Schwazze (OTCQX:SHWZ, NEO:SHWZ) is building a premier vertically integrated regional cannabis company with assets in Colorado and New Mexico and will continue to take its operating system to other states where it can develop a differentiated regional leadership position. Schwazze is the parent company of a portfolio of leading cannabis businesses and brands spanning seed to sale. The Company is committed to unlocking the full potential of the cannabis plant to improve the human condition. Schwazze is anchored by a high-performance culture that combines customer-centric thinking and data science to test, measure, and drive decisions and outcomes. The Company’s leadership team has deep expertise in retailing, wholesaling, and building consumer brands at Fortune 500 companies as well as in the cannabis sector. Schwazze is passionate about making a difference in our communities, promoting diversity and inclusion, and doing our part to incorporate climate-conscious best practices.

Joe Gomes, Managing Director – Generalist Analyst, Noble Capital Markets, Inc.

Joshua Zoepfel, Research Associate, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

4Q22 Results. Revenue was $40.1 million, up 51.4% y-o-y from $26.5 million. Adjusted EBITDA was $13.3 million, or 33.1% of revenue in the quarter, up from $7.5 million, or 28.3%, a year ago. Schwazze reported a net loss to common shareholders of $29.8 million, or a loss of $0.53/sh in the quarter, versus $5.5 million of net income, or $0.12/sh. last year. Both periods were impacted by one-time items.

Key Metrics. For the eighth consecutive quarter, Schwazze outpaced the Colorado industry, this time by 11%, but, once again, ongoing weakness in the Colorado market resulted in declines in key performance metrics. Colorado two year stacked IDs for same store sales in the fourth quarter were down 6%, and down 9% for the one year period. The same measurements for New Mexico were up 57% and 43%, respectively. Average basket size fell 11.8% in New Mexico but was up 1.5% in Colorado. Customer visits declined 10.5% in Colorado and were up 61.7% in New Mexico.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

Cocrystal Pharma, Inc. is a clinical-stage biotechnology company discovering and developing novel antiviral therapeutics that target the replication process of influenza viruses, coronaviruses (including SARS-CoV-2), hepatitis C viruses and noroviruses. Cocrystal employs unique structure-based technologies and Nobel Prize-winning expertise to create first- and best-in-class antiviral drugs. For further information about Cocrystal, please visit www.cocrystalpharma.com.

Robert LeBoyer, Vice President, Research Analyst, Life Sciences , Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

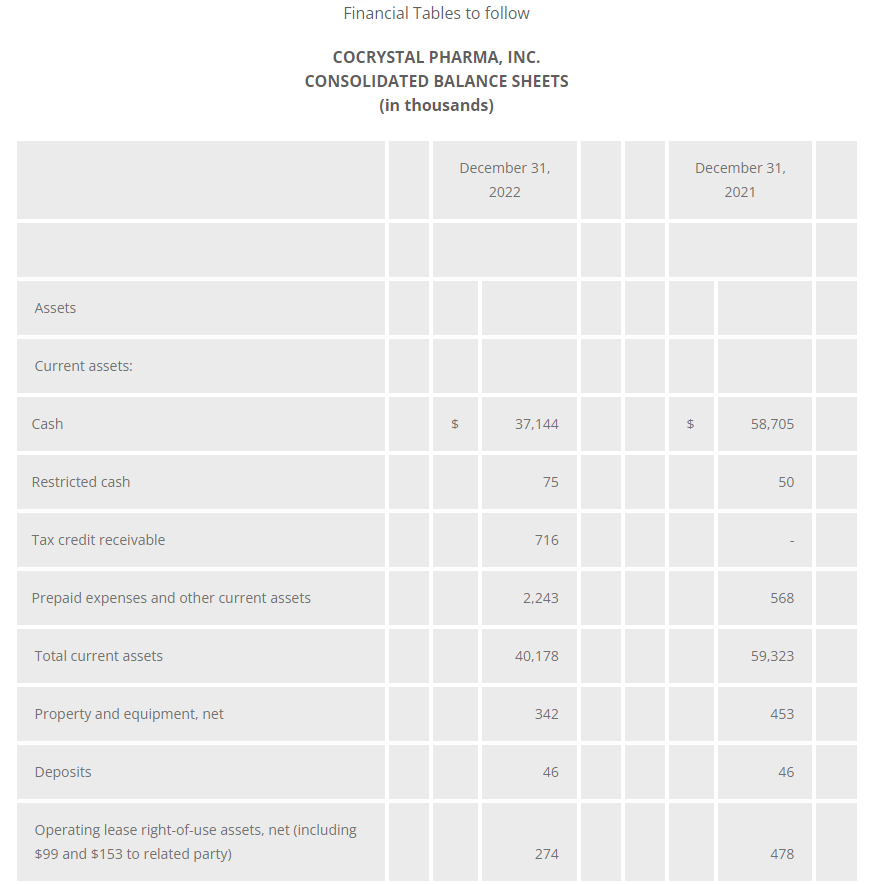

Financial Results. Cocrystal reported a 4Q loss of $4.5 million or $(0.55) per share and a FY2022 loss of $38.8 million or $(4.77) per share. The full-year results included a non-cash charge of $19.1 million for the impairment of goodwill in 2Q22. Excluding the charge, expenses levels for Research and Development and General and Administrative expense were close to expectations. The company ended FY2022 with $37.1 million in cash.

Influenza Clinical Trial Expected To Begin In 2H2023. In December 2022, Cocrystal reported preliminary safety and tolerability results from its dose-ranging Phase 1 study for orally administered CC-42344 for influenza. A Phase 2a study has been designed to challenge healthy human volunteers with pharmaceutically-produced influenza A virus, then treat with CC-42344. An application to start trials in the UK is planned for 1H2023, with enrollment beginning in 2H23. Preclinical development of an inhaled formulation of CC-42344 continues.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

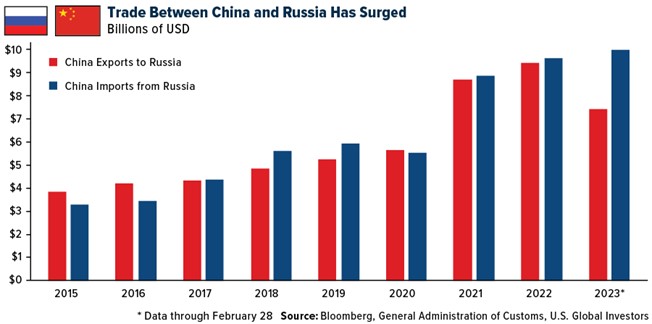

Petrodollar Dusk, Petroyuan Dawn: What Investors Need To Know

While most investors were trying to gauge the Federal Reserve’s next moves in light of recent bank failures last week, something interesting happened in Moscow.

During a three-day state visit, Chinese President Xi Jinping held friendly talks with Russian President Vladimir Putin in a show of unity, as both countries increasingly seek to position themselves as leaders of what they call a “multipolar world order,” one that challenges U.S.-centric alliances and agreements.

Among those agreements is the petrodollar, which has been in place for over 50 years.

In case you’re wondering, “petrodollars” are not a real currency. They’re simply dollars being used to trade oil. Early in the 1970s, the U.S. government provided economic aid to Saudi Arabia, its chief oil-producing rival, in exchange for assurances that Riyadh would price its crude exports exclusively in the U.S. dollar. In 1975, other members of the Organization of Petroleum Exporting Countries (OPEC) followed suit, and the petrodollar was born.

This had the immediate effect of strengthening the U.S. dollar. Since countries around the world had to have dollars on hand in order to buy oil (and other key commodities such as gold, also priced in dollars), the greenback became the world’s reserve currency, a status formerly enjoyed by the British pound, French franc and Dutch guilder.

All things must come to an end, however. We may be witnessing the end of the petrodollar as more and more countries, including China and Russia, are agreeing to make settlements in currencies other than the U.S. dollar. This could have wide-ranging implications on not just a macro scale but also investment portfolios.

This article was republished with permission from Frank Talk, a CEO Blog by Frank Holmes of U.S. Global Investors (GROW). Find more of Frank’s articles here – Originally published March 27, 2023

Dawn For The Petroyuan?

Putin couldn’t have been more explicit. During Xi’s state visit, he named the Chinese yuan as his favored currency to conduct trade in. Ever since Western sanctions were levied on the Eastern European country for its invasion of Ukraine early last year, Russia has increasingly depended on its southern neighbor to buy the oil other countries won’t touch.

In just the first two months of 2023, China’s imports from Russia totaled $9.3 billion, exceeding full-year 2022 imports in dollar terms. In February alone, China imported over 2 million barrels of Russian crude, a new record high.

Except that now, the yuan is presumably being used to make these settlements.

As Zoltar Pozsar, New York-based economist and investment research director at Credit Suisse, put it recently: “That’s dusk for the petrodollar… and dawn for the petroyuan.”

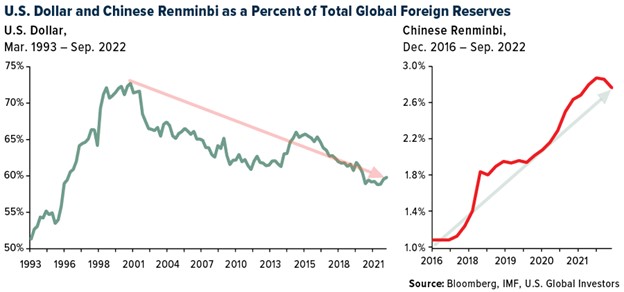

U.S. Dollar Still The World’s Reserve Currency, But Its Dominance Is Slipping

Before you dismiss Pozsar’s comment as an exaggeration, consider that other major OPEC nations and BRICS members (Brazil, Russia, India, China and South Africa) are either accepting yuan already or strongly considering it. Russia, Iran and Venezuela account for about 40% of the world’s proven oilfields, and the three sell their oil in exchange for yuan. Turkey, Argentina, Indonesia and heavyweight oil producer Saudi Arabia have all applied for admittance into BRICS, while Egypt became a new member this week.

What this suggests is that the yuan’s role as a reserve currency will continue to strengthen, signifying a broader shift in the global power balance and potentially giving China a bigger hand with which to shape economic policies that affect us all.

To be clear, the U.S. dollar remains the world’s top reserve currency for now, though its share of global central banks’ official holdings has slipped in the past 20 years, from 72% in 2001 to just under 60% today. By contrast, the yuan’s share of official holdings has more than doubled since 2016. The Chinese currency accounted for about 2.8% of reserves as of September 2022.

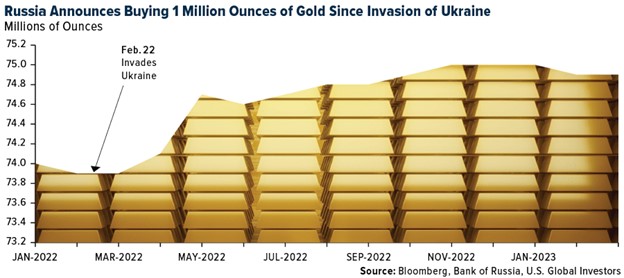

Russia Diversifying Away From The Dollar By Loading Up On Gold

It’s not all about the yuan, of course. Gold has also increased as a foreign reserve, especially among emerging economies that seek to diversify away from the dollar.

Last week, Russia announced that its bullion holdings jumped by approximately 1 million ounces over the past 12 months as its central bank loaded up on gold in the face of Western sanctions. The bank reported having nearly 75 million ounces at the end of February 2023, up from about 74 million a year earlier.

Long-Term Implications For Investors

The implications of the dollar potentially losing its status as the global reserve are numerous. Obviously, there may be currency risks, and a decrease in demand for U.S. Treasury bonds could result in rising interest rates. I would expect to see massive swings in commodity prices, especially oil prices, which could be an opportunity if you can stomach the volatility.

Gold would look exceptionally attractive, I think. A significant decrease in the relative value of the dollar would be supportive of the gold price, and I would be surprised not to see new highs. It’s for reasons like these that I always recommend a 10% weighting in gold, with 5% in physical bullion and the other 5% in high-quality gold mining equities. Be sure to rebalance at least on an annual basis.

All opinions expressed and data provided are subject to change without notice. Some of these opinions may not be appropriate to every investor. By clicking the link(s) above, you will be directed to a third-party website(s). U.S. Global Investors does not endorse all information supplied by this/these website(s) and is not responsible for its/their content.

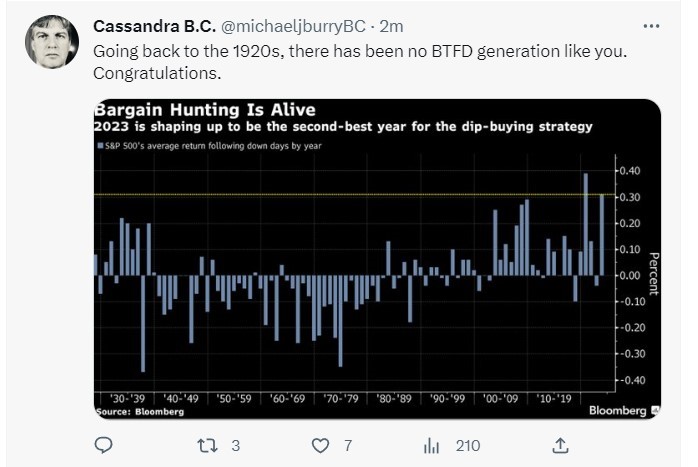

Michael Burry’s New Comments Highlight the Importance of Pivoting

With most major indexes in positive territory for the year but still, well below their 2022 starting point, are markets moving to make up their losses? Michael Burry thinks so. In the most positive tweet I have seen from him in almost four years, Burry posted he was “wrong to say sell.” As recently as late January, Burry posted a one-word tweet, “Sell.” The pundits read into it that perhaps another economic crisis similar to the one that occurred in 2008 will crush markets. His almost cult-like following was built by being one of the few individuals who correctly positioned his investments for the housing and subprime mortgage problems that shook the U.S. in late 2008.

Michael Burry Suggests We Have a Bull Market

Market participants are surprised at both Burry’s bullishness and open acknowledgment that he believes he was overly negative and has gotten it wrong this time. The widely followed investor has been bearish and broadcasting this sentiment to his 1.4 million Twitter followers. The suggestions have been that they should consider lightening their holdings. Burry even caught investor attention with his own 13F reported short position in Apple (AAPL).

Burry points to high levels of dip buying, which may have changed today’s market landscape. This is backed up by other reports, including one from Bloomberg that gives a reason that 2023 is shaping up to be one of the best years for dip-buyers.

Importance of Pivoting

He may not have been “wrong.” The best investors understand their time frame and will recognize when market moves are not as expected. On February 2nd, a few days after Burry’s January 31st “sell” tweet, the S&P 500 index closed at 4,180 just after the Fed interest rate target increased by 25 basis points. To date, that is the large-cap index’s highest close of 2023, as weeks of declines followed. The NDX had fallen nearly 3% since that day.

But the trend, if it continues, appears to have changed. The equity market in March has been surprisingly resilient. It has been able to shrug off multi-country concerns surrounding the banks, elevated expectations of an economic downturn, and forecasts that S&P 500 companies will report their biggest quarterly earnings decline since the second quarter of 2020.

Moving from a sell to a more bullish position, for those that are looking to capture short-term moves, seems to be what is implied in his tweet. It may be that Michael Burry was not wrong in direction, as the markets did fall, just wrong in how long they would stay weak.

Take Away

There are long-term trends and short-term trends. Also, trends that are weak and strong through different sectors at the same time. While time will tell if Burry is correct in his most recent direction, the ability to see market sentiment changing and go with it is characteristic of a successful trader.

BOTHELL, Wash., March 29, 2023 (GLOBE NEWSWIRE) — Cocrystal Pharma, Inc. (Nasdaq: COCP) reports financial results for the 12 months ended December 31, 2022, and provides updates on its antiviral pipeline, upcoming milestones and business activities.

“This is an eventful time for Cocrystal with multiple near-term milestones with our highly promising antiviral programs,” said Sam Lee, Ph.D., President and co-CEO of Cocrystal. “Preparations are ongoing with a UK regulatory filing to begin an influenza A Phase 2a human challenge study with our novel oral PB2 inhibitor CC-42344. Pending regulatory clearance, we expect patient enrollment to begin in the second half of this year.

“We are also preparing to file with the Australian regulatory agency to begin a first-in-human trial in our oral COVID-19 program with our novel, broad-spectrum protease inhibitor CDI-988. This trial is also slated to begin in the first half of 2023, subject to regulatory clearance,” he added. “In our norovirus program, preclinical development activities are ongoing and we plan to select a lead oral candidate by mid-2023.”

“We made significant progress over the past year that put us on pace to initiate two clinical trials during 2023,” said James Martin, CFO and co-CEO. “We expect our cash will be sufficient to fund operating activities for the coming year as we tightly manage our financial resources under our cost-efficient operating model. We also intend to pursue non-dilutive funding to further support development of our promising antiviral programs.”

Antiviral Product Pipeline Overview

We are developing antiviral therapeutics that inhibit the essential viral replication function of RNA viruses that cause acute and chronic viral diseases. Our drug discovery process focuses on the highly conserved regions of the viral enzymes and inhibitor-enzyme interactions at the atomic level. It differs from traditional, empirical medicinal chemistry approaches that often require iterative high-throughput compound screening and lengthy hit-to-lead processes. In designing drug candidates, we seek to anticipate and avert potential viral mutations leading to resistance. By designing and selecting drug candidates that interrupt the viral replication process and have specific binding characteristics, we seek to develop drugs that not only are effective against both the virus and possible mutants of the virus, but also have reduced off-target interactions that may cause undesirable clinical side effects. We will continue developing preclinical and clinical drug candidates using our proprietary drug discovery technology.

Influenza Programs

Influenza is a severe respiratory illness caused by either the influenza A or B virus that results in disease outbreaks mainly during the winter months. The global seasonal influenza market was valued at $6.5 billion in 2021 and is projected to reach up to $27.95 billion by 2029, according to Data Bridge Market Research.

Pandemic and Seasonal Influenza A

Our novel oral PB2 inhibitor, CC-42344, has shown excellent antiviral activity against influenza A strains including pandemic and seasonal strains, as well as strains resistant to Tamiflu® and Xofluza®.

In March 2022 we initiated enrollment in our randomized, double-controlled, dose-escalating Phase 1 study to evaluate the safety, tolerability and pharmacokinetics of orally administered CC-42344 in healthy adults.

In April 2022 we announced preliminary Phase 1 study data demonstrating a favorable safety and pharmacokinetic (PK) profile in the first two cohorts in the single-ascending dose portion of the study.

In July 2022 we reported PK results from the single-ascending dose of the study supporting once-daily dosing.

In December 2022 we reported favorable safety and tolerability results from the Phase 1 study with CC-42344 for influenza A.

We entered into an agreement with a UK-based clinical research organization to conduct a Phase 2a human challenge study evaluating safety, viral and clinical measures of orally administered CC-42344 in influenza A-infected subjects. Under the human challenge model, healthy adults will be infected with the influenza A virus under carefully controlled conditions, which we believe will hasten trial enrollment.

We expect to submit an application with the United Kingdom Medicines and Healthcare Products Regulatory Agency in the first half of 2023 to conduct this study. Pending clearance by the agency, we expect to initiate the study in the second half of 2023.

Preclinical development is underway with an inhaled formulation of CC-42344 as a treatment and prophylaxis for influenza A.

Pandemic and Seasonal Influenza A/B Program

Merck recently notified the Company that they continue development activities with the compounds discovered under this agreement and that they have filed on behalf of both companies multiple U.S. and international patent applications associated with these compounds. Merck continues to be responsible for managing the patents.

In January 2019 we entered into an Exclusive License and Research Collaboration Agreement with Merck Sharp & Dohme Corp. (Merck) to discover and develop certain proprietary influenza antiviral agents that are effective against both influenza A and B strains. This agreement includes milestone payments of up to $156 million plus royalties on sales of products discovered under the agreement.

In January 2021 we announced completion of all research obligations under the agreement. Merck is now solely responsible for further preclinical and clinical development of compounds discovered under this agreement.

COVID-19 and Other Coronavirus Programs

By targeting viral replication enzymes and protease, we believe it is possible to develop an effective treatment for all coronavirus diseases including COVID-19, Severe Acute Respiratory Syndrome (SARS) and Middle East Respiratory Syndrome (MERS). Our main SARS-CoV-2 protease inhibitors showed potent in vitro pan-viral activity against common human coronaviruses, rhinoviruses and respiratory enteroviruses that cause the common cold, as well as against noroviruses that can cause symptoms of acute gastroenteritis.

Oral Protease Inhibitor CDI-988

We selected CDI-988 as our lead candidate for development as a potential oral treatment for SARS-CoV-2. CDI-988, which was designed and developed using our proprietary structure-based drug discovery platform technology, targets a highly conserved region in the active site of SARS-CoV-2 3CL (main) protease required for viral RNA replication.

CDI-988 exhibited superior in vitro potency against SARS-CoV-2 with activity maintained against current variants of concern, and demonstrated a safety profile and PK properties that are supportive of daily dosing.

We are currently conducting good laboratory practice (GLP) toxicology studies in preparation for a Phase 1 study.

Preparations are underway to submit an application to the Australian regulatory authority for a planned randomized, double-blind, placebo-controlled Phase 1 study. Pending regulatory clearance, we expect to initiate the study in the first half of 2023. We believe the FDA’s guidance for further development of our antiviral candidate CDI-45205 (described below) also provides us with a clearer pathway for our planned Phase 1 study with CDI-988, as well as directives for designing a subsequent Phase 2 study.

Intranasal/Pulmonary Protease Inhibitor CDI-45205

An IND-enabling study is ongoing with CDI-45205, our novel SARS-CoV-2 3CL (main) protease inhibitor being developed as a potential treatment for SARS-CoV-2 and its variants.

We received guidance from the FDA regarding further preclinical and clinical development of CDI-45205 that provides a clearer pathway for future clinical development.

CDI-45205 and several analogs showed potent in vitro activity against the main SARS-CoV-2 variants to date including the Omicron variant, surpassing the activity observed with the original Wuhan strain.

CDI-45205 demonstrated good bioavailability in mouse and rat PK studies via intraperitoneal injection, and no cytotoxicity against a variety of human cell lines. CDI-45205 also demonstrated a strong synergistic effect with the FDA-approved COVID-19 medicine remdesivir.

CDI-45205 was among the broad-spectrum viral protease inhibitors we obtained from Kansas State University Research Foundation (KSURF) under an exclusive license agreement announced in April 2020. We believe the protease inhibitors obtained from KSURF have the ability to inhibit the inactive SARS-CoV-2 polymerase replication enzymes into an active form.

Replication Inhibitors

We are using our proprietary structure-based drug discovery platform technology to discover replication inhibitors for orally administered therapeutic and prophylactic treatments for SARS-CoV-2. Replication inhibitors hold potential to work with protease inhibitors in a combination therapy regimen.

Norovirus Program

We are developing certain proprietary broad-spectrum, non-nucleoside polymerases for the treatment of human norovirus infections using our proprietary structure-based drug design technology platform. We also hold exclusive rights to norovirus protease inhibitors for use in humans under the KSURF license.

We are targeting the selection of an oral preclinical lead in the first half of 2023.

Norovirus is a global public health problem responsible for nearly 90% of epidemic, non-bacterial outbreaks of gastroenteritis around the world.

Hepatitis C Program

We are seeking a partner to advance the development of CC-31244 following the successful completion of a Phase 2a study. This compound has shown favorable safety and preliminary efficacy in a triple-regimen Phase 2a study in combination with Epclusa (sofosbuvir/velpatasvir) for the ultra-short duration treatment of individuals infected with the hepatitis C virus (HCV).

HCV is a viral infection of the liver that causes both acute and chronic infection. In June 2022 the World Health Organization estimates that 58 million people worldwide have chronic HCV infection.

2022Financial Results

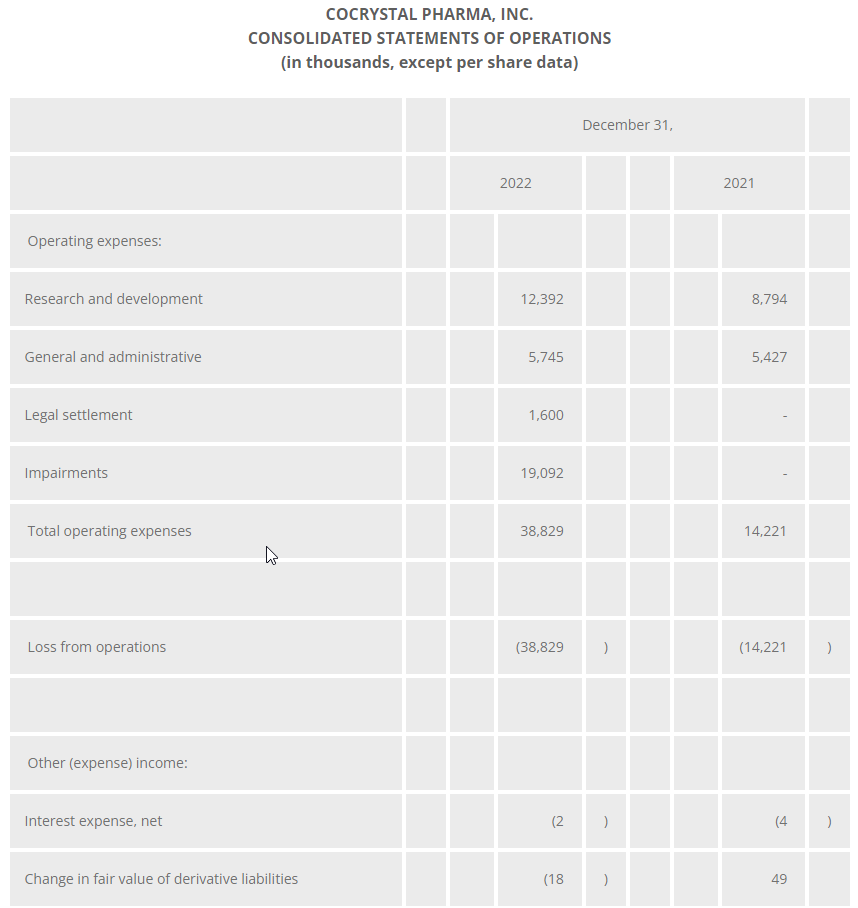

Research and development expenses for 2022 were $12.4 million compared with $8.8 million for 2021, with the increase primarily due to advancing our influenza lead candidate CC-42344 through a Phase 1 trial and preparation for a Phase 2a clinical trial planned for 2023, as well as advancing our lead COVID-19 clinical oral candidate CDI-988 in preparation for a Phase 1 clinical trial planned for 2023. General and administrative expenses for 2022 were $5.7 million compared with $5.4 million for 2021, with the increase primarily due to professional fees and litigation expenses.

The Company’s litigation with an insurer resulted in the insurance company obtaining a summary judgment during the second quarter of 2022 and accounted for a potential $1.6 million adverse award. The Company filed an appeal in July 2022. Pending the outcome of the appeal, the Company paid $1.6 million into the registry of the court, which stayed execution of the judgment. The United States Court of Appeals for the Third Circuit held oral argument on the appeal on March 8, 2023, and the parties are still awaiting a ruling on the appeal.

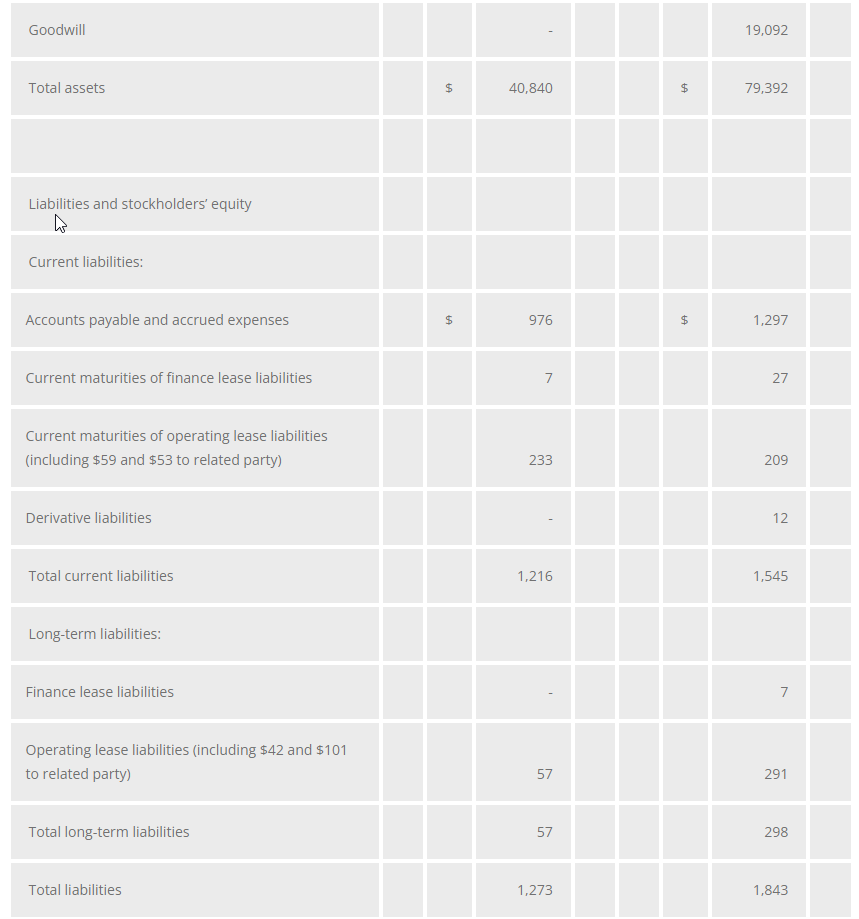

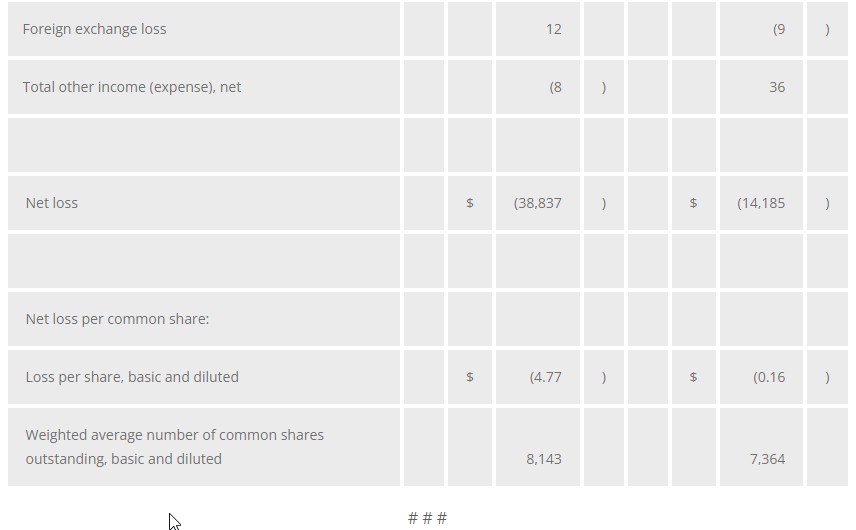

The net loss for 2022 was $38.8 million, or $4.77 per share, compared with the net loss for 2021 of $14.2 million, or $0.16 per share. This increase was primarily due to a $19.1 million non-cash impairment-loss of goodwill and an increase in R&D expenses as we continue to advance CC-42344, CDI-988 and other product candidates.

Cocrystal reported unrestricted cash of $37.1 million as of December 31, 2022 compared with $58.7 million as of December 31, 2021. Net cash used in operating activities for 2022 was $21.4 million. The Company reported working capital of $39.0 million and 8.1 million common shares outstanding as of December 31, 2022.

About Cocrystal Pharma, Inc.

Cocrystal Pharma, Inc. is a clinical-stage biotechnology company discovering and developing novel antiviral therapeutics that target the replication process of influenza viruses, coronaviruses (including SARS-CoV-2), hepatitis C viruses and noroviruses. Cocrystal employs unique structure-based technologies and Nobel Prize-winning expertise to create first- and best-in-class antiviral drugs. For further information about Cocrystal, please visit www.cocrystalpharma.com.

This press release contains forward-looking statements within the meaning of the Private Securities Litigation Reform Act of 1995, including statements regarding our plans for the future development of preclinical and clinical drug candidates, our expectations regarding future characteristics of the product candidates we develop, the expected time of achieving certain value driving milestones in our programs, including, preparation, commencement and advancement of clinical studies for certain product candidates in 2023, the viability and efficacy of potential treatments for coronavirus and other diseases, expectations for the markets for certain therapeutics, our ability to execute our clinical and regulatory goals and deploy regulatory guidance towards future studies, the expected sufficiency of our cash balance to fund our planned operations, our liquidity and planned cost-efficient management of our financial resources, and our continued pursuit of non-dilutive funding. The words “believe,” “may,” “estimate,” “continue,” “anticipate,” “intend,” “should,” “plan,” “could,” “target,” “potential,” “is likely,” “will,” “expect” and similar expressions, as they relate to us, are intended to identify forward-looking statements. We have based these forward-looking statements largely on our current expectations and projections about future events. Some or all of the events anticipated by these forward-looking statements may not occur. Important factors that could cause actual results to differ from those in the forward-looking statements include, but are not limited to, the risks and uncertainties arising from the impact of COVID-19 (including long-term and pervasive effects of the virus), inflation, interest rate increases and the Ukraine war on our Company, our collaboration partners, and on the U.S., U.K., Australia and global economies, including manufacturing and research delays arising from raw materials and labor shortages, supply chain disruptions and other business interruptions including any adverse impacts on our ability to obtain raw materials and test animals as well as similar problems with our vendors and our current Contract Research Organization (CRO) and any future CROs and Contract Manufacturing Organizations, the results of the studies for CC-42344 and CDI-988, the ability of our CROs to recruit volunteers for, and to proceed with, clinical studies, our reliance on Merck for further development in the influenza A/B program under the license and collaboration agreement, our and our collaboration partners’ technology and software performing as expected, financial difficulties experienced by certain partners, the results of future preclinical and clinical trials, general risks arising from clinical trials, receipt of regulatory approvals, regulatory changes, development of effective treatments and/or vaccines by competitors, including as part of the programs financed by the U.S. government, potential mutations in a virus we are targeting which may result in variants that are resistant to a product candidate we develop, and the outcome of our appeal of the summary judgment. Further information on our risk factors is contained in our filings with the SEC, including our Annual Report on Form 10-K for the year ended December 31, 2022. Any forward-looking statement made by us herein speaks only as of the date on which it is made. Factors or events that could cause our actual results to differ may emerge from time to time, and it is not possible for us to predict all of them. We undertake no obligation to publicly update any forward-looking statement, whether as a result of new information, future developments or otherwise, except as may be required by law.

FLORHAM PARK, N.J., March 29, 2023 (GLOBE NEWSWIRE) — PDS Biotechnology Corporation (Nasdaq: PDSB), a clinical-stage immunotherapy company developing a growing pipeline of targeted immunotherapies for cancer and infectious disease, today announced that Dr. Frank Bedu-Addo, President and Chief Executive Officer, will participate in Cantor’s Future of Oncology Virtual Symposium being held on April 3-5, 2023.

Cantor Symposium Presentation Date: Tuesday, April 4, 2023 Time: 3:00 PM ET

For more information about the conference, please contact your Cantor representative directly.

About PDS Biotechnology PDS Biotech is a clinical-stage immunotherapy company developing a growing pipeline of targeted cancer and infectious disease immunotherapies based on our proprietary Versamune®, Versamune® plus PDS0301, and Infectimune™ T cell-activating platforms. We believe our targeted immunotherapies have the potential to overcome the limitations of current immunotherapy approaches through the activation of the right type, quantity and potency of T cells. To date, our lead clinical candidate, PDS0101, has demonstrated the ability to reduce tumors and stabilize disease in combination with approved and investigational therapeutics in patients with a broad range of HPV16-associated cancers. Our Infectimune™ based vaccines have also demonstrated the potential to induce not only robust and durable neutralizing antibody responses, but also powerful T cell responses, including long-lasting memory T cell responses in pre-clinical studies to date. To learn more, please visit www.pdsbiotech.com or follow us on Twitter at @PDSBiotech.

Conference Call and Webcast will be held on March 29, 2023 at 11:00am ET

TORONTO–(BUSINESS WIRE)– Sierra Metals Inc. (TSX: SMT) (“Sierra Metals” or the “Company”) announces fourth quarter and year-end 2022 consolidated financial results. All amounts are in US dollars, unless otherwise noted.

Fourth Quarter and Year-End 2022 Operating and Financial Highlights

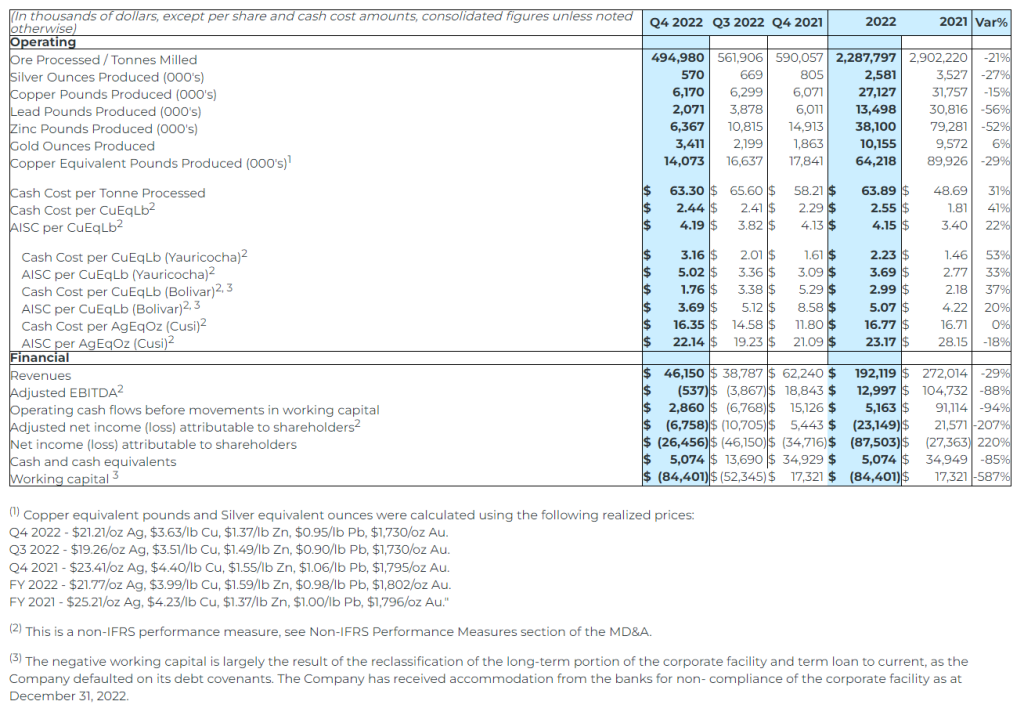

Revenue from metals payable of $46.2 million in Q4 2022 and $192.1 million in 2022.

Adjusted EBITDA(1) of ($0.5) million in Q4 2022 and $13.0 million in 2022.

Net loss attributable to shareholders for Q4 2022 of $26.5 million, or $0.16 per share and $87.5 million, or $0.53 per share in 2022.

Net loss of $88.3 million, or $0.54 in 2022, which includes impairment charges of $25.0 million for the Bolivar mine and $25.0 million for the Cusi mine; and $5.3 million non-cash depletion.

Cash and cash equivalents as at December 31, 2022 was $5.1 million; negative working capital of $84.4 million.

The focus in 2023 is to improve safety practices, reduce costs, improve productivity through increased equipment availability.

On March 13, 2023, the Company improved short-term liquidity through refinancing $6,250,000 of debt repayments due March 2023, with negotiations ongoing to refinance a total of $18,750,000 of term loan amortization payments due in 2023.

Ernesto Balarezo Valdez, Sierra Metals’ Interim CEO comments, “Sierra Metals enters 2023 with positive momentum. Since the start of 2023, we have stabilized our operations and begun to implement a program to optimize our operating performance, all with safety as the top priority. The expected operational improvements, alongside the corporate initiatives to improve our balance sheet, which includes the recently announced debt refinancing initiatives, has set the stage for Sierra Metals to increase production, lower costs and improve our financial position.”

(1) This is a non-IFRS performance measure, see Non-IFRS Performance Measures section of the MD&A.

Strategic Update

As first announced on October 18, 2022, a special committee comprised of the Company’s independent directors (the “Special Committee”) is undertaking a strategic review process. The mandate of the Special Committee includes exploring, reviewing and considering options to optimize the operations of the Company and possible financing, restructuring and strategic options in the best interests of the Company. The Company has engaged CIBC Capital Markets as a financial advisor in this process.

The Special Committee continues to evaluate certain strategic alternatives. The Company will report to shareholders upon completion of the Special Committee’s review. Concurrently, over the course of the strategic review process the Special Committee and the management team have identified and have implemented a number of opportunities to improve the Company’s operational and financial position.

Progress made to-date includes the following:

Successfully implementing a transition of executive level management.

Organizational changes designed to create a shift in the corporate culture and instill a more “hands-on” approach to operations.

Placing a renewed emphasis on safety and employee engagement. The Company has hired a VP of Health and Safety, instituted new safety protocols across all of its operations, increased training and communication efforts, and invested in remote-controlled equipment which is designed to reduce risk of injury.

Streamlining operations to reduce costs, and refinancing debt obligations in order to preserve working capital as production levels improve.

Advancing discussions with secured lenders on refinancing of material short-term obligations, and steps to improve short-term liquidity through ancillary financing arrangements.

Initiatives to increase productivity at the mines, including increasing asset utilization, focused underground development of mine sequencing, and improvements to ventilation and pumping systems.

Prioritizing spending to focus resources on the Company’s core assets at Yauricocha and Bolivar.

Initiating activities designed to identify additional mineral resources at the Yauricocha and Bolivar mines to sustain long-term production increases.

Enhancements to internal financial forecasting, reporting and integration of information across functions to ensure timely decision making.

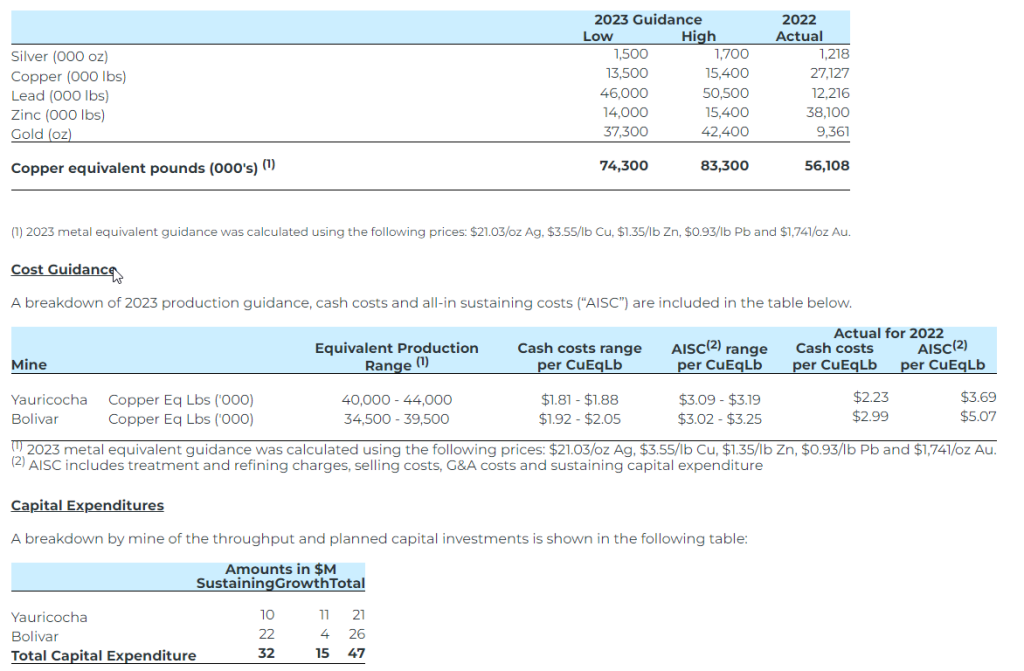

2023 Guidance

Production Guidance

The Bolivar mine exited fourth quarter 2022 with improved operations and expectations of continued improved performance throughout 2023. The Yauricocha mine is expected to gradually and safely ramp up production throughout 2023 at the current depth. Meanwhile, Yauricocha’s focus will remain on obtaining the necessary permits to access the deeper, high-grade ore bodies.

The table summarizing 2023 production guidance from the Yauricocha and the Bolivar mines is provided below. Management considers the Cusi mine as ‘non-core’ and it has been excluded from the guidance.

Total sustaining capital for 2023, excluding Cusi, is expected to be $32.0 million, mainly comprised of mine development ($3.0 million) and drainage ($2.3 million) in Yauricocha, and mine development ($11.3 million), infill drilling ($5.3 million) and equipment replacement ($3.9 million) at the Bolivar mine.

Growth capital for 2023, projected at $15.0 million, includes costs of tailings dam expansion ($5.6 million) and Yauricocha shaft ($3.2 million) in Peru. Growth capital at Bolivar includes costs of the tailings dam and the starter dam.

Management will continue to review performance throughout the year, while exploring value enhancing opportunities.

Conference Call & Webcast

The Company will host a conference call on Wednesday, March 29, 2023, at 11:00 AM EDT to discuss the results. Details of the conference call and webcast are as follows:

The webcast, presentation slides and 2022 Financial Statements and Management Discussion and Analysis will be available at www.sierrametals.com, with an archive of the webcast available for 180 days.

Summary of Operating and Financial Results

The information provided below are excerpts from the Company’s Annual Financial Statements and Management’s Discussion and Analysis, which are available on the Company’s website (www.sierrametals.com) and on SEDAR (www.sedar.com) under the Company’s profile.

2022 Consolidated Financial Summary

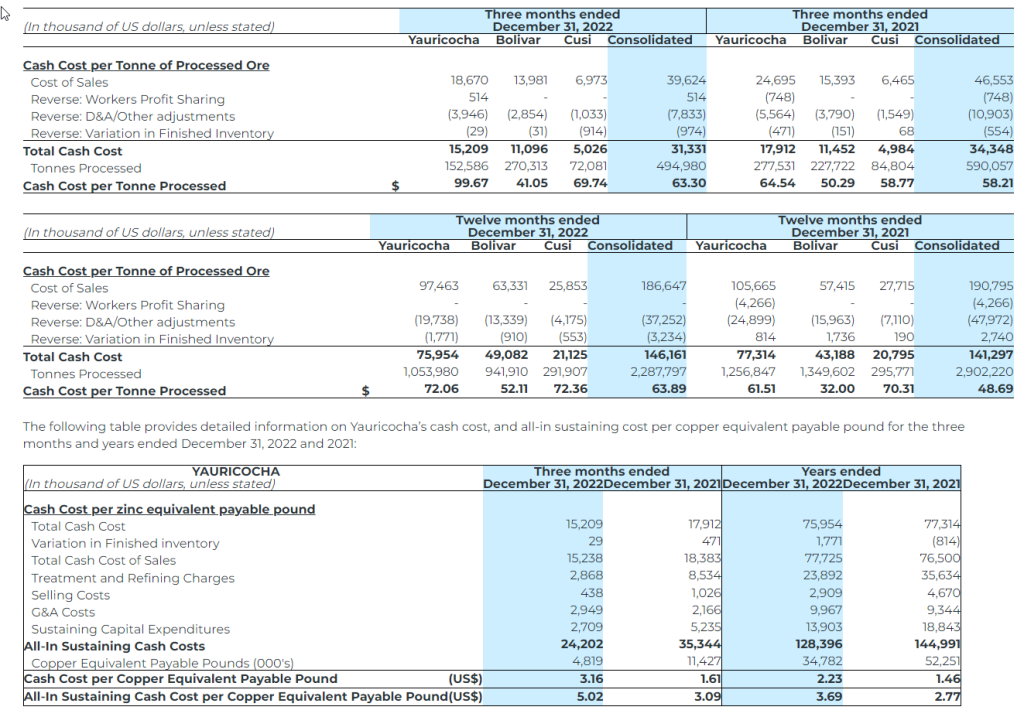

Revenue from metals payable of $192.1 million in 2022, a decrease of 29% from 2021 annual revenue of $272.0 million. Lower revenue resulted from the decrease in throughput and grades at the Yauricocha and Bolivar mines;

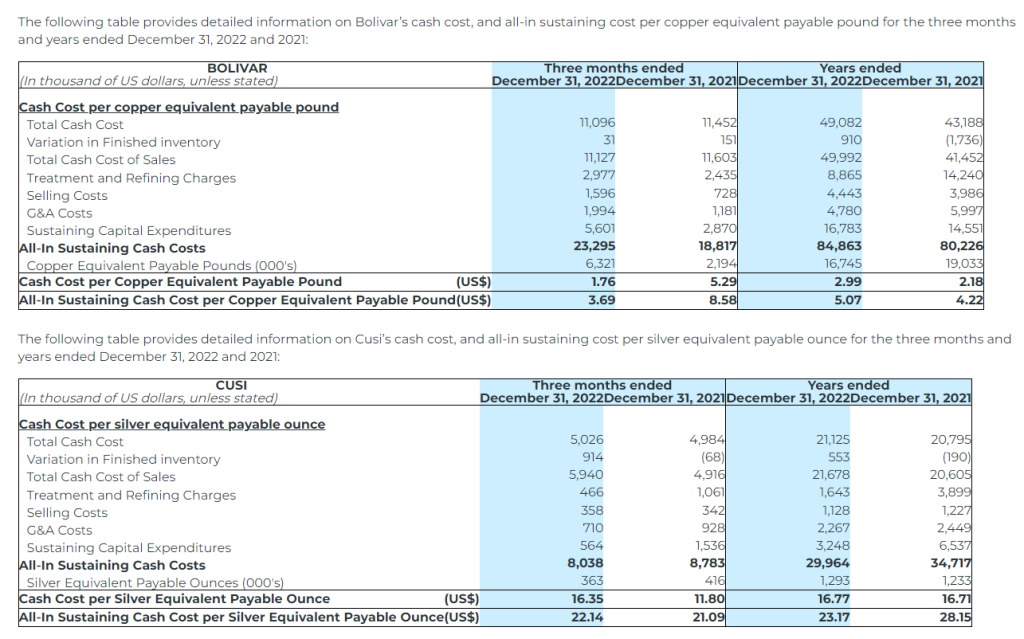

Yauricocha’s cash cost per copper equivalent payable pound(1) was $2.23 (2021 – $1.46), and AISC per copper equivalent payable pound(1) of $3.69 (2021 – $2.77);

Bolivar’s cash cost per copper equivalent payable pound(1) was $2.99 (2021 – $2.18), and AISC per copper equivalent payable pound(1) was $5.07 (2021 – $4.22);

Cusi’s cash cost per silver equivalent payable ounce(1) was $16.77 (2021 – $16.71), and AISC per silver equivalent payable ounce(1) was $23.17 (2021 – $28.15);

Adjusted EBITDA(1) of $13.0 million for 2022, a decrease from the adjusted EBITDA(1) of $104.7 million for 2021;

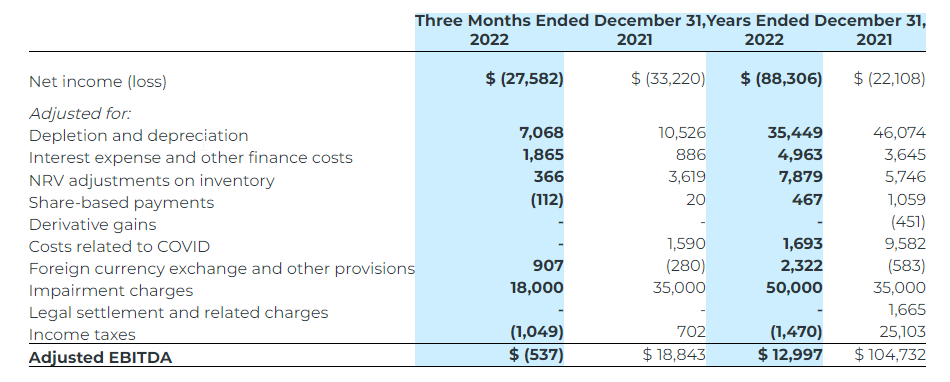

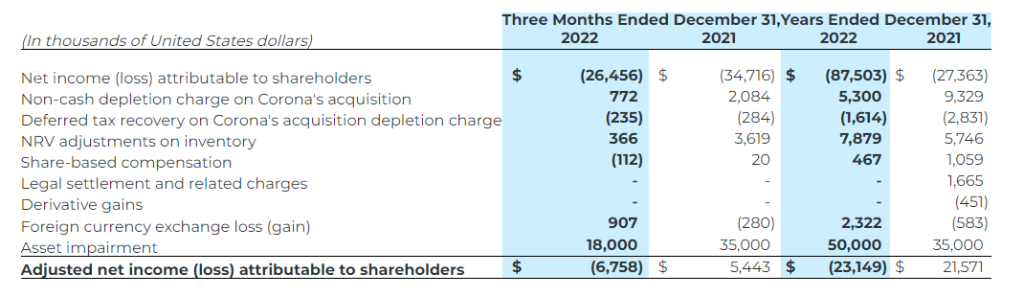

Net loss attributable to shareholders for 2022 was $87.5 million or $0.53 per share (2021: net loss of $27.4 million, $0.17 per share). Net loss for the year ended 2022 includes an impairment charge of $25.0 million on the Bolivar mine and $25.0 million on the Cusi mine (2021: impairment of $35.0 million on the Cusi mine);

Adjusted net loss attributable to shareholders(1) of $23.1 million, or $0.14 per share, for 2022 compared to the adjusted net income(1) of $21.6 million, or $0.13 per share for 2021;

A large component of the net income (loss) for every period is the non-cash depletion charge in Peru, which was $5.3 million for 2022 (2021: $9.3 million). The non-cash depletion charge is based on the aggregate fair value of the Yauricocha mineral property at the date of acquisition of Sociedad Minera Corona S.A. de C.V. (“Corona”) of $371.0 million amortized over the life of the mine;

Cash flow generated from operations before movements in working capital of $5.2 million for 2022 was lower than the $91.1 million in 2021, mainly due to lower revenues and higher operating costs; and

Cash and cash equivalents of $5.1 million and working capital of $(84.4) million as at December 31, 2022 compared to $34.9 million and $17.3 million, respectively, at the end of 2021. Cash and cash equivalents decreased during 2022 as the $38.3 million used in investing activities exceeded the $1.1 million generated from financing activities and $7.3 million generated from operating activities.

(1) This is a non-IFRS performance measure, see Non-IFRS Performance Measures section of the MD&A.

Non-IFRS Performance Measures

The non-IFRS performance measures presented do not have any standardized meaning prescribed by IFRS and are therefore unlikely to be directly comparable to similar measures presented by other issuers.

Non-IFRS reconciliation of adjusted EBITDA

EBITDA is a non-IFRS measure that represents an indication of the Company’s continuing capacity to generate earnings from operations before taking into account management’s financing decisions and costs of consuming capital assets, which vary according to their vintage, technological currency, and management’s estimate of their useful life. EBITDA comprises revenue less operating expenses before interest expense (income), property, plant and equipment amortization and depletion, and income taxes. Adjusted EBITDA has been included in this document. Under IFRS, entities must reflect in compensation expense the cost of share-based payments. In the Company’s circumstances, share-based payments involve a significant accrual of amounts that will not be settled in cash but are settled by the issuance of shares in exchange for cash. As such, the Company has made an entity specific adjustment to EBITDA for these expenses. The Company has also made an entity-specific adjustment to the foreign currency exchange (gain)/loss. The Company considers cash flow before movements in working capital to be the IFRS performance measure that is most closely comparable to adjusted EBITDA.

The following table provides a reconciliation of adjusted EBITDA to the consolidated financial statements for the three months and years ended December 31, 2022 and 2021:

Non-IFRS Reconciliation of Adjusted Net Income (Loss)

Adjusted net income (loss) attributable to shareholders represents net income (loss) attributable to shareholders excluding certain impacts, net of taxes, such as non-cash depletion charge due to the acquisition of Corona, impairment charges and reversal of impairment charges, write-down of assets, and certain non-cash and non-recurring items including but not limited to share-based compensation and foreign exchange (gain) loss.The Company believes that, in addition to conventional measures prepared in accordance with IFRS, certain investors may want to use this information to evaluate the Company’s performance and ability to generate cash flows. Accordingly, it is intended to provide additional information and should not be considered in isolation or as a substitute for measures of performance in accordance with IFRS.

The following table provides a reconciliation of adjusted net income (loss) to the consolidated financial statements for the three months and years ended December 31, 2022 and 2021:

Cash Cost per Silver Equivalent Payable Ounce and Copper Equivalent Payable Pound

The Company uses the non-IFRS measure of cash cost per silver equivalent ounce and copper equivalent payable pound to manage and evaluate operating performance. The Company believes that, in addition to conventional measures prepared in accordance with IFRS, certain investors use this information to evaluate the Company’s performance and ability to generate cash flows. Accordingly, it is intended to provide additional information and should not be considered in isolation or as a substitute for measures of performance prepared in accordance with IFRS. The Company considers cost of sales per silver equivalent payable ounce and copper equivalent payable pound to be the most comparable IFRS measure to cash cost per silver equivalent payable ounce, copper equivalent payable pound, and zinc equivalent payable pound, and has included calculations of this metric in the reconciliations within the applicable tables to follow.

All-in Sustaining Cost per Silver Equivalent Payable Ounce and Copper Equivalent Payable Pound

All‐In Sustaining Cost (“AISC”) is a non‐IFRS measure and was calculated based on guidance provided by the World Gold Council (“WGC”) in June 2013. WGC is not a regulatory industry organization and does not have the authority to develop accounting standards for disclosure requirements. Other mining companies may calculate AISC differently as a result of differences in underlying accounting principles and policies applied, as well as differences in definitions of sustaining versus development capital expenditures.

AISC is a more comprehensive measure than cash cost per ounce/pound for the Company’s consolidated operating performance by providing greater visibility, comparability and representation of the total costs associated with producing silver and copper from its current operations.

The Company defines sustaining capital expenditures as, “costs incurred to sustain and maintain existing assets at current productive capacity and constant planned levels of productive output without resulting in an increase in the life of assets, future earnings, or improvements in recovery or grade. Sustaining capital includes costs required to improve/enhance assets to minimum standards for reliability, environmental or safety requirements. Sustaining capital expenditures excludes all expenditures at the Company’s new projects and certain expenditures at current operations which are deemed expansionary in nature.”

Consolidated AISC includes total production cash costs incurred at the Company’s mining operations, including treatment and refining charges and selling costs, which forms the basis of the Company’s total cash costs. Additionally, the Company includes sustaining capital expenditures and corporate general and administrative expenses. AISC by mine does not include certain corporate and non‐cash items such as general and administrative expense and share-based payments. The Company believes that this measure represents the total sustainable costs of producing silver and copper from current operations and provides the Company and other stakeholders of the Company with additional information of the Company’s operational performance and ability to generate cash flows. As the measure seeks to reflect the full cost of silver and copper production from current operations, new project capital and expansionary capital at current operations are not included. Certain other cash expenditures, including tax payments, dividends and financing costs are also not included.

The following table provides a reconciliation of cash costs to cost of sales, as reported in the Company’s consolidated statement of income for the three months and years ended December 31, 2022 and 2021:

Additional Non-IFRS Measures

The Company uses other financial measures, the presentation of which is not meant to be a substitute for other subtotals or totals presented in accordance with IFRS, but rather should be evaluated in conjunction with such IFRS measures. The following other financial measures are used:

Operating cash flows before movements in working capital – excludes the movement from period-to-period in working capital items including trade and other receivables, prepaid expenses, deposits, inventories, trade and other payables and the effects of foreign exchange rates on these items.

The terms described above do not have a standardized meaning prescribed by IFRS, and therefore the Company’s definitions are unlikely to be comparable to similar measures presented by other companies. The Company’s management believes that their presentation provides useful information to investors because cash flows generated from operations before changes in working capital excludes the movement in working capital items. This, in management’s view, provides useful information of the Company’s cash flows from operations and are considered to be meaningful in evaluating the Company’s past financial performance or its future prospects. The most comparable IFRS measure is cash flows from operating activities.

About Sierra Metals

Sierra Metals is a diversified Canadian mining company with green metal exposure including copper, zinc and lead production with precious metals byproduct credits, focused on the production and development of its Yauricocha Mine in Peru and its Bolivar Mine in Mexico. The Company is focused on the safety and productivity of its producing mines. The Company also has large land packages with several prospective regional targets providing longer-term exploration upside and mineral resource growth potential.

For further information regarding Sierra Metals, please visit www.sierrametals.com.

This press release contains forward-looking information within the meaning of Canadian securities legislation. Forward-looking information relates to future events or the anticipated performance of Sierra and reflect management’s expectations or beliefs regarding such future events and anticipated performance based on an assumed set of economic conditions and courses of action, including the accuracy of the Company’s current mineral resource estimates; that the Company’s activities will be conducted in accordance with the Company’s public statements and stated goals; that there will be no material adverse change affecting the Company, its properties or its production estimates (which assume accuracy of projected ore grade, mining rates, recovery timing, and recovery rate estimates and may be impacted by unscheduled maintenance, labour and contractor availability and other operating or geo-political uncertainties on the Company’s production, workforce, business, operations and financial condition); the expected trends in mineral prices, inflation and currency exchange rates; that all required approvals will be obtained for the Company’s business and operations on acceptable terms; that there will be no significant disruptions affecting the Company’s operations. In certain cases, statements that contain forward-looking information can be identified by the use of words such as “plans”, “expects”, “is expected”, “budget”, “scheduled”, “estimates”, “forecasts”, “intends”, “anticipates”, “believes” or variations of such words and phrases or statements that certain actions, events or results “may”, “could”, “would”, “might”, or “will be taken”, “occur” or “be achieved” or the negative of these words or comparable terminology. Forward-looking statements include those relating to the Company’s guidance on the timing and amount of future production and its expectations regarding the results of operations; expected costs; permitting requirements and timelines; anticipated market prices of metals; the Company’s ability to comply with contractual and permitting or other regulatory requirements; formalizing the refinancing contract and the timeline related thereto and the timing of senior management’s conference call to discuss the Company’s financial and operating results for the year ended December 31, 2022. By its very nature forward-looking information involves known and unknown risks, uncertainties and other factors that may cause actual performance of Sierra to be materially different from any anticipated performance expressed or implied by such forward-looking information.

Forward-looking information is subject to a variety of risks and uncertainties, which could cause actual events or results to differ from those reflected in the forward-looking information, including, without limitation, the risks of not meeting the expectations contemplated herein and the risks described under the heading “Risk Factors” in the Company’s annual information form dated March 28, 2023 for its fiscal year ended December 31, 2022 and other risks identified in the Company’s filings with Canadian securities regulators, which filings are available at www.sedar.com.

The risk factors referred to above are not an exhaustive list of the factors that may affect any of the Company’s forward-looking information. Forward-looking information includes statements about the future and is inherently uncertain, and the Company’s actual achievements or other future events or conditions may differ materially from those reflected in the forward-looking information due to a variety of risks, uncertainties and other factors. The Company’s statements containing forward-looking information are based on the beliefs, expectations, and opinions of management on the date the statements are made, and the Company does not assume any obligation to update such forward-looking information if circumstances or management’s beliefs, expectations or opinions should change, other than as required by applicable law. For the reasons set forth above, one should not place undue reliance on forward-looking information.

Investor Relations Sierra Metals Inc. Tel: +1 (416) 366-7777 Email: info@christiana-papadopoulossierrametals-com

Noble Capital Markets Annual Investor Conference – NobleCon – to be held at Florida Atlantic University December 3-5

Boca Raton, FL, March 1, 2023 (GLOBE NEWSWIRE) — In a joint statement, Noble Capital Markets, Inc. (“Noble”) and Florida Atlantic University announced today that NobleCon19 – Noble’s 19th Annual Small Cap Investor Conference – will be held at the University’s College of Business Executive Education facility, Dec. 3-5, 2023, in Boca Raton, Florida. The 52,000 square foot, state-of-the-art facility was opened August 2020.

Noble has worked with the University for over a decade and was instrumental in the development of their Financial Analyst Program, and Noble’s Intern Program has generated great assets with graduates from the University. “We are extremely proud of our long-standing relationship with Florida Atlantic University,” said Nico Pronk, Noble’s President & CEO. “This new collaboration certainly elevates it to a whole new level.”

Vegar Wiik, Executive Director of the College of Business, Executive Education agrees, stating “Our vision for the College and this magnificent structure is to effectively integrate our curriculum with established businesses. Daniel Gropper, dean of FAU’s College of Business, said the financial industry is an important, integral part of the economy. “I can’t think of a better way to expose our students to the importance of emerging growth companies than to have 100 plus executive teams in the halls of our campus,” he said.

The entire College of Business Executive Education facility will transform into NobleCon19. Each presentation room will accommodate investors, in tiered seating with personal monitors. High-definition cameras, full-room microphones (to capture audience questions), three large screens, and full webcasting capabilities will offer the most technologically advanced conference environment on the circuit. Attendees will also experience similarly equipped rooms for panel presentations, private breakouts, and meetings, and in large gathering spaces, both indoors and out, as well as 800 free covered parking spaces. Florida Atlantic University is centrally located in Boca Raton, off I-95, only minutes from the Boca Raton Airport, and less than half an hour from Fort Lauderdale International Airport. Privaira, located at Boca Raton Airport is the official private air charter company for NobleCon19. A wide range of hotel accommodations are available within a five-mile radius, from economy to the ultra-luxurious “The Boca Raton.” Noble will be working with several properties to offer NobleCon19 attendees discounted rates.

The format of NobleCon will include company presentations followed by fire-side chats with Noble analysts, and select one-on-one meetings for qualified investors only, as well as several industry panel presentations. On the networking side, Noble is planning for informative keynote speakers and live entertainment, in an effort expand the business day in a more casual, conversational environment. All company presentations and panel discussions will be digitally streamed and made available exclusively on www.channelchek.com – Noble’s proprietary investment community portal.

Who should attend? Public companies from any business sector with market capitalizations of below $3-4 billion. Private companies planning a capital raise, considering becoming public, or an M&A event. NobleCon19 will suit every level of investor; high net worth individuals, family offices, self-directed investors, private equity, RIAs, financial advisors, equity analysts, and institutional investors. www.NobleCon19.com

About Florida Atlantic University

Florida Atlantic University, established in 1961, officially opened its doors in 1964 as the fifth public university in Florida. Today, the University serves more than 30,000 undergraduate and graduate students across six campuses located along the southeast Florida coast. In recent years, the University has doubled its research expenditures and outpaced its peers in student achievement rates. Through the coexistence of access and excellence, FAU embodies an innovative model where traditional achievement gaps vanish. FAU is designated a Hispanic-serving institution, ranked as a top public university by U.S. News & World Report and a High Research Activity institution by the Carnegie Foundation for the Advancement of Teaching. For more information, visit www.fau.edu.

About Noble Capital Markets

Noble Capital Markets, Inc. was incorporated in 1984 as a full-service SEC / FINRA registered broker-dealer, dedicated exclusively to serving underfollowed emerging growth companies through investment banking, wealth management, trading & execution, and equity research activities. Over the past 39 years, Noble has raised billions of dollars for companies and published more than 45,000 equity research reports. www.noblecapitalmarkets.comcontact@noblecapitalmarkets.com

PDS Biotech is a clinical-stage immunotherapy company developing a growing pipeline of molecularly targeted cancer and infectious disease immunotherapies based on the Company’s proprietary Versamune® and Infectimune™ T-cell activating technology platforms. Our Versamune®-based products have demonstrated the potential to overcome the limitations of current immunotherapy by inducing in vivo, large quantities of high-quality, highly potent polyfunctional tumor specific CD4+ helper and CD8+ killer T-cells. PDS Biotech has developed multiple therapies, based on combinations of Versamune® and disease-specific antigens, designed to train the immune system to better recognize diseased cells and effectively attack and destroy them. The Company’s pipeline products address various cancers including HPV16-associated cancers (anal, cervical, head and neck, penile, vaginal, vulvar) and breast, colon, lung, prostate and ovarian cancers.

Robert LeBoyer, Vice President, Research Analyst, Life Sciences , Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

FY2022 Reported With Clinical Progress Updates. PDS Biotech reported a 4Q22 loss of $19.1 million or $(0.61) per share and a FY2022 loss of $40.9 million or $(1.43) per share. The loss included $10 million in licensing fees for PDS0301, paid with $5 million in cash and $5 million in stock. Management updated its plans for Phase 3 trials for PDS0101 and PDS0301 during 2023. Cash on hand on December 31, 2022 was $73.8 million, which is expected to fund operations through 3Q24.

PDS Expects To Begin VERSATILE-003 In 4Q23. The Phase 2 VERSATILE-002 trial has reported strong results testing PDS0101 with Keytruda (pembrolizumab, a checkpoint inhibitor) for recurrent or metastatic head and neck cancer. Based on this data, PDS has received FDA guidance for the Phase 3 VERSATILE-003 trial. The trial protocols are being finalized with an IND submission expected in 2H23 and start of enrollment in 4Q23.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

ARLP is a diversified natural resource company that generates operating and royalty income from coal produced by its mining complexes and royalty income from mineral interests it owns in strategic oil & gas producing regions in the United States, primarily the Permian, Anadarko and Williston basins. ARLP currently produces coal from seven mining complexes its subsidiaries operate in Illinois, Indiana, Kentucky, Maryland and West Virginia. ARLP also operates a coal loading terminal on the Ohio River at Mount Vernon, Indiana. ARLP markets its coal production to major domestic and international utilities and industrial users and is currently the second largest coal producer in the eastern United States. In addition, ARLP is positioning itself as an energy provider for the future by leveraging its core technology and operating competencies to make strategic investments in the fast growing energy and infrastructure transition.

Mark Reichman, Senior Research Analyst, Natural Resources, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

Lowering estimates. We have lowered our 2023 EBITDA and earnings per share estimates to $1.09 billion and $5.50 from $1.14 billion and $5.90, respectively. While we lowered our first half revenue expectations, our full year revenue estimate was increased based on greater contributions from the coal segment and expectations for an improved commodity price environment in the second half of the year. Notably, we refined and increased our operating cost estimates to reflect higher labor costs, sales-related expenses, and operational costs related to longwall moves within the mining segment.

First half challenged by declining commodity prices. Prices for crude oil and natural gas have declined throughout the year. While coal prices have softened in recent weeks, 34.7 million tons of the partnership’s 2023 planned coal sales, or 94% at the mid-point of guidance, were committed and priced as of the date of ARLP’s fourth quarter conference call. Year-to-date through March 28, crude oil and natural gas futures prices averaged $76.33 per barrel and $2.84 per thousand cubic feet (Mcf) compared to $80.47 per barrel and $4.48 per Mcf at the end of 2022 and $73.38 per barrel and $2.16 per Mcf as of March 28. As a result, we lowered our expectations for the oil & gas royalty segment.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

SVB’s Newfangled Failure Fits a Century-Old Pattern of Bank Runs, With a Social Media Twist

The history of bank failures all have a familiar pattern. Based on past history, problems may still bubble up over the coming months. The internet and the ability for online withdrawals could elevate risks to banks. Rodney Ramcharan a Professor of Finance and Business Economics, University of Southern California, points out the similarities, the new challenges and provides his thoughts in his article that has been reprinted with permission from The Conversation.

The failure of Silicon Valley Bank on March 10, 2023, came as a shock to most Americans. Even people like myself, a scholar of the U.S. banking system who has worked at the Federal Reserve, didn’t expect SVB’s collapse.

Usually banks, like all companies, fail after a prolonged period of lackluster performance. But SVB, the nation’s 16th-largest bank, had been stable and highly profitable just a few months before, having earned about US$1.5 billion in profits in the last quarter of 2022.

However, financial history is filled with examples of seemingly stable and profitable banks that unexpectedly failed.

The demise of Lehman Brothers and Bear Stearns, two prominent investment banks, and Countrywide Financial Corp., a subprime mortgage lender, during the 2008-2009 financial crisis; the Savings and Loan banking crisis in the 1980s; and the complete collapse of the U.S. banking system during the Great Depression didn’t unfold in exactly the same way. But they had something in common: An unexpected change in economic conditions created an initial bank failure or two, followed by general panic and then large-scale economic distress.

The main difference this time, in my view, is that modern innovations may have hastened SVB’s demise.

Great Depression

The Great Depression, which lasted from 1929 to 1941, epitomized the public harm that bank runs and financial panic can cause.

Following a rapid expansion of the “Roaring Twenties,” the U.S. economy began to slow in early 1929. The stock market crashed on Oct. 24, 1929 – a date known as “Black Tuesday.”

The massive losses investors suffered weakened the economy and led to distress at some banks. Fearing that they would lose all their money, customers began to withdraw their funds from the weaker banks. Those banks, in turn, began to rapidly sell their loans and other assets to pay their depositors. These rapid sales pushed prices down further.

As this financial crisis spread, depositors with accounts at nearby banks also began queuing up to withdraw all their money, in a quintessential bank run, culminating in the failure of thousands of banks by early 1933. Soon after President Franklin D. Roosevelt’s first inauguration, the federal government resorted to shutting all banks in the country for a whole week.

These failures meant that banks could no longer lend money, which led to more and more problems. The unemployment rate spiked to around 25%, and the economy shrank until the outbreak of World War II.

Determined to avoid a repeat of this debacle, the government tightened banking regulations with the Glass-Steagall Act of 1933. It prohibited commercial banks, which serve consumers and small and medium-size businesses, from engaging in investment banking and created the Federal Deposit Insurance Corporation, which insured deposits up to a certain threshold. That limit has risen sharply over the past 90 years, from $2,500 in 1933 to $250,000 in 2010 – the same limit in place today.

S&L Crisis

The nation’s new and improved banking regulations ushered in a period of relative stability in the banking system that lasted about 50 years.

But in the 1980s, hundreds of the small banks known as savings and loan associations failed. Savings and loans, also called “thrifts,” were generally small local banks that mainly made mortgage loans to households and collected deposits from their local communities.

Beginning in 1979, the Federal Reserve began to hike interest rates very aggressively to fight the high inflation rates that had become entrenched.

By the early 1980s, Congress began allowing banks to pay market interest rates on depositers’ accounts. As a result, the interest rate S&Ls had to pay their customers was much higher than the interest income they were earning on the loans they had made in prior years. That imbalance caused many of them to lose money.

Even though about 1 in 3 S&Ls failed from around 1986 through 1992 – somewhere around 750 banks – most depositors at small S&Ls were protected by the FDIC’s then-$100,000 insurance limit. Ultimately, resolving that crisis cost taxpayers the equivalent of about $250 billion in today’s dollars.

Because the savings and loans industry was not directly connected to the big banks of that era, their collapse did not cause runs at the bigger institutions. Nevertheless, the S&L collapse and the government’s regulatory response did reduce the supply of credit to the economy.

As a result, the U.S. economy underwent a mild recession in the latter half of 1990 and first quarter of 1991. But the banking system escaped further distress for nearly two decades.

Great Recession

Against this backdrop of relative stability, Congress repealed most of Glass-Steagall in 1999 – eliminating Depression-era regulations that restricted the scope of businesses that banks could engage in.

Those changes contributed to what happened when, at the start of a recession that began in December 2007, the entire financial sector suffered a panic.

At that time, large banks, freed from the Depression-era restrictions on securities trading, as well as investment banks, hedge funds and other institutions outside the traditional banking system, had heavily invested in mortgage-backed securities, a kind of bond backed by pooled mortgage payments from lots of homeowners. These bonds were highly profitable amid the housing boom of that era, and they helped many financial institutions reap record profits.

But the Federal Reserve had been increasing interest rates since 2004 to slow the economy. By 2007, many households with adjustable-rate mortgages could no longer afford to make their larger-than-expected home loan payments. That led investors to fear a rash of mortgage defaults, and the values of securities backed by mortgages plunged.

It wasn’t possible to know which investment banks owned a lot of these vulnerable securities. Rather than wait to find out and risk not getting paid, most of the depositors rushed to get their money out by late 2007. This stampede led to cascading failures in 2008 and 2009, and the federal government responded with a series of big bailouts.

The government even bailed out General Motors and Chrysler, two of the country’s three largest automakers, in December 2008 to keep the industry from going bankrupt. That happened because the major car companies relied on the financial system to provide potential car buyers with credit to purchase or lease new cars. But when the financial system collapsed, buyers could no longer obtain credit to finance or lease new vehicles.

The Great Recession lasted until June 2009. Stock prices plummeted by more than 50%, and unemployment peaked at around 10% – the highest rate since the early 1980s.

As with the Great Depression, the government responded to this financial crisis with significant new regulations, including a new law known as the Dodd-Frank Act of 2010. It imposed stringent new requirements on banks with assets above $50 billion.

Close-Knit Customers

Congress rolled back some of Dodd-Frank’s most significant changes only eight years after lawmakers approved the measure.

Notably, the most stringent requirements were now reserved for banks with more than $250 billion in assets, up from $50 billion. That change, which Congress passed in 2018, paved the way for regional banks like SVB to rapidly expand with much less regulatory oversight.

But still, how could SVB collapse so suddenly and without any warning?

Banks take deposits to make loans. But a loan is a long-term contract. Mortgages, for example, can last for 30 years. And deposits can be withdrawn at any time. To reduce their risks, banks can invest in bonds and other securities that they can quickly sell in case they need funds for their customers.

In the case of SVB, the bank invested heavily in U.S. Treasury bonds. Those bonds do not have any default risk, as they are debt issued by the federal government. But their value declines when interest rates rise, as newer bonds pay higher rates compared with the older bonds.

SVB bought a lot of Treasury bonds it had on hand when interest rates were close to zero, but the Fed has been steadily raising interest rates since March 2022, and the yields available for new Treasurys sharply increased over the next 12 months. Some depositors became concerned that SVB might not be able to sell these bonds at a high enough price to repay all its customers.

Unfortunately for SVB, these depositors were very close-knit, with most in the tech sector or startups. They turned to social media, group text messages and other modern forms of rapid communication to share their fears – which quickly went viral.

Many large depositors all rushed at the same time to get their funds out. Unlike what happened nearly a century earlier during the Great Depression, they generally tried to withdraw their money online – without forming chaotic lines at bank branches.

Will More Shoes Drop?

The government allowed SVB, which is being sold to First Citizens Bank, and Signature Bank, a smaller financial institution, to fail. But it agreed to repay all depositors – including those with deposits above the $250,000 limit.

While the authorities have not explicitly guaranteed all deposits in the banking system, I see the bailout of all SVB depositors as a clear signal that the government is prepared to take extraordinary steps to protect deposits in the banking system and prevent an overall panic.

I believe that it is too soon to say whether these measures will work, especially as the Fed is still fighting inflation and raising interest rates. But at this point, major U.S. banks appear safe, though there are growing risks among the smaller regional banks.

Washington DC Law Firm that Won Operation Choke Hold Suit, Gives Congress Advice

Are private digital assets, under unlawful attack by regulators? Sounds conspiratorial, but a D.C. law firm that successfully sued the FDIC, Federal Reserve, and Office of the Controller of the Currency (OCC), says they are doing just that. The firm Cooper & Kirk, won a large lawsuit dubbed against the agencies for their part in, “Operation Choke Point.” That was a decade ago, the law firm now claims they have uncovered a coordinated campaign by bank regulators to drive crypto out of the U.S. financial system.

The new “Operation Choke Point 2.0,” according to the firms website, “have published informal guidance documents that single out cryptocurrency and cryptocurrency customers as a risk to the banking system.” According to an informational paper published by the D.C. firm, “businesses in the cryptocurrency marketplace are losing their bank accounts, or their access to the ACH network, suddenly, and with no explanation from their bankers, the paper continued, “the owners and employees of cryptocurrency firms are even having their personal accounts closed without explanation.”

As an example of could be viewed as overstepping their charters, the firm pointed out that, “over the past two weeks, federal regulators have shut down a solvent bank that was known to be serving the crypto industry and, although it is required to resolve banks through the “least cost resolution” to the Deposit Insurance Fund, the FDIC chose to shutter rather than sell the part of the bank that serves digital asset customers, costing the Fund billions of dollars.” The overall theme of the 37 page paper is that the targeting of certain businesses is going on to force them out of existence.

Depriving businesses of their constitutional right to due process. This is a fifth amendment right that says that an entity tagging another with a derogatory label that causes injury (like lose bank accounts) The firm accuses that this is what the regulators have done by “labeling crypto a threat to the financial system.”

Violating both the non-delegation and anticommandeering doctrine by, “depriving Americans of Key Structural constitutional protections against the arbitrary exercise of government power.”

Refusing to perform their non-discretionary duties “when doing so will benefit the cryptocurrency industry.”

Evading rules that require periods of notice and comment of the rulemaking requirements of the administrative procedure act. It claims circumventing this is, “undemocratic.”

Acting in an arbitrary and capricious fashion by avoiding explaining underlying rules for their decisions. “It is difficult to imagine a more arbitrary and capricious agency action that simultaneously placing a solvent bank into receivership solely because it provided financial services to the cypto industry, while permitting insolvent institutions not tied to the crypto industry to continue operations.”

What is the Law Firms Stated Intent

Cooper and Kirk urge the U.S. Congress to perform its role and hold the agencies accountable. The firm urges the Congress to ask for all communications records related to these matters from the regulators.

The firm also would like for them to explain the basis for their conclusion that safety and soundness of the banking system requires the banking system be insulated from crypto. They would also like for it to be made clear to the agencies that the comment period of the Administrative procedure act is mandatory. It wanst an investigation into why Signature Bank was closed.

The last stated hope is fro Congress to investigate whether bank regulators are working to squelch innovation from the private sector in order to clear out competition for the benefit of existing regulated banks and a new federal crypto asset.

Take Away

Just like the first Operation Choke Point was targeting specific players, the new version does the same. The law firms stops short of any threats in their open paper, but it makes clear that the firm has solid experience achieving compliance if these maters.

Baudax Bio is a pharmaceutical company focused on innovative products for acute care settings. ANJESO is the first and only 24-hour, intravenous (IV) COX-2 preferential non-steroidal anti-inflammatory (NSAID) for the management of moderate to severe pain. In addition to ANJESO, Baudax Bio has a pipeline of other innovative pharmaceutical assets including two novel neuromuscular blocking agents (NMBs) and a proprietary chemical reversal agent specific to these NMBs. For more information, please visit www.baudaxbio.com.

Gregory Aurand, Senior Research Analyst, Healthcare Services & Medical Devices, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.