Joe Gomes, Managing Director, Equity Research Analyst, Generalist , Noble Capital Markets, Inc.

Joshua Zoepfel, Research Associate, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

New Awards. Orion has been the recipient of two significant awards from the Army Corps of Engineers in the last two days, according to the DoD. Together, the new awards represent some $58 million of new dredging business, which typically has had an outsized impact on profit. We are encouraged by the recent awards and are hopeful proposal and award activity from the Corps ramps up to more historic levels.

Contract One. Last night, the DoD, in its daily contract awards press release, noted that Orion Marine Construction Inc., Tampa, Florida, was awarded a $40 million firm-fixed-price contract for Atchafalaya Basin, Gulf Intracoastal Waterway dredging. Work locations and funding will be determined with each order, with an estimated completion date of July 27, 2025.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

Mark Reichman, Managing Director, Equity Research Analyst, Natural Resources, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

Douay first phase deep drilling program. Maple Gold Mines released complete gold assay results from the first phase of deep drilling at the Douay Gold Project which is held in a 50/50 joint venture between the company and Agnico Eagle Mines Limited (NYSE: AEM). During the first half of 2023, the joint venture completed a total of 5,793 meters of drilling in three new holes and two extension holes. The deep drilling program is intended to test the potential for a much larger gold system at Douay while demonstrating continuity of mineralization beneath the currently defined mineral resource.

All five drill holes intersected gold mineralization. All five drill holes intersected gold mineralization greater than 1 gram of gold per tonne, with 10 intercepts greater than 2.5 grams of gold per tonne and several broad low-grade intervals averaging 0.1 to 0.3 grams of gold per tonne. The drilling affirmed the continuity of the gold system down to at least approximately 1,600 meters vertical depth or up to four times deeper than Douay’s currently defined mineral resources.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

Lee Enterprises, Incorporated provides local news, information, and advertising primarily in midsize markets in the United States. It publishes 49 daily newspapers, as well as offers 300 weekly newspapers and specialty publications in 23 states. The company also provides online advertising and services; and online infrastructure and online publishing services for approximately 1,500 daily and weekly newspapers and shoppers. In addition, it offers commercial printing services. The company has a strategic alliance with Yahoo!, Inc. to provide its classified employment advertising customer base the opportunity to post job listings and other employment products on Yahoo!�s HotJobs national platform. Lee Enterprises, Incorporated was founded in 1890 and is based in Davenport, Iowa.

Michael Kupinski, Director of Research, Equity Research Analyst, Digital, Media & Technology , Noble Capital Markets, Inc.

Patrick McCann, CFA, Research Analyst, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

Solid Q3 results. The company reported fiscal Q3 revenue and adj. EBITDA slightly below our expectations. Revenue was $171.3 million and adj. EBITDA was $23.2 million, compared with our estimates of $174.0 million and $25.6 million, respectively. Revenue was impacted by self induced cuts in its print business, the savings of which will flow through fiscal 2024 as well. While Q3 results were slightly lower than our estimates, we view the quarter favorably given strong digital revenue growth of 14.8% and improved print margins.

Strong digital growth. The company’s digital business had another strong quarter, with total digital revenue growing a strong 14.8%, comprising 41% of total company revenues. Notably, the company has been leading the industry in digital subscriber growth for the last 14 quarters, growing at a CAGR of 44%. Digital subscribers reached 606,000 and subscription revenue grew 43% from the prior year period. In our view, its goals of 900,000 Digital subscribers and $100 million in Digital subscription revenue by 2026 appears well within its reach.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

ISG (Information Services Group) (Nasdaq: III) is a leading global technology research and advisory firm. A trusted business partner to more than 700 clients, including more than 75 of the world’s top 100 enterprises, ISG is committed to helping corporations, public sector organizations, and service and technology providers achieve operational excellence and faster growth. The firm specializes in digital transformation services, including automation, cloud and data analytics; sourcing advisory; managed governance and risk services; network carrier services; strategy and operations design; change management; market intelligence and technology research and analysis. Founded in 2006, and based in Stamford, Conn., ISG employs more than 1,300 digital-ready professionals operating in more than 20 countries—a global team known for its innovative thinking, market influence, deep industry and technology expertise, and world-class research and analytical capabilities based on the industry’s most comprehensive marketplace data. For additional information, visit www.ISG-One.com

Joe Gomes, Managing Director, Equity Research Analyst, Generalist , Noble Capital Markets, Inc.

Joshua Zoepfel, Research Associate, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

Record 2Q23 Top Line. Record 2Q revenueof $74.6 million, up 5.5% y-o-y. Currency translation negatively impacted reported revenue by $0.1 million. By geography, Americas revenue rose 7% to $42.3 million, Europe was up 5% on a reported basis to $24.4 million, and Asia-Pacific revenue of $8 million was flat to the prior year. We were at $75 million.

Increasing Recurring Revenues. Strong demand for research and platform services in the second quarter led to 21% growth in recurring revenues, which now represent more than 40% of Company revenue. ISG’s mix of portfolio solutions and services around cost optimization and digital transformation continues to resonate with clients.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

Haynes International, Inc. is a leading developer, manufacturer and marketer of technologically advanced, nickel and cobalt-based high-performance alloys, primarily for use in the aerospace, industrial gas turbine and chemical processing industries.

Mark Reichman, Managing Director, Equity Research Analyst, Natural Resources, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

Third quarter financial results. Haynes International reported third quarter fiscal 2023 net income of $8.8 million or $0.68 per share compared to $15.6 million or $1.24 per share during the prior year period and $12.3 million or $0.96 per share during the prior quarter. We had forecast net income of $8.5 million or $0.67 per share. Revenues of $143.9 million increased 10.6% on a year-over-year basis but declined 5.8% compared to the prior quarter. A June cybersecurity incident negatively impacted net revenues by an estimated $18 to $20 million and earnings per share by $0.40 to $0.45. Earnings were also negatively impacted by raw material fluctuations, primarily for cobalt, which resulted in a $0.09 per share impact. The prior year period benefited from a raw material tailwind of $0.25 per diluted share.

Growing order backlog. Orders during the quarter resulted in a record backlog of $468.1 million as of June 30th and represented a 4.8% increase compared to the prior quarter and a 38.4% increase on a year-over-year basis. Backlog pounds increased 3.2% during the third quarter to approximately 14.6 million pounds and increased 20.7% compared to the prior year period driven by strong demand in the aerospace and industrial gas turbine markets.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

Entravision Communications Corporation is a diversified Spanish-language media company utilizing a combination of television and radio operations to reach Hispanic consumers across the United States, as well as the border markets of Mexico. Entravision owns and/or operates 53 primary television stations and is the largest affiliate group of both the top-ranked Univision television network and Univision’s TeleFutura network, with television stations in 20 of the nation’s top 50 Hispanic markets. The Company also operates one of the nation’s largest groups of primarily Spanish-language radio stations, consisting of 48 owned and operated radio stations.

Michael Kupinski, Director of Research, Equity Research Analyst, Digital, Media & Technology , Noble Capital Markets, Inc.

Patrick McCann, CFA, Research Analyst, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

Mixed Q2 results. While revenues beat expectations ($273.4 million versus our $262.9 million estimate), adj. EBITDA was 13% lower than expected ($14.2 million versus our $16.4 million estimate). The revenue variance was due to its Digital revenue, $10 million above our expectations. Notably, the biggest adj. EBITDA variance was due to lower margins in its Digital Media segment.

A Facebook faceplant. The company’s Digital Media margins going forward will be adversely affected by Meta (Facebook) is reducing Entravision’s commission revenue, from 10% to 7%. We estimate that this will adversely affect the company by over $8 million in adj. EBITDA in the second half 2023. While margins will take a hit, the company’s Digital Media revenue growth appears favorable and adj. EBITDA is expected to grow strong double digits in 2024.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

FAT Brands (NASDAQ: FAT) is a leading global franchising company that strategically acquires, markets, and develops fast casual, quick-service, casual dining, and polished casual dining concepts around the world. The Company currently owns 17 restaurant brands: Round Table Pizza, Fatburger, Marble Slab Creamery, Johnny Rockets, Fazoli’s, Twin Peaks, Great American Cookies, Hot Dog on a Stick, Buffalo’s Cafe & Express, Hurricane Grill & Wings, Pretzelmaker, Elevation Burger, Native Grill & Wings, Yalla Mediterranean and Ponderosa and Bonanza Steakhouses, and franchises and owns over 2,300 units worldwide. For more information on FAT Brands, please visit www.fatbrands.com.

Joe Gomes, Managing Director, Equity Research Analyst, Generalist , Noble Capital Markets, Inc.

Joshua Zoepfel, Research Associate, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

2Q23 Results. FAT Brands reported 2Q23 revenue of $106.8 million, up 3.9% y-o-y from $102.8 million in the year ago quarter. System-wide sales growth was 1.7%. Same Store Sales were up 1.9%. FAT reported adjusted EBITDA of $23.1 million in the quarter, compared to $29.5 million in 2Q22. Net loss for the quarter was $7.1 million, or $0.53/sh, compared to a net loss of $9.8 million, or $0.60/sh last year. Adjusted net income for the quarter was $3.0 million, or EPS of $0.08/sh, compared to a net loss of $3.1 million, or a loss of $0.29/sh, last year. We had projected revenue of $106.8 million and a net loss of $26 million, or a loss of $1.57/sh.

Development Continues. YTD, FAT has opened 66 restaurants, including 25 in 2Q and the Company remains on track to open 175 locations in 2023. YTD, over 150 new franchise agreements have been signed, bringing the total pipeline to over 1,100 signed agreements.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

DLH delivers improved health and readiness solutions for federal programs through research, development, and innovative care processes. The Company’s experts in public health, performance evaluation, and health operations solve the complex problems faced by civilian and military customers alike, leveraging digital transformation, artificial intelligence, advanced analytics, cloud-based applications, telehealth systems, and more. With over 2,300 employees dedicated to the idea that “Your Mission is Our Passion,” DLH brings a unique combination of government sector experience, proven methodology, and unwavering commitment to public health to improve the lives of millions. For more information, visit www.DLHcorp.com.

Joe Gomes, Managing Director, Equity Research Analyst, Generalist , Noble Capital Markets, Inc.

Joshua Zoepfel, Research Associate, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

Standing Ready. With its acquisitions of S3, IBA, and, most recently GRSi, DLH has truly morphed into a one stop shop platform to address a broader range of client’s solution needs with expertise in science, research and development, systems engineering, and integration.

Promising Pipeline. Although the contract award environment continues to experience some headwinds, there does appear to be some movement both with anticipated proposals from previously won ID/IQ contracts as well as normal ongoing business. Overall, we believe there is significant demand from its clients for the services DLH provides.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

Beasley Broadcast Group, Inc. owns and operates 61 stations (47 FM and 14 AM) in 15 large- and mid-size markets in the United States. Approximately 20 million consumers listen to the Company’s radio stations weekly over-the-air, online and on smartphones and tablets, and millions regularly engage with the Company’s brands and personalities through digital platforms such as Facebook, Twitter, text messaging, digital and web applications and email. The Overwatch League’s Houston Outlaws esports team is a wholly owned subsidiary. The Company also owns BeasleyXP, a national esports content hub, and AXLR-R8, a Rocket League Championship Series team, in its esports portfolio. For more information, please visit www.bbgi.com.

Michael Kupinski, Director of Research, Equity Research Analyst, Digital, Media & Technology , Noble Capital Markets, Inc.

Jacob Mutchler, Research Associate, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

Solid Q2 results. The company reported revenue of $63.5 million, in-line with our estimate of $63.7 million. Adj. EBITDA of $7.7 million, beat our estimate of $6.5 million by 18.2%. Notably, the quarter was driven by strong digital revenue growth of14.8% and cash flow was supported by meaningful cost reductions and permanently reduced headcount.

Strong digital growth. The bulk of digital revenue growth in the quarter came from high margin content creation on the company’s owned and operated platforms. Importantly, Q2 digital accounted for 19.4% of total revenue, only slightly below management’s target of 20% to 30% for full year 2023.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

DeSantis Thinks the Federal Reserve, Elitists, and China, Should all Have Less Power in Our Financial Lives

Federal Reserve Chairman Jerome Powell, appointed by President Trump, then reappointed by President Biden recently got a lot of attention from Florida governor and presidential hopeful Ron DeSantis – and it wasn’t the kind of attention someone in Powell’s position would welcome. This week, in his first big speech on the economy, DeSantis separated himself from the top candidates from each political party by vowing to “rein in” the Fed.

The platform DeSantis unveiled this week helps establish his position and puts a face on his campaign that is decidedly above the culture wars of other political campaigns. It also creates a clear difference in economic issues between himself and his party’s frontrunner, also from Florida, Donald Trump.

In a campaign speech in New Hampshire, DeSantis blamed the US central bank for high inflation, and its dipping a toe into social policy. He was also very critical of the Fed considering a digital dollar that would compete with private crypto, which the candidate does not oppose.

The overall tone as he began to lay out his economic agencda, was one of looking to curb the power of large corporations, limit ties to China, and stand against powerful elites. “We need to rein in the Federal Reserve. It is not designed or supposed to be an economic central planner. It is not supposed to be indulging in social justice or social engineering,” the governor said. He continued, “It’s got one job, maintaining stable prices, and it has departed from that with what it’s done over the past many years.”

Coming to Florida this December is the premier investor conference, NobleCon19. You’re invited to join over 100 company executives and investors from around the globe as they seek better understanding of opportunities direct from senior management, then network in an environment that fosters making great contacts.

As statements that could be taken as a shot at the current Fed chairman, DeSantis said he would not likely support another term for Powell. “I will appoint a Chair of the Federal Reserve who understands the limited role that it has and focuses on making sure that prices are stable for American businesses and consumers, said DeSantis.

What seemed to be his biggest gripe with how the Federal Reserve has been run is with monetary policy. He believes that policy was kept too easy for too long after the financial crisis and pandemic. He believes this contributed to the high inflation, which forced a rapid tightening from policy makers.

The popular governor of the third most populace state, also railed against the Fed’s steps toward creating a central bank digital currency (CBDC), saying it was trying to crush financial liberty and seize more control over financial transactions.

“Why did they want this? They want to go to a cashless society. They want to eliminate cryptocurrency and they want all the transactions to go through this central bank digital currency,” DeSantis proclaimed.

The DeSantis economic vision, as described, was consistent with his reputation as Florida’s executive which is one that stands against the abuses of government power and big business. “We cannot have policy that kowtows to the largest corporations and Wall Street at the expense of small businesses and average Amerricans.” He continued, “There is a difference between a free-market economy, which we want, and corporatism in which the rules are jiggered to be able to help incumbent companies.”

He also expressed concern over loss of economic sovereignty sharply saying, “We have to restore the economic sovereignty of this country and take back control of our economy from China. This abusive relationship between two countries, must come to an end.”

Take Away

DeSantis is on the road, both showing he has an understanding of economics and unveiling a plan that is distinct from the top two candidates, both of which have already occupied the White House. DeSantis is being watched very closely by both political parties as he is a very popular governor with a lot of admiration and a large following. Florida remains a beneficiary of the large migration of businesses and families out of other states looking for a more innovative, fiscally responsible, less constricting place to live and do business.

Plans for the Platform Formerly Known as “Twitter”

Elon Musk, who counts the old Twitter among the companies he oversees, has plans for a mega-financial component to the social media platform that has been rebranded as X. The serial entrepreneur has in the past discussed the “everything” app WeChat as a model for X’s direction. WeChat is a product available to banking clients in China, as a useful do-it-all tool chest. Musk says it has no equal in the U.S. Part of what is expected from Elon’s team is enabling users of X to trade stock and cryptocurrencies and also perform all that fintech companies like PayPal provide.

Embracing a New Direction

Molding X into the ultimate multi-functional app may be beginning to take shape and gain momentum. Musk may not have invented Twitter, but he plans on reinventing it with some very aggressive plans under the new name.

Evidence of this comes from Musk and his team’s discussions with a prominent financial data powerhouse to establish a trading hub within the X platform, including real-time market data. Leaked documents, as reported by the news source Semafor, and conversations with insiders have revealed the huge initiative. It is unclear whether X has secured partnerships for its additional direction at this point.

Fuzzy Business Benefit to Partnerships

X’s outreach to potential partners highlights the company’s promise of access to a massive social media user base numbering in the hundreds of millions. The proposal requests don’t mention compensation for the project, according to Liz Hoffman at Semafor.

Plans of incorporating a trading hub within the X platform have been brought up in the past. Not long ago eTORO, a unique social investment platform, had unveiled plans to facilitate the trading of various assets, including cryptocurrencies, directly to users, through a strategic partnership of what was then Twitter.

If the plans for an in-app trading hub materialize, given Musk’s evident familiarity with Dogecoin and other digital assets, X could potentially become a hub for cryptocurrency trading. Much of the the crypto regulatory world is still being written on a battlefield by various parties with different interests. This prospect might extend to established cryptocurrencies like bitcoin (BTC), which could be perceived as a relatively secure asset within some regulatory frameworks.

Elon Musk’s innovative drive is propelling X towards uncharted territory. As the app evolves, the prospect of a comprehensive trading hub integrated seamlessly within the platform could redefine the way users engage with their finances and investments. While details are understandably not public, knowledge that this may be unfolding and the potential power and disruption it may create are undeniable.

In a reply to a social post on X by @unusual_whales which read, “Twitter/X is planning to launch its own stock trading platform, per XNewsDaily,” Musk did not completely dismiss the existence of any plans but did not in any way confirm that there has been any real movement in this direction.

Company to host conference call and webcast at 4:30 p.m. ET on Thursday, August 10, 2023

NEWTOWN, Pa., Aug. 03, 2023 (GLOBE NEWSWIRE) — Onconova Therapeutics, Inc. (NASDAQ: ONTX), (“Onconova” or “the Company”), a clinical-stage biopharmaceutical company focused on discovering and developing novel products for patients with cancer, today announced that the Company intends to release its second quarter 2023 financial results on Thursday, August 10, 2023. Management plans to host a conference call and live webcast at 4:30 p.m. ET on the same day to discuss these results and provide an update on its pipeline programs.

Conference Call and Webcast Information

Interested parties who wish to participate in the conference call may do so by dialing:

(800) 715-9871 for domestic and

(646) 307-1963 for international callers and

Using conference ID 9506701.

Those interested in listening to the conference call via the internet may do so by visiting the investors and media page on the Company’s website at www.onconova.com and clicking on the webcast link. In addition to the live webcast, a replay will be available on the Onconova website for 90 days following the call.

About Onconova Therapeutics, Inc. Onconova Therapeutics is a clinical-stage biopharmaceutical company focused on discovering and developing novel products for patients with cancer. The Company has proprietary targeted anti-cancer agents designed to disrupt specific cellular pathways that are important for cancer cell proliferation.

Onconova’s novel, proprietary multi-kinase inhibitor narazaciclib (formerly ON 123300) is being evaluated in a Phase 1/2 combination trial with the estrogen blocker, letrozole, in advanced low grade endometrial cancer (NCT05705505). Based on preclinical and clinical studies of CDK 4/6 inhibitors, Onconova is also evaluating opportunities for combination studies with narazaciclib in additional indications.

Onconova’s product candidate rigosertib is being studied in multiple investigator-sponsored studies. These studies include a dose-escalation and expansion Phase 1/2a study of oral rigosertib in combination with nivolumab in patients with KRAS+ non-small cell lung cancer (NCT04263090), a Phase 2 program evaluating oral or IV rigosertib monotherapy in advanced squamous cell carcinoma complicating recessive dystrophic epidermolysis bullosa (RDEB-associated SCC (NCT03786237, NCT04177498), and a Phase 2 trial evaluating rigosertib in combination with pembrolizumab in patients with metastatic melanoma(NCT05764395).

Forward Looking Statements Some of the statements in this release are forward-looking statements within the meaning of Section 27A of the Securities Act of 1933, as amended, Section 21E of the Securities Exchange Act of 1934, as amended, and the Private Securities Litigation Reform Act of 1995, and involve risks and uncertainties. These statements relate to Onconova’s expectations regarding its clinical development and trials, its product candidates and its business and financial position. Onconova has attempted to identify forward-looking statements by terminology including “believes,” “estimates,” “anticipates,” “expects,” “plans,” “intends,” “may,” “could,” “might,” “will,” “should,” “preliminary,” “encouraging,” “approximately” or other words that convey uncertainty of future events or outcomes. Although Onconova believes that the expectations reflected in such forward-looking statements are reasonable as of the date made, expectations may prove to have been materially different from the results expressed or implied by such forward-looking statements. These statements are only predictions and involve known and unknown risks, uncertainties, and other factors, including the success and timing of Onconova’s clinical trials, investigator-sponsored trials, regulatory agency and institutional review board approvals of protocols, Onconova’s collaborations, market conditions and those discussed under the heading “Risk Factors” in Onconova’s most recent Annual Report on Form 10-K and quarterly reports on Form 10-Q. Any forward-looking statements contained in this release speak only as of its date. Onconova undertakes no obligation to update any forward-looking statements contained in this release to reflect events or circumstances occurring after its date or to reflect the occurrence of unanticipated events.

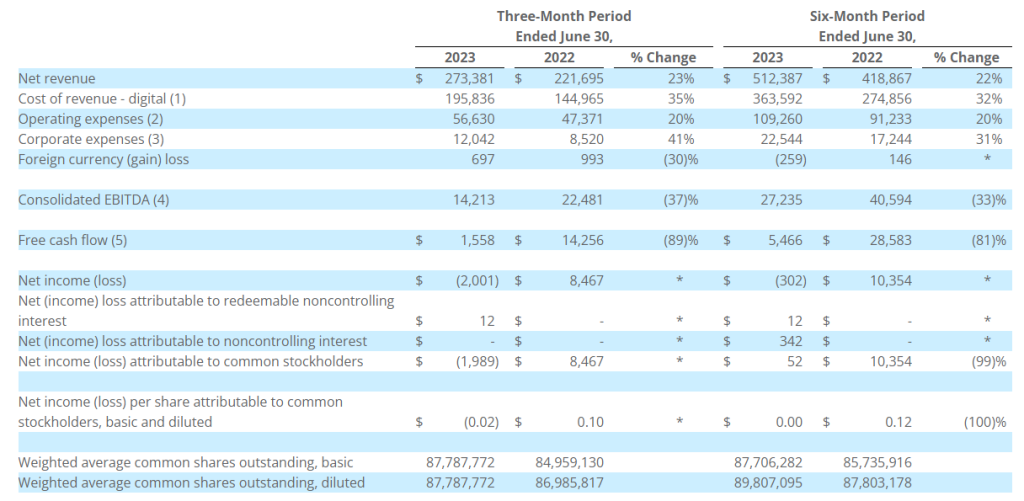

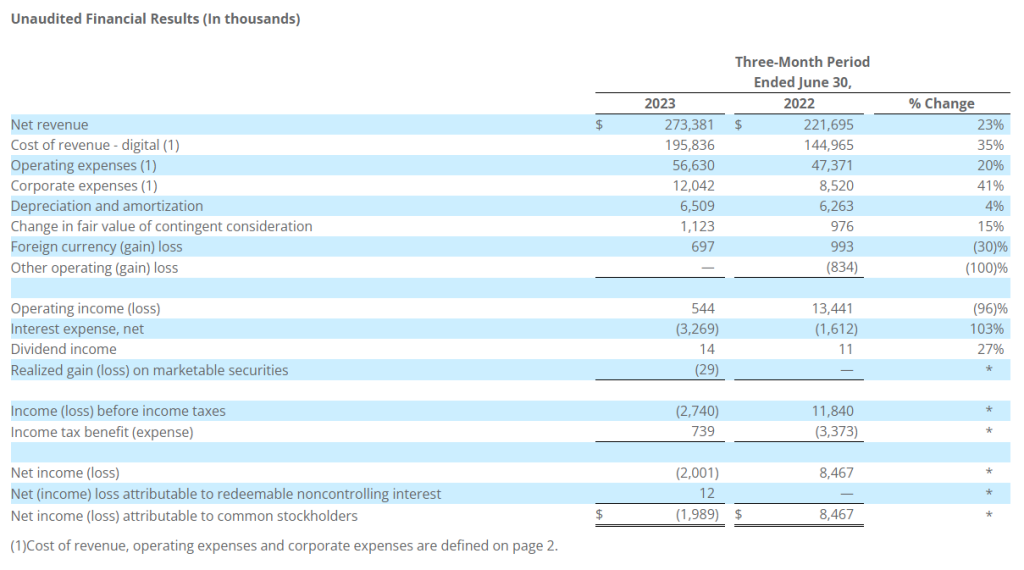

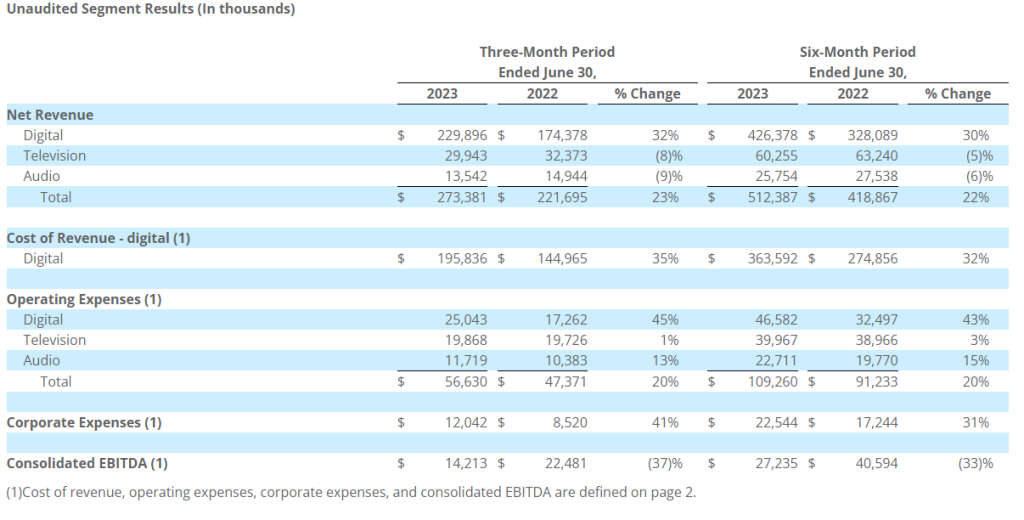

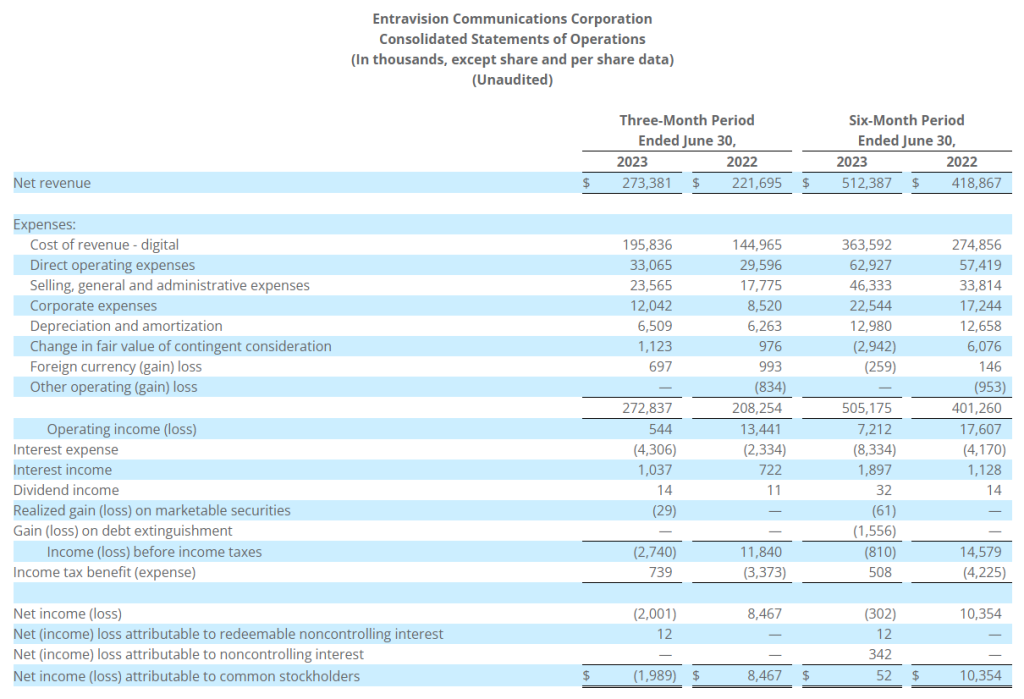

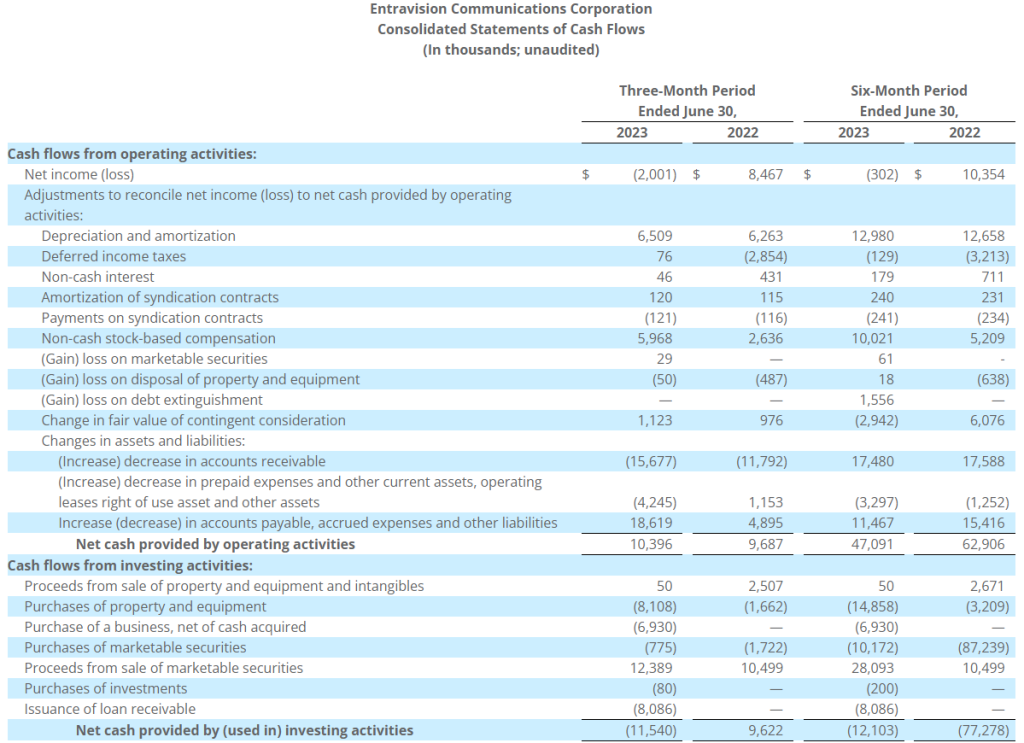

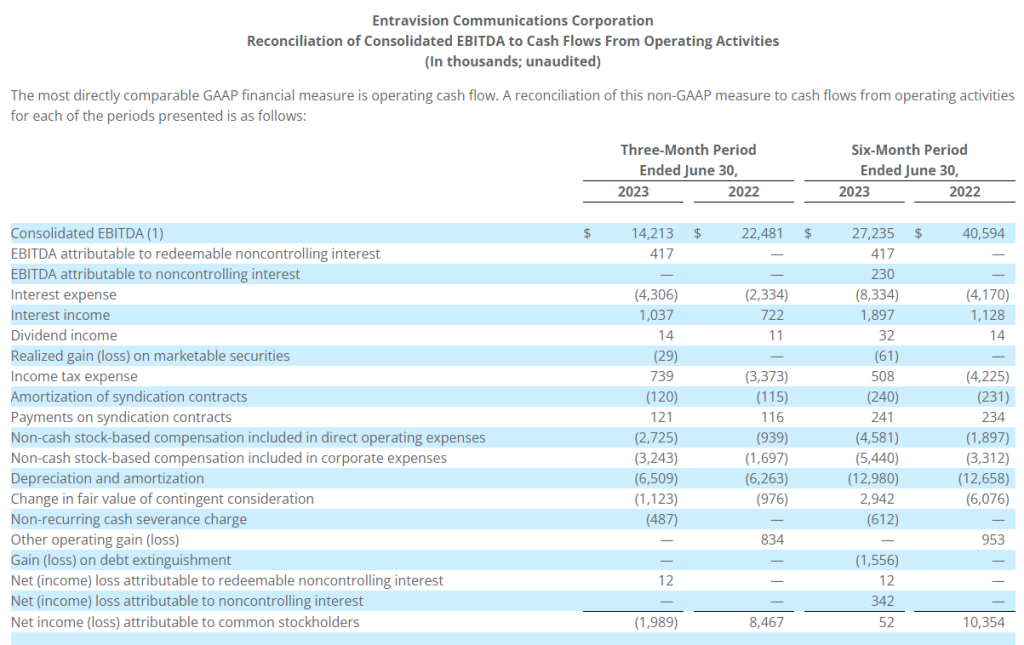

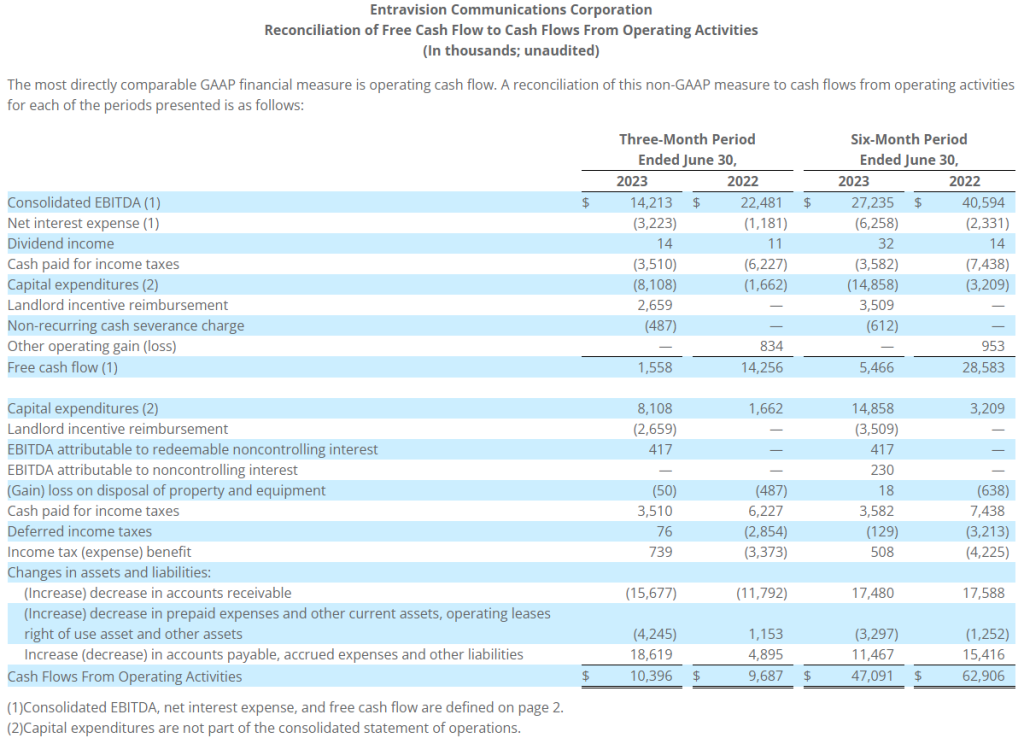

SANTA MONICA, Calif.–(BUSINESS WIRE)– Entravision Communications Corporation (NYSE: EVC), a leading global advertising solutions, media and technology company, today announced financial results for the three- and six-month periods ended June 30, 2023.

Second Quarter 2023 Highlights

Record quarterly advertising revenue

Net revenue up 23% over the prior-year quarter

Net loss attributable to common stockholders of $2.0 million compared to net income attributable to common stockholders of $8.5 million in the prior-year quarter

Consolidated EBITDA down 37% compared to the prior-year quarter

Operating cash flow up 7% over the prior-year quarter

Free cash flow down 89% compared to the prior-year quarter

Quarterly cash dividend of $0.05 per share

“We delivered another strong quarter at Entravision with record quarterly revenue of $273.4 million, increasing 23% year-over-year,” said Chris Young, Chief Financial Officer. “While elevated operating expenses led to a decline in adjusted EBITDA, we remain focused on managing expenses and leveraging our strong balance sheet to ensure we are well-positioned to grow in the current macroeconomic environment. We were also excited to welcome Michael Christenson as our new CEO at the beginning of July. We look forward to continuing to drive growth under his leadership.”

Quarterly Cash Dividend

The Company announced today that its Board of Directors approved a quarterly cash dividend to shareholders of $0.05 per share on the Company’s Class A and Class U common stock, in an aggregate amount of $4.4 million. The quarterly dividend will be payable on September 29, 2023 to shareholders of record as of the close of business on September 15, 2023, and the common stock will trade ex-dividend on September 14, 2023. The Company currently anticipates that future cash dividends will be paid on a quarterly basis; however, any decision to pay future cash dividends will be subject to approval by the Board.

Non-GAAP Financial Measures

This press release contains certain non-GAAP financial measures as defined by SEC Regulation G. The GAAP financial measure most directly comparable to each of these non-GAAP financial measures, and a table reconciling each of these non-GAAP financial measures to its most directly comparable GAAP financial measure is included beginning on page 10.

Net revenue in the second quarter of 2023 totaled $273.4 million, up 23% from $221.7 million in the prior-year period. Of the overall increase, $55.5 million was attributable to our digital segment and was primarily due to advertising revenue growth from our digital commercial partnerships business, and due to various acquisitions, which did not contribute to our financial results in our digital segment in the comparable period. The overall increase was partially offset by a decrease of $2.5 million attributable to our television segment, primarily due to decreases in political advertising revenue and national advertising revenue, partially offset by increases in local advertising revenue, spectrum usage rights revenue and retransmission consent revenue. In addition, the overall increase was partially offset by a decrease of $1.4 million attributable to our audio segment, primarily due to a decrease in political advertising revenue, and decreases in local and national advertising revenue.

Cost of revenue in the second quarter of 2023 totaled $195.8 million, up 35% from $145.0 million in the prior-year period. The increase was primarily due to increased cost of revenue related to advertising revenue growth from our digital commercial partnerships business, and due to various acquisitions, which did not contribute to our financial results in our digital segment in the comparable period.

Operating expenses in the second quarter of 2023 totaled $56.6 million, up 20% from $47.4 million in the prior-year period. Of the overall increase, $7.8 million was attributable to our digital segment and was primarily due to an increase in non-cash stock-based compensation, which is mainly a result of the timing of the 2023 annual restricted stock unit (“RSU”) grant to certain employees, which was made in February 2023 compared to the 2022 annual grant, which was made in December 2022, and due to an increase in expenses associated with the increase in digital advertising revenue, an increase in salary expense, and due to various acquisitions, which did not contribute to our financial results in our digital segment in the comparable period. Additionally, of the overall increase in operating expenses, $0.1 million was attributable to our television segment primarily due to an increase in non-cash stock-based compensation, which is mainly a result of the 2023 annual RSU grant timing mentioned above, partially offset by a decrease in bad debt expense. In addition, of the overall increase in operating expenses, $1.3 million was attributable to our audio segment primarily due to an increase in non-cash stock-based compensation, which is mainly a result of the 2023 annual RSU grant timing mentioned above, and due to an increase in salaries and increased rent expense in the temporary office space until the move to our new permanent offices, which was completed in June 2023.

Corporate expenses in the second quarter of 2023 totaled $12.0 million, up 41% from $8.5 million in the prior-year period. The increase was primarily due to an increase in non-cash stock-based compensation, which is mainly a result of the 2023 annual RSU grant timing mentioned above, and increases in professional service fees.

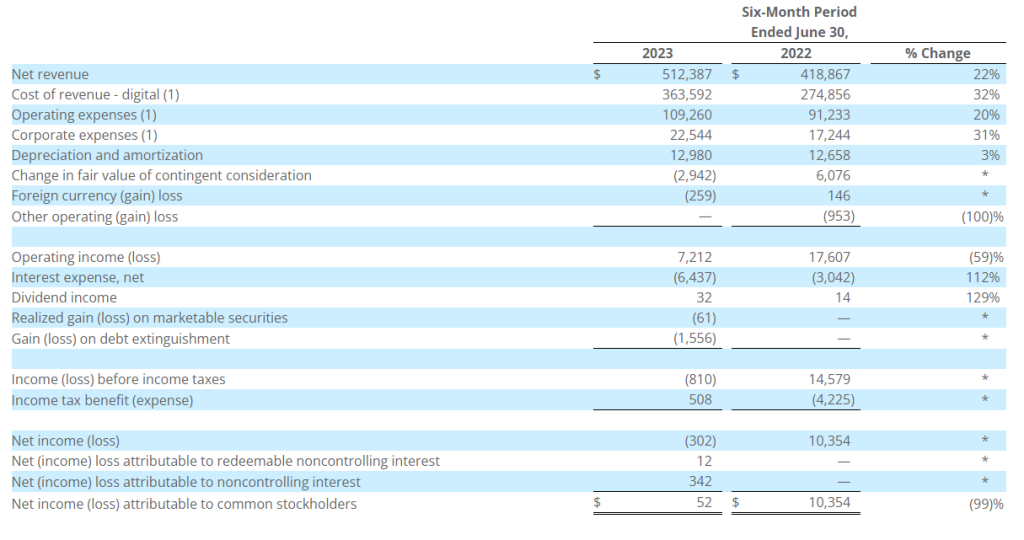

Net revenue for the six-month period of 2023 totaled $512.4 million, up 22% from $418.9 million in the prior-year period. Of the overall increase, $98.3 million was attributable to our digital segment and was primarily due to advertising revenue growth from our digital commercial partnerships business, and due to various acquisitions, which did not contribute to our financial results in our digital segment in the comparable period. The overall increase was partially offset by a decrease of $2.9 million attributable to our television segment, primarily due to decreases in political advertising revenue and national advertising revenue, partially offset by increases in local advertising revenue, spectrum usage rights revenue and retransmission consent revenue. In addition, the overall increase was partially offset by a decrease of $1.7 million attributable to our audio segment, primarily due to a decrease in political advertising revenue, and decreases in local and national advertising revenue.

Cost of revenue for the six-month period of 2023 totaled $363.6 million, up 32% from $274.9 million in the prior-year period. The increase was primarily due to increased cost of revenue related to advertising revenue growth from our digital commercial partnerships business, and due to various acquisitions, which did not contribute to our financial results in our digital segment in the comparable period.

Operating expenses for the six-month period of 2023 totaled $109.3 million, up 20% from $91.2 million in the prior-year period. Of the overall increase, $14.1 million was attributable to our digital segment and was primarily due to an increase in non-cash stock-based compensation, which is mainly a result of the 2023 annual RSU grant timing mentioned above, and due to an increase in expenses associated with the increase in digital advertising revenue, an increase in salary expense, and due to various acquisitions, which did not contribute to our financial results in our digital segment in the comparable period. Additionally, of the overall increase in operating expenses, $1.0 million was attributable to our television segment primarily due to an increase in non-cash stock-based compensation, which is mainly a result of the 2023 annual RSU grant timing mentioned above. In addition, of the overall increase in operating expenses, $2.9 million was attributable to our audio segment primarily due to an increase in non-cash stock-based compensation, which is mainly a result of the 2023 annual RSU grant timing mentioned above, and due to an increase in salaries and increased rent expense in the temporary office space until the move to our new permanent offices, which was completed in June 2023.

Corporate expenses for the six-month period of 2023 totaled $22.5 million, up 31% from $17.2 million in the prior-year period. The increase was primarily due to an increase in non-cash stock-based compensation, which is mainly a result of the 2023 annual RSU grant timing mentioned above, and increases in professional service fees, audit fees and rent expense.

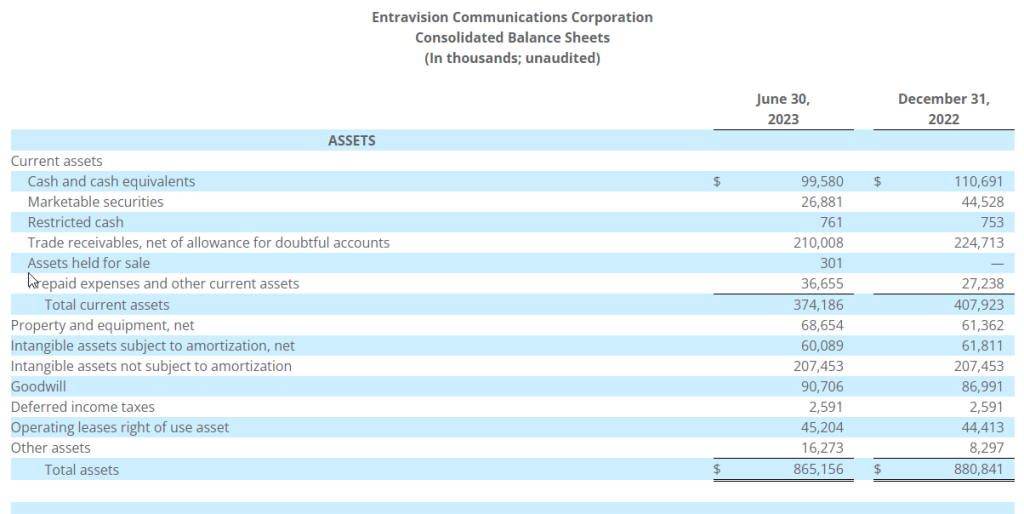

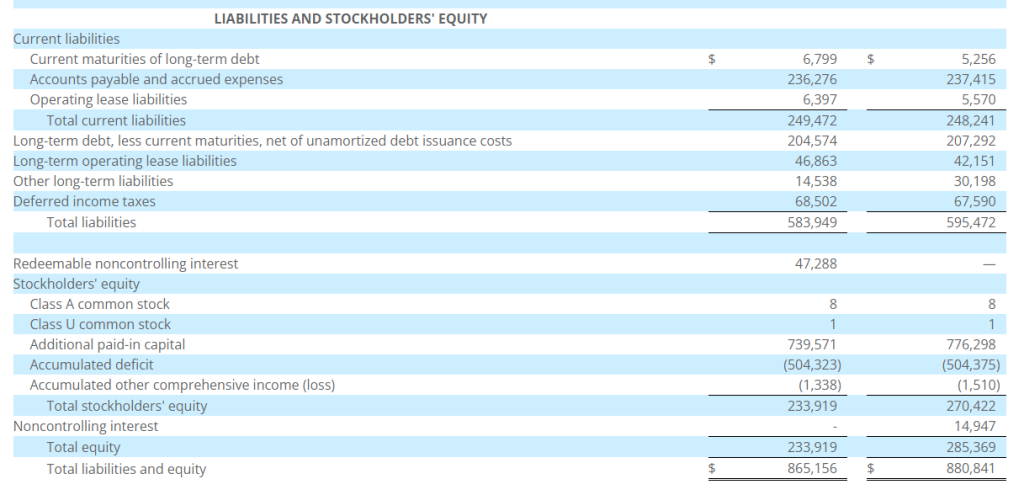

Balance Sheet and Related Metrics

Cash and marketable securities as of June 30, 2023 totaled $126.5 million. Total debt under the Company’s credit agreement was $210.3 million. Net of $50 million of cash and marketable securities, total leverage as defined in the Company’s credit agreement was 1.8 times as of June 30, 2023. Net of total cash and marketable securities, total leverage was 1.0 times.

Notice of Conference Call

Entravision Communications Corporation will hold a conference call to discuss its second quarter 2023 results on Thursday, August 3, 2023 at 5:00 p.m. Eastern Time. To access the conference call, please dial (844) 836-8739 (U.S.) or (412) 317-5440 (Int’l) ten minutes prior to the start time and reference Conference ID number 10180063. The call will also be available via live webcast on the investor relations portion of the Company’s website located at www.entravision.com.

About Entravision Communications Corporation

Entravision is a global advertising solutions, media and technology company. Over the past three decades, we have strategically evolved into a digital powerhouse, expertly connecting brands to consumers in the U.S., Latin America, Europe, Asia and Africa. Our digital segment, the company’s largest by revenue, offers a full suite of end-to-end advertising services in 40 countries. We have commercial partnerships with Meta, X Corp. (formerly known as Twitter), TikTok, and Spotify, and marketers can use our Smadex and other platforms to deliver targeted advertising to audiences around the globe. In the U.S., we maintain a diversified portfolio of television and radio stations that target Hispanic audiences and complement our global digital services. Entravision remains the largest affiliate group of the Univision and UniMás television networks. Shares of Entravision Class A Common Stock trade on the NYSE under ticker: EVC. Learn more about our offerings at entravision.com or connect with us on LinkedIn and Facebook.

Forward-Looking Statements

This press release contains certain forward-looking statements. These forward-looking statements, which are included in accordance with the safe harbor provisions of the Private Securities Litigation Reform Act of 1995, may involve known and unknown risks, uncertainties and other factors that may cause the Company’s actual results and performance in future periods to be materially different from any future results or performance suggested by the forward-looking statements in this press release. Although the Company believes the expectations reflected in such forward-looking statements are based upon reasonable assumptions, it can give no assurance that actual results will not differ materially from these expectations, and the Company disclaims any duty to update any forward-looking statements made by the Company. From time to time, these risks, uncertainties and other factors are discussed in the Company’s filings with the Securities and Exchange Commission.

Christopher T. Young Chief Financial Officer and Treasurer Entravision Communications Corporation 310-447-3870