Monday, October 12, 2020

Digital, Media & Entertainment Industry Report

Quarterly Review: Has The Market Already Factored In The Elections?

Michael Kupinski, DOR, Senior Research Analyst, Noble Capital Markets, Inc.

Refer to end of report for Analyst Certification & Disclosures

Overview: The fog of the elections. Some companies have provided positive updated revenues/guidance, but the stocks have had little reaction. We ponder if investors are focused on the outcome of the upcoming elections and not on the positive, current fundamental developments.

Television: Ion provides a positive boost. The Television stocks slightly underperformed the general market in the latest quarter, although E.W. Scripps had a great quarter, up 30.7%. Scripps surprised the investment community by making a $2.65 billion acquisition of Ion Media, in the midst of a pandemic. The shake-up in the wake of that acquisition leaves us to take a closer look at Gray Television.

Radio: Positive updates provided little investor interest. The Noble Radio Index was the worse performing in the media sector, down 6.2% in the latest quarter. Notably, investors brushed off some positive, updated revenue numbers by Urban One and Townsquare Media. The Townsquare update, in particular, implies that it will solidly beat Q3 expectations. We highlight this sector as among our favored play for the upcoming quarter.

Publishing: Can the momentum continue? The Tribune shares outperformed the general market and most of its peers in the third quarter, up 16.7% versus 8.5% for the general market. We believe that the outperformance of the industry in the quarter, in general, and that of Tribune, in particular, has investors possibly rethinking their view of the industry.

Digital/Entertainment: Gaming is hot. Gaming and esports have garnered attention of Wall Street with an active number of deals. In this broad sector, we highlight the recent initiation of Travelzoo, a unique way to play the advertising recovery in the travel industry. In addition, we highlight the strong performance of 1800Flowers.com. The stock was up 144% in the quarter, benefiting from the surge in online retail. We recently raised our price target on the FLWS shares.

Overview

The Fog Of The Elections

Most media stock indices were in line to slightly outperforming the general market in the third quarter, save the Radio stocks, as the following figure illustrates. The overall media performance is disappointing given that media stocks tend to outperform the general market in the early stage of an economic recovery. The media indices are market cap weighted. What is notable regarding the media performance is that there was a disparity between larger cap and smaller cap companies. For instance, the average media stock was down in the quarter.

Off of a difficult (to say the least) second quarter, revenue trends are expected to sequentially improve in the third quarter, fueled by Political advertising and digital revenues. Investors have now realized, however, that the shape of the advertising recovery is not likely to be “V” shaped. Third quarter revenues, excluding Political, are expected to be down double-digits for many advertising driven mediums, in the range of 10% to 15% versus 30% to 40% experienced on average in the second quarter. For mediums that benefit from Political advertising, we believe that there likely will be some positive upside Q3 revenue and cash flow surprise potential. Political is coming in better than expected and some companies, discussed later in this report, gave updated third quarter and/or Political guidance. The question will be whether investors will brush off the potential revenue and cash flow upside surprise?

We believe that investors are heavily engaged in the outcome of the general elections and implications for the broader economy. Investors worry that a Biden win could imply that tax rates will go up, given his tax platform plans to rollback the Trump tax cuts. We are often asked, when should we lock in gains? Now? Or, after the election? That question is not of significant importance for most media investors. The only media sectors that investors may have gains over the course of the last year are Publishing and Digital Media stocks, up 13% and 19%, respectively. Television and Radio stocks are down 27% and 46% respectively.

In addition, with many state economies not fully opened, investors are likely concerned about the sustainability of the economic recovery, especially without visibility of a Covid vaccine. Given these concerns, investors may have already discounted the potential revenue and cash flow upside in the third and fourth quarters from Political advertising. We highlight the fact that Townsquare Media’s (view report) stock did not significantly react to the company’s updated third quarter revenue guidance on September 21, which provided positive upside in revenue and implied positive cash flow expectations. The TSQ shares increased a modest 5% since that announcement. As such, while we believe that fundamentals are improving, it appears likely that the media stocks may be range bound until the elections are over, or that there is a developed timetable for a Covid vaccine, which may allow some normalcy to reopening the US economy.

Tradition Media

Television

Ion Got Investors Positively Excited

The Television stocks slightly under-performed the general market in the last quarter, up 6.9% versus 8.5% for the market as measured by the S&P 500 Index. The best performing stocks in the index were ViacomCBS and E.W. Scripps, up 20.1% and 30.7% respectively. In the case of E.W. Scripps, the company announced a significant $2.65 billion acquisition of Ion Media, with the backing of Warren Buffet’s Berkshire Hathaway. Notably, the acquisition will bring Scripps to the current ownership cap of 39% of US TV households. This takes another potential buyer of local TV stations out of the market, leaving Gray Television as among the few large broadcasters with the ability to add stations. Gray Television currently covers 24% of the nation’s TV households, with a significant runway to get to 39%. The question will be whether another inning of consolidation is in the offing with the mid tier broadcast groups, like Meredith and Graham Holdings. But, there is no mistaking, the industry is in the final innings of consolidation, unless there is relaxation of ownership rules.

Such a prospect may come from the courts. Recently, the U.S. Supreme Court agreed to examine the media ownership rules that the FCC directed to relax, but was blocked by the 3rd Circuit Court of Appeals. The FCC would have ended or loosened ownership limits such as 1) the elimination of the newspaper/television cross ownership rule (which would allow a company to own a newspaper and television station in a single market), 2) the elimination of radio/television cross ownership, 3) the elimination of owning two of the top four stations in a market, and 4) allow a company to own two TV stations in a single market. The prospective appointment of another conservative on the bench, like Amy Coney Barrett, could significantly improve the chances that the FCC would win the appeal.

For most investors, these rules don’t matter much. The Television industry is not likely to buy a newspaper or radio in an existing market. In many cases, public market values for television groups are double that of a publishing or radio company. Investors would frown on potentially lowering the stock valuation on such an acquisition. In addition, the history of broadcasters successfully integrating and operating a newspaper in market or even radio stations under grandfathered rules have not been that good. TV broadcasters would more likely seek to own two of the Big Four Network affiliates in market. This is where a broadcaster would get the biggest bang for the buck and investors would cheer. Those opportunities will be few and far between given the recent consolidation. Consequently, we view the prospective rule ownership changes as ho hum from a TV perspective. It would be far more beneficial to the TV stocks to see the ownership cap lifted from the current 39%. There does not seem to be any political will or leadership to push for that change.

Consequently, we believe that management’s will turn their attention to seek opportunities for internal growth. Recently, a number of broadcasters have launched expanded news programming. We believe that it is likely that broadcasters will invest in original programming to take advantage of their increased scale. News programming tends to be the lowest hanging fruit for a broadcaster. But, development of original programming is only modest incremental steps toward enhanced cash flow growth. In our view, broadcasters will need to seek ways to take advantage of their spectrum and find innovative revenue opportunities, possibly through the implementation of the new broadcast standard, ATSC 3.0.

As we look toward the third quarter reports and fourth quarter guidance, investors will look toward the revenue recovery for some direction. There were some early indications that it will be a strong Q3 revenue quarter, fueled by Political advertising. E.W. Scripps (view report) raised its Political advertising guidance from $200 million to over $230 million. That guide was impressive given that it was based solely on the strength of Political advertising in the third quarter. The company may once again increase its guidance, if, as we expect, the Political advertising momentum continues into the fourth quarter. Political advertising carries very high margins. As such, it is likely that there will be positive upside surprises in the quarterly results.

Given that the vast majority of the Television stocks have not performed well in the latest quarter, we believe that there should be better performance in the fourth quarter. In our view, the market has not baked in the improving revenue trends and the upside surprise potential from Political. In addition, the stocks should perform better as the fate of the upcoming elections is known. We remain constructive on the television sector, with our favorites currently Gray Television (view report) and Entravision (view report).

Radio

Did Investors Overlook The Favorable News?

Radio stocks under performed the general market in the third quarter, down 6.2% versus an 8.4% gain for the market as measured by the S&P 500 Index. The Noble Radio index is market weighted, and, as such, the performance was skewed by the larger cap stocks in the index. The average stock was down greater than 6% and closer to 10%, with the worse performing stocks in the latest quarter Beasley Broadcast Group (BBGI), Salem Media (SALM) (view report) and Saga Communications (SGA), down 49%, 19% and 22%, respectively. The shares of Cumulus Media (CMLS) outperformed the group, up 35.9% in the quarter, with Entercom (ETM) coming in second, up 16.7% and Townsquare Media (TSQ) up 4.3%. The outperformance of the Cumulus Media shares in the second quarter was off of a very low base established at the end of the first quarter, when the shares dropped from a high of over $16 to near $4.

The under performance of the Radio stocks is in spite of the expected sequential improvement in third quarter revenues from the second quarter, when some radio broadcasters reported revenues down as much as 60%. Recently, Urban One announced in an 8K filing that its radio revenues declined 40% in July and 38% in August, with September down a more modest 11%. Combined with the company’s other businesses outside of radio, Urban One’s third quarter total company revenue is expected to be down in the high teens percent. Townsquare Media appears to be doing better than most in the industry. It updated its investor presentation on September 21st and indicated that its July and August total company revenues declined 21% in July and 16% in August. We expect that. much like Urban One, there will be a significant improvement in revenues for September. In addition to a higher than expected amount of Political advertising, Townsquare appeared to be benefit from strength in its Digital businesses. The company indicated that its Townsquare Interactive business increased revenues in July and August by 13% and 15%, respectively. We believe that investors have not fully baked in the significance of this revenue improvement. In addition, given the high margin revenue, we believe that there are positive upside cash flow surprise potential.

Radio is among the most out of favored stocks in the traditional media landscape. The recent under performance of the sector is likely a combination of the industry’s relatively high debt leverage and an extraordinary impact from Covid mitigation efforts. Given that the stocks are down an average of 52.4% year to date, the Radio stocks have been the poster industry for among the worse performing of many industries adversely affected by Pandemic. Are investors paying attention to the improving revenue trends? Surprisingly, the shares of Townsquare Media increased a modest 5% following the company’s announcement that implied it will exceed third quarter revenue and cash flow expectations. In our view, there likely will be further positive developments into the fourth quarter as well. So, in our view, the answer is no.

Given the relative under performance thus far, Radio stocks lead as among our favorites for the upcoming quarter. We believe that the stocks do not reflect the prospect for positive revenue and cash flow upside surprise potential, nor the prospect that expectations may be raised for the fourth quarter. Our current favorites include Townsquare Media, Cumulus Media and Salem Media, in that order.

Publishing

The Dinosaurs Just Beat The Market!

The Publishing stocks had a relatively good quarter, up 9.1%, slightly outperforming the general market as measured by the S&P 500 Index. The three largest cap stocks in the index News Corp., New York Times and Tribune Publishing accounted for the gains, with News Corp. and Tribune accounting for the majority of the third quarter out performance, up 18.2% and 16.7%, respectively. Notably, all three companies have significant digital businesses, which have weathered well in the Pandemic given increased digital subscriptions, visitors and engagement.

Focusing on Tribune, we believe that in spite of the recent rise, the shares are significantly undervalued. Trading at roughly 4.5 times Enterprise Value to our estimated cash flow, we believe that the shares do not reflect the underlying value of its assets, particularly its e-commerce business, BestReviews, nor reflect the positive upside cash flow potential. In spite of recent upward revisions to our estimates, we believe that earlier cost cutting actions at the company are not fully realized. Our third quarter estimate was revised upward, but was at the lower end of the company’s guidance. In addition, we believe that we were conservative in our fourth quarter estimates.

Given the improved fundamentals, the company is building its cash hoard, estimated to be over $90 million. Given the prospect that the company may sell BestReviews and given its pristine balance sheet, with virtually no debt, the company’s board may reinstate its $0.25 per share quarterly dividend. The dividend was suspended in the second quarter due to concerns over Covid.

The shares of Tribune (view report) are among our favorite economic recovery plays. Nearly one third of the company’s market cap is reflected in its cash position. Another third of the company’s market cap is reflected in the value of its 60% owned BestReviews business. This leaves only one third of the value of the company reflected in the cash flow generating publishing and digital businesses. Notably, should the company reinstate its dividend, near current levels, the shares would offer an annualized dividend yield of over 7%. We continue to view the TPCO shares as among our favorites.

Digital/Entertainment

Gaming Sector Receives A Pandemic Tailwind

Video games has been one of the few sectors of the economy to benefit from Covid-19. Covid-19 lockdowns have boosted user engagement with video games and esports as consumers shelter in place. The pandemic is accelerating existing trends in the gaming industry. In April, the first full month of sheltering in place resulted in a 50% sequential increase in gaming hours watched on Twitch, the most popular video game streaming platform. Viewer engagement numbers for 2Q 2020 (which are not out yet) are expected to reach all-time highs. According to market research firm NPD Group, 244 million people in the U.S., or three out of every four, play video games, an increase of 32 million people in the last two years alone.

As millions have been quarantined at home, many have looked to esports for entertainment. Deloitte’s 2020 digital media trends survey found that, during the crisis, a third of consumers have, for the first time, subscribed to a video gaming service, used a cloud gaming service, or watched esports or a virtual sporting event. According to Nielsen, while most consumers prefer to play games rather than watch others play, one-third of esports fans say they watched esports as an alternative to traditional TV content.

Like many ecommerce or online businesses, the pandemic has pulled forward and accelerated many trends that were already underway. It will be interesting to see whether these gains can be maintained as people slowly return to work.

Gaming Sector M&A Heats Up

The significant increase in time spent streaming games has helped to drive M&A activity in the gaming space to new levels. Noble tracked 14 gaming transactions in the third quarter with a transaction value of $11.7 billion. Two transactions alone account for $11.2 billion of this total: Microsoft’s $7.5 billion acquisition of gaming studio/game developer ZeniMax Media, and the $3.5 billion reverse merger between esports platform Skillz and the SPAC Flying Eagle Acquisition Corp. Historically Noble tracks M&A transactions in the internet and digital media sectors and focuses on transactions in North America and Europe. The chart below shows the largest gaming/esports transactions in 3Q 2020 in those respective regions. We should note that the largest number of M&A deals in the sector in 3Q took place in Asia, which is home to the largest gaming audiences.

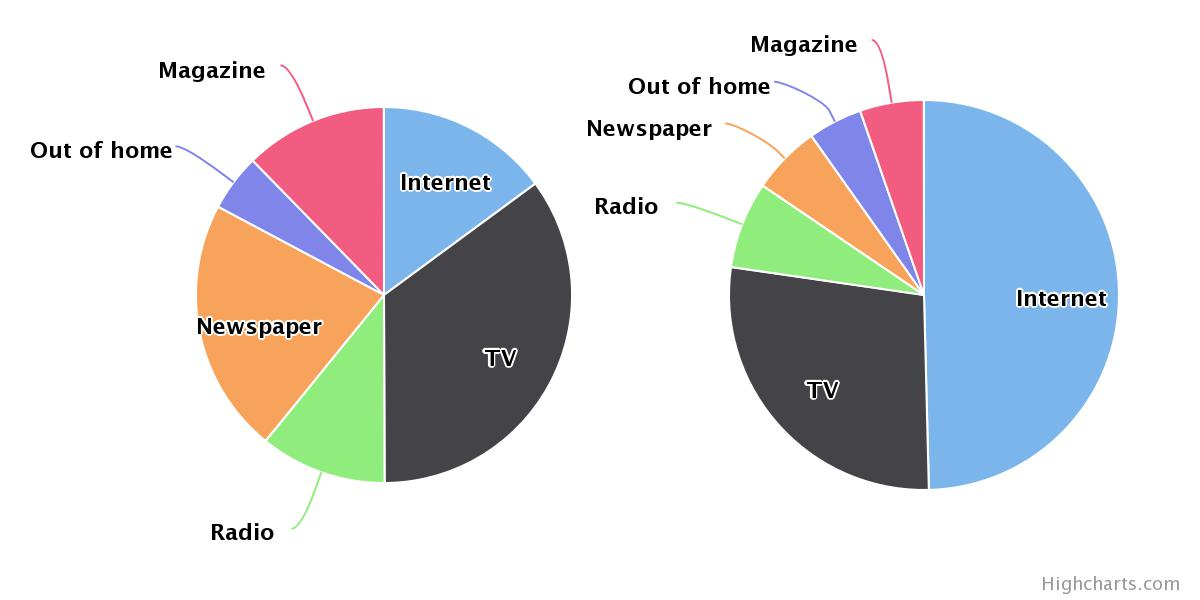

Internet & Digital Media M&A Sees Sequential Improvement in 3Q 2020

During the third quarter, Noble tracked 105 M&A transactions in the internet and digital media sector. This represents a 5% sequential improvement over the 100 M&A transactions we tracked in 2Q 2020. Third quarter deal values totaled $28.1 billion, a 118% increase over 2Q 2020 levels, as four deals alone accounted for nearly $25 billion worth of deal value. The largest deal was Adevinta’s acquisition of eBay Classified Group for $9.2 billion, followed by the gaming deals mentioned earlier (Microsoft’s $7.5 billion acquisition of gaming studio/game developer ZeniMax Media, and Skillz’ $3.5 billion reverse merger with Flying Eagle Acquisition Corp). Blackstone’s $4.7 billion acquisition of information/genealogy company Ancestry.com was the fourth deal of more than $1 billion that we tracked.

Of the 105 deals we tracked in 3Q 2020, 37 of them were in the digital content category, while the marketing technology sector trailed with 26 deals, followed by the always active advertising agency deals with 23. These three sectors were also the most active sectors in the first and second quarters of 2020.

The digital content sector had not just the largest number of transactions, but also the largest value of deals in the third quarter, with $22.2 billion of deals, or 79% of the entire deal value of the internet and digital media deals we track. Within the digital content segment, the gaming sector accounted for 14 of the 37 transactions and totaled $11.7 billion in deal value or nearly 53% of total digital content deal value.

Other segments of digital content where M&A was strong includes video focused transactions (6 transactions), publishing (4 transactions) and audio (5 transactions, 4 of which were in the podcast space). Notable video focused deals include CuriosityStream’s $512 million reverse merger with the SPAC Software Acquisition Group, and Enthusiast Gaming’s $34 million acquisition of Omnia Media, a YouTube Video Gaming Network. Notable digital publishing deals include Red Venture’s $500 million acquisition of CNET Media Group from ViacomCBS. Notable audio deals include SiriusXM’s $325 million acquisition of podcast network Stitcher from E.W. Scripps; The New York Times’ $25 million acquisition of podcast programmer Serial; and the $70 million acquisition of Rhapsody International from MelodyVR Group.

Internet and Digital Media Stocks Continued To Rebound

In our 2Q media newsletter we noted that every single stock in the four sectors we monitor was up in the quarter. While 3Q 2020’s performance was not nearly as strong, all sectors performed well, and three of the four sectors outperformed the S&P 500. In the third quarter the S&P 500 index increased by 8.5%, while Noble’s Adtech Index increased by 26%, Noble’s MarTech Index increased by 19%, Noble’s Social Media Index increased by 16%, and Noble’s Digital Media Index increased by 4%.

While last quarter saw 5 stocks more than double off their March lows, only one company, Autoweb (AUTO, +143%), posted a more than doubling of their stock price. The stock surged when the company provided a 3Q mid-quarter update that showed that gross margins in July 2020 had nearly doubled from July 2019 levels resulting in positive adjusted EBITDA (versus a loss a year-ago), and provided further evidence of the company’s turnaround.

Autoweb wasn’t the only adtech stock to perform well during the quarter. E-commerce retailing was hot, driven by stay at home mandates and social distancing. 1800Flowers.com’s (view report) stock increased 144% from March lows in the latest quarter. The company reported that its fiscal fourth quarter end June 30 revenues increased a strong 61%. We believe that e-commerce trends will remain strong even as the pandemic subsides. Other notable performers included the stocks of Quinstreet (QNST,+51%) and Fluent (FLNT, +39%). It’s interesting to note that all three of the best performing advertising technology companies are lead generation businesses. As companies re-open their businesses post-pandemic, it’s expected that performance marketing companies will do well as companies focus less on branding and more on generating new business, an imperative for many businesses that have struggled during the pandemic. Several other adtech stocks performed well during the quarter including the stocks of Synacor (SYNC, +34%), Perion Networks (PERI, +34%), The Trade Desk (TTD, +28%) and Interclick Interactive (ICLK, +25%).

Marketing tech stocks that performed well during the quarter include Salesforce (CRM, +34%), Hubspot (HUBS, +30%), Brightcove (BCOV, +30%), SharpSpring (SHSP, +27%), and LivePerson (LPSN, +26%). As noted in our M&A study, MarTech was one of the most active sectors in M&A during 3Q 2020, but M&A was not a driver of stock price performance. Strong organic revenue appears to be the sector driver, with revenue growth exceeding 20% on average.

Social media stocks also performed well during the quarter, with our index up 16%. Our index is market cap weighted so it generally performs in-line with how Facebook has performed. Nevertheless, several social media stocks significantly outperformed, including Twitter (TWTR, +49%) and Spark Networks (LOV, +48%). While the stock of Snap Interactive (SNAP, +11%) underperformed its peers during the quarter, it consolidated its gains for the year (+60%) and is the strongest performing social media stock in 2020.

Digital media stocks were the only stock sector to underperform the S&P 500, as shares of Google (GOOG.L) were up only 3%, and Google represents 73% of the market cap of this market-cap weighted sector. Google posted its first year-over-year quarterly revenue decline in the company’s history and like Apple, Amazon and Facebook, is under intense regulatory scrutiny as the Justice Department reviews potential anti-competitive behavior among big tech companies. Despite Google weighing on the sector, several digital media stocks performed well including The Leaf Group (LEAF, +37%), The Maven (MVEN, +37%), Travelzoo (TZOO, +14%) and Netflix (NFLX, +10%). We encourage investors to focus on the advertising recovery in the travel industry and the unique way to play the space with Travelzoo (view report), among our favorites.

GENERAL DISCLAIMERS

All statements or opinions contained herein that include the words “we”, “us”, or “our” are solely the responsibility of Noble Capital Markets, Inc.(“Noble”) and do not necessarily reflect statements or opinions expressed by any person or party affiliated with the company mentioned in this report. Any opinions expressed herein are subject to change without notice. All information provided herein is based on public and non-public information believed to be accurate and reliable, but is not necessarily complete and cannot be guaranteed. No judgment is hereby expressed or should be implied as to the suitability of any security described herein for any specific investor or any specific investment portfolio. The decision to undertake any investment regarding the security mentioned herein should be made by each reader of this publication based on its own appraisal of the implications and risks of such decision.

This publication is intended for information purposes only and shall not constitute an offer to buy/sell or the solicitation of an offer to buy/sell any security mentioned in this report, nor shall there be any sale of the security herein in any state or domicile in which said offer, solicitation or sale would be unlawful prior to registration or qualification under the securities laws of any such state or domicile. This publication and all information, comments, statements or opinions contained or expressed herein are applicable only as of the date of this publication and subject to change without prior notice. Past performance is not indicative of future results. Noble accepts no liability for loss arising from the use of the material in this report, except that this exclusion of liability does not apply to the extent that such liability arises under specific statutes or regulations applicable to Noble. This report is not to be relied upon as a substitute for the exercising of independent judgement. Noble may have published, and may in the future publish, other research reports that are inconsistent with, and reach different conclusions from, the information provided in this report. Noble is under no obligation to bring to the attention of any recipient of this report, any past or future reports. Investors should only consider this report as single factor in making an investment decision.

IMPORTANT DISCLOSURES

This publication is confidential for the information of the addressee only and may not be reproduced in whole or in part, copies circulated, or discussed to another party, without the written consent of Noble Capital Markets, Inc. (“Noble”). Noble seeks to update its research as appropriate, but may be unable to do so based upon various regulatory constraints. Research reports are not published at regular intervals; publication times and dates are based upon the analyst’s judgement. Noble professionals including traders, salespeople and investment bankers may provide written or oral market commentary, or discuss trading strategies to Noble clients and the Noble proprietary trading desk that reflect opinions that are contrary to the opinions expressed in this research report.

The majority of companies that Noble follows are emerging growth companies. Securities in these companies involve a higher degree of risk and more volatility than the securities of more established companies. The securities discussed in Noble research reports may not be suitable for some investors and as such, investors must take extra care and make their own determination of the appropriateness of an investment based upon risk tolerance, investment objectives and financial status.

Company Specific Disclosures

The following disclosures relate to relationships between Noble and the company (the “Company”) covered by the Noble Research Division and referred to in this research report.

Noble is not a market maker in any of the companies mentioned in this report. Noble intends to seek compensation for investment banking services and non-investment banking services (securities and non-securities related) with any or all of the companies mentioned in this report within the next 3 months

ANALYST CREDENTIALS, PROFESSIONAL DESIGNATIONS, AND EXPERIENCE

Senior Equity Analyst focusing on Basic Materials & Mining. 20 years of experience in equity research. BA in Business Administration from Westminster College. MBA with a Finance concentration from the University of Missouri. MA in International Affairs from Washington University in St. Louis.

Named WSJ ‘Best on the Street’ Analyst and Forbes/StarMine’s “Best Brokerage Analyst.”

FINRA licenses 7, 24, 63, 87

WARNING

This report is intended to provide general securities advice, and does not purport to make any recommendation that any securities transaction is appropriate for any recipient particular investment objectives, financial situation or particular needs. Prior to making any investment decision, recipients should assess, or seek advice from their advisors, on whether any relevant part of this report is appropriate to their individual circumstances. If a recipient was referred to Noble Capital Markets, Inc. by an investment advisor, that advisor may receive a benefit in respect of

transactions effected on the recipients behalf, details of which will be available on request in regard to a transaction that involves a personalized securities recommendation. Additional risks associated with the security mentioned in this report that might impede achievement of the target can be found in its initial report issued by Noble Capital Markets, Inc.. This report may not be reproduced, distributed or published for any purpose unless authorized by Noble Capital Markets, Inc..

RESEARCH ANALYST CERTIFICATION

Independence Of View

All views expressed in this report accurately reflect my personal views about the subject securities or issuers.

Receipt of Compensation

No part of my compensation was, is, or will be directly or indirectly related to any specific recommendations or views expressed in the public

appearance and/or research report.

Ownership and Material Conflicts of Interest

Neither I nor anybody in my household has a financial interest in the securities of the subject company or any other company mentioned in this report.

| NOBLE RATINGS DEFINITIONS |

% OF SECURITIES COVERED |

% IB CLIENTS |

| Outperform: potential return is >15% above the current price |

88% |

41% |

| Market Perform: potential return is -15% to 15% of the current price |

12% |

5% |

| Underperform: potential return is >15% below the current price |

0% |

0% |

NOTE: On August 20, 2018, Noble Capital Markets, Inc. changed the terminology of its ratings (as shown above) from “Buy” to “Outperform”, from “Hold” to “Market Perform” and from “Sell” to “Underperform.” The percentage relationships, as compared to current price (definitions), have remained the same. Additional information is available upon request. Any recipient of this report that wishes further information regarding the subject company or the disclosure information mentioned herein, should contact Noble Capital Markets, Inc. by mail or phone.

Noble Capital Markets, Inc.

225 NE Mizner Blvd. Suite 150

Boca Raton, FL 33432

561-994-1191

Noble Capital Markets, Inc. is a FINRA (Financial Industry Regulatory Authority) registered broker/dealer.

Noble Capital Markets, Inc. is an MSRB (Municipal Securities Rulemaking Board) registered broker/dealer.

Member – SIPC (Securities Investor Protection Corporation)

Report ID: 11744

Each event in our popular Virtual Road Shows Series has maximum capacity of 100 investors online. To take part, listen to and perhaps get your questions answered, see which virtual investor meeting intrigues you

Each event in our popular Virtual Road Shows Series has maximum capacity of 100 investors online. To take part, listen to and perhaps get your questions answered, see which virtual investor meeting intrigues you