Palladium One step out hole delivers wide, high-grade mineralization at Kaukua South

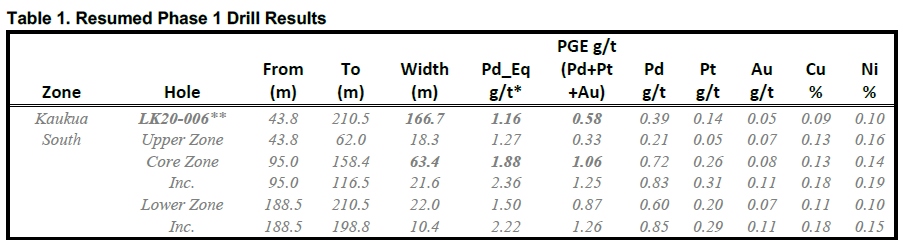

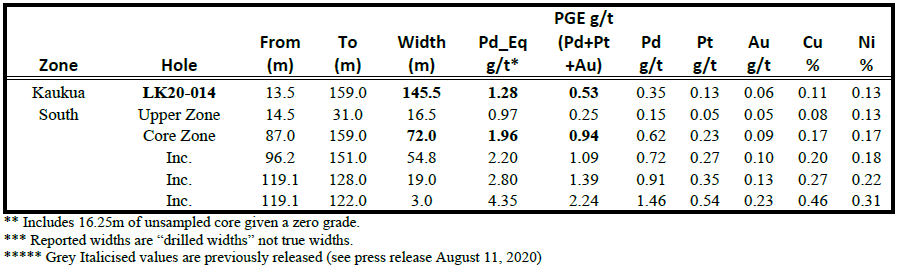

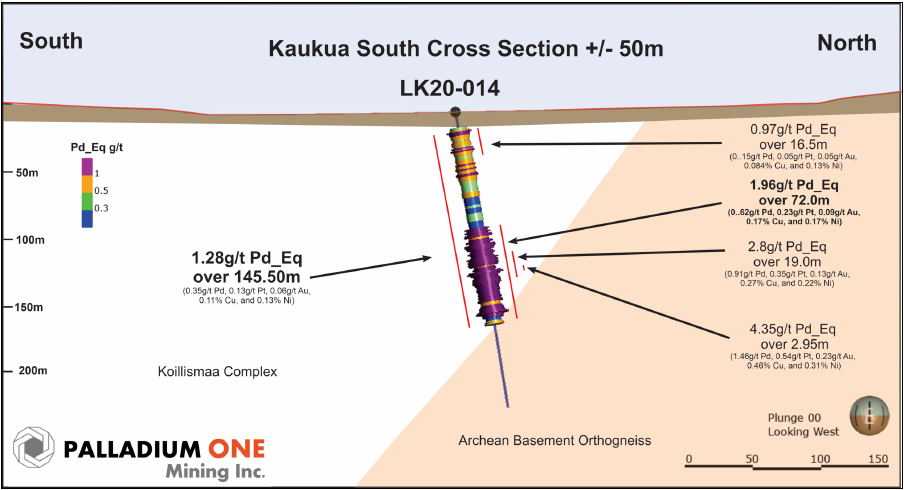

October 06, 2020 – Toronto, Ontario – The first assay results from the resumed Phase I drill program at the LK Project in Finland has retuned a wide zone, of shallow, high grade palladium mineralization in the Kaukua South Extension, said Palladium One Mining Inc. (“Palladium One” or the “Company”) (TSXV: PDM, FRA: 7N11, OTC: NKORF) today. Hole LK20-014 returned a core zone of 72.0 m at 1.96 g/t palladium equivalent (Pd_Eq)* within a wider zone of 145.5m at 1.26 g/t Pd_Eq.

Key highlights:

- Continuity between holes LK20-006 and LK20-014 demonstrates potential to rapidly add tonnes and thereby scale to existing NI 43-101 resources.

- Shallow mineralization developing at scale within the Kaukua South Zone.

- Starting at only 13.5 meters downhole, hole LK20-014 returned 145.5 m at 1.26 g/t Pd_Eq. with a core zone of 72 m at 1.96 g/t Pd_Eq.

- Hole LK20-014 is 100 m east of hole LK20-006 which returned 166.7 m at 1.27 g/t Pd_Eq. with a core zone of 63.4 m at 1.88 g/t Pd_Eq.

“Results from the Kaukua South Zone continue to indicate that the Kaukua area hosts the footprint of a large-scale, shallow, mineralized system displaying continuity,” said Derrick Weyrauch, President and Chief Executive Officer.

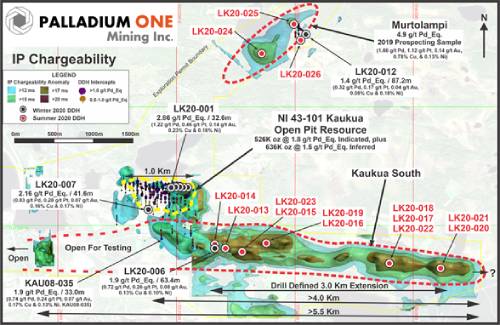

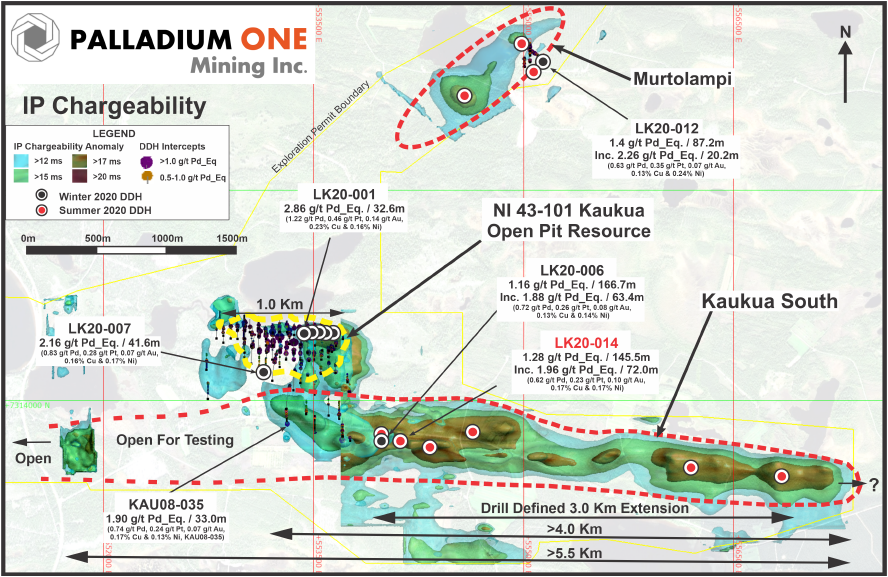

Hole LK20-014 is 100 m east of hole LK20-006 (see news release dated August 11, 2020), which returned nearly identical grades and widths (Table 1) and is 800 m east of hole KAU-08-035, which returned a core zone of 33 m at 1.90 g/t Pd_Eq (Figure 1).

These consistent core intercepts validate the Company’s thesis that there are more tonnes than initially thought at Palladium One’s LK Project in Finland. The shallow and high-grade core intercepts provide the opportunity to significantly increase the existing NI 43-101 Kaukua open pit resource.

Phase 1 Drill Program Update

The Company continues to log and sample the drill core from the recently completed drilling program. Fourteen holes totalling 2,566 m were completed during the resumed program in August and September, bringing the total Phase I exploration drilling program to 26 holes totalling 4,490 m.

*Palladium Equivalent

Palladium equivalent (Pd_Eq) is calculated using US$1,100/oz for palladium, US$950/oz for platinum, US$1,300/oz for gold, US$6,614/t for copper and US$15,432/t for nickel as used in the Company’s 2019, 43-101 mineral resource estimate on the Kaukua Deposit (see press release September 9, 2019).

Figure 1

This figure shows the greater Kaukua Area, the NI 43-101 compliant Kaukua Open Pit resource, Murtolampi and Kaukua South zones. The new drill defined three-kilometer eastern extension of the Kaukua South zone is shown with the resumed Phase I drill holes labelled in red.

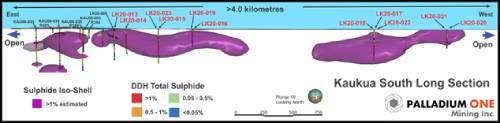

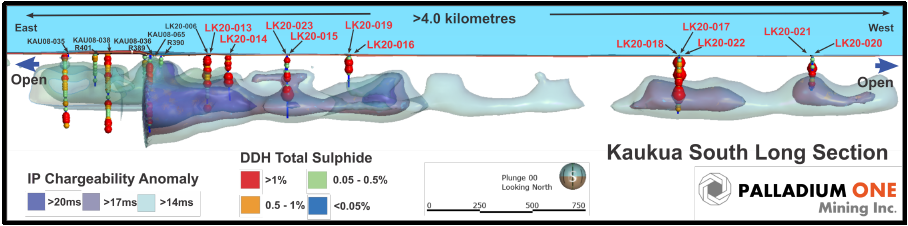

Figure 2

Kaukua South Long section showing IP Chargeability isoshells and down hole logged sulfide percentages, resumed Phase I drill holes labelled in red.

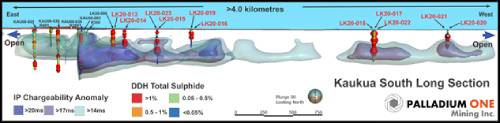

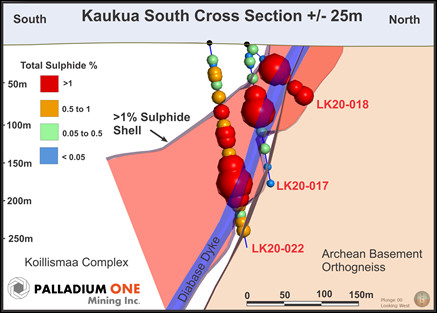

Figure 3

Kaukua South cross section, looking west showing hole LK20-014.

QA/QC

The Phase I drilling program was carried out under the supervision of Neil Pettigrew, M.Sc., P. Geo., Vice President of Exploration and a director of the Company.

Drill core samples were split using a rock saw by Company staff, with half retained in the core box and stored indoors in a secure facility, in Taivalkoski, Finland. The drill core samples were transported by courier from the Company’s core handling facility in Taivalkoski, Finland, to ALS Global (“ALS”) laboratory in Outokumpu, Finland. ALS, is an accredited lab and are ISO compliant (ISO 9001:2008, ISO/IEC 17025:2005). PGE analysis was performed using a 30 grams fire assay with an ICP-MS or ICP-AES finish. Multi-element analyses, including copper and nickel were analysed by four acid digestion using 0.25 grams with an ICP-AES finish.

Certified standards, blanks and crushed duplicates are placed in the sample stream at a rate of one QA/QC sample per 10 core samples. Results are analyzed for acceptance at the time of import. All standards associated with the results in this press release were determined to be acceptable within the defined limits of the standard used.

Qualified Person

The technical information in this release has been reviewed and verified by Neil Pettigrew, M.Sc., P. Geo., Vice President of Exploration and a director of the Company and the Qualified Person as defined by National Instrument 43- 101.

About Palladium One

Palladium One Mining Inc. is an exploration company targeting district scale, platinum-group-element (PGE)-coppernickel deposits in Finland and Canada. Its flagship project is the Läntinen Koillismaa or LK Project, a palladiumdominant platinum group element-copper-nickel project in north-central Finland, ranked by the Fraser Institute as one of the world’s top countries for mineral exploration and development. Exploration at LK is focused on targeting disseminated sulfides along 38 kilometers of favorable basal contact and building on an established NI 43-101 open pit resource.

ON BEHALF OF THE BOARD

“Derrick Weyrauch”

President & CEO, Director

For further information contact:

Derrick Weyrauch, President & CEO

Email: info@palladiumoneinc.com

Neither the TSX Venture Exchange nor its Market Regulator (as that term is defined in the policies of the TSX Venture Exchange) accepts responsibility for the adequacy or accuracy of this release.

This press release is not an offer or a solicitation of an offer of securities for sale in the United States of America. The common shares of Palladium One Mining Inc. have not been and will not be registered under the U.S. Securities Act of 1933, as amended, and may not be offered or sold in the United States absent registration or an applicable exemption from registration.

Information set forth in this press release may contain forward-looking statements. Forward-looking statements are statements that relate to future, not past events. In this context, forward-looking statements often address a company’s expected future business and financial performance, and often contain words such as “anticipate”, “believe”, “plan”, “estimate”, “expect”, and “intend”, statements that an action or event “may”, “might”, “could”, “should”, or “will” be taken or occur, or other similar expressions. By their nature, forward-looking statements involve known and unknown risks, uncertainties and other factors which may cause our actual results, performance or achievements, or other future events, to be materially different from any future results, performance or achievements expressed or implied by such forward-looking statements. Such factors include, among others, risks associated with project development; the need for additional financing; operational risks associated with mining and mineral processing; fluctuations in palladium and other commodity prices; title matters; environmental liability claims and insurance; reliance on key personnel; the absence of dividends; competition; dilution; the volatility of our common share price and volume; and tax consequences to Canadian and U.S. Shareholders. Forward-looking statements are made based on management’s beliefs, estimates and opinions on the date that statements are made and the Company undertakes no obligation to update forward-looking statements if these beliefs, estimates and opinions or other circumstances should change. Investors are cautioned against attributing undue certainty to forward-looking statements.