FAT Brands (NASDAQ: FAT) is a leading global franchising company that strategically acquires, markets, and develops fast casual, quick-service, casual dining, and polished casual dining concepts around the world. The Company currently owns 17 restaurant brands: Round Table Pizza, Fatburger, Marble Slab Creamery, Johnny Rockets, Fazoli’s, Twin Peaks, Great American Cookies, Hot Dog on a Stick, Buffalo’s Cafe & Express, Hurricane Grill & Wings, Pretzelmaker, Elevation Burger, Native Grill & Wings, Yalla Mediterranean and Ponderosa and Bonanza Steakhouses, and franchises and owns over 2,300 units worldwide. For more information on FAT Brands, please visit www.fatbrands.com.

Joe Gomes, Managing Director, Equity Research Analyst, Generalist , Noble Capital Markets, Inc.

Joshua Zoepfel, Research Associate, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

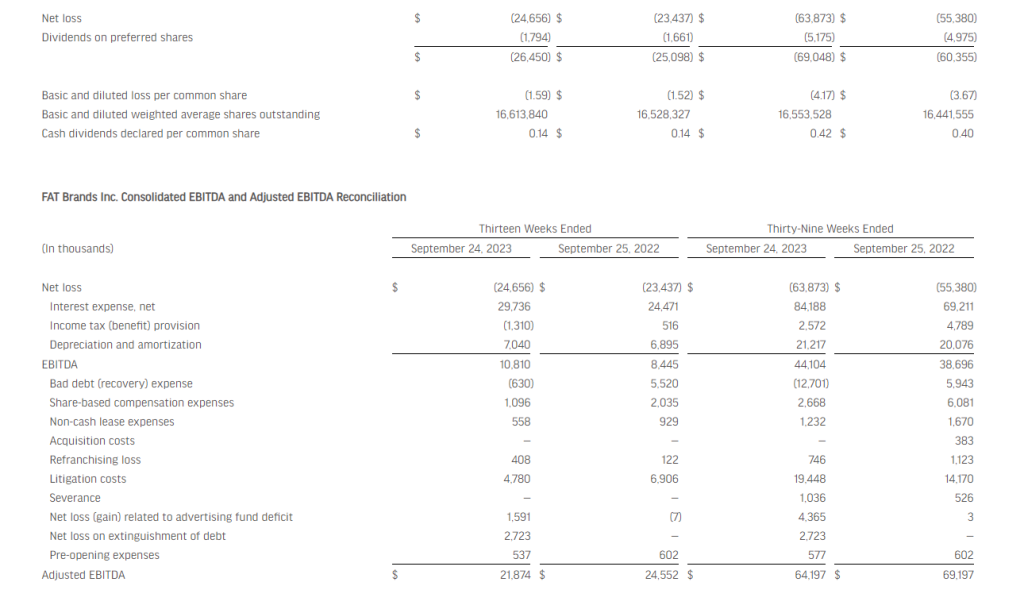

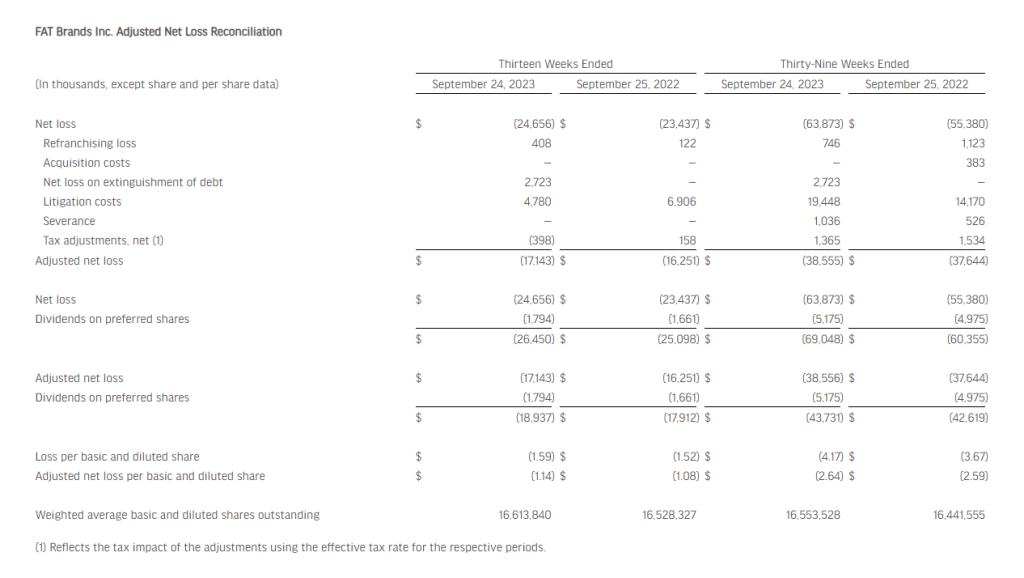

3Q23 Results. FAT Brands reported 3Q23 revenue of $109.4 million, up 6% y-o-y from $103.2 million in the year ago quarter. System-wide sales growth was 0.8%. FAT reported adjusted EBITDA of $21.9 million in the quarter, compared to $24.6 million in 3Q22 (which included $7.2 million of tax credits). Net loss for the quarter was $26.5 million, or $1.59/sh, compared to a net loss of $25.1 million, or $1.52/sh last year. Adjusted net loss for the quarter was $18.9 million, or $1.14/sh, compared to a net loss of $17.9 million, or a loss of $1.08/sh, last year. We had projected revenue of $107 million and a net loss of $28.4 million, or a loss of $1.71/sh.

Ongoing Development. YTD, FAT has opened 96 restaurants, including 30 in 3Q. The Company expects to see 150 openings 2023. YTD, over 200 new franchise agreements have been signed, bringing the total pipeline to over 1,100 signed agreements. This pipeline will add some $60 million to adjusted EBITDA.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

Cumulus Media (NASDAQ: CMLS) is an audio-first media company delivering premium content to over a quarter billion people every month — wherever and whenever they want it. Cumulus Media engages listeners with high-quality local programming through 406 owned-and-operated radio stations across 86 markets; delivers nationally-syndicated sports, news, talk, and entertainment programming from iconic brands including the NFL, the NCAA, the Masters, CNN, the AP, the Academy of Country Music Awards, and many other world-class partners across more than 9,500 affiliated stations through Westwood One, the largest audio network in America; and inspires listeners through the Cumulus Podcast Network, its rapidly growing network of original podcasts that are smart, entertaining and thought-provoking. Cumulus Media provides advertisers with personal connections, local impact and national reach through broadcast and on-demand digital, mobile, social, and voice-activated platforms, as well as integrated digital marketing services, powerful influencers, full-service audio solutions, industry-leading research and insights, and live event experiences. Cumulus Media is the only audio media company to provide marketers with local and national advertising performance guarantees. For more information visit www.cumulusmedia.com.

Michael Kupinski, Director of Research, Equity Research Analyst, Digital, Media & Technology , Noble Capital Markets, Inc.

Jacob Mutchler, Research Associate, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

In-line quarter. Revenues of $207.4 million, down 11.2% from year earlier levels, were in line with our $207.8 million estimate. Costs came in lower than expected, and, as a result, adj. EBITDA was 14.1% better than expected at $26.9 million versus our $23.6 million estimate.

Green shoots? The company completed a successful upfront with strong Network sales. We believe that cancellations will be much less than the 50% that it experienced last year, which should provide for the prospect for a meaningful turnaround in its high margin Network business in 2024.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

ARLP is a diversified natural resource company that generates operating and royalty income from coal produced by its mining complexes and royalty income from mineral interests it owns in strategic oil & gas producing regions in the United States, primarily the Permian, Anadarko and Williston basins. ARLP currently produces coal from seven mining complexes its subsidiaries operate in Illinois, Indiana, Kentucky, Maryland and West Virginia. ARLP also operates a coal loading terminal on the Ohio River at Mount Vernon, Indiana. ARLP markets its coal production to major domestic and international utilities and industrial users and is currently the second largest coal producer in the eastern United States. In addition, ARLP is positioning itself as an energy provider for the future by leveraging its core technology and operating competencies to make strategic investments in the fast growing energy and infrastructure transition.

Mark Reichman, Managing Director, Equity Research Analyst, Natural Resources, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

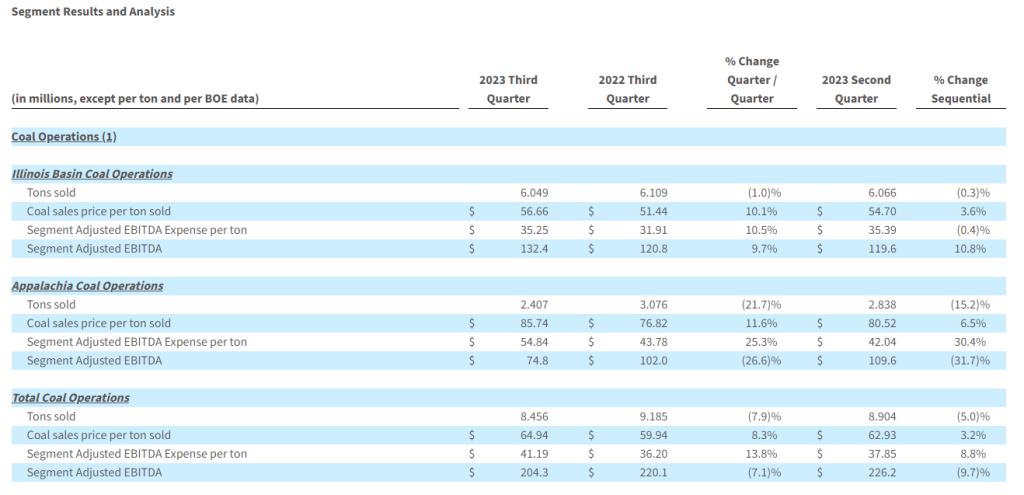

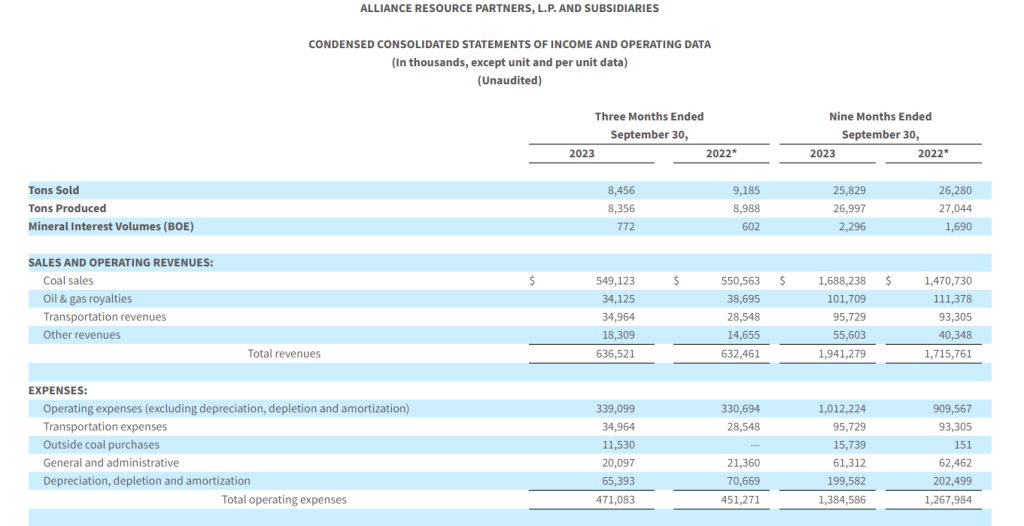

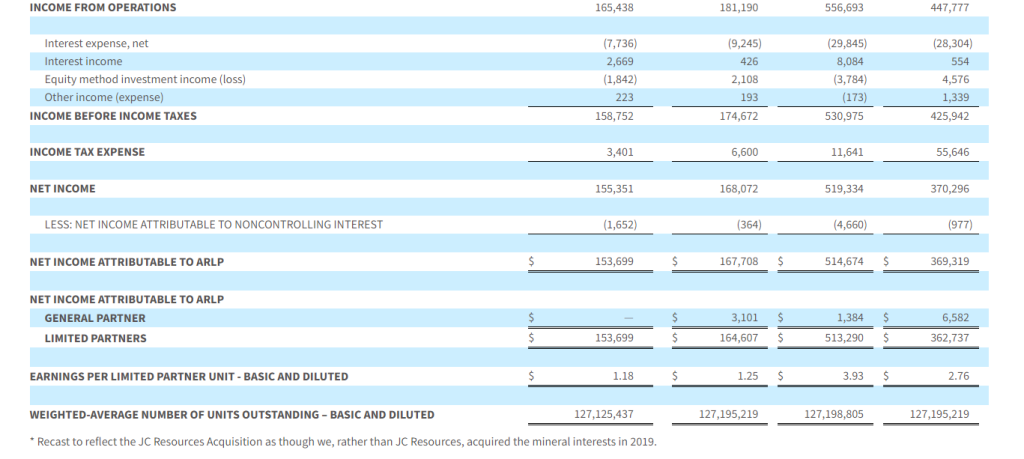

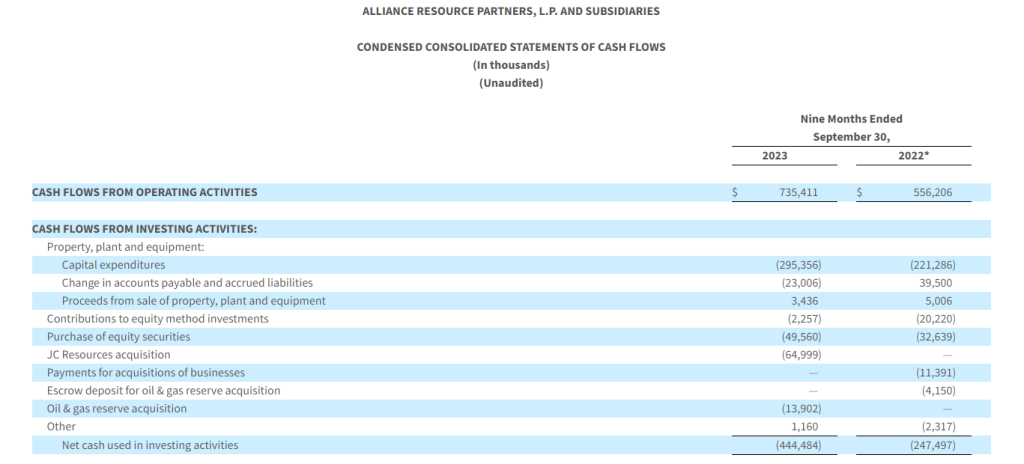

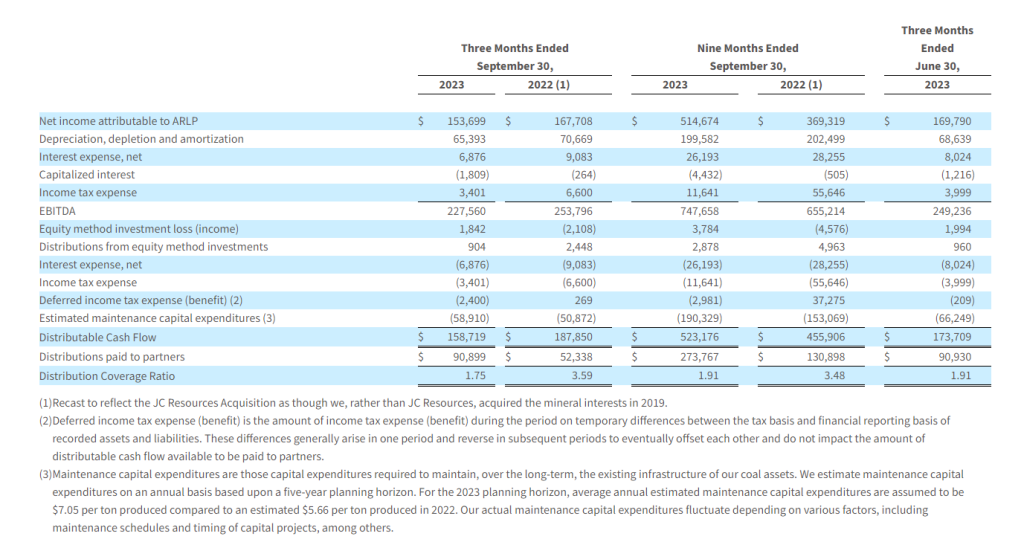

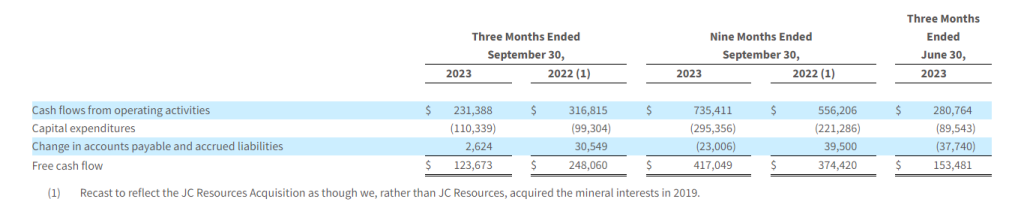

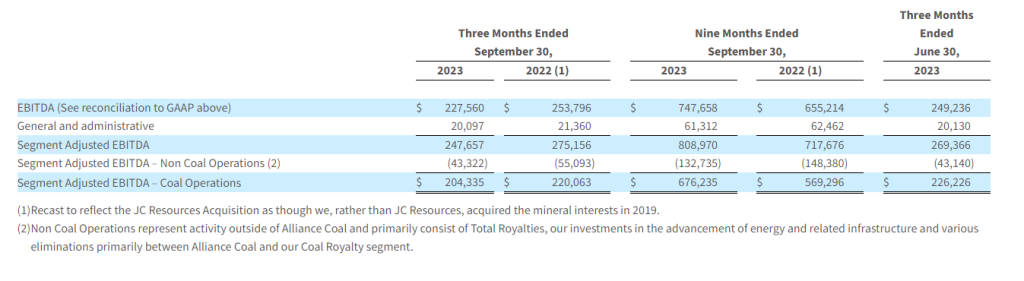

Third quarter financial results. Alliance reported third quarter EBITDA and earnings per unit (EPU) of $227.6 million and $1.18, respectively, compared to $253.8 million and $1.25 during the prior year period. We had forecast EBITDA and EPU of $240.3 million and $1.20. Revenue increased 0.6% to $636.5 million, while income from operations declined 8.7% to $165.4 million. The company generated free cash flow of $123.7 million and distributable cash flow provided quarterly cash distribution coverage of 1.75x. Third quarter financial results were negatively impacted by lower coal sales volumes and higher costs at its coal operations in Appalachia.

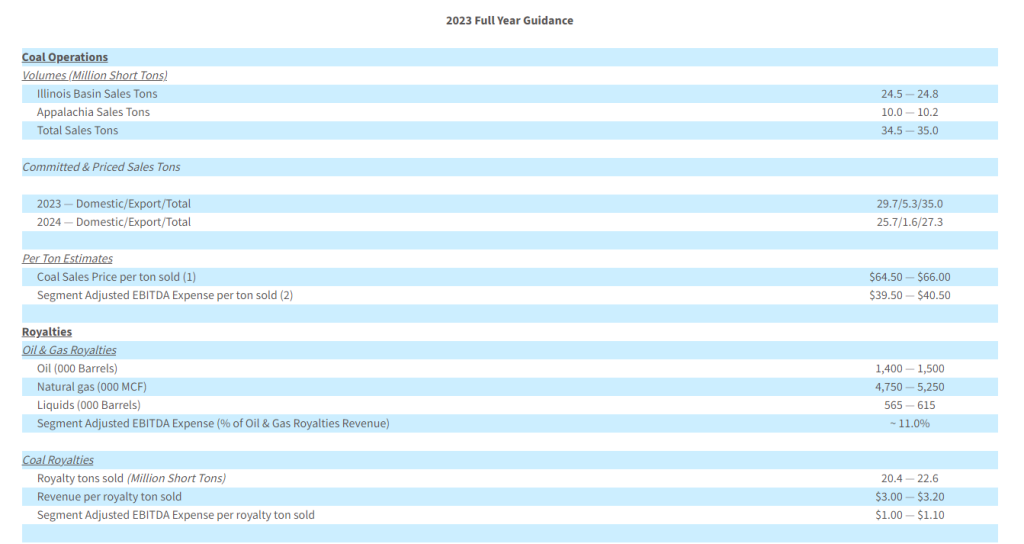

Refined management guidance. Alliance provided updated guidance for the remainder of the year which we have incorporated into our estimates as detailed in the body of this note. Total coal sales are expected to be in the range of 34.5 million to 35.0 million tons compared to previous expectations of 35.5 million to 36.0 million tons, while the coal sales price per ton is expected to be in the range of $64.50 to $66.00 compared to previous guidance of $65.00 to $66.00. Segmented adjusted EBITDA expense per ton sold is expected to be $39.50 to $40.50 compared to previous guidance of $38.00 to $41.00.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

Portsmouth, New Hampshire-based medical device manufacturer Laborie Medical Technologies announced it has acquired Minnesota company Urotronic in a deal worth up to $600 million. The acquisition provides Laborie entry into the interventional urology market and adds Urotronic’s novel Optilume drug-coated balloon technology to its product portfolio.

The definitive agreement was signed on September 6, 2023 with an upfront payment of $255 million in cash to close the deal. Up to $345 million more is payable based on certain commercial and reimbursement milestones being achieved.

Optilume is a minimally invasive surgical therapy (MIST) that combines mechanical dilation with delivery of the chemotherapy drug paclitaxel to treat urinary tract conditions like urethral strictures and benign prostatic hyperplasia (BPH), also known as enlarged prostate.

BPH affects over 40 million men in the United States alone and the global market for BPH treatment is valued at over $4 billion. Current surgical interventions for BPH like transurethral resection of the prostate (TURP) or laser procedures can have side effects and long recovery times.

Optilume has already gained FDA approval and CE Mark in Europe for treating BPH. This regulatory clearance, along with positive clinical data showing good safety and efficacy, were key factors in Laborie’s decision to acquire Urotronic.

The Optilume technology represents a paradigm shift in how urologists can treat patients suffering from BPH and urethral strictures. Rather than invasive surgery or permanent implants, the drug-coated balloon can be inserted cystoscopically and then inflated to dilate the urethra and deliver the paclitaxel to the tissue. The minimally invasive approach leads to fast patient recovery compared to other options.

According to Laborie Medical President and CEO Michael Frazzette, “There has never been a minimally invasive, combination drug-device therapy like Optilume before, leading to a highly disruptive, paradigm change for physicians treating urethral strictures and BPH.”

Urotronic CEO David Perry likewise noted that “Backed by positive clinical data, the Optilume BPH therapy is truly groundbreaking as the only MIST option that doesn’t require cutting, burning, steaming or a permanent implant.”

The Urotronic acquisition represents a strategic move for Laborie Medical Technologies to push further into the global urology market. Laborie is focused on high-growth segments including urology, gastroenterology, gynecology, and obstetrics.

According to Patricia Industries, which owns Laborie, the deal furthers Laborie’s long-term growth strategy by adding an innovative product with strong potential to its portfolio. Urotronic’s employees and assets will be fully integrated into Laborie Medical after the acquisition.

Laborie itself was acquired by Patricia Industries in 2017 for an estimated $2.4 billion and has gone through a period of rapid growth since then. The company manufactures a range of diagnostic equipment like urodynamic systems as well as therapy products such as electrodes for pelvic floor stimulation.

The global medical device market has seen a surge of M&A activity in recent years. Strategic mergers and acquisitions allow companies to expand their product lines, access new technology, enter new geographic markets, and consolidate to gain economies of scale.

Medtech titan Boston Scientific for example has made 10 acquisitions in the past 5 years totaling over $10 billion to become a leading player in less invasive device treatments. Teleflex likewise acquired Neotract and its novel UroLift system for treating BPH in a $1 billion purchase in 2017.

The closing of the Urotronic acquisition provides another growth milestone for Laborie Medical as it executes its strategy of providing innovative therapeutic solutions to physicians and hospitals involved in urological procedures. Adding Optilume’s promising technology gives it a differentiated offering in the nonsurgical treatment of enlarged prostate and strengthens Laborie’s portfolio for continued expansion in the urology device sector.

Coal sales price realizations of $64.94 per ton sold, up 8.3% year-over-year

Record oil & gas royalty volumes of 772 MBOE sold, up 28.2% year-over-year

Completed two strategic new ventures investments, totaling approximately $50.0 million

Declares a quarterly cash distribution of $0.70 per unit, or $2.80 per unit annualized, up 40.0% year-over-year

Reduced outstanding senior notes by $54.6 million during the 2023 Quarter, resulting in total and net leverage ratio of 0.36 times and 0.17 times, respectively

TULSA, Okla.–(BUSINESS WIRE)– Alliance Resource Partners, L.P. (NASDAQ: ARLP) (“ARLP” or the “Partnership”) today reported financial and operating results for the quarter ended September 30, 2023 (the “2023 Quarter”). Total revenues in the 2023 Quarter increased slightly to $636.5 million compared to $632.5 million for the quarter ended September 30, 2022 (the “2022 Quarter”) primarily as a result of higher transportation and other revenues, partially offset by lower oil & gas royalties. Net income for the 2023 Quarter was $153.7 million, or $1.18 per basic and diluted limited partner unit, compared to $167.7 million, or $1.25 per basic and diluted limited partner unit, for the 2022 Quarter as a result of increased total operating expenses, partially offset by higher interest income and lower income tax expense. EBITDA for the 2023 Quarter was $227.6 million compared to $253.8 million in the 2022 Quarter. (Unless otherwise noted, all references in the text of this release to “net income” refer to “net income attributable to ARLP.”)

Compared to the quarter ended June 30, 2023 (the “Sequential Quarter”), total revenues in the 2023 Quarter decreased 0.8% primarily as a result of lower coal sales volumes of 8.5 million tons sold compared to 8.9 million tons sold in the Sequential Quarter, partially offset by higher average coal sales prices, which increased 3.2% to $64.94 per ton sold in the 2023 Quarter. Lower revenues and higher total operating expenses contributed to a reduction in net income and EBITDA of 9.5% and 8.7%, respectively, compared to the Sequential Quarter. (For a definition of EBITDA and related reconciliation to its comparable GAAP financial measure, please see the end of this release.)

Financial and operating results for the nine months ended September 30, 2023 (the “2023 Period”) increased compared to the nine months ended September 30, 2022 (the “2022 Period”). Coal sales prices and coal sales revenues during the 2023 Period were higher by 16.8% and 14.8%, respectively, compared to the 2022 Period. Increased revenues and lower income tax expense were partially offset by higher total operating expenses in the 2023 Period, which resulted in higher net income and EBITDA by 39.4% and 14.1%, respectively, both as compared to the 2022 Period.

CEO Commentary

“Our well-contracted coal order book enabled us to navigate an otherwise challenging operating environment during the 2023 Quarter,” commented Joseph W. Craft III, Chairman, President and Chief Executive Officer. “Our coal segment achieved higher realized pricing per ton sold relative to both the 2022 and Sequential Quarters, a theme that continues to favorably impact year-to-date results, particularly with regards to EBITDA and net income. However, we faced some difficult mining conditions in Appalachia at all three mines during the 2023 Quarter, which resulted in higher operating costs and fewer tons produced versus previous expectations.”

Mr. Craft added, “Our Oil & Gas Royalties segment reported continued growth resulting in record production volumes, underscoring the success of recent acquisitions in core parts of the prolific Permian Basin. Although average realized pricing per BOE during the 2023 Quarter was lower compared to near record levels in the 2022 Quarter, our royalty portfolio is well-positioned to provide significant cash flow via hedge-free exposure to commodity price and cost-free organic growth.”

Mr. Craft concluded, “We are excited to announce direct investments in Ascend Elements and Infinitum during the 2023 Quarter. These companies are led by proven management teams and possess innovative, commercial technologies that, in our view, will reshape their respective industries. Beyond our direct investments, we are actively engaged in discussions with both companies to explore additional strategic opportunities intended to unlock value and growth for our unitholders.”

Coal Operations

ARLP’s coal sales prices per ton increased in all regions compared to both the 2022 and Sequential Quarters. Improved domestic pricing, partially offset by lower export price realizations, drove coal sales prices higher by 10.1% and 3.6% in the Illinois Basin and 11.6% and 6.5% in Appalachia as compared to the 2022 and Sequential Quarters, respectively. Tons sold decreased by 21.7% and 15.2% in Appalachia compared to the 2022 and Sequential Quarters, respectively, due to reduced volumes across the region caused by lock outages, customer plant maintenance, reduced operating units at MC Mining, and unique geologic conditions that delayed development of a new district at our Mettiki longwall operation. ARLP ended the 2023 Quarter with total coal inventory of 1.8 million tons, representing an increase of 0.5 million tons compared to the end of the 2022 Quarter and comparable to the end of the Sequential Quarter.

Segment Adjusted EBITDA Expense per ton for the 2023 Quarter increased by 10.5% in the Illinois Basin compared to the 2022 Quarter, resulting from increased sales-related expenses due to higher price realizations and higher labor-related, roof support and maintenance costs due to days lost by a sizable roof fall in July and a longwall move in August at our Hamilton mine. Segment Adjusted EBITDA Expense per ton in Appalachia increased by 25.3% and 30.4% compared to the 2022 and Sequential Quarters, respectively, due primarily to lower production volumes, purchased coal and increased labor-related, roof support, maintenance and selling expenses per ton.

Royalties

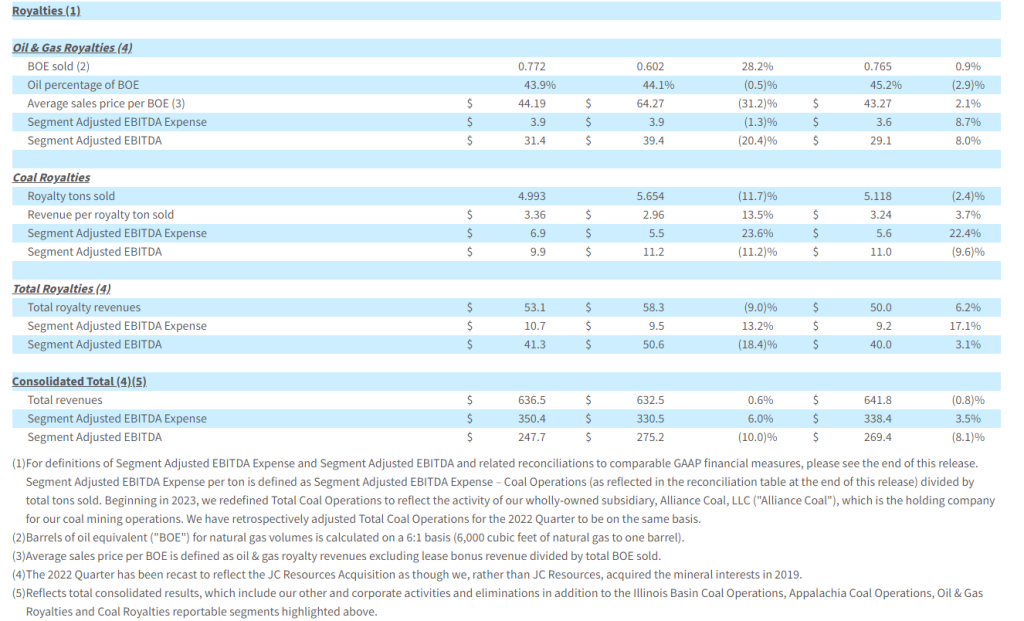

Segment Adjusted EBITDA for the Oil & Gas Royalties segment decreased to $31.4 million in the 2023 Quarter compared to $39.4 million in the 2022 Quarter. The decrease was directly connected to lower price realizations, which decreased by 31.2%, partially offset by record oil & gas volumes, which increased 28.2% to 772 MBOE sold in the 2023 Quarter. Compared to the Sequential Quarter, Segment Adjusted EBITDA increased by 8.0% due to higher prices and volumes. Higher volumes during the 2023 Quarter resulted from increased drilling and completion activities on our interests and the acquisition of additional oil & gas mineral interests.

Segment Adjusted EBITDA for the Coal Royalties segment was $9.9 million for the 2023 Quarter, representing a decrease of $1.3 million and $1.1 million compared to the 2022 and Sequential Quarters, respectively, as a result of lower royalty tons sold and increased selling expenses, partially offset by higher average royalty rates per ton received from the Partnership’s mining subsidiaries.

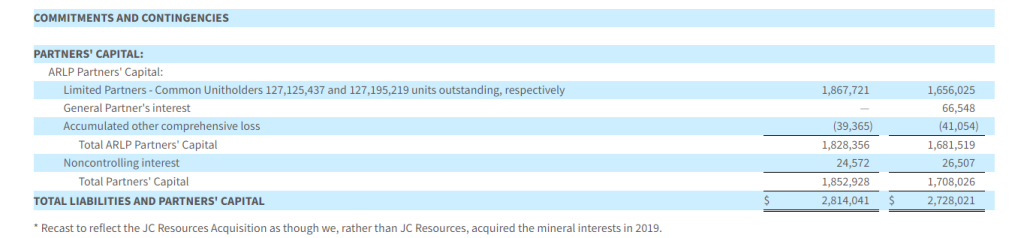

Balance Sheet and Liquidity

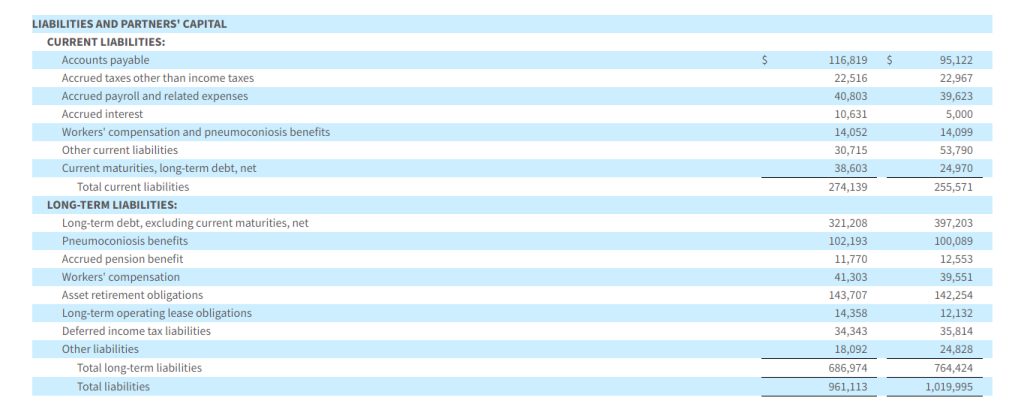

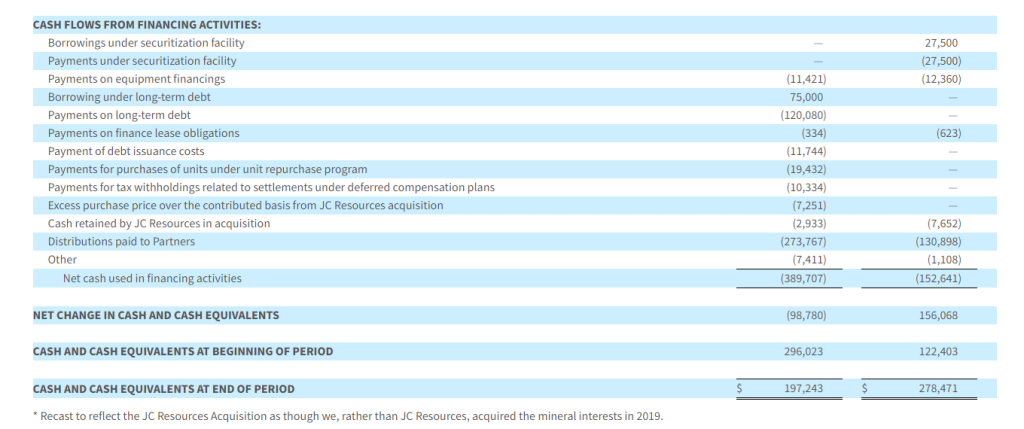

As of September 30, 2023, total debt and finance leases outstanding were $371.0 million, including $284.6 million in ARLP’s 2025 senior notes. During the 2023 Quarter, ARLP redeemed $50.0 million and repurchased $4.6 million of its senior notes due May 1, 2025. The Partnership’s total and net leverage ratio was 0.36 times and 0.17 times, respectively, as of September 30, 2023. ARLP ended the 2023 Quarter with total liquidity of $629.5 million, which included $197.2 million of cash and cash equivalents and $432.3 million of borrowings available under its revolving credit and accounts receivable securitization facilities.

Distributions

On October 25, 2023, the Board of Directors of ARLP’s general partner (the “Board”) approved a cash distribution to unitholders for the 2023 Quarter of $0.70 per unit (an annualized rate of $2.80 per unit), payable on November 14, 2023, to all unitholders of record as of the close of trading on November 7, 2023. The announced distribution represents a 40.0% increase over the cash distribution of $0.50 per unit for the 2022 Quarter and is consistent with the Sequential Quarter cash distribution.

Strategic Investments

During the 2023 Quarter, ARLP invested approximately $50 million in two companies that align with the Partnership’s strategy to allocate a portion of excess cash flows into high-growth businesses where ARLP can leverage its core competencies to generate meaningful, risk-adjusted returns.

Ascend Elements, Inc. (“Ascend Elements”)

As previously announced, on September 6, 2023, ARLP invested $25 million in Ascend Elements, a U.S.-based manufacturer and recycler of sustainable, engineered battery materials for electric vehicles, as part of its $460 million Series D funding round. This capital, combined with $480 million in total grants awarded by the Department of Energy, will advance construction of North America’s first commercial-scale manufacturing facility, located near Hopkinsville, Kentucky, producing cathode materials for electric vehicle batteries.

In close proximity to ARLP’s western Kentucky mining operations, when complete, the 1-million-square-foot manufacturing facility will produce enough cathode materials for 750,000 electric vehicles per year. ARLP intends to explore other strategic opportunities with Ascend Elements to expand investment in the battery recycling industry and leverage our unique operational expertise, geographic footprint, and strategic relationships in Kentucky and the surrounding battery-belt states to drive value creation for both companies.

Infinitum

During the 2023 Quarter, ARLP invested an additional $24.6 million in Infinitum, a Texas-based developer and manufacturer of high-efficiency electric motors, as part of their ongoing Series E equity raise. The incremental amount brings ARLP’s total investment in the company to approximately $67 million. Infinitum believes that its patented air core motors offer superior performance in half the weight and size, at a fraction of the carbon footprint of traditional motors, making them pound for pound the most efficient in the world.

In addition to the investment, ARLP’s wholly-owned subsidiary Matrix Design Group LLC (“Matrix“) and Infinitum are actively evaluating opportunities to combine Matrix’s underground mining expertise with Infinitum’s technology to deliver much needed innovation to the growing global mining industry by improving the safety, efficiency, and performance of certain mining machinery.

Outlook

“As we assess current market conditions, we have elected to slightly adjust our full year 2023 guidance for coal sales volumes and pricing, which will be highly dependent on logistics during the fourth quarter,” commented Mr. Craft. “We expect Appalachia operating expense per ton sold to be 8-10% higher during the fourth quarter of 2023 as development for the new district at Mettiki is not expected to be complete until late November 2023 and Tunnel Ridge has a normally scheduled longwall move. The new longwall district at Mettiki allows us to develop longer panels that will increase production and reduce unit costs in 2024.”

Mr. Craft closed, “As we look beyond 2023, we are encouraged by improving fundamentals for coal export demand based on recent trends in international benchmark pricing and emerging opportunities we see in the market. On the domestic front, we hold firm in our conviction that the reliability of our product is highly valued by our customers and the long-term potential for higher natural gas prices and growth in electric demand will sustain our projections for coal demand and lead to a slowing in the pre-mature closure of coal-fired power plants in the eastern U.S.”

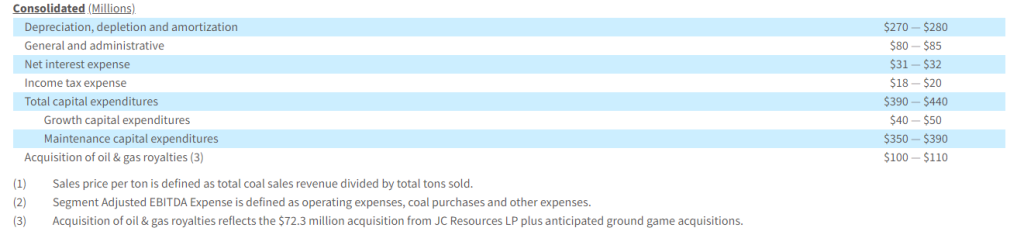

ARLP is providing the following updated guidance for the 2023 full year:

Conference Call

A conference call regarding ARLP’s 2023 Quarter financial results is scheduled for today at 10:00 a.m. Eastern. To participate in the conference call, dial (877) 407-0784 and request to be connected to the Alliance Resource Partners, L.P. earnings conference call. International callers should dial (201) 689-8560 and request to be connected to the same call. Investors may also listen to the call via the “investors” section of ARLP’s website at www.arlp.com.

An audio replay of the conference call will be available for approximately one week. To access the audio replay, dial U.S. Toll Free (844) 512-2921; International Toll (412) 317-6671 and request to be connected to replay using access code 13741573.

Concurrent with this announcement, we are providing qualified notice to brokers and nominees that hold ARLP units on behalf of non-U.S. investors under Treasury Regulation Section 1.1446-4(b) and (d) and Treasury Regulation Section 1.1446(f)-4(c)(2)(iii). Brokers and nominees should treat one hundred percent (100%) of ARLP’s distributions to non-U.S. investors as being attributable to income that is effectively connected with a United States trade or business. In addition, brokers and nominees should treat one hundred percent (100%) of the distribution as being in excess of cumulative net income for purposes of determining the amount to withhold. Accordingly, ARLP’s distributions to non-U.S. investors are subject to federal income tax withholding at a rate equal to the highest applicable effective tax rate plus ten percent (10%). Nominees, and not ARLP, are treated as the withholding agents responsible for withholding on the distributions received by them on behalf of non-U.S. investors.

About Alliance Resource Partners, L.P.

ARLP is a diversified energy company that is currently the largest coal producer in the eastern United States, supplying reliable, affordable energy domestically and internationally to major utilities, metallurgical and industrial users. ARLP also generates operating and royalty income from mineral interests it owns in strategic coal and oil & gas producing regions in the United States. In addition, ARLP is evolving and positioning itself as a reliable energy partner for the future by pursuing opportunities that support the advancement of energy and related infrastructure.

News, unit prices and additional information about ARLP, including filings with the Securities and Exchange Commission (“SEC”), are available at www.arlp.com. For more information, contact the investor relations department of ARLP at (918) 295-7673 or via e-mail at investorrelations@arlp.com.

***

The statements and projections used throughout this release are based on current expectations. These statements and projections are forward-looking, and actual results may differ materially. These projections do not include the potential impact of any mergers, acquisitions or other business combinations that may occur after the date of this release. We have included more information below regarding business risks that could affect our results.

FORWARD-LOOKING STATEMENTS: With the exception of historical matters, any matters discussed in this press release are forward-looking statements that involve risks and uncertainties that could cause actual results to differ materially from projected results. Those forward-looking statements include expectations with respect to our future financial performance, coal and oil & gas consumption and expected future prices, our ability to increase unitholder distributions in future quarters, business plans and potential growth with respect to our energy and infrastructure transition investments, optimizing cash flows, reducing operating and capital expenditures, preserving liquidity and maintaining financial flexibility, and our future repurchases of units and senior notes, among others. These risks to our ability to achieve these outcomes include, but are not limited to, the following: decline in the coal industry’s share of electricity generation, including as a result of environmental concerns related to coal mining and combustion and the cost and perceived benefits of other sources of electricity and fuels, such as oil & gas, nuclear energy, and renewable fuels; changes in macroeconomic and market conditions and market volatility, and the impact of such changes and volatility on our financial position; changes in global economic and geo-political conditions or changes in industries in which our customers operate; changes in commodity prices, demand and availability which could affect our operating results and cash flows; the outcome or escalation of current hostilities in Ukraine and the Israel-Gaza conflict; the severity, magnitude and duration of any future pandemics and impacts of such pandemics and of businesses’ and governments’ responses to such pandemics on our operations and personnel, and on demand for coal, oil, and natural gas, the financial condition of our customers and suppliers, available liquidity and capital sources and broader economic disruptions; actions of the major oil-producing countries with respect to oil production volumes and prices could have direct and indirect impacts over the near and long term on oil & gas exploration and production operations at the properties in which we hold mineral interests; changes in competition in domestic and international coal markets and our ability to respond to such changes; potential shut-ins of production by operators of the properties in which we hold oil & gas mineral interests due to low commodity prices or the lack of downstream demand or storage capacity; risks associated with the expansion of our operations and properties; our ability to identify and complete acquisitions and to successfully integrate such acquisitions into our business and achieve the anticipated benefits therefrom; our ability to identify and invest in new energy and infrastructure transition ventures; the success of our development plans for our wholly owned subsidiary, Matrix Design Group, LLC, and our investments in emerging infrastructure and technology companies; dependence on significant customer contracts, including renewing existing contracts upon expiration; adjustments made in price, volume, or terms to existing coal supply agreements; the effects of and changes in trade, monetary and fiscal policies and laws; central bank policy actions, bank failures and associated liquidity risks; the effects of and changes in taxes or tariffs and other trade measures adopted by the United States and foreign governments; legislation, regulations, and court decisions and interpretations thereof, both domestic and foreign, including those relating to the environment and the release of greenhouse gases, mining, miner health and safety, hydraulic fracturing, and health care; deregulation of the electric utility industry or the effects of any adverse change in the coal industry, electric utility industry, or general economic conditions; investors’ and other stakeholders’ increasing attention to environmental, social, and governance matters; liquidity constraints, including those resulting from any future unavailability of financing; customer bankruptcies, cancellations or breaches to existing contracts, or other failures to perform; customer delays, failure to take coal under contracts or defaults in making payments; our productivity levels and margins earned on our coal sales; disruptions to oil & gas exploration and production operations at the properties in which we hold mineral interests; changes in equipment, raw material, service or labor costs or availability, including due to inflationary pressures; changes in our ability to recruit, hire and maintain labor; our ability to maintain satisfactory relations with our employees; increases in labor costs including costs of health insurance and taxes resulting from the Affordable Care Act, adverse changes in work rules, or cash payments or projections associated with workers’ compensation claims; increases in transportation costs and risk of transportation delays or interruptions; operational interruptions due to geologic, permitting, labor, weather, supply chain shortage of equipment or mine supplies, or other factors; risks associated with major mine-related accidents, mine fires, mine floods or other interruptions; results of litigation, including claims not yet asserted; foreign currency fluctuations that could adversely affect the competitiveness of our coal abroad; difficulty maintaining our surety bonds for mine reclamation as well as workers’ compensation and black lung benefits; difficulty in making accurate assumptions and projections regarding post-mine reclamation as well as pension, black lung benefits, and other post-retirement benefit liabilities; uncertainties in estimating and replacing our coal mineral reserves and resources; uncertainties in estimating and replacing our oil & gas reserves; uncertainties in the amount of oil & gas production due to the level of drilling and completion activity by the operators of our oil & gas properties; uncertainties in the future of the electric vehicle industry and the market for EV charging stations; the impact of current and potential changes to federal or state tax rules and regulations, including a loss or reduction of benefits from certain tax deductions and credits; difficulty obtaining commercial property insurance, and risks associated with our participation in the commercial insurance property program; evolving cybersecurity risks, such as those involving unauthorized access, denial-of-service attacks, malicious software, data privacy breaches by employees, insiders or others with authorized access, cyber or phishing-attacks, ransomware, malware, social engineering, physical breaches, or other actions; and difficulty in making accurate assumptions and projections regarding future revenues and costs associated with equity investments in companies we do not control.

Additional information concerning these, and other factors can be found in ARLP’s public periodic filings with the SEC, including ARLP’s Annual Report on Form 10-K for the year ended December 31, 2022, filed on February 24, 2023,and ARLP’s Quarterly Reports on Form 10-Q for the quarters ended March 31, 2023 and June 30, 2023, filed on May 9, 2023 and August 8, 2023, respectively. Except as required by applicable securities laws, ARLP does not intend to update its forward-looking statements.

Reconciliation of Non-GAAP Financial Measures

Reconciliation of GAAP “net income attributable to ARLP” to non-GAAP “EBITDA” and “Distributable Cash Flow” (in thousands).

EBITDA is defined as net income attributable to ARLP before net interest expense, income taxes and depreciation, depletion and amortization. Distributable cash flow (“DCF”) is defined as EBITDA excluding equity method investment earnings, interest expense (before capitalized interest), interest income, income taxes and estimated maintenance capital expenditures and adding distributions from equity method investments. Distribution coverage ratio (“DCR”) is defined as DCF divided by distributions paid to partners.

Management believes that the presentation of such additional financial measures provides useful information to investors regarding our performance and results of operations because these measures, when used in conjunction with related GAAP financial measures, (i) provide additional information about our core operating performance and ability to generate and distribute cash flow, (ii) provide investors with the financial analytical framework upon which management bases financial, operational, compensation and planning decisions and (iii) present measurements that investors, rating agencies and debt holders have indicated are useful in assessing us and our results of operations.

EBITDA, DCF and DCR should not be considered as alternatives to net income attributable to ARLP, net income, income from operations, cash flows from operating activities or any other measure of financial performance presented in accordance with GAAP. EBITDA and DCF are not intended to represent cash flow and do not represent the measure of cash available for distribution. Our method of computing EBITDA, DCF and DCR may not be the same method used to compute similar measures reported by other companies, or EBITDA, DCF and DCR may be computed differently by us in different contexts (i.e., public reporting versus computation under financing agreements).

Reconciliation of GAAP “Cash flows from operating activities” to non-GAAP “Free cash flow” (in thousands).

Free cash flow is defined as cash flows from operating activities less capital expenditures and the change in accounts payable and accrued liabilities from purchases of property, plant and equipment. Free cash flow should not be considered as an alternative to cash flows from operating activities or any other measure of financial performance presented in accordance with GAAP. Our method of computing free cash flow may not be the same method used by other companies. Free cash flow is a supplemental liquidity measure used by our management to assess our ability to generate excess cash flow from our operations.

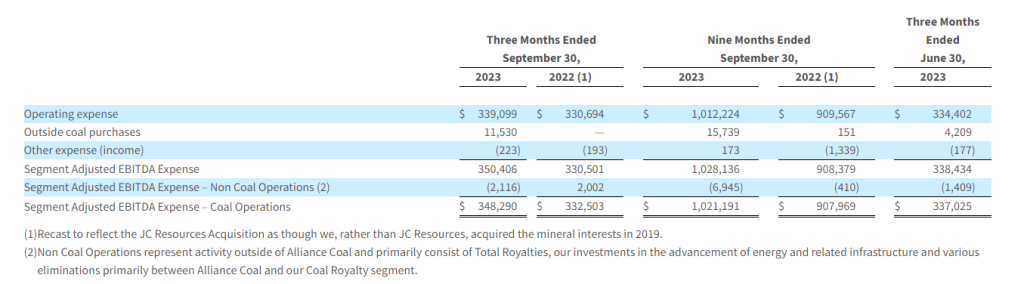

Reconciliation of GAAP “Operating Expenses” to non-GAAP “Segment Adjusted EBITDA Expense” and Reconciliation of non-GAAP ” EBITDA” to “Segment Adjusted EBITDA” (in thousands).

Segment Adjusted EBITDA Expense includes operating expenses, coal purchases, if applicable, and other income or expense. Transportation expenses are excluded as these expenses are passed on to our customers and, consequently, we do not realize any margin on transportation revenues. Segment Adjusted EBITDA Expense is used as a supplemental financial measure by our management to assess the operating performance of our segments. Segment Adjusted EBITDA Expense is a key component of EBITDA in addition to coal sales, royalty revenues and other revenues. The exclusion of corporate general and administrative expenses from Segment Adjusted EBITDA Expense allows management to focus solely on the evaluation of segment operating performance as it primarily relates to our operating expenses. Segment Adjusted EBITDA Expense – Coal Operations represents Segment Adjusted EBITDA Expense from our wholly-owned subsidiary, Alliance Coal, which holds our coal mining operations and related support activities.

Segment Adjusted EBITDA is defined as net income attributable to ARLP before net interest expense, income taxes, depreciation, depletion and amortization and general and administrative expenses. Segment Adjusted EBITDA – Coal Operations represents Segment Adjusted EBITDA from our wholly-owned subsidiary, Alliance Coal, which holds our coal mining operations and related support activities and allows management to focus primarily on the operating performance of our Illinois Basin and Appalachia segments.

Investor Relations Contact Cary P. Marshall Senior Vice President and Chief Financial Officer 918-295-7673 investorrelations@arlp.com

LAKE ZURICH, Ill.–(BUSINESS WIRE)– ACCO Brands Corporation (NYSE: ACCO) today announced that its board of directors has declared a quarterly cash dividend of $0.075 per share. The dividend will be paid on December 6, 2023, to stockholders of record as of the close of business on November 15, 2023.

“This is the Company’s 24th quarterly cash dividend since it began paying dividends in 2018. The Company’s dividend has become an important part of our capital allocation strategy and we remain committed to supporting our quarterly dividend with our robust free cash flow. At the current stock price, on an annualized basis, our shareholders are receiving an almost 6% yield on their investment,” said Tom Tedford, President and Chief Executive Officer of ACCO Brands.

About ACCO Brands Corporation

ACCO Brands, the Home of Great Brands Built by Great People, designs, manufactures and markets consumer and end-user products that help people work, learn, play and thrive. Our widely recognized brands include AT-A-GLANCE®, Five Star®, Kensington®, Leitz®, Mead®, PowerA®, Swingline®, Tilibra® and many others. More information about ACCO Brands Corporation (NYSE: ACCO) can be found at www.accobrands.com.

Leaders with Amazon, Atos, Foundever, Kinseed and Unisys named winners in five award categories

LONDON–(BUSINESS WIRE)– Information Services Group (ISG) (Nasdaq: III), a leading global technology research and advisory firm, today announced the winners of the first ISG Women in Digital Awards program for the Europe, Middle East and Africa (EMEA) region, recognizing women and their achievements in the digital world.

At a live, virtual award ceremony yesterday, leaders with Amazon, Atos, Foundever, Kinseed and Unisys were honored as winners in five categories, as selected by a panel of industry judges.

“The winners of the inaugural ISG Women in Digital Awards program in EMEA were chosen from an exceptional field of more than 100 highly accomplished finalists,” said Steve Hall, partner and president, ISG EMEA. “It is an honor to recognize the accomplishments and skills our nominees and winners are bringing to the digital industry.”

An independent panel of judges, comprised of Helen Ricardo, vice president, head of Strategic Growth, Atos; Isabelle Roux-Chenu, former group general counsel, head of Group Commercial & Contract Management and senior advisor to Group Chairman & CEO for Capgemini, and Ola Chowning, partner and Digital lead for ISG North Europe, evaluated the nominations and selected the following winners:

Rising Star: for demonstrating exceptional and continuous growth, with increasing levels of leadership, responsibility and sphere of impact: Gold Winner: Mariana Diniz, vice president, head of global digital solutions, Foundever Silver Winner: Aditi Sarao, senior director, new business UK&I, Tech Mahindra Bronze Winner: Alexandra Dehnert, vice president, Genpact

Women’s Advocate: for playing an active role guiding women to succeed in the digital world: Gold Winner: Mitali Gohel, senior program manager, Amazon Silver Winner: Karin Schönwetter, vice president and technology managing director, IBM Bronze Winner: Vinoliah Martin, client executive, Microsoft South Africa

Digital Innovator: for making a significant impact on an organization, business or client through creative use of digital solutions: Gold Winner: Pal Bhusate, CEO and founder of Kinseed Silver Winner: Ruha Antony, lead innovation and technology, Nestlé Germany Bronze Winner: Anca Iordanescu, vice president of engineering – Stores of the Future, IKEA

Rock Star Leader: for leading a major transformation with significant business impact and demonstrating exceptional leadership skills: Gold Winner: Berenice Chassagne, CEO of Growing Markets, Atos Silver Winner: Nicole Henderson, deputy director, Business Relationship Management, UNHCR Bronze Winner: Moira Cheng, senior manager, IT Operations & Experience, Vodafone

Patrycja Sobera, global vice president of delivery for Digital Workplace Solutions, Unisys, was chosen by the judges as the Digital Titan of the Year for EMEA from the entire pool of regional nominees, recognizing her as the most outstanding woman in digital for the region for 2023.

The awards program, launched in the Americas in 2022, was expanded for 2023 to the EMEA and Asia Pacific regions, including India. The global program received a total of 327 nominees, who are listed in an online ISG Women in Digital eBook. Awards for EMEA were presented October 26, at 6 p.m., BST. Awards for the Americas were presented on September 7, and Awards for Asia Pacific and India were presented on October 11.

“Women are breaking barriers and making lasting, positive changes in digital and technology leadership roles,” said Kimberly Tobias, ISG director and head of the ISG Women in Digital program. “We are honored to recognize the success of each person nominated. Congratulations to our 2023 winners.”

Created in 2018, the ISG Women in Digital community provides a platform to exchange practical advice and innovative ideas on diversity and advancement in the workplace. The community hosts a LinkedIn page, an ongoing ISG Digital Dish podcast series, and regular events for ISG employees and the greater IT and business services industry.

For more information about the ISG Women in Digital Awards, contact ISG.

About ISG

ISG (Information Services Group) (Nasdaq: III) is a leading global technology research and advisory firm. A trusted business partner to more than 900 clients, including more than 75 of the world’s top 100 enterprises, ISG is committed to helping corporations, public sector organizations, and service and technology providers achieve operational excellence and faster growth. The firm specializes in digital transformation services, including automation, cloud and data analytics; sourcing advisory; managed governance and risk services; network carrier services; strategy and operations design; change management; market intelligence and technology research and analysis. Founded in 2006, and based in Stamford, Conn., ISG employs more than 1,600 digital-ready professionals operating in more than 20 countries—a global team known for its innovative thinking, market influence, deep industry and technology expertise, and world-class research and analytical capabilities based on the industry’s most comprehensive marketplace data. For more information, visit www.isg-one.com.

LOS ANGELES, Oct. 26, 2023 (GLOBE NEWSWIRE) — FAT (Fresh. Authentic. Tasty.) Brands Inc. (NASDAQ: FAT) (“FAT Brands” or the “Company”) today reported financial results for the fiscal third quarter ended September 24, 2023.

Andy Wiederhorn, Chairman of FAT Brands, commented, “With the acquisition of Smokey Bones early in the fourth quarter, we have grown the FAT Brands portfolio to 18 iconic restaurant brands with annualized system wide sales of $2.4 billion. Year to date through the third quarter, we have opened 96 restaurants, including 30 that opened in the third quarter, and are on track to open 150 new restaurants in 2023. We are seeing strong franchisee interest in development opportunities, having signed over 200 development agreements in 2023, bringing our total pipeline to over 1,100 units. This represents the potential for over 50% EBITDA growth over the next several years.”

Rob Rosen, Co-Chief Executive Officer of FAT Brands, commented, “While franchise interest remains high across all of our brands, we continue to be focused on the expansion of Twin Peaks. This year, we plan to open 15 to 17 new lodges, of which 11 have been opened so far. We expect to end the year with over 110 lodges, a 35% increase since acquiring the brand in 2021. Our growth pipeline includes over 125 lodges and Smokey Bones’ healthy real estate portfolio provides us with the opportunity to convert over 40 locations into Twin Peaks lodges, with the potential to significantly accelerate the growth of the brand.”

Ken Kuick, Co-Chief Executive Officer of FAT Brands, commented, “We believe there are significant opportunities on the horizon for FAT Brands. Our seasoned leadership team and strong brand management platform allow us to efficiently integrate new brands while maintaining a healthy and evolving pipeline for organic growth. These strengths position us for continued growth in the future, which will help deleverage our balance sheet.”

Fiscal ThirdQuarter 2023Highlights

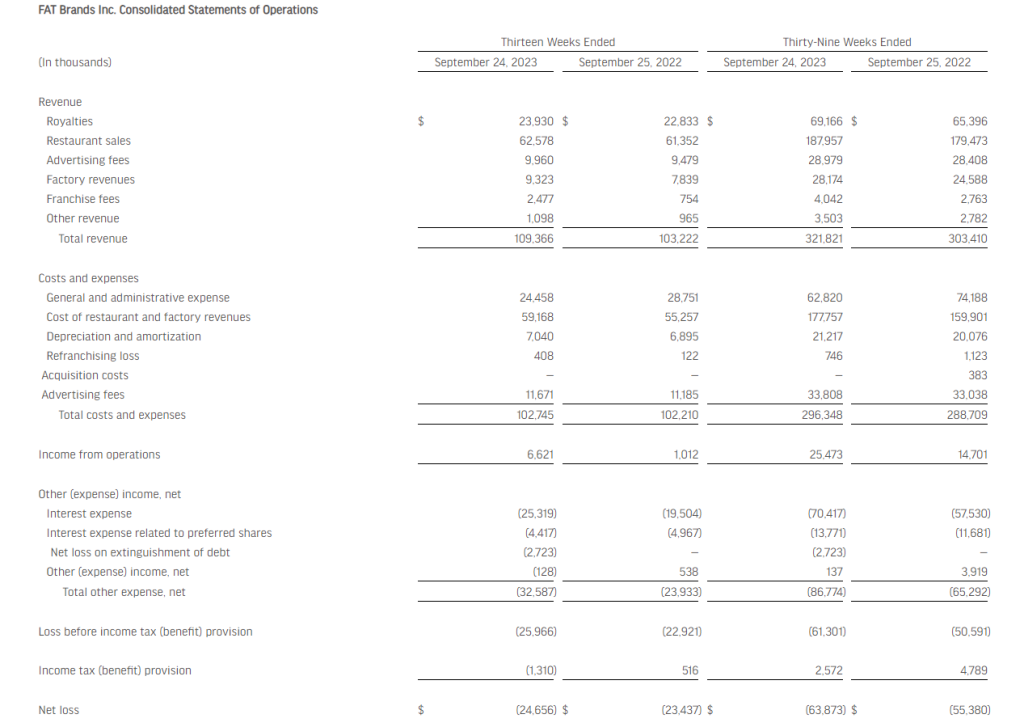

• Total revenue improved 6.0% to $109.4 million compared to $103.2 million in the fiscal third quarter of 2022

◦ System-wide sales growth of 0.8% in the fiscal third quarter of 2023 compared to the prior year fiscal quarter ◦ Year-to-date system-wide same-store sales growth of 1.3% in the fiscal third quarter of 2023 compared to the prior year ◦ 30 new store openings during the fiscal third quarter of 2023

• Net loss of $24.7 million, or $1.59 per diluted share, compared to $23.4 million, or $1.52 per diluted share, in the fiscal third quarter of 2022 • Adjusted EBITDA(1) of $21.9 million compared to $24.6 million in the fiscal third quarter of 2022 • Adjusted net loss(1) of $17.1 million, or $1.14 per diluted share, compared to adjusted net loss of $16.3 million, or $1.08 per diluted share, in the fiscal third quarter of 2022

(1) EBITDA, Adjusted EBITDA and adjusted net loss are non-GAAP measures defined below, under “Non-GAAP Measures”. Reconciliation of GAAP net loss to EBITDA, adjusted EBITDA and adjusted net loss are included in the accompanying financial tables.

Summary of Fiscal ThirdQuarter 2023Financial Results

Total revenue increased $6.2 million, or 6.0%, in the third quarter of 2023 to $109.4 million compared to $103.2 million in the same period of 2022, driven by a 4.8% increase in royalties, a 2.0% increase in company-owned restaurant revenues, a 228.5% increase in franchise fees and an 18.9% increase in revenues from our manufacturing facility.

Costs and expenses consist of general and administrative expense, cost of restaurant and factory revenues, depreciation and amortization, refranchising net loss and advertising fees. Costs and expenses remained largely unchanged in the third quarter, increasing 0.5% in the third quarter of 2023 compared to the same period in the prior year.

General and administrative expense decreased $4.3 million, or 14.9%, in the third quarter of 2023 compared to the same period in the prior year, primarily due to the recognition of $1.0 million related to Employee Retention Credits during the third quarter of 2023 and lower professional fees related to certain litigation matters.

Cost of restaurant and factory revenues increased $3.9 million, or 7.1%, in the third quarter of 2023 compared to the same period in the prior year, primarily due to Employee Retention Credits recognized during the third quarter of 2022 and higher company-owned restaurant and dough factory revenues.

Depreciation and amortization increased $0.1 million, or 2.1% in the third quarter of 2023 compared to the same period in the prior year, primarily due to depreciation of new property and equipment at company-owned restaurant locations.

Advertising expenses in the third quarter of 2023 increased $0.5 million compared to the prior year period. These expenses vary in relation to advertising revenues.

Total other expense, net, for the third quarter of 2023 and 2022 was $32.6 million and $23.9 million, respectively, which is inclusive of interest expense of $29.7 million and $24.5 million, respectively. Total other expense, net for the third quarter of 2023 also included a $2.7 million net loss on extinguishment of debt.

Adjusted net loss(1) of $17.1 million, or $1.14 per diluted share, compared to adjusted net loss of $16.3 million, or $1.08 per diluted share, in the fiscal third quarter of 2022.

Key Financial Definitions

New store openings – The number of new store openings reflects the number of stores opened during a particular reporting period. The total number of new stores per reporting period and the timing of stores openings has, and will continue to have, an impact on our results.

Same-store sales growth – Same-store sales growth reflects the change in year-over-year sales for the comparable store base, which we define as the number of stores open and in the FAT Brands system for at least one full fiscal year. For stores that were temporarily closed, sales in the current and prior period are adjusted accordingly. Given our focused marketing efforts and public excitement surrounding each opening, new stores often experience an initial start-up period with considerably higher than average sales volumes, which subsequently decrease to stabilized levels after three to six months. Additionally, when we acquire a brand, it may take several months to integrate fully each location of said brand into the FAT Brands platform. Thus, we do not include stores in the comparable base until they have been open and in the FAT Brands system for at least one full fiscal year.

System-wide sales growth – System wide sales growth reflects the percentage change in sales in any given fiscal period compared to the prior fiscal period for all stores in that brand only when the brand is owned by FAT Brands. Because of acquisitions, new store openings and store closures, the stores open throughout both fiscal periods being compared may be different from period to period.

Conference Call and Webcast

FAT Brands will host a conference call and webcast to discuss its fiscal third quarter 2023 financial results today at 4:30 PM ET. Hosting the conference call and webcast will be Andy Wiederhorn, Chairman of the Board, and Ken Kuick, Co-Chief Executive Officer and Chief Financial Officer.

The conference call can be accessed live over the phone by dialing 1-844-826-3035 from the U.S. or 1-412-317-5195 internationally. A replay will be available after the call until Thursday, November 16, 2023, and can be accessed by dialing 1-844-512-2921 from the U.S. or 1-412-317-6671 internationally. The passcode is 10183290. The webcast will be available at www.fatbrands.com under the “Investors” section and will be archived on the site shortly after the call has concluded.

About FAT (Fresh. Authentic. Tasty.) Brands

FAT Brands (NASDAQ: FAT) is a leading global franchising company that strategically acquires, markets, and develops fast casual, quick-service, casual dining, and polished casual dining concepts around the world. The Company currently owns 18 restaurant brands: Round Table Pizza, Fatburger, Marble Slab Creamery, Johnny Rockets, Fazoli’s, Twin Peaks, Smokey Bones, Great American Cookies, Hot Dog on a Stick, Buffalo’s Cafe & Express, Hurricane Grill & Wings, Pretzelmaker, Elevation Burger, Native Grill & Wings, Yalla Mediterranean and Ponderosa and Bonanza Steakhouses and franchises and owns approximately 2,300 units worldwide. For more information, please visit www.fatbrands.com.

Forward-Looking Statements

This press release contains forward-looking statements within the meaning of the Private Securities Litigation Reform Act of 1995, including statements relating to the future financial and operating results of the Company, estimates of future EBITDA, the timing and performance of new store openings, future reductions in cost of capital and leverage ratio, our ability to conduct future accretive acquisitions and our pipeline of new store locations. Forward-looking statements generally use words such as “expect,” “foresee,” “anticipate,” “believe,” “project,” “should,” “estimate,” “will,” “plans,” “forecast,” and similar expressions, and reflect our expectations concerning the future. Forward-looking statements are subject to significant business, economic and competitive risks, uncertainties and contingencies, many of which are difficult to predict and beyond our control, which could cause our actual results to differ materially from the results expressed or implied in such forward-looking statements. We refer you to the documents that we file from time to time with the Securities and Exchange Commission, such as our reports on Form 10-K, Form 10-Q and Form 8-K, for a discussion of these and other risks and uncertainties that could cause our actual results to differ materially from our current expectations and from the forward-looking statements contained in this press release. We undertake no obligation to update any forward-looking statements to reflect events or circumstances occurring after the date of this press release.

Non-GAAP Measures (Unaudited)

This press release includes the non-GAAP financial measures of EBITDA, adjusted EBITDA and adjusted net loss.

EBITDA is defined as earnings before interest, taxes, and depreciation and amortization. We use the term EBITDA, as opposed to income from operations, as it is widely used by analysts, investors, and other interested parties to evaluate companies in our industry. We believe that EBITDA is an appropriate measure of operating performance because it eliminates the impact of expenses that do not relate to business performance. EBITDA is not a measure of our financial performance or liquidity that is determined in accordance with generally accepted accounting principles (“GAAP”), and should not be considered as an alternative to net loss as a measure of financial performance or cash flows from operations as measures of liquidity, or any other performance measure derived in accordance with GAAP.

Adjusted EBITDA is defined as EBITDA (as defined above), excluding expenses related to acquisitions, refranchising loss, impairment charges, and certain non-recurring or non-cash items that the Company does not believe directly reflect its core operations and may not be indicative of the Company’s recurring business operations.

Adjusted net loss is a supplemental measure of financial performance that is not required by or presented in accordance with GAAP. Adjusted net loss is defined as net loss plus the impact of adjustments and the tax effects of such adjustments. Adjusted net loss is presented because we believe it helps convey supplemental information to investors regarding our performance, excluding the impact of special items that affect the comparability of results in past quarters to expected results in future quarters. Adjusted net loss as presented may not be comparable to other similarly titled measures of other companies, and our presentation of adjusted net loss should not be construed as an inference that our future results will be unaffected by excluded or unusual items. Our management uses this non-GAAP financial measure to analyze changes in our underlying business from quarter to quarter based on comparable financial results.

Reconciliations of net loss presented in accordance with GAAP to EBITDA, adjusted EBITDA and adjusted net loss are set forth in the tables below.

JPMorgan Chase CEO Jamie Dimon is cashing out for the first time in his 17 years leading the banking giant. Dimon and his family are planning to unload $141 million worth of JPMorgan stock starting next year. The sale of one million shares marks the first time Dimon has trimmed his stake since taking the helm in 2006.

While surprising, the stock sale doesn’t represent a loss of faith by Dimon in JPMorgan’s future. According to a securities filing, Dimon “continues to believe the company’s prospects are very strong.” Even after shedding $141 million in stock, Dimon will still own around 7.6 million shares in the bank, worth over $1 billion at current prices.

Dimon timed the sale to take advantage of a rebound in JPMorgan’s stock, which is up 5% year-to-date despite headwinds facing the banking sector. With the Fed boosting interest rates aggressively to combat inflation, demand for loans has slowed. Banks are also earning less on their bond holdings as rates rise.

Yet JPMorgan has managed to deliver solid earnings this year, with profit jumping 35% last quarter. The acquisition of assets from failed West Coast lender First Republic enhanced results. Dimon has praised JPMorgan’s “fortress balance sheet” that has it positioned to weather economic storms.

While JPMorgan has excelled recently, Dimon has sounded the alarm on gathering risks. He warned the Fed’s inflation fight may tip the remarkably resilient U.S. economy into recession. Geopolitical tensions around the world are also a rising threat. “Now may be the most dangerous time the world has seen in decades,” Dimon said earlier this month.

With risks rising, Dimon seems to be taking money off the table while JPMorgan’s stock still hovers near 52-week highs. The sale allows him to lock in returns after a tremendous 17-year run as CEO. Since taking the helm, Dimon has led JPMorgan to become the nation’s most profitable bank, raking in $48 billion last year alone.

Yet even after the stock sale, Dimon maintains immense exposure to JPMorgan’s fortunes. His remaining 7.6 million shares give him a built-in incentive to keep delivering results and driving the stock higher. While handing some risk off to the market, Dimon remains invested in JPMorgan’s success.

Dimon’s high-profile stock sale could potentially have ripple effects across the stock market. Some may view the move as Dimon lacking confidence in the markets and economy, sparking wider selling. JPMorgan’s share price often acts as a bellwether for overall market sentiment. If investors interpret Dimon’s sale as a warning sign, it could drag down indices and lead to a pullback in stocks. However, most analysts believe the sale is simply prudent financial planning by Dimon rather than a market call. With risks rising, Dimon is wisely diversifying his holdings after a long run-up in JPMorgan’s shares. Therefore, while the sale makes waves in the news, it likely won’t dramatically sway broader market direction. But in jittery times, even a whiff of pessimism from an influential CEO like Dimon can impact overall investor psychology.

Some view the stock sale as a shot across the bow at the Federal Reserve. Dimon may be signaling that excessive rate hikes could stifle the economy and hurt the banking sector. By cashing out now, Dimon is suggesting trouble may lie ahead.

Nonetheless, JPMorgan insists Dimon has confidence in the bank’s “very strong” prospects. The stock sale appears to be prudent risk management rather than a warning. As a savvy leader, Dimon knows the value of diversification.

With markets on edge, Dimon’s stock sale provides a dose of foreboding. Yet JPMorgan remains well-positioned to weather any storm. As long as Dimon is at the helm, don’t expect one stock sale to derail JPMorgan’s trajectory anytime soon.

With more than 60 units, RCI Hospitality Holdings, Inc., through its subsidiaries, is the country’s leading company in adult nightclubs and sports bars/restaurants. Clubs in New York City, Chicago, Dallas-Fort Worth, Houston, Miami, Minneapolis, Denver, St. Louis, Charlotte, Pittsburgh, Raleigh, Louisville, and other markets operate under brand names such as Rick’s Cabaret, XTC, Club Onyx, Vivid Cabaret, Jaguars Club, Tootsie’s Cabaret, Scarlett’s Cabaret, Diamond Cabaret, and PT’s Showclub. Sports bars/restaurants operate under the brand name Bombshells Restaurant & Bar.

Joe Gomes, Managing Director, Equity Research Analyst, Generalist , Noble Capital Markets, Inc.

Joshua Zoepfel, Research Associate, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

A Modification. RCI announced the Company modified $15.7 million in debt due October 2024 through extending maturities of the notes to free up more cash to buy back shares. The notes will continue to be unsecured at 12% interest, with $9.1 million due October 1, 2026, interest-only payable monthly, and $6.6 million due November 1, 2027, with monthly payments of interest and principal based on a 10-year amortization.

Buying Up Shares. With the modification in place for the debt, the Company has over $15 million to buy back shares. Using the Company’s closing price on October 26 of $52.70, RCI can purchase up to 297,912 shares. If the Company were to do so, this lowers the Company’s outstanding shares to roughly 9.1 million.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

Oil prices surged over $2 per barrel on Friday as rising geopolitical tensions in the Middle East sparked fears of potential supply disruptions. Brent crude jumped 2.3% to nearly $90 per barrel, while WTI crude also gained 2.3% to exceed $85 per barrel. The abrupt price spike reflects growing worries among traders that intensifying regional conflicts could impact oil exports.

The increase came after U.S. forces conducted airstrikes on Iranian-backed militias in Syria. This retaliatory move followed attacks on American troops in the region by Iran-supported groups. The escalating tit-for-tat strikes raised concerns that oil-rich Iran could get dragged into a wider regional conflagration.

Iran’s foreign minister warned that the U.S. would “not be spared” from retaliation if Israel does not halt its ongoing offensive against Hamas forces in Gaza. Iran is a major oil producer and key Hamas backer, so any disruption to its exports would impact global supply.

The Gaza conflict has already killed dozens and shows no signs of abating despite international efforts. Israel continues to pound Hamas targets and says preparations for a ground invasion are underway. The potential for the violence to spill over into neighboring countries and inflame sectarian divisions adds another worrying dimension for oil markets.

While no direct oil infrastructure has been affected yet, the market is trading on fears of what could transpire if hostilities spread further. Key transit points like the Strait of Hormuz could be threatened if regional clashes escalate. About 17% of global oil shipments flow through this narrow passage from the Persian Gulf.

Even Saudi Arabia, the world’s top oil exporter, could see its supply chains disrupted if the chaotic conflicts metastasize. While its production facilities remain insulated so far, continued attacks between Israel and Hamas, along with the risk of Iranian retaliation on U.S. forces, are setting markets on edge.

Traders are operating with limited visibility into how much further tensions may rise or which countries could get sucked in. Major oil producers like Saudi Arabia, Iraq, and the UAE would be hard pressed to supplant any lost Iranian barrels in a tight market. The low spare capacity leaves oil supplies extremely vulnerable to regional instability.

With myriad conflicts simmering, anxious traders are bidding up prices based on a worst-case scenario of supply shocks. However, this geopolitical risk premium could evaporate quickly if the situation de-escalates. Much depends on how hardline regimes like Iran choose to counter Israeli and U.S. actions in the days ahead.

For now, investors should brace for more volatility as headlines oscillate between conflict and ceasefire. Oil markets will remain on edge, with prices whip-sawing on any indications that Middle East disputes could jeopardize supply flows. While an outright supply crunch may not emerge, the risk has clearly increased.

Traders are weighing these bullish supply disruption anxieties against bearish demand uncertainties. Resurgent Covid cases in China along with broader inflationary pressures and economic weakness continue to dampen the consumption outlook. For oil markets, layers of complexity will drive price gyrations going forward. Strap in for a bumpy ride.

SANTA MONICA, Calif.–(BUSINESS WIRE)– Entravision (NYSE: EVC), a leading global advertising solutions, media and technology company, announced that it will release its third quarter 2023 financial results after market close on Thursday, November 2, 2023. The Company will host a conference call that day at 5:00 p.m. Eastern Time to discuss the third quarter 2023 results.

To access the conference call, please dial (844) 836-8739 (U.S.) or (412) 317-5440 (International) ten minutes prior to the start time. The call will also be available via live webcast on the investor relations portion of the Company’s website located at www.entravision.com.

If you cannot listen to the conference call at its scheduled time, there will be a replay available through Thursday, November 16, 2023, which can be accessed by dialing (844) 512-2921 (U.S.) or (412) 317-6671 (International) and entering the passcode 10182461. The webcast will also be archived on the Company’s website.

About Entravision

Entravision is a global advertising solutions, media and technology company. Over the past three decades, we have strategically evolved into a digital powerhouse, expertly connecting brands to consumers in the U.S., Latin America, Europe, Asia and Africa. Our digital segment, the company’s largest by revenue, offers a full suite of end-to-end advertising services in 40 countries. We have commercial partnerships with Meta, X Corp. (formerly known as Twitter), TikTok, and Spotify, and marketers can use our Smadex and other platforms to deliver targeted advertising to audiences around the globe. In the U.S., we maintain a diversified portfolio of television and radio stations that target Hispanic audiences and complement our global digital services. Entravision remains the largest affiliate group of the Univision and UniMás television networks. Shares of Entravision Class A Common Stock trade on the NYSE under ticker: EVC. Learn more about our offerings at entravision.com or connect with us on LinkedIn and Facebook.

Christopher T. Young Chief Financial Officer Entravision 310-447-3870

Holding Group’s Colossus SSP Integrates with Basis to Increase Advertisers’ Programmatic Reach of Multicultural / Diverse Media Inventory

Buy-Side Company Huddled Masses Collaborates with Basis to Serve SMB & Middle-Market Advertisers

HOUSTON and CHICAGO, Oct. 26, 2023 /PRNewswire/ — Direct Digital Holdings, Inc. (Nasdaq: DRCT) (“Direct Digital Holdings” or the “Company”), a leading advertising and marketing technology platform operating through its companies Colossus Media, LLC (“Colossus SSP”), Huddled Masses LLC (“Huddled Masses”) and Orange142, LLC (“Orange142”), today announced a new partnership with Basis Technologies (“Basis”), a global provider of programmatic advertising and media automation solutions.

As part of the agreement, Colossus SSP has directly integrated with the Basis media automation platform to enable more agencies and brands to increase diversity, equity and inclusion efforts by scaling spend on multicultural / diverse audiences and media, and minority-owned properties such as Blavity, Ebony and Univision.

In addition, Basis has been named a preferred demand-side platform (DSP) by Huddled Masses – which specializes in working with small- and mid-sized business (SMB) and middle-market business clients. With these types of advertisers often having smaller budgets, preventing them from accessing bigger technology platforms, this deal enables Basis to increase its reach with this set of underserved marketers.

“Basis Technologies is aligned with Direct Digital Holding’s focus on democratizing programmatic advertising for all,” said Mark Walker, CEO and Co-Founder, Direct Digital Holdings. “The omnichannel capabilities and wide scale of Basis will bolster Colossus SSP’s and Huddled Masses’ abilities. In turn, the relationship with Huddled Masses is also giving Basis expanded reach to an often overlooked – but extremely valuable – group of advertisers.”

“Direct Digital Holdings and Basis Technologies want to be part of the solution to overcome the barriers that underserved groups on the buy- and sell-side face in digital media,” said Tyler Kelly, President, Basis Technologies. “The need for the technology and services that Direct Digital Holdings offers is obvious, as they provide the heft and influence that can channel ad technology innovations for the benefit of a wider set of organizations.”

Currently, Colossus SSP represents 22,000 media properties – offering inventory from both multicultural / diverse and general market publishers. The company has 136,000 advertisers accessing its platform monthly, generating over 250 billion impressions per month across display, CTV, in-app and other media.

Huddled Masses is a marketing technology partner passionate about helping clients grow their business and serves as a long-term partner extension of the team, with decades of expertise to maximize the impact and efficiency of every client’s media investment as well as drive performance marketing.

About Basis Technologies

Basis Technologies is a global provider of programmatic advertising and media automation software and services for enterprises. The Basis platform improves omnichannel marketing performance by unifying programmatic and direct media buying, workflow automation, cross-channel campaign planning, universal reporting and business intelligence. It delivers a comprehensive selection of buying methods across all channels and devices, utilizing all major creative types and formats. Delivered through a world-class media services team or a SaaS model, Basis solves digital media complexity and drives profitability through a single system of record, seamless team collaboration, and actionable data-driven insights. Headquartered in Chicago with offices servicing North America, South America, and Europe, Basis Technologies has received numerous accolades for its commitment to employees and workplace culture. Learn more at https://basis.com.

About Direct Digital Holdings

Direct Digital Holdings (Nasdaq: DRCT), owner of operating companies Colossus SSP, Huddled Masses, and Orange 142, brings state-of-the-art sell- and buy-side advertising platforms together under one umbrella company. Direct Digital Holdings’ sell-side platform, Colossus SSP, offers advertisers of all sizes extensive reach within general market and multicultural media properties. The Company’s subsidiaries Huddled Masses and Orange142 deliver significant ROI for middle market advertisers by providing data-optimized programmatic solutions at scale for businesses in sectors that range from energy to healthcare to travel to financial services. Direct Digital Holdings’ sell- and buy-side solutions manage on average over 136,000 clients monthly, generating approximately 250 billion impressions per month across display, CTV, in-app and other media channels.

Forward-Looking Statements

This press release may contain forward-looking statements within the meaning of federal securities laws, including the Private Securities Litigation Reform Act of 1995, Section 27A of the Securities Act of 1933, as amended, and Section 21E of the Securities Exchange Act of 1934, as amended, and which are subject to certain risks, trends and uncertainties.

As used below, “we,” “us,” and “our” refer to Direct Digital Holdings. We use words such as “could,” “would,” “may,” “might,” “will,” “expect,” “likely,” “believe,” “continue,” “anticipate,” “estimate,” “intend,” “plan,” “project” and other similar expressions to identify forward-looking statements, but not all forward-looking statements include these words. All statements contained in this release that do not relate to matters of historical fact should be considered forward-looking statements.

All of our forward-looking statements involve estimates and uncertainties that could cause actual results to differ materially from those expressed in or implied by the forward-looking statements. Our forward-looking statements are based on assumptions that we have made in light of our industry experience and our perceptions of historical trends, current conditions, expected future developments and other factors we believe are appropriate under the circumstances. Although we believe that these forward-looking statements are based on reasonable assumptions, many factors could affect our actual operating and financial performance and cause our performance to differ materially from the performance expressed in or implied by the forward-looking statements, including, but not limited to: our dependence on the overall demand for advertising, which could be influenced by economic downturns; any slow-down or unanticipated development in the market for programmatic advertising campaigns; the effects of health epidemics, such as the ongoing global COVID-19 pandemic; operational and performance issues with our platform, whether real or perceived, including a failure to respond to technological changes or to upgrade our technology systems; any significant inadvertent disclosure or breach of confidential and/or personal information we hold, or of the security of our or our customers’, suppliers’ or other partners’ computer systems; any unavailability or non-performance of the non-proprietary technology, software, products and services that we use; unfavorable publicity and negative public perception about our industry, particularly concerns regarding data privacy and security relating to our industry’s technology and practices, and any perceived failure to comply with laws and industry self-regulation; restrictions on the use of third-party “cookies,” mobile device IDs or other tracking technologies, which could diminish our platform’s effectiveness; any inability to compete in our intensely competitive market; any significant fluctuations caused by our high customer concentration; any violation of legal and regulatory requirements or any misconduct by our employees, subcontractors, agents or business partners; any strain on our resources, diversion of our management’s attention or impact on our ability to attract and retain qualified board members as a result of being a public company; our dependence, as a holding company, of receiving distributions from Direct Digital Holdings, LLC to pay our taxes, expenses and dividends; and other factors and assumptions discussed in the “Risk Factors,” “Management’s Discussion and Analysis of Financial Conditions and Results of Operations” and other sections of our filings with the SEC that we make from time to time. Should one or more of these risks or uncertainties materialize or should any of these assumptions prove to be incorrect, our actual operating and financial performance may vary in material respects from the performance projected in these forward-looking statements. Further, any forward-looking statement speaks only as of the date on which it is made, and except as required by law, we undertake no obligation to update any forward-looking statement contained in this release to reflect events or circumstances after the date on which it is made or to reflect the occurrence of anticipated or unanticipated events or circumstances, and we claim the protection of the safe harbor for forward-looking statements contained in the Private Securities Litigation Reform Act of 1995.

Media Contacts Laura Goldberg LBG Public Relations for Direct Digital Holdings laura@lbgpr.com +1-347-683-1859