Beasley Broadcast Group, Inc. owns and operates 61 stations (47 FM and 14 AM) in 15 large- and mid-size markets in the United States. Approximately 20 million consumers listen to the Company’s radio stations weekly over-the-air, online and on smartphones and tablets, and millions regularly engage with the Company’s brands and personalities through digital platforms such as Facebook, Twitter, text messaging, digital and web applications and email. The Overwatch League’s Houston Outlaws esports team is a wholly owned subsidiary. The Company also owns BeasleyXP, a national esports content hub, and AXLR-R8, a Rocket League Championship Series team, in its esports portfolio. For more information, please visit www.bbgi.com.

Michael Kupinski, Director of Research, Equity Research Analyst, Digital, Media & Technology , Noble Capital Markets, Inc.

Jacob Mutchler, Research Associate, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

Solid Q2 results. The company reported revenue of $63.5 million, in-line with our estimate of $63.7 million. Adj. EBITDA of $7.7 million, beat our estimate of $6.5 million by 18.2%. Notably, the quarter was driven by strong digital revenue growth of14.8% and cash flow was supported by meaningful cost reductions and permanently reduced headcount.

Strong digital growth. The bulk of digital revenue growth in the quarter came from high margin content creation on the company’s owned and operated platforms. Importantly, Q2 digital accounted for 19.4% of total revenue, only slightly below management’s target of 20% to 30% for full year 2023.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

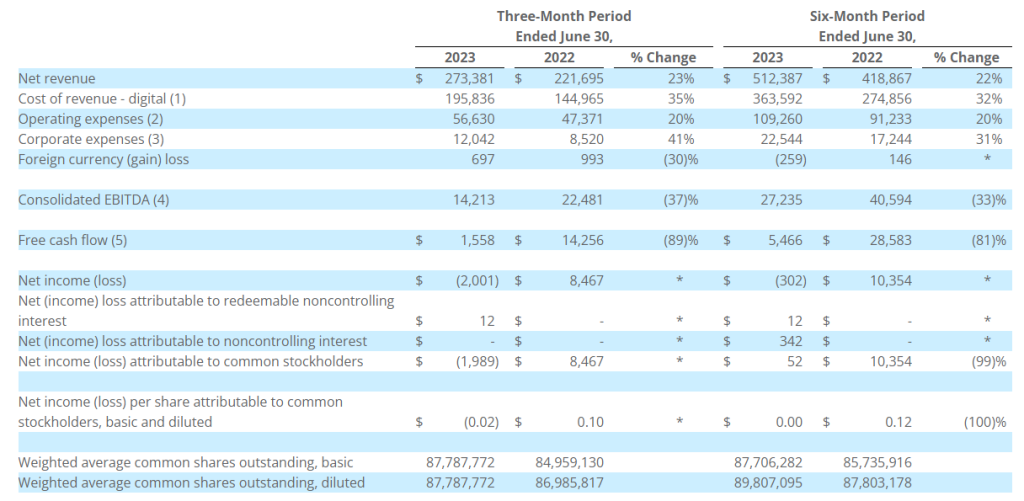

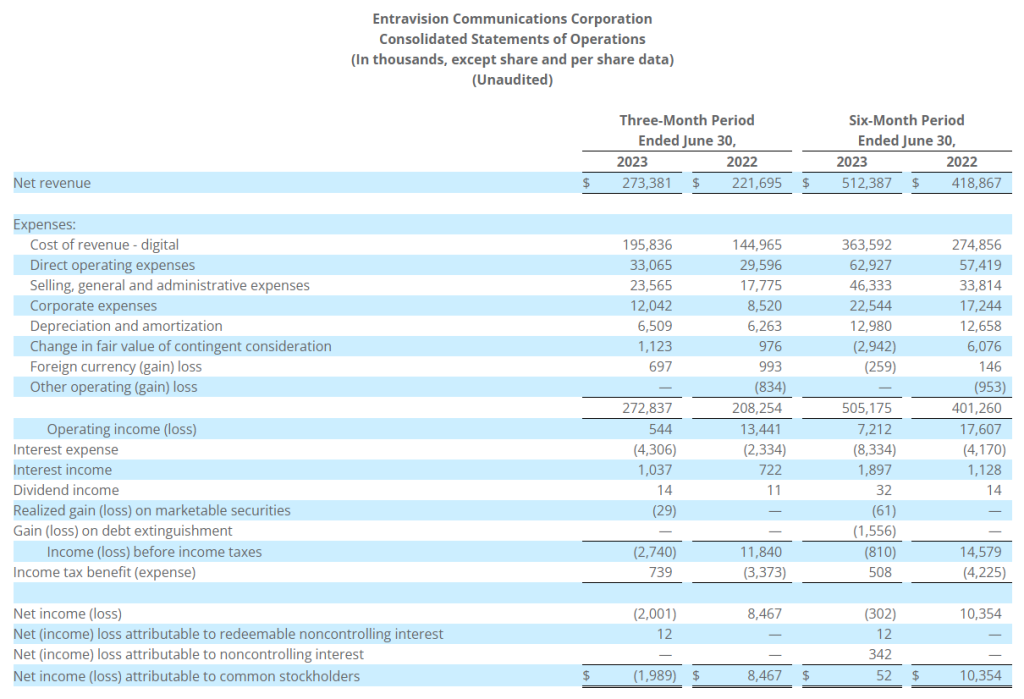

SANTA MONICA, Calif.–(BUSINESS WIRE)– Entravision Communications Corporation (NYSE: EVC), a leading global advertising solutions, media and technology company, today announced financial results for the three- and six-month periods ended June 30, 2023.

Second Quarter 2023 Highlights

Record quarterly advertising revenue

Net revenue up 23% over the prior-year quarter

Net loss attributable to common stockholders of $2.0 million compared to net income attributable to common stockholders of $8.5 million in the prior-year quarter

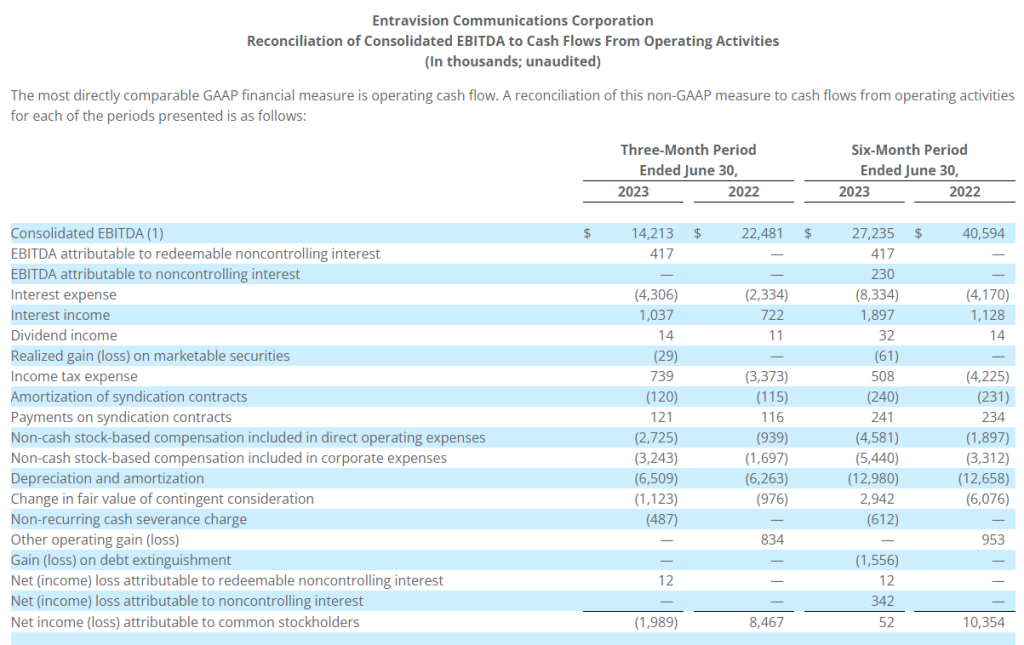

Consolidated EBITDA down 37% compared to the prior-year quarter

Operating cash flow up 7% over the prior-year quarter

Free cash flow down 89% compared to the prior-year quarter

Quarterly cash dividend of $0.05 per share

“We delivered another strong quarter at Entravision with record quarterly revenue of $273.4 million, increasing 23% year-over-year,” said Chris Young, Chief Financial Officer. “While elevated operating expenses led to a decline in adjusted EBITDA, we remain focused on managing expenses and leveraging our strong balance sheet to ensure we are well-positioned to grow in the current macroeconomic environment. We were also excited to welcome Michael Christenson as our new CEO at the beginning of July. We look forward to continuing to drive growth under his leadership.”

Quarterly Cash Dividend

The Company announced today that its Board of Directors approved a quarterly cash dividend to shareholders of $0.05 per share on the Company’s Class A and Class U common stock, in an aggregate amount of $4.4 million. The quarterly dividend will be payable on September 29, 2023 to shareholders of record as of the close of business on September 15, 2023, and the common stock will trade ex-dividend on September 14, 2023. The Company currently anticipates that future cash dividends will be paid on a quarterly basis; however, any decision to pay future cash dividends will be subject to approval by the Board.

Non-GAAP Financial Measures

This press release contains certain non-GAAP financial measures as defined by SEC Regulation G. The GAAP financial measure most directly comparable to each of these non-GAAP financial measures, and a table reconciling each of these non-GAAP financial measures to its most directly comparable GAAP financial measure is included beginning on page 10.

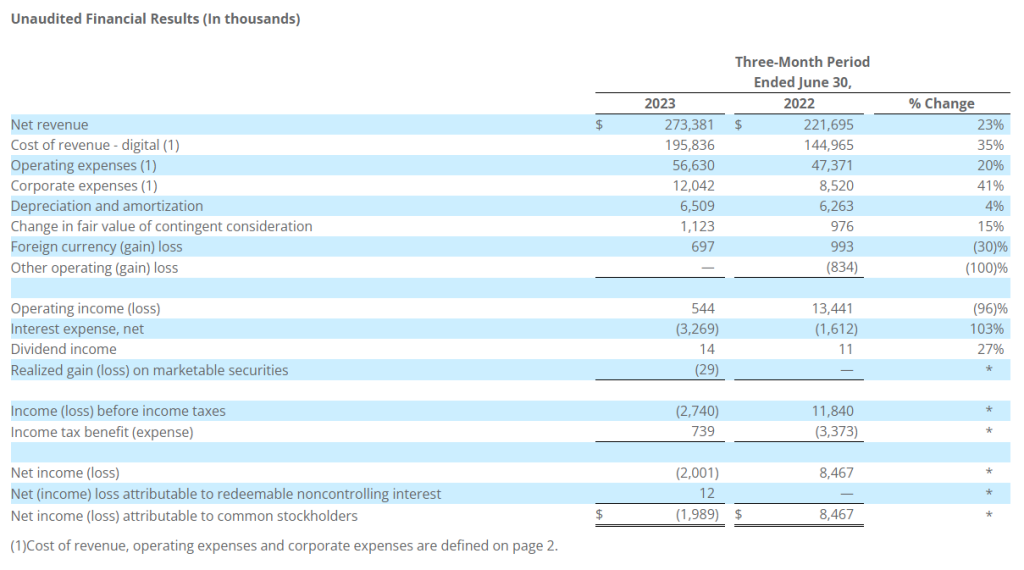

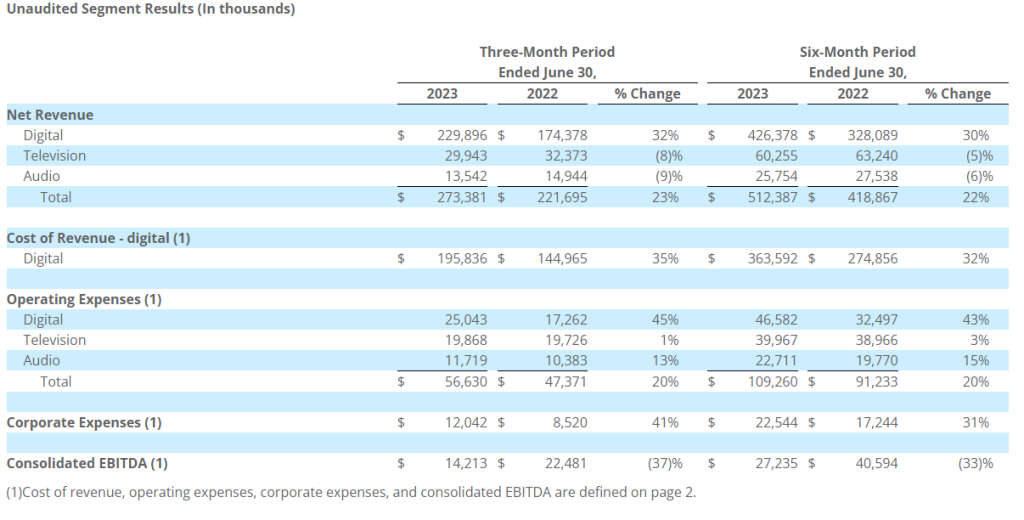

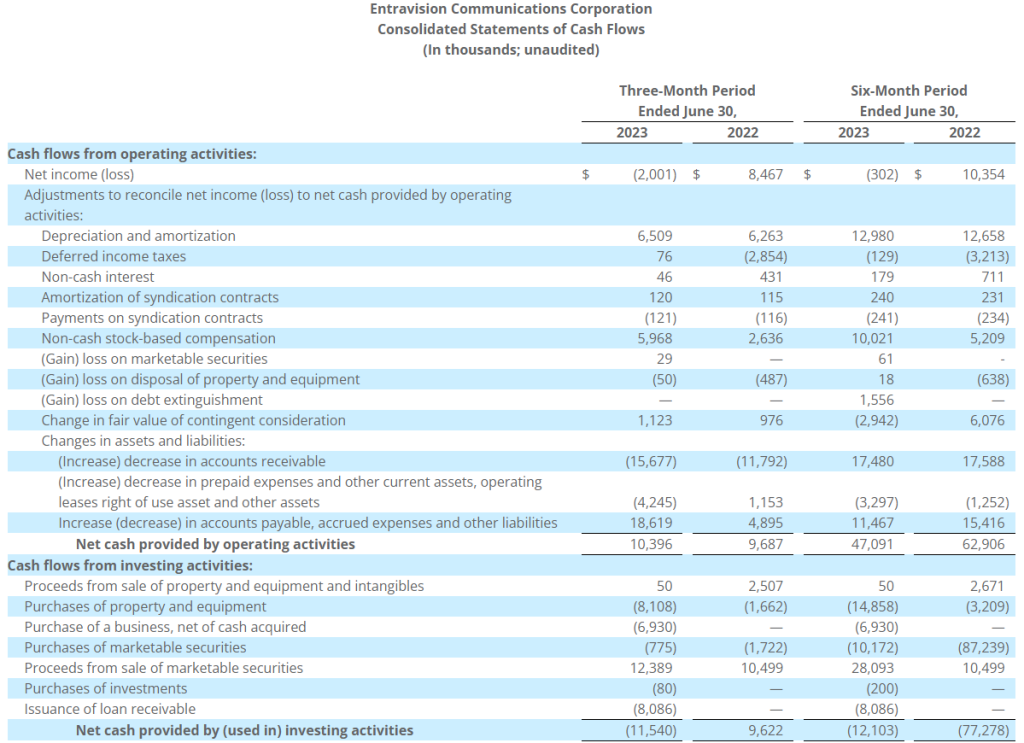

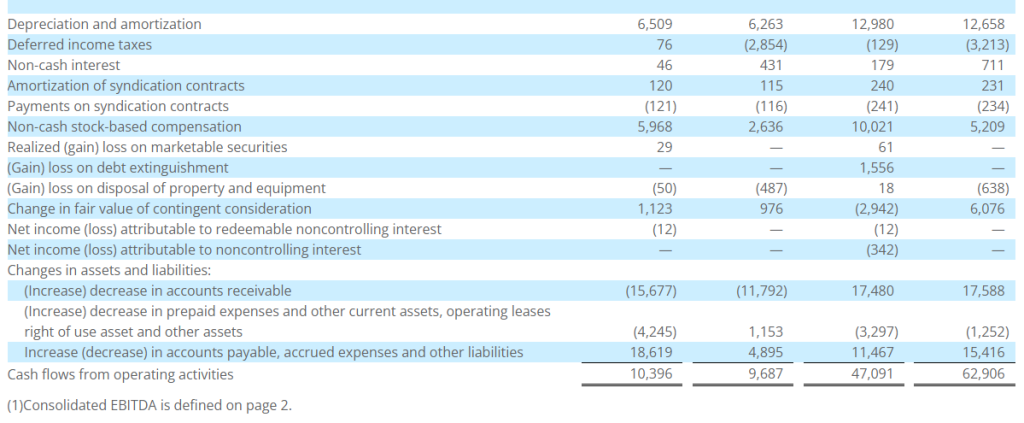

Net revenue in the second quarter of 2023 totaled $273.4 million, up 23% from $221.7 million in the prior-year period. Of the overall increase, $55.5 million was attributable to our digital segment and was primarily due to advertising revenue growth from our digital commercial partnerships business, and due to various acquisitions, which did not contribute to our financial results in our digital segment in the comparable period. The overall increase was partially offset by a decrease of $2.5 million attributable to our television segment, primarily due to decreases in political advertising revenue and national advertising revenue, partially offset by increases in local advertising revenue, spectrum usage rights revenue and retransmission consent revenue. In addition, the overall increase was partially offset by a decrease of $1.4 million attributable to our audio segment, primarily due to a decrease in political advertising revenue, and decreases in local and national advertising revenue.

Cost of revenue in the second quarter of 2023 totaled $195.8 million, up 35% from $145.0 million in the prior-year period. The increase was primarily due to increased cost of revenue related to advertising revenue growth from our digital commercial partnerships business, and due to various acquisitions, which did not contribute to our financial results in our digital segment in the comparable period.

Operating expenses in the second quarter of 2023 totaled $56.6 million, up 20% from $47.4 million in the prior-year period. Of the overall increase, $7.8 million was attributable to our digital segment and was primarily due to an increase in non-cash stock-based compensation, which is mainly a result of the timing of the 2023 annual restricted stock unit (“RSU”) grant to certain employees, which was made in February 2023 compared to the 2022 annual grant, which was made in December 2022, and due to an increase in expenses associated with the increase in digital advertising revenue, an increase in salary expense, and due to various acquisitions, which did not contribute to our financial results in our digital segment in the comparable period. Additionally, of the overall increase in operating expenses, $0.1 million was attributable to our television segment primarily due to an increase in non-cash stock-based compensation, which is mainly a result of the 2023 annual RSU grant timing mentioned above, partially offset by a decrease in bad debt expense. In addition, of the overall increase in operating expenses, $1.3 million was attributable to our audio segment primarily due to an increase in non-cash stock-based compensation, which is mainly a result of the 2023 annual RSU grant timing mentioned above, and due to an increase in salaries and increased rent expense in the temporary office space until the move to our new permanent offices, which was completed in June 2023.

Corporate expenses in the second quarter of 2023 totaled $12.0 million, up 41% from $8.5 million in the prior-year period. The increase was primarily due to an increase in non-cash stock-based compensation, which is mainly a result of the 2023 annual RSU grant timing mentioned above, and increases in professional service fees.

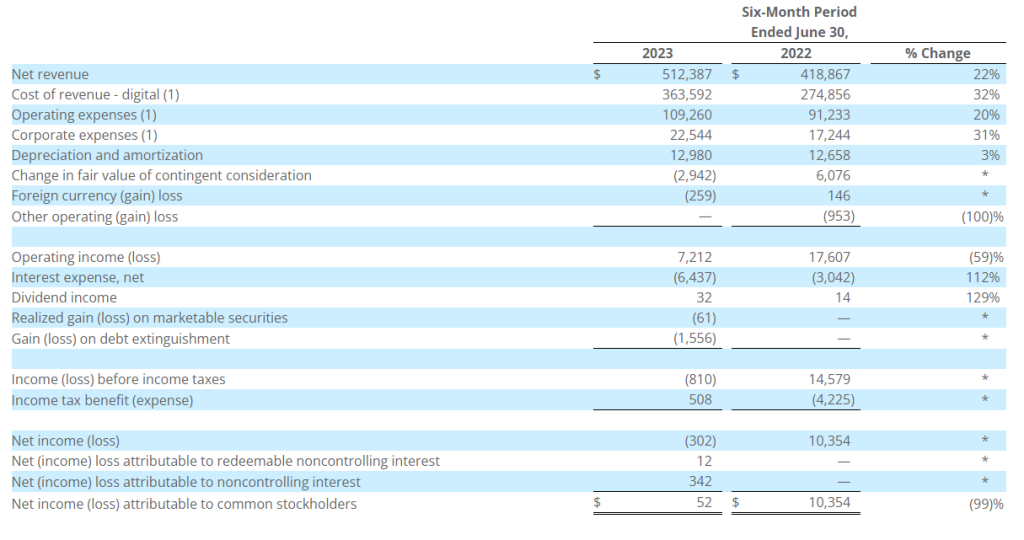

Net revenue for the six-month period of 2023 totaled $512.4 million, up 22% from $418.9 million in the prior-year period. Of the overall increase, $98.3 million was attributable to our digital segment and was primarily due to advertising revenue growth from our digital commercial partnerships business, and due to various acquisitions, which did not contribute to our financial results in our digital segment in the comparable period. The overall increase was partially offset by a decrease of $2.9 million attributable to our television segment, primarily due to decreases in political advertising revenue and national advertising revenue, partially offset by increases in local advertising revenue, spectrum usage rights revenue and retransmission consent revenue. In addition, the overall increase was partially offset by a decrease of $1.7 million attributable to our audio segment, primarily due to a decrease in political advertising revenue, and decreases in local and national advertising revenue.

Cost of revenue for the six-month period of 2023 totaled $363.6 million, up 32% from $274.9 million in the prior-year period. The increase was primarily due to increased cost of revenue related to advertising revenue growth from our digital commercial partnerships business, and due to various acquisitions, which did not contribute to our financial results in our digital segment in the comparable period.

Operating expenses for the six-month period of 2023 totaled $109.3 million, up 20% from $91.2 million in the prior-year period. Of the overall increase, $14.1 million was attributable to our digital segment and was primarily due to an increase in non-cash stock-based compensation, which is mainly a result of the 2023 annual RSU grant timing mentioned above, and due to an increase in expenses associated with the increase in digital advertising revenue, an increase in salary expense, and due to various acquisitions, which did not contribute to our financial results in our digital segment in the comparable period. Additionally, of the overall increase in operating expenses, $1.0 million was attributable to our television segment primarily due to an increase in non-cash stock-based compensation, which is mainly a result of the 2023 annual RSU grant timing mentioned above. In addition, of the overall increase in operating expenses, $2.9 million was attributable to our audio segment primarily due to an increase in non-cash stock-based compensation, which is mainly a result of the 2023 annual RSU grant timing mentioned above, and due to an increase in salaries and increased rent expense in the temporary office space until the move to our new permanent offices, which was completed in June 2023.

Corporate expenses for the six-month period of 2023 totaled $22.5 million, up 31% from $17.2 million in the prior-year period. The increase was primarily due to an increase in non-cash stock-based compensation, which is mainly a result of the 2023 annual RSU grant timing mentioned above, and increases in professional service fees, audit fees and rent expense.

Balance Sheet and Related Metrics

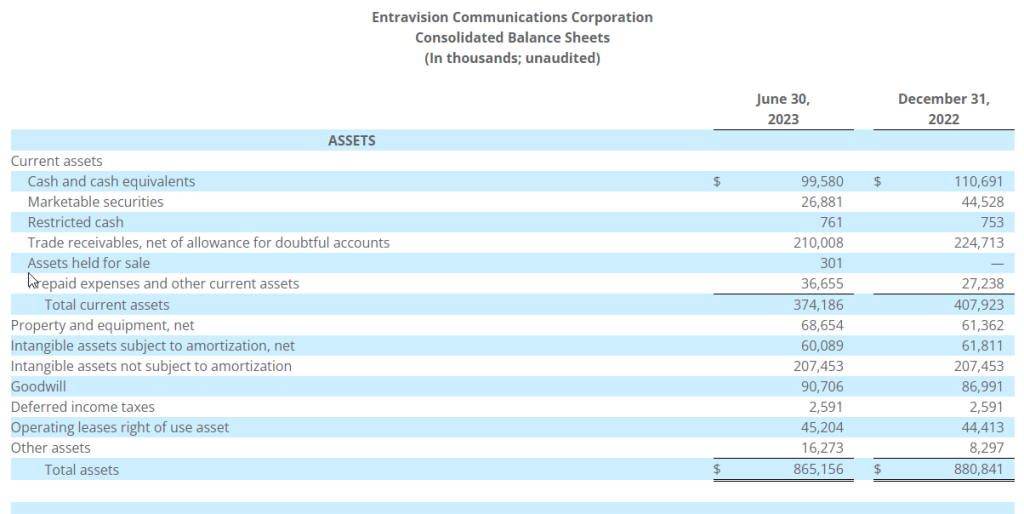

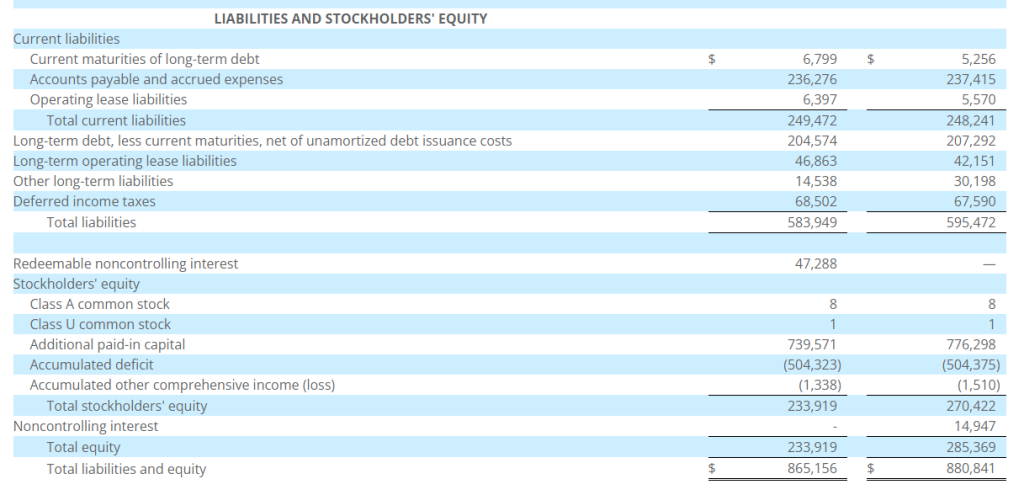

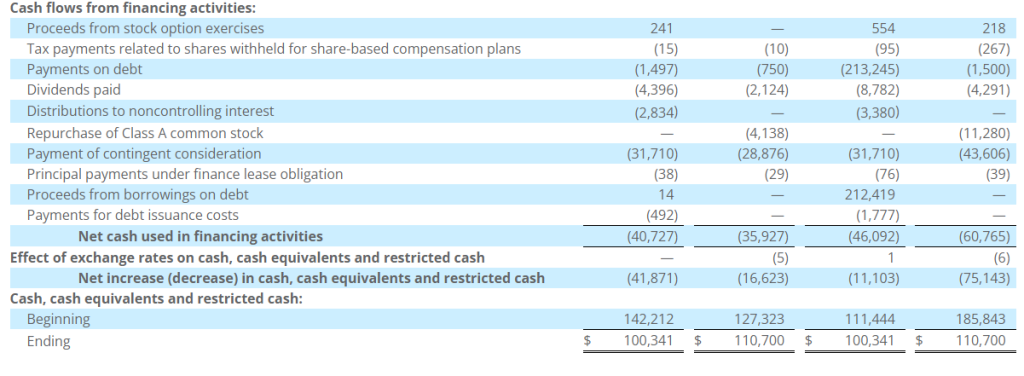

Cash and marketable securities as of June 30, 2023 totaled $126.5 million. Total debt under the Company’s credit agreement was $210.3 million. Net of $50 million of cash and marketable securities, total leverage as defined in the Company’s credit agreement was 1.8 times as of June 30, 2023. Net of total cash and marketable securities, total leverage was 1.0 times.

Notice of Conference Call

Entravision Communications Corporation will hold a conference call to discuss its second quarter 2023 results on Thursday, August 3, 2023 at 5:00 p.m. Eastern Time. To access the conference call, please dial (844) 836-8739 (U.S.) or (412) 317-5440 (Int’l) ten minutes prior to the start time and reference Conference ID number 10180063. The call will also be available via live webcast on the investor relations portion of the Company’s website located at www.entravision.com.

About Entravision Communications Corporation

Entravision is a global advertising solutions, media and technology company. Over the past three decades, we have strategically evolved into a digital powerhouse, expertly connecting brands to consumers in the U.S., Latin America, Europe, Asia and Africa. Our digital segment, the company’s largest by revenue, offers a full suite of end-to-end advertising services in 40 countries. We have commercial partnerships with Meta, X Corp. (formerly known as Twitter), TikTok, and Spotify, and marketers can use our Smadex and other platforms to deliver targeted advertising to audiences around the globe. In the U.S., we maintain a diversified portfolio of television and radio stations that target Hispanic audiences and complement our global digital services. Entravision remains the largest affiliate group of the Univision and UniMás television networks. Shares of Entravision Class A Common Stock trade on the NYSE under ticker: EVC. Learn more about our offerings at entravision.com or connect with us on LinkedIn and Facebook.

Forward-Looking Statements

This press release contains certain forward-looking statements. These forward-looking statements, which are included in accordance with the safe harbor provisions of the Private Securities Litigation Reform Act of 1995, may involve known and unknown risks, uncertainties and other factors that may cause the Company’s actual results and performance in future periods to be materially different from any future results or performance suggested by the forward-looking statements in this press release. Although the Company believes the expectations reflected in such forward-looking statements are based upon reasonable assumptions, it can give no assurance that actual results will not differ materially from these expectations, and the Company disclaims any duty to update any forward-looking statements made by the Company. From time to time, these risks, uncertainties and other factors are discussed in the Company’s filings with the Securities and Exchange Commission.

Christopher T. Young Chief Financial Officer and Treasurer Entravision Communications Corporation 310-447-3870

Michael Kupinski, Director of Research, Equity Research Analyst, Digital, Media & Technology , Noble Capital Markets, Inc.

Patrick McCann, CFA, Research Analyst, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

Upcoming quarterly results. The company is expected to report second quarter results on Thursday, August 10th with an investor call scheduled for 5pm ET. The dial in number is (888) 350-2056.

Mixed results. We believe that the company will be in line with our revenue estimate of $29.65 million, up 39.5%, reflecting modest Buy-side advertising growth of 3.5% and strong Sell-side advertising growth of roughly 67%. Sell-side margins are expected to decline to roughly 12.5%, due to a step up in costs for additional servers. We do not believe that the increase costs will be ongoing and that Sell-side margins should rebound to the near 14% range for the balance of the year.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

IRVING, Texas–(BUSINESS WIRE)– Salem Media Group, Inc. (NASDAQ: SALM) announced today that it plans to report its second quarter 2023 financial results after the market closes on August 8, 2023.

The company also plans to host a teleconference to discuss its results on August 8, 2023, at 4:00 PM Central Time. To access the teleconference, please dial (888) 770-7291, and then ask to be joined to the Salem Media Group Second Quarter 2023 call or listen to the webcast.

A replay of the teleconference will be available through August 22, 2023, and can be heard by dialing (800) 770-2030 – replay pin number 2413416, or on the investor relations portion of the company’s website, located at investor.salemmedia.com.

ABOUT SALEM MEDIA GROUP:

Salem Media Group is America’s leading multimedia company specializing in Christian and conservative content, with media properties comprising radio, digital media and book and newsletter publishing. Each day Salem serves a loyal and dedicated audience of listeners and readers numbering in the millions nationally. With its unique programming focus, Salem provides compelling content, fresh commentary and relevant information from some of the most respected figures across the Christian and conservative media landscape. Learn more about Salem Media Group, Inc. at www.salemmedia.com, Facebook and Twitter.

Snail is a leading, global independent developer and publisher of interactive digital entertainment for consumers around the world, with a premier portfolio of premium games designed for use on a variety of platforms, including consoles, PCs and mobile devices.

Michael Kupinski, Director of Research, Equity Research Analyst, Digital, Media & Technology , Noble Capital Markets, Inc.

Patrick McCann, CFA, Research Analyst, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

Multi-year server hosting agreement. The company disclosed a new agreement with Marbis GmbH, owner of Nitrado servers. As part of the agreement, Marbis will become the exclusive server provider for Snail’s ARK games for 7 years. In return, Marbis will make a $4.05 million interest-free loan commitment to Snail, which will serve as a bridge loan as the company builds toward positive cash flow generation.

Favorable terms. As part of the agreement, Snail will be required to repay the loan with a 20% share of all monthly gross revenue from the release of its upcoming title, ARK: Survival Ascended, until the loan balance has been repaid in full. We expect any outstanding balance to be repaid very quickly upon the game’s release in Q4.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

Saga Communications, Inc. is a broadcast company whose business is primarily devoted to acquiring, developing and operating radio stations, television stations and state radio networks. Saga currently owns or operates broadcast properties in 26 markets, including 61 FM and 30 AM radio stations, 3 state radio networks, 2 farm radio networks, 5 television stations and 4 low power television stations. Saga’s strategy is to operate top billing radio and television stations in mid sized markets, defined as markets ranked (by market revenues) from 20 to 200. Saga’s radio stations employ a myriad of programming formats, including Classic Hits, Adult Contemporary, Active Rock, Oldies, News/Talk, Country and Classical. Saga’s television stations are affiliated with CBS and Fox in Joplin, MO; CBS in Greenville, MS; ABC, Fox, NBC, Telemundo and Univision in Victoria, TX. In operating its stations, Saga concentrates on the development of strong decentralized local management, which is responsible for the day-to-day operations of the stations in their market area and is compensated based on their financial performance as well as other performance factors that are deemed to effect the long-term ability of the stations to achieve financial objectives. Saga began operations in 1986 and became a publicly traded company in December 1992. The stock trades on the NYSE Amex under the ticker symbol “SGA”.

Michael Kupinski, Director of Research, Equity Research Analyst, Digital, Media & Technology , Noble Capital Markets, Inc.

Jacob Mutchler, Research Associate, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

Non-deal Roadshow highlights. On July 27, Chris Forgy, CEO, and Sam Bush, CFO, hosted investor meetings in St. Louis. We believe that the management team was sanguine about favorable revenue and cash flow growth prospects. This report highlights the company’s resilient local radio operations, strong balance sheet and emergent digital revenues.

Strong local presence. The company operates primarily in small and midsize markets outside the top 50. We believe its highly localized footprint provides more revenue stability relative to its nationally focused peers. Additionally, we believe its strong local relationships will assist in accelerating digital revenue growth. Notably, management highlighted its commitment to local audiences, given its ethos is grounded in localism.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

Travelzoo® provides its 30 million members with exclusive offers and one-of-a-kind experiences personally reviewed by our deal experts around the globe. We have our finger on the pulse of outstanding travel, entertainment, and lifestyle experiences. We work in partnership with more than 5,000 top travel suppliers—our long-standing relationships give Travelzoo members access to irresistible deals.

Michael Kupinski, Director of Research, Equity Research Analyst, Digital, Media & Technology , Noble Capital Markets, Inc.

Patrick McCann, CFA, Research Analyst, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

Solid Q2 results. The company reported better than expected revenue and adj. EBITDA in Q2. Revenue was $21.1 million and adj. EBITDA was $4.2 million, compared with our estimates of $20.5 million and $3.4 million, respectively. Revenue growth accelerated to 19% in Q2, compared with 17% growth in Q1.

Strong margins. Adj. EBITDA margins were up to nearly 20%, due in large part to 27% operating profit margins in the North America business segment. Operating profit in Europe, though, still negative, improved to nearly flat (-3%).

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

SANTA MONICA, Calif.–(BUSINESS WIRE)– Entravision (NYSE: EVC), a leading global advertising solutions, media and technology company, announced that it will release its second quarter 2023 financial results after market close on Thursday, August 3, 2023. The Company will host a conference call that day at 5:00 p.m. Eastern Time to discuss the second quarter 2023 results.

To access the conference call, please dial (844) 836-8739 (U.S.) or (412) 317-5440 (International) ten minutes prior to the start time. The call will also be available via live webcast on the investor relations portion of the Company’s website located at www.entravision.com.

If you cannot listen to the conference call at its scheduled time, there will be a replay available through Thursday, August 17, 2023, which can be accessed by dialing (844) 512-2921 (U.S.) or (412) 317-6671 (International) and entering the passcode 10180063. The webcast will also be archived on the Company’s website.

About Entravision

Entravision is a global advertising solutions, media and technology company. Over the past three decades, we have strategically evolved into a digital powerhouse, expertly connecting brands to consumers in the U.S., Latin America, Europe, Asia and Africa. Our digital segment, the company’s largest by revenue, offers a full suite of end-to-end advertising services in 40 countries. We have commercial partnerships with Meta, Twitter, TikTok and Spotify, and marketers can use our Smadex and other platforms to deliver targeted advertising to audiences around the globe. In the U.S., we maintain a diversified portfolio of television and radio stations that target Hispanic audiences and complement our global digital services. Entravision remains the largest affiliate group of the Univision and UniMás television networks. Shares of Entravision Class A Common Stock trade on the NYSE under ticker: EVC. Learn more about our offerings at entravision.com or connect with us on LinkedIn and Facebook.

Christopher T. Young Chief Financial Officer Entravision 310-447-3870

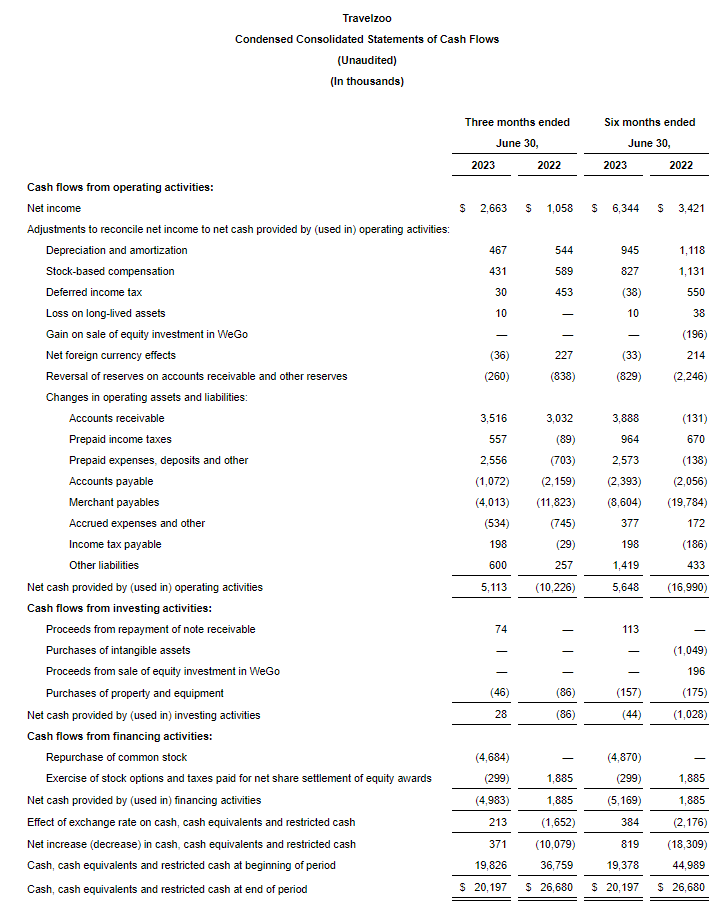

NEW YORK, July 27, 2023 /PRNewswire/ — Travelzoo® (NASDAQ: TZOO):

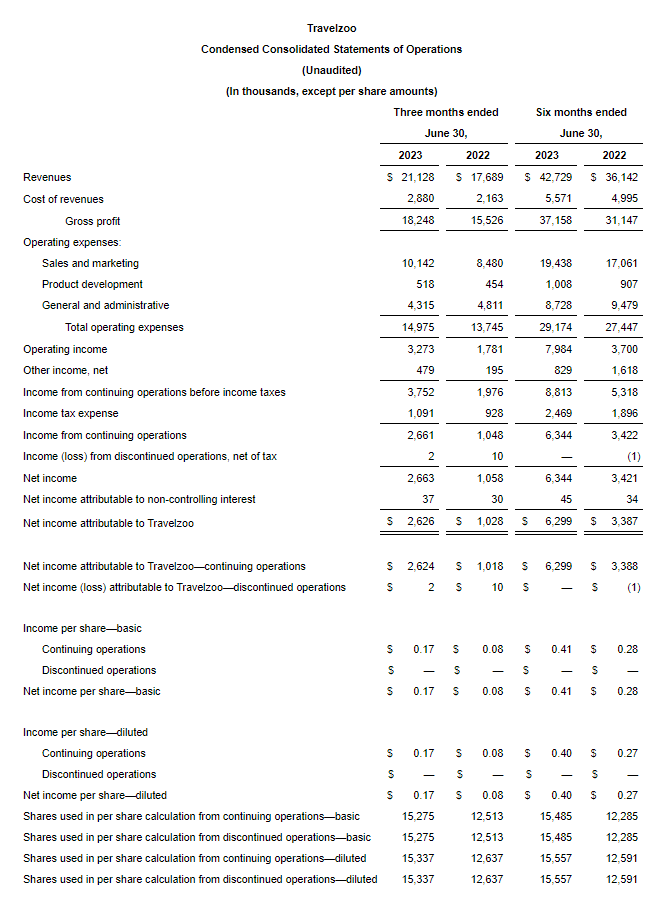

Revenue of $21.1 million, up 19% year-over-year

Consolidated operating profit of $3.3 million

Non-GAAP consolidated operating profit of $4.2 million

Cash flow from operations of $5.1 million

Earnings per share (EPS) of $0.17

Travelzoo, a global Internet media company that provides exclusive offers and experiences for members, today announced financial results for the Second quarter ended June 30, 2023. Consolidated revenue was $21.1 million, up 19% from $17.7 million year-over-year. In constant currencies, revenue was $21.2 million, up 20% year-over-year. Travelzoo’s reported revenue consists of advertising revenues and commissions, derived from and generated in connection with purchases made by Travelzoo members.

The reported net income attributable to Travelzoo from continuing operations was $2.6 million for Q2 2023. At the consolidated level, including minority interests, the reported net income from continuing operations was $2.7 million. EPS from continuing operations was $0.17, compared to $0.08 in the prior-year period.

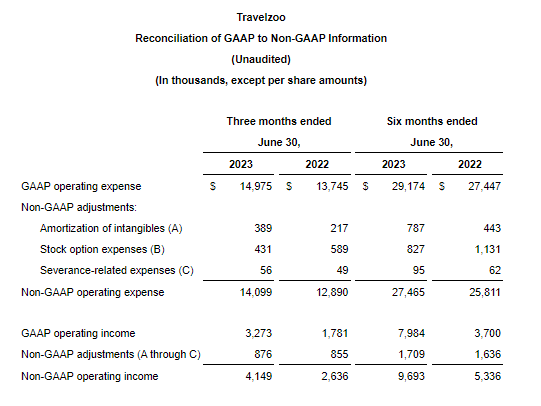

Non-GAAP operating profit was $4.2 million. The calculation of non-GAAP operating profit excludes amortization of intangibles ($0.4 million), stock option expenses ($0.4 million) and severance-related expenses ($56,000). See section “Non-GAAP Financial Measures” below.

“Year-over-year revenue growth accelerated from Q1 to Q2,” said Holger Bartel, Travelzoo’s Global CEO. “We will continue to leverage Travelzoo’s global reach, trusted brand, and strong relationships with top travel suppliers to negotiate more exclusive offers for Travelzoo members. With more than 30 million members, 8 million mobile app users, and 4 million social media followers, Travelzoo is loved by travel enthusiasts who are affluent, active, and open to new experiences.”

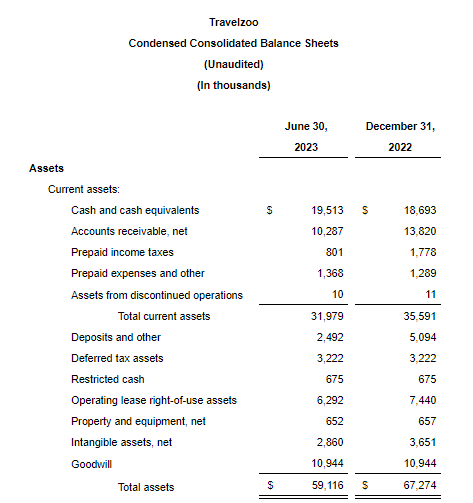

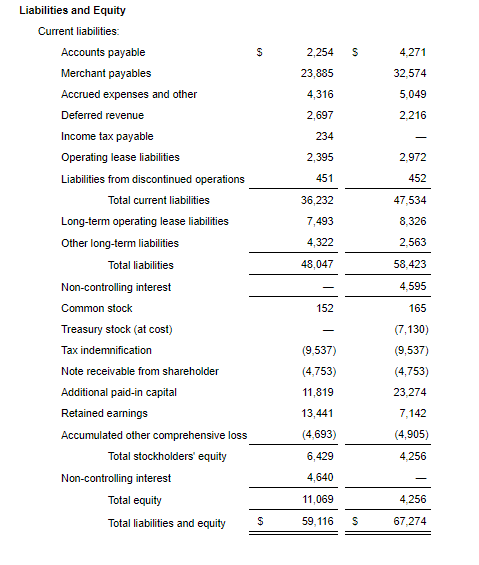

Cash Position

As of June 30, 2023, consolidated cash, cash equivalents and restricted cash were $20.2 million. Net cash provided by operations was $5.1 million.

Travelzoo North America

North America business segment revenue increased 14% year-over-year to $14.1 million. Operating profit for Q2 2023 was $3.8 million, or 27% of revenue, compared to an operating profit of $3.3 million in the prior-year period.

Travelzoo Europe

Europe business segment revenue increased 35% year-over-year to $5.9 million. At constant currencies, Europe business segment revenue increased 36% year-over-year. Operating loss for Q2 2023 was $239,000, compared to an operating loss of $1.5 million in the prior-year period.

Jack’s Flight Club

Jack’s Flight Club business segment revenue increased 15% year-over-year to $1.1 million. Jack’s Flight Club is a membership subscription service in which Travelzoo has a 60% ownership interest. The number of premium subscribers increased 30% year-over-year. Revenue from increases in subscribers is reported with a lag because we recognize revenue from subscriptions monthly pro rata over the subscription period (quarterly, semi-annually, annually). Operating profit for Q2 2023 was $97,000, compared to an operating profit of $161,000 in the prior-year period. Non-GAAP operating profit for Q2 2023 was $255,000. Non-GAAP operating profit excludes amortization of intangibles ($0.2 million) related to the acquisition.

New Initiatives

New Initiatives business segment revenue, which includes Licensing and Travelzoo META, was $13,000. Operating loss for Q2 2023 was $338,000.

In June 2020, Travelzoo entered into a royalty-bearing licensing agreement with a local licensee in Japan for the exclusive use of Travelzoo’s brand, business model, and members in Japan. In August of 2020, Travelzoo entered into a royalty-bearing licensing agreement with a local licensee in Australia for the exclusive use of Travelzoo’s brand, business models, and members in Australia, New Zealand, and Singapore. Under these arrangements, Travelzoo’s existing members in Australia, Japan, New Zealand, and Singapore will continue to be owned by Travelzoo as the licensor. Licensing revenue is booked with a lag of one quarter. Travelzoo recorded $4,000 in licensing revenue from the licensee in Japan in Q2 2023. Travelzoo recorded $9,000 in licensing revenue from the licensee in Australia, New Zealand, and Singapore in Q2 2023. Licensing revenue is expected to increase going forward.

Members and Subscribers

As of June 30, 2023, we had 30.8 million members worldwide. In North America, the unduplicated number of Travelzoo members was 16.2 million as of June 30, 2023, down 2% from June 30, 2022. In Europe, the unduplicated number of Travelzoo members was 9.2 million as of June 30, 2023, up 1% from June 30, 2022. Jack’s Flight Club had 2.2 million subscribers as of June 30, 2023, up 22% from June 30, 2022.

Discontinued Operations

As announced in a press release on March 10, 2020, Travelzoo decided to exit its Asia Pacific business and operate it as a licensing business going forward. Consequently, the Asia Pacific business has been classified as discontinued operations since March 31, 2020. Prior periods have been reclassified to conform with the current presentation. Certain reclassifications have been made for current and prior periods between the continued operations and the discontinued operations in accordance with U.S. GAAP.

Income Taxes

A provision of $1.1 million for income taxes was recorded for Q2 2023, compared to an income tax expense of $928,000 in the prior-year period. The provision for Q2 2023 does not reflect the expected utilization of NOLs by Travelzoo in the U.S.

Non-GAAP Financial Measures

Management calculates non-GAAP operating income when evaluating the financial performance of the business. Travelzoo’s calculation of non-GAAP operating income, also called “non-GAAP operating profit” in this press release and today’s earnings conference call, excludes the following items: amortization of intangibles, stock option expenses, and severance-related expenses. This press release includes a table which reconciles GAAP operating income to the calculation of non-GAAP operating income. Non-GAAP operating income is not required by, or presented in accordance with, generally accepted accounting principles in the United States of America (“GAAP”). This information should be considered as supplemental in nature and should not be considered in isolation or as a substitute for the financial information prepared in accordance with GAAP. In addition, these non-GAAP financial measures may not be the same as similarly titled measures reported by other companies.

Looking Ahead

For Q3 2023, we currently expect growth in revenue and growth in operating profit to continue year-over-year. During the pandemic, we have been able to lower our fixed costs. We believe we can keep our fixed costs relatively low in the foreseeable future.

download the management presentation (PDF format) to be discussed in the conference call

access the webcast.

About Travelzoo

Travelzoo® provides its 30 million members with exclusive offers and one-of-a-kind experiences personally reviewed by our deal experts around the globe. We have our finger on the pulse of outstanding travel, entertainment, and lifestyle experiences. We work in partnership with more than 5,000 top travel suppliers—our long-standing relationships give Travelzoo members access to irresistible deals.

Certain statements contained in this press release that are not historical facts may be forward-looking statements within the meaning of Section 27A of the Securities Act of 1933 and Section 21E of the Securities and Exchange Act of 1934. These forward-looking statements may include, but are not limited to, statements about our plans, objectives, expectations, prospects and intentions, markets in which we participate and other statements contained in this press release that are not historical facts. When used in this press release, the words “expect”, “predict”, “project”, “anticipate”, “believe”, “estimate”, “intend”, “plan”, “seek” and similar expressions are generally intended to identify forward-looking statements. Because these forward-looking statements involve risks and uncertainties, there are important factors that could cause actual results to differ materially from those expressed or implied by these forward-looking statements, including changes in our plans, objectives, expectations, prospects and intentions and other factors discussed in our filings with the SEC. We cannot guarantee any future levels of activity, performance or achievements. Travelzoo undertakes no obligation to update forward-looking statements to reflect events or circumstances occurring after the date of this press release.

Travelzoo and Jack’s Flight Club are registered trademarks of Travelzoo.

NEW YORK, July 26, 2023 /PRNewswire/ — Travelzoo® (NASDAQ: TZOO), a global Internet media company that provides exclusive offers and experiences for members, today announced that its board of directors has authorized the repurchase of up to 1,000,000 shares of the Company’s outstanding common stock.

Purchases may be made, from time to time, in the open market and will be funded from available cash. The number of shares to be purchased and the timing of purchases will be based on the level of Travelzoo’s cash balances, general business and market conditions, and other factors, including alternative investment opportunities.

About Travelzoo

Travelzoo® provides its 30 million members with exclusive offers and one-of-a-kind experiences personally reviewed by our deal experts around the globe. We have our finger on the pulse of outstanding travel, entertainment, and lifestyle experiences. We work in partnership with more than 5,000 top travel suppliers—our long-standing relationships give Travelzoo members access to irresistible deals.

Travelzoo, Top 20, and Jack’s Flight Club are registered trademarks of Travelzoo.

Michael Kupinski, Director of Research, Noble Capital Markets, Inc.

Jacob Mutchler, Research Associate, Noble Capital Markets, Inc.

Refer to the bottom of the report for important disclosures

Overview: Is The Recession Here? Economic activity is slowing, taking pressure off of inflation. But, the Fed seems intent on pushing interest rates higher, likely through the balance of this year. As such, recent economic forecasts anticipate GDP to contract over the next few quarters. This does not paint a favorable picture for advertising in the very near term. But, given the increased likelihood of a recession, has timeliness in media stocks improved?

Digital Media & Technology:A broad based recovery? For the second quarter in a row, the best performing index was Noble’s Social Media Index, which increased by 34% in 2Q 2023, followed by Noble’s Ad Tech Index (+24%), MarTech Index (+18%), Digital Media Index (+16%), and Video Gaming Index (+5%). The largest stocks carried the performance in each of the indices. Can the stocks hold on to recent gains?

Broadcast Television: Are ad trends really improving? Recent reports indicate that television advertising is showing some improvement. While it is likely that Auto and Political advertising are bright spots, we remain skeptical that core advertising pacings are improving in the third quarter given the weak economic outlook. Nonetheless, the TV stocks appear to be cheap and we highlight a few of our key favorites.

Broadcast Radio:The pall over radio. Soft advertising trends heading into an economic downturn does not bode well for companies, like Audacy, that are in the midst of a financial restructuring. We believe that high debt leverage is the pall over the stocks. It is likely that many radio companies will go through a round of cost cutting to shore up cash flow in the midst of an economic downturn.

Publishing: Cash flow gurus. We do not believe that the Publishing industry will be spared from the weak advertising environment. The industry has a playbook for cutting costs, however, and has a history of maintaining cash flow through difficult times.

Overview

The Recession Is Here

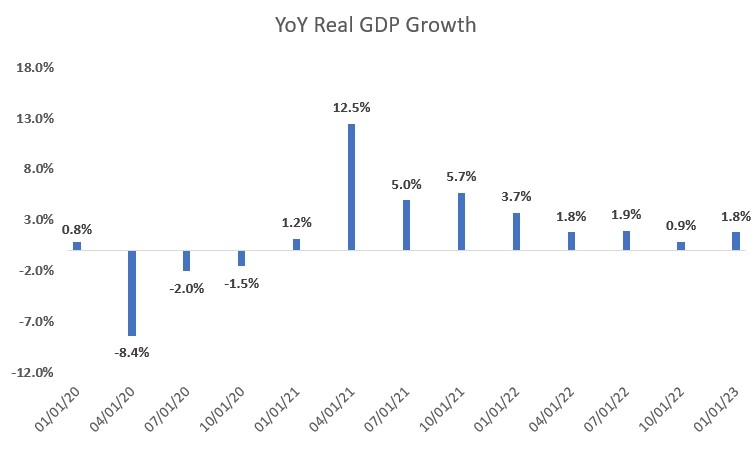

Figure #1 YoY Real GDP Growth illustrates that the economy grew post pandemic through the first quarter 2023, reflecting a rebounding economy, fueled by government spending. But, economic activity is slowing, taking pressure off of inflation. Nonetheless, the Fed seems intent on pushing interest rates higher, likely through the balance of this year. Most economists anticipate that the Fed will raise interest rates by 25 basis points two times in the second half of this year. Not only will the interest rate increases be a headwind for the economy, but government spending, a key driver to the economy this year, is likely to wane. Recent economic forecasts anticipate GDP to contract over the next few quarters, a classic definition of an economic recession. The Conference Board of Economic Forecasts anticipate that the US economy will contract -1.2% in Q3 2023, -1.9% in Q4 2023, and -1.1% in Q1 2024.

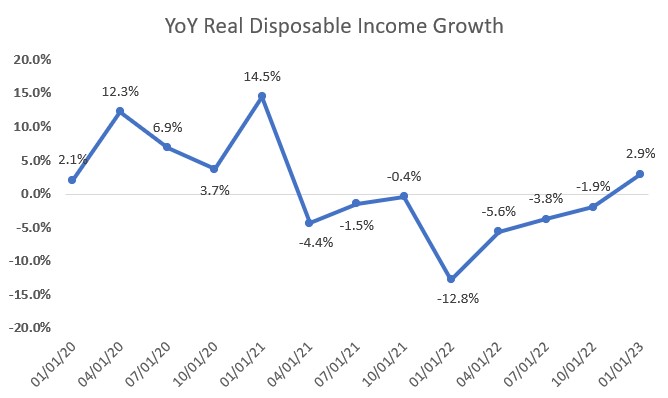

This does not paint a favorable picture for advertising in the very near term. Advertising is highly correlated to personal disposable income, particularly discretionary income. If consumers have discretionary income, companies advertise for them to spend. As Figure #2 YoY Real Disposable Income Growth highlights, disposable income has declined over the past 18 months. Not surprisingly, economically sensitive National advertising has been down nearly 4 quarters and at high double digit rates. Given the significant declines, as much as 25% in each quarter for the past year, National advertising trends should moderate, given that the comps get easier. As such, even with an economic downturn becoming more visible, it is possible that National advertising declines may moderate.

National advertisers tend to spend when there is light toward the end of an economic recession, when consumer personal disposable income shows signs that it will improve and consumers have the propensity to spend. In our view, that light at the end of the tunnel is still pretty dim given the economic forecast that anticipates a decline in GDP through the Q1 2024. While the visibility of an improvement in National advertising seems to have improved as we enter an economic downturn, especially given the easing comps and the benefit from Political advertising (expected to begin in Q3 2023), we think that it is too early to be optimistic. The length and severity of an economic downturn is not yet visible.

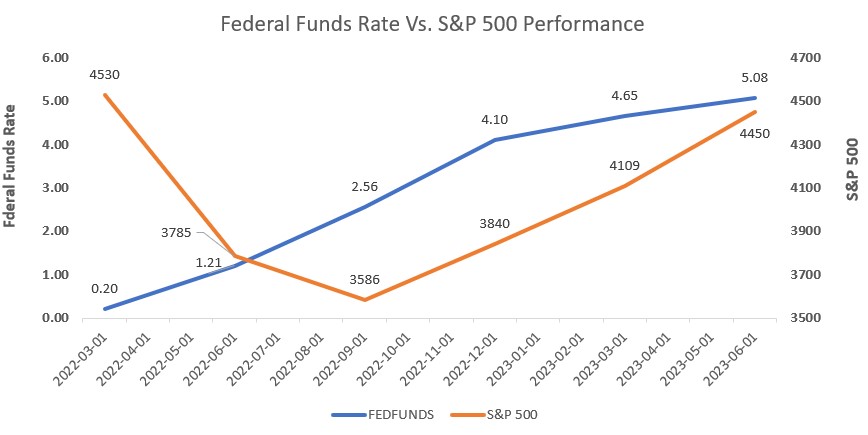

What does this mean for the stock market and for media stocks? Figure #3 Federal Funds Rate Vs. S&P 500 performance illustrates the recent increases in Fed Funds rates had little effect on the general stock market as measured by the S&P 500 Index. Unfortunately, late cycle and economically sensitive media companies declined or under performed the stock market. In spite of Fed Fund rate increases over the past year, the S&P 500 Index increased 18% in the last 12 months. The anticipation of an economic recession, however, weighed on media stocks. The stock performance of the various media sectors that we follow are discussed in this report, but have generally under performed the market. The exception to the poor performance were the Internet and Digital Media stocks, which had a broad based recovery. Is it possible that early cycle media stocks will outperform the general market in the near term? In our view, yes. But, this may mean that the general market may decline as media stocks decline less. Historically, it has been the case to buy media stocks in the midst of a recession as media stocks strongly outperform the general market in a economic recovery. But given the likely disappointment in revenue in the coming quarters, it is likely that media stocks will be volatile as investors weigh the near term revenue and earnings disappointments to the prospect of a revenue rebound in an improved economic scenario. This would suggest that if one would try to time the stocks, investors may want to wait a quarter or two, buy on the improved momentum. This may mean that one might miss the large gains. As such, for long term investors, we believe that we are nearer to the bottom and that the downside appears relatively limited, valuations appear compelling. But, given the anticipate volatility in the near term, media investors should look for opportunistic purchases and accumulate positions in our favorite media names highlighted in this report.

Figure #1 YoY Real GDP Growth

Source: Federal Reserve Bank of St. Louis

Figure #2 YoY Real Disposable Income Growth

Source: Federal Reserve Bank of St. Louis

Figure #3 Federal Funds Rate Vs. S&P 500 performance

Source: Federal Reserve Bank of St. Louis & Yahoo Finance

Digital Media & Technology

A Broad-Based Recovery in Shares

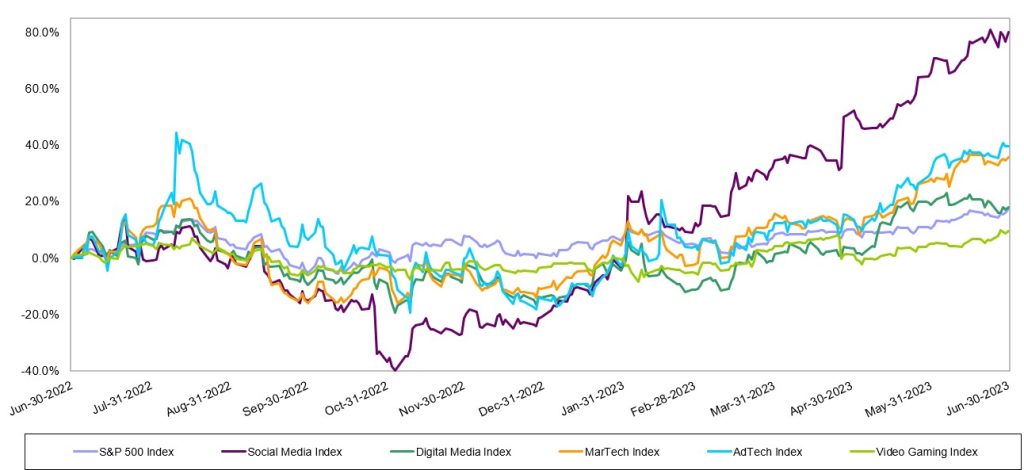

The Internet and Digital Media sectors rebounded nicely over the last 12 months (LTM). As Figure #4 LTM Internet & Digital Technology Performance illustrates, the Video Gaming index was the only sector that underperformed the S&P 500 over the last year. The S&P 500 Index was up 17.6% over the LTM, outperforming the Video gaming index’s increase of 9.7% and in line with Noble’s Digital Media Index increase of 18%. The MarTech Index and AdTech Index both performed strongly, increasing 35.8% and 39.8%, respectively. The Social Media index had the strongest performance of the indices, increasing an impressive 80.2% over the LTM.

Figure #4 LTM Internet & Digital Technology Performance

Source: Capital IQ

Despite macroeconomic headwinds that include higher interest rates, a regional banking crisis, elevated inflation and a war in Europe, the S&P 500 powered higher for the third quarter in a row. The S&P 500 Index continued its streak of steady increases, with an 8% increase in the Index in 2Q 2023, which followed a 7% increase in 1Q 2023 and a 7% increase in 4Q 2022. The broad index is up a healthy 24% since the end of the third quarter of 2022. The S&P 500 bottomed on October 12, 2022, and is up 26% from that date through mid-July.

The S&P 500’s performance was driven primarily by its largest constituents. As a market weighted index, the largest stocks have an outsized impact on its performance, and that was certainly the case in 2Q. Eight of the largest stocks in the S&P 500 Index were up in 2Q 2023 by 2x-3x or more than the Index’s 8% gain. Stocks that powered the Index higher included Nvidia (NVDA, +52%), Meta Platforms (a.k.a Facebook, META, +35%), Netflix (NFLX, +28%), Amazon (AMZN, +26%), Tesla (TSLA, +26%), Microsoft (MSFT, +18%), Apple (AAPL, +18%) and Google (GOOGL, +15%).

Noble’s Internet and Digital Media Indices, which are also market cap weighted, also powered higher thanks to the biggest constituents in their respective Indices. Each of these Indices posted double digital percent increases, with only the exception being Noble’s Video Gaming Index (+5%), which slightly underperformed the broader market/S&P Index. For the second quarter in a row, the best performing index was Noble’s Social Media Index, which increased by 34% in 2Q 2023, followed by Noble’s Ad Tech Index (+24%), MarTech Index (+18%), Digital Media Index (+16%), and Video Gaming Index (+5%).

Meta Powers the Social Media Index Higher

We attribute the strength of the Social Media Index to its largest constituent, Meta Platforms, whose shares increased by 35% in the second quarter. We noted last quarter that Meta appeared to be returning to its roots and focusing on profitability, rather than its nascent and riskier web3 initiatives. That return to its core strengths has been greatly rewarded by investors. Shares of Meta were up 225% from its 52-week low of $88.09 per share in early November through the end of June. Shares are up another 8% since the start of the third quarter with the launch of Threads, Meta’s answer to Twitter. Over 100 million people signed up for Threads within the first five days of its rollout. Meta has not yet begun to monetize this opportunity, but it will clearly add to its growth in coming quarters.

Ad Tech Stocks Embark on a Broad-Based Recovery Following a Difficult 2022

Noble’s AdTech Index increased by 24% in 2Q 2023, and this performance was very broad based, with 15 of the 24 stocks in the sector up, and a dozen of the stocks up by double digits. Ad Tech stocks that performed best during the quarter include Applovin (APP, +63%), Magnite (MGNI, +47%), Tremor International (TRMR, +37%), Pubmatic (PUBM, +32%), Double Verify (DV, +29%), The Trade Desk (+27%), and Integral Ad Science (IAS, +26%). Ad Tech stocks were the worst performing sector in our universe in 2022, with the index down 63% for the year in 2022. The strong performance in 2Q 2023 in many respects reflects a bounce back off multi-year lows for several stocks. Year-to-date, one standout in particular is Integral Ad Science, whose shares were up 104% in the first half of 2023.The company continues to expand its product suite, scale its social media offerings (i.e., for TikTok) and is well positioned to continue to benefit from the shift from linear TV to connected TV (CTV). The company is benefiting from new partnerships with YouTube and Netflix and shares likely benefited during the quarter from anticipation of the company’s mid-June analyst day presentation.

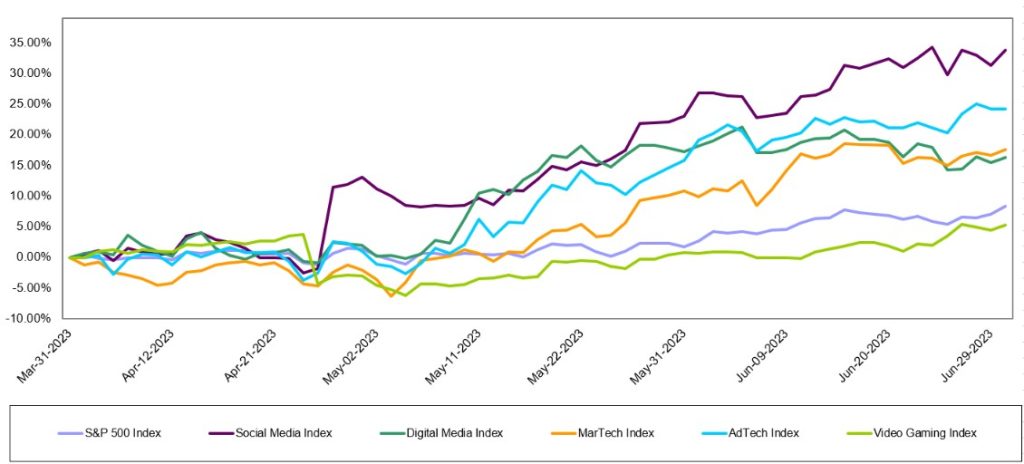

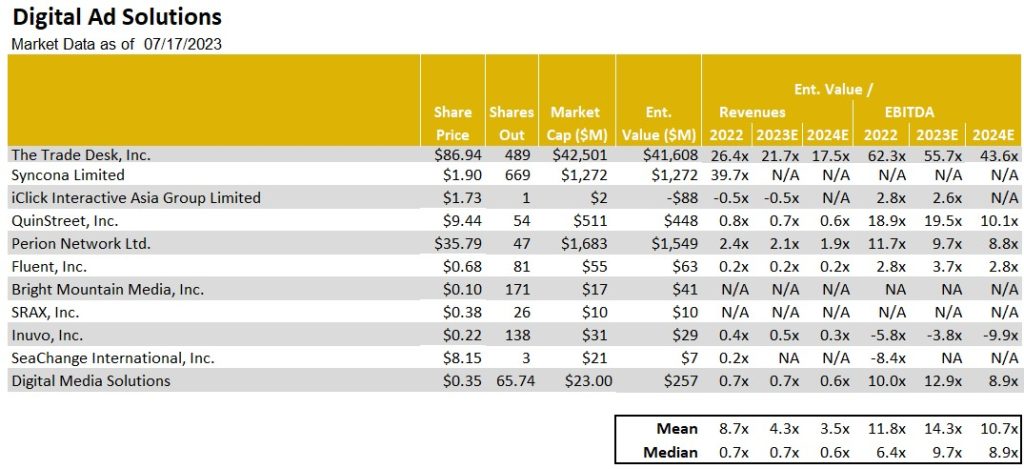

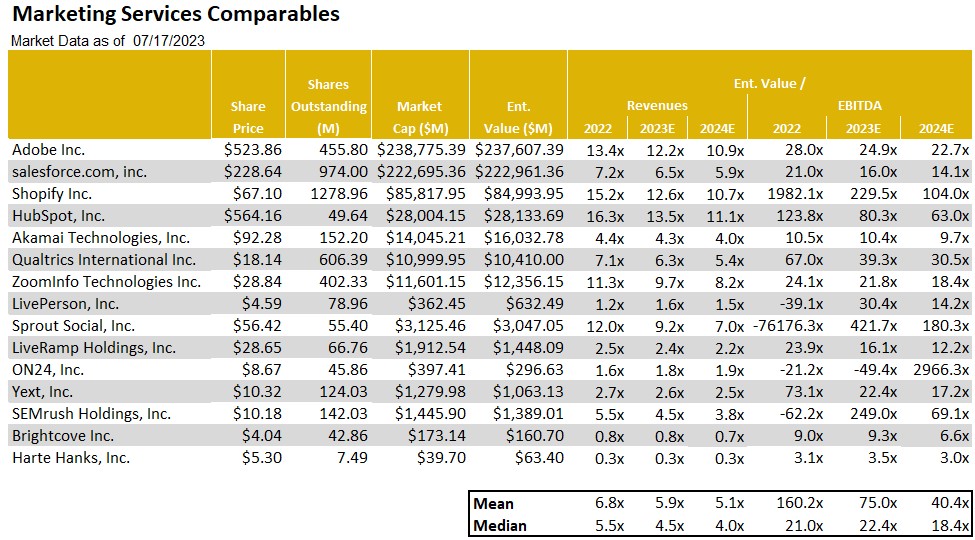

Noble’s MarTech Index was up 18%, with performance within the group also broad based. The Digital Media & Technology indices market-cap weighted performances in 2Q are illustrated in Figure #5 2Q Internet & Digital Technology Performance. Thirteen of the 20 stocks in the Index were up in the quarter. MarTech stocks that performed best during the quarter include Cardlytics (CDLX, +86%), Shopify (SHOP, +35%), Live Ramp (RAMP, +30%), Adobe (ADBE, +27%), and Hubspot (NUBS, +24%). One of the poor performers in the group was one of our closely followed stocks, Harte Hanks, which declined 42% in the latest quarter. The stock gave back nearly all of its 54% gains in the prior year. The weakness was due to a disappointing quarterly revenue outlook as the company indicated that it is seeing economic headwinds and more difficult second half comparables. Notably, the company has significant levers to maintain much of its favorable cash flow outlook and is well positioned for growth as those headwinds diminish. We believe that downside risk in the HHS shares appear limited and view the shares as among our favorite rebound plays. Overall, MarTech stocks were victims of their own success: the group traded at double digit revenue multiples in 2021, but the sector’s revenue multiples were more than halved in 2022. The group currently trades at 5.9x 2023E revenues, up from 4.1x 2023E revenues at the end of the first quarter, and 3.5x 2023E revenues at the start of the year. Current trading multiples are illustrated in Figure #7 MarTech Comparables.

Finally, the Digital Media Index was up 16% in 2Q 2023, and here again, the performance was broad based with 8 of the 12 stocks in the Index posting gains. Digital Media stocks that performed best during the quarter include Fubo TV (FUBO, +72%), Travelzoo (TZOO, +31%), Netflix (NFLX, +28%), Interactive Corp (IAC, +22%), and Spotify (SPOT, +20%). Year-to-date, the two best performing Digital Media stocks are Spotfiy (+103% YTD), which has shifted its priority to running a profitable company and took additional steps in 2Q to achieve it, for instance, by consolidating and streamlining several of its podcast company acquisitions from recent years. The second best performing Digital Media stock through the first half of the year was Travelzoo (TZOO), whose shares were up 77% in the first half of the year. The company continues to benefit from pent up demand that helped a surge in travel as the pandemic ebbed. Lodging and domestic travel demand rebounded first, but Travelzoo appears to be benefiting from cruises and international travel, where pent up demand took longer to recover. Management indicated that travel related advertising may increase as economic headwinds adversely affect hotel and air travel occupancy, forcing these travel businesses to offer discounts. We rate the TZOO shares as Outperform.

Figure #5 2Q Internet & Digital Technology Performance

Source: Capital IQ

Figure #6 AdTech Comparables

Source: Company filings & Eikon

Figure #7 MarTech Comparables

Source: Noble estimates & Eikon

Traditional Media

Traditional media stocks largely underperformed the general market over the LTM, the Radio sector was the hardest hit. As Figure #8 LTM Traditional Media Performance illustrates, the Noble Radio Index decreased 37.7% over the LTM, compared with the general market increasing 17.6%, as measured by the S&P 500 over the same period. The Television Index was down 14.8% and the Publishing index outperformed the general market, increasing 28.4% over the LTM. Notably, there were company stock performance disparities within each sector, highlighted later in this report. Given the indices are market cap weighted, larger market capitalized companies skewed the indices’ performance.

The traditional media industry is still finding its footing in the difficult economic environment, given the indices performance in Q2. While the Newspaper and Radio indices performed better in Q2 than Q1, the TV Index did not. The general market, as measured by the S&P 500, increased 8.3% over the last quarter and outperformed all but one traditional media sector. The Newspaper Index, which increased 8.5% over the same period narrowly outperformed the general market. The TV Index was the hardest hit traditional media sector and decreased -11.1%. While the Radio index underperformed the market in Q2, it improved upon a difficult Q1 and increased 3.1%, as illustrated in Figure #9 Q2 Traditional media performance.

Figure #8 LTM Traditional Media Performance

Source: Capital IQ

Figure #9 Q2 Traditional Stock Performance

Source: Capital IQ

Broadcast Television

Are ad trends really improving?

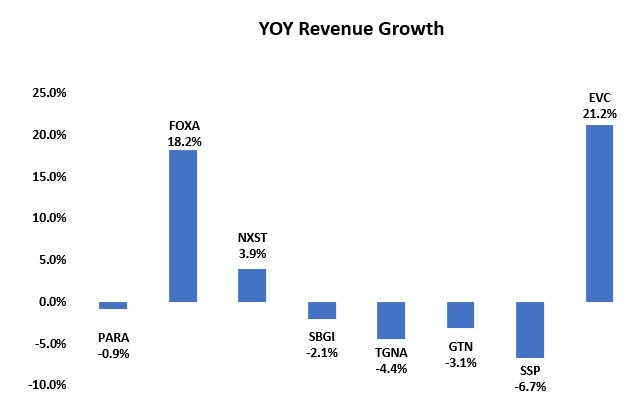

The TV Index underperformed the general market in the second quarter. While none of the stocks in the TV Index increased in the second quarter, many performed better than the market cap weighted return of -11.1%. Fox Corporation (FOXA; down 0.1%), E.W Scripps (SSP; down 2.8%), Nexstar (NXST; down 3.5%) and Gray Television (GTN; down 9.6%) were among the best performing stocks in the hard-hit TV index. The stocks hit the hardest in Q2 were Sinclair Broadcast Group (SBGI; down 19.5%) and Entravision (EVC; down 27.4%). Given the recent turmoil in TV stock performances we view the depressed prices as a potential opportunity given the prospect of an advertising recovery over the next few quarters.

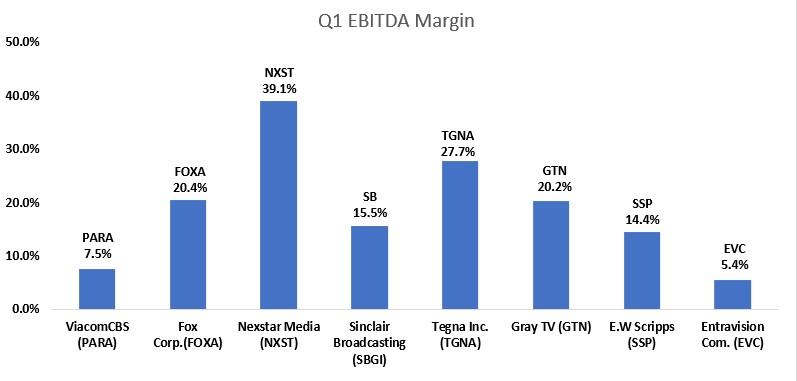

While there have been some recent reports indicating that television advertising is improving, possibly related to increased political advertising and Auto advertising in the third quarter, we remain skeptical that the improvement is sustainable given the prospect of a weakening economy. Nonetheless, the TV stocks appear cheap. One of our favorites in the index is Entravision (EVC) which is among the industry leaders in revenue growth as illustrated in Figure #10 TV Q1 YoY Revenue Growth. While the EVC shares had a poor performance in Q2, down 27.4%, the shares had increased 26% in Q1. Entravision’s revenue growth is the product of a robust digital business that comprises approximately 80% of total revenue. We believe that the recent under performance is related to Meta’s (Facebook’s) announcement that it plans to implement efficiencies, implying that it may take margin away from some of its advertising agencies, like Entravision, which represents Facebook in Latin America. In our view, Entravision is in a strong position to push back on that prospect given its favorable business relationship with the company. Given the influx of lower margin digital revenues, Entravision’s EBITDA margin is much lower than industry peers, illustrated in Figure #11 TV Industry Q1 EBITDA Margin. But, importantly, the company has one of the better revenue and cash flow growth profiles.

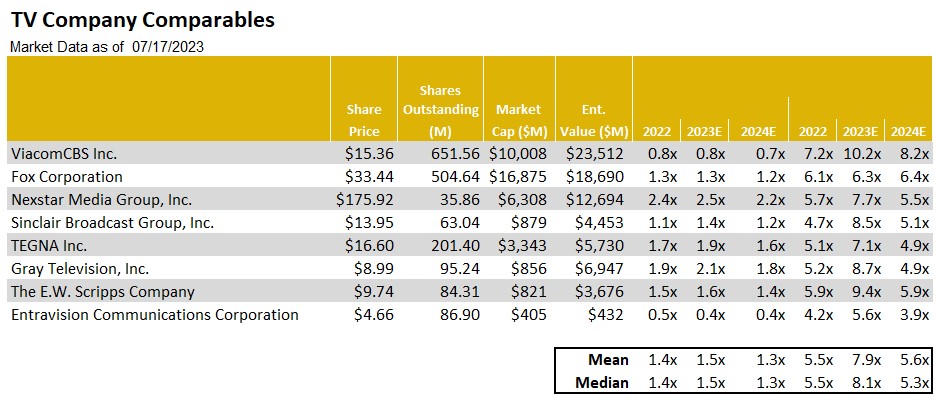

Figure #12 TV Company Comparablesillustrates the trading levels of the companies in the index. Some of our favorites Entravision (EVC) and E.W Scripps (SSP) trade at multiples well below the industry peer group highs. While E.W Scripps had modest year over year revenue decline, we believe it will benefit from favorable Retransmission revenue, strong Political advertising and improved margins in 2024. Given the SSP shares low float, the shares tend to underperform when industry is out of favor and outperform when the industry is back in favor. As for Entravision, we view the company’s digital transformation favorably and, notably, the shares are trading at a modest 3.9 times Enterprise Value to our 2024 Adj. EBITDA estimate. In our view, there appearas to be limited downside risk. The EVC shares and SSP shares, in our view, both offer a favorable risk reward relationship.

Figure #10 TV Q1 YoY Revenue Growth

Source: Company filings

Figure #11 TV Industry Q1 EBITDA Margin

Source: Company filings & Eikon

Figure #12 TV Company Comparables

Source: Noble Estimates & Eikon

Broadcast Radio

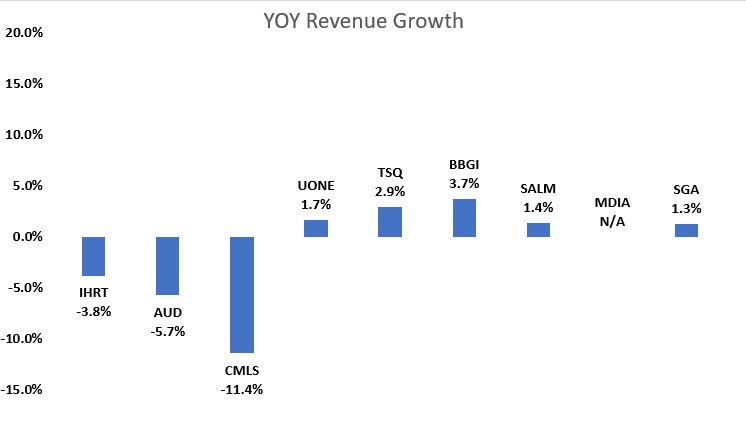

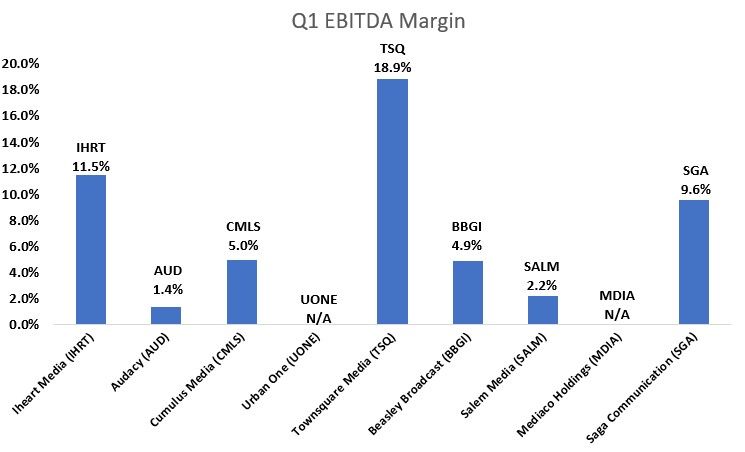

While the Radio Index underperformed the S&P 500 in Q2, it was an improvement from a difficult Q1. Notably, there were a few strong performances in the market cap weighted index. Beasley Broadcast Group (BBGI, up 24.4%) , Cumulus Media (CMLS, up 11.1%) and Townsquare (TSQ, up 48.9%) all strongly outperformed the S&P 500 in Q2. The largest stocks in the group did not perform well in the quarter skewing the index lower, Audacy (AUD, up 2.6%) and iHeart Media (IHRT, down 6.7%). The second quarter stock performances were a mixed bag and largely did not reflect the first quarter operating results. As Figure #13 Radio Q1 YoY Revenue Growth illustrates, most companies had modest revenue growth. The larger Radio companies that rely more on National advertising had the greatest declines of YoY revenue. With CMLS being the exception, the larger Radio companies underperformed relative to Radio companies with a stronger digital and highly localized presence. Figure #14 Radio Industry Q1 EBITDA Margin Margins illustrate that the margins for the industry remain relatively healthy.

Some of our favorite Radio stocks have strong digital businesses and highly localized footprints, which provides some shelter from weakness in national advertising. Those stocks included Townsquare, Beasley Broadcast Group, Salem Media (SALM; down 12.1%) and Saga Communications (SGA, down 3.9%). While the shares of Saga Communications (SGA) were down 3.9%, the performance did not reflect its favorable first quarter operating results. Importantly, Saga grew revenues a modest 1.3% and had an above average Q1 EBITDA margin of 9.6%. Saga has a highly localized footprint, as approximately 90% of revenues come from local sources. Furthermore, the company has been placing more importance on growing a profitable digital business in recent years. While Saga’s Digital business is early in its development, management is focused on growing digital revenues from 7.5% of total revenue in Q1 to 20% of total revenue over the next couple years. Additionally, we believe the company is likely to maintain a strong cash position given the economic uncertainty.

We view Townsquare Media (TSQ), Salem Media (SALM), Beasley Broadcast (BBGI) and Saga Communications (SGA) as among our favorites in the industry given the diverse revenue streams and localized footprints. While these companies are not immune to the economic headwinds, we believe that its Digital businesses and local footprints should offer some ballast to its more sensitive Radio business. Beasley’s recent digital revenue growth has been robust, digital revenue was 17% of total revenue in Q1 and is expected to reach 20% to 30% of total revenue for full year 2023. In the case of Salem, 30% of its revenues are from reliable block programming.

We believe that Radio advertising pacings likely will be problematic in the second half given the economic headwinds. Unlike Television, the industry does not benefit as much from Political advertising. As such, we expect that advertising pacings likely will be lower in Q3 than the Q2 results. It is likely that many radio companies, especially those with higher debt leverage, will implement cost cutting measures. With many of the radio companies already relatively lean from the Pandemic, it is likely that such measures will be difficult.

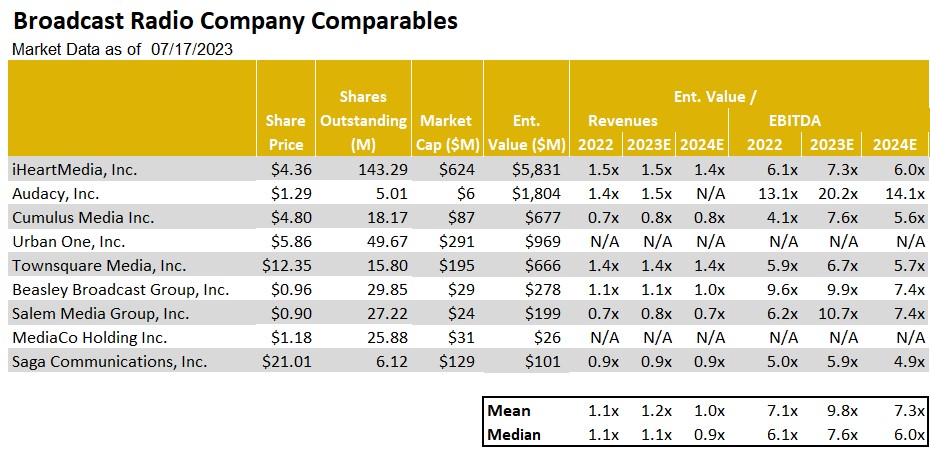

As Figure #15 Radio Company Comparables illustrates, the shares of Townsquare and Saga are among the cheapest in the industry, trading below peer group averages. Notably, Townsquare implemented a hefty dividend in Q1, providing the unique opportunity to get a return of capital while waiting for a turn toward more favorable fundamentals. As such, the shares of TSQ tops our list of favorites. We also view the shares of Saga as among our favorites. The company is early in its transition toward digital and has a lot of headroom for enhanced revenue growth.

Figure #13 Radio Q1 YoY Revenue Growth

Source: Company filings

Figure #14 Radio Industry Q1 EBITDA Margin

Source: Company filings & Eikon

Figure #15 Radio Company Comparables

Source: Noble estimates & Eikon

Publishing

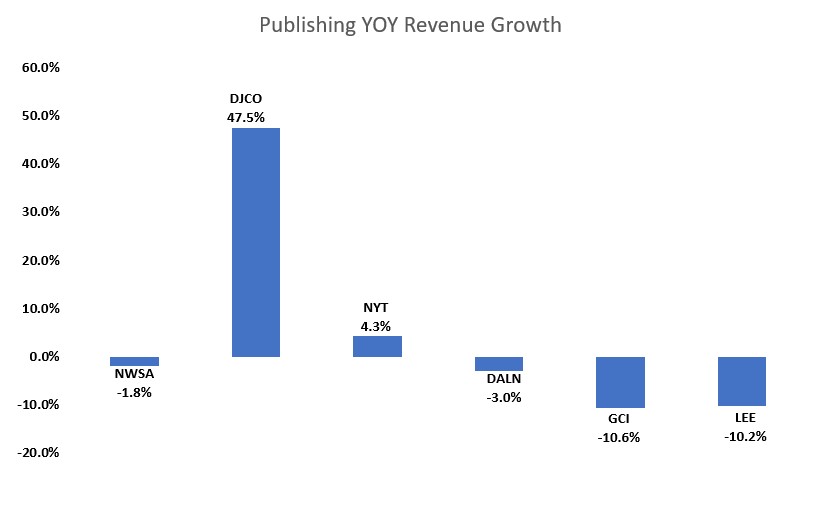

The Publishing industry is no exception to the advertising weakness that is impacting the broader Media landscape. As such, revenues are likely to continue to decline, despite an already weak performance in the first quarter of the year. Figure #16 Publishing Q1 YoY Revenue Growth illustrates the predominantly negative trends in the industry in the most recently reported quarter. The advertising challenges are hitting the traditional Print side of the publishing business hardest. For example, Lee Enterprises (LEE), one of our favorites in the industry, reported a 10% Print advertising revenue decline for the quarter ended March 31st, while Digital advertising grew a modest 2%. The company’s adj. EBITDA generation fell 15% compared with a more moderate 2% drop in total company revenues.

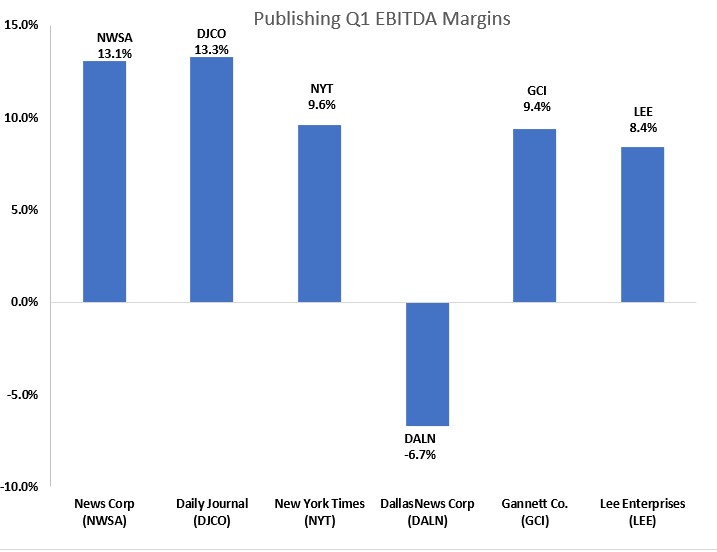

Not surprisingly, the dampened industry revenue resulted in lower industry cash flow generation with EBITDA margins averaging in the 10% range, as illustrated in Figure #17 Publishing Industry Q1 EBITDA Margins. Yet despite the constraints on cash flow generation on Lee and the other Publishers, we believe the companies have the ability to cut costs to help offset the pressure on cash flow generation. In particular, companies could cut costs in their Print manufacturing and distribution operations, reducing overhead in the same business segments where revenues are expected to lag. Publishing companies have a playbook on cutting legacy print costs and have the ability to maintain cash flow. However, cost cuts can take time to go into full effect, which could result in poor cash flow performance over the next quarter or so.

In spite of the nearer term economic headwinds impacting the operating performance of the industry, we believe that the industry is near an inflection point towards revenue growth. This dynamic is related to the degree of the recovery in its digital media businesses, a key driver to the industry’s overall revenue performance. While there are secular challenges to the industry’s print business, digital revenues account for an increasing portion of total revenues. For companies like Lee Enterprises, digital accounts for over 38% of total revenues in the most recent quarter. In our view, publishing companies will be a player in the advertising recovery as economic prospects improve. Furthermore, we believe that stock valuations are compelling.

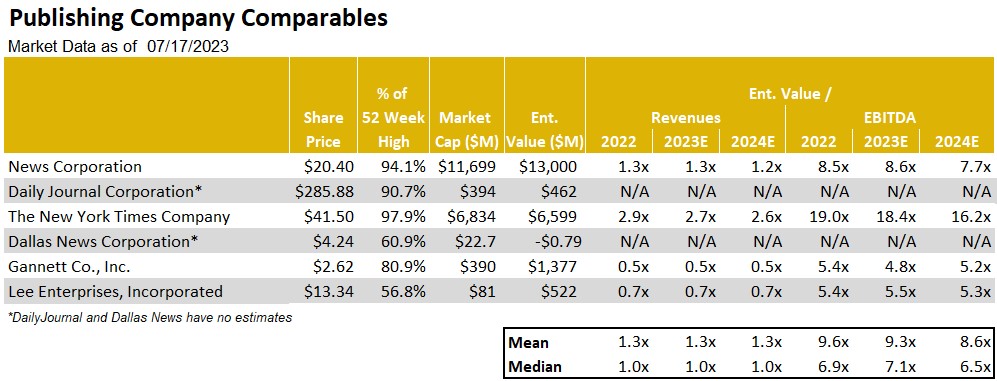

Figure #18 Publishing Company Comparables illustrates the Publishing companies trading levels. Notably, the New York Times (NYT) trades well above the levels of the rest of its peers. In comparison, Lee and Gannett appear to be compelling. However, both Lee and Gannett are highly levered. Yet, in our view, Lee’s debt profile has several favorable characteristics, such as a fixed 9% annual rate, no fixed principal payments, no performance covenants and a 25 year maturity. Given that the LEE shares trade near 5.3 times enterprise value to our 2024 adj. EBITDA forecast, we believe the shares offer limited downside risk. With a favorable Digital transformation of the business well underway, we believe the LEE shares could close the valuation gap with some of its higher trading peers. As such, the LEE shares represent one of our favorites in the industry, especially as the economic downturn bottoms out and the prospect for a recovery begins to come to the forefront. As such, the LEE shares are among our favorite recovery plays.

Figure #16 Publishing Q1 YoY Revenue Growth

Source: Company filings & Eikon

Figure #17 Publishing Industry Q1 EBITDA Margins

Source: Company filings & Eikon

Figure # 18 Publishing Company Comparables

Source: Noble estimates & Eikon

The following companies are highlighted in this report. Click on the links for additional information and disclosures.

All statements or opinions contained herein that include the words “we”, “us”, or “our” are solely the responsibility of Noble Capital Markets, Inc.(“Noble”) and do not necessarily reflect statements or opinions expressed by any person or party affiliated with the company mentioned in this report. Any opinions expressed herein are subject to change without notice. All information provided herein is based on public and non-public information believed to be accurate and reliable, but is not necessarily complete and cannot be guaranteed. No judgment is hereby expressed or should be implied as to the suitability of any security described herein for any specific investor or any specific investment portfolio. The decision to undertake any investment regarding the security mentioned herein should be made by each reader of this publication based on its own appraisal of the implications and risks of such decision.

This publication is intended for information purposes only and shall not constitute an offer to buy/sell or the solicitation of an offer to buy/sell any security mentioned in this report, nor shall there be any sale of the security herein in any state or domicile in which said offer, solicitation or sale would be unlawful prior to registration or qualification under the securities laws of any such state or domicile. This publication and all information, comments, statements or opinions contained or expressed herein are applicable only as of the date of this publication and subject to change without prior notice. Past performance is not indicative of future results. Noble accepts no liability for loss arising from the use of the material in this report, except that this exclusion of liability does not apply to the extent that such liability arises under specific statutes or regulations applicable to Noble. This report is not to be relied upon as a substitute for the exercising of independent judgement. Noble may have published, and may in the future publish, other research reports that are inconsistent with, and reach different conclusions from, the information provided in this report. Noble is under no obligation to bring to the attention of any recipient of this report, any past or future reports. Investors should only consider this report as single factor in making an investment decision.

IMPORTANT DISCLOSURES

This publication is confidential for the information of the addressee only and may not be reproduced in whole or in part, copies circulated, or discussed to another party, without the written consent of Noble Capital Markets, Inc. (“Noble”). Noble seeks to update its research as appropriate, but may be unable to do so based upon various regulatory constraints. Research reports are not published at regular intervals; publication times and dates are based upon the analyst’s judgement. Noble professionals including traders, salespeople and investment bankers may provide written or oral market commentary, or discuss trading strategies to Noble clients and the Noble proprietary trading desk that reflect opinions that are contrary to the opinions expressed in this research report. The majority of companies that Noble follows are emerging growth companies. Securities in these companies involve a higher degree of risk and more volatility than the securities of more established companies. The securities discussed in Noble research reports may not be suitable for some investors and as such, investors must take extra care and make their own determination of the appropriateness of an investment based upon risk tolerance, investment objectives and financial status.

Company Specific Disclosures

The following disclosures relate to relationships between Noble and the company (the “Company”) covered by the Noble Research Division and referred to in this research report. Noble is not a market maker in any of the companies mentioned in this report. Noble intends to seek compensation for investment banking services and non-investment banking services (securities and non-securities related) with any or all of the companies mentioned in this report within the next 3 months

ANALYST CREDENTIALS, PROFESSIONAL DESIGNATIONS, AND EXPERIENCE

Senior Equity Analyst focusing on Basic Materials & Mining. 20 years of experience in equity research. BA in Business Administration from Westminster College. MBA with a Finance concentration from the University of Missouri. MA in International Affairs from Washington University in St. Louis. Named WSJ ‘Best on the Street’ Analyst and Forbes/StarMine’s “Best Brokerage Analyst.” FINRA licenses 7, 24, 63, 87

WARNING

This report is intended to provide general securities advice, and does not purport to make any recommendation that any securities transaction is appropriate for any recipient particular investment objectives, financial situation or particular needs. Prior to making any investment decision, recipients should assess, or seek advice from their advisors, on whether any relevant part of this report is appropriate to their individual circumstances. If a recipient was referred to Noble Capital Markets, Inc. by an investment advisor, that advisor may receive a benefit in respect of transactions effected on the recipients behalf, details of which will be available on request in regard to a transaction that involves a personalized securities recommendation. Additional risks associated with the security mentioned in this report that might impede achievement of the target can be found in its initial report issued by Noble Capital Markets, Inc.. This report may not be reproduced, distributed or published for any purpose unless authorized by Noble Capital Markets, Inc..

RESEARCH ANALYST CERTIFICATION

Independence Of View All views expressed in this report accurately reflect my personal views about the subject securities or issuers.

Receipt of Compensation No part of my compensation was, is, or will be directly or indirectly related to any specific recommendations or views expressed in the public appearance and/or research report.

Ownership and Material Conflicts of Interest Neither I nor anybody in my household has a financial interest in the securities of the subject company or any other company mentioned in this report.

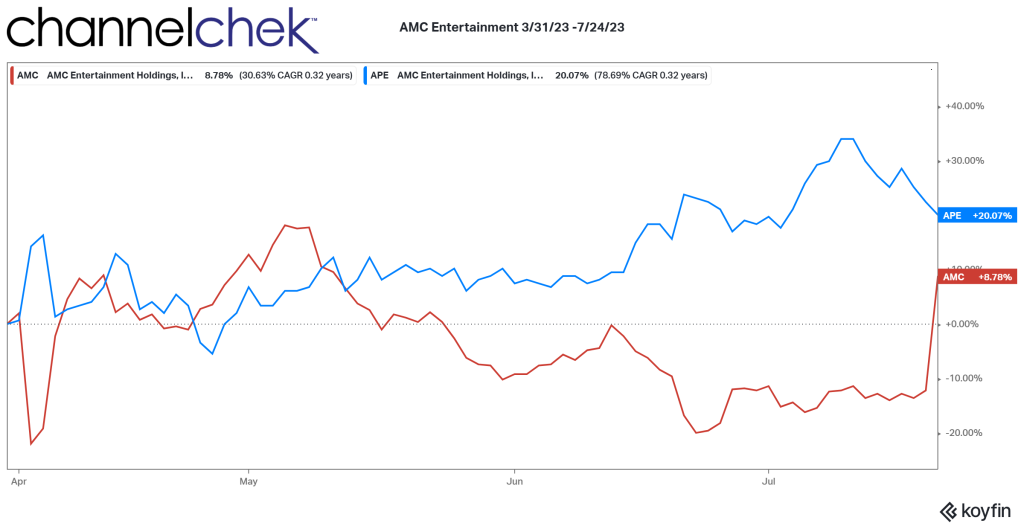

Adam Aron Explains the Reasons Share Conversion and Issuance is Good for APE Shares

Meme stocks are getting attention again as the movie Dumb Money is set for release in late September, GameStop (GME) is implementing a strategy to use its stores as fulfillment centers, and AMC Theatres (AMC) has a court ruling on its APE shares that has added significant volatility, including a 67% upward spike after hours on Friday July 21. The AMC story is involved and likely to cause wide swings until resolved as investors wrestle with guessing what a new ruling means for the company’s financial strength, and whether the judge’s decision could be overturned on appeal or through shareholder approval.

The main source of the ongoing dramatic moves in AMC stems from its proposed APE shares conversion. These preferred shares were provided as a dividend with a 1:1 conversion feature. If/when converted to regular AMC shares, they will dilute the regular shares. When issued, APE shares were considered a brilliant financing mechanism and method to determine if any fraudulent units were used to create a naked short.

In late July a judge blocked the proposed settlement on AMC Entertainment Holdings stock conversion plan that would also allow the company to issue more shares. The stock had been depressed in anticipation of the additional shares that would have been created. With the thought that additional shares won’t be entering the market, common shares (AMC) soared, and preferred shares (plummeted).

The Delaware chief judge Morgan Zurn said in her ruling that she cannot approve the deal, which would provide AMC common stockholders with shares worth an estimated $129 million. The company was sued in February for allegedly rigging a shareholder vote that would allow the entertainment company to convert preferred stock to common stock and issue hundreds of millions of new shares. The investors who sued alleged AMC had enacted the plan to circumvent the will of common stock holders who opposed the company diluting their holdings.

Without the proposed settlement, common stockholders and preferred shareholders would end up owning 34.28% and 65.72% of AMC, respectively. Under the ruling, common stockholders and preferred shareholders would own 37.15% and 62.85%, respectively.

Judge Zurn wrote that while the deal would compensate common stockholders for the dilution, they had no right to settle potential claims by holders of preferred stock in this way. The settlement received more than 2,800 objections from shareholders, a level of interest Zurn called “unprecedented.” She said “AMC’s stockholder base is extraordinary,” adding many “care passionately about their stock ownership and the company.”

But what appears short term to be good for common shares, may actually weaken the financial position of the company over time according to AMC’s chairman. In an open letter, AMC chairman Adam Aron wrote, “What may not be clear to AMC’s shareholders is that if the company is unable to convert APE shares, AMC will be forced to issue significantly more APE shares to cover its upcoming cash requirements.”

Aron explained AMC is burning cash at an unsustainable rate and warned that an inability to raise capital could force the company into bankruptcy. Selling more shares would enable it to pay down some of its $5.1 billion in debt. These financial matters are further complicated by the writers and actors strike which according to Aron could delay the release of movies currently scheduled for 2024 and 2025.

NEW YORK, July 21, 2023 /PRNewswire/ — Travelzoo® (NASDAQ: TZOO):

WHAT:

Travelzoo, a global Internet media company that provides exclusive offers and experiences for members, will host a conference call to discuss the Company’s financial results for the second quarter ended June 30, 2023. Travelzoo will issue a press release reporting its results before the market opens on July 27, 2023.

WHEN:

July 27, 2023 at 11:00 AM ET

HOW:

A live webcast of Travelzoo’s Q2 2023 earnings conference call can be accessed athttp://ir.travelzoo.com/events-presentations. The webcast will be archived within 2 hours of the end of the call and will be available through the same link.

Travelzoo® provides its 30 million members with exclusive offers and one-of-a-kind experiences personally reviewed by our deal experts around the globe. We have our finger on the pulse of outstanding travel, entertainment, and lifestyle experiences. We work in partnership with more than 5,000 top travel suppliers—our long-standing relationships give Travelzoo members access to irresistible deals.