Nearly 90% of Diverse / Multicultural Consumers Report Taking Positive Action as a Result of a Marketer Purposefully Investing in Their Communities, Including Switching Brands

Majority Cite More Favorable Feelings About Brands That Advertise in Diverse / Multicultural Media; 4 in 10 More Likely to Notice Ads on Those Properties Compared with Mainstream Media

HOUSTON, Feb. 14, 2023 /PRNewswire/ — Direct Digital Holdings, Inc. (Nasdaq: DRCT) (“Direct Digital Holdings” or the “Company”), a leading advertising and marketing technology platform operating through its companies Colossus Media, LLC (“Colossus SSP”), Huddled Masses LLC (“Huddled Masses”) and Orange142, LLC (“Orange142”), today released a new whitepaper, Dollars & DEI: Multicultural Consumers’ Insights on Brands’ Media Buying and Marketing Practices. The findings reveal that brands, at a time of economic uncertainty, are currently missing out on significant revenue and market share growth opportunities – and jeopardizing future growth – due to a lack of appropriate and purposeful focus on the Black, Hispanic / Latin, AAPI and LGBTQIA+ communities.

The whitepaper centers on exclusive research, commissioned by Direct Digital Holdings and conducted by Horowitz Research. An in-depth survey, the results spotlight the perspectives of diverse / multicultural consumers, a group that comprises two-fifths of the American consumer market, yet has not had proportionate attention from the advertising business.

The research tapped 1,342 U.S. adults 18+ from the Black, Hispanic / Latin, AAPI and LGBTQIA+ communities to share their attitudes and behaviors in light of the marketing world’s scattershot diversity efforts.

According to the findings, almost 90 percent of diverse / multicultural consumers report taking action because of a company investing in their community, including telling others about the brand, sharing their support on social media – or even switching to a brand, away from a competitor that does not invest in their community.

Other takeaways have major implications and offer guidance to brands, including:

8 out of 10 diverse consumers said they feel more positively about brands that live up to promises to make a concerted effort of support to their communities, and alternatively, 8 in 10 say they feel negatively about brands that don’t live up to their promises.

The large majority of diverse consumers, about 8 in 10, feel more positively about brands that advertise in targeted diverse/multicultural media.

Nearly 7 out of 10 said that purposely investing ad dollars with media that is owned or focused on their respective communities strongly demonstrates support.

4 out of 10 of respondents said they notice ads more when they appear on targeted diverse / multicultural media channels versus mainstream media.

In addition, while ad spending was found to be one of the most impactful ways for marketers to demonstrate a commitment to these audiences, creating ads and content that are inclusive of diverse communities was cited as another strong demonstration of support. To put the findings into sharper focus, both came out ahead of simply sharing social posts.

“Given this compelling data for a growing U.S. economic market segment, there should be no more reason for brands to move slowly in diversifying their media allocations,” said Mark D. Walker, CEO and Co-Founder of Direct Digital Holdings, who penned the introduction to the whitepaper. “If we put aside all the rhetoric and platitudes, this is an industry that has always been and should still be about reaching customers and driving revenue.”

Alongside the survey findings, the paper includes insights from brand leaders from HP, McDonald’s and Visa; media and marketing agency executives from Mediahub Worldwide and One50One; publishers of diverse properties such as Black Enterprise, Glitter Magazine, ODK Media, NGL Collective and Pink Media; the architect behind the new DEI trade group BRIDGE; the chairman and CEO of MediaLink; and the head of Colossus SSP.

“Siloing multicultural and diverse audiences into a separate line item in marketing plans needs to be a thing of the past,” added Alejandro Clabiorne, EVP, Executive Director, New York, Mediahub Worldwide. “This whitepaper not only makes clear that these groups are critical to marketers’ bottom lines, but also provides the types of insights that will show brands how to effectively reach and resonate with these prospective customers, building traction and brand loyalty that can fuel growth.”

“The research demonstrates that across the board, diverse and multicultural consumers recognize, appreciate and have the disposable income to spend on brands that target their communities either through authentic ad messages or media,” said Lashawnda Goffin, CEO, Colossus SSP, the sell-side technology company within Direct Digital Holdings. “Brands that have intentionally and sincerely engaged with these audiences have seen the benefit – and those looking to grow their customer base need to follow suit.”

“Making the right consumer connections is about to take on factorial proportions and while values and outlook may hold groups of targets together, beliefs and aspirations will splinter them, requiring, as the research confirms, much deeper considerations for message tone, creative and of course media placement,” said Sheryl Daija, Founder and CEO, BRIDGE. “It’s time for our industry to move from DEI as a philosophy to inclusion as a core business practice and growth driver.”

To download the whitepaper: Dollars & DEI: Multicultural Consumers’ Insights on Brands’ Media Buying and Marketing Practices, go to https://directdigitalholdings.com/whitepaper.

Methodology This study included qualitative and quantitative research conducted by Horowitz Research (www.horowitzresearch.com). The online surveys were conducted September – December 2022 among 1,342 U.S. adults 18+, including over 300 respondents each from the Black, Hispanic / Latin, AAPI and LGBTQIA+ communities.

About Direct Digital Holdings Direct Digital Holdings (Nasdaq: DRCT), owner of operating companies Colossus SSP, Huddled Masses and Orange 142, brings state-of-the-art sell- and buy-side advertising platforms together under one umbrella company. Direct Digital Holdings’ sell-side platform, Colossus SSP, offers advertisers of all sizes extensive reach within general market and multicultural media properties. The company’s subsidiaries Huddled Masses and Orange142 deliver significant ROI for middle market advertisers by providing data-optimized programmatic solutions at scale for businesses in sectors that range from energy to healthcare to travel to financial services. Direct Digital Holdings’ sell- and buy-side solutions manage approximately 90,000 clients monthly, generating over 100 billion impressions per month across display, CTV, in-app, and other media channels. Direct Digital Holdings is the ninth Black-owned company to go public in the U.S and was named a top minority-owned business by The Houston Business Journal.

Forward-Looking Statements This press release may contain forward-looking statements within the meaning of federal securities laws, including the Private Securities Litigation Reform Act of 1995, Section 27A of the Securities Act of 1933, as amended, and Section 21E of the Securities Exchange Act of 1934, as amended, and which are subject to certain risks, trends and uncertainties.

As used below, “we,” “us,” and “our” refer to Direct Digital Holdings. We use words such as “could,” “would,” “may,” “might,” “will,” “expect,” “likely,” “believe,” “continue,” “anticipate,” “estimate,” “intend,” “plan,” “project” and other similar expressions to identify forward-looking statements, but not all forward-looking statements include these words. All statements contained in this release that do not relate to matters of historical fact should be considered forward-looking statements.

All of our forward-looking statements involve estimates and uncertainties that could cause actual results to differ materially from those expressed in or implied by the forward-looking statements. Our forward-looking statements are based on assumptions that we have made in light of our industry experience and our perceptions of historical trends, current conditions, expected future developments and other factors we believe are appropriate under the circumstances. Although we believe that these forward-looking statements are based on reasonable assumptions, many factors could affect our actual operating and financial performance and cause our performance to differ materially from the performance expressed in or implied by the forward-looking statements, including, but not limited to: our dependence on the overall demand for advertising, which could be influenced by economic downturns; any slow-down or unanticipated development in the market for programmatic advertising campaigns; the effects of health epidemics, such as the ongoing global COVID-19 pandemic; operational and performance issues with our platform, whether real or perceived, including a failure to respond to technological changes or to upgrade our technology systems; any significant inadvertent disclosure or breach of confidential and/or personal information we hold, or of the security of our or our customers’, suppliers’ or other partners’ computer systems; any unavailability or non-performance of the non-proprietary technology, software, products and services that we use; unfavorable publicity and negative public perception about our industry, particularly concerns regarding data privacy and security relating to our industry’s technology and practices, and any perceived failure to comply with laws and industry self-regulation; restrictions on the use of third-party “cookies,” mobile device IDs or other tracking technologies, which could diminish our platform’s effectiveness; any inability to compete in our intensely competitive market; any significant fluctuations caused by our high customer concentration; any violation of legal and regulatory requirements or any misconduct by our employees, subcontractors, agents or business partners; any strain on our resources, diversion of our management’s attention or impact on our ability to attract and retain qualified board members as a result of being a public company; our dependence, as a holding company, of receiving distributions from Direct Digital Holdings, LLC to pay our taxes, expenses and dividends; and other factors and assumptions discussed in the “Risk Factors,” “Management’s Discussion and Analysis of Financial Conditions and Results of Operations” and other sections of our filings with the SEC that we make from time to time. Should one or more of these risks or uncertainties materialize or should any of these assumptions prove to be incorrect, our actual operating and financial performance may vary in material respects from the performance projected in these forward-looking statements. Further, any forward-looking statement speaks only as of the date on which it is made, and except as required by law, we undertake no obligation to update any forward-looking statement contained in this release to reflect events or circumstances after the date on which it is made or to reflect the occurrence of anticipated or unanticipated events or circumstances, and we claim the protection of the safe harbor for forward-looking statements contained in the Private Securities Litigation Reform Act of 1995.

The Lucky Stars Seem to Have Aligned for Online Gambling Companies

Public companies involved in sports betting may find their shareholders are the real winners. Between the increased number of states that have legalized sports betting over recent years, the enhanced betting opportunities, and the nature of the Superbowl win, luck seems to have weighed heavily on the side of these businesses. It will take time for the actual numbers to be reported. Just last year FanDuel became the first sportsbook to be profitable, it will report again in March. DraftKings, BetMGM, and Caesars, have yet to turn a profit in sports betting.

Superbowl Win Favors Companies

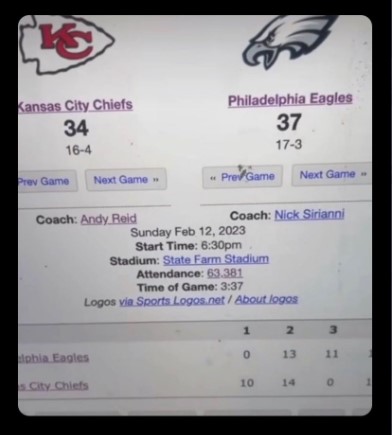

Close to 60% of bets were for the Philadelphia Eagles to be the outright winner of the game, according to FanDuel. FanDuel is the largest online sportsbook operator in the U.S. The less-expected 38-35 win for the Kansas City Chiefs over the Philadelphia Eagles at the Super Bowl will mean less wagered money will have to be distributed to customers. The team that was considered the underdog, having come out ahead, should add revenue to the bottom line of gambling companies.

The reason, of course, is companies like DraftKings and FanDuel will not have to pay out on many of the most popular bets, including widespread predictions for a 37-34 victory for the Eagles after online speculation over a ‘leaked script’ for the game.

Other Popular Bets

Before Sunday’s kick-off, Twitter and other social media conversations referred to the “leaked script.” An image was being shared that showed the Eagles winning 37-34. The image had millions of impressions on Twitter across all the shares.

Various Twitter Posts Highlighted this Image Pre-Game

Bettors could also wager on who may come out as the most valuable player. The Chiefs tight end Travis Kelce was the most selected based on bets for this honor, according to FanDuel. Instead, the MVP award was won by Chiefs quarterback Patrick Mahomes.

During a heavy betting period, there was an issue with Caesars Entertainment subsidiary William Hill US. This issue was affecting users in Nevada by preventing them from logging in on Sunday. Frustrated users took to social media outlets to complain of their difficulties during the game. The company tweeted that it was still in the process of settling all Super Bowl wagers after the game on Sunday.

Take Away

Online sports gambling is experiencing dramatic growth. Each year more states allow the practice within their borders. At the same time, technology allows betting on slices of the game, even on in-play situations never before available. With both FanDuel and DraftKings advertising to the large Superbowl audience, the practice of gambling online on sports is becoming more and more understood and common place. The 2023 Superbowl may have helped the bottom line of these companies. That will be seen when the numbers for this quarter are released. Investors are paying attention as it would seem that there is plenty of room for further growth.

There’s a lot of money being made through the business of professional sports leagues. The NBA, MLB, NHL, all have very profitable business models, and although the businesses are all similar, the NFL leads the other U.S. based leagues in generating revenue. The once tax-exempt entity has a dual business structure with multiple layers of income that continues to expand. Below we cover the multiple ways the NFL, and the months-long drive of more than 30 teams to the Superbowl, ring the register.

In 2015, the National Football League forfeited its tax-exempt status with the IRS. The league had benefitted from the unique status beginning in 1942. The decision was based in part on mounting criticism over its rapidly growing earnings streams.

These streams largely come from the 32 teams that make up the NFL, thirty-one of the ball clubs are privately owned, while just one, the Green Bay Packers, continues to operate under a non-profit public corporation status. The clubs all form a trade association through which funds are directed back to the NFL board, some find their way distributed back to the teams.

This form of entertainment rakes in money on many fronts. In-person attendance, TV viewers, different forms of wagering, and advertising dollars all feed into overall league revenue after costs such as salaries that can $50 million annually.

Tickets to the Super Bowl 2023 event between the Kansas City Chiefs and the Philadelphia Eagles are averaging about $10,000. The higher end seats are in the $40,000 range, about the same as a Tesla Model S.

Tax Exemption of Teams

The team with tax-exempt status is exempt from paying all or some of federal income taxes. This status had been maintained by all NFL teams from 1945 through 2015.

The NFL voluntarily opted to give up its tax-exempt status in 2015 and began paying taxes. Some contend this change avoids further negative public outcry. It seems the economic benefits were not as significant as the public relations disadvantages.

Business Structure

The league separates its income streams into local and national categories. On the national side, the NFL negotiates national merchandise, licensing, and television contracts. The 32 teams receive equal shares of this money, regardless of individual team performance.

Local income is generated through concession sales, ticket sales, and corporate sponsors. This doesn’t nearly cover the cost of fielding a professional football team. Using the Green Bay Packers as a benchmark, the team had expenses totaling $410 million in its fiscal year 2021. Most of this number was attributable to player salaries, with the remainder used for stadium maintenance, advertising, and team and administration expenses.

How Teams Make Money

The majority of any NFL team’s revenue comes from TV arrangements. Ticket revenues, licensing, merchandising agreements, and endorsement deals are additional income sources.

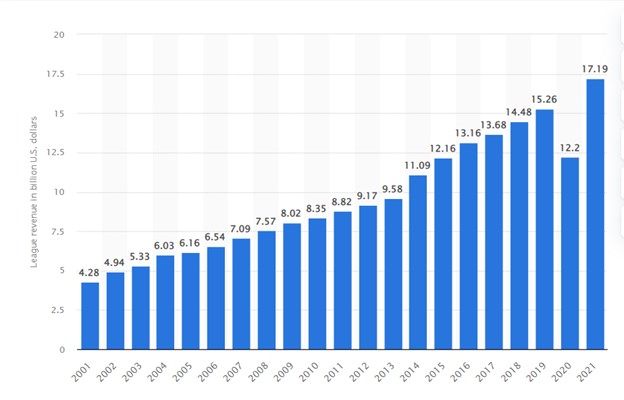

Revenue of All National Football League Teams from 2001 to 2021 (in billion U.S. dollars)

Televised Rights and Deals – The Super Bowl is among the most watched television events in America each year. The regular games broadcast on Sundays, Mondays, and Thursdays throughout the regular season will consistently have the best TV ratings. This is why media corporations pay an above average amount for the right to broadcast them.

The traditional television industry now competes with other video-based programming, all pulling the attention of those seeking entertainment. The NFL audience and draw are not in decline. NFL teams still generate massive local and even international revenue through TV contracts. The individual clubs receive significant amounts from television providers thanks to multibillion-dollar contracts, and there are even more television viewers and broadcasts of games than other programs on set.

Image Credit: Karen (Flickr)

Tickets and Vendor Rental – Far below the rapidly increasing money from TV deals, ticket sales are a large source of income for individual teams. NFL games often sell out, with an estimated average ticket price of $151 and a stadium capacity of roughly 70,000. It’s a nice add-on to broadcast viewership.

NFL teams can also use their stadiums to hold non-football activities, like concerts within local restrictions.

The cash flow on the rental of space to vendors to sell food and drinks at games are also significant in a stadium with 70,000 fans as a captive audience.

Image Credit: RaymondClarkeImages (Flickr)

Official Sponsorships – Corporate sponsors pay NFL teams to put their logos on products, TV transitions, player jerseys, etc. The franchise rights to NFL grounds naming of stadiums are extremely desirable among corporate advertisers.

The naming right to So-Fi Stadium in LA, home of the Los Angeles Rams, is in the neighborhood of $30 million annually, and similar rights to Allegiant Stadium in Las Vegas is estimated at between $20 and $25 million annually.

Gambling Franchises – Some NFL teams take advantage of this method by opening betting platforms in their stadiums, collaborating with well-known casinos, creating online sports betting websites, and other strategies. This is an area of rapid expansion as sports betting becomes legalized across the US and technology provides opportunities for betting on fragments of the game in addition to the more traditional methods. Incremental income from these growing arrangements has expanded income opportunities among teams.

Image Credit: Karen (Flickr)

Costs

Overall, like any business, the NFL will undoubtedly explore all the opportunities for meaningful income that present itself. Of course the overall income is best measured net of expenditures that include marketing, cost of athletes and other entertainers, management, upkeep, and renovations.

Take Away

One of the most financially successful professional sports leagues in the US and across the globe is the NFL. Most of the teams’ revenues are generated from broadcasting and licensing deals. The growth in revenue, with the exception of one year during the pandemic curbs, has been accelerating. Technology has brought new methods to gamble on sports, along with some friendly gaming legislation across the nation. This is additive to the bottom line.

It appears that the trend, which has survived some public relations setbacks, isn’t going to continue as Americans tend to spend many hours during the winter months immersed in the sport of football.

Twitter’s New Data Fees Leave Scientists Scrambling for Funding – or Cutting Research

Twitter is ending free access to its application programming interface, or API. An API serves as a software “middleman” allowing two applications to talk to each other. An API is an accessible way to collect and share data within and across organizations. For example, researchers at universities unaffiliated with Twitter can collect tweets and other data from Twitter through their API.

Starting Feb. 9, 2023, those wanting access to Twitter’s API will have to pay. The company is looking for ways to increase revenue to reverse its financial slide, and Elon Musk claimed that the API has been abused by scammers. This cost is likely to hinder the research community that relies on the Twitter API as a data source.

The Twitter API launched in 2006, allowing those outside of Twitter access to tweets and corresponding metadata, information about each tweet such as who sent it and when and how many people liked and retweeted it. Tweets and metadata can be used to understand topics of conversation and how those conversations are “liked” and shared on the platform and by whom.

This article was republished with permission from The Conversation, a news site dedicated to sharing ideas from academic experts. It represents the research-based findings and thoughts of, Jon-Patrick Allem, Assistant Professor of Research in Population and Public Health Sciences, University of Southern California.

As a scientist and director of a research lab focused on collecting and analyzing posts from social media platforms, I have relied on the Twitter API to collect tweets pertinent to public health for over a decade. My team has collected more than 80 million observations over the past decade, publishing dozens of papers on topics from adolescents’ use of e-cigarettes to misinformation about COVID-19.

Twitter has announced that it will allow bots that it deems provide beneficial content to continue unpaid access to the API, and that the company will offer a “paid basic tier,” but it’s unclear whether those will be helpful to researchers.

Blocking Out and Narrowing Down

Twitter is a social media platform that hosts interesting conversations across a variety of topics. As a result of free access to the Twitter API, researchers have followed these conversations to try to better understand public attitudes and behaviors. I’ve treated Twitter as a massive focus group where observations – tweets – can be collected in near real time at relatively low cost.

The Twitter API has allowed me and other researchers to study topics of importance to society. Fees are likely to narrow the field of researchers who can conduct this work, and narrow the scope of some projects that can continue. The Coalition for Independent Technology Research issued a statement calling on Twitter to maintain free access to its API for researchers. Charging for access to the API “will disrupt critical projects from thousands of journalists, academics and civil society actors worldwide who study some of the most important issues impacting our societies today,” the coalition wrote.

@SMLabTO (Twitter)

The financial burden will not affect all academics equally. Some scientists are positioned to cover research costs as they arise in the course of a study, even unexpected or unanticipated costs. In particular, scientists at large research-heavy institutions with grant budgets in the millions of dollars are likely to be able to cover this kind of charge.

However, many researchers will be unable to cover the as yet unspecified costs of the paid service because they work on fixed or limited budgets. For example, doctoral students who rely on the Twitter API for data for their dissertations may not have additional funding to cover this charge. Charging for access to the Twitter API will ultimately reduce the number of participants working to understand the world around us.

The terms of Twitter’s paid service will require me and other researchers to narrow the scope of our work, as pricing limits will make it too expensive to continue to collect as much data as we would like. As the amount of data requested goes up, the cost goes up.

We will be forced to forgo data collection on some topic areas. For example, we collect a lot of tobacco-related conversations, and people talk about tobacco by referencing the behavior – smoking or vaping – and also by referencing a product, like JUUL or Puff Bar. I add as many terms as I can think of to cast a wide net. If I’m going to be charged per word, it will force me to rethink how wide a net I cast. This will ultimately reduce our understanding of issues important to society.

Difficult Adjustments

Costs aside, many academic institutions are likely to have a difficult time adapting to these changes. For example, most universities are slow-moving bureaucracies with a lot of red tape. To enter into a financial relationship or complete a small purchase may take weeks or months. In the face of the impending Twitter API change, this will likely delay data collection and potential knowledge.

Unfortunately, everyone relying on the Twitter API for data was given little more than a week’s notice of the impending change. This short period has researchers scrambling as we try to prepare our data infrastructures for the changes ahead and make decisions about which topics to continue studying and which topics to abandon.

If the research community fails to properly prepare, scientists are likely to face gaps in data collection that will reduce the quality of our research. And in the end that means a loss of knowledge for the world.

HOUSTON, Feb. 6, 2023 /PRNewswire/ — Direct Digital Holdings, Inc. (Nasdaq: DRCT) (“Direct Digital Holdings” or the “Company”), a leading advertising and marketing technology platform operating through its companies Colossus Media, LLC (“Colossus SSP”), Huddled Masses LLC (“Huddled Masses”) and Orange142, LLC (“Orange142”), today announced that the Company will ring the Nasdaq closing bell on Tuesday, February 14, 2023, in celebration of one year since the Company listed on The Nasdaq Capital Market under ticker “DRCT”.

Company attendees at the closing bell ceremony include:

Mark D. Walker, Chairman, Co-Founder & Chief Executive Officer

Tonie Leatherberry, Director, Direct Digital Holdings

Richard Cohen, Director, Direct Digital Holdings

Misty Locke, Director, Direct Digital Holdings

The live broadcast will start at 3:45 PM Eastern Time on February 14, 2023 from the Nasdaq MarketSite Tower in New York City, New York. Please tune in to the broadcast by visiting www.nasdaq.com/marketsite/bell-ringing-ceremony.

Mark D. Walker commented on the occasion, stating, “As the ninth black-owned company to go public in the U.S., we are thrilled to be recognized by Nasdaq and thankful for the opportunity to ring the closing bell. To us, this ceremony will commemorate a year of tremendous growth and success since we first went public in February of 2022. We remain committed to delivering high-quality, technology-led digital advertising solutions to our clients and are excited for the further growth that access to the public markets allows us.”

About Direct Digital Holdings

Direct Digital Holdings (Nasdaq: DRCT), owner of operating companies Colossus SSP, Huddled Masses, and Orange 142, brings state-of-the-art sell- and buy-side advertising platforms together under one umbrella company. Direct Digital Holdings’ sell-side platform, Colossus SSP, offers advertisers of all sizes extensive reach within general market and multicultural media properties. The company’s subsidiaries Huddled Masses and Orange142 deliver significant ROI for middle market advertisers by providing data-optimized programmatic solutions at scale for businesses in sectors that range from energy to healthcare to travel to financial services. Direct Digital Holdings’ sell- and buy-side solutions manage approximately 90,000 clients monthly, generating over 100 billion impressions per month across display, video, CTV, in-app and other media channels. Direct Digital Holdings is the ninth black-owned company to go public in the U.S and was named a top minority-owned business by The Houston Business Journal.

Forward Looking Statements

This press release may contain forward-looking statements within the meaning of federal securities laws, including the Private Securities Litigation Reform Act of 1995, Section 27A of the Securities Act of 1933, as amended, and Section 21E of the Securities Exchange Act of 1934, as amended, and which are subject to certain risks, trends and uncertainties.

As used below, “we,” “us,” and “our” refer to Direct Digital Holdings. We use words such as “could,” “would,” “may,” “might,” “will,” “expect,” “likely,” “believe,” “continue,” “anticipate,” “estimate,” “intend,” “plan,” “project” and other similar expressions to identify forward-looking statements, but not all forward-looking statements include these words. All statements contained in this release that do not relate to matters of historical fact should be considered forward-looking statements.

All of our forward-looking statements involve estimates and uncertainties that could cause actual results to differ materially from those expressed in or implied by the forward-looking statements. Our forward-looking statements are based on assumptions that we have made in light of our industry experience and our perceptions of historical trends, current conditions, expected future developments and other factors we believe are appropriate under the circumstances. Although we believe that these forward-looking statements are based on reasonable assumptions, many factors could affect our actual operating and financial performance and cause our performance to differ materially from the performance expressed in or implied by the forward-looking statements, including, but not limited to: our dependence on the overall demand for advertising, which could be influenced by economic downturns; any slow-down or unanticipated development in the market for programmatic advertising campaigns; the effects of health epidemics, such as the ongoing global COVID-19 pandemic; operational and performance issues with our platform, whether real or perceived, including a failure to respond to technological changes or to upgrade our technology systems; any significant inadvertent disclosure or breach of confidential and/or personal information we hold, or of the security of our or our customers’, suppliers’ or other partners’ computer systems; any unavailability or non-performance of the non-proprietary technology, software, products and services that we use; unfavorable publicity and negative public perception about our industry, particularly concerns regarding data privacy and security relating to our industry’s technology and practices, and any perceived failure to comply with laws and industry self-regulation; restrictions on the use of third-party “cookies,” mobile device IDs or other tracking technologies, which could diminish our platform’s effectiveness; any inability to compete in our intensely competitive market; any significant fluctuations caused by our high customer concentration; any violation of legal and regulatory requirements or any misconduct by our employees, subcontractors, agents or business partners; any strain on our resources, diversion of our management’s attention or impact on our ability to attract and retain qualified board members as a result of being a public company; our dependence, as a holding company, of receiving distributions from Direct Digital Holdings, LLC to pay our taxes, expenses and dividends; and other factors and assumptions discussed in the “Risk Factors,” “Management’s Discussion and Analysis of Financial Conditions and Results of Operations” and other sections of our filings with the SEC that we make from time to time. Should one or more of these risks or uncertainties materialize or should any of these assumptions prove to be incorrect, our actual operating and financial performance may vary in material respects from the performance projected in these forward-looking statements. Further, any forward-looking statement speaks only as of the date on which it is made, and except as required by law, we undertake no obligation to update any forward-looking statement contained in this release to reflect events or circumstances after the date on which it is made or to reflect the occurrence of anticipated or unanticipated events or circumstances, and we claim the protection of the safe harbor for forward-looking statements contained in the Private Securities Litigation Reform Act of 1995.

CHELMSFORD, MA / ACCESSWIRE / January 31, 2023 / Harte Hanks, Inc. (HHS), a leading global customer experience company, today announced it is working with leading kitchen, bath, and outdoor retailer PIRCH on a series of lead generation and integrated direct marketing initiatives in Southern California.

Harte Hanks will provide PIRCH with a series of targeted communications to reach and engage shoppers at key moments in the home remodeling journey.

Harte Hanks first identified potential PIRCH customers using strategic demographics surrounding the company’s target luxury audience. Armed with this data, direct mail formats will be tested to determine a continuous marketing cadence.

“Nobody knows direct marketing like Harte Hanks,” noted Gene Hodges, VP Marketing, PIRCH. I have worked with them for many years including my time at The Home Depot and Bed, Bath & Beyond. Their expertise in strategy, customer profiling, creative, fulfillment and analytics is unrivaled. Partnering with them means we can launch our campaigns in record time with a team that will guide us through the entire process.”

Janel Harris, Managing Director, Harte Hanks Marketing Services added “PIRCH sets the standard for exceptional customer experience. We’re honored to provide them with turnkey services to help them identify, reach, and secure new customers as they turn dream-home projects into reality.”

About PIRCH:

Founded in 2009, PIRCH is a privately held fixture and appliance retailer for kitchen, bath and outdoor products based in San Diego, CA. The company operates seven Southern California showrooms and provides kitchen, bath, and outdoor design and installation from the world’s most coveted brands.PIRCH stores are experiential showrooms that allow consumers to explore appliances, plumbing fixtures, and hardware in lifestyle displays and envision how they would look and feel in their homes. Learn more at pirch.com.

About Harte Hanks:

Harte Hanks (Nasdaq:HHS) is a leading global customer experience company that partners with clients to provide them with CX strategy, data-driven analytics and actionable insights combined with seamless program execution to better understand, attract and engage their customers.

Using its resources and talent in the areas of Customer Care, Fulfillment, Logistics, and Marketing Services, Harte Hanks has driven results for some of the world’s premier brands, including Bank of America, GlaxoSmithKline, Unilever, Pfizer, HBOMax, Volvo, Ford, FedEx, Midea, Sony and IBM. Headquartered in Chelmsford, Massachusetts, Harte Hanks has over 2,500 employees in offices across the Americas, Europe, and Asia Pacific. For more information, visit hartehanks.com.

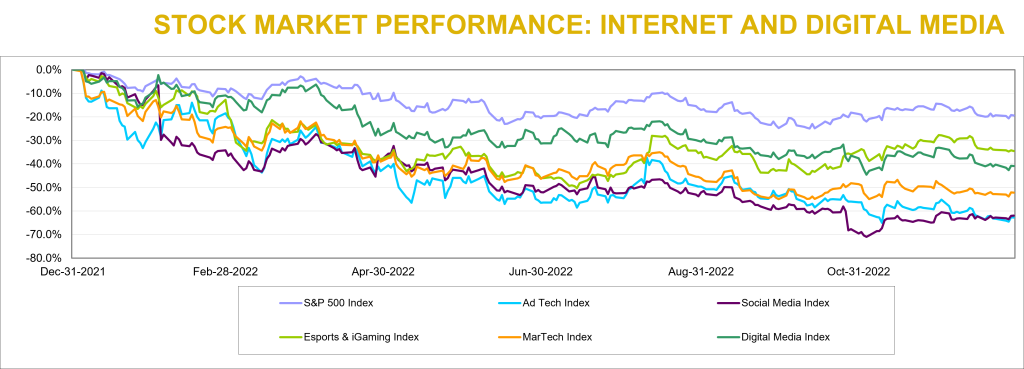

The S&P 500 increased by 7% during the fourth quarter of 2022, marking the first time the Index had increased since fourth quarter of 2021. We also saw signs of life in two of Noble’s Internet and Digital Media Indices: Noble’s eSports and iGaming Index increased (+13%) and outperformed the broader market (which we define as the S&P 500) while Noble’s MarTech Index also increased (+6%), roughly in-line with the market. This marked the second quarter in a row in which the eSports and iGaming Index not only increased but significantly outperformed the broader market, following several quarters of underperformance. Laggards during the fourth quarter were Noble’s Digital Media Index (-5%), Social Media Index (-7%) and Ad Tech Index (-20%).

Noble Indices are market cap weighted, and we attribute the relative strength of the eSports and iGaming Index to its largest constituent, Flutter Entertainment (ISE: FLTR). Flutter shares finished the year at $127.80, down only 8% from the start of the year, despite trading as low as $76 per share in mid-July. Investors appear to appreciate Flutter’s FanDuel business and its market leading position and competitive advantage, something that Flutter management highlighted during a November Investor Day. Management also laid out a case to increase U.S. revenues by 5x and achieve margins of 25%-30% implying EBITDA of up to $5 billion in 8 years-time, quadruple its levels today. Despite the overall strength of the eSports and iGaming Index, share price gains within the sector were not widely dispersed. Only 3 of the 16 stocks in eSports and iGaming sector finished the quarter up, including Engine Gaming and Media (GAME, +71%) and SportRadar Group (SRAD; +13%).

Noble’s MarTech Index increased by 6% with 11 of the 22 stocks in the index posting gains, led by Yext (YEXT; +46%), Shopify (SHOP; +29%), LiveRamp (RAMP; +29%) and Adobe (ADBE; +22%). This marks significant improvement from last quarter when only 4 of the sectors’ stocks finished the quarter in positive territory. MarTech stocks have suffered from a market resetting of revenue multiples which began when the Fed began raising rates. MarTech share price declines in the first, second and third quarters of 2022 were mostly driven by multiple compression as investors rotated out of high-flying tech sectors where companies had chased growth at all costs (at the expense of profitability). Only 7 of the MarTech companies in the Index posted positive EBITDA in the latest quarter.

2022 – A Year That Internet and Digital Media Investors Would Like to Forget

While there were signs of life in the fourth quarter of 2022 for the Internet and Digital Media sectors, 2022 was a year most investors in these sectors would like to forget. Every one of these sectors substantially underperformed the S&P 500 last year. The S&P 500 Index finished the year down 19% which was substantially better than Noble’s eSports and iGaming Index (-35%), Digital Media Index (-41%), MarTech Index (-52%), Social Media Index (-63%), and Ad Tech Index (-63%). Rather than focus on the stocks that significantly underperformed their respective Indices (and there are many), we would rather focus on the three stocks that finished 2022 up for the year.

Harte Hanks (HHS) – Shares of Harte Hanks increased by 53% in 2022, which continued its multi-year turnaround from a highly levered and unprofitable business (in 2019), to a double-digit EBITDA margin business with a debt-free balance sheet (in 2022).

Tencent (TME) – Shares of Tencent increased by 21% in 2022. Shares declined earlier in the year as China’s economy slowed as it maintained its Zero Covid-19 lockdown, but surged in the fourth quarter as it appeared that the company would enjoy an increase in demand as China begins easing Covid restrictions.

Perion Networks (PERI) – Perion shares increased by 5% in 2022 as Perion consistently beat expectations and raised its guidance throughout 2022. In the first week of 2023, the company once again pre-announced better than expected results for the fourth quarter, and shares are already up 18% since the start of the new year.

2022 M&A – A Tale of Two Halves

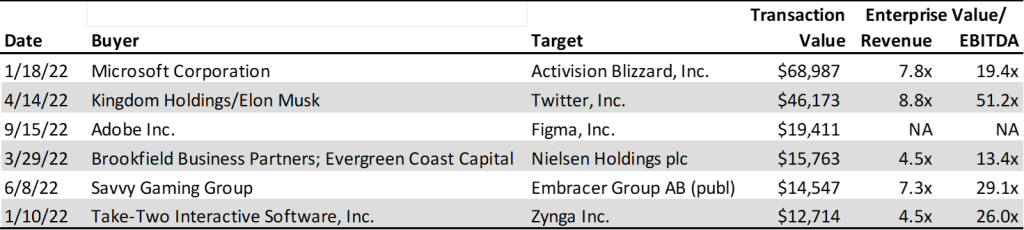

When we look back at last year from an M&A perspective, we can say that 2022 was another year of robust M&A activity. The total number of deals increased by just under 2%, as we tracked 667 deals in 2022 compared to 657 deals in 2021. Deal values were up a robust 71% in 2022 to $241 billion, up from $141 billion in 2021. The fact that deal value was so significantly higher happened despite the fact that there were far fewer deals where the transaction value was disclosed in 2022 compared to 2021. In 2022, there were 184 deals where the purchase price was disclosed, significantly lower than the 264 deals where the purchase price was disclosed in 2021.

2022 – A Year of Mega Deals

The biggest difference between 2022 and 2021 was two “mega” deals that were announced in 2022: Microsoft’s $69 billion announced acquisition of Activision Blizzard (which the Federal Trade Commission is seeking to block) and Elon Musk/Kingdom Holding’s $46 billion acquisition of Twitter. In fact, there were six transactions in 2022 that exceeded $10 billion in deal value, while there were only 2 such deals in 2021. Five of the 6 largest transactions of 2022 took place in the first half of the year. Half the largest M&A deals in 2022 were in the video or mobile gaming sector.

Only Adobe’s $19 billion announced acquisition of Figma took place in the second half of the year, which is not surprising given that the cost of financing M&A transactions using debt increased by approximately 300 basis points as the Fed continued to raise rates to fight inflation. Given the higher cost of financing deals, in 2023 we are not likely to see as many mega deals particularly at the relatively elevated EBITDA multiples shown above.

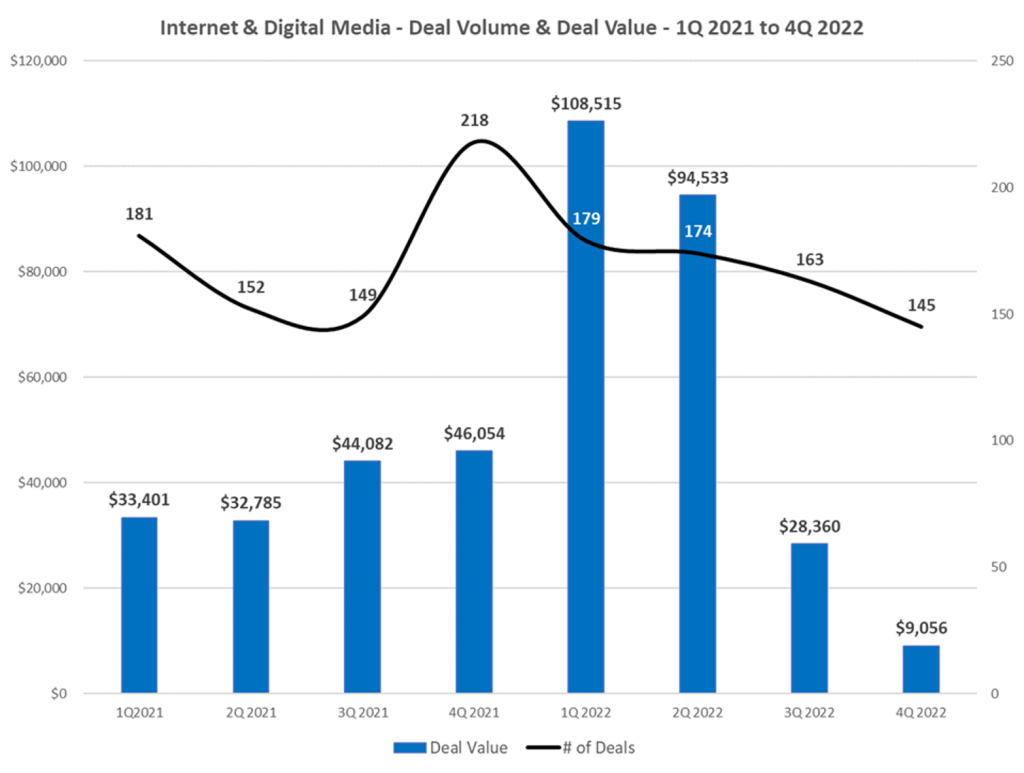

4Q 2022 M&A: A Chink in the Armor – M&A Activity and Deal Values Slide

Through the first three quarters of the year in 2022, we noted how well M&A had held up despite public equity market declines, Fed rate hikes, elevated inflation, contractionary monetary policy and geopolitical conflict. While the M&A market stayed resilient throughout most of 2022, it is clear that we began to see some “chinks in the armor” in 4Q 2022. We are not surprised by this relative weakness given the economic uncertainty and an inability to accurately forecast revenue and earnings trends for both acquirors and target companies alike.

Deal making in the fourth quarter of 2022 slowed both from a deal volume and deal value perspective. The total number of deals we tracked in the Internet and Digital Media space fell by 17% to 145 deals in 4Q 2022 compared to 174 deals in 4Q 2021. On a sequential basis, the total number of deals fell by 14% to 143 deals compared to 167 deals in 3Q 2022.

The biggest change was in deal value, where the total dollar value of deals fell by 70% to $9.1 billion in 4Q 2022 compared to $30.1 billion in 4Q 2021. On a sequential basis, deal value fell by 69% in 4Q 2022 from $29.1 billion in deal value in 3Q 2022.

The tale of two halves is best represented by the chart below.

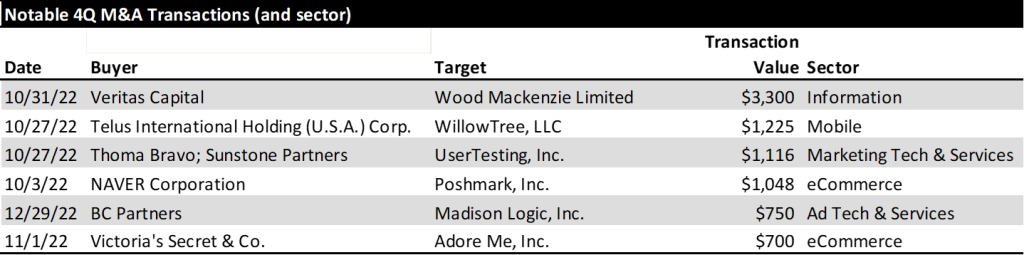

From a deal volume perspective, the most active sectors we tracked were Digital Content (40 deals), Marketing Tech (36 deals), Agency & Analytics (32 deals) and Information Services (12 deals). From a deal value perspective, the Information Services sector had the largest dollar value of transactions ($3.3 billion), followed by eCommerce ($1.7 billion), Mar Tech ($1.2 billion), and Mobile ($1.2 billion).

During the fourth quarter there were a dozen announced deals in the video gaming sector, but the sector did not register as a top sector based on deal value. In fact, only 2 of the 12 deals that were announced included the purchase price: Churchill Down’s $250 million acquisition of horse racing game provider Exacta Systems and Playstudios’ $97 million acquisition of mobile game developer Branium Studios. The largest deals in the quarter by dollar value are shown below.

Digital Advertising

Digital Advertising Outlook for 2023

Last October eMarketer revised lower its 2023 U.S. digital advertising forecast by $5.5 billion, from $284.1 billion to $278.6 billion. While this sounds like a substantial drop, in percentage terms they lowered their 2023 forecast by only 2 percentage points, from 14% growth to 12% growth. Most of the global ad agencies expect digital to continue to grow by double digits driven by dollars migrating to such digital ad channels as retail media and connected TV. Both sectors continue to demonstrate impressive growth.

Retail Media – A retail media network is a retailer-owned advertising service that allows marketers to purchase advertising space across all digital assets owned by a retail business, using the retailer’s first-party data to connect with shoppers throughout their buying journey. eMarketer forecasts that retail media ad spending in the U.S. grew by 31% last year to $41 billion and will grow to $61 billion over the next two years, by which time it will equate to 20% of all digital advertising. The leaders in retail media are Amazon, Walmart and Instacart.

Through a retail media network, partners (advertisers) get direct access to a retailer’s customers. The benefit to the partners/advertisers is that they get access to first party data. Retailers own and store this data and allow advertisers to access them through their retail media programs. The first party data is valuable because it is collected at the point of sale allowing brands to get better insights into purchase behavior. Traditional retailers are beginning to follow suit. Traditional retailers with the largest digital audiences (per comScore) are Walmart, Target, Home Depot, Lowes, CVS, Walgreens, Costco and Kohls.

On January 10th, Microsoft announced that it intended to create the industry’s most complete omnichannel retail media technology stack supported by its Promote IQ platform, a company Microsoft acquired in 2019. We expect companies that serve the retail media sector from an Ad Tech or Mar Tech standpoint are poised to benefit from secular trends in this sector.

Connected TV (CTV) – Last July, Nielsen announced that for the first time U.S. streaming TV viewership was larger than cable TV viewing. In July 2022, eMarketer forecast that CTV advertising would reach $18.9 billion in 2022. However, in October 2022,

eMarketer raised its forecast for CTV advertising by $2.3 billion to $21.2 billion in 2022. In October, the forecaster also raised its 2023 CTV advertising forecast by $3 billion to $26.9 billion, up from $23.9 billion in the July 2022 forecast. The big increase is due primarily to Netflix and Disney+ announcing they were launching ad supported tiers to their streaming offerings.

The ability to target specific audiences and measure specific outcomes tied to the ads that viewers watched has made CTV a force to be reckoned with, particularly for those advertisers that are never quite sure which of their advertising mediums provide the highest returns. Historically, TV was a mass medium used by large brands that wanted massive reach. CTV has opened the door to a wider variety of advertisers that are looking to reach more targeted, even niche, audiences. According to MNTN, a connected TV performance marketing platform, many CTV advertisers are first-time TV advertisers. With new FAST (Free Ad-Supported Streaming TV) channels coming online every month, there is no shortage of supply coming to market. This is just one reason why eMarketer predicts CTV advertising to grow by $10+ billion over the next two years and reach nearly $32 billion in advertising revenue in 2024. Ad Tech or Mar Tech companies that serve this market are also poised to benefit from secular viewing trends and the advertising dollars that are migrating to these platforms.

TRADITIONAL MEDIA COMMENTARY

The following is an excerpt from a recent note by Noble’s Media Equity Research Analyst Michael Kupinski

Overview – Will It Be A Happy New Year?

2022 was one of the worst for media stock performance in recent memory, with stocks across traditional and digital media sectors down over 40% or more. Media stocks underperformed the general market, as measured by the S&P 500 Index, which was down a more moderate 19% on a comparable basis for the full year 2022. It is typical for media stocks to underperform in a late-stage economic cycle or in the midst of an economic downturn, but the significant stock declines are stunning. Macro-economic issues including inflation, rising interest rates, and the prospect of a looming economic downturn all contributed to the poor performance.

The question is “will 2023 be better?” We believe so. There has been recent signs of life. The S&P 500 increased by 7% during the fourth quarter of 2022, marking the first time the Index had increased since fourth quarter of 2021. Notably, the Noble Publishing Index outperformed the general market in the latest quarter. However, the full impact of the recent interest rate increase likely have not been reflected in the economy. Many media stocks seem to anticipate an economic downturn, but current fundamentals do not appear to be in a freefall and may be better than expected. If the economy further deteriorates from the recent or future rate hikes, it appears now that it may adversely affect the second half of 2023. Advertising pacings appear to be holding up well so far in the first half 2023. Notably, media stocks may begin to anticipate an improving economic outlook and overlook the weak fundamental environment in the second half.

Conventional thought anticipates that increasing concerns over an economic recession may prompt mortgage rates to trend lower in 2023. Furthermore, it is possible that the Fed may lower interest rates if inflation moderates, although the Fed is not currently anticipating rate decreases in 2023. Nonetheless, this paints a favorable picture for media stocks in 2023. Traditionally, the best time to buy media stocks is in the midst of an economic downturn. In addition, these consumer cyclical stocks tend to be among the first movers in an early-stage economic cycle and tend to perform well in a moderating interest rate environment. As mentioned earlier, the stocks may currently be oversold given the prospect that the current fundamental environment is better than anticipated.

What is the risk to this favorable outlook? We believe that the resurging Chinese economy may be disruptive. Within the last month, China’s economy has been reopened from Covid lockdowns, which may put pressure on global energy prices. Such a prospect may make the Fed’s fight on inflation more stubborn to combat, potentially throwing off our favorable outlook for moderating interest rates. Given the prospect that these stocks tend to outperform the market in an early-stage economic recovery, we believe it is time for investors to accumulate positions in the media sectors.

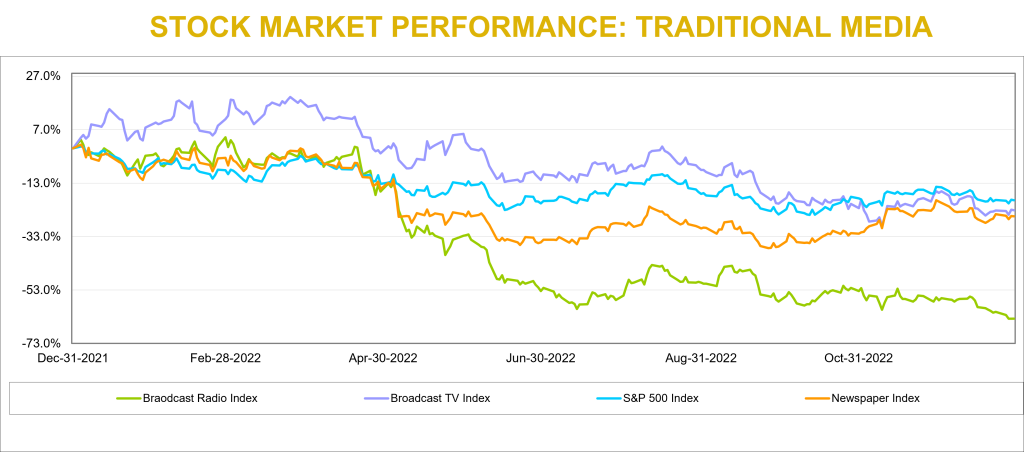

Traditional Media – Another Quarter of Moderating Stock Performance

Traditional media stocks underperformed the general market in 2022, with the Radio sector the hardest hit. The Noble Radio Index declined 64% versus 19% for the general market, as measured by the S&P 500, in a comparable time period. Television and Publishing stocks were down 23% and 25%, respectively, more in line with the general market returns. But there were notable company stock performance disparities within each sector, highlighted later in this report. Larger market capitalized companies performed better, which skewed the market cap weighted Indices.

Traditional media stocks seemed to have stabilized from the rapid declines in early 2022. The Publishing sector once again outperformed the general market in the quarter. Noble’s Television Index declined 3%, but this decline moderated from the 10% decline in the third quarter. The Radio industry still has not yet stabilized, with the Noble Radio Index down 15% in the latest quarter.

Broadcast Television

Will Netflix suck the air out of the room?

Netflix launched a new pricing plan on November 3rd which offers a basic tier with advertising at a low price point of $6.99. This compares with its previous tiers of $9.99 and $19.99 for advertising-free streaming. While reports indicate that the advertising platform is off to a slow start, we believe that the Netflix move could be disruptive to the broadcast television network business as its lower price basic service gains traction. It is likely that there will be some cannibalization from its higher pricing tier, but we believe that the move will broaden its subscriber base. While Netflix has not considered offering live sports on its streaming platform given the cost of sports rights, we believe that the potential success of its subscription/advertising tier may provide a platform to upend that decision. There is a strong tailwind for viewership trends on streaming platforms, which now exceed that of broadcast television viewing. A decision to enter sports will be a big deal and disruptive to network broadcasting.

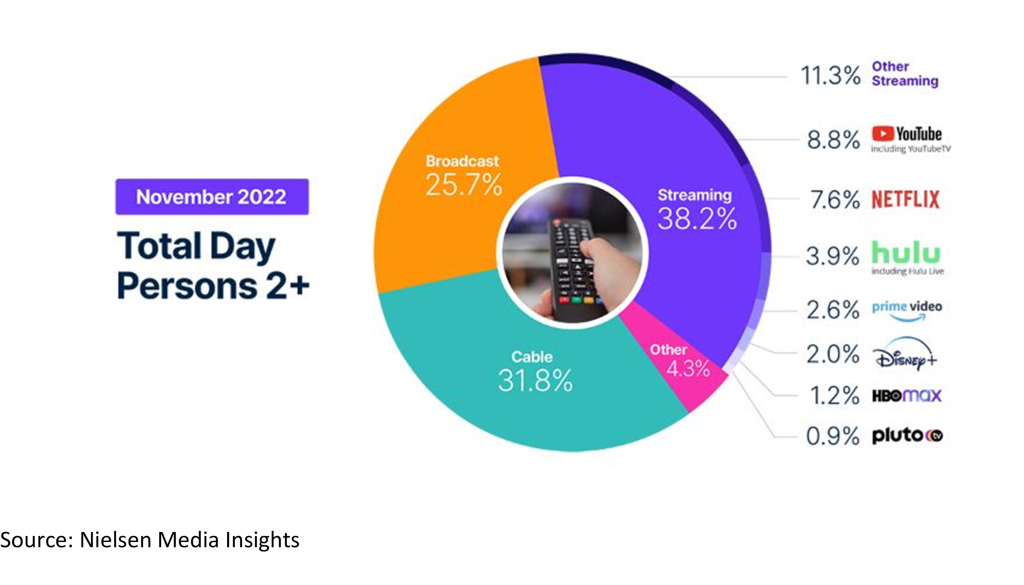

Streaming viewership not only eclipsed television viewing in July 2022, but also that of cable viewing, 34.8% versus 34.4%. In addition, based on the latest Nielsen data from November 2022, streaming now accounts for 38.2% of total viewing with Broadcast at 25.7% and cable at 31.8%, as shown in the chart below. While TV viewership increased 7.8% in November, largely due to sports content, streaming usage year over year was up more than 41%.

Scripps Plans To Expand Sports

The declining cable subscriptions and cable viewership, especially on regional sports networks, led E.W. Scripps to launch a new Scripps Sports division. This division plans to seek broadcast rights from teams and leagues and bring that programming to broadcast television. The company plans to obtain rights either in local TV markets where it can partner with local teams or on a national basis, utilizing its distribution on its Ion Network. It is important to note that ION is unique from other networks. Ion’s distribution is nearly 100% of the US television market given that it has local licenses and local towers in every market, it is fully distributed on cable and satellite, and is offered over the air. As such, we believe that Scripps offers a unique proposition to sports teams interested in building its audiences.

Will ATSC 3.0 Stream The Tide?

Furthermore, the broadcast industry appears to be more aggressively ramping its own streaming capabilities with the rollout of its new broadcast standard, ATSC 3.0. ATSC 3.0 is built on the same Internet Protocol as other streaming platforms which enables broadcast programming and internet content to be accessible in the car, on mobile devices, and in the home. While there are many opportunities for the new standard, services and offerings are still being developed. ATSC 3.0 offers promising opportunities for broadcasters to compete with streaming services in the future. We expect that the industry will make more announcements about this promising technology at future events, including the upcoming NAB Show, April 16-19 in Las Vegas, NV.

Are We In A Recession?

In our view, the current fundamentals may be better than the stocks project. Advertising seems to be holding up, post political advertising. Most companies in the industry reported strong Q3 revenue growth, influenced by a large influx of political advertising. The largest broadcasters, particularly Nexstar, have the largest EBITDA margins. The two stocks with the highest revenue growth in the quarter, Entravision and E.W. Scripps, saw their shares perform the best in the fourth quarter.

Notably, local advertising appears to be fairing better than national advertising. Based on our estimates, core local advertising is expected to be down in the range of 5% to 8%, with core national down as much as double digits. We believe that some large advertising categories like auto, retail and home improvement will show improving trends. The first quarter 2023 appears to be consistent with the fourth quarter. Broadcast network TV is another story, which we believe is weak. Network has potential heightened competition from streamers such as Netflix and Disney+ which have just launched ad-supported streaming tiers.

Is There Room For Upside?

Most TV stocks are trading in a tight range of each other. The biggest variance in stock valuations is Entravision, which is trading at 5.9x EV to our 2023 EBITDA estimate, well below that of its industry peers which trade on average at 7.7x. One might argue that Entravision, which has migrated to become a leading Digital Media company which contributes roughly 80% of its total company revenues, ought to trade at a premium to its broadcast peers, rather than at a discount. Investors appear to be somewhat confused by the company’s relatively low EBITDA margins, which is a function of how revenues are accounted for in its digital media division. We would also note that its capital structure is among the best in the industry, with a large cash position and modest net debt position.

As mentioned earlier, the Noble Broadcast TV Index declined 3% in the latest quarter, underperforming the general market’s 7% advance. E.W. Scripps, which increased 6% and Entravision, which increased 5% were among the strongest revenue performers in the third quarter. Among the poor performers were shares of Gray Television, down a significant 34% and Sinclair Broadcasting, which was down 24%. With the TV stocks down a significant 23% for the year, have the stocks already assumed that the industry is in an economic downturn? We believe that the stocks may be oversold based on the prospect that advertising is currently holding up in the first quarter.

Broadcast Radio

Digital Is Bolstering Performance

The radio industry index was the worst performing index in the traditional media segment, declining 15% in 4Q22 and 64% for the year. The radio industry is feeling the pressure that recessionary concerns place on the demand for advertising. In addition to increased competition for audiences from digital music providers and shifting advertising dollars from radio to a more targeted advertising medium, digital media.

For the third quarter Urban One and Townsquare Media top its peers with revenue growth of 9% and 8%, respectively. A common theme with companies that grew fastest was diversified revenue streams. Salem Media and Beasley Broadcast Group grew less quickly but are taking steps to further diversify revenue. Salem has diversified into content creation and digital media and Beasley is continuing to pursue a digital agency model. The median Q3 revenue growth rate was 1.5%, and the average revenue growth was -1%. The average growth rate of -1% is skewed due to the poor performance of Medico Holdings (MDIA). In previous quarters Medico benefited from Covid-19 vaccine advertising campaigns and ticket sales for an annual outdoor live event that took place in Q3 of 2021. Without Covid vaccine advertising and Medico’s concert being held in Q2 2022 instead of Q3 resulted in revenue declining 34% on a year over year basis.

After the 2022 calendar year ended, Moody’s downgraded Cumulus Media’s Corporate Family Rating to B3 from B2. Moody’s believes Cumulus Media will face a further decline in advertising demand as the economy weakens. Moody’s could upgrade its rating if leverage decreases to 5x as a result of positive performance and could downgrade its rating if leverage ratio increases to 7x as a result of poor performance. It should be noted that Cumulus has a large cash position of $118 million and could access an additional $100 million through an asset backed loan.

However, there are several companies in the radio industry with improving leverage profiles. We believe that radio companies are diversifying traditional revenue streams with digital revenue. In our view, companies that achieved a greater degree of digital transformation and are better shielded from macroeconomic headwinds. Townsquare Media, Cumulus Media, and Salem Media are among the cheapest in the group. For those companies with substantial digital media businesses that are growing rapidly, like Townsquare Media and Beasley, we believe that advertising pacings in the first quarter are likely to be positive. On the low end pacings are expected to be flat to plus 3% and may even be stronger, up 8% or more in the second quarter (although this is too early to bank). In our view, advertising for these companies do not appear to be falling off of a cliff as the stocks seem to project. Therefore, we believe that the Radio sector appears to be in an oversold position and should have some upside prospects in 2023.

Publishing

Publishing stocks had a pretty good quarter, up 18% as measured by the Noble Publishing Index versus the general market as measured by the S&P 500 Index up 7%. But the largest stocks in the index, New York Times and News Corp, were the only stocks that were up in the sector. Given that the Noble Publishing Index is market cap weighted, it was the reason that the Index was up in the quarter. Lee Enterprises was down a very modest 2% in the quarter. The relatively favorable performance of the index was primarily due to its largest constituents, News Corp. and The New York Times, which rebounded from -30% and -39%, respectively in Q2 2022, to -3% and +3%, respectively, in Q3 2022 and then up 17% and 16%, respectively, in Q4 2022.

We believe that Gannett, the nation’s largest newspaper company, continues to create a pall over the publishing group as it continues to struggle to manage cash flows with its heavy debt burden. In August, the company announced a round of layoffs of 400 employees and then announced another 200 in December. We believe that the company is trying to shore up its cash flow amidst a weak fundamental environment. Not surprisingly, GCI shares (-30%) were among the worst performers in the sector in the fourth quarter. To a large extent, the stock performance in the latest quarter reflected the various company results in Q3.

Q3 publishing revenue declined on average 1%, which excludes the strong revenue growth of the Daily Journal. The company benefited from its Journal Technologies consulting fees which bolstered revenues in its fiscal Q4 results. In addition, during the year, the company sold marketable securities for roughly $80.6 million, realizing net gains of $14.2 million. We have backed out the extraordinary results of the Daily Journal from our industry averages. Notably, Gannett had the weakest revenue performance in the fourth quarter, down 10%.

Notable exceptions to the overall weak industry revenue performance was The New York Times, up 7.5% in Q3 revenues, which reflected a moderation in revenue growth from the prior quarter of an increase of 12%. News Corp, declined 1%, which was well below the 7% gain in the prior quarter. Importantly, Lee Enterprises’ fiscal quarter revenue was down a modest 0.2%, a sequential improvement from the modest 0.7% decrease in the prior fiscal quarter. We believe that Lee’s digital strategy continues to gain traction and that the company is very close to an inflection point toward revenue growth. We continue to note that Lee’s digital subscriptions currently lead the industry. The company has exceeded all of its peers in terms of digital subscription growth in the past 11 consecutive quarters. Furthermore, over 50% of its advertising is derived from digital. Currently, roughly 30% of the company’s total revenues are derived from digital, still short of the 55% at The New York Times, but closing the gap.

Not only is Lee performing well on the digital revenue front, but the company has industry leading margins. Lee’s Q3 EBITDA margins were industry leading at 16.7%. We believe that Lee’s margins are notable given that it demonstrates that the company is managing its margins in spite of the investments in its digital media businesses. Its margins place it on par with its digital media focused peers, such as the New York Times.

LEE’s shares trade at an average industry multiple of 5.7x Enterprise Value to our 2023 adj. EBITDA estimate. Notably, the company is closing the gap with its digital media revenue contribution to that of New York Times. The New York Times carries a significantly higher stock valuation, currently trading at an estimated 15.8x EV to 2023 adj. EBITDA. We believe that the valuation gap with the New York Times should close.

This newsletter was prepared and provided by Noble Capital Markets, Inc. For any questions and/or requests regarding this news letter, please contact Chris Ensley

DISCLAIMER

All statements or opinions contained herein that include the words “ we”,“ or “ are solely the responsibility of NOBLE Capital Markets, Inc and do not necessarily reflect statements or opinions expressed by any person or party affiliated with companies mentioned in this report Any opinions expressed herein are subject to change without notice All information provided herein is based on public and non public information believed to be accurate and reliable, but is not necessarily complete and cannot be guaranteed No judgment is hereby expressed or should be implied as to the suitability of any security described herein for any specific investor or any specific investment portfolio The decision to undertake any investment regarding the security mentioned herein should be made by each reader of this publication based on their own appraisal of the implications and risks of such decision This publication is intended for information purposes only and shall not constitute an offer to buy/ sell or the solicitation of an offer to buy/sell any security mentioned in this report, nor shall there be any sale of the security herein in any state or domicile in which said offer, solicitation or sale would be unlawful prior to registration or qualification under the securities laws of any such state or domicile This publication and all information, comments, statements or opinions contained or expressed herein are applicable only as of the date of this publication and subject to change without prior notice Past performance is not indicative of future results.

Please refer to the above PDF for a complete list of disclaimers pertaining to this newsletter

Cathie Wood Reveals 2022’s Most Disruptive and Innovative Technologies

ARK Invest’s Cathie Wood penned a lookback-themed article about the innovations and disruptive companies of 2022. The purpose seemed to be to remind followers that although during the year, investors may have become disheartened with innovation, ‘look at the amazing opportunities that occurred.’ The innovations and companies highlighted were somewhat overlooked; following the path we are accustomed to from many breakthroughs, they fly under the radar. Then, suddenly they’re widely adopted. Below are many of her picks for innovation and companies she may now wish her funds held large positions in.

The Future of Internet

Suddenly everyone is talking about ChatGPT. According to Wood, artificial intelligence (AI), specifically, ChatGPT is advancing at a pace that is surprising even by standards set by earlier versions. This version of GPT-3, optimized for conversation, signed up one million users in just five days. By comparison, this onboarding of users is incredibly fast benchmarked against the original GPT-3, which took 24 months to reach the same level.

In 2022, TV advertising in the US underwent significant changes. Traditional, non-addressable, non-interactive TV ad spending dropped by 2% to $70 billion, according to Wood. Connected TV (CTV) ad spending on the same terms increased by 14% to ~$21 billion. Pure-play CTV operator Roku’s advertising platform revenue increased 15% year-over-year in the third quarter, the latest report available, while traditional TV scatter markets plummeted 38% year-over-year in the US. Roku maintained its position in the CTV market as the leading smart TV vendor in the US, accounting for 32% of the market.

Digital Wallets are replacing both credit cards and cash. In the category of offline commerce. They overtook cash as the top transaction method in 2020 and accounted for 50% of global online commerce volume in 2021. As an example of the growth, Square’s payment volume soared 193%, six times faster than the 30% increase in total retail spending 2019-2022 (relative to pre-COVID levels).

While overall e-commerce spending increased by 99% over the last three years, social commerce merchandise volume grew even faster. Shopify’s gross merchandise volume grew by 312%, almost four times faster than overall e-commerce and taking a significant share from other retail.

Underlying public blockchains continue to process transactions despite what may be going on surrounding the connected industries. Wood says it highlights that “their transparent, decentralized, and auditable ledgers could be a solution to the fraud and mismanagement associated with centralized, opaque institutions.” She explains, “After the FTX collapse, the share of trading volume on decentralized exchanges, which allow for trading without a central intermediary, rose 37% from 8.35% to 11.44%.

Genomic Revolution

Base editing and multiplexing have the potential to provide more effective CAR-T treatments for patients with otherwise incurable cancers. Cathie Wood provided an example from 2022 about a young girl in the UK with leukemia that went from hopeless in May to Canver-free in November.

In 2022 Dutch scientists at the Hubrecht Institute, UMC Utrecht, and the Oncode Institute used another form of gene editing called prime editing to correct the mutation that causes cystic fibrosis in human stem cells. Another example of how it is being adopted comes from Korean researchers at Yonsei University that used prime editing successfully to treat liver and eye diseases in adult mice.

CRISPR gene editing in Cathie’s words, “has delivered functional cures for beta-thalassemia and sickle cell disease.” She gives examples: CRISPR Therapeutics and Vertex Pharmaceuticals which together have treated more than 75 patients, resulting in some well-publicized “functional cures”. They are expecting FDA approval for Exa-Cel, the treatment for sickle cell and beta thalassemia, in early 2023.

In the category the Ark Invest founder referred to as other cell and gene therapies, she says in 2022, regulators approved several landmark cell and gene therapies. The examples she used to highlight this are Hemgenix for the treatment of Haemophilia B, Zyntelgo for beta thalassemia, Skysona for cerebral adrenoleukodystrophy, Yescarta and Breyanzi for Non-Hodgkin lymphoma, Tecartus for mantle cell lymphoma, and Carvykti and Abecma for multiple myeloma.

Liquid biopsies, blood tests via molecular diagnostic testing are enabling the early detection of colorectal cancer which, if discovered at or before stage 1, have a five-year survival rate greater than 90%. Late-stage or metastatic cancers account for more than 55% of deaths over a five-year period, but only 17% of new diagnoses.

Autonomous Technology & Robotics

During 2022 electric vehicle maker Tesla sales increased by 49% even as automobile sales declined by 8%. Tesla’s share of total auto sales in the US has increased to 3.8% from 1.4% in three years.

During 2022, GM expanded its autonomous driving taxi service to most of San Francisco in the first large-scale rollout in a major US city. Then it launched in both Phoenix and Austin late in the year. The automaker with a stodgy reputation, managed to compress the time to commercialization from nine years in San Francisco to just 90 days in Austin. Tesla, for its part, expanded access to its FSD (full self-driving) beta software to all owners in North America who had requested access.

By January 4, 2023, both Amazon and Walmart had begun deliveries using drones in select US cities. Autonomous logistics technology is no longer futuristic and is likely to continue being adopted and expanded.

Across the top 50 medical device companies, 90% rely on 3D printing for prototyping, testing, and even in some cases printing medical devices.

In 2022, SpaceX nearly doubled the number of rockets it launched to 61. It reused the same rocket in as few as 21 days, a dramatic improvement over the 356 days required for its first rocket reuse. Private Space Exploration is a reality. 61 rockets is an average of more than one per week.

Take Away

Hedge fund manager Cathie Wood took the new year as an opportunity to communicate examples of game-changing innovation that the equity market largely ignored in 2022. She finds these as confidence building that the premise of many of her managed funds is with merit. More importantly, in the face of market headwinds and media criticism, she wants these examples to help boost investor confidence “that ARK’s strategies are on the right side of change.” She tells readers, “innovation solves problems and has historically gained share during turbulent times.”

CHELMSFORD, MA / ACCESSWIRE / January 9, 2023 / Harte Hanks, Inc. (Nasdaq:HHS), a leading global customer experience company, today announced that management will present at the Sidoti & Company Virtual Micro-Cap Conference on January 18, 2023 at 10:45 a.m. ET. In addition, management will virtually host one-on-one meetings with participating investors on Wednesday, January 18 and Thursday, January 19, 2023.

A webcast of the company’s conference presentation will be available on the Harte Hanks investor relations website at https://investors.hartehanks.com.

Investors interested in a meeting with Harte Hanks management can contact their Sidoti representative or email hhs@fnkir.com.

About Harte Hanks

Harte Hanks (Nasdaq:HHS) is a leading global customer experience company whose mission is to partner with clients to provide them with CX strategy, data-driven analytics and actionable insights combined with seamless program execution to better understand, attract, and engage their customers.

Using its unparalleled resources and award-winning talent in the areas of Customer Care, Fulfillment and Logistics, and Marketing Services, Harte Hanks has a proven track record of driving results for some of the world’s premier brands including Bank of America, GlaxoSmithKline, Unilever, Pfizer, HBOMax, Volvo, Ford, FedEx, Midea, Sony and IBM, among others. Headquartered in Chelmsford, Massachusetts, Harte Hanks has over 2,500 employees in offices across the Americas, Europe, and Asia Pacific.

As used herein, “Harte Hanks” or “the Company” refers to Harte Hanks, Inc. and/or its applicable operating subsidiaries, as the context may require. Harte Hanks’ logo and name are trademarks of Harte Hanks.

Investor Relations Contact:

FNK IR Rob Fink or Tom Baumann (646) 809-4048 / (646) 349-6641 HHS@fnkir.com

NEW YORK, NY / ACCESSWIRE / January 4, 2023 / Engine Gaming and Media, Inc. (“Engine” or the “Company”) (NASDAQ:GAME)(TSXV:GAME),a data-driven, gaming, media and influencer marketing platform company, today announced that it will issue a press release promptly after the market close on Tuesday, January 17, 2023, summarizing its financial results for the fiscal first quarter of 2023 ended November 30, 2022. The Company will also host a conference call the same day at 4:30 p.m. Eastern Time to discuss its financial results in further detail. The call will conclude with Q&A from participants.

Please dial in at least 10 minutes before the start of the call to ensure timely participation.

A playback of the call will be available through January 24, 2023, on Engine Gaming and Media, Inc.’s Investor Relations website at ir.enginemediainc.com or via telephone replay by dialing 1-844-512-2921 or 1-412-317-6671. The Access Code is 13735206.

About Engine Gaming and Media, Inc.

Engine Gaming and Media, Inc. (NASDAQ:GAME)(TSXV:GAME) provides unparalleled live streaming data and social analytics, influencer relationship management and monetization, and programmatic advertising to support the world’s largest video gaming companies, brand marketers, ecommerce companies, media publishers and agencies to drive new streams of revenue. The company’s subsidiaries include Stream Hatchet, the global leader in gaming video distribution analytics; Sideqik, a social influencer marketing discovery, analytics, and activation platform; and Frankly Media, a digital publishing platform used to create, distribute, and monetize content across all digital channels. Engine Gaming generates revenue through a combination of software-as-a-service subscription fees, managed services, and programmatic advertising. For more information, please visit www.enginegaming.com.

Cautionary Statement on Forward-Looking Information

This news release contains forward-looking statements. Forward-looking statements involve known and unknown risks, uncertainties and other factors which may cause the actual results, performance or achievements of Engine to be materially different from any future results, performance or achievements expressed or implied by the forward-looking statements. Often, but not always, forward-looking statements can be identified by the use of words such as “plans”, “expects” or “does not expect”, “is expected”, “estimates”, “intends”, “anticipates” or “does not anticipate”, or “believes”, or variations of such words and phrases or state that certain actions, events or results “may”, “could”, “would”, “might” or “will” be taken, occur or be achieved. In respect of the forward-looking information contained herein, Engine has provided such statements and information in reliance on certain assumptions that management believed to be reasonable at the time. Forward-looking information involves known and unknown risks, uncertainties and other factors which may cause the actual results, performance or achievements stated herein to be materially different from any future results, performance or achievements expressed or implied by the forward-looking information. Actual results could differ materially from those currently anticipated due to a number of factors and risks. Accordingly, readers should not place undue reliance on forward-looking information contained in this news release.