Canada Nickel Company Announces Significant Mineral Resource Update at Crawford Nickel-Cobalt Sulphide Project

Highlights

-

Resource update more than doubles Measured and Inferred resources

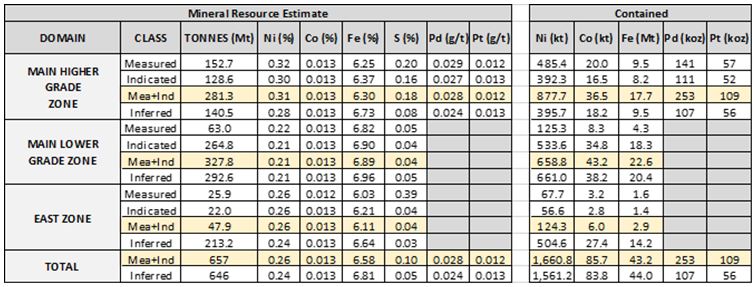

- Main Higher Grade Zone Measured resource increased by 162% to 153 Mt at 0.32% nickel (485 kt nickel). Total M&I resource increased by 9% to 657 Mt at 0.26% nickel (1.7 Mt nickel).

- Total Inferred resource increased by 121% to 646 Mt at 0.24% nickel (1.6 Mt nickel) including an increase of 50% in Main Zone (433 Mt @ 0.23% nickel) and an initial resource from East Zone of 213 Mt at 0.24% nickel (505 kt nickel).

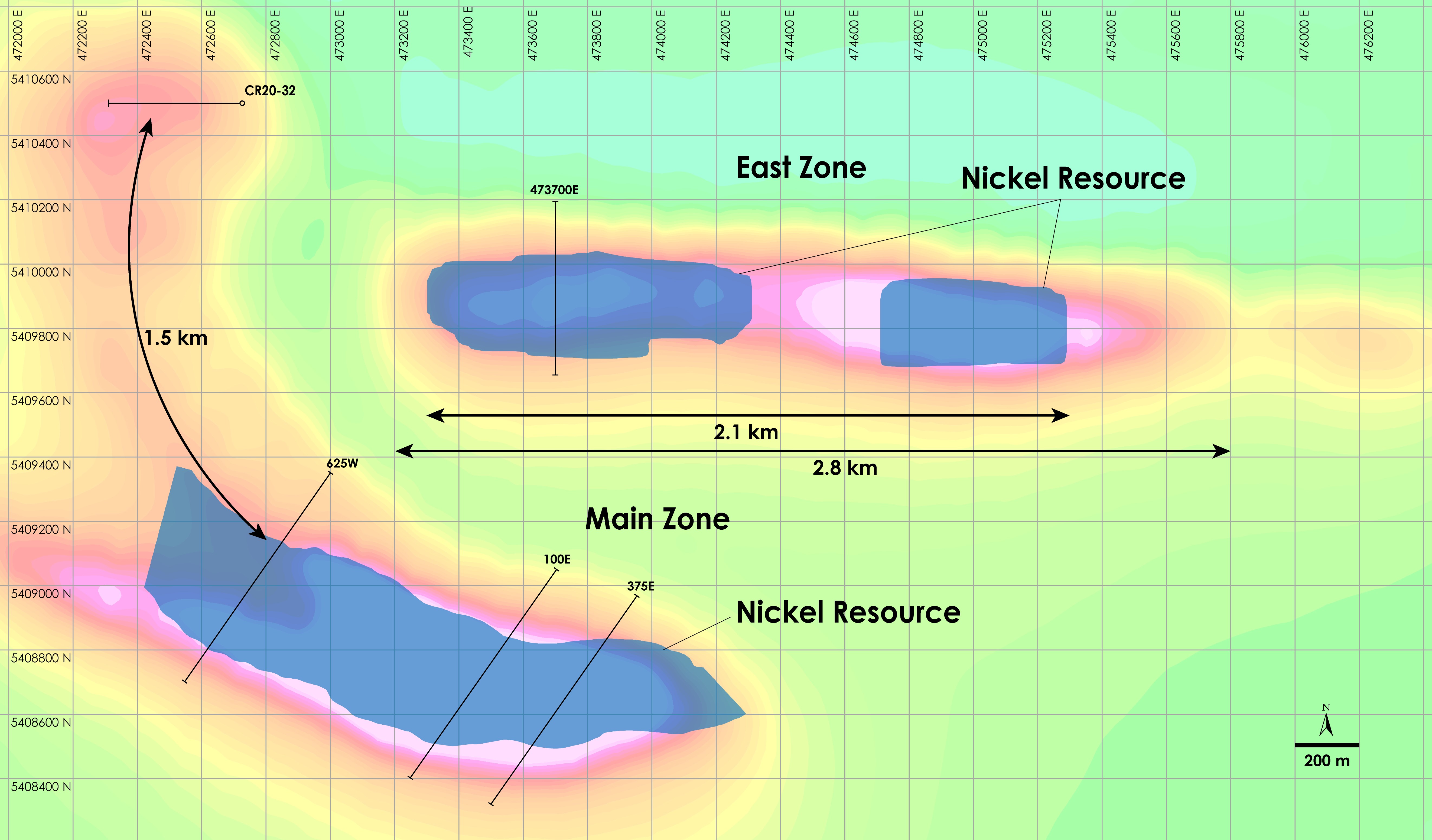

- Significant exploration potential remains with approximately 50% of Crawford structure untested and is now actively being explored. The Main Zone remains open to the west and the East Zone has more than 2.8 kilometres of strike length (40%) remaining to be drilled.

TORONTO, October 21, 2020 – Canada Nickel Company Inc. (TSX-V:CNC) (“Canada Nickel” or the “Company“) today announced an updated mineral resource for its 100% owned Crawford Nickel-Cobalt Sulphide Project (“Crawford”) near Timmins, Ontario which more than doubles mineral resources in both Measured and Inferred resource categories. This report includes a resource update for its previously reported Main Zone and an initial resource for its East Zone.

Mark Selby, Chair and CEO of Canada Nickel commented, “This latest drilling phase did an outstanding job of delivering on both of its key objectives – better defining and increasing the Main-Higher Grade Zone and establishing an initial resource in the East Zone. With a 162% increase in the Measured High Grade Zone nickel content, a 121% increase in total inferred resources, and an initial East Zone resource, this resource update puts us in excellent position for the delivery of a Preliminary Economic Analysis (“PEA”) by year-end. I look forward to continued drilling results as we explore several highly prospective nickel and PGM targets at Crawford, and to completing the remaining metallurgical and engineering testing for the PEA. With the recently completed financing, the Company is well-positioned to aggressively advance Crawford towards a Feasibility Study expected by year-end 2021.”

The Crawford Nickel-Cobalt Sulphide Project is located in the heart of the prolific Timmins-Cochrane mining camp in Ontario, Canada, and is adjacent to well-established, major infrastructure associated with over 100 years of regional mining activity. Canada Nickel has launched wholly-owned NetZero Metals Inc. with the aim to develop zero-carbon production of nickel, cobalt, and iron at the Crawford Project.

Crawford Mineral Resource Estimate Update

For the update to the initial Mineral Resource Estimate, a total of 30,519 metres of core drilling in 62 drill holes was utilized to calculate the Mineral Resources in the three categories as provided in Table 1 below, and specifically Measured + Indicated Resources of 657 million tonnes grading 0.26% Ni and Inferred Resources of 646 million tonnes grading 0.24% Ni. A cut-off grade of 0.15% Ni was used for the low-grade domain and 0.25% Ni for the higher-grade domain (Higher Grade Core) of the Mineral Resource Estimate. Example cross-section and block model views of the resource estimate are provided in Figures 1 through 5 below.

The drilling program was launched in the fourth quarter of 2019, continued through 2020, and achieved the objectives of finding extensions around the initial resource and new areas of mineralization, as well as proving up the extension and the continuity of the mineralization.

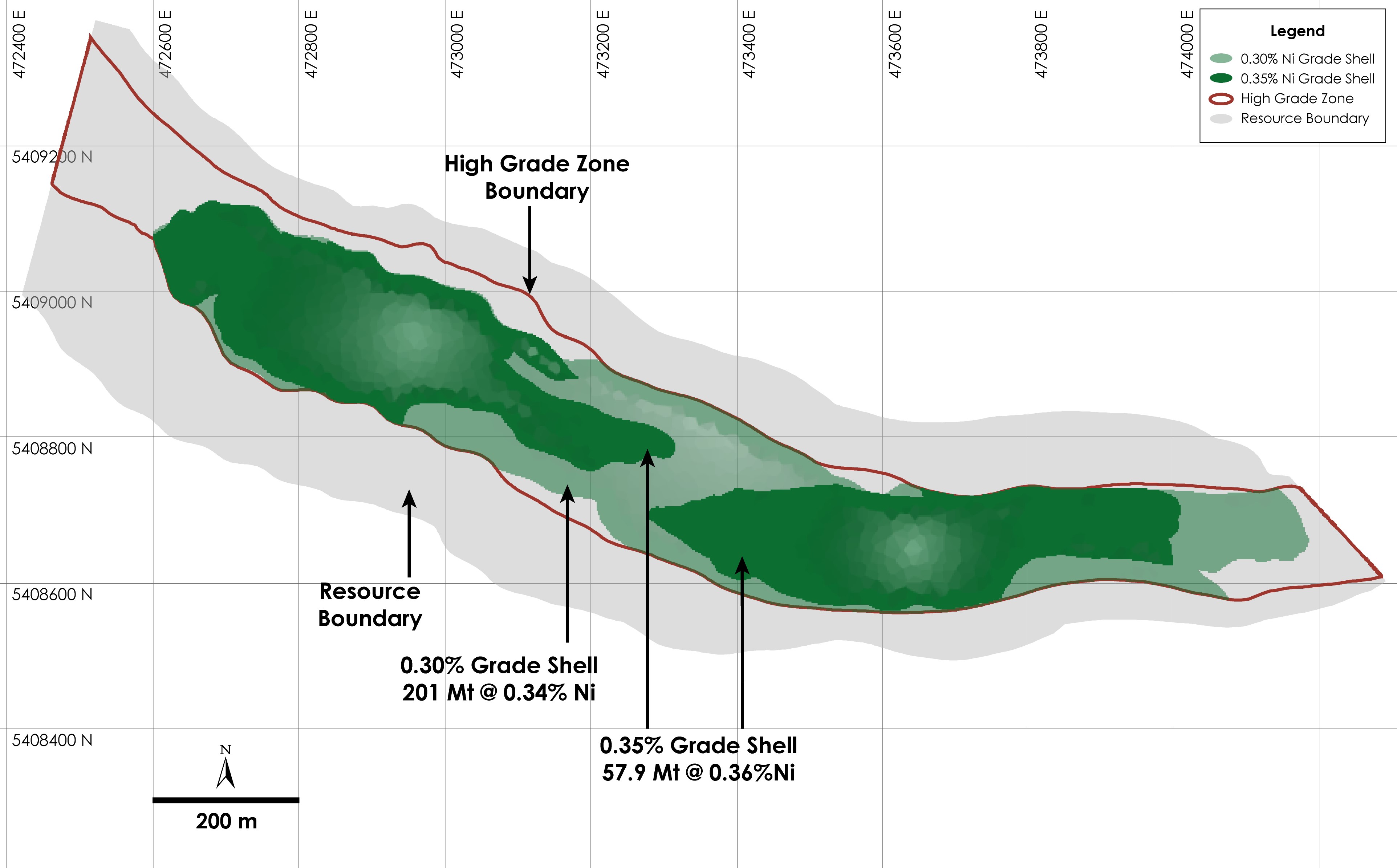

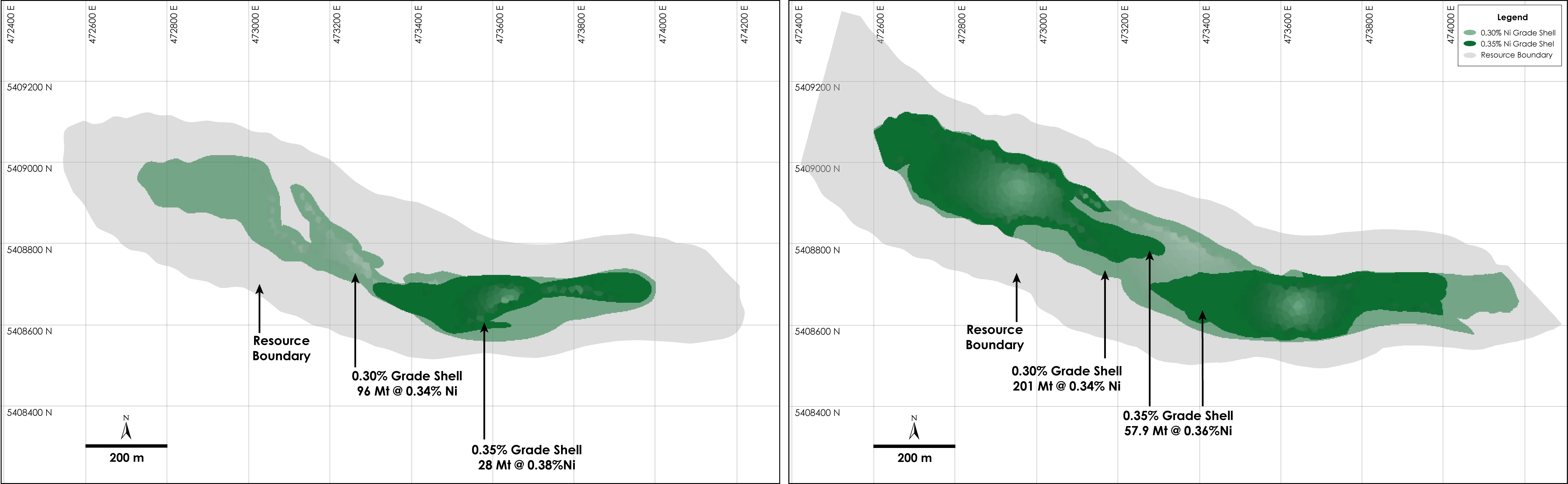

The higher grade mineralization at Crawford has been significantly expanded. This resource update increased the contained nickel in the 0.35% grade shell by 96% to 208kt (58 Mt at 0.36% nickel) and in the 0.30% grade shell by 109% to 683kt (201 Mt at 0.34% nickel).

Canada Nickel announced on May 19, 2020 the discovery of the East Zone. After an 11-hole, 5,328-metres drilling campaign, Canada Nickel is pleased to declare an initial Measured + Indicated Resources on the East Zone of 47.9 million tonnes grading 0.26% Ni and Inferred Resources of 213.2 million tonnes grading 0.24% Ni. A cut-off grade of 0.15% Ni was used.

This Mineral Resource Estimate was prepared by Caracle Creek International Consulting Inc. in accordance with CIM Definition Standards on Mineral Resources and Reserves. A Technical Report in support of the Mineral Resource Estimate will be filed on SEDAR (https://www.sedar.com) within 45 days. The Mineral Resource Estimate is effective as of October 18, 2020.

Table 1 – Updated Total Mineral Resource Estimate for the Crawford Nickel-Cobalt Sulphide Project, Ontario

- The independent Qualified Person for the Mineral Resource Estimate, as defined by NI 43-101, is Mr. Luis Oviedo, P.Geo. (Chilean Mining Commission: RM, CMC #013), of Caracle Creek International Consulting Inc. and Atticus Chile S.A. The effective date of the Mineral Resource Estimate is October 18, 2020.

- These Mineral Resources are not Mineral Reserves as they do not have demonstrated economic viability. The quantity and grade of reported Inferred Resources in this Mineral Resource Estimate are uncertain in nature and there has been insufficient exploration to define these Inferred Resources as Indicated or Measured, however it is reasonably expected that the majority of Inferred Mineral Resources could be upgraded to Indicated Mineral Resources with continued exploration.

- A cut-off grade of 0.15% Ni was used for the low-grade domains (Main and East zones) and cut-off grades of 0.25% Ni (Main Zone) and 0.21% Ni (East Zone) were used for the high-grade domains. Cut-offs were determined on the basis of core assay geostatistics and drill core lithologies for the deposit, and by comparison to analogous deposit types. Given the current stage of the Project, the mineral resources contained within the Main and East zone deposits have not been constrained by open pit optimization. The Company is planning to complete open pit optimization and present pit-constrained mineral resources as part of its Preliminary Economic Assessment (“PEA”) scheduled to be completed by year-end 2020.

- Geological and block models for the Mineral Resource Estimate used data from a total of 62 surface drill holes (51 in the Main Zone and 11 in the East Zone), completed by Spruce Ridge Resources (4 holes in 2018) and Noble Mineral Exploration and Canada Nickel Company (58 holes in 2019-2020). The drill database was validated prior to resource estimation and QA/QC checks were made using industry-standard control charts for blanks, core duplicates and commercial certified reference material inserted into assay batches by CNC and by comparison of umpire assays performed at a second laboratory.

- Estimates in Table 1 have been rounded to two significant figures.

- The Mineral Resource Estimate was prepared following the CIM Estimation of Mineral Resources & Mineral Reserves Best Practice Guidelines (November 29, 2019).

MAIN ZONE

- The geological model as applied to the Mineral Resource Estimate for the Main Zone comprises three mineralized domains hosted by variably serpentinized ultramafic rocks: a relatively high-grade core (largely dunite) and two northern and southern lower grade envelopes (combination of dunite and peridotite). Individual wireframes were created for each domain.

- The block model was prepared using Micromine 2020. A 12 m x 12 m x 9 m block model was created and samples were composited at 4.5 m intervals. Grade estimation from drill hole data was carried out for Ni, Co, Fe, S, Pd and Pt using the Ordinary Kriging interpolation method.

- Grade estimation was validated by comparison of input and output statistics (nearest neighbour and inverse distance cubed), swath plot analysis, and by visual inspection of the assay data, block model, and grade shells in cross-sections.

- Density estimation was carried out for the mineralized domains using the Ordinary Kriging interpolation method, on the basis of 3,270 specific gravity measurements collected during the core logging process, using the same block model parameters of the grade estimation. As a reference, the average estimated density value within the high-grade is 2.64 g/cm3 (t/m3), while low-grade domains of the resource model yielded averages of 2.63 g/cm3 (t/m3) in the north and 2.71 g/cm3 (t/m3) in the south.

EAST ZONE

- The geological model as applied to the Mineral Resource Estimate for the East Zone comprises three mineralized domains hosted by variably serpentinized ultramafic rocks: a relatively high-grade core (largely dunite) and two northern and southern lower grade envelopes (largely peridotite). Individual wireframes were created for each domain.

- The block model was prepared using Micromine 2020. A 20 m x 20 m x 15 m block model was created and samples were composited at 3 m intervals. Grade estimation from drill hole data was carried out for Ni, Co, Fe and S using the Inverse Distance Squared method.

- Grade estimation was validated by comparison of input and output statistics (nearest neighbour), swath plot analysis, and by visual inspection of the assay data, block model, and grade shells in cross-sections.

- An average bulk density value for each mineralized domain was calculated on the basis of 244 specific gravity measurements collected during the core logging process. Blocks within the high-grade were assigned a single bulk density value of 2.62 g/cm3 (t/m3), while low-grade domains of the resource model were assigned single bulk density values of 2.66 g/cm3 (t/m3) in the north and 2.72 g/cm3 (t/m3) in the south.

Figure 1 – Plan view of Main Zone & East Zone Nickel Resources, Crawford Nickel-Cobalt Sulphide Project, Ontario.

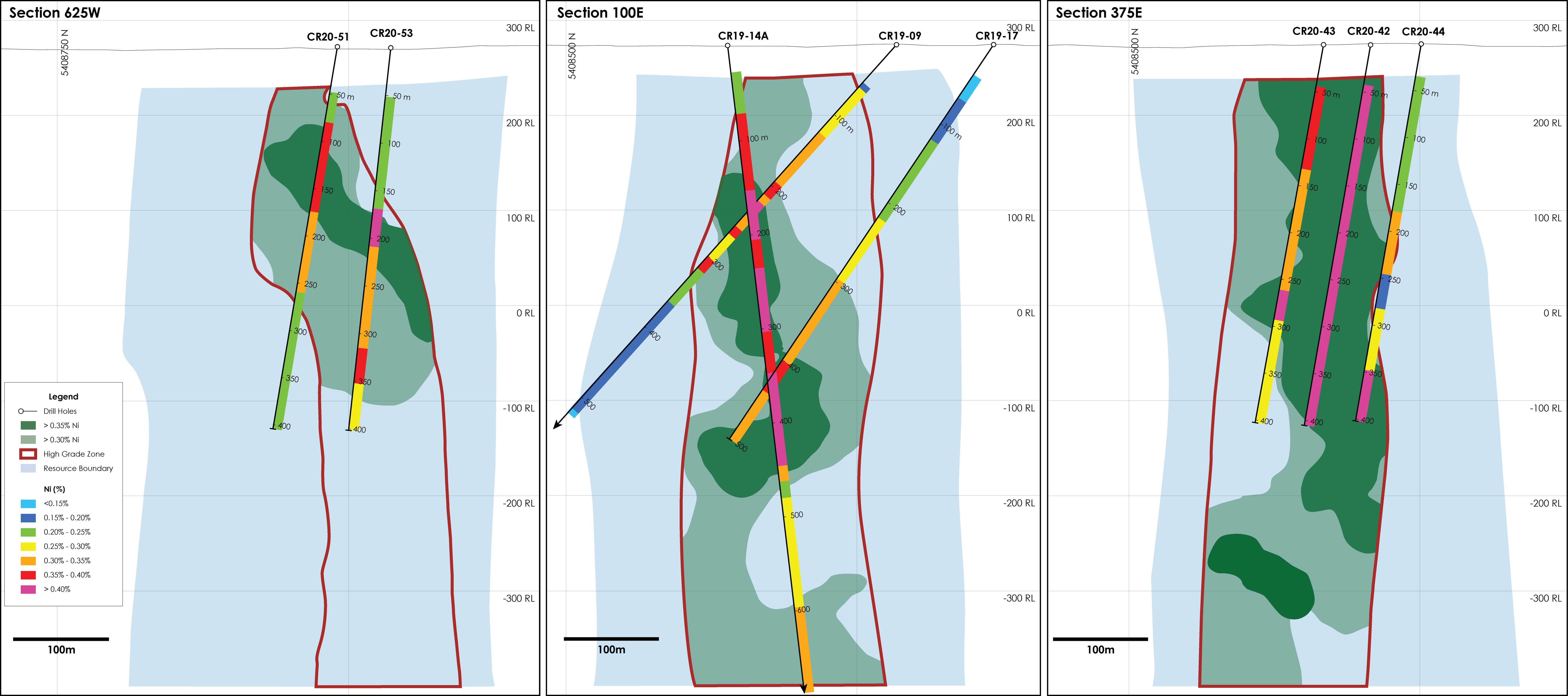

Figure 2 – Crawford Nickel-Cobalt Sulphide Project – Main Zone Sections (625E, 175E, 375E) With Resource Boundaries & 0.3% and 0.35% Grade Shells

Figure 3 – Plan View of Main Zone Resource at the Crawford Nickel-Cobalt Sulphide Project, Ontario.

Figure 4 – Plan View of Main Zone – Comparison of Current and Prior Mineral Resource and Grade Shells at the Crawford Nickel-Cobalt Sulphide Project, Ontario.

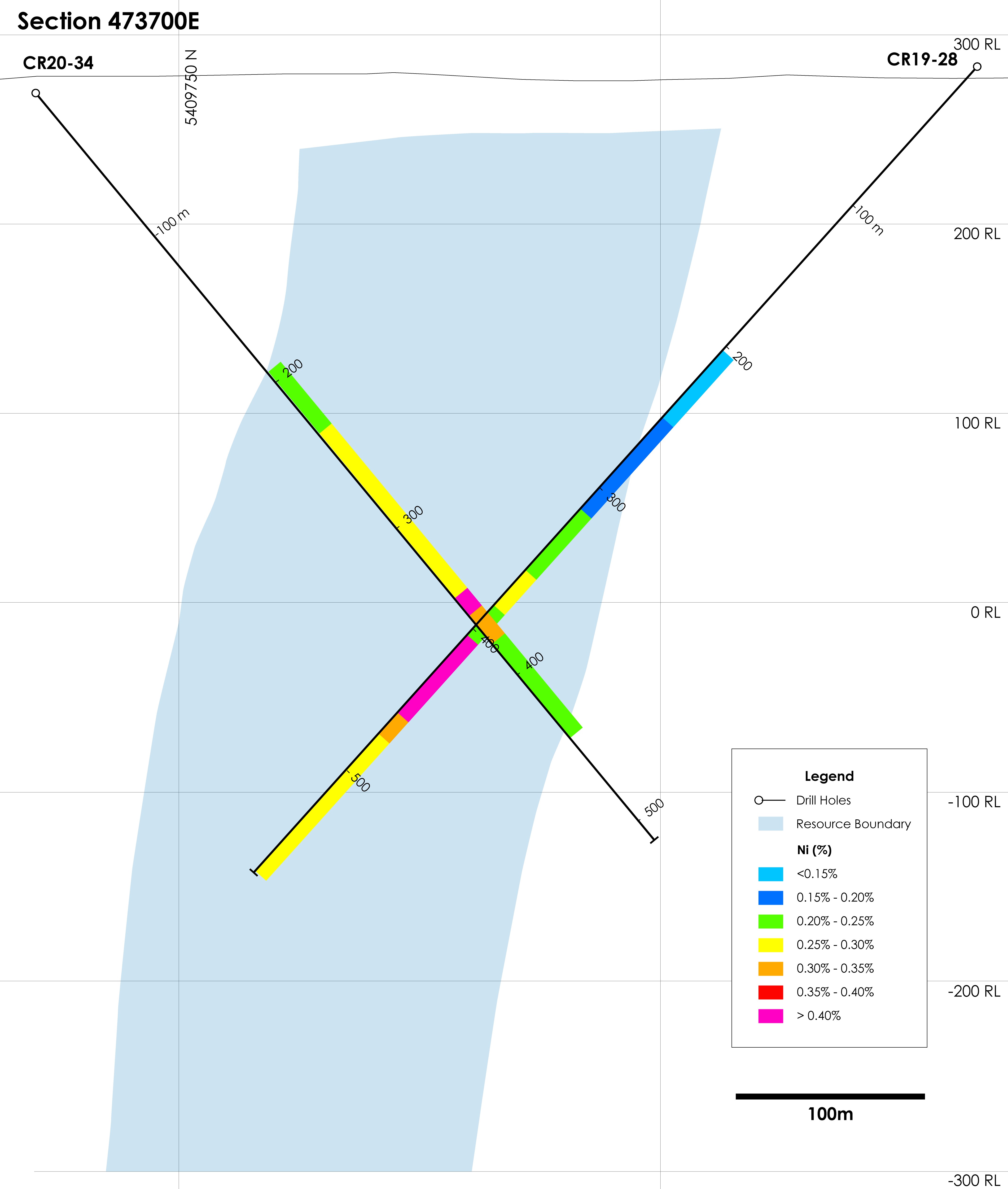

Figure 5 – Cross-section of the East Zone Mineral Resource, Crawford Nickel-Cobalt Sulphide Project, Ontario.

Next Steps

- A technical report with respect to the Mineral Resource Estimate Update disclosed today will be filed within 45 days as required by The National Instrument 43-101.

- Mineralogical studies and metallurgical testwork will continue through the fourth quarter of 2020, and will be incorporated into the PEA expected to be completed by the end of 2020.

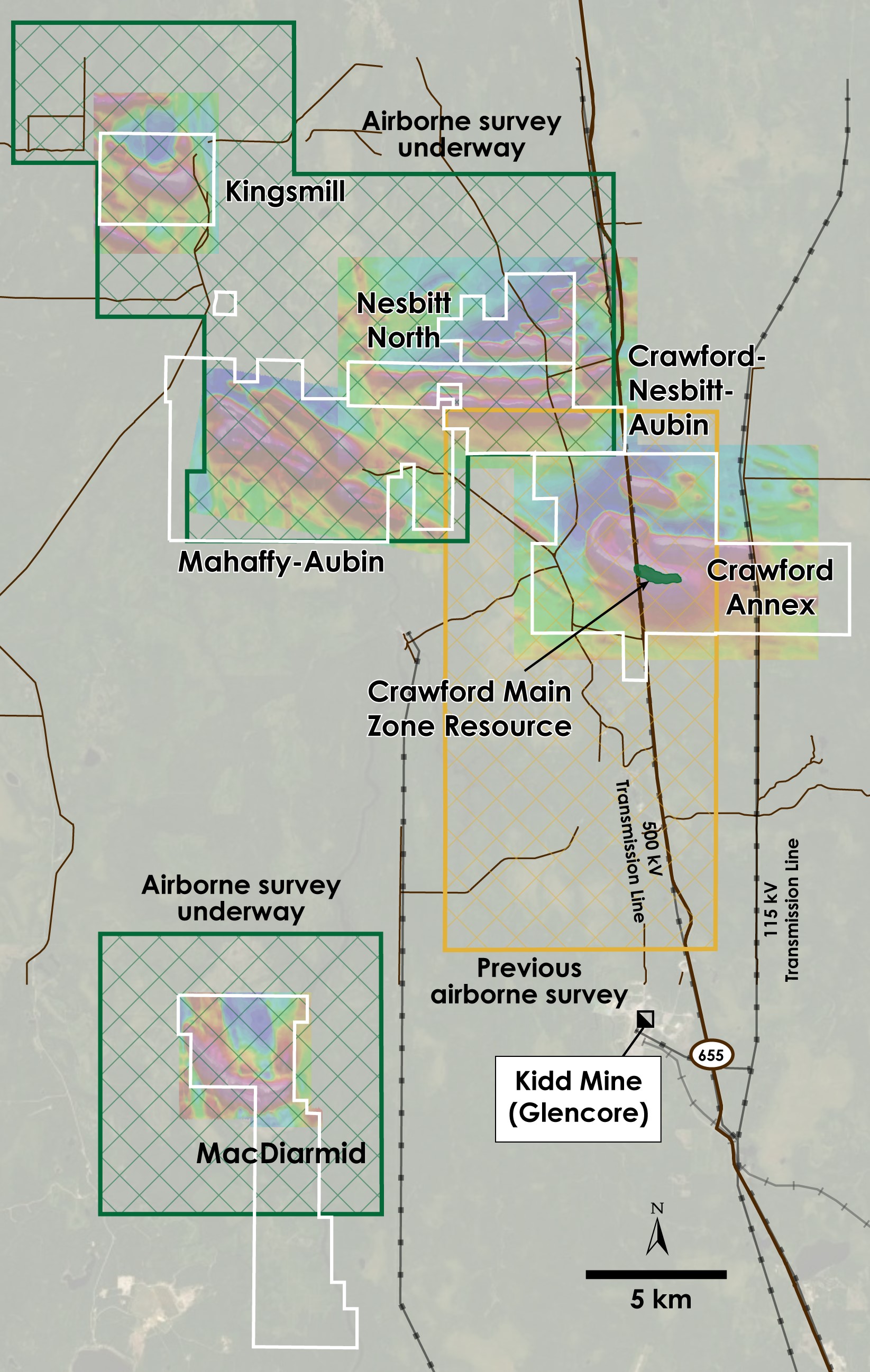

- Drilling has begun on other prospective geophysical targets on the several kilometres of the Crawford structure, including those which were previously untested on the west side of the highway. An airborne geophysical survey on regional option properties has been completed and interpretation work now underway will inform a regional drilling program expected to be completed this winter. See Figure 6.

Figure 6 – Planned and Previous Airborne Geophysical Survey Areas over Crawford, Kingsmill, Nesbitt-Aubin, Nesbit North, MacDiarmid and Mahaffy-Aubin Properties, Ontario.

Issuance of Shares

The Company also announced today that it will be issuing a total of 200,000 of its common shares to third parties in satisfaction of certain contractual obligations. The shares will be subject to a four-month hold period under applicable securities laws.

Conference Call Details

Canada Nickel is hosting a live Q&A conference call on October 22 at 10:00 a.m. Eastern time (7:00 a.m. Pacific time). Participants may join the call by dialing:

Local: Toronto: 416-764-8688

North American Toll Free: 888-390-0546

Webcast URL: https://produceredition.webcasts.com/starthere.jsp?ei=1389471&tp_key=79c1b4fb17

A playback version will be available for two weeks after the call at +1-416-764-8677 (local or international) or toll free at +1-888-390-0541 (passcode 442999#).

Assays, Quality Assurance/Quality Control and Drilling and Assay Procedures

William E. MacRae, MSc, P.Geo., a Qualified Person as defined by NI 43-101, is responsible for the on-going drilling and sampling program, including quality assurance (QA) and quality control (QC). The core is collected from the drill in sealed core trays and transported to the core logging facility. The core is marked and sampled at 1.5 metre lengths and cut with a diamond blade saw. Samples are bagged with QA/QC samples inserted in batches of 35 samples per lot. Samples are transported in secure bags directly from the Canada Nickel core shack to Actlabs Timmins, an ISO/IEC 17025 accredited lab. Analysis for precious metals (gold, platinum and palladium) are completed by Fire Assay while analysis for nickel, cobalt, sulphur and 17 other elements are performed using a peroxide fusion and ICP-OES analysis. Certified standards and blanks are inserted at a rate of one QA/QC sample per 32 core samples making a batch of 35 samples that are submitted for analysis.

Qualified Person and Data Verification

Dr. Scott Jobin-Bevans (P.Geo., APGO #0183), independent of the Company and a Qualified Person as defined by NI 43-101, has reviewed and approved the scientific and technical content of this news release. The independent Qualified Person for the Mineral Resource Estimate, as defined by NI 43-101, is Mr. Luis Oviedo (P.Geo., Chilean Mining Commission: RM, CMC #013), of Caracle Creek International Consulting Inc. and Atticus Chile S.A. The Quality Control-Quality Assurance review was conducted by independent engineer Mr. John Siriunas (P.Eng., APEO #42706010), a Qualified Person as defined by NI 43-101.

About Canada Nickel Company

Canada Nickel Company Inc. is advancing the next generation of nickel-cobalt sulphide projects to deliver nickel and cobalt required to feed the high growth electric vehicle and stainless steel markets. Canada Nickel Company has applied in multiple jurisdictions to trademark the terms NetZero NickelTM, NetZero CobaltTM, NetZero IronTM and is pursuing the development of processes to allow the production of net zero carbon nickel, cobalt, and iron products. Canada Nickel provides investors with leverage to nickel and cobalt in low political risk jurisdictions. Canada Nickel is currently anchored by its 100% owned flagship Crawford Nickel-Cobalt Sulphide Project in the heart of the prolific Timmins-Cochrane mining camp.

Cautionary Statement Concerning Forward-Looking Statements

This press release contains certain information that may constitute “forward-looking information” under applicable Canadian securities legislation. Forward looking information includes, but is not limited to, drill results relating to the Crawford Nickel-Cobalt Sulphide Project, the potential of the Crawford Nickel-Cobalt Sulphide Project, timing of economic studies and resource estimates, strategic plans, including future exploration and development results, and corporate and technical objectives. Forward-looking information is necessarily based upon a number of assumptions that, while considered reasonable, are subject to known and unknown risks, uncertainties, and other factors which may cause the actual results and future events to differ materially from those expressed or implied by such forward-looking information. Factors that could affect the outcome include, among others: future prices and the supply of metals, the future demand for metals, the results of drilling, inability to raise the money necessary to incur the expenditures required to retain and advance the property, environmental liabilities (known and unknown), general business, economic, competitive, political and social uncertainties, results of exploration programs, timing of the updated resource estimate, risks of the mining industry, delays in obtaining governmental approvals, and failure to obtain regulatory or shareholder approvals. There can be no assurance that such information will prove to be accurate, as actual results and future events could differ materially from those anticipated in such information. Accordingly, readers should not place undue reliance on forward-looking information. All forward-looking information contained in this press release is given as of the date hereof and is based upon the opinions and estimates of management and information available to management as at the date hereof. Canada Nickel disclaims any intention or obligation to update or revise any forward-looking information, whether as a result of new information, future events or otherwise, except as required by law.

For further information, please contact:

Mark Selby, Chair and CEO

Phone: 647-256-1954

Email: info@canadanickel.com