The Connection Between Producer Price (PPI) and Consumer Price (CPI) Inflation

Does a higher PPI mean a higher CPI? A newly released report shows U.S. suppliers raised prices by 0.4% in September from August, when the Producer Price Index report had shown a 0.2% drop. The inflation measure that has impacted the stock market most severely this year is the Consumer Price Index. The two Bureau of Labor Statistics (BLS) releases are related but not directly correlated and are often used to measure different things by economists and those in industry.

The PPI rose 8.5% in September from a year before, down from its 8.7% annual increase in August and 11.3% in June. – BLS

How CPI and PPI are Different

The PPI for personal consumption includes all marketable production sold by U.S.-domiciled businesses for personal consumption. The majority of the products sold by domestic producers come from non-governmental sectors. However, government produces some marketable output that is under the PPI umbrella. In contrast to the PPI’s components, CPI includes goods and services provided by businesses or governments when direct costs to the consumer are levied.

The most heavily weighted item in CPI is rent. It’s weighted at 24% of the index. What the BLS calls owners’ equivalent rent is the implied rent occupants would have to pay if they were renting their homes. This is how the Bureau of Labor Statistics captures the cost of housing for owner-occupied and rented housing. This heavily weighted component is not in PPI – obviously, owners’ equivalent rent is not a domestically produced output.

The PPI for personal consumption and the CPI also differ in their treatment of imports. The CPI includes, within its basket, goods and services purchased by domestic consumers and therefore includes imports. The PPI, in contrast, does not include imports because imports are, by definition, not produced by domestic firms.

How PPI Impacts CPI

The PPI trends often work their way into consumer price movements, but not at a one-to-one basis or even a standard delayed interval. The demand component of consumer’s impact, what the consumers are willing to consume at certain price levels, is at play with what is charged for goods at the retail level. So even if the cost to manufacture goods has risen, passing the cost on is not always possible without hurting sales. At some level of price increases, demand decreases. This is different for each type of product. For instance, food, medical care, and housing may not be impacted as much as recreation, clothing, and other items which are easier to put off or do without.

Companies are trying to manage higher costs without alienating consumers who are weary of price increases. So far in the 2022 U.S. economy, consumer spending has remained strong despite the rate of CPI, but economists worry that we’re approaching a tipping point.

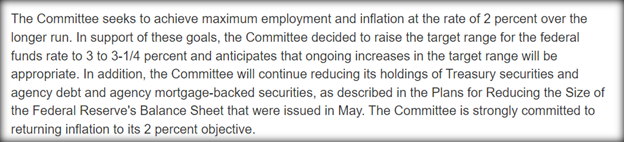

The Fed has raised the benchmark federal funds rate at its last three meetings by 0.75 percentage points, it now sits in the range of 3% and 3.25%. Officials have indicated they are prepared to raise rates over the course of their final two gatherings this year to around 4.25%.

Today, with consumer inflation running at a four-decade high and savings measurements trending lower, consumers are expected to begin to change buying habits. This overall is bad for business and the economy, which is why the Federal Reserve is expected to continue its fight against price increases, despite their lack of popularity with the financial markets.

“Monetary policy will be restrictive for some time to ensure that inflation moves back” Fed Vice Chair Lael Brainard (October 10).

Prices have begun to fall for some goods and services, including commodities, freight shipping, and housing. Those declines have led some Fed watchers to warn that the central bank risks tightening financial conditions too much.

Take Away

Increases in producer prices are passed to consumers when they can be. However, there is only so much a consumer is willing to pay for a purchase they can put off or substitute for something cheaper. This has ramifications for investors.

Companies where demand will wain when prices rise, may find earnings weaken; these could include producers of discretionary goods. Stocks that are shares of consumer staple companies may not feel the brunt of consumer pushback; those that produce more cost-effective brands, including white label providers, may outshine their brand name competitors if consumers increase their substituting for lower priced alternatives. Health care is one area where demand changes little as prices change at the producer or consumer level.

Managing Editor, Channelchek

Sources

https://www.wsj.com/articles/producer-prices-inflation-september-2022-11665541647?mod=hp_lead_pos2