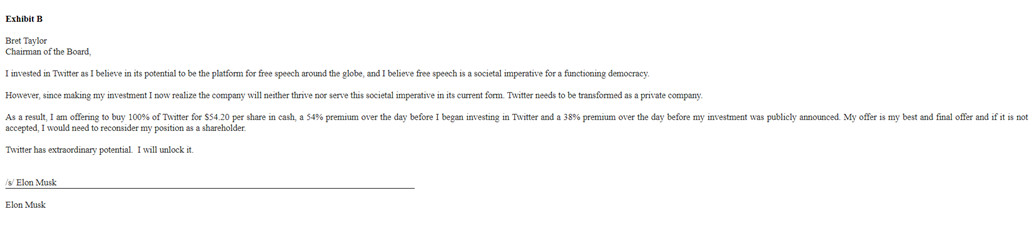

Ocugen, Inc. to Commercialize COVAXIN™ in Mexico, Rights Now Encompassing All of North America

Research, News, and Market Data on Ocugen

• Ocugen responsible for commercialization of COVAXIN™ in Mexico

• COVAXIN™, already authorized for emergency use in adults by health regulators in Mexico, has been submitted for Emergency Use Authorization for children aged 2-18 years

MALVERN, Pa. and HYDERABAD, India, April 18, 2022 (GLOBE NEWSWIRE) — Ocugen, Inc. (“Ocugen”) (NASDAQ: OCGN), a biotechnology company focused on discovering, developing, and commercializing novel gene therapies, biologicals and vaccines, and Bharat Biotech (BBIL), a global leader in vaccine innovation, today announced that they have entered into an amendment to their Co-development, Supply and Commercialization Agreement to expand Ocugen’s exclusive territory to include commercialization of COVAXIN™ in Mexico. This gives Ocugen COVAXIN™ commercialization rights for all of North America.

“We’re excited to commercialize COVAXIN™ in Mexico, as authorities there have made conquering this pandemic a major priority. After meeting with Mexico’s Secretary of Foreign Affairs, Marcelo Ebrard, in Delhi, we are encouraged by the role COVAXIN™ can play in Mexico’s continuing efforts to defeat the COVID-19 pandemic. COVAXIN™ is currently under review by COFEPRIS (Comisión Federal para la Protección contra Riesgos Sanitarios) for emergency use among children between 2 and 18 years of age, and Ocugen is prepared to collaborate with the public health community to help their efforts. We also thank Bharat Biotech for helping make this opportunity a reality,” said Dr. Shankar Musunuri, Chairman of the Board, Chief Executive Officer and Co-founder of Ocugen, Inc.

COVAXIN™ can be an ideal vaccination option for Mexico at this stage of the pandemic. As a whole virion, inactivated vaccine, it elicits robust cellular immune memory to SARS-CoV-2 and Variants of Concern. It offers logistical advantages that could support vaccine access in hard-to-reach communities.

“We are delighted to announce our partnership with Ocugen for Mexico, along with the United States and Canada. COVAXIN™ is a safe and efficacious inactivated vaccine for all age groups as evident from its data from global introduction. We are fully supportive of team Ocugen in our endeavor to expedite technology transfer activities towards commercial scale manufacturing of COVAXIN™ in North America,” said Dr. Krishna Ella, Chairman and Managing Director, Bharat Biotech.

The license extension between Ocugen and Bharat Biotech with respect to commercialization in Mexico includes the same profit share structure as in the United States.

About COVAXIN™ (BBV152)

COVAXIN™ is a whole virion, inactivated vaccine that combines an inactivated SARS-CoV-2 antigen with an adjuvant (6?g + Algel–IMDG[TLR7/8]). It was developed by Bharat Biotech in collaboration with the Indian Council of Medical Research (ICMR) – National Institute of Virology (NIV). COVAXIN™ is a highly purified and inactivated vaccine that is manufactured using a vero cell manufacturing platform. With supplies of more than 350 million doses globally for adults and children, COVAXIN™ is currently authorized under emergency use in more than 25 countries, including Mexico, and applications for emergency use authorization are pending in more than 60 other countries. The World Health Organization (WHO) added COVAXIN™ to its list of vaccines authorized for emergency use. And, as many as 110 countries have agreed to mutual recognition of COVID-19 vaccination certificates with India that includes vaccination using COVAXIN™.

About Ocugen, Inc.

Ocugen, Inc. is a biotechnology company focused on discovering, developing, and commercializing novel gene therapies, biologicals and vaccines that improve health and offer hope for people and global communities. We are making an impact through courageous innovation, taking science in new directions in service of patients. Our breakthrough modifier gene therapy platform has the potential to treat multiple diseases with one drug and we are advancing research in other therapeutic areas to offer new options for people with unmet medical needs. Discover more at www.ocugen.com and follow us on Twitter and LinkedIn.

About Bharat Biotech

Bharat Biotech has established an excellent track record of innovation with more than 145 global patents, a wide product portfolio of more than 16 vaccines, 4 bio-therapeutics, registrations in more than 123 countries, and the World Health Organization (WHO) Prequalifications. Located in Genome Valley in Hyderabad, India, a hub for the global biotech industry, Bharat Biotech has built a world-class vaccine & bio-therapeutics, research & product development, Bio-Safety Level 3 manufacturing, and vaccine supply and distribution. Having delivered more than 5 billion doses of vaccines worldwide, Bharat Biotech continues to lead innovation and has developed vaccines for influenza H1N1, Rotavirus, Japanese Encephalitis (JENVAC®), Rabies, Chikungunya, Zika, Cholera, and the world’s first tetanus-toxoid conjugated vaccine for Typhoid. Bharat’s commitment to global social innovation programs and public-private partnerships resulted in introducing path-breaking WHO pre-qualified vaccines BIOPOLIO®, ROTAVAC®, ROTAVAC 5D®, and Typbar TCV® combatting polio, rotavirus, typhoid infections, respectively. As a leader of pandemic vaccines, Bharat Biotech has successfully delivered COVAXIN®, India’s 1st indigenous vaccine against COVID-19. In November 2021, COVAXIN® received WHO EUL. The acquisition of Chiron Behring Vaccines has positioned Bharat Biotech as the world’s largest rabies vaccine manufacturer with Chirorab® and Indirab®. To learn more about Bharat Biotech, visit www.bharatbiotech.com

Cautionary Note on Forward-Looking Statements

This press release contains forward-looking statements within the meaning of The Private Securities Litigation Reform Act of 1995, which are subject to risks and uncertainties. Such forward-looking statements within this press release include, without limitation, Ocugen’s plans with respect to development and commercialization of COVAXIN™ in Mexico. Ocugen may, in some cases, use terms such as “predicts,” “believes,” “potential,” “proposed,” “continue,” “estimates,” “anticipates,” “expects,” “plans,” “intends,” “may,” “could,” “might,” “will,” “should,” or other words that convey uncertainty of future events or outcomes to identify these forward-looking statements. Such statements are subject to numerous important factors, risks and uncertainties that may cause actual events or results to differ materially from our current expectations, such as market and other conditions. These and other risks and uncertainties are more fully described in Ocugen’s periodic filings with the Securities and Exchange Commission (the “SEC”), including the risk factors described in the section entitled “Risk Factors” in the quarterly and annual reports that we file with the SEC. Any forward-looking statements that Ocugen makes in this press release speak only as of the date of this press release. Except as required by law, Ocugen assumes no obligation to update forward-looking statements contained in this press release whether as a result of new information, future events or otherwise, after the date of this press release.

Ocugen Contact:

Ken Inchausti

Head, Investor Relations & Communications

ken.inchausti@ocugen.com

Please submit investor-related inquiries to: IR@ocugen.com