With New Money Deposited Into Their IRA Accounts, Savers Are Faced With an Age-Old Question

With days until the IRS is expecting our tax filings, IRA season is in full swing. With this comes contributions to IRA accounts and individual investment decisions. This year economic uncertainty is a regular topic of conversation; the question has come up in both personal and professional conversations whether or not this money should be invested immediately or wait for a clearer sign of economic and market direction. I asked three financial professionals, each of whose opinion I respect. Did I get three different answers? You be the judge.

Robert R. Johnson, PhD, CFA, CAIA, is the former deputy CEO of the CFA Institute and was President of the College of Financial Services. Currently Dr. Johnson is a Professor of Finance, Heider College of Business at Creighton University. His credentials also include co-author of The Tools and Techniques of Investment Planning, Strategic Value Investing, Investment Banking for Dummies, and others. Overall, his response argues for not shying away from what traditionally has been better-performing investments over time.

He highlighted that investing for as long as possible should involve not waiting until a week before the tax date and making a maximum deposit. If your money is sitting in cash rather than invested, there is a cash performance drag as cash including money markets, more often than not, is a worse performer than equities.

The finance professor pointed out the statistical truth that holding significant amounts of cash ensures that one will suffer significant opportunity losses. Johnson says, “when it comes to building wealth, one can either sleep well or eat well.” He explains, “investing conservatively allows one to sleep well, as there isn’t much volatility. But, it doesn’t allow you to eat well in the long run because your account won’t grow much.”

He backs this up with data compiled by Ibbotson Associates data on large capitalization stocks (think S&P 500), which returned 10.1% compounded annually from 1926-2022. Johnson points out that during the same years, government bonds returned 5.2% annually and T-bills returned 3.2% annually. He explained, “to put it in perspective, $1.00 in invested in the S&P 500 at the start of 1926 would have grown to $11,307.59 (with all dividends reinvested).” He then compared, “that same dollar invested in T-bills would have grown to $21.23.”

What to invest in is certainly an important decision, Dr. Johnson explained, “The surest way to build wealth over long time horizons is to invest in a diversified portfolio of common stocks. Someone with a long time horizon should not have exposure to money market instruments, yet many investors do because they fear the volatility of the stock market.”

Dennie Ceelen, CFP has been part of the Noble Capital Markets Private Client Group in Boca Raton, FL since 2002. He provides wealth management services to NOBLE Clients. He’s also a committee member of The Society of Financial Service Professionals.

When asked if one should invest or wait, he apologetically answered, “it depends.”

Mr. Ceelen explains that when it comes to investments, one size does not fit all. A nineteen-year-old with little or no table income and only an extra $1,000 to put away may be better off investing in education or a car to get them to work. This idea of no IRA deposit at all could even be true of a couple saving to buy their first home. If putting the maximum away for retirement, 40 years away, prevents the purchase of a home in the next year or two, it may not make sense to fund an IRA at all for them this tax year.

For those that are regularly funding an IRA he said, “if your timeline is 30-years until you retire, invest immediately.” Ceelen explained, the general rule of thumb is that the markets over time will go up, the market will be higher in 30 years,” is the expectation based on past experience.

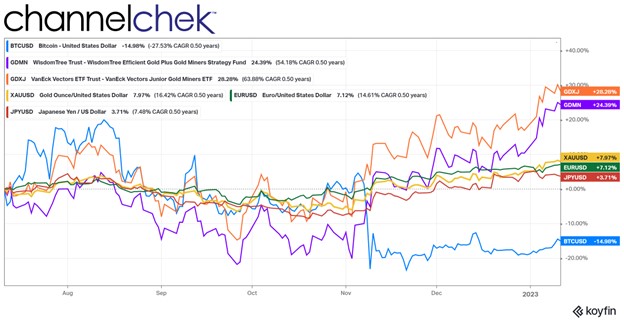

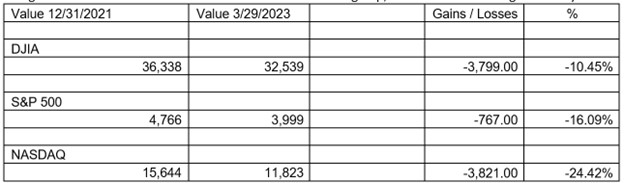

While talking about those with far less than 30-years until retirement, he pulled out a simple spreadsheet that shows that markets don’t always go up. A screenshot of this spreadsheet of major index performance from the close of business the last day of 2021 until March 29, 2023 is provided below.

Dennie Ceelen used the spreadsheet to show why he said “it depends.” He said, “if you are retiring in the next two years, make the contribution, take advantage of the tax break but let it sit in cash, or take advantage of the high rates on money markets/short term CD’s.”

“There is no reason to partake in this volatile market if you are that close to retirement,” he cautioned for those close to retirement. Making decisions like this is why many hire financial professionals.

David M. Wright, CLU, ChFC, president and owner of Wright Financial Group, with offices in Ohio and Florida is a 36-year veteran in the financial services industry. He hosts a local radio show called Retirement Income Source with David Wright, and is a frequent guest on TD Ameritrade Insights. One of Mr. Wright’s focuses is on providing workable retirement solutions for those in or close to retirement. His upcoming book, Bonfire of the Sanities: Reset Your Retirement Portfolio for Today’s Financial Lunacy, will be available later this year.

“How you invest your IRA for the 2022-23 tax season has been and always will be a function of your time horizon and propensity for risk,” Wright was quick to point out.

Wright’s explanation as to whether the timing is right also included what he believes would be the more suitable investment. He offered, “for individuals who are more than 10-15 years away from needing to access their cash, choosing high quality, dividend-paying companies with good cash flow are probably the best bet right now, given the economic tightening that will certainly impact more highly leveraged companies that have to refinance their debt in the future.” He cautioned that those in the age category above, “growth stocks, in particular those that pay very small dividends will probably be the most impacted by the Federal Reserve’s mandate to fight inflation by raising rates.”

For those even closer to retirement, five to ten years, he said that a dollar-cost averaging strategy to more slowly enter the market is more prudent, “you are systematically buying into the market without worrying about the purchase price of the investment itself,” Wright said.

“For those individuals that are within five years or less of retirement, pushing the pause button and purchasing short duration treasuries probably makes the most sense right now due to the higher yields offered courtesy of the Federal Reserve – with 3 month yields 4.8% at the moment,” David Wright explained for those with less time before needing the account for living expenses.

Wright added one more note of advice for the current tax season, “with the mixed signals of financial news from bank failures to reducing inflation, it probably makes sense to be more cautious right now until the financial storms subside.”

Take Away

There are many right ways to do anything. Multiply that by the different stages of life, and then there are many more. If you are making a last-minute 2022 tax year IRA deposit, hopefully, there are words of wisdom among these three professionals that have been useful.

Overall it seems time in the market is expected to outperform time out of the market, with the caveat, over the short term, anything can happen.

Managing Editor, Channelchek