The Disappearing Broker-Dealer Equity Analyst – Why it Hurts Investors

Stock research or equity analysis is an irreplaceable resource for investors to determine the fair stock price of a company. The value of in-depth research is understood by large institutional investors such as mutual funds, pensions, and insurance companies, this is why they hire in-house stock analysts. Portfolio managers at these firms immerse themselves in information from a variety of trusted sources, they then get guidance from their own staff of highly compensated stock and industry analysts.

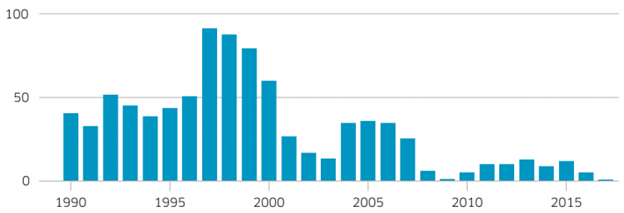

Covered Companies Continues to Shrink

The number of covered names analyzed by bulge bracket investment banks has been shrinking in recent years. Company analysis and research are now primarily reserved for the most lucrative corporate customers with several high-profit banking relationships. This has been causing private investment advisors along with self-directed investors that had relied on the research of the followed companies to look for other in-depth institutional caliber research to review. The reduction in coverage of smaller worthwhile companies left many with either fewer firms covering them or completely orphaned. For a company, coverage by several firms is ideal – astute Investors and advisors weigh consistency among research analysts in their stock selection.

Ongoing consolidation within the broker dealer industry of firms including TD Ameritrade, Eaton Vance, E*Trade, Charles Schwab, Morgan Stanley and others is further shrinking the research available to investors. This is because many of the firms folding into each other had overlapping covered equites. This follows years where these same broker dealers were reducing their research coverage.

The absence of one or more research firms regularly reporting on once covered companies is putting money managers in a position with fewer names to choose from. This is especially true of those professionals that make prudent use of Investment Policy Statements.

Investment Policy Statement (IPS)

Prudent investment management on behalf of others dictates an Investment Policy Statement. The Chartered Financial Analyst Institute (CFA) defines the role of the IPS as:

“The investment policy statement (IPS) serves as a strategic guide to the planning and implementation of an investment program. When implemented successfully, the IPS anticipates issues related to governance of the investment program, planning for appropriate asset allocation, implementing an investment program with internal and/or external managers, monitoring the results, risk management, and appropriate reporting.”

Two common elements of most IPS are the Limits on Investments and Relative

Constraints section. Within these sections it is not uncommon for the IPS to have wording which includes analyst rating at or above their mid-rating. Or, in other cases it may require the average of at least three analyst ratings above or at the mid-point. Other language may allow investing down to the lowest rating but limit the total portfolio percentage in this category. If a company isn’t rated it may not be allowed in consideration. There are of course other possibilities that eliminate a stock from being purchased in order to comply with what was agreed upon with the client or trust agreement. The reduction in coverage of companies by firms, and fewer firms covering those companies, eliminates many that otherwise would be a fit. That they can’t be considered is not good for the investor or the company.

Alternatives

Other research is filling the information gap made even wider by Wall Street. Independent research firms and boutique research-oriented investment banks are providing research on the stocks that have been left hanging by Wall Street. This means that independent research firms are becoming a primary source of information on a high percentage of publicly traded stocks. Some of this is subscription-based from investors. Another model which is gaining more prominence and acceptance is fee-based research where the cost of high caliber research is covered by the company itself. This model, often referred to as company-sponsored research is beginning to fill what would be a widening gap with broker dealer consolidations. It provides investors adhering to an IPS that would otherwise be required to exclude uncovered stocks the ability to consider them. The research also provides investors with details on company projections they would not have otherwise had for use in making decisions at no cost to the investor. Public companies securing this service have additional benefit since, unlike subscription-based, the research is available to all.

Company Sponsored vs. Promotional

It’s important to differentiate between unbiased fee-based research and research that is promotional. Objective fee-based research is similar to the role of your doctor. You pay a doctor not to tell you that you are well, but to give you his or her educated and truthful opinion of your condition.

Professional fee-based research is an objective analysis and opinion of a company’s investment potential. This is not to be confused with promotional write-ups. These write-ups are short on analysis, long on hype, and often written by marketers, not investment professionals.

Look for these characteristics to determine a research firm’s legitimacy:

- They provide analytical, not promotional services

- They are paid contractually in cash, (not any form of equity)

- They provide full and clear disclosure of the relationship between the company and the researcher

Some company-sponsored research firms have taken additional steps including requiring FINRA registrations of its analysts to demonstrate a high level of understanding, promote ethical behavior, and subject the analyst and the firm to punishment including loss of career, if some guidelines are not adhered to. This additional step punctuates the ethics, diligence and authenticity under which the evaluations were conducted.

Companies That Would Benefit from Research:

- Its shares may be undervalued because investors are not familiar with the company

- It has fewer than two respected firms covering the name which may take it out of consideration by professionals

- It believes that its story, financials, and management can withstand objective analysis

Take-Away

The visibility, credibility, and investability of a company hinge on investors recognizing and understanding the company. It also has to meet the criteria of the IPS of those firms it would like to attract. The company should also try to avoid tarnishing its reputation by not associating itself with hype masquerading as research. Similarly, a research firm may have its own criteria for selecting which stocks they want to analyze. Investors should make certain they are looking at high caliber research and not hyped marketing. The need left by large broker dealers, both by reducing covered companies, and also by merging with firms where there was a duplicate coverage situation is being filled by company-sponsored research firms. Their value is becoming better understood as the best solution to the problems left by the large Wall Street houses.

Suggested Reading:

Is Company Sponsored Research the Future for Small-Cap Stock Investors?

Small Cap Stocks Can Increase Your Portfolio Diversification

Large and Small Cap Return Probabilities

Do You Know a Student Interested in Equity Research?

They Could Win Up To $7,500 !

Tell them about the College Challenge!

Sources:

Elements of an Investment Policy for Institutional Investors

Each event in our popular Virtual Road Shows Series has a maximum capacity of 100 investors online. To take part, listen to and perhaps get your questions answered, see which virtual investor meeting intrigues you

Each event in our popular Virtual Road Shows Series has a maximum capacity of 100 investors online. To take part, listen to and perhaps get your questions answered, see which virtual investor meeting intrigues you