Why Diversify Your Portfolio Into Smaller Government Contractors

Will there be a recession, or will the Fed orchestrate a rare soft landing? Coming off a down year last year, with the stock market now up mid-year by 7%, which is the average expected return for a full year of the broader indexes, many investors find themselves straddling a fence. On one side of the fence is the fear of missing out (FOMO), and on the other is a money market rate that is higher than it has been in decades. In a weakening economy, investors don’t have to exit the stock market completely to find stocks that are not expected to be negatively impacted. Until there is more clarity, perhaps it is worth taking a portion of your holdings on a side trip, to look at government contractors.

When company earnings are dependent on the consumer, its stock price may be tied to the pace of the economy – it’s likely to at least be correlated to activity within its industry. While many investment options are available, one often overlooked but potentially rewarding segment is companies that generate revenue through government contracts, not consumer sales or business-to-business. Let’s explore the benefits of investing in such companies, particularly smaller ones where a new contract is most impactful to the bottom line. These company’s still have above average growth potential but can be quite resilient during economic downturns.

Stable Revenue Streams

Companies that secure government contracts often enjoy stable and predictable revenue streams, they also are billing an entity that can tax and is not reliant on stable earnings itself. Government contracts typically involve long-term agreements that provide a consistent flow of income for the duration of the contract. This stability can be particularly beneficial for investors seeking reliable returns on their investments. Aerospace companies, for instance, often receive substantial contracts for the production and maintenance of military aircraft, providing a steady stream of income.

Reduced Vulnerability to Recessions

One of the key advantages of investing in companies with government contracts is their potential indifference to economic downturns. During recessions or periods of economic uncertainty, government spending has even been known to increase as a means to stimulate a weak economy. This increased spending often benefits companies with government contracts, as governments prioritize projects related to defense, infrastructure development, and public services. This makes aerospace and dredging companies, which are heavily involved in such projects, relatively impervious to recessions.

Long-Term Growth Opportunities

Government contracts often involve large-scale projects that span several years or even decades. This long-term nature provides companies with ample opportunities for growth and expansion. For example, aerospace companies may secure contracts to develop advanced military aircraft, including drones, or provide satellite-based communication systems. Similarly, dredging companies might be contracted for extensive port development projects. These opportunities allow companies to invest in research, development, and innovation, positioning them for sustained growth and profitability.

Competitive Advantage of Being Established

Government contracts typically involve rigorous bidding processes and stringent eligibility criteria. Companies that successfully secure these contracts gain a competitive advantage over their peers. Once established, they often become preferred suppliers for subsequent projects, further solidifying their market position. This advantage can translate into increased market share, higher profitability, and enhanced investor confidence, making these companies attractive for long-term investments.

Great Lakes Dredge & Dock Corporation (GLDD) would seem to fit the above criteria. It is the largest provider of dredging services in the United States, and is engaged in expanding its core business into the rapidly developing offshore wind energy industry. Great Lakes also has a history of securing significant international projects. GLDD has a 132-year history, has a market-cap of $542 million, and is up 37% year-to-date.

The most recent research note from Noble Capital Markets on GLDD is available here.

Kratos Defense & Security Solutions, Inc. (KTOS), a military contractor that has admirable specialties compared to the large names that typically come to mind. Kratos is changing the way transformative breakthrough technology for the industry is rapidly brought to market through proven approaches, including proactive research and streamlined development processes. KTOS treats affordability as a technology that needs to be considered. It specializes in unmanned systems, satellite communications, cyber security/warfare, microwave electronics, missile defense, hypersonic systems, training, combat systems and next generation turbo jet and turbo fan engine development. KTOS has a $1.72 billion market-cap and is up 31% year-to-date.

The most recent research note from Noble Capital Markets on KTOS is available here.

Technological Advancements and Spin-Off Opportunities

Working on government contracts often requires companies to push the boundaries of technology and innovation. Aerospace companies, for example, are at the forefront of developing advanced defense systems, satellite technologies, and commercial aircraft. Similarly, dredging companies and those involved in wind energy may invest in state-of-the-art equipment and techniques to execute complex infrastructure projects. These advancements can lead to spin-off opportunities in commercial markets, expanding the company’s revenue streams beyond government contracts.

Take Away

Investing in companies that recieve revenue primarily through government contracts, particularly those that are small cap companies, may provide a recession-fearful investor with some comfort that the stock(s) they are investing in are less likely to suffer from consumers tightening their wallets, yet they have potential to grow.

As with all investing and forecasting the future, if it was easy, everyone would already be doing it. But, the two examples listed above may be a good start to help inspire discovering stocks that are situated differently than traditional consumer or business-to-business companies.

SAN DIEGO, June 05, 2023 (GLOBE NEWSWIRE) — Kratos Defense & Security Solutions, Inc. (NASDAQ: KTOS), a Technology Company in the Defense, National Security and Global Markets, has been awarded a contract by the Naval Surface Warfare Center Dahlgren Division (NSWCDD) for thermo-mechanical and aerothermal ground testing of thermal protection system materials in ballistic reentry and reentry-like environments in its Kratos SRE business unit in Birmingham, Alabama. The five-year contract includes options with a total value up to $46.7 million, with an initial award of $8.6 million under a cost-plus-fixed-fee contract.

The effort will test materials supporting technical efforts for the U.S. and the U.K. with direct oversight from the NSWCDD Reentry Systems Office. The support includes sample preparation, instrumentation, testing and gathering thermo-mechanical data on materials at extremely high temperatures and in high heat flux/shear environments. The contract enables Kratos SRE to conduct ground testing of thermal protection materials at external ground test facilities and produce flight hardware for the Navy. It requires the unique ability to test and collect data at maximum temperatures of 5,500 degrees Fahrenheit to properly test materials in reentry-like environments.

Michael Johns, Senior Vice President of Kratos SRE, said, “We are honored to support NSWCDD for this important program and are proud that we have been able to do so for decades. We bring a unique capability to this program and through the hard work of our expert team, we look forward to helping our nation as part of the larger Navy team.”

Dave Carter, President of Kratos’ Defense & Rocket Support Services Division, said, “Our division has a long and valued relationship with the Navy supporting research rocket and ballistic missile target programs. The addition of the NSWCDD RSO work by adding KSRE to our division team is exciting, and we look forward to continuing our role as a trusted provider for the Navy.”

Kratos SRE, formerly part of Southern Research and acquired by Kratos in May 2022, is an advanced concept group within Kratos’ Defense & Rocket Support Services (KDRSS) Division. SRE currently employs about 175 engineers, technicians and program support professionals conducting work in support of the space community, the Department of Defense and other national security customers.

About Kratos Defense & Security Solutions Kratos Defense & Security Solutions, Inc. (NASDAQ: KTOS) is a Technology Company that develops and fields transformative, affordable systems, products and solutions for United States National Security, our allies and global commercial enterprises. At Kratos, Affordability is a Technology, and Kratos is changing the way breakthrough technology is rapidly brought to market – at a low cost – with actual products, systems and technologies rather than slide decks or renderings. Through proven commercial and venture capital backed approaches, including proactive, internally funded research and streamlined development processes, Kratos is focused on being First to Market with our solutions, well in advance of competition. Kratos is the recognized Technology Disruptor in our core market areas, including Space and Satellite Communications, Cyber Security and Warfare, Unmanned Systems, Rocket and Hypersonic Systems, Next-Generation Jet Engines and Propulsion Systems, Microwave Electronics, C5ISR and Virtual and Augmented Reality Training Systems. For more information, please visit www.KratosDefense.com.

Notice Regarding Forward-Looking Statements Certain statements in this press release may constitute “forward-looking statements” within the meaning of the Private Securities Litigation Reform Act of 1995. These forward-looking statements are made on the basis of the current beliefs, expectations, and assumptions of the management of Kratos and are subject to significant risks and uncertainty. Investors are cautioned not to place undue reliance on any such forward-looking statements. All such forward-looking statements speak only as of the date they are made, and Kratos undertakes no obligation to update or revise these statements, whether as a result of new information, future events or otherwise. Although Kratos believes that the expectations reflected in these forward-looking statements are reasonable, these statements involve many risks and uncertainties that may cause actual results to differ materially from what may be expressed or implied in these forward-looking statements. For a further discussion of risks and uncertainties that could cause actual results to differ from those expressed in these forward-looking statements, as well as risks relating to the business of Kratos in general, see the risk disclosures in the Annual Report on Form 10-K of Kratos for the year ended December 25, 2022, and in subsequent reports on Forms 10-Q and 8-K and other filings made with the SEC by Kratos.

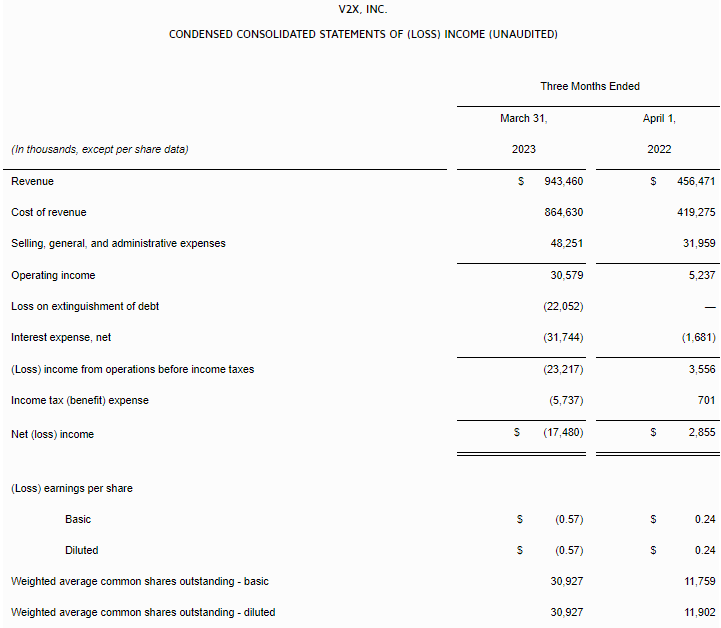

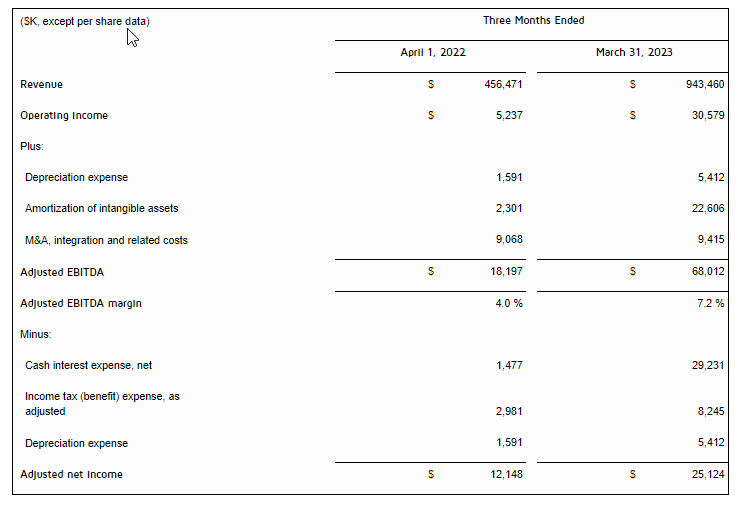

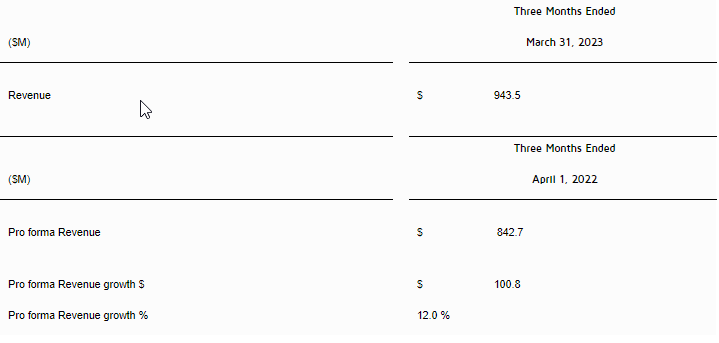

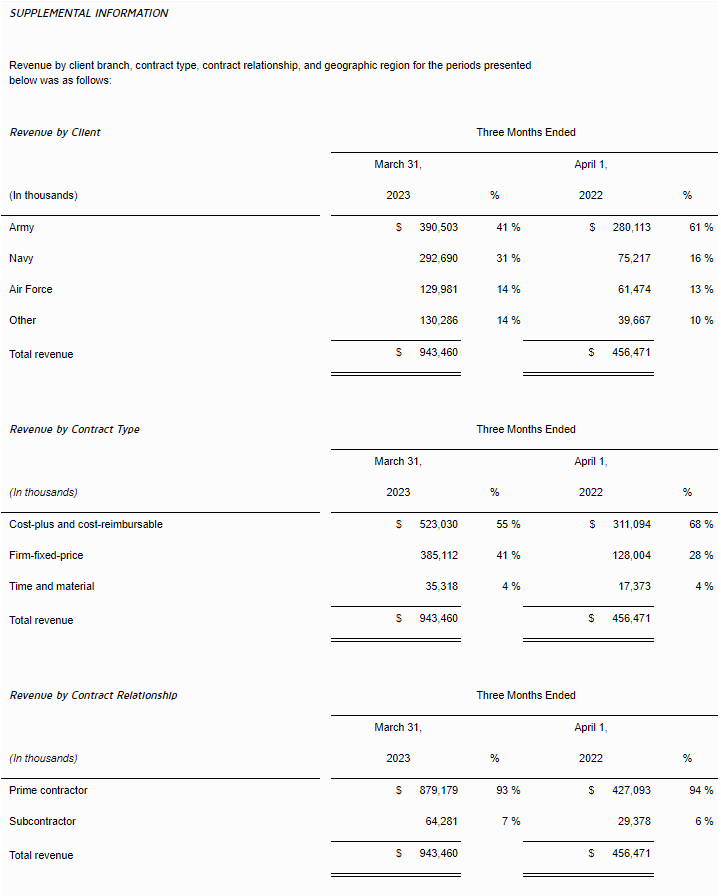

Revenue of $943.5 million, up 12.0% y/y on a pro forma basis

Continued expansion in the Pacific driving strong revenue growth of ~300% y/y

Awarded new contracts valued at ~$600 million and secured ~$250 million in recompetes

Reported operating income of $30.6 million; adjusted operating income1 of $62.6 million

Adjusted EBITDA1 of $68.0 million with a margin1 of 7.2%

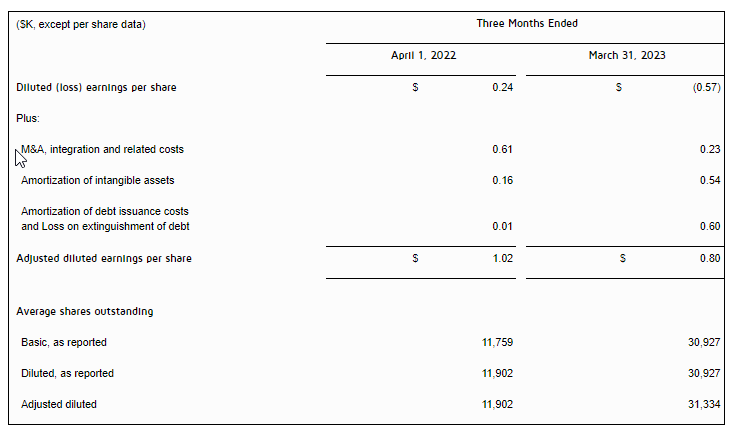

Diluted EPS of ($0.57); adjusted diluted EPS1 of $0.80

2023 Guidance:

Reiterating full-year 2023 guidance

MCLEAN, Va., May 9, 2023 /PRNewswire/ — V2X, Inc. (NYSE:VVX) announced first quarter 2023 financial results.

“V2X reported an excellent start to the year with revenue increasing 12.0% year-over-year, on a pro forma basis during the first quarter,” said Chuck Prow, President and Chief Executive Officer of V2X. “Adjusted EBITDA for the quarter was $68.0 million or a 7.2% margin and reflects a benefit from strong revenue volume and program productivity. The pace of award activity is improving and was exemplified by approximately $600 million in new business awarded to V2X. With over $4 billion in bids under evaluation and a robust backlog of ~$12 billion, the outlook for V2X remains solid.”

“Revenue growth in the quarter was generated by continued expansion on existing programs, contribution from new awards, as well as success in securing recompete wins late last year and in early 2023,” said Mr. Prow. “Our teams continued to drive momentum with several notable wins in the quarter. This has been achieved while successfully expanding on our core programs. Importantly, we continue to experience significant growth in the Pacific or INDOPACOM, with our presence and footprint in the region proving to be a key channel to support increasing mission requirements.”

Mr. Prow continued, “Our growth activities during the quarter were robust. In March, we were awarded two strategically important new business contracts. Firstly, we were the successful bidder on the Naval Test Wing Pacific contract valued at $440 million over seven years, which further builds on the services V2X is providing under the $880 million Naval Test Wing Atlantic program. This effort to support the critical test and evaluation activities performed by the Naval Test Wing Pacific leveraged V2X’s proprietary and innovative technology-based solution, AMMO®, and demonstrates our commitment to maintaining high levels of mission readiness. We are honored to be selected to support the Navy’s preeminent organization for flight testing and flight test support of the latest systems. Secondly, V2X was also awarded a three-year, approximately $100 million contract to provide critical cybersecurity support services to a government client. This is a key win for V2X in the cyber and IT support domain and leverages our core mission of intersecting our technology and operations capabilities.”

“In addition, during the first quarter, we were awarded over $250 million in recompetes,” said Mr. Prow. “This includes a five-year, $142 million contract with Naval Air Systems Command (NAVAIR) PMA 281 in support of mission planning systems. PMA-281 is responsible for the acquisition and life cycle management of a range of mission planning, control system and execution tools that are developed and integrated in partnership with other services, and foreign nation partners. This recompete win with the Navy represents successful execution on this deliberate client engagement campaign. We also secured a five-year recompete contract valued at over $90 million with a National Security client. Transition to the new contract is complete and I’d like to thank our team for their exceptional performance and dedication to this important client.”

Mr. Prow concluded, “The significant momentum in harnessing combined V2X solutions offers an opportunity to deliver growth with access to pursuits that would not have been achievable in the past. We remain focused on delivering on our strategy to drive growth by creating more value in our core markets with converged solutions, increasing market share where our operational knowledge sets us apart, and expanding mission capabilities into adjacent markets.”

First Quarter 2023 Results

On July 5, 2022 (“Closing Date”), Vectrus, Inc. (“Vectrus”) completed its merger (“the Merger”) with Vertex Aerospace Services Holding Corp. (“Vertex”), thereby forming V2X, Inc. First quarter 2022 “reported results” reflect the contributions of Vectrus from January 1, 2022, through March 31, 2022, unless otherwise noted. Comparisons to historical periods are relative to legacy Vectrus results, unless otherwise noted.

Revenue of $943.5 million, up 12.0% y/y on a pro forma basis

Operating income of $30.6 million, including merger and integration related costs of $9.4 million, and amortization of acquired intangible assets of $22.6 million

Adjusted operating income1 of $62.6 million

Adjusted EBITDA1 of $68.0 million with a 7.2% adjusted EBITDA margin1

Diluted EPS of ($0.57)

Adjusted diluted EPS1 of $0.80

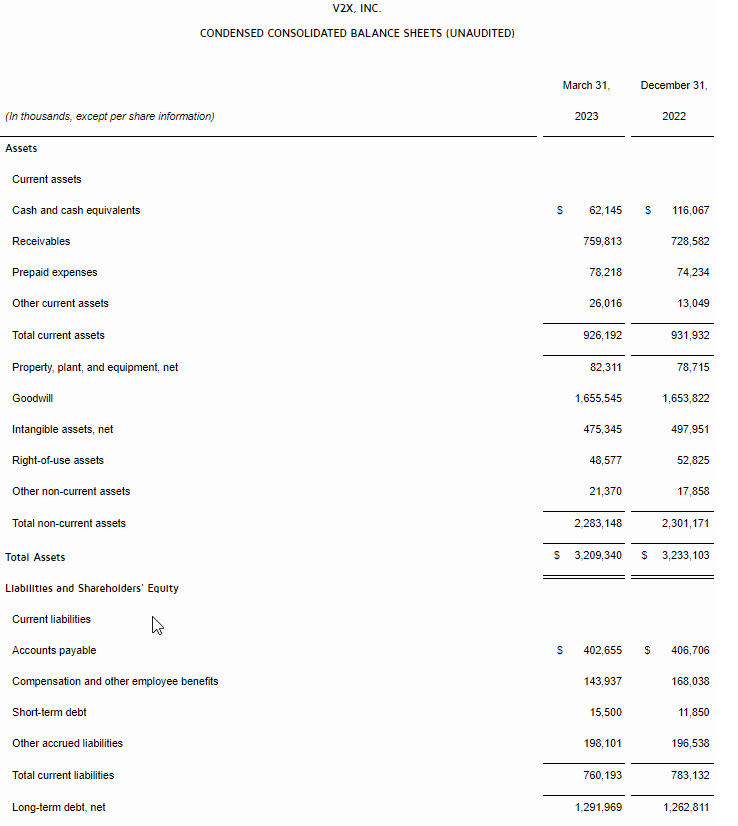

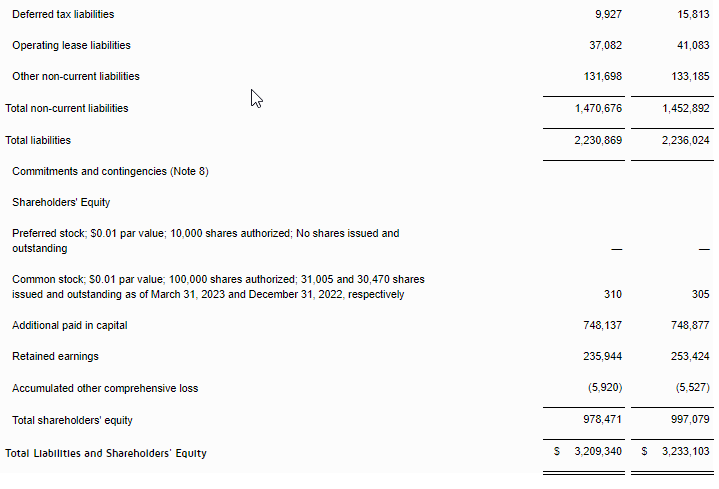

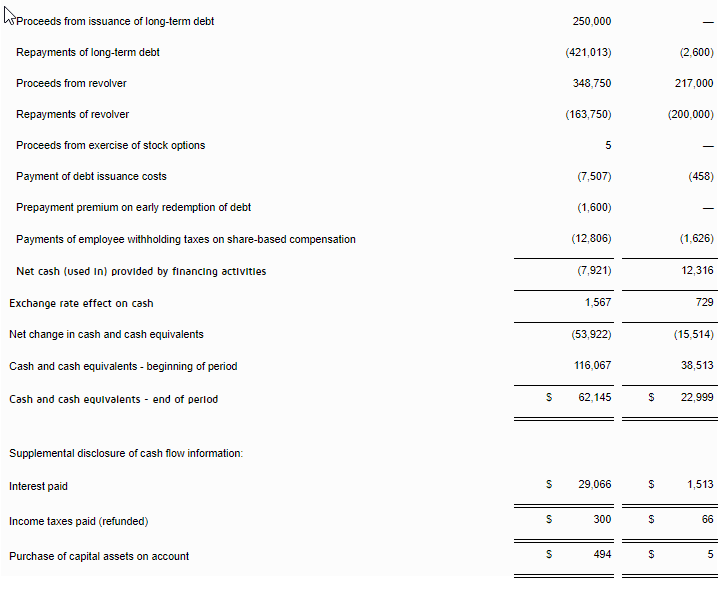

Net debt as of March 31, 2023 of $1,288.6 million

Total backlog as of March 31, 2023 of $11.8 billion

“Our first quarter financial results were a strong start to the year,” said Susan Lynch, Senior Vice President and Chief Financial Officer. “Pro forma revenue increased 12.0% year-over-year to $943.5 million. Revenue growth was driven by momentum in the Pacific, expansion on existing programs, and the contribution from new business wins awarded in 2022 and 2023. Notably, revenue from the Pacific increased approximately 300% year-over-year and 18% sequentially, reflecting our agile readiness position to support the increased operational tempo of mission exercises in the region.”

For the quarter, the Company reported operating income of $30.6 million and adjusted operating income1 of $62.6 million. Adjusted EBITDA1 was $68.0 million with a margin of 7.2%. First quarter diluted EPS was ($0.57), due primarily to merger and integration related costs, loss on extinguishment of debt, amortization of acquired intangible assets, and interest expense. Adjusted diluted EPS1 for the quarter was $0.80 cents.

Ms. Lynch continued, “In the first quarter, V2X successfully enhanced its capital structure through a lower cost credit facility with greater liquidity. The new $750 million credit facility eliminated the second lien term loan B, the incremental portion of the first lien term loan B, and the asset-based loan revolver and was replaced with a lower cost $500 million revolver and a $250 million term loan A. In order to manage interest rate risk and uncertainty, the Company also entered into interest rate swaps, converting 30% of its variable-rate term loan debt into fixed rate-debt. I would like to thank our banking partners for their support and trust in our business. At the end of the quarter, our net consolidated indebtedness to EBITDA1 (net leverage ratio) was 3.8x. We are focused on reducing debt and expect that our leverage ratio will show further improvement in 2023.”

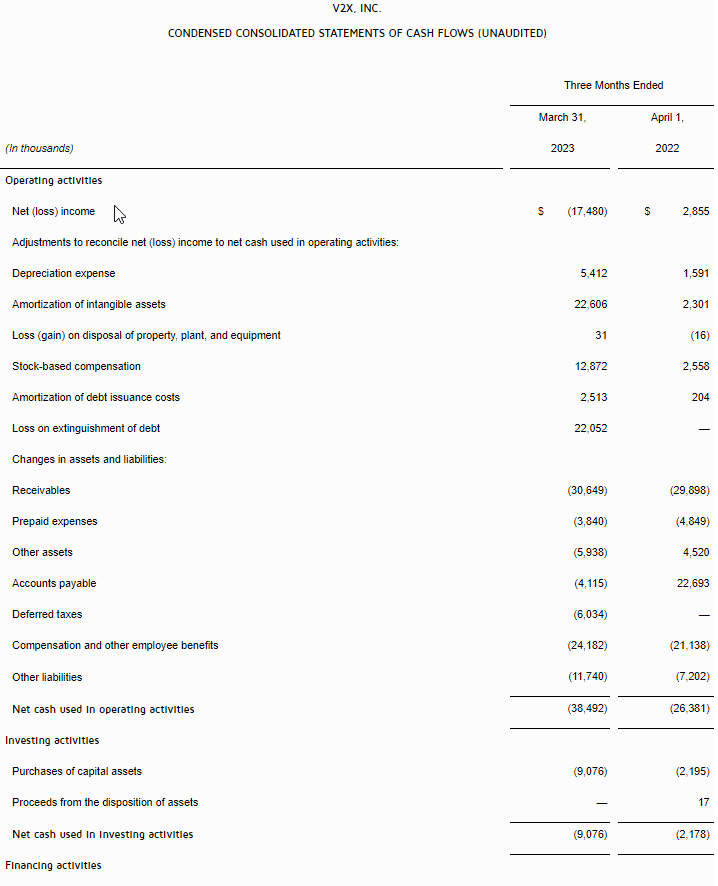

“Net cash used in operating activities for the quarter was $38.5 million. Adjusted net cash used in operating activities1 was $23.4 million, which adds back $13.4 million of CARES Act related payments and $1.7 million of M&A and integration costs,” said Ms. Lynch. “Cash flow followed our normal seasonal pattern and we expect operating cash flow to ramp to our previously communicated guidance.”

Total backlog as of March 31, 2023, was $11.8 billion and funded backlog was $2.6 billion. The trailing twelve-month book-to-bill was 1.4x.

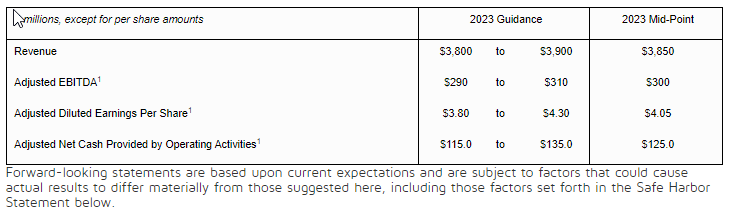

Reiterating 2023 Guidance

Ms. Lynch concluded, “I am pleased with our strong start to the year. Our teams continue to work together seamlessly, making notable progress on integration milestones while driving results across the board. We have made great strides in harmonizing our processes, technology, and applications, which is allowing us to deliver on our commitments. As such, the Company is reiterating its guidance for 2023.” Guidance for 2023 remains as follows:

$ millions, except for per share amounts

2023 Guidance

2023 Mid-Point

Revenue

$3,800

To

$3,900

$3,850

Adjusted EBITDA1

$290

To

$310

$300

Adjusted Diluted Earnings Per Share1

$3.80

To

$4.30

$4.05

Adjusted Net Cash Provided by Operating Activities 1

$115.0

To

$135.0

$125.0

Forward-looking statements are based upon current expectations and are subject to factors that could cause actual results to differ materially from those suggested here, including those factors set forth in the Safe Harbor Statement below.

First Quarter 2023 Conference Call

Management will conduct a conference call with analysts and investors at 4:30 p.m. ET on Tuesday, May 9, 2023. U.S.-based participants may dial in to the conference call at 888-886-7786, while international participants may dial 416-764-8658. A live webcast of the conference call as well as an accompanying slide presentation will be available here: https://app.webinar.net/4AayJaN5XPr

A replay of the conference call will be posted on the V2X website shortly after completion of the call and will be available for one year. A telephonic replay will also be available through May 23, 2023, at 844-512-2921 (domestic) or 412-317-6671 (international) with passcode 30124902.

Presentation slides that will be used in conjunction with the conference call will also be made available online in advance at https://investors.vectrus.com/. V2X recognizes its website as a key channel of distribution to reach public investors and as a means of disclosing material non-public information to comply with its obligations under the U.S. Securities and Exchange Commission (“SEC”) Regulation FD.

Footnotes: 1 See “Key Performance Indicators and Non-GAAP Financial Measures” for descriptions and reconciliations.

About V2X

V2X is a leading provider of critical mission solutions and support to defense clients globally, formed by the 2022 Merger of Vectrus and Vertex to build on more than 120 combined years of successful mission support. The Company delivers a comprehensive suite of integrated solutions across the operations and logistics, aerospace, training and technology markets to national security, defense, civilian and international clients. Our global team of approximately 15,000 employees brings innovation to every point in the mission lifecycle, from preparation, to operations, to sustainment, as it tackles the most complex challenges with agility, grit, and dedication.

Safe Harbor Statement

Safe Harbor Statement under the Private Securities Litigation Reform Act of 1995 (the “Act”): Certain material presented herein includes forward-looking statements intended to qualify for the safe harbor from liability established by the Act. These forward-looking statements include, but are not limited to, all the statements and items listed under “Reiterating 2023 Guidance” above and other assumptions contained therein for purposes of such guidance, other statements about our 2023 performance outlook, revenue, contract opportunities, and any discussion of future operating or financial performance.

Forward-looking statements generally can be identified by the use of forward-looking terminology such as “may,” “will,” “expect,” “intend,” “estimate,” “anticipate,” “believe,” “could,” “potential,” “continue” or similar terminology. These statements are based on the beliefs and assumptions of the management of the Company based on information currently available to management.

These forward-looking statements are not guarantees of future performance, conditions, or results, and involve a number of known and unknown risks, uncertainties, assumptions, and other important factors, many of which are outside our management’s control, that could cause actual results to differ materially from the results discussed in the forward-looking statements. In addition, forward-looking statements are subject to certain risks and uncertainties that could cause actual results to differ materially from the Company’s historical experience and our present expectations or projections. For a discussion of some of the risks and uncertainties that could cause actual results to differ from such forward-looking statements, see the risks and other factors detailed from time to time our Annual Report on Form 10-K, Quarterly Reports on Form 10-Q, and other filings with the SEC.

We undertake no obligation to update any forward-looking statements, whether as a result of new information, future events or otherwise, except as required by law.

Key Performance Indicators and Non-GAAP Measures

The primary financial performance measures we use to manage our business and monitor results of operations are revenue trends and operating income trends. Management believes that these financial performance measures are the primary drivers for our earnings and net cash from operating activities. Management evaluates its contracts and business performance by focusing on revenue, operating income, and operating margin. Operating income represents revenue less both cost of revenue and selling, general and administrative (SG&A) expenses. Cost of revenue consists of labor, subcontracting costs, materials, and an allocation of indirect costs, which includes service center transaction costs. SG&A expenses consist of indirect labor costs (including wages and salaries for executives and administrative personnel), bid and proposal expenses and other general and administrative expenses not allocated to cost of revenue. We define operating margin as operating income divided by revenue.

We manage the nature and amount of costs at the program level, which forms the basis for estimating our total costs and profitability. This is consistent with our approach for managing our business, which begins with management’s assessing the bidding opportunity for each contract and then managing contract profitability throughout the performance period.

In addition to the key performance measures discussed above, we consider adjusted net income, adjusted diluted earnings per share, adjusted operating income, adjusted EBITDA, adjusted EBITDA margin, adjusted operating cash flow, and pro forma revenue to be useful to management and investors in evaluating our operating performance, and to provide a tool for evaluating our ongoing operations. This information can assist investors in assessing our financial performance and measures our ability to generate capital for deployment among competing strategic alternatives and initiatives. We provide this information to our investors in our earnings releases, presentations, and other disclosures.

Adjusted net income, adjusted diluted earnings per share, adjusted operating income, adjusted EBITDA, adjusted EBITDA margin, adjusted operating cash flow, and pro forma revenue, however, are not measures of financial performance under GAAP and should not be considered a substitute for financial measures determined in accordance with GAAP. Definitions and reconciliations of these items are provided below.

Pro forma revenue is defined as the combined results of our operations for the three months ended March 31, 2023 and April 1, 2022 as if the Merger had occurred on January 1, 2021.

Adjusted operating income is defined as operating income, adjusted to exclude items that may include, but are not limited to, significant charges or credits, and unusual and infrequent non-operating items that impact current results but are not related to our ongoing operations, such as M&A, integration, and related costs.

Adjusted EBITDA is defined as operating income, adjusted to exclude depreciation and amortization of intangible assets, and items that may include, but are not limited to, significant charges or credits, and unusual and infrequent non-operating items that impact current results but are not related to our ongoing operations, such as M&A, integration, and related costs.

Adjusted EBITDA margin is defined as adjusted EBITDA divided by revenue.

Adjusted net income is defined as net income, adjusted to exclude items that may include, but are not limited to, significant charges or credits, and unusual and infrequent non-operating items that impact current results but are not related to our ongoing operations, such as M&A, integration and related costs, amortization of acquired intangible assets, amortization of debt issuance costs, and loss on extinguishment of debt.

Adjusted diluted earnings per share is defined as adjusted net income divided by the weighted average diluted common shares outstanding.

Cash interest, net is defined as interest expense, net adjusted to exclude amortization of debt issuance costs.

Adjusted operating cash flow is defined as net cash provided by (or used in) operating activities adjusted to exclude infrequent non-operating items, such as M&A payments and related costs.

In this document, the Company presents certain forward-looking non-GAAP metrics. The Company does not provide outlook on a GAAP basis because the items that the Company excludes from GAAP to calculate the comparable non-GAAP measure can be dependent on future events that are less capable of being controlled or reliably predicted by management and are not part of the Company’s routine operating activities. Additionally, management does not forecast many of the excluded items for internal use and therefore cannot create or rely on outlook done on a GAAP basis. The occurrence, timing and amount of any of the items excluded from GAAP to calculate non-GAAP could significantly impact the Company’s fiscal 2023 GAAP results.

MCLEAN, Va., April 25, 2023 /PRNewswire/ — V2X, Inc., (NYSE: VVX), a leading provider of critical mission solutions and support to defense clients globally, will report first quarter 2023 financial results on Tuesday, May 9, 2023, after market close. Senior management will conduct a conference call at 4:30 p.m. ET that same day.

U.S.-based participants may dial in to the conference call at 888-886-7786, while international participants may dial 416-764-8658. A live webcast of the conference call as well as an accompanying slide presentation will be available under the Investors section of the V2X website at https://gov2x.com/.

A replay of the conference call will be posted on the V2X website shortly after completion of the call and will be available for one year. A telephonic replay will also be available through May 23, 2023, at 844-512-2921 (domestic) or 412-317-6671 (international) with passcode 30124902.

ABOUT V2X V2X is a leading provider of critical mission solutions and support to defense clients globally, formed by the 2022 merger of Vectrus and Vertex to build on more than 120 combined years of successful mission support. The Company delivers a comprehensive suite of integrated solutions across the operations and logistics, aerospace, training and technology markets to national security, defense, civilian and international clients. Our global team of approximately 15,000 employees brings innovation to every point in the mission lifecycle, from preparation, to operations, to sustainment, as they tackle the most complex challenges with agility, grit and dedication.

SAN DIEGO, April 24, 2023 (GLOBE NEWSWIRE) — Kratos Defense & Security Solutions, Inc. (NASDAQ: KTOS), a Technology Company in the Defense, National Security and Global Markets, announced today that it will publish financial results for the first quarter 2023 after the close of market on Wednesday, May 3rd. Management will discuss the Company’s operations and financial results in a conference call beginning at 2:00 p.m. Pacific (5:00 p.m. Eastern).

The call will be available at www.kratosdefense.com. Participants may register for the call using this Online Form. Upon registration, all telephone participants will receive the dial-in number along with a unique PIN that can be used to access the call. For those who cannot access the live broadcast, a replay will be available on Kratos’ website.

About Kratos Defense & Security Solutions Kratos Defense & Security Solutions, Inc. (NASDAQ: KTOS) is a Technology Company that develops and fields transformative, affordable systems, products and solutions for United States National Security, our allies and global commercial enterprises. At Kratos, Affordability is a Technology, and Kratos is changing the way breakthrough technology is rapidly brought to market – at a low cost – with actual products, systems, and technologies rather than slide decks or renderings. Through proven commercial and venture capital backed approaches, including proactive, internally funded research and streamlined development processes, Kratos is focused on being First to Market with our solutions, well in advance of competition. Kratos is the recognized Technology Disruptor in our core market areas, including Space and Satellite Communications, Cyber Security and Warfare, Unmanned Systems, Rocket and Hypersonic Systems, Next-Generation Jet Engines and Propulsion Systems, Microwave Electronics, C5ISR and Virtual and Augmented Reality Training Systems. For more information, visit www.KratosDefense.com.

Partnership Focuses on Delivering Fully Digital-Enabled Edge Terminal Solutions

SAN DIEGO and READING, United Kingdom, April 17, 2023 (GLOBE NEWSWIRE) — Kratos Defense & Security Solutions, Inc. (Nasdaq: KTOS), a technology company specializing in defense, national security and communications solutions, and ALL.SPACE, the world’s only provider of multi-orbit smart terminals, announced today a strategic partnership aimed at jointly developing and delivering solutions that will enable software-defined satellite ground systems to better leverage the capabilities of next-generation smart terminals. The combined solutions are expected to enhance dynamic operations end-to-end across the ground segment from the gateway to the network’s edge, placing more application power in the hands of end users and greatly expanding flexibility beyond today’s proprietary, purpose-built, satellite terminals.

The space industry is immersed in a renaissance driven by technology breakthroughs such as software-defined payloads, small satellite constellations, multi-orbit services and more. On the ground, advances in satellite networks are occurring as well, including the growth of ground station-as-a-service, virtualized ground systems and the need to better mainstream with terrestrial and cellular communications networks. These advances at both ends of the space/ground connection mean that satellite network systems must come to act more dynamically, adapting on-the-fly to changing needs, conditions and business or mission requirements.

Today’s announcement is part of a multi-year collaboration to integrate and enhance both companies’ products. It is supported by a joint development roadmap focused on new features, functions and capabilities that will deliver more powerful, flexible and agile terminal capabilities at the network’s edge for both defense and commercial uses, such as advanced support for multi-mission and multi-orbit capabilities.

According to Greg Quiggle, Senior Vice President of Space Product Management at Kratos, “Historically, satellite terminals have been defined by proprietary technologies resident on purpose-built hardware, severally limiting what users could accomplish at the network’s edge. That all changes with software-defined networking, which has long been the standard in global terrestrial communications and is now available for satellite network operators through the OpenSpace Platform. ALL.SPACE is a leader in smart terminal technology and a profound partner for Kratos to work with in revolutionizing what users can accomplish at the satellite network’s edge.”

“We are creating a new generation of digital, flexible terminals featuring both a multi-beam antenna and a platform capable of hosting software-defined applications,” said John-Paul Szczepanik, Chief Technology Officer for ALL.SPACE. “ALL.SPACE’s multilink terminal delivers the combined strengths of all orbits by unlocking simultaneous access to multiple networks. We believe pairing this flexibility with the Kratos OpenSpace Platform will dramatically enhance dynamic operations at the edge.”

Kratos and ALL.SPACE have already begun integrating their respective technologies, including elements of Kratos’ OpenSpace® software-defined ground system, such as its OpenSpace virtual modem (vModem) and OpenEdge™ 2500 digitizer, with ALL.SPACE’s S2000 Smart Terminal.

The jointly developed solutions will conform to industry standards for maximum flexibility, including the IEEE-ISTO Std 4900-2021: Digital IF Interoperability Standard from the Digital IF Interoperability (DIFI) Consortium (DIFI). Both companies believe that common standards are essential for the space industry to realize the opportunities on the horizon and to advance the industry’s integration with the larger global communications infrastructure. Both are founding members of DIFI, an independent organization created to develop and promote standards for interoperability in space and satellite systems.

About Kratos Defense & Security Solutions Kratos Defense & Security Solutions, Inc. (NASDAQ: KTOS) is a technology company that develops and fields transformative, affordable systems, products and solutions for United States National Security, its allies and global commercial enterprises. At Kratos, affordability is a technology, and Kratos is changing the way breakthrough technology is rapidly brought to market with actual products, systems and technologies rather than slide decks or renderings. Through proven commercial and venture capital backed approaches, including proactive, internally funded research and streamlined development processes, Kratos is focused on being first to market with our solutions, well in advance of competition. Kratos is the recognized Technology Disruptor in our core market areas, including Space and Satellite Communications, Cyber Security and Warfare, Unmanned Systems, Rocket and Hypersonic Systems, Next-Generation Jet Engines and Propulsion Systems, Microwave Electronics, C5ISR and Virtual and Augmented Reality Training Systems. For more information, visit www.KratosDefense.com.

About ALL.SPACE Headquartered in Reading, UK, ALL.SPACE is the first and only field-proven platform to simultaneously deliver full-performance connections across all significant orbits from a single device. The company recently concluded live field tests with the US and UK governments and several satellite operators demonstrating multiple, simultaneous connections across LEO, MEO and GEO orbits, which empowers users in markets ranging from government and defence to maritime, aero and land mobile to harness the full benefits of new satellite constellations and the convergence of GEO and NGSO (Non-Geostationary Orbit) services.

Notice Regarding Forward-Looking Statements Certain statements in this press release may constitute “forward-looking statements” within the meaning of the Private Securities Litigation Reform Act of 1995. These forward-looking statements are made on the basis of the current beliefs, expectations and assumptions of the management of Kratos and are subject to significant risks and uncertainty. Investors are cautioned not to place undue reliance on any such forward-looking statements. All such forward-looking statements speak only as of the date they are made, and Kratos undertakes no obligation to update or revise these statements, whether as a result of new information, future events or otherwise. Although Kratos believes that the expectations reflected in these forward-looking statements are reasonable, these statements involve many risks and uncertainties that may cause actual results to differ materially from what may be expressed or implied in these forward-looking statements. For a further discussion of risks and uncertainties that could cause actual results to differ from those expressed in these forward-looking statements, as well as risks relating to the business of Kratos in general, see the risk disclosures in the Annual Report on Form 10-K of Kratos for the year ended December 25, 2022, and in subsequent reports on Forms 10-Q and 8-K and other filings made with the by Kratos.

Kratos Press Contact: Yolanda White 858-812-7302 Direct

SAN DIEGO, April 13, 2023 (GLOBE NEWSWIRE) — Kratos Defense & Security Solutions, Inc. (Nasdaq: KTOS), a leading National Security Solutions provider, announced today that it was awarded a contract by a DoD Prime contractor to provide a concurrency upgrade to multiple ground tactical platform maintenance training systems.

Commenting on the award, Jose Diaz, Sr. Vice President at Kratos Training Solutions, stated: “Over the last 25 years Kratos has supported DoD and allied military customers by designing, developing and delivering advanced maintenance training systems. We are committed to delivering the same high level of quality with these upgrades.”

Due to customer, competitive, security-related and other considerations, no additional information will be provided related to this contract award.

Kratos develops advanced, cost-effective maintenance and operational training solutions for U.S. and allied forces to enhance warfighter readiness and survivability. Kratos is driving innovation in military simulation and training programs through application of immersive technologies within advanced simulation systems for air, ground, maritime and space domains.

About Kratos Defense & Security Solutions

Kratos Defense & Security Solutions, Inc. (NASDAQ: KTOS) is a Technology Company that develops and fields transformative, affordable systems, products and solutions for United States National Security, our allies and global commercial enterprises. At Kratos, Affordability is a Technology, and Kratos is changing the way breakthrough technology is rapidly brought to market – at a low cost – with actual products, systems and technologies rather than slide decks or renderings. Through proven commercial and venture capital backed approaches, including proactive, internally funded research and streamlined development processes, Kratos is focused on being First to Market with our solutions, well in advance of competition. Kratos is the recognized Technology Disruptor in our core market areas, including Space and Satellite Communications, Cyber Security and Warfare, Unmanned Systems, Rocket and Hypersonic Systems, Next-Generation Jet Engines and Propulsion Systems, Microwave Electronics, C5ISR and Virtual and Augmented Reality Training Systems. For more information, visit www.KratosDefense.com.

Notice Regarding Forward-Looking Statements

Certain statements in this press release may constitute “forward-looking statements” within the meaning of the Private Securities Litigation Reform Act of 1995. These forward-looking statements are made on the basis of the current beliefs, expectations, and assumptions of the management of Kratos and are subject to significant risks and uncertainty. Investors are cautioned not to place undue reliance on any such forward-looking statements. All such forward-looking statements speak only as of the date they are made, and Kratos undertakes no obligation to update or revise these statements, whether as a result of new information, future events or otherwise. Although Kratos believes that the expectations reflected in these forward-looking statements are reasonable, these statements involve many risks and uncertainties that may cause actual results to differ materially from what may be expressed or implied in these forward-looking statements. For a further discussion of risks and uncertainties that could cause actual results to differ from those expressed in these forward-looking statements, as well as risks relating to the business of Kratos in general, see the risk disclosures in the Annual Report on Form 10-K of Kratos for the year ended December 25, 2022, and in subsequent reports on Forms 10-Q and 8-K and other filings made with the SEC by Kratos.

V2X awarded O-level maintenance contract for Naval Test Wing Pacific

MCLEAN, Va., April 5, 2023 /PRNewswire/ — Vertex, a V2X company (NYSE: VVX), was awarded a $440 million contract by the U.S. Navy to provide aircraft maintenance support for Naval Test Wing Pacific (NTWP) VX-30 and VX-31 at Point Mugu, CA and China Lake, CA. Under this contract, V2X, under its legacy company Vertex, is the chosen provider of flightline maintenance, logistics, and technical support for the two weapons development and test squadrons. This important mission complements NAVAIR’s efforts to develop, test and sustain the Navy’s most current suite of capabilities.

“V2X is honored to be selected to support the critical test and evaluation activities performed at Naval Test Wing Pacific,” said Chuck Prow, V2X CEO. “Our established history and record of performance providing maintenance, repair, overhaul and technical support for a variety of Naval Aviation platforms demonstrate our commitment to maintaining high levels of mission readiness.”

NTWP provides safe, effective, and efficient ground and flight test, airborne flight test support, and experimental operations of manned and unmanned aircraft, weapons, and weapons systems for the Department of the Navy.

This contract has a seven-year award period ending in March 2030.

ABOUT V2X

V2X is a leading provider of critical mission solutions and support to defense clients globally, formed by the 2022 Merger of Vectrus and Vertex to build on more than 120 combined years of successful mission support. The Company delivers a comprehensive suite of integrated solutions across the operations and logistics, aerospace, training, and technology markets to national security, defense, civilian and international clients. Our global team of approximately 15,000 employees brings innovation to every point in the mission lifecycle, from preparation to operations to sustainment, as it tackles the most complex challenges with agility, grit, and dedication.

On July 5, 2022 (“Closing Date”), Vectrus, Inc. (“Vectrus”) completed its merger (“the Merger”) with Vertex Aerospace Services Holding Corp. (“Vertex”), thereby forming V2X, Inc. Fourth quarter “reported results” reflect the contributions of Vectrus and Vertex from October 1, 2022, through December 31, 2022. Full year 2022 “reported results” reflect the contributions of Vectrus from January 1, 2022, through December 31, 2022, and Vertex from the Closing Date through December 31, 2022, unless otherwise noted. Comparisons to historical periods are relative to legacy Vectrus results, unless otherwise noted.

Fourth Quarter 2022 Highlights:

Revenue of $978.2 million, up 20% y/y on a pro forma basis

Grew INDOPACOM revenue sevenfold as presence and footprint continues to expand

Recently awarded two key contracts with Space Command and a National Security client

Reported operating income of $31.0 million; adjusted operating income1 of $74.5 million

Adjusted EBITDA1 of $79.3 million with a margin1 of 8.1%

Diluted EPS of ($0.35); adjusted diluted EPS1 of $0.92

Repaid $25.0 million of debt and in February 2023 executed a more efficient credit facility with substantial interest savings and improved liquidity

2023 Guidance:

Establishing full-year 2023 guidance with revenue growth of 5% and adjusted EBITDA1 growth of 8% at the mid-point

MCLEAN, Va., March 2, 2023 /PRNewswire/ — V2X, Inc. (NYSE:VVX) announced fourth quarter and full-year 2022 financial results.

“This was a very successful year, achieving several milestones, including the completion of the merger with Vertex and making significant progress on the integration while driving strong results with high quality uninterrupted service and support to our clients,” said Chuck Prow, President and Chief Executive Officer of V2X. “Our teams came together seamlessly, demonstrating agility and outstanding performance, delivering 9% pro forma revenue growth for the full year. Importantly, current demand and leading indicators for our business remain strong with a substantial backlog of over $12 billion and close to 4.5 years of future revenue already under contract for our top ten programs. With our enhanced and differentiated capabilities, we are providing increased innovation and technology to our clients’ complex mission requirements and believe we have meaningful opportunity for future growth with our expanded addressable market of approximately $160 billion dollars.”

Mr. Prow continued, “We capped off the year with 20% year-over-year pro forma revenue growth in the fourth quarter, driven by new business wins, successful recompetes, and continued expansion on our core programs. Importantly, we demonstrated significant growth in the Pacific or INDOPACOM, as our presence and footprint expands to support increasing mission requirements. Our momentum is continuing this year, and in January 2023 we were awarded a strategically important five-year recompete contract valued at over $90 million with a National Security client. I’d like to thank our team for their exceptional performance and dedication, which has resulted in significant growth with this client over the past several years. Adjusted EBITDA margin1 was 8.1%, due to favorable program performance, strong execution, and the acceleration of program productivity that was expected in 2023. Our integration related activities continue to progress, and we were successful in delivering our expected cost synergies for the quarter. We remain on track to achieve our integration milestones and previously communicated cost synergies.”

Mr. Prow concluded, “The significant momentum in our business, a robust backlog exceeding $12 billion, and limited recompete risk, provides solid visibility that we believe should drive revenue growth of approximately 5% at the mid-point in 2023. Importantly, over 90% of 2023 revenue is expected to be generated from existing contracts. Furthermore, recompetes are expected to comprise only 2% of revenue. In 2023, we remain focused on delivering on our strategy to drive growth and value creation by providing converged solutions that fuse the digital and physical aspects of our clients’ missions. We have much to be excited about and will continue to execute our strategic framework to: Expand the Base, Capture New Markets, Deliver with Excellence, and Enhance Culture.”

Fourth Quarter 2022 Results

Revenue of $978.2 million, up 20% y/y on a pro forma basis

Operating income of $31.0 million, including merger and integration related costs of $23.4 million and amortization of acquired intangible assets of $20.1 million

Adjusted operating income1 of $74.5 million

Adjusted EBITDA1 of $79.3 million with an 8.1% adjusted EBITDA margin1

Diluted EPS of ($0.35) including merger and integration related costs

Adjusted diluted EPS1 of $0.92

Net debt as of December 31, 2022, of $1,221 million, representing an $87 million decrease from the Merger closing on July 5, 2022

The Company was undrawn on its revolver as of December 31, 2022

Total backlog as of December 31, 2022, of $12.3 billion

“Our fourth quarter financial results were strong and provide great traction for V2X leading into 2023,” said Susan Lynch, Senior Vice President and Chief Financial Officer. “Pro forma revenue increased 20% year-over-year to $978.2 million. Revenue growth was driven by continued expansion in INDOPACOM and on LOGCAP, volume associated with rapid response efforts in Europe, and growth associated with new programs including Fort Benning, E-6B, Advanced Helicopter Training System, Navy Test Wing Atlantic, and Global Strike programs. Notably, revenue from INDOPACOM increased sevenfold year-over-year to $54.4 million, reflecting our additional work throughout the region, including Kwajalein and the Philippines.”

Ms. Lynch continued, “In the fourth quarter, V2X leveraged its solid cash position to repay $25 million of its second lien term loan. Importantly, our strong fundamentals and visibility have allowed V2X to significantly improve its capital structure by refinancing portions of its debt into a lower cost, pro rata credit facility. This new, five-year $750 million credit facility is expected to generate substantial interest expense savings and drive value for our shareholders. At the end of the fourth quarter, our net consolidated indebtedness to EBITDA1 (net leverage ratio) was 3.7x, a 0.3x improvement from Merger close. We have been able to reduce our leverage in line with plan and anticipate that our leverage ratio will show further improvement in 2023.”

Full-Year 2022 Results

Full-year revenue was $2.891 billion and pro forma revenue was $3.670 billion, up 8.8% pro forma year-on-year. The Company reported full-year operating income of $55.8 million and adjusted operating income1 of $187.5 million. Full-year EBITDA1 was $201.0 million with a margin of 7.0%. Full year pro forma Adjusted EBITDA1 was $278.0 million with a margin of 7.6%. Full-year diluted EPS was ($0.68), due primarily to Merger and integration related costs, amortization of acquired intangible assets and interest expense. Adjusted diluted EPS1 for 2022 was $4.60.

Cash provided by operating activities for the year was $93.5 million, compared to $61.3 million in 2021 for legacy Vectrus. Pro forma adjusted operating cash flow for the year was $85.8 million and excludes $62 million of Merger related payments and $8 million of repayments tied to the CARES Act. Lynch continued, “Our ability to generate strong cash flow with low capital intensity is an important attribute of our business.”

During the second half of the year, V2X lowered its net debt balance by $87 million resulting in an ending balance of $1,220.7 million. Cash at year-end was $116.1 million up from $38.5 million at the end of 2021.

Total backlog as of December 31, 2022 was $12.3 billion and funded backlog was $2.6 billion. The trailing twelve-month book-to-bill was 1.3x.

2023 Guidance

Ms. Lynch concluded, “Based on our expected continued strong demand trends and operational execution, we are setting the mid-point of our guidance for revenue at $3.850 billion, representing approximately 5% pro forma growth and Adjusted EBITDA1 of $300 million, representing 8% pro forma growth.”

Guidance for 2023 is as follows:

Fourth Quarter 2022 Conference Call

Management will conduct a conference call with analysts and investors at 4:30 p.m. ET on Thursday, March 2, 2023. U.S.-based participants may dial in to the conference call at 877-506-6380, while international participants may dial 412-542-4198. A live webcast of the conference call as well as an accompanying slide presentation will be available here: https://app.webinar.net/EZQ7LMALNPo

A replay of the conference call will be posted on the V2X website shortly after completion of the call and will be available for one year. A telephonic replay will also be available through March 16, 2023, at 844-512-2921 (domestic) or 412-317-6671 (international) with passcode 10174938.

Presentation slides that will be used in conjunction with the conference call will also be made available online in advance at https://investors.vectrus.com/. V2X recognizes its website as a key channel of distribution to reach public investors and as a means of disclosing material non-public information to comply with its obligations under the U.S. Securities and Exchange Commission (“SEC”) Regulation FD.

Footnotes: 1 See “Key Performance Indicators and Non-GAAP Financial Measures” for descriptions and reconciliations.

About V2X

V2X is a leading provider of critical mission solutions and support to defense clients globally, formed by the 2022 Merger of Vectrus and Vertex to build on more than 120 combined years of successful mission support. The Company delivers a comprehensive suite of integrated solutions across the operations and logistics, aerospace, training and technology markets to national security, defense, civilian and international clients. Our global team of approximately 14,000 employees brings innovation to every point in the mission lifecycle, from preparation, to operations, to sustainment, as it tackles the most complex challenges with agility, grit, and dedication.

Safe Harbor Statement

Safe Harbor Statement under the Private Securities Litigation Reform Act of 1995 (the “Act”): Certain material presented herein includes forward-looking statements intended to qualify for the safe harbor from liability established by the Act. These forward-looking statements include, but are not limited to, all the statements and items listed under “2023 Guidance” above and other assumptions contained therein for purposes of such guidance, other statements about our 2023 performance outlook, revenue, contract opportunities, and any discussion of future operating or financial performance.

Forward-looking statements generally can be identified by the use of forward-looking terminology such as “may,” “will,” “expect,” “intend,” “estimate,” “anticipate,” “believe,” “could,” “potential,” “continue” or similar terminology. These statements are based on the beliefs and assumptions of the management of the Company based on information currently available to management.

These forward-looking statements are not guarantees of future performance, conditions, or results, and involve a number of known and unknown risks, uncertainties, assumptions, and other important factors, many of which are outside our management’s control, that could cause actual results to differ materially from the results discussed in the forward-looking statements. In addition, forward-looking statements are subject to certain risks and uncertainties that could cause actual results to differ materially from the Company’s historical experience and our present expectations or projections. For a discussion of some of the risks and uncertainties that could cause actual results to differ from such forward-looking statements, see the risks and other factors detailed from time to time our Annual Report on Form 10-K, Quarterly Reports on Form 10-Q, and other filings with the SEC.

We undertake no obligation to update any forward-looking statements, whether as a result of new information, future events or otherwise, except as required by law.

Virtualized software apps bring more power and flexibility to the edge by replacing dedicated hardware

SAN DIEGO, Feb. 22, 2023 (GLOBE NEWSWIRE) — Kratos Defense & Security Solutions, Inc. (Nasdaq: KTOS), a leading National Security Solutions provider, released the first of its new OpenEdge™ products, the industry’s first open standards-based and software-enabled satellite terminals. Part of Kratos’ OpenSpace® Platform, OpenEdge is the first generally available family of satellite network edge devices employing a modern, software-defined approach for a range of communications, observation, sensing and TT&C uses. OpenEdge is the next step in Kratos’ ongoing effort to support the mainstreaming of satellite services by enabling satellite ground systems to operate seamlessly with today’s wireless and terrestrial networks.

Until OpenEdge, satellite terminals─ the devices that end users employ at the far edge of a satellite ground network to transmit and receive data─ have been purpose-built hardware devices that seriously restrict functionality and flexibility at the network’s edge. OpenEdge disrupts these limitations by:

employing virtualized software modems that can run on general purpose, off-the-shelf compute, and

adding far more power and versatility by enabling additional apps to run at the network’s edge, fully orchestrated across service delivery

Bringing Flexibility to the Network’s Edge Today’s satellite terminals consist of purpose-built hardware components that are limited to performing a dedicated function, for example a satellite modem performing modulation/demodulation functions. OpenEdge uses a different model for operating at the edge, one that employs standards already widely adopted across the larger global telecommunications industry to expand terminal functions and make them more flexible. These standards are what enable mobile devices such as smartphones to support roaming, use cloud-based functions, interoperate with other networks and do much more. While satellites present a more complex technology challenge, the goal of OpenSpace and OpenEdge is to help satellite operators make their services as mainstream as cellular communications and to capitalize on new services such as 5G.

“OpenEdge satellite terminals extend the dynamic operations of the OpenSpace Platform beyond the core and gateway out to the network’s far edge,” said Greg Quiggle, Senior Vice President of Space Product Management at Kratos, “As a result, signal processing and other value-added network functions happen closer to the end user. This enables satellite service providers to deploy new services in minutes while dramatically reducing the overall lifecycle cost of their network.

Intelsat, one of the world’s largest commercial satellite operators, will be among the first to supplant traditional satellite terminals with OpenEdge capabilities.

“OpenEdge technology powers Intelsat’s family of smart edge satellite terminals providing a highly dynamic and application-optimized customer experience. Through this open and virtualized platform, we are able to deliver new services and features to the customer edge on-demand,” commented Blane Boynton, VP Product Development at Intelsat. “We expect this technology to benefit customers across multiple industries and applications, from fixed cellular backhaul and enterprise connectivity, to inflight and maritime applications. In the near future, we’ll rely on OpenEdge technology to help us be the first to transition to 5G, standards based, service delivery for non-terrestrial applications.”

Adding Power at the Edge The OpenEdge advantage starts with Kratos’ virtual modem, replacing the traditional hardware box with software that can run on off-the-shelf x86 compute devices, such as a generic server, a laptop or in the cloud. It can interface directly with a digitally-enabled antenna or be configured with a built-in digitizer that converts the satellite’s analog RF signals into standard Internet Protocol (IP) packets that can be operated upon digitally.

Because OpenEdge effectively turns the traditional, purpose-built terminal into a generic, off-the-shelf computer─ sometimes referred to as universal customer premises equipment (uCPE)─ it can incorporate any x86 applications into operations at the edge. For example, a spectrum monitoring app can be loaded so that end users in the field can quickly find alternate routes for avoiding interference or intentional jamming of satellite signals. In fact, operators or mission controllers can actually turn the terminal into a remote hub in minutes simply by remotely enabling additional software directly into the terminal. The Value of Orchestration At a time when satcom equipment vendors are still struggling to virtualize even basic network functions, Kratos has done that and more by delivering orchestrated virtual network functions today. Orchestration is the ability to specify and automate how network functions will interoperate with each other to support specific services, missions, customer requirements and satellite payloads, and to intelligently configure and reconfigure themselves in real time as needs and demands change. While common across the global communications infrastructure, orchestration has not been employed to great degree in satellite networks, in part due to the challenge of virtualizing unique satcom functions. However, traditional hardware-based ground systems and terminals simply can no longer keep up with the increasingly dynamic advances in both the space layer, such as software-defined satellites and constellations of smallsats, nor in the world’s global communications networks, such as automated provisioning and mobility. In contrast, OpenSpace can ably support these necessary dynamic operations.

Additional OpenEdge Advantages The dynamic advances in OpenEdge support additional benefits to network operators and their customers with more power and flexibility at the edge, including:

Support for Multiple Missions and Markets. OpenEdge terminals simultaneously support a variety of fixed and mobile satellite use cases, including two-way Satellite Communication (satcom), Earth Observation and Remote Sensing (EO/RS), and Telemetry, Tracking & Command (TT&C). Additionally, they can deliver complementary end-user services in the same way that a terrestrial network does, such as enterprise network extension, cellular backhaul, telecom trunking and defense and government applications.

Lower Hardware Cost, Smaller Footprint. OpenEdge terminals reduce the overall hardware footprint to a single box. As a generic x86 device, it both costs less than proprietary units while enabling more power simply by adding complementary software apps. Because the digitizer can be built in, OpenEdge terminals can work with virtually any mission-suitable antenna.

Enhanced Security at the Edge. Any x86-based app can be loaded on the OpenEdge terminal, including firewalls, encrypters and more advanced or custom security applications for highly sensitive uses.

Eliminate Vendor Lock-In. Today’s purpose-built terminals all employ proprietary architectures which lock customers into their equipment for given services, especially in satcom. In contrast, OpenEdge, and the entire OpenSpace Platform, embrace commonly accepted industry interoperability standards, enabling OpenEdge terminals to work side-by-side with standards compliant devices from other companies. In addition, network operators will find much greater success integrating their space-based offerings into the global communications mainstream, expanding their reach, services and revenue.

About Kratos OpenSpace Kratos’ OpenSpace family of solutions enables the digital transformation of satellite ground systems to become a more dynamic and powerful part of the space network. The family consists of three product lines: OpenSpace SpectralNet for converting satellite RF signals to be used in digital environments; OpenSpace quantum products, which are virtual versions of traditional hardware components; and the OpenSpace Platform, the first commercially available, fully orchestrated, software-defined ground system. These three OpenSpace lines enable satellite operators and other service providers to implement digital operations at their own pace and in ways that meet their unique mission goals and business models. For more information about the OpenSpace family visit http://KratosDefense.com/OpenSpace.

About Kratos Defense & Security Solutions Kratos Defense & Security Solutions, Inc. (NASDAQ:KTOS) develops and fields transformative, affordable technology, platforms and systems for United States National Security related customers, allies and commercial enterprises. Kratos is changing the way breakthrough technology for these industries are rapidly brought to market through proven commercial and venture capital backed approaches, including proactive research, and streamlined development processes. At Kratos, affordability is a technology, and we specialize in unmanned systems, satellite communications, cyber security/warfare, microwave electronics, missile defense, hypersonic systems, training, combat systems and next generation turbo jet and turbo fan engine development. For more information go to www.KratosDefense.com.

Notice Regarding Forward-Looking Statements Certain statements in this press release may constitute “forward-looking statements” within the meaning of the Private Securities Litigation Reform Act of 1995. These forward-looking statements are made on the basis of the current beliefs, expectations and assumptions of the management of Kratos and are subject to significant risks and uncertainty. Investors are cautioned not to place undue reliance on any such forward-looking statements. All such forward-looking statements speak only as of the date they are made, and Kratos undertakes no obligation to update or revise these statements, whether as a result of new information, future events or otherwise. Although Kratos believes that the expectations reflected in these forward-looking statements are reasonable, these statements involve many risks and uncertainties that may cause actual results to differ materially from what may be expressed or implied in these forward-looking statements. For a further discussion of risks and uncertainties that could cause actual results to differ from those expressed in these forward-looking statements, as well as risks relating to the business of Kratos in general, see the risk disclosures in the Annual Report on Form 10-K of Kratos for the year ended December 26, 2021, and in subsequent reports on Forms 10-Q and 8-K and other filings made with the SEC by Kratos.

Image: Marine Corps Warfighting Laboratory MAGTAF Integrated Experiment (MCWL) 160709-M-OB268-165.jpg

War in Ukraine Accelerates Global Drive Toward Killer Robots

The U.S. military is intensifying its commitment to the development and use of autonomous weapons, as confirmed by an update to a Department of Defense directive. The update, released Jan. 25, 2023, is the first in a decade to focus on artificial intelligence autonomous weapons. It follows a related implementation plan released by NATO on Oct. 13, 2022, that is aimed at preserving the alliance’s “technological edge” in what are sometimes called “killer robots.”

Both announcements reflect a crucial lesson militaries around the world have learned from recent combat operations in Ukraine and Nagorno-Karabakh: Weaponized artificial intelligence is the future of warfare.

“We know that commanders are seeing a military value in loitering munitions in Ukraine,” Richard Moyes, director of Article 36, a humanitarian organization focused on reducing harm from weapons, told me in an interview. These weapons, which are a cross between a bomb and a drone, can hover for extended periods while waiting for a target. For now, such semi-autonomous missiles are generally being operated with significant human control over key decisions, he said.

Pressure of War

But as casualties mount in Ukraine, so does the pressure to achieve decisive battlefield advantages with fully autonomous weapons – robots that can choose, hunt down and attack their targets all on their own, without needing any human supervision.

This month, a key Russian manufacturer announced plans to develop a new combat version of its Marker reconnaissance robot, an uncrewed ground vehicle, to augment existing forces in Ukraine. Fully autonomous drones are already being used to defend Ukrainian energy facilities from other drones. Wahid Nawabi, CEO of the U.S. defense contractor that manufactures the semi-autonomous Switchblade drone, said the technology is already within reach to convert these weapons to become fully autonomous.

Mykhailo Fedorov, Ukraine’s digital transformation minister, has argued that fully autonomous weapons are the war’s “logical and inevitable next step” and recently said that soldiers might see them on the battlefield in the next six months.

Proponents of fully autonomous weapons systems argue that the technology will keep soldiers out of harm’s way by keeping them off the battlefield. They will also allow for military decisions to be made at superhuman speed, allowing for radically improved defensive capabilities.

Currently, semi-autonomous weapons, like loitering munitions that track and detonate themselves on targets, require a “human in the loop.” They can recommend actions but require their operators to initiate them.

This article was republished with permission from The Conversation, a news site dedicated to sharing ideas from academic experts. It represents the research-based findings and thoughts of, James Dawes, Professor, Macalester College.

By contrast, fully autonomous drones, like the so-called “drone hunters” now deployed in Ukraine, can track and disable incoming unmanned aerial vehicles day and night, with no need for operator intervention and faster than human-controlled weapons systems.

Calling for a Timeout

Critics like The Campaign to Stop Killer Robots have been advocating for more than a decade to ban research and development of autonomous weapons systems. They point to a future where autonomous weapons systems are designed specifically to target humans, not just vehicles, infrastructure and other weapons. They argue that wartime decisions over life and death must remain in human hands. Turning them over to an algorithm amounts to the ultimate form of digital dehumanization.

Together with Human Rights Watch, The Campaign to Stop Killer Robots argues that autonomous weapons systems lack the human judgment necessary to distinguish between civilians and legitimate military targets. They also lower the threshold to war by reducing the perceived risks, and they erode meaningful human control over what happens on the battlefield.

This composite image shows a ‘Switchblade’ loitering munition drone launching from a tube and extending its folded wings. U.S. Army AMRDEC Public Affairs

The organizations argue that the militaries investing most heavily in autonomous weapons systems, including the U.S., Russia, China, South Korea and the European Union, are launching the world into a costly and destabilizing new arms race. One consequence could be this dangerous new technology falling into the hands of terrorists and others outside of government control.

The updated Department of Defense directive tries to address some of the key concerns. It declares that the U.S. will use autonomous weapons systems with “appropriate levels of human judgment over the use of force.” Human Rights Watch issued a statement saying that the new directive fails to make clear what the phrase “appropriate level” means and doesn’t establish guidelines for who should determine it.

But as Gregory Allen, an expert from the national defense and international relations think tank Center for Strategic and International Studies, argues, this language establishes a lower threshold than the “meaningful human control” demanded by critics. The Defense Department’s wording, he points out, allows for the possibility that in certain cases, such as with surveillance aircraft, the level of human control considered appropriate “may be little to none.”

The updated directive also includes language promising ethical use of autonomous weapons systems, specifically by establishing a system of oversight for developing and employing the technology, and by insisting that the weapons will be used in accordance with existing international laws of war. But Article 36’s Moyes noted that international law currently does not provide an adequate framework for understanding, much less regulating, the concept of weapon autonomy.

The current legal framework does not make it clear, for instance, that commanders are responsible for understanding what will trigger the systems that they use, or that they must limit the area and time over which those systems will operate. “The danger is that there is not a bright line between where we are now and where we have accepted the unacceptable,” said Moyes.

Impossible Balance?

The Pentagon’s update demonstrates a simultaneous commitment to deploying autonomous weapons systems and to complying with international humanitarian law. How the U.S. will balance these commitments, and if such a balance is even possible, remains to be seen.

The International Committee of the Red Cross, the custodian of international humanitarian law, insists that the legal obligations of commanders and operators “cannot be transferred to a machine, algorithm or weapon system.” Right now, human beings are held responsible for protecting civilians and limiting combat damage by making sure the use of force is proportional to military objectives.

If and when artificially intelligent weapons are deployed on the battlefield, who should be held responsible when needless civilian deaths occur? There isn’t a clear answer to that very important question.

MCLEAN, Va., Feb. 15, 2023 /PRNewswire/ — V2X, Inc., (NYSE: VVX), a leading provider of critical mission solutions and support to defense clients globally, will report 2022 fourth quarter and full year financial results on Thursday, March 2, 2023, after market close. Senior management will conduct a conference call at 4:30 p.m. ET that same day.

U.S.-based participants may dial in to the conference call at 877-506-6380, while international participants may dial 412-542-4198. A live webcast of the conference call as well as an accompanying slide presentation will be available on the V2X Investor Relations website at http://investors.vectrus.com.

A replay of the conference call will be posted on the V2X website shortly after completion of the call and will be available for one year. A telephonic replay will also be available through March 16, 2023, at 844-512-2921 (domestic) or 412-317-6671 (international) with passcode 10174938.

ABOUT V2X V2X is a leading provider of critical mission solutions and support to defense clients globally, formed by the 2022 merger of Vectrus and Vertex to build on more than 120 combined years of successful mission support. The Company delivers a comprehensive suite of integrated solutions across the operations and logistics, aerospace, training and technology markets to national security, defense, civilian and international clients. Our global team of approximately 14,000 employees brings innovation to every point in the mission lifecycle, from preparation, to operations, to sustainment, as they tackle the most complex challenges with agility, grit and dedication.

SAN DIEGO, Feb. 14, 2023 (GLOBE NEWSWIRE) — Kratos Defense & Security Solutions, Inc. (NASDAQ: KTOS), a leading National Security Solutions provider, announced today that it will publish financial results for the fourth quarter and Fiscal Year End of 2022 after the close of market on Thursday, February 23rd. Management will discuss the Company’s operations and financial results in a conference call beginning at 2:00 p.m. Pacific (5:00 p.m. Eastern).

The call will be available at www.kratosdefense.com. Participants may register for the call using this Online Form. Upon registration, all telephone participants will receive the dial-in number along with a unique PIN that can be used to access the call. For those who cannot access the live broadcast, a replay will be available on Kratos’ website.