LAKE ZURICH, Ill.–(BUSINESS WIRE)– ACCO Brands Corporation (NYSE: ACCO) today announced that its board of directors has declared a quarterly cash dividend of $0.075 per share. The dividend will be paid on September 12, 2023, to stockholders of record as of the close of business on August 22, 2023.

“This is the Company’s 23rd quarterly cash dividend since it began paying dividends in 2018. The Company’s dividend has become an important part of our capital allocation strategy and we remain committed to supporting our quarterly dividend with our robust free cash flow. At the current stock price, on an annualized basis, our shareholders are receiving an almost 5% yield on their investment,” said Boris Elisman, Chairman and Chief Executive Officer of ACCO Brands.

About ACCO Brands Corporation

ACCO Brands, the Home of Great Brands Built by Great People, designs, manufactures and markets consumer and end-user products that help people work, learn, play and thrive. Our widely recognized brands include AT-A-GLANCE®, Five Star®, Kensington®, Leitz®, Mead®, PowerA®, Swingline®, Tilibra® and many others. More information about ACCO Brands Corporation (NYSE: ACCO) can be found at www.accobrands.com.

Mark Reichman, Managing Director, Equity Research Analyst, Natural Resources, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

Sale of Saskatchewan properties. LithiumBank executed a definitive agreement to sell the company’s three lithium brine projects in Saskatchewan, Canada to Pristine Lithium Corp. The strategic sale is expected to expedite the development of the Saskatchewan properties while allowing LithiumBank to maintain a financial interest in the properties through an ownership interest in Pristine Lithium. LithiumBank is now positioned to focus on the development of Boardwalk and Park Place in the province of Alberta without having to dilute its resources by developing multiple projects in two jurisdictions.

Financial terms. LithiumBank will receive cash consideration of C$2,000,000, including a C$250,000 deposit and an additional C$1,750,000 payable upon closing. LithiumBank will receive 40 million common shares in the capital of Pristine Lithium, or buyer shares, representing roughly 47% of the outstanding buyer shares on a post-financing basis, along with 20 million warrants, each exercisable into one buyer share for a period of two years from the date of issuance. Upon filing a NI 43-101 compliant preliminary economic assessment technical report, Pristine will issue buyer shares or cash representing C$1,000,000 of consideration to LithiumBank.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

Saga Communications, Inc. is a broadcast company whose business is primarily devoted to acquiring, developing and operating radio stations, television stations and state radio networks. Saga currently owns or operates broadcast properties in 26 markets, including 61 FM and 30 AM radio stations, 3 state radio networks, 2 farm radio networks, 5 television stations and 4 low power television stations. Saga’s strategy is to operate top billing radio and television stations in mid sized markets, defined as markets ranked (by market revenues) from 20 to 200. Saga’s radio stations employ a myriad of programming formats, including Classic Hits, Adult Contemporary, Active Rock, Oldies, News/Talk, Country and Classical. Saga’s television stations are affiliated with CBS and Fox in Joplin, MO; CBS in Greenville, MS; ABC, Fox, NBC, Telemundo and Univision in Victoria, TX. In operating its stations, Saga concentrates on the development of strong decentralized local management, which is responsible for the day-to-day operations of the stations in their market area and is compensated based on their financial performance as well as other performance factors that are deemed to effect the long-term ability of the stations to achieve financial objectives. Saga began operations in 1986 and became a publicly traded company in December 1992. The stock trades on the NYSE Amex under the ticker symbol “SGA”.

Michael Kupinski, Director of Research, Equity Research Analyst, Digital, Media & Technology , Noble Capital Markets, Inc.

Jacob Mutchler, Research Associate, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

Non-deal Roadshow highlights. On July 27, Chris Forgy, CEO, and Sam Bush, CFO, hosted investor meetings in St. Louis. We believe that the management team was sanguine about favorable revenue and cash flow growth prospects. This report highlights the company’s resilient local radio operations, strong balance sheet and emergent digital revenues.

Strong local presence. The company operates primarily in small and midsize markets outside the top 50. We believe its highly localized footprint provides more revenue stability relative to its nationally focused peers. Additionally, we believe its strong local relationships will assist in accelerating digital revenue growth. Notably, management highlighted its commitment to local audiences, given its ethos is grounded in localism.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

Stocks, Bonds, and Real Estate Markets are All Impacted By U.S. Debt Levels

Who will buy all the U.S. Treasury debt issuance? This week the Treasury Department hinted at its borrowing needs estimate for the third quarter. Its estimated need is $1 trillion-plus, the largest third-quarter need ever. At the same time, the Federal Reserve is reducing its holdings of U.S. debt by a cumulative $90 billion each month, and the U.S. dollar is on a weakening trend which reduces demand for dollar-denominated assets. There are now concerns being raised about the extent to which domestic and foreign demand for U.S. debt issuance will be able to grow to match issuance.

More details surrounding the Treasuries financing needs will be released at 8:30 on Wednesday August 2nd. The large estimate already shared in advance, $1.007 trillion, has analysts beginning to conclude that the U.S. could become hampered with a deteriorating fiscal deficit outlook amid continuing pressure to borrow more.

Two months ago, analysts at Fitch Ratings, a bond credit rating company, put the United States on Rating Watch Negative (RWN) citing, among other things, “fiscal and debt trajectories.” The initial ratings watch came at a time when there was uncertainty about whether the U.S. debt ceiling would be raised. It was not only increased, on June 2nd President Biden signed Congresses bill removing any upper limit on debt issuance until January 2025. The increase in debt, reduced number of buyers, lack of fiscal guardrails, and already higher interest rates on rollover debt could have consequences for all markets. Fitch may be prompted to replace the AAA rating on US Treasuries by assigning a lower rating.

At stake for the broader fixed-income market is that most corporate debt issuance is spread to U.S. Treasury rates of similar duration bonds. If large ongoing auctions over the third quarter deplete demand at market levels Treasury yields would have to trade higher, or government debt would face being illiquid or even default.

In the past U.S. Treasury borrowing need has been met by the perceived safety in the country’s ability to prosper and pay its debts, as well as the reliability of the U.S. dollar as a reserve currency. It’s unclear with less stable relations with China (a large holder of U.S. debt) and the BRICS nations plans to create a gold-based fiat currency, if demand will shrink or grow while U.S. debt issuance climbs.

At stake for the broader real estate market, which is heavily leveraged and therefore greatly impacted by interest rate expenses, is for the cost of borrowing to rise should demand for Treasuries not meet new issuance levels. Thirty-year residential loans are spread off ten-year Treasuries. Further increases in mortgage rates would serve to slow down real estate transactions.

The stock market would likely become bifurcated with stocks tied to big ticket items, typically bought by securing financing, weakening, and stocks that benefit from a strong dollar (higher comparative rates strengthen a native currency) could also do well. These stocks include companies that don’t have a large overseas customer base — if they are net importers, they may benefit even more. Companies that have large borrowing needs, will find their cost of capital has increased as they compete with U.S. Treasury rates. This is why small cap companies, that have very little borrowing needs, tend to perform better than large-cap companies with high debt levels in similar industries.

One Federal government expense that it can’t exercise immediate control over is the interest rate expense of its debt. Over $32 trillion in debt, spread out to mature through 30 years, now holds an average rate of near 2.50%. New debt is issued with almost double that interest rate. This is evident in the chart above that shows interest on debt from 2020 until today increased by $400 billion – with no expected change in its growth rate.

In a Tuesday note title “Treasury Tsunami,” rates strategists at Barclays Anshul Pradhan and Andres Mok wrote, the “Treasury’s latest financing estimates point to a worsening fiscal profile” and “the fiscal picture has worsened significantly since last year.” They point to the likelihood of “a sharp increase in the supply of notes and bonds over the coming quarters,” and cautioned investors against expecting “a typical end-of-cycle bond market rally.”

Whether or not the Fed continues to remain hawkish, if this recipe of greater U.S. debt issuance need continues on its trajectory, with fewer buyers, interest rates will rise. For investors with the common 60/40 portfolios, that is to say 40% in bonds, higher rates will mathematically cause prices of their fixed income holdings to decline. They may receive interest payments every six months, but if interest rates keep increasing, what others are willing to pay for that payment stream declines. In this way, bonds and other fixed income is only the place to hide if you want to be certain of declining values of your holdings.

Take Away

The Fed could stop tightening, and still there would be upward pressure on Treasury rates because of increased supply. Interestingly, this would serve to create a normally sloped yield curve (not inverted) which, according to many that were saying this year’s inverted yield curve is an unmistakable sign of impending recession, they would have another chance at being wrong again by saying an upwardly sloping yield curve is signs the market expects robust growth. Taken in the context of all of 2023s market dynamics and manipulations, neither textbook simplification fits.

If the scenario of higher rates out on the curve unfolds, a higher cost of capital will impact some industries more than others, and international companies differently than pure domestic operations. Consider this as you make your own interest rate and economic projections and adjust your holdings accordingly.

Looking Back at the Markets in July and Forward to August

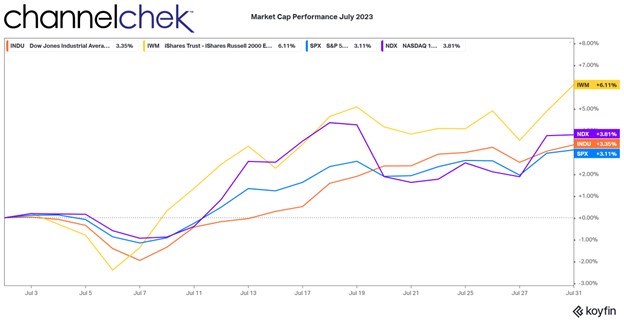

Enthusiasm for the overall stock market remained strong in July. The major indices were all up, and every S&P sector closed in positive territory. Despite the Federal Reserve which continued its monetary policy tightening, and suggestion that it is not finished, markets looked at waning inflation and still strong employment and began to believe a soft landing is now more likely. During the month Nasdaq decided to rebalance the Nasdaq 100, this was completed as of the market open on July 31. The purpose was to allow the index to better reflect price movements in the top 100 Nasdaq stocks. As with the S&P 500, the weighting of the five largest companies represented in the index, has been a concern for many investors that don’t believe the index represents the overall market moves well. On the other side of the scale, for the second month in a row, the small cap Russell 2000 index led the other popular market indexes by a wide margin.

Earnings season or second quarter reporting, which kicked off mid-July, has so far exceeded estimates for many highly followed companies; this has also kept the markets rising in July. Whether the strong market momentum continues through August may depend on if inflation continues to show signs of coming down toward the Fed’s 2% target.

Four broad stock market indices were positive in June. In order, the Russell 2000 Small Caps, Nasdaq 100 Large Caps, the Dow Jones Industrials, and S&P 500 Large Caps.

Small cap stocks are the big winner in June as investors went looking for value. The Russell 2000 rose 6.11%, which follows a large 8.07% gain the previous month. The smaller stocks may now have more positive impetus that could carry over into August. Just prior to the beginning of July, Goldman Sachs had estimated that based on their models, small cap stocks could rise 14% over the next 12 months. This helped small cap stocks continue their outperformance as more investors begin to exercise caution toward the high P/E ratios in larger companies and recognize the historical value still represented in small cap company valuations.

The Nasdaq maintained its growth as big tech retained its appeal despite individual company market caps that have exceeded those of developed countries. The Nasdaq 100 was up 3.81%, following 6.49% in June. The Dow 30 Industrials made headlines for a week as it had a 13 day winning streak. It returned 3.35% during July after a 4.56% increase in June. The S&P 500 was the worst performing index at 3.11% after rising 6.47% the previous month. All major indices are off their all time highs that were reached in Winter 2021.

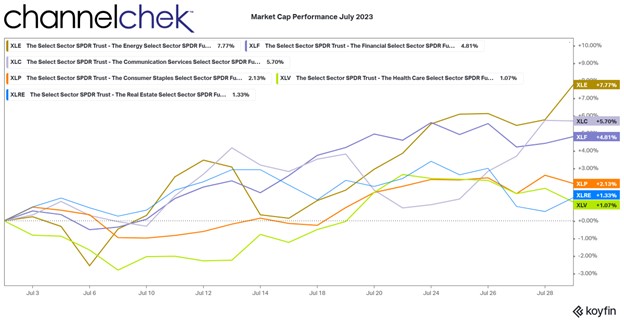

Of the 11 S&P market sectors (SPDRs), even the lowest performer had an above-average one-month return. The chart above reflects the three best-performing sectors and the three worst. The top performer demonstrated the strength of energy during the month as oil and natural gas prices rose.

The energy sector had the best return at 7.77% during July. Continued disruption as countries work toward renewables, the war in Ukraine, and even a coup in Niger all helped the sector attract investors.

Communications was second with a 5.70% return. On June 26, the White House announced internet infrastructure spending plans that helped support and should continue to help many companies in this sector.

Investors began returning to companies in the financial sector as a rebound from March and April when investors became leary after a few bank failures. Bank earnings in July showed better-than-expected performance on many of the large banks. This helped the move back into financials. The sector returned 4.81% in July.

The three worst-performing sectors also indicate the month was very positive. Consumer Staples which was third from the bottom returned a respectable 2.13%. Investors view this sector as a defensive play in times of economic uncertainty. Its move shows less interest as investors become more positive on the economic outlook.

The second to weakest performer is Real Estate. The sector has held up fairly well considering how closely its performance can be tied to interest rates. The 1.33% return in June is indicative of the entire market’s resilience yet lower probability of the sector in light of a still hawkish Fed.

Health Care is still out of favor. Investors had a lower level of interest in healthcare stocks, which are also considered defensive. Lower market volatility and a brighter economic outlook have investors less interested in defensive stocks. Also, interest rates could be affecting big pharma as dividends on the stocks become less appealing as bond yields rise.

Looking Forward

The job market is strong, inflation is tapering, and consumers are more confident. Analysts are now expecting that companies that have been waiting for a more friendly market to go public are considering now as a good time for their IPO.

Bitcoin and other cryptocurrencies, along with stocks of crypto exchanges, are still faced with uncertain legal outcomes and regulatory positioning. Artificial intelligence as a growing component of many industries, is driving interest as investors look to uncover those companies that will benefit the most both directly (ie: selling chips) or indirectly (ie: gain efficiency).

The rotation to small caps and sectors that perform better when the economy improves has a lot of momentum heading into August. This sector has a long way to run before it catches up with the large cap sectors that it historically surpasses over time.

Take-Away

The market showed more signs of relief in July as the conversation changed from an upcoming recession to a likely soft landing. With five more months in 2023, the markets have rallied and are not showing signs of retrenching. This is especially true of small cap stocks that for the second month have handily outperformed large caps.

Preliminary Data Show that Oxytocin Decreases Impulsivity and Reduces Food Intake

TNX-1900 (Intranasal Potentiated Oxytocin) May Serve as a Novel Neuroendocrine Treatment for Binge-Eating Disorder

CHATHAM, N.J., July 31, 2023 (GLOBE NEWSWIRE) — Tonix Pharmaceuticals Holding Corp. (Nasdaq: TNXP) (Tonix or the Company), a clinical-stage biopharmaceutical company, today announced that the first participant was enrolled in the investigator-initiated Phase 2 Study of The Results of Oxytocin in Binge Eating ‘STROBE’ study of TNX-1900 (intranasal potentiated oxytocin) for the treatment of binge-eating disorder at the Massachusetts General Hospital (MGH). The aim of the study is to investigate the efficacy and safety of TNX-1900 as a novel therapeutic agent to reduce binge eating frequency in adults with binge-eating disorder. Tonix is supporting the STROBE study through a clinical trial agreement with MGH. MGH is the sponsor of the trial, which is being conducted under an investigator-initiated investigational new drug (IND) application.

The 8-week double-blind, placebo-controlled trial has a target enrollment of at least 60 participants 18-45 years old with binge-eating disorder.

“Binge-eating disorder is identified as a reduced ability to control behavioral impulses and formed habits, disrupting the regulation of food intake and energy balance,”1-4 said Seth Lederman, M.D., Chief Executive Officer of Tonix Pharmaceuticals. “While existing treatment options may produce remission from binge eating in some cases, up to 50% of patients continue to engage in binge eating.”5-7

Elizabeth A. Lawson, M.D., M.M.Sc., Director, Interdisciplinary Oxytocin Research Program in the Neuroendocrine Unit, Department of Medicine, Massachusetts General Hospital and principal investigator of the study added, “Individuals with binge-eating disorder experience loss of control over eating that is thought to be driven by increased hedonic drive to eat as well as impulsivity.8-10 The oxytocin system has been linked to likelihood of lifetime binge eating in women11, and our preliminary studies of intranasal oxytocin at the dose used in this trial show that oxytocin modulates areas of the brain responsible for hedonic eating and impulse control12, improves impulsivity13, and reduces caloric intake.14 The goal of the STROBE study is to assess whether 8 weeks intranasal administration of oxytocin will decrease binge eating frequency by lowering the drive to eat and improving impulse control.”

About the Phase 2 STROBE Study

The Phase 2 STROBE study is a randomized, double blind, placebo-controlled study to evaluate the efficacy and safety of TNX-1900 for the treatment of binge-eating disorder in adults. The 8-week trial has a target enrollment of at least 60 participants 18-45 years old with binge-eating disorder. Subjects will be randomized to receive TNX-1900 or placebo and will be studied at Massachusetts General Hospital. Subjects will self-administer TNX-1900 or placebo as two sprays total (one spray in each nostril) up to four times per day for 8 weeks. The primary endpoint is 8-week change from baseline in binge frequency.

For more information, see ClinicalTrials.gov Identifier: NCT05664516

About Binge Eating Disorder

Binge-eating disorder (BED) is a psychiatric illness characterized by frequent episodes of uncontrollable consumption of large amounts of food. It is the most common eating disorder and often leads to obesity-associated complications and later psychopathology15. BED is characterized by increased homeostatic appetite and sensitivity to reward (including food reward)16, which may lead to initiation of binge episodes, and a reduced ability to control behavioral impulses and formed habits, creating an imbalance in the sensitive interplay between these bottom-up and top-down processes governing the adaptive regulation of food intake and energy balance1-4.

About TNX-1900

TNX-1900 (intranasal potentiated oxytocin) is a proprietary formulation of oxytocin in development as a candidate for prevention of chronic migraine and other conditions. In 2020, TNX-1900 was acquired from Trigemina, Inc. who had licensed the technology underlying the composition and method from Stanford University. TNX-1900 is a drug-device combination product, based on an intranasal actuator device that delivers oxytocin into the nasal cavity. Oxytocin is a naturally occurring human peptide hormone that also acts as a neurotransmitter in the brain. Oxytocin has no recognized addiction potential. It has been observed that low oxytocin levels in the body are associated with increases in migraine headache frequency, and that increased oxytocin levels are associated with fewer migraine headaches. Certain other chronic pain conditions are also associated with decreased oxytocin levels. Migraine attacks are caused, in part, by the activity of pain-sensing trigeminal neurons which, when activated, release of calcitonin gene-related peptide (CGRP) which binds to receptors on other nerve cells and starts a cascade of events that is believed to result in headache. Oxytocin when delivered via the nasal route, concentrates in the trigeminal system17 resulting in binding of oxytocin to receptors on neurons in the trigeminal system, inhibiting the release of CGRP and transmission of pain signals returning from the site of CGRP release.18 Blocking CGRP release is a distinct mechanism compared with CGRP antagonist and anti-CGRP antibody drugs, which block the binding of CGRP to its receptor. With TNX-1900, the addition of magnesium to the oxytocin formulation enhances oxytocin receptor binding19 as well as its inhibitory effects on trigeminal neurons and resultant craniofacial analgesic effects, as demonstrated in animal models20. Intranasal oxytocin has been shown to be well tolerated in several clinical trials in both adults and children21. Targeted nasal delivery results in low systemic exposure and lower risk of non-nervous system, off-target effects, which could potentially occur with systemic CGRP antagonists such as anti-CGRP antibodies22. For example, CGRP has roles in dilating blood vessels in response to ischemia, including in the heart. The Company believes nasally targeted delivery of oxytocin could translate into selective blockade of CGRP release from neurons in the trigeminal ganglion and not throughout the body, which could be a potential safety advantage over systemic CGRP inhibition. In addition, daily dosing is more rapidly reversible, in contrast to monthly or quarterly dosing, as is the case with anti-CGRP antibodies, giving physicians and their patients greater control. In addition to chronic migraine, TNX-1900 will be developed for treatment of episodic migraine, binge eating disorder, craniofacial pain conditions, and insulin resistance. Tonix also has a license with the University of Geneva to use TNX-1900 for the treatment of insulin resistance and related conditions.

About TNX-2900

TNX-2900 is another intranasal potentiated oxytocin-based therapeutic candidate, being developed for the treatment of Prader-Willi syndrome, or PWS. The technology for TNX-2900 was licensed from the French National Institute of Health and Medical Research. PWS, an orphan condition, is a rare genetic disorder of failure to thrive in infancy, associated with uncontrolled appetite later in childhood.

1Dawe S and Loxton NJ. NeurosciBiobehav Rev. 2004; 28(3):343-351 2Giel KE, et al. Nutrients. 2017; 9(11) 3Hernandez D, et al. Obesity (Silver Spring). 2019; 27(4):629-635 4Schag K, et al. Obes Rev. 2013; 14(6):477-495 5Hilbert A, et al. Int J Eat Disord. 2020; 53(9):1353-1376 6Reas DL and Grilo CM. Expert OpinEmerg Drugs. 2014; 19(1):99-142 7Wilson GT. Psychiatr Clin North Am. 2011; 34(4):773-783 8Giel KE, et al. Nutrients. 2017. 9(11) 9Hernandez D, et al. Obesity (Silver Spring). 2019. 27(4):629-635 10Schag K, et al. Obes Rev. 2013. 14(6):477-95 11Micali N, et al. Eur Eat Disord Rev. 2017; 25(1):19-25 12Plessow F, et al. Neuropsychopharmacology. 2018. 43(3):638-645 13Plessow F, et al. Obesity (Silver Spring), 2021. 29(1):56-61 14Lawson EA, et al. Obesity (Silver Spring). 2015; 23(5):950-956 15Field A, et al. Pediatrics. 2012; 130 (2):e289–e295 16Bulik CM, et al. Nature Neuroscience. 2022. 25(5):543-554 17Yeomans DC, et al. Transl Psychiatry. 2021. 11(1):388 18Tzabazis A, et al. Cephalalgia. 2016. 36(10):943-50 19Antoni FA and Chadio SE. Biochem J. 1989. 257(2):611-4 20Cai Q, et al. Psychiatry Clin Neurosci. 2018. 72(3):140-151 21Yeomans, DC et al. 2017. US patent US2017368095 22MaassenVanDenBrink A, et al. Trends Pharmacol Sci. 2016. 37(9):779-788

Tonix Pharmaceuticals Holding Corp.*

Tonix is a biopharmaceutical company focused on commercializing, developing, discovering and licensing therapeutics to treat and prevent human disease and alleviate suffering. Tonix markets Zembrace® SymTouch® (sumatriptan injection) 3 mg and Tosymra® (sumatriptan nasal spray) 10 mg. Zembrace SymTouch and Tosymra are each indicated for the treatment of acute migraine with or without aura in adults. Tonix’s development portfolio is composed of central nervous system (CNS), rare disease, immunology and infectious disease product candidates. Tonix’s CNS development portfolio includes both small molecules and biologics to treat pain, neurologic, psychiatric and addiction conditions. Tonix’s lead CNS candidate, TNX-102 SL (cyclobenzaprine HCl sublingual tablet), is in mid-Phase 3 development for the management of fibromyalgia, nearing complete enrollment in a potentially registration-enabling study, with topline data expected in the fourth quarter of 2023. TNX-102 SL is also being developed to treat Long COVID, a chronic post-acute COVID-19 condition. Enrollment in a Phase 2 study has been completed, and topline results are expected in the third quarter of 2023. TNX-601 ER (tianeptine hemioxalate extended-release tablets), a once-daily formulation being developed as a treatment for major depressive disorder (MDD), is nearing complete enrollment with topline results expected in the fourth quarter of 2023. TNX-4300 (estianeptine) is a small molecule oral therapeutic in preclinical development to treat MDD, Alzheimer’s disease and Parkinson’s disease. TNX-1900 (intranasal potentiated oxytocin), in development for chronic migraine, is currently enrolling with topline data expected in the fourth quarter of 2023. TNX-1300 (cocaine esterase) is a biologic designed to treat cocaine intoxication and has been granted Breakthrough Therapy designation by the FDA. A Phase 2 study of TNX-1300 is expected to be initiated in the third quarter of 2023. Tonix’s rare disease development portfolio includes TNX-2900 (intranasal potentiated oxytocin) for the treatment of Prader-Willi syndrome. TNX-2900 has been granted Orphan Drug designation by the FDA. Tonix’s immunology development portfolio includes biologics to address organ transplant rejection, autoimmunity and cancer, including TNX-1500, which is a humanized monoclonal antibody targeting CD40-ligand (CD40L or CD154) being developed for the prevention of allograft rejection and for the treatment of autoimmune diseases. A Phase 1 study of TNX-1500 is expected to be initiated in the third quarter of 2023. Tonix’s infectious disease pipeline includes TNX-801, a vaccine in development to prevent smallpox and mpox. TNX-801 also serves as the live virus vaccine platform or recombinant pox vaccine platform for other infectious diseases. The infectious disease development portfolio also includes TNX-3900 and TNX-4000, classes of broad-spectrum small molecule oral antivirals.

*Tonix’s product development candidates are investigational new drugs or biologics and have not been approved for any indication.

Tonix Medicines has contracted to acquire the Zembrace SymTouch and Tosymra registered trademarks. Intravail is a registered trademark of Aegis Therapeutics, LLC, a wholly owned subsidiary of Neurelis, Inc.

This press release and further information about Tonix can be found at www.tonixpharma.com.

Forward Looking Statements

Certain statements in this press release are forward-looking within the meaning of the Private Securities Litigation Reform Act of 1995. These statements may be identified by the use of forward-looking words such as “anticipate,” “believe,” “forecast,” “estimate,” “expect,” and “intend,” among others. These forward-looking statements are based on Tonix’s current expectations and actual results could differ materially. There are a number of factors that could cause actual events to differ materially from those indicated by such forward-looking statements. These factors include, but are not limited to, risks related to the failure to obtain FDA clearances or approvals and noncompliance with FDA regulations; risks related to the failure to successfully market any of our products; risks related to the timing and progress of clinical development of our product candidates; our need for additional financing; uncertainties of patent protection and litigation; uncertainties of government or third party payor reimbursement; limited research and development efforts and dependence upon third parties; and substantial competition. As with any pharmaceutical under development, there are significant risks in the development, regulatory approval and commercialization of new products. Tonix does not undertake an obligation to update or revise any forward-looking statement. Investors should read the risk factors set forth in the Annual Report on Form 10-K for the year ended December 31, 2022, as filed with the Securities and Exchange Commission (the “SEC”) on March 13, 2023, and periodic reports filed with the SEC on or after the date thereof. All of Tonix’s forward-looking statements are expressly qualified by all such risk factors and other cautionary statements. The information set forth herein speaks only as of the date thereof.

Zembrace® SymTouch® (sumatriptan Injection): IMPORTANT SAFETY INFORMATION

Zembrace SymTouch (Zembrace) can cause serious side effects, including heart attack and other heart problems, which may lead to death. Stop use and get emergency help if you have any signs of a heart attack:

discomfort in the center of your chest that lasts for more than a few minutes or goes away and comes back

severe tightness, pain, pressure, or heaviness in your chest, throat, neck, or jaw

pain or discomfort in your arms, back, neck, jaw or stomach

shortness of breath with or without chest discomfort

breaking out in a cold sweat

nausea or vomiting

feeling lightheaded

Zembrace is not for people with risk factors for heart disease (high blood pressure or cholesterol, smoking, overweight, diabetes, family history of heart disease) unless a heart exam shows no problem.

Do not use Zembrace if you have:

history of heart problems

narrowing of blood vessels to your legs, arms, stomach, or kidney (peripheral vascular disease)

uncontrolled high blood pressure

hemiplegic or basilar migraines. If you are not sure if you have these, ask your provider.

had a stroke, transient ischemic attacks (TIAs), or problems with blood circulation

severe liver problems

taken any of the following medicines in the last 24 hours: almotriptan, eletriptan, frovatriptan, naratriptan, rizatriptan, ergotamines, dihydroergotamine.

are taking certain antidepressants, known as monoamine oxidase (MAO)-A inhibitors or it has been 2 weeks or less since you stopped taking a MAO-A inhibitor. Ask your provider for a list of these medicines if you are not sure.

an allergy to sumatriptan or any of the components of Zembrace

Tell your provider about all of your medical conditions and medicines you take, including vitamins and supplements.

Zembrace can cause dizziness, weakness, or drowsiness. If so, do not drive a car, use machinery, or do anything where you need to be alert.

Zembrace may cause serious side effects including:

changes in color or sensation in your fingers and toes

sudden or severe stomach pain, stomach pain after meals, weight loss, nausea or vomiting, constipation or diarrhea, bloody diarrhea, fever

cramping and pain in your legs or hips; feeling of heaviness or tightness in your leg muscles; burning or aching pain in your feet or toes while resting; numbness, tingling, or weakness in your legs; cold feeling or color changes in one or both legs or feet

increased blood pressure including a sudden severe increase even if you have no history of high blood pressure

medication overuse headaches from using migraine medicine for 10 or more days each month. If your headaches get worse, call your provider.

serotonin syndrome, a rare but serious problem that can happen in people using Zembrace, especially when used with anti-depressant medicines called SSRIs or SNRIs. Call your provider right away if you have: mental changes such as seeing things that are not there (hallucinations), agitation, or coma; fast heartbeat; changes in blood pressure; high body temperature; tight muscles; or trouble walking.

hives (itchy bumps); swelling of your tongue, mouth, or throat

seizures even in people who have never had seizures before

The most common side effects of Zembrace include: pain and redness at injection site; tingling or numbness in your fingers or toes; dizziness; warm, hot, burning feeling to your face (flushing); discomfort or stiffness in your neck; feeling weak, drowsy, or tired.

Tell your provider if you have any side effect that bothers you or does not go away. These are not all the possible side effects of Zembrace. For more information, ask your provider.

This is the most important information to know about Zembrace but is not comprehensive. For more information, talk to your provider and read the Patient Information and Instructions for Use. You can also visit www.upsher-smith.com or call 1-888-650-3789.

You are encouraged to report adverse effects of prescription drugs to the FDA. Visit www.fda.gov/medwatch, or call 1-800-FDA-1088.

INDICATION AND USAGE

Zembrace is a prescription medicine used to treat acute migraine headaches with or without aura in adults who have been diagnosed with migraine.

Zembrace is not used to prevent migraines. It is not known if it is safe and effective in children under 18 years of age.

Tosymra can cause serious side effects, including heart attack and other heart problems, which may lead to death. Stop Tosymra and get emergency medical help if you have any signs of heart attack:

discomfort in the center of your chest that lasts for more than a few minutes or goes away and comes back

severe tightness, pain, pressure, or heaviness in your chest, throat, neck, or jaw

pain or discomfort in your arms, back, neck, jaw, or stomach

shortness of breath with or without chest discomfort

breaking out in a cold sweat

nausea or vomiting

feeling lightheaded

Tosymra is not for people with risk factors for heart disease (high blood pressure or cholesterol, smoking, overweight, diabetes, family history of heart disease) unless a heart exam is done and shows no problem.

Do not use Tosymra if you have:

history of heart problems

narrowing of blood vessels to your legs, arms, stomach, or kidney (peripheral vascular disease)

uncontrolled high blood pressure

severe liver problems

hemiplegic or basilar migraines. If you are not sure if you have these, ask your healthcare provider.

had a stroke, transient ischemic attacks (TIAs), or problems with blood circulation

taken any of the following medicines in the last 24 hours: almotriptan, eletriptan, frovatriptan, naratriptan, rizatriptan, ergotamines, or dihydroergotamine. Ask your provider if you are not sure if your medicine is listed above.

are taking certain antidepressants, known as monoamine oxidase (MAO)-A inhibitors or it has been 2 weeks or less since you stopped taking a MAO-A inhibitor. Ask your provider for a list of these medicines if you are not sure.

an allergy to sumatriptan or any ingredient in Tosymra

Tell your provider about all of your medical conditions and medicines you take, including vitamins and supplements.

Tosymra can cause dizziness, weakness, or drowsiness. If so, do not drive a car, use machinery, or do anything where you need to be alert.

Tosymra may cause serious side effects including:

changes in color or sensation in your fingers and toes

sudden or severe stomach pain, stomach pain after meals, weight loss, nausea or vomiting, constipation or diarrhea, bloody diarrhea, fever

cramping and pain in your legs or hips, feeling of heaviness or tightness in your leg muscles, burning or aching pain in your feet or toes while resting, numbness, tingling, or weakness in your legs, cold feeling or color changes in one or both legs or feet

increased blood pressure including a sudden severe increase even if you have no history of high blood pressure

medication overuse headaches from using migraine medicine for 10 or more days each month. If your headaches get worse, call your provider.

serotonin syndrome, a rare but serious problem that can happen in people using Tosymra, especially when used with anti-depressant medicines called SSRIs or SNRIs. Call your provider right away if you have: mental changes such as seeing things that are not there (hallucinations), agitation, or coma; fast heartbeat; changes in blood pressure; high body temperature; tight muscles; or trouble walking.

hives (itchy bumps); swelling of your tongue, mouth, or throat

seizures even in people who have never had seizures before

The most common side effects of Tosymra include: tingling, dizziness, feeling warm or hot, burning feeling, feeling of heaviness, feeling of pressure, flushing, feeling of tightness, numbness, application site (nasal) reactions, abnormal taste, and throat irritation.

Tell your provider if you have any side effect that bothers you or does not go away. These are not all the possible side effects of Tosymra. For more information, ask your provider.

This is the most important information to know about Tosymra but is not comprehensive. For more information, talk to your provider and read the Patient Information and Instructions for Use. You can also visit www.upsher-smith.com or call 1-888-650-3789.

You are encouraged to report negative side effects of prescription drugs to the FDA. Visit www.fda.gov/medwatch, or call 1-800-FDA-1088.

INDICATION AND USAGE Tosymra is a prescription medicine used to treat acute migraine headaches with or without aura in adults.

Tosymra is not used to treat other types of headaches such as hemiplegic or basilar migraines or cluster headaches.

Tosymra is not used to prevent migraines. It is not known if Tosymra is safe and effective in children under 18 years of age.

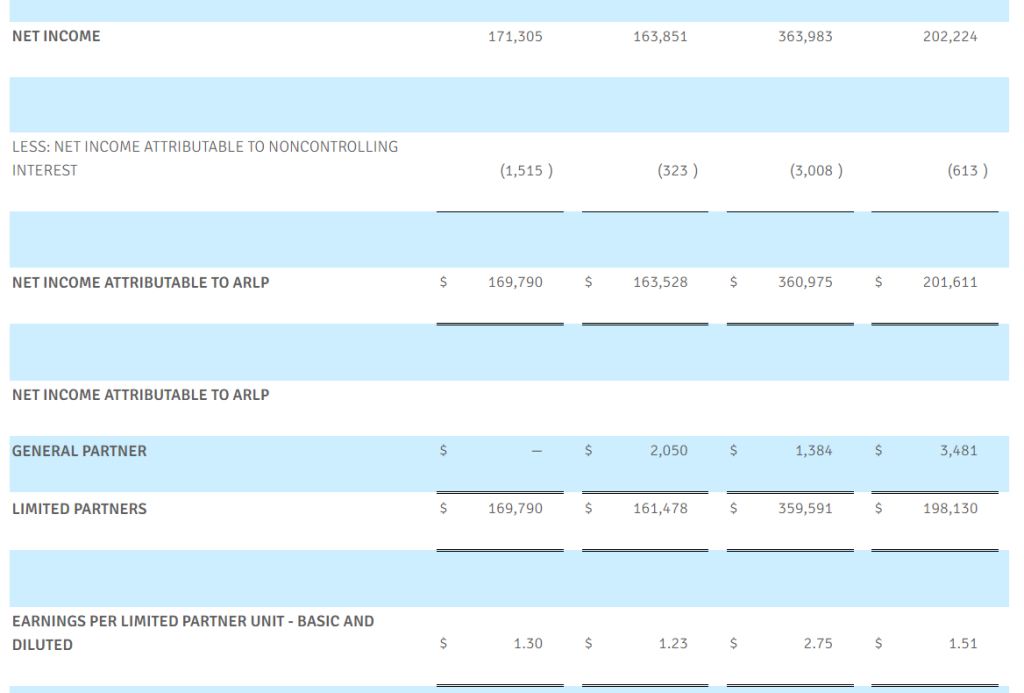

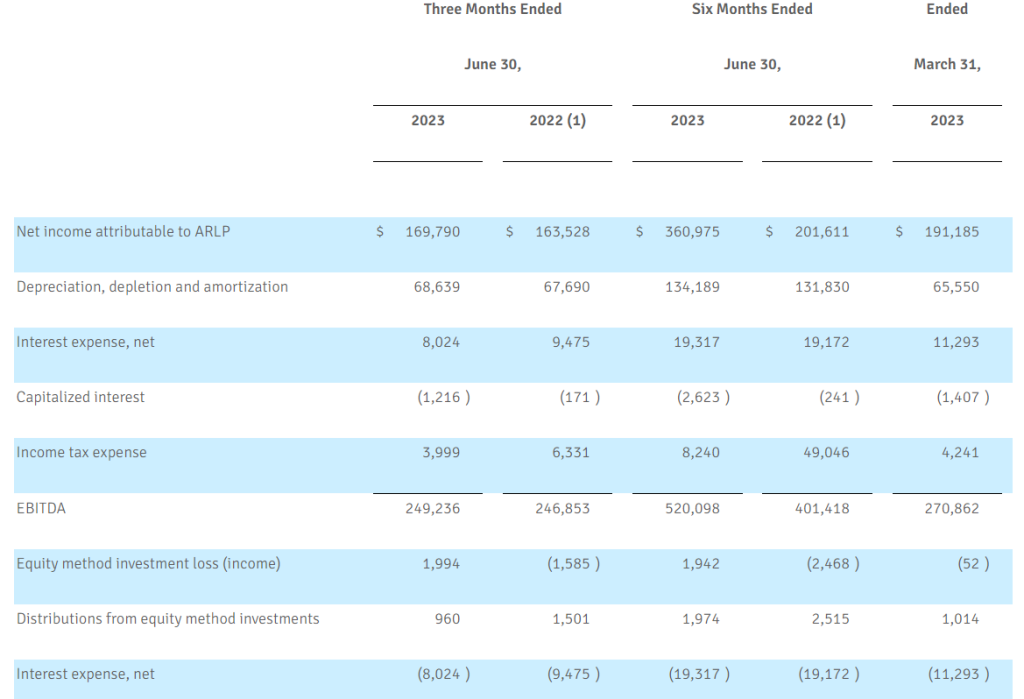

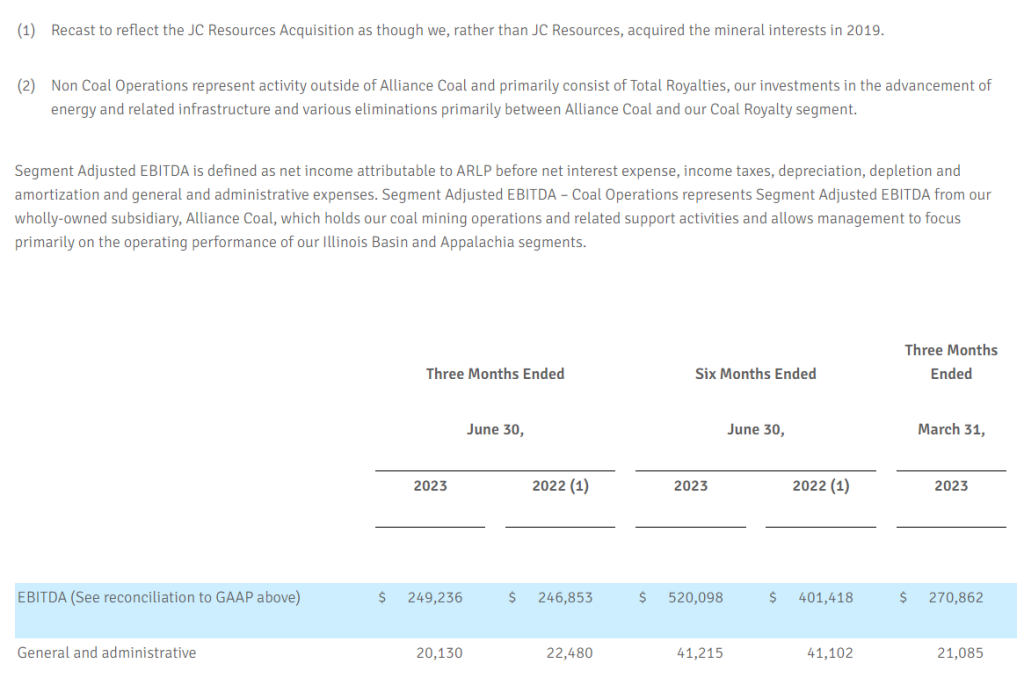

Net income of $169.8 million, or $1.30 per unit, a 3.8% increase compared to $163.5 million, or $1.23 per unit for the 2022 Quarter

EBITDA of $249.2 million, up 1.0% year-over-year

Repurchased $34.2 million of outstanding senior notes during the 2023 Quarter and redeemed an additional $50.0 million of senior notes in July 2023

Declared a quarterly cash distribution in July 2023 of $0.70 per unit, or $2.80 per unit annualized, up 75.0% year-over-year

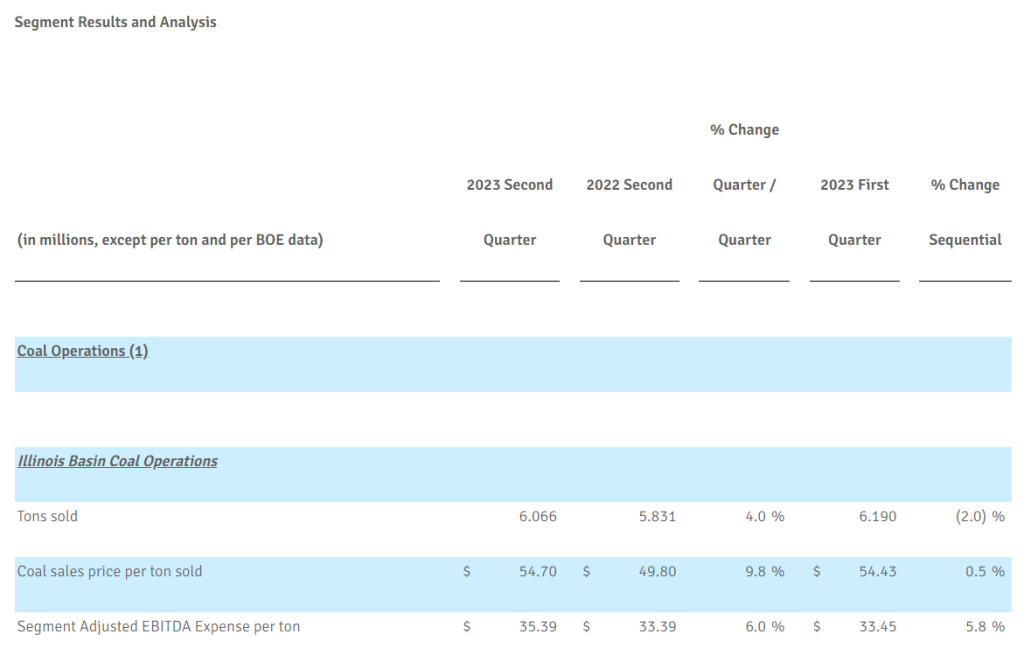

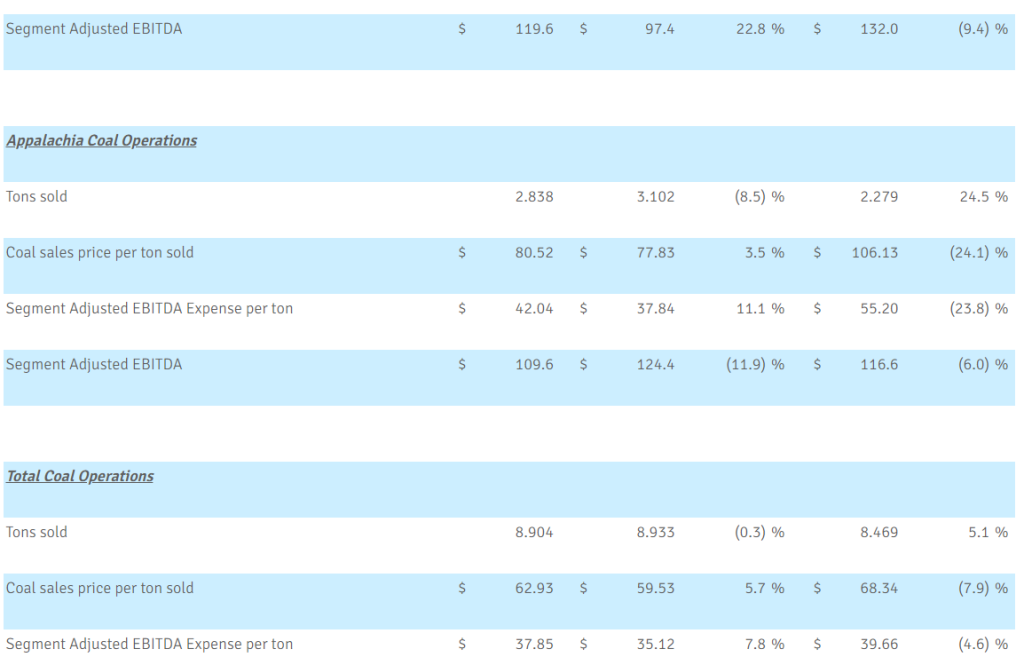

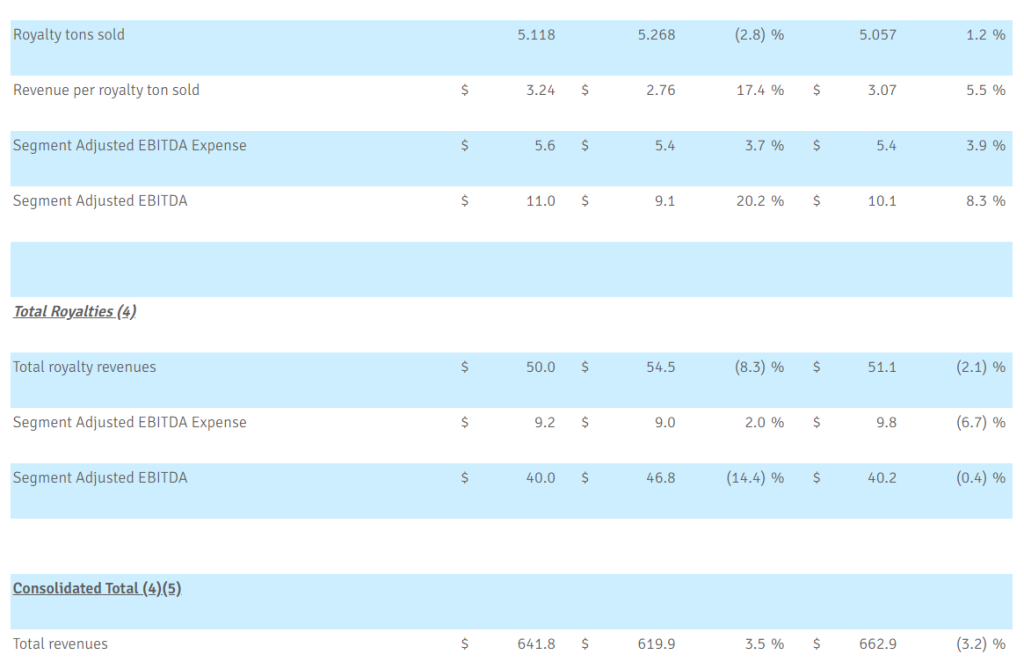

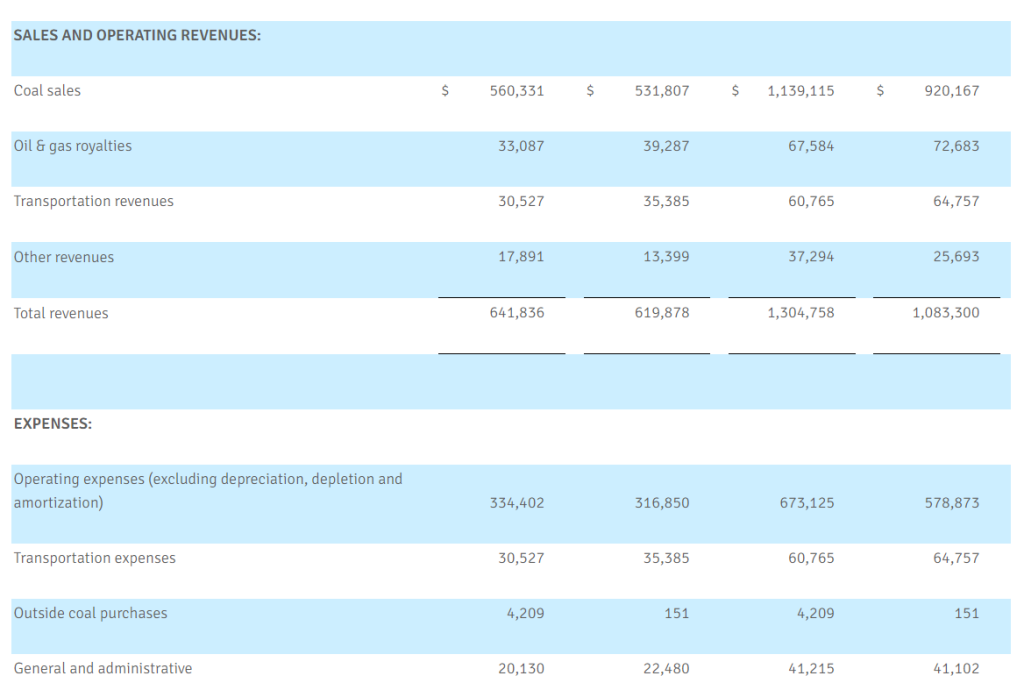

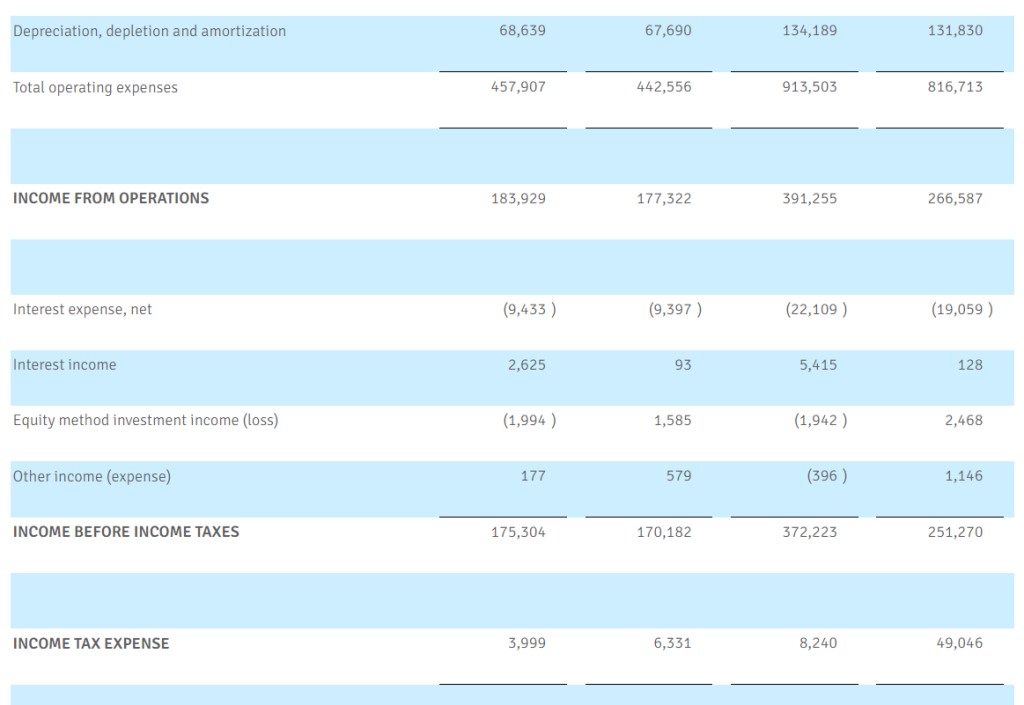

TULSA, Okla.–(BUSINESS WIRE)– Alliance Resource Partners, L.P. (NASDAQ: ARLP) (“ARLP” or the “Partnership”) today reported increased financial and operating results for the quarter ended June 30, 2023 (the “2023 Quarter”) compared to the quarter ended June 30, 2022 (the “2022 Quarter”). Total revenues in the 2023 Quarter increased 3.5% to $641.8 million compared to $619.9 million for the 2022 Quarter driven primarily by higher coal sales price per ton, which rose by 5.7%, partially offset by lower oil & gas royalty prices. Increased revenues, partially offset by higher total operating expenses, led to net income for the 2023 Quarter of $169.8 million, or $1.30 per basic and diluted limited partner unit, compared to $163.5 million, or $1.23 per basic and diluted limited partner unit, for the 2022 Quarter. (Unless otherwise noted, all references in the text of this release to “net income” refer to “net income attributable to ARLP.”)

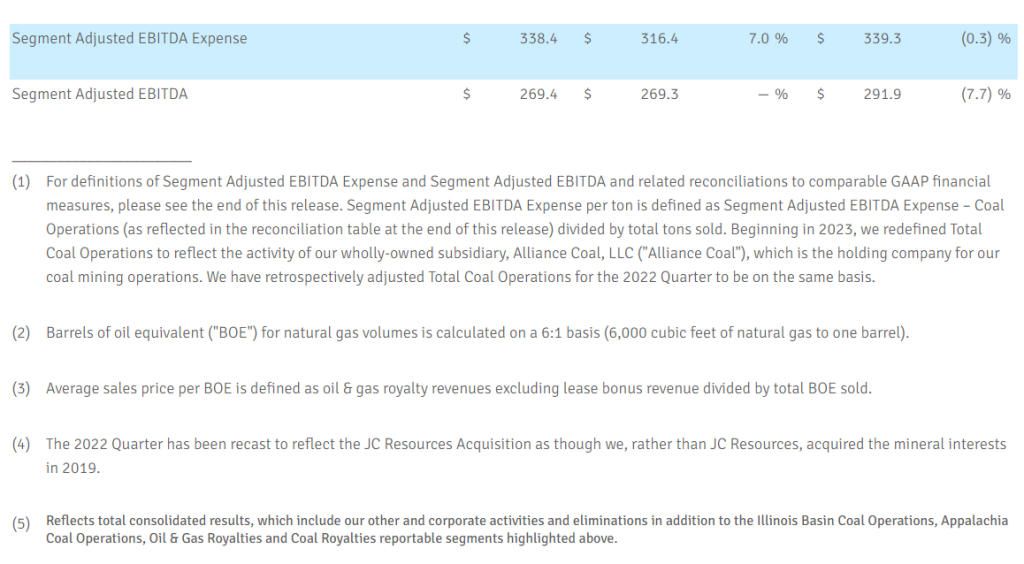

Compared to the quarter ended March 31, 2023 (the “Sequential Quarter”), total revenues in the 2023 Quarter decreased by 3.2% primarily as a result of lower average coal sales prices of $62.93 per ton sold compared to $68.34 per ton sold in the Sequential Quarter, partially offset by higher coal sales volumes, which rose 5.1% to 8.9 million tons sold in the 2023 Quarter. Lower revenues contributed to a reduction in net income and EBITDA of 11.2% and 8.0%, respectively, compared to the Sequential Quarter. (For a definition of EBITDA and related reconciliation to its comparable GAAP financial measure, please see the end of this release.)

Financial and operating results for the six months ended June 30, 2023 (the “2023 Period”) increased compared to the six months ended June 30, 2022 (the “2022 Period”). Coal sales prices and coal sales revenues during the 2023 Period were higher by 21.8% and 23.8%, respectively, compared to the 2022 Period. Increased revenues and lower income tax expense, partially offset by higher total operating expenses, in the 2023 Period drove net income higher by 79.0% and EBITDA increased 29.6%, both as compared to the 2022 Period.

CEO Commentary

“ARLP delivered solid results during the second quarter of 2023, keeping us on track to deliver record financial results this year,” commented Joseph W. Craft III, Chairman, President and Chief Executive Officer. “Continued strength in our contract book positioned our coal operations to achieve higher realized pricing per ton sold and Segment Adjusted EBITDA relative to the 2022 Quarter and the 2022 Period. Our year-to-date results have been impressive despite coal demand, both domestically and globally, being lower than we expected entering this year, due to slower economic growth, mild weather in our targeted markets, and lower natural gas prices.”

Mr. Craft added, “Recent reports of sustained, record heat in many parts of the U.S. should once again emphasize our nation’s critical need for a reliable, affordable, and diverse energy mix. Markets can turn quickly in response to moderate swings in demand, particularly when supply remains constrained and policy decisions impact reliability. Our operations continue to provide a low-cost, secure source of supply for our customers, and with our recent actions to further strengthen our balance sheet, we expect to do so well into the future.”

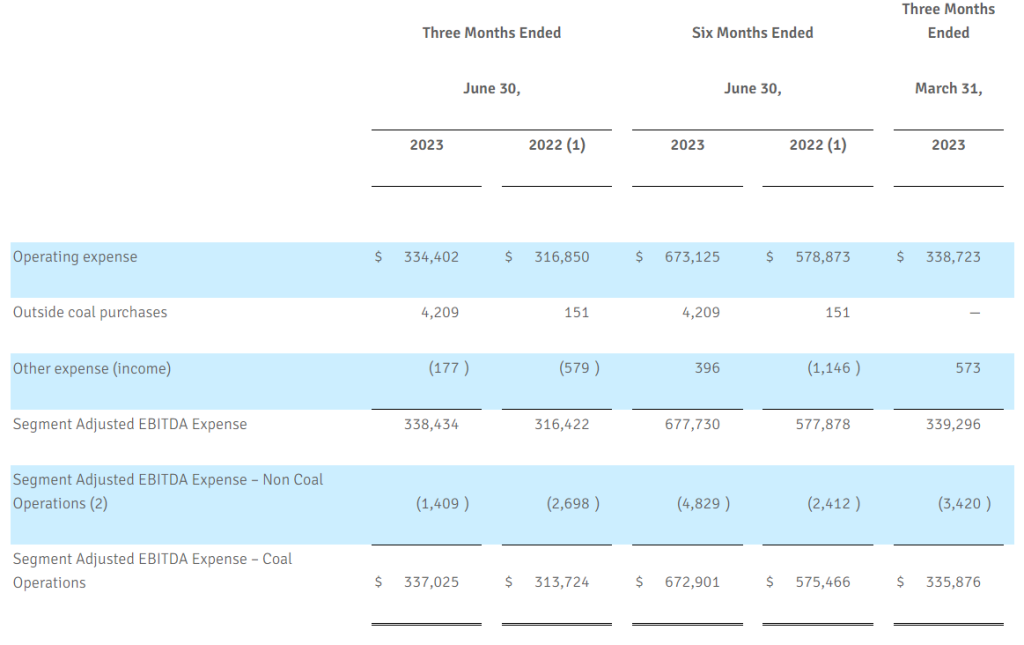

Coal Operations

ARLP’s coal sales prices per ton increased compared to the 2022 Quarter as improved domestic price realizations drove coal sales prices higher by 9.8% and 3.5% in the Illinois Basin and Appalachia, respectively. Compared to the Sequential Quarter, lower domestic and export prices led to a decrease of 24.1% in coal sales prices in Appalachia. Tons sold increased by 4.0% in the Illinois Basin compared to the 2022 Quarter due primarily to increased volumes from the Hamilton and Warrior mines. Appalachia coal sales volumes decreased by 8.5% compared to the 2022 Quarter as a result of reduced export sales across the region and lower production from our MC Mining operation. Compared to the Sequential Quarter, Illinois Basin coal sales volumes decreased 2.0% due to lower volumes from River View while coal sales volumes increased by 24.5% in Appalachia due to higher volumes from Tunnel Ridge as a result of longwall moves at the mine in the Sequential Quarter. ARLP ended the 2023 Quarter with total coal inventory of 1.8 million tons, representing an increase of 0.2 million tons and 0.5 million tons compared to the end of the 2022 and Sequential Quarters, respectively.

Segment Adjusted EBITDA Expense per ton increased by 6.0% in the Illinois Basin compared to the 2022 Quarter, resulting from higher labor-related expenses and maintenance costs as well as increased sales-related expenses due to higher price realizations. Segment Adjusted EBITDA Expense per ton in Appalachia increased by 11.1% compared to the 2022 Quarter, due primarily to increased labor-related expenses, purchased coal and higher inventory charges, partially offset by increased recoveries and lower selling expenses due to a greater mix of coal sales from operations in states with lower severance taxes per ton during the 2023 Quarter. Compared to the Sequential Quarter, Segment Adjusted EBITDA Expense per ton increased 5.8% in the Illinois Basin primarily due to reduced coal sales volumes from our lower cost Gibson South and River View mines during the 2023 Quarter. In Appalachia, Segment Adjusted EBITDA Expense per ton decreased 23.8% compared to the Sequential Quarter as a result of higher sales volumes from our lower cost Tunnel Ridge mine during the 2023 Quarter, increased recoveries across the region and longwall moves at Tunnel Ridge during the Sequential Quarter.

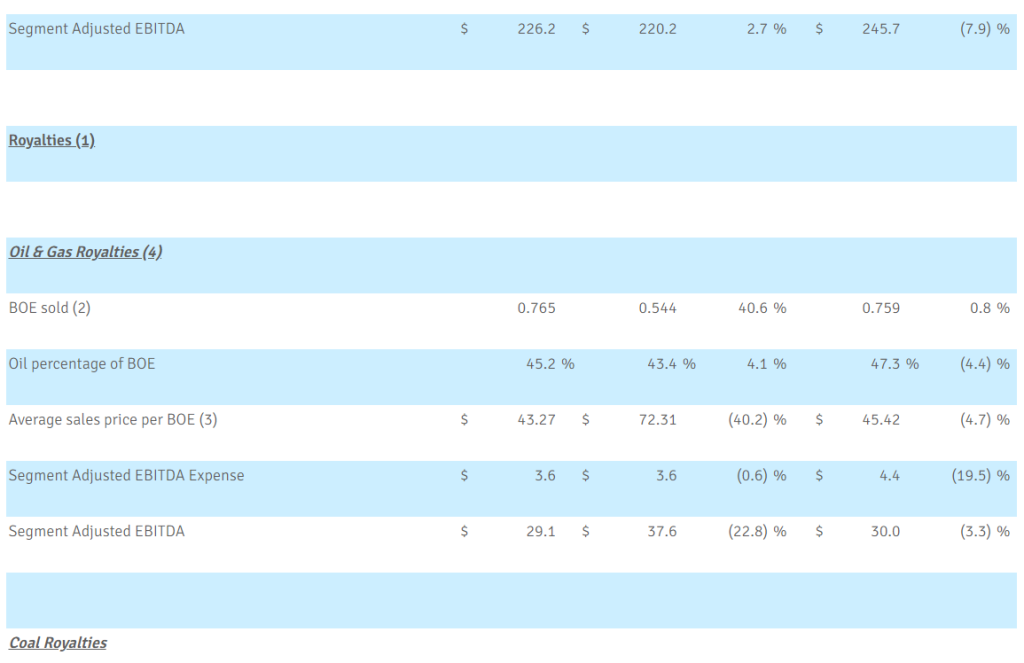

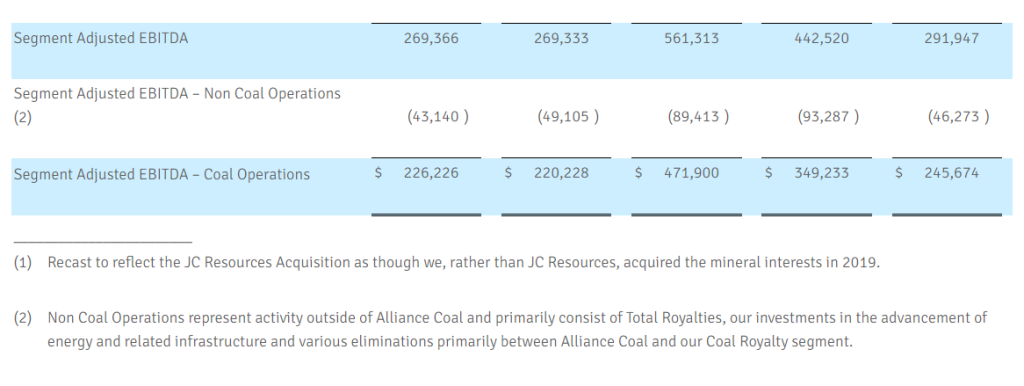

Royalties

Segment Adjusted EBITDA for the Oil & Gas Royalties segment decreased to $29.1 million in the 2023 Quarter compared to $37.6 million and $30.0 million in the 2022 and Sequential Quarters, respectively, primarily due to lower average sales prices per BOE, partially offset by higher BOE volumes sold. Higher BOE volumes during the 2023 Quarter compared to the 2022 Quarter resulted from increased drilling and completion activities on our interests and the acquisition of additional oil & gas mineral interests.

Segment Adjusted EBITDA for the Coal Royalties segment increased to $11.0 million for the 2023 Quarter compared to $9.1 million and $10.1 million for the 2022 and Sequential Quarters, respectively, as a result of higher average royalty rates per ton received from the Partnership’s mining subsidiaries.

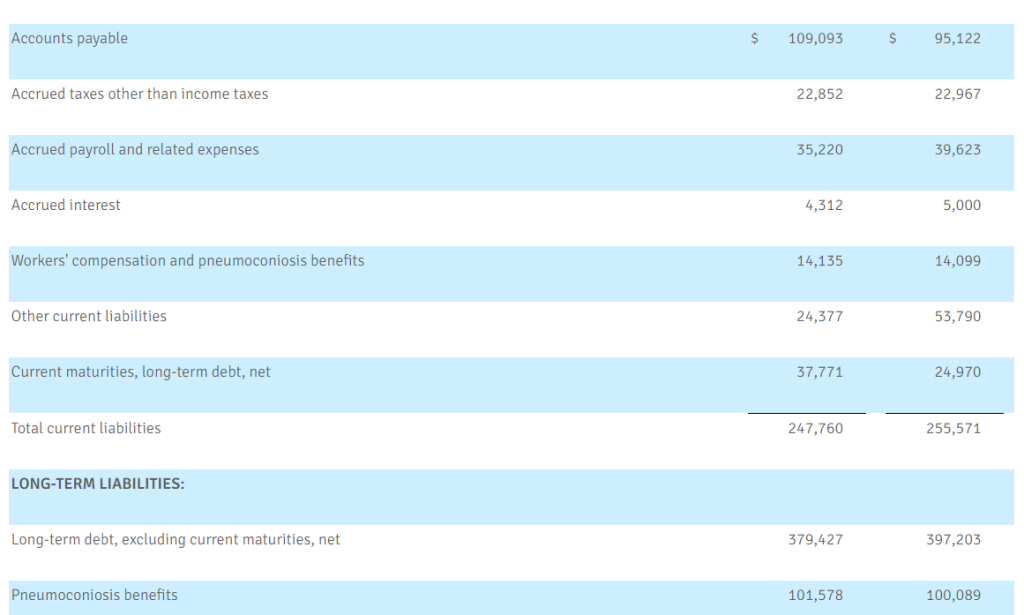

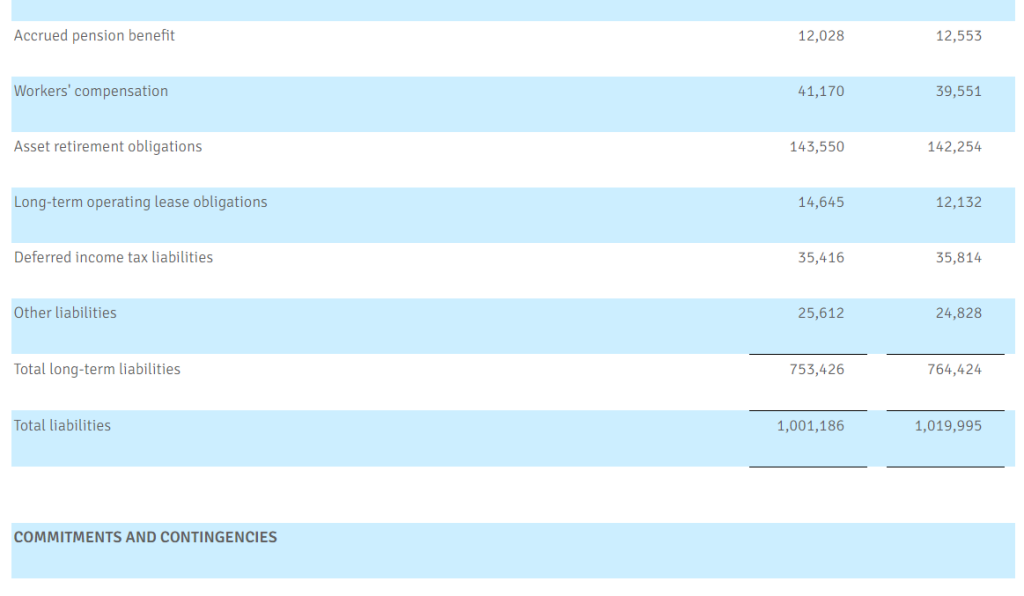

Balance Sheet and Liquidity

During the 2023 Quarter, ARLP repurchased $34.2 million of its senior notes due May 1, 2025 and began principal payments on its term loan. In July 2023, ARLP redeemed an additional $50.0 million of its senior notes.

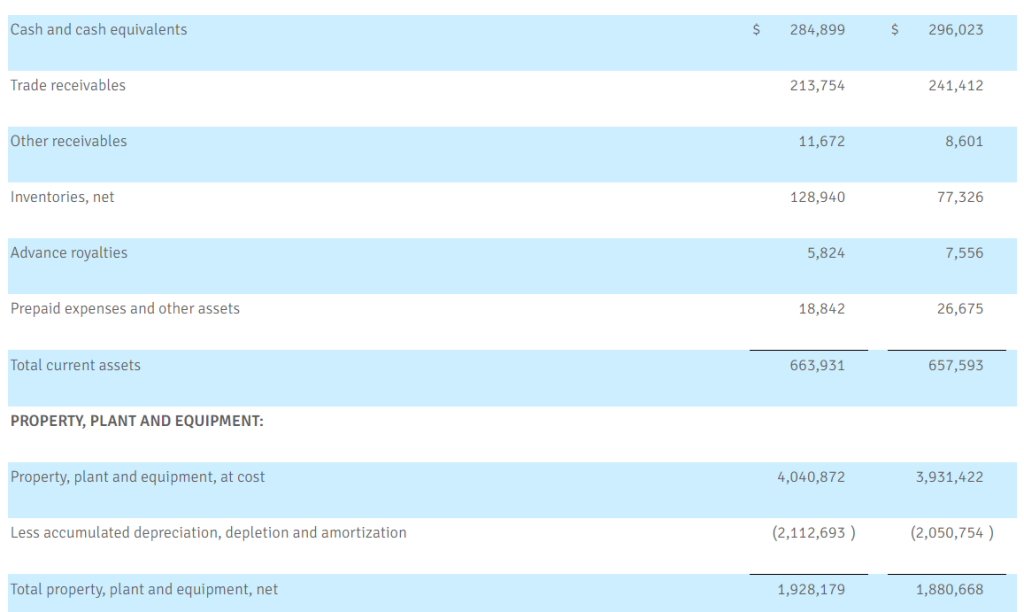

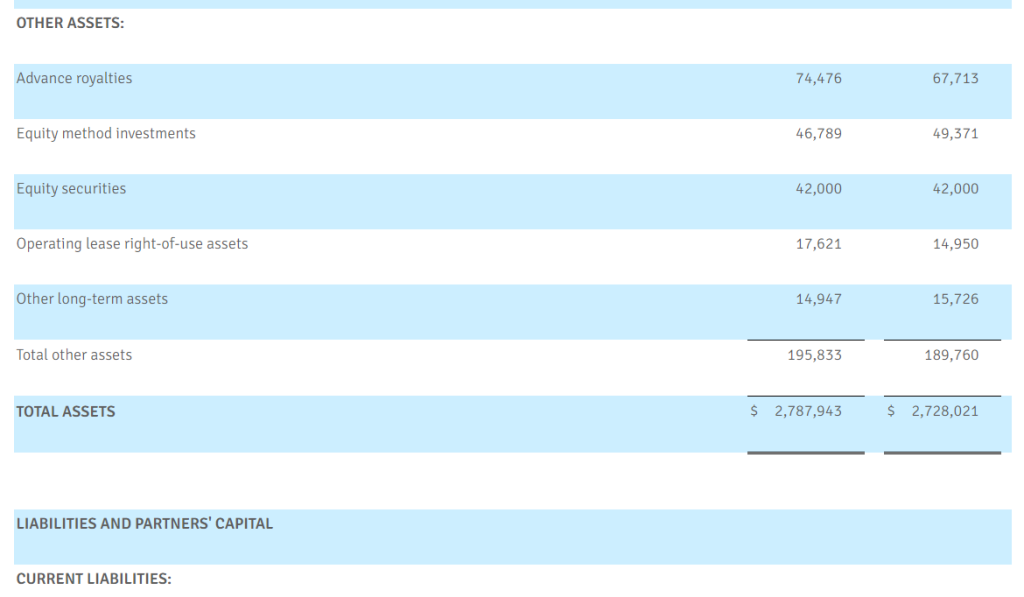

As of June 30, 2023, total debt and finance leases outstanding were $417.8 million, including $339.2 million in ARLP’s 2025 senior notes. The Partnership’s total and net leverage ratio was 0.40 times and 0.14 times, respectively, as of June 30, 2023. ARLP ended the 2023 Quarter with total liquidity of $717.2 million, which included $284.9 million of cash and cash equivalents and $432.3 million of borrowings available under its revolving credit and accounts receivable securitization facilities.

Distributions

As previously announced, on July 28, 2023, the Board of Directors of ARLP’s general partner (the “Board”) approved a cash distribution to unitholders for the 2023 Quarter of $0.70 per unit (an annualized rate of $2.80 per unit), payable on August 14, 2023, to all unitholders of record as of the close of trading on August 7, 2023. The announced distribution represents a 75.0% increase over the cash distribution of $0.40 per unit for the 2022 Quarter and is consistent with the Sequential Quarter cash distribution.

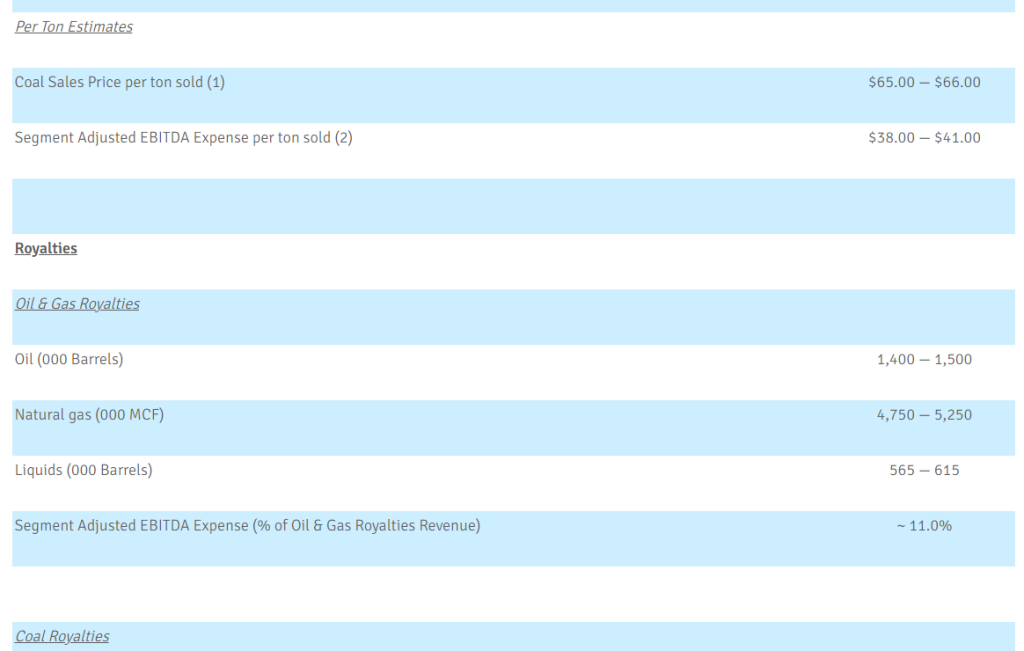

Outlook

“The recent heat wave has supported additional coal burn this summer for both the domestic and export markets. However, until Henry Hub natural gas prices rise above $3.00 per million Btu, we do not expect any meaningful gas-to-coal switching domestically. Therefore, we have chosen to reduce our coal production and sales volume guidance for 2023. Production targets have been reduced at our River View and Gibson operations in the Illinois Basin and at our Mettiki operation in Appalachia,” commented Mr. Craft. “Committed and priced sales tons currently represent 96% to 97% of our updated guidance range, and we plan to sell any remaining uncontracted tonnage primarily into international markets from these three mines. We have also adjusted the top end of our coal sales price per ton sold range downward based upon recent market analysis. On the positive side, we are lowering our cost estimates for the year as our team continues to find ways to reduce expenses in a stubbornly volatile inflationary environment.”

Mr. Craft added, “During the 2023 Quarter, we agreed to sell an additional 8.6 million tons with multiple customers for coal to be delivered over the 2024 to 2026 time period. We expect there will be more opportunities this year to fill out our future contract book.”

Mr. Craft closed, “These modest guidance revisions have not changed our view that we remain on track to achieve record financial results this year. As we look beyond 2023, we are encouraged by growth opportunities being pursued by our New Ventures group, the recent increase in the forward oil and gas price curves and acquisition prospects for our Oil & Gas Royalties segment. We are also seeing stability for coal demand over the next several years. Many of our coal customers are projecting significant growth in electricity demand as record numbers of new manufacturing facilities are being announced to come online over the next several years. All of these announced projects require exceptionally large electrical loads, adding to the reliability concerns of the stakeholders responsible for meeting the rising energy needs of their customers. The increased electricity demand should lead to slowing the pre-mature closing of coal-fired power plants in the eastern United States. We also expect the growth in LNG terminals coming online over the next five years will support higher domestic natural gas prices further supporting stable demand expectations for our coal operations over the next five to ten years.”

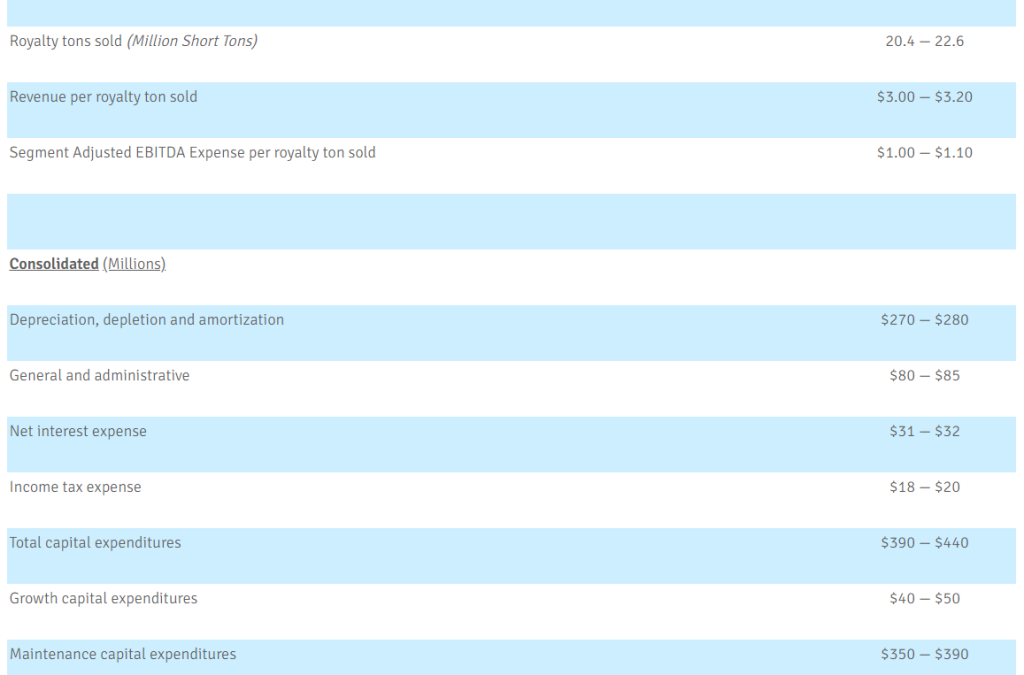

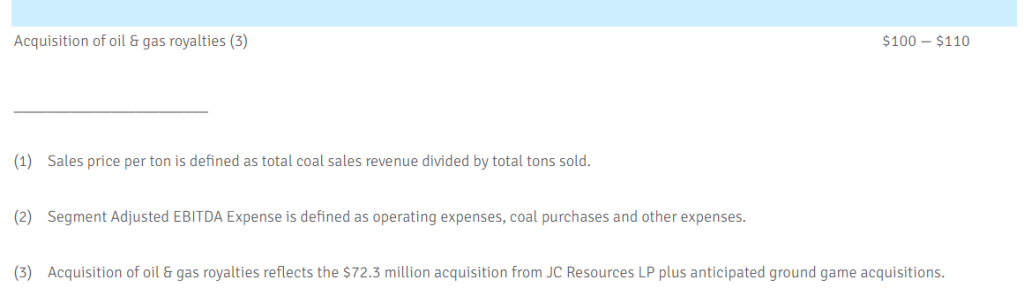

ARLP is providing the following updated guidance for the 2023 full year:

Conference Call

A conference call regarding ARLP’s 2023 Quarter financial results is scheduled for today at 10:00 a.m. Eastern. To participate in the conference call, dial (877) 407-0784 and request to be connected to the Alliance Resource Partners, L.P. earnings conference call. International callers should dial (201) 689-8560 and request to be connected to the same call. Investors may also listen to the call via the “investor relations” section of ARLP’s website at www.arlp.com.

An audio replay of the conference call will be available for approximately one week. To access the audio replay, dial U.S. Toll Free (844) 512-2921; International Toll (412) 317-6671 and request to be connected to replay using access code 13739987.

About Alliance Resource Partners, L.P.

ARLP is a diversified energy company that is currently the largest coal producer in the eastern United States, supplying reliable, affordable energy domestically and internationally to major utilities, metallurgical and industrial users. ARLP also generates operating and royalty income from mineral interests it owns in strategic coal and oil & gas producing regions in the United States. In addition, ARLP is evolving and positioning itself as a reliable energy partner for the future by pursuing opportunities that support the advancement of energy and related infrastructure.

News, unit prices and additional information about ARLP, including filings with the Securities and Exchange Commission (“SEC”), are available at www.arlp.com. For more information, contact the investor relations department of ARLP at (918) 295-7673 or via e-mail at investorrelations@arlp.com.

The statements and projections used throughout this release are based on current expectations. These statements and projections are forward-looking, and actual results may differ materially. These projections do not include the potential impact of any mergers, acquisitions or other business combinations that may occur after the date of this release. We have included more information below regarding business risks that could affect our results.

FORWARD-LOOKING STATEMENTS: With the exception of historical matters, any matters discussed in this press release are forward-looking statements that involve risks and uncertainties that could cause actual results to differ materially from projected results. Those forward-looking statements include expectations with respect to our future financial performance, coal and oil & gas consumption and expected future prices, our ability to increase unitholder distributions in future quarters, business plans and potential growth with respect to our energy and infrastructure transition investments, optimizing cash flows, reducing operating and capital expenditures, preserving liquidity and maintaining financial flexibility, and our future repurchases of units and senior notes, among others. These risks to our ability to achieve these outcomes include, but are not limited to, the following: decline in the coal industry’s share of electricity generation, including as a result of environmental concerns related to coal mining and combustion and the cost and perceived benefits of other sources of electricity and fuels, such as oil & gas, nuclear energy, and renewable fuels; changes in macroeconomic and market conditions and market volatility, and the impact of such changes and volatility on our financial position; changes in global economic and geo-political conditions or changes in industries in which our customers operate; changes in commodity prices, demand and availability which could affect our operating results and cash flows; the outcome or escalation of current hostilities in Ukraine; the severity, magnitude, and duration of any future pandemics and impacts of the pandemic and of businesses’ and governments’ responses to the pandemic on our operations and personnel, and on demand for coal, oil, and natural gas, the financial condition of our customers and suppliers, available liquidity and capital sources and broader economic disruptions; actions of the major oil-producing countries with respect to oil production volumes and prices could have direct and indirect impacts over the near and long term on oil & gas exploration and production operations at the properties in which we hold mineral interests; changes in competition in domestic and international coal markets and our ability to respond to such changes; potential shut-ins of production by operators of the properties in which we hold oil & gas mineral interests due to low commodity prices or the lack of downstream demand or storage capacity; risks associated with the expansion of our operations and properties; our ability to identify and complete acquisitions and to successfully integrate such acquisitions into our business and achieve the anticipated benefits therefrom; our ability to identify and invest in new energy and infrastructure transition ventures; the success of our development plans for our wholly owned subsidiary, Matrix Design Group, LLC, and our investments in emerging infrastructure and technology companies; dependence on significant customer contracts, including renewing existing contracts upon expiration; adjustments made in price, volume, or terms to existing coal supply agreements; the effects of and changes in trade, monetary and fiscal policies and laws; central bank policy actions, bank failures and associated liquidity risks; the effects of and changes in taxes or tariffs and other trade measures adopted by the United States and foreign governments; legislation, regulations, and court decisions and interpretations thereof, both domestic and foreign, including those relating to the environment and the release of greenhouse gases, mining, miner health and safety, hydraulic fracturing, and health care; deregulation of the electric utility industry or the effects of any adverse change in the coal industry, electric utility industry, or general economic conditions; investors’ and other stakeholders’ increasing attention to environmental, social, and governance matters; liquidity constraints, including those resulting from any future unavailability of financing; customer bankruptcies, cancellations or breaches to existing contracts, or other failures to perform; customer delays, failure to take coal under contracts or defaults in making payments; our productivity levels and margins earned on our coal sales; disruptions to oil & gas exploration and production operations at the properties in which we hold mineral interests; changes in equipment, raw material, service or labor costs or availability, including due to inflationary pressures; changes in our ability to recruit, hire and maintain labor; our ability to maintain satisfactory relations with our employees; increases in labor costs including costs of health insurance and taxes resulting from the Affordable Care Act, adverse changes in work rules, or cash payments or projections associated with workers’ compensation claims; increases in transportation costs and risk of transportation delays or interruptions; operational interruptions due to geologic, permitting, labor, weather, supply chain shortage of equipment or mine supplies, or other factors; risks associated with major mine-related accidents, mine fires, mine floods or other interruptions; results of litigation, including claims not yet asserted; foreign currency fluctuations that could adversely affect the competitiveness of our coal abroad; difficulty maintaining our surety bonds for mine reclamation as well as workers’ compensation and black lung benefits; difficulty in making accurate assumptions and projections regarding post-mine reclamation as well as pension, black lung benefits, and other post-retirement benefit liabilities; uncertainties in estimating and replacing our coal mineral reserves and resources; uncertainties in estimating and replacing our oil & gas reserves; uncertainties in the amount of oil & gas production due to the level of drilling and completion activity by the operators of our oil & gas properties; uncertainties in the future of the electric vehicle industry and the market for EV charging stations; the impact of current and potential changes to federal or state tax rules and regulations, including a loss or reduction of benefits from certain tax deductions and credits; difficulty obtaining commercial property insurance, and risks associated with our participation in the commercial insurance property program; evolving cybersecurity risks, such as those involving unauthorized access, denial-of-service attacks, malicious software, data privacy breaches by employees, insiders or others with authorized access, cyber or phishing-attacks, ransomware, malware, social engineering, physical breaches, or other actions; and difficulty in making accurate assumptions and projections regarding future revenues and costs associated with equity investments in companies we do not control.

Additional information concerning these, and other factors can be found in ARLP’s public periodic filings with the SEC, including ARLP’s Annual Report on Form 10-K for the year ended December 31, 2022, filed on February 24, 2023,and ARLP’s Quarterly Report on Form 10-Q for the quarter ended March 31, 2023, filed on May 9, 2023. Except as required by applicable securities laws, ARLP does not intend to update its forward-looking statements.

Reconciliation of Non-GAAP Financial Measures

Reconciliation of GAAP “net income attributable to ARLP” to non-GAAP “EBITDA” and “Distributable Cash Flow” (in thousands).

EBITDA is defined as net income attributable to ARLP before net interest expense, income taxes and depreciation, depletion and amortization. Distributable cash flow (“DCF”) is defined as EBITDA excluding equity method investment earnings, interest expense (before capitalized interest), interest income, income taxes and estimated maintenance capital expenditures and adding distributions from equity method investments. Distribution coverage ratio (“DCR”) is defined as DCF divided by distributions paid to partners.

Management believes that the presentation of such additional financial measures provides useful information to investors regarding our performance and results of operations because these measures, when used in conjunction with related GAAP financial measures, (i) provide additional information about our core operating performance and ability to generate and distribute cash flow, (ii) provide investors with the financial analytical framework upon which management bases financial, operational, compensation and planning decisions and (iii) present measurements that investors, rating agencies and debt holders have indicated are useful in assessing us and our results of operations.

EBITDA, DCF and DCR should not be considered as alternatives to net income attributable to ARLP, net income, income from operations, cash flows from operating activities or any other measure of financial performance presented in accordance with GAAP. EBITDA and DCF are not intended to represent cash flow and do not represent the measure of cash available for distribution. Our method of computing EBITDA, DCF and DCR may not be the same method used to compute similar measures reported by other companies, or EBITDA, DCF and DCR may be computed differently by us in different contexts (i.e., public reporting versus computation under financing agreements).

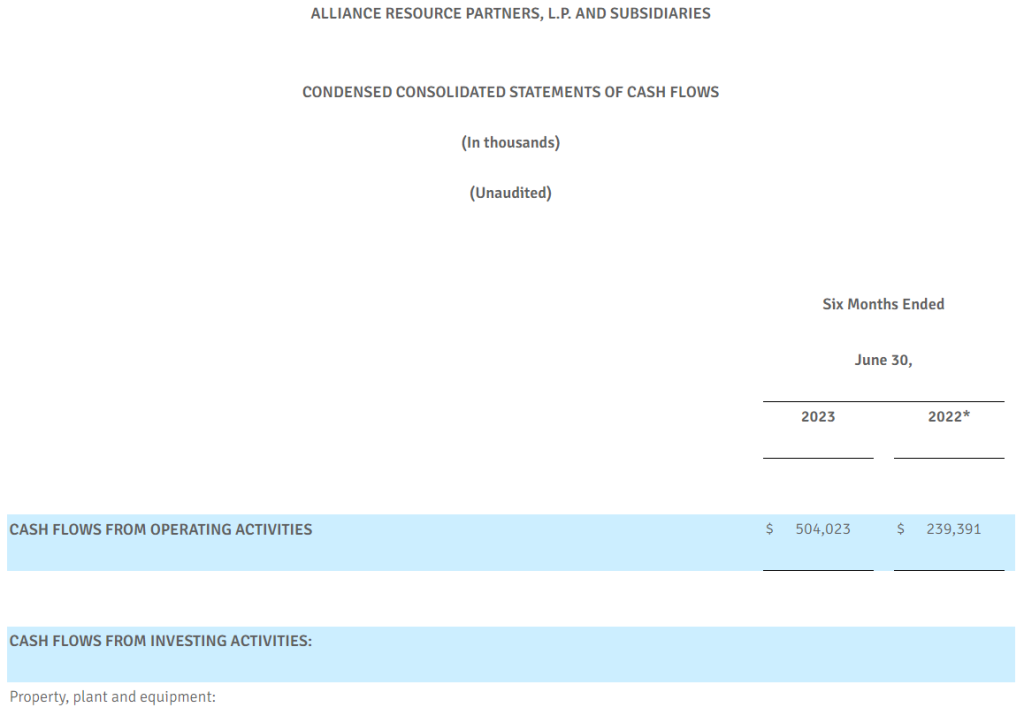

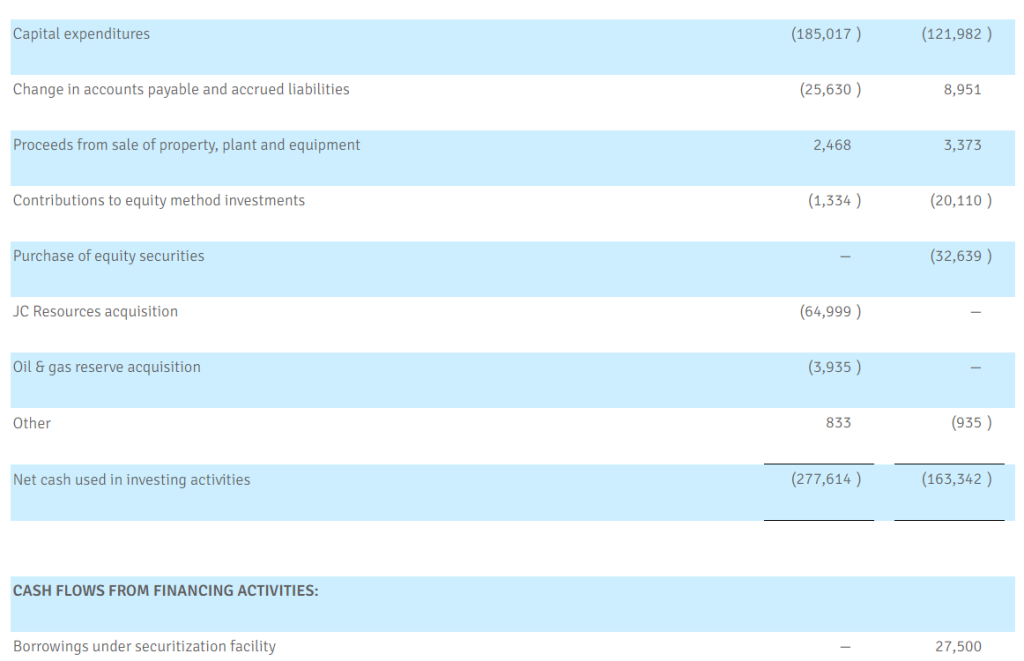

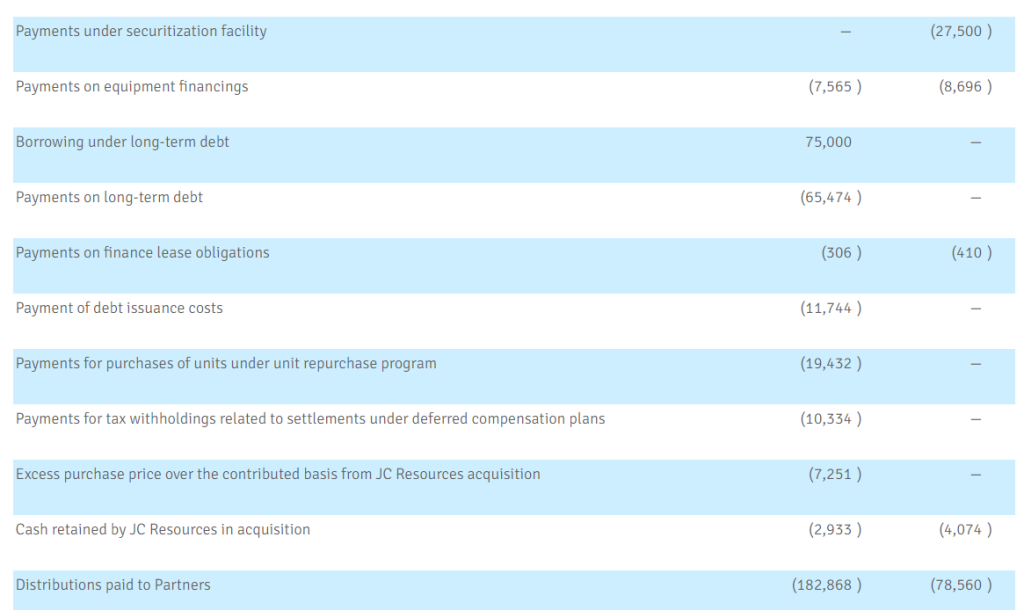

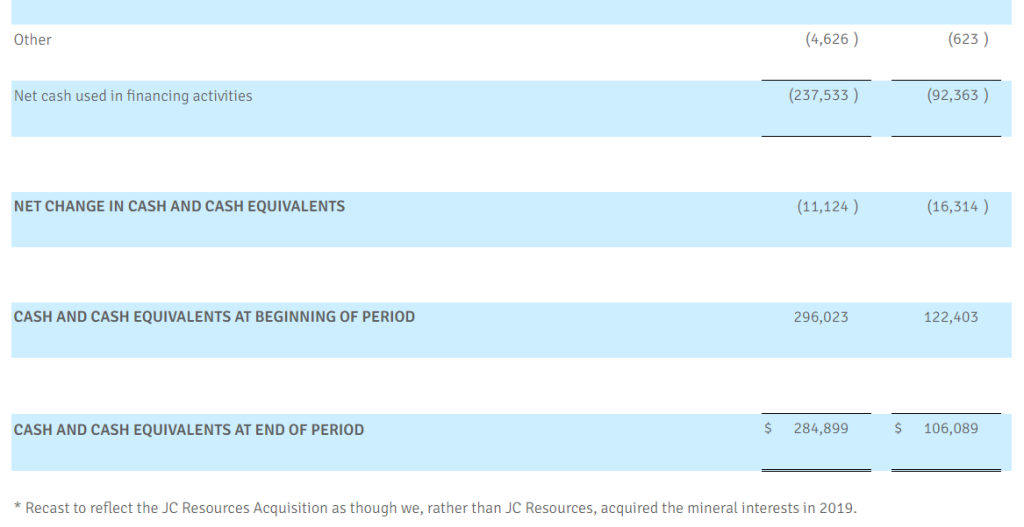

Reconciliation of GAAP “Cash flows from operating activities” to non-GAAP “Free cash flow” (in thousands).

Free cash flow is defined as cash flows from operating activities less capital expenditures and the change in accounts payable and accrued liabilities from purchases of property plant and equipment. Free cash flow should not be considered as an alternative to cash flows from operating activities or any other measure of financial performance presented in accordance with GAAP. Our method of computing free cash flow may not be the same method used by other companies. Free cash flow is a supplemental liquidity measure used by our management to assess our ability to generate excess cash flow from our operations.

Reconciliation of GAAP “Operating Expenses” to non-GAAP “Segment Adjusted EBITDA Expense” and Reconciliation of non-GAAP ” EBITDA” to “Segment Adjusted EBITDA” (in thousands).

Segment Adjusted EBITDA Expense includes operating expenses, coal purchases, if applicable, and other income or expense. Transportation expenses are excluded as these expenses are passed on to our customers and, consequently, we do not realize any margin on transportation revenues. Segment Adjusted EBITDA Expense is used as a supplemental financial measure by our management to assess the operating performance of our segments. Segment Adjusted EBITDA Expense is a key component of EBITDA in addition to coal sales, royalty revenues and other revenues. The exclusion of corporate general and administrative expenses from Segment Adjusted EBITDA Expense allows management to focus solely on the evaluation of segment operating performance as it primarily relates to our operating expenses. Segment Adjusted EBITDA Expense – Coal Operations represents Segment Adjusted EBITDA Expense from our wholly-owned subsidiary, Alliance Coal, which holds our coal mining operations and related support activities.

Cary P. Marshall Senior Vice President and Chief Financial Officer 918-295-7673 investorrelations@arlp.com

Great Lakes Dredge & Dock Corporation is the largest provider of dredging services in the United States. In addition, Great Lakes is fully engaged in expanding its core business into the rapidly developing offshore wind energy industry. The Company has a long history of performing significant international projects. The Company employs experienced civil, ocean and mechanical engineering staff in its estimating, production and project management functions. In its over 131-year history, the Company has never failed to complete a marine project. Great Lakes owns and operates the largest and most diverse fleet in the U.S. dredging industry, comprised of approximately 200 specialized vessels. Great Lakes has a disciplined training program for engineers that ensures experienced-based performance as they advance through Company operations. The Company’s Incident-and Injury-Free® (IIF®) safety management program is integrated into all aspects of the Company’s culture. The Company’s commitment to the IIF® culture promotes a work environment where employee safety is paramount.

Joe Gomes, Managing Director, Equity Research Analyst, Generalist , Noble Capital Markets, Inc.

Joshua Zoepfel, Research Associate, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

Two New Awards. Great Lakes was announced as the recipient of two awards by the Department of Defense last week, hopefully an indication of a return to a more normal award pace by the Army Corps of Engineers. In total, the two awards represent $36.7 million of new business for Great Lakes.

Award 1. Great Lakes was awarded a $20.7 million firm-fixed-price contract for Atchafalaya River basin maintenance dredging. Work will be performed in Morgan City, Louisiana, with an estimated completion date of February 15, 2024. Fiscal 2023 civil construction funds in the amount of $20.7 million were obligated at the time of the award.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

Cumulus Media (NASDAQ: CMLS) is an audio-first media company delivering premium content to over a quarter billion people every month — wherever and whenever they want it. Cumulus Media engages listeners with high-quality local programming through 406 owned-and-operated radio stations across 86 markets; delivers nationally-syndicated sports, news, talk, and entertainment programming from iconic brands including the NFL, the NCAA, the Masters, CNN, the AP, the Academy of Country Music Awards, and many other world-class partners across more than 9,500 affiliated stations through Westwood One, the largest audio network in America; and inspires listeners through the Cumulus Podcast Network, its rapidly growing network of original podcasts that are smart, entertaining and thought-provoking. Cumulus Media provides advertisers with personal connections, local impact and national reach through broadcast and on-demand digital, mobile, social, and voice-activated platforms, as well as integrated digital marketing services, powerful influencers, full-service audio solutions, industry-leading research and insights, and live event experiences. Cumulus Media is the only audio media company to provide marketers with local and national advertising performance guarantees. For more information visit www.cumulusmedia.com.

Michael Kupinski, Director of Research, Equity Research Analyst, Digital, Media & Technology , Noble Capital Markets, Inc.

Jacob Mutchler, Research Associate, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

Q2 operating results. The company reported quarterly revenue of $210.1 million, in line with our estimate of $208.3 million. While National/Network advertising remains weak, Local advertising has some greenshoots particularly with Digital Marketing Services revenue. Adj. EBITDA in the quarter was $28.7 million, beating our estimate of $21.8 million by an impressive 32%, excluding a $2 million nonrecurring benefit. The adj. EBITDA surprise was attributed to aggressive cost cutting efforts.

Positive DMS outlook. Digital Marketing Services performed strongly, with revenue up 21% in the latest quarter. Management believes there is significant untapped growth potential in local DMSand is tripling its salesforce. Management anticipates an increase of 3x to 4x its current revenue run rate of $40 million in the next few years.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

Critical Thinking and Analytical Skills Will Not Easily Be Replaced

Ever since the industrial revolution, people have feared that technology would take away their jobs. While some jobs and tasks have indeed been replaced by machines, others have emerged. The success of ChatGPT and other generative artificial intelligence (AI) now has many people wondering about the future of work – and whether their jobs are safe.

A recent poll found that more than half of people aged 18-24 are worried about AI and their careers. The fear that jobs might disappear or be replaced through automation is understandable. Recent research found that a quarter of tasks that humans currently do in the US and Europe could be automated in the coming years.

The increased use of AI in white-collar workplaces means the changes will be different to previous workplace transformations. That’s because, the thinking goes, middle-class jobs are now under threat.

The future of work is a popular topic of discussion, with countless books published each year on the topic. These books speak to the human need to understand how the future might be shaped.

This article was republished with permission from The Conversation, a news site dedicated to sharing ideas from academic experts. It represents the research-based findings and thoughts of, Elisabeth Kelan, Professor of Leadership and Organization, University of Essex.

I analyzed 10 books published between 2017 and 2020 that focused on the future of work and technology. From this research, I found that thinking about AI in the workplace generally falls into two camps. One is expressed as concern about the future of work and security of current roles – I call this sentiment “automation anxiety”. The other is the hope that humans and machines collaborate and thereby increase productivity – I call this “augmentation aspiration”.

Anxiety and Aspiration

I found a strong theme of concern in these books about technology enabling certain tasks to be automated, depriving many people of jobs. Specifically, the concern is that knowledge-based jobs – like those in accounting or law – that have long been regarded as the purview of well-educated professionals are now under threat of replacement by machines.

Automation undermines the idea that a good education will secure a good middle-class job. As economist Richard Baldwin points out in his 2019 book, The Globotics Upheaval, if you’ve invested a significant amount of money and time on a law degree – thinking it is a skill set that will keep you permanently employable – seeing AI complete tasks that a junior lawyer would normally be doing, at less cost, is going to be worrisome.

But there is another, more aspirational way to think about this. Some books stress the potential of humans collaborating with AI, to augment each other’s skills. This could mean working with robots in factories, but it could also mean using an AI chatbot when practicing law. Rather than being replaced, lawyers would then be augmented by technology.

In reality, automation and augmentation co-exist. For your future career, both will be relevant.

Future-Proofing Yourself

As you think about your own career, the first step is to realize that some automation of tasks is most likely going to be something you’ll have to contend with in the future.

In light of this, learning is one of the most important ways you can future-proof your career. But should you spend money on further education if the return on investment is uncertain?

It is true that specific skills risk becoming outdated as technology develops. However, more than learning specific abilities, education is about learning how to learn – that is, how to update your skills throughout your career. Research shows that having the ability to do so is highly valuable at work.

This learning can take place in educational settings, by going back to university or participating in an executive education course, but it can also happen on the job. In any discussion about your career, such as with your manager, you might want to raise which additional training you could do.

Critical thinking and analytical skills are going to be particularly central for how humans and machines can augment one another. When working with a machine, you need to be able to question the output that is produced. Humans are probably always going to be central to this – you might have a chatbot that automates parts of legal work, but a human will still be needed to make sense of it all.

Finally, remember that when people previously feared jobs would disappear and tasks would be replaced by machines, this was not necessarily the case. For instance, the introduction of automated teller machines (ATMs) did not eliminate bank tellers, but it did change their tasks.

Above all, choose a job that you enjoy and keep learning – so that if you do need to change course in the future, you know how to.

The Back Story on Why Uranium Investors Saw a Spike Up in Values

Nuclear energy now provides 10% of the world’s electricity. If a major supplier of uranium becomes unavailable, it could be very disruptive. For countries such as France that derives 68% of their electricity from nuclear power plants, it can become more than disruptive. This is why the coup in Niger, which provides 15% of of the uranium used in French power plants is generating so much concern.

Background

Over the past few days, a successful military coup in Niger has sparked concerns in the EU and especially in France regarding the potential ramifications on uranium imports crucial for powering the country’s nuclear plants. As a major supplier, Niger currently fulfills 15% of France’s uranium needs and holds a significant 20% share of the EU’s total uranium imports. French authorities, along with energy officials have been quick to address public concerns. While the short-term implications are minimal, long-term uranium requirements could become a challenge for France and other countries within the EU. The block of nations has already been engaged with efforts to reduce dependency on Russia, another prominent uranium supplier for European nuclear facilities.

France, is unusually reliant on nuclear power. Orano, the French state-controlled nuclear fuel producer, has maintained its operations in Niger despite the coup, with the company asserting its primary focus is on ensuring the safety of its employees in the region.

Existing uranium stocks are expected to sustain France’s uranium requirements for approximately two years. Therefore, the French government is confident that the current tensions in Niger will not immediately impact their uranium needs.

Long-Term Concerns for Europe’s Uranium Needs

While immediate disruptions seem improbable, Europe could face challenges in its uranium supply chain in the long run, particularly as the continent strives to diminish its reliance on Russian uranium. Niger, as the top uranium supplier to the EU in 2021, alongside Kazakhstan and Russia, play a critical role in sustaining Europe’s nuclear power sector.

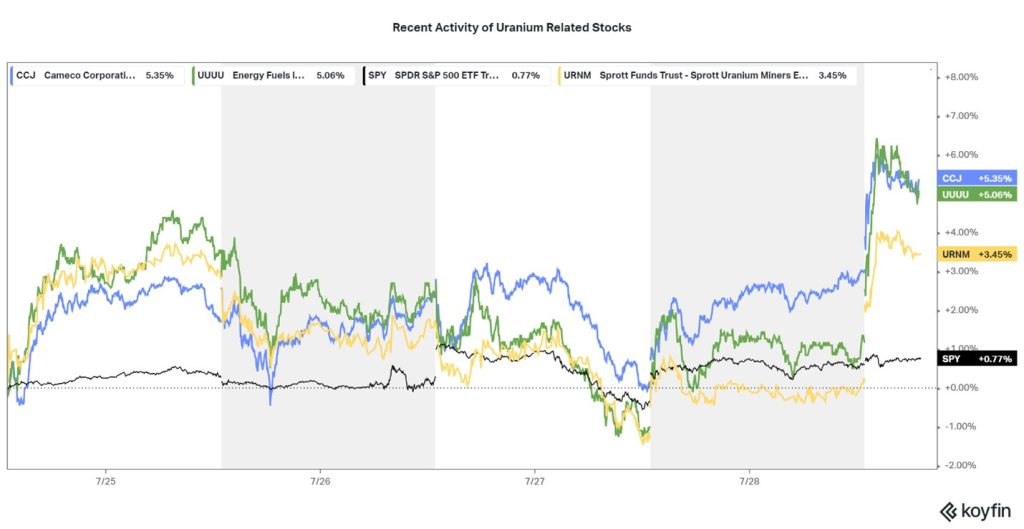

While it may seem cold to think of one’s investment portfolio when trouble befalls others, it is the flow of money in the capital markets that often helps allow for corrective actions that lessen the problem. The plot lines on the chart above represent Cameco (CCJ) a Canadian company that is one of the largest providers of uranium fuel. Energy Fuels (UUUU) which is the leading U.S. producer of uranium, Sprott Uranium Miners (URNM) invests in an index designed to track the performance of companies that devote at least 50% of their assets to the uranium mining industry. The fourth plotline is the S&P 500.

The gap up after the news is unmistakable and suggests investors immediately expect reduced supply from the coup to cause current production to become more valuable as it meets unchanged demand.

Take Away