Townsquare Media (TSQ) Corporate Presentation from NobleCon18Research, News and Market Data on Townsquare MediaNobleCon 18 Complete Rebroadcast

|

Category: Media and Marketing

Beasley Broadcast Group (BBGI) – A Path Toward Enhanced Revenue and Cash Flow Growth

Thursday, April 28, 2022

Beasley Broadcast Group (BBGI)

A Path Toward Enhanced Revenue and Cash Flow Growth

Beasley Broadcast Group Inc is a radio broadcasting company, engaged in operating radio stations throughout the United States. It operates radio stations including FM and AM radio stations located in large and mid-sized markets in the United States. The company owns and operates radio stations in the following radio markets: Atlanta, GA, Augusta, GA, Boston, MA, Charlotte, NC, Detroit, MI, Fayetteville, NC, Fort Myers-Naples, FL, Las Vegas, NV, Middlesex, NJ, Monmouth, NJ, Morristown, NJ, Philadelphia, PA, Tampa-Saint Petersburg, FL, West Palm Beach-Boca Raton, FL, and Wilmington, DE. It is also a multi-platform, marketing solutions provider that offers on-air, online, and mobile and social media applications. The main source of revenue is the sale of advertising.

Michael Kupinski, Director of Research, Noble Capital Markets, Inc.

Patrick McCann, Research Associate, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

NobleCon18 highlights. Marie Tedesco, CFO, described the company’s roadmap towards an acceleration in revenue growth and higher profitability. The company plans to develop a Digital Agency business in its medium to large markets. To watch a full replay of the presentation, please click here.

Local Radio drives growth. Beasley’s 3 key markets, Boston, Philadelphia, and Detroit, represent over 50% of the company’s total revenues. Notably, its stations clusters have a more than 30% market share in each market. Retail and entertainment ad categories are recovering beyond pre-pandemic levels, offsetting the headwinds in auto. Additionally, a boost could come from sports betting, should …

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

SPACtrac Report – Forbes Global Media: A Compelling Growth Story

Thursday, April 28, 2021

Forbes Global Media: A Compelling Growth Story

Michael Kupinski, Director of Research, Noble Capital Markets, Inc.

Refer to end of report for Analyst Certification & Disclosures

Noblecon 18 highlights. Forbes CEO, Mike Federle, and CFO, Mike York, presented at Noblecon18, speaking on several topics, such as Forbes recent strong results and outlook for 2022, the impacts of Forbes’ brand elasticity on its growth prospects, how the company plans to leverage its in-house technology stack, a strategic investment from Binance, and when the SPAC merger is likely to close. The full video of the presentation can be found here.

2022 pacing well. Management stated that 2022 is off to a good start and expects a strong year of growth. Our full year 2022 revenue estimate is $290 million, which assumes 12% growth over 2021.

Technological advantages. During the presentation Forbes management stressed the importance of modern media companies having a strong technological foundation. Forbes has such a foundation with its analytics platform, ForbesOne, which gathers over 600 data points per user. This data allows the company to identify audience cohorts to improve content offerings as well as increase the value proposition for advertising partners.

SPAC merger update. The SPAC is expected to close by May 31. Upon the completion of the merger, shares of the SPAC (OPA) will convert to common stock of Forbes Global Media (FRBS).

Attractive valuation. Near current levels, the OPA shares trade at 9.4 times enterprise value to expected 2022 EBITDA and 7.5 times EV to expected 2023 EBITDA. Our price target of $16 represents a 60% premium to near current levels and a target EV/2022 EBITDA multiple of 16.5 times.

GENERAL DISCLAIMERS

All statements or opinions contained herein that include the words “we”, “us”, or “our” are solely the responsibility of Noble Capital Markets, Inc.(“Noble”) and do not necessarily reflect statements or opinions expressed by any person or party affiliated with the company mentioned in this report. Any opinions expressed herein are subject to change without notice. All information provided herein is based on public and non-public information believed to be accurate and reliable, but is not necessarily complete and cannot be guaranteed. No judgment is hereby expressed or should be implied as to the suitability of any security described herein for any specific investor or any specific investment portfolio. The decision to undertake any investment regarding the security mentioned herein should be made by each reader of this publication based on its own appraisal of the implications and risks of such decision.

This publication is intended for information purposes only and shall not constitute an offer to buy/sell or the solicitation of an offer to buy/sell any security mentioned in this report, nor shall there be any sale of the security herein in any state or domicile in which said offer, solicitation or sale would be unlawful prior to registration or qualification under the securities laws of any such state or domicile. This publication and all information, comments, statements or opinions contained or expressed herein are applicable only as of the date of this publication and subject to change without prior notice. Past performance is not indicative of future results.

Noble accepts no liability for loss arising from the use of the material in this report, except that this exclusion of liability does not apply to the extent that such liability arises under specific statutes or regulations applicable to Noble. This report is not to be relied upon as a substitute for the exercising of independent judgement. Noble may have published, and may in the future publish, other research reports that are inconsistent with, and reach different conclusions from, the information provided in this report. Noble is under no obligation to bring to the attention of any recipient of this report, any past or future reports. Investors should only consider this report as single factor in making an investment decision.

IMPORTANT DISCLOSURES

This publication is confidential for the information of the addressee only and may not be reproduced in whole or in part, copies circulated, or discussed to another party, without the written consent of Noble Capital Markets, Inc. (“Noble”). Noble seeks to update its research as appropriate, but may be unable to do so based upon various regulatory constraints. Research reports are not published at regular intervals; publication times and dates are based upon the analyst’s judgement. Noble professionals including traders, salespeople and investment bankers may provide written or oral market commentary, or discuss trading strategies to Noble clients and the Noble proprietary trading desk that reflect opinions that are contrary to the opinions expressed in this research report.

The majority of companies that Noble follows are emerging growth companies. Securities in these companies involve a higher degree of risk and more volatility than the securities of more established companies. The securities discussed in Noble research reports may not be suitable for some investors and as such, investors must take extra care and make their own determination of the appropriateness of an investment based upon risk tolerance, investment objectives and financial status.

Company Specific Disclosures

The following disclosures relate to relationships between Noble and the company (the “Company”) covered by the Noble Research Division and referred to in this research report.

Company Specific Disclosures

The following disclosures relate to relationships between Noble and the company (the “Company”) covered by the Noble Research Division and referred to in this research report.

The SPAC Company in this report is a participant in the Company Sponsored Research Program (CSRP); Noble receives compensation from the Company for such participation. No part of the CSRP compensation was, is, or will be directly or indirectly related to any specific recommendations or views expressed by the analyst in this research report.

Noble is not a market maker in any of the companies mentioned in this report. Noble intends to seek compensation for investment banking services and non-investment banking services (securities and non-securities related) with any or all of the companies mentioned in this report within the next 3 months

ANALYST CREDENTIALS, PROFESSIONAL DESIGNATIONS, AND EXPERIENCE

Director of Research. Senior Equity Analyst specializing in Media & Entertainment. 34 years of experience as an analyst. Member of the National Cable Television Society Foundation and the National Association of Broadcasters. BS in Management Science, Computer Science Certificate and MBA specializing in Finance from St. Louis University.

Named WSJ ‘Best on the Street’ Analyst six times.

FINRA licenses 7, 24, 66, 86, 87

WARNING

This report is intended to provide general securities advice, and does not purport to make any recommendation that any securities transaction is appropriate for any recipient particular investment objectives, financial situation or particular needs. Prior to making any investment decision, recipients should assess, or seek advice from their advisors, on whether any relevant part of this report is appropriate to their individual circumstances. If a recipient was referred to Noble Capital Markets, Inc. by an investment advisor, that advisor may receive a benefit in respect of transactions effected on the recipients behalf, details of which will be available on request in regard to a transaction that involves a personalized securities recommendation. Additional risks associated with the security mentioned in this report that might impede achievement of the target can be found in its initial report issued by Noble Capital Markets, Inc.. This report may not be reproduced, distributed or published for any purpose unless authorized by Noble Capital Markets, Inc.

RESEARCH ANALYST CERTIFICATION

Independence Of View

All views expressed in this report accurately reflect my personal views about the subject securities or issuers.

Receipt of Compensation

No part of my compensation was, is, or will be directly or indirectly related to any specific recommendations or views expressed in the public

appearance and/or research report.

Ownership and Material Conflicts of Interest

Neither I nor anybody in my household has a financial interest in the securities of the subject company or any other company mentioned in this report.

| NOBLE RATINGS DEFINITIONS | % OF SECURITIES COVERED | % IB CLIENTS |

| Outperform: potential return is >15% above the current price | 99% | 28% |

| Market Perform: potential return is -15% to 15% of the current price | 6% | 3% |

| Underperform: potential return is >15% below the current price | 0% | 0% |

NOTE: On August 20, 2018, Noble Capital Markets, Inc. changed the terminology of its ratings (as shown above) from “Buy” to “Outperform”, from “Hold” to “Market Perform” and from “Sell” to “Underperform.” The percentage relationships, as compared to current price (definitions), have remained the same.

Additional information is available upon request. Any recipient of this report that wishes further information regarding the subject company or the disclosure information mentioned herein, should contact Noble Capital Markets, Inc. by mail or phone.

Noble Capital Markets, Inc.

150 East Palmetto Park Rd., Suite 110

Boca Raton, FL 33432

561-994-1191

Noble Capital Markets, Inc. is a FINRA (Financial Industry Regulatory Authority) registered broker/dealer.

Noble Capital Markets, Inc. is an MSRB (Municipal Securities Rulemaking Board) registered broker/dealer.

Member – SIPC (Securities Investor Protection Corporation)

Report ID: 24770

Release – Entravision Schedules First Quarter 2022 Earnings Release and Conference Call

![]()

Entravision Schedules First Quarter 2022 Earnings Release and Conference Call

Research, News, and Market Data on Entravision

SANTA MONICA, Calif.–(BUSINESS WIRE)– Entravision (NYSE: EVC), a leading global advertising solutions, media and technology company, announced that it will release its first quarter 2022 financial results after market close on Thursday, May 5, 2022. The Company will host a conference call that day at 5:00 p.m. Eastern Time to discuss the first quarter 2022 results.

To access the conference call, please dial (877) 407-9716 (U.S.) or (201) 493-6779 (International) ten minutes prior to the start time. The call will also be available via live webcast on the investor relations portion of the Company’s website located at www.entravision.com.

If you cannot listen to the conference call at its scheduled time, there will be a replay available through Thursday, May 19, 2022 which can be accessed by dialing (844) 512-2921 (U.S.) or (412) 317-6671 (International) and entering the passcode 13728063. The webcast will also be archived on the Company’s website.

About Entravision

Entravision is a leading global advertising, media and ad-tech solutions company connecting brands to consumers by representing top platforms and publishers. Our dynamic portfolio includes digital, television and audio offerings. Digital, our largest revenue segment, is comprised of four business units: our digital sales representation business; Smadex, our programmatic ad purchasing platform; our branding and mobile performance solutions business; and our digital audio business. Through our digital sales representation business, we connect global media companies such as Meta, Twitter, TikTok and Spotify with advertisers in primarily emerging growth markets worldwide. Smadex is our mobile-first demand side platform, enabling advertisers to execute performance campaigns using machine learning. We also offer a branding and mobile performance solutions business, which provides managed services to advertisers looking to connect with global consumers, primarily on mobile devices, and our digital audio business provides digital audio advertising solutions for advertisers in the Americas. In addition to digital, Entravision has 49 television stations and is the largest affiliate group of the Univision and UniMás television networks. Entravision also manages 46 primarily Spanish-language radio stations that feature nationally recognized, Emmy award-winning talent. Shares of Entravision Class A Common Stock trade on the NYSE under ticker: EVC. Learn more about our offerings at entravision.com or connect with us on LinkedIn and Facebook.

Christopher T. Young

Chief Financial Officer

Entravision

310-447-3870

Kimberly Esterkin

Addo Investor Relations

310-829-5400

evc@addo.com

Source: Entravision

Trump Media De-Spac in Face of Musk Twitter Purchase

Image Credit: Diverse Stock Photos (Flickr)

The DWAC SPAC Acquiring Trump Media Keeps Investors on Edge

When a SPAC, such as Digital World Acquisition Corp. (DWAC), soon to become Trump Media & Technology Group (TMTG), enters the DeSPAC phase, the terms are set, but the world keeps turning. For this reason, investors and potential investors need to continue to monitor events impacting the industry and the company to be acquired. There have been many surprises since October for DWAC shareholders, the past three days have been particularly challenging for investors to unravel.

Background

Since Trump Media agreed to be acquired on October 20, 2021, much has happened that could impact the company and the industry. These include an SEC probe of the deal, post-pandemic changes in users’ lifestyles, a frigid national relationship developing with Russia, and Twitter agreeing to be taken private by a “free speech” purchaser. Even when a SPAC’s formal ownership change hasn’t yet taken place, understanding the stock’s outlook (and future versions of the company) is as important as any other public company, perhaps a little more complex.

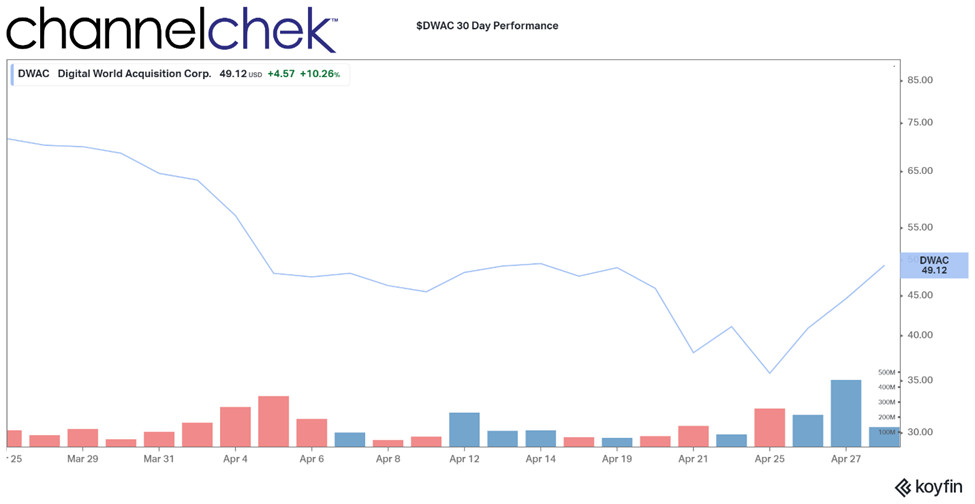

Source: Koyfin

The Trump Media example is star-studded and has faced renewed uncertainty within the past two weeks. When Elon Musk succeeded in striking a deal to take Twitter private for the purpose of providing a “platform for free speech around the globe,” this instantly created competition for the media start-up being acquired by the Digital Media SPAC. And it has caused gyrations in the price for the pre-merger stage for DWAC, which hit a 30-day low of $33.25 the day of the announcement (April 25) and then bounced significantly up to $47.36 as the future owner of the well-established Twitter demonstrated through various Tweets, that the companies are not really competitors, but instead exist for similar purposes.

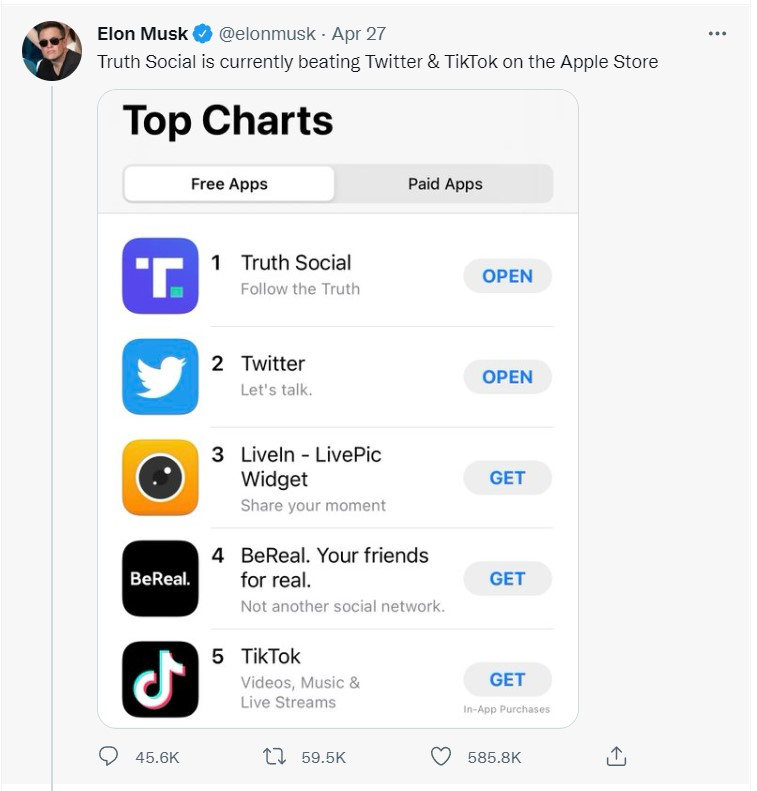

On April 27 Elon Musk gave DWACs share price a boost when he Tweeted “Truth Social is currently beating Twitter & TikTok on the Apple Store.” While Musk envisions Twitter as providing a platform for free speech around the globe, the smaller start-up social platform claims to be, “a free-speech haven without viewpoint discrimination or oppressive censorship.” If Musk is true to his stated purpose, the two may actually complement each other.

Take-Away

Investing in a SPAC with the trust that the acquisition company can steer the capital into a purchase you may not otherwise have been fortunate enough to participate in, is one reason for investors to allocate assets to SPACs. When the target has been identified and the deal requires a choice by the investor, information is important. Should an investor decide to be part of the deal and hold the acquisition company during the De-SPAC stage, they need to continue to be alert as to changes in the industry and the now identified company to be merged.

A perfect example of the challenges is the DWAC / Twitter scenario that DWAC shareholders are faced with. The company to be acquired seems to have had one of its mega-competitors working to steer its product line even closer to that of the small fledgling company.

Channelchek helps keep investors in smaller companies informed with quality research, insightful articles, and SPACtrac for select SPACs. Register for emails here.

As for the former President’s comments, Trump said,

“I am not going on Twitter, I am going to stay on TRUTH,” Prior to the purchase the former President stated, “I hope Elon buys Twitter because he’ll make improvements to it and he is a good man”

Managing Editor, Channelchek

Suggested Content

Investors Watch Media SPAC Stay in the Green as Markets Falter

|

De-SPAC – The Final Phase of a Special Purpose Acquisition Company

|

SPACtrac Report – Forbes Global Media Holdings

|

Capstar Special Purpose Acquisition Corp. Class A (Video)

|

Sources

https://www.sec.gov/Archives/edgar/data/0001849635/000110465921128231/tm2130724d1_ex99-1.htm

https://www.prnewswire.com/news-releases/elon-musk-to-acquire-twitter-301532245.html

https://www.cbsnews.com/news/trump-media-technology-group-investors-digital-world-acquisition-spac/

Stay up to date. Follow us:

|

Engine Gaming and Media (GAME)(GAME:CA) – A Streamlined Path Toward Positive Cash Flow

Wednesday, April 27, 2022

Engine Gaming and Media (GAME)(GAME:CA)

A Streamlined Path Toward Positive Cash Flow

Engine Media Holdings Inc is engaged in esports data provision, esports tournament hosting, and esports racing. Its brand profile includes Eden Games, Allin sports, and UMG, and others. The company’s operating segments include E-Sports; Media and Advertising and Corporate and Other. It generates maximum revenue from the Media and Advertising segment. The Media and Advertising segment includes platform and advertising services provided to other broadcasters, primarily local tv and radio broadcasters.

Michael Kupinski, Director of Research, Noble Capital Markets, Inc.

Patrick McCann, Research Associate, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

Noblecon 18 highlights. Tom Rogers, Executive Chairman, and Lou Schwartz, CEO, outlined the new strategy of the company at Noblecon18 following important recent developments, considered to be shareholder friendly. To view this fireside chat which provided detail on its plan to streamlined operations and swing toward positive cash flow, click here.

New strategy. Recently Engine shifted its focus towards media and advertising, with a special focus on social influencer marketing. Importantly, the sector trends appear favorable, with the influencer marketing industry expected to grow at a 30% CAGR from 2021 to 2025. Management identified its differentiation from competitors in the growing live-streaming platforms and social media platforms …

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

Entravision Communications (EVC) – The One To Watch

Wednesday, April 27, 2022

Entravision Communications (EVC)

The One To Watch

Entravision Communications Corporation is a diversified Spanish-language media company utilizing a combination of television and radio operations to reach Hispanic consumers across the United States, as well as the border markets of Mexico. Entravision owns and/or operates 53 primary television stations and is the largest affiliate group of both the top-ranked Univision television network and Univision’s TeleFutura network, with television stations in 20 of the nation’s top 50 Hispanic markets. The Company also operates one of the nation’s largest groups of primarily Spanish-language radio stations, consisting of 48 owned and operated radio stations.

Michael Kupinski, Director of Research, Noble Capital Markets, Inc.

Patrick McCann, Research Associate, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

Noblecon 18 highlights. CEO, Chris Young, touched on several topics including the company’s digital and global transformation, attractive leverage position, the company’s high cash flow, its attractive Latino TV business, and recent expense reductions. The full replay of the presentation can be found here.

Digital sales rep. Over the last several years, the company’s acquisitions of businesses like Cisneros, Media Donuts, and 365 Digital, have transformed it into a digital-based media company. Many of the digital businesses focus on selling advertisements for social media platforms in emerging markets, like Latin America, South Africa, and the Pacific rim. Digital revenue now accounts for more than …

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

Harte Hanks (HHS) – The Art Of A Turnaround

Wednesday, April 27, 2022

Harte Hanks (HHS)

The Art Of A Turnaround

Harte-Hanks is a marketing services company that provides multichannel marketing solutions as well as consulting, data analytics, and strategic assessment. The company’s offerings focus on business-to-business, retail, finance, and automotive segments through digital, social, mobile, and print media offerings. Harte-Hanks strives to develop better customer relationships through its marketing and analytical services for clients. The majority of its revenue is derived from its marketing services in the retail, technology, and consumer brand segments.

Michael Kupinski, Director of Research, Noble Capital Markets, Inc.

Patrick McCann, Research Associate, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

NobleCon18 highlights. Brian Linscott, CEO, and Lauri Kearnes, CFO, presented at NobleCon18 highlighting that the company has successfully pivoted from surviving to thriving. To watch a full replay of the presentation, please click here.

Customer Care keeps rolling. The Customer Care segment represented 38% of total revenues in 2021, growing 27.3% on a YoY basis. As a result of technology investments and an asset-lite strategy, the company has been able to decrease fixed costs and reduce its footprint in the division. Management is optimistic about expansion opportunities. The business could have the capacity to generate $1 million …

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

Salem Media (SALM) – Highlights Its Significant Digital Businesses

Wednesday, April 27, 2022

Salem Media (SALM)

Highlights Its Significant Digital Businesses

Salem Media Group is America’s leading radio broadcaster, Internet content provider, and magazine and book publisher targeting audiences interested in Christian and family-themed content and conservative values. In addition to its radio properties, Salem owns Salem Radio Network, which syndicates talk, news and music programming to approximately 2700 affiliates; Salem Radio Representatives, a national radio advertising sales force; Salem Web Network, a leading Internet provider of Christian content and online streaming; and Salem Publishing, a leading publisher of Christian themed magazines. Salem owns and operates 115 radio stations, with 73 stations in the nation’s top 25 top markets – and 25 in the top 10. Each of our radio properties has a full portfolio of broadcast and digital marketing opportunities.

Michael Kupinski, Director of Research, Noble Capital Markets, Inc.

Patrick McCann, Research Associate, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

NobleCon18 highlights. Evan Masyr, CFO, updated the company’s presentation to highlight its compelling digital businesses, which represent a solid 29% of total company revenues. These businesses have grown revenues at a 17% compound annual growth rate over the past 3 years. To watch a full replay of the presentation, please click here.

A durable broadcast business. Block programming, in which non-profits purchase ad-free air time and fund it through contributions from their audiences, is the largest component of the Radio segment, at 47% of Radio revenue and 28% of total company revenue. There are very high renewal rates of over 95% annually for the format, which tends to be very recession resilient. In 2022, the Block …

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

Townsquare Media (TSQ) – A Mispriced Stock?

Wednesday, April 27, 2022

Townsquare Media (TSQ)

A Mispriced Stock?

Townsquare Media Inc is an entertainment and media company offering digital marketing solutions in the United States and Canada. It owns and operates radio stations, social media properties focusing the small and mid-cap companies. Services offered to the clients include live events, local advertising, digital advertising, e-commerce offerings, few others. The segments through which the company operates its businesses are classified into Local marketing solutions and Entertainment segments. Revenues are generated from commercials through broadcasts and sale of internet based advertisements.

Michael Kupinski, Director of Research, Noble Capital Markets, Inc.

Patrick McCann, Research Associate, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

Noblecon 18 highlights. Townsquare CFO, Bill Wilson, presented at Noblecon18, speaking on a range of topics such as, the company’s evolution from a pure-play broadcaster to a digital-first company, the competitive advantages to bringing a scaled operation to small markets, and the organic nature of digital revenue growth. The full replay of the presentation can be found here.

Fast-growing digital. Mr. Wilson highlighted the robust growth of the company’s Digital businesses, noting that digital advertising is the fastest growing segment of the business, growing 20.5% in 2021. The company’s digital marketing solutions business has also experienced impressive growth with record net subscriber additions in both 2020 and 2021 …

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

Cumulus Media (CMLS) – Undervalued In Spite Of The Recent Move

Tuesday, April 26, 2022

Cumulus Media (CMLS)

Undervalued In Spite Of The Recent Move

CUMULUS MEDIA, Inc. (NASDAQ: CMLS) is a leading audio-first media and entertainment company delivering premium content to over a quarter billion people every month — wherever and whenever they want it. CUMULUS MEDIA engages listeners with high-quality local programming through 428 owned-and-operated stations across 87 markets; delivers nationally-syndicated sports, news, talk, and entertainment programming from iconic brands including the NFL, the NCAA, the Masters, the Olympics, the GRAMMYS, the American Country Music Awards, and many other world-class partners across nearly 8,000 affiliated stations through Westwood One, the largest audio network in America; and inspires listeners through its rapidly growing network of original podcasts that are smart, entertaining and thought-provoking. CUMULUS MEDIA provides advertisers with local impact and national reach through on-air, digital, mobile, and voice-activated media solutions, as well as access to integrated digital marketing services, powerful influencers, and live event experiences. CUMULUS MEDIA is the only audio media company to provide marketers with local and national advertising performance guarantees.

Michael Kupinski, Director of Research, Noble Capital Markets, Inc.

Patrick McCann, Research Associate, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

NobleCon 18 highlights Frank Lopez-Balboa, CFO, and Collin Jones, Corporate Development, held a fireside chat and outlined its operational and debt reduction strategy. In addition, management highlighted an improved financial profile given a rebounding advertising environment. A replay of the company’s presentation may be found here.

Recovery at full speed. Management declared that advertising is recovering beyond pre-pandemic levels, thanks to emerging categories such as sports betting and crypto currencies, as well as a strong comeback in entertainment and finance ad categories. These trends offset auto, which is not expected to be rebound now until 2023. Additionally, in 2022, political revenue is expected to surpass the …

This research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

Lee Enterprises, Inc. (LEE) – Digital To Drive Swing Toward Revenue Growth

Tuesday, April 26, 2022

Lee Enterprises, Inc. (LEE)

Digital To Drive Swing Toward Revenue Growth

Lee Enterprises Inc is a local news publication company in the United States. Its products include daily and Sunday newspapers, weekly newspapers and classified and few other specialty publications. Its products are used as a platform for advertising in mid-size markets. Revenues are generated primarily from retail and classifieds advertising and the remaining from subscriptions to its printed and digital products.

Michael Kupinski, Director of Research, Noble Capital Markets, Inc.

Patrick McCann, Research Associate, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

Noblecon 18 highlights. Kevin Mowbray, CEO, and Tim Millage, CFO highlighted its leading digital products and services. It is differentiated from its peers with industry leading digital subscription growth, strong digital advertising revenue from its digital agency business and compelling digital reach, with 47 million unique visitors each month. To watch a full replay of the presentation, please click here.

Local focus driving subscriptions. Management highlighted the company’s fast growing local market-focused digital subscription business. Lee’s digital subscription growth has outpaced Gannett and the New York Times for the last 9 quarters running. Lee already serves 450,000 digital-only subscribers, a 57% increase on a year-over-year basis …

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

Release – Salem Media Announces the Appointment of Scott Furrow at its 99.5 KKLA Station

![]()

Salem Media Announces the Appointment of Scott Furrow at its 99.5 KKLA Station

Research, News, and Market Data on Salem Media

IRVING, Texas–(BUSINESS WIRE)– Salem Media Group, Inc. (NASDAQ: SALM) announced today that Scott Furrow has been appointed host of ‘SoCal Live’, weekday afternoons 3-5pm on 99.5 FM KKLA.

Scott Furrow (Photo: Business Wire)

Born and raised in Southern California, Scott graduated from UC Riverside, earning a bachelor’s degree in history/law and society. Scott’s career has included roles in politics, government, media relations, as well as the corporate marketplace. He received his Master of Divinity degree from Bethel Theological Seminary in San Diego. A pastor for 25 years, Scott served as Senior Pastor of the First Baptist Church of San Diego for the past 18 years.

99.5 KKLA Director of Programming, Rodney Miller commented, “Today’s announcement comes on the heels of an eight-month nationwide search which included fill-in SoCal LIVE guest hosts Bob Lepine, Pastor Dudley Rutherford, and New Life Live’s Steve Arterburn. We are grateful and appreciative to everyone who stepped in and gave so much of their time and talent during this search.”

Miller added, “I was extremely impressed with Scott Furrow’s decision two years ago to not only serve as Senior Pastor, but also host a daily radio program on sister station KPRZ in San Diego. Scott left his sermon notes at the Church and instead brought in the top news stories discussing them from a spiritual and values perspective. On ‘SoCal Live’, Scott will have two hours each weekday to bring hope and encourage our listeners to be salt and light in today’s rapidly changing culture.”

According to Salem Los Angeles Vice President/General Manager Terry Fahy, “Scott combines a quick wit, theological knowledge and wisdom, a strong grasp of the news, and empathy for issues facing our listeners. It’s a winning combination for talk radio in Southern California.”

Scott Furrow commented, “As a pastor, my passion and my calling has been encouraging people to grow in their faith and to be more Kingdom-minded in everyday life. Hosting the ‘SoCal LIVE’ weekday program on 99.5 FM KKLA will enable me to do that on a much larger scale. I can hardly wait!”

Scott Furrow will also be heard on FM 106.1/AM 1210 KPRZ weekday afternoons 3-5pm.

ABOUT SALEM MEDIA GROUP:

Salem Media Group is America’s leading multimedia company specializing in Christian and conservative content, with media properties comprising radio, digital media and book and newsletter publishing. Each day Salem serves a loyal and dedicated audience of listeners and readers numbering in the millions nationally. With its unique programming focus, Salem provides compelling content, fresh commentary and relevant information from some of the most respected figures across the Christian and conservative media landscape. Learn more about Salem Media Group, Inc. at www.salemmedia.com, Facebook and Twitter.

Evan D. Masyr

Executive Vice President and Chief Financial Officer

(805) 384-4512

evan@salemmedia.com

Source: Salem Media Group, Inc.