Nearly 70% of Served Population Face Limited Access to a Local Pharmacy

OVERLAND PARK, Kan.–(BUSINESS WIRE)– SelectQuote, Inc. (NYSE: SLQT) (the “Company”), a leading distributor of Medicare insurance policies and owner of a rapidly-growing healthcare services platform, today released a new research brief offering in-depth insights into the complex medical and social needs of the population it serves. The findings from tens of thousands of patient health needs assessments gathered by the Company’s Healthcare Select division highlight significant challenges across chronic care management, medication access, and financial security, underscoring the critical industry need for personalized, integrated healthcare solutions.

Key Research Findings:

Underserved Beneficiaries: Given that SelectQuote and Healthcare Select connect with beneficiaries telephonically, this population significantly over-indexes in historically-underserved areas lacking significant access to more traditional healthcare providers. 45% of Healthcare Select members reside in a rural zip code and 36% reside in an urban zip code, while only 11% reside in a suburban zip code.

Chronic Conditions: 74% of the population reported that they are dealing with two or more chronic conditions.

High Prescription Use: 75% of members regularly take 5 or more prescriptions.

Financial Headwinds: As 77% of SelectRx patients report annual household income of under $20,000, Social Determinants of Health often compound the treatment of health issues. 19% report having trouble accessing food on a regular basis. 36% indicate they are worried about being able to pay for bills if they were to face a serious illness.

Medication Delays: 16% of Healthcare Select members report having delayed taking medication for financial reasons.

Adherence Challenges: 40% of members have reported either forgetting to take their medications or failing to pick up prescriptions from a pharmacy. Independent studies indicate that failure to take medications consistently as prescribed (i.e., non-adherence) contributes to reduced treatment efficacy and poor disease control, higher rates of emergency department visits and hospitalizations, and increased morbidity and mortality.

Limited Pharmacy Access: Given their geographic concentration, approximately ⅔ of the population served by the Company’s SelectRx pharmacy reside in a “pharmacy desert” with limited access to local pharmacies.

Transportation: The headwinds to quality pharmacy access are exacerbated by the fact that 31% of Healthcare Select members report that they lack access to reliable transportation.

“This research provides a clear, data-driven look at the barriers to care faced by a large segment of the Medicare-eligible population,” said Bob Grant, SelectQuote President. “The high prevalence of chronic conditions, coupled with geographic and financial obstacles, illustrates why traditional one-size-fits-all healthcare is insufficient. We are committed to using this data to drive personalized solutions that effectively address these gaps.”

Mr. Grant continued, “We purpose-built Healthcare Select and our SelectRx pharmacy model to meet the needs of these underserved Medicare beneficiaries by combining telephonic outreach, personalized care coordination, direct prescription delivery, and packaging that improves adherence. By removing barriers like transportation and limited local pharmacy access, SelectRx helps patients manage complex medication regimens and improves adherence, ultimately driving better health outcomes.”

As Healthcare Select works to address members’ most pressing gaps in care — specifically in medication adherence, Social Determinants of Health, remote diagnostics and therapeutics, and chronic condition management — the Company actively seeks partners. SelectQuote invites innovative organizations and solution providers to connect with its Business Development team to collaboratively address these pressing issues impacting member care.

About SelectQuote:

Founded in 1985, SelectQuote (NYSE: SLQT) pioneered the model of providing unbiased comparisons from multiple, highly-rated insurance companies, allowing consumers to choose the policy and terms that best meet their unique needs. Two foundational pillars underpin SelectQuote’s success: a strong force of highly-trained and skilled agents who provide a consultative needs analysis for every consumer, and proprietary technology that sources and routes high-quality leads. Today, the Company operates an ecosystem offering high touchpoints for consumers across insurance, pharmacy, and virtual care.

With an ecosystem offering engagement points for consumers across insurance, Medicare, pharmacy, and value-based care, the company now has three core business lines: SelectQuote Senior, SelectQuote Healthcare Services, and SelectQuote Life. SelectQuote Senior serves the needs of a demographic that sees around 10,000 people turn 65 each day with a range of Medicare Advantage and Medicare Supplement plans. SelectQuote Healthcare Services is comprised of the SelectRx Pharmacy, a Patient-Centered Pharmacy Home™ (PCPH) accredited pharmacy, SelectPatient Management, a provider of chronic care management services, and Healthcare Select, which proactively connects consumers with a wide breadth of healthcare services supporting their needs.

Commercial Metals Company (NYSE: CMC) announced it will acquire Foley Products Company, a leading supplier of precast concrete solutions in the southeastern United States, for $1.84 billion in cash. The move marks CMC’s formal entry into the precast industry and follows its recently announced acquisition of Concrete Pipe & Precast (CP&P).

CMC said the acquisitions of Foley and CP&P will establish the company as the third largest precast platform in the U.S., operating 35 facilities across 14 states, and a market leader in the Mid-Atlantic and Southeast regions.

“The acquisition of Foley presents a unique opportunity to create immediate scale for our precast platform while adding a best-in-class business with industry-leading margins to CMC’s portfolio,” said Peter Matt, President and Chief Executive Officer of Commercial Metals. “We believe precast has significant value creation potential for CMC, and the addition of Foley will help unlock further upside from our pending acquisition of CP&P.”

Foley Products is known for its industry-leading EBITDA margins and cash flow generation, supported by well-established best practices and a broad portfolio of precast solutions. The purchase price represents a 10.3x multiple of Foley’s forecasted 2025 EBITDA, or roughly 9.2x when factoring in expected cash tax benefits.

The transaction is expected to be immediately accretive to earnings per share and free cash flow, with $25 million to $30 million in annual run-rate synergies anticipated by the third year. Synergies will primarily stem from operational efficiencies, cost reductions, and cross-selling opportunities across complementary geographic markets.

Following the integration of Foley and CP&P, CMC expects its core EBITDA margin to increase by approximately 210 basis points, with about 32% of total pro forma segment adjusted EBITDA generated by its Emerging Businesses Group and precast platform — up from 15% in fiscal 2025. The company also expects strong free cash flow generation, targeting a reduction in net leverage from 2.7x to below 2.0x within 18 months.

CMC emphasized that the precast concrete market — estimated at $30 billion in annual U.S. revenue — provides a strong strategic fit, leveraging the company’s existing relationships in early-stage construction and expanding its reach into mission-critical infrastructure applications.

Precast components, such as concrete pipes and utility structures, are manufactured off-site in controlled environments, offering faster installation times, improved quality, and reduced labor needs compared to traditional pour-in-place methods.

Noble Capital Markets Research Report Thursday, October 16, 2025

Companies contained in today’s report:

Alliance Resource Partners (ARLP)/OUTPERFORM – Highlights from the Noble Emerging Growth Virtual Conference Comstock (LODE)/MARKET PERFORM – Strategic Acquisition Expands Nevada Mining Footprint Nicola Mining Inc. (HUSIF)/OUTPERFORM – Hitting All the Right Notes

Alliance Resource Partners (ARLP/$24.6 | Price Target: $32) Mark Reichman mreichman@noblefcm.com | (561) 999-2272 Hans Baldau hbaldau@noblefcm.com | Highlights from the Noble Emerging Growth Virtual Conference Rating: OUTPERFORM

Noble virtual conference. Alliance recently participated in Noble Capital Markets’ Emerging Growth Virtual Conference. The fundamental outlook for ARLP’s coal operations and oil and gas royalty business, the two largest drivers of cash flow, remains favorable. The coal and electric power generation industries are expected to benefit from Trump Administration policies that seek to assure affordable, reliable, and secure energy sources to meet growing demand for electricity. Through 2Q 2025, Alliance has invested $758 million in its oil and gas royalty business that has generated cumulative segment adjusted EBITDA of $622 million. While they have grown the oil and gas royalty business without the use of leverage, they do have the ability to employ leverage for larger acquisitions. A link to the presentation is here.

Capital allocation. Management takes a long-term view when making capital allocation decisions, with balance sheet strength being the highest priority. The next priority is investing in its coal business to ensure it remains an efficient and low-cost producer. The third priority is reinvesting the cash flow generated by the oil and gas business to make accretive acquisitions. Lastly, the company intends to return capital to shareholders, including attractive cash distribution payments, while ensuring flexibility to fund growth opportunities.

Acquisition of Haywood Quarry. Comstock completed the acquisition of the Haywood Quarry industrial and mineral properties from Decommissioning Services LLC. The 190-acre property, located in Lyon County, Nevada, includes available power, water, and direct access to U.S. Highway 50. The site historically hosted gold mining and aggregate operations and is strategically contiguous to Comstock’s flagship Dayton gold and silver resource.

Transaction terms. Comstock acquired the property for a total of $2.2 million in cash and stock from Decommissioning Services LLC. The transaction provides Comstock with full ownership and control of the Haywood industrial and mineral properties, integrating them into its broader Lyon County mineral estate. The purchase also enhances Comstock’s strategic flexibility in advancing mine planning, resource development, and reclamation initiatives at the Dayton complex.

Nicola Mining Inc. (HUSIF/$0.77 | Price Target: $1.2) Mark Reichman mreichman@noblefcm.com | (561) 999-2272 Hitting All the Right Notes Rating: OUTPERFORM

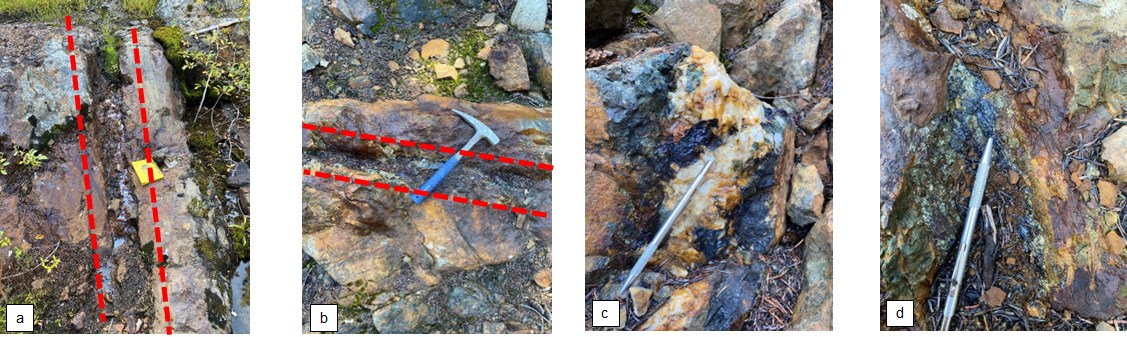

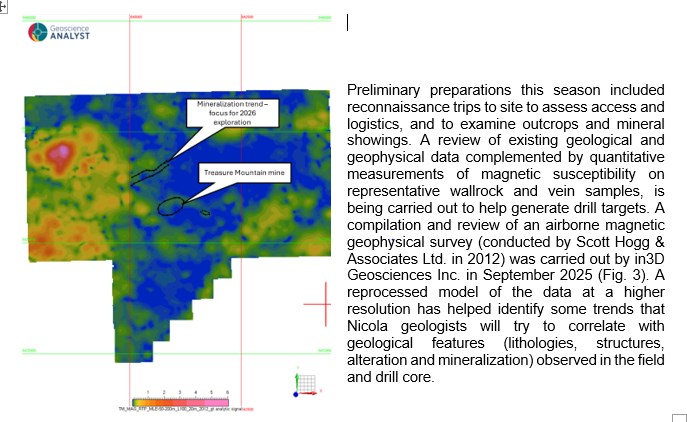

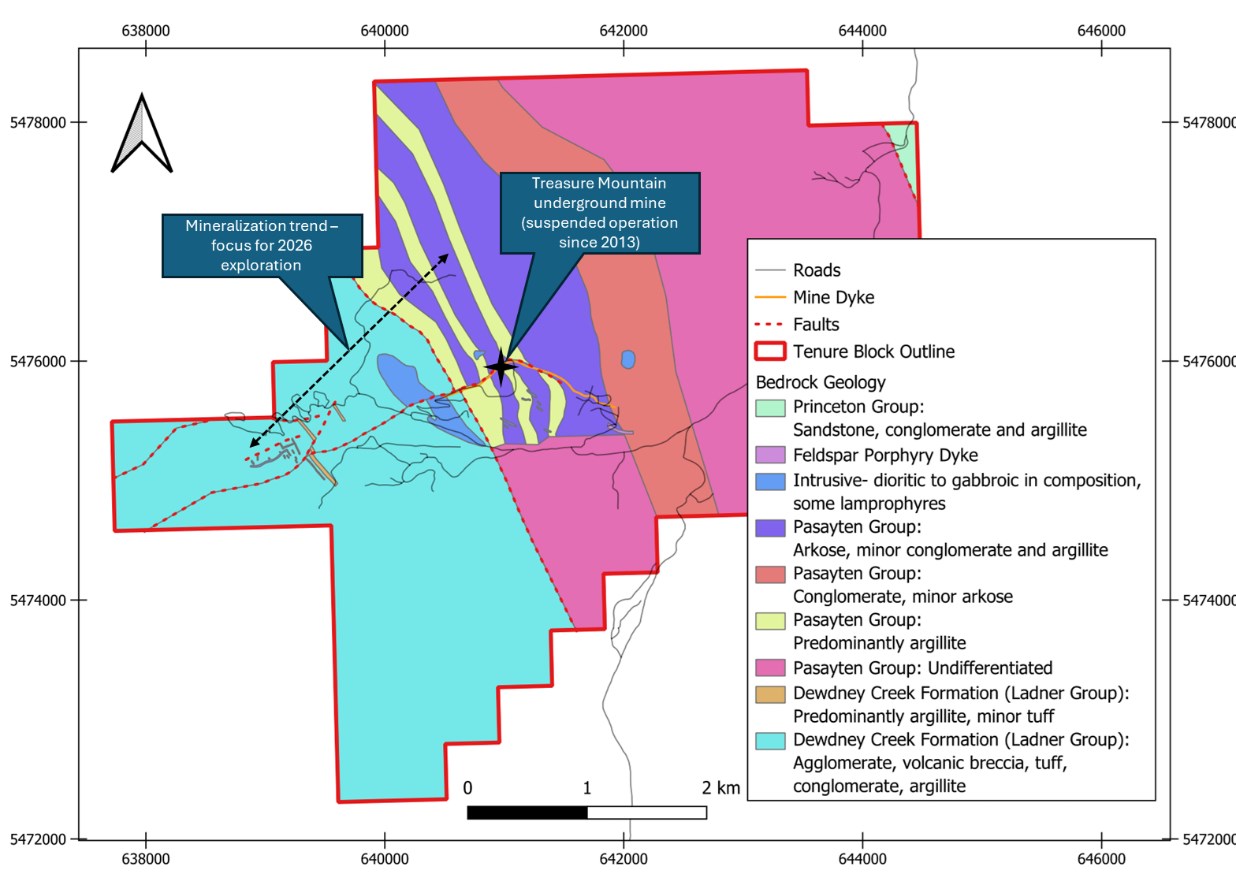

Treasure Mountain exploration. Nicola Mining Inc. (OTCQB: HUSIF, TSXV: NIM) provided an update on its plan for 2026 exploration drilling at the Treasure Mountain Silver Project. The area of exploration interest is northwest of the currently suspended mine and consists of several northeast to southwest trending and steeply dipping sulphide-rich veins. Results from previous exploration work confirmed the presence of vein-hosted silver, copper, lead, zinc, and gold, providing support for initial diamond drilling to establish the width of the trend and mineralization at depth.

Recent gold sales. Talisker Resources (OTCQB: TSKFF, TSX: TSK) has an agreement to process run-of-mine material from its Mustang Mine at Nicola’s Merritt Mill. For the quarter ending on September 30, a total of 1,569 ounces of gold were produced from Talisker’s Mustang Mine. Nicola receives a share of the gross profit from milling ore sourced from Talisker Resources Ltd. Blue Lagoon Resources Inc. (OTCQB: BLAGF, CSE: BLLG) recently announced an amended mining and milling partnership agreement with Nicola Mining, extending the partnership to a 10-year term. The agreement secures a long-term processing solution for mineralized material from Blue Lagoon’s high-grade Dome Mountain Gold Project.

Noble Capital Markets Research Report Tuesday, October 14, 2025

Companies contained in today’s report:

Alliance Entertainment Holding (AENT)/OUTPERFORM – Noble Virtual Conference Highlights EuroDry (EDRY)/MARKET PERFORM – Recovering Rates and Greater Liquidity Enhance Outlook NeuroSense Therapeutics Ltd. (NRSN)/OUTPERFORM – Novel Therapy for ALS and Neurodegenerative Diseases ONE Group Hospitality (STKS)/OUTPERFORM – Randian Adds Some Detail Saga Communications (SGA)/OUTPERFORM – Highlights From Noble’s Virtual Emerging Growth Conference Sky Harbour Group (SKYH)/OUTPERFORM – Noble Virtual Conference Highlights SKYX Platforms (SKYX)/OUTPERFORM – Noble Virtual Conference Highlights Snail (SNAL)/OUTPERFORM – Highlights From Noble’s Virtual Conference Superior Group of Companies (SGC)/OUTPERFORM – Highlights from Noble’s Virtual Conference Townsquare Media (TSQ)/OUTPERFORM – Highlights From Noble’s Virtual Conference Vince Holding Corp. (VNCE)/OUTPERFORM – Highlights From Noble’s Virtual Conference

Alliance Entertainment Holding (AENT/$6.42 | Price Target: $11) Michael Kupinski mkupinski@noblefcm.com | (561) 994-5734 Jacob Mutchler jmutchler@noblefcm.com | Noble Virtual Conference Highlights Rating: OUTPERFORM

Management appeared confident. Bruce Ogilvie, Executive Chairman, and Jeffrey Walker, CEO, presented at Noble’s October 8th & 9th Virtual Emerging Growth Conference. This report highlights the company’s presentation and fireside Q&A chat, which provided a sanguine outlook for improved margins into fiscal 2026. Investors may listen to the company’s presentation here.

Favorable margin expansion outlook. Operating margins are expected to expand in fiscal 2026, supported by a full year of the company’s high margin licensing deal with Paramount and development of its Handmade by Robots collectible line. In addition, management anticipates further operating efficiencies.

EuroDry (EDRY/$12.58) Mark Reichman mreichman@noblefcm.com | (561) 999-2272 Hans Baldau hbaldau@noblefcm.com | Recovering Rates and Greater Liquidity Enhance Outlook Rating: MARKET PERFORM

Vessel sale enhances liquidity. EuroDry recently announced an agreement to sell the M/V Eirini P. to a third party for approximately $8.5 million, with the transaction expected to close in October 2025. The sale is projected to generate a gain of approximately $0.6 million, or roughly $0.21 per share. The proceeds will enhance near-term liquidity and strengthen EuroDry’s flexibility to pursue selective investments in more efficient vessels.

Market environment improving. The dry-bulk market has shown signs of recovery as charter rates have recently rebounded from multi-year lows. The improvement reflects strengthening market sentiment, supported by limited fleet growth and rising expectations for Chinese demand. A historically low orderbook and modest fleet expansion provide a constructive foundation for rate stabilization heading into 2026.

NeuroSense Therapeutics Ltd. (NRSN/$1.22 | Price Target: $9) Robert LeBoyer rleboyer@noblefcm.com | (212) 896-4625 Novel Therapy for ALS and Neurodegenerative Diseases Rating: OUTPERFORM

We Are Initiating Coverage of NeuroSense With An Outperform Rating. NeuroSense Therapeutics is developing therapies for degenerative neurological conditions. The lead product, PrimeC, has completed two Phase 2 trials for ALS (Amyotrophic Lateral Sclerosis) and has a Phase 3 trial planned for early 2026. Initial results from Phase 2 in Alzheimer’s disease has shown promising data. Our price target is $9 per share.

The Lead Indication For PrimeC Is in ALS. PrimeC is a novel formulation containing a combination of celecoxib and ciprofloxacin. These two drugs have been used separately for anti-inflammatory and anti-antimicrobial indications. After new data showed that each drug can affect pathways of degenerative disease, scientists at NeuroSense tested the two drugs together in models of ALS and found a synergistic effect. Two Phase 2 studies showed benefits on survival, disease progression, and biomarkers of ALS activity.

ONE Group Hospitality (STKS/$2.56 | Price Target: $5) Joe Gomes, CFA jgomes@noblefcm.com | 561-999-2262 Randian Adds Some Detail Rating: OUTPERFORM

Additional Detail. Randian Capital added another post on the social media platform X, providing additional details to its proposed turnaround plan for ONE Group Hospitality. Reportedly, the latest Randian X post was in response to STKS CEO Manny Hilario and CFO Nicole Thaung stating they had not engaged with Randian and were unaware if the firm held shares. The pair reiterated that ONE Group had no changes to guidance or plans for capital deployment being made.

The Driver. As we noted in our September 29th note, Randian believes there is tangible, underutilized value in this franchise—especially in Benihana, a legendary brand with global recognition and untapped potential. However, poor capital allocation, slipping operational execution, and marketing that is failing to drive engagement have resulted in a 60% decline in the share price since the 2024 Benihana acquisition, according to Randian.

Saga Communications (SGA/$12.6 | Price Target: $18) Michael Kupinski mkupinski@noblefcm.com | (561) 994-5734 Jacob Mutchler jmutchler@noblefcm.com | Highlights From Noble’s Virtual Emerging Growth Conference Rating: OUTPERFORM

A blended growth opportunity. This report highlights a fireside chat with Christopher Forgy, CEO & President, and Samuel Bush, CFO, at Noble’s Virtual Emerging Growth Conference on October 8th & 9th. Management highlighted its attractive growth opportunities from its “blended” advertising strategy. The full presentation may be viewed here.

Blended advertising strategy. Saga’s approach integrates radio (“wanted”), search (“found”), and display (“chosen”) to capture the full consumer journey. Management targets disrupting 5% of local digital ad spend to double annual gross revenue, focusing on 27 small-to-medium-sized markets where the company has trusted community relationships.

Sky Harbour Group (SKYH/$10.07 | Price Target: $23) Patrick McCann, CFA pmccann@noblefcm.com | (314) 724-6266 Michael Kupinski mkupinski@noblefcm.com | (561) 994-5734 Noble Virtual Conference Highlights Rating: OUTPERFORM

Noble virtual conference highlights. Tal Keinan (CEO) and Francisco Gonzalez (CFO) of Sky Harbour Group (NYSE: SKYH) presented at Noble’s Emerging Growth Virtual Conference on October 8–9, 2025. Management highlighted continued lease-up at Phoenix, Dallas, and Denver, steady pre-leasing at Dulles (IAD) and Bradley (BDL), and progress on capital efficiency. A rebroadcast can be found here.

Leasing and pipeline on pace. Operations at Phoenix, Dallas, and Denver are leasing at a good clip, and the company has secured one pre-lease tenant at both IAD and BDL ahead of construction. Sky Harbour now holds long-term ground leases at 18 airports (nine operating, nine in development) and reaffirmed plans to add five more by year-end, bringing the total to 23.

SKYX Platforms (SKYX/$1.26 | Price Target: $5) Patrick McCann, CFA pmccann@noblefcm.com | (314) 724-6266 Michael Kupinski mkupinski@noblefcm.com | (561) 994-5734 Noble Virtual Conference Highlights Rating: OUTPERFORM

Highlights from Noble’s Emerging Growth Virtual Conference. Lenny Sokolow, CEO of SKYX Platforms (NASDAQ: SKYX), presented at Noble’s Virtual Conference on October 8–9, 2025. He discussed growing developer adoption, the upcoming Smart Ceiling Heater / Fan launch, progress toward mandatory code standardization, and reaffirmed expectations for adj. EBITDA inflection in Q4. A rebroadcast can be found here.

Developer partnerships gaining momentum. SKYX continues to expand across the builder channel with projects from Landmark Companies (278-unit Austin apartments), Forte Developments (luxury towers in Miami, Clearwater Beach, and Jupiter), Cavco Homes (premium prefabricated models), and the $3 billion Miami Urban Smart City. These initiatives represent large-scale unit potential and underscore accelerating adoption among professional developers.

Snail (SNAL/$1.04 | Price Target: $3.5) Michael Kupinski mkupinski@noblefcm.com | (561) 994-5734 Jacob Mutchler jmutchler@noblefcm.com | Highlights From Noble’s Virtual Conference Rating: OUTPERFORM

Prospects for Stablecoin. This report highlights key takeaways from the company’s presentation at Noble’s Virtual Emerging Growth Conference on October 8th & 9th. Heidy Chow, CFO, and Peter Lin, FP&A outlined the key growth attributes for the company, including its emerging interest in developing a stablecoin. The full presentation may be found here.

Solid 2024 Performance and Franchise Resilience. Snail delivered a strong year, with FY2024 revenue reaching $85 million, supported by its enduring ARK franchise, which has accumulated over 90 million players and 4.1 billion total playtime hours since launch.

Superior Group of Companies (SGC/$10.07 | Price Target: $16) Michael Kupinski mkupinski@noblefcm.com | (561) 994-5734 Jacob Mutchler jmutchler@noblefcm.com | Highlights from Noble’s Virtual Conference Rating: OUTPERFORM

Plowing through the trade fog. Michael Benstock, Chairman and CEO, and Michael Koempel, President and CFO, presented at Noble’s October 8th & 9th Virtual Emerging Growth Conference. This report highlights the company’s fireside Q&A chat, which provided a constructive revenue and earnings growth outlook in spite of trade policy turmoil. Investors may listen to the company’s presentation here.

Diversified operations. The company operates in three segments, healthcare apparel, branded products, and contact centers. Diversification across these three segments provides both growth potential and resilience against macroeconomic uncertainty, including tariffs and political volatility.

Townsquare Media (TSQ/$6.09 | Price Target: $21) Michael Kupinski mkupinski@noblefcm.com | (561) 994-5734 Jacob Mutchler jmutchler@noblefcm.com | Highlights From Noble’s Virtual Conference Rating: OUTPERFORM

A differentiated digital company. Bill Wilson, CEO, Stuart, Rosenstein, CFO, and Claire Yenicay, Executive Vice President, participated in a fireside chat at Noble’s Virtual Emerging Growth Conference on October 8th & 9th. The discussion focused on the company’s differentiated digital growth opportunities and compelling total return potential. This report provides some of the highlights from the discussion, but the full discussion may be viewed here.

Townsquare Interactive turning towards growth. Townsquare Interactive provides subscription-based digital marketing solutions for SMBs at ~$300/month, offering website management, CRM, email/text marketing, and payment integration. After temporary disruption in 2023–2024 due to a service model overhaul and return-to-office mandate, 2025 is returning to strong profit growth (~$3 million), with revenue growth expected to resume in 2026.

Vince Holding Corp. (VNCE/$2.66 | Price Target: $4.5) Michael Kupinski mkupinski@noblefcm.com | (561) 994-5734 Jacob Mutchler jmutchler@noblefcm.com | Highlights From Noble’s Virtual Conference Rating: OUTPERFORM

Transformational progress. Brendan Hoffman, CEO, Yuji Okumura, CFO, and Akiko Okuma, Chief Administrative Officer, discussed the significant transformation of the company toward revenue and cash flow growth and profitability at Noble’s Virtual Emerging Growth Conference on October 8th & 9th. Highlights from the fireside chat are featured in this report, and the full discussion is available here.

Minimizing the China impact. The company significantly reduced sourcing concentration from roughly 60% of production in China to approximately 25% today, offsetting the impact of tariff rates as high as 158%. Management noted that long-standing manufacturing partners in China have established sister facilities in other Asian countries, helping preserve quality standards while lowering exposure risk.

Market Share. CoreCivic remains the largest non-government owner of correctional and detention real estate in the U.S., owning approximately 57% of all privately owned correctional and detention capacity. The Company manages approximately 41% of all privately managed correctional and detention capacity.

FAT Brands (FAT/$1.98 | Price Target: $15) Joe Gomes, CFA jgomes@noblefcm.com | 561-999-2262 Some Legal Resolution Rating: OUTPERFORM

Legal Resolution. In an 8-K filing, FAT Brands disclosed that the Company and certain current and former directors and officers have reached a settlement agreement with stockholders of the Company to resolve two lawsuits known as Harris I and Harris II. The Derivative Actions were filed in June 2021, relating to the Company’s December 2020 merger with Fog Cutter Capital Group, and in March 2022, relating to the Company’s June 2021 recapitalization.

Details. Under the terms of the settlement agreement, the Company’s Board of Directors agreed to adopt and implement certain corporate governance modifications. In addition, the Company’s insurers will pay to the Company $10 million, from which fees and expenses of plaintiffs’ counsel will be deducted, and Fog Cutter Holdings LLC will contribute 200,000 Class A shares of Twin Hospitality Group Inc. to the Company.

Phase 2. NN is entering Phase 2 of its transformation program. Phase 1 structurally rebuilt NN’s operating performance and efficiency through fixing unprofitable areas, improving margins, and entering new markets. Phase 2 is a growth and de-leverage focus, implementing new business programs, expanding the TAM, and addressing the preferred stock.

Resources Connection (RGP/$4.54 | Price Target: $10) Joe Gomes, CFA jgomes@noblefcm.com | 561-999-2262 Post Call Commentary Rating: OUTPERFORM

Some Positives. The Company continues on its transformation path and is seeing encouraging signs, in our opinion. For example, the Company saw a return to growth in revenue for both the Europe & Asia- Pac segment and the Outsourced Services segment, with 5% and 4% growth over the prior year quarter. Revenue from the top 10 clients also grew year-over-year, and the enterprise-wide average bill rate increased to $120 on a constant currency basis, up from $118 a year ago.

Ongoing Cost Focus. The other side of the transformation plan is a focus on cost control. RGP continues to make good progress on its SG&A, as reflected in the quarter’s numbers. Post quarter, on September 30, 2025, in the face of continued end market sluggishness, RGP commenced a global reduction in its management and administrative workforce intended to enhance efficiencies through reduced costs and streamlined operations. Management expects approximately $6 million to $8 million of annual cost savings associated with this effort.

Noble Capital Markets Research Report Friday, October 10, 2025

Companies contained in today’s report:

AZZ (AZZ)/OUTPERFORM – A Multi-Year Growth Story

AZZ (AZZ/$100.75 | Price Target: $120) Mark Reichman mreichman@noblefcm.com | (561) 999-2272 Hans Baldau hbaldau@noblefcm.com | A Multi-Year Growth Story Rating: OUTPERFORM

FY 2026 second-quarter results. AZZ reported adjusted net income of $46.9 million, or $1.55 per share, compared to $41.3 million, or $1.37 per share, during the prior year period. We projected adjusted net income of $46.7 million, or $1.54 per share. Compared to the second quarter of FY 2025, total sales increased 2.0% to $417.3 million. We had projected sales of $428.3 million. Gross margin of $101.3 million was modestly below our estimate of $104.7 million. Adjusted EBITDA declined modestly to $88.7 million compared to $91.9 million during the prior year period and our estimate of $93.4 million. Adjusted EBITDA margin as a percentage of sales declined to 21.3% compared to 22.5% during the prior year quarter.

Updating estimates. We have lowered our FY 2026 revenue, adjusted EBITDA, and adjusted EPS estimates to $1.642 billion, $369.2 million, and $5.98 per share, respectively, from $1.660 billion, $374.9 million, and $6.00 per share. Our revised forecasts reflect second-quarter results and more moderate sales growth in the second half of the year. Our longer-term estimates through FY 2031 reflect multi-year growth and are summarized at the end of this report. Our estimates could prove conservative if AZZ is successful in consummating acquisitions, which we do not reflect in our estimates until announced.

Noble Capital Markets Research Report Thursday, October 9, 2025

Companies contained in today’s report:

AZZ (AZZ)/OUTPERFORM – Staying Focused on the Big Picture Bit Digital (BTBT)/OUTPERFORM – Monthly Ethereum Metrics Resources Connection (RGP)/OUTPERFORM – First Look at 1Q26

AZZ (AZZ/$105.94 | Price Target: $125) Mark Reichman mreichman@noblefcm.com | (561) 999-2272 Staying Focused on the Big Picture Rating: OUTPERFORM

FY 2026 second-quarter financial results. AZZ reported adjusted net income of $46.9 million, or $1.55 per share, compared to $41.3 million, or $1.37 per share, during the prior year period. We had forecast adjusted net income of $46.7 million, or $1.54 per share. Compared to the second quarter of FY 2025, total sales increased 2.0% to $417.3 million. We had projected sales of $428.3 million. Gross margin of $101.3 million was modestly below our estimate of $104.7 million. Sales and gross margins trailed our expectations for both segments. However, operating income of $68.5 million exceeded our estimate of $66.1 million due to lower selling, general, and administrative expenses. Adjusted EBITDA declined modestly to $88.7 million compared to $91.9 million during the prior year period and our estimate of $93.4 million. Adjusted EBITDA margin as a percentage of sales declined to 21.3% compared to 22.5% during the second quarter of FY 2025.

Results were mixed. While Metal Coatings sales were up 10.8% compared to the prior year quarter, Precoat Metals sales were down 4.3%. Metal Coatings delivered higher sales due to increased volume driven by infrastructure-related projects in several end markets. Precoat Metals experienced lower sales due to weaker end markets, including building construction, HVAC, and appliance.

Bit Digital (BTBT/$4.04 | Price Target: $5.5) Joe Gomes, CFA jgomes@noblefcm.com | 561-999-2262 Monthly Ethereum Metrics Rating: OUTPERFORM

Data. Bit Digital reported its monthly Ethereum (“ETH”) treasury and staking metrics for the month of September 2025. As of September 30, 2025, the Company held approximately 121,187 ETH, versus 121,252 ETH at the end of August. Included in the ETH holdings were approximately 15,075 ETH and ETH-equivalents held in an externally managed fund, and approximately 5,142 ETH presented on an as-converted basis from LsETH using the Coinbase conversion rate as of 9/30/25. The Company’s total staked ETH was approximately 99,936 as of September 30th.

Yield and Value. Staking operations generated approximately 291 ETH in rewards during September, representing an annualized yield of approximately 3.37%. Based on a closing ETH price of $4,145.99, as of September 30, 2025, the market value of the Company’s ETH holdings was approximately $506.6 million.

Resources Connection (RGP/$4.95 | Price Target: $15) Joe Gomes, CFA jgomes@noblefcm.com | 561-999-2262 First Look at 1Q26 Rating: OUTPERFORM

A Beat. Resources Connection reported first quarter revenue, gross margin, and SG&A expenses better than expected, although the top line continued to decline y-o-y, as expected. RGP is engaging with clients on more consulting opportunities, which have higher bill rates, larger deal size, and often create more extension and cross selling. However, the macro environment remains unpredictable, which makes clients hesitant to begin new projects.

Details. 1Q26 revenue came in at $120.2 million, down from $136.9 million in 1Q25, but above the $120 million high-end of management’s guidance. Gross margin came in at 39.5%, a significant y-o-y improvement from 36.5% in 1Q25 and above the 36-37% guidance range. SG&A expense of $47.9 million improved from $48.9 million in 1Q25. RGP recorded a GAAP net loss of $2.4 million, or $0.07/sh, compared to a $5.7 million, or $0.17/sh, net loss, in 1Q25. Adjusted EPS was $0.03/sh versus breakeven last year.

Noble Capital Markets Research Report Monday, October 6, 2025

Companies contained in today’s report:

Alliance Entertainment Holding (AENT)/OUTPERFORM – Delivering Music To Our Ears: Cash Flow And Earnings Growth SKYX Platforms (SKYX)/OUTPERFORM – Strengthening Position Among Residential Developers Xcel Brands (XELB)/OUTPERFORM – Exiting A Successful Run

Alliance Entertainment Holding (AENT/$6.73 | Price Target: $11) Michael Kupinski mkupinski@noblefcm.com | (561) 994-5734 Patrick McCann, CFA pmccann@noblefcm.com | (314) 724-6266 Delivering Music To Our Ears: Cash Flow And Earnings Growth Rating: OUTPERFORM

Initiating coverage with Outperform rating. Alliance Entertainment is a leading distributor of physical products, including vinyl records, music CDs, Blu-ray and 4K Movies, Video Games and Electronics, and Collectibles. While some of its business lines are mature, there are attractive growth opportunities in developing revenue streams that carry higher margins. As such, we believe that the company is on the cusp of generating significant cash flow and earnings growth.

Expanding margin outlook. In spite of anticipated modest revenue growth of 2.4% in fiscal 2026, we anticipate a nearly 140 basis point improvement in adj. EBITDA margins in fiscal 2026, given our expectation of higher margin, developing revenue streams and the company’s focus on efficiencies. We expect an acceleration in revenue in fiscal 2027 to 3.1% with another 60 basis point improvement in margins.

SKYX Platforms (SKYX/$1.13 | Price Target: $5) Patrick McCann, CFA pmccann@noblefcm.com | (314) 724-6266 Michael Kupinski mkupinski@noblefcm.com | (561) 994-5734 Strengthening Position Among Residential Developers Rating: OUTPERFORM

Landmark partnership expands builder channel. SKYX announced it will supply more than 10,000 smart plug-and-play lighting and safety products to a 278-apartment project in Austin, Texas led by Landmark Companies. We believe this marks another important step in the company’s efforts to penetrate the builder channel, signaling traction with traditional residential developers.

Potential for broader builder relationships. By establishing a relationship with a large developer like Landmark, SKYX positions itself for additional project opportunities if early deployments prove successful. This deal highlights the potential for SKYX to extend its platform into the broader residential developer market, with initial supply expected to begin as early as within the next quarter or two.

Xcel Brands (XELB/$2.38 | Price Target: $7) Michael Kupinski mkupinski@noblefcm.com | (561) 994-5734 Jacob Mutchler jmutchler@noblefcm.com | Exiting A Successful Run Rating: OUTPERFORM

Exits its Mizrahi interest. The company transferred its remaining 17.5% interest in Isaac Mizrahi to IM Topco, effectively exiting its interest in the brand. The exit of the Mizrahi relationship with Xcel caps a storied and successful run with the company since 2011. Under Xcel, Mizrahi expanded its categories and collections on QVC and into such retailers as Bloomingdale’s and Nordstrom.

Financial upside. Xcel has a participation right should IM Topco sell the company above $46.0 million, coincidentally, the price that Xcel sold its 60% interest. Xcel would receive 15% of the net consideration in excess of the $46 million. In addition, we believe that the company will benefit from the absent of costs related to the brand, particularly employee costs.

Noble Capital Markets Research Report Friday, October 3, 2025

Companies contained in today’s report:

Bitcoin Depot (BTM)/OUTPERFORM – Favorable Preliminary Results and Tuck-in Acquisition

Bitcoin Depot (BTM/$3.83 | Price Target: $9) Patrick McCann, CFA pmccann@noblefcm.com | (314) 724-6266 Michael Kupinski mkupinski@noblefcm.com | (561) 994-5734 Favorable Preliminary Results and Tuck-in Acquisition Rating: OUTPERFORM

Strong preliminary results. Bitcoin Depot announced preliminary Q3 results of approximately $160M in revenue (+18% Y/Y) and roughly 50% growth in adj. EBITDA versus the prior year. Both topline and profitability are tracking well ahead of management’s prior Q2 guidance of high-single-digit revenue and 20–30% adj. EBITDA growth.

Beating expectations. In light of these results, the company is expected to exceed our Q3 forecast of $146.5M in revenue and $11.0M in adj. EBITDA. Preliminary figures imply approximately $13.8M in adj. EBITDA, meaning profitability should surpass our expectations by nearly 25%.

Noble Capital Markets Research Report Thursday, October 2, 2025

Companies contained in today’s report:

Century Lithium Corp. (CYDVF)/OUTPERFORM – Progress on the Permitting Front CoreCivic, Inc. (CXW)/OUTPERFORM – An Award for Diamondback Seanergy Maritime (SHIP)/OUTPERFORM – Strategic Vessel Sale and Improving Capesize Fundamentals V2X (VVX)/OUTPERFORM – Some More Awards

Century Lithium Corp. (CYDVF/$0.29 | Price Target: $2.35) Mark Reichman mreichman@noblefcm.com | (561) 999-2272 Hans Baldau hbaldau@noblefcm.com | Progress on the Permitting Front Rating: OUTPERFORM

Moving through the permitting process. Century has completed all required environmental baseline studies to begin Angel Island’s National Environmental Policy Act (NEPA) permitting process, which is expected to take up to two years before reaching a record of decision. The studies will be used by the Bureau of Land Management (BLM) to support the company’s upcoming Plan of Operations submission and subsequent NEPA analysis.

FAST-41 designation. In August 2025, Angel Island was formally designated as a FAST-41 Transparency project under a federal initiative designed to improve the transparency, coordination, and timeliness of the federal environmental review and permitting process. The designation reflects Angel Island’s strategic importance in supporting the U.S. critical minerals supply chain. We think the Angel Island project is well-positioned for a timely progression through the permitting process.

CoreCivic, Inc. (CXW/$20.55 | Price Target: $28) Joe Gomes, CFA jgomes@noblefcm.com | 561-999-2262 An Award for Diamondback Rating: OUTPERFORM

Diamondback. Yesterday, CoreCivic announced it was awarded a new contract under an Intergovernmental Services Agreement between the Oklahoma Department of Corrections and U.S. Immigration and Customs Enforcement (“ICE”) to resume operations at the Company’s 2,160-bed Diamondback Correctional Facility, a facility that has been idle since 2010.

Details. The new contract commenced on September 30, 2025, for a term of five years and may be extended through bilateral modification. The agreement provides for a fixed monthly payment plus an incremental per diem payment based on detainee populations. Total annual revenue once the facility is fully activated is expected to be approximately $100 million. The facility should begin receiving detainees in the first quarter of 2026, with the full ramp estimated to be complete in the second quarter of 2026.

Seanergy Maritime (SHIP/$8.58 | Price Target: $11) Mark Reichman mreichman@noblefcm.com | (561) 999-2272 Hans Baldau hbaldau@noblefcm.com | Strategic Vessel Sale and Improving Capesize Fundamentals Rating: OUTPERFORM

Sale of M/V Geniuship. Seanergy announced the sale of the M/V Geniuship, a 170,057 dwt Capesize vessel, for approximately $21.6 million, generating net cash proceeds of $12.0 million and a profit of about $2.5 million. The sale was timed to take advantage of improved vessel valuations while avoiding the costs of the vessel’s scheduled dry-docking. The transaction enhances liquidity, improves near-term earnings, and aligns with the company’s ongoing fleet renewal strategy.

Capesize market gains momentum. The Capesize market has strengthened in recent months, supported by iron ore and bauxite projects in the Atlantic basin and West Africa, while volatility due to tariffs has moderated. The orderbook remains limited, with shipyard slots not available until 2029. Rising vessel values, together with higher construction costs, have further restricted orders. Overall, we expect market conditions to remain favorable, with 2026 showing improvement over 2025.

V2X (VVX/$58.08 | Price Target: $72) Joe Gomes, CFA jgomes@noblefcm.com | 561-999-2262 Some More Awards Rating: OUTPERFORM

Awards. V2X has been the recipient of new awards, including one focused on extending the life-cycle of existing platforms and another driving connectivity and communications. In total, the three new awards total over $580 million of contract value, assuming all funds are spent. We view the recent wins as further confirmation of V2X’s ability to provide full mission lifecycle solutions.

Center Display Units. V2X’s Vertex Modernization and Sustainment unit was awarded by the Air Force a five-year ID/IQ contract with a single five-year option (10 years total) with a contract ceiling of $425 million for center display units (CDU), according to the Department of War’s daily contract awards. V2X will supply the Air Force with the following hardware during this period: CDU full kits, CDU line replaceable units, CDU shop replaceable units, and various other support hardware as required.

Noble Capital Markets Research Report Wednesday, October 1, 2025

Companies contained in today’s report:

Bit Digital (BTBT)/OUTPERFORM – A Convertible Note Offering The GEO Group (GEO)/OUTPERFORM – Retains ISAP Contract

Bit Digital (BTBT/$3 | Price Target: $5.5) Joe Gomes, CFA jgomes@noblefcm.com | 561-999-2262 A Convertible Note Offering Rating: OUTPERFORM

An Offering. Bit Digital is offering $135 million of convertible notes. The deal is upsized from an original $100 million. Net proceeds from the offering will be used primarily to purchase Ethereum, and may be used for general corporate purposes, including potential investments, acquisitions, and other business opportunities. The capital raise continues management’s goal of becoming a major Ethereum treasury company, in our view.

Details. The Notes will be senior, unsecured obligations of the Company and will accrue interest at a rate of 4.00% per year, payable semiannually in arrears. The Notes will mature on October 1, 2030. The initial conversion rate will be 240.3846 shares per $1,000 principal amount of Notes (equivalent to an initial conversion price of $4.16 per ordinary share and represents a conversion premium of 30% above the last reported sale price of the ordinary shares on September 29, 2025, which was $3.20).

The GEO Group (GEO/$20.49 | Price Target: $35) Joe Gomes, CFA jgomes@noblefcm.com | 561-999-2262 Retains ISAP Contract Rating: OUTPERFORM

ISAP Award. As we had expected, The GEO Group has retained the Intensive Supervision Appearance Program (“ISAP”) contract. U.S. Immigration and Customs Enforcement (“ICE”) awarded the contract to GEO’s BI subsidiary for the continued provision of electronic monitoring, case management, and supervision services. It is a two-year contract, which will have an initial term of one year, effective October 1, 2025, with an additional one-year option period.

Long-time Services Provider. BI has provided technology solutions, holistic case management, supervision, monitoring, and compliance services under the ISAP contract for over 21 years and has achieved high levels of compliance using a wide range of technologies and case management services over that time.

Noble Capital Markets Research Report Tuesday, September 30, 2025

Companies contained in today’s report:

Alliance Resource Partners (ARLP)/OUTPERFORM – U.S. Coal as a Strategic and Competitive Advantage CoreCivic, Inc. (CXW)/OUTPERFORM – Letter Contracts to Contract Awards ONE Group Hospitality (STKS)/OUTPERFORM – Activist Investor Sees $10+ Stock in 12-18 Months

Alliance Resource Partners (ARLP/$25.02 | Price Target: $32) Mark Reichman mreichman@noblefcm.com | (561) 999-2272 Hans Baldau hbaldau@noblefcm.com | U.S. Coal as a Strategic and Competitive Advantage Rating: OUTPERFORM

Investments to reinvigorate the U.S. coal industry. The U.S. Department of Energy announced a $625 million program to expand and reinvigorate the U.S. coal industry. This includes $350 million to recommission or modernize coal power units, $175 million for coal power projects directly benefiting rural communities, $50 million to support advanced wastewater management systems to enable coal plants to extend their service life and reduce operational costs, $25 million for dual-firing retrofits, and $25 million for development and testing of natural gas cofiring systems.

Expanded coal leasing on federal lands. Moreover, the U.S. Department of the Interior announced it is making up to 13.1 million acres of federal land available for coal leasing and streamlining approvals for projects. The Department is accelerating efforts to fast-track projects that can recover strategic minerals from mine waste and abandoned sites. The One Big Beautiful Bill, passed on July 4, established lower coal leasing royalty rates of not more than 7% for both surface and underground mines for the period July 4, 2025, to September 30, 2034.

CoreCivic, Inc. (CXW/$21.54 | Price Target: $28) Joe Gomes, CFA jgomes@noblefcm.com | 561-999-2262 Letter Contracts to Contract Awards Rating: OUTPERFORM

Contract Awards. As anticipated, U.S. Immigration and Customs Enforcement (ICE) awarded CoreCivic two new contracts, which, once fully activated, would generate total annual revenue of approximately $200 million. The two facilities, California City and Midwest Regional, had been operating under Letter Contracts with ICE, which enable CoreCivic to begin operations at a facility while negotiating a longer-term contract. Both facilities were idle at the beginning of the year.

California City. CoreCivic has been preparing to accept detainees at the 2,560-bed California City facility since April 1, 2025. The Company began receiving detainees at the facility on August 27, 2025. Management currently expects the activation to be complete in 1Q26, achieving a normalized run-rate in 2Q26. Total annual revenue, once the activation is complete, is expected to be approximately $130 million. The new contract expires in August 2027.

ONE Group Hospitality (STKS/$3.12 | Price Target: $5) Joe Gomes, CFA jgomes@noblefcm.com | 561-999-2262 Activist Investor Sees $10+ Stock in 12-18 Months Rating: OUTPERFORM

Activist Investor. Randian Capital, part of the “retail activist” group behind the sharp rise in Opendoor Technologies (OPEN) stock from less than a $1 mid-summer to around $8.20 today, released on social media platform X a turnaround proposal for The ONE Group. In a nutshell, the plan consists of Refocus the Portfolio, Revitalize the Brand, Strengthen Operations, and Capital Discipline & Growth. Radian sees a path to a $10+ stock over the next 12-18 months. STKS shares rose over 26% yesterday on the news.

Refocus & Revitalize. Randian calls for ONE Group to refocus solely on its Benihana concept, selling off all other concepts. The activist investor believes the STK concept alone could be worth more than the current market cap. Randian suggests rebranding as Benihana Group and changing the stock symbol. Revitalization by elevating the dining experience and engaging with cultural icons, among other changes.

Noble Capital Markets Research Report Friday, September 26, 2025

Companies contained in today’s report:

Aurania Resources (AUIAF)/OUTPERFORM – Heightened Risk in Ecuador AZZ (AZZ)/OUTPERFORM – Revising Estimates; Growth Outlook Remains Favorable Steelcase (SCS)/MARKET PERFORM – A Better Than Expected 2Q26

Aurania Resources (AUIAF/$0.1 | Price Target: $0.35) Mark Reichman mreichman@noblefcm.com | (561) 999-2272 Heightened Risk in Ecuador Rating: OUTPERFORM

Second quarter financial results. As an exploration company, Aurania does not generate revenue and has expenses to advance its projects. During the second quarter of 2025, the company generated a net loss of C$1,610,843 or C$0.01 per share. We had projected a loss of C$1,432,419 or C$0.01 per share. The variance to our estimate was mostly due to higher exploration expenditures, along with higher stock-based compensation. We project a full-year 2025 net loss of C$11.1 million, or C$(0.10) per share, compared to our prior loss estimate of C$10.5 million, or C$(0.09) per share.

Mining service fee. Ecuador recently implemented a new mining service fee on the resource sector (refer to our note dated July 29, 2025). The Ecuadorian Control and Regulation Agency (ARCOM) requested payment from Aurania of US$2,012,618 by July 31, 2025, representing one month of the total annual fee of US$24,151,420. While the penalty for non-payment is unclear, we think Aurania is withholding payment until it becomes clear whether TASA will stand in its current form due to multiple constitutional challenges.

AZZ (AZZ/$110.64 | Price Target: $125) Mark Reichman mreichman@noblefcm.com | (561) 999-2272 Hans Baldau hbaldau@noblefcm.com | Revising Estimates; Growth Outlook Remains Favorable Rating: OUTPERFORM

Updating estimates. We are lowering our second-quarter revenue, adjusted EBITDA, and adjusted EPS estimates to $428.3 million, $93.4 million, and $1.54, respectively, from $433.5 million, $101.1 million, and $1.59. While we have increased our revenue estimate for the Metal Coatings segment, we lowered expectations for Precoat Metals due to anticipated weakness in building construction. Our FY 2026 revenue, adjusted EBITDA, and adjusted EPS estimates are $1.660 billion, $374.9 million, and $6.00, respectively, compared to our prior estimates of $1.680 billion, $388.3 million, and $6.00. Our revised estimates reflect lower interest expense, along with modestly lower depreciation and amortization expense.

Organic and acquired growth. AZZ’s three-year goals include generating sales of two billion dollars or more in fiscal year 2028, compared to its trailing twelve-month sales of $1.6 billion. Organic growth is expected to exceed GDP growth, and AZZ is targeting acquisitions that strengthen both of its business segments. While we do not forecast sales of $2.0 billion until 2031, our model does not reflect acquisitions until they are announced.

Steelcase (SCS/$16.7) Joe Gomes, CFA jgomes@noblefcm.com | 561-999-2262 A Better Than Expected 2Q26 Rating: MARKET PERFORM

2Q26. In what is likely the Company’s final quarterly report as a public company, Steelcase reported better than expected results. Results benefitted from continued strengthening of demand from large corporate customers and International growth driven by India, China, and the United Kingdom. Improved International volume drove a $5 million reduction in y-o-y adjusted operating loss in the International segment. These were Steelcase’s highest quarterly results over the past five years.

Financials. Revenue of $897.1 million rose 4.8% y-o-y and exceeded the $890 million high end of management’s guidance. We were at $875 million. Gross margin of 34.4% was flat y-o-y and exceeded the 33.5% high end of guidance. Adjusted EBITDA totaled $99.6 million, or 11.1% of revenue, up from $89.5 million and 10.5% in 2Q25. Adjusted EPS was $0.45, versus $0.39 last year and above management’s $0.40 high end guide. We were at $0.36.

Noble Capital Markets Research Report Wednesday, September 24, 2025

Companies contained in today’s report:

SelectQuote (SLQT)/OUTPERFORM – Reaches Milestone in Helping Medicare-Eligible Seniors

SelectQuote (SLQT/$2.08 | Price Target: $7) Patrick McCann, CFA pmccann@noblefcm.com | (314) 724-6266 Michael Kupinski mkupinski@noblefcm.com | (561) 994-5734 Reaches Milestone in Helping Medicare-Eligible Seniors Rating: OUTPERFORM

Milestone in Findhelp partnership. SelectQuote announced that it has referred more than 200,000 low-income seniors to Findhelp, with nearly 50,000 of those individuals accessing free or reduced-cost services. The milestone demonstrates SelectQuote’s role in addressing the needs of Medicare-eligible consumers.

Partnership connects consumers to critical support. Findhelp is a closed-loop referral management software platform that connects individuals with community resources such as food, housing, transportation, and financial aid. SelectQuote has partnered with Findhelp for several years, directing seniors to assistance programs. The initiative does not generate revenue, but it extends SelectQuote’s Medicare distribution model by providing tangible value to consumers.

Noble Capital Markets Research Report Tuesday, September 23, 2025

Companies contained in today’s report:

The ODP Corporation (ODP)/MARKET PERFORM – To Be Acquired for $28/sh

The ODP Corporation (ODP/$27.68) Joe Gomes, CFA jgomes@noblefcm.com | 561-999-2262 To Be Acquired for $28/sh Rating: MARKET PERFORM

An Acquisition. Yesterday morning, The ODP Corporation announced it entered into a definitive agreement to be acquired by an affiliate of Atlas Holdings for $28/sh. The purchase price represents a premium of 34% to Friday’s closing price. ODP’s Board is supporting the transaction, which is expected to close by the end of 2025.

Who Is Atlas Holdings? Founded in 2002 by Andrew Bursky and Tim Fazio, Greenwich, CT-based Atlas Holdings owns and operates a global family of manufacturing and distribution businesses that together generate more than $20 billion in annual revenue. Atlas has experience in the office supplies sector through its LSC Communications unit, a leader in organizational solutions through brands such as Pendaflex.

Noble Capital Markets Research Report Monday, September 22, 2025

Companies contained in today’s report:

Information Services Group (III)/OUTPERFORM – Raising Price Target

Information Services Group (III/$5.38 | Price Target: $6.5) Joe Gomes, CFA jgomes@noblefcm.com | 561-999-2262 Raising Price Target Rating: OUTPERFORM

Raising Price Target. We are raising our price target on III shares to $6.50 from a prior $5, as III shares have exceeded our price target. The recent and expected future interest rate cuts, ongoing cost optimization efforts from clients, and the increasing pace of AI adoption will continue to drive ISG’s operating performance, in our view.

Valuation. At our $6.50 price target, III shares would trade at 1.4x our 2026 revenue estimate on an EV/sales basis, 10.7x on an EV/projected 2026 adjusted EBITDA basis, and 19.1x adjusted 2026 earnings. This compares to a peer group that trades at 1.3x, 10x, and 15.8x, respectively, consensus 2026 estimates.

Noble Capital Markets Research Report Friday, September 19, 2025

Companies contained in today’s report:

Ocugen (OCGN)/OUTPERFORM – OCU400 Licensing Agreement For Korea Completed

Ocugen (OCGN/$1.4 | Price Target: $8) Robert LeBoyer rleboyer@noblefcm.com | (212) 896-4625 OCU400 Licensing Agreement For Korea Completed Rating: OUTPERFORM

OCU400 Licensing Completed. Ocugen has announced the completion of a licensing agreement for Korea with Kwangdong Pharmaceutical, Co., Ltd., a diversified pharmaceutical company in the Republic of South Korea. This finalizes the term sheet announced in August with the 2Q25 business update. We have based our revenue expectations on US and Europe, with the Korea agreement adding additional cash upon the signing and downstream royalties.

Agreement Provides Cash, Milestones, and Royalties. The terms provide Ocugen with signing and near-term milestones of $7.5 million. Under the agreement, Ocugen will manufacture and supply OCU400 in exchange for a royalty of 25% of Net Sales plus sales milestones of $1 million for every $15 million in Net Sales, or roughly 32% per $15 million in sales. There are an estimated 7,000 retinitis pigmentosa (RP) patients in Korea, with an estimated market of about $180 million over the first 10 years of sales. We estimate these potential payments at about $65 million to Ocugen.

Noble Capital Markets Research Report Thursday, September 18, 2025

Companies contained in today’s report:

FreightCar America (RAIL)/OUTPERFORM – RAIL Adopts Stockholder Rights Plan Great Lakes Dredge & Dock (GLDD)/OUTPERFORM – A Month of Awards Nicola Mining Inc. (HUSIF)/OUTPERFORM – Updating Our Sum-of-the-Parts Valuation; Increasing PT to US$1.05 or C$1.45

FreightCar America (RAIL/$8.71 | Price Target: $17) Mark Reichman mreichman@noblefcm.com | (561) 999-2272 Hans Baldau hbaldau@noblefcm.com | RAIL Adopts Stockholder Rights Plan Rating: OUTPERFORM

Protecting the interests of all shareholders. Following a review of the company’s current ownership structure, FreightCar America announced that its Board of Directors adopted a limited-duration stockholder rights plan.The rights plan will expire on August 5, 2026, unless terminated earlier by the Board. The Rights Plan is intended to reduce the likelihood that any person or group gains control of the company through open-market accumulation or other tactics without paying an appropriate control premium. The plan also ensures the Board has sufficient time to make informed decisions that protect the interests of the company and all RAIL shareholders.

Increasing 2026 estimates. We have increased our 2026 EBITDA and EPS estimates to $53.6 million and $0.65, respectively, from $53.2 million and $0.64. Our estimate update reflects stronger deliveries in the second half of the year, with a full-year estimate of 4,850 compared with our previous estimate of 4,800. We now expect quarterly deliveries of: 1Q: 982, 2Q: 1,200, 3Q: 1,284, and 4Q: 1,384. Previously we had assumed: 1Q: 1,346, 2Q: 1,275, 3Q: 1,058, and 4Q: 1,121.

Great Lakes Dredge & Dock (GLDD/$11.97 | Price Target: $14) Joe Gomes, CFA jgomes@noblefcm.com | 561-999-2262 A Month of Awards Rating: OUTPERFORM

More Business. Over the past month, Great Lakes continued to be awarded additional business, according to the Department of War’s daily contract awards release. In total, the announced awards (and recall not all awards are included in the daily notice), totaled approximately $80 million, demonstrating Great Lakes’ operating capabilities as well as the ongoing demand from the government.

September. Most recently, Great Lakes was awarded a $27.9 million firm-fixed-price contract for the removal and disposal of hopper dredge material. Work will be performed in Venice, Louisiana, with an estimated completion date of April 7, 2026. Fiscal 2025 civil operation and maintenance funds in the amount of $27.9 million were obligated at the time of the award.

Nicola Mining Inc. (HUSIF/$0.78 | Price Target: $1.05) Mark Reichman mreichman@noblefcm.com | (561) 999-2272 Updating Our Sum-of-the-Parts Valuation; Increasing PT to US$1.05 or C$1.45 Rating: OUTPERFORM

New Craigmont mining lease extensions. Nicola Mining Inc. (OTCQB: HUSIF, TSX.V: NIM) secured a five-year extension for six mining leases at its New Craigmont Property from the Ministry of Mining and Critical Minerals. The New Craigmont property encompasses over 10,800 hectares and is adjacent to Teck Resources Limited’s (NYSE: TECK, TSX: TECK.A and TECK.B) Highland Valley Copper Mine, the largest copper mine in Canada. On June 1, Nicola commenced a 4,000-to-5,000-meter diamond drill program at the New Craigmont project. The mining lease extension ensures continuity through the project’s lifecycle.

Shipments of gold concentrate. Earlier this month, Nicola announced that it had commenced shipping gold concentrate via a partnership with Talisker Resources Ltd. (TSX: TSK, OTCQX: TSKFF). Under a Mining, Milling, and Smelting Agreement, the parties sold 707 ounces of gold in August, generating gross proceeds of approximately US$2.3 million. Production benefited from upgrades to the Merritt Mill, including the installation of a large concentrator that optimized free gold recovery.

Noble Capital Markets Research Report Wednesday, September 17, 2025

Companies contained in today’s report:

Commercial Vehicle Group (CVGI)/OUTPERFORM – Activist Shareholder Calls for Strategic Review The GEO Group (GEO)/OUTPERFORM – A Renewal and Two New Contracts V2X (VVX)/OUTPERFORM – Continuing to Lighten Vince Holding Corp. (VNCE)/OUTPERFORM – A Closer Look Supports Our Favorable Outlook

Commercial Vehicle Group (CVGI/$1.94 | Price Target: $4) Joe Gomes, CFA jgomes@noblefcm.com | 561-999-2262 Activist Shareholder Calls for Strategic Review Rating: OUTPERFORM

Call For A Review. In an amended Schedule 13D filing, investor Lakeview Opportunity Fund has communicated its views on the Company to the CVG management and Board on opportunities for value creation, including through a review process that explores strategic alternatives, including a sale of the Company.

Who Is Lakeview? With Managing Partner Ari Levy, Lakeview is a concentrated and opportunistic multi-strategy fund. The Fund focuses on underfollowed or ignored market areas, such as small and mid-cap value equities, niche Wall Street vehicles, options, and selective shareholder activism, where Lakeview helps companies, generally trading at significant discounts to private market value, unlock shareholder value.

The GEO Group (GEO/$22.04 | Price Target: $35) Joe Gomes, CFA jgomes@noblefcm.com | 561-999-2262 A Renewal and Two New Contracts Rating: OUTPERFORM

Contracts. The Florida Department of Corrections has issued Notices of Intent to Award three managed-only contracts to GEO for the assumption of management and support services at the 985-bed Bay Correctional and Rehabilitation Facility and the 1,884-bed Graceville Correctional and Rehabilitation Facility and for the continuation of management and support services at the 985-bed Moore Haven Correctional and Rehabilitation Facility.

Details. The three contracts are expected to have an initial term of three years, effective July 1, 2026, with unlimited two-year renewal option periods. On a combined basis, the three contracts are expected to generate approximately $130 million in annualized revenues, including approximately $100 million in new incremental annualized revenues for GEO. While the new contracts will not begin until next year, the new awards reflect GEO’s ability to provide the services demanded by its government partners, in our view.

V2X (VVX/$56.62 | Price Target: $72) Joe Gomes, CFA jgomes@noblefcm.com | 561-999-2262 Continuing to Lighten Rating: OUTPERFORM

Another Sale. Private-equity firm American Industrial Partners (AIP), through its Vertex Aerospace subsidiary, sold another 1.7 million VVX shares on September 11th. According to the amended 13D filing, the shares were sold at a price of $52.203 per share through a Rule 144 sale. As we have stated in the past, we continue to expect AIP to sell off its V2X holding over time.

Ownership. Following the most recent share sale, AIP’s ownership is now 8,467,286 VVX shares, representing 26.9% of the outstanding common of V2X. This is down from the 18,591,866 VVX shares, or 61.1% of the then outstanding common, held by AIP just after the Vectrus/Vertex merger in July 2022.

Vince Holding Corp. (VNCE/$2.63 | Price Target: $4.5) Michael Kupinski mkupinski@noblefcm.com | (561) 994-5734 Jacob Mutchler jmutchler@noblefcm.com | A Closer Look Supports Our Favorable Outlook Rating: OUTPERFORM

Solid Q2 Results. The company reported Q2 revenue of $73.2 million, modestly beating our estimate of $72.0 million, and adj. EBITDA of $6.7 million, which strongly outperformed our estimate of $0.85 million by 685%. The strong adj. EBITDA was largely driven by management’s ability to execute on its tariff mitigation strategies, resulting in an improved gross profit margin.

Mitigating tariff impacts. Importantly, the company’s gross profit margin increased 300 basis points over the prior year period. The improvement was driven by lower product costing and higher pricing, contributing a 340 basis point improvement, as well as less discounting, which resulted in a 210 basis point improvement. However, the positive margin contributions were softened by tariff and freight impacts of 170 basis points and 100 basis points, respectively.

Noble Capital Markets Research Report Tuesday, September 16, 2025

Companies contained in today’s report:

Cadrenal Therapeutics (CVKD)/OUTPERFORM – Acquisition Builds The Pipeline With Anticoagulants In Development

Cadrenal Therapeutics (CVKD/$13.37 | Price Target: $45) Robert LeBoyer rleboyer@noblefcm.com | (212) 896-4625 Acquisition Builds The Pipeline With Anticoagulants In Development Rating: OUTPERFORM

Cadrenal Acquires Complimentary Cardiovascular Products. Cadrenal announced that it has acquired the anti-coagulant assets of eXlthera Pharmaceuticals. The products include frunexian, a Pre-Phase-2 anti-coagulant drug that inhibits a different step in the coagulation cascade from tecarfarin. Frunexian is in development for different indications and could extend Cadrenal’s product line to additional indications that are not served by current drugs. The acquisition also includes an oral formulation and other research-stage molecules.

Frunexian Has Several Distinguishing Features. The lead product from eXlthera is frunexian, a Factor XIa inhibitor. Most of the DOAC (direct-acting oral anticoagulant) class target Factor Xa and have been developed for long-term use on an outpatient basis. In contrast, frunexian targets Factor XIa, a different component of the coagulation cascade.

Noble Capital Markets Research Report Monday, September 15, 2025

Companies contained in today’s report:

Euroseas (ESEA)/OUTPERFORM – Favorable Time Charter Contract for the M/V Jonathan P Greenwich LifeSciences, Inc. (GLSI)/OUTPERFORM – Fast Track Designation Gives Benefits Now And In The Future Metals & Mining (Metals & Mining) – Insights from the Precious Metals Summit

Euroseas (ESEA/$63.97 | Price Target: $71) Mark Reichman mreichman@noblefcm.com | (561) 999-2272 Hans Baldau hbaldau@noblefcm.com | Favorable Time Charter Contract for the M/V Jonathan P Rating: OUTPERFORM

New time charter contract. Euroseas Ltd. announced a new time charter for the M/V Jonathan P at a gross daily rate of $25,000 for a minimum of 11 months, with an option to extend to a maximum of 12 months at the charterer’s option. The charter will commence on November 17th.

Attractive rate and improved charter coverage. The new contract is in direct continuation of the current charter and represents a $5,000 per day increase. It is expected to contribute approximately $5.7 million in EBITDA over the minimum contract period and raise Euroseas’ charter coverage to 100% for the remainder of 2025 and 70% for 2026.

Greenwich LifeSciences, Inc. (GLSI/$11.23 | Price Target: $45) Robert LeBoyer rleboyer@noblefcm.com | (212) 896-4625 Fast Track Designation Gives Benefits Now And In The Future Rating: OUTPERFORM

GLSI-100 Received Fast Track Designation. Greenwich LifeSciences announced that GLSI-100 has received Fast Track designation from the FDA. In the near term, this designation allows GLSI increased communications and more FDA meetings regarding regulatory requirements for its clinical trial data and use of biomarkers. Once the FLAMINGO-01 trial is completed, GLSI will be eligible to apply for Accelerated Approval and Priority Review, potentially shortening the time to market.

The Designation Mirrors The Trial Entry Criteria. GLSI-100 has received Fast Track Designation from the FDA for the treatment of “patients with HLA-A*02 genotype and HER2-positive breast cancer who have completed treatment with standard of care HER2/neu targeted therapy to improve invasive breast cancer free survival…” This includes the clinical trial entry criteria and endpoints for the current double-blind arms of the trial.

Metals & Mining Mark Reichman mreichman@noblefcm.com | (561) 999-2272 Insights from the Precious Metals Summit

Precious Metals Summit. Noble Capital Markets was well represented at The Precious Metals Summit on September 9-12at the Beaver Creek Resort in Colorado. The conference attracted 1,700 registrants compared to approximately 1,200 in 2024 and included a broad spectrum of mining companies and institutional investors. Collectively, Noble had private meetings with over 70 company management teams during the invitation-only event.

Relative performance. Year-to-date through September 12,mining companies (as measured by the XME) appreciated 51.2% compared to a gain of 11.9% for the S&P 500 index. The VanEck Vectors Gold Miners (GDX) and Junior Gold Miners (GDXJ) ETFs were up 105.7% and 110.6%, respectively. Platinum, silver, and gold futures prices have gained 55.0%, 46.5%, and 39.6%, respectively, while copper, lead, and nickel increased 15.5%, 3.4% and 0.4%. Zinc declined 1.0%. Precious metals have led the charge as Central Banks around the world have added to global gold reserves, along with greater portfolio allocations among investors to precious metals as a hedge against rising inflation, a depreciating U.S. dollar, concerns about government debt, and increased geopolitical uncertainty. Moreover, there has been a desire among some nations to diversify away from the U.S. dollar as the benchmark reserve currency. Gold has become the global asset of choice to preserve value amid declining confidence in fiat currencies and an era of global monetary, geopolitical, and fiscal uncertainty.

Noble Capital Markets Research Report Friday, September 12, 2025

Companies contained in today’s report:

Nutriband (NTRB)/OUTPERFORM – Nutriband Reports 2Q26 With Product Progress SEGG Media Corporation (SEGG)/OUTPERFORM – Leveraging Strong Brands As A Foundation For Growth

Nutriband (NTRB/$6.93 | Price Target: $15) Robert LeBoyer rleboyer@noblefcm.com | (212) 896-4625 Nutriband Reports 2Q26 With Product Progress Rating: OUTPERFORM

AVERSA Fentanyl Is Moving Forward. Nutriband reported results from 2Q26, ended July 31, 2025, with a loss of $2.12 per share. Revenues for 2Q26 were $0.6 million compared with $0.4 million in 2Q25. The increase was attributed to the expansion of contract manufacturing services in the Pocono Pharma division that produces kinesiology tape. Net loss was $2.0 million before Preferred Dividends of $21.8 million, bringing Net Loss Available To Shareholders to $23.8 million. Cash at the end of the quarter was $6.9 million.

Meeting With The FDA Later In September. The company has scheduled a meeting with the FDA on September 18, 2025, to discuss the upcoming Phase 1 clinical trial for AVERSA Fentanyl. This is a Type C Meeting, requested by the company to discuss product development. The meeting agenda includes the CMC (Chemistry, Manufacturing, and Controls) and other aspects of the Investigational New Drug Application (IND) using the 505(b)(2) route of regulatory approval.

SEGG Media Corporation (SEGG/$5.63 | Price Target: $20) Michael Kupinski mkupinski@noblefcm.com | (561) 994-5734 Jacob Mutchler jmutchler@noblefcm.com | Leveraging Strong Brands As A Foundation For Growth Rating: OUTPERFORM

Initiation of coverage with Outperform rating and $20 price target. We are initiating coverage on SEGG Media (NASDAQ: SEGG) with an Outperform rating and $20 target. The company is a development-stage operator of international sports and gaming businesses, anchored by valuable brand assets including Sports.com, Lottery.com, TicketStub.com, and Concerts.com.

Developmental stage. Formed out of Lottery.com’s collapse, SEGG has been reconstituted under new leadership with a defined focus on leveraging globally recognized brands. Management is pursuing an asset-light model combining digital platforms, sports media rights, and consumer venues. We believe this strategy positions SEGG to re-establish credibility and execute a compelling growth plan.

Noble Capital Markets Research Report Thursday, September 11, 2025

Companies contained in today’s report:

Lucky Strike Entertainment (LUCK)/OUTPERFORM – Initiated Debt Refinancing Vince Holding Corp. (VNCE)/OUTPERFORM – Delivered A Strong Quarter

Lucky Strike Entertainment (LUCK/$9.6 | Price Target: $17.5) Michael Kupinski mkupinski@noblefcm.com | (561) 994-5734 Jacob Mutchler jmutchler@noblefcm.com | Initiated Debt Refinancing Rating: OUTPERFORM

Strategic update. On September 10, the company announced that its wholly-owned subsidiary Kingpin Intermediate Holdings LLC initiated a private offering of $700 million in new senior secured notes, due in 2032. Concurrently, the company launched a refinancing of its corporate term loan and revolving credit facility. The company expects the initial amount of the refinanced term loan and revolving credit facility to be $1 billion and $400 million, respectively.

Use of capital. Importantly, the net proceeds from the new debt offering and the refinanced credit facilities are earmarked for retiring the company’s existing term loan, revolving credit facility, and bridge loan, which was used to acquire 58 real estate assets in July. Furthermore, the remaining proceeds will be used to fund the company’s strategic initiatives.

Vince Holding Corp. (VNCE/$1.66 | Price Target: $4.5) Michael Kupinski mkupinski@noblefcm.com | (561) 994-5734 Jacob Mutchler jmutchler@noblefcm.com | Delivered A Strong Quarter Rating: OUTPERFORM

Solid Q2 Results. The company reported Q2 revenue of $73.2 million, modestly beating our estimate of $72.0 million, and adj. EBITDA of $6.7 million, which strongly outperformed our estimate of $0.85 million by 685%, as illustrated in Figure #1 Q2 Results. The strong adj. EBITDA was largely driven by management’s ability to execute on its tariff mitigation strategies, resulting in an improved gross profit margin.

Mitigating tariff impacts. Importantly, the company’s gross profit margin increased 300 basis points over the prior year period. The improvement was driven by lower product costing and higher pricing, contributing a 340 basis point improvement, as well as less discounting, which resulted in a 210 basis point improvement. However, the positive margin contributions were softened by tariff and freight impacts of 170 basis points and 100 basis points, respectively.

Noble Capital Markets Research Report Tuesday, September 9, 2025

Companies contained in today’s report:

Gyre Therapeutics, Inc (GYRE)/OUTPERFORM – Positioned To End YE2025 With Strong Products and Pipeline Development

Gyre Therapeutics, Inc (GYRE/$7.89 | Price Target: $20) Robert LeBoyer rleboyer@noblefcm.com | (212) 896-4625 Positioned To End YE2025 With Strong Products and Pipeline Development Rating: OUTPERFORM

Gyre Has Made Strong YTD Progress. Gyre has made significant progress during the first three quarters of FY2025 that we believe positions the company for a strong year-end. These developments include continued sales growth from two products introduced in 1H25, an application for Hydronidone approval in China, and the start of a Phase 2 clinical trial for Hydronidone in the US. The company also announced the appointment of Dr. Han Ying as the new CEO, a member of the Board of Directors since January 2025.

Hydronidone Data Showed Efficacy and Proof of Concept. The pivotal Phase 3 trial testing Hydronidone in Chronic Hepatitis B-associated fibrosis has met its primary endpoint of fibrosis regression. The study was conducted in China, and an application for approval by the NMPA (the Chinese regulatory authority) is planned for 3Q2025. Hydronidone has received Breakthrough Therapy Designation, allowing for accelerated review. We expect approval in 2H2026, followed by launch in FY2027.

Praxis Precision Medicines, Inc. (NASDAQ: PRAX) announced positive topline results from its Essential3 Phase 3 program evaluating ulixacaltamide HCl for the treatment of essential tremor (ET). The company reported that both pivotal studies met their pre-specified primary endpoints, with all key secondary endpoints also achieved, and ulixacaltamide was generally well tolerated with no drug-related serious adverse events.

In the parallel-group study (Study 1), patients treated with ulixacaltamide demonstrated a mean improvement of 4.3 points from baseline in the Modified Activities of Daily Living 11 (mADL11) at Week 8 (p<0.0001). All key secondary endpoints, including rate of disease improvement over 12 weeks, Patient Global Impression of Change (PGI-C), and Clinical Global Impression of Severity (CGI-S), were statistically significant (p<0.001).

In Study 2, a randomized-withdrawal design, patients maintained superior treatment effects on ulixacaltamide versus placebo (p=0.0369), with the first key secondary endpoint — rate of disease improvement — also demonstrating a statistically significant benefit (p=0.0042).

“Patients in the Essential3 program had been living with essential tremor for an average of 30 years, with worsening symptoms and no effective treatment options,” said Marcio Souza, President and CEO of Praxis Precision Medicines. “The strong results underscore the large unmet need for a therapy like ulixacaltamide. We look forward to discussing a potential NDA with the FDA in the near term.”

The Essential3 program enrolled over 700 patients across two studies using a decentralized design in the United States. Study 1 was a 12-week, double-blind, placebo-controlled trial evaluating change in mADL11 at Week 8. Study 2 enrolled stable responders to ulixacaltamide and assessed maintenance of effect during a four-week randomized-withdrawal phase.

Ulixacaltamide is a selective T-type calcium channel inhibitor designed to block abnormal neuronal burst firing in the Cerebello-Thalamo-Cortical circuit, which is associated with tremor activity. The therapy is the most advanced program in Praxis’ Cerebrum™ small molecule platform.

Essential tremor is the most common movement disorder in the U.S., affecting roughly 7 million people, and currently has limited treatment options. Propranolol is the only approved therapy, with limited efficacy and tolerability, leaving a substantial patient population untreated.