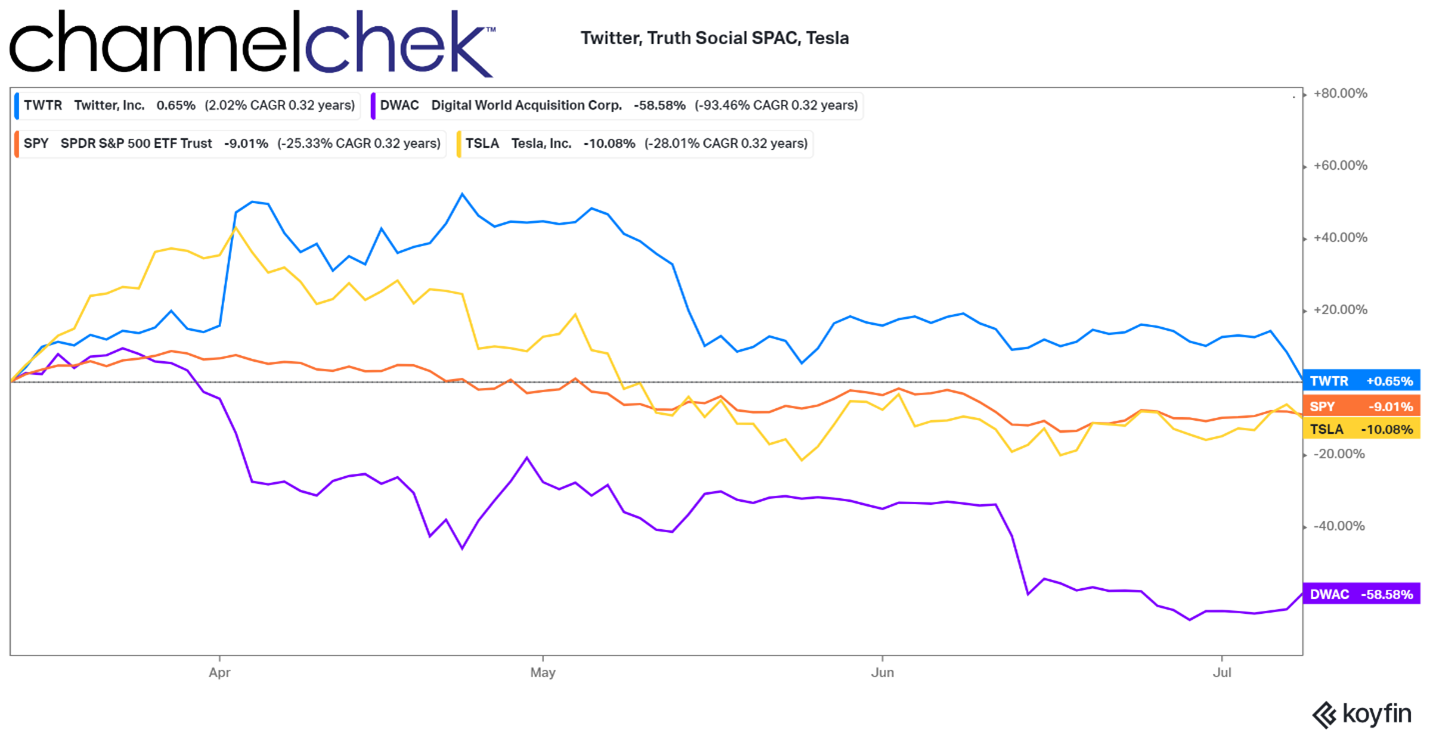

Tonix Pharmaceuticals Announces Development of TNX-601 ER, a Potential Abuse Deterrent, Extended-Release Formulation of Tianeptine Oxalate for the Treatment of Major Depressive Disorder

Research, News, and Market Data on Tonix Pharmaceuticals

Naloxone-Free

Formulation of Tianeptine is an Extended-Release Tablet that Includes Inactive

Ingredients and Compression Properties Designed to Confer Abuse Deterrence

Once-Daily Tablet Formulation

of Tianeptine is Bioequivalent to the Three Times a Day Antidepressant Marketed

in Europe for Over 30 years

Tianeptine’s Enhancement of

Neuroplasticity in Animal Models of Stress Implies a Distinct Indirect

Glutamatergic Mechanism of Action Relative to Antidepressants Marketed in the

U.S.

Planning to Initiate Enrollment

in U.S. Phase 2 Study in First Quarter 2023, Pending FDA Clearance of IND

CHATHAM, N.J., July 11, 2022 (GLOBE NEWSWIRE) — Tonix Pharmaceuticals Holding Corp. (Nasdaq: TNXP) (Tonix or the Company), a clinical-stage biopharmaceutical company, today announced development of TNX-601 ER (tianeptine oxalate extended-release tablets), a naloxone-free formulation of TNX-601 designed to confer abuse-deterrence, for the treatment of major depressive disorder (MDD)1. Tonix expects to initiate a Phase 2 study of TNX-601 ER for the treatment of MDD in the first quarter of 2023, pending U.S. Food and Drug Administration (FDA) clearance of its Investigational New Drug (IND) application.

Tonix’s TNX-601 ER is being developed as a treatment for MDD, posttraumatic stress disorder, and neurocognitive dysfunction associated with corticosteroid use. Tianeptine sodium (amorphous) immediate release (IR) tablets have been available in Europe and many countries in Asia and Latin America for the treatment of MDD over the more than three decades since it was first marketed in France in 1989. No tianeptine-containing product has been approved by the FDA. The proposed mechanism of action of TNX-601 ER is distinct from traditional monoaminergic antidepressants in the U.S. In addition to its glutamatergic properties central to its antidepressant effect, tianeptine has weak µ-opioid receptor agonist properties and has been linked to illicit misuse at much higher doses than those reported to be effective in the treatment of MDD2. Previously, Tonix was developing a naloxone-containing tablet, TNX-601 CR (tianeptine oxalate and naloxone controlled-release) for MDD, that was designed to mitigate the risk of parenteral abuse.

“TNX-601 ER is a naloxone-free tablet formulated with inactive ingredients that we believe will make the tablet more difficult to adulterate for misuse and abuse, while maintaining extended-release characteristics, even if the tablet is subjected to physical manipulation, and/or chemical extraction,” said Seth Lederman, M.D., President and Chief Executive Officer of Tonix Pharmaceuticals. “The potentially abuse deterrent ingredients include gel forming polymers which impede extraction, and excipients which cause nasal irritation. In addition, the tablet’s hardness makes it difficult to crush, cut or grind to fine particle size, which hinders efforts to misuse by insufflation or intravenous routes.”

“The efficacy of tianeptine sodium IR is comparable to both selective serotonin inhibitor (SSRI) and tricyclic antidepressants

3,4 while being associated with a low incidence of sexual dysfunction than either of those classes5,6, and no associated derangement of sleep architecture, sedation effects, weight gain, or cognitive impairment,7” said Gregory Sullivan, M.D., Chief Medical Officer of Tonix Pharmaceuticals. “Given tianeptine’s unique metabolic pathway, which is independent of the hepatic P450 system, we believe that TNX-601 ER has a reduced risk of drug-drug interactions compared to most antidepressants7. Tianeptine’s antidepressant activity is believed to relate to indirect modulation of the glutamatergic system. While it does not have measurable interactions with the NMDA, AMPA or kainate receptors, tianeptine is known to modulate AMPA receptor trafficking and to promote synaptic plasticity in hippocampus under conditions of stress or corticosteroid use. In animal models, tianeptine restores neuroplasticity and reverses stress-induced impairments in synaptic glutamate neurotransmission, which are perturbed in depression.8 Additionally, TNX-601 ER is designed for once daily dosing, which is believed to provide an adherence advantage relative to the three times per day dosing of the immediate-release sodium salt products available in Europe and other jurisdictions around the world.”

1TNX-601 ER is in the pre-IND (Investigational New Drug) stage of development and is not approved for any indication

2Lauhan, R., et al. Psychosomatics 2018, 59 (6), 547–553.

3Jeon, H. J., et al. .J. Clin. Psychopharmacol. 2014, 34 (2), 218–225.

4Emsley, R., et al. J. Clin. Psychiatry 2018, 79 (4)

5Bonierbale M, et al. Curr Med Res Opin 2003, 19(2):114-124.

6Costa e Silva, J. A., et al. Neuropsychobiology 1997, 35 (1), 24–29.

7Wagstaff, A. J. et al. CNS

Drugs 2001, 15 (3), 231–259.

8McEwen, B. S., et al. Mol.

Psychiatry 2010, 15 (3), 237–249.

About Depression

According to the National Institute of Mental Health, an estimated 21 million adults in the U.S. in 2020 experienced at least one major depressive episode1, with highest prevalence among individuals aged 18-25 at a rate of 17.0%. For approximately 2.5 million adults in the U.S., adjunctive therapies are necessary for depression treatment.2,3 Depression is a condition characterized by symptoms such as a depressed mood or loss of interest or pleasure in daily activities most of the time for two weeks or more, accompanied by appetite changes, sleep disturbances, motor restlessness or retardation, loss of energy, feelings of worthlessness or excessive guilt, poor concentration, and suicidal thoughts and behaviors. These symptoms cause clinically significant distress or impairment in social, occupational, or other important areas of functioning. The majority of people who suffer from depression do not respond adequately to initial antidepressant therapy.4

1Data Courtesy of SAMHSA on Past Year Prevalence of Major Depressive Episode Among U.S. Adults (2020). Retrieved from

http://www.nimh.nih.gov/health/statistics/major-depression.shtml

2IMS NSP, NPA, NDTI MAT-24-month data through Aug 2017.

3Kubitz N, et al. (2013) PLOS One,. 8(10):e76882. doi: 10.1371/journal.pone.0076882. PMID: 24204694;

4Rush AJ, et al. (2007) Am J.

Psychiatry 163:11, pp. 1905-1917 (STAR*D Study).

About TNX-601 ER

TNX-601 ER is a novel oral formulation of tianeptine oxalate designed for once-daily daytime dosing that is in the pre-IND (Investigational New Drug) stage of development for the treatment of MDD. Tonix reported the official minutes of an FDA Pre-IND meeting on March 22, 2021. Tianeptine sodium (amorphous) immediate release (3 times daily) was first marketed for depression in France in 1989 and has been available for decades in Europe, Russia, Asia, and Latin America for the treatment of depression. Tianeptine sodium has an established safety profile from decades of use in these jurisdictions. Currently there is no tianeptine-containing product approved in the U.S. and no extended-release tianeptine product approved in any jurisdiction. Tonix discovered a novel oxalate salt of tianeptine that may provide improved stability, consistency, and manufacturability compared to known salt forms of tianeptine. Tianeptine is believed to work in depression as an indirect modulator of the glutamatergic system, without direct binding NMDA, AMPA or kainate receptors. Tianeptine reverses stress induced increases in AMPA receptor trafficking, restoring hippocampal long-term potentiation and reversing the neuroplastic changes from stress and corticosteroid exposure. Tianeptine and its MC5 metabolite are also weak mu-opioid receptor (MOR) agonists, that present a potential abuse liability if illicitly misused in large quantities (8-80 times the therapeutic dose). In patients who were prescribed tianeptine for depression, the French Transparency Committee found an incidence of misuse of approximately 1 case per 1,000 patients treated1 suggesting low abuse liability when used at the antidepressant dose in patients prescribed tianeptine for depression. Clinical trials have shown that cessation of a therapeutic course of tianeptine does not appear to result in dependence or withdrawal symptoms following 6-weeks2,3,4–6, 3-months7, or 12-months8 of treatment. Tianeptine’s reported pro-cognitive and anxiolytic effects as well as its ability to attenuate the neuropathological effects of excessive stress responses suggest that it may also be used to treat posttraumatic stress disorder. TNX-601 ER is expected to have patent protection through 2037.

1Haute Authorite de Sante; Transparency Committee Opinion. Stablon 12.5 Mg, Coated Tablet, Re- Assessment of Actual Benefit at the Request of the Transparency Committee. December 5, 2012.

2Emsley, R., et al. J. Clin.

Psychiatry 2018, 79 (4)

3Bonierbale M, et al. Curr Med

Res Opin 2003, 19(2):114-124.4Guelfi, J. D., et al. Neuropsychobiology 1989, 22 (1), 41–48.

5Invernizzi, G. et al., Neuropsychobiology 1994, 30 (2–3), 85–93.

6Lepine, J. P., et al. Hum. Psychopharmacol. 2001, 16 (3), 219–227.

7Guelfi, J. D. et al., Neuropsychobiology 1992, 25 (3), 140–148.

8Lôo, H. et al., Br. J. Psychiatry. Suppl. 1992, No. 15, 61–65.

Tonix

Pharmaceuticals Holding Corp. *

Tonix is a clinical-stage biopharmaceutical company focused on discovering, licensing, acquiring and developing therapeutics to treat and prevent human disease and alleviate suffering. Tonix’s portfolio is composed of central nervous system (CNS), rare disease, immunology and infectious disease product candidates. Tonix’s CNS portfolio includes both small molecules and biologics to treat pain, neurologic, psychiatric and addiction conditions. Tonix’s lead CNS candidate, TNX-102 SL (cyclobenzaprine HCl sublingual tablet), is in mid-Phase 3 development for the management of fibromyalgia with a new Phase 3 study launched in the second quarter of 2022 and interim data expected in the first quarter of 2023. TNX-102 SL is also being developed to treat Long COVID, a chronic post-acute COVID-19 condition. Tonix expects to initiate a Phase 2 study in Long COVID in the third quarter of 2022. TNX-1300 (cocaine esterase) is a biologic designed to treat cocaine intoxication that is Phase 2 ready and has been granted Breakthrough Therapy Designation by the FDA. TNX-1900 (intranasal potentiated oxytocin), a small molecule in development for chronic migraine, is expected to enter the clinic with a Phase 2 study in the second half of 2022. Tonix’s rare disease portfolio includes TNX-2900 (intranasal potentiated oxytocin) for the treatment of Prader-Willi syndrome. TNX-2900 has been granted Orphan-Drug Designation by the FDA. TNX-601 ER (tianeptine oxalate extended-release tablet) is being developed as an antidepressant in the U.S., with a Phase 2 study expected to be initiated in first quarter of 2023 pending IND clearance. Tonix’s immunology portfolio includes biologics to address organ transplant rejection, autoimmunity and cancer, including TNX-1500, which is a humanized monoclonal antibody targeting CD40-ligand being developed for the prevention of allograft and xenograft rejection and for the treatment of autoimmune diseases. A Phase 1 study of TNX-1500 is expected to be initiated in the second half of 2022. Tonix’s infectious disease pipeline consists of a vaccine in development to prevent smallpox and monkeypox called TNX-801, next-generation vaccines to prevent COVID-19, and a platform to make fully human monoclonal antibodies to treat COVID-19. Tonix’s lead vaccine candidates for COVID-19 are TNX-1840 and TNX-1850, which are live virus vaccines based on Tonix’s recombinant pox live virus vector vaccine platform.

*All of

Tonix’s product candidates are investigational new drugs or biologics and have

not been approved for any indication.

This press release and further information about Tonix can be found at www.tonixpharma.com.

Forward

Looking Statements

Certain statements in this press release are forward-looking within the meaning of the Private Securities Litigation Reform Act of 1995. These statements may be identified by the use of forward-looking words such as “anticipate,” “believe,” “forecast,” “estimate,” “expect,” and “intend,” among others. These forward-looking statements are based on Tonix’s current expectations and actual results could differ materially. There are a number of factors that could cause actual events to differ materially from those indicated by such forward-looking statements. These factors include, but are not limited to, risks related to the failure to obtain FDA clearances or approvals and noncompliance with FDA regulations; delays and uncertainties caused by the global COVID-19 pandemic; risks related to the timing and progress of clinical development of our product candidates; our need for additional financing; uncertainties of patent protection and litigation; uncertainties of government or third party payor reimbursement; limited research and development efforts and dependence upon third parties; and substantial competition. As with any pharmaceutical under development, there are significant risks in the development, regulatory approval and commercialization of new products. Tonix does not undertake an obligation to update or revise any forward-looking statement. Investors should read the risk factors set forth in the Annual Report on Form 10-K for the year ended December 31, 2021, as filed with the Securities and Exchange Commission (the “SEC”) on March 14, 2022, and periodic reports filed with the SEC on or after the date thereof. All of Tonix’s forward-looking statements are expressly qualified by all such risk factors and other cautionary statements. The information set forth herein speaks only as of the date thereof.

Contacts

Jessica Morris (corporate)

Tonix Pharmaceuticals

investor.relations@tonixpharma.com

(862) 904-8182

Olipriya Das, Ph.D. (media)

Russo Partners

Olipriya.Das@russopartnersllc.com

(646) 942-5588

Peter Vozzo (investors)

Westwicke/ICR

peter.vozzo@westwicke.com

(443) 213-0505

Source: Tonix Pharmaceuticals Holding Corp.