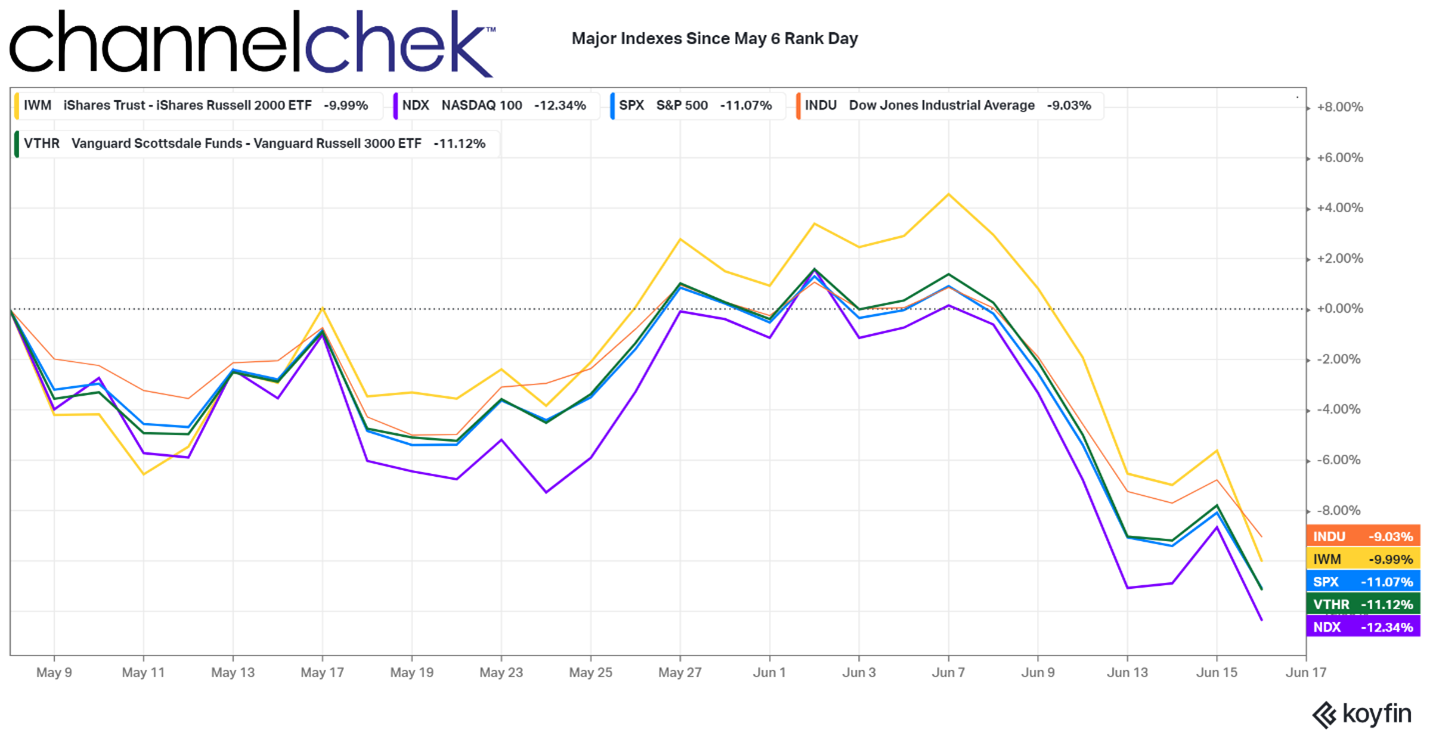

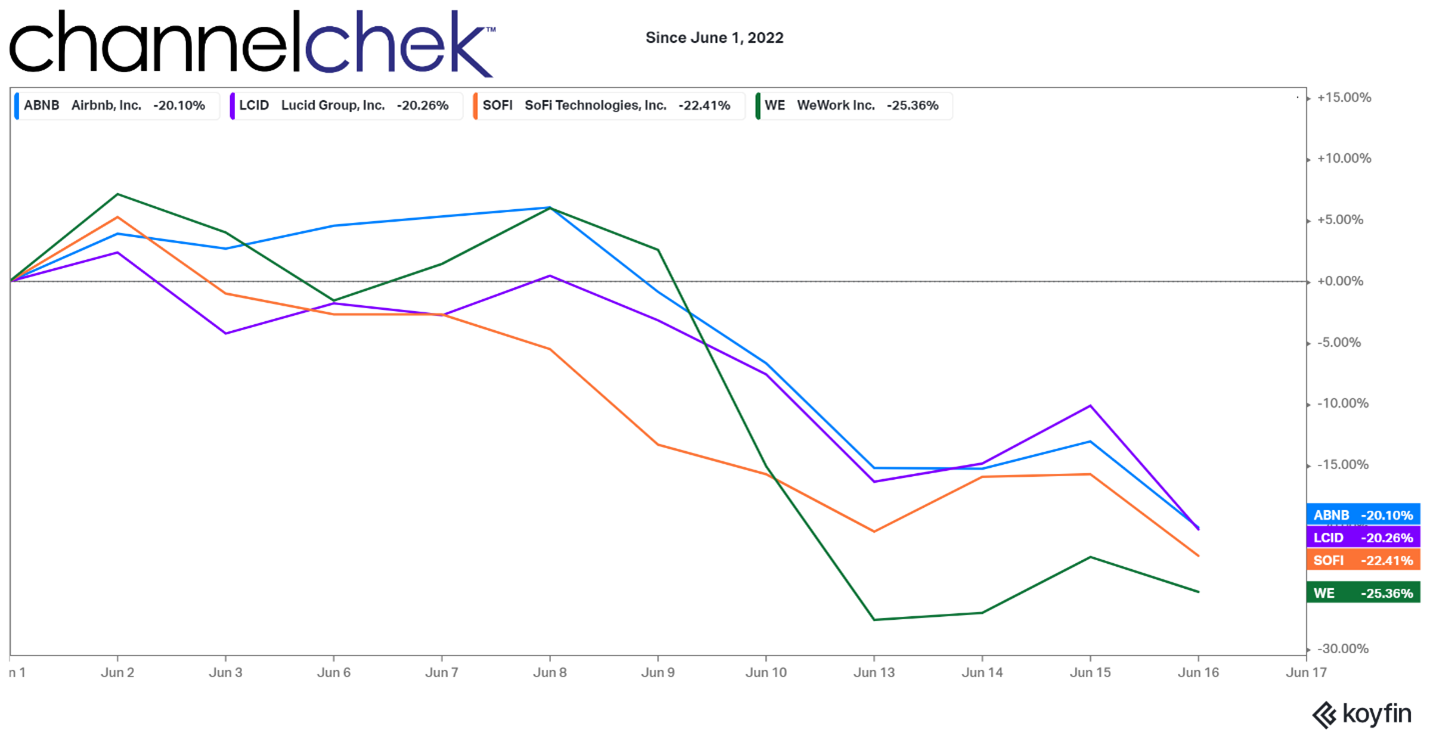

![]()

Bunker Hill Announces Appointment Of General Manager And Secures Mining Contractor

News and Market Data on Bunker Hill Mining

Bunker Hill Announces $15 Million Convertible Debt FinancingBunker Hill to Host Live Interactive 6ix Summit on Wednesday, June 22 @ 2:00pm ET / 11:00am PT TORONTO, June 20, 2022 – Bunker Hill Mining Corp. (the “Company”) (CSE: BNKR; OTCQB: BHLL) is pleased to announce the execution and closing of a new $15 million convertible debenture financing (the “Series 2 Convertible Debentures”) with Sprott Private Resources Streaming & Royalty Corp. (“SRSR” or “Sprott”). All figures in this news release are in US dollars unless otherwise stated. Sam Ash, CEO, stated “We are very pleased to announce this new $15 million financing, representing an increase in our project finance package with Sprott to $66 million. Together with our recent equity raise, this materially improves our working capital position, enables us to meet our financial assurance obligations with the EPA, and funds several key workstreams over the coming months including completion of the underground decline, demobilization of the Pend Oreille mill, and further engineering optimization in preparation for the mine restart.” Investors are invited to register for the live interactive 6ix Summit at: CONVERTIBLE DEBENTURE The Series 2 Convertible Debentures bear interest at an annual rate of 10.5%, payable in cash or shares at the Company’s option, and mature on March 31, 2025. Repayments of $2 million shall be made at the end of each calendar quarter, starting on 30 June 2024, with the remaining $9 million due on March 31, 2025. The Series 2 Convertible Debentures are convertible into shares of the Company at a share price of CAD 0.29 per share until the maturity date. The Company may elect to re-pay the Convertible Debenture early; if SRSR elects not to exercise its conversion option at such time, a minimum of 12 months of interest would apply. The Series 2 Convertible Debentures will be secured by the same security package that has been put in place to secure the $8 million Royalty Convertible Debenture and the aggregate $6 million Convertible Debentures (the “Series 1 Convertible Debentures”) that closed in January 2022. The parties have also agreed to a number of changes to the previously announced project finance package of up to $51 million (of which $14 million has been advanced to date), consisting of the Royalty Convertible Debenture, Series 1 Convertible Debentures, and the Stream. Firstly, the maturity dates of the Royalty Convertible Debenture and Series 1 Convertible Debentures have been extended to March 31, 2025 (previously July 7, 2023). As previously envisaged, the Royalty Convertible Debenture will convert to a 1.85% life of mine royalty or be repaid when the Stream is advanced. However, in the event of conversion, the Company will enter into a Royalty Put Option entitling the royalty holder to resell the royalty to the Company for $8 million upon default under the Series 1 Convertible Debentures or Series 2 Convertible Debentures until such time that the Series 1 Convertible Debentures and Series 2 Convertible Debentures are paid in full. The Series 1 Convertible Debentures will remain outstanding until March 31, 2025, regardless of whether the Stream is advanced, unless the Company elects to exercise its option of early repayment. Lastly, the minimum quantity of metal delivered under the Stream, if advanced, will increase by 10% relative to amounts announced in the news release of December 20, 2021. In light of the Series 2 Convertible Debenture financing, the previously permitted additional senior secured indebtedness of up to $15 million for project finance has been removed. However, the Company and Sprott have agreed that the Company is permitted to sell an additional $5 million of the Series 2 Convertible Debentures to other investors until August 1, 2022. The net proceeds of the financing will be primarily used to satisfy the Company’s financial assurance obligations with the US Environmental Protection Agency (“EPA”) and the advancement of mine restart activities, including the completion of the underground decline, demobilization of the Pend Oreille mill, and advancement of EPCM activities in anticipation of mill construction in the fourth quarter of 2022. NEXT STEPS Additional optimization opportunities have been identified as technical work on the Prefeasibility Study (“PFS”) has advanced. In order to incorporate these into the PFS, technical work is continuing and the PFS is now expected to be completed later in the third quarter of 2022. The advancement of the Stream is also expected to take place at approximately that time. While this additional technical work is in progress, development drifting will continue with an expected breakthrough into the internal ramp between the 6 and 8 levels to occur in September 2022. Relocation of the Pend Oreille Mill will continue throughout the summer with a key milestone being the disassembly and transport of the primary ball mills in August. RELATED PARTY The financing transactions described in this press release (the “Transactions”) constitute related party transactions pursuant to Multilateral Instrument 61-101 – Protection of Minority Security Holders in Special ABOUT BUNKER HILL MINING Under new Idaho-based leadership the Bunker Hill Mining Corp, intends to sustainably restart and develop the Bunker Hill Mine as the first step in consolidating a portfolio of North American precious-metal assets with a focus on silver. Information about the Company is available on its website, www.bunkerhillmining.com, or within the SEDAR and EDGAR databases. For additional David Wiens, CFA CAUTIONARY STATEMENTS Certain |

|

Contact Info: Bunker Hill Mining Corp. |