HOUSTON, July 27, 2023 /PRNewswire/ — Direct Digital Holdings, Inc. (Nasdaq: DRCT) (“Direct Digital Holdings” or the “Company”), a leading advertising and marketing technology platform operating through its companies Colossus Media, LLC (“Colossus SSP”), Huddled Masses LLC (“Huddled Masses”) and Orange142, LLC (“Orange142”), today announced that the Company will report financial results for the second quarter of fiscal year 2023 ended June 30, 2023 on Thursday, August 10, 2023 after the U.S. stock market closes. Management will host a conference call and webcast on the same day at 5:00 PM ET to discuss the results.

About Direct Digital Holdings Direct Digital Holdings (Nasdaq: DRCT), owner of operating companies Colossus SSP, Huddled Masses, and Orange 142, brings state-of-the-art sell- and buy-side advertising platforms together under one umbrella company. Direct Digital Holdings’ sell-side platform, Colossus SSP, offers advertisers of all sizes extensive reach within general market and multicultural media properties. The company’s subsidiaries Huddled Masses and Orange142 deliver significant ROI for middle market advertisers by providing data-optimized programmatic solutions at scale for businesses in sectors that range from energy to healthcare to travel to financial services. Direct Digital Holdings’ sell- and buy-side solutions manage approximately 153,000 clients monthly, generating over 100 billion impressions per month across display, CTV, in-app and other media channels. Direct Digital Holdings is the ninth black-owned company to go public in the U.S. and was named a top minority-owned business by The Houston Business Journal.

CHELMSFORD, MA / ACCESSWIRE / July 27, 2023 /Harte Hanks, Inc. (NASDAQ:HHS), a leading global customer experience company focused on bringing companies closer to customers for nearly 100 years, announced today that the company will release financial results for the second quarter period ended June 30, 2023 on Thursday, August 10, 2023 after the close of the market.

The Company will host a conference call and live webcast to discuss these results at 4:30 p.m. EST on the same day. Interested parties may access the webcast at https://investors.hartehanks.com/events or may access the conference call by dialing 877-545-0320in the United States or 973-528-0002from outside the U.S. and using access code 183563.

A replay of the call can also be accessed via phone through August 24, 2023 by dialing (877) 481-4010 from the U.S., or (919) 882-2331 from outside the U.S. The conference call replay passcode is 48804.

About Harte Hanks:

Harte Hanks (NASDAQ:HHS) is a leading global customer experience company whose mission is to partner with clients to provide them with CX strategy, data-driven analytics and actionable insights combined with seamless program execution to better understand, attract and engage their customers.

Using its unparalleled resources and award-winning talent in the areas of Customer Care, Fulfillment and Logistics, and Marketing Services, Harte Hanks has a proven track record of driving results for some of the world’s premier brands, including Bank of America, GlaxoSmithKline, Unilever, Pfizer, HBOMax, Volvo, Ford, FedEx, Midea, Sony and IBM among others. Headquartered in Chelmsford, Massachusetts, Harte Hanks has over 2,500 employees in offices across the Americas, Europe, and Asia Pacific.

As used herein, “Harte Hanks” or “the Company” refers to Harte Hanks, Inc. and/or its applicable operating subsidiaries, as the context may require. Harte Hanks’ logo and name are trademarks of Harte Hanks.

Investor Relations Contact:

Rob Fink or Tom Baumann 646.809.4048 / 646.349.6641 FNK IR HHS@fnkir.com

HOUSTON, July 13, 2023 /PRNewswire/ — Direct Digital Holdings, Inc. (Nasdaq: DRCT) (“Direct Digital Holdings” or the “Company”), a leading advertising and marketing technology platform operating through its companies Colossus Media, LLC (“Colossus SSP”), Huddled Masses LLC (“Huddled Masses”) and Orange142, LLC (“Orange142”), is pleased to announce it has entered into a $5 million revolving credit facility (the “Credit Facility”) with East West Bank.

In addition to the principal amount of up to $5 million, the Company has access to up to an additional $5 million uncommitted incremental revolving facility, which may increase the aggregate principal amount of the credit facility to $10 million. Loans under the Credit Facility mature on July 7, 2025, unless the Credit Facility is otherwise terminated pursuant to its terms.

Mark D. Walker, Chairman & Chief Executive Officer of Direct Digital Holdings, commented, “We are excited to begin our relationship with East West Bank and are appreciative of the financial flexibility and liquidity that this partnership provides. We look forward to continuing to invest in and grow our businesses through this new source of non-dilutive capital.”

For more information, please view our Form 8-K filed with the Securities and Exchange Commission at www.sec.gov.

About Direct Digital Holdings

Direct Digital Holdings (Nasdaq: DRCT), owner of operating companies Colossus SSP, Huddled Masses, and Orange 142, brings state-of-the-art sell- and buy-side advertising platforms together under one umbrella company. Direct Digital Holdings’ sell-side platform, Colossus SSP, offers advertisers of all sizes extensive reach within general market and multicultural media properties. The company’s subsidiaries Huddled Masses and Orange142 deliver significant ROI for middle market advertisers by providing data-optimized programmatic solutions at scale for businesses in sectors that range from energy to healthcare to travel to financial services. Direct Digital Holdings’ sell- and buy-side solutions manage approximately 153,000 clients monthly, generating over 100 billion impressions per month across display, CTV, in-app and other media channels. Direct Digital Holdings is the ninth black-owned company to go public in the U.S. and was named a top minority-owned business by The Houston Business Journal.

Forward Looking Statements

This press release may contain forward-looking statements within the meaning of federal securities laws, including the Private Securities Litigation Reform Act of 1995, Section 27A of the Securities Act of 1933, as amended, and Section 21E of the Securities Exchange Act of 1934, as amended, and which are subject to certain risks, trends and uncertainties.

As used below, “we,” “us,” and “our” refer to Direct Digital Holdings. We use words such as “could,” “would,” “may,” “might,” “will,” “expect,” “likely,” “believe,” “continue,” “anticipate,” “estimate,” “intend,” “plan,” “project” and other similar expressions to identify forward-looking statements, but not all forward-looking statements include these words. All statements contained in this release that do not relate to matters of historical fact should be considered forward-looking statements.

All of our forward-looking statements involve estimates and uncertainties that could cause actual results to differ materially from those expressed in or implied by the forward-looking statements. Our forward-looking statements are based on assumptions that we have made in light of our industry experience and our perceptions of historical trends, current conditions, expected future developments and other factors we believe are appropriate under the circumstances. Although we believe that these forward-looking statements are based on reasonable assumptions, many factors could affect our actual operating and financial performance and cause our performance to differ materially from the performance expressed in or implied by the forward-looking statements, including, but not limited to: our dependence on the overall demand for advertising, which could be influenced by economic downturns; any slow-down or unanticipated development in the market for programmatic advertising campaigns; the effects of health epidemics, such as the ongoing global COVID-19 pandemic; operational and performance issues with our platform, whether real or perceived, including a failure to respond to technological changes or to upgrade our technology systems; any significant inadvertent disclosure or breach of confidential and/or personal information we hold, or of the security of our or our customers’, suppliers’ or other partners’ computer systems; any unavailability or non-performance of the non-proprietary technology, software, products and services that we use; unfavorable publicity and negative public perception about our industry, particularly concerns regarding data privacy and security relating to our industry’s technology and practices, and any perceived failure to comply with laws and industry self-regulation; restrictions on the use of third-party “cookies,” mobile device IDs or other tracking technologies, which could diminish our platform’s effectiveness; any inability to compete in our intensely competitive market; any significant fluctuations caused by our high customer concentration; any violation of legal and regulatory requirements or any misconduct by our employees, subcontractors, agents or business partners; any strain on our resources, diversion of our management’s attention or impact on our ability to attract and retain qualified board members as a result of being a public company; our dependence, as a holding company, of receiving distributions from Direct Digital Holdings, LLC to pay our taxes, expenses and dividends; changes in the overall credit market or our creditworthiness; and other factors and assumptions discussed in the “Risk Factors,” “Management’s Discussion and Analysis of Financial Conditions and Results of Operations” and other sections of our filings with the SEC that we make from time to time. Should one or more of these risks or uncertainties materialize or should any of these assumptions prove to be incorrect, our actual operating and financial performance may vary in material respects from the performance projected in these forward-looking statements. Further, any forward-looking statement speaks only as of the date on which it is made, and except as required by law, we undertake no obligation to update any forward-looking statement contained in this release to reflect events or circumstances after the date on which it is made or to reflect the occurrence of anticipated or unanticipated events or circumstances, and we claim the protection of the safe harbor for forward-looking statements contained in the Private Securities Litigation Reform Act of 1995.

AdTech company co-founders selected for prestigious regional award celebrating ambitious entrepreneurs who are building a better world

HOUSTON, June 20, 2023 /PRNewswire/ — Direct Digital Holdings, Inc. (Nasdaq: DRCT) (“Direct Digital Holdings” or the “Company”), a leading advertising and marketing technology platform operating through its companies Colossus Media, LLC (“Colossus SSP”), Huddled Masses LLC (“Huddled Masses”) and Orange142, LLC (“Orange142”), today announced that its co-founders, Mark D. Walker, Chairman and CEO, and Keith Smith, President, were selected by Ernst & Young LLP (EY US) as Entrepreneur Of The Year® 2023 Gulf South Award winners.

Direct Digital Holdings and its subsidiaries create a unique advertising ecosystem that offers services on both the ad-buy and ad-sell sides, strategically positioning the company to reach consumers, brands and publishers of all sizes. The Company has been particularly successful in focusing on opportunities in small-to-mid-sized media markets and multicultural communities, which are often overlooked and undervalued in the advertising industry.

“As someone who was raised in the Houston-area, winning a Gulf South Award for the company I co-founded with my good friend, Keith, is thrilling and a testament to what we have accomplished in disrupting the ad space,” said Walker. “We are grateful to Ernst & Young, for the recognition, and recognize the incredible talent and dedication of those working at our portfolio companies, Colossus SSP, Huddled Masses and Orange142. Keith and I also thank the entire Direct Digital Holdings team including our partners and clients who made this all possible.”

Direct Digital Holdings has continued to see robust financial performance, experiencing 131% and 87% year-over-year Revenue growth in fiscal year 2022 and the first quarter of fiscal 2023, respectively. The Company processed approximately 207 billion monthly impressions and received more than six billion bid responses in the first quarter of 2023, increases of more than 130% and 81% over the same period in 2022, respectively.

“Direct Digital Holdings’ success is rooted in the hard work and commitment we have long seen in taking advantage of advertising opportunities targeting underserved communities and markets often overlook,” added Smith. “Mark and I are enormously proud of this accomplishment and the contributions of our dedicated employees. We also want to thank Ernst & Young and congratulate all of the other finalists and our fellow winners for their entrepreneurial accomplishments.”

The Entrepreneur Of The Year Awards program is one of the preeminent competitive awards for entrepreneurs and leaders of high-growth companies. Walker and Smith were selected by an independent judging panel made up of previous award winners, leading CEOs, investors and other regional business leaders. The candidates were evaluated based on their demonstration of building long-term value through entrepreneurial spirit, purpose, growth and impact, among other core contributions and attributes.

Entrepreneur Of The Year Award winners become lifetime members of a global, multi-industry community of entrepreneurs, with exclusive, ongoing access to the experience, insight and wisdom of program alumni and other ecosystem members in over 60 countries. Since 1986, the Entrepreneur Of The Year program has recognized more than 11,000 US executives.

As a Gulf South award winner, Walker and Smith are now eligible for consideration for the Entrepreneur Of The Year 2023 National Awards. The National Award winners including the Entrepreneur Of The Year National Overall Award winner will be announced in November at the Strategic Growth Forum®, one of the nation’s most prestigious gatherings of high-growth, market-leading companies. The Entrepreneur Of The Year National Overall Award winner will then move on to compete for the World Entrepreneur Of The Year® Award in June 2024.

About Direct Digital Holdings Direct Digital Holdings (Nasdaq: DRCT), owner of operating companies Colossus SSP, Huddled Masses, and Orange 142, brings state-of-the-art sell- and buy-side advertising platforms together under one umbrella company. Direct Digital Holdings’ sell-side platform, Colossus SSP, offers advertisers of all sizes extensive reach within general market and multicultural media properties. The company’s subsidiaries Huddled Masses and Orange142 deliver significant ROI for middle market advertisers by providing data-optimized programmatic solutions at scale for businesses in sectors that range from energy to healthcare to travel to financial services. Direct Digital Holdings’ sell- and buy-side solutions manage approximately 153,000 clients monthly, generating over 100 billion impressions per month across display, CTV, in-app and other media channels. Direct Digital Holdings is the ninth black-owned company to go public in the U.S and was named a top minority-owned business by The Houston Business Journal.

About Entrepreneur Of The Year® Entrepreneur Of The Year® is the world’s most prestigious business awards program for unstoppable entrepreneurs. These visionary leaders deliver innovation, growth and prosperity that transform our world. The program engages entrepreneurs with insights and experiences that foster growth. It connects them with their peers to strengthen entrepreneurship around the world. Entrepreneur Of The Year is the first and only truly global awards program of its kind. It celebrates entrepreneurs through regional and national awards programs in more than 145 cities in over 60 countries. National Overall Award winners go on to compete for the World Entrepreneur Of The Year® title.

HOUSTON, May 31, 2023 /PRNewswire/ — Direct Digital Holdings, Inc. (Nasdaq: DRCT) (“Direct Digital Holdings” or the “Company”), a leading advertising and marketing technology platform operating through its companies Colossus Media, LLC (“Colossus SSP”), Huddled Masses LLC (“Huddled Masses”) and Orange142, LLC (“Orange142”), today announced that the Company will participate in The Roth MKM Internet Virtual Summit being held virtually from June 11-15, 2023.

Mark Walker, Chairman & Chief Executive Officer of Direct Digital Holdings, will be hosted in a fireside chat by Darren Aftahi, Managing Director and Senior Research Analyst of Roth MKM at 9:00 AM PT on Tuesday, June 13, 2023.

For more information, please reach out to your Roth MKM representative.

About Direct Digital Holdings Direct Digital Holdings (Nasdaq: DRCT), owner of operating companies Colossus SSP, Huddled Masses, and Orange 142, brings state-of-the-art sell- and buy-side advertising platforms together under one umbrella company. Direct Digital Holdings’ sell-side platform, Colossus SSP, offers advertisers of all sizes extensive reach within general market and multicultural media properties. The company’s subsidiaries Huddled Masses and Orange142 deliver significant ROI for middle market advertisers by providing data-optimized programmatic solutions at scale for businesses in sectors that range from energy to healthcare to travel to financial services. Direct Digital Holdings’ sell- and buy-side solutions manage approximately 153,000 clients monthly, generating over 100 billion impressions per month across display, CTV, in-app and other media channels. Direct Digital Holdings is the ninth black-owned company to go public in the U.S and was named a top minority-owned business by The Houston Business Journal.

HOUSTON, May 23, 2023 /PRNewswire/ — Direct Digital Holdings, Inc. (Nasdaq: DRCT) (“Direct Digital Holdings” or the “Company”), a leading advertising and marketing technology platform operating through its companies Colossus Media, LLC (“Colossus SSP”), Huddled Masses LLC (“Huddled Masses”) and Orange142, LLC (“Orange142”), today announced that the Company will participate in the Stifel 2023 Cross Sector Insight Conference taking place June 6-7, 2023 at The InterContinental Boston in Boston, Massachusetts.

Mark Walker, Chairman & Chief Executive Officer, Keith Smith, President, and Susan Echard, Chief Financial Officer, will be attending on behalf of the Company. Management will be presenting on Tuesday, June 6, 2023 at 10:20 AM ET and will also be available for meetings during the conference.

For more information, or to schedule a meeting with management, please reach out to your Stifel representative.

About Direct Digital Holdings

Direct Digital Holdings (Nasdaq: DRCT), owner of operating companies Colossus SSP, Huddled Masses, and Orange 142, brings state-of-the-art sell- and buy-side advertising platforms together under one umbrella company. Direct Digital Holdings’ sell-side platform, Colossus SSP, offers advertisers of all sizes extensive reach within general market and multicultural media properties. The company’s subsidiaries Huddled Masses and Orange142 deliver significant ROI for middle market advertisers by providing data-optimized programmatic solutions at scale for businesses in sectors that range from energy to healthcare to travel to financial services. Direct Digital Holdings’ sell- and buy-side solutions manage approximately 153,000 clients monthly, generating over 100 billion impressions per month across display, CTV, in-app and other media channels. Direct Digital Holdings is the ninth black-owned company to go public in the U.S and was named a top minority-owned business by The Houston Business Journal.

PHOENIX, May 12, 2023 (GLOBE NEWSWIRE) — QuoteMedia, Inc. (OTCQB: QMCI), a leading provider of market data and financial applications, announced financial results for the quarter ended March 31, 2023.

QuoteMedia provides banks, brokerage firms, private equity firms, financial planners and sophisticated investors with a more economical, higher quality alternative source of stock market data and related research information. We compete with several larger legacy organizations and a modest community of other smaller companies. QuoteMedia provides comprehensive market data services, including streaming data feeds, on-demand request-based data (XML/JSON), web content solutions (financial content for website integration) and applications such as Quotestream Professional desktop and mobile.

Highlights for Q1 2023 include the following:

Quarterly revenue increased by 11% to $4,750,048 in Q1 2023 from $4,263,796 in 2022, an increase of $486,252.

On an FX-neutral basis, revenue growth for Q1 2023 vs Q1 2022 was 14% (1) .

Quarter-over-quarter revenue increased 4% when comparing Q1 2023 to Q4 2022.

Adjusted EBITDA for Q1 2023 was $829,585 compared to $680,424 in Q1 2022, an improvement of $149,161 (22%) (1) .

“2022 was another great year for QuoteMedia, and as anticipated, that momentum is carrying forward into 2023,” said Robert J. Thompson, Chairman of the Board. “We expect improved revenue growth for the remainder of the year, and record profitability for fiscal 2023. These are truly exciting times for QuoteMedia, as we continue to expand our product lines, develop new partnerships, increase our market share and broaden our presence in the financial data industry. We are very pleased with our results to date; and anticipate extending QuoteMedia’s growth and profitability into the foreseeable future.”

QuoteMedia will host a conference call Monday, May 15, 2023 at 2:00 PM Eastern Time to discuss the Q1 2023 financial results and provide a business update.

Conference Call Details:

Date: May 15, 2023

Time: 2:00 PM Eastern

Dial-in number: 800-245-3047

Conference ID: QUOTEMEDIA

An audio rebroadcast of the call will be available later at: www.quotemedia.com

About QuoteMedia

QuoteMedia is a leading software developer and cloud-based syndicator of financial market information and streaming financial data solutions to media, corporations, online brokerages, and financial services companies. The Company licenses interactive stock research tools such as streaming real-time quotes, market research, news, charting, option chains, filings, corporate financials, insider reports, market indices, portfolio management systems, and data feeds. QuoteMedia provides industry leading market data solutions and financial services for companies such as the Nasdaq Stock Exchange, TMX Group (TSX Stock Exchange), Canadian Securities Exchange (CSE), London Stock Exchange Group, FIS, U.S. Bank, Bank of Montreal (BMO), Broadridge Financial Systems, JPMorgan Chase, Scotiabank, CI Financial, Canaccord Genuity Corp., Hilltop Securities, Avantax, Stockhouse, Zacks Investment Research, General Electric, Boeing, Bombardier, Telus International, Business Wire, PR Newswire, The Goldman Sachs Group, Regal Securities, ChoiceTrade, Cetera Financial Group, Dynamic Trend, Inc., Credential Qtrade Securities, CNW Group, iA Private Wealth, Ally Invest, Inc., Suncor, Leede Jones Gable, Firstrade Securities, Charles Schwab, First Financial, Equisolve, Stock-Trak, Mergent, Cision and others. Quotestream®, QMod™ and Quotestream Connect™ are trademarks of QuoteMedia. For more information, please visit www.quotemedia.com .

Statements about QuoteMedia’s future expectations, including future revenue, earnings, and transactions, as well as all other statements in this press release other than historical facts are “forward-looking statements” within the meaning of the Private Securities Litigation Reform Act of 1995. QuoteMedia intends that such forward-looking statements be subject to the safe harbors created thereby. These statements involve risks and uncertainties that are identified from time to time in the Company’s SEC reports and filings and are subject to change at any time. QuoteMedia’s actual results and other corporate developments could differ materially from that which has been anticipated in such statements.

Below are the specific forward-looking statements included in this press release:

We expect improved revenue growth for the remainder of the year, and record profitability for fiscal 2023.

We believe that Adjusted EBITDA, as a non-GAAP pro forma financial measure, provides meaningful information to investors in terms of enhancing their understanding of our operating performance and results, as it allows investors to more easily compare our financial performance on a consistent basis compared to the prior year periods. This non-GAAP financial measure also corresponds with the way we expect investment analysts to evaluate and compare our results. Any non-GAAP pro forma financial measures should be considered only as supplements to, and not as substitutes for or in isolation from, or superior to, our other measures of financial information prepared in accordance with GAAP, such as net income attributable to QuoteMedia, Inc.

We define and calculate Adjusted EBITDA as net income attributable to QuoteMedia, Inc., plus: 1) depreciation and amortization, 2) stock compensation expense, 3) interest expense, 4) foreign exchange loss (or minus a foreign exchange gain), and 5) income tax expense. We disclose Adjusted EBITDA because we believe it is a useful metric by which to compare the performance of our business from period to period. We understand that measures similar to Adjusted EBITDA are broadly used by analysts, rating agencies, investors and financial institutions in assessing our performance. Accordingly, we believe that the presentation of Adjusted EBITDA provides useful information to investors. The table below provides a reconciliation of Adjusted EBITDA to net income attributable to QuoteMedia, Inc., the most directly comparable GAAP financial measure.

QuoteMedia, Inc. Adjusted EBITDA Reconciliation to Net Income:

Three-months ended March 31,

2023

2022

Net income

$

113,290

$

149,041

Depreciation and amortization

627,987

487,095

Stock-based compensation

78,125

59,864

Interest expense

1,452

1,224

Foreign exchange loss (gain)

8,001

(17,590

)

Income tax expense

730

790

Adjusted EBITDA

$

829,585

$

680,424

In addition to the non-GAAP measures discussed above, we also analyze certain measures, including net revenues and operating expenses, on an FX-neutral basis to better measure the comparability of operating results between periods. Management believes that changes in foreign currency exchange rates are not indicative of the company’s operations and evaluating growth in net revenues and operating expenses on an FX-neutral basis provides an additional meaningful and comparable assessment of these measures to both management and investors. FX-neutral results are calculated by translating the current period’s local currency results with the prior period’s exchange rate. FX-neutral growth rates are calculated by comparing the current period’s FX-neutral results by the prior period’s results.

Goffin Recognized for Driving Company & Team Growth at Colossus SSP, a Direct Digital Holdings Company

HOUSTON, April 28, 2023 /PRNewswire/ — Direct Digital Holdings, Inc. (Nasdaq: DRCT) (“Direct Digital Holdings” or the “Company”), a leading advertising and marketing technology platform operating through its companies Colossus Media, LLC (“Colossus SSP”), Huddled Masses LLC (“Huddled Masses”) and Orange142, LLC (“Orange142”), today announced that Lashawnda Goffin, Chief Executive Officer of Colossus SSP, has been selected to win the 2023 Catalyst Award, a special accolade that is part of the AdExchanger and AdMonsters’ 2023 Top Women in Media & Ad Tech program. The award is given to a woman industry leader who has driven a tremendous amount of growth for the business and team over the past year.

“Since Lashawnda began her leadership role with Direct Digital Holdings’ supply-side platform, Colossus SSP, she has been a major force in its rapid growth. Year-over-year revenues between 2021 and 2022 more than tripled – an impressive achievement,” said Mark D. Walker, CEO and Co-Founder of Direct Digital Holdings. “She is deserving of this award for her work at Colossus SSP, as well as for advancing diversity and progress within our industry.”

“Throughout my time at Direct Digital Holdings, I’ve encouraged my team at Colossus SSP to adopt innovative ways to grow our business, while working towards building a more inclusive marketplace by empowering niche and multicultural publishers,” said Goffin. “I am very honored to receive this award and will accept it as recognition of the exceptional business results my entire team continues to achieve.”

Currently, Colossus SSP represents 26,000 media properties – offering inventory from both multicultural/diverse and general market publishers. The company has 163,000 advertisers accessing its platform monthly, generating over 130 billion impressions per month across display, CTV, in-app and other media.

Lashawnda Goffin will receive the 2023 Catalyst Award on Monday, June 5 at the AdExchanger and AdMonsters’ Top Women in Media & Ad Tech Awards Gala, which will be held at the Metropolitan Pavilion in New York City.

About Direct Digital Holdings Direct Digital Holdings (Nasdaq: DRCT), owner of operating companies Colossus SSP, Huddled Masses and Orange 142, brings state-of-the-art sell- and buy-side advertising platforms together under one umbrella company. Direct Digital Holdings’ sell-side platform, Colossus SSP, offers advertisers of all sizes extensive reach within general market and multicultural media properties. The company’s subsidiaries Huddled Masses and Orange142 deliver significant ROI for middle market advertisers by providing data-optimized programmatic solutions at scale for businesses in sectors that range from energy to healthcare to travel to financial services. Direct Digital Holdings’ sell- and buy-side solutions manage approximately 90,000 clients monthly, generating over 100 billion impressions per month across display, CTV, in-app, and other media channels. Direct Digital Holdings is the ninth Black-owned company to go public in the U.S and was named a top minority-owned business by The Houston Business Journal.

Forward-Looking Statements This press release may contain forward-looking statements within the meaning of federal securities laws, including the Private Securities Litigation Reform Act of 1995, Section 27A of the Securities Act of 1933, as amended, and Section 21E of the Securities Exchange Act of 1934, as amended, and which are subject to certain risks, trends and uncertainties.

As used below, “we,” “us,” and “our” refer to Direct Digital Holdings. We use words such as “could,” “would,” “may,” “might,” “will,” “expect,” “likely,” “believe,” “continue,” “anticipate,” “estimate,” “intend,” “plan,” “project” and other similar expressions to identify forward-looking statements, but not all forward-looking statements include these words. All statements contained in this release that do not relate to matters of historical fact should be considered forward-looking statements.

All of our forward-looking statements involve estimates and uncertainties that could cause actual results to differ materially from those expressed in or implied by the forward-looking statements. Our forward-looking statements are based on assumptions that we have made in light of our industry experience and our perceptions of historical trends, current conditions, expected future developments and other factors we believe are appropriate under the circumstances. Although we believe that these forward-looking statements are based on reasonable assumptions, many factors could affect our actual operating and financial performance and cause our performance to differ materially from the performance expressed in or implied by the forward-looking statements, including, but not limited to: our dependence on the overall demand for advertising, which could be influenced by economic downturns; any slow-down or unanticipated development in the market for programmatic advertising campaigns; the effects of health epidemics, such as the ongoing global COVID-19 pandemic; operational and performance issues with our platform, whether real or perceived, including a failure to respond to technological changes or to upgrade our technology systems; any significant inadvertent disclosure or breach of confidential and/or personal information we hold, or of the security of our or our customers’, suppliers’ or other partners’ computer systems; any unavailability or non-performance of the non-proprietary technology, software, products and services that we use; unfavorable publicity and negative public perception about our industry, particularly concerns regarding data privacy and security relating to our industry’s technology and practices, and any perceived failure to comply with laws and industry self-regulation; restrictions on the use of third-party “cookies,” mobile device IDs or other tracking technologies, which could diminish our platform’s effectiveness; any inability to compete in our intensely competitive market; any significant fluctuations caused by our high customer concentration; any violation of legal and regulatory requirements or any misconduct by our employees, subcontractors, agents or business partners; any strain on our resources, diversion of our management’s attention or impact on our ability to attract and retain qualified board members as a result of being a public company; our dependence, as a holding company, of receiving distributions from Direct Digital Holdings, LLC to pay our taxes, expenses and dividends; and other factors and assumptions discussed in the “Risk Factors,” “Management’s Discussion and Analysis of Financial Conditions and Results of Operations” and other sections of our filings with the SEC that we make from time to time. Should one or more of these risks or uncertainties materialize or should any of these assumptions prove to be incorrect, our actual operating and financial performance may vary in material respects from the performance projected in these forward-looking statements. Further, any forward-looking statement speaks only as of the date on which it is made, and except as required by law, we undertake no obligation to update any forward-looking statement contained in this release to reflect events or circumstances after the date on which it is made or to reflect the occurrence of anticipated or unanticipated events or circumstances, and we claim the protection of the safe harbor for forward-looking statements contained in the Private Securities Litigation Reform Act of 1995.

A Focus on Profitability Drives A Strong Start to the Year

Last quarter we wrote that the S&P 500 increased for the first time since the fourth quarter of 2021 and that we were beginning to see signs of life in Noble’s Internet and Digital Media Indices as well. Those signs of life continued to bear fruit throughout the first quarter, as every one of Noble’s Internet and Digital Media Indices not only finished the quarter up, but significantly outperformed the S&P 500. The best performing index was Noble’s Social Media Index, which increased by 70% in the first quarter of 2023, followed by Noble’s eSports & iGaming Index (+32%), Ad Tech Index (+31%), MarTech Index (+30%), and Digital Media Index (+18%).

Noble’s Indices are market cap weighted, and we attribute the strength of the Social Media Index to its largest constituent, Meta Platforms (META; a.k.a. Facebook) whose shares increased by 76% in the first quarter. We attribute this increase to management’s 4Q 2022 earnings call when they spent most of their time talking about “efficiency”, which investors interpreted to mean that Meta was newly focused on profitability. After a relatively disastrous 3Q 2022 earnings call, after which shares fell by 25%, the company demonstrated on its 4Q 2022 earnings call that it clearly had

gotten the message: investors were not enamored about the company’s plans in October 2022 to spend billions of dollars to develop its Metaverse initiatives. Rather, on its fourth quarter call, management focused on driving its short form video initiative Reels (i.e., becoming more TikTok like), reducing its headcount by reducing layers of management, lowering its operating expenses and reducing its capital expenditures. Investors applauded this newfound focus on profitability and shares rebounded from a low of $88.90 per share in early November to $211.94 at the March quarter-end.

Noble’s eSports and iGaming Index increased by 32% as 9 of the 16 stocks in the index posted gains, the two largest market cap weighted stocks. Shares of the largest stock in the index, Flutter Entertainment (FLTR) increased by 31%) while shares of the second largest stock in the index, DraftKings (DKNG) increased by 70%. Flutter’s improvement is likely due to an improved inflection point in the company’s U.S. operations which include its FanDuel operations. DraftKings also beat revenue and EBITDA expectations in 4Q 2022 and appears to be proving out its path to profitability. In both cases, investors are rewarding companies who are accelerating their path to profitability.

The next best performing index was Noble’s Ad Tech Index which increased by 31% during 1Q 2023. Fourteen of the 23 stocks in the index were up in the first quarter. Standouts during the quarter were Integral Ad Science (IAS; +62%) and Perion Networks (PERI; +56%). Integral Ad Science exceeded expectations in its fourth quarter results and guided to better-than-expected results in 1Q 2023. The company continues to expand its product suite, scale its social media offerings (i.e., for TikTok) and is well positioned to continue to benefit from the shift from linear TV to connected TV (CTV). Perion shares continued their winning streak: Perion was the only ad tech stock whose shares were up in 2022. Perion’s 56% increase in 1Q 2023 reflected beat on both revenues (by 2%) and EBITDA (by 10%) as well as improved guidance for 1Q 2023. Perion’s profitability increased significantly in 2022, with EBITDA nearly doubling (+90%) from $70 million in 2021 to $132 million in 2022.

Noble’s MarTech Index increased by 30% with 14 of the 22 stocks in the index posting increases in 1Q 2023. The best performing stocks were Qualtrics (XM; +70%) Sprinklr (CXM; +59%), Salesforce (CRM; +51%), Hubspot (HUBS; +48%) and Yext (YEXT; +47%). Qualtrics agreed to be acquired for $12.5 billion by Silver Lake and the Canadian Pension Plan Investment Board, which came at a 73% premium to its 30-day volume weighted stock price. Sprinklr beat revenue expectations and significantly beat EBITDA expectations (doubling the Street expectations) and guided to a current year forecast that focuses more on efficiency and profitability. MarTech stocks have been victims of their own success. Two years ago at this time the sector was trading at 11.3x forward revenue estimates, and a year ago the group was trading at 6.5x forward revenues. Today the group trades at 4.1x forward revenues and investors appear to be wading back into the sector.

Finally, Noble’s Digital Media Index, while lagging that of its digital peers posted an 18% increase and significantly outperformed the S&P 500 (+7%) with a broad based recovery in which 9 of the sector’s 11 stocks increase during 1Q 2023. The best performing stock was Spotify (SPOT; +69%), whose revenues fell short of expectations by less than 1%, significantly beat consensus Street EBITDA expectations by $58M and more importantly pivoted towards demonstrating operating leverage. Spotify, which posted an EBITDA loss of nearly $500 million 2022 is expected to generate $650 million in EBITDA in 2024, according Street estimates. A deteriorating ad market 2022 combined with higher interest rates likely prompted the company to shift its priorities to running a profitable company and doing it more quickly. The second best performing stock was Travelzoo (TZOO; +36%), as the company’s 4Q 2022 revenues and EBITDA increased by 31% and 328%, respectively. Notably, Travelzoo’s EBITDA came in 58% higher than Street consensus. The company appears to be benefiting from pent up demand for travel and management highlighted the opportunity for margin expansion in the coming quarters.

Sluggish M&A Market Carries Over into 2023

Last quarter we remarked that M&A deals in the Internet and Digital Media sector had held up well through the first three quarters of 2022 despite economic headwinds. However, the number of deals slowed in 4Q 2022 (by 17%) and total deal value fell dramatically (by 70%). The slowdown carried over into 1Q 2023. According to Dealogic, Global M&A fell by 48% to $575 billion in 1Q 2023 compared to $1.1 trillion in 1Q 2022. Global M&A dollar values fell to their lowest level in a decade. In the U.S., deal values fell by 44% to $283 billion from $176 billion in 1Q 2022.

The M&A market had weathered stock price declines, Fed rate hikes, elevated inflation, and geopolitical conflict in 2022. In 1Q 2023, to this “recession that never comes” economic environment we added increased volatility and uncertainty caused by banking failures. One of the biggest impediments to deals is debt financing. Private equity firms have had to write larger check in lieu of a robust debt financing market. Banks have been less willing to provide financing because some have had to hold loans on their balance sheet or take losses when selling debt to investors while smaller regional banks have seen deposits flee to larger banks, especially those considered too big to fail.

Finally, increased antitrust scrutiny likely has played a role in the M&A deal slowdown. Lengthy merger reviews resulted in three public transactions being blocked by regulators: Standard General’s acquisition of Tegna; JetBlue’s acquisition of Spirit Airlines, and Intercontinental Exchange’s acquisition of Black Knight, Inc.

1Q 2023 Internet and Digital Media M&A: A Dearth of Large Deals

Based on Noble’s analysis, deal making in the first quarter of 2023 in the Internet and Digital Media sectors actually increased by 11% compared to 1Q 2022. The total number of deals we tracked in the Internet and Digital Media space increased to 202 deals in 1Q 2023 compared to 182 deals in 1Q 2022. On a sequential basis, the total number of deals increased by 39% compared to 145 deals in 4Q 2022. The only explanation we can provide for this is that with the expectation that an economic slowdown was pending, many companies likely made the decision to sell in mid-2022, with the deals being announced in 1Q 2023.

The biggest change was in the first quarter’s M&A deal value, where the total dollar value of deals fell by 95% to $5.4 billion of announced deals in 1Q 2023 compared to $108.5 billion in announced deals in 1Q 2022. On a sequential basis, deal value fell by 40% from $9.1 billion in deal value in 4Q 2022.

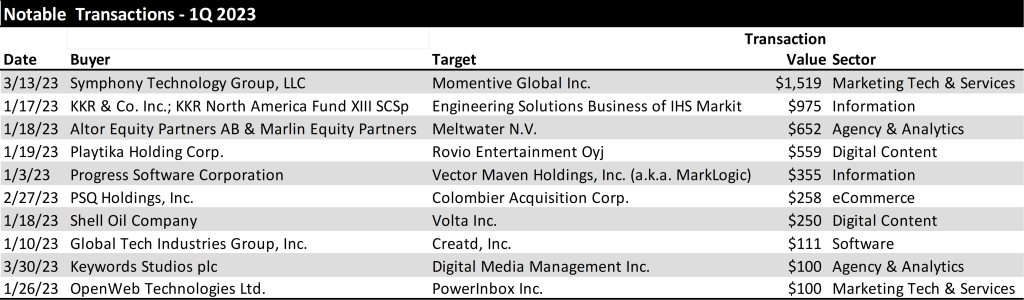

From a deal volume perspective, the most active sectors we tracked were Digital Content (59 deals), Agency & Analytics (51 deals), and MarTech (39), followed by Information Services (17 deals), Ad Tech (11 deals) and eCommerce sectors (10 deals). From a dollar value perspective, MarTech led the way with $1.6 billion in transactions, followed by Information Services ($1.4 billion), Digital Content ($922 million) and Agency and Analytics ($875 million). The largest deals in the quarter by dollar value are shown below.

Notably, there were no mega deals ($10B+) in the first quarter of 2023, compared to the first quarter of 2022 when Microsoft agreed to by Activision Blizzard for $68 billion and Take-Two Interactive agreed to acquire Zynga for $12 billion. Once the Fed stops hiking rates and visibility into operating trends returns, we may begin to see an environment in which mega deals will be contemplated again.

TRADITIONAL MEDIA COMMENTARY

The following is an excerpt from a recent note by Noble’s Media Equity Research Analyst Michael Kupinski

The NAB Show Stopper

Media investors are unpacking all of information from last week’s National Association of Broadcasters (NAB) convention. There is a lot to digest given that there were over 1,400 exhibits, and 140 new exhibitors this year. Because of the overwhelming number of exhibitors, many that go to Vegas for this annual convention do not go to the convention floor. It is a shame. There is a lot to see and learn. Noble’s Media & Entertainment Analyst Michael Kupinski walked the convention floor, which covers 4.6 million square feet of exhibit halls and meeting rooms. He stopped by booths and taped presentations to explain the new technologies, the plan for implementation of new services, and the prospect for revenue monetization. One important demonstration focused on the new broadcast standard, ATSC 3.0, the hope for a bright future for the television industry. This new standard should allow the industry to become more contemporary in terms of how its audience consumes video and information. In addition, it offers the ability for the industry to participate in new revenue streams, including datacasting, which may become bigger than Retransmission revenue in the future.

In addition to touring the floor, he participated in NAB panel discussions and hosted meetings with media management teams in a fireside chat format to discuss current business trends, the new technologies (including Artificial Intelligence (AI)) and the new broadcast standard. In addition, these C-suite management teams provided their key takeaways from the NAB convention and offered why they participated in the conference this year. These discussions will be available for free to Channelchek users on Channelchek.com on April 27th as a virtual conference. In this upcoming Channelchek Takeaway Series on the NAB Show, Michael offers his key takeaways, including the current advertising outlook, his take on the monetization of the new technologies and what media investors should do now given the current economic and advertising environment. Free registration to this informative event is available here.

This report highlights the performance of the media sectors over the past 12 months and past quarter. Overall, media stocks struggled in the past year, but there has been some improved quarterly performance, particularly in Digital Media and Broadcast Television, discussed later. All media stocks are struggling to offset losses over the course of the past year with trailing 12 months stocks down in the range of 5% on the low end to as high as down 68%.

In the first quarter, stock performance was mixed. The best performers in the traditional media sectors were Broadcast Television stocks, up nearly 10% versus the general market which increased 7% in the comparable period. However, the individual TV stock performance reflected a different story, explained later in this report. The worse performer for the quarter were the radio stocks, driven by a Wall Street downgrade of one of the leading radio broadcasters. We believe that stock performance will be a roller coaster for at least another quarter or two as the weight of the Fed rate increases begin to adversely affect the economy.

While national advertising has remained weak, we believe that local advertising is now beginning to moderate as well. The local advertising weakness appears to be in the smaller markets as well as the larger markets. This is somewhat different than the most recent economic cycles whereby the smaller markets were somewhat resilient. It seems that the smaller markets are feeling the adverse affects from inflation, rising employment costs and tightening bank credit. In our view, the disappointing advertising outlook likely will cause second quarter revenue estimates to come down, creating a difficult environment for media stocks.

Broadcast Television

Weak Current Revenue Trends

TV stocks outperformed the general market in the first quarter. This market cap weighted index masked the performance of many poor performing stocks in the quarter. Sinclair Broadcasting (up 10%), Entravision (up a strong 26%), and Fox (up 12%) were the best performing stocks and favorably influenced the TV index in the quarter. But, there were many poor performing stocks including E.W. Scripps (down 29%), Gray Television (down 22%) and Tegna (down 20%). We believe that there was heightened interest in Entravision given its favorable Q1 results which was fueled by its fast growing digital advertising business. Entravision’s Q4 revenue performance was among the best in the industry. While Entravision was among the best revenue performer, its margins are below that of its peer group EBITDA Margins. This is due to the accounting treatment of its digital revenues given that it is an agency business.. The poorer performing stocks are among the higher debt levered in the industry. The underperformance reflects concern of a slowing economy and investors flight to quality in the sector.

We do not believe that we are out of the woods with the TV stocks and the market is expected to be volatile. The advertising environment appears to be deteriorating given weakening economic conditions. There are bright spots which include some improvement in the Auto category. Dealerships appear to be stepping up advertising given higher inventory levels. In addition, broadcasters appear optimistic about political advertising, which could begin in the third quarter 2023. There is a planned Republican presidential candidate debate schedule in August. There is some promise that candidates will advertise in advance of that debate and into the fourth quarter given the early primary season. We do not believe that political and auto will be enough to offset the weakness in national and Local advertising. In our view, Q2 and full year 2023 estimates are likely to come down. Furthermore, we believe that broadcasters will be shy about predicting political advertising even into 2024 given the past disappointments in management forecasts in the last political cycle.

Broadcast Radio

All Out of Love

Radio stocks had another tough quarter, down 17% versus a 7% gain for the general market. Notably, there was a wide variance in the individual stock performance, with the largest stocks in the group having the worst performance in the quarter, including Audacy (AUD down 40%), Cumulus Media (CMLS down 41%) and iHeart Media (IHRT down 36%). The first quarter stock performance did not appear to reflect the fourth quarter results, during which revenues were relatively okay, with some exceptions. Some of the larger radio companies which have a large percentage of national advertising, underperformed relative to the more diversified radio companies, especially those with a strong digital segment presence. Margins for the industry remain relatively healthy.

The weakness in the Radio stocks was fueled in the quarter from a downgrade to Underperform on the shares of iHeart by a Wall Street firm. Many radio stocks were down in sympathy. The analyst attributed the downgrade to the current macro environment and its heavy floating rate debt burden. The company is not expected to generate enough free cash flow to de-lever its balance sheet. We believe the downgrade as well as the excessive debt profile of Audacy, another industry leader which likely will need to restructure, sent all radio stocks tumbling. Some stocks performed better than others. While Cumulus Media’s debt profile is not as levered as iHeart or Audacy, the shares were caught in the net of a weak advertising outlook. Cumulus is among the most sensitive to national advertising, which currently continues to be weak.

Some of our favorite stocks which are diversified and have developing digital businesses performed better. Those stocks included Townsquare Media (TSQ, up 10%), and Salem Media (SALM, up 4%). Notably, while the shares of Beasley Broadcasting (BBGI) were down 10%, the shares performed better than the 17% decline for the industry in the quarter. Importantly, Beasley recently provided favorable updated Q1 guidance for the first quarter. Q1 revenues are expected to increase 1% to 2.5% and EBITDA growth is expected to be in the range of 40% to 50%, significantly better than our estimates. Furthermore, management provided a sanguine outlook for 2023 and 2024. Digital revenue is expected to reach 20% to 30% of total revenue with a goal of reaching 40% in 2024. By comparison, digital revenue was 17% of total revenue in the fourth quarter 2022. Furthermore, the company is sitting on roughly $35 million in cash. It has opportunistically repurchased $10 million of its bonds at a significant discount. We believe that it is likely to maintain a strong cash position given the economic uncertainty.

Townsquare Media (TSQ), Salem Media (SALM) and Beasley Broadcast (BBGI) are all diversifying their revenue streams. While these companies are not immune to the economic headwinds, we believe theirdigital businesses should offer some ballast to its more sensitive Radio business. In the case of Salem, 30% of its revenues are relatively stable with block programming.

Publishing

After a period of moderating revenue trends, publishers reported a weakened advertising environment. Revenue trends deteriorated with print advertising taking a nose dive. This trend was illustrative in the results from Lee Enterprises. After a fiscal fourth quarter flat revenue performance, the company reported a 8.5% decline in its fiscal first quarter. The Q1 revenue performance reflected an 18.5% decrease in print advertising, an acceleration in the rate of the 11% decline in the previous quarter.

The surprisingly weak quarter hit the company’s adj. EBITDA margins. Traditionally, Lee maintained some of the best margins in the industry., but the company fell in ranking to among the lowest in the sector. Importantly, in spite of the revenue weakness, the company maintained its previous adj. EBITDA guidance of $94 million to $100 million for F2023. To achieve its cash flow target in light of the soft revenue outlook, Lee implemented a round of expense cuts to bolster cash flow. Cost reductions are expected to result in $40 million of savings in FY 23, and $60 million in annualized savings going forward. While the company’s print business declined more than expected , the company’s digital businesses remains favorably robust. In addition, its digital business is turning toward contributing margins; another step in the company’s digital evolution.

This newsletter was prepared and provided by Noble Capital Markets, Inc. For any questions and/or requests regarding this news letter, please contact Chris Ensley

DISCLAIMER

All statements or opinions contained herein that include the words “ we”,“ or “ are solely the responsibility of NOBLE Capital Markets, Inc and do not necessarily reflect statements or opinions expressed by any person or party affiliated with companies mentioned in this report Any opinions expressed herein are subject to change without notice All information provided herein is based on public and non public information believed to be accurate and reliable, but is not necessarily complete and cannot be guaranteed No judgment is hereby expressed or should be implied as to the suitability of any security described herein for any specific investor or any specific investment portfolio The decision to undertake any investment regarding the security mentioned herein should be made by each reader of this publication based on their own appraisal of the implications and risks of such decision This publication is intended for information purposes only and shall not constitute an offer to buy/ sell or the solicitation of an offer to buy/sell any security mentioned in this report, nor shall there be any sale of the security herein in any state or domicile in which said offer, solicitation or sale would be unlawful prior to registration or qualification under the securities laws of any such state or domicile This publication and all information, comments, statements or opinions contained or expressed herein are applicable only as of the date of this publication and subject to change without prior notice Past performance is not indicative of future results.

Please refer to the above PDF for a complete list of disclaimers pertaining to this newsletter

HOUSTON, April 20, 2023 /PRNewswire/ — Direct Digital Holdings, Inc. (Nasdaq: DRCT) (“Direct Digital Holdings” or the “Company”), a leading advertising and marketing technology platform operating through its companies Colossus Media, LLC (“Colossus SSP”), Huddled Masses LLC (“Huddled Masses”) and Orange142, LLC (“Orange142”), today announced that the Company will report financial results for the first quarter of fiscal year 2023 ended March 31, 2023 on Thursday, May 11, 2023 after the U.S. stock market closes. Management will host a conference call and webcast on the same day at 5:00 PM ET to discuss the results.

About Direct Digital Holdings Direct Digital Holdings (Nasdaq: DRCT), owner of operating companies Colossus SSP, Huddled Masses, and Orange 142, brings state-of-the-art sell- and buy-side advertising platforms together under one umbrella company. Direct Digital Holdings’ sell-side platform, Colossus SSP, offers advertisers of all sizes extensive reach within general market and multicultural media properties. The company’s subsidiaries Huddled Masses and Orange142 deliver significant ROI for middle market advertisers by providing data-optimized programmatic solutions at scale for businesses in sectors that range from energy to healthcare to travel to financial services. Direct Digital Holdings’ sell- and buy-side solutions manage over 100,000 clients monthly, generating over 100 billion impressions per month across display, CTV, in-app and other media channels. Direct Digital Holdings is the ninth black-owned company to go public in the U.S and was named a top minority-owned business by The Houston Business Journal.

Revision Reflects an Increase of Revenue at the Company’s Colossus SSP Subsidiary for FY 2022

Results in Full-Year Revenue of $89.4 Million, or EPS of $0.33

HOUSTON, April 17, 2023 /PRNewswire/ — Direct Digital Holdings, Inc. (Nasdaq: DRCT) (“Direct Digital Holdings” or the “Company”), a leading advertising and marketing technology platform operating through its companies Colossus Media, LLC (“Colossus SSP”), Huddled Masses LLC (“Huddled Masses”) and Orange142, LLC (“Orange142”), today announced an upward revision of the preliminary financial results originally published in its March 23, 2023 press release.

These financial results, which are reflected in the Company’s Annual Report on Form 10-K filed with the SEC today, resulted in an increase in revenues of $1.3 million over the previously published preliminary results, which increased net income to $4.2 million and increased EPS to $0.33 per share for the 12-month period ended December 31, 2022.

The updated amounts have no effect upon the cash flows for the affected periods, and will not affect forward revenue guidance for 2023 of $118 million to $122 million as issued on March 23, 2023.

About Direct Digital Holdings Direct Digital Holdings (Nasdaq: DRCT), owner of operating companies Colossus SSP, Huddled Masses, and Orange 142, brings state-of-the-art sell- and buy-side advertising platforms together under one umbrella company. Direct Digital Holdings’ sell-side platform, Colossus SSP, offers advertisers of all sizes extensive reach within general market and multicultural media properties. The company’s subsidiaries Huddled Masses and Orange142 deliver significant ROI for middle market advertisers by providing data-optimized programmatic solutions at scale for businesses in sectors that range from energy to healthcare to travel to financial services. Direct Digital Holdings’ sell- and buy-side solutions manage approximately 90,000 clients monthly, generating over 100 billion impressions per month across display, video, CTV, in-app and other media channels. Direct Digital Holdings is the ninth black-owned company to go public in the U.S and was named a top minority-owned business by The Houston Business Journal.

Forward Looking Statements This press release may contain forward-looking statements within the meaning of federal securities laws, including the Private Securities Litigation Reform Act of 1995, Section 27A of the Securities Act of 1933, as amended, and Section 21E of the Securities Exchange Act of 1934, as amended, and which are subject to certain risks, trends and uncertainties.

As used below, “we,” “us,” and “our” refer to the Company. We use words such as “could,” “would,” “may,” “might,” “will,” “expect,” “likely,” “believe,” “continue,” “anticipate,” “estimate,” “intend,” “plan,” “project” and other similar expressions to identify forward-looking statements, but not all forward-looking statements include these words. All statements contained in this press release that do not relate to matters of historical fact should be considered forward-looking statements.

All of our forward-looking statements involve estimates and uncertainties that could cause actual results to differ materially from those expressed in or implied by the forward-looking statements. Our forward-looking statements are based on assumptions that we have made in light of our industry experience and our perceptions of historical trends, current conditions, expected future developments and other factors we believe are appropriate under the circumstances. Although we believe that these forward-looking statements are based on reasonable assumptions, many factors could affect our actual operating and financial performance and cause our performance to differ materially from the performance expressed in or implied by the forward-looking statements, including, but not limited to: our dependence on the overall demand for advertising, which could be influenced by economic downturns; any slow-down or unanticipated development in the market for programmatic advertising campaigns; the effects of health epidemics; operational and performance issues with our platform, whether real or perceived, including a failure to respond to technological changes or to upgrade our technology systems; any significant inadvertent disclosure or breach of confidential and/or personal information we hold, or of the security of our or our customers’, suppliers’ or other partners’ computer systems; any unavailability or non-performance of the non-proprietary technology, software, products and services that we use; unfavorable publicity and negative public perception about our industry, particularly concerns regarding data privacy and security relating to our industry’s technology and practices, and any perceived failure to comply with laws and industry self-regulation; restrictions on the use of third-party “cookies,” mobile device IDs or other tracking technologies, which could diminish our platform’s effectiveness; any inability to compete in our intensely competitive market; any significant fluctuations caused by our high customer concentration; our limited operating history, which could result in our past results not being indicative of future operating performance; any violation of legal and regulatory requirements or any misconduct by our employees, subcontractors, agents or business partners; any strain on our resources, diversion of our management’s attention or impact on our ability to attract and retain qualified board members as a result of being a public company; our dependence, as a holding company, of receiving distributions from Direct Digital Holdings, LLC to pay our taxes, expenses and dividends; and other factors and assumptions discussed in the “Risk Factors,” “Management’s Discussion and Analysis of Financial Conditions and Results of Operations” and other sections of our filings with the Securities and Exchange Commission that we make from time to time. Should one or more of these risks or uncertainties materialize or should any of these assumptions prove to be incorrect, our actual operating and financial performance may vary in material respects from the performance projected in these forward-looking statements. Further, any forward-looking statement speaks only as of the date on which it is made, and except as required by law, we undertake no obligation to update any forward-looking statement contained in this Current Report on Form 8-K to reflect events or circumstances after the date on which it is made or to reflect the occurrence of anticipated or unanticipated events or circumstances, and we claim the protection of the safe harbor for forward-looking statements contained in the Private Securities Litigation Reform Act of 1995.

HOUSTON, TX / ACCESSWIRE / April 17, 2023 / Direct Digital Holdings, Inc (Nasdaq:DRCT) (“Direct Digital Holdings” or the “Company”) , a leading advertising and marketing technology platform operating through its companies Colossus Media, LLC (“Colossus SSP”), Huddled Masses LLC (“Huddled Masses”) and Orange142, LLC (“Orange142”), today announced that it will be presenting at the Planet MicroCap Showcase: VEGAS 2023 on Wednesday, April 26, 2023 at 2:30PM (Local Time – PST). President & Co-Founder of Direct Digital Holdings, Keith Smith, and Chief Financial Officer of Direct Digital Holdings, Susan Echard, will be hosting the presentation and answering questions at the conclusion. The Company will also be hosting 1×1 meetings on Thursday, April 27, 2023.

To access the live presentation, please use the following information:

Planet MicroCap Showcase: VEGAS 2023

Date: Wednesday, April 26, 2023

Time: 5:30 PM Eastern Time (2:30 PM Pacific Time)

Direct Digital Holdings continues to demonstrate robust financial performance, significant operational expansion and continued gains in market share as it capitalizes on strong macroeconomics tailwinds in digital advertising and media. The Company continues to implement strategic growth initiatives to position the Company to continue to deliver high-quality, technology-led digital advertising solutions to its expanding customer network. Direct Digital Holdings is the ninth black-owned company to go public in the U.S. and is pioneering the AdTech space as a leader in programmatic advertising leveraging its technology and strategy to focus on reaching consumers and publishers in mid-sized and multicultural markets. The Company recently released a whitepaper conducted by Horowitz research that garnered key insights into the importance on effectively engaging with diverse communities and media properties.

If you would like to book 1×1 investor meetings with Direct Digital Holdings, and to attend the Planet MicroCap Showcase: VEGAS 2023, please make sure you are registered here: https://planetmicrocapshowcase.com/signup

1×1 meetings will be scheduled and conducted in person at the conference venue in LAS VEGAS.

Direct Digital Holdings (Nasdaq: DRCT), owner of operating companies Colossus SSP, Huddled Masses, and Orange 142, brings state-of-the-art sell- and buy-side advertising platforms together under one umbrella company. Direct Digital Holdings’ sell-side platform, Colossus SSP, offers advertisers of all sizes extensive reach within general market and multicultural media properties. The company’s subsidiaries Huddled Masses and Orange142 deliver significant ROI for middle market advertisers by providing data-optimized programmatic solutions at scale for businesses in sectors that range from energy to healthcare to travel to financial services. Direct Digital Holdings’ sell- and buy-side solutions manage approximately 90,000 clients monthly, generating over 100 billion impressions per month across display, CTV, in-app and other media channels. Direct Digital Holdings is the ninth black-owned company to go public in the U.S and was named a top minority-owned business by The Houston Business Journal.

About Planet MicroCap

Planet MicroCap is a global multimedia financial news, publishing and events company focused on news dissemination, providing information, data and analytics for the MicroCap investing community. We have cultivated an active and engaged audience of folks that are interested in learning about and to stay ahead of the curve in the MicroCap space.

Elon Musk Announces New Financial Functionality on Twitter

Starting today, Twitter will provide tweeters the ability to buy and sell stocks and crypto on its platform via eTORO. Twitter owner, Elon Musk has been indicating he intends to turn the popular micro-blogging platform into a “super app.” Today’s move shows substantial headway in allowing financial transactions to be conducted on the social media platform. Other company goals since Musk’s purchase of the company include ride hailing, and attracting video influencers that may be disenchanted with YouTube restrictions on speech.

What Will the Twitter eTORO Partnership Provide?

Founded in 2007, eTORO has become one of the largest social investment networks and trading platforms. According to its website, it is “built on social collaboration and investor education: a community where users can connect, share, and learn.”

Twitter will partner with the platform to allow users (known as tweeters and Twitterers) to trade stocks and cryptocurrencies as part of a deal with the social investing company.

This partnership will provide access to view charts and trade stocks, cryptocurrencies, and other investment assets from eToro via its mobile platform. Together this significantly expands real-time trading data available to users who already have access on Twitter to real-time data, however this arrangement adds all the bells and whistles a modern trading app can provide.

Twitter will be expanding its use of cashtags as well. Twitter added pricing data for $Cashtags (company ticker preceded by “$”) in December 2022. Since January, there have been more than 420 million searches using Cashtags – the number of searches averages 4.7 million a day.

eToro CEO Yoni Assia told CNBC the deal will help better connect the two brands, adding that in recent years its users have increasingly turned to Twitter to “educate themselves about the markets.”

Assia said there is a great deal of “very high quality” content available in real-time and that the partnership with Twitter will help eToro expand to reach new audiences tapping this as a source of information.

Update on Elon

After Musk’s purchase of Twitter, many advertisers stepped back and watched to see how far the company would go to allow less moderated interaction. On Wednesday (April 12) Musk said that “almost all” advertisers had returned to the app. However, Stellantis and Volkswagen, two large competitors with Musk run Tesla, said they do not yet plan to resume advertising.

Musk told a Morgan Stanley conference last month he wants Twitter to become “the biggest financial institution in the world.” This begs those that follow Musk to ask, “Why stop there, why not include Mars?”

What Else

Be sure to follow Channelchek on Twitter (@channelchek) to stay up to date on market insights, news, videos, and of course, top-tier investment analyst research on small and microcap opportunities.