Robert LeBoyer, Senior Vice President, Equity Research Analyst, Biotechnology, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

Potential Breakthroughs In Xenotransplantation. The journal Nature has published a preclinical study by Eledon’s research collaborator detailing genetic changes to porcine (pig) cells and the results of their transplantation to monkeys. In September, the second successful transplant of an engineered pig heart to a human patient used Eledon’s tegoprubart for immune suppression. Both developments have overcome many technological barriers and could make trans-species organ transplantation a clinical reality.

Publication Details Some Of The Changes To Make Xenotransplants Compatible. Transplanting organs from a non-human species has many additional challenges than transplantation from one human to another (allografts). The Nature article, from Eledon’s collaborator eGenesis, describes the design, creation, and function of kidney grafts from a genetically engineered porcine transplant into a cynomolgus monkey model. The article describes 69 genomic edits to the donor tissue, addition of 7 human genes, and inactivation of endogenous retroviruses. The transplanted monkeys survived up to 758 days (108 weeks).

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

CoreCivic is a diversified, government-solutions company with the scale and experience needed to solve tough government challenges in flexible, cost-effective ways. We provide a broad range of solutions to government partners that serve the public good through high-quality corrections and detention management, a network of residential and non-residential alternatives to incarceration to help address America’s recidivism crisis, and government real estate solutions. We are the nation’s largest owner of partnership correctional, detention and residential reentry facilities, and believe we are the largest private owner of real estate used by government agencies in the United States. We have been a flexible and dependable partner for government for nearly 40 years. Our employees are driven by a deep sense of service, high standards of professionalism and a responsibility to help government better the public good. Learn more at www.corecivic.com.

Joe Gomes, Managing Director, Equity Research Analyst, Generalist , Noble Capital Markets, Inc.

Joshua Zoepfel, Research Associate, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

Amended Facility. Late last week, CoreCivic announced it had amended its credit agreement. The new facility effectively replaces CoreCivic’s Third Amended and Restated Credit Agreement dated May 12, 2022. The new facility is in the aggregate principal amount of $400 million, consisting of a $125 million term loan and a $275 million revolving credit facility. The new facility provides greater flexibility, in our view.

Details. The new facility increases in size from $350 million to $400 million. In addition, the Company has an option to increase the availability under the revolving credit facility and to request term loans from the lenders in an aggregate amount not to exceed the greater of (a) $200 million and (b) 50% of consolidated EBITDA for the most recently ended four-quarter period. Maturity has been extended until October 11, 2028 from May 12, 2026.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

Michael Kupinski, Director of Research, Noble Capital Markets, Inc.

Jacob Mutchler, Research Associate, Noble Capital Markets, Inc.

Refer to the bottom of the report for important disclosures

Overview: A new small-cap cycle?Small cap stocks have underperformed the large cap stocks for the past several years. Notably, there is a sizable valuation disparity between the two classes, one of the largest in over 20 years. Some of the small cap stocks we follow trade at a modest 2 times Enterprise Value to EBITDA, compared with large cap valuations as high as 13 to 15 times. Are we on a cusp of a small cap cycle?

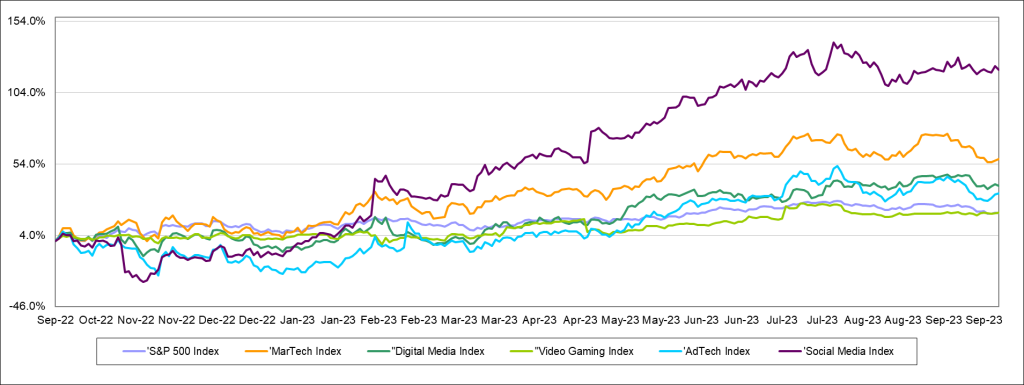

Digital Media & Technology:Stocks Outperform – But Don’t Get Too Excited. Each of Noble’s Internet and Digital Media Indices, which are market cap weighted, outperformed the S&P 500 in the third quarter, but the double-digit gains from the previous quarter moderated significantly. Despite these relatively positive results, the prevailing theme within each sector was that the largest cap stocks performed the best, while smaller cap stocks across a variety of sectors struggled.

Television Broadcasting:Advertising Stabilizing?As we look toward the third quarter, local advertising appears to be weakening as the economy appears to be slowing. But, national appears to be improving. In addition, while it was assumed that Political would increase in the fourth quarter due to the run-off of the Republican presidential candidates, we believe that President Biden has recently stepped-up advertising in the third quarter, particularly in Hispanic communities.

Radio Broadcasting:Shoring up balance sheets.As many radio companies face a challenged revenue environment and at the same time invested in faster growth digital revenue, some companies have been caught carrying a substantial amount of debt. In this report, we highlight one company that was able to shore up its balance sheet through asset sales.

Publishing:Stocks outperform. It may be hard to imagine for some investors, but the Publishing stocks outperformed in both the latest quarter and for the trailing 12 months the S&P 500! But, there is still a wide valuation gap between most of Publishers and the shares of The New York Times, with the NYT shares at 15 times cash flow and the rest near 5.

Overview

The case for small caps

Small cap investors have gone through a rough period. For the past several years, investors have anticipated an economic downturn. With these concerns, investors turned toward “safe haven” large cap stocks, which typically have the ability to weather the economic headwinds and have enough trading volume should investors need to exit the position. Since 2018, small cap stocks have underperformed the general stock market, with annualized returns of just 3.7% as measured by the S&P 600 Small Cap Index versus the general market of 10.2% as measured by the S&P 500 Index. Another small cap index, the Russell 2000, increased a more modest 2.9% annually over the comparable period. The S&P 500 is larger cap, with the minimum market cap of $14.6 billion. The S&P 600 is smaller cap, a range of $850 million to $3.7 billion, with the Russell 2000 median market cap $950 million. Some of the even smaller cap stocks, those between $100 million to $850 million, have significantly underperformed the S&P 600. This is the first time that small caps underperformed a bullish period for all stocks since the 1940s. Notably, there is a sizable valuation disparity between the two classes, large and small cap, one of the largest in over 20 years.

Some of the small cap stocks we follow trade at a modest 2 times Enterprise Value to EBITDA, compared with large cap valuations as high as 13 to 15 times. By another measure, small cap stocks may be the only class trading below historic 25 year average to the median Enterprise Value to EBIT. Why the large valuation disparity? We believe that there is higher risk in the small cap stocks, especially given that some companies may not be cash flow positive, have capital needs, or have limited share float. But, investors seem to have thrown the baby out with the bathwater. While those small cap stocks are on the more speculative end of the scale, many small cap stocks are growing revenues and cash flow, have capable balance sheets, and/or are cash flow positive. For attractive emerging growth companies, the trading activity will resolve itself over time. Some market strategists suggest that small cap stocks trade at the most undervalued in the market, as much as a 30% to 40% discount to fair value.

Are we on a cusp of a small cap cycle? Some fund managers think so. Such a cycle could last 10 years or longer. In this report, we highlight a few of our small cap favorites in the Media sector, those include companies that have attractive growth characteristics, some with or without an improving economy, capable balance sheets, and limited capital needs. Our current favorites based on growth opportunity and stock valuation include: Direct Digital (DRCT), Entravision (EVC), E.W. Scripps (SSP), Gray Television (GTN), and Townsquare Media (TSQ).

After increasing by 8% in the second quarter of 2023, the S&P 500 was unable to hold onto those gains in the third quarter. The S&P Index decreased by 3.6% in the third quarter, a decline which we attribute to the market revising its interest rate expectations to one in which rates would remain “higher for longer”. Large cap stocks that weighed on the broad market index included tech stocks such as Apple (AAPL: -12%), Microsoft (MSFT: -7%) and Tesla (TSLA: -4%). Despite this small step backwards, the S&P 500 Index increased by 20% through the first nine months of the year.

Each of Noble’s Internet and Digital Media Indices, which are market cap weighted, outperformed the S&P 500 in the third quarter, but the double-digit gains from the previous quarter (2Q 2023) moderated significantly. Digital Media 3-Month Performance Sectors that outperformed the S&P 500’s 4% decrease include Noble’s Digital Media Index (+6%), Social Media Index (+4%), Gaming Index (+3%), Ad Tech Index (+1%) and MarTech Index (-3%). Despite these relatively positive results, the prevailing theme within each sector was that the largest cap stocks performed the best while smaller cap stocks across a variety of sectors struggled.

Figure #1 Digital Media 3-Month Performance

Source: Capital IQ

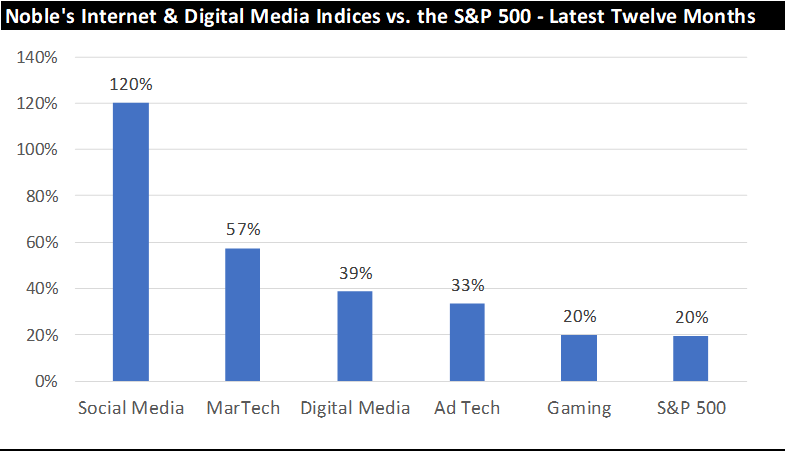

Perhaps more importantly, each of Noble’s Internet and Digital Media Indices have outperformed the S&P 500 over the latest twelve months as illustrated in Figure #2 Digital Versus S&P 500 LTM. The S&P 500 Index has increased by 20% over the last year (through 9/30/2023), which trailed the performance of the each of Noble’s Internet and Digital Media Indices, as shown in Figure #3 Digital Media LTM Performance.

Figure #2 Digital Versus S&P 500 LTM

Figure #3 Digital Media LTM Performance

Source: Capital IQ

Alphabet Powers Digital Media Index Higher Despite Broader-Based Sector Weakness

The best performing index during the quarter was the Noble’s Digital Media Index, but the sector’s “strong” performance is deceiving. Shares of Alphabet (a.k.a. Google: GOOGL) increased by 9% during the quarter, and the company size relative to its peers helps explain the vast majority of the sector’s performance. Google’s market cap is 8x larger than its next largest “peer” in Netflix, and it is 160 times that of the average market cap of its Digital Media peers. Google beat expectations across all metrics (revenue, EBITDA, free cash flow) and guided to improved profitability as it streamlines workflows. The company is also increasingly perceived as a beneficiary of AI. While Alphabet shares performed well, they mask the fact that shares of only 2 of the sector’s 12 stocks were up during the third quarter. The other Digital Media stock that performed well in the quarter was FUBO (FUBO), whose shares increased by 29% in 3Q 2023. Of the 10 other digital content providers in the sector, 7 of them posted double-digit stock price declines in the third quarter.

Large Cap Meta Powers the Social Media Index Higher

Shares in Meta Platforms (formerly Facebook) rose for the third straight quarter. Shares increased by 5% and were up 150% through the first nine months of the year. Meta shares increased by 8% at the start of the third quarter due to excitement around the launch of Threads, Meta’s answer to Twitter. Over 100 million people signed up for Threads within the first five days of its rollout and positions the company well for continued revenue growth once it begins to monetize this new opportunity.

As with the Digital Media Index, the Social Media Index masked underlying weakness across several smaller cap stocks. Of the 6 stocks in the Social Media Index, only Meta shares increased during the quarter. Several social media companies performed poorly during the quarter including Spark Networks (LOVL.Y: -59%), which filed to delist its shares, Nextdoor Holdings (KIND: -44%), which has struggled to reach profitability, and Snap (SNAP: -25%), which guided to revenue declines in 3Q 2023.

“No Love” For Small Cap Stocks

As was the case in the Digital Media and Social Media sectors, the same trends held true in the other sectors: in general, large cap stocks outperformed small cap stocks. For example, Noble’s Video Gaming Index increased by 3% in the third quarter, driven by Activision Blizzard (ATVI: +11%), and to a lesser extent SciPlay Corp (SCP: +16%). However, 7 other stocks in the video gaming sector posted stock price declines in the third quarter. Larger cap names such as EA Sports (EA: -7%) and Take-Two Interactive (TTWO: -5%) posted mid-single digit stock price declines while every small cap video gaming stock posted double digit declines.

Noble’s Ad Tech Index increased by 1% during the quarter driven by shares of AppLovin (APP: +55%), and Taboola (TBLA: +22%). However, just 7 of the sector’s 20 stocks were up for the quarter, and 10 stocks in the sector posted double digit declines. One of our favorites is an attractive growth, small cap company, Direct Digital. The DRCT shares declined 20% in the quarter, in spite of posting favorable Q2 revenue that beat expectations and raising full year revenue estimates. Direct Digital leads our list of favorites in the digital Ad Tech companies. As Figure #4 Ad Tech Comparables indicate, Direct Digital is among the cheapest in the industry trading at 4.7 Enterprise Value to our 2024 adj. EBITDA estimate, well below larger cap peers trading at multiples of 12, 13, or even much higher. Finally, Noble’s MarTech Index decreased by 3% (the only index that declined during the quarter), with the sector’s largest companies, Adobe (ADBE: +4%) and Shopify (SHOP: -16%) posting mixed results. Outside of these mega-cap stocks, the theme of underlying weakness prevailed: only 5 of the 20 stocks in the sector posted stock price increases, while one was flat and the other 14 were down. Eleven of the 20 stocks in the MarTech sector posted double digit stock price declines. One of our favorites in the sector, Harte Hanks performed well in the quarter up 18.8%. This was a welcomed bounce from the steep decline in the shares over the past 12 months, down 44%. The company stumbled on quarterly expectations. We believe that the sell-off was over done, providing a compelling opportunity for investors. As Figure #5 MarTech Comparables illustrates, the HHS shares trade at 3.8 times Enterprise Value to our 2024 adj. EBITDA estimate, a fraction of the multiples of many of its larger cap peers. We view the HHS shares as among our favorites in the sector.

Figure #4 Ad Tech Comparables

Source: Company filings & Eikon

Figure #5 MarTech Comparables

Source: Noble estimates & Company filings

Traditional Media

Virtually all traditional media stocks underperformed the general market in the past quarter and trailing 12 months, as illustrated in Figure #6 Traditional Media LTM Performance, save the Publishing group. In the latest quarter, Publishing stocks outperformed the general market, up 3.0% versus down 3.6% for the general market as measured by the S&P 500 Index. The average Publishing stock is up 6.9% over the past 12 months, with some of the larger cap publishing stocks up significantly more, over 20%. More details on the Publishing performance is in the Publishing section of this report. In the last quarter, the Radio stocks were the worse performing group, down on average 10.2%, As illustrated in Figure #7 Traditional Media 3-Month Performance. In addition, the Radio stocks were the worst performing group in the third quarter as well, down and average of 12.7% for the quarter.

Figure #6 Traditional Media LTM Performance

Source: Capital IQ

Figure #7 Traditional Media 3-Month Performance

Source: Capital IQ

Television Broadcasting

Have the TV stocks discounted too much?

We believe that the economic headwinds of rising interest rates and inflation have begun to hit local advertising. Local advertising had been relatively stable, favorably influenced by a resurgence of Auto advertising. Notably, local advertising fared much better than national advertising, which was down in the absence of Political advertising. As we look toward the fourth quarter, local advertising appears to be weakening. But, notably, national advertising appears to be doing much better, driven by an early influx of Political advertising. While it was assumed that Political would increase in the fourth quarter due to the run-off of the Republican presidential candidates, especially in early primary States, we believe that President Biden has recently stepped-up advertising, particularly to the Hispanic community. We have noticed Biden advertising even in Florida! So, what does this mean for media fundamentals?

It is difficult to predict where Political dollars will be spent and not all Political dollars will be spent evenly, geographically or by stations in a particular market. Furthermore, Political dollars may be pulled back in a market should a particular candidate pull ahead in the polls. Political dollars were anticipated to be spent in early primary States, specifically for the Republican candidates. But, the Biden money is a surprise. Biden appears to be spending early and in areas to solidify a key voting block, Hispanics. Of course, the Biden campaign may broaden its spending to other voting blocks as well. In our view, 2024 will be a banner year for Political advertising given the large amount of Political fundraising by the candidates and by Political Action Committees. The prospect of weak local advertising, however, may cast a pall over the current expected strong revenue growth in 2024. Many analysts, including myself, expected that economic prospects would improve in 2024, which would have provided a favorable tailwind for a significant improvement in total TV advertising in 2024. Certainly, it is likely that the Fed may lower interest rates in 2024, potentially providing a boost to local advertising prospects, but that improvement may come late in the year. But, overall, in spite of the weakening Local advertising environment, given the improving National advertising trends, overall TV advertising appears to have stabilized.

For now, we are cautiously optimistic about 2024, with the caveat that revenue growth may be somewhat tempered given the current weak local advertising trends. Nonetheless, we believe that we are nearing the trough for this economic cycle. Some companies, like E.W. Scripps, are in a favorable cycle for Retransmission renewals. Retransmission revenues now account for a hefty 50% of Scripps’ total broadcast revenue. In Scripps’ case, 75% of its subscribers are under renewal, which it recently announced was completed. As such, the company reaffirmed guidance that Retransmission revenue will increase 15% in 2024 and lead to a substantial increase in net Retransmission revenue. We remain constructive on TV stocks, as high margin Political advertising should boost balance sheets and improve stock valuations.

In the latest quarter, TV stocks underperformed the general market. As Figure #7 Traditional Media 3-Month Performanceillustrates, the Noble TV Index decreased 13.2%, underperforming the 3.6% decline in the general market as measured by the S&P 500. The poor performance of the latest quarter adversely affected the trailing 12 month performance, bringing the Noble TV Index to a 17.6% decline for the trailing 12 months. Individual stocks performed more poorly, with only the shares of Fox Corporation registering a modest gain for the trailing 12 months of 2.7%. The Noble TV Index is market cap weighted, and, as such, Fox with a $15 billion market cap, carried the index. Outside of the relatively strong performance of this large cap stock, all of the TV stocks were down and down big, between 18% to 59% over the past 12 months.

We believe that investors have shied away from cyclicals, smaller cap stocks, and from companies with higher debt levels. This accounts for the poor performance of Gray Television and E.W. Scripps, both of which have elevated debt leverage given recent acquisitions. Both were among the poorest performers for the latest quarter and for the trailing 12 months. The GTN shares were down 12% in the third quarter and 38% for the last 12 months; the SSP shares down 40% and 58%, respectively.

We believe that the sell-off has been overdone, especially as the industry is expected to cycle toward an improved fundamental environment in 2024. As Figure #8 TV Industry Comparables indicate, the Broadcast TV stocks trade at a modest 5.3 times Enterprise Value to our 2024 adj. EBITDA estimates, well below historic 20 year average trading multiples of 8 to 12 times. We believe that the depressed valuations largely discount the prospect of an economic downturn and do not reflect the revenue and cash flow upside as we cycle into a Political year. Given the steep valuation discount to historic levels, we believe that the stocks are 15% to 20% below levels where the stocks normally would be given a favorable Political cycle. Our favorites in the TV space include: Entravision (EVC), one of the beneficiaries of the influx of Political advertising to Hispanics; E.W. Scripps (SSP), a play on Political, with the favorable fundamental tailwind of strong Retransmission revenue growth; and, Gray Television (GTN), one of the leading Political advertising plays.

Figure #8 TV Industry Comparables

Source: Noble estimates & Eikon

Radio Broadcasting

Shoring up balance sheets.

The Radio industry has struggled in the first half as National advertising weakened throughout the year. On average National advertising was down roughly20% or more for many Radio broadcasters. Local held up relatively well, although down in the range of 3% to 5%. Fortunately, for many broadcasters, a push into Digital, which grew in the first half, helped to stabilize total company revenues. As we look to the fourth quarter, we believe that Local advertising is weakening, expected to be down in the range of 5% to 7%, or more in some of the larger markets. But, for some, National advertising is improving, driven by Political advertising. But, Political is not evenly spread. As such, we anticipate that there will be a cautious outlook for many in the industry for the second half of the year.

For some in the industry, the challenged revenue environment has put a strain on managing cash flows to maintain hefty debt loads. We believe that debt leverage is among the top concern for investors. Many of the poorest performing stocks in the quarter and for the trailing 12 months carry some of the highest debt leverage in the industry. The Noble Radio Index decreased a significant 13.7% in the latest quarter compared with a 3.7% decline for the general market. But, a look at the individual stock performance tells a more disappointing story. The shares of Salem Media declined 38% in the latest quarter, bringing 12 month performance to a 44% decline. The shares of iHeart Media decline 49% for the year.

Notably, Salem Media assuaged much of its liquidity concerns with recent asset sales. Such sales will bring in roughly $30 million, allowing it to fully pay off its $22 million revolver and have some flexibility with remaining cash on its balance sheet. We do not believe that investors have fully credited the significance of the recent asset sales.

One bright spot in the group has been the shares of Townsquare Media. While the TSQ shares gave back a significant 27% in the third quarter, the shares are still up 20% over the past 12 months, among one of the best performance in the industry. We believe that the company’s initiation of a substantial dividend resonated with investors.

While the industry faces fundamental headwinds given the current economic challenges, we believe that most companies have made a shift toward faster growth, digital business models. In addition, we believe that Radio will see a lift from Political advertising in 2024, although not to the extent that the TV industry will see. Nonetheless, we look for an improving advertising scenario in 2024. As such, we are constructive on the industry. One of our current favorites leads the industry in its Digital transition, Townsquare Media. As Figure #9 Radio Industry Comparables indicates, the TSQ shares are among the cheapest in the industry, trading at 5.1 times EV to our 2024 adj. EBITDA estimate, well below the average of 7.1 times for the industry. In addition, we like Saga Communications, one of the cheapest stocks in the industry, trading near 4 times EV to 2024 adj. EBITDA.

Figure #9 Radio Industry Comparables

Source: Noble estimates & Eikon

Publishing

Further cost cutting will cut deep.

Publishers are not likely to be spared from the weakening local advertising business. But, publishers have a play book on areas to cut expenses to manage cash flows. Certainly, we believe that its Digital businesses should help offset some of the anticipated revenue declines on its print legacy business. We believe that publishers are eliminating print days. Such a move likely will indicate further pressure on print revenues, but would not proportionately decrease cash flow. Some print days have very little advertising and/or advertisers may shift some spending to other print days. Lee Enterprises indicated in its last call that it will go down to 3 print days in 44 of its smaller markets. We believe that the move has been a success. While revenues may have decreased slightly more than expected given the current weak advertising environment, we believe that cost savings have been more than anticipated.

While many publishers would like to have a long runway for its cash flowing print business, such possible moves would necessarily increase the digital transition. Notably, with just some stabilization of revenues on the print side, many publishers have the potential to show total company revenue growth given benefit from digital revenue. With the prospect of strategies that may cut print days and the current weak local advertising environment, we believe that total revenue growth may be pushed out to 2025.

Many of the Publishing stocks were written off long ago. But, surprisingly, the Publishing stocks have been among the best stock performers in the latest quarter and for the trailing 12 months. The Noble Publishing Index increased a solid 36% in the trailing 12 months, outperforming the general market (as measured by the S&P 500) of 19% in the comparable time frame. In the third quarter, Publishing stocks increased 3.5%, outperforming the S&P 500, which declined 3.7%. All of the publishers increased, with the exception of Lee Enterprises. The Lee shares increased substantially a year earlier on takeover rumors. Since then the shares have come back down to earth, while the rest of the industry moved higher. The stronger performers in the industry, however, were the larger cap companies, such as News Corp and The New York Times. In the latest quarter, the shares of The New York Times increased roughly 5% and the shares are up 27% for the trailing 12 months. The shares of Gannett increased a solid 9% in the latest quarter, as well.

As Figure #10 Publishing Industry Comparables illustrate, there is a disparity among some of the larger, more diversified companies, like The New York Times and News Corporation. The NYT shares trade at a hefty 15.7 times EV to 2024 adj. EBITDA estimates, well above much of the pack currently trading in the 5 multiple range. We believe that this valuation gap should narrow, especially as many of the companies, like Lee and Gannett, have a burgeoning Digital business. While the industry faces secular challenges of its Print business and there are economic headwinds in the very near term, we believe that companies like Lee Enterprises have the ability to manage cash flows and grow its Digital businesses. Given the compelling stock valuation disparity, the shares of Lee Enterprises lead our list of favorites in the sector.

Figure #10 Publishing Industry Comparables

Source: Noble estimates & Eikon

For more information and disclosures on companies mentioned in this report, click on the following:

All statements or opinions contained herein that include the words “we”, “us”, or “our” are solely the responsibility of Noble Capital Markets, Inc.(“Noble”) and do not necessarily reflect statements or opinions expressed by any person or party affiliated with the company mentioned in this report. Any opinions expressed herein are subject to change without notice. All information provided herein is based on public and non-public information believed to be accurate and reliable, but is not necessarily complete and cannot be guaranteed. No judgment is hereby expressed or should be implied as to the suitability of any security described herein for any specific investor or any specific investment portfolio. The decision to undertake any investment regarding the security mentioned herein should be made by each reader of this publication based on its own appraisal of the implications and risks of such decision.

This publication is intended for information purposes only and shall not constitute an offer to buy/sell or the solicitation of an offer to buy/sell any security mentioned in this report, nor shall there be any sale of the security herein in any state or domicile in which said offer, solicitation or sale would be unlawful prior to registration or qualification under the securities laws of any such state or domicile. This publication and all information, comments, statements or opinions contained or expressed herein are applicable only as of the date of this publication and subject to change without prior notice. Past performance is not indicative of future results. Noble accepts no liability for loss arising from the use of the material in this report, except that this exclusion of liability does not apply to the extent that such liability arises under specific statutes or regulations applicable to Noble. This report is not to be relied upon as a substitute for the exercising of independent judgement. Noble may have published, and may in the future publish, other research reports that are inconsistent with, and reach different conclusions from, the information provided in this report. Noble is under no obligation to bring to the attention of any recipient of this report, any past or future reports. Investors should only consider this report as single factor in making an investment decision.

IMPORTANT DISCLOSURES

This publication is confidential for the information of the addressee only and may not be reproduced in whole or in part, copies circulated, or discussed to another party, without the written consent of Noble Capital Markets, Inc. (“Noble”). Noble seeks to update its research as appropriate, but may be unable to do so based upon various regulatory constraints. Research reports are not published at regular intervals; publication times and dates are based upon the analyst’s judgement. Noble professionals including traders, salespeople and investment bankers may provide written or oral market commentary, or discuss trading strategies to Noble clients and the Noble proprietary trading desk that reflect opinions that are contrary to the opinions expressed in this research report. The majority of companies that Noble follows are emerging growth companies. Securities in these companies involve a higher degree of risk and more volatility than the securities of more established companies. The securities discussed in Noble research reports may not be suitable for some investors and as such, investors must take extra care and make their own determination of the appropriateness of an investment based upon risk tolerance, investment objectives and financial status.

Company Specific Disclosures

The following disclosures relate to relationships between Noble and the company (the “Company”) covered by the Noble Research Division and referred to in this research report. Noble is not a market maker in any of the companies mentioned in this report. Noble intends to seek compensation for investment banking services and non-investment banking services (securities and non-securities related) with any or all of the companies mentioned in this report within the next 3 months

ANALYST CREDENTIALS, PROFESSIONAL DESIGNATIONS, AND EXPERIENCE

Senior Equity Analyst focusing on Basic Materials & Mining. 20 years of experience in equity research. BA in Business Administration from Westminster College. MBA with a Finance concentration from the University of Missouri. MA in International Affairs from Washington University in St. Louis. Named WSJ ‘Best on the Street’ Analyst and Forbes/StarMine’s “Best Brokerage Analyst.” FINRA licenses 7, 24, 63, 87

WARNING

This report is intended to provide general securities advice, and does not purport to make any recommendation that any securities transaction is appropriate for any recipient particular investment objectives, financial situation or particular needs. Prior to making any investment decision, recipients should assess, or seek advice from their advisors, on whether any relevant part of this report is appropriate to their individual circumstances. If a recipient was referred to Noble Capital Markets, Inc. by an investment advisor, that advisor may receive a benefit in respect of transactions effected on the recipients behalf, details of which will be available on request in regard to a transaction that involves a personalized securities recommendation. Additional risks associated with the security mentioned in this report that might impede achievement of the target can be found in its initial report issued by Noble Capital Markets, Inc.. This report may not be reproduced, distributed or published for any purpose unless authorized by Noble Capital Markets, Inc..

RESEARCH ANALYST CERTIFICATION

Independence Of View All views expressed in this report accurately reflect my personal views about the subject securities or issuers.

Receipt of Compensation No part of my compensation was, is, or will be directly or indirectly related to any specific recommendations or views expressed in the public appearance and/or research report.

Ownership and Material Conflicts of Interest Neither I nor anybody in my household has a financial interest in the securities of the subject company or any other company mentioned in this report.

Baudax Bio is a pharmaceutical company focused on innovative products for acute care settings. ANJESO is the first and only 24-hour, intravenous (IV) COX-2 preferential non-steroidal anti-inflammatory (NSAID) for the management of moderate to severe pain. In addition to ANJESO, Baudax Bio has a pipeline of other innovative pharmaceutical assets including two novel neuromuscular blocking agents (NMBs) and a proprietary chemical reversal agent specific to these NMBs. For more information, please visit www.baudaxbio.com.

Gregory Aurand, Senior Vice President, Equity Research Analyst, Healthcare Services & Medical Devices, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

Meeting Held October 12, 2023. In an October 13th filing, Baudax Bio reported that proposals submitted to shareholders for a Special Meeting of Shareholders passed. In particular, the Series X convertible preferred stock conversion to common shares was approved. The preferred shares were issued in conjunction with the TeraImmune merger announcement in June. In the merger agreement, Baudax Bio issued 1.212 million shares of common stock, and 27,089.719 shares of Series X convertible preferred to TeraImmune shareholders, with each preferred share convertible into 1,000 shares of common stock.

Amended and Restated Articles of Incorporation Approved. Shareholders also approved an amendment to effect a reverse stock split to be determined by the Board of Directors at any time in the next year, at the Board’s discretion. The Board can set the reverse split within a range of 1:10 to 1:40.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

Shares of clinical-stage biotech Prothena Corp skyrocketed over 20% on Monday amid reports the company is exploring strategic options including a potential sale. Prothena specializes in developing therapies for neurodegenerative diseases like Alzheimer’s, making it a hot target for larger pharmaceutical firms hungry for new assets in this space.

Based in Ireland and spun off from Elan Corp in 2012, Prothena focuses on protein misfolding disorders. Its pipeline features several promising programs targeting proteins believed to play a key role in Alzheimer’s and other neurological conditions with high unmet need.

Prothena’s lead candidate is birtamimab, an antibody-based therapy for AL amyloidosis in late-stage studies. Results expected later this year or in early 2024 could support regulatory filings. Beyond amyloidosis, the company is going all-in on Alzheimer’s research.

The most advanced Alzheimer’s asset is PRX012, an antibody targeting amyloid beta proteins thought to drive disease progression. Prothena is also developing a dual vaccine dubbed PRX012/PRX123 against amyloid beta and tau proteins. Reducing both proteins simultaneously may provide better clinical benefit.

These programs have already attracted partnership interest. Prothena has neuroscience collaborations with pharmaceutical giants Bristol Myers Squibb, Roche, and Novo Nordisk. Just this month, Bristol Myers exercised an option to license PRX005, Prothena’s anti-tau antibody, for nearly $60 million upfront.

But Prothena may seek an acquirer willing to buy the entire company outright. The potential payoff from Alzheimer’s success is massive given the huge unmet need. With late-stage data upcoming, now may be the optimal time for a sale.

Any acquirer would gain full access to Prothena’s Alzheimer’s pipeline, along with its programs for Parkinson’s disease and other neurodegenerative disorders. Adding these diverse assets to an existing neuroscience portfolio could create exciting synergistic opportunities.

Prothena’s small size also makes it financially digestible for big pharma buyers. The company’s market cap sits around $2.5 billion, presenting a worthwhile gamble for majors like Roche or Bristol Myers with scores of billions in annual revenue.

News of the company exploring strategic options sent Prothena shares surging 25% on nearly 6x normal volume. Investors are betting a buyout could be announced in coming months. Prothena’s pipeline progress makes it an alluring target.

Upcoming clinical results will prove whether Prothena’s Alzheimer’s bet pays off scientifically. But from a business perspective, the stars may be aligning for a near-term acquisition. Cash-rich pharmas need new prospects to bolster aging portfolios, and Prothena boasts some of the most exciting neurological assets out there.

If Prothena’s Alzheimer’s programs demonstrate strong efficacy, bidding wars could drive the buyout price sky-high. With biotech valuations rebounding from lows, management may see now as the perfect time to capitalize on these assets. Whether via sale, partnership or remaining independent, Prothena’s future direction should become clearer soon.

Internet & Digital Media Stocks Outperform – But Don’t Get Too Excited

After increasing by 8% in the second quarter of 2023, the S&P 500 was unable to hold onto those gains in the third quarter. The S&P index decreased by 4% in the third quarter, a decline which we attribute to the market revising its interest rate expectations to one in which rates would remain “higher for longer”. Large cap stocks that weighed on the broad market index included tech stocks such as Apple (AAPL: -12%), Microsoft (MSFT: -7%) and Tesla (TSLA: -4%). Despite this small step backwards, the S&P 500 Index increased by 20% through the first nine months of the year.

Each of Noble’s Internet and Digital Media Indices, which are market cap weighted, outperformed the S&P 500 in the third quarter, but the double-digit gains from the previous quarter (2Q 2023) moderated significantly. Sectors that outperformed the S&P 500’s 4% increase include Noble’s Digital Media Index (+6%), Social Media Index (+4%), Gaming Index (+3%), Ad Tech Index (+1%) and MarTech Index (-3%). Despite these relatively positive results, the prevailing theme within each sector was that the largest cap stocks performed the best while smaller cap stocks across a variety of sectors struggled.

STOCK MARKET PERFORMANCE: INTERNET AND DIGITAL MEDIA

Perhaps more importantly, each of Noble’s Internet and Digital Media Indices have outperformed the S&P 500 over the latest twelve months. The S&P 500 Index has increased by 20% over the last year (through 9/30/2023), which trailed the performance of the each of Noble’s Internet and Digital Media Indices, as shown below:

Alphabet Powers Digital Media Index Higher Despite Broader-Based Sector Weakness

The best performing index during the quarter was the Noble’s Digital Media Index, but the sector’s “strong” performance is deceiving. Shares of Alphabet (a.k.a. Google: GOOGL) increased by 9% during the quarter, and the company size relative to its peers helps explain the vast majority of the sector’s performance. Google’s market cap is 8x larger than its next largest “peer” in Netflix, and it is 160 times that of the average market cap of its Digital Media peers. Google beat expectations across all metrics (revenue, EBITDA, free cash flow) and guided to improved profitability as it streamlines workflows. The company is also increasingly perceived as a beneficiary of AI. While Alphabet shares performed well, they mask the fact that shares of only 2 of the sector’s 12 stocks were up during the third quarter. The other Digital Media stock that performed well in the quarter was FUBO (FUBO), whose shares increased by 29% in 3Q 2023. Of the 10 other digital content providers in the sector, 7 of them posted double-digit stock price declines in the third quarter.

Large Cap Meta Powers the Social Media Index Higher

Shares in Meta Platforms (formerly Facebook) rose for the third straight quarter. Shares increased by 5% and were up 150% through the first nine months of the year. Meta shares increased by 8% at the start of the third quarter due to excitement around the launch of Threads, Meta’s answer to Twitter. Over 100 million people signed up for Threads within the first five days of its rollout and positions the company well for continued revenue growth once it begins to monetize this new opportunity.

As with the Digital Media Index, the in the Social Media Index masked underlying weakness across several smaller cap stocks. Of the 6 stocks in the Social Media Index, only Meta shares increased during the quarter. Several social media companies performed poorly during the quarter including Spark Networks (LOVL.Y: -59%), which filed to delist its shares, Nextdoor Holdings (KIND: -44%), which has struggled to reach profitability, and Snap (SNAP: -25%), which guided to revenue declines in 3Q 2023.

Video Gaming, Ad Tech and MarTech Indices Continue the Trend: “No Love” For Small Cap Stocks

As was the case in the Digital Media and Social Media sectors, the same trends held true in the other sectors: in general, large cap stocks outperformed small cap stocks. For example, Noble’s Video Gaming Index increased by 3% in the third quarter, driven by Activision Blizzard (ATVI: +11%), and to a lesser extent SciPlay Corp (SCP: +16%). However, 7 other stocks in the video gaming sector posted stock price declines in the third quarter. Larger cap names such as EA Sports (EA: -7%) and Take-Two Interactive (TTWO: -5%) posted mid-single digit stock price declines while every small cap video gaming stock posted double digit declines.

Noble’s Ad Tech Index increased by 1% during the quarter driven by shares of AppLovin (APP: +55%), and Taboola (TBLA: +22%). However, just 7 of the sector’s 20 stocks were up for the quarter, and 10 stocks in the sector posted double digit declines.

Finally, Noble’s MarTech Index decreased by 3% (the only index that declined during the quarter), with the sector’s largest companies, Adobe (ADBE: +4%) and Shopify (SHOP: -16%) posting mixed results. Outside of these mega-cap stocks, the theme of underlying weakness prevailed: only 5 of the 20 stocks in the sector posted stock price increases, while one was flat and the other 14 were down. Eleven of the 20 stocks in the MarTech sector posted double digit stock price declines.

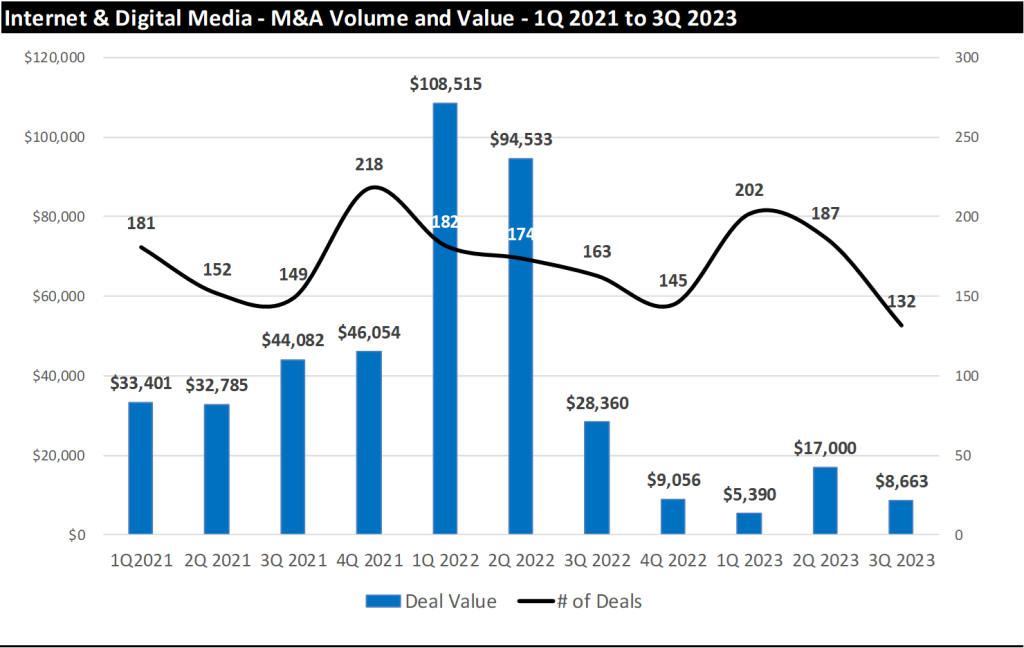

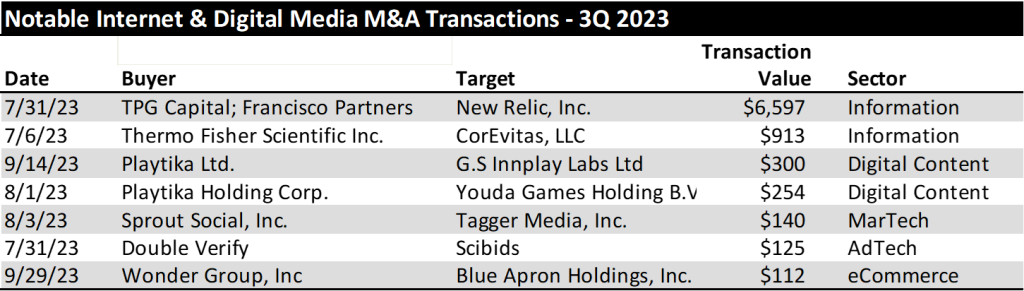

3Q 2023 Internet and Digital Media M&A – A Significant Slowdown

According to Dealogic, which tracks global M&A, deal activity in North America decreased by 37% to 8,600 deals in the third quarter, however, the value of deals in North America increased by 34% to $375 billion. Dealogic noted that there was an increase in the number of scaled transactions (those with deal values in the $1 billion to $2 billion range), which increased to the highest level in 7 quarters. We did not see this phenomenon in Noble’s Internet & Digital Media sectors.

Based on our analysis, deal making in the Internet & Digital Media sectors in the third quarter of 2023 slowed rather dramatically. The total number of Internet & Digital Media deals we tracked in the quarter decreased by 29% sequentially to 132 deals in 3Q 2023 down from 169 deals in 2Q 2023. On a year-over-year basis, the total number of deals decreased by 22% to 132 deals in 3Q 2023 from 187 deals in the third 3Q 2022.

The decline in the number of deals was exceeded only by the decline in the dollar value of M&A deals. Announced M&A deal value fell sequentially by 50% to $8.7 billion in 3Q 2023 compared to $17.2 billion in announced deals in 2Q 2023. While total deal value of announced deals decreased significantly on a quarter-over-quarter basis, the decrease was even more pronounced on a year-over-year basis, as deal values decreased by 71% to $8.7 billion in deal value from $29.4 billion in 3Q 2022, as shown in the chart on the next page.

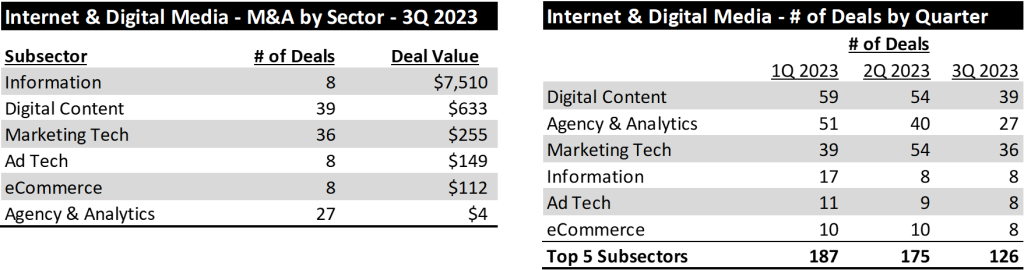

From a deal activity perspective, the most active sectors we tracked were Digital Content (39 deals), MarTech (36 deals) and Agency & Analytics (27 deals). From a dollar value perspective, Information Services led with $7.5 billion, followed by Digital Content with $633 million and MarTech with $255 million, as shown below (left).

As shown above (right), the number of transactions has fallen in each of the last two quarters. Across the top 5 subsectors of Internet and Digital Media, the number of transactions has fallen from 187 transactions in the first quarter to 126 transactions in the third quarter.

We attribute this decline to a variety of factors. First, an increase in interest rates has resulted in far fewer transactions in excess of $10 billion. With rates 300 basis points higher than at the start of the year, an incremental $10 billion in debt implies a $30 million per year increase in interest expense. These higher rates result in lower returns for acquirers. Second, we believe traditional lenders have become more cautious in providing the necessary capital to fund acquisitions. Some have pointed to commercial banks and their large exposure to commercial real estate as a reason for this more cautious view. Finally, for advertising-based businesses, there are some indications that brands are waiting longer before committing to or booking ad campaigns, which has reduced visibility and made financial forecasting more difficult.

Information and Video Gaming Deals Drive the Largest Transactions in 3Q 2023

There were far fewer $100M+ transactions 3Q 2023. In the second quarter of 2023 there were 16 transactions in the Internet & Digital Media sector with transaction values greater than $100 million. In the third quarter, that amount slowed to less than half: just 7 transactions exceeded $100 million in purchase price. The Information Services sector accounted for the two largest transactions in the quarter, followed by Digital Content deals, in particular gaming deals. The list of M&A transactions that exceeded $100 million are shown in the chart below.

We believe the M&A market has slowed as corporations get accustomed to the prospect of higher rates for longer. One key driver of future M&A could come from distressed M&A dealmaking. Finally, another area of increased activity could come from U.S. corporations acquiring European companies where relatively weaker European currencies are making the valuations of European companies look more attractive.

TRADITIONAL MEDIA COMMENTARY

The following is an excerpt from a recent note by Noble’s Media Equity Research Analyst Michael Kupinski

Overview – The Case for Small Caps

Small cap investors have gone through a rough period. For the past several years, investors have anticipated an economic downturn. With these concerns, investors turned toward “safe haven,” large cap stocks, which typically have the ability to weather the economic headwinds and have enough trading volume should investors need to exit the position. Since 2018, small cap stocks have underperformed the general stock market, with annualized returns of just 3.7% as measured by the S&P 600 Small Cap Index versus the general market of 10.2% as measured by the S&P 500 Index. Another small cap index, the Russell 2000, increased a more modest 2.9% annually over the comparable period. The S&P 500 is larger cap, with the minimum market cap of $14.6 billion. The S&P 600 is smaller cap, a range of $850 million to $3.7 billion, with the Russell 2000 median market cap $950 million. Some of the even smaller cap stocks, those between $100 million to $850 million, have significantly underperformed the S&P 600. This is the first time that small caps underperformed a bullish period for all stocks since the 1940s. Notably, there is a sizable valuation disparity between the two classes, large and small cap, one of the largest in over 20 years.

Some of the small cap stocks we follow trade at a modest 2x Enterprise Value to EBITDA, compared with large cap valuations as high as 13x to 15x. By another measure, small cap stocks may be the only class trading below historic 25 year average to the median Enterprise Value to EBIT. Why the large valuation disparity? We believe that there is higher risk in the small cap stocks, especially given that some companies may not be cash flow positive, have capital needs, or have limited share float. But investors seem to have thrown the baby out with the bathwater. While those small cap stocks are on the more speculative end of the scale, many small cap stocks are growing revenues and cash flow, have capable balance sheets, and/or are cash flow positive. For attractive emerging growth companies, the trading activity will resolve itself over time. Some market strategists suggest that small cap stocks trade at the most undervalued in the market, as much as a 30% to 40% discount to fair value.

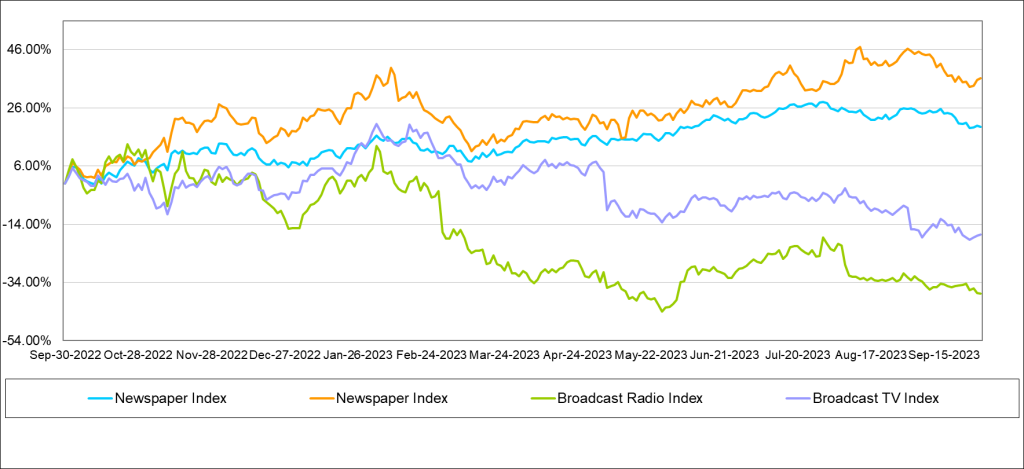

STOCK MARKET PERFORMANCE: TRADITIONAL MEDIA

Are we on the cusp of a small cap cycle? Some fund managers think so. Such a cycle could last 10 years or longer. In this report, we highlight a few of our small cap favorites in the Media sector, those include companies that have attractive growth characteristics, some with or without an improving economy, capable balance sheets, and limited capital needs. Our current favorites based on growth opportunity and stock valuation include: Direct Digital (DRCT), Entravision (EVC), E.W. Scripps (SSP), Gray Television (GTN), and Townsquare Media (TSQ).

Traditional Media Stock Price Performance

Virtually all traditional media stocks underperformed the general market in the past quarter and trailing 12 months, except for the Publishing group, as shown in the chart at the bottom of the previous page. In the latest quarter, Publishing stocks outperformed the general market, up 3% versus down 4% for the general market as measured by the S&P 500 Index. The average Publishing stock is up 7% over the past 12 months, with some of the larger cap publishing stocks up significantly more, over 20%. More details on the Publishing performance is in the Publishing section of this report. In the last quarter, the Radio stocks were the worst performing group, down on average 10%. In addition, the Radio stocks were the worst performing group in the third quarter as well, down an average of 13% for the quarter.

Broadcast Television

Have TV Stocks Been Discounted Too Much?

We believe that the economic headwinds of rising interest rates and inflation have begun to hit local advertising. Local advertising had been relatively stable, favorably influenced by a resurgence of auto advertising. Notably, local advertising fared much better than national advertising, which was down in the absence of political advertising. As we look toward the third quarter, local advertising appears to be weakening, but notably, national advertising appears to be doing much better, driven by an early influx of political advertising. While it was assumed that political would increase in the fourth quarter due to the run-off of the Republican presidential candidates, especially in early primary States, we believe that President Biden has recently stepped-up advertising, particularly to the Hispanic community. We have noticed Biden advertising even in Florida! So, what does this mean for media fundamentals?

It is difficult to predict where political dollars will be spent and not all political dollars will be spent evenly, geographically or by stations in a particular market. Furthermore, political dollars may be pulled back in a market should a particular candidate pull ahead in the polls. Political dollars were anticipated to be spent in early primary States, specifically for the Republican candidates. But the Biden money is a surprise. Biden appears to be spending early and in areas to solidify a key voting block, Hispanics. Of course, the Biden campaign may broaden its spending to other voting blocks as well. In our view, 2024 will be a banner year for political advertising given the large amount of political fundraising by the candidates and by Political Action Committees.

The prospect of weak local advertising, however, may cast a pall over the current expected strong revenue growth in 2024. Many analysts, including myself, expected that economic prospects would improve in 2024, which would have provided a favorable tailwind for a significant improvement in total TV advertising in 2024. Certainly, it is likely that the Fed may lower interest rates in 2024, potentially providing a boost to local advertising prospects, but that improvement may come late in the year. Overall, in spite of the weakening Local advertising environment, given the improving National advertising trends, overall TV advertising appears to have stabilized.

For now, we are cautiously optimistic about 2024, with the caveat that revenue growth may be somewhat tempered given the current weak local advertising trends. Nonetheless, we believe that we are nearing the trough for this economic cycle. Some companies, like E.W. Scripps, are in a favorable cycle for retransmission renewals. Retransmission revenues now account for a hefty 50% of Scripps’ total broadcast revenue. In Scripps’ case, 75% of its subscribers are under renewal, which it recently announced was completed. As such, the company reaffirmed guidance that retransmission revenue will increase 15% in 2024 and lead to a substantial increase in net retransmission revenue. We remain constructive on TV stocks, as high margin political advertising should boost balance sheets and improve stock valuations.

In the latest quarter, TV stocks underperformed the general market. The Noble TV Index decreased 13%, underperforming the 4% decline in the general market as measured by the S&P 500. The poor performance of the latest quarter adversely affected the trailing 12 month performance, bringing the Noble TV Index to a 18% decline for the trailing 12 months. Individual stocks performed more poorly, with only the shares of Fox Corporation registering a modest gain for the trailing 12 months of 3%. The Noble TV Index is market cap weighted, and, as such, Fox with a $15 billion market cap, carried the index. Outside of the relatively strong performance of this large cap stock, all of the TV stocks were down and down big, between 18% to 59% over the past 12 months.

We believe that investors have shied away from cyclicals, smaller cap stocks, and from companies with higher debt levels. This accounts for the poor performance of Gray Television (GTN) and E.W. Scripps (SSP), both of which have elevated debt leverage given recent acquisitions. Both were among the poorest performers for the latest quarter and for the trailing 12 months. GTN shares were down 12% in the third quarter and 38% for the last 12 months; the SSP shares down 40% and 58%, respectively.

We believe that the sell-off has been overdone, especially as the industry is expected to cycle toward an improved fundamental environment in 2024. As shown in the comp sheet on page 20, Broadcast TV stocks trade at a modest 5.3x Enterprise Value to our 2024 adj. EBITDA estimates, well below historic 20-year average trading multiples of 8x to 12x. We believe that the depressed valuations largely discount the prospect of an economic downturn and do not reflect the revenue and cash flow upside as we cycle into a political year. Given the steep valuation discount to historic levels, we believe that the stocks are 15% to 20% below levels where the stocks normally would be given a favorable political cycle. Our favorites in the TV space include: Entravision (EVC), one of the beneficiaries of the influx of political advertising to Hispanics; E.W. Scripps (SSP), a play on political, with the favorable fundamental tailwind of strong retransmission revenue growth; and, Gray Television (GTN), one of the leading political advertising plays.

Broadcast Radio

Shoring Up Balance Sheets

The Radio industry has struggled in the first half as National advertising weakened throughout the year. On average National advertising was down roughly 20% or more for many Radio broadcasters. Local held up relatively well, although down in the range of 3% to 5%. Fortunately, for many broadcasters, a push into digital, which grew in the first half, helped to stabilize total company revenues. As we look to the third and fourth quarters, we believe that Local advertising is weakening, expected to be down in the range of 5% to 7%, or more in some of the larger markets. For some, National advertising is improving, driven by political advertising. However, political is not evenly spread, so we anticipate that there will be a cautious outlook for many in the industry for the second half of the year.

For some in the industry, the challenged revenue environment has put a strain on managing cash flows to maintain hefty debt loads. We believe that debt leverage is among the top concerns for investors. Many of the poorest performing stocks in the quarter and for the trailing 12 months carry some of the highest debt leverage in the industry. The Noble Radio Index decreased a significant 14% in the latest quarter compared with a 4% decline for the general market. A look at the individual stock performance tells a more disappointing story. Shares of Salem Media declined 38% in the latest quarter, bringing 12-month performance to a 44% decline. Shares of iHeart Media declined 49% for the year.

Notably, Salem Media assuaged much of its liquidity concerns with recent asset sales. Such sales will bring in roughly $30 million, allowing it to fully pay off its $22 million revolver and have some flexibility with remaining cash on its balance sheet. We do not believe that investors have fully credited the significance of the recent asset sales.

One bright spot in the group was the shares of Townsquare Media (TSQ). While TSQ shares gave back a significant 27% in the third quarter, the shares are still up 20% over the past 12 months, among one of the best performing in the industry. We believe that the company’s initiation of a substantial dividend resonated with investors.

While the industry faces fundamental headwinds given the current economic challenges, we believe that most companies have made a shift toward faster growth, digital business models. In addition, we believe that Radio will see a lift from political advertising in 2024, although not to the extent that the TV industry will see. Nonetheless, we look for an improving advertising scenario in 2024, and as a result, we are constructive on the industry. One of our current favorites leads the industry in its Digital transition, Townsquare Media. As shown in the comp sheet on page 21, TSQ shares are among the cheapest in the industry, trading at 5.1x EV to our 2024 adj. EBITDA estimate, well below the average of 7.1x for the industry.

Publishing

Further Cost Cutting Will Cut Deep

Publishers are not likely to be spared from the weakening local advertising business, but publishers have a playbook on areas to cut expenses to manage cash flows. We believe that its Digital businesses should help offset some of the anticipated revenue declines on its print legacy business. We believe that the next round will cut deep into its legacy business, through the elimination of print days. Such a move likely will indicate further pressure on print revenues but would not proportionately decrease cash flow. Some print days have very little advertising and/or advertisers may shift some spending to other print days.

While many publishers would like to have a long runway for its cash flowing print business, such possible moves would accelerate the digital transition. Notably, with just some stabilization of revenues on the print side, many publishers have the potential to show total company revenue growth given benefit from digital revenue. With the prospect of strategies that may cut print days, we believe that total revenue growth may be pushed out to 2025.

Many of the Publishing stocks were written off long ago, but surprisingly, the Publishing stocks have been among the best stock performers in the latest quarter and for the trailing 12 months. The Noble Publishing Index increased a solid 36% in the trailing 12 months, outperforming the general market (as measured by the S&P 500) of 19% in the comparable time frame.

In the third quarter, Publishing stocks increased 4%, outperforming the S&P 500, which declined 4%. All of the publishers increased, with the exception of Lee Enterprises (LEE). Lee shares increased substantially a year earlier on takeover rumors. Since then, the shares have come back down to earth, while the rest of the industry moved higher. The stronger performers in the industry, however, were the larger cap companies, such as News Corp (NWSA) and The New York Times (NYT). In the latest quarter, the shares of The New York Times increased roughly 5% and the shares are up 27% for the trailing 12 months. The shares of Gannett increased a solid 9% in the latest quarter, as well.

As the Newspaper comp sheet on page 22 illustrates, there is a disparity among some of the larger, more diversified companies, like The New York Times and News Corporation. NYT shares trade at a hefty 15.7x EV to 2024 adj. EBITDA estimates, well above much of the pack currently trading in the 5x multiple range. We believe that this valuation gap should narrow, especially as many of the companies, like Lee and Gannett, have a burgeoning Digital business. While the industry faces secular challenges of its print business and there are economic headwinds in the very near term, we believe that companies like Lee Enterprises have the ability to manage cash flows and grow its digital businesses. Given the compelling stock valuation disparity, the shares of Lee Enterprises lead our list of favorites in the sector.

This newsletter was prepared and provided by Noble Capital Markets, Inc. For any questions and/or requests regarding this news letter, please contact Chris Ensley

DISCLAIMER

All statements or opinions contained herein that include the words “ we”,“ or “ are solely the responsibility of NOBLE Capital Markets, Inc and do not necessarily reflect statements or opinions expressed by any person or party affiliated with companies mentioned in this report Any opinions expressed herein are subject to change without notice All information provided herein is based on public and non public information believed to be accurate and reliable, but is not necessarily complete and cannot be guaranteed No judgment is hereby expressed or should be implied as to the suitability of any security described herein for any specific investor or any specific investment portfolio The decision to undertake any investment regarding the security mentioned herein should be made by each reader of this publication based on their own appraisal of the implications and risks of such decision This publication is intended for information purposes only and shall not constitute an offer to buy/ sell or the solicitation of an offer to buy/sell any security mentioned in this report, nor shall there be any sale of the security herein in any state or domicile in which said offer, solicitation or sale would be unlawful prior to registration or qualification under the securities laws of any such state or domicile This publication and all information, comments, statements or opinions contained or expressed herein are applicable only as of the date of this publication and subject to change without prior notice Past performance is not indicative of future results.

Please refer to the above PDF for a complete list of disclaimers pertaining to this newsletter.

Pharmaceutical giant Pfizer stunned investors on Friday by making drastic reductions to its 2023 earnings and revenue guidance, driven entirely by rapidly declining demand for its COVID-19 vaccine and treatment.

The company now expects full-year sales of $58-61 billion, far below its previous projection of $67-70 billion. Adjusted earnings per share were cut even more drastically, from an expected $3.25-3.45 down to just $1.45-1.65.

The huge forecast reduction was prompted by a projected $7 billion drop in sales of Pfizer’s COVID treatment Paxlovid and a $2 billion decline for its Comirnaty vaccine. This comes amidst clear signs of “COVID fatigue” as vaccination rates slow and cases become milder.

Pfizer’s update led to a sell-off of its stock on Friday. Rival vaccine maker Moderna’s shares also dropped on the news, reflecting similar downbeat trends for COVID products industrywide.

However, Pfizer regained some losses after executives held a call on Monday to outline plans for weathering the abrupt COVID revenue downturn. This includes a new cost-cutting program aiming to deliver $1 billion in savings this year and $2.5 billion by 2024.

The planned cuts will touch all business segments and regions, though details remain scarce. Pfizer says one-time costs to implement the reductions will be approximately $3 billion, including severance charges and other expenses.

This belt-tightening comes after Pfizer hinted in August it was prepared to trim expenses if COVID product sales continued to deteriorate. “We are in the middle of the COVID fatigue. Nobody wants to speak about COVID,” acknowledged CEO Albert Bourla.

Indeed, uptake for Pfizer’s updated Omicron booster has been lackluster since launching last month. Logistical hurdles and lack of awareness around eligibility have hampered rollout. Waning concern over infections has also lowered demand.

Paxlovid prescriptions have similarly collapsed as immunity from vaccines and prior disease leaves most cases mild. Bourla said this means the remaining demand is coming from the minority focused on prevention and protection.

Looking beyond COVID products, Pfizer still expects to complete its pending $12 billion acquisition of cancer detection leader Seagen on schedule. Executives said the belt-tightening and forecast revisions will not impact those plans.

Pfizer is not alone in adapting to new COVID realities. Moderna has delayed advancing new boosters and vaccines meant to target emerging variants. Merck has paused production of its Molnupiravir antiviral.

But Pfizer’s aggressive pandemic investments leave it most exposed to lasting changes in demand. The company marshaled its resources early on to supply over 3.5 billion vaccine doses worldwide, along with millions of Paxlovid courses.

Now, the record revenues these products delivered are evaporating almost overnight. And as the market leader, Pfizer’s woes signal a new chapter for the entire vaccine and antiviral space.

Of course, the pandemic is not over, and COVID will remain a threat demanding vaccines and treatments. But with most people vaccinated, reinfected, or both, demand and profits are inevitable casualties absent a dangerous new variant.

For pharmaceutical firms like Pfizer and Moderna, the cash windfall from COVID spending is clearly drawing to a close. With customers, cash flows and share prices dropping, a reckoning has arrived. Massive cost cuts offer one path forward, with layoffs and restructuring the vaccines’ unintended side effect.

With the recent rise in mergers and acquisitions in the biotech sector, some analysts believe that now is an opportune time for investors to start positioning themselves in small and microcap biotech stocks. Though these smaller companies have been out of favor with investors in the post-pandemic environment, the current conditions suggest their fortunes may soon change.

The biotech sector saw a surge of interest during the pandemic, as companies raced to develop vaccines, treatments and diagnostics for COVID-19. Many smaller biotechs saw their values skyrocket on the hope that they would come up with a breakthrough. However, once the initial rush of COVID-related products came to market, investors began rotating out of pandemic darlings and into recovery plays. This led to a dramatic decline in the valuations of micro and small cap biotechs.

Despite this negative sentiment, mergers and acquisitions in biotech have been increasing over the past year. Pharma giants have been scooping up smaller firms to replenish their drug pipelines. While the big deals have gotten all the headlines, analysts say more deal-making is starting to occur further down the market cap scale. This suggests that the fundamentals of select smaller biotechs remain strong, though valuations do not yet reflect it.

Take Eledon Pharmaceuticals (ELDN) for example. This clinical stage biotech has a market cap of only $35 million, which is about half its cash on their 6/30/23 balance sheet . Though its lead drug candidate is in Phase 2 trials for several indications, the company’s stock price has languished. However, with ample cash to support ongoing trials and an approved IND for another preclinical asset, Eledon seems significantly undervalued based on peers.

In fact, many small biotechs appear mispriced today based on the potential of their underlying technology and pipelines. These companies are developing innovative new platforms and drug candidates across therapeutic areas like oncology, rare diseases, neurology, and ophthalmology. While risks are high during the R&D process, achieving clinical milestones and a path to successful commercialization could drive exponential growth.

Consider the market opportunity for breakthrough platforms like CRISPR gene editing or cell therapy. Many smaller firms are advancing novel applications of these cutting-edge technologies. If proven successful in clinical studies, even niche indications could generate billions in peak annual sales.

Additionally, smaller firms tend to be more targeted in their R&D approach. Rather than spreading efforts across numerous indications, microcaps often concentrate on 1-2 assets with large treatment populations. This focused strategy allows them to achieve key milestones more economically. Partnerships with larger biopharma companies can also help offset expenses in later stage development.

The current biotech environment shares some similarities with pandemic euphoria. Today’s misery and fear echoes the extreme euphoria felt by investors three years ago. Just as sentiment eventually turned negative on pandemic darlings, the same could occur for today’s recovery favorites. Already, tech giants like Meta, Nvidia and Tesla have fallen substantially from their highs, suggesting a potential peak.

While rotating out of pandemic favorites made sense as reopening plays gained momentum, the economic backdrop is cloudier now. High inflation, rising rates, geopolitical tensions and recession fears have driven significant equity declines and increased market volatility this year. This has led some investors to question whether stocks still offer favorable risk-reward profiles.

With bonds and equity markets declining in tandem, some investors have turned to cash equivalents like money market funds. While these instruments can provide principal protection, their yields could still lag inflation, given its uncertain outlook. Accounting for taxes owed on interest earned further reduces the chances of a real return. Therefore, holding too much cash during periods of high inflation could erode purchasing power over time.

Rather than accept guaranteed, but potential negative real returns in cash, investors may want to revisit beaten-down assets with asymmetric upside, like small cap biotech stocks. Some of these companies offer innovative technologies that could drive explosive growth if their development and commercialization efforts prove successful, and investor sentiment in this sector turns around.

To identify promising opportunities in the space, investors need to educate themselves on individual companies, study various ideas and leverage resources like Channelchek. While risks for small biotech stocks are always high, those able to discern winners from losers can potentially generate substantial outsized gains.

After years of hype around pandemic favorites, optimism needs to be rekindled for forgotten pockets of the market like micro and small cap biotech stocks. For investors with the appropriate time horizon and risk tolerance, now could be the ideal time to start building positions. If M&A activity continues apace, it likely will not be long before positive fundamentals translate into rising valuations.

HOUSTON, Oct. 13, 2023 (GLOBE NEWSWIRE) — Orion Group Holdings, Inc. (NYSE: ORN) (“Orion” and “Company”), a leading specialty construction and engineering company today announced a significant contract award valued at over $100 million for its Marine and Engineering business. The contract was awarded by Grand Bahama Shipyard Limited (GBSL) for the turnkey design-build of the Grand Bahama Shipyard Dry Dock Replacement Project, situated in Grand Bahama, Bahamas. In addition, the Company was recently awarded new contracts in both its Concrete and Marine segments for a combined total of $121 million.

Orion Group Holdings won the Grand Bahama Shipyard Dry Dock award through a competitive bid/negotiation process based on demonstrating its multiple core skill competencies. The scope of work includes marine works and infrastructure construction, dredging, creating new mooring facilities, and providing enhancements to shore stability. In addition, Orion will modify and extend service piers for the installation of two cutting-edge floating dry docks, which are among the largest in the western hemisphere. The project is set to commence immediately and will conclude in late 2025. Orion will be working with Bahamian subcontractors on the project.

Travis Boone, President and Chief Executive Officer of Orion Group Holdings, said, “The scope of the Bahama project demonstrates the extensive capabilities and commitment to predictable excellence that our integrated Marine & Engineering teams can deliver to large-scale and complex projects. We are excited to embark on this project and look forward to contributing to the growth and success of the Grand Bahama Shipyard.”

“When completed, the Grand Bahama dry docks will be a milestone in the maritime industry. With this enormous undertaking, Grand Bahama Shipyard will have the first floating dry docks for the Atlantic region capable of lifting the largest cruise ships in the world. The installation of two state-of-the-art floating dry docks, categorized as XL and Mega XL, promises substantial efficiency and cost savings for GBSL’s customers.”