

4Q Results. Sales for the fourth quarter were $1.62 billion compared to $1.80 billion last year but were above our expectations at $1.55 billion and consensus at $1.61 billion. Net loss totaled $3 million, or $0.10/sh, compared to a loss of $37 million, or $0.96/sh, in the prior year. Adjusted EPS was $0.66 versus $1.13 last year. We were at $0.40 and $0.68, respectively. Adjusted EBITDA totaled $58 million, down from $83 million last year, and we were at $49 million.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

Travelzoo® provides its 30 million members with exclusive offers and one-of-a-kind experiences personally reviewed by our deal experts around the globe. We have our finger on the pulse of outstanding travel, entertainment, and lifestyle experiences. We work in partnership with more than 5,000 top travel suppliers—our long-standing relationships give Travelzoo members access to irresistible deals.

Michael Kupinski, Director of Research, Equity Research Analyst, Digital, Media & Technology , Noble Capital Markets, Inc.

Jacob Mutchler, Research Associate, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

In line quarter. The company reported Q4 revenue and adj. EBITDA of $20.7 million and $5.4 million, both of which are in line with our estimates of $21.5 million and $5.1 million, respectively. The recent results were adversely affected by weakness in Europe, primarily Germany, which we believe is temporary. In our view, investors should focus on the improving fundamental trends likely beginning in the first quarter of 2025.

Europe lags, but appears temporary. The company’s North American segment had a solid quarter, while revenue was relatively flat compared to the prior year period, operating margins improved from 29% to 33%. Additionally, Jack’s Flight Club grew revenue and posted a positive operating income. Europe experienced a tough quarter, largely attributed to political uncertainty and advertising issues in Germany, which are not expected to continue.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

ACCO Brands Corporation is one of the world’s largest designers, marketers and manufacturers of branded academic, consumer and business products. Our widely recognized brands include AT-A-GLANCE®, Esselte®, Five Star®, GBC®, Kensington®, Leitz®, Mead®, PowerA®, Quartet®, Rapid®, Rexel®, Swingline®, Tilibra®, and many others. Our products are sold in more than 100 countries around the world. More information about ACCO Brands, the Home of Great Brands Built by Great People, can be found at www.accobrands.com.

Joe Gomes, CFA, Managing Director, Equity Research Analyst, Generalist , Noble Capital Markets, Inc.

Joshua Zoepfel, Research Associate, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

An Overreaction. ACCO shares fell over 17% Friday, hitting a new 52-week low, on 4.5x normal daily volume. We believe the move to be misguided and not reflective of ongoing opportunities for the Company. We would reiterate, excluding unexpectedly negative forex, that ACCO’s 4Q24 results were in line with expectations.

Go Forward. While the operating environment remains challenging, there are green shoots of opportunity for the Company, such as the renewed back to office movement. Management is placing a primary focus on improving sales trends through a number of efforts, which, when combined with cost reduction efforts, places ACCO in position to generate substantial returns once the top line improves.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

Key Points: – Celsius acquires Alani Nutrition in a $1.8 billion deal, expected to close in Q2 2025. – The merger aims to create a leading functional beverage platform, catering to growing demand for zero-sugar alternatives. – Celsius projects $2 billion in sales post-acquisition, with $50 million in cost synergies over two years.

Celsius Holdings has announced plans to acquire Alani Nutrition in a landmark $1.8 billion deal, marking a major consolidation in the U.S. energy drink market. The agreement, expected to be finalized in the second quarter of 2025, includes a net purchase price of $1.65 billion and $150 million in tax assets.

Alani Nutrition, founded in 2018, has built a reputation as a “female-focused” brand offering functional beverages and snacks tailored to Gen Z and millennial consumers. The Kentucky-based company, previously operated by Congo Brands, produces energy drinks, protein shakes, snacks, and protein powders. The acquisition will transfer ownership from co-founders Katy and Haydn Schneider, as well as Congo Brands’ co-founders Max Clemons and Trey Steiger, to Celsius Holdings.

Celsius believes the deal will create a powerful synergy, forming a “leading better-for-you, functional lifestyle platform.” By integrating Alani Nu’s products, Celsius aims to expand its reach in the functional beverage space and tap into growing demand for zero-sugar alternatives. The company expects the merger to drive approximately $2 billion in sales, leveraging the combined distribution networks, brand awareness, and innovation capabilities of both entities.

John Fieldly, Chairman and CEO of Celsius, highlighted the strategic benefits of the acquisition, stating that it will “broaden the availability of Alani Nu’s functional products” and strengthen the company’s presence in new market segments. The transaction is projected to be accretive to cash earnings per share (EPS) within the first full year of ownership, with an estimated $50 million in cost synergies to be realized over two years post-closing.

Max Clemons of Congo Brands expressed confidence in the deal, emphasizing that Celsius will “unlock key growth opportunities” for Alani Nu, particularly in expanding its distribution and consumer engagement.

The acquisition announcement coincided with Celsius reporting its fourth-quarter and full-year financial results for 2024. The company posted annual revenue of $1.36 billion, reflecting a 3% increase over the prior year. North American sales accounted for $1.28 billion, growing by 1%, while international revenues surged 37% to $74.7 million. Despite the revenue growth, Celsius experienced a decline in profitability, with adjusted EBITDA down 13% to $255.7 million and net profit falling 36% to $145.1 million.

Industry analysts view this acquisition as a strategic move that could help Celsius regain momentum in a highly competitive market. By capitalizing on Alani Nu’s strong brand presence and consumer loyalty, Celsius aims to solidify its position as a leader in the energy and functional beverage sector. The deal also signals an increasing trend of consolidation in the market, as major players look to expand their portfolios to meet shifting consumer preferences.

As the acquisition moves forward, investors and industry watchers will closely monitor how Celsius integrates Alani Nu into its operations and whether the expected synergies materialize. If successful, the merger could serve as a blueprint for future partnerships in the rapidly evolving health and wellness beverage industry.

Key Points: – New tariffs on building materials and sustained high mortgage rates are dampening homebuilder confidence. – Delinquency on government-backed loans is increasing, signaling strain among lower-income homeowners. – Inflation and interest rates continue to influence housing affordability, with potential broader market implications.

In a troubling sign for the U.S. housing market, homebuilder confidence has plummeted to its lowest level in five months, primarily due to rising costs from new tariffs and high mortgage rates. The National Association of Home Builders (NAHB)/Wells Fargo Housing Market Index dropped to 42 in February, down from expectations of 46, indicating more builders view current conditions as poor. This downturn comes at a time when President Trump’s new tariffs on steel and aluminum, set to impact construction costs, are causing significant concern among builders.

Simultaneously, the mortgage landscape is growing more challenging for homeowners, particularly those with government-backed loans. Delinquency rates on Federal Housing Administration (FHA) and Veterans Affairs (VA) loans have surged past pre-pandemic levels, reaching 11.03% and 4.7% respectively. This rise underscores the financial strain felt by lower-income brackets amidst persistent inflation and elevated borrowing costs. Despite a slight decrease in interest rates in late 2024, the current economic climate has left many homeowners struggling to keep up with their mortgage payments, with job loss and excessive debt cited as major reasons for delinquency.

The broader economic implications are significant. While conventional mortgage delinquencies remain near historical lows, the uptick in FHA and VA loan issues might foreshadow a wider trend if economic conditions do not improve. Analysts like James Knightley from ING point out that while higher-income households might have seen benefits from stock market gains, the lower-income segment is feeling the squeeze from both rising costs and stagnant or reduced real income.

Moreover, recent data from ICE Mortgage Technology suggests that even high-income earners are beginning to show signs of financial stress, with delinquencies on various types of debt increasing. This could signal a more widespread economic downturn if not addressed. The housing market, often a bellwether for economic health, is thus at a critical juncture, with builders and buyers alike looking for signs of relief or further policy adjustments to navigate these turbulent times.

The current scenario might lead to a more cautious approach from builders. With 26% of builders cutting home prices in February and 59% offering incentives, it’s clear the market is feeling the pressure. Additionally, the NAHB survey’s indicators for future sales and buyer traffic have seen significant declines, suggesting a potential slowdown in housing activity unless there are interventions to ease the financial burden on potential buyers and builders alike.

As the market braces for these economic headwinds, stakeholders are watching closely for any policy shifts that could alleviate the pressures on the housing sector. Whether through regulatory reforms, adjustments in monetary policy, or international trade negotiations to mitigate tariff impacts, the path forward for housing will be shaped by how these challenges are met.

The ripple effects of these economic pressures could extend beyond the housing market, potentially impacting related industries like construction materials, home furnishing, and real estate services. There’s a growing concern that if the housing market continues to struggle, it might pull down consumer spending, which constitutes a significant portion of U.S. GDP, leading to a broader economic slowdown.

In response, some in the industry are calling for more robust support mechanisms, like expanded first-time buyer incentives or government-backed initiatives to stimulate construction activity. The hope is that such measures could help stabilize the market and protect the livelihoods of those dependent on the housing sector, while also ensuring that the American dream of homeownership remains within reach for the next generation.

Key Points: – Steve Madden has announced a definitive agreement to acquire UK-based Kurt Geiger for approximately £289 million ($365 million) in cash. – The acquisition aligns with Steve Madden’s strategic goals of international expansion and strengthening its accessories and direct-to-consumer business. – Kurt Geiger has seen significant growth in recent years, with an estimated annual revenue of £400 million.

Steve Madden (Nasdaq: SHOO), a leading designer and marketer of fashion footwear, accessories, and apparel, has reached a definitive agreement to acquire British luxury footwear and accessories brand Kurt Geiger. The transaction, valued at approximately £289 million ($365 million), marks a significant step in Steve Madden’s expansion into the international luxury and premium fashion market. The deal is expected to close in the second quarter of 2025, pending regulatory approvals and customary closing conditions.

This acquisition supports Steve Madden’s broader strategy of expanding into international markets while also strengthening its presence in the accessories category. Kurt Geiger, a brand renowned for its high-quality, fashion-forward designs, has built a strong reputation in the global fashion landscape. Known for its statement handbags and footwear, the brand’s alignment with Steve Madden’s existing portfolio makes it a compelling addition.

Edward Rosenfeld, Chairman and Chief Executive Officer of Steve Madden, highlighted the value of Kurt Geiger’s differentiated brand positioning and strong consumer appeal. “Kurt Geiger London has demonstrated exceptional growth, thanks to its unique brand image and high-quality product offerings,” Rosenfeld said. “Its strong British DNA and expanding global footprint align perfectly with our strategic focus areas, making this acquisition a natural fit.”

Founded in the 1960s, Kurt Geiger has evolved into a globally recognized luxury brand, with a presence in major department stores like Harrods and Selfridges. In addition to its flagship Kurt Geiger London brand, the company also operates KG Kurt Geiger and Carvela, catering to a broad spectrum of consumers within the luxury and premium fashion markets.

Neil Clifford, CEO of Kurt Geiger, expressed confidence in the brand’s continued success under the Steve Madden umbrella. “We are incredibly proud of what we’ve built at Kurt Geiger and the strong response our designs have received worldwide. With Steve Madden’s expertise and global infrastructure, we see tremendous opportunities for expansion and growth in the years ahead.”

The acquisition comes at a time when the fashion industry is witnessing increased consolidation, with companies seeking to strengthen their market presence through strategic acquisitions. As consumers continue to prioritize premium, high-quality products, brands like Kurt Geiger stand to benefit from the growing demand for luxury fashion and accessories.

Moreover, Steve Madden’s move underscores the broader trend of U.S.-based fashion companies investing in European heritage brands to enhance their global appeal. With Kurt Geiger’s strong direct-to-consumer strategy and emphasis on premium accessories, the acquisition is expected to bolster Steve Madden’s competitive position in the evolving retail landscape.

For investors interested in the apparel and retail sector, another brand to watch is Vince Holdings, a premium fashion retailer covered by Noble research analyst Michael Kupinski. Vince Holdings has carved out a niche in the luxury apparel space, offering sophisticated styles with a focus on quality and craftsmanship.

Key Points: – Hyatt to acquire Playa Hotels & Resorts for $2.6 billion, including $900 million in debt. – The deal expands Hyatt’s all-inclusive footprint across Mexico, the Dominican Republic, and Jamaica. – Hyatt plans to maintain an asset-light model by selling Playa’s owned properties post-acquisition.

Hyatt Hotels Corporation (NYSE: H) has announced a definitive agreement to acquire Playa Hotels & Resorts N.V. (NASDAQ: PLYA) in a transaction valued at approximately $2.6 billion, including $900 million in debt. This move solidifies Hyatt’s dominance in the all-inclusive resort sector while expanding its footprint across key markets in Mexico, the Dominican Republic, and Jamaica.

Since its initial investment in Playa in 2013, Hyatt has leveraged its relationship to establish the Hyatt Ziva and Hyatt Zilara brands. Playa currently owns and operates eight of Hyatt’s all-inclusive resorts, and this acquisition will allow Hyatt to take full control of these properties, securing long-term management agreements and reinforcing its presence in the luxury all-inclusive space.

“Hyatt has firmly established itself as a leader in the all-inclusive space,” said Mark Hoplamazian, President and CEO of Hyatt. “This pending transaction allows us to broaden our portfolio while providing more value to all of our stakeholders through an expanded management platform for all-inclusive resorts.”

With Playa’s diverse portfolio of high-end resorts, the acquisition enhances Hyatt’s distribution channels, incorporating Playa’s properties into Hyatt’s expansive network. Hyatt’s ALG Vacations and Unlimited Vacation Club will further drive guest engagement and maximize revenue potential across the brand’s growing all-inclusive segment.

Hyatt’s latest acquisition aligns with its aggressive growth strategy in the all-inclusive segment. The company previously acquired Apple Leisure Group in 2021 and completed a joint venture with Grupo Piñero in 2024, adding the Bahia Principe Hotels & Resorts portfolio to its Inclusive Collection. Hyatt now boasts a formidable presence in Latin America, the Caribbean, and Europe, with approximately 55,000 rooms across its all-inclusive brands.

Despite the acquisition, Hyatt remains committed to its asset-light business model. The company plans to sell Playa’s owned properties and expects to generate at least $2.0 billion from asset sales by 2027. Hyatt anticipates that asset-light earnings will exceed 90% on a pro forma basis by that time.

Hyatt intends to fund the acquisition entirely through new debt financing and aims to pay down over 80% of the new debt with proceeds from asset sales. The deal is expected to close later this year, subject to regulatory and Playa shareholder approval.

The transaction has received backing from leading financial institutions, with BDT & MSD Partners serving as lead financial advisor to Hyatt. Berkadia is acting as Hyatt’s real estate advisor, while BofA Securities, J.P. Morgan, and Wells Fargo have provided fully committed bridge financing.

With this acquisition, Hyatt continues to reinforce its leadership in the luxury all-inclusive market, ensuring greater value for guests, stakeholders, and investors alike.

For more than 45 years, 1-800-Flowers.com has offered truly original floral arrangements, plants and unique gifts to celebrate birthdays, anniversaries, everyday occasions, and seasonal holidays, and to deliver comfort during times of grief. Backed by a caring team obsessed with service, 1-800-Flowers.com provides customers thoughtful ways to express themselves and connect with the most important people in their lives. 1-800-Flowers.com is part of the 1-800-FLOWERS.COM, Inc. family of brands. Shares in 1-800-FLOWERS.COM, Inc. are traded on the NASDAQ Global Select Market, ticker symbol: FLWS.

Michael Kupinski, Director of Research, Equity Research Analyst, Digital, Media & Technology , Noble Capital Markets, Inc.

Jacob Mutchler, Research Associate, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

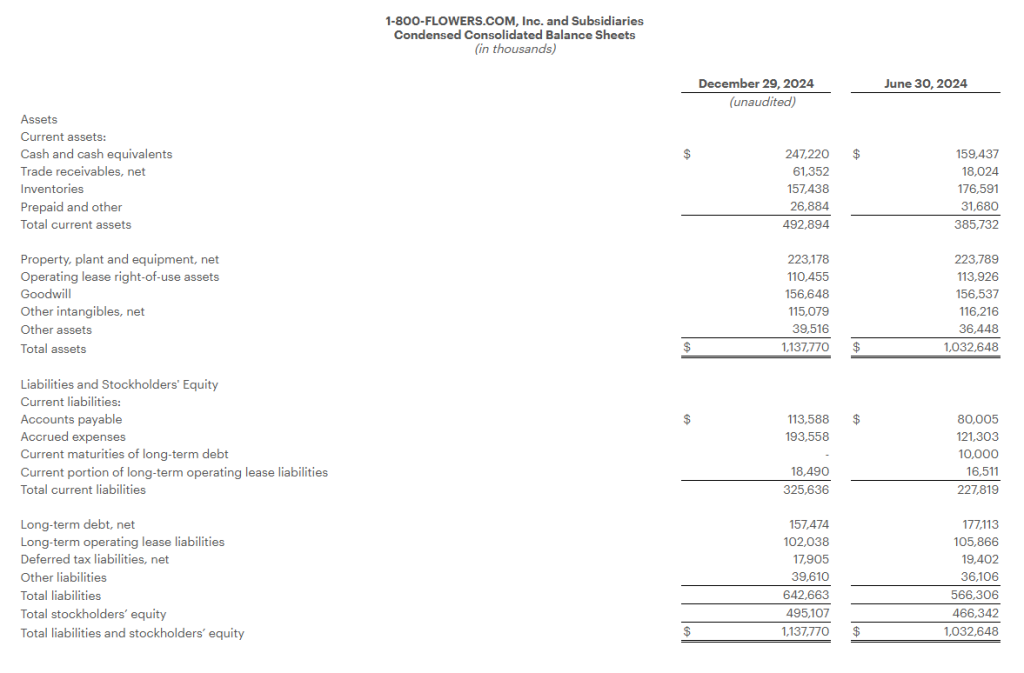

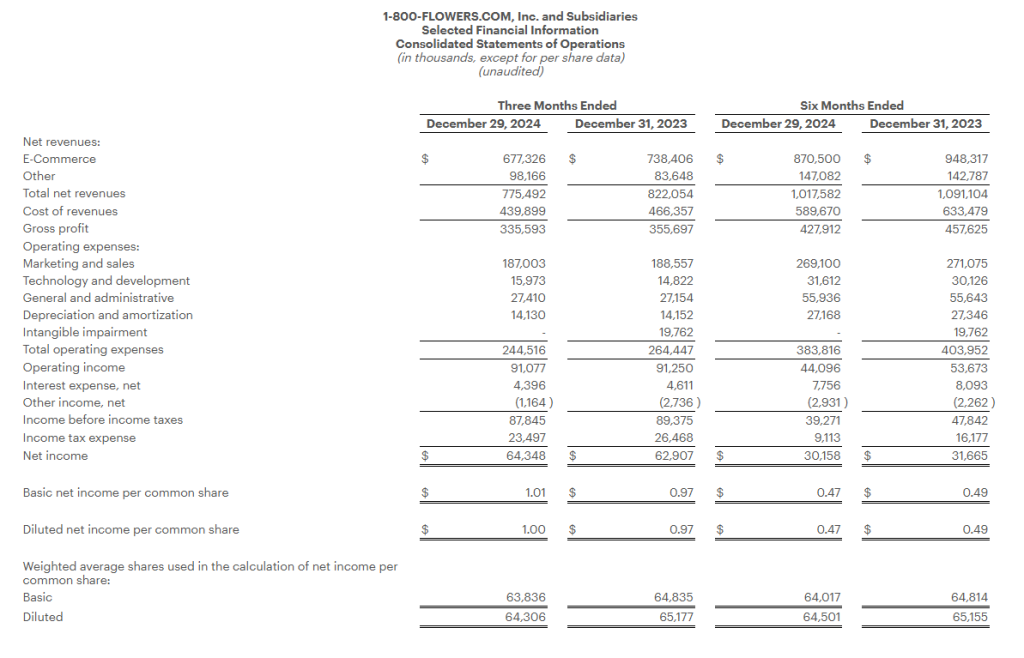

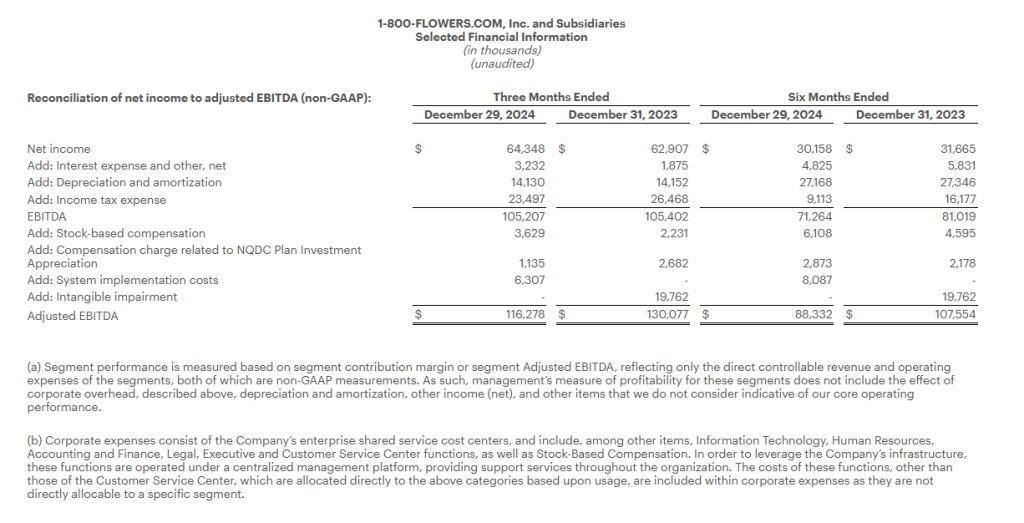

Fiscal Q2 Results. The company reported fiscal Q2 revenue and adj. EBITDA of $775.5 million and $116.3 million, both of which were lower than our estimates of $801.1 million and $124.7 million, respectively. Notably, an order management system (OMS) that was implemented in Q2 for Harry & David faced issues with complicated orders during periods of high volume. The OMS issue, which was resolved in the quarter, resulted in roughly $20 million of lost revenue and is largely to blame for the downside variance.

Strategic initiatives. Importantly, the company remains focused on reducing costs through increased automation, increasing investments in sales and marketing, and broadening its product offerings for its price-sensitive customers. Notably, management highlighted that the savings from its cost reduction efforts will largely fund its increased investment in sales and marketing in an effort to broaden its customer base.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

Generates Revenues of $775.5 million and Net Income of $64.3 million

Reports Adjusted EBITDA(1) of $116.3 million

Updates Fiscal Year 2025 Outlook

(1) Refer to “Definitions of Non-GAAP Financial Measures” and the tables attached at the end of this press release for reconciliation of non-GAAP results to applicable GAAP results.

JERICHO, N.Y.–(BUSINESS WIRE)– 1-800-FLOWERS.COM, Inc. (NASDAQ: FLWS), a leading provider of gifts designed to help inspire customers to give more, connect more, and build more and better relationships, today reported results for its Fiscal 2025 second quarter ended December 29, 2024.

“Our second quarter revenue declined 5.7%, showing year-over-year improvement, but not at the pace that we had been anticipating,” said Jim McCann, Chairman and Chief Executive Officer of 1-800-FLOWERS.COM, Inc. “Our business experienced a softer than anticipated and highly promotional consumer environment, along with a pullback in corporate gifting orders, which were slightly offset by an improvement in our wholesale business. These trends were further exacerbated by issues with our new Harry & David order management system implementation.”

Mr. McCann continued, “Shifting patterns in consumer engagement have affected our performance. We are implementing actions to accelerate our Work Smarter efficiency initiatives that will in turn fund investments in our growth-oriented Relationship Innovation™ initiatives and marketing and sales strategies. As we focus on expanding our customer base, we see significant opportunities to leverage new technology to enhance engagement and build deeper relationships with our customers. We are confident that our dedicated team and innovative solutions will help us navigate these headwinds and emerge stronger.”

Fiscal 2025 Second Quarter Highlights

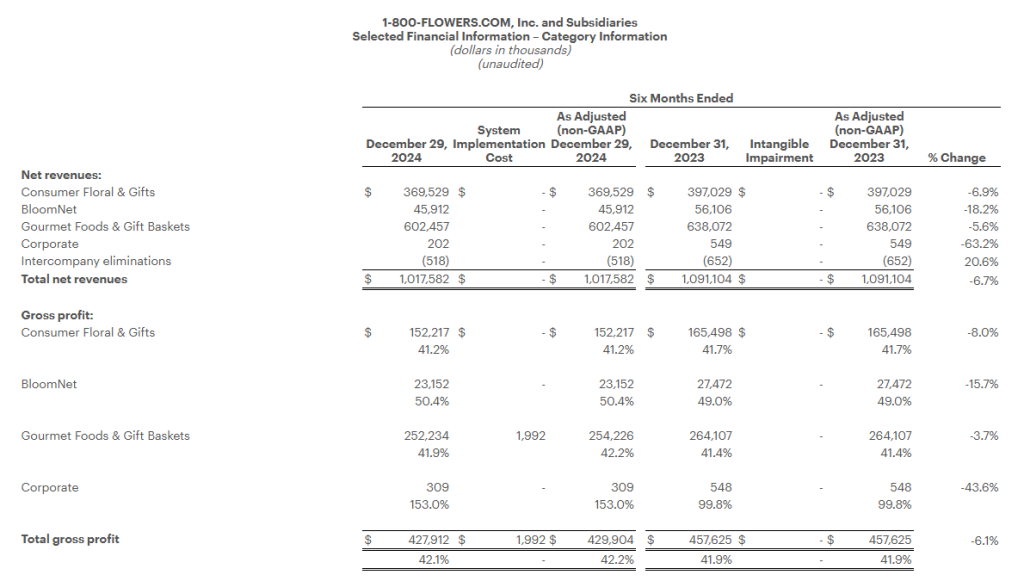

Total consolidated revenues decreased 5.7% to $775.5 million, as compared with the prior year period.

Gross profit margin of 43.3% was flat with the prior year period.

Operating expenses declined $19.9 million to $244.5 million, as compared with the prior year period. Excluding the impact of non-recurring charges in the current period associated with new systems implementation costs, impairment charges in the prior year period, as well as the impact of the Company’s non-qualified deferred compensation plan in both periods, operating expenses declined by $2.9 million to $239.1 million, as compared with the prior year period.

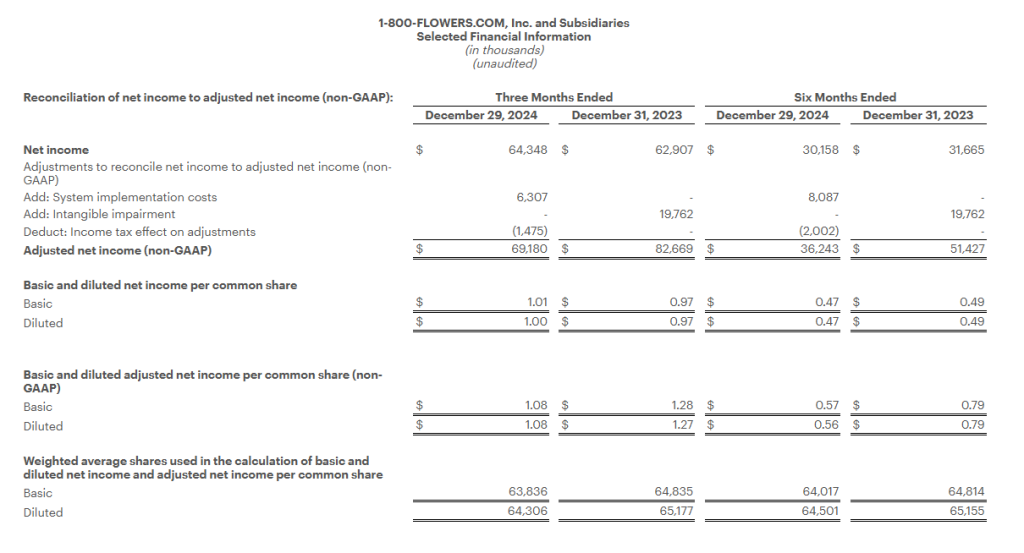

Net income for the quarter was $64.3 million, or $1.00 per diluted share, as compared with net income of $62.9 million, or $0.97 per diluted share in the prior year period.

Adjusted Net Income1 was $69.2 million, or $1.08 per diluted share, compared with an Adjusted Net Income1 of $82.7 million, or $1.27 per diluted share, in the prior year period.

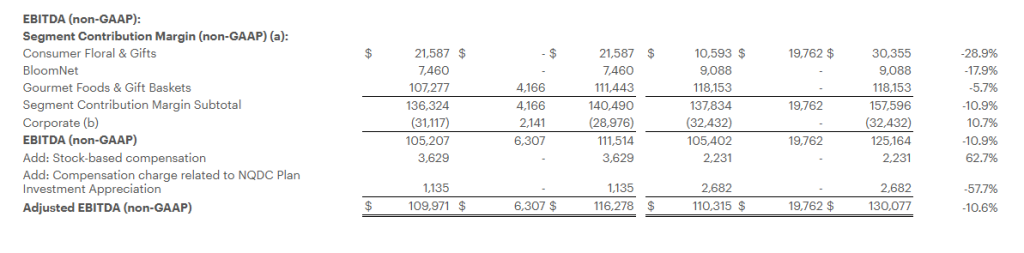

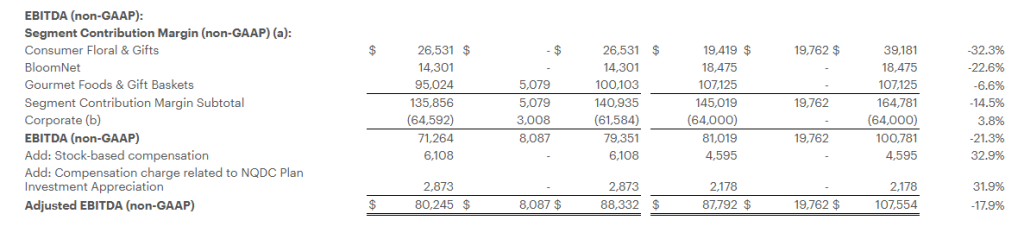

Adjusted EBITDA1 for the quarter was $116.3 million, as compared with Adjusted EBITDA1 of $130.1 million in the prior year period.

Segment Results

The Company provides Fiscal 2025 second quarter financial results for its Gourmet Foods and Gift Baskets, Consumer Floral and Gifts, and BloomNet® segments in the tables attached to this release and as follows:

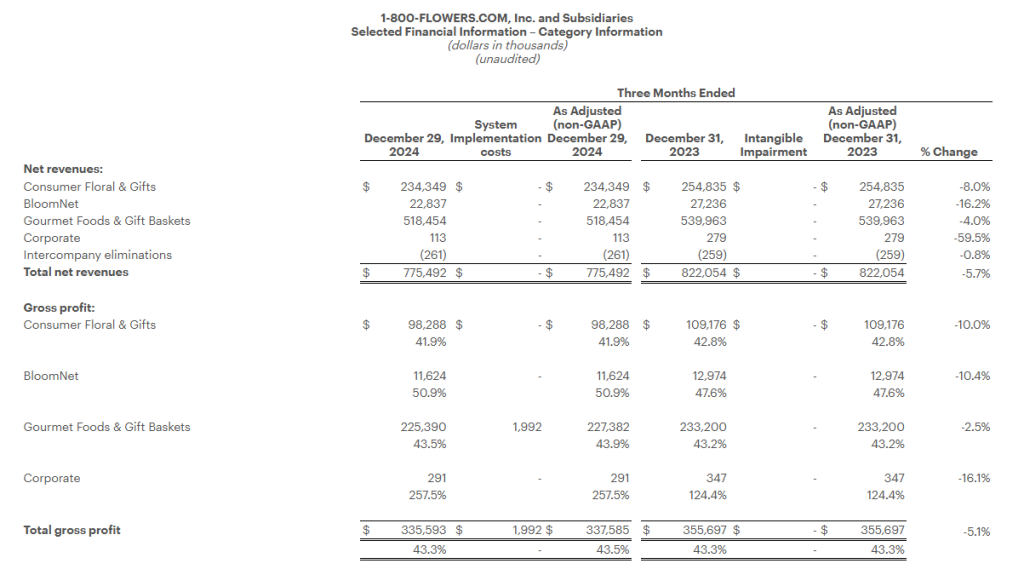

Gourmet Foods and Gift Baskets: Revenues for the quarter declined 4.0% to $518.5 million as compared with the prior year period. The Company estimates that the issues associated with the implementation of its new order management system resulted in lost revenue of approximately $20 million. Gross profit margin increased 30 basis points to 43.5%, benefiting from the Company’s inventory and labor optimization efforts that offset the incremental costs associated with the order management system issues. Excluding the impact of the systems implementation costs, adjusted segment contribution margin1 was $111.4 million, as compared with segment contribution margin1 of $118.2 million in the prior year period.

Consumer Floral & Gifts: Revenues for the quarter declined 8.0% to $234.3 million as compared with the prior year period. Gross profit margin decreased 90 basis points to 41.9%, primarily due to deleveraging on the sales decline and a promotional consumer environment. Segment contribution margin1 was $21.6 million, compared with adjusted segment contribution margin1 of $30.4 million in the prior year period, excluding the intangible impairment.

BloomNet: Revenues for the quarter declined 16.2% to $22.8 million as compared with the prior year period. Revenue and gross margin were impacted by the lower volume of lower margin orders processed by BloomNet. Gross profit margin increased 330 basis points to 50.9% due to lower florist rebates. Segment contribution margin1 was $7.5 million, compared with $9.1 million in the prior year period.

Company Guidance

Based on the Company’s performance during its fiscal second quarter, the Company is updating its Fiscal 2025 guidance as outlined below. The Company expects its revenue trends to improve as the fiscal year progresses, benefiting from its Relationship Innovation initiatives that have expanded the Company’s offerings, broadened price points and enhanced the user experience.

For Fiscal 2025, the company now expects:

total revenues to decline in the mid-single digits on a percentage basis, as compared with the prior year;

Adjusted EBITDA1 to be in a range of $65 million to $75 million; and

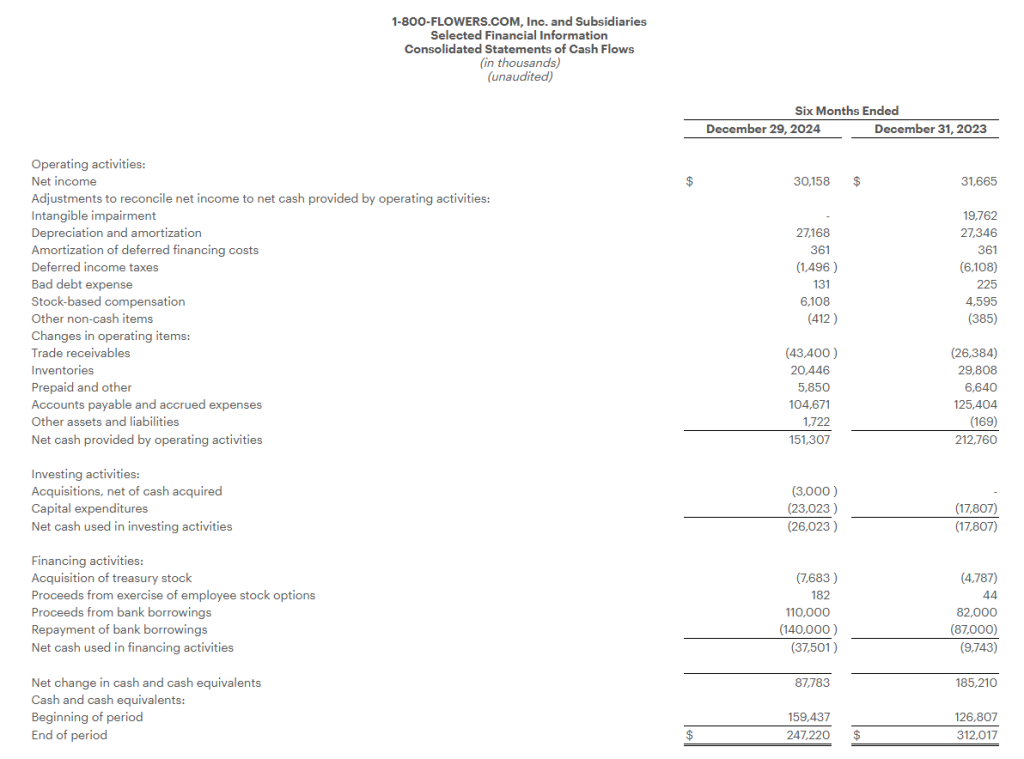

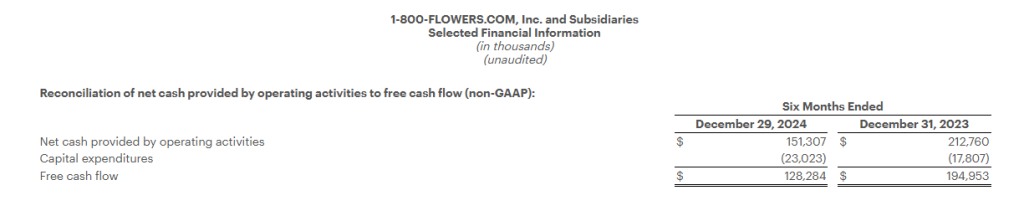

Free Cash Flow1 to be in a range of $25 million to $35 million.

Credit Agreement Amendment

The Company today announced that it has amended its credit agreement in order to provide more clarity and flexibility to the Company going forward.

Key changes effected by the amendment include revising the definition of Consolidated EBITDA, clarifying the application of optional term loan prepayments toward scheduled principal payments, and revising the definition of Consolidated Fixed Charges. Additional information can be found in the Company’s Form 8-K that was filed with the SEC this morning.

Conference Call

The Company will conduct a conference call to discuss the above details and attached financial results today, January 30, 2025, at 8:00 a.m. (ET). The conference call will be webcast from the Investors section of the Company’s website at www.1800flowersinc.com. A recording of the call will be posted on the Investors section of the Company’s website within two hours of the call’s completion. A telephonic replay of the call can be accessed beginning at 2:00 p.m. (ET) today through February 6, 2025, at: (US) 1-877-344-7529; (Canada) 855-669-9658; (International) 1-412-317-0088; enter conference ID #: 4981439.

Definitions of non-GAAP Financial Measures:

We sometimes use financial measures derived from consolidated financial information, but not presented in our financial statements prepared in accordance with U.S. generally accepted accounting principles (“GAAP”). Certain of these are considered “non-GAAP financial measures” under the U.S. Securities and Exchange Commission rules. Non-GAAP financial measures referred to in this document are either labeled as “non-GAAP” or designated as such with a “1”. See below for definitions and the reasons why we use these non-GAAP financial measures. Where applicable, see the Selected Financial Information below for reconciliations of these non-GAAP measures to their most directly comparable GAAP financial measures. Reconciliations for forward-looking figures would require unreasonable efforts at this time because of the uncertainty and variability of the nature and amount of certain components of various necessary GAAP components, including, for example, those related to compensation, tax items, amortization or others that may arise during the year, and the Company’s management believes such reconciliations would imply a degree of precision that would be confusing or misleading to investors. For the same reasons, the Company is unable to address the probable significance of the unavailable information. The lack of such reconciling information should be considered when assessing the impact of such disclosures.

EBITDA and Adjusted EBITDA:

We define EBITDA as net income (loss) before interest, taxes, depreciation, and amortization. Adjusted EBITDA is defined as EBITDA adjusted for the impact of stock-based compensation, Non-Qualified Deferred Compensation Plan (“NQDC”) Investment appreciation/depreciation, and for certain items affecting period-to-period comparability. See Selected Financial Information for details on how EBITDA and Adjusted EBITDA were calculated for each period presented. The Company presents EBITDA and Adjusted EBITDA because it considers such information meaningful supplemental measures of its performance and believes such information is frequently used by the investment community in the evaluation of similarly situated companies. The Company uses EBITDA and Adjusted EBITDA as factors to determine the total amount of incentive compensation available to be awarded to executive officers and other employees. The Company’s credit agreement uses EBITDA and Adjusted EBITDA to determine its interest rate and to measure compliance with certain covenants. EBITDA and Adjusted EBITDA are also used by the Company to evaluate and price potential acquisition candidates. EBITDA and Adjusted EBITDA have limitations as analytical tools and should not be considered in isolation or as a substitute for analysis of the Company’s results as reported under GAAP. Some of the limitations are: (a) EBITDA and Adjusted EBITDA do not reflect changes in, or cash requirements for, the Company’s working capital needs; (b) EBITDA and Adjusted EBITDA do not reflect the interest expense, or the cash requirements necessary to service interest or principal payments, on the Company’s debts; and (c) although depreciation and amortization are non-cash charges, the assets being depreciated and amortized may have to be replaced in the future and EBITDA does not reflect any cash requirements for such capital expenditures. EBITDA and Adjusted EBITDA should only be used on a supplemental basis combined with GAAP results when evaluating the Company’s performance.

Segment Contribution Margin and Adjusted Segment Contribution Margin

We define Segment Contribution Margin as earnings before interest, taxes, depreciation, and amortization, before the allocation of corporate overhead expenses. Adjusted Segment Contribution Margin is defined as Segment Contribution Margin adjusted for certain items affecting period-to-period comparability. See Selected Financial Information for details on how Segment Contribution Margin and Adjusted Segment Contribution Margin were calculated for each period presented. When viewed together with our GAAP results, we believe Segment Contribution Margin and Adjusted Segment Contribution Margin provide management and users of the financial statements meaningful information about the performance of our business segments. Segment Contribution Margin and Adjusted Segment Contribution Margin are used in addition to and in conjunction with results presented in accordance with GAAP and should not be relied upon to the exclusion of GAAP financial measures. The material limitation associated with the use of Segment Contribution Margin and Adjusted Segment Contribution Margin is that they are an incomplete measure of profitability as they do not include all operating expenses or non-operating income and expenses. Management compensates for this limitation when using these measures by looking at other GAAP measures, such as Operating Income and Net Income.

Adjusted Net Income (Loss) and Adjusted or Comparable Net Income (Loss) Per Common Share:

We define Adjusted Net Income (Loss) and Adjusted or Comparable Net Income (Loss) Per Common Share as Net Income (Loss) and Net Income (Loss) Per Common Share adjusted for certain items affecting period-to-period comparability. See Selected Financial Information below for details on how Adjusted Net Income (Loss) Per Common Share and Adjusted or Comparable Net Income (Loss) Per Common Share were calculated for each period presented. We believe that Adjusted Net Income (Loss) and Adjusted or Comparable Net Income (Loss) Per Common Share are meaningful measures because they increase the comparability of period-to-period results. Since these are not measures of performance calculated in accordance with GAAP, they should not be considered in isolation of, or as a substitute for, GAAP Net Income (Loss) and Net Income (Loss) Per Common Share, as indicators of operating performance and they may not be comparable to similarly titled measures employed by other companies.

Free Cash Flow:

We define Free Cash Flow as net cash provided by operating activities less capital expenditures. The Company considers Free Cash Flow to be a liquidity measure that provides useful information to management and investors about the amount of cash generated by the business after the purchases of fixed assets, which can then be used to, among other things, invest in the Company’s business, make strategic acquisitions, strengthen the balance sheet, and repurchase stock or retire debt. Free Cash Flow is a liquidity measure that is frequently used by the investment community in the evaluation of similarly situated companies. Since Free Cash Flow is not a measure of performance calculated in accordance with GAAP, it should not be considered in isolation or as a substitute for analysis of the Company’s results as reported under GAAP. A limitation of the utility of Free Cash Flow as a measure of financial performance is that it does not represent the total increase or decrease in the Company’s cash balance for the period.

About 1-800-FLOWERS.COM, Inc.

1-800-FLOWERS.COM, Inc. is a leading provider of gifts designed to help inspire customers to give more, connect more, and build more and better relationships. The Company’s e-commerce business platform features an all-star family of brands, including: 1-800-Flowers.com®, 1-800-Baskets.com®, CardIsle®, Cheryl’s Cookies®, Harry & David®, PersonalizationMall.com®, Shari’s Berries®, FruitBouquets.com®, Things Remembered®, Moose Munch®, The Popcorn Factory®, Wolferman’s Bakery®, Vital Choice®, Simply Chocolate® and Scharffen Berger®. Through the Celebrations Passport® loyalty program, which provides members with free standard shipping and no service charge on eligible products across our portfolio of brands, 1-800-FLOWERS.COM, Inc. strives to deepen relationships with customers. The Company also operates BloomNet®, an international floral and gift industry service provider offering a broad-range of products and services designed to help members grow their businesses profitably; Napco℠, a resource for floral gifts and seasonal décor; DesignPac Gifts, LLC, a manufacturer of gift baskets and towers; Alice’s Table®, a lifestyle business offering fully digital livestreaming and on demand floral, culinary and other experiences to guests across the country; and Card Isle®, an e-commerce greeting card service. 1-800-FLOWERS.COM, Inc. was recognized among America’s Most Trustworthy Companies by Newsweek for 2024. 1-800-FLOWERS.COM, Inc. was also recognized as one of America’s Most Admired Workplaces for 2025 by Newsweek and was named to the Fortune 1000 list in 2022. Shares in 1-800-FLOWERS.COM, Inc. are traded on the NASDAQ Global Select Market, ticker symbol: FLWS. For more information, visit 1800flowersinc.com.

FLWS–COMP FLWS-FN

Special Note Regarding Forward Looking Statements:

This press release contains forward-looking statements within the meaning of the Private Securities Litigation Reform Act of 1995. These forward-looking statements represent the Company’s current expectations or beliefs concerning future events and can generally be identified using statements that include words such as “estimate,” “expects,” “project,” “believe,” “anticipate,” “intend,” “plan,” “foresee,” “forecast,” “likely,” “should,” “will,” “target” or similar words or phrases. These forward-looking statements are subject to risks, uncertainties, and other factors, many of which are outside of the Company’s control, which could cause actual results to differ materially from the results expressed or implied in the forward-looking statements, including, but not limited to, statements regarding the Company’s ability to achieve its guidance for the full Fiscal year; the Company’s ability to leverage its operating platform and reduce its operating expense ratio; its ability to successfully integrate acquired businesses and assets; its ability to successfully execute its strategic initiatives; its ability to cost effectively acquire and retain customers; the outcome of contingencies, including legal proceedings in the normal course of business; its ability to compete against existing and new competitors; its ability to manage expenses associated with sales and marketing and necessary general and administrative and technology investments; its ability to reduce promotional activities and achieve more efficient marketing programs; and general consumer sentiment and industry and economic conditions that may affect levels of discretionary customer purchases of the Company’s products. The Company undertakes no obligation to publicly update any of the forward-looking statements, whether because of new information, future events or otherwise, made in this release or in any of its SEC filings. Consequently, you should not consider any such list to be a complete set of all potential risks and uncertainties. For a more detailed description of these and other risk factors, refer to the Company’s SEC filings, including the Company’s Annual Reports on Form 10-K and its Quarterly Reports on Form 10-Q.

Note: The following tables are an integral part of this press release without which the information presented in this press release should be considered incomplete.

Key Points: – Acquires DealerClub for $25 million to revolutionize dealer-to-dealer digital auctions with reputation-based transparency. – Integrates DealerClub’s innovative platform with AccuTrade, creating a seamless retail and wholesale ecosystem for automotive dealers. – Strengthens Cars Commerce’s role in the $10B wholesale market, empowering dealers to optimize inventory and boost profitability.

Cars Commerce, the parent company of Cars.com, is making a bold move into the wholesale automotive market with its acquisition of DealerClub, a reputation-driven digital auction platform. This purchase, finalized for $25 million in cash with the potential for up to $88 million in performance-based payouts, reflects Cars Commerce’s strategic vision to streamline how dealers trade vehicles and optimize inventory management.

DealerClub’s innovative platform has made waves in the industry since its launch in 2024. Unlike traditional wholesale systems, DealerClub focuses on reputation-based transactions, which foster trust between dealers and reduce common challenges like arbitration disputes and title issues. This groundbreaking approach has attracted over 650 dealers to the platform and provides Cars Commerce with a strong foothold in the $10 billion wholesale used car market.

Revolutionizing Wholesale with Technology

The acquisition builds on Cars Commerce’s mission to use technology to simplify the car-buying and selling process. DealerClub’s platform, designed to facilitate seamless dealer-to-dealer transactions, aligns perfectly with this goal.

“This is a critical step for us,” said Alex Vetter, CEO of Cars Commerce. “Dealers need efficient, transparent solutions to manage inventory and boost profitability. DealerClub’s technology adds a new dimension to our platform, making it easier for dealers to trade within a trusted network while keeping more profit in their pockets.”

Cars Commerce plans to integrate DealerClub with its existing tools, such as the AccuTrade appraisal platform, creating a full-service solution that combines retail and wholesale capabilities. This unified ecosystem will allow dealers to handle every aspect of vehicle trading—from appraisal to resale—on a single platform.

What It Means for Dealers

The acquisition introduces several new opportunities for automotive dealers:

Greater Transparency: DealerClub’s reputation-based model brings a level of trust and clarity to the wholesale market that hasn’t been seen before, mirroring Cars Commerce’s success in consumer and dealer reviews.

Efficiency Gains: Dealers can now manage wholesale transactions with minimal risk and streamlined processes, saving time and money.

New Revenue Potential: Cars Commerce’s transactional model, combined with its established subscription business, promises long-term financial benefits for both the company and its dealer partners.

The integration also strengthens Cars Commerce’s position as a technology leader in the automotive space. As the industry moves toward digitization, platforms like DealerClub are becoming essential tools for dealers looking to stay competitive.

What’s Next for Cars Commerce?

While the acquisition is expected to have minimal financial impact in 2025, Cars Commerce sees it as a long-term investment. The company is committed to scaling DealerClub, even if it means short-term costs. Given the proven track record of DealerClub’s founder, Joe Neiman—who previously built ACV Auctions into an industry leader—expectations are high for the platform’s growth and success.

This move highlights Cars Commerce’s broader ambition to be a one-stop shop for all aspects of the car trade, from consumer-facing marketplaces to behind-the-scenes wholesale operations. As dealers continue to navigate challenges like inventory shortages and shifting market demands, Cars Commerce is positioning itself as the partner they can rely on for innovative solutions.

With DealerClub in its portfolio, Cars Commerce is no longer just a leader in the retail automotive space; it’s reshaping the future of wholesale as well.

Brendan Hoffman Expected to Become CEO of Vince Holding Corp.

NEW YORK–(BUSINESS WIRE)– Vince Holding Corp., (NYSE: VNCE) (“VNCE” or the “Company”), a global contemporary retailer, today announced that P180, a new venture focused on accelerating growth and profitability in the luxury apparel sector, acquired a majority stake in VNCE (the “P180 Acquisition”) from affiliates of Sun Capital Partners, Inc. (collectively, “Sun Capital”).

In conjunction with the P180 Acquisition, Brendan Hoffman is expected to assume the role of Chief Executive Officer of VNCE effective on or around February 3, 2025, subject to finalization of his employment terms. With this transition, David Stefko is expected to step down as Interim CEO of VNCE and continue to serve on the VNCE Board of Directors. In addition, Matthew Garff resigned from the VNCE Board of Directors in connection with the P180 Acquisition.

“VNCE is the perfect partner for P180; the brand’s dominance in the luxury contemporary market aligns seamlessly with our acquisition strategy. In addition, as VNCE has evolved its operating model, we believe having access to the technology and team of CaaStle, founded by Christine Hunsicker, my co-founder at P180, will further advance the company’s momentum in driving improved profitability while enhancing its omni-channel experience.” Mr. Hoffman added, “Personally, I have a strong connection to the Vince brand, having served as VNCE CEO for five years. I am excited to lead the team again as we continue to unlock new growth opportunities, drive innovation, enhance the brand’s market position, and focus on monetizing the Company’s inventory to ensure continued long-term success.”

“P180’s acquisition represents a transformative opportunity for VNCE. With this transaction, we will gain the operational expertise and cutting-edge digital capabilities needed to drive the brand’s future success,” commented Michael Mardy, Chairman of VNCE. “On behalf of the Board and the organization, I would also like to thank Dave for stepping into the interim CEO role for the past year. Through his leadership, the company has continued to execute and deliver results by operating a healthier full price model. We are glad to have Dave remain on the Board and are excited to welcome Brendan back to lead the organization into its next chapter.”

This acquisition marks the third strategic deal for P180 since its inception in 2024 and follows its recent investment with the prestigious fashion label Altuzarra and digital partnership with the multi-brand premium retailer elysewalker.

VNCE Significantly Reduces Debt

Simultaneously with the P180 Acquisition, an indirectly wholly owned subsidiary of VNCE, V Opco, LLC (“V Opco”), amended its existing credit agreement (the “ABL Credit Facility”) with Bank of America, N.A. (“BofA”). The amendment consents to, among other things, the change in control in connection with the P180 Acquisition, as well as a partial pay down of the subordinated debt (“Sun Debt Facility”) with SK Financial Services, LLC, an affiliate of Sun Capital, through increased borrowings under the ABL Credit Facility. On the same day, V Opco paid $15 million to SK Financial Services, LLC using proceeds from the ABL Credit Facility, which resulted in a pay-down of $20 million under the Sun Debt Facility (the “Sun Debt Paydown”).

In addition, P-180 acquired and assumed $7 million of the loans (the “P-180 Assumed Loan”) outstanding pursuant to the Sun Debt Facility and immediately thereafter cancelled such $7 million (the “P-180 Debt Forgiveness”).

Following the Sun Debt Paydown and P-180 Debt Forgiveness, the outstanding principal amount of subordinated loans is reduced by approximately $27 million with $7.5 million remaining outstanding under the Sun Debt Facility, which will continue to accrue payment-in-kind interest in accordance with, and otherwise be subject to, the terms and conditions therein.

Immediately following the P-180 Acquisition, P180 beneficially owned approximately 65% of all outstanding shares of common stock of VNCE and affiliates of Sun Capital continue to beneficially own approximately 2% of the Company’s outstanding common stock.

As part of the terms to the transactions described above, P-180 agreed to reimburse the Company for certain fees and expenses incurred in connection with such transactions, including the Company’s legal fees as well as the consent fee to BofA.

About P180:

P180, a new venture co-founded by Christine Hunsicker (founder and CEO of CaaStle, Inc.) and Brendan Hoffman, is dedicated to driving brand and retailer profitability by providing operational expertise and access to leading industry resources, including CaaStle’s innovative monetization platform. P180’s core mission is to invest in or acquire brands and retailers that stand to benefit from digital expertise and inventory monetization.

About VNCE:

Vince Holding Corp. is a global retail company that operates the Vince brand women’s and men’s ready to wear business. Vince, established in 2002, is a leading global luxury apparel and accessories brand best known for creating elevated yet understated pieces for every day effortless style. Vince Holding Corp. operates 47 full-price retail stores, 14 outlet stores, and its e-commerce site, vince.com and through its subscription service Vince Unfold, www.vinceunfold.com, operated by CaaStle, as well as through premium wholesale channels globally. Please visit www.vince.com for more information.

Forward-Looking Statements: This document contains forward-looking statements under the Private Securities Litigation Reform Act of 1995. Forward-looking statements include statements regarding, among other things, our planned transformation program and our current expectations about possible or assumed future results of operations of the Company and are indicated by words or phrases such as “may,” “will,” “should,” “believe,” “expect,” “seek,” “anticipate,” “intend,” “estimate,” “plan,” “target,” “project,” “forecast,” “envision” and other similar phrases. Although we believe the assumptions and expectations reflected in these forward-looking statements are reasonable, these assumptions and expectations may not prove to be correct and we may not achieve the results or benefits anticipated. These forward-looking statements are not guarantees of actual results, and our actual results may differ materially from those suggested in the forward-looking statements. These forward-looking statements involve a number of risks and uncertainties, some of which are beyond our control, including, without limitation: our ability to successfully manage the transition of VNCE majority ownership to P180 and to execute P180’s strategies for the Company; our ability to execute and realize the enhanced profitability expectations of our planned transformation program; our ability to maintain the license agreement with ABG Vince, a subsidiary of Authentic Brands Group; ABG Vince’s expansion of the Vince brand into other categories and territories; ABG Vince’s approval rights and other actions; our ability to maintain adequate cash flow from operations or availability under our revolving credit facility to meet our liquidity needs; our ability to realize the benefits of our strategic initiatives; general economic conditions; further impairment of our goodwill; the execution and management of our direct-to-consumer business growth plans; our ability to make lease payments when due; our ability to maintain our larger wholesale partners; our ability to remediate the identified material weakness in our internal control over financial reporting; our ability to comply with domestic and international laws, regulations and orders; our ability to anticipate and/or react to changes in customer demand and attract new customers, including in connection with making inventory commitments; our ability to remain competitive in the areas of merchandise quality, price, breadth of selection and customer service; our ability to attract and retain key personnel; seasonal and quarterly variations in our revenue and income; our ability to mitigate system security risk issues, such as cyber or malware attacks, as well as other major system failures; our ability to optimize our systems, processes and functions; our ability to comply with privacy-related obligations; our ability to ensure the proper operation of the distribution facilities by third-party logistics providers; fluctuations in the price, availability and quality of raw materials; commodity, raw material and other cost increases; the extent of our foreign sourcing; our reliance on independent manufacturers; other tax matters; and other factors as set forth from time to time in our Securities and Exchange Commission filings, including those described under “Item 1A—Risk Factors” in our Annual Report on Form 10-K and Quarterly Reports on Form 10-Q. We intend these forward-looking statements to speak only as of the time of this release and do not undertake to update or revise them as more information becomes available, except as required by law.

JERICHO, N.Y.–(BUSINESS WIRE)– 1-800-FLOWERS.COM, Inc. (NASDAQ: FLWS) (the “Company”),a leading provider of gifts designed to help inspire customers to give more, connect more, and build more and better relationships, today announced that the Company will release financial results for its fiscal 2025 second quarter on Thursday, January 30, 2025. The press release will be issued prior to market opening and will be followed by a conference call with members of senior management at 8:00 a.m. (ET).

The conference call will be available via live webcast from the Investors section of the Company’s website at www.1800flowersinc.com/investors. A recording of the call will be posted on the website within two hours of the call’s completion. A telephonic replay of the call can be accessed beginning at 2:00 p.m. (ET) on January 30, 2025, through February 6, 2025, at: (US) 1-877-344-7529; (Canada) 855-669-9658; (International) 1-412-317-0088; enter conference ID: #4981439.

Special Note Regarding Forward-Looking Statements:

Some of the statements contained in the Company’s scheduled Thursday, January 30, 2025, press release and conference call regarding its results for its fiscal 2025 second quarter, other than statements of historical fact, may be forward-looking within the meaning of the Private Securities Litigation Reform Act of 1995. These statements involve risks and uncertainties that could cause actual results to differ materially from those expressed or implied in the applicable statements. For a more detailed description of these and other risk factors, please refer to the Company’s SEC filings including its Annual Reports and Forms 10K and 10Q available at the Investor Relations section of the Company’s website at 1800flowersinc.com. The Company expressly disclaims any intent or obligation to update any of the forward-looking statements made in the scheduled conference call and any recordings thereof, or in any of its SEC filings, except as may be otherwise stated by the Company.

About 1-800-FLOWERS.COM, Inc.

1-800-FLOWERS.COM, Inc. is a leading provider of gifts designed to help inspire customers to give more, connect more, and build more and better relationships. The Company’s e-commerce business platform features an all-star family of brands, including: 1-800-Flowers.com®, 1-800-Baskets.com®, Cheryl’s Cookies®, Harry & David®, PersonalizationMall.com®, Shari’s Berries®, FruitBouquets.com®, Things Remembered®, Moose Munch®, The Popcorn Factory®, Wolferman’s Bakery®, Vital Choice®, Simply Chocolate® and Scharffen Berger®. Through the Celebrations Passport® loyalty program, which provides members with free standard shipping and no service charge on eligible products across our portfolio of brands, 1-800-FLOWERS.COM, Inc. strives to deepen relationships with customers. The Company also operates BloomNet®, an international floral and gift industry service provider offering a broad-range of products and services designed to help members grow their businesses profitably; Napco℠, a resource for floral gifts and seasonal décor; DesignPac Gifts, LLC, a manufacturer of gift baskets and towers; Alice’s Table®, a lifestyle business offering fully digital livestreaming and on demand floral, culinary and other experiences to guests across the country; and Card Isle®, an e-commerce greeting card service. 1-800-FLOWERS.COM, Inc. was recognized among America’s Most Trustworthy Companies by Newsweek. 1-800-FLOWERS.COM, Inc. was also recognized as one of America’s Most Admired Workplaces for 2025 by Newsweek and was named to the Fortune 1000 list in 2022. Shares in 1-800-FLOWERS.COM, Inc. are traded on the NASDAQ Global Select Market, ticker symbol: FLWS. For more information, visit 1800flowersinc.com.

Key Points: – U.S. holiday spending in 2024 is projected to reach nearly $1 trillion, driven by wage growth and consumer demand. – Over one-third of Americans incurred debt this holiday season, with an average balance of $1,181. – Credit card interest rates remain above 20%, making it crucial to pay off balances quickly to avoid long-term financial strain.

As the holiday season winds down, American consumers are grappling with the financial aftermath of record-breaking spending. Fueled by strong consumer demand and elevated prices, holiday expenditures are set to reach historic levels. However, this surge in spending has coincided with a sharp rise in credit card debt, painting a mixed picture of financial resilience and vulnerability.

According to the National Retail Federation (NRF), U.S. holiday spending for the 2024 season is projected to hit between $979.5 billion and $989 billion. These numbers reflect robust consumer activity from November 1 through December 31, buoyed by wage growth, modest inflation, and healthy household balance sheets.

Jack Kleinhenz, the NRF’s chief economist, commented that these factors have “led to solid holiday spending.” Despite economic uncertainties, consumers have shown remarkable willingness to shop for gifts, experiences, and celebrations.

This holiday season, however, many Americans have leaned heavily on credit cards to fund their purchases. A LendingTree survey revealed that 36% of shoppers took on debt during the season, with the average amount owed climbing to $1,181, up from $1,028 last year.

Matt Schulz, chief credit analyst at LendingTree, pointed to inflation as a key driver behind this trend, saying, “Prices are still really high, and that means lots of Americans simply didn’t have any choice.” For many, the combination of rising costs and the desire to maintain holiday traditions has outweighed concerns about accumulating debt.

Even before the holiday shopping frenzy, credit card debt in the U.S. was at an all-time high. Data from the Federal Reserve Bank of New York shows that balances were 8.1% higher year-over-year heading into the season. Compounding this issue, a NerdWallet report found that 28% of consumers had not fully paid off the credit card debt incurred during last year’s holiday season.

While some see increased spending as a sign of consumer confidence, the costs associated with credit card borrowing remain a significant concern. Interest rates on credit cards now average more than 20%, with some retail card rates climbing even higher.

For those unable to pay off their balances quickly, the financial repercussions can be steep. LendingTree’s survey indicated that 21% of those with holiday debt expect it to take five months or longer to pay off. This extended timeline can lead to ballooning interest charges, diminishing consumers’ ability to save or meet other financial goals.

Schulz warns, “High-interest debt means less money to put towards building an emergency fund, saving for college, or even covering basic expenses. In extreme cases, it can lead to financial insecurity.”

As the new year approaches, financial experts urge consumers to prioritize paying down holiday debt as quickly as possible. Strategies such as creating a repayment plan, consolidating debt, or transferring balances to a lower-interest option can help mitigate the impact of high interest rates.

While the 2024 holiday season may have been a record-setter in terms of spending, its legacy will likely serve as a cautionary tale about the dangers of relying too heavily on credit in an era of rising costs.